socio-economic performance · socio-economic performance & integration into the global economy...

TRANSCRIPT

Socio-Economic Performance & Integration into the Global Economy

2

Resilience in the Face of Slow Global Recovery

Africa’s recent economic performance is unmatched in the history of the continent

West Africa

Central Africa

Southern Africa

North Africa

East Africa

* Southeast Asia, China and India

5,5%

2,9%

5,1%

3,3%

6,4%

3,9%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

2008 2009 2010 2011 2012 2013

Emerging Asia* Lat Am & Caribbean

United States Euro Area

GDP growth

3

A result of growing domestic demand

Natural resources fueling growth, however, good

performance from countries not richly

endowed with natural resources

Africa

Better macroeconomic management

Higher inflows of financial resources

Higher commodity prices

Good policies to attract domestic &

foreign investments

Africa North Africa

West Africa

East Africa

Central Africa

Southern Africa

Total external debt (% of GDP)

23.2% 16.4% 13.9% 38.0% 16.3% 34.2%

Debt service (% of exports)

10.7% 5.9% 3.6% 6.2% 3.8% 22.3%

Manageable External Debt on the Continent

4

2013 GDP growth

Countries in transition: Countries that can access the Bank’s Fragile States Facility (although not all choose to do so) to consolidate peace, stabilize economies and lay the foundation for sustainable poverty-reduction and long-term economic growth of the eligible countries Factor-driven economies: Low income countries and exporters of raw commodities Investment-driven economies: Countries in transition from the primary sector towards manufacturing and services

A Diverse Economic Landscape Countries in

transition Factor-driven

economies Major oil exporters

Investment-driven economies

DRC, Côte d’Ivoire, Liberia,

Sierra-Leone, South Sudan

Djibouti, Togo

Burundi, Chad, Comoros, Congo,

São Tomé & P., Sudan, Zimbabwe

Eritrea, Guinea

CAR, Guinea-Bissau

Ethiopia

Benin, Burkina Faso, Gambia, Malawi, Mali,

Mauritania, Mozambique, Tanzania,

Uganda, Zambia

Cameroon, Ghana, Lesotho, Niger,

Senegal, Rwanda

Madagascar

–

Angola, Gabon

–

Equatorial Guinea, Libya

Botswana

Kenya, Mauritius, Morocco, Namibia,

Seychelles, Swaziland

Cape Verde, Egypt, South Africa, Tunisia

Nigeria –

–

Algeria

Somalia not included for lack of data

5

>7%

5%–7%

3%–4.9%

1%–2.9%

<1%

6

Stable Macroeconomic Environment Drawing Investors’ Interest

0

20

40

60

Remittances FDI (net inflows)ODA (net inflows)

Remarkable shift in external financing

1,6% 1,4%

-4,1% -2,6% -3,0% -2,9% -3,9%

7.3% 7%

0.4% 0.1% -0.7% -1.6%

-2.7%

-6%

-2%

2%

6%

10%

2007 2008 2009 2010 2011 2012 2013

Fiscal Balance as % of GDP

Current Account Balance (% of GDP)

6,8%

11,3%

9,1%

7,3%

9,1% 8,9%

6,7%

5,0%

7,0%

9,0%

11,0%

13,0%

2007 2008 2009 2010 2011 2012 2013

Inflation

…lowest level in more than 5 years ...countries experiencing social

disruptions under more pressure

…however financing gap still

substantial

Expansionary monetary & fiscal policies support Africa’s growth

Contained inflation

In USD billion

Bright Outlook with Challenges Ahead

GDP expected to grow from 4.8% in 2014 to 5.7% in 2015

Volatility in emerging markets could weaken exports Weakening OECD economies could slow down FDI flows to Africa Home-grown risks: political instability that could undermine a decade of robust growth Deterioration of fiscal balances

Threatened by…

Natural resources and strong domestic demand Investments in infrastructure and expansion of export capacity Africa’s ability to attract FDI and better position itself on the global value chain Africa’s capacity to embark on sustainable industrialization and trade in manufactured products Increasing remittances

Driven by…

7

Scoring Top Marks on Three MDGs

*Best performers represent countries with the greatest improvement from initial conditions

Goal 6: Combat HIV/AIDS, TB, malaria and other diseases

•Target 6A: To have halted by 2015 and begun to reverse the spread of HIV/AIDS

Best performers: *Côte d’Ivoire, Namibia, South Africa, Zimbabwe

•Target 6B: Achieve by 2015 universal access to treatment to HIV/AIDS for all those who need it

Best performers: *Botswana, Comoros, Namibia, Rwanda

Goal 3: Promote gender equality and empower women

•Indicator 3.1: Ratios of girls to boys in primary, secondary and tertiary education

About half of the countries in Africa achieved gender parity in primary school while secondary and tertiary still a challenge

Best performers: *The Gambia, Ghana, Mauritius, Rwanda, São Tome and Príncipe

•Indicator 3.3: Proportion of seats held by women in national parliaments

The proportion of seats held by women in national parliaments in Africa is surpassed only in Latin America and the Caribbean

Best performers: *Angola, Mozambique, Rwanda, Seychelles, South Africa

Goal 2: Achieve universal primary education

•Indicator 2.1: Net enrollment in primary education

Most countries have almost achieved universal primary enrolment, with rates above 90%

Best performers: *Algeria, Egypt, Rwanda, São Tomé and Príncipe

8

Though success stories are emerging

MDGs, an Unfinished Agenda

Goal 7: Ensure environmental sustainability

Mozambique has prioritized water-related infrastructure development with the financing of large-scale rainwater harvesting programs to minimize droughts

Goal 8: Global partnership for development

Increased regionalization and trade with other emerging economies has been a hallmark of growth in Africa over the past decade

Goal 5: Improve maternal health

Universal healthcare in the Seychelles is behind the substantial drop in maternal and child mortality rates

Goal 4: Reduce child mortality

Despite significant challenges, a sustained push by Liberia has resulted in vastly improved child survival rates even exceeding MDG targets

Goal 1: Eradicate extreme poverty and hunger

Extreme poverty almost halted in Tunisia and hunger reduced by over 50% in Ghana and Mauritius in the last decade

9

Overarching goal Eradicate poverty and reduce inequality within the

framework of inclusive and sustainable development underpinned by decent jobs

Africa’s common position on its post-2015

MDG agenda

Africa United on its Post-2015 Development Agenda

Agreed pillars, built on lessons learnt from the implementation of the MDGs

10

UNECA African Union

Unlocking Africa’s Potential Global Value Chains

Infrastructure

development

Regional

integration

Private

sector

development

Governance

&

accountability

Skills

&

technology

Bank’s 10-Year Strategy will help position the continent higher on the Global Value Chain

