small & medium enterprises - credit rating … digest... · digest small & medium...

TRANSCRIPT

�Electronic Bill Factoring Exchange

�SME Listing without IPO

�Management and mitigation of project risk by SMEs

�Indian Leather industry

January 2014

SMECARE

DigestS M A L L & M E D I U M E N T E R P R I S E S

CARE SME Digest January 2014

2

About CARECARE Ratings commenced operations in April 1993 and over nearly two decades; it has established itself as the second-largest credit rating agency in India. With the rating volume of debt of around Rs.48,250 bn (as on March 31, 2013), CARE Ratings is proud of its rightful place in the Indian capital market built around investor confidence. CARE Ratings has also emerged as the leading agency for covering many segments like that for banks, sub-sovereigns and IPO gradings.

CARE Ratings provides the entire spectrum of credit rating that helps the corporates to raise capital for their various requirements and assists the investors to form an informed investment decision based on the credit risk and their own risk-return expectations. Our rating and grading service offerings leverage our domain and analytical expertise backed by the methodologies congruent with the international best practices.

With majority shareholding by leading domestic banks and financial institutions in India, CARE’s intrinsic strengths have also attracted many other investors.

CARE’s registered office and head office, is located at 4th floor, Godrej Coliseum, Somaiya Hospital Road, Sion (East), Mumbai 400 022. It has also started its second office in Mumbai at Andheri since June 2013. In addition, CARE has regional offices at Ahmedabad, Bangalore, Chandigarh, Chennai, Hyderabad, Jaipur, Kolkata, New Delhi, Pune and international operations in Male’ in the Republic of Maldives. With independent and unbiased credit rating opinions forming the core of its business model, CARE Ratings has the unique advantage in the form an External Rating Committee to decide on the ratings. Eminent and experienced professionals constitute CARE’s Rating Committee.

CARE’s SME VerticalValue-added services for SMEs

• Wide product offering: MSE Rating, SME Rating, Bank Loan Ratings, Due Diligence Services• Data base of more than 6,000 SME entities • SME digest: A Quarterly publication for analytical inputs• SME Newsletter: Daily publication on news in SME sector• Operating from ten branches across India• MoU with leading banks for interest & rating fee concession • A team of qualified analysts

Compilation Team

Mehul Pandya : Chief General Manager Email: [email protected] Cell: +91-79-40265656

Yogesh Shah : Dy. General Manager Email: [email protected] Cell: +91-79-40265603

Nitin Jha : Manager Email: [email protected] Cell: +91-79-40265619

Sameer Shaikh : Graphic Designer Email: [email protected] Tel: +91-22-6144 3510

CARE SME Digest January 2014

3

Table of ContentFrom DeskMr.D. R. Dogra, MD & CEO - CARE Ratings .............................................................................. 6

Mr. Mehul Pandya, Head - SME, CARE Ratings ......................................................................... 7

Research & Articles1. Electronic Bill Factoring Exchange – An Unconventional Trade Credit Alternative ....... 10

2. MSME Sector – Central Bank’s initiatives .............................................................................. 13

3. SME Listing without IPO!! ........................................................................................................ 17

4. Management and mitigation of project risks by SMEs ......................................................... 19

5. Trend of PE Investment in SME Segment .............................................................................. 25

Industry Articles1. Indian Leather Industry ............................................................................................................ 28

Rating Guide1. Rating approach for SME/MSE ratings ................................................................................... 34

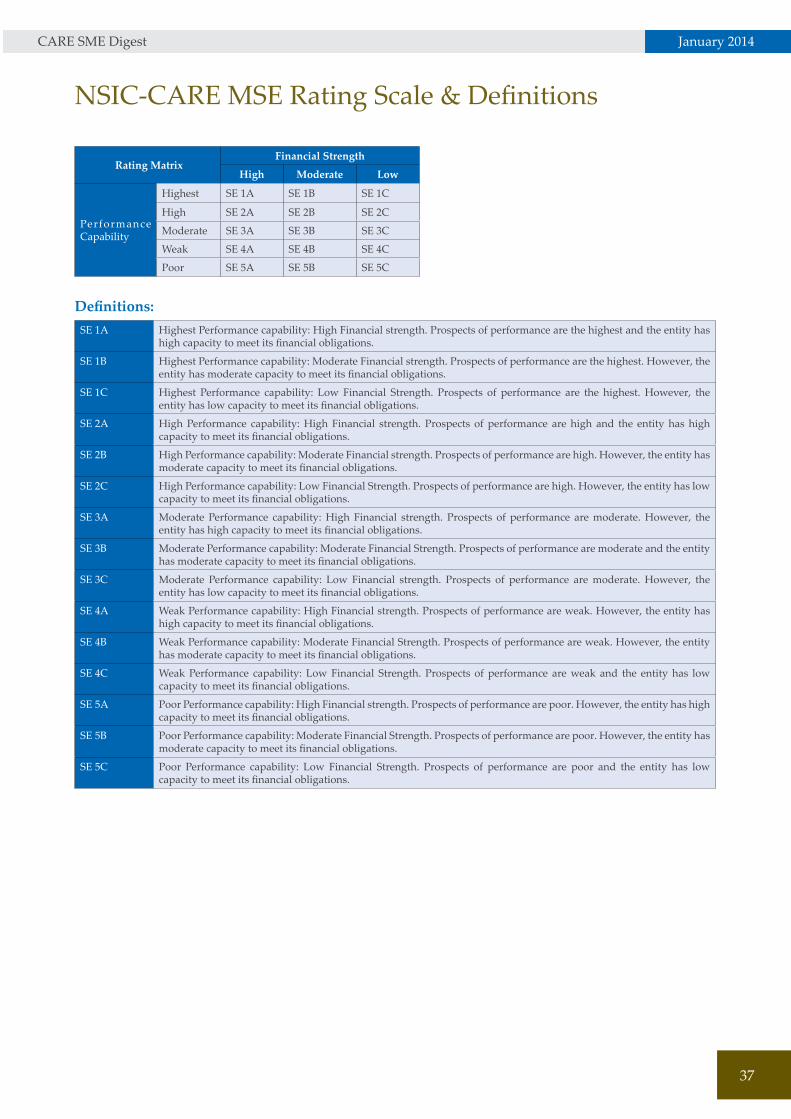

2. NSIC-CARE MSE Rating Scale & Definitions ........................................................................ 37

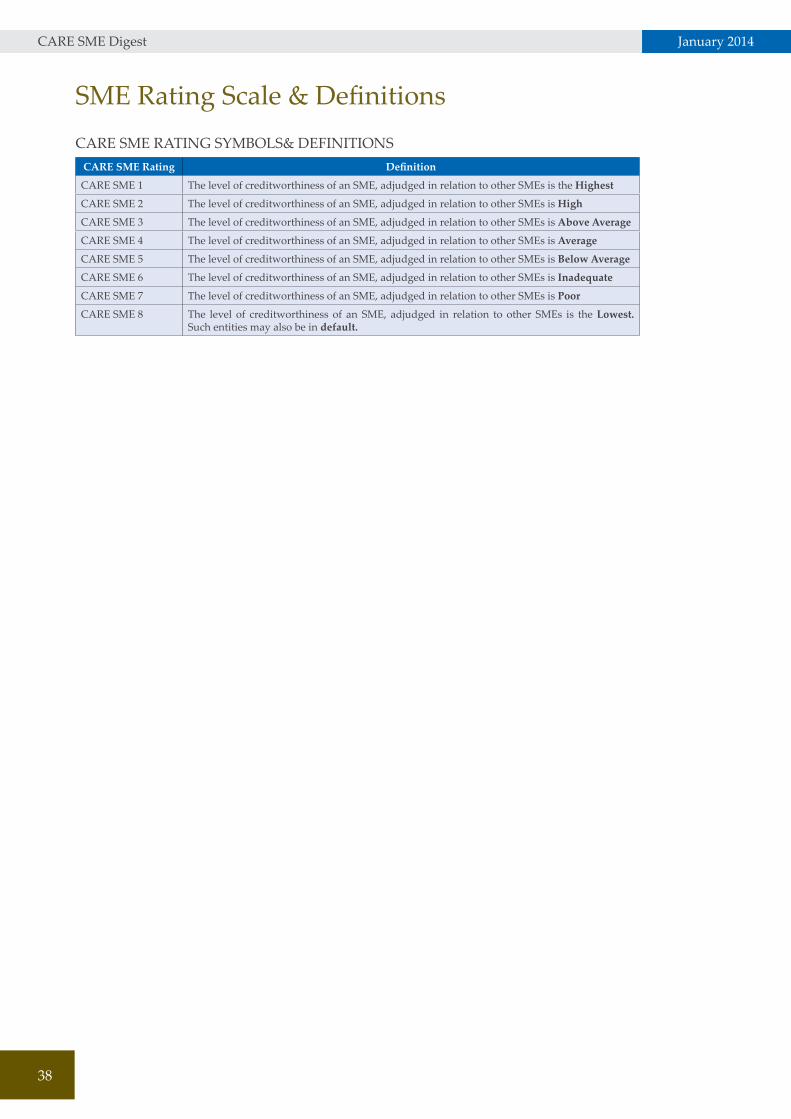

3. SME Rating Scale & Definitions ............................................................................................... 38

Leading SMEs1. Analysis of highly rated small-scale entities .......................................................................... 40

2. Summary profile of micro & small enterprises rated by CARE .......................................... 42

3. Profiles of top rated micro & small enterprises ..................................................................... 43

