smart balance - nyu stern school of...

TRANSCRIPT

SMART BALANCE

Todd Tamagnini

Neha Gaddam

Overview

• Company description

• Products

– Market Share

– Supply chain

• Growth catalysts

• Risks

• Valuation

The Company

• Smart Balance distributes heart healthy and low fat

food products (‘functional foods’) in the United

States

• Products include buttery spreads, Popcorn, Oil, Oil

spray, mayonnaise, cheese, Peanut Butter

• $500m market cap

• SB acquired by boulder specialty brands (BSB) in ‘07

for $491m

Notable Features

• #3 player in Margarine (13% of 1.1B market)

• Patented technology for naturally occurring Trans fat-free oils, expires in 2015

• Outsourced Manufacturing - Virtual Business model, focus on Sales and marketing

• No fixed assets, Third part distribution network, National

sales agency (Acosta), Co-manufacturing, Value added

management (Close Relationship With Acosta)

What’s So Special About SB?

• Improves the HDl/LDL ratio (promotes ‘good’ cholesterol)

• Free of hydrogenated oils and trans fatty acids

• Unlike other brands, it doesn’t use sterol or stanol esters

Corporate History

Pre-1996: Robert Harris

(Weight Watchers) starts GFA

brands

1996: GFA licenses a patented blend of natural

vegetable oils

1997: GFA launches

Smart Balance margarine

2005: Boulder specialty

brands (BSB) formed as a blank check

company

2007: BSB acquired GFA and changes its name to

Smart Balance

Capital Structure

Price 7.90

Shares Outstanding 62,000

Market Cap 49,4000

Cash 7,000

Debt 90,000

Enterprise Value 580,000

• Recently recalled all preferred stock and warrants

•Used proceeds to pay down debt

Buttery Facts

Market Share increased from 2.4% to 12.6%

Smart BalanceTM Products

Current Products Recent launches (2007) Future scope (2009?)

Buttery spreads Butter Blend Stick Yogurt

Omega Peanut Butter Milk(with omega-3s and Vit E)