Reduce the cost

of doing business

Private sector development, a

powerful instrument for the

promotion of industrialization

Knowledge generation and

capacity building important to

industrialize Africa

Sustain a large and

competitive regional industry

Improvements in institutional quality

key for competitiveness

and economic stability

Reduce the cost of doing business

Capable states, visionary leadership and strong institutions

Government and private sector collaboration

Supportive environment for competitiveness

Leverage and develop a knowledge base and investing in people

Increase global and intra-Africa trade

Special economic zones drive entry into global value chains

Fragile states Gender Agriculture

& Food Security

11

Realizing the Value Chain Potential

The pathway to job creation and industrialization

Morocco’s Auto-Parts Industry

• Two free-trade zones: the Tangier Automotive City and

the Atlantic Free Zone both dedicated to the automotive

industry

• Capacity to produce 490,000 vehicles a year

• Delivery of spare parts to Renault’s global network

• 42% of parts in Morocco-made Renault cars provided by

local suppliers

• 60,000 employees in the auto sector and supports many

more jobs indirectly

• Africa’s most important auto producer after South Africa

Kenya’s Flower Industry

• One of the largest in the world with a 38% market share of cut

flowers exported to the EU, key foreign exchange earner

• About 65% of its exported flowers are sold through Dutch

auctions

• Bulk of cut flower processing done in Kenya

• Industry employs close to 500,000 people

• Smallholder farmers in the flower industry profit more than

those in the tea or coffee sectors

• Heavy investment in greenhouses, machinery, irrigation

systems and cold storage facilities. This vertically-integrated

value chain allows for quick adjustment to market conditions

• Flower associations are important agencies of self-regulation,

introducing international best practices

12

The Next 50 Years

13

Contributing to Agenda 2063 through the implementation of its 10-year strategy and the

creation of Africa50 for the delivery of transformational infrastructure.

AU, NEPAD & UNECA endorsed the creation of Africa50 as the major instrument that will realize

Africa’s Agenda 2063

The role of the AfDB Reducing fragmented and spatial exclusion will help Africa

realize its potential for sustainable and inclusion

growth

Regional integration

Innovation, entrepreneurship, developing human capital are

essential

Generating productive employment for Africa's large and youthful

populations to ensure social and political stability

Should be supported by strong, well-functioning institutions and

an enabling business environment

Strategic policy leadership is crucial A prosperous continent based on inclusive and

environmentally sustainable growth An integrated continent based on political unity and

pan-Africanism A continent characterized by good governance,

democracy, respect of human rights and the rule of law A peaceful and secure continent with strong cultural

identity, values and ethics A strong and influential global partner

Our aspirations

Spearhead Africa’s transformation. A continent that ends the cycle of

violence, chronic poverty, inequality and exclusion.

State building, overcoming fragility, restore connections on cross

border natural resources management and monitoring

Containing conflict and fragility

Africa’s Agenda 2063

Facilitating Structural Transformation & Inclusive Growth

14

A 50-year Journey into Africa’s Development

Strong level of approvals

0

5 000

10 000

15 000 ADB Approvals ADF Approvals

15

2009: a year of exceptional demand for Bank Group resources due to the global financial crisis

50-years of progress at the AfDB with over 4,501 projects approved amounting to USD 118.7 billion

Projects approved for the period 1967–2013

910 Agriculture & rural development

projects

USD 13,001 million

22 Environment projects

USD 365 million

285 Finance projects

USD 13,013 million

1,404 Infrastructure

projects

USD 45,455 million

550 Multisector projects

USD 17,212 million

681 Social projects

USD 10,251 million

148 Industry, mining, and

quarrying projects

USD 4,875 million

498 Other approvals*

USD 14,512 million

USD 4.4 million

3 Urban development

projects

* Includes HIPC Debt Relief, Equity Participation, Guarantee, Loan Reallocations, Post Conflict Country Facility and Special Fund for Water

In USD million

Tackling the Infrastructure Deficit

USD 1.8 billion in transport

USD 3.2 billion approved in infrastructure

in 2013

USD 882 million in energy

USD 462 million in water

USD 54 million in communications

Africa’s rail network density ranges from 30–50 km/million people vs

Europe’s 200–1000 km/million people

Under 20% of African roads are paved

Only 43% of Africans have access to

electricity compared to 82% globally

Only 28% of Sub-Saharan Africans have access

to improved sanitation facilities

More than 50% of Africa’s improved growth performance in recent years due to investments in infrastructure

AfDB is the largest external financier for infrastructure in Africa

AfDB established the Africa50 Fund to deliver infrastructure through a new global partnership

platform

16

Championing projects that tackle Africa’s

infrastructure deficit

Namibia – Walvis Bay Container Terminal Project (USD 338 million approved in 2013)

Gateway to international markets for Botswana, South Africa, Zambia, Zimbabwe and the DRC

Increase capacity from 355,000 TEUs* to 1,005,000 TEUs

More efficient at handling a higher volume of cargo Better regional trade integration Private sector development in Namibia 900 nationals employed

* Twenty-foot equivalent unit

Refurbishment and expansion of an integrated rail system across Kenya and Uganda has reduced transit times

Modernization of railways with train delays falling from 91% in 2004 to 25% in 2012

50 km Nairobi–Thika superhighway, reduces travel time from 2–3 hours to 30–45 minutes

32 km, 4 to 6-lane Dakar Diamniadio Toll Road, which drastically reduced travel time to and from Dakar

Connecting the Continent

17

Senegal

Tunisia Uganda–Kenya

Kenya

Powering a Greener Africa

24 million inhabitants will benefit from reliable electric power at a competitive cost

Increase energy access to 33% Connect 125 locations to electricity including

70 schools, 30 health centers & 1,500 SMEs Reduce CO2 emissions by 5.6 million tons

per year 1,400 km of new transmission lines

Côte d’Ivoire, Liberia, Sierra Leone, Guinea – Electricity Interconnection (USD 198.6 million approved in 2013) Securing power supply for four Mano River Union countries

DRC – Inga Site Development & Electricity Access Support Project (USD 68.8 million approved in 2013) Key support of the AfDB for the development of mega-hydro Inga 3 project

Game-changing project infrastructure Fostering sustainable energy access for millions Foundation of 44,800 MW Grand Inga hydropower

project – half of the continent’s installed capacity Finalize the preparation of the 4,800 MW Inga 3

(phase 1 of the Grand Inga) ADB financed groundbreaking feasibility studies Connect 25,000 households in Kinshasa

Provide 300 MW additional power Increase access to energy in rural Kenya by 10% by 2020 Reduce CO2 emissions by 1.5 million tons per year 428 km of new transmission lines

Kenya – Lake Turkana Wind Power Project (USD 179.5 million approved in 2013) Financing Africa’s largest wind project

378 km of transmission lines distributing power to the 3 countries

1.5 million inhabitants will benefit from reliable electric power at a competitive cost

