solvency ii breakfast briefing 10 november 2015 - deloitte us · solvency ii breakfast briefing 10...

TRANSCRIPT

Solvency II Breakfast Briefing10 November 2015

Leading business advisersSolvency II Breakfast Briefing

Glenn Gillard - PartnerOpening Remarks

Solvency II Breakfast Briefing2

Tax in

Solvency II

Nathan Powell

Tax Director

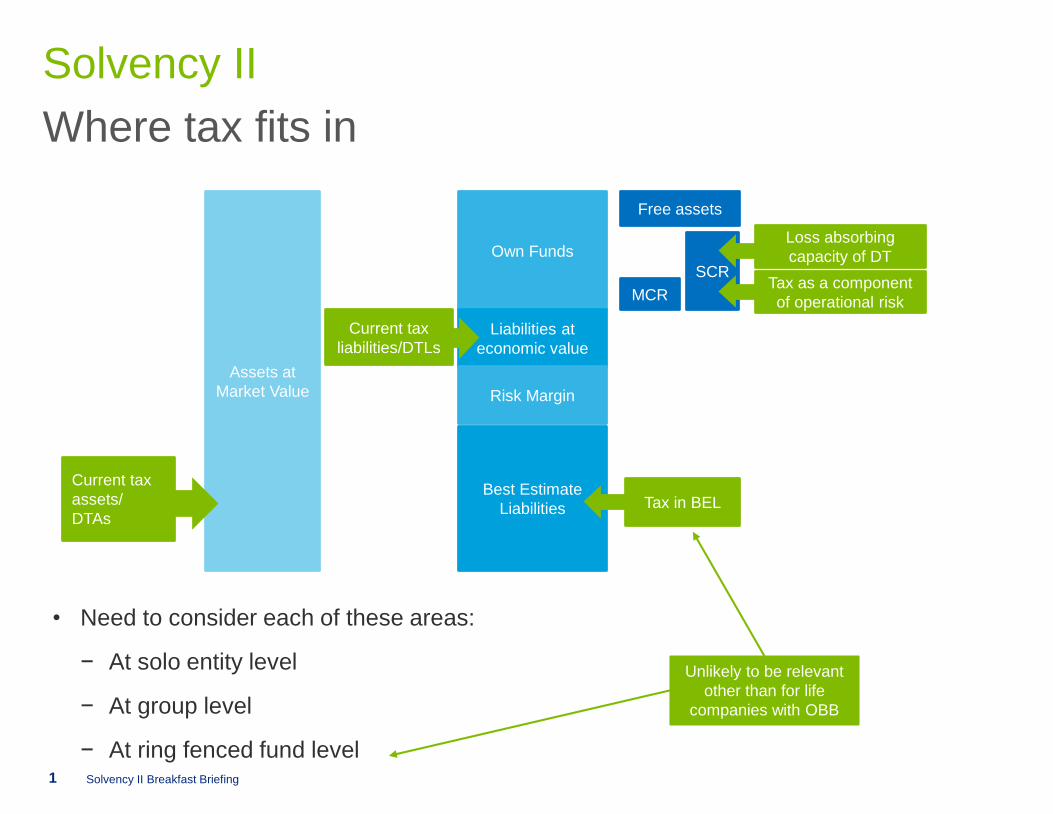

Solvency II

• Need to consider each of these areas:

− At solo entity level

− At group level

− At ring fenced fund level

SCR

Assets at

Market Value

Own Funds

Liabilities at

economic value

Risk Margin

Best Estimate

Liabilities

Current tax

assets/

DTAs

Current tax

liabilities/DTLs

MCRTax as a component

of operational risk

Loss absorbing

capacity of DT

Tax in BEL

Unlikely to be relevant

other than for life

companies with OBB

Where tax fits in

Free assets

Solvency II Breakfast Briefing1

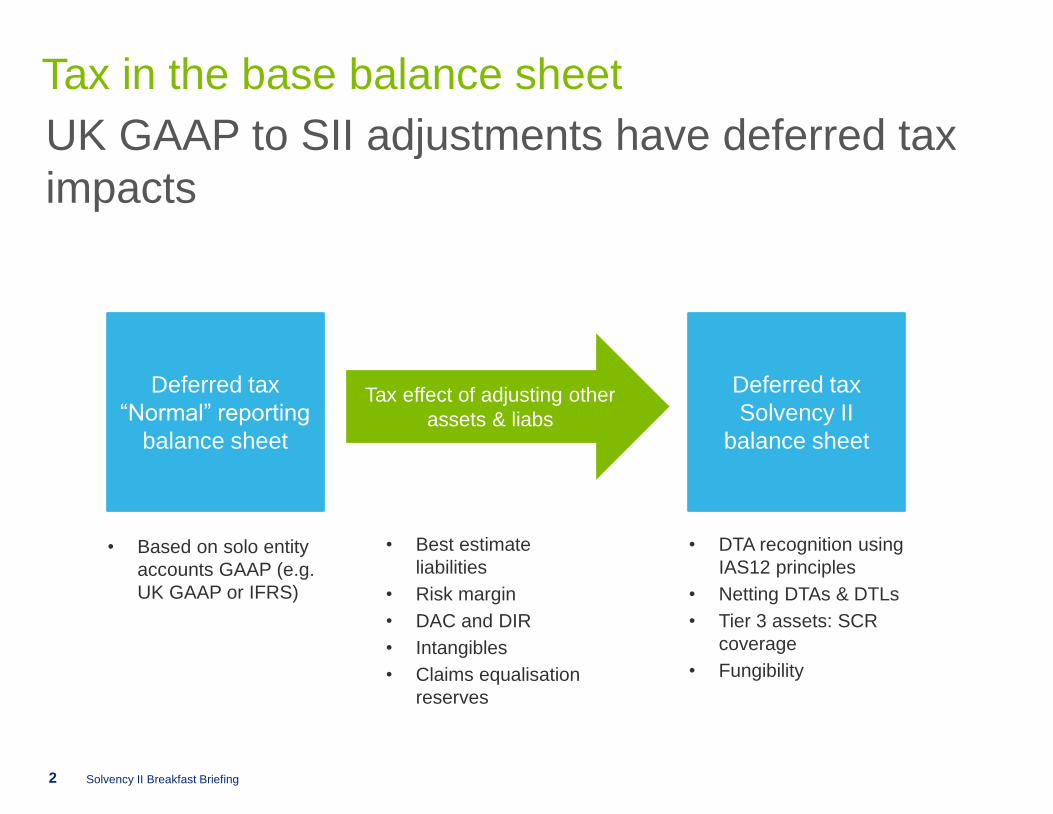

Tax in the base balance sheet

UK GAAP to SII adjustments have deferred tax

impacts

Deferred tax

“Normal” reporting

balance sheet

Deferred tax

Solvency II

balance sheet

Tax effect of adjusting other

assets & liabs

• DTA recognition using

IAS12 principles

• Netting DTAs & DTLs

• Tier 3 assets: SCR

coverage

• Fungibility

• Best estimate

liabilities

• Risk margin

• DAC and DIR

• Intangibles

• Claims equalisation

reserves

• Based on solo entity

accounts GAAP (e.g.

UK GAAP or IFRS)

Solvency II Breakfast Briefing2

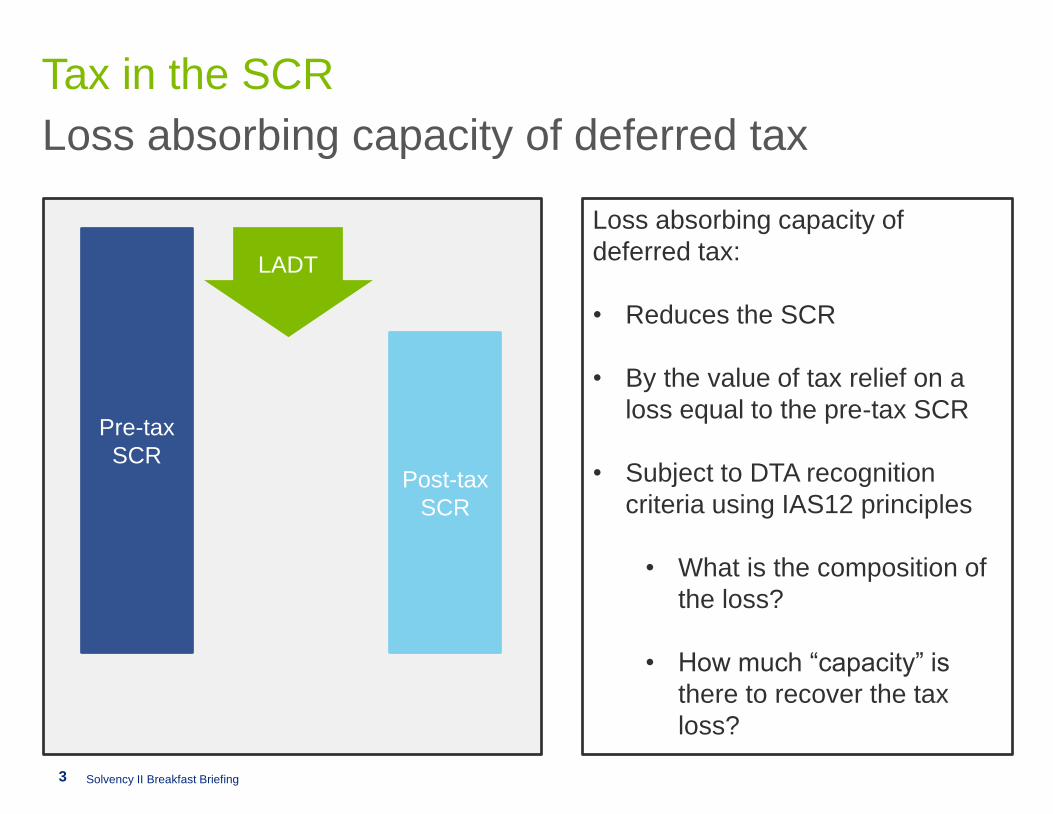

Tax in the SCR

Loss absorbing capacity of deferred tax

Pre-tax

SCRPost-tax

SCR

LADT

Loss absorbing capacity of

deferred tax:

• Reduces the SCR

• By the value of tax relief on a

loss equal to the pre-tax SCR

• Subject to DTA recognition

criteria using IAS12 principles

• What is the composition of

the loss?

• How much “capacity” is

there to recover the tax

loss?

