solvency ii: a market risk perspective · solvency ii: a market risk perspective ... • client...

TRANSCRIPT

Solvency II: A Market Risk Perspective

September 2010

David Lomas, ACII

Managing Director

FOR PROFESSIONAL INVESTORS ONLY

2

Agenda

I. BlackRock Overview

II. Solvency II v Market Reality

III.Conclusions

3

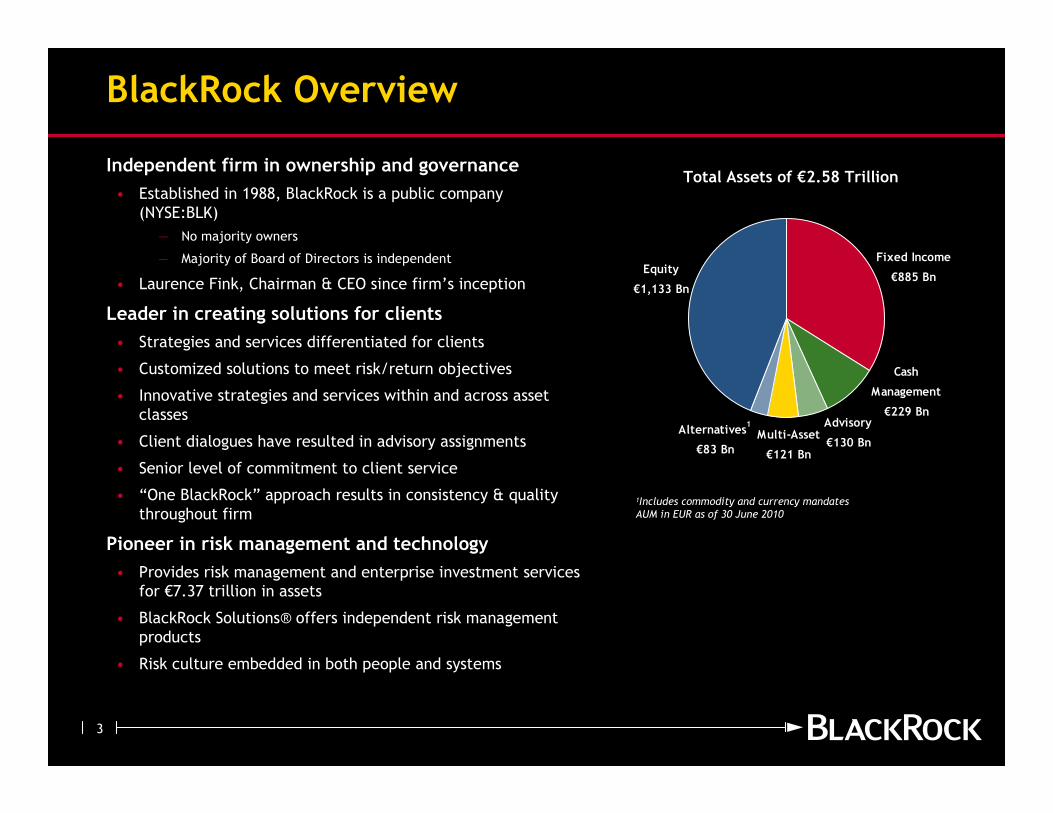

Multi-Asset

€121 Bn

Advisory

€130 BnAlternatives

1

€83 Bn

Equity

€1,133 Bn

Cash

Management

€229 Bn

Fixed Income

€885 Bn

BlackRock Overview

Independent firm in ownership and governance

• Established in 1988, BlackRock is a public company

(NYSE:BLK)

— No majority owners

— Majority of Board of Directors is independent

• Laurence Fink, Chairman & CEO since firm’s inception

Leader in creating solutions for clients

• Strategies and services differentiated for clients

• Customized solutions to meet risk/return objectives

• Innovative strategies and services within and across asset

classes

• Client dialogues have resulted in advisory assignments

• Senior level of commitment to client service

• “One BlackRock” approach results in consistency & quality

throughout firm

Pioneer in risk management and technology

• Provides risk management and enterprise investment services

for €7.37 trillion in assets

• BlackRock Solutions® offers independent risk management

products

• Risk culture embedded in both people and systems

Total Assets of €2.58 Trillion

1Includes commodity and currency mandatesAUM in EUR as of 30 June 2010

4

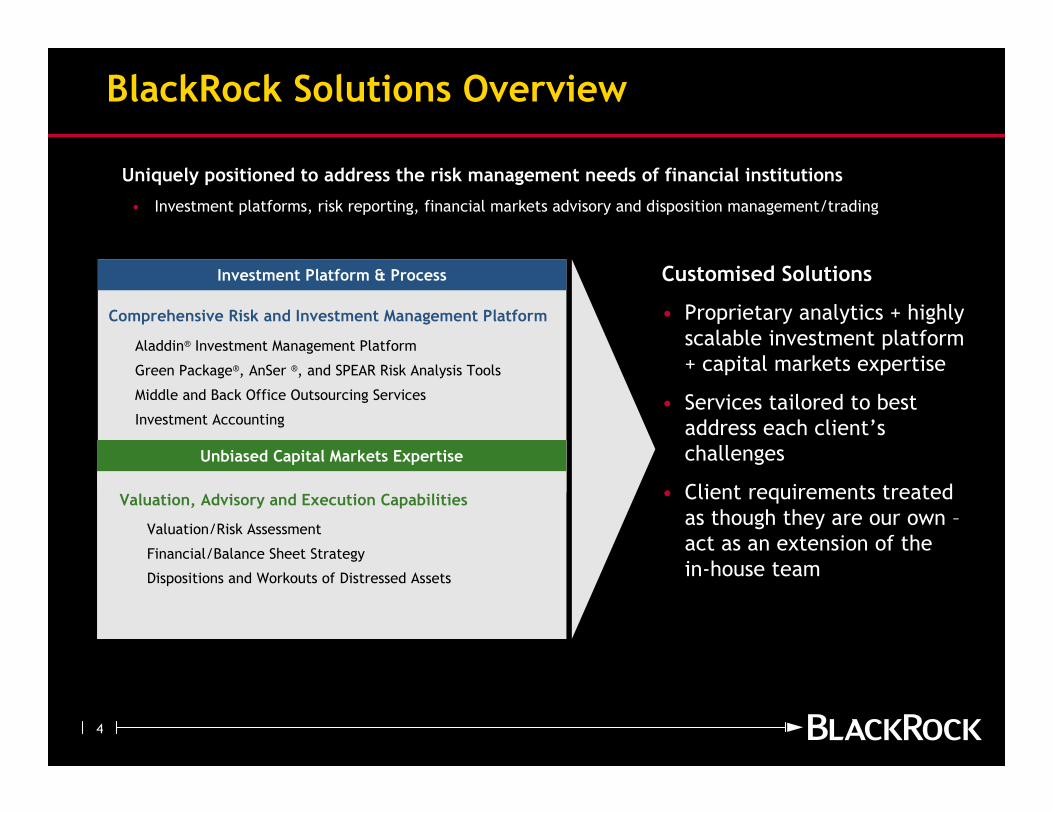

BlackRock Solutions Overview

Uniquely positioned to address the risk management needs of financial institutions

• Investment platforms, risk reporting, financial markets advisory and disposition management/trading

Customised Solutions

• Proprietary analytics + highly

scalable investment platform

+ capital markets expertise

• Services tailored to best

address each client’s

challenges

• Client requirements treated

as though they are our own –

act as an extension of the

in-house team

Investment Platform & Process

Aladdin® Investment Management Platform

Green Package®, AnSer ®, and SPEAR Risk Analysis Tools

Middle and Back Office Outsourcing Services

Investment Accounting

Comprehensive Risk and Investment Management Platform

Unbiased Capital Markets Expertise

Valuation, Advisory and Execution Capabilities

Valuation/Risk Assessment

Financial/Balance Sheet Strategy

Dispositions and Workouts of Distressed Assets

5

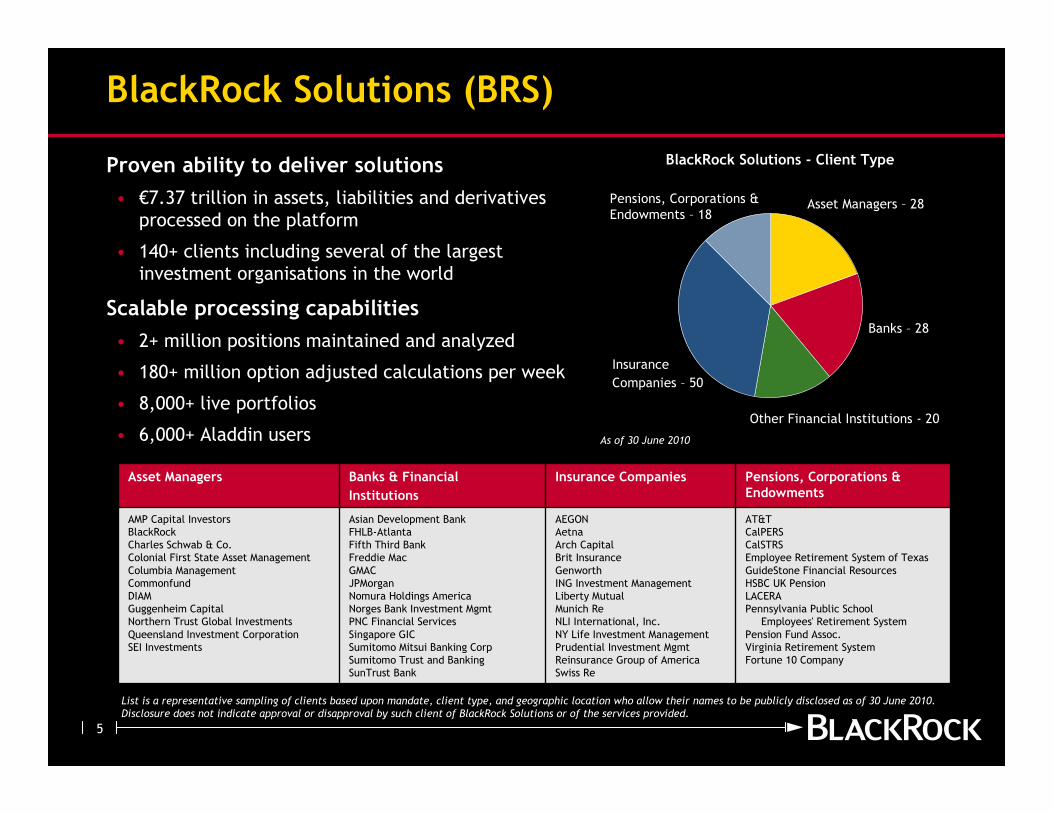

BlackRock Solutions (BRS)

Proven ability to deliver solutions

• €7.37 trillion in assets, liabilities and derivatives

processed on the platform

• 140+ clients including several of the largest

investment organisations in the world

Scalable processing capabilities

• 2+ million positions maintained and analyzed

• 180+ million option adjusted calculations per week

• 8,000+ live portfolios

• 6,000+ Aladdin users

BlackRock Solutions - Client Type

Banks – 28

Asset Managers – 28

Insurance

Companies – 50

Other Financial Institutions - 20

Pensions, Corporations &

Endowments – 18

List is a representative sampling of clients based upon mandate, client type, and geographic location who allow their names to be publicly disclosed as of 30 June 2010. Disclosure does not indicate approval or disapproval by such client of BlackRock Solutions or of the services provided.

AT&T

CalPERS

CalSTRS

Employee Retirement System of Texas

GuideStone Financial Resources

HSBC UK Pension

LACERA

Pennsylvania Public School

Employees' Retirement System

Pension Fund Assoc.

Virginia Retirement System

Fortune 10 Company

Pensions, Corporations & Endowments

AMP Capital Investors

BlackRock

Charles Schwab & Co.

Colonial First State Asset Management

Columbia Management

Commonfund

DIAM

Guggenheim Capital

Northern Trust Global Investments

Queensland Investment Corporation

SEI Investments

Asset Managers

AEGON

Aetna

Arch Capital

Brit Insurance

Genworth

ING Investment Management

Liberty Mutual

Munich Re

NLI International, Inc.