Burundi, Rwanda, Tanzania – Regional Rusomo Falls Hydro Power Project (USD 99.9 million approved in 2013) Managing joint renewable energy resources to power three countries

18

The Bank Group has invested USD 4.5 billion in the electricity sector

over the past 2 decades

African countries combined generate as much power as

Germany…

Over the past 3 years, the AfDB financed more than 978 MW of new power, of which 324 MW

from renewable resources

Environmental Sustainability for Future Generations

Cannot afford to ‘grow today and clean up tomorrow’

The Congo Basin forests are estimated to contain between 25–30 billion tons of carbon (4 years of current GHG emissions)

Source: AfDB 2010

Africa is a low emitter but will be among the most impacted by the effects of climate change

The cost of climate change is huge… …but Africa has more than half of the world’s clean energy potential

19

Renewable energy is expected to account for 40% of Africa’s total energy production in 20 years (from 17% in 2010)

6

5

4

3

2

1

0

Temperature increase (degrees Celsius) on pre-industrial temperatures

2 2.5 3 3.5 4 4.5 5 5.5 6

US

Eurasia

Africa

EU

China

Japan

India

OHI

Russia

Middle East

Other Asia

Da

mag

es

as a

mu

ltip

l

e of

Af

rica

nd

am

ages

wit

h 2

de

gre

es

incr

eas

es

Small difference

between Africa and other regions

Large difference

between Africa and other regions

Latin

America

Climate-Smart Development

• USD 60 million trust fund unlocking private sector investments in small and medium sized clean energy and energy efficiency projects

• Commitment rate of 78% (USD 43.4 million) and an anchor investor in the “African Renewable Energy Fund”

• Greening Bank projects and programs through co-financing

• USD 200 million of GEF resources approved in addition to USD 1.2 billion of co-financing

• Piloting low emissions and climate resilient development solutions while scaling up renewable energy

• AfDB is an implementing agency of the CIF Trust Funds

• Over half of CIF portfolio approved, with USD 1.1 billion from AfDB and USD 500 million from CIF

By the end of the century, temperatures will rise by 3.6°C in the Sahara and an average of 3.2°C in the coolest part (East Africa) – 1.5x greater than the global mean increase

In both West and East Africa, the chances of extremely wet seasons will increase to over 20%, due to greater atmospheric water vapor

USD 128.5 million approved across 6 projects in the area of green growth and Climate Investment Funds

REDD: Reducing Emissions from Deforestation and forest Degradation

Burkina Faso – Gazetted Forests Participatory Management

Project for REDD+

DRC – Integrated REDD+ project in the Mbuji-Mayi/Kananga and

Kisangani Basins

Ghana – Engaging Local Communities in

REDD+/Enhancement of Carbon Stocks

Scaling-up blended finance for climate solutions

20

An Integrated Safeguards System

Cornerstone of the Bank’s strategy to promote growth that is socially inclusive

and environmentally sustainable

Safeguards as a tool for identifying risks, reducing development costs, and

improving project sustainability

Encourages greater transparency and accountability through project-level grievance and redress mechanisms

21

Structure of the Integrated Safeguards System

(OS)

OS 1

OS 2

OS 3

OS 4

OS 5

Environmentaland Social Assessment

Involuntary Resettlement: Land Acquisition, Population Displacement and Compensation

Biodiversity and Ecosystem Services

Pollution Prevention and Control, Greenhouse Gases, Hazardous Materials and Resource Efficiency

Labour Conditions, Health and Safety

Integrated safeguards policy statement

Operational safeguards (OS)

Environmental and Social Assessment Procedures

revised

Integrated Environmental and Social Impact

Assessment guidance notes revised

Declaration of commitment to environmental and social sustainability

and reducing risk of noncompliances

Short and focused policy statements that follow Bank commitments and establish

operational parameters

Procedural and process guidance (documentation, analysis, review and reporting)

at each stage of project cycle

Detailed (methodological, sectoral and thematic) guidance on integrated environmental and social

impact assessment

Sustainable Land Management and Agriculture

Africa’s rate of deforestation is twice the world rate, losing 4 million hectares of forest annually

Africa imports USD 30 billion in foodstuff annually while

chronic hunger persists

Nearly 70% of Africa’s labor force works on family farms

Deforestation and poor agricultural practices account

for 65% of Africa’s carbon emissions

Environmental degradation is both a cause and a result of poverty

Transforming African agriculture

USD 822.1 million approved for agriculture and food security in 2013 Rehabilitation of infrastructure

for crop, fisheries and livestock production

Construction of access and feeder roads

Biodiversity conservation Strengthening climate resilience

Sustainable forest management and conservation

Nigeria – Agricultural Transformation Agenda Support Program (USD 153.6 million approved in 2013)

Increase the income of 45,430 farmers and rural entrepreneurs Create 120,000 jobs Additional 20 million metric tonnes domestic food supply each

year

Maintaining global ecological balance

Mano River Forest Ecosystems Conservation Program (USD 17.8 million approved in 2013)

Sustainable management of the Upper Guinea forest ecosystems

Carbon sequestration and climate change mitigation Improved livelihoods of local communities and gender

mainstreaming Nearly 2 million ha of transboundary forest sites targeted

in 4 beneficiary countries (Côte d'Ivoire, Guinea, Liberia and Sierra Leone)

Water catchments, habitat for wildlife, and improved amenities provided

AfDB Group rural livelihoods programs are demonstrating the potential of agriculture to create jobs and increase food security

22

Most of agriculture portfolio devoted to rural infrastructure, including irrigation, water storage, energy connections and feeder roads

Water Security Vital for Sustainable Development

AfDB Group has a USD 3.3 billion active portfolio of 72 operations in 35 countries

Per capita water storage capacity is less than 200 m3

Cultivated land under irrigation is about 6%

Utilized hydropower potential is less than 10%

Africa is 50 years away from achieving universal access

to modern sanitation services

Population with improved sanitation facilities is about 40%

Rural Water Supply and Sanitation Initiative

African Water Facility Multi-Donor Water

Partnership Program

AfDB’s flagship water initiative

Since 2003, USD 1.9 billion invested across 32 countries

Leveraged over USD 5.1 billion from other donors

80 million people with access to water supply

55 million people with access to improved sanitation

Catalytic instrument focused on leveraging investments to help achieve the objectives of the Africa Water Vision 2025

Since 2006, 90 projects approved, for USD 150 million

164,000 people (provided access to water supply; 437,000) gained access to sanitation; and 2,040,650 people to water for multiple uses

Core facility for developing the Bank’s and continent’s capacity in Integrated Water Resources Management as well as in promoting learning and innovation across a range of water sector issues

In 2013, MDWPP supported the support the Bank’s regional integration agenda on transboundary water resources and drought control in the Sahel

Africa has 22% of the world’s land, 14% of its population, but only 9% of its renewable water resources

