socially responsible financing for enhancing … responsible financing for enhancing economic and...

TRANSCRIPT

Socially Responsible Financing for Enhancing Economic and Financial Stability-Glimpses from South Asia

Atiur Rahman, Ph.D.Governor, Bangladesh BankEmail: [email protected]

1

Asian Institute Technology (AIT)Bangkok-Thailand

Financial stability everywhere a high priority after global financial crisis

2

The Global Financial Crisis (GFC, 2007-2009) brought financialstability to the forefront of policy priorities at national, regional andglobal levels.

The GFC highlighted importance of innovative approaches ofprotecting and strengthening financial stability.

Global liquidity expansion out of line with global output growth, akey cause of the GFC, continued in ‘Quantitative Easing’ (QE)pursued to overcome growth slowdown in advanced economies.This caused inflows-driven asset price bubbles and attendantinstability risks in Emerging Market (EM) economies.

The recent tapering of QE in advanced economies is creating newinstability risks by triggering investment outflow surges from EMeconomies.

3

Bidden by G24, Basel based financial supervisory standardsetters have revised and expanded macro and micro-prudentialregulations and supervisory norms and standards.

Regulatory reforms alone will not ensure future stabilityhowever, risk buildups triggering the global crisis arose morefrom regulatory compliance negligence in good times ratherthan from gaps and shortcomings in regulations.

Reorienting motivations away from greed driven imprudentrisk taking to a socially responsible business ethos is arequisite for lasting stability, besides regulatory reforms.

Financial stability everywhere a high priority after global financial crisis

Inclusiveness and greening are the two main thrusts of SRF

4

Largely ignored until lately by advanced economies, sociallyresponsible financing is growing healthily in bothdeveloping and developed economies, driven by worldwidedemand from civil society coalitions and movements.

Inclusive financing involves reaching out with financial servicesto all economic activities of all population segments in thesociety.

Environment friendly (green) financing involves lending onlyto project proposals that meet acceptable standards inenvironmental impact assessment; and in supportingtransition from traditional output practices to low-carbon,more energy efficient ones.

Inclusive finance now in focus as global priority

5

Inclusive financing enhances stability by diversifying credit riskin numerous smaller loans for diverse purposes, and bybringing in stable bases of numerous small deposits from newinclusion clients.

Cooperation and networking among socially responsiblefinancial and nonfinancial businesses and regulators has beenflourishing, under such umbrellas as the UNGC and AFI.

Basel based global standard setters have also lately begunpaying attention to costs and instability risks from financialexclusion.

Inclusive financing not always immediate business cases

6

Inclusive financing of client segments in dispersed remotelocations being costly, may often not be immediate businesscases.

Governments and central banks step in to drive down financialservices delivery costs, with such support measures as puttingin place mobile phone/smart card based ICT infrastructure foroff branch financial service delivery, low cost funding/refinancing lines and so forth.

Socially responsible inclusive financing in South Asia

7

Inclusive financing has helped South Asian economies upholddomestic output and demand during and after the globalfinancial crisis, amid export growth weakness.

Bangladesh Bank (BB) and other South Asian central bankshave recognized and utilized early on the stability gains frominclusive financing.

South Asian central banks are using the SAARCFINANCEforum for mutual learning and experience sharing onapproaches of socially responsible inclusive financing.

BB is also active in AFI and regional forums promoting inclusivefinancing

Socially Responsible Financing : Bangladesh

8

In Bangladesh, socially responsible financing began outsidemainstream banking as microfinance movement of non-government microfinance institutions (MFIs) in the post-liberation 1970s.

Directed lending in the post liberation nationalized banking systemtook care of social priorities in lending. Directed lending becameinfeasible with reappearance of private sector banks, and wasabolished in 1990; raising the need of a new approach for sociallyresponsible financing.

SRF in Bangladesh covers:Agricultural and SME financingGreen financing

Socially Responsible Financing in Bangladesh : Bangladesh Bank

9

BB responded by launching an initiative of mainstreamingsocially responsible institutional ethos in the financial sector.