Solvency II Breakfast Briefing3

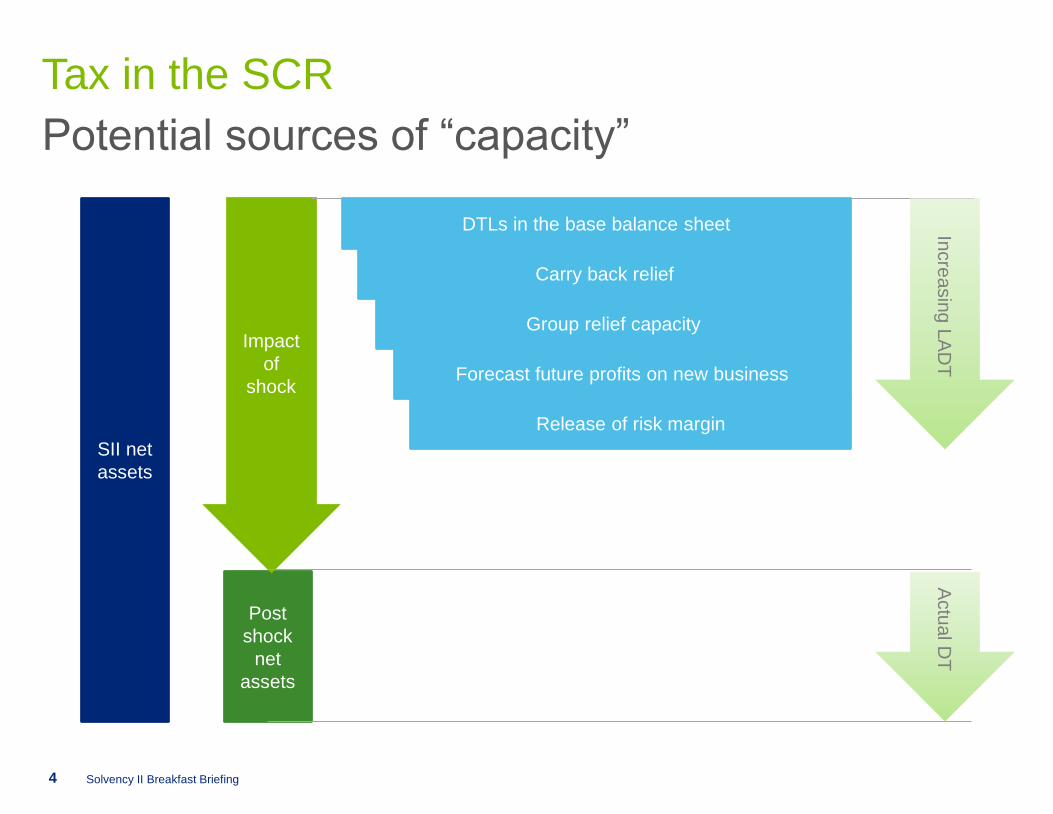

Tax in the SCR

SII net

assets

Post

shock

net

assets

Impact

of

shock

DTLs in the base balance sheet

Carry back relief

Group relief capacity

Forecast future profits on new business

Release of risk margin

Incre

asin

g L

AD

TA

ctu

al D

T

Potential sources of “capacity”

Solvency II Breakfast Briefing4

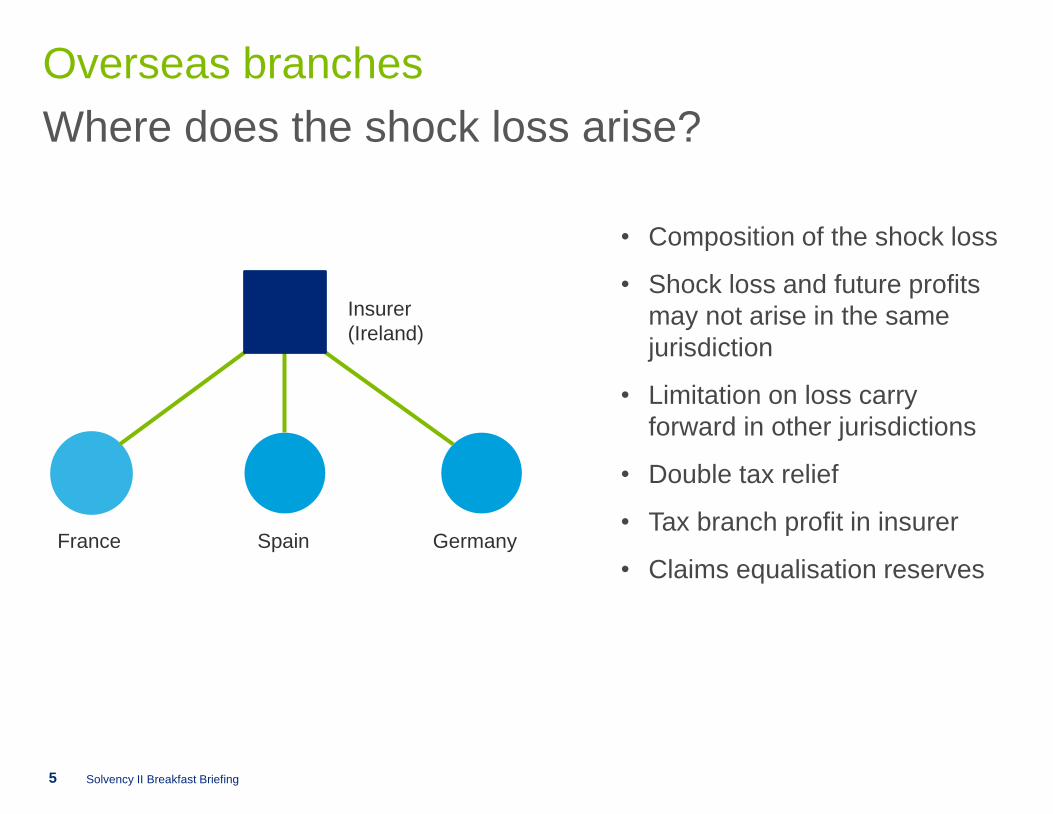

Overseas branches

Where does the shock loss arise?

Insurer

(Ireland)

France Spain Germany

• Composition of the shock loss

• Shock loss and future profits

may not arise in the same

jurisdiction

• Limitation on loss carry

forward in other jurisdictions

• Double tax relief

• Tax branch profit in insurer

• Claims equalisation reserves

Solvency II Breakfast Briefing5

Pillar 3Public

Disclosures

Carol Lynch

Director Audit and Advisory

© 2015 Deloitte Touche Tohmatsu

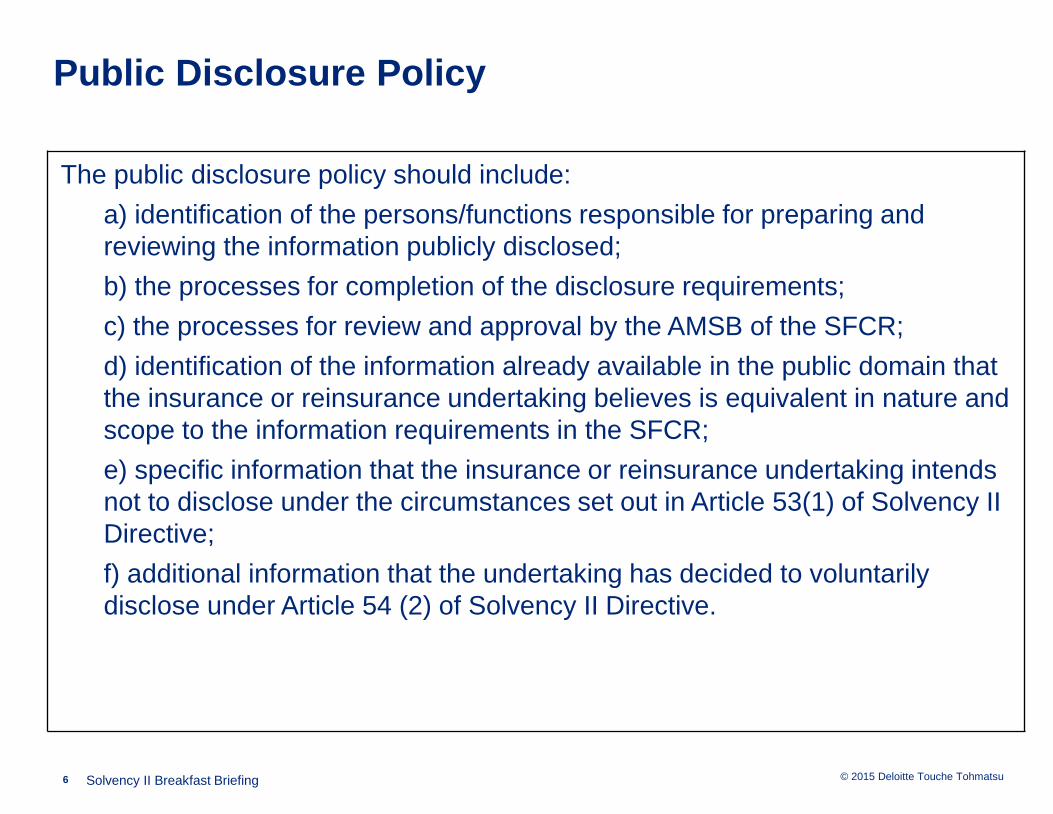

Public Disclosure Policy

The public disclosure policy should include:

a) identification of the persons/functions responsible for preparing and

reviewing the information publicly disclosed;

b) the processes for completion of the disclosure requirements;

c) the processes for review and approval by the AMSB of the SFCR;

d) identification of the information already available in the public domain that

the insurance or reinsurance undertaking believes is equivalent in nature and

scope to the information requirements in the SFCR;

e) specific information that the insurance or reinsurance undertaking intends

not to disclose under the circumstances set out in Article 53(1) of Solvency II

Directive;

f) additional information that the undertaking has decided to voluntarily

disclose under Article 54 (2) of Solvency II Directive.