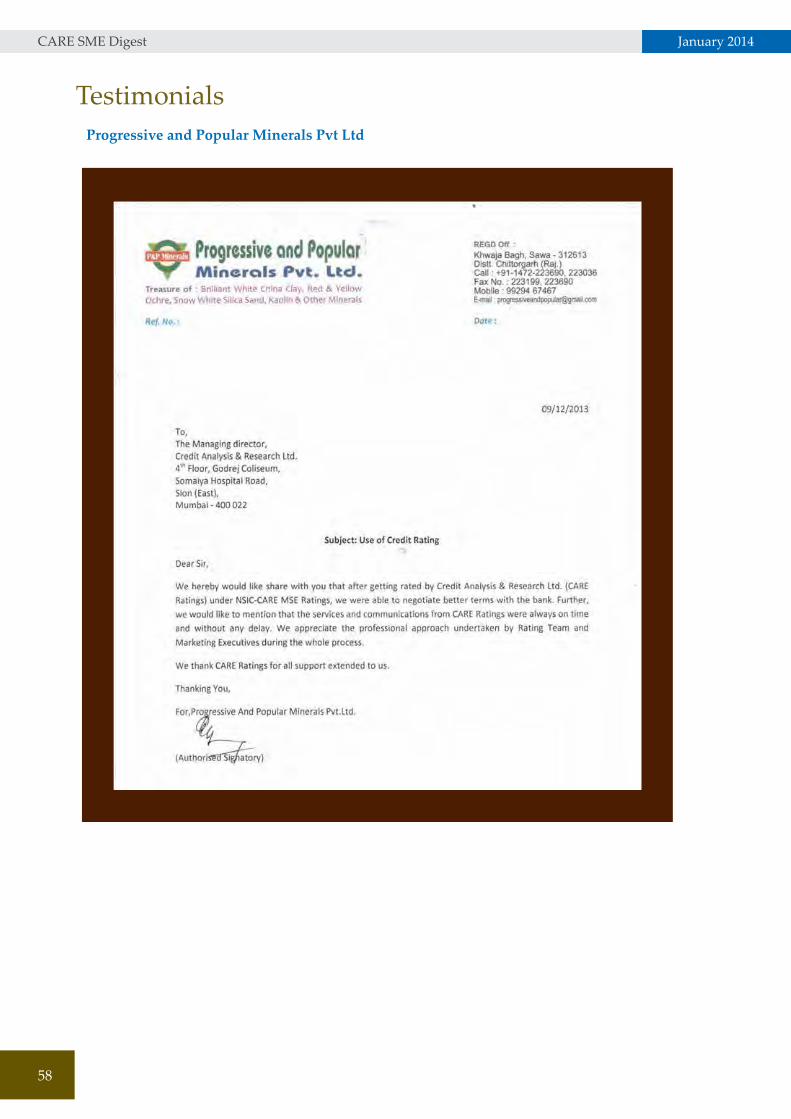

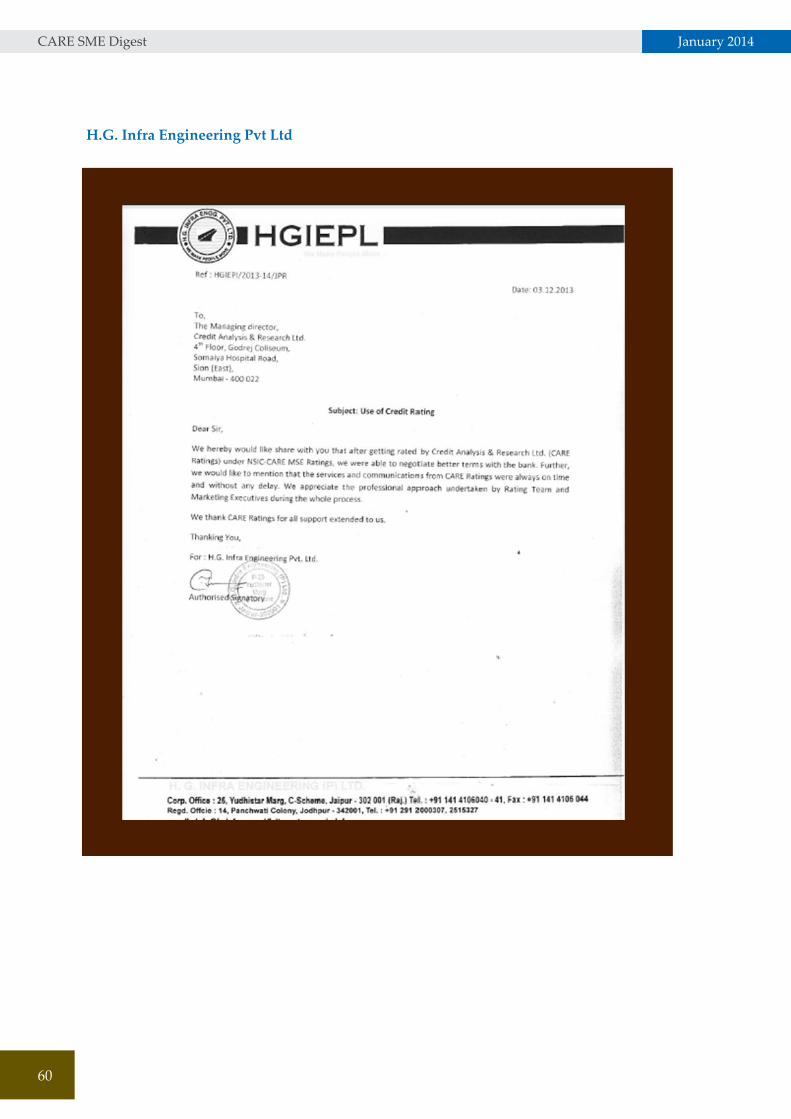

Recognition1. Testimonials from entities rated by CARE ............................................................................. 58

Awareness Efforts1. Synopsis of seminars and events organised by CARE ......................................................... 62

2. MSME News updates ................................................................................................................ 65

This pag

e is i

ntentio

nally

left b

lank

From Desk

CARE SME Digest January 2014

6

We have observed that progressively a large number of SMEs have realized the need to go in for credit ratings in order to have better access to credit. This we believe is necessary for sustainable growth of a sector which has become more important in terms of productivity, employment generation, contribution to industrial and exports growth.

Bank credit during the period April-December has grown at a higher rate of 9.4% in 2013 relative to that in 2012. RBI data for April-November indicates that growth has been higher during April-November in case of agriculture, services and personal loans while that to industry has been lower. This can be linked to the overall state of the industry where growth in manufacturing, in particular for the first eight months of the year, was lower at -0.6% as against +0.9% during the same period of last year.

The higher growth in credit to agriculture may be attributed to the expected better kharif crop which as announced by the Ministry of Agriculture. The lower growth to industry, while linked to the overall state of industry, shows a differential picture across sectors. The SME segment has witnessed higher levels of borrowing while that to the large firms has slowed down. The latter could be due to the fact that larger firms have access to ECBs and have looked more closely at this route given the interest rate differential. However, given that the rupee was volatile, the relative attractiveness of such loans could have come down. In absolute terms, the total ECB approvals from RBI were lower during April-October 2013 at US$ 16.8 billion as against US$ 18.6 billion during the same period of last year.

As we move towards the fiscal year end, it would be interesting to see how the economic and debt market scenario unfurls with obvious challenges in front. We are still looking at growth approaching the 5% mark in FY14 with some marginal recovery in industrial growth which should augur well for the markets and we could start the new financial year on a more hopeful note.

D.R. Dogra,MD & CEO, CARE Ratings

From MD’s Desk

CARE SME Digest January 2014

7

CARE Ratings acted as the Knowledge Partner for the MSME Banking Excellence Awards, 2013 organised by the Chamber of Micro, Small and Medium Enterprises at New Delhi on January 9, 2014.

The theme paper highlighted three studies covering the impact of the challenging economic scenario on the financials of some the CARE rated MSMEs, default study for MSEs and an assessment of SME lending being too risky.

Our studies have highlighted the fact that given the level of financial discipline demonstrated as compared to the large corporates and the extent of financial exclusion in the SME sector apart from the importance of the sector for the overall economy, banks need to urgently step up lending to the sector. To put it succinctly, developing a proper understanding of the business of MSMEs and keeping a control over operating cost per MSME would be the key for extending the reach of the banks. On both these counts, CARE can partner Indian banks.

Our guest columnist from one of the public sector banks highlights in this issue of SME Digest about various initiatives taken by their bank for allowing credit facilities to entities within the MSME domain to suit their needs. Apart from this, we have articles on SME Listing without IPO, Electronic Bill Factoring Exchange, why managing project risk is necessary and trend of PE investment in SME segment are good reads which I hope would encourage many of our clients to take advantage of such favourable scenario coming up to increase their presence in the overall market.

“To perceive a need and to meet it, is one secret of good business”

Mehul Pandya Head – SME, CARE Ratings

From Head-SME

This pag

e is i

ntentio

nally

left b

lank

Research & Articles

CARE SME Digest January 2014

10

Electronic Bill Factoring Exchange -An Unconventional Trade Credit Alternative This is well known that many small businesses rate the lack of finance for working capital needs as the major bottleneck to run the business efficiently. The major component of the working capital gap of SMEs is the outstanding receivables from their reputed and much larger (in size and bargaining power) corporate buyers. Presently, corporate accounts receivables (trade credit) are not securitized as the existing RBI guidelines do not make it clear whether revolving assets such as trade credit or working capital loans, etc can be securitized. A mechanism like Electronic Bill Factoring Exchange which works on the principles of reverse factoring is one of the solutions prescribed by the current RBI Governor, Mr Raghuram Rajan in September 2013. He first floated the idea of such exchange in India in his report on financial reforms ‘A Hundred Small Steps’ published in 2008.

Reverse factoringThe traditional factoring is a type of mechanism where the supplier’s receivables are sold to a factor at a discount and receive immediate cash. In the traditional factoring, the factor purchases the receivables from the various buyers of a single seller, ie, the credit risk of many buyers is sold to a single factor. Though the reverse factoring technique is similar to the traditional factoring in many ways, the prime distinctive parameter here is the initiating party. In reverse factoring, the buyer (generally large corporate) initiates the transaction in order to help their small suppliers finance their receivables. Its advantages over traditional factoring are:

1. Cash flow optimization tool for both seller and buyer as the seller gets quick payment of its goods and buyer gets an elongated period to make the payment.

2. Comprehensive credit information of the high quality buyers (unlike SMEs and mid corporate) is available with the credit information bureau or in public domain.

3. Credit risk for factor is equal to the default risk of high quality customer and not the risky SME.4. Allows SMEs to factor without recourse.

Need for exchangeFor all firms together, the share of trade credit in total corporate financing has grown steadily from 16% to almost 19% during 2005–10. SMEs could reduce their investment in working capital, and thus their need for finance, significantly if the receivables due to them from large firms could be securitized. In principle, such receivables, if accepted, are essentially commercial paper with the high credit ratings of the large firms. Furthermore, if SME can securitize and sell its receivable claim, it will result in smaller and better capitalized balance sheet which would ultimately improve its credit worthiness and credit rating. Though the securitization process is similar to factoring, it could be more cost effective than bank funding, factoring and letters of credit. A negotiable Bill of Exchange (BoE) issued by a buyer against goods received provides a form of securitization of trade credit. The supplier can have the BoE discounted with any financial intermediary in a private transaction. The supplier and the intermediary can also endorse the bill in favour of any other party. Currently, mostly banks deal in BoEs, and usually the acceptance and discounting are kept under the credit limit set up for the buyer. However, the nature of the transactions and the physical format of BoEs rules out a sizable secondary market in them.

