smallholder development directorate: small holder development date: 20 october 2011

TRANSCRIPT

SMALLHOLDER DEVELOPMENT

DIRECTORATE: SMALL HOLDER DEVELOPMENT

DATE: 20 OCTOBER 2011

BACKGROUND

• NB to note that South Africa’s farmers, subsistence, smallholder and commercial, all play an important role; a role with various dimensions

• Smallholder sector produces less and sales may be relatively small, this sector plays a pivotal role in the communities where smallholder farmers operate.

• Main reasons for production is food production, income generation, employment creation, provide a social safety net, capital formation and for various cultural reasons.

• Commercial Agricultural Sector is well developed and private and public services rendered to this component of the Sector are comparable with the best in the world.

• Subsistence and smallholder farmers and their plight is often exacerbated by the fact that they are usually totally dependent on public services

• Emphasis on subsistence and small holder producers due to their ability to:- Promote food security- Market access- Job creation and sustainable livelihoods.

2

FARMER DEFINITIONS (3 categories)

• Subsistence/resource-poor farmers NB: USE OF PRODUCER VS FARMER

- Farmers that, due to resource constraints, and using limited technology, produce food to supplement their household food needs, with little or no selling of produce to the market.

• Smallholder farmers

- The smallholder farmers produce for household consumption and markets, earn revenue from their farming businesses as a source of income for the family. Farming is erratic and not always the main source of income; diverse non-farm sources of income exist to sustain the family. There is potential to expand operations and graduate to commercial farmers, if provided comprehensive support (technical, financial and managerial instruments).

• Commercial farmers

- Farmer’s production primarily for the market and makes considerable living from farming. Classification as commercial: farm income must exceed a minimum economic size. Due to the expensive nature of capital formation and implementation of technological processes, the landowners of such farms are often large in scale to counteract the low returns on investment of the sector.

3

SMALLHOLDER PRODUCER SUPPORT MANDATE

DAFF is committed to the following national and international agendas:

The CAADP framework is built around 4 main technical pillars:

• Expanding the area under sustainable land management and reliable water control systems- reduce fertility loss & resource (land, forestry, water) degradation: smallholder & commercial sectors.

• Improving rural infrastructure and trade-related capacities for market access – NGP?.

• Increasing food supply and reducing hunger: Zero Hunger Plan??

• Expanding agricultural research and the dissemination and adoption of technology -FARA.