NY Life Investment Management

Prudential Investment Mgmt

Reinsurance Group of America

Swiss Re

Insurance Companies Banks & Financial

Institutions

Asian Development Bank

FHLB-Atlanta

Fifth Third Bank

Freddie Mac

GMAC

JPMorgan

Nomura Holdings America

Norges Bank Investment Mgmt

PNC Financial Services

Singapore GIC

Sumitomo Mitsui Banking Corp

Sumitomo Trust and Banking

SunTrust Bank

As of 30 June 2010

6

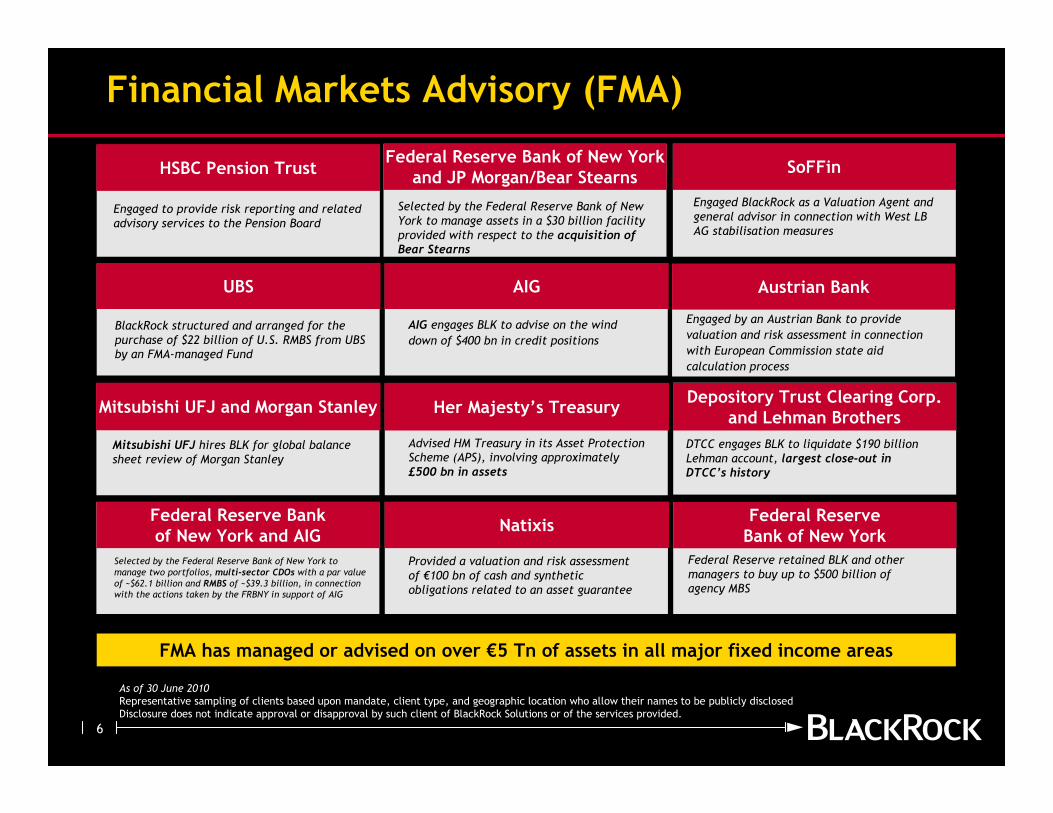

Financial Markets Advisory (FMA)

Engaged to provide risk reporting and related advisory services to the Pension Board

Selected by the Federal Reserve Bank of New York to manage assets in a $30 billion facility provided with respect to the acquisition of Bear Stearns

BlackRock structured and arranged for the purchase of $22 billion of U.S. RMBS from UBS by an FMA-managed Fund

AIG engages BLK to advise on the wind

down of $400 bn in credit positions

Engaged by an Austrian Bank to provide

valuation and risk assessment in connection

with European Commission state aid

calculation process

Mitsubishi UFJ hires BLK for global balance sheet review of Morgan Stanley

Advised HM Treasury in its Asset Protection Scheme (APS), involving approximately £500 bn in assets

DTCC engages BLK to liquidate $190 billion Lehman account, largest close-out in DTCC’s history

As of 30 June 2010Representative sampling of clients based upon mandate, client type, and geographic location who allow their names to be publicly disclosed

Disclosure does not indicate approval or disapproval by such client of BlackRock Solutions or of the services provided.

HSBC Pension TrustFederal Reserve Bank of New York

and JP Morgan/Bear Stearns

UBS AIG Austrian Bank

Mitsubishi UFJ and Morgan Stanley Her Majesty’s TreasuryDepository Trust Clearing Corp.

and Lehman Brothers

Provided a valuation and risk assessment of €100 bn of cash and synthetic obligations related to an asset guarantee

Federal Reserve retained BLK and other managers to buy up to $500 billion of agency MBS

Selected by the Federal Reserve Bank of New York to manage two portfolios, multi-sector CDOs with a par value of ~$62.1 billion and RMBS of ~$39.3 billion, in connection with the actions taken by the FRBNY in support of AIG

Federal Reserve Bank of New York and AIG

NatixisFederal Reserve Bank of New York

FMA has managed or advised on over €5 Tn of assets in all major fixed income areas

Engaged BlackRock as a Valuation Agent and general advisor in connection with West LB AG stabilisation measures

SoFFin

7

Agenda

I. BlackRock Overview

II. Solvency II v Market Reality

III.Conclusions

8

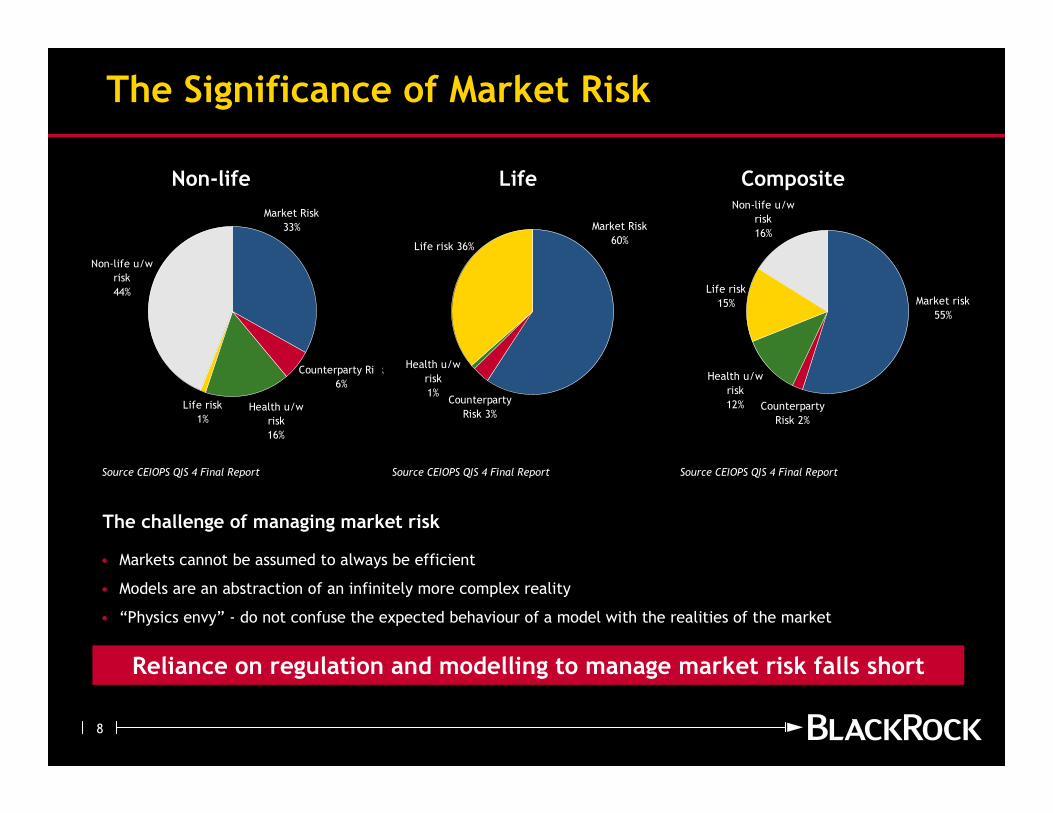

Market risk

55%

Non-life u/w

risk

16%

Health u/w

risk

12%

Life risk

15%

Counterparty

Risk 2%

Health u/w

risk

1%

Life risk 36%

Market Risk

60%

Counterparty

Risk 3%

Market Risk

33%

Non-life u/w

risk

44%

Life risk

1%Health u/w

risk

16%

Counterparty Risk

6%

The Significance of Market Risk

Reliance on regulation and modelling to manage market risk falls short

The challenge of managing market risk

Life Composite

Source CEIOPS QIS 4 Final Report

• Markets cannot be assumed to always be efficient

• Models are an abstraction of an infinitely more complex reality

• “Physics envy” - do not confuse the expected behaviour of a model with the realities of the market

Non-life

Source CEIOPS QIS 4 Final Report Source CEIOPS QIS 4 Final Report

9

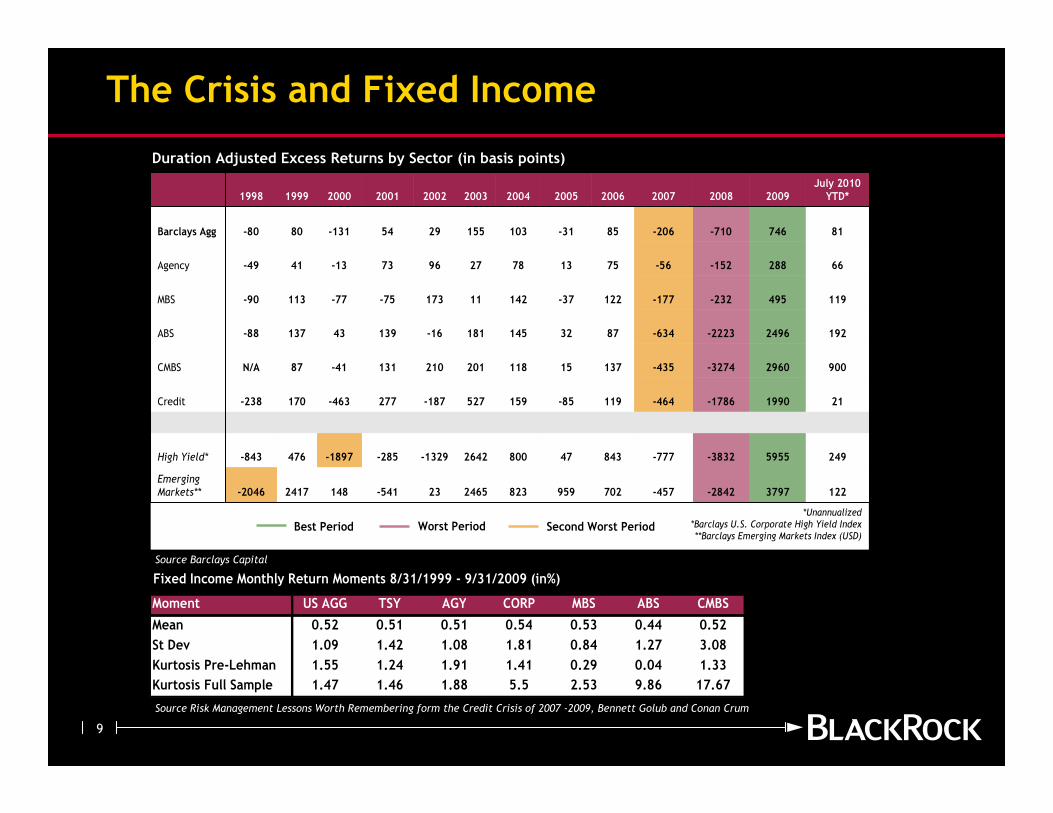

Moment US AGG TSY AGY CORP MBS ABS CMBS

Mean 0.52 0.51 0.51 0.54 0.53 0.44 0.52

St Dev 1.09 1.42 1.08 1.81 0.84 1.27 3.08

Kurtosis Pre-Lehman 1.55 1.24 1.91 1.41 0.29 0.04 1.33

Kurtosis Full Sample 1.47 1.46 1.88 5.5 2.53 9.86 17.67

Fixed Income Monthly Return Moments 8/31/1999 - 9/31/2009 (in%)

Worst Period Second Worst PeriodBest Period

*Unannualized*Barclays U.S. Corporate High Yield Index**Barclays Emerging Markets Index (USD)

3797

5955

1990

2960

2496

495

288

746

2009

122

249

21

900

192

119

66

81

July 2010 YTD*

-2842-457702959823246523-5411482417-2046Emerging Markets**

-3832-777843478002642-1329-285-1897476-843High Yield*

-1786

-3274

-2223

-232

-152

-710

2008

-464119-85159527-187277-463170-238Credit

-43513715118201210131-4187N/ACMBS

-6348732145181-1613943137-88ABS

-177122-3714211173-75-77113-90MBS

-56751378279673-1341-49Agency

-20685-311031552954-13180-80Barclays Agg

2007200620052004200320022001200019991998

3797

5955

1990

2960

2496

495

288

746

2009

122

249

21

900

192

119

66

81

July 2010 YTD*

-2842-457702959823246523-5411482417-2046Emerging Markets**

-3832-777843478002642-1329-285-1897476-843High Yield*

-1786

-3274

-2223

-232

-152

-710

2008

-464119-85159527-187277-463170-238Credit

-43513715118201210131-4187N/ACMBS

-6348732145181-1613943137-88ABS

-177122-3714211173-75-77113-90MBS

-56751378279673-1341-49Agency

-20685-311031552954-13180-80Barclays Agg

2007200620052004200320022001200019991998

The Crisis and Fixed Income

Source Barclays Capital

Source Risk Management Lessons Worth Remembering form the Credit Crisis of 2007 -2009, Bennett Golub and Conan Crum

Duration Adjusted Excess Returns by Sector (in basis points)

Fixed Income Monthly Return Moments 8/31/1999 - 9/31/2009 (in%)

10

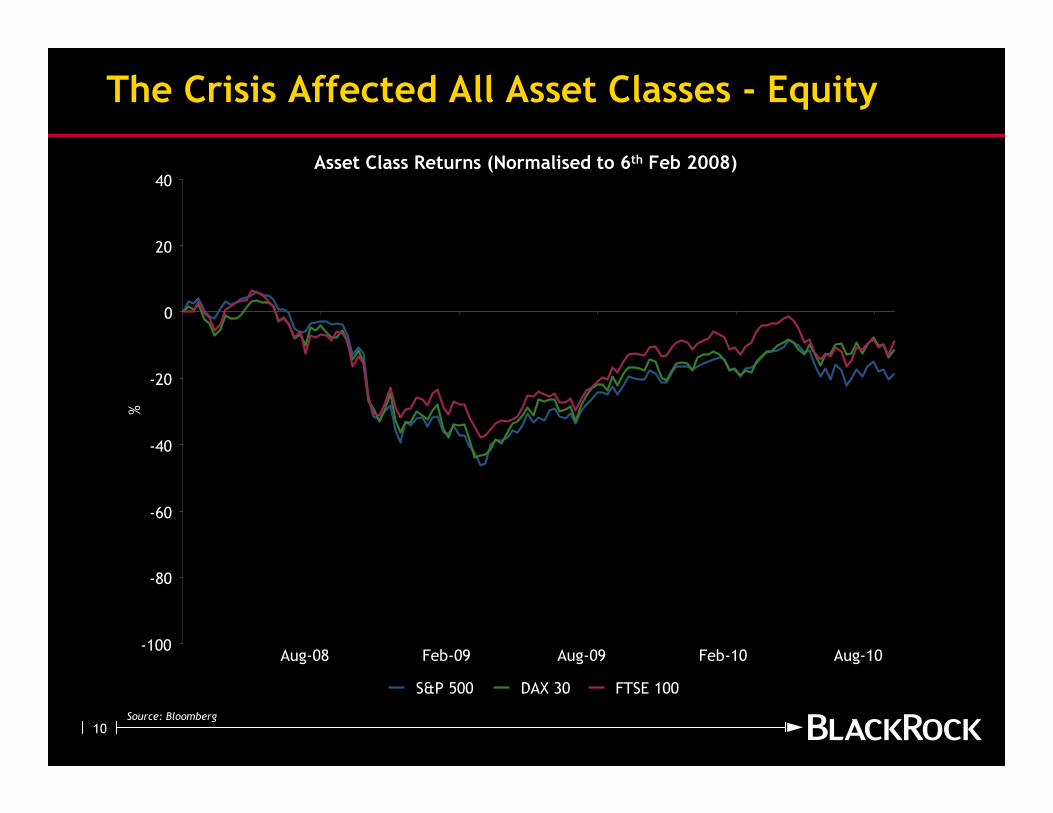

The Crisis Affected All Asset Classes - Equity

Asset Class Returns (Normalised to 6th Feb 2008)