23

USD 552.9 million approved in 2013 for water supply and sanitation in urban and rural areas

Scaling up access to safe water and sanitation

Promoting innovative technologies

Water-related knowledge management activities and investment channeled through the Three Water Initiatives

Private Sector, a Development Catalyst

The private sector generates 70% of Africa’s output, 70% of its investment, and 90% of its employment

AfDB Private Sector Development Strategy 2013–2017

• Only 22% of African companies hold a loan or a line of credit, vs Asia (31%), America (47%) and Europe (48%)

• Poor infrastructure adds 30–40% to the costs of goods traded among African countries and cuts business productivity by as much as 30%

• Further goals include supporting fragile states, emphasis on gender, as well as on agriculture and rural development

i. Improve Africa’s investment and business climate by helping strengthen the legal and regulatory environment

ii. Expansion of business access to social and economic infrastructure

iii. Promotion of enterprise development through improved access to finance, skills enhancement and value addition

Working with governments to simplify bureaucratic processes in establishing new businesses and obtaining licenses and other approvals

24

Growing footprint in private sector financing

In USD million

Mobilizing private investment in infrastructure development through public–private partnerships

0

500

1 000

1 500

2 000

2 500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Over USD 1.06 billion government revenue generated

Over 480 thousand jobs created

Over 4.5 million people benefitting from investee projects and microfinance

Performance Scorecard – Private Sector Development (2011–2013)

Private Sector, a Catalyst for Inclusive Growth

USD 1.6 billion approved to finance 37 new private sector operations in 2013

25

A four-year, USD 125-million funding program to support micro, small and medium enterprises

USD 3.98-million technical assistance package by the Fund for African Private Sector Assistance for building capacities in 25 participating financial institutions, improve their operational efficiencies (credit assessment risk management)

Provide standardized lines of credit, mostly in local currency, and technical assistance to targeted financial institutions, predominantly in low-income countries

Longer-term resources to thousands of SMEs particularly those employing women and youth, thus contributing to job creation, poverty reduction and inclusive growth on the continent

Africa SME Program

Small and micro businesses important for promoting inclusive growth

Microfinance is combined with training an mentoring to enable micro businesses to use the funds to best effect

Trade Finance Lines of Credit

Soft Commodity Finance Facilities

Risk Participation Agreements (Guarantee)

Trade Finance Program and Business Plan seeks to reduce the trade finance gap in Africa by providing guarantees and liquidity support for on lending to SMEs with 7 operations approved for a

total value of USD 590 million in 2013

Ecobank Transnational (USD 100mn)

Shelter Afrique Habitat & Housing (USD 20mn)

UT Bank, Ghana (USD 20.6mn)

Finance

Mauritius Commercial Bank (USD 150mn)

Lake Turkana Wind Power, Kenya (USD 152mn)

African Renewable Energy Fund (USD 25mn)

CIPREL Power expansion plant (USD 69mn)

Energy

Maamba Power plant, Zambia (USD 150mn)

Indorama Fertilizer Plant, Nigeria (USD 100.9mn)

Olam Group Africa Program (USD 82.9mn)

Agriculture

Skills training program in Morocco

Reform of medical insurance coverage in Morocco

Other

Capable, Accountable and Responsible Governments a Precondition to Achieve Inclusive Growth

USD 722 million approved for 54 projects and programs in

2013 in support of good governance across 30 countries

USD 301 million to improve governance in

Nigeria’s transport

sector

USD 16.9 million to modernize revenue

administration in the

DRC and strengthen

statistical capabilities

A public international organization created and hosted by the AfDB

Assistance primarily initiated by governments ALSF has 56 members, including 50 states and

six international organizations Overall portfolio: 35 diverse projects, targeting

23 countries Work of the ALSF was acknowledged by

leaders at the G8 meeting Negotiation of complex commercial

transactions Capacity building Commercial creditor litigation

African Legal Support Facility

Balancing the playing field for Africa

26

AfDB Group areas of intervention Rapid social, economic and environmental change placing African societies under considerable strain and can be an impediment to development

AfDB improving governance on infrastructure, natural resources and social sectors

Macroeconomic policies, efficient revenue mobilization, sound public financial management,

economic governance, governance of natural resources

95 000 people benefitting from vocational training with a strong focus on women and vulnerable groups

Around 2.8 million people benefitting from better access to education

Skills Crucial for Job Creation USD 524 million approved for social sector and human

development operations

RWANDA – Skills, Employability and Entrepreneurship Project (USD 37.5 million)

Focus on skills and employability as well as on entrepreneurship development

Reforms to address critical skills gaps Increased private sector participation in education reform Incentives for the acquisition of skills on demand Mechanisms to monitor the relevance of training for the labour market Create an environment that supports entrepreneurship

27

Performance Scorecard – Skills & Technology (2011–2013)

AfDB promoting a New Education Model for Africa, which will be ICT based and linked to the needs of the labor market. This will equip the youth with skills in science, technology and critical thinking, so that they can be agents of change in their societies

Africa’s 200 million youth are making the transition from education to the labor market in high numbers: 122 million will enter the market within the next 10 years

Transforming Africa through Gender Equality

Created an innovative referral and counter-referral system through which the country could begin paying more attention to Gender Based Violence (GBV)

US Treasury award for the Multisector Gender Support Project in Côte d’Ivoire (USD 31 million approved in 2013)

Gender Strategy 2014–2018 Mainstreaming Gender in operations

• Women’s legal status and property rights

• Women’s economic empowerment

• Knowledge management and capacity building for gender equality

• Leadership and Commitment

• Capacity and Finances

• Operational Procedures

• Institutional Authority

• Accountability

28

Helped the lives of victims of GBV through a USD 31 million grant

3,500 women benefitted directly thousands more indirectly

Building Resilience

29

First phase of the broader Drought Resilience and Sustainable Livelihoods Program covering Djibouti, Eritrea, Ethiopia, Kenya, Somalia, South Sudan, Sudan and Uganda

Developing regional systems to deal with the impact of deteriorating environmental conditions

Improvements in managing natural resources, enhancing livestock market infrastructure and animal health systems, bettering livelihoods for agro-pastoralists, and boosting management of trans-boundary natural resources

AfDB promoting regional cooperation on drivers of fragility and building resilience at the national level

Recurrent drought has led to conflict over diminishing water resources and pasturage

Report of the High Level Panel on Fragile States

Promote youth employment

Support private investment

Support women’s empowerment

Contribute to the provision of security and justice services

Build capacity to address fragility in water resources and extractive industries

Enable swift & flexible response to countries emerging from conflict

Build partnerships with other institutions on issues of conflict

Opportunities for building peace and resilience

Fragility holds back development prospects of entire regions

Countries in transition present some of the most intractable problems in development