• Realization of the MDG 1 - Eradication of extreme poverty and hunger by 2015

• Maputo AU Declaration on Agriculture and Food Security in Africa of 2003

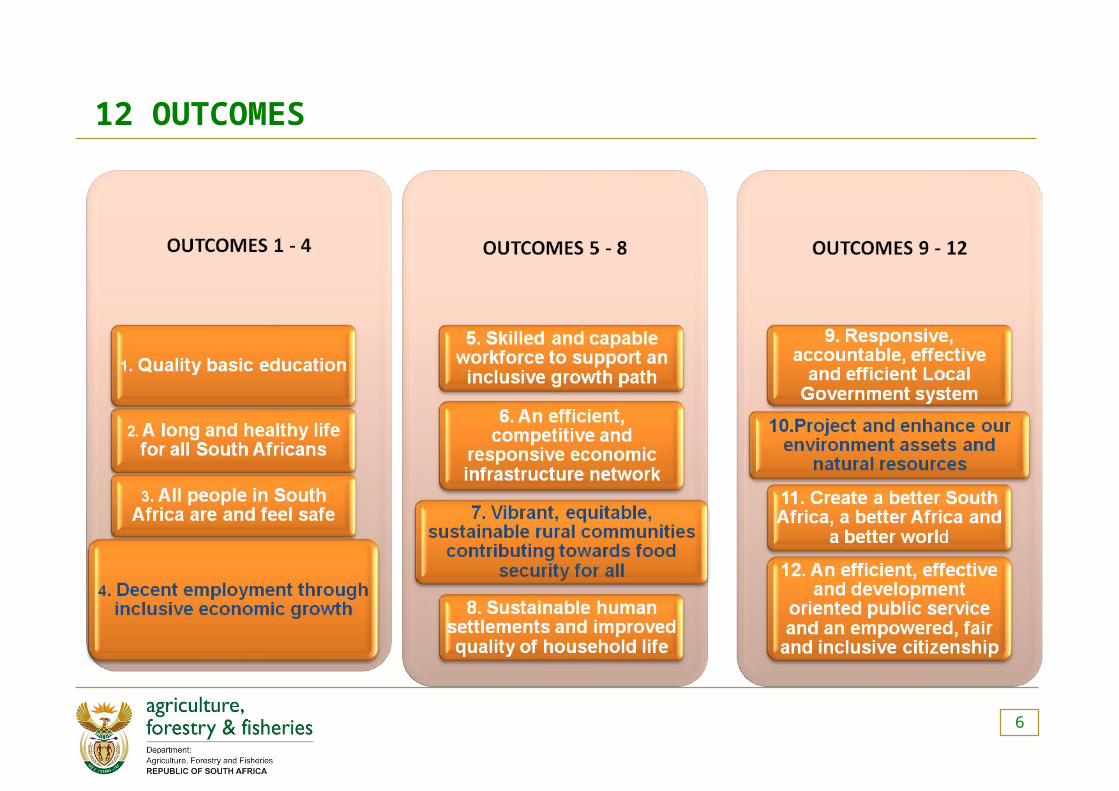

• Contributing meaningfully to the realization of SA government’s Programme of Action – 12 Outcomes, particularly outcomes 4, 7 & 10 (4 – jobs; 7 – support & develop 50 000 smallholder producers & 10 – enhanced environmental assets & natural resources).

4

PRODUCER SUPPORT MANDATE

• Sections 27 (1) (b) and 32 (1) (a) of the Constitution, 1996, right to access food & information.

• Contributing to the New Growth Path: 2020 target: opportunities for 300 000 smallholder producers, 145 000 jobs in agro-processing & improved conditions for 660 000 farm workers.

• Support to smallholder producers - ensures food security, full utilization of resources, e.g. land, job creation and the overall achievement of the Presidential

Outcomes, in particular Outcome 7: outputs 1 and 5: target 50 000 newly established smallholder producers by 2013/14 and 30% of producers organised into associations/ commodity groups for improved market access, respectively

5

12 OUTCOMES

6

CAADP & CURRENT INITIATIVES: ZERO HUNGER INITIATIVE

CAADP’s goals are that by 2015 Africa should less than 5 years from now:

• Attain food security;

• Improve agricultural productivity to attain a 6 percent annual growth rate - OECD;

• Develop dynamic regional and sub-regional agricultural markets;

• Integrate farmers into a market economy; and

• Achieve a more equitable distribution of wealth.

Objectives of the Zero Hunger Programme

• Ensure access to food by the poor and vulnerable members of our society

• Improve food production capacity of resource poor farmers.

• Improve nutrition security of the citizens.

• Develop market channels through bulk government and private sector procurement of food linked to the emerging agricultural sector.

• Fostering partnerships with relevant stakeholders within the food supply chain.

7

CAADP & CURRENT INITIATIVES: SMALLHOLDER PRODUCERS

SHP: FOCUS • The former homelands - a large concentration of subsistence & smallholder

producers with a sizable number of hectares of under-utilized arable land –estimated at 60%.

• Smallholder Producers - that will be established and supported on land acquired through land reform, in close collaboration with DRDLR.

• Conservation agriculture becomes critical due to its labour and cost saving ability

• The call for improved technology and better production systems – research

• Assumption for zero hunger: Subsistence producers may contribute 20% and smallholder producers should contribute 80% of their produce towards the programme.

