smart products nigeria plc management …...smart products nigeria plc notes to the financial...

TRANSCRIPT

SMART PRODUCTS NIGERIA PLC

MANAGEMENT ACCOUNTS FOR

THE PERIOD ENDED 30THSEPTEMBER, 2016

SMART PRODUCT NIGERIA PLC

MANAGEMENT ACCOUNTS FOR

THE PERIOD ENDED 3OTHSEPTEMBER, 2016

CONTENTS PAGE

Statement of financial position 1

Statement of comprehensive income 2

Notes to the management accounts 3 - 18

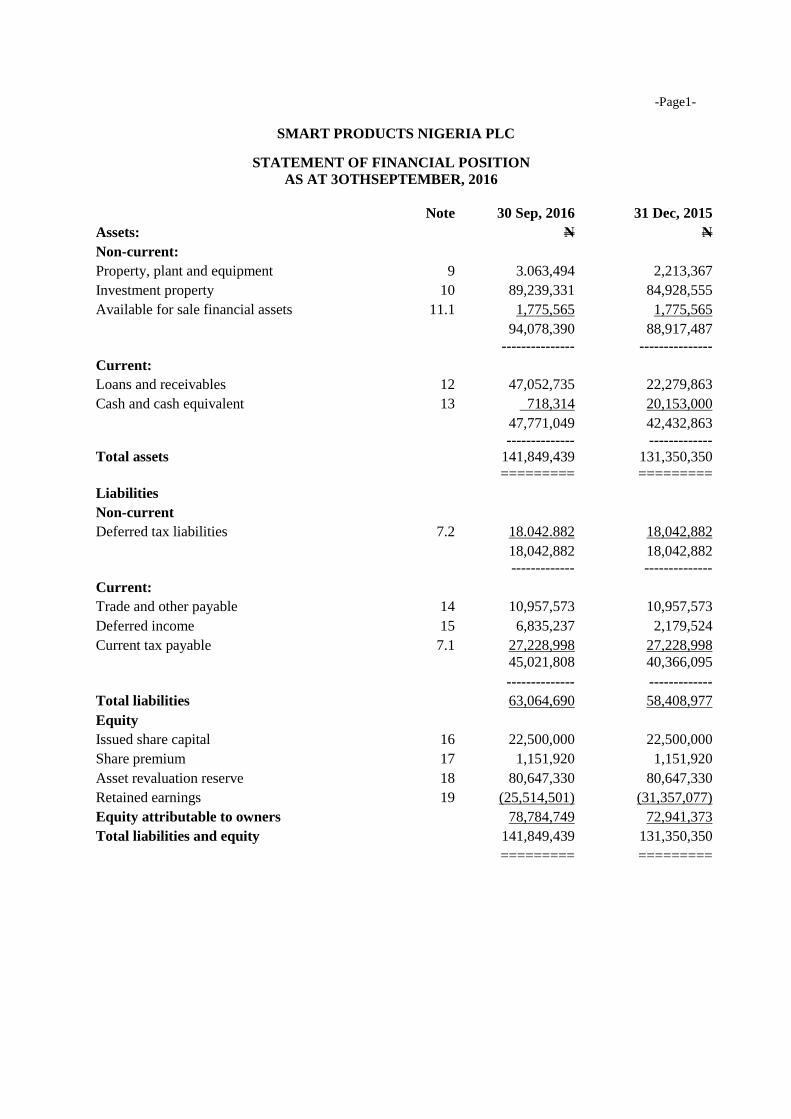

-Page1-

SMART PRODUCTS NIGERIA PLC

STATEMENT OF FINANCIAL POSITION

AS AT 3OTHSEPTEMBER, 2016

Note 30 Sep, 2016 31 Dec, 2015

Assets: N N

Non-current:

Property, plant and equipment 9 3.063,494 2,213,367

Investment property 10 89,239,331 84,928,555

Available for sale financial assets 11.1 1,775,565 1,775,565

94,078,390 88,917,487

--------------- ---------------

Current:

Loans and receivables 12 47,052,735 22,279,863

Cash and cash equivalent 13 718,314 20,153,000

47,771,049 42,432,863

-------------- -------------

Total assets 141,849,439 131,350,350

========= =========

Liabilities

Non-current

Deferred tax liabilities 7.2 18.042.882 18,042,882

18,042,882 18,042,882

------------- --------------

Current:

Trade and other payable 14 10,957,573 10,957,573

Deferred income 15 6,835,237 2,179,524

Current tax payable 7.1 27,228,998 27,228,998

45,021,808 40,366,095

-------------- -------------

Total liabilities 63,064,690 58,408,977

Equity

Issued share capital 16 22,500,000 22,500,000

Share premium 17 1,151,920 1,151,920

Asset revaluation reserve 18 80,647,330 80,647,330

Retained earnings 19 (25,514,501) (31,357,077)

Equity attributable to owners 78,784,749 72,941,373

Total liabilities and equity 141,849,439 131,350,350

========= =========

-Page2-

SMART PRODUCTS NIGERIA PLC

STATEMENT OF COMPREHENSIVE INCOME

FOR THE PERIOD ENDED 30THSEPTEMBER 2016

Note 30 Sep, 2016 31 Dec, 2015

N N

Revenue 3 33,210,176 45,190,169

Other income 4 3,773,406 7,665,204

Total revenue 36,983,582 52,855,373

Personnel expenses 5 (5,511,900) (5,971,814)

Other operating expenses 6 (16,268,307) (23,818,746)

Profit before tax 15,203,375 23,064,813

Income tax expenses 7.1 - (8,323,112)

Deferred tax expenses 7.2 - 1,915,763

Profit for the period after tax 19 15,203,375 16,657,464

Other comprehensive income

Appreciation on available for sale financial assets 11.1 - 235,843

Total comprehensive income for the period 15,203,375 16,893,307

======== ========

Earnings per share

Basic profit for the period attributable to

ordinary equity holders 8 0.34 0.37

===== =====

................................................................................. …………………………

Mr. Abiola A. Aderonmu Mr. Amin A. Amzat

Managing Director Chie Finance Officer FRC/2014/NIM/00000007253 FRC/2014/ICAN/00000006914

-Page3-

SMART PRODUCTS NIGERIA PLC

NOTES TO THE FINANCIAL STATEMENTS

1. Corporate information

The company, Smart Product Nigeria Plc (formerly Associated Press Limited) was

incorporated on 11 January, 1966 as a limited liability company and commenced

business as a legal entity immediately. It was converted to a public limited liability

company in 1991. The registered office is located at 373, Agege Motor Road,

Challenge, Mushin, Lagos. The principal activity of the company is the management

and administration of the company’s properties and investments from where it derives

income.