Working mechanismThe Electronic Bill Factoring Exchange provides an effective channel for selling corporate receivables through an electronic marketplace to a global network of institutional buyers. The generally followed mechanism internationally requires the registration of sellers and their large corporate buyers. Sellers can post as many

CARE SME Digest January 2014

11

eligible receivables as they wish, as often as they like, and set the terms (the duration of the auction, the maximum discount fee to be paid, and the “buyout price”). The factors compete to purchase invoices, enabling companies to monetize receivables at a competitive cost. The sale of receivables from the supplier to the factor and the transfer of funds from the factor to the supplier are done electronically. The corporate buyer also receives the intimation of the said transaction and pays the due amount to the factor directly on the maturity date.

The exchange enables to gain quick access to working capital by selling invoices online. By connecting with a community of banks, financing companies and factors looking to purchase outstanding invoices, receivables can be turned into cash quickly. Few takeaways from global examples

The best example of the successful implementation of an electronic exchange especially for SMEs is by a Mexican bank, Nafin, where any small firm could present receivables from a number of large firms. Nafin has a pre-defined mechanism in place with these large firms beforehand to have these receivables presented and accepted electronically. The accepted receivables, now full-fledged claims on the large firms, were then auctioned off in the market, and the proceeds are paid out to the small firms.

Similarly, MarketInvoice is the UK’s first online funding portal allowing businesses to draw down fast and flexible funds against their outstanding long-dated invoices. MarketInvoice was incorporated in late 2010 and opened its door to the public in February 2011. MarketInvoice is backed by a group of experienced private investors, including successful business owners, entrepreneurs, financial services experts, and angel investors. However, none of MarketInvoice’s activities fall under the definition of a regulated activity at present.

Indian perspectiveIt is the need of hour to implement similar practice in India as well. Recently in November 2013, on the similar lines, RBI decided to provide Rs.5,000 crore refinance grant to Small Industrial Bank of India (SIDBI) against the financing of receivables of SMEs due from the large organisations. It is also a major step towards easing the financing of receivables of SMEs and indicates the focus of the government to remove this major bottleneck faced by SMEs. Hence, it may not be a surprise if the proposal of setting up such an exchange in India gets approved. However, in order to successfully implement an Electronic Bill Factoring Exchange, various below mentioned initiatives are required:

• An organization like NSDL and CDSL to provide dematerialization capability.• Regulating body such as RBI and SEBI to regulate the operations.• An intermediary along the lines of Nafin could tie up with large buyers and an authorized list of

their suppliers to have automatic bill presentment and acceptance facilities. Such bills could then be auctioned and the existing exchanges and reporting mechanisms (NSE/BSE) be used to trade and settle these instruments.

• Access to technically-equipped, safe and secure platform to cater the large traffic of SMEs across the country.

By the end of 2010, 55% of the total portfolio of loans granted to SMEs by commercial banks is channeled through Nafin. On an average, 1 billion pesos (USD 76 million) gets traded every day, granting immediate liquidity to over 25,800 SMEs that are suppliers of the Federal Government, State and Municipal Governments and some of the country’s large private companies.

In September 2013, MarketInvoice was chosen to channel government funding to UK SMEs via Department of Business Innovation and Skills (DIS). By the end of 2013, more than £100 million funds have been advanced through this platform and the Government has also committed an initial amount of £5 million to be put through this platform.

CARE SME Digest January 2014

12

Conclusion The Indian Credit Bureau lags behind its Asian counterparts in terms of the coverage of population (the individuals or firms having repayment history, unpaid debts or credit outstanding against adult population). In 2012, the Indian coverage was just 15% compared with 100% coverage in Japan and 82% coverage in Malaysia (as per the World Bank). As reverse factoring tool offers good alternative factoring technology in the economies with weak credit information, there is a fair chance that this model gets success in India. However, the key sensitivity area will include the support received from the political, banks/financial institutions and corporate.

Contributed by: Uday Shah, Analyst

Mohit Agrawal, Manager

CARE SME Digest January 2014

13

MSME Sector – Central Bank’s initiatives

The Micro, Small and Medium enterprises (MSMEs) have been accepted as the engine of economic growth and play an important role in the equitable economic development of the country. The major advantage of the sector is its employment potential at low capital cost. The labour intensity of the MSME sector is much higher than that of the large enterprises. The MSMEs constitute over 90% of total enterprises in most of the economies and are credited with generating the highest rates of employment growth and account for a major share of industrial production and exports.

MSMEs have been established in almost all-major sectors in the Indian industry such as:• Food Processing• Agricultural Inputs• Chemicals & Pharmaceuticals• Engineering; Electrical, Electronics• Electro-medical equipment• Textiles and Garments• Leather and leather goods• Meat products• Bio-engineering• Sports goods• Plastics products• Computer Software, etc.

The Government of India has enacted the Micro, Small and Medium Enterprises Development (MSMED) Act, 2006 on June 16, 2006, which was notified on October 2, 2006. With the enactment of MSMED Act, 2006, the paradigm shift that has taken place is the inclusion of the services sector in the definition of micro, small & medium enterprises, apart from extending the scope to medium enterprises. The MSMED Act, 2006 has modified the definition of micro, small and medium enterprises engaged in manufacturing or production and providing or rendering of services. The Reserve Bank as notified the changes to all scheduled commercial banks. Furthermore, the definition, as per the Act, has been adopted for purposes of bank credit vide RBI circular ref. RPCD.PLNFS. BC.No.63/ 06.02.31/ 2006-07 dated April 4, 2007.

The enterprises engaged in the manufacture or production, processing or preservation of goods as specified below:

I. A micro enterprise is an enterprise where investment in plant and machinery does not exceed Rs.25 lakh;

II. A small enterprise is an enterprise where the investment in plant and machinery is more than Rs.25 lakh but does not exceed Rs.5 crore; and

III. A medium enterprise is an enterprise where the investment in plant and machinery is more than Rs.5 crore but does not exceed Rs.10 crore.

In case of the above enterprises, investment in plant and machinery is the original cost excluding land and building and the items specified by the Ministry of Small Scale Industries vide its notification No.S.O. 1722(E) dated October 5, 2006.

CARE SME Digest January 2014

14

Enterprises engaged in providing or rendering of services and whose investment in equipment (original cost excluding land and building and furniture, fittings and other items not directly related to the service rendered or as may be notified under the MSMED Act, 2006) are specified below.

I. A micro enterprise is an enterprise where the investment in equipment does not exceed Rs.10 lakh;II. A small enterprise is an enterprise where the investment in equipment is more than Rs.10 lakh but does

not exceed Rs.2 crore; andIII. A medium enterprise is an enterprise where the investment in equipment is more than Rs.2 crore but

does not exceed Rs.5 crore.

These will include small road & water transport operators, small business, retail trade, professional & self-employed persons and other service enterprises.

Central Bank of India, one of the premier public sector banks, has brought about various innovative schemes to encourage the MSME sector. Of course all banks may have schemes in place. But the banks that provide tailor made schemes for various activities will have an edge over others. Some of the latest schemes introduced in Central Bank of India are discussed here-under. All the traditional lending schemes such as Cash Credit [working capital finance], term loans, bill discounting facility, export finance, letter of credit, bank guarantees, etc, are available for entrepreneurs. The schemes that are discussed here-under are special schemes, which are tailor made to the specific enterprises.

Cent Sahayog This is a unique scheme to finance micro and small units in manufacturing and service sectors. This is ideal for self-employment and for creating employment for others. It covers activities such as repairing shops, sweet meat, bakeries, taxi, auto, function/marriage halls, beauty parlors, saloons, small shoe makers, professionals, consultants, etc. The loan amount that can be sanctioned under this scheme is Rs.100 lakhs. The processing fee ranges from Rs.100 to Rs.25,000 depending on the loan amount. The margin ranges from 10% to 20%. The collateral security is not insisted; but CGTMSE covers the loan amount. The rate of interest is BR + 0.50 up to Rs.10 lakh limit and BR + 1.00 up to 100 lakh. As for risk assessment, the minimum hurdle score is 50. This scheme provides for the sanction of term loan, cash credit and overdraft as need-based. For new entrepreneurs, the turn over method is applicable.

Cent Protsahan SchemeThis scheme is formulated for marketing, branding and promoting domestic trade and exports for micro and small Enterprises. It is used to meet exhibition participation fees, transit and living expenses of proprietors/partners/directors of firms engaged in India and abroad to market their products/services of MSE. The facility is in the form of term loan and the maximum loan amount is Rs.4 lakh for domestic and Rs.15 lakh for overseas exhibitions.

Cent KalyaniWomen empowerment is on upsurge in the world and India is no exception. Although Indian women have been a traditional lot, their entry into the world of industry and business, of late, is prolific. It is estimated that 10% of the total entrepreneurs in India are women and the number may get doubled in a short span of time. With this background, the Central Bank of India introduced a unique scheme, Cent Kalyani, exclusively for women entrepreneurs on the last International Women’s Day.

The scheme envisages the generation of continuous and sustainable employment opportunities for women entrepreneurs. Under this scheme, finance is available to the enterprises where a woman holds at least 51% of

CARE SME Digest January 2014

15

the stake and at least 51% of the employees are women. The quantum of finance under this scheme is pegged at Rs.100 lakh. The nature of finance could be term loan, working capital limit, non-fund based and/or OD. The interest rate is fixed at BR + 0.25% for the finance up to Rs.10 lakh and BR + 0.50% above Rs.10 lakh and up to Rs.100 lakh. Risk rating hurdle rate is 51 marks. Another important feature of this scheme is that the bank will pay CGTMSE premium for the first year. As the loan is covered under the CGTMSE scheme, there is no requirement of collateral security. Interest rate concession is allowed up to 0.25% in case external rating agencies accord the high and highest ratings. Other attractive features of the scheme are complete waiver of processing fee and concession under tenure premium of 0.05% up to three years and 0.10% from three years to seven years.