8

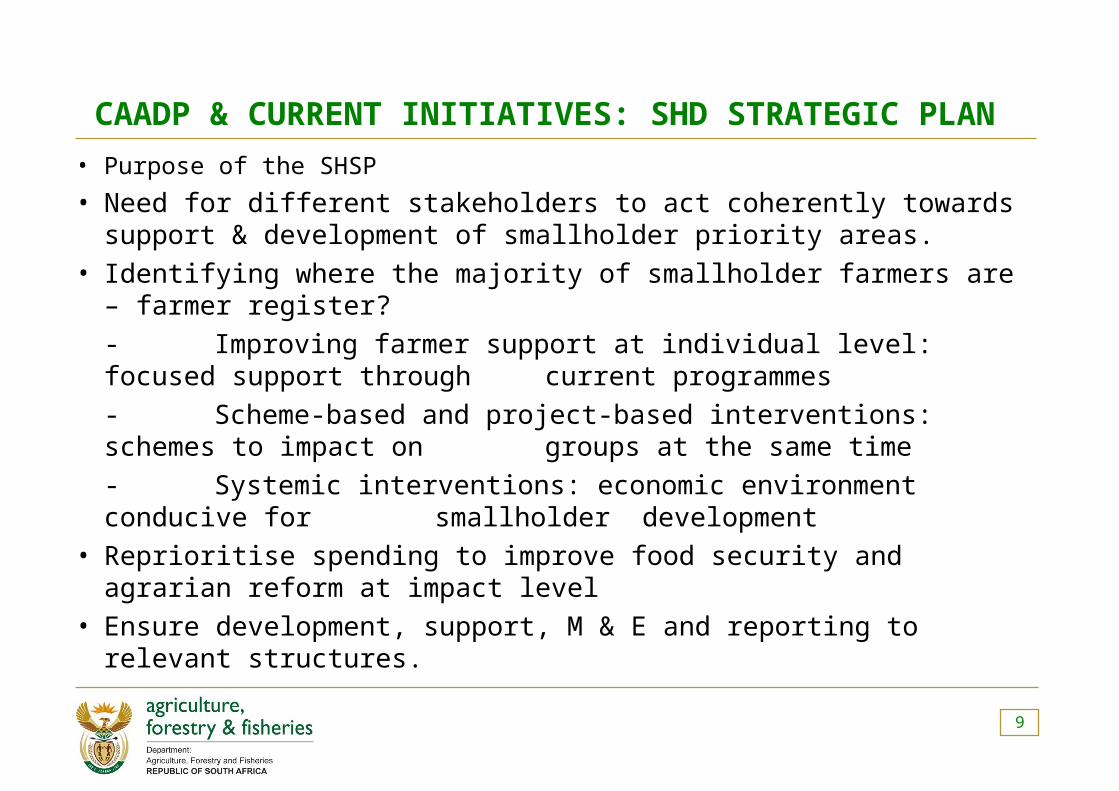

CAADP & CURRENT INITIATIVES: SHD STRATEGIC PLAN

• Purpose of the SHSP

• Need for different stakeholders to act coherently towards support & development of smallholder priority areas.

• Identifying where the majority of smallholder farmers are – farmer register?

- Improving farmer support at individual level: focused support through current programmes

- Scheme-based and project-based interventions: schemes to impact on groups at the same time

- Systemic interventions: economic environment conducive for smallholder development

• Reprioritise spending to improve food security and agrarian reform at impact level

• Ensure development, support, M & E and reporting to relevant structures.