2. Accounting policies

The principal accounting policies adopted in the preparation of these management

accounts are set out below. These policies have been consistently applied to all the

periods presented, unless otherwise stated.

2.1 Basis of preparation

The management accounts have been prepared on an historical cost basis, except for

those available-for-sale financial assets that have been measured at fair value. The

financial statements values are presented in the Nigerian Naira (N), which is the

Company’s presentation currency, unless otherwise indicated.

2.1.1 Statement of compliance

The financial statements of the Company have been prepared in accordance with

International Financial Reporting Standards (IFRS) as issued by the International

Accounting Standards Board (IASB). Additional information required by national

regulations is included where appropriate.

The Company presents its statement of financial position with necessary analysis of

the items presented in the respective notes. An analysis regarding recovery or

settlement within 12 months after the reporting date (current) and more than 12

months after the reporting date (non-current) form an integral part of each of the notes

where applicable.

Financial assets and financial liabilities are offset and the net amount reported in the

statement of financial position only when there is a legally enforceable right to offset

the recognized amount and there is an intention to settle on a net basis, or to realize

the assets and settled the liability simultaneously.

-Page 4-

2.2 Summary of significant accounting policies

The following are the significant accounting policies adopted by the Company in

preparing its management accounts:

2.2.1 Property, plant and equipment

Property, plant and equipment are stated at cost less accumulated depreciation and

accumulated impairment losses (if any). The cost of property, plant and equipment

includes expenditure incurred during construction, delivery and modification. Other

subsequent expenditure is capitalised only when it increases the future economic

benefits associated with the asset to which it relates. Where a substantial period of

time is required to bring the asset into use, attributable finance costs are capitalised

and included in the cost of the relevant asset. Depreciation is provided on straight line

basis to allocate the cost/revalued amounts less their residual values over the

estimated useful lives of the various classes of assets.

The principal rates used are:

Plant and machinery 10 years

Motor vehicles 4 years

Furniture, fixtures and equipment 10 years

Generator 3 years

Depreciation is charged based on usage in the year of purchase.

The asset’s residual values, useful lives and method of depreciation are reviewed at

each financial year end and adjusted prospectively if appropriate to reflect the relevant

market conditions and expectations, obsolescence and normal wear and tear.

Impairment review is carried out when events or changes in circumstances indicate

that the carrying value may not be recoverable. Impairment losses on non-revalued

assets are recognised in the income statement as an expense, while reversals of

impairment losses are also stated in the income statement.

An item of property, plant and equipment and any significant part initially recognised

is derecognised upon disposal or when no future economic benefits are expected from

its use or disposal. Any gain or loss arising on derecognition of the asset (calculated

as the difference between the net disposal proceeds and the carrying amount of the

asset) is included in the income statement when the asset is derecognised.

2.2.2 Investment properties

Leasehold property

The company has opted to use the carrying cost of its investment property as deemed

cost upon transition to IFRS and subsequently measure it using the cost model.

Investment properties (including borrowing cost attributable to their construction,

acquisition and production) are capitalised and are initially measured at cost;

-Page 5-

subsequently, they are amortised over the remaining leasehold life of the lease

agreement (less any accumulated impairment losses). The company however

discloses the fair value of its investment properties as at the end of the financial period

in compliance with paragraph 79 of IAS 40. The fair value is determined every three

years by external independent valuers who are registered with the Financial Reporting

Council (FRC) of Nigeria. Increase in their carrying amount are credited to

revaluation reserve in shareholder’s equity. Decreases that offset previous increases

of the same properties are charged against revaluation reserve while, all other

decreases are charged to the income statement. Revaluation surplus on disposed

properties are written back to income in line with the provisions of IAS 40. The

company’s investment property is amortised over the remaining life of the lease

agreement. The lease expires by 2052.

2.2.3 Intangible assets

Intangible assets acquired separately are measured on initial recognition at cost. After

initial recognition, intangible assets are carried at cost less accumulated amortisation

and accumulated impairment losses (if any).

Capitalization of expenditure ceases when the asset is in the condition necessary for it

to be capable of operating in the manner intended by management.

Depreciable amount is allocated on a systematic basis over its useful life using the

straight line basis in which charges for each period are recognised in the profit or loss.

Direct computer software development costs recognised as intangible assets are

amortised on a straight line basis over four years and are carried at cost less any

accumulated amortisation and any accumulated impairment losses.

The useful life of the asset is reviewed at each financial year end. If the expected

useful life is different from the previous estimates, the amortisation period will

change. And if there is a change due to the expected pattern of consumption of the

future economic benefits embodied in the asset, the amortisation period will be

changed to reflect the pattern which will be accounted for as a change in accounting

estimate. However, the company did not have any intangible asset as at 30 September,

2016.

2.2.4 Taxation

a) Current income tax

Current income tax liabilities and assets for the current and prior periods is measured

at the amount expected to be paid to or recovered from the taxation authorities, using

the tax rates and tax laws that have been enacted or substantively enacted at the

reporting date.Current income tax assets and liabilities also include adjustments for

tax expected to be payable or recoverable in respect of previous periods.

b) Deferred tax

Deferred tax is provided using the liability method on temporary differences at the

reporting date between the tax bases of assets and liabilities and their carrying

amounts for financial reporting purposes. Deferred tax assets and liabilities are

calculated in respect of temporary differences using the balance sheet liability

method. -Page 6-

Deferred tax assets are recorded only to the extent that it is probable that taxable

profit will be available against which the deferred tax asset will be realized or if it can

be offset against existing deferred tax liabilities. The carrying amount of deferred tax

assets is reviewed at each reporting date and reduced to the extent that it is no longer

probable that sufficient taxable profit will be available to allow all or part of the

deferred income tax asset to be utilized. Unrecognised deferred tax assets are

reassessed at each reporting date and are recognised to the extent that it has become

probable that future taxable profit will allow the deferred tax asset to be recovered.