USD 2.5 billion ADB support provided since 2008

Growing Franchise Value

30

Expanding the scope of the Bank’s intervention

Innovative solutions crowding-in transformative infrastructure projects

New avenues for financing and partnerships

0

2 500

5 000

7 500

10 000

Amount subscribed Internally generated resources Total

Marking 40 Years of the Fund

Two African countries joined as donors in 2013

Angola Libya

Reaffirmed commitment to Africa’s transformation

ADF resources multiplied 10x between 1976–1996

Tripling of resources between 1999–2013

31

Cumulative resources of the ADF around USD 50 billion

Over the past 40 years, an amount of USD 49 billion directed to Africa’s

poorest countries

Internally generated resources boosted significantly since ADF-10

Strong support for Africa’s

transformation agenda

Total Resources level over USD 7 billion*,

a significant achievement in light of tough fiscal situation

faced by donors

In line with the Bank’s Ten-Year Strategy and operational priorities

of the Fund

Successful 13th Replenishment of ADF

* Excluding the technical gap

In USD million

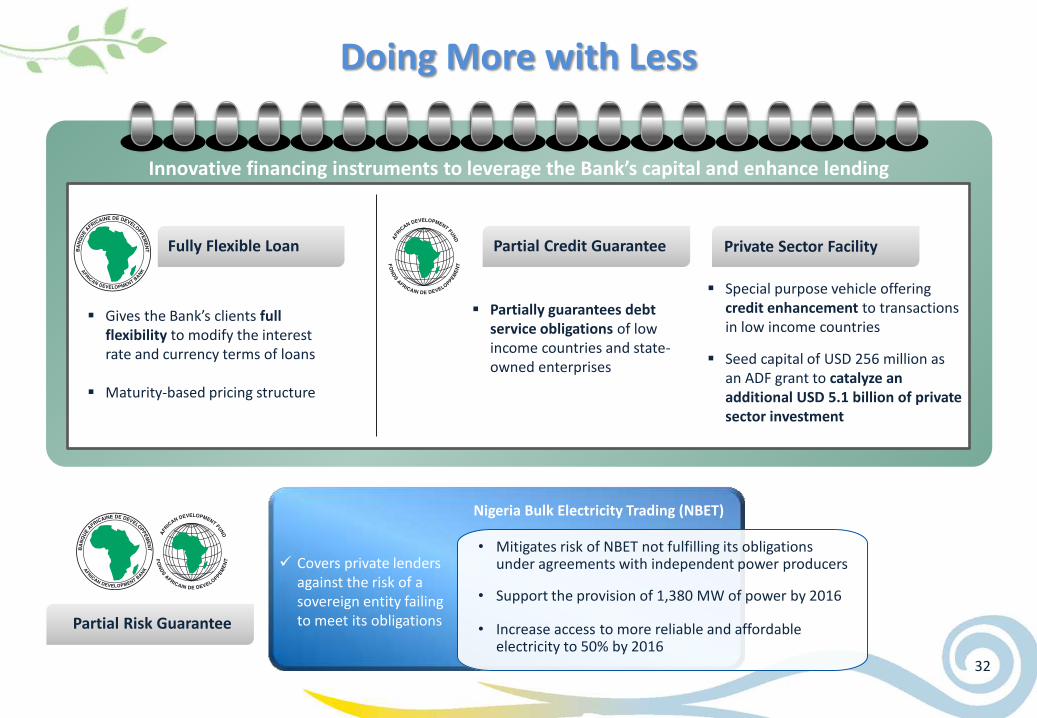

Doing More with Less

32

Innovative financing instruments to leverage the Bank’s capital and enhance lending

Gives the Bank’s clients full flexibility to modify the interest rate and currency terms of loans

Maturity-based pricing structure

Partially guarantees debt service obligations of low income countries and state-owned enterprises

Special purpose vehicle offering credit enhancement to transactions in low income countries

Seed capital of USD 256 million as an ADF grant to catalyze an additional USD 5.1 billion of private sector investment

Partial Credit Guarantee Private Sector Facility Fully Flexible Loan

Partial Risk Guarantee

Nigeria Bulk Electricity Trading (NBET)

• Mitigates risk of NBET not fulfilling its obligations under agreements with independent power producers

• Support the provision of 1,380 MW of power by 2016

• Increase access to more reliable and affordable electricity to 50% by 2016

Covers private lenders against the risk of a sovereign entity failing to meet its obligations

Propelling the Continent Forward

Lack of well prepared projects

Lack of public resources

Lack of early risk takers

Lack of “smart capital”

Lack of transaction advisors

A comprehensive set of solutions to

address Africa’s infrastructure deficit

Mobilizing private financing, bringing projects to bankability, accelerating the development of transformative infrastructure projects

Project development business line: To allow successful raising of long-term capital, reduce risk of delays, and ensure operational, financial and economical sustainability of investments

33

Africa Transport

ICT

Energy

Water

Project finance business line: To channel long-term funding in an efficient and timely manner

Aims to cut the period between project conception and financial close from 7 to 3 years

Target equity investment of USD 10 billion will leverage USD 100 billion worth of resources

Development-oriented and commercially operated entity

AfDB to invest up to USD 500 million

Medium-term target equity of USD 3 billion, to grow over time to USD 10 billion

Closer, on the Ground

Decentralization with delegations and safeguards

34

= Field office

= Regional Resource Center

Tunisia (TRA)

Egypt

Uganda

Malawi

Ghana

South Africa

Madagascar

Gabon

Mali

Nigeria

Tanzania

Zambia

Algeria

Ethiopia

Sudan

Kenya

Chad

Angola

Zimbabwe

Burundi

Togo CAR

Ivory Coast (HQ)

South Sudan

Mauritius Mozambique

Liberia Cameroon

Burkina Faso Senegal

Sierra Leone

Rwanda DRC

Morocco

Increased field presence from 4 in 2002 to 37 countries in 2013

About 50% of projects managed from the field

About 40% of operations staff work from the field

Reinforced presence in Benin, Guinea (Conakry), Guinea Bissau, Mauritania, Mauritius and São Tomé and Príncipe

42% of projects supervision led by field offices

v

• Enhanced partnership with clients

• Better integration and oversight

• Proactivity and increased responsiveness

• Reduced procurement turn-around time

• Better use of resources

• Opportunity to reduce delays in loan disbursements

São Tomé and

Príncipe

Financial Profile

35

An Extremely Strong Financial Profile with Shareholders’ Support

36

AAA/Stable "The (Bank’s AAA) ratings mainly reflect the strong support the Bank enjoys from African and non-African member countries; its solid financial base; its prudent financial and risk management policies; and its status as a “preferred creditor."

10 July 2013

AAA/Stable/A-1+ "The Bank benefits from a solid liquidity and capital position, along with wide support from its member countries, including “AAA” sovereigns."