9

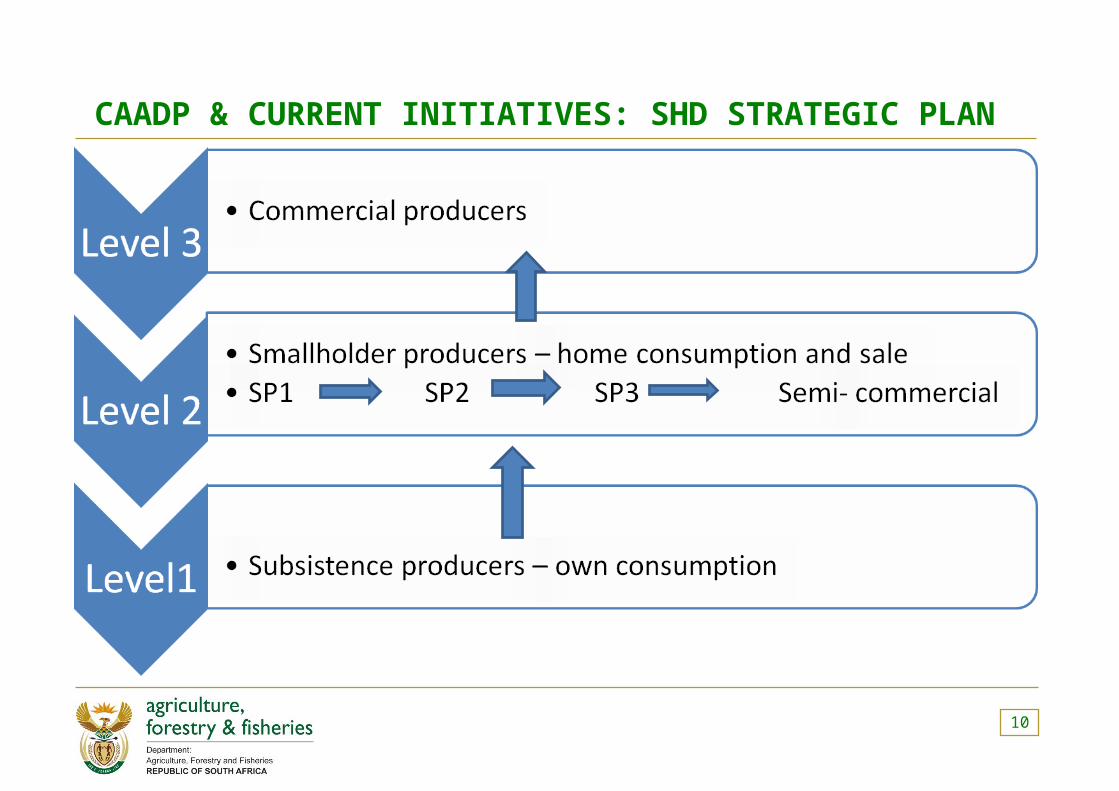

CAADP & CURRENT INITIATIVES: SHD STRATEGIC PLAN

10

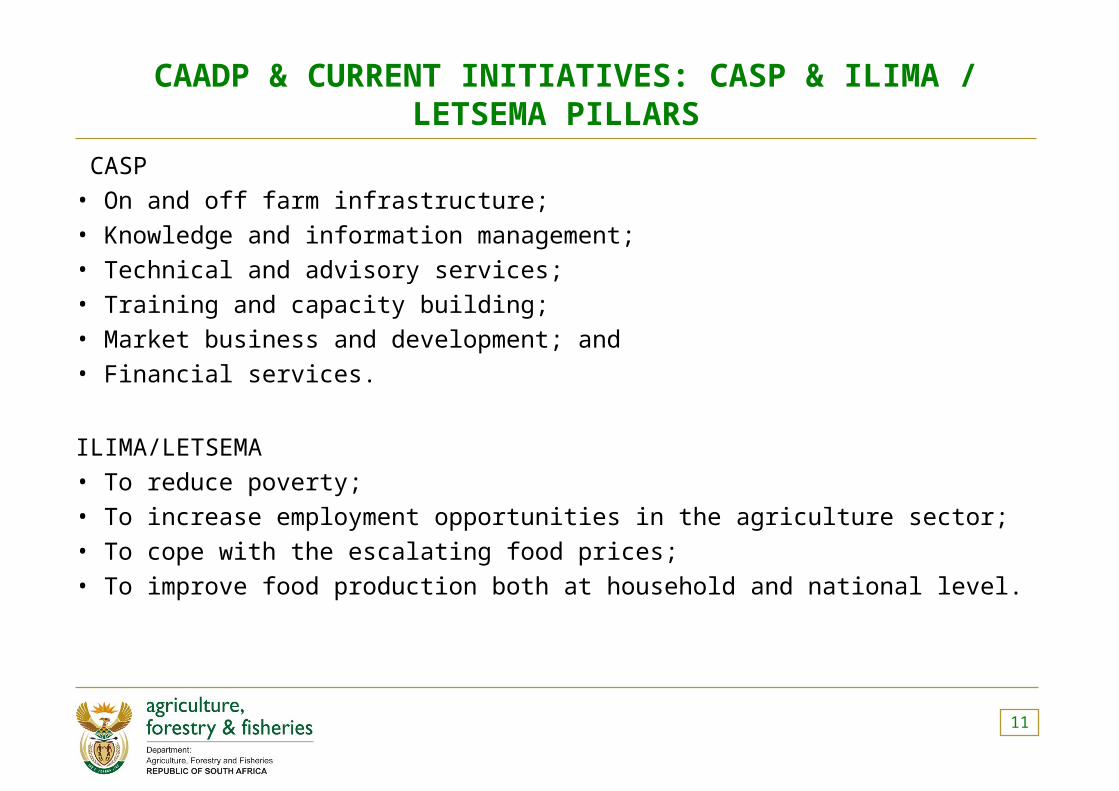

CAADP & CURRENT INITIATIVES: CASP & ILIMA / LETSEMA PILLARS

CASP

• On and off farm infrastructure;

• Knowledge and information management;

• Technical and advisory services;

• Training and capacity building;

• Market business and development; and

• Financial services.