Deferred tax liabilities are recognised for all taxable temporary differences, except

when the deferred tax liability arises from the initial recognition of goodwill or of an

asset or liability in a transaction that is not a business combination and, at the time of

the transaction, affects neither the accounting profit nor taxable profit or loss.

Deferred tax assets and liabilities are measured at tax rates that are expected to apply

to the period when the asset is realized or the liability is settled, based on tax rates that

have been enacted or substantively enacted at the reporting period. Such assets and

liabilities are not recognised if the temporary difference arises from goodwill or from

initial recognition (other than in a business combination) of other assets and liabilities

in a transaction that affects neither the taxable profit nor the accounting profit.

Deferred tax assets and deferred tax liabilities are offset, if a legally enforceable right

exists to set off current tax assets against current income tax liabilities and the

deferred taxes relate to the same taxable entity and the same taxation authority.

2.2.5 Employee’s retirement benefits

Defined contribution

The Company operates a funded defined contributory scheme with some Pension

Fund Administrators. This is in compliance with the provisions of the Pension Reform

Act, 2004 whereby employer and employees contribute minimum of 10% and 8%

respectively of the employees’ eligible emoluments. Staff contributions to the scheme

are funded through payroll deductions, while the Company’s contribution is charged

to the income statement.

When an employee has rendered service to an entity during a period, the company

recognises the contribution payable to a defined contribution plan in exchange for that

service (a) as a liability (accrued expenses), after deducting any contribution already

paid, (b) as an expense.

2.2.6 Revenue

Revenue is recognised to the extent that it is probable that the economic benefits will

flow to the company and the revenue can be reliably measured, regardless of when the

payment is being made. Revenue is measured at the fair value of the consideration

received or receivable, taking into account contractually defined terms of payment and

excluding taxes. The following specific recognition criteria must also be met before

revenue is recognised for each of the two major income sources available to the

company as follows:- -Page 7-

Rental income

This income is generated from rent paid by tenants on the company’s property and is

being recognised on time basis. Rent received for the period is recognised in the

income statement as turnover for the period while amount relating to the period yet to

expire is deferred and recognised as payable in the statements of financial position.

Investment income

Investment income is generated through dividend from equity investment. This

income is recognised in the statement of comprehensive income as income when the

company’s right to receive the payment is established.

2.2.7 Financial Instruments

i) Financial assets

Initial recognition and measurement

Financial assets within the scope of IAS 39 are classified as financial assets at fair

value through profit or loss, loans and receivables, held-to-maturity investments,

available-for-sale financial assets, as appropriate.

The company’s financial assets include cash and short-term deposits, fixed deposits,

loans and other receivables, quoted equity investment. The company recognises three

classes of financial assets:

a) Available for sale financial investments

b) Held to maturity investment

c) Loans and receivables

All financial assets are recognised initially at fair value plus transaction costs.

Subsequent measurement

The subsequent measurement of financial assets depends on their classification as

follows:

Available for sale financial investments

Equity investments classified as available-for-sale are those that are neither classified

as held for trading nor designated at fair value through profit or loss.

After initial measurement, available-for-sale financial investments are subsequently

measured at fair value with unrealised gains or losses recognised in the available-for-

sale reserve through other comprehensive income until the investment is

derecognised, at which time the cumulative gain or loss is recognised in other

operating income or the investment is determined to be impaired, when the

cumulative loss is reclassified from the available-for sale reserve to the income

statement. -Page 8-

Investments in unquoted equity instruments that do not have an active market and

whose fair value cannot be reliably measured and or derivatives that is linked to and

must be settled by delivery of such unquoted equity instruments are measured at cost.

For a financial asset reclassified out of the available-for-sale category, any previous

gain or loss on that asset that has been recognised in equity is amortised to profit or

loss over the remaining life of the investment using the Effective Interest Rate (EIR).

Any difference between the new amortised cost and the expected cash flows is also

amortised over the remaining life of the asset using the EIR. If the asset is

subsequently determined to be impaired, then the amount recorded in equity is

reclassified to the income statement.

Held –to- maturity investments

Non-derivative financial assets with fixed or determinable payments and fixed

maturities are classified as held-to maturity when the Company has the positive

intention and ability to hold them to maturity. After initial measurement, held-to-

maturity investments are measured at amortised cost using the EIR, less impairment.

Amortised cost is calculated by taking into account any discount or premium on

acquisition and fees or costs that are an integral part of the EIR. The EIR amortisation is

included in finance income in the income statement. Gains and losses are recognised in the

income statement when the investments are derecognised or impaired, as well as through

the amortisation process.

Included in this classification are Investments in Treasury bills and Bonds issued by

federal government and state government. However, the company did not have any held -

to -maturity investments as at 30 September, 2016.

Loans and receivables

Loans and receivables are non-derivative financial assets with fixed or determinable

payments that are not quoted in an active market. After initial measurement, such financial

assets are subsequently measured at amortised cost using the EIR method, less

impairment. Amortised cost is calculated by taking into account any discount or premium

on acquisition and fees or costs that are an integral part of the EIR. The EIR amortisation is

included in finance income in the income statement. Gains and losses are recognised in the

income statement when the investments are derecognised or impaired, as well as through

the amortisation process.

Included in this classification are personal loans, car loan and mortgage loan given to

employees.

Derecognition

A financial asset (or, where applicable, a part of a financial asset or part of a group of

similar financial assets) is derecognised when:

The right to receive cash flows from the asset have expired; and -Page 9-

The Company has transferred its rights to receive cash flows from the asset or has

assumed an obligation to pay the received cash flows in full without material delay

to a third party under a ‘pass-through’ arrangement; and either (a) the Company

has transferred substantially all the risks and rewards of the asset, or (b) the

Company has neither transferred nor retained substantially all the risks and

rewards of the asset, but has transferred control of the asset.

When the Company has transferred its rights to receive cash flows from an asset or has

entered into a pass-through arrangement, it evaluates if and to what extent it has retained

the risks and rewards of ownership. When it has neither transferred nor retained

substantially all of the risks and rewards of the asset, nor transferred control of the asset,

the asset is recognised to the extent of the Company’s continuing involvement in the asset.