Sour cream

Omega Cooking Oil Cream Cheese Oatmeal

Omega plus light Mayonnaise

Popcorn

Cheese

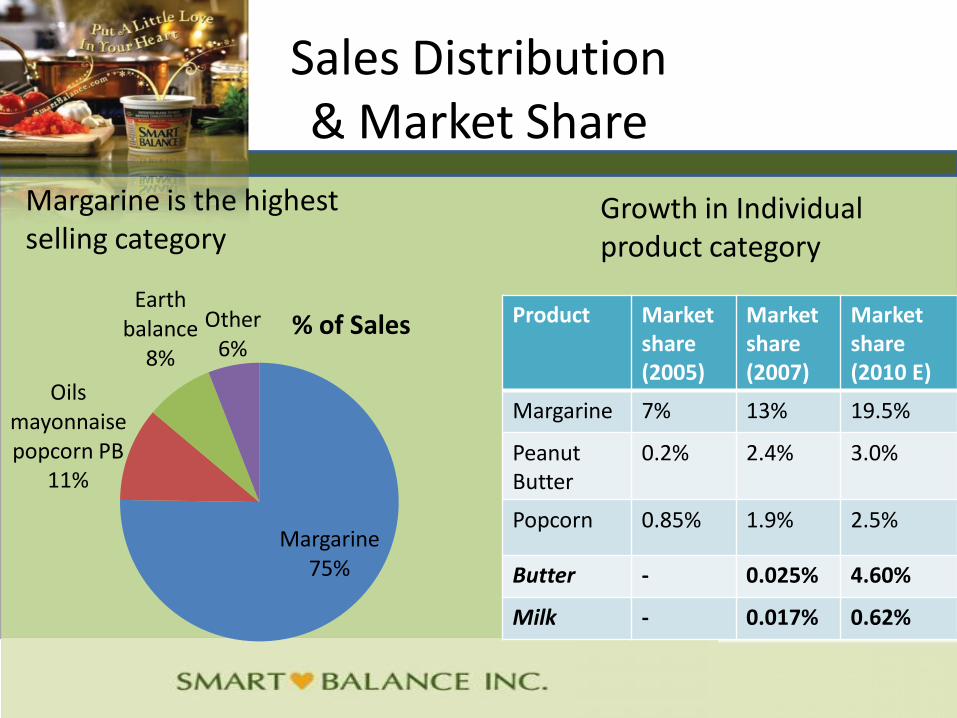

Sales Distribution& Market Share

Margarine75%

Oils mayonnaise popcorn PB

11%

Earth balance

8%

Other6%

% of Sales Product Market share (2005)

Market share (2007)

Marketshare(2010 E)

Margarine 7% 13% 19.5%

PeanutButter

0.2% 2.4% 3.0%

Popcorn 0.85% 1.9% 2.5%

Butter - 0.025% 4.60%

Milk - 0.017% 0.62%

Margarine is the highest selling category

Growth in Individual product category

19.8% 19.1% 19.0%18.0% 17.6% 17.5%

13%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

San Francisco

New York Portland Boise Denver Seattle Total US

Smartbalance Mkt Share

Select Markets

Target Market

1B

5B

25B

0

5

10

15

20

25

30

Core (margarine)Initial Expansion (oil, PB, popcorn, mayo)Target Expansion (cheese, cream cheese, milk, other)

Market Size ($Billion)

Supply Chain & Control

Outsourced Manufacturers

Third party Distributors, Warehouses Supermarket chains

• Business model that works on 50 employees

• Consultants at each site, quality control reportsNegotiate certain commodities & packaging costs with suppliers

Price = Cost of ingredients + Packaging + Fixed toll charge

Pay monthly handling and logistics fees, freight charges

Internal sales force and sales agency Acosta, Inc.