Source: Bloomberg

-100

-80

-60

-40

-20

0

20

40

Aug-08 Feb-09 Aug-09 Feb-10 Aug-10

%

S&P 500 DAX 30 FTSE 100

11

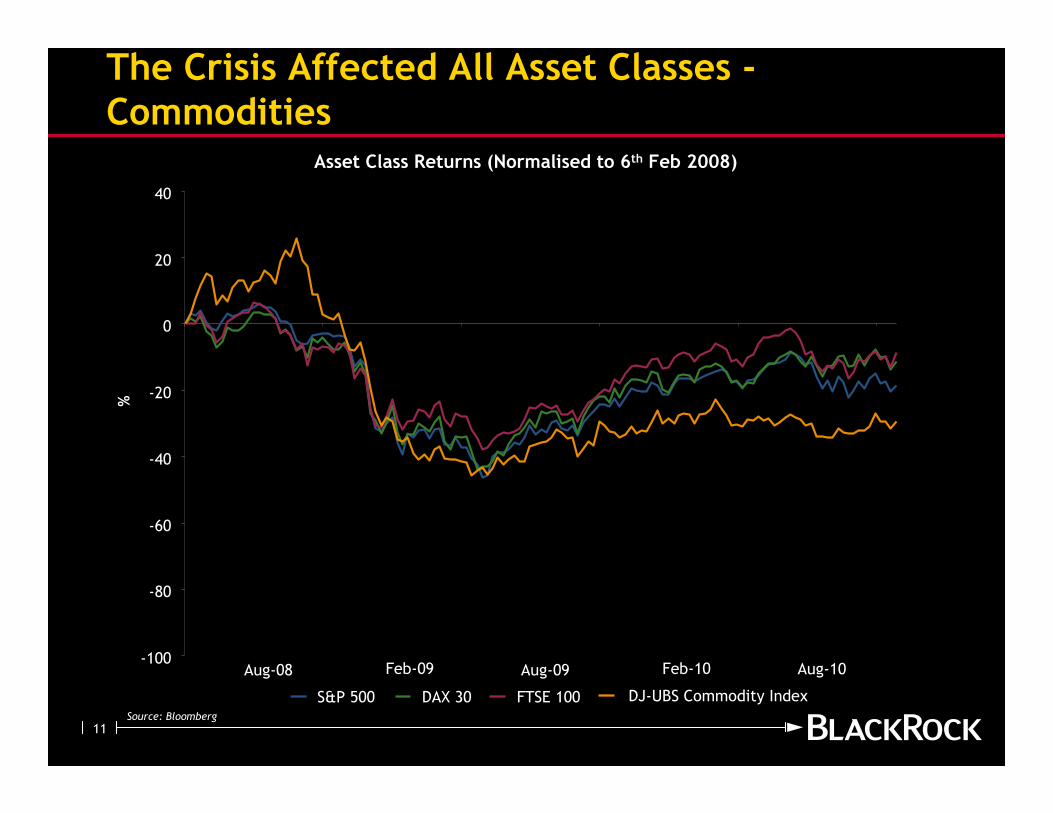

-100

-80

-60

-40

-20

0

20

40

Aug-08 Feb-09 Aug-09 Feb-10 Aug-10

%

DJ-UBS Commodity Index

The Crisis Affected All Asset Classes -Commodities

Asset Class Returns (Normalised to 6th Feb 2008)

Source: Bloomberg

S&P 500 DAX 30 FTSE 100

12

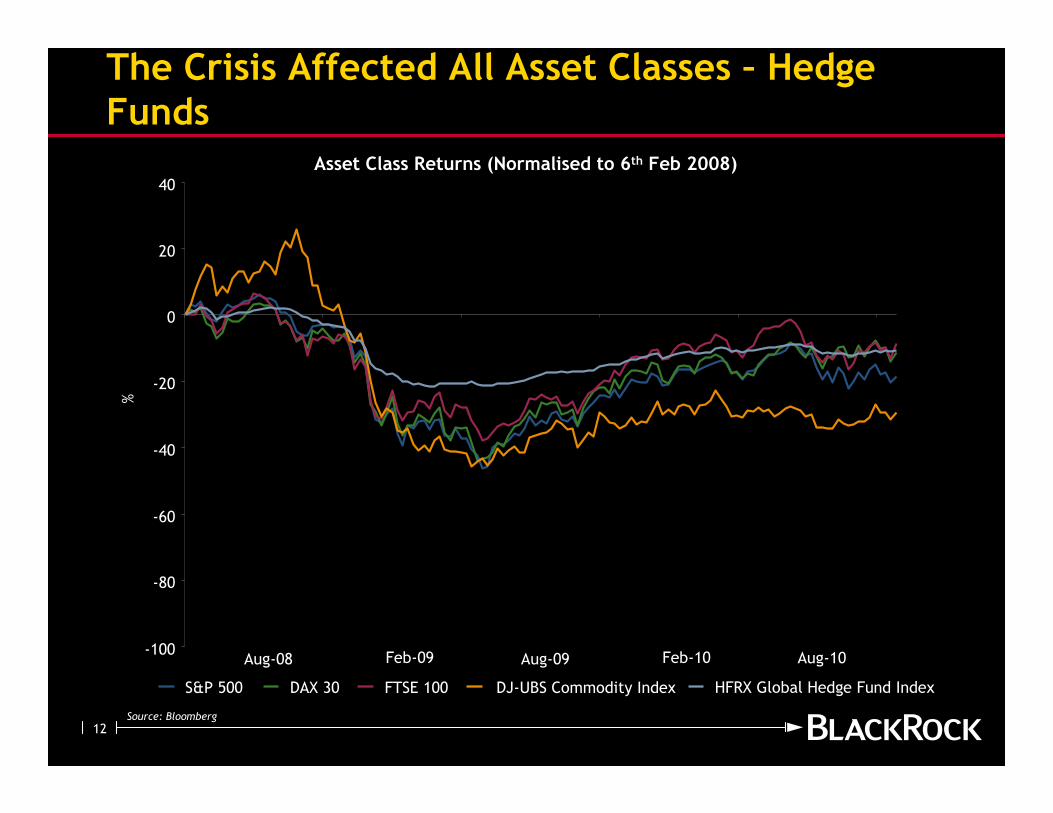

-100

-80

-60

-40

-20

0

20

40

%

HFRX Global Hedge Fund Index

The Crisis Affected All Asset Classes – Hedge Funds

Asset Class Returns (Normalised to 6th Feb 2008)

Source: Bloomberg

Aug-08 Feb-09 Aug-09 Feb-10 Aug-10

DJ-UBS Commodity IndexS&P 500 DAX 30 FTSE 100

13

-100

-80

-60

-40

-20

0

20

40

%

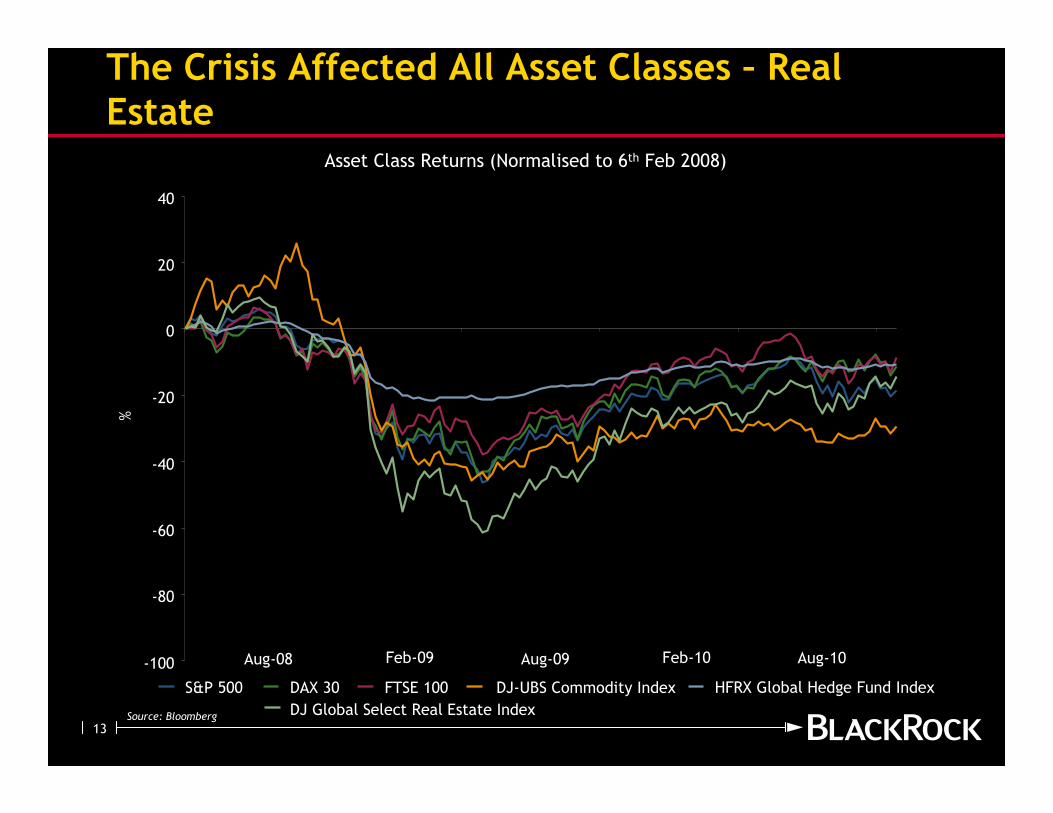

DJ Global Select Real Estate Index

The Crisis Affected All Asset Classes – Real Estate

Asset Class Returns (Normalised to 6th Feb 2008)

Source: Bloomberg

Aug-08 Feb-09 Aug-09 Feb-10 Aug-10

HFRX Global Hedge Fund IndexDJ-UBS Commodity IndexS&P 500 DAX 30 FTSE 100

14

-100

-80

-60

-40

-20

0

20

40

%

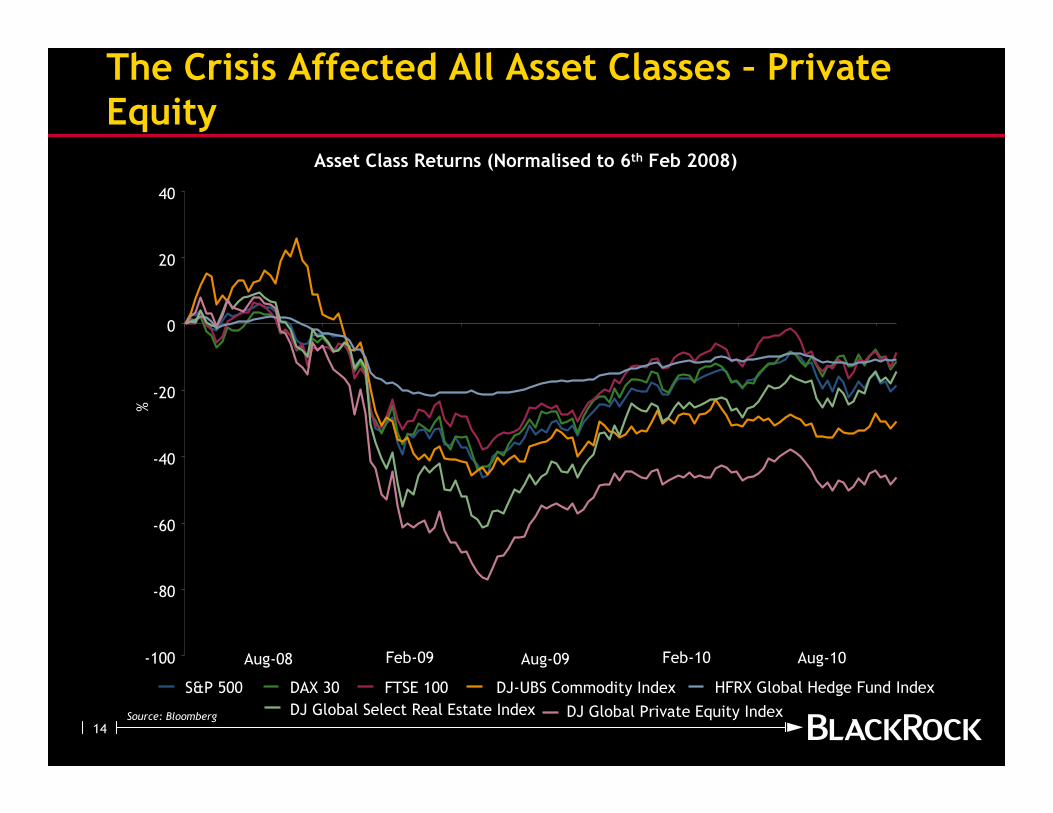

DJ Global Private Equity Index

The Crisis Affected All Asset Classes – Private Equity

Asset Class Returns (Normalised to 6th Feb 2008)