Solvency II Breakfast Briefing6

© 2015 Deloitte Touche Tohmatsu

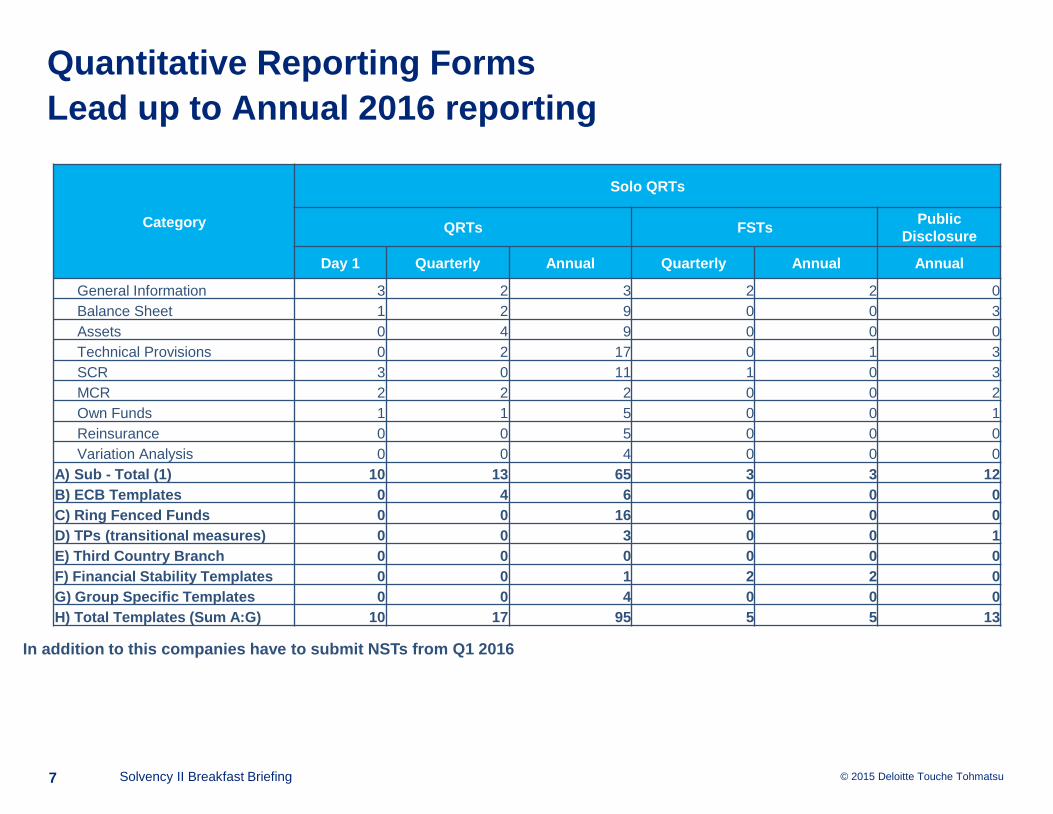

Quantitative Reporting Forms

Lead up to Annual 2016 reporting

Category

Solo QRTs

QRTs FSTsPublic

Disclosure

Day 1 Quarterly Annual Quarterly Annual Annual

General Information 3 2 3 2 2 0

Balance Sheet 1 2 9 0 0 3

Assets 0 4 9 0 0 0

Technical Provisions 0 2 17 0 1 3

SCR 3 0 11 1 0 3

MCR 2 2 2 0 0 2

Own Funds 1 1 5 0 0 1

Reinsurance 0 0 5 0 0 0

Variation Analysis 0 0 4 0 0 0

A) Sub - Total (1) 10 13 65 3 3 12

B) ECB Templates 0 4 6 0 0 0

C) Ring Fenced Funds 0 0 16 0 0 0

D) TPs (transitional measures) 0 0 3 0 0 1

E) Third Country Branch 0 0 0 0 0 0

F) Financial Stability Templates 0 0 1 2 2 0

G) Group Specific Templates 0 0 4 0 0 0

H) Total Templates (Sum A:G) 10 17 95 5 5 13

In addition to this companies have to submit NSTs from Q1 2016

Solvency II Breakfast Briefing7

© 2015 Deloitte Touche Tohmatsu12

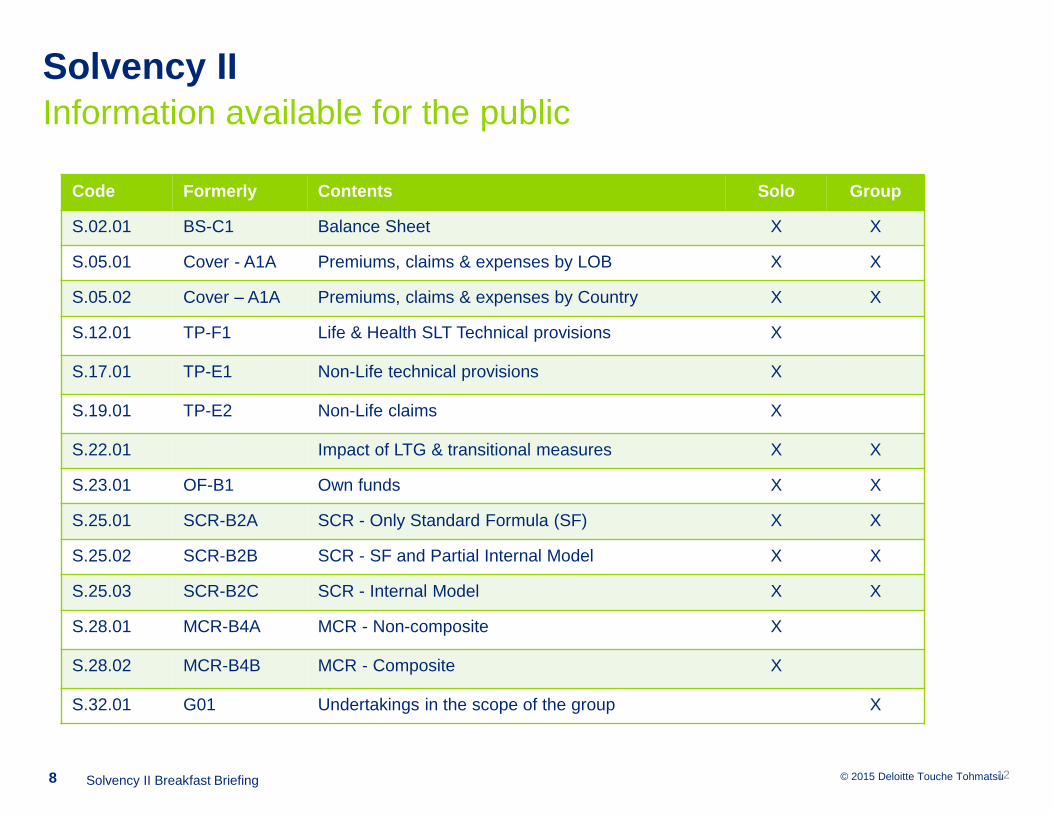

Code Formerly Contents Solo Group

S.02.01 BS-C1 Balance Sheet X X

S.05.01 Cover - A1A Premiums, claims & expenses by LOB X X

S.05.02 Cover – A1A Premiums, claims & expenses by Country X X

S.12.01 TP-F1 Life & Health SLT Technical provisions X

S.17.01 TP-E1 Non-Life technical provisions X

S.19.01 TP-E2 Non-Life claims X

S.22.01 Impact of LTG & transitional measures X X

S.23.01 OF-B1 Own funds X X

S.25.01 SCR-B2A SCR - Only Standard Formula (SF) X X

S.25.02 SCR-B2B SCR - SF and Partial Internal Model X X

S.25.03 SCR-B2C SCR - Internal Model X X

S.28.01 MCR-B4A MCR - Non-composite X

S.28.02 MCR-B4B MCR - Composite X

S.32.01 G01 Undertakings in the scope of the group X

Solvency II

Information available for the public

Solvency II Breakfast Briefing8

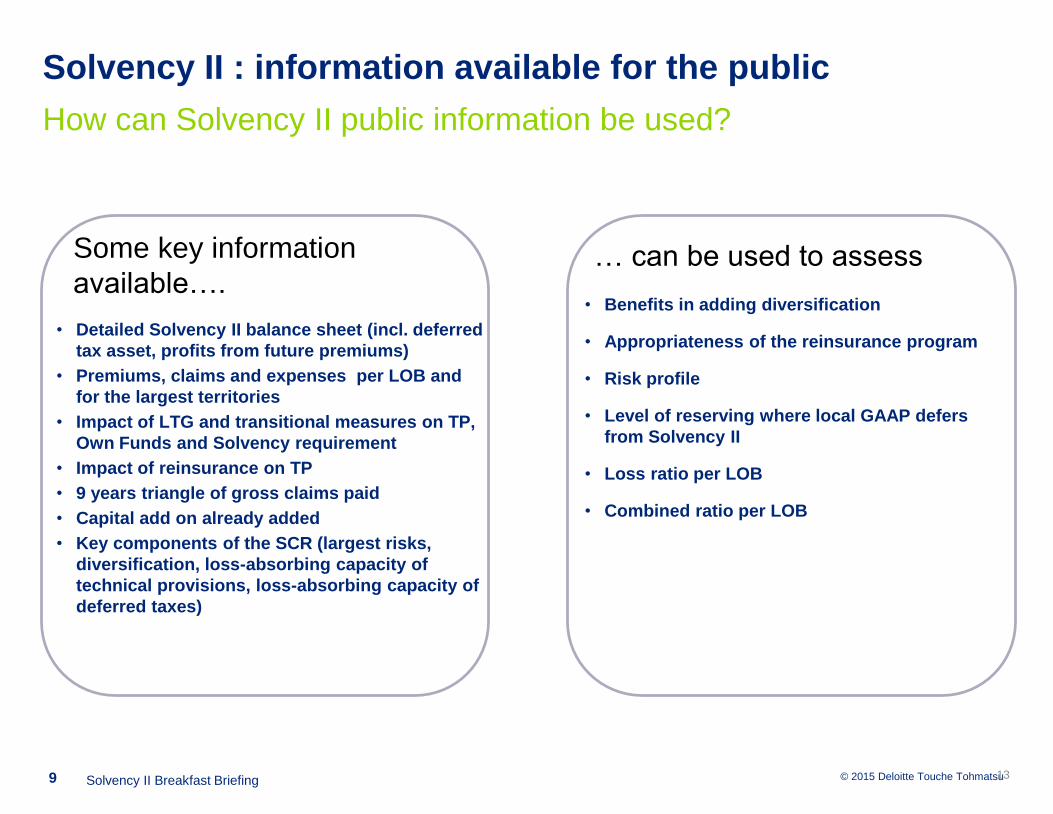

© 2015 Deloitte Touche Tohmatsu

How can Solvency II public information be used?

• Detailed Solvency II balance sheet (incl. deferred

tax asset, profits from future premiums)

• Premiums, claims and expenses per LOB and

for the largest territories

• Impact of LTG and transitional measures on TP,

Own Funds and Solvency requirement

• Impact of reinsurance on TP

• 9 years triangle of gross claims paid

• Capital add on already added

• Key components of the SCR (largest risks,

diversification, loss-absorbing capacity of

technical provisions, loss-absorbing capacity of

deferred taxes)

13

• Benefits in adding diversification

• Appropriateness of the reinsurance program

• Risk profile

• Level of reserving where local GAAP defers

from Solvency II

• Loss ratio per LOB

• Combined ratio per LOB

Some key information

available….… can be used to assess

Solvency II : information available for the public

Solvency II Breakfast Briefing9

© 2015 Deloitte Touche Tohmatsu

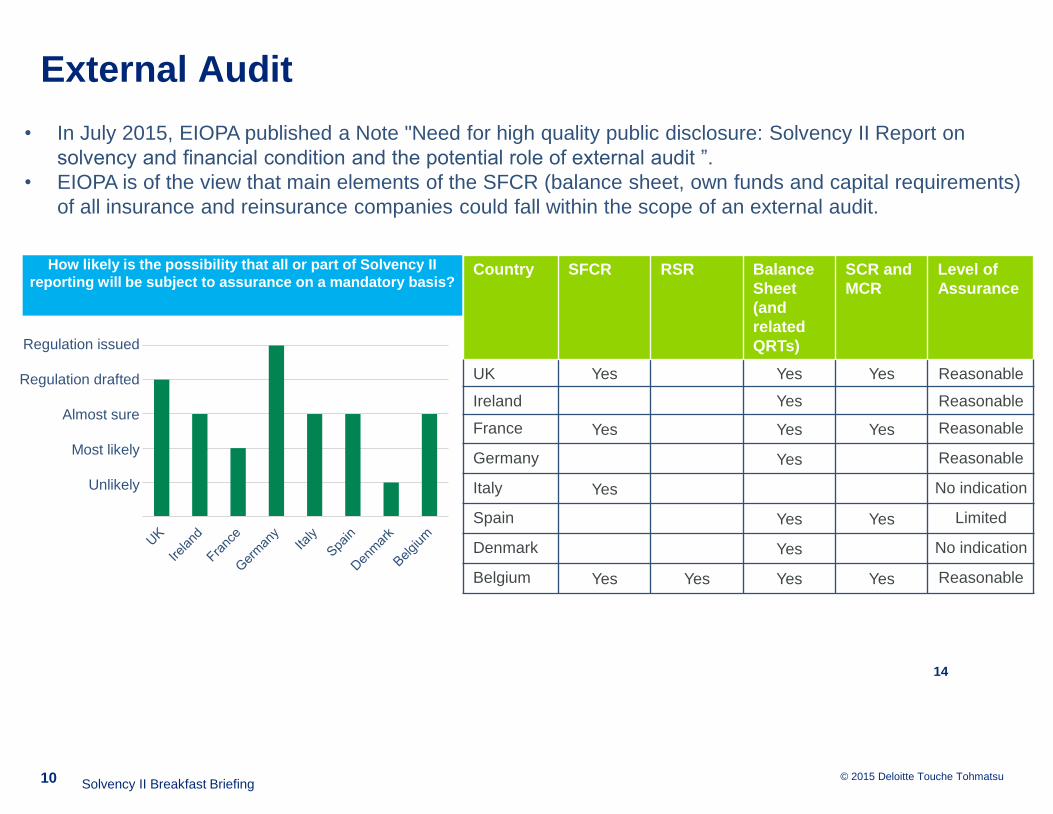

External Audit

14

Regulation issued

Regulation drafted

Almost sure

Most likely

Unlikely

How likely is the possibility that all or part of Solvency II

reporting will be subject to assurance on a mandatory basis?Country SFCR RSR Balance

Sheet

(and

related

QRTs)

SCR and

MCR

Level of

Assurance

UK Yes Yes Yes Reasonable

Ireland Yes Reasonable

France Yes Yes Yes Reasonable

Germany Yes Reasonable

Italy Yes No indication

Spain Yes Yes Limited

Denmark Yes No indication

Belgium Yes Yes Yes Yes Reasonable

• In July 2015, EIOPA published a Note "Need for high quality public disclosure: Solvency II Report on

solvency and financial condition and the potential role of external audit ”.