Leading Customers

• Wal- Mart

• C&S Wholesale

• Kroger

• Publix

• Safeway

Growth Catalysts

• Rapid growth of the company

• Expansion in product lines & consumer retention

• Increase marketing spending

• Great management

• Drivers of functional food industry

• Penetration opportunity

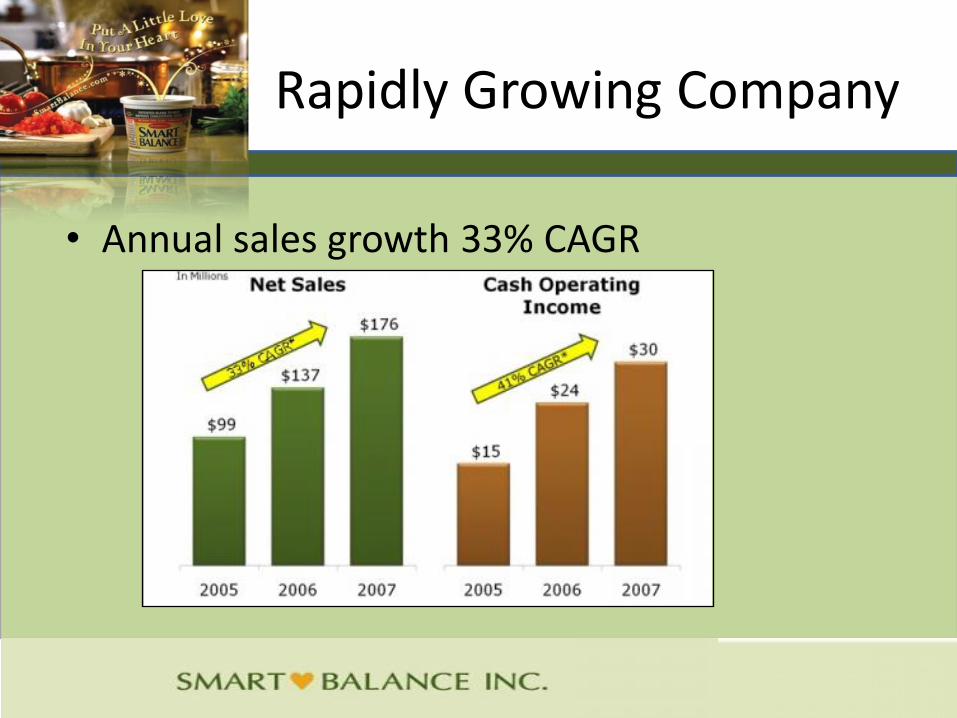

Rapidly Growing Company

• Annual sales growth 33% CAGR

Expanding Product Lines & Consumer Loyalty

• Expansion into other product lines –cheese, milk, cream cheese

• Ability to retain old consumers and attract new ones

57%

42% 42% 46%

33%

50%41%

35%

Smart Balance

Mayonnaise w/ Omega

Smart Balance

Cooking Oil

Smart Balance Popcorn

Smart Balance Peanut

Butter w/ Omega

Analysis of consumers

% tried SB Spreads % New to SB

• Increase in marketing spending, and target population base

– Increase marketing expense from $20m to $40m

– Research on consumers: 80% revenues generated by 2-4m of 44m potential households

– Pay higher slotting fee

Increase Marketing

High-caliber leadership –Stephen Hughes

• CEO – Stephen Hughes (25 years)– (1988-1992) led the development of Healthy Choice frozen food line

(revenues grew from 0 to 1B)

– (1994-1996) executive vice president of Tropicana Products (Led turnaround of US business, increasing sales from 1B-2B in four years)

– (1997-2000) CEO of Celestial Seasonings (Grew Revenue from 75-125m)

– (2000-2002) CEO of Frontier Natural Product

– (2002-2004) White Wave Foods (Part of Dean Foods) Grew Silk brand from 175-400m in two years

• CFO – Bob Gluck– Bestfoods

– Unilever

• Management Stock Ownership: 6%

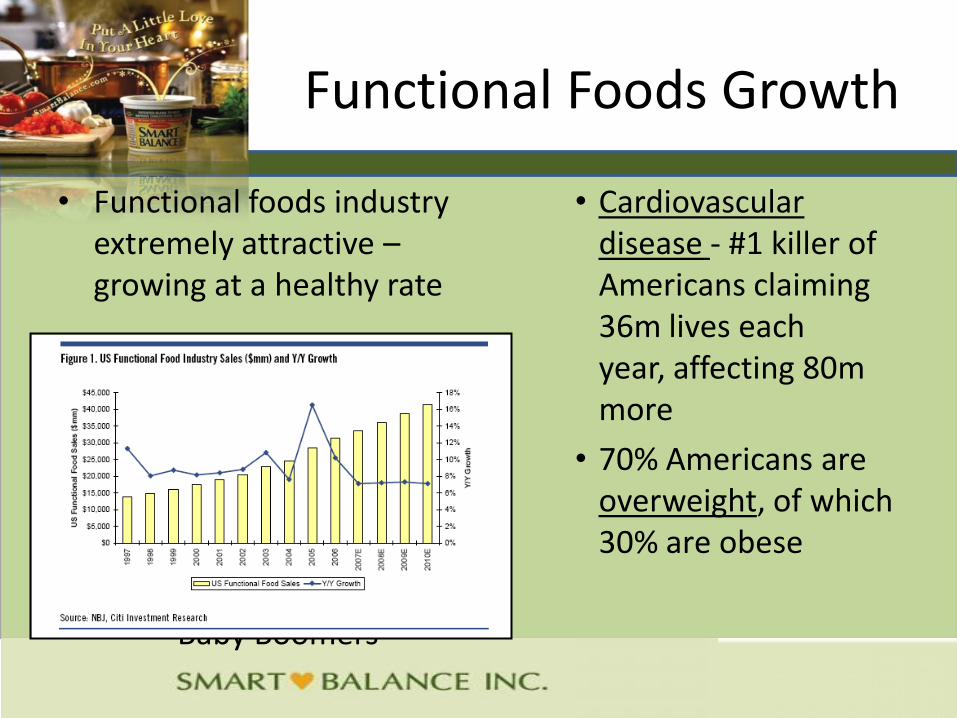

Functional Foods Growth

• Functional foods industry extremely attractive –growing at a healthy rate

• Baby Boomers

• Cardiovascular disease - #1 killer of Americans claiming 36m lives each year, affecting 80m more