19 December 2013

Aaa/Stable/P-1 "Because of the high risk environment under which it operates, the AfDB, perhaps more than any other MDB, constantly tries to improve its risk management as well as operational efficiency."

30 September 2013

Solid liquidity Extremely strong capitalization Very strong support from shareholders Preferred creditor status

Strict internal prudential framework on capitalization, borrowing and liquidity

Intrinsic financial strength Franchise value

"Capitalization is extremely strong, and is one of the key factors supporting its (AAA) ratings. The ratio of usable capital to required capital ratio, at 16.2x at end-2012, is also higher than for most of its peers."

16 August 2013

AAA/Stable/F1+

Strengthening the Foundations of the Bank

4 002 4 046 3 894

4 100 4 400

3 431 3 377 3 601

4 108

4 581

-

2 000

4 000

6 000

8 000

10 000

2009 2010 2011 2012 2013

Reserves Paid-in capital

GCI-VI payments and transfers to reserves provide capital boost

In USD million

7,433 7,424 7,494 8,208

8,980

Risk-Bearing Capacity increased by more than 20% since 2009

Additional Paid-in capital

of USD 2.85 billion

expected from 2014 to 2023

37

Risk-Bearing Capacity

Risk capital consumption

In USD million Sovereign 36%

Non-Sovereign 11%

Equity 9%

Treasury 5%

Operational 1%

Benefits Plan 3%

Diversification -3%

Total Risk Capital Consumption 62%

38% of risk capital available to support business growth

38

5 433

8 980

3 159

949

788 420 80

276 239

Available risk capital

Risk Class AfDB

Rating International

Rating Assessment

Very Low Risk

1+ A+ and above Excellent 1 A

1- A- 2+ BBB+

Strong 2 BBB 2- BBB-

Low Risk 3+ BB+

Good 3 BB 3- BB-

Moderate Risk

4+ B+ Satisfactory 4

B 4- 5+

B- Acceptable 5

High Risk

5- CCC+ Marginal

6+ 6 CCC

Special

Attention 6-

Very high Risk

7 CCC- Substandard

8 9 CC Doubtful

10 C Loss

Systematic Credit Risk Assessment Sovereign credit ratings are derived from a risk assessment that includes macroeconomic performance, debt sustainability, socio-political factors, business environment and the Bank’s portfolio performance

Non-sovereign credit ratings derived on the basis of several pre-determined critical factors including overall financial strength, industry outlook, competitive position, management strength and host country risk rating

Portfolio risk profile measured by the Weighted Average Risk Rating (WARR) under the Bank’s 22-grade master rating scale

0%

20%

40%

60%

80%

100%

2009 2010 2011 2012 2013

very low risk low risk moderate risk high risk very high risk

Non-Sovereign Portfolio risk profile

Sovereign Portfolio risk profile

0%

20%

40%

60%

80%

100%

2009 2010 2011 2012 2013

very low risk low risk moderate risk high risk very high risk

39

Growing Development-Related Exposure

Portfolio credit quality remains strong, and at the lower range of our defined risk appetite of "good" to "satisfactory" risk

More than 50% increase in the business portfolio since 2009

9 666 10 309 11 605 13 243

13 917 2 470 2 829 3 203

4 279 4 638

2,60 2,30 2,73 2,74 3,00

2009 2010 2011 2012 2013

Sovereign Portfolio Non-Sovereign Portfolio Weighted Average Risk Rating (WARR) *

12,136 13,138

14,808 17,522

18,555 In USD million

A broad suite of products supporting the clients financial needs

Equity and quasi- equity investments

Foreign and local currency loans

Partial Risk Guarantees

Partial credit Guarantees

Syndicated Loans

Trade Finance Risk management

products

Agency lines to fund SMEs via financial

intermediaries

* Portfolio risk profile measured by the Weighted Average Risk Rating (WARR) under the Bank’s 22-grade master rating scale

40

Capital preservation, liquidity and reasonable returns drive our investment strategy

14% 3% 5%

45%

3% 14% 16%

Strong liquidity risk management framework

Investment strategy regularly adapted to rapidly changing global financial markets, aims to strengthen credit quality and the liquidity profile of the portfolios while limiting the volatility of their returns

Controlled Market Risks

Targeting top quality investments

51% 44%

5%

AAA AA+ to AA- A and below

as of 31 December 2013

4 000

6 000

8 000

10 000

12 000

1Q10 3Q10 1Q11 3Q11 1Q12 3Q12 1Q13 3Q13 1Q14

Prudential Minimum Level of Liquidity Liquidity Level

Liquidity policy ensures that the Bank can, at all times, meet its loan disbursements, operational cash flow requirements, service debt and honor its guarantees for at least 1 year without resorting to additional funding from the capital markets

USD 10.84 billion of liquid assets 41

In USD million

Currency and Counterparty Credit Risk Management

451

1 679 1 830

1 609

838

132 148 224 168 206

-

400

800

1 200

1 600

2 000

2009 2010 2011 2012 2013

Fair Value Net Exposure AA+ to AA- A+ and Lower

Counterparty Risk Currency Exchange Risk

In USD million

as of 31 December 2013

Derivatives Portfolio Credit Risk Profile of Net Exposure

Prohibited from taking direct currency risk, matches liabilities in any one currency with assets in the same currency

Potential fluctuation of the value of the Bank’s net worth minimized by matching the currency composition of net assets with the UA

Administrative expenses hedged to protect the Bank from adverse exchange rate movements

Mitigates counterparty credit risk through minimum credit ratings, exposure limits and collateral exchange

agreements for derivatives

Strict minimum short-term credit rating for trading counterparties

Minimum rating of A-/A3 for derivatives counterparties, requiring one-way collateral

agreements. Daily collateral exchanges to maintain net exposures at acceptable levels

42

60% 58% 60% 58% 62%

2009 2010 2011 2012 2013

Insulating Stakeholders

Capital utilization Conservative leverage

Limit (100%) Limit (100%)

Robust level of capitalization and low leverage ratio allow for the smooth implementation of the Bank’s business plan

Risk Capital Utilization Rate = Σ ((Exposure) x (Risk capital allocation)) / Total risk capital

Usable Capital = Σ (Paid-in capital, Reserves, Callable capital of non-borrowing countries rated A- and above)

Debt to Usable Capital Risk Capital Utilization Rate

86% 84%

55% 50% 48%

2009 2010 2011 2012 2013

43

Income before distributions

Solid Internal Capital Generation

167

362

329

253

301 278

2004 2009 2010 2011 2012 2013. . .