• EIOPA is of the view that main elements of the SFCR (balance sheet, own funds and capital requirements)

of all insurance and reinsurance companies could fall within the scope of an external audit.

Solvency II Breakfast Briefing10

© 2015 Deloitte & Touche11

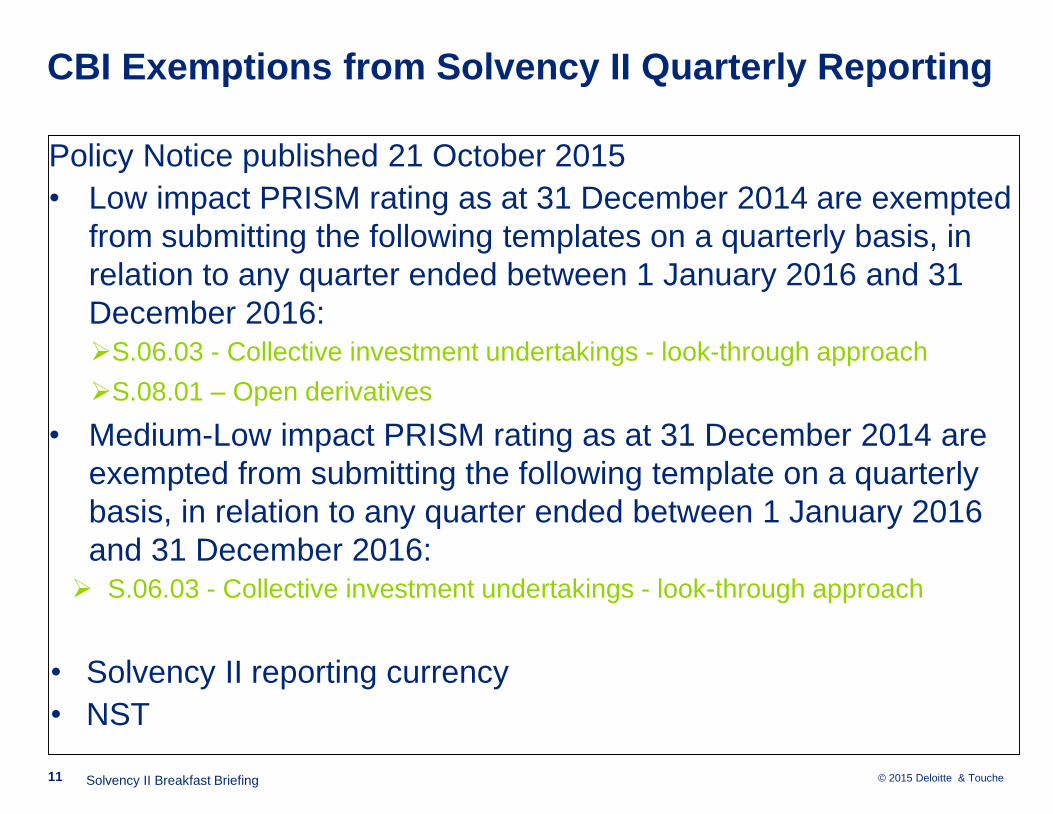

CBI Exemptions from Solvency II Quarterly Reporting

Policy Notice published 21 October 2015

• Low impact PRISM rating as at 31 December 2014 are exempted

from submitting the following templates on a quarterly basis, in

relation to any quarter ended between 1 January 2016 and 31

December 2016: S.06.03 - Collective investment undertakings - look-through approach

S.08.01 – Open derivatives

• Medium-Low impact PRISM rating as at 31 December 2014 are

exempted from submitting the following template on a quarterly

basis, in relation to any quarter ended between 1 January 2016

and 31 December 2016: S.06.03 - Collective investment undertakings - look-through approach

• Solvency II reporting currency

• NST

Solvency II Breakfast Briefing

© 2015 Deloitte Touche Tohmatsu

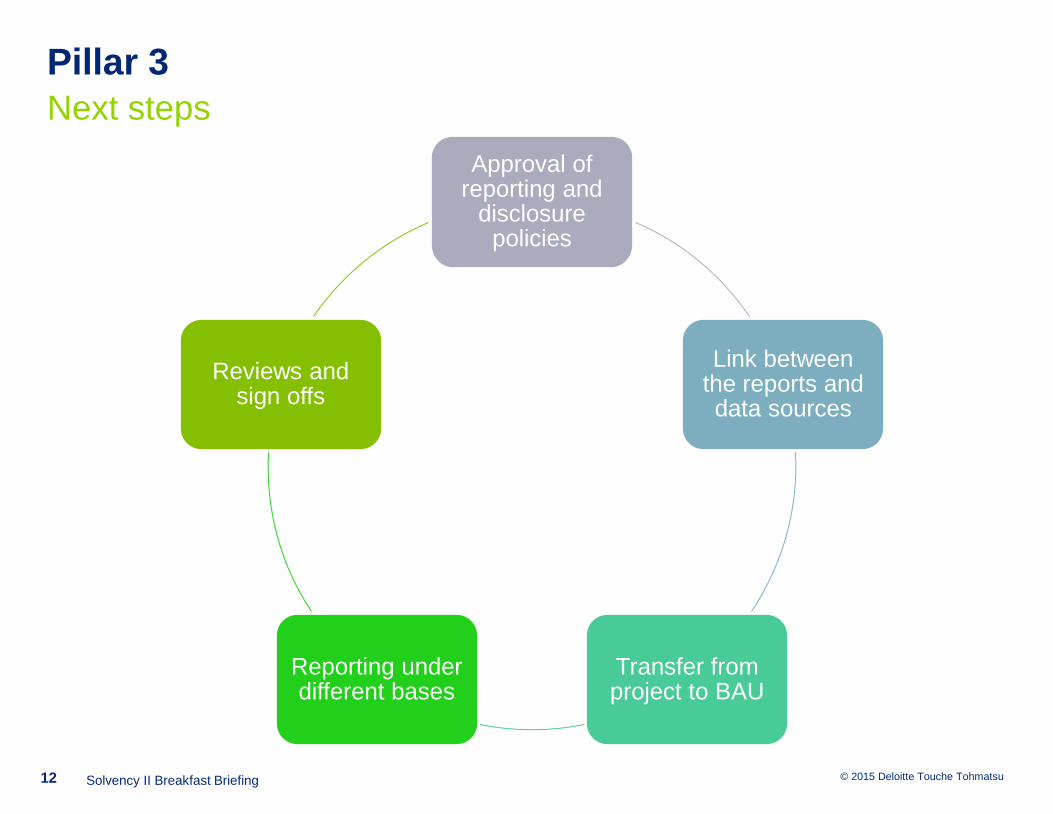

Pillar 3

Next steps

Approval of reporting and

disclosure policies

Link between the reports and data sources

Transfer from project to BAU

Reporting under different bases

Reviews and sign offs

Solvency II Breakfast Briefing12

ORSA/FLAOR

Carmel Niven, Senior Manager

Darren Shaughnessy, Manager

18

New for 2015

CBI Feedback – May 2015

Further Deloitte insights

13

The main sources of the ORSA requirements are:

• Solvency II Directive (Articles 36, 45 and 246)

• Delegated Acts (Articles 262 and 306)

• EIOPA Guidelines on Own Risk and Solvency Assessment

• CBI Guidelines on Preparing for Solvency II – Forward Looking Assessment of

Own Risks

• CBI’s Feedback Statement on the Domestic Actuarial Regime and Related

Governance Requirements under Solvency II (CP92)

The slides which follow provide a summary of our interpretation of the

requirements for ORSA. We recommend that you refer to the Directive,

Delegated Acts, and the relevant guidelines to develop your understanding

of the regulatory requirements.

Understanding and implementing the requirements for

ORSA/FLAORSources of Regulatory Requirements

Solvency II Breakfast Briefing

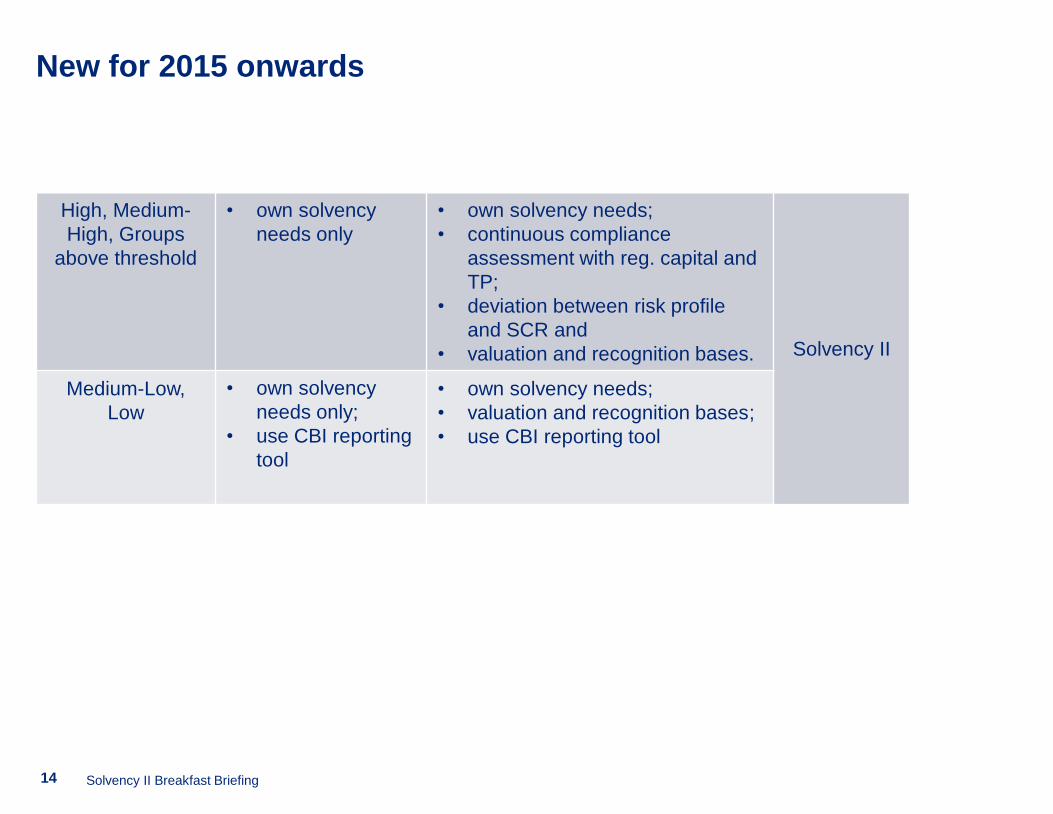

New for 2015 onwardsRequirements at a glance

PRISM Rating 2014 2015 2016

High, Medium-

High, Groups

above threshold

• own solvency

needs only

• own solvency needs;

