social security | (240) 499 – 0390 | [email protected] 101 presented by fepfep a 501(c)(3)...

TRANSCRIPT

FEP

Social SECURITY

w w w. f e p o n l i n e . o r g | ( 2 4 0 ) 4 9 9 – 0 3 9 0 | i n f o @ f e p o n l i n e . o r g

101

P R E S E N T E D B Y

FEPA 5 0 1 ( C ) ( 3 ) N O N P R O F I T O R G A N I Z A T I O N

The Financial Education Partnership

FEP

Why are we here today?

Social Security represents the most important source of income in retirement.

There are literally thousands of ways to claim Social Security benefits, and you need to make sure you know how to, and are able to, optimize your selections.

*!

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

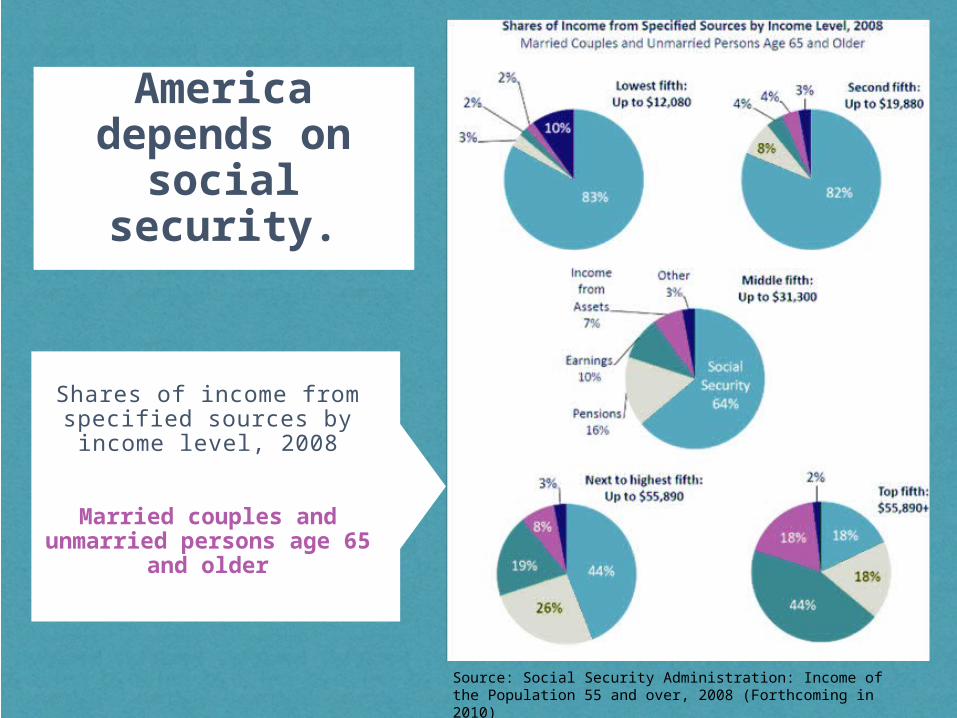

America depends on

social security.

Shares of income from specified sources by income level, 2008

Married couples and unmarried persons age 65 and older

Source: Social Security Administration: Income of the Population 55 and over, 2008 (Forthcoming in 2010)

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

First, a quick history lesson:

Social Security was originally designed to help senior citizens during the Great Depression. It was created as a self-financing program that would collect payroll taxes from workers, which would immediately be paid out in benefits to retirees.

Millions of Americans depend on Social Security as their major source of income in retirement.

Sadly, however, only .013% of Americans correctly optimize their benefits.

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

What Social Security means today:

Predictable, Steady Income: When benefits are claimed, it ensures you receive a fixed starting amount that can never go below that amount.

Lifetime Income: Delivers an income that never runs out.

Inflation-adjusted Income: Annually, Social Security benefits are increased for inflation. We call these cost-of-living adjustments (COLAs)

Survivor Benefits: Benefits continue to be paid to surviving spouses and dependents.

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

But will it ever go away?

“Social Security is not in imminent danger of running out of money, but it faces a financial crunch a bit further out – around 2035. That is when Social Security's Trust Fund is projected to be exhausted due to the drawdown of benefits by the baby-boom generation. At that point, the program would have sufficient tax revenue to pay only about 76% of promised benefits.”

So, while the future of Social Security appears to be okay with potential issues farther ahead, you can start planning and implementing a plan for

garnering the most out of Social Security benefits now.

Not for a long time, if ever. According to Reuters and Steve Goss, chief actuary of the Social Security Administration:

“

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

Understanding Full Retirement

Age(FRA)

FRA is based on your

birth year, and can

gradually move from

age 65 to age 67

Year of Birth Full Retirement Age

1937 or earlier 65

1938 65 and 2 months

1939 65 and 4 months

1940 65 and 6 months

1941 65 and 8 months

1942 65 and 10 months

1943-1954 66

1955 66 and 2 months

1956 66 and 4 months

1957 66 and 6 months

1958 66 and 8 months

1959 66 and 10 months

1960 and beyond 67

Age to Receive Full Social Security

Benefits

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

FRA & Receiving Benefits

For example, FRA for people born between 1943 and 1954 is 66.

This is the age you can begin receiving your full, unreduced primary insurance amount (PIA) – a calculation method used by the administration

Early eligibility begins at 62 but reduces benefits

Timing is one of the most crucial aspects of Social Security planning, and by delaying – which can be hard for many people – you can grow your income by 8% and leverage those funds later!

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

The numbers don’t lie;Americans don’t optimize!