In that case, the Company also recognises an associated liability. The transferred asset and

the associated liability are measured on a basis that reflects the rights and obligations that

the Company has retained.

ii) Impairment of financial assets

The company assesses at each reporting date whether there is any objective evidence that a

financial asset or a group of financial assets is impaired. A financial asset or a group of

financial assets is deemed to be impaired if, and only if, there is objective evidence of

impairment as a result of one or more events that has occurred after the initial recognition

of the asset (an incurred ‘loss event’) and that loss event has an impact on the estimated

future cash flows of the financial asset or the group of financial assets that can be reliably

estimated. Evidence of impairment may include indications that the debtors or a group of

debtors is experiencing significant financial difficulty, default or delinquency in interest or

principal payments, the probability that they will enter bankruptcy or other financial

reorganisation and where observable data indicate that there is a measurable decrease in

the estimated future cash flows, such as changes in arrears or economic conditions that

correlate with defaults.

Financial assets carried at amortised cost

For financial assets carried at amortised cost, the company first assesses whether

objective evidence of impairment exists individually for financial assets that are

individually significant, or collectively for financial assets that are not individually

significant. If the company determines that no objective evidence of impairment exists

for an individually assessed financial asset, whether significant or not, it includes the

asset in a group of financial assets with similar credit risk characteristics and

collectively assesses them for impairment. Assets that are individually assessed for

impairment and for which an impairment loss is, or continues to be, recognised are

not included in a collective assessment of impairment.

If there is objective evidence that an impairment loss has been incurred, the amount of the

loss is measured as the difference between the asset’s carrying amount and the present

value of estimated future cash flows (excluding future expected credit losses that have not

yet been incurred). The present value of the estimated future cash flows is discounted at

the financial asset’s original effective interest rate. If a loan has a variable interest rate, the

discount rate for measuring any impairment loss is the current EIR. -Page 10-

The carrying amount of the asset is reduced through the use of an allowance account and

the amount of the loss is recognised in the income statement. Interest income continues to

be accrued on the reduced carrying amount and is accrued using the rate of interest used to

discount the future cash flows for the purpose of measuring the impairment loss. The

interest income is recorded as part of investment income in the income statement. Loans

together with the associated allowance are written off when there is no realistic prospect of

future recovery and all collateral has been realised or has been transferred to the Company.

If, in a subsequent year, the amount of the estimated impairment loss increases or

decreases because of an event occurring after the impairment was recognised, the

previously recognised impairment loss is increased or reduced by adjusting the allowance

account. If a future write-off is later recovered, the recovery is recognised in the income

statement.

Available for sale financial investments

For available-for-sale financial investments, the Company assesses at each reporting date

whether there is objective evidence that an investment or a group of investments is

impaired.

In the case of equity investments classified as available-for-sale, objective evidence would

include a significant or prolonged decline in the fair value of the investment below its cost.

‘Significant’ is evaluated against the original cost of the investment and ‘prolonged’

against the period in which the fair value has been below its original cost. When there is

evidence of impairment, the cumulative loss – measured as the difference between the

acquisition cost and the current fair value, less any impairment loss on that investment

previously recognised in the income statement – is removed from other comprehensive

income and recognised in the income statement. Impairment losses on equity investments

are not reversed through the income statement; increases in their fair value after

impairment are recognised directly in other comprehensive income.

A threshold of 20% is applied consistently to conclude whether or not the decline in

fair value is significant.

iii) Financial liabilities

Initial recognition and measurement

Financial liabilities within the scope of IAS 39 are classified as financial liabilities at fair

value through profit or loss, loans and borrowings, or as derivatives designated as hedging

instruments in an effective hedge, as appropriate. The company determines the

classification of its financial liabilities at initial recognition.

All financial liabilities are recognised initially at fair value and, in the case of loans and

borrowings, carried at amortised cost, this includes directly attributable transaction costs.

The company’s financial liabilities include trade and other payables.

Derecognition

A financial liability is derecognised when the obligation under the liability is discharged or

cancelled or expires.

When an existing financial liability is replaced by another from the same lender on

substantially different terms, or the terms of an existing liability are substantially modified, -Page 11-

Such an exchange or modification is treated as the derecognition of the original liability

and the recognition of a new liability. The difference in the respective carrying amounts is

recognised in the income statement.

iv) Offsetting of financial instruments

Financial assets and financial liabilities are offset and the net amount reported in the

statement of financial position if, and only if:

There is a currently enforceable legal right to offset the recognised amounts; and

There is an intention to settle on a net basis, or to realise the assets and settle the

liabilities simultaneously

v) Fair value of financial instruments

The fair value of financial instruments that are traded in active markets are determined at

each reporting date by reference to quoted market prices or dealer price quotations.

For financial instruments not traded in an active market, the fair value is determined using

appropriate valuation techniques. Such techniques may include:

Using recent arm’s length market transactions

Reference to the current fair value of another instrument that is substantially the

same

A discounted cash flow analysis or other valuation models.

2.2.8 Cash and cash equivalent

Cash and cash equivalent in the statement of financial position comprise cash at banks and

on hand and short-term deposits with a maturity of three months or less.

For the purpose of statement of cash flows, cash and cash equivalents consist of cash and

short-term deposits as defined above, net of outstanding bank overdrafts (if any).

2.2.9 Provision

A provision is recognised if as a result of past event the Company has a present legal or

constructive obligation that can be estimated reliably, and it is probable that an outflow of

economic benefits will be required to settle the obligation. Amounts are recorded based on

management’s best estimate of the amount needed to settle the obligation, which includes,

among other things, management’s experience in similar transactions.

Where the effect of the time value of money is significant, the provision is discounted at a

rate that reflects the estimated timing of payment, if the timing can be reasonably

determined, as well as the risk associated with the liability.