BB has taken on board all banks and financial institutions inBangladesh in a countrywide inclusive financing promotioncampaign, with three main thrusts:

1. Small holder and sharecropper agriculture2. Micro, small and medium scale productive rural and urban enterprises

(MSMEs).3. Renewable energy generation, effluent treatment, and other projects of

adoption of new energy efficient, GHG emission reducing outputpractices.

Socially Responsible Financing in Bangladesh : Bangladesh Bank

10

Support and facilitation measures taken by BB in promotingsocially responsible financing include:

Modernization of the payment system and financial servicesICT infrastructure, enabling introduction of mobilephone/smart card based off-branch financial service delivery.

Liberally granting licenses for new rural bank branches,permitting engagement of MFIs for bank loan disbursementand recovery.

Refinance lines against agricultural, SME, and green financing.

Bangladesh: Enabling and facilitating measures in support of SRF

11

Policy support from Bangladesh Bank for Green Financing:

BB has set up a Taka 2 billion revolving refinance scheme to supportlenders to green financing initiatives. Under this scheme, banks canclaim refinance facility from BB at the bank rate (5%) against theirdirect finance at 9% for green products and 11% in case of financingthrough MFI linkage. BB has introduced 10 green new products in July01, 2013 and now banks may claim refinance facility from BB for atotal of 16 green products.

The ADB has contributed USD 50 million to this refinancing scheme,to support lending for replacement of traditional smokes brick kilnswith energy efficient modern ones.

BB has introduced detailed Guidelines on Environmental RiskManagement (ERM) and Policy Guidelines for Green Banking in 2011.

Bangladesh: Enabling and facilitating measures in support of SRF

12

No-frills accounts for farmers and other underprivilegedpeople

Available windows of low cost BB refinance line

Effective use of Bank-MFIs partnership

Engaging public and private stakeholders for SMEsdevelopment

Progress in financial inclusion

13

During the past five years Bangladesh Bank has brought 13.3 millionpeople under banking service which includes farmers, hardcorepoor population, unemployed young men/women, freedom fighters,beneficiaries of social security program, small life insurance policyholders, students of schools etc.

Other than farmers' Tk. 10 account, 3.6 million accounts have beenopened to distribute financial aid to different social securityprogram beneficiaries, unemployed young men/women, hardcorepoor, freedom fighters, destitute beneficiaries under Hindu WelfareTrust, small life insurance policy holders and school students.

47 banks have launched school banking schemes reaching out toyoung school students. Up to December 31 2013, a total of2,86,479 students have opened accounts with savings of Tk. 3.04billion.

Progress in financial inclusion: Sharecroppers loan

14

Bangladesh Bank has taken an innovative re-financing scheme of Tk. 5.0 billion revolving fund with BRAC in 2009 at 10 percent interest per year on flat rate for the neglected sharecroppers who have hardly any formal access to finance.

Under the Credit Program for Sharecroppers starting from FY 2009-10, Tk. 11.886 billion has been disbursed to 801,587 sharecroppers up to February 2014.

The outstanding sum is Tk. 7.873 billion. The BRAC has been operating this program in 250 upazillas of 48 districts across the country.

10 Taka bank account for street children

15

After introducing various types of banking services for

farmers, sharecroppers and some other unprivileged

segments of the population, Bangladesh Bank has now

extended its initiatives to bring street urchins and street

children under institutional financial support. They have

their own bank account just for Taka 10 (12 cents).

BRPD circular 05 (March 09, 2014)

Landscape of Financial Services: Quasi-formal (Microfinance) market dominatesInformal market still has significant presence

Access to any

financial services in any market

Access to any financial services

(excluding insurance)

Access to formal and

quasi-formal finance

Access to quasi-formal finance

Access to formal

financial services

Access to informal finance

National 76.77 73.34 65.69 43.23 37.02 26.19

Poverty Status

Non-poor 79.39 75.96 68.37 39.67 44.42 27.69

Poor 70.57 67.14 59.32 51.70 19.43 22.63

Region

Rural 75.52 71.89 64.02 46.39 32.8 27.35

Urban 81.68 79.02 72.21 30.88 53.53 21.66

Access to Credit: Lowest in Formal market

Highest in Micro credit marketRural and Poor HHs have more access

Access to credit (Formal, Quasi-formal, and Informal)

Access to formal and quasi-formal credit

Access to formal credit

Access to quasi-formal credit

Access to informal credit

National 54.12 42.75 7.99 36.64 21.78

Urban 46.10 35.37 9.56 27.00 16.83

Rural 56.17 44.64 7.59 39.10 23.05

Non-poor 52.08 40.04 9.06 32.94 22.59

Poor 58.97 49.22 5.44 45.42 19.86

MFS in Bangladesh

18

All six mobile phone operators are involved with MFS providers in some capacity. By now, 28 Banks have MFS permission and 19 are in active operation that includes BRAC Bank’s dedicated MFS, bKash.