• continuous compliance

assessment with reg. capital and

TP;

• deviation between risk profile

and SCR and

• valuation and recognition bases. Solvency II

Medium-Low,

Low

• own solvency

needs only;

• use CBI reporting

tool

• own solvency needs;

• valuation and recognition bases;

• use CBI reporting tool

Solvency II Breakfast Briefing14

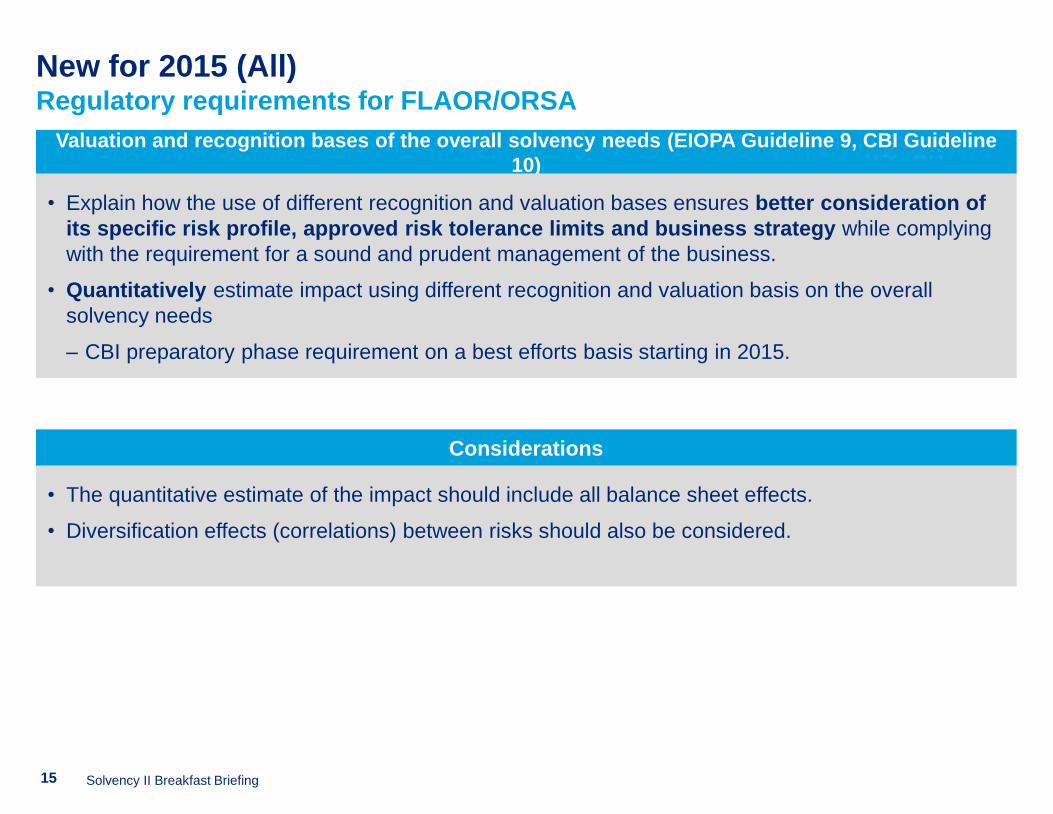

New for 2015 (All)Regulatory requirements for FLAOR/ORSA

Valuation and recognition bases of the overall solvency needs (EIOPA Guideline 9, CBI Guideline

10)

• Explain how the use of different recognition and valuation bases ensures better consideration of

its specific risk profile, approved risk tolerance limits and business strategy while complying

with the requirement for a sound and prudent management of the business.

• Quantitatively estimate impact using different recognition and valuation basis on the overall

solvency needs

‒ CBI preparatory phase requirement on a best efforts basis starting in 2015.

Considerations

• The quantitative estimate of the impact should include all balance sheet effects.

• Diversification effects (correlations) between risks should also be considered.

Solvency II Breakfast Briefing15

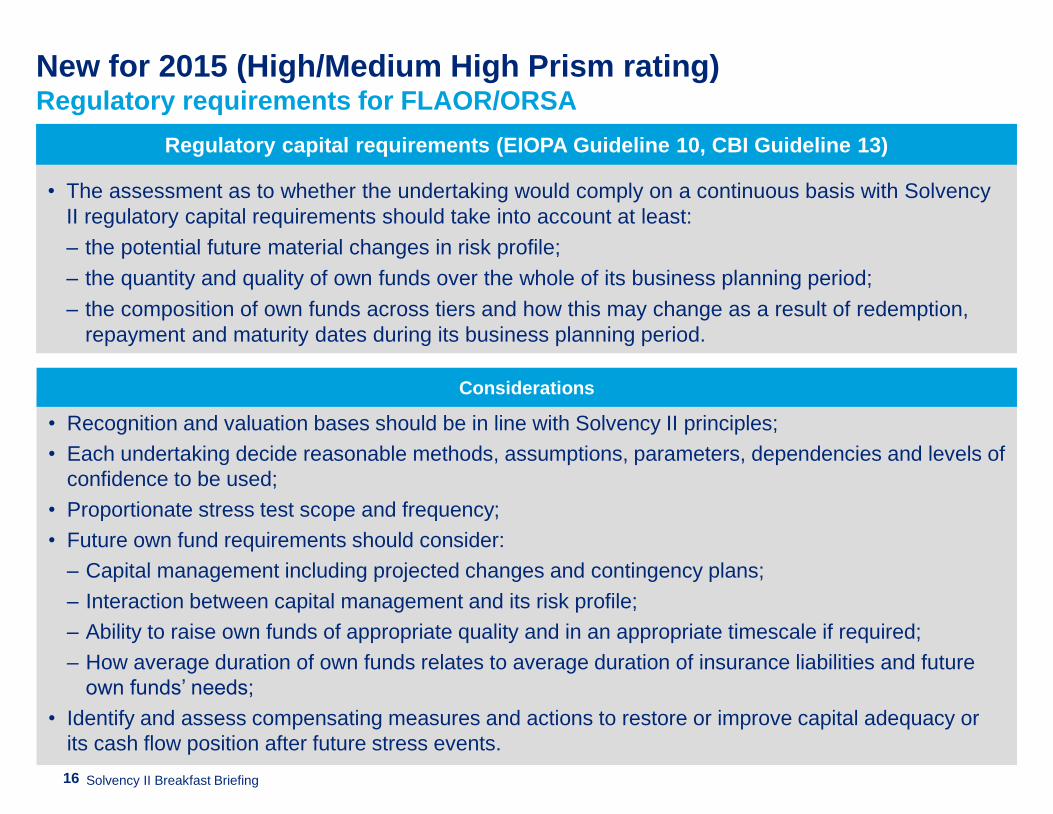

New for 2015 (High/Medium High Prism rating)Regulatory requirements for FLAOR/ORSA

• The assessment as to whether the undertaking would comply on a continuous basis with Solvency

II regulatory capital requirements should take into account at least:

‒ the potential future material changes in risk profile;

‒ the quantity and quality of own funds over the whole of its business planning period;

‒ the composition of own funds across tiers and how this may change as a result of redemption,

repayment and maturity dates during its business planning period.

Regulatory capital requirements (EIOPA Guideline 10, CBI Guideline 13)

• Recognition and valuation bases should be in line with Solvency II principles;

• Each undertaking decide reasonable methods, assumptions, parameters, dependencies and levels of

confidence to be used;

• Proportionate stress test scope and frequency;

• Future own fund requirements should consider:

‒ Capital management including projected changes and contingency plans;

‒ Interaction between capital management and its risk profile;

‒ Ability to raise own funds of appropriate quality and in an appropriate timescale if required;

‒ How average duration of own funds relates to average duration of insurance liabilities and future

own funds’ needs;

• Identify and assess compensating measures and actions to restore or improve capital adequacy or

its cash flow position after future stress events.

Considerations

Solvency II Breakfast Briefing16

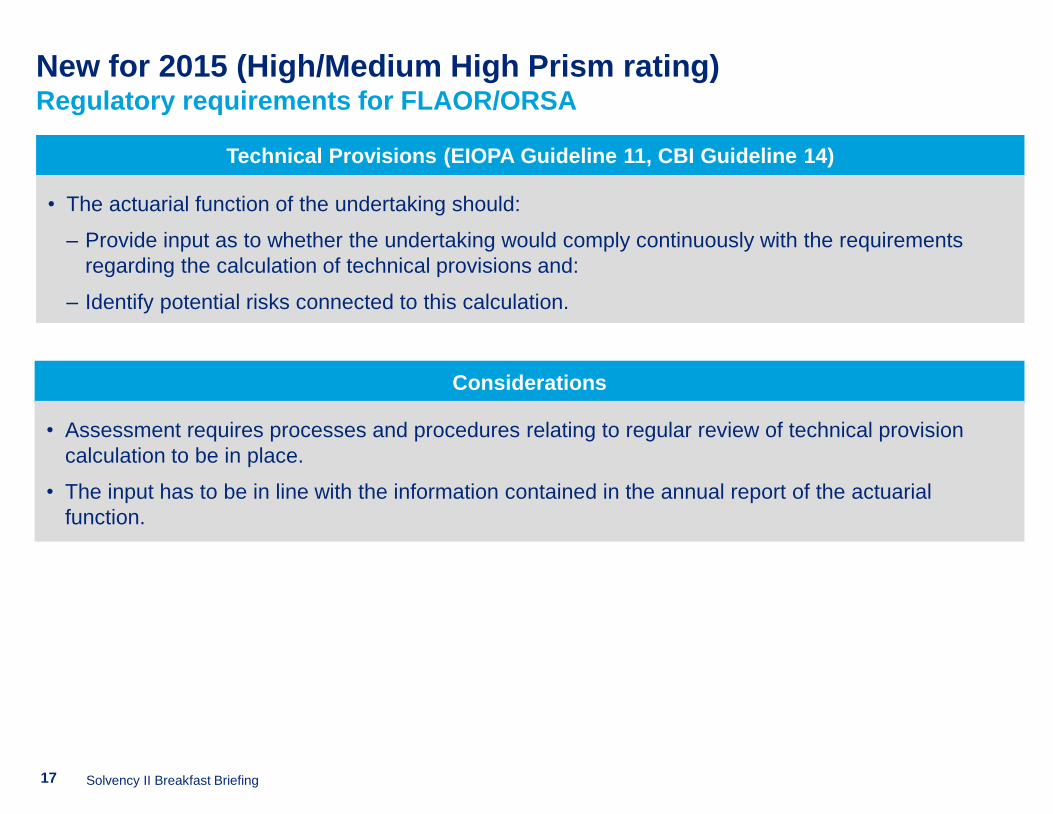

New for 2015 (High/Medium High Prism rating)Regulatory requirements for FLAOR/ORSA

Technical Provisions (EIOPA Guideline 11, CBI Guideline 14)

• The actuarial function of the undertaking should:

‒ Provide input as to whether the undertaking would comply continuously with the requirements

regarding the calculation of technical provisions and:

‒ Identify potential risks connected to this calculation.

Considerations

• Assessment requires processes and procedures relating to regular review of technical provision

calculation to be in place.