-Page12-

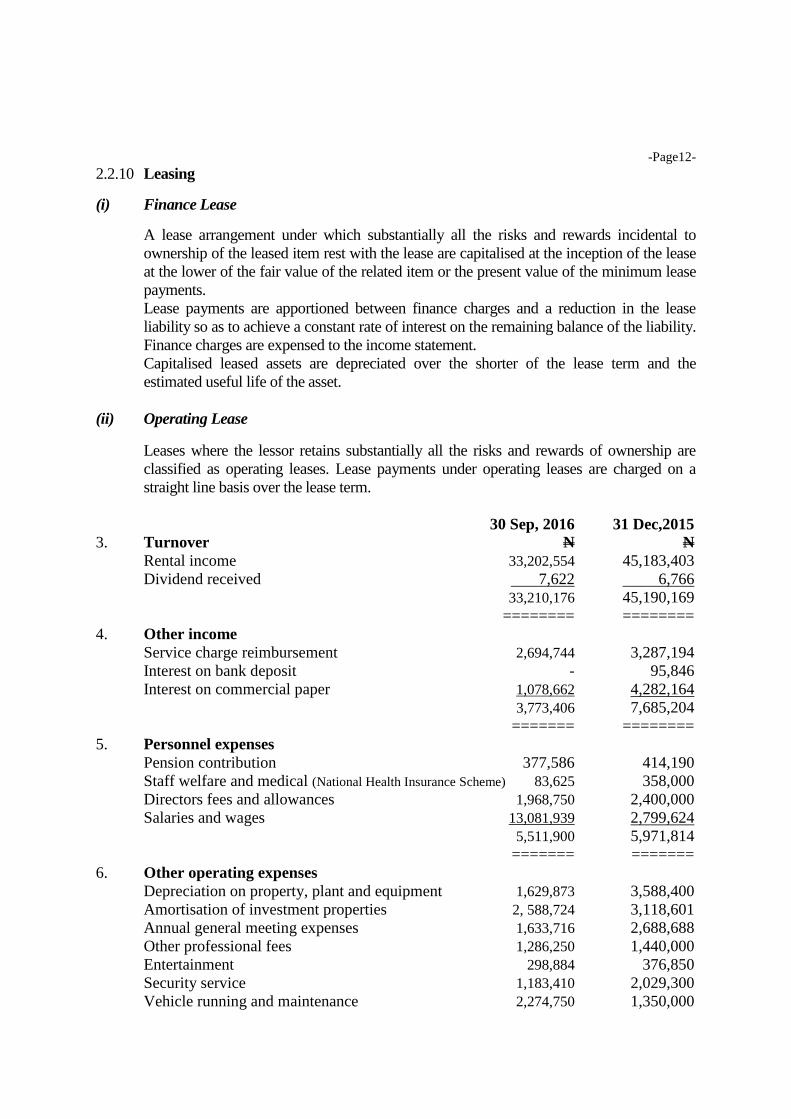

2.2.10 Leasing

(i) Finance Lease

A lease arrangement under which substantially all the risks and rewards incidental to

ownership of the leased item rest with the lease are capitalised at the inception of the lease

at the lower of the fair value of the related item or the present value of the minimum lease

payments.

Lease payments are apportioned between finance charges and a reduction in the lease

liability so as to achieve a constant rate of interest on the remaining balance of the liability.

Finance charges are expensed to the income statement.

Capitalised leased assets are depreciated over the shorter of the lease term and the

estimated useful life of the asset.

(ii) Operating Lease

Leases where the lessor retains substantially all the risks and rewards of ownership are

classified as operating leases. Lease payments under operating leases are charged on a

straight line basis over the lease term.