Key players in MFS are bKash, DBBL Mobile Money and M-Cash of IBBL with 13.3 million registered customers with about 2 lacs agents nationwide generating (on average) more than 1.0 million transactions amounting more than Tk. 2.21 billion per day.

MFS in Bangladesh

19

One interesting feature of MFS in Bangladesh is that most of the cash-ins are happening in major metro cities while cash-outs are spreading to the rural areas making significant contribution in terms of financial inclusion and there by inclusive growth.

BAGE

RHAT

BAND

ARBA

NBA

RGUN

ABA

RISA

LBH

OLA

BOGR

ABR

AHM

ANBA

RIA

CHAN

DPUR

CHAP

AINA

WAB

GANJ

CHIT

TAGO

NGCH

UADA

NGA

COM

ILLA

COXS

BAZ

ARDH

AKA

DINA

JPUR

FARI

DPUR

FENI

GAIB

ANDH

AGA

ZIPU

RGO

PALG

ANJ

HOBI

GANJ

JAM

ALPU

RJE

SSOR

EJH

ALOK

ATHI

JHEN

AIDA

HJO

YPUR

HAT

KHAG

RACH

HARI

KHUL

NAKI

SHOR

EGAN

JKU

RIGR

AMKU

STIA

LAKS

HMIP

URLA

LMON

IRHA

TM

ADAR

IPUR

MAG

URA

MAN

IKGA

NJM

AULV

IBAZ

ARM

EHER

PUR

MUN

SHIG

ANJ

MYM

ENSI

NGH

NAOG

AON

NARA

ILNA

RAYA

NGAN

JNA

RSIN

GDI

NATO

RENE

TRAK

ONA

NILP

HAM

ARI

NOAK

HALI

PABN

APA

NCHA

GARH

PATU

AKHA

LIPI

ROJP

URRA

JBAR

IRA

JSHA

HIRA

NGAM

ATI

RANG

PUR

SATK

HIRA

SHAR

IATP

URSH

ERPU

RSI

RAJG

ANJ

SUNA

MGA

NJSY

LHET

TANG

AIL

THAK

URGA

ON

Cash In Count Cash Out Count

Agent Banking

20

The Bangladesh Bank (BB) has recently announced “agent banking” guideline aimed at providing financial services to the people living in remote villages.

The people would get the opportunity to carry out financial transaction through banking channel after introduction of the system, as the bank would employ agent in the remote areas where it has no branch, according to the guideline.

The people of remote and geographically separated areas would be the target of agent banking, as the regular banking is not yet possible in that areas considering business aspects. They could deposit and withdraw money, collect remittance and loan as well as pay utility bills through the agent banking.

Corporate Social Responsibility (CSR)

21

Bangladesh Bank (BB), as the regulator of the financial sector, is guiding the commercial banks in providing necessary support to poor, underprivileged, meritorious and rural background students under their Corporate Social Responsibility (CSR) activities.

Already a few commercial banks have introduced a number of schemes to help the most deserving students at the secondary and higher secondary levels of their studies.

As per the latest data, education sector got the highest proportion (32.29%) of total CSR expenditure.

Bangladesh Bank has recently provided about 4.25 crore Taka to nine institutions for social and humanitarian development from its own CSR fund.

Mandatory agricultural credit

22

The contribution of agriculture is around 19 % to the national GDP supplying required food to feed around 160 million population in the country.

Bangladesh Bank made it mandatory for all commercial banks domestic and foreign to disburse at least 2 % percent of their total loan and advances, which is a bit higher i.e., 5 % for newly licensed banks in Bangladesh.

As of January 2014, outstanding loan disbursement to agriculture stood at a total Tk. 320.7 billion.