• 70% Americans are overweight, of which 30% are obese

Low Penetration, High Growth = ‘Smart’ Opportunity

5%-1%

6% 9%

52%

40%

2% 3%

Breakfast Foods Fresh Juice Dressings & spreads

Dairy (milk, butter)

Y/Y growth Functional food penetration

SB product categories: Dairy & condiments, dressings spreads, sauces – low penetration and high growth

• Strong Insider Buying

• Large hedge funds in stock, more coming in

• O. O. S. Capital

Insider Buying /Large Institutions

It tastes good..

Our Final Pitch

• American Culinary ChefBest award:

judged best among

competitors

• Great consumer reviews and brand

loyalty

Risks

• Product concentration

• Customer concentration

• Commodities

• Competition

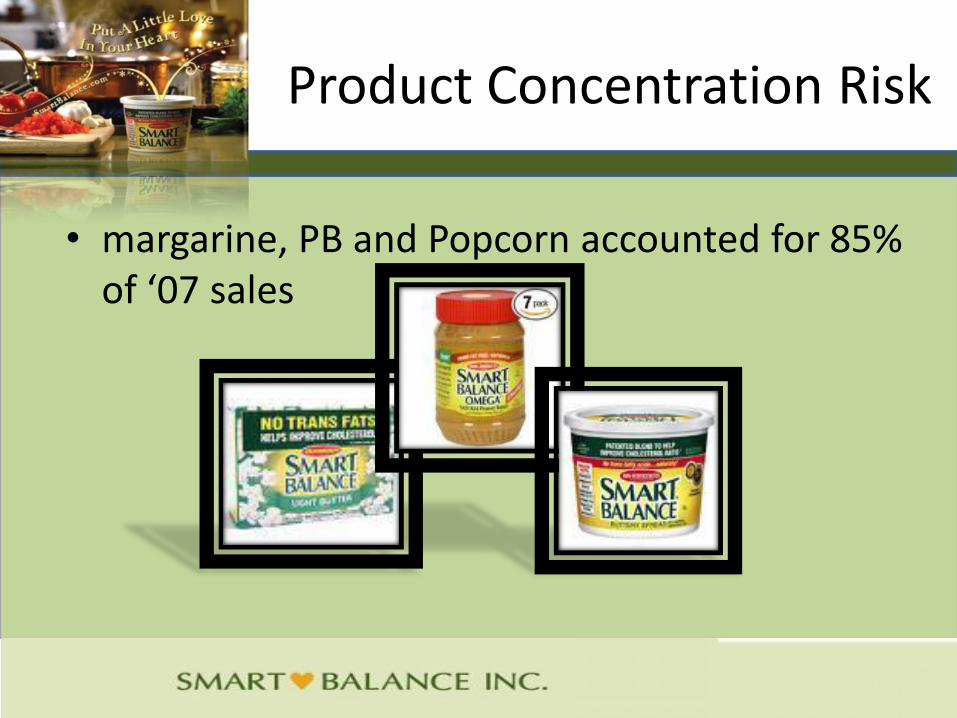

Product Concentration Risk

• margarine, PB and Popcorn accounted for 85% of ‘07 sales

Wal-Mart

• Customer concentration risk : Top three customers = 32% of sales

• Wal-mart = 13%

• However, wal-mart is the biggest player for most other products as well!