• The input has to be in line with the information contained in the annual report of the actuarial

function.

Solvency II Breakfast Briefing17

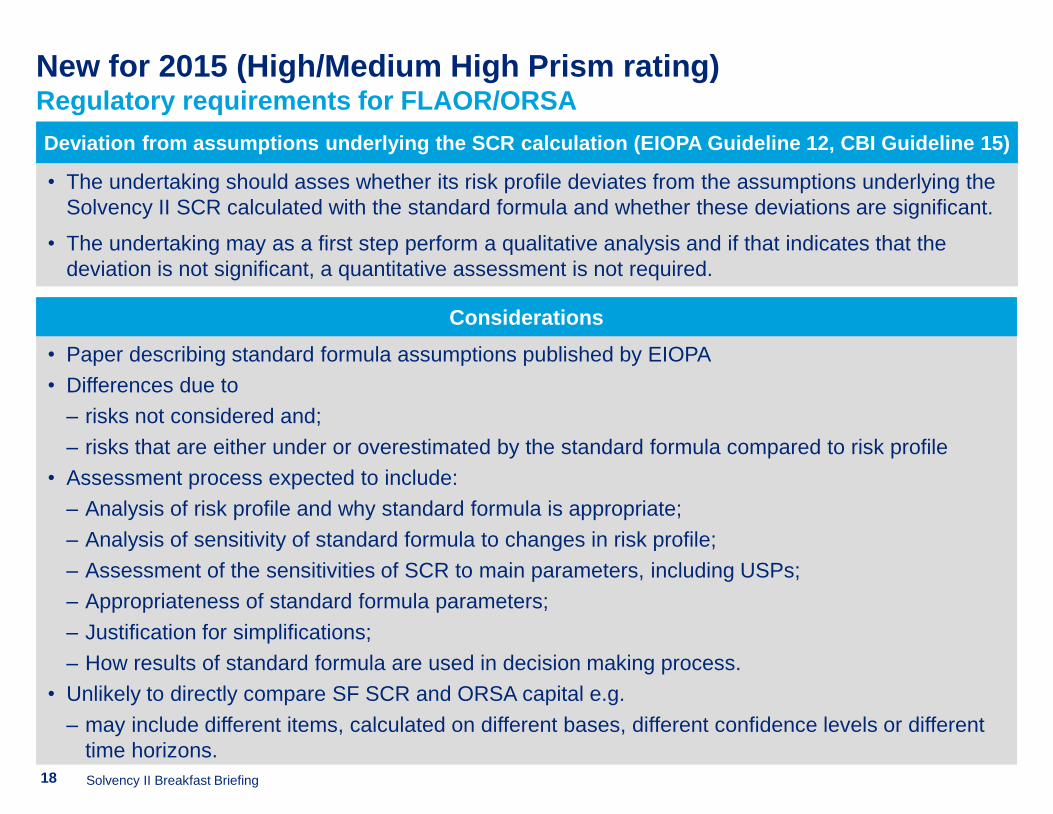

New for 2015 (High/Medium High Prism rating)Regulatory requirements for FLAOR/ORSA

• The undertaking should asses whether its risk profile deviates from the assumptions underlying the

Solvency II SCR calculated with the standard formula and whether these deviations are significant.

• The undertaking may as a first step perform a qualitative analysis and if that indicates that the

deviation is not significant, a quantitative assessment is not required.

Deviation from assumptions underlying the SCR calculation (EIOPA Guideline 12, CBI Guideline 15)

• Paper describing standard formula assumptions published by EIOPA

• Differences due to

‒ risks not considered and;

‒ risks that are either under or overestimated by the standard formula compared to risk profile

• Assessment process expected to include:

‒ Analysis of risk profile and why standard formula is appropriate;

‒ Analysis of sensitivity of standard formula to changes in risk profile;

‒ Assessment of the sensitivities of SCR to main parameters, including USPs;

‒ Appropriateness of standard formula parameters;

‒ Justification for simplifications;

‒ How results of standard formula are used in decision making process.

• Unlikely to directly compare SF SCR and ORSA capital e.g.

‒ may include different items, calculated on different bases, different confidence levels or different

time horizons.

Considerations

Solvency II Breakfast Briefing18

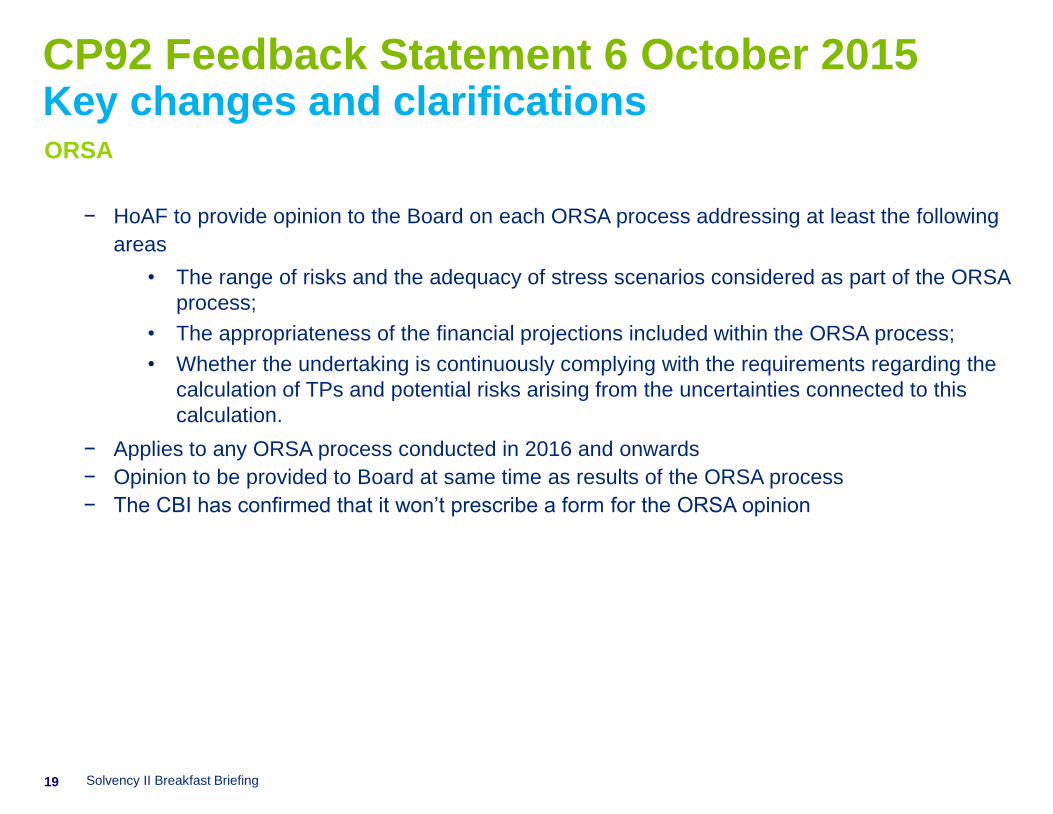

CP92 Feedback Statement 6 October 2015Key changes and clarificationsORSA

− HoAF to provide opinion to the Board on each ORSA process addressing at least the following

areas

• The range of risks and the adequacy of stress scenarios considered as part of the ORSA

process;

• The appropriateness of the financial projections included within the ORSA process;

• Whether the undertaking is continuously complying with the requirements regarding the

calculation of TPs and potential risks arising from the uncertainties connected to this

calculation.

− Applies to any ORSA process conducted in 2016 and onwards

− Opinion to be provided to Board at same time as results of the ORSA process

− The CBI has confirmed that it won’t prescribe a form for the ORSA opinion

19 Solvency II Breakfast Briefing

26

New for 2015

CBI Feedback – May 2015

Further Deloitte insights

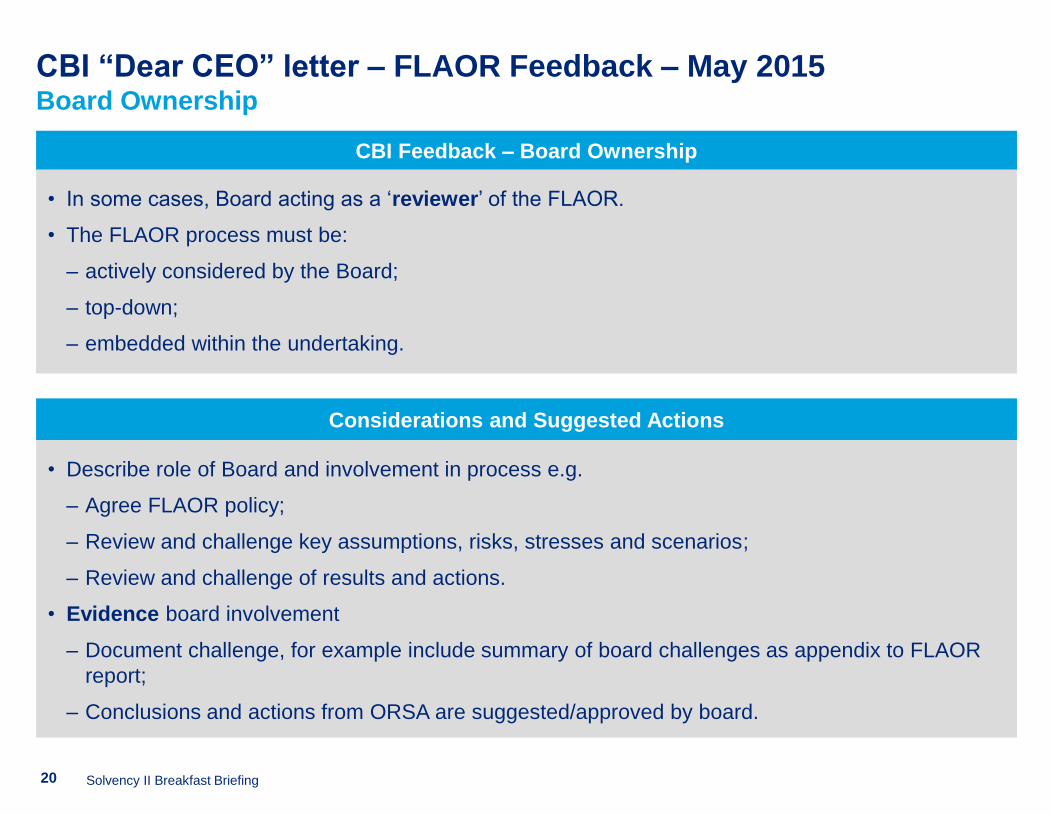

CBI “Dear CEO” letter – FLAOR Feedback – May 2015Board Ownership

CBI Feedback – Board Ownership

• In some cases, Board acting as a ‘reviewer’ of the FLAOR.

• The FLAOR process must be:

‒ actively considered by the Board;

‒ top-down;

‒ embedded within the undertaking.

Considerations and Suggested Actions

• Describe role of Board and involvement in process e.g.

‒ Agree FLAOR policy;

‒ Review and challenge key assumptions, risks, stresses and scenarios;

‒ Review and challenge of results and actions.

• Evidence board involvement

‒ Document challenge, for example include summary of board challenges as appendix to FLAOR

report;

‒ Conclusions and actions from ORSA are suggested/approved by board.