Credit to SME

23

SME sector is another thrust area for our SRF activities. A total of Tk. 853.2 billion has been disbursed to more than 700 thousand entrepreneurs in 2013 reaching to an outstanding amount of Tk. 1156.3 billion at the end of December 2013.

More than 50 % of the total disbursed amount went to purely small enterprise sector.

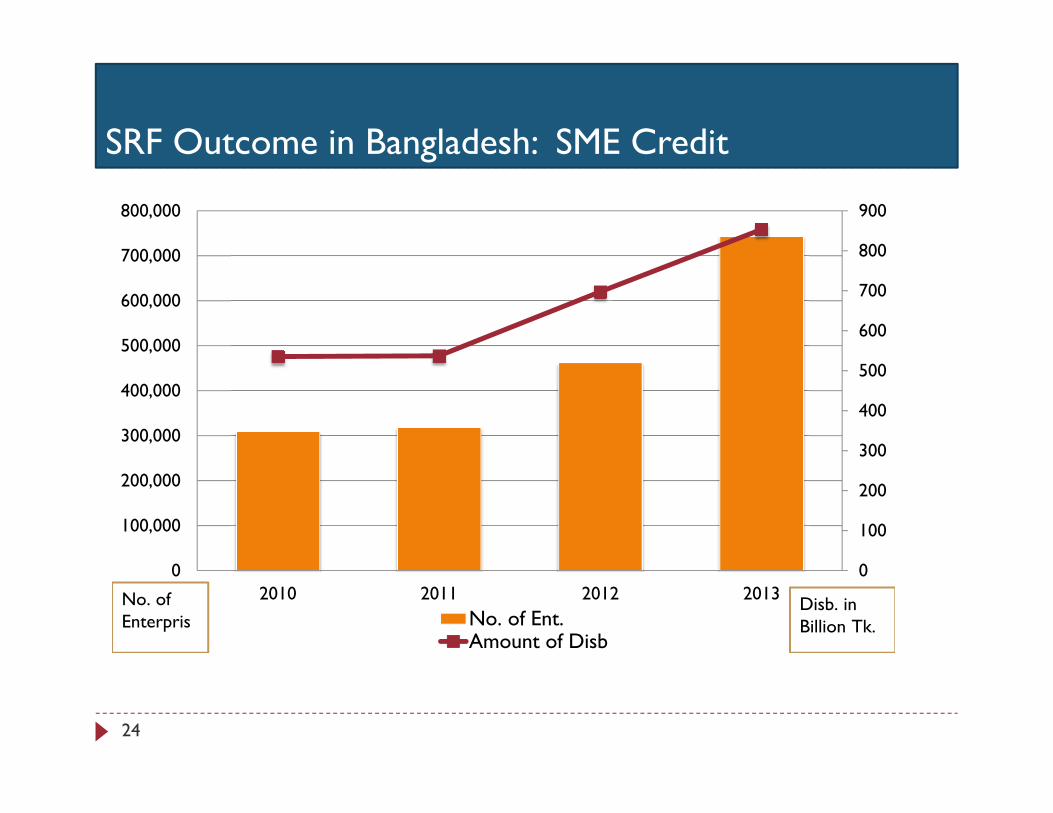

SRF Outcome in Bangladesh: SME Credit

24

0

100

200

300

400

500

600

700

800

900

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

2010 2011 2012 2013No. of Ent.Amount of Disb

No. of Enterpris

Disb. in Billion Tk.