Source: Bloomberg

Aug-08 Feb-09 Aug-09 Feb-10 Aug-10

DJ Global Select Real Estate Index

HFRX Global Hedge Fund IndexDJ-UBS Commodity IndexS&P 500 DAX 30 FTSE 100

15

-100

-80

-60

-40

-20

0

20

40

%

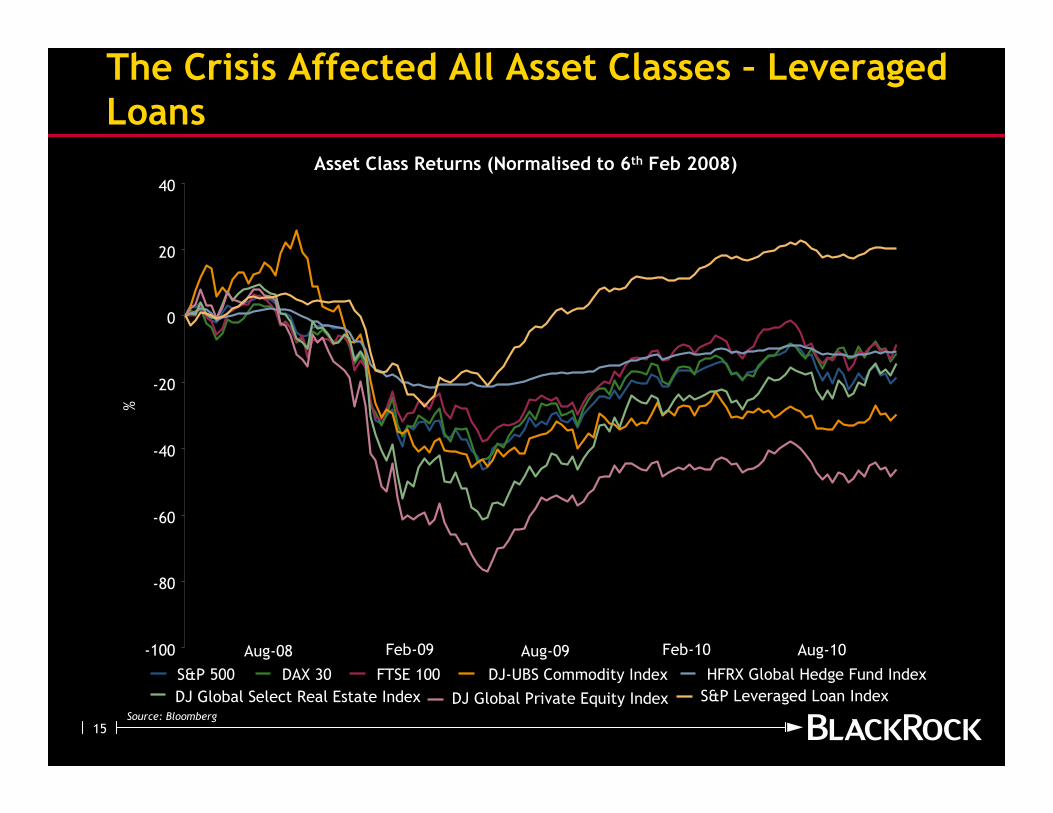

S&P Leveraged Loan Index

The Crisis Affected All Asset Classes – Leveraged Loans

Asset Class Returns (Normalised to 6th Feb 2008)

Source: Bloomberg

Aug-08 Feb-09 Aug-09 Feb-10 Aug-10

DJ Global Private Equity IndexDJ Global Select Real Estate Index

HFRX Global Hedge Fund IndexDJ-UBS Commodity IndexS&P 500 DAX 30 FTSE 100

16

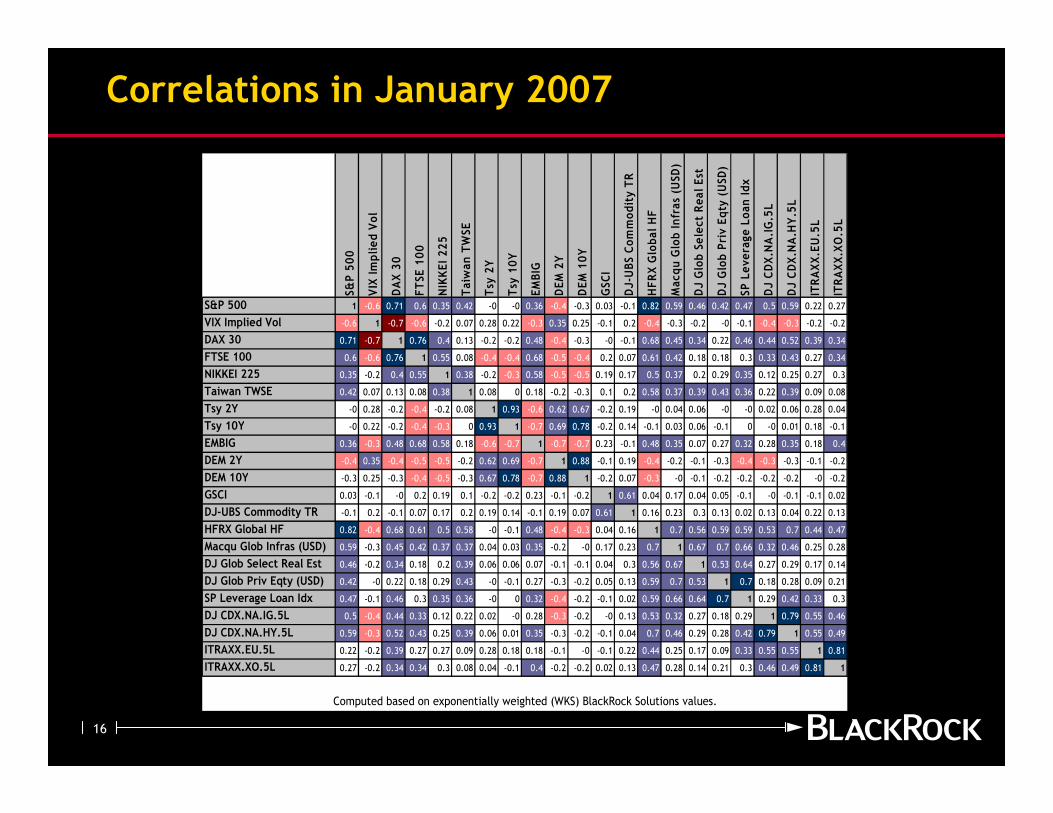

Correlations in January 2007

S&P 500

VIX Implied Vol

DAX 30

FTSE 100

NIKKEI 225

Taiwan TWSE

Tsy 2Y

Tsy 10Y

EMBIG

DEM 2Y

DEM 10Y

GSCI

DJ-UBS Commodity TR

HFRX Global HF

Macqu Glob Infras (USD)

DJ Glob Select Real Est

DJ Glob Priv Eqty (USD)

SP Leverage Loan Idx

DJ CDX.NA.IG.5L

DJ CDX.NA.HY.5L

ITRAXX.EU.5L

ITRAXX.XO.5L

S&P 500 1 -0.6 0.71 0.6 0.35 0.42 -0 -0 0.36 -0.4 -0.3 0.03 -0.1 0.82 0.59 0.46 0.42 0.47 0.5 0.59 0.22 0.27

VIX Implied Vol -0.6 1 -0.7 -0.6 -0.2 0.07 0.28 0.22 -0.3 0.35 0.25 -0.1 0.2 -0.4 -0.3 -0.2 -0 -0.1 -0.4 -0.3 -0.2 -0.2

DAX 30 0.71 -0.7 1 0.76 0.4 0.13 -0.2 -0.2 0.48 -0.4 -0.3 -0 -0.1 0.68 0.45 0.34 0.22 0.46 0.44 0.52 0.39 0.34

FTSE 100 0.6 -0.6 0.76 1 0.55 0.08 -0.4 -0.4 0.68 -0.5 -0.4 0.2 0.07 0.61 0.42 0.18 0.18 0.3 0.33 0.43 0.27 0.34

NIKKEI 225 0.35 -0.2 0.4 0.55 1 0.38 -0.2 -0.3 0.58 -0.5 -0.5 0.19 0.17 0.5 0.37 0.2 0.29 0.35 0.12 0.25 0.27 0.3

Taiwan TWSE 0.42 0.07 0.13 0.08 0.38 1 0.08 0 0.18 -0.2 -0.3 0.1 0.2 0.58 0.37 0.39 0.43 0.36 0.22 0.39 0.09 0.08

Tsy 2Y -0 0.28 -0.2 -0.4 -0.2 0.08 1 0.93 -0.6 0.62 0.67 -0.2 0.19 -0 0.04 0.06 -0 -0 0.02 0.06 0.28 0.04

Tsy 10Y -0 0.22 -0.2 -0.4 -0.3 0 0.93 1 -0.7 0.69 0.78 -0.2 0.14 -0.1 0.03 0.06 -0.1 0 -0 0.01 0.18 -0.1

EMBIG 0.36 -0.3 0.48 0.68 0.58 0.18 -0.6 -0.7 1 -0.7 -0.7 0.23 -0.1 0.48 0.35 0.07 0.27 0.32 0.28 0.35 0.18 0.4

DEM 2Y -0.4 0.35 -0.4 -0.5 -0.5 -0.2 0.62 0.69 -0.7 1 0.88 -0.1 0.19 -0.4 -0.2 -0.1 -0.3 -0.4 -0.3 -0.3 -0.1 -0.2

DEM 10Y -0.3 0.25 -0.3 -0.4 -0.5 -0.3 0.67 0.78 -0.7 0.88 1 -0.2 0.07 -0.3 -0 -0.1 -0.2 -0.2 -0.2 -0.2 -0 -0.2

GSCI 0.03 -0.1 -0 0.2 0.19 0.1 -0.2 -0.2 0.23 -0.1 -0.2 1 0.61 0.04 0.17 0.04 0.05 -0.1 -0 -0.1 -0.1 0.02

DJ-UBS Commodity TR -0.1 0.2 -0.1 0.07 0.17 0.2 0.19 0.14 -0.1 0.19 0.07 0.61 1 0.16 0.23 0.3 0.13 0.02 0.13 0.04 0.22 0.13

HFRX Global HF 0.82 -0.4 0.68 0.61 0.5 0.58 -0 -0.1 0.48 -0.4 -0.3 0.04 0.16 1 0.7 0.56 0.59 0.59 0.53 0.7 0.44 0.47

Macqu Glob Infras (USD) 0.59 -0.3 0.45 0.42 0.37 0.37 0.04 0.03 0.35 -0.2 -0 0.17 0.23 0.7 1 0.67 0.7 0.66 0.32 0.46 0.25 0.28

DJ Glob Select Real Est 0.46 -0.2 0.34 0.18 0.2 0.39 0.06 0.06 0.07 -0.1 -0.1 0.04 0.3 0.56 0.67 1 0.53 0.64 0.27 0.29 0.17 0.14

DJ Glob Priv Eqty (USD) 0.42 -0 0.22 0.18 0.29 0.43 -0 -0.1 0.27 -0.3 -0.2 0.05 0.13 0.59 0.7 0.53 1 0.7 0.18 0.28 0.09 0.21

SP Leverage Loan Idx 0.47 -0.1 0.46 0.3 0.35 0.36 -0 0 0.32 -0.4 -0.2 -0.1 0.02 0.59 0.66 0.64 0.7 1 0.29 0.42 0.33 0.3

DJ CDX.NA.IG.5L 0.5 -0.4 0.44 0.33 0.12 0.22 0.02 -0 0.28 -0.3 -0.2 -0 0.13 0.53 0.32 0.27 0.18 0.29 1 0.79 0.55 0.46

DJ CDX.NA.HY.5L 0.59 -0.3 0.52 0.43 0.25 0.39 0.06 0.01 0.35 -0.3 -0.2 -0.1 0.04 0.7 0.46 0.29 0.28 0.42 0.79 1 0.55 0.49

ITRAXX.EU.5L 0.22 -0.2 0.39 0.27 0.27 0.09 0.28 0.18 0.18 -0.1 -0 -0.1 0.22 0.44 0.25 0.17 0.09 0.33 0.55 0.55 1 0.81

ITRAXX.XO.5L 0.27 -0.2 0.34 0.34 0.3 0.08 0.04 -0.1 0.4 -0.2 -0.2 0.02 0.13 0.47 0.28 0.14 0.21 0.3 0.46 0.49 0.81 1

Computed based on exponentially weighted (WKS) BlackRock Solutions values.

17

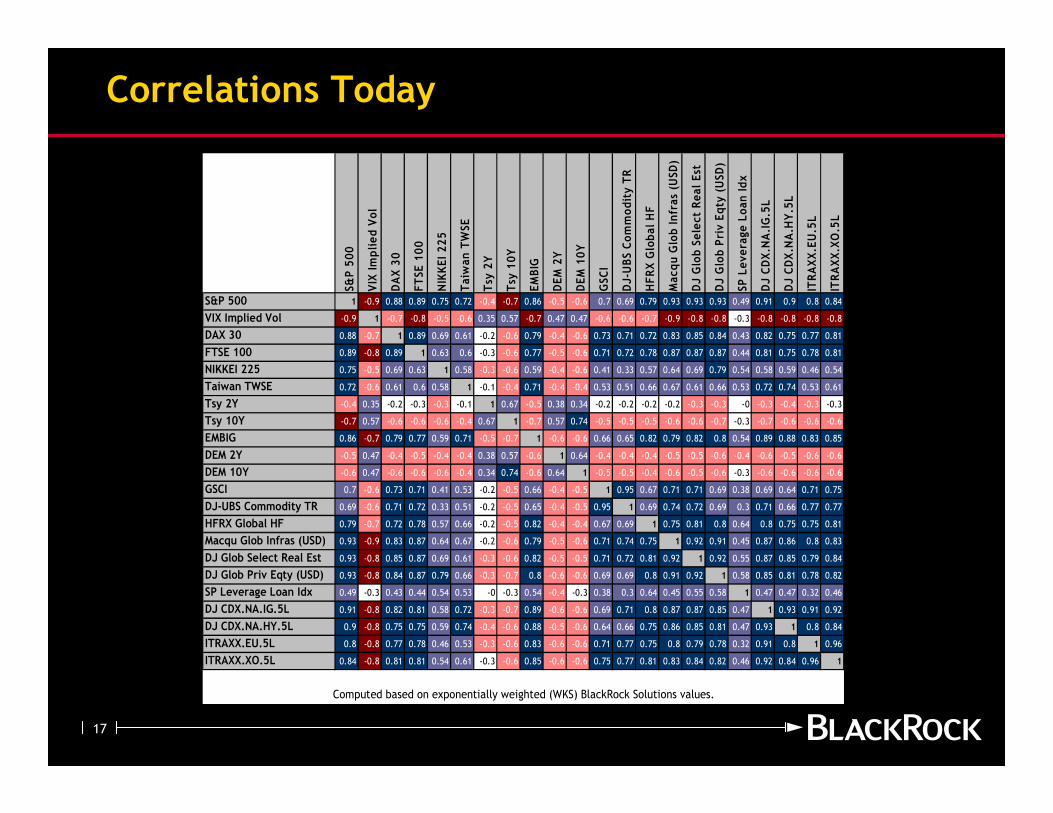

Correlations Today

S&P 500

VIX Implied Vol

DAX 30

FTSE 100

NIKKEI 225

Taiwan TWSE

Tsy 2Y

Tsy 10Y

EMBIG

DEM 2Y

DEM 10Y

GSCI

DJ-UBS Commodity TR

HFRX Global HF

Macqu Glob Infras (USD)