Cent Construction Equipment FinanceCentral Bank of India introduced this scheme to enable firms, companies, contractors engaged in road construction, infrastructure development, mining, oil exploration, railway contractors, power, irrigation, civil contractors and sub-contractors for the purchase of new backhoe loaders, excavators, tipper/dumpers, transit mixers, cranes (pick n carry, heavy duty, tower & derrick), wheel loaders, compactors, road rollers, pavers, dozers, graders, compressors, drills, hot mix plants, concrete pumps/boom placers, crushing plants, RMC plants, rock breakers, WMM plants , DG sets, fork-lifts, reach stackers, piling rigs and many more.

Cent Contractor Civil Contractors play a vital role in the growth of infrastructure. They provide a wide range of civil construction works to business in the government sector including roads, buildings, canals, oil and gas sector, privately owned companies, energy companies and resource based companies etc. With certain eligibility criteria like previous experience of two years in the line, approval/registration with government, PSBs, defence, reputed private organizations, minimum number of [three] contracts on hand, etc; cash credit, term loan for purchase of equipment, overdraft, DPG, performance guarantee, bid bond guarantee, bills purchased limit, etc, are considered for sanction. Interest will be charged at BR + 0.50% up to Rs.10 lakh and at BR + 1.0% for limits above Rs.10 lakh and up to Rs.100 lakh. In case of limits above Rs.100 lakh, the interest rate will vary depending on the risk rating; but in any case the maximum rate is BR + 4% only. The processing fee is fixed at a reasonable rate of 1% of loan amount subject to a maximum of Rs.2 lakh. The collateral is moderately fixed at 100% value up to Rs.100 lakh [or if the limit is covered by CGTMSE no collateral required] and in case of limits above Rs.100 lakh, the value of collateral security shall be 150%. Wherever risk rating is done by approved external agencies and high or the highest rating is given, a concession of 50% in processing fee and 0.25% in interest rate are allowed.

Cent Food Processing PlusAgro-processing is regarded as the most promising and sunrise sector of the Indian economy in view of its large potential for growth. It has the potential to be the driver of economic growth and enhance rural incomes. Agro processing is defined as a set of techno-economic activities, applied to all the produces, originating from agricultural farm, livestock, aqua cultural sources and forests for their conservation, handling and value-addition to make them usable as food, feed, fibre, fuel or industrial raw materials. With an intention to encourage such a promising sector, the Central Bank of India introduced the Cent Food Processing Plus Scheme.

The activities covered under this scheme include the following:Fruits & vegetable processing industry, food grain milling industry which includes dal mills, oil mills, wheat, flour and suji mills etc; dairy products such as milk powder, infant milk food, malted milk food, etc; processing and refrigeration of poultry and eggs, meat and meat products, processing of fish (including canning and

CARE SME Digest January 2014

16

freezing), establishment and servicing of the development councils for food processing industries, technical assistance and advice to food processing industry, fishing and fisheries beyond territorial waters, industries relating to bread, oilseeds, meals (edible), breakfast foods, biscuits, confectionery (including cocoa processing and chocolate making), malt extract, protein isolate, high protein food, weaning food and extruded food products (including other ready–to–eat foods), specialized packing for food processing industries, beer, including non-alcoholic beer, alcoholic drinks from non-molasses bases, aerated waters/soft drinks and other processed food.

The existing and new units can seek limits under this scheme. The minimum hurdle score of 51 is considered. Term loan for purchase of machinery, working capital limit, packing credit, non-fund based limits like guarantee and letter of credit wherever required will be considered. The interest rate up to Rs.100 lakh is BR + 0.50% and above Rs.100 lakh, interest will be fixed according to the collateral security coverage. If collateral value is 100% or above, interest will be charged at BR + 0.50%. Processing charges are collected at a low level. While there is no processing fee for the limit sanctioned up to Rs.25,000, only Rs.500 is charged up to Rs.2 lakh. The maximum processing charges are levied at 0.40% for limit above Rs.100 lakh. In case of extreme emergencies and subject to certain conditions, temporary ad-hoc will be considered to meet with such exigencies. With certain usual conditions, limits will be considered even for the units taken on lease basis. The value of collateral security offered is 50% of the limit, except where the loan is covered by CGTMSE. Wherever risk rating is done by approved external agencies and high or the highest rating is given, a concession of 50% in processing fee and 0.25% in interest rate are allowed.

In addition to the latest schemes narrated above, the bank has Cent Mortgage scheme for personal and business requirements, Cent Trade for business requirements, Cent Doctor, Cent Dentist, etc, to cater to the needs of individuals, business entrepreneurs and professionals.

Central Bank of India has been serving the nation for over 101 years and is always ahead in meeting with the customers’ demands. The bank believes in customer delight and ecstasy and is poised to serve them with efficacy and remains to serve the entrepreneurs in meeting their ever increasing needs.

Contributed by: N. K. Balakrishnan- General Manager

Central Bank of India, Zonal Office, Bank StreetHyderabad – 500 095

“The author is General Manager at the Zonal Office of Central Bank of India, Hyderabad. The published views / contents are as per his own submission and request. The same have not been independently verified by CARE.”

CARE SME Digest January 2014

17

SME Listing without IPO!!

Recently, the Securities and Exchange Board of India (SEBI) issued the regulations on listing of Specified Securities on Institutional Trading Platform (ITP), which enables Small and Medium Enterprises (SME) to list on the stock exchanges without going through an Initial Public Offering (IPO). This is another step in creating special avenues for SMEs to raise capital and to provide their shareholders (private equity and venture capital funds) with liquidity as well easy exit mechanisms.

BackgroundSME plays a crucial role in nation building and their potential in terms of generating employment and income as well as encouraging innovation and enterprise. Therefore, it is essential that the necessary enabling environment is provided for SMEs to flourish. However, the risk of failure for SME is quiet high as compared with companies which have already grown larger. Apart from the risk of business failure, the risk of investment being locked-in for very long durations is also one of the constraints faced by investors who are investing in SMEs which drive up their cost of capital. As a result, SME’s find it difficult to raise capital compared with larger companies due to their higher risk profile.

In this context, if the securities of a company were listed, it would give a better visibility and thereby widen reach to investors. Standardized norms of entry for SME and continuous disclosure thereafter will also attract more investors. Furthermore, listing of the securities would also mitigate the exit risk and such risk reduction will automatically result in a lower cost of capital as well as easy and more capital flow.

Presently, in-order to get listed, even on the SME platform, regulatory provisions require an unlisted company to make an IPO and offer up to 25% of its shareholding to public through an offer document. Making an IPO involves a lot of cost and procedures per say appointing intermediaries like merchant bankers for due-diligence, marketing the issue and overall issue management, bankers to an issue for collection of funds, syndicate members for distribution and collection of application. These procedural and economic costs of making an IPO including advertising and other intermediary fees, is too high to be absorbed by the SMEs. Besides, the promoters are normally not interested in diluting 25% of the shareholding to public at an early stage of the company’s life cycle as the obtainable valuations are low at this stage.

New Mantra: Listing without IPOThe Finance Minister of India in the Union Budget for the year 2013-2014 (February 20, 2013) announced changes in the capital market for SMEs so as to help them grow big with the liberalized policy. SMEs will be able to raise public money and trade their shares on exchanges without an IPO, but the participation will be restricted to “Informed Investors”. The informed investors can broadly define as investors like Venture Capital Funds (VCFs), Angel Investors or such Alternate Investment Funds (AIFs). These investors have the funds to undertake such due-diligence process and analysis on their own and arrive at a decision. With such customized norms for informed investors, SMEs may find it easier to get listed which is accessible only to informed investors without having to make an IPO.

RequirementsThis separate institutional trading platform is available in an SME exchange for listing and trading of specified securities of SMEs for informed investors. Such listing may be availed of without going through a public offering process. In other words, this provides exit options to investors even where the company or the promoters do not require additional capital to be raised from the public.

CARE SME Digest January 2014

18

This facility is available to SMEs that meet certain conditions. Some of the conditions are as follows:1. The company has to meet entry norms specific to this segment to qualify for such listing without IPO. For

example, the company must be an SME judged by parameters such as revenues and paid up capital. Hence, the facility is available to companies that have completed not more than 10 years after incorporation and where their revenues have not exceeded Rs.100 crore in any of the previous financial years. Moreover, the paid up capital of the company must not have exceeded Rs.25 crore in any of the previous financial years.

2. In-order to ensure that the promoters continue to remain committed to the company even after listing, the regulator has made it mandatory that the promoters shareholding will be put under three years lock-in to the extent of 20% of shares held by him at the time of listing. Also, the companies that seek listing on this platform are not allowed to raise capital at time of listing. However, post listing they may raise capital through private placement under the extant regulations in this regard or through rights issue without the option to renunciation of rights.

3. The company must have a credible supporter who has a financial stake in it. This can include an alternative investment fund, angel investor, project financier, merchant banker, qualified institutional buyer or the like who has taken at least a certain financial stake (in equity or debt, as appropriate) in the company.

4. There are certain disqualification requirements, in the sense that the company should not be subject to certain circumstances such as winding up, labeling as a wilful defaulter, or the subject of a regulatory action under relevant legislation.

Apart from the above conditions, the SME who desire to list on this platform, the regulator has made it mandatory to provide timely disclosures like financial results and shareholding pattern on half yearly basis, corporate actions where corporate benefits are involved (like dividend, split, buyback, bonus, rights) and disclosure related to further raising of funds etc.

Exit from platformIf companies which get listed on ITP continue to be listed on it even after it has achieved a certain size, it may end up disproportionately consuming the capital which otherwise would go to SMEs. Therefore in-order to encourage companies which have grown beyond a size since listing to move to main market where there is wider investor participation and more capital available, SEBI says that companies which exceed Rs.25 crore in capital or revenues or market capitalization, are required to exit the platform within a period of 18 months. Also, companies which have remained listed on this platform for 10 years may also be required to compulsorily exit the platform after such period.

ConclusionThe regulations are timely in that they provide an exit opportunity to investors investing in SME. Since the regulator amended public issue norms to enable SMEs list without an IPO in October 2013, Delhi-based Gracious Software Limited and Kolkata-based Jaisukh Dealers Limited have approached to list their equity shares on Institution Trading Platform (ITP) of BSE SME. These companies are eligible for the listing in terms of 106 Y and other provisions of Chapter XC of the SEBI (ICDR) Regulations, 2009. The regulator is expecting around 10 to 15 companies to get list under this platform in a year’s time.

This may, in turn, help in raising capital by SME on better terms. It may also have an overall impact on the economy as the SME play an important role in growth and productivity. Besides, it is a good initiative to list companies, as when one gets listed on the ITP, it will put some corporate governance in place, which will make secondary sales easier. However, it would be interesting to see whether the SME and investor communities will adopt this route in line with the regulatory expectations.