Credit to SME & Agriculture as % of Domestic Credit is increasing

25

19.5817.69

20.65

23.00 22.86 22.52 22.98 23.27

0

5

10

15

20

25

FY 06 FY 07 FY 08 FY 09 FY 10 FY 11 FY 12 FY 13

%

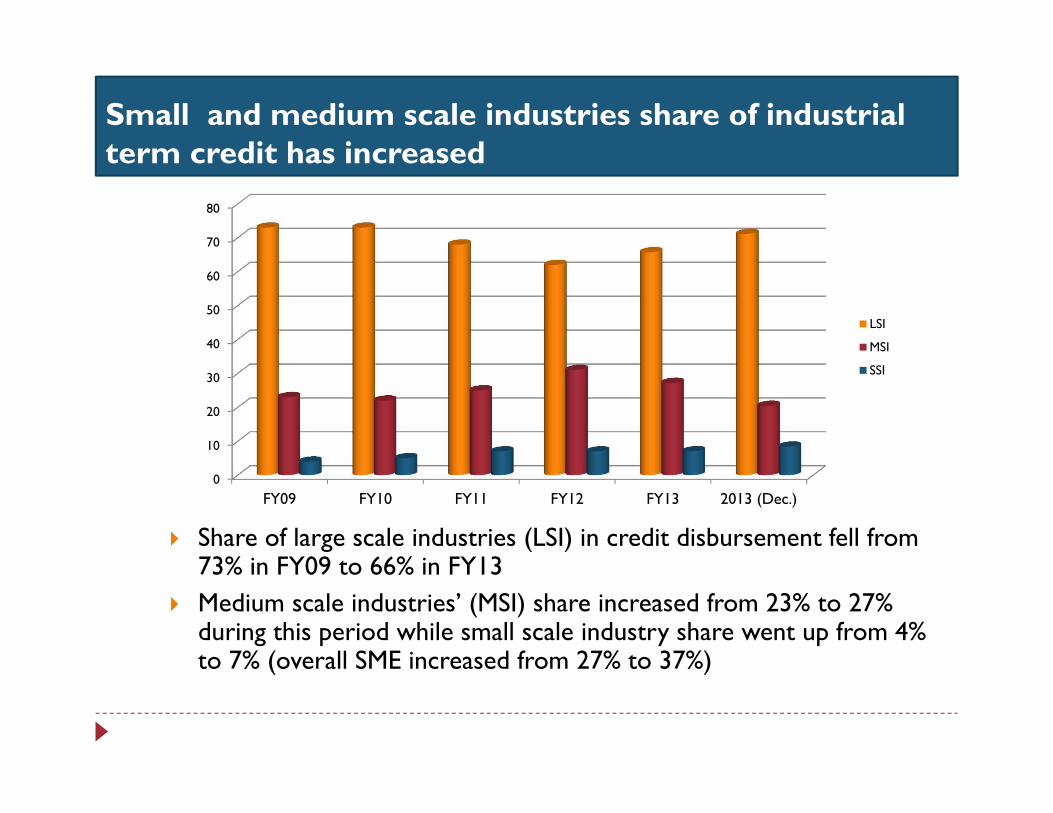

Share of large scale industries (LSI) in credit disbursement fell from 73% in FY09 to 66% in FY13

Medium scale industries’ (MSI) share increased from 23% to 27% during this period while small scale industry share went up from 4% to 7% (overall SME increased from 27% to 37%)

Small and medium scale industries share of industrial term credit has increased

0

10

20

30

40

50

60

70

80

FY09 FY10 FY11 FY12 FY13 2013 (Dec.)

LSI

MSI

SSI

Inclusive financing has upheld output growth stability in Bangladesh economy

27

5.266.27 5.96

6.63 6.43 6.195.74 6.07

6.71 6.236.13

012345678

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

Real GDP growth trend

Six-plus percent annual average real GDP growth for over a decade

Output response from inclusive financing has helped stabilize CPI inflation

28

7.2 7.2

9.9

6.77.3

8.8 8.6 8.0 7.5

0

2

4

6

8

10

12

CPI inflation trend

Inflation moderate at single digit

Rural and urban branches per 100,000 adults (source CGAP)

0.48

6.48

6.41

6.39

6.40

11.11

1.10

2.43

7.46

4.05

3.24

2.63

0 2 4 6 8 10 12

Afghanistan

Bangladesh

India

Pakistan

SA

Developing

Number of branches per 100,000 adults (commercial banks)