DJ Glob Select Real Est

DJ Glob Priv Eqty (USD)

SP Leverage Loan Idx

DJ CDX.NA.IG.5L

DJ CDX.NA.HY.5L

ITRAXX.EU.5L

ITRAXX.XO.5L

S&P 500 1 -0.9 0.88 0.89 0.75 0.72 -0.4 -0.7 0.86 -0.5 -0.6 0.7 0.69 0.79 0.93 0.93 0.93 0.49 0.91 0.9 0.8 0.84

VIX Implied Vol -0.9 1 -0.7 -0.8 -0.5 -0.6 0.35 0.57 -0.7 0.47 0.47 -0.6 -0.6 -0.7 -0.9 -0.8 -0.8 -0.3 -0.8 -0.8 -0.8 -0.8

DAX 30 0.88 -0.7 1 0.89 0.69 0.61 -0.2 -0.6 0.79 -0.4 -0.6 0.73 0.71 0.72 0.83 0.85 0.84 0.43 0.82 0.75 0.77 0.81

FTSE 100 0.89 -0.8 0.89 1 0.63 0.6 -0.3 -0.6 0.77 -0.5 -0.6 0.71 0.72 0.78 0.87 0.87 0.87 0.44 0.81 0.75 0.78 0.81

NIKKEI 225 0.75 -0.5 0.69 0.63 1 0.58 -0.3 -0.6 0.59 -0.4 -0.6 0.41 0.33 0.57 0.64 0.69 0.79 0.54 0.58 0.59 0.46 0.54

Taiwan TWSE 0.72 -0.6 0.61 0.6 0.58 1 -0.1 -0.4 0.71 -0.4 -0.4 0.53 0.51 0.66 0.67 0.61 0.66 0.53 0.72 0.74 0.53 0.61

Tsy 2Y -0.4 0.35 -0.2 -0.3 -0.3 -0.1 1 0.67 -0.5 0.38 0.34 -0.2 -0.2 -0.2 -0.2 -0.3 -0.3 -0 -0.3 -0.4 -0.3 -0.3

Tsy 10Y -0.7 0.57 -0.6 -0.6 -0.6 -0.4 0.67 1 -0.7 0.57 0.74 -0.5 -0.5 -0.5 -0.6 -0.6 -0.7 -0.3 -0.7 -0.6 -0.6 -0.6

EMBIG 0.86 -0.7 0.79 0.77 0.59 0.71 -0.5 -0.7 1 -0.6 -0.6 0.66 0.65 0.82 0.79 0.82 0.8 0.54 0.89 0.88 0.83 0.85

DEM 2Y -0.5 0.47 -0.4 -0.5 -0.4 -0.4 0.38 0.57 -0.6 1 0.64 -0.4 -0.4 -0.4 -0.5 -0.5 -0.6 -0.4 -0.6 -0.5 -0.6 -0.6

DEM 10Y -0.6 0.47 -0.6 -0.6 -0.6 -0.4 0.34 0.74 -0.6 0.64 1 -0.5 -0.5 -0.4 -0.6 -0.5 -0.6 -0.3 -0.6 -0.6 -0.6 -0.6

GSCI 0.7 -0.6 0.73 0.71 0.41 0.53 -0.2 -0.5 0.66 -0.4 -0.5 1 0.95 0.67 0.71 0.71 0.69 0.38 0.69 0.64 0.71 0.75

DJ-UBS Commodity TR 0.69 -0.6 0.71 0.72 0.33 0.51 -0.2 -0.5 0.65 -0.4 -0.5 0.95 1 0.69 0.74 0.72 0.69 0.3 0.71 0.66 0.77 0.77

HFRX Global HF 0.79 -0.7 0.72 0.78 0.57 0.66 -0.2 -0.5 0.82 -0.4 -0.4 0.67 0.69 1 0.75 0.81 0.8 0.64 0.8 0.75 0.75 0.81

Macqu Glob Infras (USD) 0.93 -0.9 0.83 0.87 0.64 0.67 -0.2 -0.6 0.79 -0.5 -0.6 0.71 0.74 0.75 1 0.92 0.91 0.45 0.87 0.86 0.8 0.83

DJ Glob Select Real Est 0.93 -0.8 0.85 0.87 0.69 0.61 -0.3 -0.6 0.82 -0.5 -0.5 0.71 0.72 0.81 0.92 1 0.92 0.55 0.87 0.85 0.79 0.84

DJ Glob Priv Eqty (USD) 0.93 -0.8 0.84 0.87 0.79 0.66 -0.3 -0.7 0.8 -0.6 -0.6 0.69 0.69 0.8 0.91 0.92 1 0.58 0.85 0.81 0.78 0.82

SP Leverage Loan Idx 0.49 -0.3 0.43 0.44 0.54 0.53 -0 -0.3 0.54 -0.4 -0.3 0.38 0.3 0.64 0.45 0.55 0.58 1 0.47 0.47 0.32 0.46

DJ CDX.NA.IG.5L 0.91 -0.8 0.82 0.81 0.58 0.72 -0.3 -0.7 0.89 -0.6 -0.6 0.69 0.71 0.8 0.87 0.87 0.85 0.47 1 0.93 0.91 0.92

DJ CDX.NA.HY.5L 0.9 -0.8 0.75 0.75 0.59 0.74 -0.4 -0.6 0.88 -0.5 -0.6 0.64 0.66 0.75 0.86 0.85 0.81 0.47 0.93 1 0.8 0.84

ITRAXX.EU.5L 0.8 -0.8 0.77 0.78 0.46 0.53 -0.3 -0.6 0.83 -0.6 -0.6 0.71 0.77 0.75 0.8 0.79 0.78 0.32 0.91 0.8 1 0.96

ITRAXX.XO.5L 0.84 -0.8 0.81 0.81 0.54 0.61 -0.3 -0.6 0.85 -0.6 -0.6 0.75 0.77 0.81 0.83 0.84 0.82 0.46 0.92 0.84 0.96 1

Computed based on exponentially weighted (WKS) BlackRock Solutions values.

18

Lessons from the Crisis

• The paramount importance of liquidity – the life blood of commerce

— What is the market value of an asset that does not trade?

• Risk models require vigilance and scepticism - assumptions are just assumptions

— Risk analytics and processes need to be constantly reviewed and reinvented

• Look beyond securitised products to the behaviour of underlying assets

— Need an in depth and direct understanding of the behaviours, incentives and practices of

borrowers, servicers and the origination process

— Incorporate this understanding properly into risk analytics and models to manage model risk

• The sources of risk are not constant and can change quickly

— Power and control over financial systems is shifting to political capitals

• You can’t cram for a crisis

— A robust risk management process requires a material commitment of resources and

“institutional buy-in”

• Risk takers must think like risk managers

— Must provide portfolio managers with the necessary tools to help them make the

appropriate risk-return trade off

• Has the portfolio manager identified the relevant risk drivers?

• Does the portfolio manager have access to accurate and timely ex ante metrics / an appropriate risk

dashboard?

19

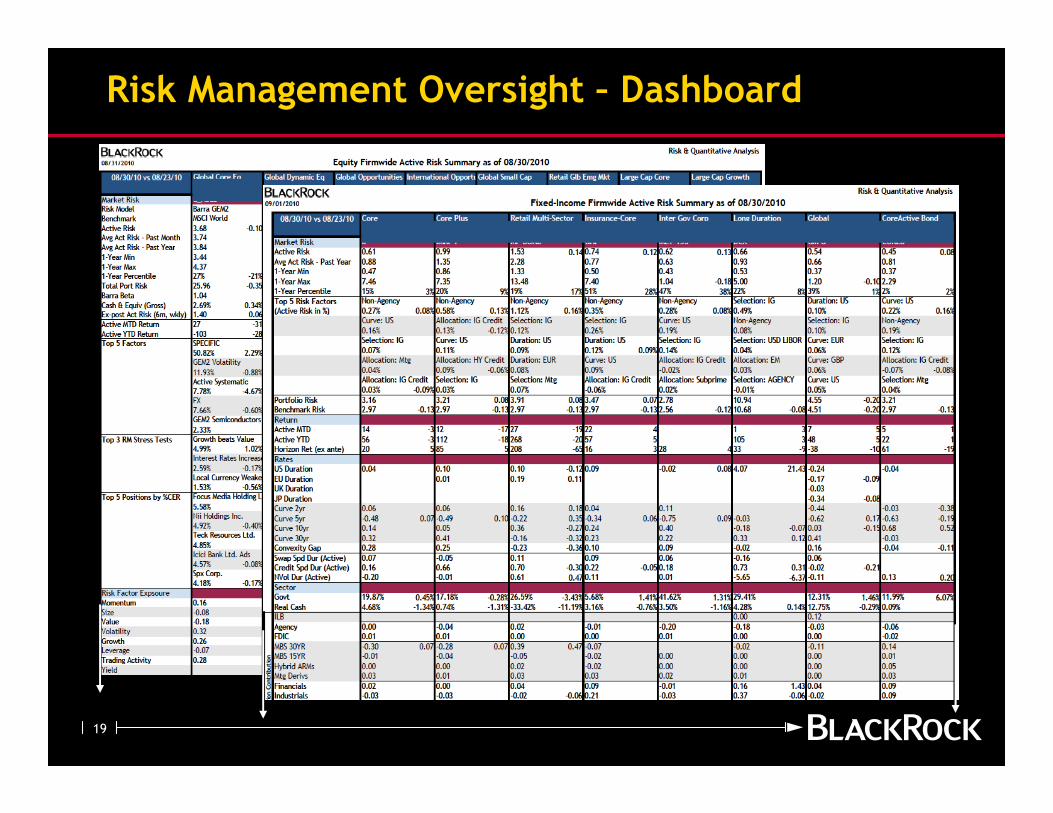

Risk Management Oversight – Dashboard

20

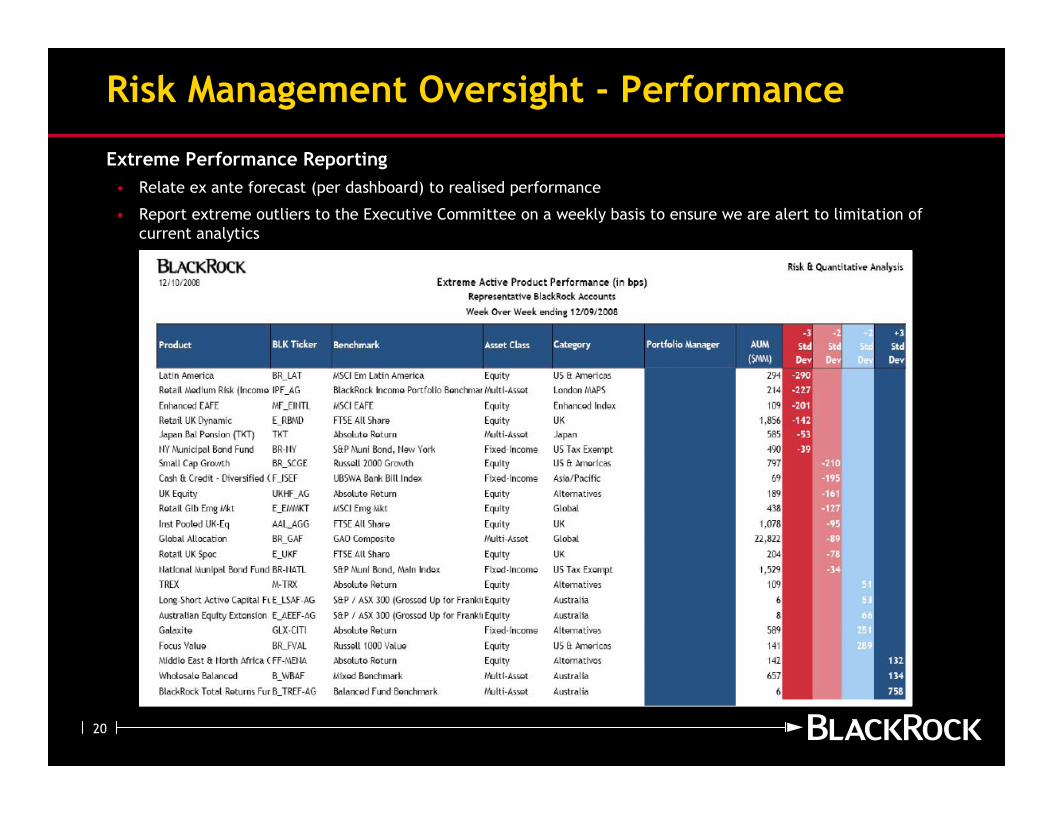

Risk Management Oversight - Performance

Extreme Performance Reporting

• Relate ex ante forecast (per dashboard) to realised performance

• Report extreme outliers to the Executive Committee on a weekly basis to ensure we are alert to limitation of