Contributed by: Jagrut Khairnar, Manager

CARE SME Digest January 2014

19

Management and mitigation of project risks by SMEs

What is a project?According to the Project Management Institute, “a Project is a temporary group activity designed to produce a unique product, service or result. A project is temporary in that it has a defined beginning and end in time, and therefore defined scope and resources. A project is unique in that it is not a routine operation, but a specific set of operations designed to accomplish a singular goal. Projects must be expertly managed to deliver the on-time, on-budget results, learning and integration that organizations need. Project management, then, is the application of knowledge, skills and techniques to execute projects effectively and efficiently. It is a strategic competency for organizations, enabling them to tie project results to business goals — and thus, better compete in their markets”.

Essentially project, put in in simple terminology - in relation to the ongoing/existing businesses - is an additional activity, aside from the existing business operations, undertaken with clear timelines of start and end dates, with a view to deliver a clear result, most often in business perspective - the addition of capacity/infrastructure/markets to grow the business scale, at a certain pre-decided cost. These lead to the need for scope management, time management, cost management, other resources management and finally bringing the project related capex into commercial use, towards getting the incremental revenues from the same.

Project risk from a SME perspective Project risk in a typical SME setting is said to arise when the said entity plans to go in for the expansion of capacity. Where the size of the expansion is relatively high in relation to the existing available capacity and where the amount of investment involved is also high as a result, then the expansion assumes the nature of a project. For example: where a company has an existing spinning capacity of 16,000 spindles and it plans to double the capacity, then it is a project to be undertaken since the company is planning to enhance its capacity by 100%. Furthermore, the amount of investment in fixed assets planned in relation to the existing fixed asset base/net-worth has a bearing on whether expansion is in the nature of a project. For example, a company into the manufacture of castings with a fixed asset base of Rs.10 crore, now plans to replace a portion of the machinery which is old at a cost of Rs.1 crore, the same does not assume the complexion of a project.

This essentially is the definition of the scope of the project. What is the planned capex? For example, let us assume that Mr Sharma, who is in the hospitality business has planned to construct a 150-room new hotel at a cost of Rs.100 crore, this essentially is the scope of the project. It is important that SMEs fix the scope of the project clearly, because that will have a bearing on funding, planned incremental revenues, etc. If for example, the scope in the above instance increases to 250 rooms, then the funding pattern, the very layout and plans will all change significantly. Moreover, whether the additional 150 rooms will be absorbed by available demand, needs to be seen. Therefore, scope planning and management is critical.

Before we discuss the key project risks in detail, it would be pertinent to look at how project risk is perceived from the credit rating perspective.

Given the significant risks attached to the project, where a firm is amidst a project expansion or has planned for such project, the same will have to be considered carefully at the time of credit rating. Where a SME has planned to take on significant expansion, which is debt funded, the past experience of the promoters in the business and demonstrated capability at such previous capacity expansions are looked into. The ability of the company to tie up funds and the financial flexibility available is taken into consideration. Past demonstration

CARE SME Digest January 2014

20

of financial discipline or otherwise such as delays in project, cost, time over runs, past restructuring, stability of existing cash flows to support project obligations are considered.

The demand for the product and industry scenario is considered. Since rating is over the medium term, the present stage of the project is considered. Where it is at nascent stages with a long way to completion, it is a key risk as the outcome is dependent on number of variables over a long time horizon. As the rating is reviewed at periodical intervals, the status of the project is taken into consideration and depending on the intensity of the issues, where required, rating action is considered. Hence project risk, and past demonstration of the firm at handling such risk, do have a significant impact on rating.

What are the typical risks?Can the planned additional capacity be absorbed? A company which has embarked on a project of, let us assume, increasing the capacity of its plant from 150,000 diaries to 300,000 diaries would be faced with the following questions, which are essentially the key risks attached in this proposed expansion.

1. What is the addressable market?2. What is the present demand for the diaries?3. What is the present capacity which is being utilized?4. What is the additional demand in the market?5. Is there a need to add capacity given the present utilization levels?6. Can the incremental demand be sustained?7. Can the demand be met through job work?

The key issue here is that the significant addition to capacity comes at a high cost, in terms of the entire infrastructure to be created, the addition to employees, the additional raw materials to be sourced, the finance costs to be serviced, the relatively high principal repayment obligations, etc. So, the most important decision is whether the promoters believe that there is enough demand in the market to justify the doubling of capacity. Again while the promoters may believe that there is a case for expansion, this expansion itself may take six months to two years, depending on the project. During this period, the demand for the product may fall because subsequently, competitively priced products have come into the market, there are new substitutes, demand falls due to the cyclicality of the product, etc. These essentially embody the risk that the incremental capacity may not be effectively utilized because the incremental demand -and hence additional sales is misjudged.

For example, Mr Anand has a production capacity for 1 lakh non-critical auto components. He operates the same in a company, where he had a track record of 15 years, supplying the components to tier I suppliers, who in turn sold them to a large passenger car maker. His key client’s business was growing and Mr Anand also planned to add new clients. In anticipation of demand from the well-known tier I supplier (his key client), Mr Anand planned to expand his capacity by another 75,000 units. However, when the expansion project was nearing completion, Mr Anand received an unexpected jolt, that the passenger car maker was planning his own captive component unit, and hence the tier I supplier’s offtake was only expected to decrease not increase, as Mr Anand had envisaged. It is a case of inability to foresee what could be the turn of fortunes. Mr Anand had invested in additional machinery, increased the labour force and had taken additional electrical and other connections. More than Rs.10 crore invested till date in that project had now become redundant, with the additional need to service the principal and interest obligation on the debt drawn for creating fixed assets from which no incremental revenues will be seen!! The additional fixed costs to be borne without incremental revenues, leading to operating and net losses, meagre accruals (cash profits) and erosion of net-worth, purely because the decision to expand was taken without long term perspective.

CARE SME Digest January 2014

21

The decision on whether to get into the project needs to be firmly taken with the promoters experience in the business and supported by consultants in the respective fields. Once a firm decision is taken, where possible, a senior employee should be made in charge of the project with full responsibility, accountability and autonomy to ensure that the project is completed as planned and successfully integrated into the main business. He should be supported by a team of employees from the existing pool. However, given that SMEs continue to be one–man armies, the additional responsibility of this project needs to be ably tackled by the company owner/MD as the case may be.

Are physical resources available to support the expansion?If the promoters have a firm view that there is incremental demand to be met which can be done only through permanent addition to capacity, then the following additional questions arise:

8. Can the additional volume be sold at higher price to cover the incremental costs?9. What are the marketing arrangements that need to be made to sell the additional production?10. How many additional employees have to be recruited in the marketing department?11. Is there sufficient space available in the existing location of the plant to expand?12. Are there adequate supplies of utilities such as water, power etc?13. How many employees need to be added in the expanded plant?14. Is there enough availability of raw material to meet the incremental requirements?15. Negotiation with suppliers on the price and quantity of such raw material?16. Networking among existing and new clients, new markets to be tapped to absorb the additional

production, need to be carried out on war footing?17. Whether banks would support additional scale of operations by way of working capital funding needs

to be seen?

In the instance of availability of space for further expansion, it is more a question of investment in plant and machinery. However, if the existing space is not enough for the expansion, then the company needs to invest in land, which could prove to be relatively costly. Furthermore, whether the same would be available in the immediate vicinity of the existing plant is also a point of decision. If the distance between the existing and new plant is long, it may result in duplication of support systems.

The establishment of additional capacity such as plant and machinery requires a coordinated investment decision. The decision to procure machinery involves selection of most effective machinery, in terms of productivity and technology. At the same time, the availability of the same from domestic suppliers or the need to import needs to be looked at. Furthermore, the costs, logistics, forex impact arising from the import of capital equipment need to be managed.

How to fund the project The next critical question - once it is decided that project capex needs to be taken up - is the very means of funding such capex. Typically, the investment involved is high, much more than the accumulated net-worth of the company over the years. Given that SMEs are operated by entrepreneurs with relatively tight means of personal wealth, the ability of the promoters to bring in significant portion of the planned investment is relatively limited. The company has to necessarily look to term debt from banks to fund the capex, although a portion of it may be funded by additional equity/unsecured loans from the promoters. Also a smaller portion has to be funded out of the company’s profits.

Such funding by banks brings with it the need to service interest on a monthly basis and repay the principal as per agreed schedule. Furthermore, the banks would release the term loans upon achievement of certain

CARE SME Digest January 2014

22

milestones, after ensuring that the promoters have brought in their margin up to that stage. Additionally, the debt commitments need to be met out of the cash profits of the existing business. So, till such time that the additional capacity is brought to commercial use, no revenues would be generated therefrom. On the other hand, a number of additional costs such as employee costs, rent for additional space, interest, etc need to be supported out of the revenues from the existing business.

Although there is a moratorium provided for the term loan repayments and despite some of the costs not being charged to the profit and loss account, being classified as part of capital work in progress, still these additional expenses do impact the overall profitability. The PBILDT margins are impacted due to the higher operating costs (while revenues are delayed) and PAT is impacted by higher interest and depreciation charges As a result, the very accruals which have to support the additional principal obligations fall.

Where a project capex was planned to be completed after a gestation of one year, unfortunately gets delayed by say six months, the impact could be really high. This is because, the repayments of the additional debt would have been planned to commence from, let us say January 2014, on the premise that the capex would be completed by September 2013. So, additional repayments will have to be made from January 2014. But if as of December 2013, the project is only 70% complete, because initial delays in getting approvals resulted in dragging the project COD by three months, what essentially results are the following:

1. Date of commercial operations commencement gets delayed.2. This results in delay in production and attendant impact by way of delay in meeting the available demand.3. In case the product is custom made, delay in COD will result in delay in going to the market – as a result

some prospects may remain untapped, resulting in lower incremental client base.4. With delay in product, market penetration is delayed, thus leading to lower sales/share of incremental

business.5. With lower incremental revenues, the incremental fixed costs may not be fully covered, resulting in low

PBILDT margin/losses at the operating level itself for the incremental capacity.6. The huge interest and principal servicing however need to be complied with high incremental principal

commitments from January 2014.7. With the result, again the existing cash flows would be strained since they have to fund the losses of the

additional capacity.

Time delays in projects going on steam are one of the reasons for restructuring of term loans. Such restructuring of debt conveys poor financial discipline in the company.