Solvency II Breakfast Briefing20

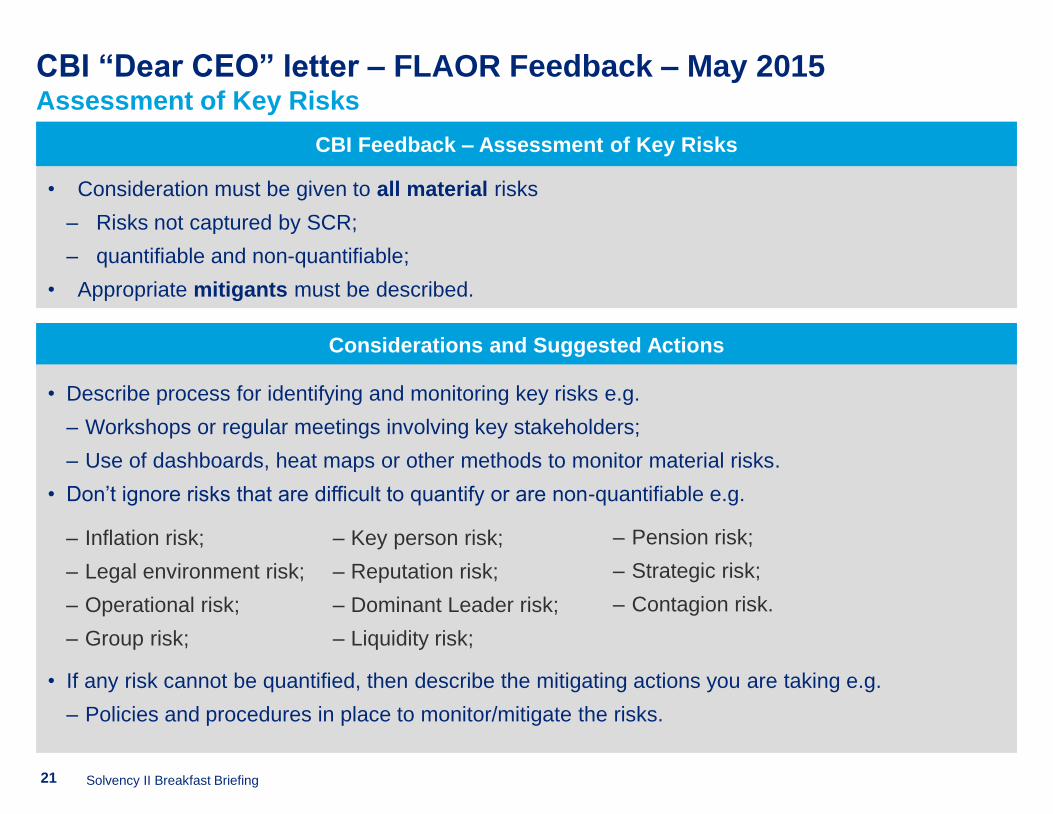

CBI “Dear CEO” letter – FLAOR Feedback – May 2015Assessment of Key Risks

• Consideration must be given to all material risks

‒ Risks not captured by SCR;

‒ quantifiable and non-quantifiable;

• Appropriate mitigants must be described.

CBI Feedback – Assessment of Key Risks

Considerations and Suggested Actions

• Describe process for identifying and monitoring key risks e.g.

‒ Workshops or regular meetings involving key stakeholders;

‒ Use of dashboards, heat maps or other methods to monitor material risks.

• Don’t ignore risks that are difficult to quantify or are non-quantifiable e.g.

• If any risk cannot be quantified, then describe the mitigating actions you are taking e.g.

‒ Policies and procedures in place to monitor/mitigate the risks.

‒ Key person risk;

‒ Reputation risk;

‒ Dominant Leader risk;

‒ Liquidity risk;

‒ Inflation risk;

‒ Legal environment risk;

‒ Operational risk;

‒ Group risk;

‒ Pension risk;

‒ Strategic risk;

‒ Contagion risk.

Solvency II Breakfast Briefing21

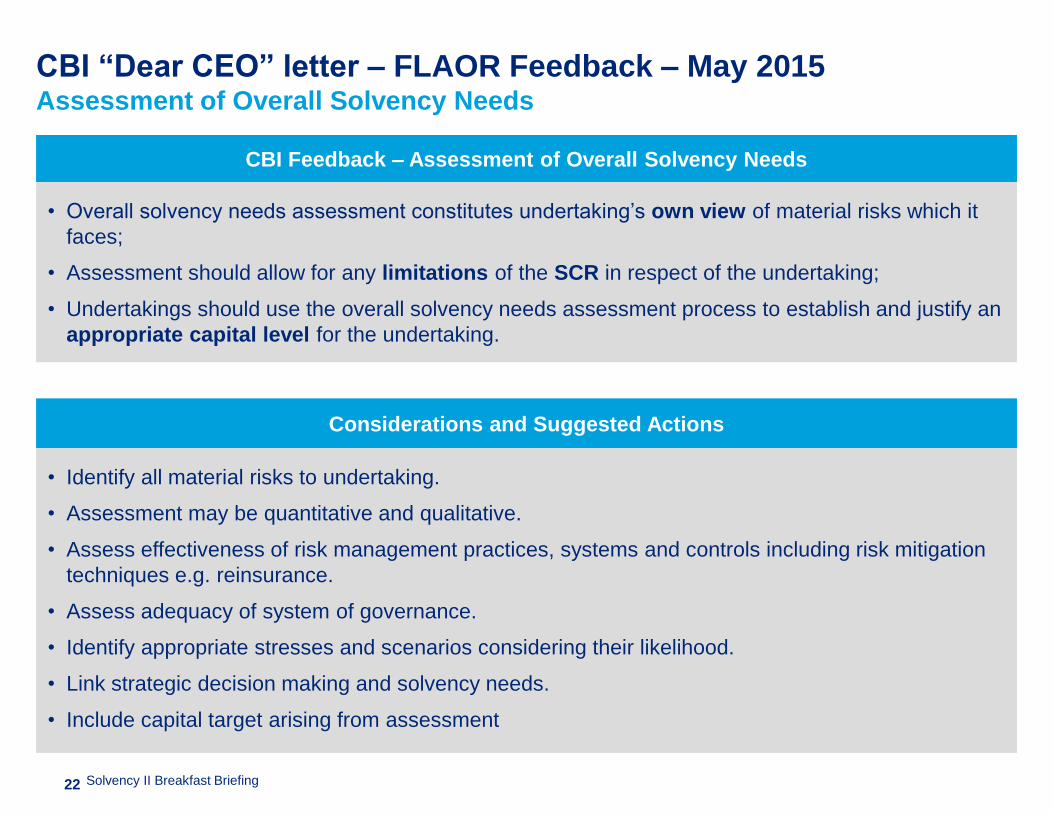

CBI “Dear CEO” letter – FLAOR Feedback – May 2015Assessment of Overall Solvency Needs

CBI Feedback – Assessment of Overall Solvency Needs

• Overall solvency needs assessment constitutes undertaking’s own view of material risks which it

faces;

• Assessment should allow for any limitations of the SCR in respect of the undertaking;

• Undertakings should use the overall solvency needs assessment process to establish and justify an

appropriate capital level for the undertaking.

Considerations and Suggested Actions

• Identify all material risks to undertaking.

• Assessment may be quantitative and qualitative.

• Assess effectiveness of risk management practices, systems and controls including risk mitigation

techniques e.g. reinsurance.

• Assess adequacy of system of governance.

• Identify appropriate stresses and scenarios considering their likelihood.

• Link strategic decision making and solvency needs.

• Include capital target arising from assessment

Solvency II Breakfast Briefing22

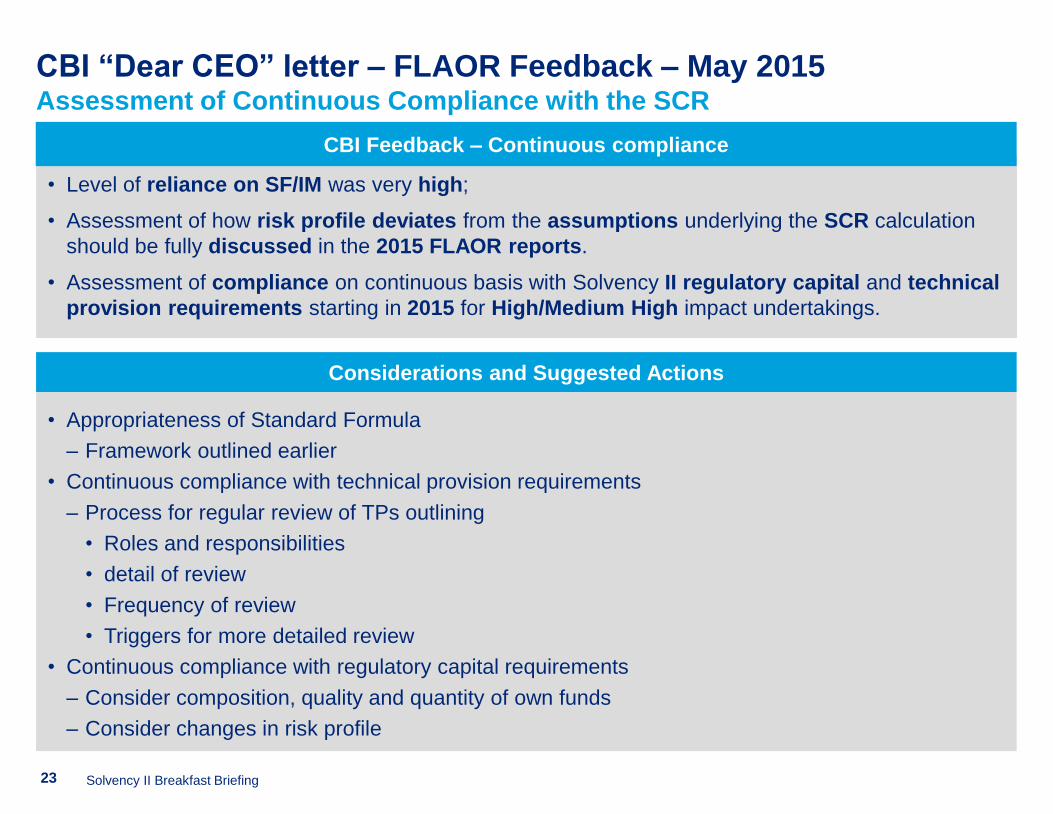

CBI “Dear CEO” letter – FLAOR Feedback – May 2015Assessment of Continuous Compliance with the SCR

• Level of reliance on SF/IM was very high;

• Assessment of how risk profile deviates from the assumptions underlying the SCR calculation

should be fully discussed in the 2015 FLAOR reports.

• Assessment of compliance on continuous basis with Solvency II regulatory capital and technical

provision requirements starting in 2015 for High/Medium High impact undertakings.