Strong financial performance, despite the prevailing low interest rate environment of recent years

44

In USD million

Financial Capacity to Support Development Initiatives

Commitments under the Special Relief Fund to respond to emergency relief requests

Assistance to drought affected populations

Somalia

Relief to victims of locust invasion

Madagascar

Support to victims of terrorism

Kenya

Aid to 2013 food disaster

Mozambique

Fight against cholera epidemic

Guinea-Bissau

45

* Allocable income: income adjusted for unrealized gains (losses) on derivatives and borrowings, translation and fair valuation of macro hedge swaps

Increasing risk bearing capacity: USD 88 million transfer to reserves

Supporting more development activities in economically challenged countries: USD 65 million transfer to ADF

Participating in multilateral and bilateral reconstruction efforts: USD 82 million allocated to DRC mechanism

Extending humanitarian relief: USD 7.75 million allocation to the Special Relief Fund

Delivering transformational projects in Africa: USD 31 million to the Africa50 Fund

From the Bank’s allocable Income* From the Bank’s surplus account

Note: Allocation of income subject to approval by the Board of Governors Exchange rate as at 30 April 2014

Solid Showing in Capital Markets

46

47

USD 100 million 10.50% due October 1995

Kidder Peabody October 1985

USD 500 million 3.25% due July 2005

BNP Paribas, Daiwa SMBC July 2002

AUD 450 million 4.40% due February 2008

Daiwa January 2003

USD 1 billion 3.25% due August 2008 Goldman Sachs, HSBC,

Lehman Brothers August 2003

AUD 300 million 5.50% due February 2011

TD Securities February 2006

JPY 15 billion 7.40% due April 1997 Nomura, Bank of Tokyo

April 1985

JPY 30 billion 5.125% due May 2000

Yamaichi Securities April 1988

Long-term loans from non-regional governments

Commercial Banking Market

Syndicated Loans

USD 300 million 7.875% due April 2002 Swiss Bank Corporation

April 1992

USD 500 million 7.375% due April 2023 Goldman Sachs, Lehman

Brothers, SBC March 1993

ZAR 100 million 15% due March 1999

Hambros Bank March 1997

JPY 10 billion 3.19% in USD due July 2007

Yamaichi Securities July 1997

First Global Benchmark First Uridashi First Billion Global First Kangaroo

First Yankee Bond First Samurai First Daimyo The Early years

First Eurodollar First 30 Year Eurodollar First EuroRand First Private Placement

A Trip Down Memory Lane

47

649

2 770 3 772 3 844

5 578 4 739

2004 2010 2011 2012 2013 2014

Cost-Effective Resources Spurring Development

. . .

Borrowing program size in line with lending activities

48

Use of derivative instruments for asset and

liability management purposes

Meet lending and liquidity requirements

Develop access to markets across the world

In USD million

Raising Funds Around the World

49

A Global Issuer

Outstanding borrowings before swap As of 30 April 2014

USD 13mn

USD 1,566mn

USD 208mn

USD 315mn

USD 694mn

USD 12,543mn

USD 426mn

USD 196mn

USD 99mn

USD 132mn

USD 3,255mn

USD 31mn

USD 395mn

USD 349mn

USD 20mn

USD 24mn

USD 585mn

USD 1,131mn

Billion Dollar Benchmark Transactions Spark Interest

Distribution by investor type

Asset Managers

7%

Banks 23%

Central Bank / OIs* 67%

Corporates 3%

Africa Americas Asia Europe MiddleEast

11%

29%

41%

14% 5%

*Official Institutions

Distribution by region

Distribution by investor type

Asset Managers

19%

Banks 14%

Central Bank / OIs* 67%

Africa Americas Asia Europe MiddleEast

4%

32% 23%

37%

4%

Distribution by region

USD 2.175 billion 0.875% due March 2018 USD 1 billion 0.875% due May 2017

Highly oversubscribed (USD 2 billion of orders) and priced at mid-swaps plus 1bp (US Treasuries + 22.85 bps)

Over 50 investors, highlighting strong penetration across different geographical regions

First time participation of two African Central Banks, and repeated support from another two

Largest AfDB bond outstanding Increased four times from the initial USD 1 Billion, each time at a

tighter spread to US Treasuries Latest reopening at UST + 12.1 bps

50

Green Unleashed, Debut Green Bond Opens Doors

51

Going Green Worldwide

USD 500 million 0.75% due October

2016 JP Morgan, Morgan

Stanley, SEB October 2013

Support AfDB’s strategic objective of supporting Africa’s gradual transition to green growth

… and in Sweden

SEK 1 billion 1.75% due March

2019 Nordea

March 2014

SEK 1 billion Floating Rate Note due February 2019

Nordea February 2014

What Can Be Financed with AfDB Green Bonds

Greenfield Renewable Energy Generation (e.g. solar, wind, geothermal, and ocean power)

Biosphere conservation projects (reduce emissions from deforestation and degradation of ecosystems)

Solid Waste Management (e.g. incineration of waste, landfill gas capture and landfill gas combustion)

Demand-side Brownfield and Greenfield Energy Efficiency (e.g. energy efficiency improvements in lighting and equipment; retrofit of transmission lines, substations or distribution systems to reduce technical losses)

Vehicle energy efficiency fleet retrofit or urban transport modal change

Water Supply and Access (e.g. water-saving measures such as introduction of less water intensive crops or preservation of soil moisture and fertility)

Urban Development (e.g. rehabilitation and upgrade of urban water drainage systems in areas vulnerable to frequency and/or severity of flash floods and storm surges brought by climate change)

Industrial Processes (reduce GHG emissions from industrial processes improvements and cleaner production)

Fugitive emissions and carbon capture (e.g. carbon capture and storage, reduction of gas flaring or methane fugitive emissions in the oil and gas industry, coal mine methane capture)

52

Going Strong in Australia

Distribution by region

Distribution by investor type

AUD 1 billion 5.25% due March 2022

Delivering stable secondary market performance

(ASW mid levels)

Australian dollar, the second currency of funding of the Bank in 2012 and 2013

0,00

0,50

1,00

1,50

2011 2012 2013 2014*

Kangaroo Issuance Volume In AUD billion

* Year to date Fund Manager

60% Bank 22%

Insurance 15%

Central Bank 1%

Commercial Bank 2%

0%

20%

40%

60%

80%

Asia Australia Europe NorthAmerica

70%

24%

2% 5%

-

10,0

20,0

30,0

40,0

50,0

60,0

Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Jan-14 Feb-14 Mar-14

AfDB Jan-16 AfDB Jan-18 AfDB Feb-19

AfDB March-22 AfDB March-24

53

First Sterling Bond in Over 20 Years

54

Central Bank / OIs*

30%

Asset Managers

9% Banks 56%

Institutions/Private

Fund 4%

Corporate 1%

Distribution by investor type

Africa Americas Asia Europe UK/Ireland

4%

12%

27%

5%

52%

Distribution by region

December 2016 GBP 350 million 1.125% launched in 2014

GBP 250 million 3-year benchmark launched in January 2014

Priced at UK Treasury 4% Sep 2016 + 35 basis points

*Official Institutions

GBP 100 million increase executed in April 2014

Priced at UK Treasury 4% Sep 2016 + 34 basis points

Championing African Capital Markets

55

Strategy in support of Regional Financial Integration

Harmonization of financial governance and standards

Regional payment systems

AFMI website provides accurate data on African debt markets since May 2013

AFMI is also developing an African Bond Index

Knowledge management The African Financial Market Initiative (AFMI)