30 Sep, 2016 31 Dec,2015

3. Turnover N N

Rental income 33,202,554 45,183,403

Dividend received 7,622 6,766

33,210,176 45,190,169

======== ========

4. Other income

Service charge reimbursement 2,694,744 3,287,194

Interest on bank deposit - 95,846

Interest on commercial paper 1,078,662 4,282,164

3,773,406 7,685,204

======= ========

5. Personnel expenses

Pension contribution 377,586 414,190

Staff welfare and medical (National Health Insurance Scheme) 83,625 358,000

Directors fees and allowances 1,968,750 2,400,000

Salaries and wages 13,081,939 2,799,624

5,511,900 5,971,814

======= =======

6. Other operating expenses

Depreciation on property, plant and equipment 1,629,873 3,588,400

Amortisation of investment properties 2, 588,724 3,118,601

Annual general meeting expenses 1,633,716 2,688,688

Other professional fees 1,286,250 1,440,000

Entertainment 298,884 376,850

Security service 1,183,410 2,029,300

Vehicle running and maintenance 2,274,750 1,350,000

Repairs and maintenance 405,564 747,350

Travelling 798,264 1,073,250

Printing and stationary 189,414 709,405 -Page13-

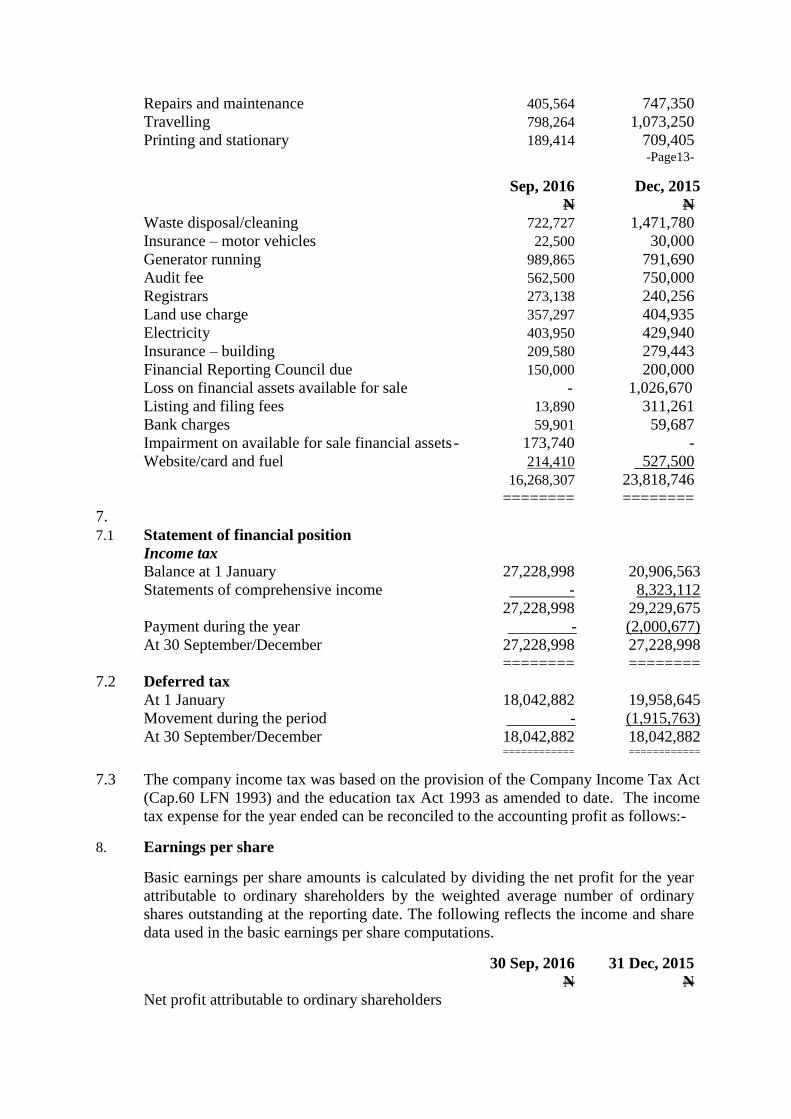

Sep, 2016 Dec, 2015

N N Waste disposal/cleaning 722,727 1,471,780

Insurance – motor vehicles 22,500 30,000

Generator running 989,865 791,690

Audit fee 562,500 750,000

Registrars 273,138 240,256

Land use charge 357,297 404,935

Electricity 403,950 429,940

Insurance – building 209,580 279,443

Financial Reporting Council due 150,000 200,000

Loss on financial assets available for sale - 1,026,670

Listing and filing fees 13,890 311,261

Bank charges 59,901 59,687

Impairment on available for sale financial assets - 173,740 -

Website/card and fuel 214,410 527,500

16,268,307 23,818,746

======== ========

7.

7.1 Statement of financial position

Income tax

Balance at 1 January 27,228,998 20,906,563

Statements of comprehensive income - 8,323,112

27,228,998 29,229,675

Payment during the year - (2,000,677)

At 30 September/December 27,228,998 27,228,998

======== ========

7.2 Deferred tax

At 1 January 18,042,882 19,958,645

Movement during the period - (1,915,763)

At 30 September/December 18,042,882 18,042,882 ============ ============

7.3 The company income tax was based on the provision of the Company Income Tax Act

(Cap.60 LFN 1993) and the education tax Act 1993 as amended to date. The income

tax expense for the year ended can be reconciled to the accounting profit as follows:-

8. Earnings per share

Basic earnings per share amounts is calculated by dividing the net profit for the year

attributable to ordinary shareholders by the weighted average number of ordinary

shares outstanding at the reporting date. The following reflects the income and share

data used in the basic earnings per share computations.