How to avoid time delays in the project – Essence of project managementTime delays in projects are best avoided provided sufficient and in depth planning has gone into various facets of the project. The analysis of what are the variables which would constrain the project needs to be done thoroughly. For example, many projects could get delayed due to delay in getting regulatory approvals such as pollution control clearances. The key is to factor in the time required for getting these approvals at the time of envisioning the project. Another parameter is to ensure that activities in the project are broken down into manageable modules. Each such module should have a clear commencement and completion time to be monitored continuously. No slippages should be allowed on the same. Every minor delay or deviation should be reported and analyzed so that as a culture, no such delays are tolerated. Every module needs to be completed as planned and the head of the business has to drive everybody involved towards this end. The essence of the project is execution as per specification within the scheduled timeline. This aspect should be the focus of all attention.

CARE SME Digest January 2014

23

Cost over runs – another major riskThe project may have been envisaged at a total cost of say Rs.30 crore involving the construction of factory shed and installation of custom made machinery, towards increasing capacity. But while the project is underway, the cost of cement bags increase and labour shortage arising, requiring higher remuneration to be paid to labour. Also, steel prices and other input costs for building the customized machinery by the vendor have increased by let us say 20% in a volatile environment. Though a normal contingency of about 5% is envisaged in the project cost, the sudden increase of 20%, results into a cost overrun bringing with it immediate problems, the most important being how to fund the cost escalation.

This is because funds have been tied up and raised on a base case investment premise which itself has now been significantly altered. Unless the additional funds are made available, the project progress will be stalled. As a result, the financial plans for incremental revenue would be laid haywire. This is the impact of cost over runs. Although the same may eventually be funded through additional term loan/unsecured loans, the time delay in raising the funds would impact the revenue generation timeline from this project. The financial flexibility or the ability to raise funds at relatively short notice may not be an attribute of many SMEs, given the small size of net-worth. Also, such cost over runs show up the company in poor light in terms of poor financial discipline.

Managing project costs Hence, strict project cost control is critical. This can be brought about by daily/weekly variance reporting. This involves analyzing what was the scope of completion this week, requiring the use of what physical resources such as quantum of cement bags, at what purchase price/cost and comparing the same item by item, with the actual physical completion, physical resources actually utilized and the cost of the resource. This will throw up the positive and negative variances. Every material variance needs to be analyzed. Such meticulous control ensures the top management is aware of ground realities and can plan for looming problems. It will also provide physical as well as financial control to the project. It will also ensure that the project team is forever vigilant in task completion given the strict control and reporting at the top management level. This would also ensure that payments to contractors are thoroughly verified and retention money is retained to ensure performance for a particular predefined time period. Furthermore, such controls also lead to bankers’ confidence level being maintained or increased, thus creating the goodwill as well as the cushion to support any unforeseen contingencies.

Other project related slip-ups It is to be noted that this project is an additional and critical activity which essentially eats into the available time of the management. It is also possible that with significant attention being diverted to this project by the managing director, (who mostly is the individual responsible for overall management), the other aspects of the existing business may suffer since the management may not be able to concentrate on the market, make client calls as before, meet suppliers frequently, etc.

Furthermore, whenever there is a cost overrun, during the period that additional funds are being tied up, the company may draw on the available working capital funds to bridge the requirement. This will result in the existing operations being starved of working capital borrowings to fund the cash flow mismatches. Additionally, it also results in short term funds being used for long term purposes, which shows poor financial discipline. Adding to that if unfortunately, the business is cyclical and it happens to be a cash loss that year, even the small window available would be closed.

Hence, the project in-charge also needs to plan his/her time towards the existing business as well as the project in a SME set up.

CARE SME Digest January 2014

24

Project integration and commercial operationWith such meticulous control, the final step is to declare that the project is satisfactorily complete and it has established the objective earlier set out for it. This enables the additional capacity to be brought into commercial use. This also requires that immediately the other resources have to be so organized that incremental production/sales can happen smoothly. It also requires bringing the employees who were deputed to the project completion, into the main line business. Such integration of additional capacity would result in teething problems, which should be deftly handled.

ConclusionWhile projects are the key to grow the scale of operations and thus improve on many parameters such as market share, profitability, efficiencies in operation, etc, the same comes with numerous risks which have to be handled with great care and attention. This would essentially separate the best SME organizations from the relatively mediocre, because project risk management is fraught with challenges and a SME which has handled it well, would surely be stronger with the experience and thus set newer horizons for itself.

Contributed by:TA Seethalakshmi, Manager

CARE SME Digest January 2014

25

Trend of PE Investments in SME Segment

In the past few years, it has been observed that among the emerging markets, India has been the trendsetter than otherwise. The interest rates and amount of liquidity affect the yields on treasuries, which have shown an upward trend recently in the US, when that happens, it has a major impact on the global capital flows. This time is no exception; as a result emerging markets have seen large outflows.

Investments are driven by economic conditionsThe role of finance institution changes towards the private sector funding in financing projects as the countries they serve increasingly become “engines of global growth”, with the capacity, resources and entrepreneurial talent to make their own economic destinies.

Apart from the phase of economy, another major driver of PE investment is economic condition prevailing in the country. In India, though SME contributes significant towards the manufacturing sector output and presents opportunity for higher returns, the slowdown in economy has dampened the PE investor sentiment. The RBI’s financial stability report also raises concerns over the asset quality with total stressed advances ratio rose significantly to 10.2% of total advances as at end of September 2013 from 9.2% of March 2013 and highlighted that ‘medium and large’ sized industries contributed more towards stressed advances than ‘micro & small’ sized industries. This had resulted in lower PE investments following the general notion of SMEs being less resilient compared with large corporates in economic downturn.

TrendThe overall PE investment in India had followed the increasing trend with PE deals in July-September quarter grossing US$ 2.1 billion taking the total for the first nine months to US$ 8.13 billion which is 34% higher compared with the same period in 2012.

However, when we look towards investments into small and medium enterprises (SMEs), it had witnessed 25% fall on year to year basis (till November 2013). In 2013, investments into SME space totalled US$ 970 million across 132 transactions, whereas in 2012 investments for the similar period totalled US$1,296 million across 176 transactions. Comparable for 2011 were US$ 1,542 million across 202 transactions and US$ 1,258 million across 169 deals in 2010. (Source: Venture Intelligence report).

Investors are expecting trend to continue for 1-2 years, the improvement in economy can be good trigger point for new fund raisings pipeline which are focused on SMEs.

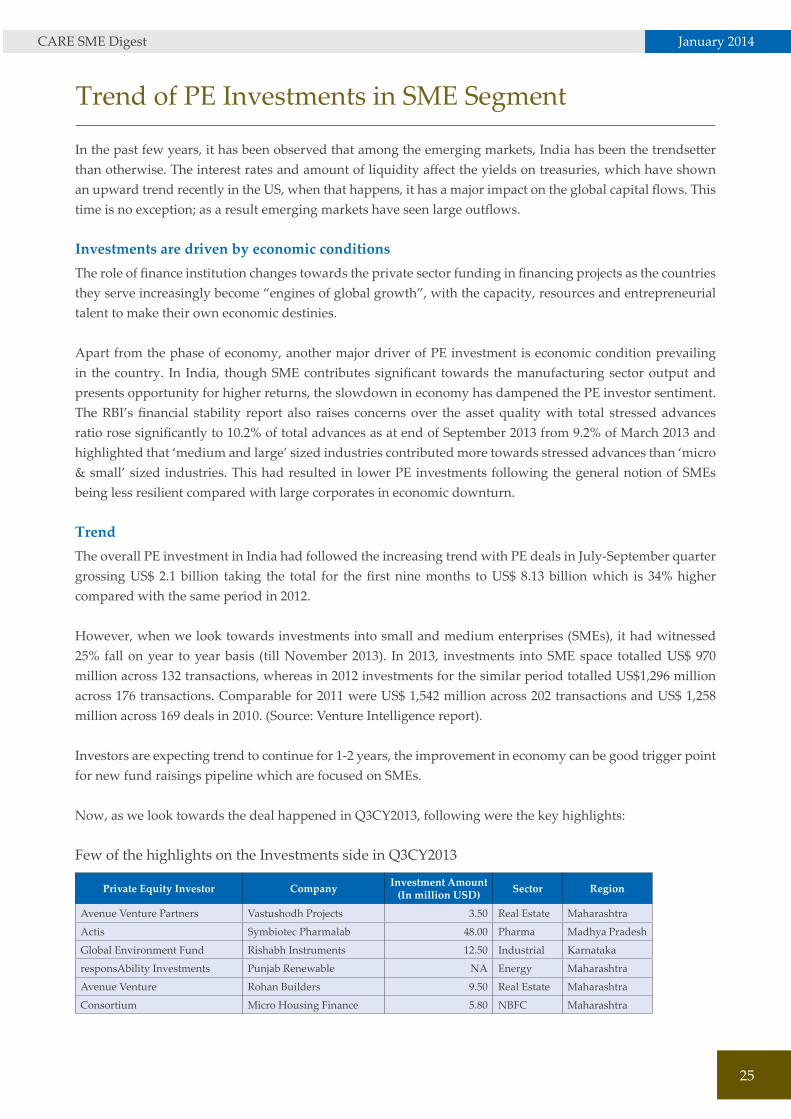

Now, as we look towards the deal happened in Q3CY2013, following were the key highlights:

Few of the highlights on the Investments side in Q3CY2013

Private Equity Investor Company Investment Amount (In million USD) Sector Region

Avenue Venture Partners Vastushodh Projects 3.50 Real Estate Maharashtra

Actis Symbiotec Pharmalab 48.00 Pharma Madhya Pradesh

Global Environment Fund Rishabh Instruments 12.50 Industrial Karnataka

responsAbility Investments Punjab Renewable NA Energy Maharashtra

Avenue Venture Rohan Builders 9.50 Real Estate Maharashtra

Consortium Micro Housing Finance 5.80 NBFC Maharashtra

CARE SME Digest January 2014

26

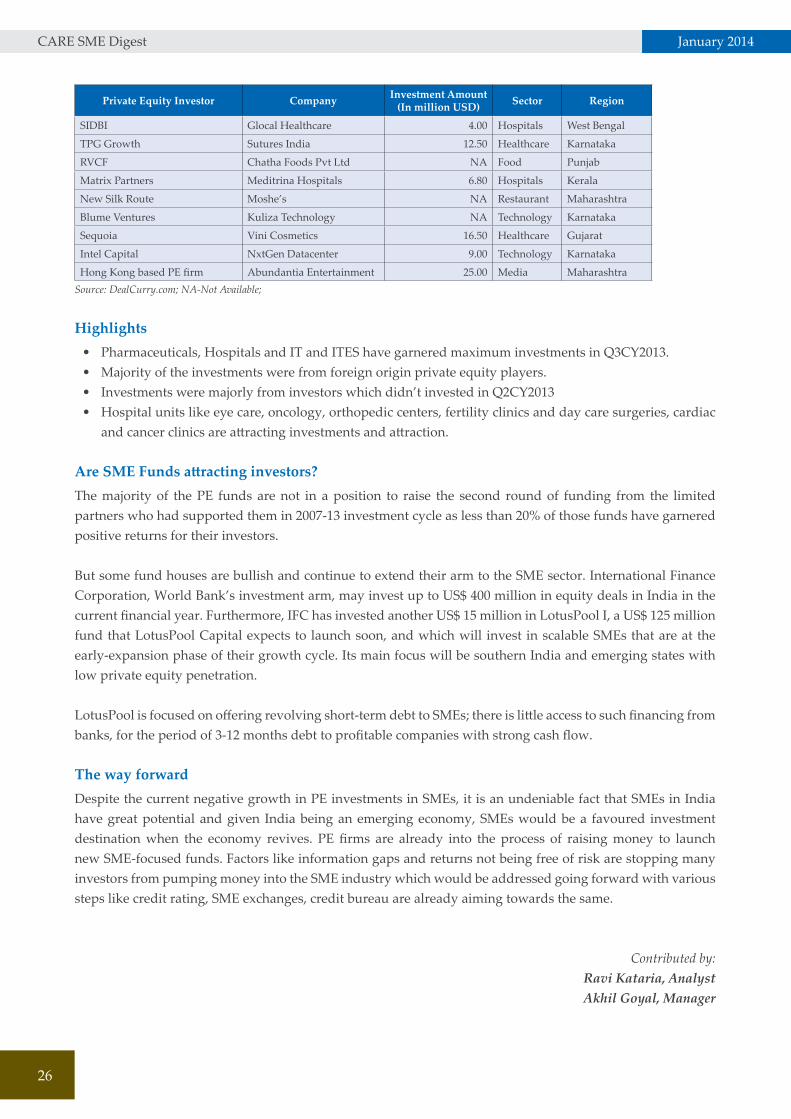

Private Equity Investor Company Investment Amount (In million USD) Sector Region

SIDBI Glocal Healthcare 4.00 Hospitals West Bengal

TPG Growth Sutures India 12.50 Healthcare Karnataka

RVCF Chatha Foods Pvt Ltd NA Food Punjab

Matrix Partners Meditrina Hospitals 6.80 Hospitals Kerala

New Silk Route Moshe’s NA Restaurant Maharashtra

Blume Ventures Kuliza Technology NA Technology Karnataka

Sequoia Vini Cosmetics 16.50 Healthcare Gujarat

Intel Capital NxtGen Datacenter 9.00 Technology Karnataka

Hong Kong based PE firm Abundantia Entertainment 25.00 Media MaharashtraSource: DealCurry.com; NA-Not Available;

Highlights• Pharmaceuticals, Hospitals and IT and ITES have garnered maximum investments in Q3CY2013. • Majority of the investments were from foreign origin private equity players.• Investments were majorly from investors which didn’t invested in Q2CY2013• Hospital units like eye care, oncology, orthopedic centers, fertility clinics and day care surgeries, cardiac

and cancer clinics are attracting investments and attraction.

Are SME Funds attracting investors? The majority of the PE funds are not in a position to raise the second round of funding from the limited partners who had supported them in 2007-13 investment cycle as less than 20% of those funds have garnered positive returns for their investors.

But some fund houses are bullish and continue to extend their arm to the SME sector. International Finance Corporation, World Bank’s investment arm, may invest up to US$ 400 million in equity deals in India in the current financial year. Furthermore, IFC has invested another US$ 15 million in LotusPool I, a US$ 125 million fund that LotusPool Capital expects to launch soon, and which will invest in scalable SMEs that are at the early-expansion phase of their growth cycle. Its main focus will be southern India and emerging states with low private equity penetration.

LotusPool is focused on offering revolving short-term debt to SMEs; there is little access to such financing from banks, for the period of 3-12 months debt to profitable companies with strong cash flow.

The way forward Despite the current negative growth in PE investments in SMEs, it is an undeniable fact that SMEs in India have great potential and given India being an emerging economy, SMEs would be a favoured investment destination when the economy revives. PE firms are already into the process of raising money to launch new SME-focused funds. Factors like information gaps and returns not being free of risk are stopping many investors from pumping money into the SME industry which would be addressed going forward with various steps like credit rating, SME exchanges, credit bureau are already aiming towards the same.

Contributed by:Ravi Kataria, AnalystAkhil Goyal, Manager

Industry Articles

CARE SME Digest January 2014

28

Indian Leather Industry

The Indian leather & allied industries are the country’s one of the oldest manufacturing industries which have been catering to the international market since the beginning. The leather industry has significant socio-economic importance in the Indian economy with it providing huge employment opportunities (approximately 2.5 million people, out of which around 30% are women), earning foreign exchange (equivalent to

4% of total export earning) and with more than two third of production contributed by small scale units. The leather & allied industries can broadly be classified into the tanning sector, footwear sector, leather garment sectors and leather accessories sector (including saddlery and harness). There are around 3,000 tanneries in India which produces around 2 billion square feet of finished leather annually.

Structure of the industry The leather and allied products industry in India includes fully integrated as well as standalone companies. The integrated player operates right from the collection of hides & skins, tanning & finishing and converting finished leather into leather products. The Indian leather industry is geographically well diversified. The production centres of leather and leather products are located at Chennai, Ambur, Ranipet, Vaniyambadi, Trichy, Dindigul in Tamil Nadu (TN), Kolkata in West Bengal, Kanpur and Agra in UP, Jallandhar in Punjab, Delhi, Hyderabad in Andhra Pradesh, Bangalore in Karnataka and Mumbai in Maharashtra. Tamil Nadu continues to be the largest export of finished leather & allied products from India.

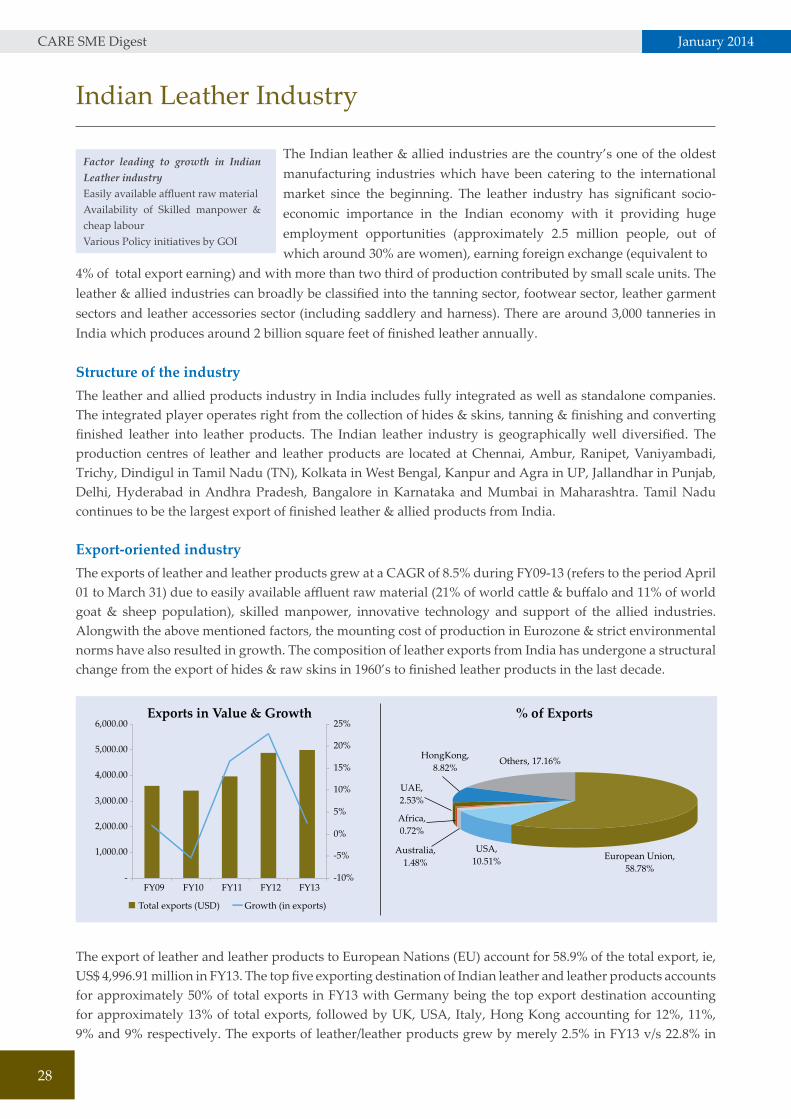

Export-oriented industryThe exports of leather and leather products grew at a CAGR of 8.5% during FY09-13 (refers to the period April 01 to March 31) due to easily available affluent raw material (21% of world cattle & buffalo and 11% of world goat & sheep population), skilled manpower, innovative technology and support of the allied industries. Alongwith the above mentioned factors, the mounting cost of production in Eurozone & strict environmental norms have also resulted in growth. The composition of leather exports from India has undergone a structural change from the export of hides & raw skins in 1960’s to finished leather products in the last decade.

The export of leather and leather products to European Nations (EU) account for 58.9% of the total export, ie, US$ 4,996.91 million in FY13. The top five exporting destination of Indian leather and leather products accounts for approximately 50% of total exports in FY13 with Germany being the top export destination accounting for approximately 13% of total exports, followed by UK, USA, Italy, Hong Kong accounting for 12%, 11%, 9% and 9% respectively. The exports of leather/leather products grew by merely 2.5% in FY13 v/s 22.8% in

Factor leading to growth in Indian Leather industry Easily available affluent raw material Availability of Skilled manpower & cheap labourVarious Policy initiatives by GOI

CARE SME Digest January 2014

29

FY12, primarily due to the slowdown in the demand from European Union (wherein except for UK, all the countries had shown de-growth). However, the marginally growth was supported by growing demands from Hong Kong, USA & UK. The industry has grown by 14.69% in the H1FY14 vis-à-vis H1FY13 primarily on the account of improved realization due to depreciation of rupee.