Advisory

ZAR, ZMK

ZAR

NGN, UGX, ZAR

GHS, UGX

NGN

2011

2012

2013

2014

2010

hjjjj

GHC, KES, NGN, TZS, ZAR

GHC, ZAR

UGX, ZAR

GHS, ZAR, ZMK

2006

2007

2008

2009

2005 BWP, ZAR

AfDB AAA issuer in the Ugandan Shilling market with UGX 12.5 Billion Floating Rate Notes under established UGX 125 Billion MTN program

Approval to issue ZMW bonds in Zambia

Established a Medium Term Note (MTN) program

in Zambia, for ZMW 160,000,000 Working with government authorities and

regulators to secure approvals to issue in their local currencies designated as lending currencies

Issued USD 4 billion worth of bonds in both off-shore (currency-linked) and domestic markets since 2005

Market intervention

387 620 1240 3,696

25,105 33,892

104,894

1964 1974 1976 1981 1987 1998 2010

Evolution of the capital of the Bank In USD million

Luxembourg

Adhesion signed in May 2014

Turkey became the 78th member of the Bank in October 2013

50 Years of Partnership for the Development of Africa

606 1 307 6 634

12 673 18 598

33 217

49 588

1976 1982 1988 1996 2002 2008 2013

ADF Cumulative resources In USD million

56 (exchange rate as at 30 April 2014)

A 50-year Journey

Creation of AfDB 10 staff, 33 member countries, USD 387 million initial capital

Landmark 200% capital increase, bringing capital to nearly USD 100 billion

Temporary relocation to Tunis

1964

2014 2010 2003

Propelling forward Africa’s recent development agenda

Firmly focused on achieving mandate and supporting Africa’s transformation

Ambitious goals underpinned by robust portfolio management ensuring better results and value for money

57

Creation of ADF

1972

Creation of NTF

1976

AfDB rated AAA

1984

AfDB responds to the economic and financial crisis

2009

Capital of AfDB opened to non-Africans

1982

2,000 staff and USD 33 billion in active operations. 78 member countries

2013

Return of the Bank to Abidjan

For More Information

www.afdb.org

[email protected] Investor Contact: [email protected]

(216) 71 10 39 00 (216) 71 35 19 33

Financial and Operational Analysis

Documentation for Debt Programs

Rating Agency Reports

Financial Products for Borrowers

Annual Report

afdb_acc AfDB_Group African

Development Bank Group

58

AfDB Income Statement (UA millions)

59 1 UA = 1 SDR = 1.56769 USD (2009) = 1.54003 USD (2010) = 1.53527 USD (2011) = 1.53692 USD (2012) = 1.54000(2013)

Year Ended 31 December 2013 2012 2011 2010 2009

Operational Income and Expenses

Income from Loans 335.01 351.16 314.92 293.36 288.24

Income from Investments and related derivatives 131.24 199.35 168.85 219.22 222.96

Income from Other Securities 3.95 4.83 5.41 6.74 7.68

Total income from Loans and Investments 470.20 555.34 489.18 519.32 518.88

Interest and amortized issuance costs (302.99) (356.41) (316.82) (303.04) (306.32)

Net interest on borrowing-related derivatives 111.85 139.16 112.16 126.27 73.28

Unrealized losses on borrowings, related derivatives and others

34.11 (10.17) (3.04) (40.94) (2.92)

Provision for Impairment on Loan Principal and Charges Receivable

(41.14) (29.69) (17.68) (26.76) (11.29)

Provision for Impairment on Equity Investments 0.76 (0.05) (0.15) (0.90) (2.32)

Provision for Impairment on Investments 9.19 0.29 6.39 18.58 3.39

Translation Gains/(Losses) 13.33 (2.27) (27.95) 4.87 19.63

Other Income 12.46 15.29 4.46 (1.72) 7.34

Net Operational Income 302.98 309.79 246.55 295.66 299.67

Administrative Expenses (110.97) (107.55) (79.50) (75.00) (63.06)

Depreciation – Property, Equipment and Intangible Assets (6.70) (4.59) (4.47) (4.59) (4.68)

Sundry (Expenses)/Income (4.98) (1.94) 1.93 (2.41) (0.77)

Total Other Expenses (122.65) (114.07) (82.04) (82.00) (68.51)

Income before Distributions Approved by the Board of Governors 180.33 195.71 164.51 213.66 231.16

Distributions of Income Approved by the Board of Governors (107.50) (110.00) (113.00) (146.37) (162.68)

Net Income for the Year 72.83 85.71 51.51 67.29 68.48

As at 31 December 2013 2012 2011 2010 2009

Assets

Due from Banks 954.13 881.45 344.16 395.72 318.83

Demand Obligations 3.80 3.80 3.80 3.80 3.80

Treasury Investments 6,058.45 6,487.51 7,590.47 7,433.53 7,412.25

Derivative Assets 985.96 1,558.33 1,696.68 1,421.48 764.00

Non-Negotiable Instruments on Account of Capital 1.20 1.97 3.04 4.62 8.19

Accounts Recievable 843.86 762.67 914.85 1,341.66 924.16

Outstanding Loans 11,440.70 10,885.80 9,373.52 8,293.01 7,538.00

Hedged Loans – Fair Value Adjustment 32.49 86.85 49.87 – –

Equity Participations 525.01 438.56 309.76 272.24 234.48

Other Securities 82.90 76.54 79.99 79.75 70.81

Other Assets 41.22 31.06 13.34 12.69 11.89

Total Assets 20,996.72 21,214.55 20,261.45 19,144.29 17,184.69

Liabilities, Capital and Reserves

Accounts Payable 1,246.11 2,083.07 1,974.68 2,015.04 1,385.68

Derivative Liabilities 971.85 512.60 502.29 328.30 477.12

Borrowings 12,947.44 13,278.80 12,902.96 11,980.56 10,580.64

Capital Subscriptions Paid 3,147.08 2,839.48 2,505.97 2,355.68 2,350.26

Reserves 2,856.88 2,667.44 2,536.18 2,627.28 2,552.96

Total Liabilities, Capital and Reserves 20,996.72 21,214.55 20,261.45 19,144.29 17,184.69

AfDB Balance Sheet Highlights (UA millions)

60

1 UA = 1 SDR = 1.56769 USD (2009) = 1.54003 USD (2010) = 1.53527 USD (2011) = 1.53692 USD (2012) = 1.54000(2013)