30 Sep, 2016 31 Dec, 2015

N N

Net profit attributable to ordinary shareholders

for basic earnings 15,203,375 16,893,307

Weighted average number of ordinary shares 45,000,000 45,000,000

Basic earnings per ordinary share 0.34 0.37 ========= ==========

-Page 14-

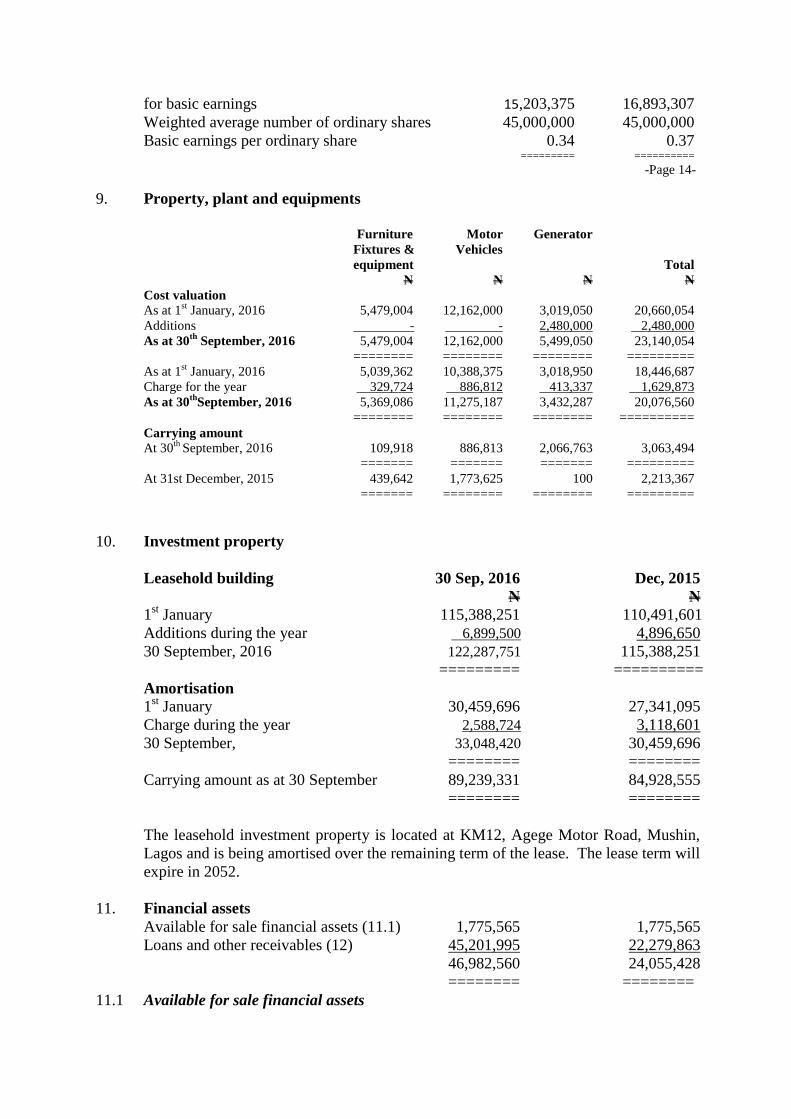

9. Property, plant and equipments

Furniture Motor Generator

Fixtures & Vehicles

equipment Total

N N N N

Cost valuation

As at 1st January, 2016 5,479,004 12,162,000 3,019,050 20,660,054

Additions - - 2,480,000 2,480,000

As at 30th

September, 2016 5,479,004 12,162,000 5,499,050 23,140,054

======== ======== ======== =========

As at 1st January, 2016 5,039,362 10,388,375 3,018,950 18,446,687

Charge for the year 329,724 886,812 413,337 1,629,873

As at 30th

September, 2016 5,369,086 11,275,187 3,432,287 20,076,560

======== ======== ======== ==========

Carrying amount

At 30th

September, 2016 109,918 886,813 2,066,763 3,063,494

======= ======= ======= =========

At 31st December, 2015 439,642 1,773,625 100 2,213,367

======= ======== ======== =========

10. Investment property

Leasehold building 30 Sep, 2016 Dec, 2015

N N

1st January 115,388,251 110,491,601

Additions during the year 6,899,500 4,896,650

30 September, 2016 122,287,751 115,388,251

========= ==========

Amortisation

1st January 30,459,696 27,341,095

Charge during the year 2,588,724 3,118,601

30 September, 33,048,420 30,459,696

======== ========

Carrying amount as at 30 September 89,239,331 84,928,555

======== ========

The leasehold investment property is located at KM12, Agege Motor Road, Mushin,

Lagos and is being amortised over the remaining term of the lease. The lease term will

expire in 2052.

11. Financial assets

Available for sale financial assets (11.1) 1,775,565 1,775,565

Loans and other receivables (12) 45,201,995 22,279,863

46,982,560 24,055,428

======== ========

11.1 Available for sale financial assets

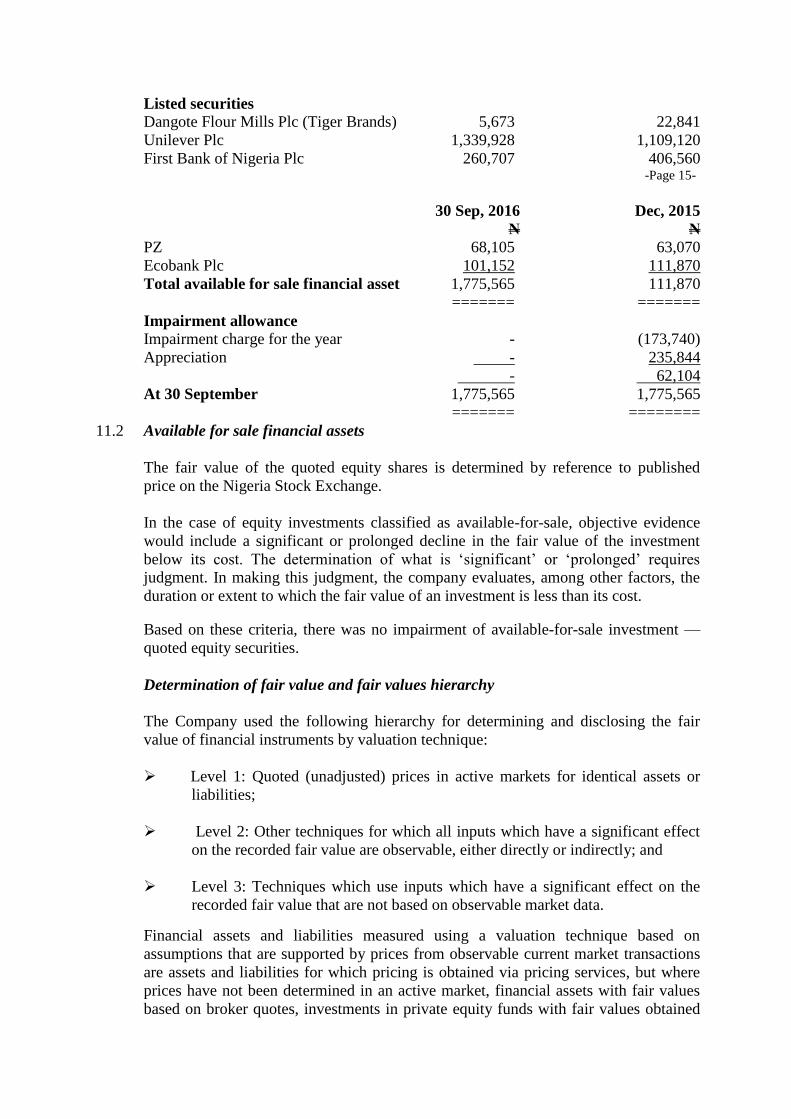

Listed securities

Dangote Flour Mills Plc (Tiger Brands) 5,673 22,841

Unilever Plc 1,339,928 1,109,120

First Bank of Nigeria Plc 260,707 406,560 -Page 15-

30 Sep, 2016 Dec, 2015

N N

PZ 68,105 63,070

Ecobank Plc 101,152 111,870

Total available for sale financial asset 1,775,565 111,870

======= =======

Impairment allowance

Impairment charge for the year - (173,740)

Appreciation - 235,844

- 62,104

At 30 September 1,775,565 1,775,565

======= ========

11.2 Available for sale financial assets

The fair value of the quoted equity shares is determined by reference to published

price on the Nigeria Stock Exchange.

In the case of equity investments classified as available-for-sale, objective evidence

would include a significant or prolonged decline in the fair value of the investment

below its cost. The determination of what is ‘significant’ or ‘prolonged’ requires

judgment. In making this judgment, the company evaluates, among other factors, the

duration or extent to which the fair value of an investment is less than its cost.

Based on these criteria, there was no impairment of available-for-sale investment —

quoted equity securities.

Determination of fair value and fair values hierarchy

The Company used the following hierarchy for determining and disclosing the fair

value of financial instruments by valuation technique:

Level 1: Quoted (unadjusted) prices in active markets for identical assets or

liabilities;

Level 2: Other techniques for which all inputs which have a significant effect

on the recorded fair value are observable, either directly or indirectly; and

Level 3: Techniques which use inputs which have a significant effect on the

recorded fair value that are not based on observable market data.

Financial assets and liabilities measured using a valuation technique based on

assumptions that are supported by prices from observable current market transactions

are assets and liabilities for which pricing is obtained via pricing services, but where

prices have not been determined in an active market, financial assets with fair values

based on broker quotes, investments in private equity funds with fair values obtained

via fund managers and assets that are valued using the Company’s own models

whereby the majority of assumptions are market observable.