• Gives higher exposure to consumers

Commodities

$-

$0.50

$1.00

$1.50

$2.00

$2.50

Milk - Last 12 months (Per Pound)

Milk - Last 12 months

Commodity prices : Spike in milk price

Commodities

Soybean spot pricesSoybean oil prices

Formidable Competition

• Competition from well establishes brands (Unilever, ConAgra, JM Smucker, Act II, etc.)

– SB margarine sales grow in spite of dip in market

Peanut Butter Market Share

36.50%

23% 21.90%

5.50%3.70% 2.40%

33.40%

20.30%19.70%

5.10%

13.10%

1.50%

Jif Skippy Private Label Smuckers Peter Pan Smart Balance

2007 2006

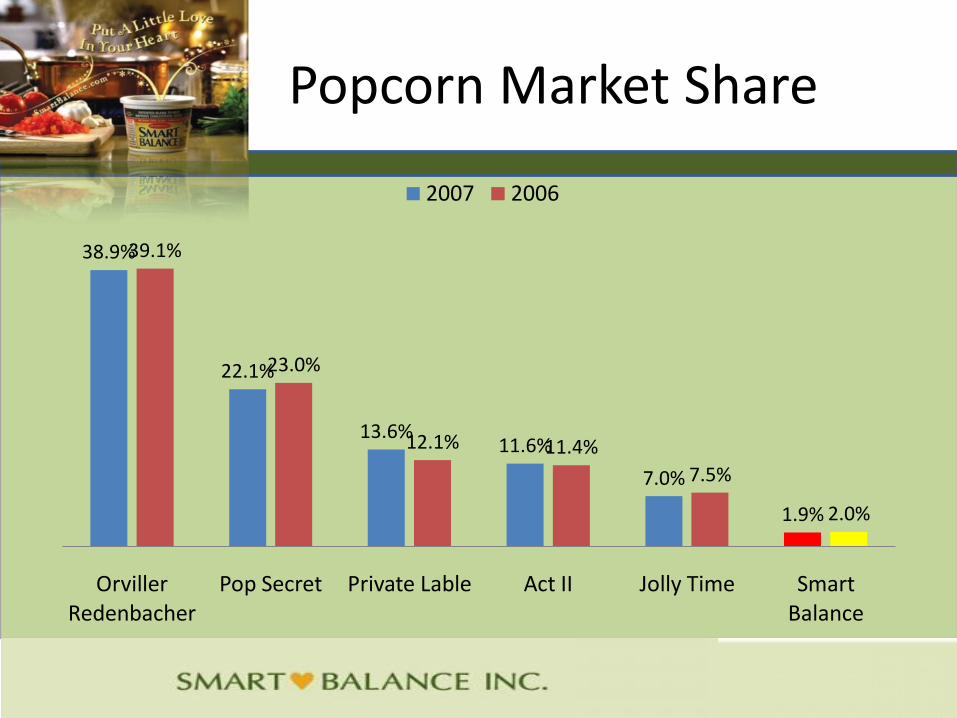

Popcorn Market Share

38.9%

22.1%

13.6%11.6%

7.0%

1.9%

39.1%

23.0%

12.1% 11.4%

7.5%

2.0%

Orviller Redenbacher

Pop Secret Private Lable Act II Jolly Time Smart Balance

2007 2006

Butter Spread Market Share

22.1%

19.5%

13.2%

7.5% 7.1%5.6% 4.8%

22%

19%

12%

8%7% 6%

5%

Shedd's Spread

I Can't Believe its Not Butter

Smart Balance

Private Lable

Blue Bonnet Parkay Land O'Lakes

2007 2006

I Like…

Marketing Strategy

Valuation

• Transaction Comps

• DCF

• No direct trading competitor

Transaction Comps

• Recent Acquisitions in the market have gone for 20x EBITDA

– 20x puts SMBL at about 600 million

• Recent Acquisitions in the market have gone for about 2x Revenue

– 2x puts SMBL at about 400 million