current analytics

21

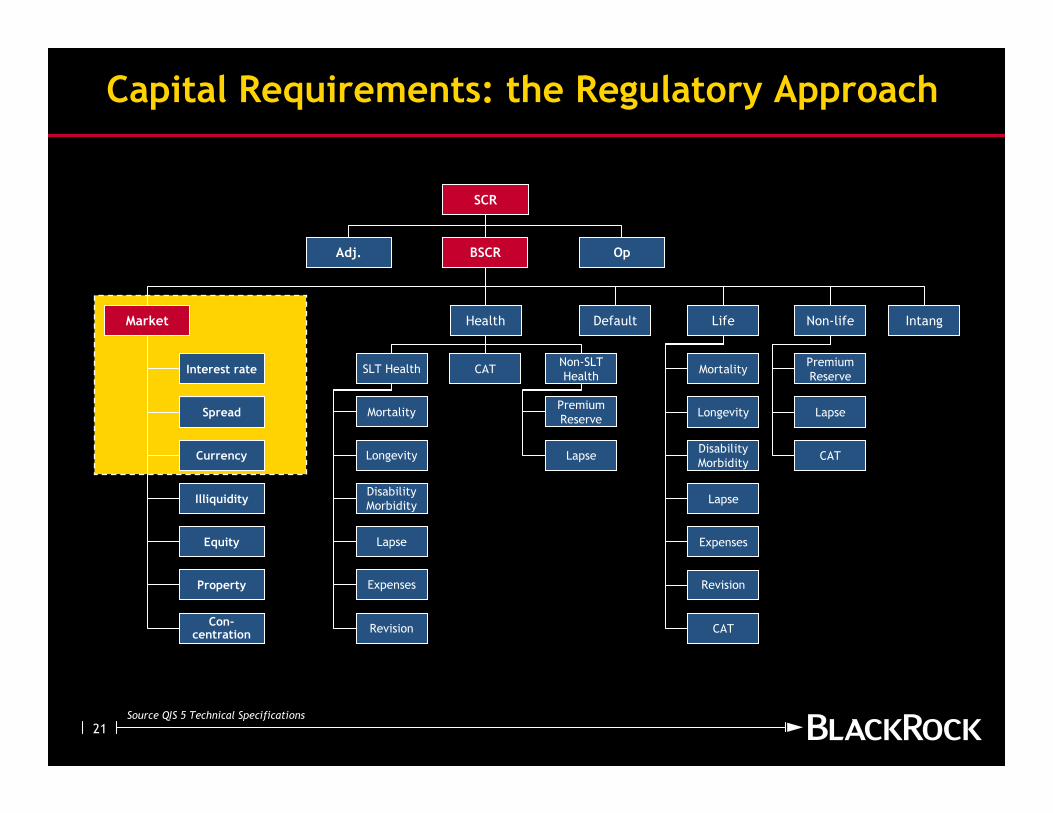

Capital Requirements: the Regulatory Approach

Adj. BSCR Op

SCR

Market Health Default Life Non-life Intang

Interest rate

Equity

Property

Spread

Currency

Con-centration

Illiquidity

SLT Health

Mortality

Longevity

Disability

Morbidity

Lapse

Expenses

Revision

CATNon-SLT

Health

Premium

Reserve

Lapse

Mortality

Longevity

Disability

Morbidity

Lapse

Expenses

Revision

CAT

Premium

Reserve

Lapse

CAT

Source QIS 5 Technical Specifications

22

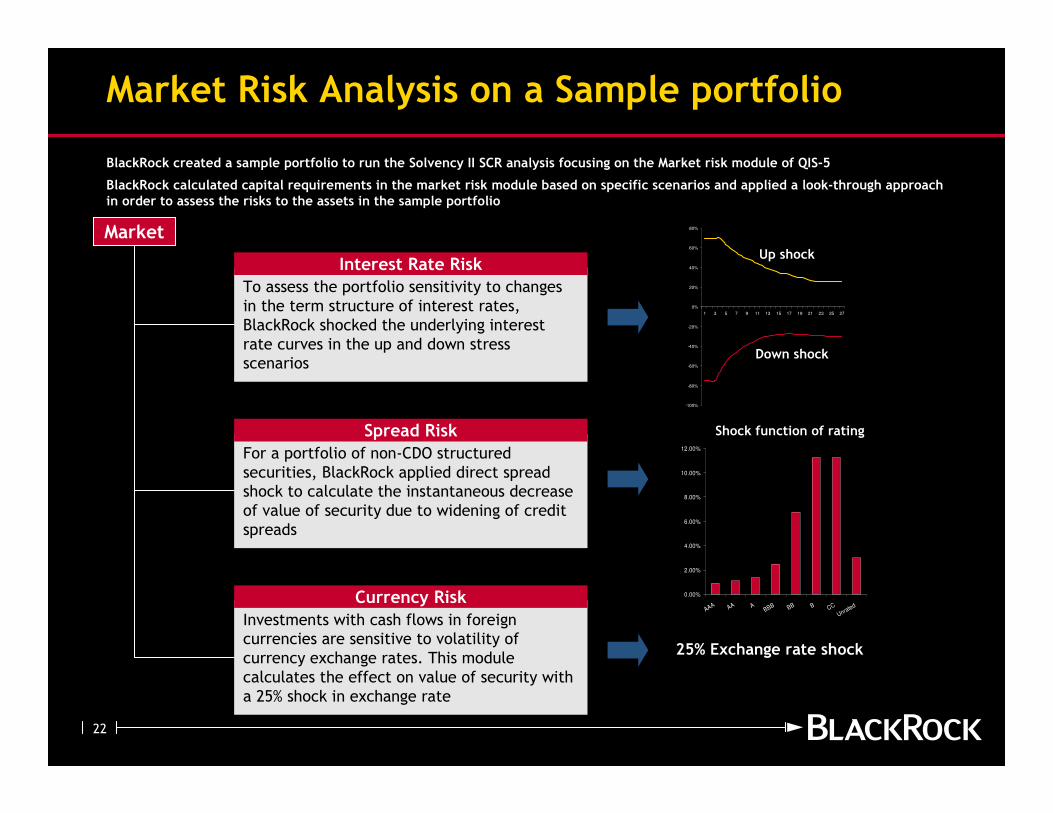

Market Risk Analysis on a Sample portfolio

BlackRock created a sample portfolio to run the Solvency II SCR analysis focusing on the Market risk module of QIS-5

BlackRock calculated capital requirements in the market risk module based on specific scenarios and applied a look-through approach in order to assess the risks to the assets in the sample portfolio

MarketUp shock

Down shock

For a portfolio of non-CDO structured

securities, BlackRock applied direct spread

shock to calculate the instantaneous decrease

of value of security due to widening of credit

spreads

Spread Risk

Investments with cash flows in foreign

currencies are sensitive to volatility of

currency exchange rates. This module

calculates the effect on value of security with

a 25% shock in exchange rate

Currency Risk

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

1 3 5 7 9 11 13 15 17 19 21 23 25 27

To assess the portfolio sensitivity to changes

in the term structure of interest rates,

BlackRock shocked the underlying interest

rate curves in the up and down stress

scenarios

Interest Rate Risk

Shock function of rating

25% Exchange rate shock

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

AAA AA ABBB BB B CC

Unrated

23

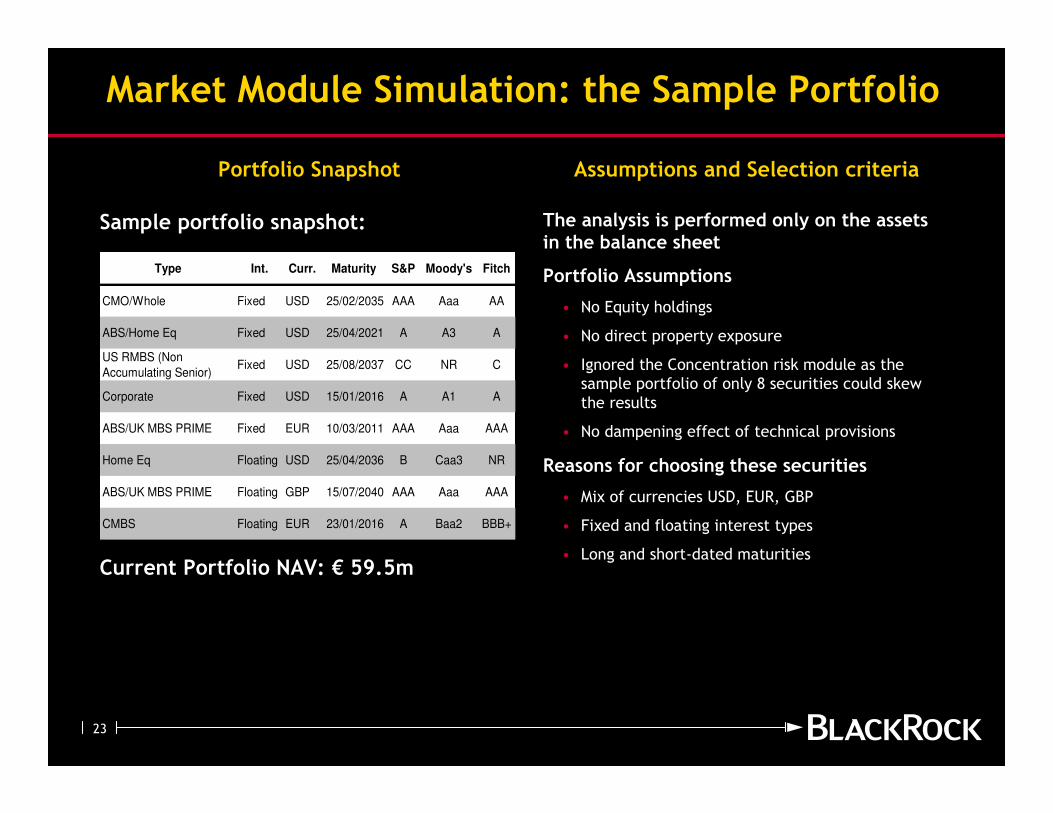

Market Module Simulation: the Sample Portfolio

Assumptions and Selection criteriaPortfolio Snapshot

Sample portfolio snapshot:

Current Portfolio NAV: € 59.5m

The analysis is performed only on the assets in the balance sheet

Portfolio Assumptions

• No Equity holdings

• No direct property exposure

• Ignored the Concentration risk module as the

sample portfolio of only 8 securities could skew

the results

• No dampening effect of technical provisions

Reasons for choosing these securities

• Mix of currencies USD, EUR, GBP

• Fixed and floating interest types

• Long and short-dated maturities

Type Int. Curr. Maturity S&P Moody's Fitch

CMO/Whole Fixed USD 25/02/2035 AAA Aaa AA

ABS/Home Eq Fixed USD 25/04/2021 A A3 A

US RMBS (Non

Accumulating Senior)Fixed USD 25/08/2037 CC NR C

Corporate Fixed USD 15/01/2016 A A1 A

ABS/UK MBS PRIME Fixed EUR 10/03/2011 AAA Aaa AAA

Home Eq Floating USD 25/04/2036 B Caa3 NR

ABS/UK MBS PRIME Floating GBP 15/07/2040 AAA Aaa AAA

CMBS Floating EUR 23/01/2016 A Baa2 BBB+

24

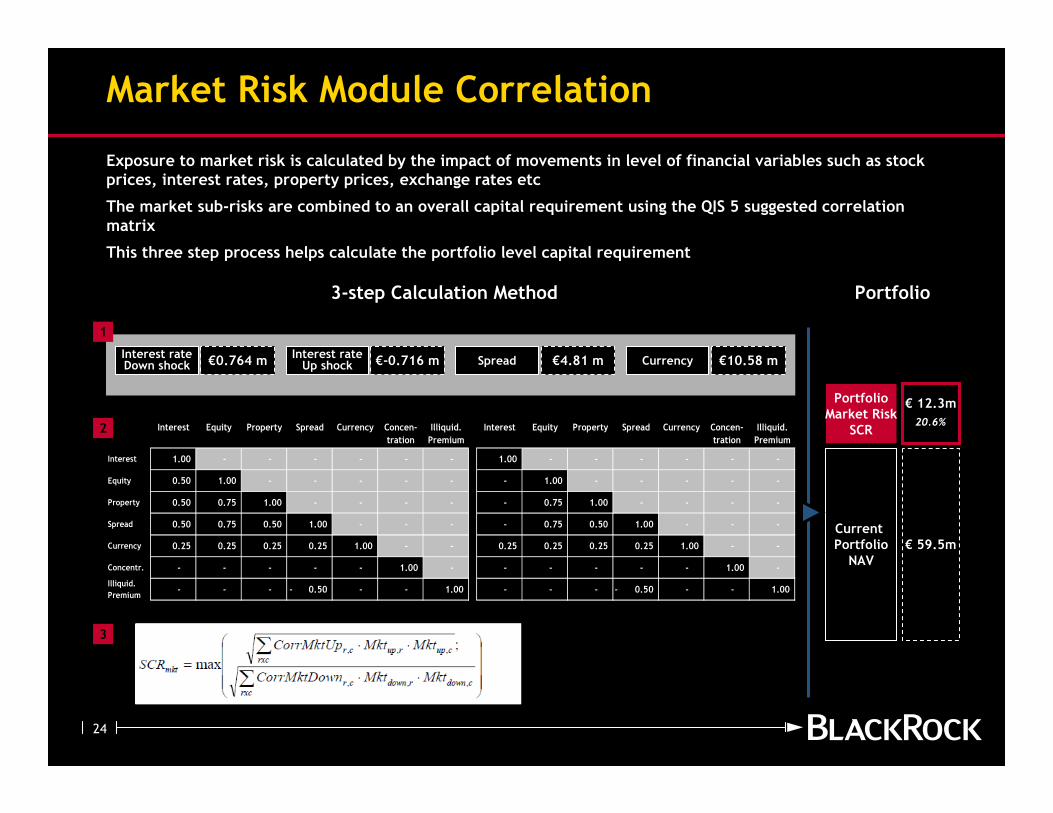

Market Risk Module Correlation

Exposure to market risk is calculated by the impact of movements in level of financial variables such as stock prices, interest rates, property prices, exchange rates etc

The market sub-risks are combined to an overall capital requirement using the QIS 5 suggested correlation matrix

This three step process helps calculate the portfolio level capital requirement

Interest rateDown shock €0.764 m Spread €4.81 m Currency €10.58 m

Interest rateUp shock €-0.716 m

1

3-step Calculation Method

3

Portfolio

€ 12.3m

20.6%

€ 59.5m

PortfolioMarket Risk

SCR

Current PortfolioNAV

2 Interest Equity Property Spread Currency Concen-

tration

Illiquid.

Premium

Interest Equity Property Spread Currency Concen-

tration

Illiquid.

Premium

Interest 1.00 - - - - - - 1.00 - - - - - -

Equity 0.50 1.00 - - - - - - 1.00 - - - - -

Property 0.50 0.75 1.00 - - - - - 0.75 1.00 - - - -

Spread 0.50 0.75 0.50 1.00 - - - - 0.75 0.50 1.00 - - -

Currency 0.25 0.25 0.25 0.25 1.00 - - 0.25 0.25 0.25 0.25 1.00 - -

Concentr. - - - - - 1.00 - - - - - - 1.00 -

Illiquid.