Rural Branches/ Rural Population Urban Branches/ Urban Population

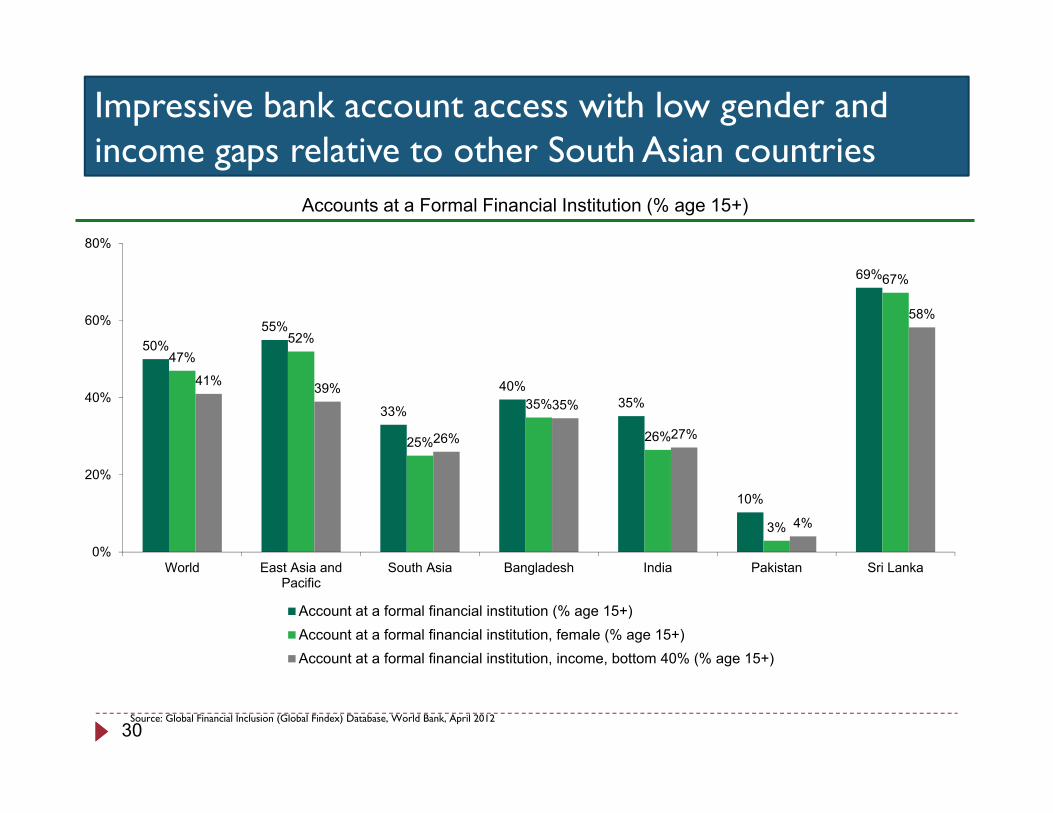

Impressive bank account access with low gender and income gaps relative to other South Asian countries

30

50%55%

33%

40%35%

10%

69%

47%52%

25%

35%

26%

3%

67%

41% 39%

26%

35%

27%

4%

58%

0%

20%

40%

60%

80%

World East Asia andPacific

South Asia Bangladesh India Pakistan Sri Lanka

Account at a formal financial institution (% age 15+)Account at a formal financial institution, female (% age 15+)Account at a formal financial institution, income, bottom 40% (% age 15+)

Source: Global Financial Inclusion (Global Findex) Database, World Bank, April 2012

Accounts at a Formal Financial Institution (% age 15+)

… but more remains to be done, especially for the extreme poor

% of population below the lower poverty line

Poverty declined substantially in the preceding decades…

% of population below the upper poverty line

56.6

48.9

40

31.5

58.7

52.3

43.8

35.2

42.7

35.2

28.4

21.3

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

1991-92 2000 2005 2010

National Rural Urban

Substantial poverty decline evidences inclusiveness of growth

Source: HIES 2005, 2010

Population in poverty fell from 61.6 million in 2000 to 44.8 million in 2010

Consumption Gini coeff. unchanged at 0.33 over ten years, evidencing social cohesion

41

34.3

25.1

17.6

43.7

37.9

28.6

21.123.6

20

14.6

7.7

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

1991-92 2000 2005 2010

National Rural Urban

31

Other South Asian Economy: India

32

The RBI has its Financial Inclusion Advisory Committee withmembers from RBI board directors, market intermediaries,experts and civil society for deliberations and suggestions ondeveloping viable:

Sustainable banking service delivery models to provide accessible,affordable financial services for population segments outside the bankingnetwork;

Also on creating an appropriate regulatory framework for financialinclusion and stability to move together.