CBI Feedback – Continuous compliance

• Appropriateness of Standard Formula

‒ Framework outlined earlier

• Continuous compliance with technical provision requirements

‒ Process for regular review of TPs outlining

• Roles and responsibilities

• detail of review

• Frequency of review

• Triggers for more detailed review

• Continuous compliance with regulatory capital requirements

‒ Consider composition, quality and quantity of own funds

‒ Consider changes in risk profile

Considerations and Suggested Actions

Solvency II Breakfast Briefing23

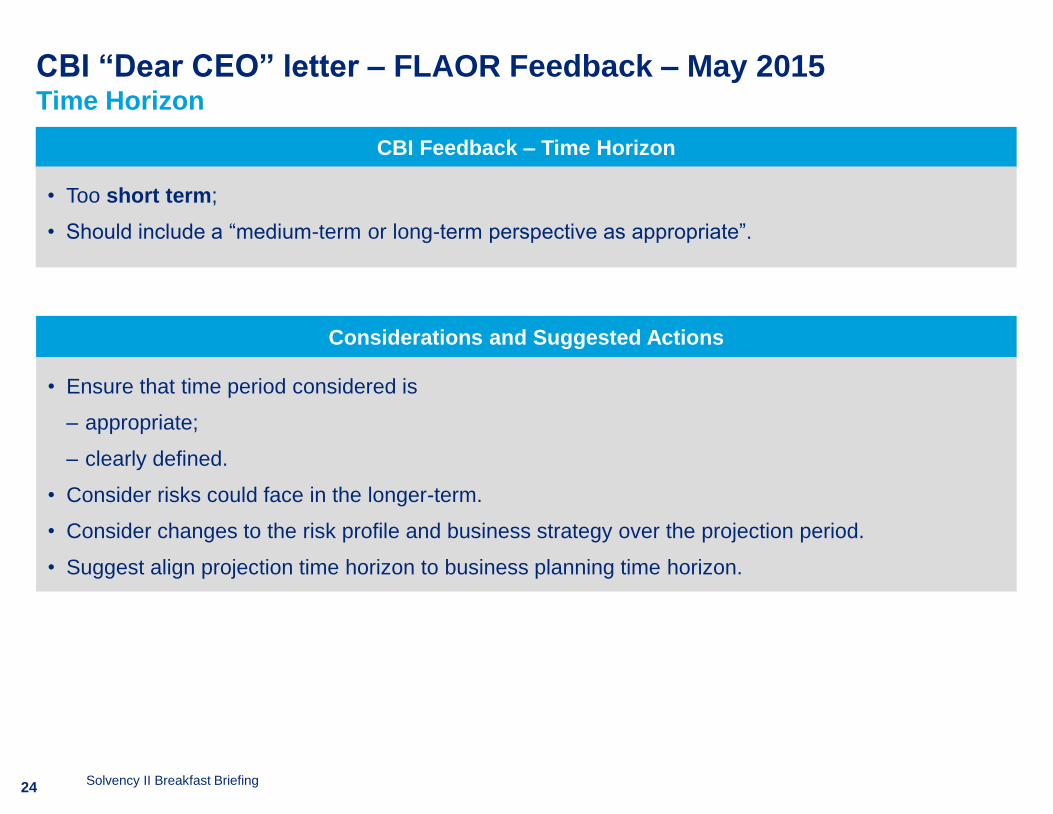

CBI “Dear CEO” letter – FLAOR Feedback – May 2015Time Horizon

CBI Feedback – Time Horizon

• Too short term;

• Should include a “medium-term or long-term perspective as appropriate”.

Considerations and Suggested Actions

• Ensure that time period considered is

‒ appropriate;

‒ clearly defined.

• Consider risks could face in the longer-term.

• Consider changes to the risk profile and business strategy over the projection period.

• Suggest align projection time horizon to business planning time horizon.

Solvency II Breakfast Briefing24

32

New for 2015

CBI Feedback – May 2015

Further Deloitte insights

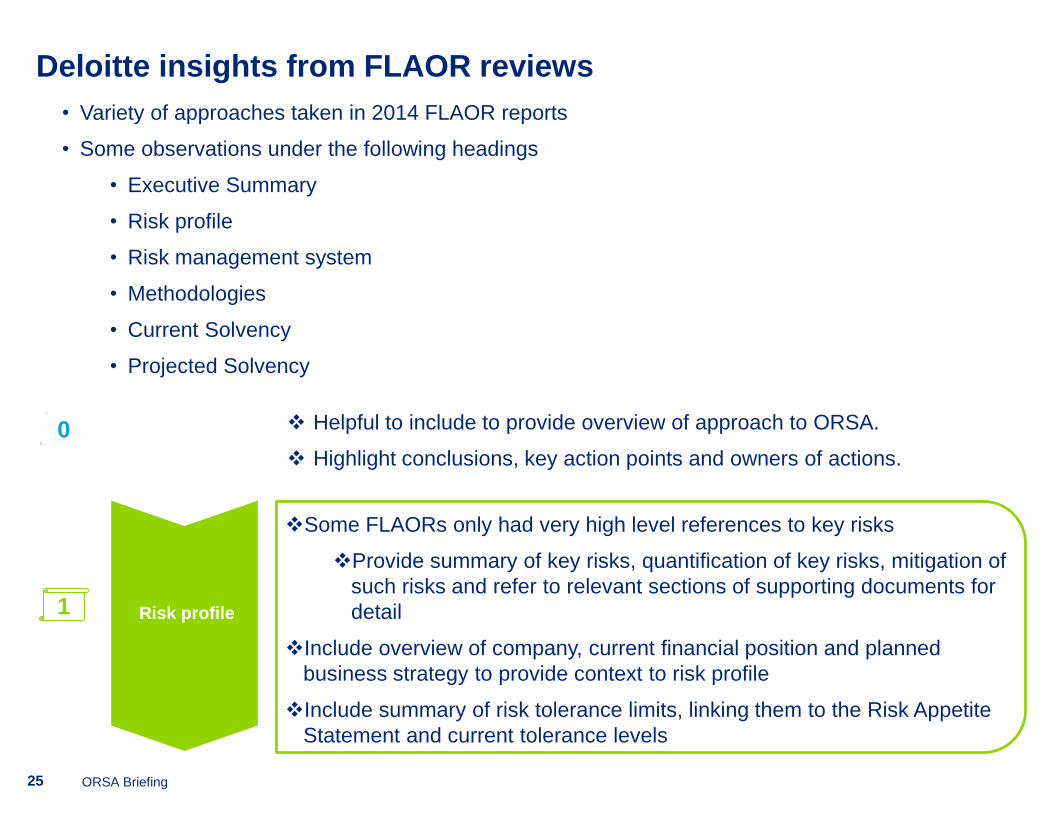

Risk profile

Some FLAORs only had very high level references to key risks

Provide summary of key risks, quantification of key risks, mitigation of

such risks and refer to relevant sections of supporting documents for

detail

Include overview of company, current financial position and planned

business strategy to provide context to risk profile

Include summary of risk tolerance limits, linking them to the Risk Appetite

Statement and current tolerance levels

1

ExecutiveSummary

0

ORSA Briefing

Helpful to include to provide overview of approach to ORSA.

Highlight conclusions, key action points and owners of actions.

• Variety of approaches taken in 2014 FLAOR reports

• Some observations under the following headings

• Executive Summary

• Risk profile

• Risk management system

• Methodologies

• Current Solvency

• Projected Solvency

Deloitte insights from FLAOR reviews

25

Risk management

system

Summarise risk management framework and any changes over year

Provide overview of FLAOR process

Discuss procedures and controls for managing non-quantifiable risks

Consider governance of risks – who owns, monitors, manages them

2

Model used

Most companies used standard formula with limited or no discussion

of its appropriateness

Where alternative economic capital models used there was

generally detail on its appropriateness relative to standard formula

Stresses/scenarios

Explain how they are identified

Limited number of stresses/scenarios in some cases

Comment on likelihood of stresses/scenarios

Key assumptions

Limited discussion of key assumptions and justification of use of

expert judgment

3 Methodologies

ORSA Briefing

Deloitte insights from FLAOR reviews

26

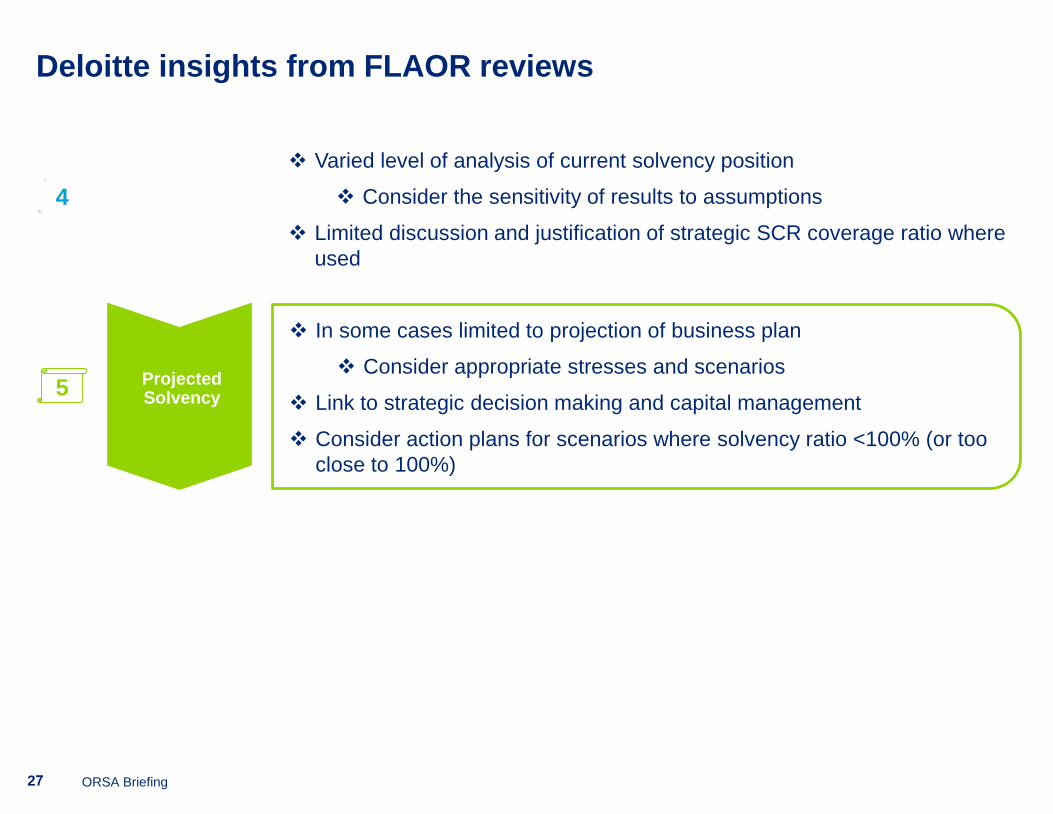

Current

Solvency

Varied level of analysis of current solvency position

Consider the sensitivity of results to assumptions

Limited discussion and justification of strategic SCR coverage ratio where

used

4

In some cases limited to projection of business plan

Consider appropriate stresses and scenarios

Link to strategic decision making and capital management

Consider action plans for scenarios where solvency ratio <100% (or too

close to 100%)

5 Projected Solvency

ORSA Briefing

Deloitte insights from FLAOR reviews

27

39

Closing Comments / Q&A

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a private company limited by guarantee, and its

network of member firms, each of which is a legally separate and independent entity. Please see

www.deloitte.com/ie/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its

member firms.

With nearly 2,000 people in Ireland, Deloitte provide audit, tax, consulting, and corporate finance to public and private

clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries,

Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address

their most complex business challenges. With over 210,000 professionals globally, Deloitte is committed to becoming

the standard of excellence.

This publication contains general information only, and none of Deloitte Touche Tohmatsu Limited, Deloitte Global

Services Limited, Deloitte Global Services Holdings Limited, the Deloitte Touche Tohmatsu Verein, any of their

member firms, or any of the foregoing’s affiliates (collectively the “Deloitte Network”) are, by means of this publication,

rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This

publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision

or action that may affect your finances or your business. Before making any decision or taking any action that may

affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte

Network shall be responsible for any loss whatsoever sustained by any person who relies on this publication.

© 2015 Deloitte. All rights reserved