Premium- - - 0.50- - - 1.00 - - - 0.50- - - 1.00

25

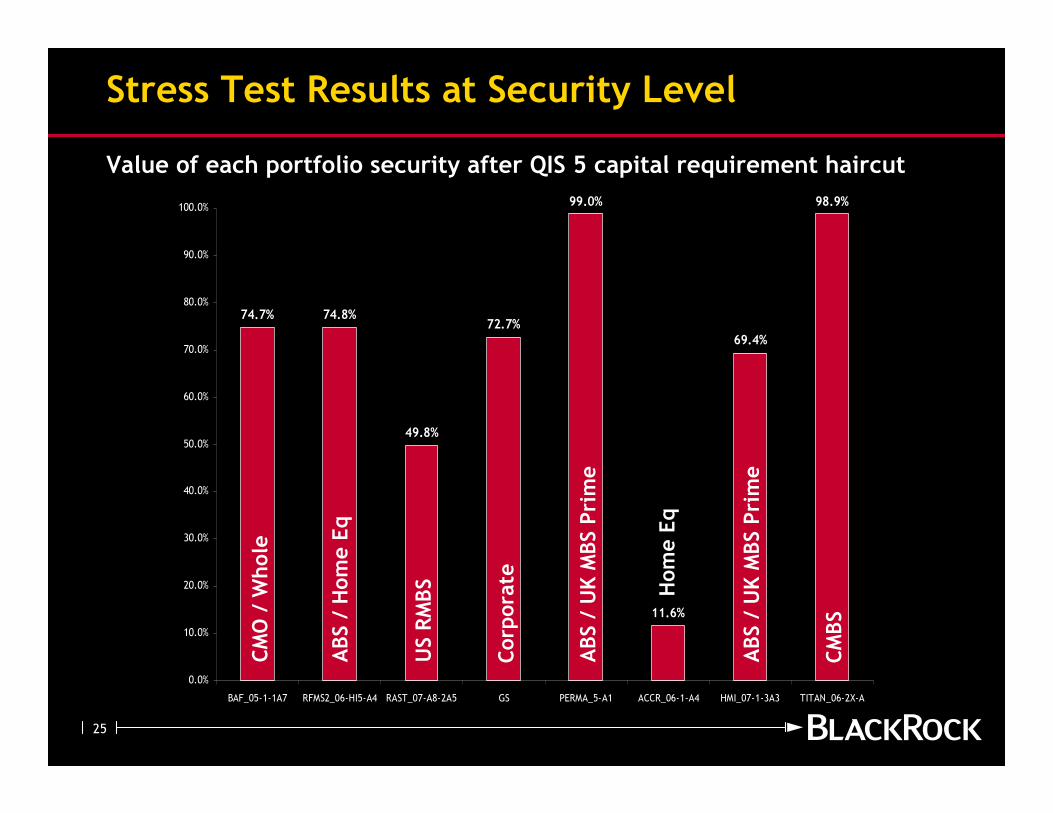

Stress Test Results at Security Level

Value of each portfolio security after QIS 5 capital requirement haircut

98.9%

69.4%

11.6%

99.0%

72.7%

49.8%

74.8%74.7%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

BAF_05-1-1A7 RFMS2_06-HI5-A4 RAST_07-A8-2A5 GS PERMA_5-A1 ACCR_06-1-A4 HMI_07-1-3A3 TITAN_06-2X-A

CMO / Whole

ABS / Home Eq

US RMBS

Corporate

ABS / UK MBS Prime

Home Eq

ABS / UK MBS Prime

CMBS

26

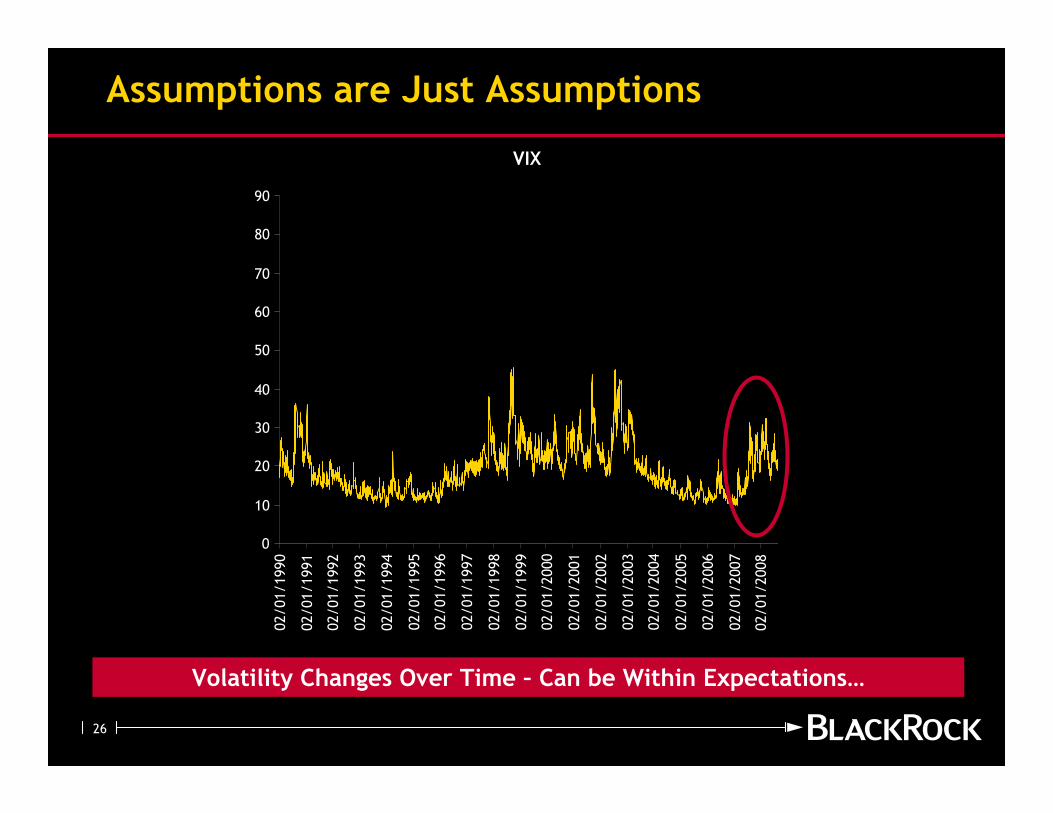

Assumptions are Just Assumptions

Volatility Changes Over Time – Can be Within Expectations…

VIX

0

10

20

30

40

50

60

70

80

90

02/01/1990

02/01/1991

02/01/1992

02/01/1993

02/01/1994

02/01/1995

02/01/1996

02/01/1997

02/01/1998

02/01/1999

02/01/2000

02/01/2001

02/01/2002

02/01/2003

02/01/2004

02/01/2005

02/01/2006

02/01/2007

02/01/2008

02/01/2009

02/01/2010

27

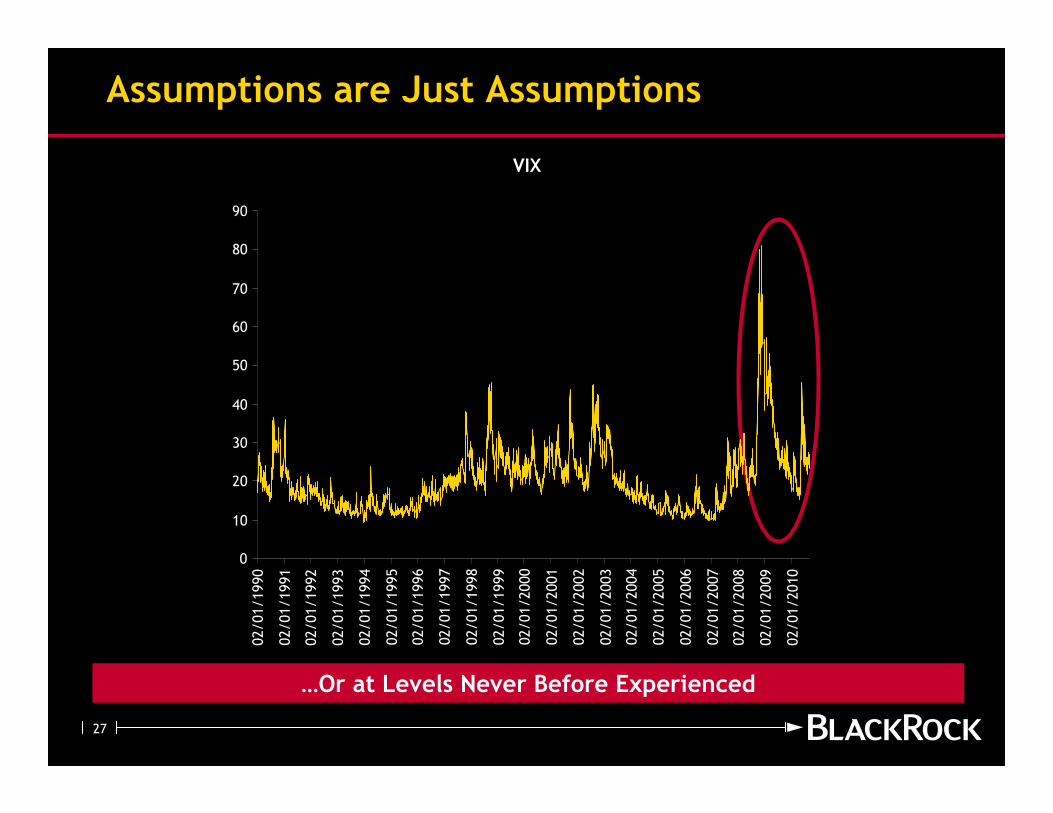

Assumptions are Just Assumptions

…Or at Levels Never Before Experienced

VIX

0

10

20

30

40

50

60

70

80

90

02/01/1990

02/01/1991

02/01/1992

02/01/1993

02/01/1994

02/01/1995

02/01/1996

02/01/1997

02/01/1998

02/01/1999

02/01/2000

02/01/2001

02/01/2002

02/01/2003

02/01/2004

02/01/2005

02/01/2006

02/01/2007

02/01/2008

02/01/2009

02/01/2010

28

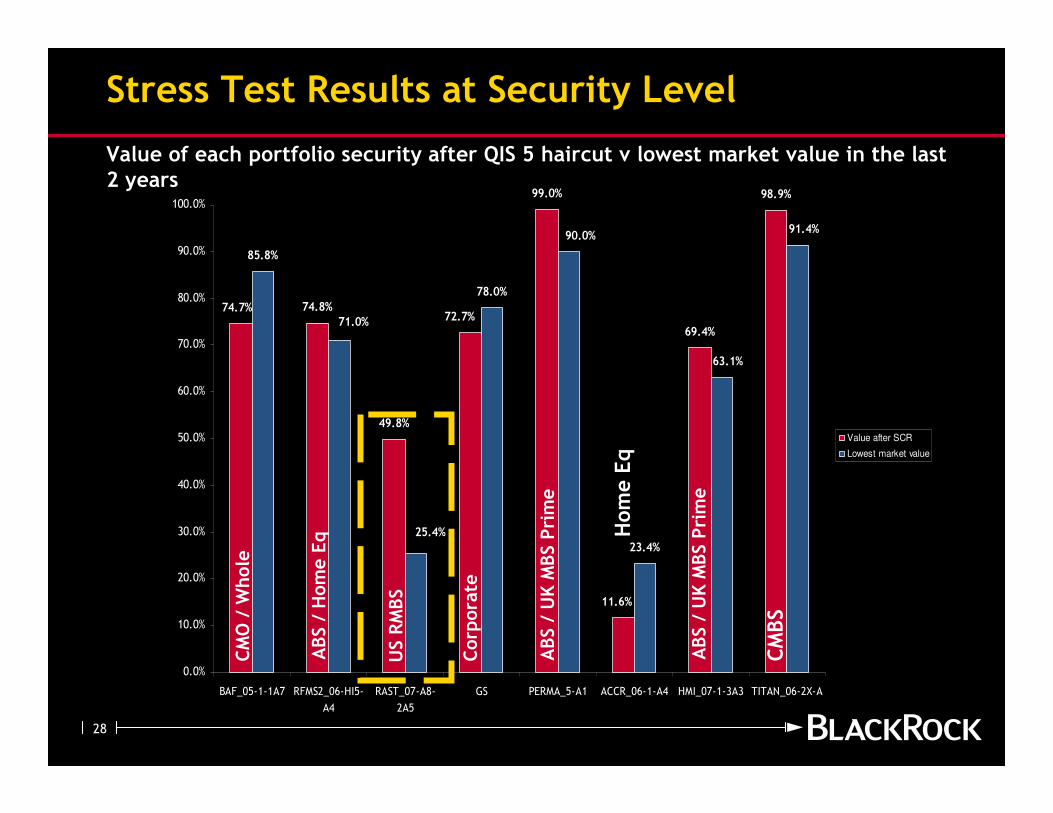

74.8%

49.8%

99.0%

69.4%

98.9%

85.8%

78.0%

23.4%

74.7%72.7%

11.6%

71.0%

25.4%

90.0%

63.1%

91.4%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

BAF_05-1-1A7 RFMS2_06-HI5-

A4

RAST_07-A8-

2A5

GS PERMA_5-A1 ACCR_06-1-A4 HMI_07-1-3A3 TITAN_06-2X-A

Value after SCR

Lowest market value

Stress Test Results at Security Level

Value of each portfolio security after QIS 5 haircut v lowest market value in the last 2 years

CMO / Whole

ABS / Home Eq

Corporate

ABS / UK MBS Prime

Home Eq

ABS / UK MBS Prime

US RMBS

CMBS

29

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

BAF_05-1-

1A7

RFMS2_06-

HI5-A4

RAST_07-A8-

2A5

GS PERMA_5-A1 ACCR_06-1-

A4

HMI_07-1-3A3 TITAN_06-2X-

A

Value after SCR

Lowest market value

Intrinsic value (base)

Intrinsic value (stress)