RBI’s priority sectors

33

The priority sectors include agriculture and weaker sections of population, education, housing, export financing.

From 2010, RBI is requiring banks to draw up their middle term (3-yr) financial inclusion action plans, guiding and facilitating their action agenda of both branch expansion based and ICT based off-branch service delivery in an agent banking model through Business Correspondents (BCs)

RBI’s approach

34

In general RBI approach to financial inclusion is similar toBangladesh with exception of agent banking and channelingsupport measures for MFIs.

In Bangladesh the choice of and responsibility for KYC andother AML CFT due diligence drills on area agents for off-branch service delivery rests with banks themselves.

In India, apparently banks can appoint agents only from list of‘Business Correspondents’ prequalified, preselected by RBIitself.

RBI’s approach

35

For MFIs in Bangladesh, MRA is for some years now thestatutory authority for regulatory oversight, with PKSFextending some wholesale fund support lines.

In India, regulatory and support interventions for MFIscontinue to rest with NABARD, the state owned bank foragricultural and rural development.

Socially Responsible Financing: Pakistan

36

In Pakistan, agriculture and SMEs are the main thrust areas ofcentral bank’s (SBP’s) interventions promoting sociallyresponsible financing, with significant role for SBP licensedformal Micro Finance Banks (MFBs) and the still largely selfregulated MFIs, alongside mainstream banks.

A large number of bank branches in Pakistan are ‘agriculturedesignated’

Socially Responsible Financing: Pakistan

37

SBP’s Financial Inclusion Program has put in place supportmeasures for boosting SME as well.

Both MFIs and MFBs in Pakistan are active inmicrofinance, the MFIs can access wholesale funding fromPakistan Poverty Alleviation Fund (PPFAF).

Socially Responsible Financing: Pakistan

38

SBP has also taken up initiative for promoting housing finance,

SBP’s branchless banking regulations encourage banks todevelop alternative service delivery channels, especially usingmobile phone technology.

Unlike BB’s choice of on bank led model for mobile phonebanking in Bangladesh, SBP’s stance on this point seems to beone of neutral indifference.

Socially Responsible Financing: Nepal

39

In Nepal, the government and the Nepal Rastra Bank (NRB,the central bank) are both engaged in promotion of inclusivefinancing, as elsewhere in South Asia.

NRB and the government’s Micro-Enterprise DevelopmentProgram (MEDP) have pooled together resources forchanneling credit to productive micro-enterprises from a RuralSelf-Reliance Fund (RSRF), through cooperatives and nongovernment MFIs.

Socially Responsible Financing: Nepal

40

NRB under its financial inclusion program encouragesopening of new branches by banks and financialinstitutions in the under-served geographically remoteareas, offering incentives and relaxations in requirements.

NRB also sets target levels of lending to be maintained bybanks and financial institutions in specified prioritysectors.

Socially Responsible Financing: Sri Lanka

41

In Sri Lanka, inclusiveness of financing is arguably already thebest in South Asia both in coverage and depth

The microfinance sector in Sri Lanka is considered to haveattained greater community orientation than elsewhere in theregion.

CBSL is also implementing several donor funded andgovernment funded programs of lending through participatingfinancial institutions in key economic sectors, includingagriculture, fisheries and livestock, SMEs and microfinance.

Summary

42

We see both commonality and diversity of approaches inSouth Asian initiatives for promoting socially responsibleinclusive financing, arising from similarities and differences inlocal environments.

Near term priorities on the way forward are to bringongoing initiatives to successful completion, and to ensuretheir sustainability by earliest attainment of viability, reaping allpossible efficiency gains.

Over the longer term new challenges to inclusiveness willemerge from new global financial instability, as unbridled globalliquidity expansion disproportionate with real output growthcontinues.

Summary

43

Successfully ingrained socially responsible ethos will keep ourfinancial institutions and markets well immunized andmotivated in inclusive financing and away from irresponsiblespeculative risk taking.

Perspectives from South Asia focused forums of academics likethis one at Harvard will be valuable in charting the path aheadfor steady enhancement of South Asia’s contribution to globalprosperity and stability.

A Video on ‘SRF activities in Bangladesh’

44

Thank You

45