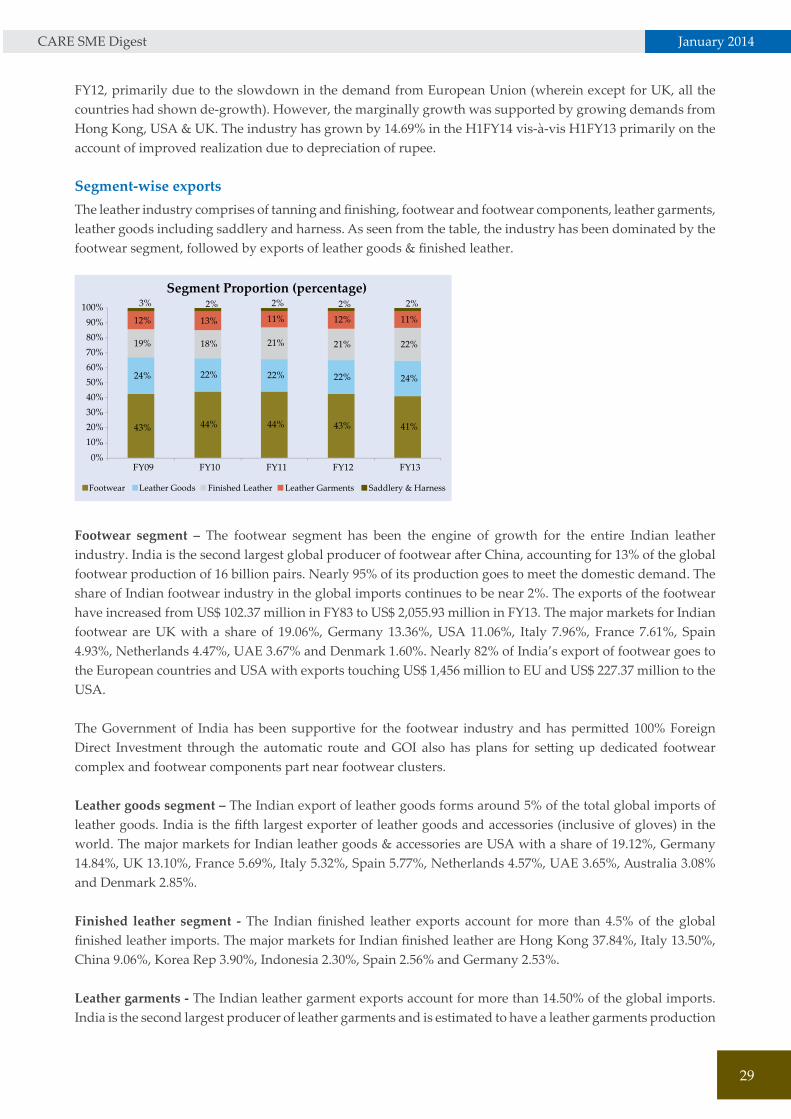

Segment-wise exports The leather industry comprises of tanning and finishing, footwear and footwear components, leather garments, leather goods including saddlery and harness. As seen from the table, the industry has been dominated by the footwear segment, followed by exports of leather goods & finished leather.

Footwear segment – The footwear segment has been the engine of growth for the entire Indian leather industry. India is the second largest global producer of footwear after China, accounting for 13% of the global footwear production of 16 billion pairs. Nearly 95% of its production goes to meet the domestic demand. The share of Indian footwear industry in the global imports continues to be near 2%. The exports of the footwear have increased from US$ 102.37 million in FY83 to US$ 2,055.93 million in FY13. The major markets for Indian footwear are UK with a share of 19.06%, Germany 13.36%, USA 11.06%, Italy 7.96%, France 7.61%, Spain 4.93%, Netherlands 4.47%, UAE 3.67% and Denmark 1.60%. Nearly 82% of India’s export of footwear goes to the European countries and USA with exports touching US$ 1,456 million to EU and US$ 227.37 million to the USA.

The Government of India has been supportive for the footwear industry and has permitted 100% Foreign Direct Investment through the automatic route and GOI also has plans for setting up dedicated footwear complex and footwear components part near footwear clusters.

Leather goods segment – The Indian export of leather goods forms around 5% of the total global imports of leather goods. India is the fifth largest exporter of leather goods and accessories (inclusive of gloves) in the world. The major markets for Indian leather goods & accessories are USA with a share of 19.12%, Germany 14.84%, UK 13.10%, France 5.69%, Italy 5.32%, Spain 5.77%, Netherlands 4.57%, UAE 3.65%, Australia 3.08% and Denmark 2.85%.

Finished leather segment - The Indian finished leather exports account for more than 4.5% of the global finished leather imports. The major markets for Indian finished leather are Hong Kong 37.84%, Italy 13.50%, China 9.06%, Korea Rep 3.90%, Indonesia 2.30%, Spain 2.56% and Germany 2.53%.

Leather garments - The Indian leather garment exports account for more than 14.50% of the global imports. India is the second largest producer of leather garments and is estimated to have a leather garments production

CARE SME Digest January 2014

30

capacity of 16 million pieces annually. The major markets for Indian leather garments are Germany with a share of 23.18%, France 13.55%, Spain 11.88%, Italy 10.99%, USA 7.49%, UK 6.16%, Netherlands 3.80%, Denmark 3.47% and Canada 2.31%.

Saddlery & Harness - The Indian export of Saddlery & Harness products forms around 8% of the total global imports. The saddlery & harness products are primarily manufactured primarily in Kanpur. The major markets of Indian saddlery & harness are Germany with a share of 20.22%, USA 15.28%, UK 11.55%, France 8.12%, Australia 7.04%, Netherlands 6.39%, Sweden 6.11%, Belgium 4.72%, Canada 3.31%, Denmark 2.82%, Spain 2.27%, Italy 2.71%.

SMEs in leather industry The Indian leather & leather product is very competitive and dominated by micro and small units, with more than two third of production & 95% of the total manufacturing units contributed by small scale units. The footwear and saddlery and harness segments have the highest shares of the household, tiny and cottage sector. In the tanneries segment, the presence of the medium and large-scale sector is the strongest with around 55% share. The presence of small- scale units is the highest at 95% in garments, followed by leather goods, saddlery and harness.

Major problems faced by the leather industry Though government policies towards the industry have been supportive both for small-scale sector development as well export promotion, the major internal factors which have acted as deterrent for the higher growth are low access to capital, high per capita cost, taxation, fluctuating currency and low investment in technology. In addition to the above, the industry is also caught up with socio-political issues relating to slaughtering of animals. Furthermore, the availability of power in the state of Tamil Nadu & others has also impacted the capacity utilization of the leather manufactures.

Heterogeneous raw material & labour intensive The essential requirement for manufacturing leather products is the production of raw hides and skins from either dead or slaughtered animals. Though India has the largest livestock population in the world, raw material availability and quality is the main constraints for the sector. The available livestock are scattered and diffused throughout the country and their collection practices vary from region to region. Recovery takes place from both slaughtered as well as fallen (dead) animals and very often livestock that die are not recovered for days and sometimes weeks, affecting the recovery rates which are much lower than their potential. Furthermore, due to religious beliefs, the slaughtering of cow is not allowed in the large parts of India. Moreover, the industry is highly labour intensive with use of technology being considered for increasing export competitiveness and improving the quality of finished goods.

CARE SME Digest January 2014

31

Working capital intensive nature of operations The finished leather & leather manufacturing industry is primarily working capital intensive in nature primarily on account of the higher credit period offered (to circumvent the lower bargaining power & intensely competitive industry landscape) coupled with the moderate to high inventory stock of both raw material & finished product. The prolonged slow down during 2009 had impacted the liquidity profile & credit worthiness of players in the leather industry.

Government policies The Government of India has identified the leather industry as a ‘focus sector’ in its foreign trade policy 2004-09, in view of its immense potential for export growth and employment generation. With leather manufacturing majorily dominated by small sector entities, the GOI has implemented various special focus initiatives (under the foreign trade policy) & export measures to improve the competitiveness of the industry on a global scale. The other areas focused by the government include skilled manpower development, availability of innovative technology, increasing industry compliance to international environmental standards and ensuring dedicated support of allied industries.

During the 11th Five Year Plan period (2007-2012), the Department of Industrial Policy & Promotion (DIPP) has implemented an Indian Leather Development Programme (ILDP) for the overall growth of the leather sector, with a total plan outlay of Rs.1,251.29 crore. However, for the 12th Five Year Plan (2012-2017), this outlay has been increased to Rs.3,600 crore. The thrust of the ILDP scheme is on technology upgradation, modernization of production units, expansion of production capacities, creation of institutional facilities in the country and training human resources for the leather sector, providing support to rural artisans for design and product development, creating market linkages and helping the tanning sector achieve environment conservation, among other things.

OutlookThe planning commission expects leather production to grow at a CAGR of 13% during FY13-15 led by a rising disposable income, lower presence of footwear and leather component in total consumption expenses of household, abundance of leather as raw material and lower cost for manufacturing set up. The ILDP scheme for modernization and technical upgradation of the Indian leather sector covering tanneries, footwear, leather goods and garments is expected to pave the way for better future growth. The exports market are expected to continue to grow amidst the EU & US crisis primarily on the account of the increase competiveness and led by footwear and leather garments.

Contributed by: Nitesh Dhoot, Manager

This pag

e is i

ntentio

nally

left b

lank

Rating Guide

CARE SME Digest January 2014

34

Rating Approach for SME / MSE Ratings

BackgroundSME (Small and Medium Enterprises) segment plays a very vital role in the economic development of our nation. On the other hand, credit risk assessment in this segment requires a specific approach as the factors affecting the creditworthiness are somewhat different compared with large corporate entities. Hence, to further support the growth for this sector and help the investors to determine the relative creditworthiness of entities belonging to this segment a need for separate rating product was felt. Accordingly, CARE introduced SME ratings in 2006, which are intended solely for Small and Medium Scale Enterprises. Furthermore, CARE has signed a Memorandum of Understanding with National Small Industries Corporation Limited (NSIC) to introduce the NSIC – CARE Performance and Credit Rating for MSEs. This is a special rating product for units registered as MSEs.

SME RatingSME Rating indicates the relative level of creditworthiness of an SME entity, adjudged in relation to other SMEs. It is an issuer-specific rating reflecting the overall general creditworthiness. It is a one-time assessment of credit risk of the rated entity in comparison with the other SMEs.