ILIMA/LETSEMA

• To reduce poverty;

• To increase employment opportunities in the agriculture sector;

• To cope with the escalating food prices;

• To improve food production both at household and national level.

11

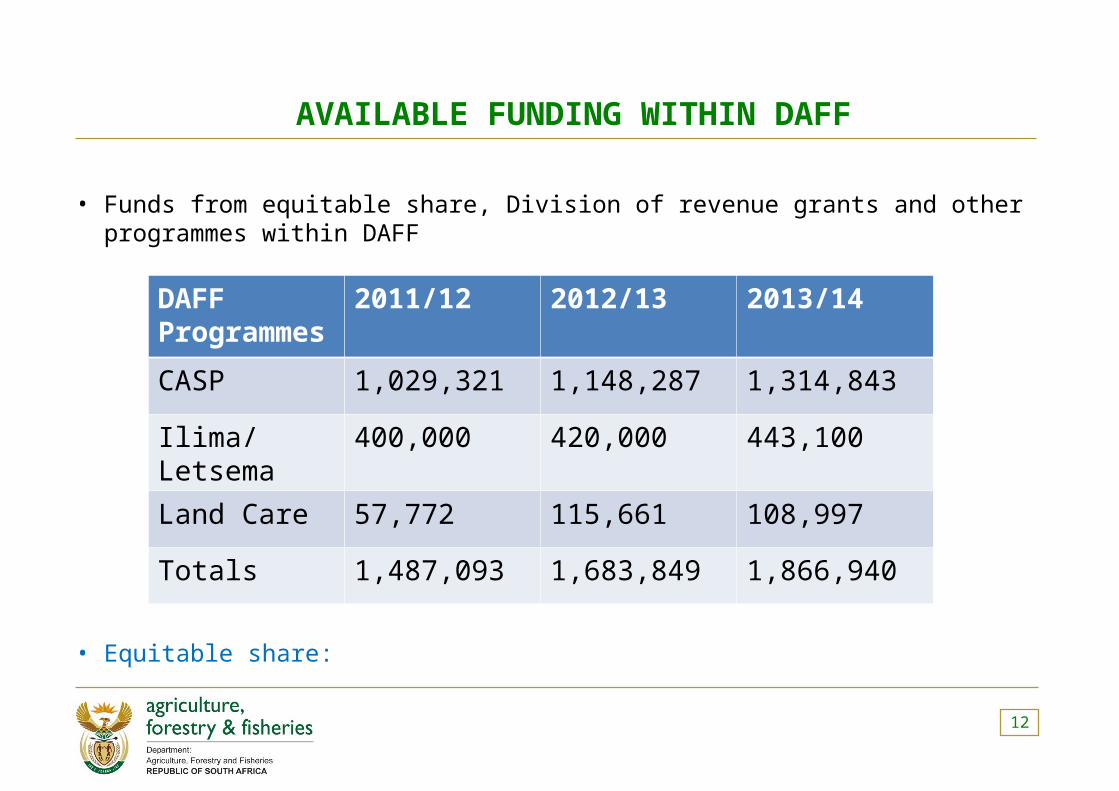

AVAILABLE FUNDING WITHIN DAFF

• Funds from equitable share, Division of revenue grants and other programmes within DAFF

• Equitable share:

12

DAFF Programmes

2011/12 2012/13 2013/14

CASP 1,029,321 1,148,287 1,314,843

Ilima/Letsema 400,000 420,000 443,100

Land Care 57,772 115,661 108,997

Totals 1,487,093 1,683,849 1,866,940

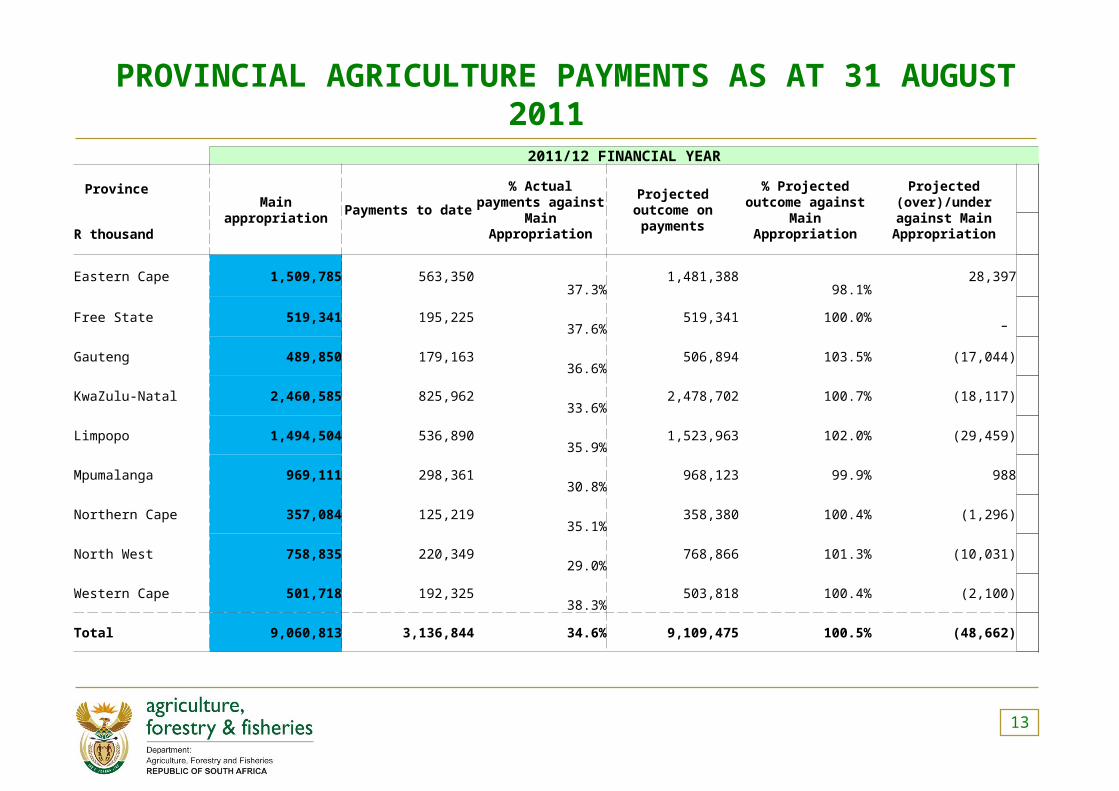

PROVINCIAL AGRICULTURE PAYMENTS AS AT 31 AUGUST 2011

13

2011/12 FINANCIAL YEAR

Province

Main appropriation Payments to date% Actual payments

against Main Appropriation

Projected outcome on payments

% Projected outcome against

Main Appropriation

Projected (over)/under against Main

AppropriationR thousand

Eastern Cape 1,509,785 563,35037.3%

1,481,38898.1%

28,397

Free State 519,341 195,22537.6%

519,341 100.0% –

Gauteng 489,850 179,16336.6%

506,894 103.5% (17,044)

KwaZulu-Natal 2,460,585 825,96233.6%

2,478,702 100.7% (18,117)

Limpopo 1,494,504 536,89035.9%

1,523,963 102.0% (29,459)

Mpumalanga 969,111 298,36130.8%

968,123 99.9% 988

Northern Cape 357,084 125,21935.1%

358,380 100.4% (1,296)

North West 758,835 220,34929.0%

768,866 101.3% (10,031)

Western Cape 501,718 192,32538.3%

503,818 100.4% (2,100)

Total 9,060,813 3,136,844 34.6% 9,109,475 100.5% (48,662)

END

IT IS ESTIMATED THAT 80% OF FARMERS IN AFRICA ARE SMALLHOLDER FARMERS – ON ± 2HA

NEED FOR LINKAGES AND INCLUSIVE PLANNING TO ACHIEVE THE SET DETAILS STATED ABOVE

THANK YOU

14