-Page 16-

Non market observable inputs means that fair values are determined, in whole or in

part, using a valuation technique (model) based on assumptions that are neither

supported by prices from observable current market transactions in the same

instrument, nor are they based on available market data. The main asset classes in this

category are unlisted equity investments and debt instruments. Valuation techniques

are used to the extent that observable inputs are not available, thereby allowing for

situations in which there is little, if any, market activity for the asset or liability at the

measurement date. However, the fair value measurement objective remains the same,

that is, an exit price from the perspective of the Company.

Therefore, unobservable inputs reflect the Company’s own assumptions about the

assumptions that market participants would use in pricing the asset or liability

(including assumptions about risk). These inputs are developed based on the best

information available, which might include the Company’s own data.

The following table shows an analysis of financial instruments recorded at fair value

by level of the fair value hierarchy:

11.2 Available for sale financial assets Level 1 Total fair

Value

N N

Equity securities 30 September, 2016 1,775,565 1,775,565

======= =======

31 December, 2015 1,775,565 1,775,565

======== =======

30 Sep, 2016 31 Dec, 2015

N N

12. Loans and receivables

Rent receivable 1,845,780 1,845,780

Sundry debtors 33,566,955 20,434,083

Deposit 11,640,000 -

47,052,735 22,279,863

------------- ----------------

Current 47,052,735 22,279,863

Non-current - -

47,052,735 22,279,863

======== ========

13. Cash and cash equivalents - current

Cash and bank balance 718,314 20,153,000

====== ========

14. Financial liability

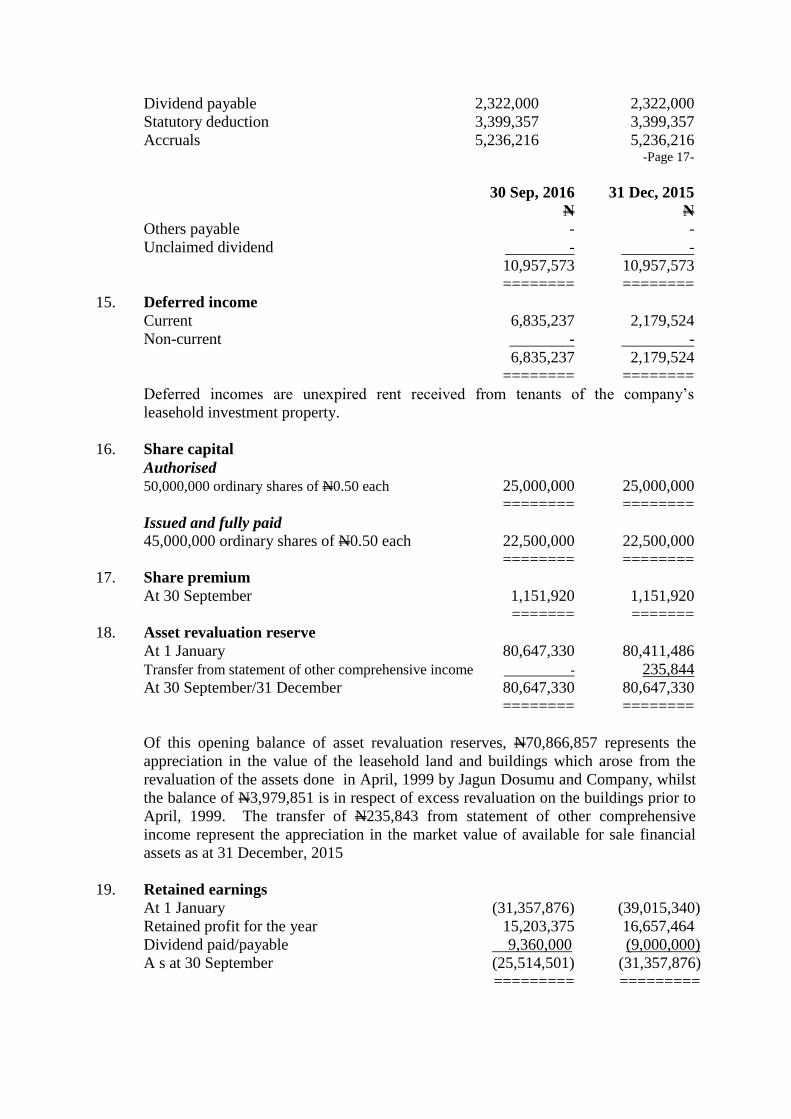

14.1 Trade and other payables- current

Dividend payable 2,322,000 2,322,000

Statutory deduction 3,399,357 3,399,357

Accruals 5,236,216 5,236,216 -Page 17-

30 Sep, 2016 31 Dec, 2015

N N

Others payable - -

Unclaimed dividend - -

10,957,573 10,957,573

======== ========

15. Deferred income

Current 6,835,237 2,179,524

Non-current - -

6,835,237 2,179,524

======== ========

Deferred incomes are unexpired rent received from tenants of the company’s

leasehold investment property.

16. Share capital

Authorised

50,000,000 ordinary shares of N0.50 each 25,000,000 25,000,000

======== ========

Issued and fully paid

45,000,000 ordinary shares of N0.50 each 22,500,000 22,500,000

======== ========

17. Share premium

At 30 September 1,151,920 1,151,920

======= =======

18. Asset revaluation reserve

At 1 January 80,647,330 80,411,486

Transfer from statement of other comprehensive income - 235,844

At 30 September/31 December 80,647,330 80,647,330

======== ========

Of this opening balance of asset revaluation reserves, N70,866,857 represents the

appreciation in the value of the leasehold land and buildings which arose from the

revaluation of the assets done in April, 1999 by Jagun Dosumu and Company, whilst

the balance of N3,979,851 is in respect of excess revaluation on the buildings prior to

April, 1999. The transfer of N235,843 from statement of other comprehensive

income represent the appreciation in the market value of available for sale financial

assets as at 31 December, 2015

19. Retained earnings

At 1 January (31,357,876) (39,015,340)

Retained profit for the year 15,203,375 16,657,464

Dividend paid/payable 9,360,000 (9,000,000)

A s at 30 September (25,514,501) (31,357,876)

========= =========

In respect of the current quarter, the directors do not propose any dividend.