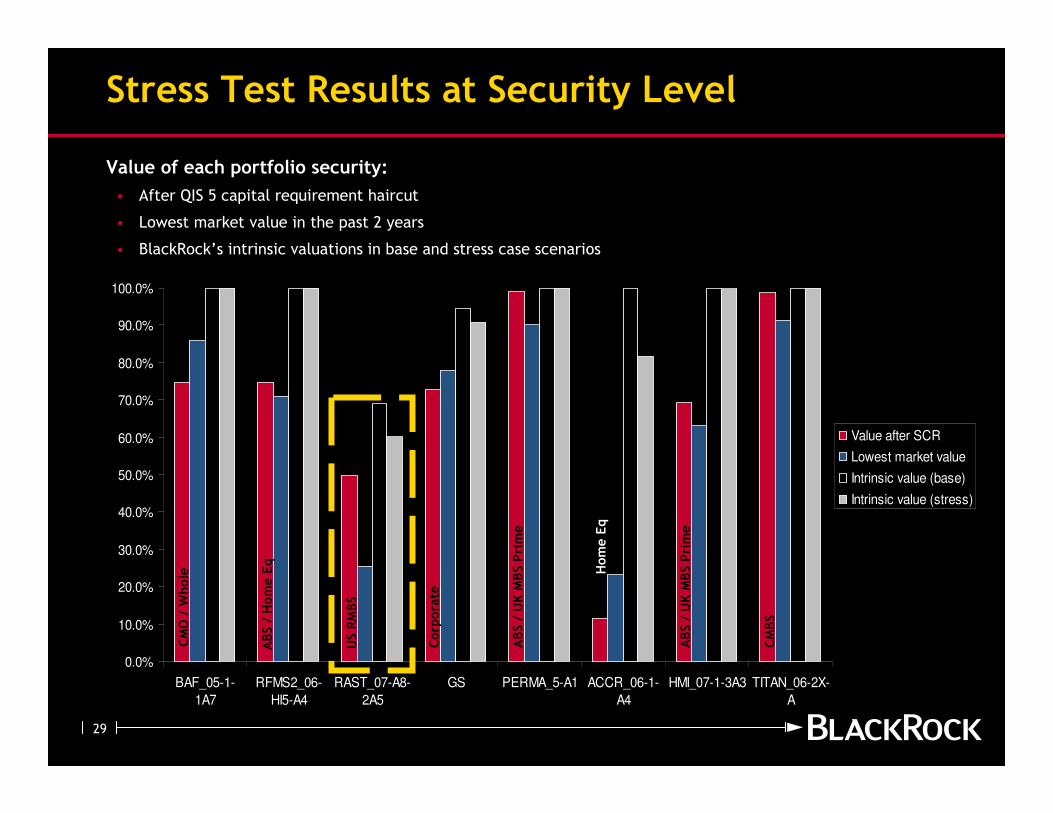

Stress Test Results at Security Level

Value of each portfolio security:

• After QIS 5 capital requirement haircut

• Lowest market value in the past 2 years

• BlackRock’s intrinsic valuations in base and stress case scenarios

CMO / Whole

ABS / Home Eq

Corporate

ABS / UK MBS Prime

Home Eq

ABS / UK MBS Prime

US RMBS

CMBS

30

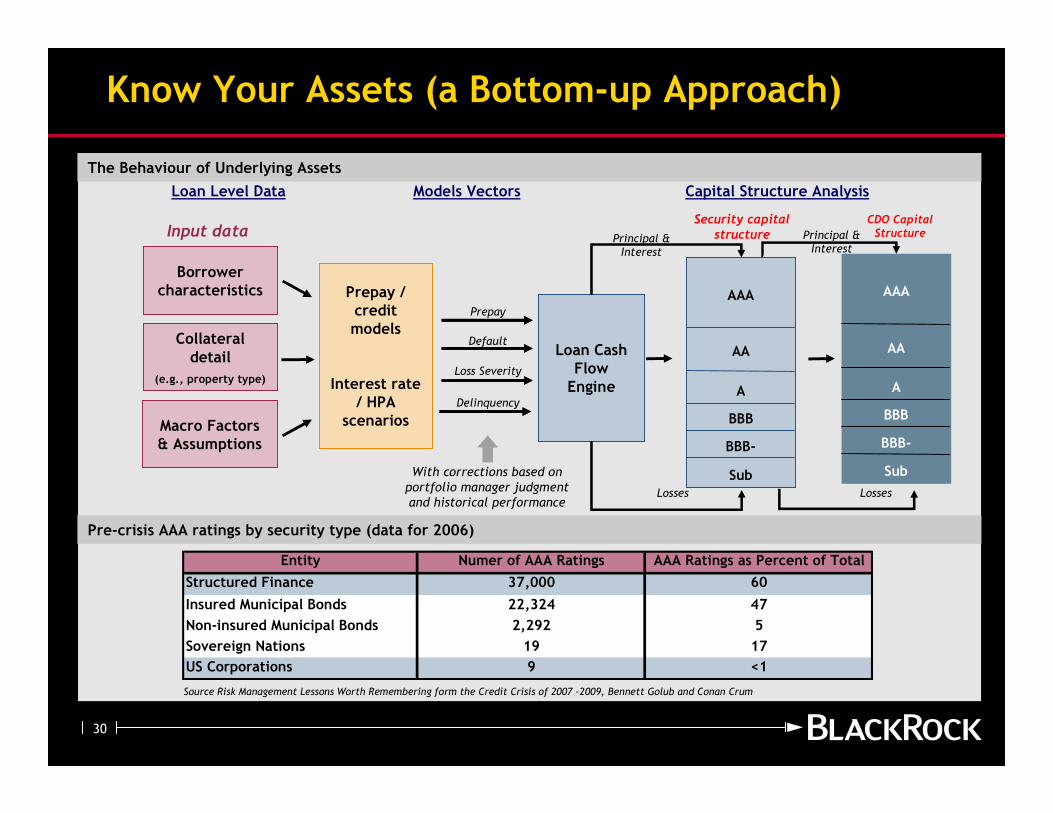

Know Your Assets (a Bottom-up Approach)

Loan Level Data Capital Structure AnalysisModels Vectors

Loan Cash Flow Engine

Prepay / credit models

Interest rate / HPA

scenarios

Prepay

Default

Loss Severity

Delinquency

Collateral detail

(e.g., property type)

Macro Factors & Assumptions

Losses

AAA

BBB

AA

A

Sub

BBB-

Principal & Interest

Security capitalstructureInput data

With corrections based on portfolio manager judgment and historical performance

Borrower characteristics

Principal & Interest

AAA

BBB

AA

A

Sub

BBB-

Losses

CDO Capital Structure

The Behaviour of Underlying Assets

Pre-crisis AAA ratings by security type (data for 2006)

Entity Numer of AAA Ratings AAA Ratings as Percent of Total

Structured Finance 37,000 60

Insured Municipal Bonds 22,324 47

Non-insured Municipal Bonds 2,292 5

Sovereign Nations 19 17

US Corporations 9 <1

Source Risk Management Lessons Worth Remembering form the Credit Crisis of 2007 -2009, Bennett Golub and Conan Crum

31

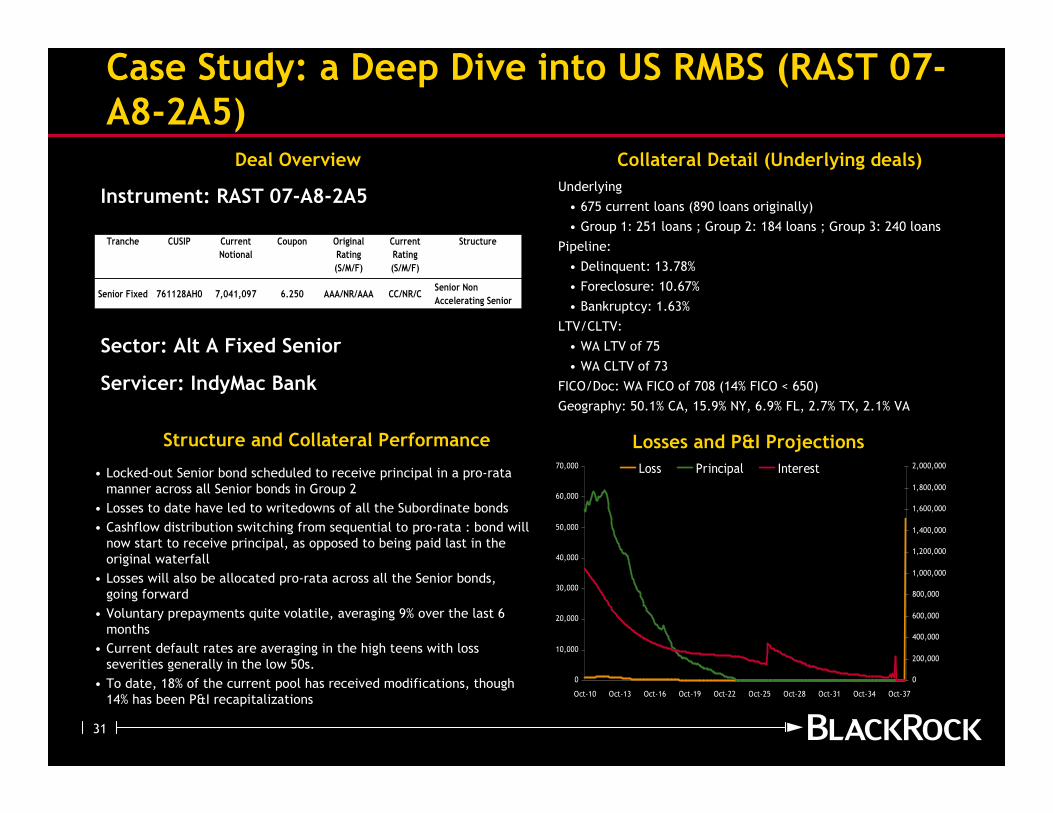

Case Study: a Deep Dive into US RMBS (RAST 07-A8-2A5)

Deal Overview

Underlying

• 675 current loans (890 loans originally)

• Group 1: 251 loans ; Group 2: 184 loans ; Group 3: 240 loans

Pipeline:

• Delinquent: 13.78%

• Foreclosure: 10.67%

• Bankruptcy: 1.63%

LTV/CLTV:

• WA LTV of 75

• WA CLTV of 73

FICO/Doc: WA FICO of 708 (14% FICO < 650)

Geography: 50.1% CA, 15.9% NY, 6.9% FL, 2.7% TX, 2.1% VA

• Locked-out Senior bond scheduled to receive principal in a pro-rata

manner across all Senior bonds in Group 2

• Losses to date have led to writedowns of all the Subordinate bonds

• Cashflow distribution switching from sequential to pro-rata : bond will

now start to receive principal, as opposed to being paid last in the

original waterfall

• Losses will also be allocated pro-rata across all the Senior bonds,

going forward

• Voluntary prepayments quite volatile, averaging 9% over the last 6

months

• Current default rates are averaging in the high teens with loss

severities generally in the low 50s.

• To date, 18% of the current pool has received modifications, though

14% has been P&I recapitalizations

Instrument: RAST 07-A8-2A5

Sector: Alt A Fixed Senior

Servicer: IndyMac Bank

Structure and Collateral Performance Losses and P&I Projections

Collateral Detail (Underlying deals)

Tranche CUSIP Current

Notional

Coupon Original

Rating

(S/M/F)

Current

Rating

(S/M/F)

Structure

Senior Fixed 761128AH0 7,041,097 6.250 AAA/NR/AAA CC/NR/CSenior Non

Accelerating Senior

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Oct-10 Oct-13 Oct-16 Oct-19 Oct-22 Oct-25 Oct-28 Oct-31 Oct-34 Oct-37

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000Loss Principal Interest

32

Agenda

I. BlackRock Overview

II. Solvency II v Market Reality

III.Conclusions

33

Market Risk Management Now and Beyond Solvency II

• Risk management must be part of an institution’s governance & culture

• Recognise limitations of regulatory compliance and models

• Solvency II still a moving target

— What will final regulations be and who will be subject to them?

• Don’t let the market determine your level of risk

• Given target returns, only assume desired types and levels of risk

• Know your assets:

— “get your hands dirty”

— invest in your information platform

• The basic principles of risk management remain relatively constant

• Risk management does not mean risk avoidance

Be Humble In Terms Of What You Know

34

The following notes should be read in conjunction with the attached document:

1. Issued by BlackRock Investment Management (UK) Limited, authorised and regulated by the Financial Services Authority. Registered

office: 33 King William Street, London, EC4R 9AS. Tel: 020 7743 3000. Registered in England No. 2020394. For your protection

telephone calls are usually recorded. BlackRock is a trading name of BlackRock Investment Management (UK) Limited.

2. Past performance is not a guide to future performance and should not be the sole factor of consideration when selecting a product.

All financial investments involve an element of risk. Therefore, the value of your investment and the income from it will vary and

your initial investment amount cannot be guaranteed. Changes in the rates of exchange between currencies may cause the value of

investments to go up and down. Fluctuation may be particularly marked in the case of a higher volatility fund and the value of an

investment may fall suddenly and substantially. Levels and basis of taxation may change from time to time.

3. Mandates we manage may be exposed to finance sector companies, as a service provider or as counterparty for financial contracts.

In recent months, liquidity in the financial markets has become severely restricted, causing a number of firms to withdrawn from the

market, or in some extreme cases, becoming insolvent. This may have an adverse affect on the mandates we manage.

4. Any research in this document has been procured and may have been acted on by BlackRock for its own purpose. The results of such

research are being made available only incidentally. The views expressed do not constitute investment or any other advice and are

subject to change. They do not necessarily reflect the views of any company in the BlackRock Group or any part thereof and no

assurances are made as to their accuracy.

5. This document is for information purposes only and does not constitute an offer or invitation to anyone to invest in any BlackRock

funds and has not been prepared in connection with any such offer.

6. This material is for distribution to Professional Clients (as defined by the FSA Rules) and should not be relied upon by any other

persons.

7. Subject to the express requirements of any client-specific investment management agreement or provisions relating to the

management of a fund, we will not provide notice of any changes to our personnel, structure, policies, process, objectives or,

without limitation, any other matter contained in this document.

8. No part of this material may be reproduced, stored in retrieval system or transmitted in any form or by any means, electronic,

mechanical, recording or otherwise, without the prior written consent of BlackRock.

UNLESS OTHERWISE SPECIFIED, ALL INFORMATION CONTAINED IN THIS DOCUMENT IS CURRENT AS AT 1 September 2010.

35