In 2011 (the most recent year we have statistics for):

1.3 million men and 1.2 million women filed for Social Security retirement benefits

Of the men, 43.6% took benefits as soon as they were eligible, at age 62. 26.1% took benefits after they became eligible at 62, but

before full retirement age

Of men and women, 13.3% took their benefits at full retirement age. Only 0.6% waited until they were age 70 or older!

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

Applying Earlier vs. Later

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

The advantage of applying after Full Retirement Age (FRA)

Social Security uses a formula based on the primary insurance amount, or PIA. If you wait to start receiving Social Security until your full retirement age (FRA), you get 100% of your PIA.

If you take it at 62, when you first become eligible, you get only 75%. But if you wait until age 70, you get 132% of the PIA!

If you delay the onset of benefits past age 66, you will earn what are called delayed actuarial credits.

For each year you delay the start of your benefits, your benefit will increase by 8% per year, up to age 70*

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

The Bread Winner Will Delay –Getting The Most Out of Your Benefits

Using delayed actuarial credits, you can find between $20,000 and $40,000 or more in benefits that could have been lost.

By delaying and optimizing, we’ve even seen couples find hundreds of thousands of dollars!

Leveraging the delayed credit system allows you to optimize spousal benefits through two key Switch Strategies

By using these two strategies, pre-retirees can maximize benefits and then redirect these additional funds into a tax-deferred annuity as one valuable option.

$

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

A Real Example

John and Susan each turned 62 in 2005, making them eligible to collect Social Security.

Their estimated full retirement age benefit was $30,000.

They planned to stop working in 2008 at age 65.

They wanted to know when they should begin taking their Social Security benefits.?

John & SusanJohn & Susan

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

The Strategy Revealed

As soon as they both retired in 2008, Susan applied for her benefit.

When John reached full retirement (age 66) in 2009, he applied for a spousal benefit.

In 2013, John applied for his own benefit.

Since John has delayed his benefit until age 70, he will receive 132% of his full retirement age benefit for the rest of his life.

[This could mean thousands of dollars more in retirement!]

* Should one spouse die, the surviving spouse will receive the higher of the two benefits for the rest of their life.

John & SusanJohn & Susan

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

Social Security Scenario #1

Married couple, both aged 62, both will retire at age 66

Spouse A: Makes $25,000 a year

Spouse B: Makes $90,000 a year

*When should they draw?

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

Social Security Scenario #2

Client is 70 years old, currently drawing Social

Security since age 69 [$2,500/month]

Spouse is 64 years old, will draw Social Security at

age 66 for approximately $1,000/month

*What’s wrong with this picture?

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

Social Security Scenario #3

Client is 55 years old, with a 66 year-old spouse

66 year-old is eligible to draw $2,100/month in Social Security and they need it now

They have $500,000 in an IRA

*What should they do?

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

Social Security Scenario #4

Client A is 65 years old, with a 64 year-old spouse (Client B)

Client A will work until age 70 Client B hasn’t worked in over 10 years

(stayed home raising kids, never went back to work)

Client B has some minimum social security benefits available

* What should they do?

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

OK, but how much will I receive?

When you turn 62, your exact amount is calculated. Annual earnings are indexed to account for wage inflation.

After every year’s earnings are indexed, the government tallies your highest 35 years of earnings. If you worked less than 35 years, any missing years are counted as zeroes.

Every year of earnings are totaled and divided by 35 which gives you your indexed monthly earnings, also known as AIME.

If you served in the military between 1957 and 2001, you will automatically receive additional credits toward your Social Security earnings up to $1,200 per year, based on $300 per quarter

It is best to use a Social Security Calculator to determine the amount.

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

Calculating Benefits

Every year, the maximum wages subject to Social Security Tax have increased.

The government takes your inflation-adjusted indexed monthly number (AIME) and applies a 3-part formula to arrive at your primary insurance amount or PIA calculation.

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

Optimization Must Start With Analysis

So, how do you truly optimize your benefits in retirement?

Start with analysis, which helps determine the right claiming strategy.

Once that is determined, then optimization happens.

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

Optimization Must Start With Questions

1. Which spouse has the higher PIA? (typically the higher earning spouse)

2. Who will reach FRA first, and by how many years?

3. Who should get spousal benefits; the husband or the wife, or perhaps one spouse first followed by the other spouse?

4. Can you use switching strategies, where a spouse may begin spousal benefits and later switch to benefits based on his or her own earnings record at a later date?

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

Optimization Must Start With Questions

5. How will the selection of one spouse's beginning date affect the level of survivor's benefits for the other spouse?

6. What is each of your standard life expectancies, and how do you think your family and personal health history and lifestyle will affect this?

7. What happens if one of you dies early and the other lives for many more years?

8. What happens if you both live a long time, or both die sooner than expected?

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

The Social Security Tax Trap

If Social Security is your only source of income, your benefits will not be taxable.

But…If you have other income from sources such as continued work, a pension, investment income, annuities, rental income, etc.,

then you could owe taxes on up to 85% of your Social Security benefits each year!

of Americans do not know this.We can also show you how to prevent this.99

%

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

Social Security Taxation

Depending on your earnings, you are responsible for paying income taxes on a portion of their benefits.

The IRS adds half of an individual's Social Security benefits plus all other income (such as pensions, CD/bond interest or capital gains) to calculate the income taxes owed.

!Sadly, some retirees will end up paying taxes on up to 85% of their benefits.

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes

FEP

The Answers May Surprise You

When should you apply? _______________________________________

Which spouse should apply first? ________________________________

Should one of you file and suspend? _____________________________

Will taxes make a difference? ____________________________________

Can you continue working? _______________________________________

What if you're single? __________________________________________

There are literally thousands of different ways to claim benefits and optimize.

FEP

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Notes