sources of accounting regulations companies legislation : companies act 1956(companies amendment...

TRANSCRIPT

SOURCES OFSOURCES OF ACCOUNTING REGULATIONS ACCOUNTING REGULATIONSCompanies Legislation : Companies Companies Legislation : Companies

Act 1956(Companies Amendment Act Act 1956(Companies Amendment Act 2002)2002)

Stock Exchange Listing Requirement Stock Exchange Listing Requirement (SEBI Amendment Act 2002)(SEBI Amendment Act 2002)

Accounting StandardsAccounting Standards

AUDITORS HALL OF SHAMEAUDITORS HALL OF SHAME Arthur AndersonArthur Anderson

PWCPWC KPMGKPMG Ernest & YoungErnest & Young

Enron, Enron, WorldCom,WorldCom,

Global Crossing, Global Crossing, Dynegy, MerckDynegy, Merck

TYCO, SatyamTYCO, Satyam

XEROXXEROX

AOLAOL

INDIAN GAAPINDIAN GAAPConsists of a set of various Consists of a set of various

pronouncementspronouncements issued by issued by different regulatory authoritiesdifferent regulatory authorities

Predominantly controlled by the Predominantly controlled by the ICAIICAI

ACCOUNTING STANDARDSACCOUNTING STANDARDS

NEEDSNEEDS To To harmoniseharmonise the diverse the diverse

accounting policies and accounting policies and practicespractices

To achieve To achieve uniformityuniformity in the in the presentation of financial presentation of financial

statementsstatements

ACCOUNTING STANDARD BOARDACCOUNTING STANDARD BOARD

To To formulateformulate Accounting Standards Accounting StandardsTo To propagatepropagate the AS & persuade the the AS & persuade the

concerned parties to adoptconcerned parties to adoptTo To issueissue guidance notes on AS & guidance notes on AS &

give clarificationgive clarificationTo periodically To periodically reviewreview the AS the AS

SCOPE & STATUSSCOPE & STATUSASs do not override the LawASs do not override the LawInitial years: ASs are Initial years: ASs are

recommendatoryrecommendatory29 Standards are now 29 Standards are now

mandatory, mandatory, 3 - Recommended3 - Recommended

PROCEDUREPROCEDUREASB decides a broad area to be ASB decides a broad area to be

standardisedstandardisedFormation of Formation of study groupstudy groupPreparation of preliminary draftPreparation of preliminary draftASB issues ASB issues Exposure DraftExposure DraftAS is issued under the authority of AS is issued under the authority of

ICAIICAI

STANDARDSTANDARD containscontains A statement of concepts & principles A statement of concepts & principles

relevant to the standardrelevant to the standard Explanation of terms to be used in Explanation of terms to be used in

StandardsStandards Presentation & disclosure requirements Presentation & disclosure requirements

relevant theretorelevant thereto Date from which the Standard is proposed Date from which the Standard is proposed

to be effectiveto be effective

IASBIASBApr, 2001Apr, 2001: IASB replaced IASC(1973): IASB replaced IASC(1973) IASC issued a total of 68 Exposure IASC issued a total of 68 Exposure

Drafts & 41 IAS(1973 to 2001)Drafts & 41 IAS(1973 to 2001) IASB publishes its standards called IASB publishes its standards called

IFRS (International Financial IFRS (International Financial Reporting Standards)Reporting Standards)

IFRSIFRSIFRS 1:First-time adoption of International IFRS 1:First-time adoption of International

Financial Reporting StandardsFinancial Reporting Standards

2:Share-based Payments2:Share-based Payments

3:Business Combinations3:Business Combinations

4:Insurance Contracts4:Insurance Contracts

5:Non-current Assets Held for Sale & 5:Non-current Assets Held for Sale & Discontinued OperationsDiscontinued Operations

6:Exploration for & Evaluation of Mineral 6:Exploration for & Evaluation of Mineral AssetsAssets

7:Financial Instruments : Disclosure7:Financial Instruments : Disclosure

8: Operating Segments8: Operating Segments

ASB & IASBASB & IASBAchievementsAchievementsFailuresFailures

IASBIASB EU & AustraliaEU & Australia: Adopted IFRS from 2005: Adopted IFRS from 2005 CanadaCanada: To replace its GAAP with IFRS : To replace its GAAP with IFRS

from 2011from 2011 China & JapanChina & Japan: Undertaken convergence : Undertaken convergence

projects with IASBprojects with IASB USUS: FASB & IASB to eliminate differences: FASB & IASB to eliminate differences

USAUSAFASBFASBSECSECSOX Act - 2002SOX Act - 2002

Sarbanes Oxly Act, 2002Sarbanes Oxly Act, 2002 Public Company Accounting Oversight Public Company Accounting Oversight

Board (Board (PCAOBPCAOB) established) established to oversee audits of public companies that are to oversee audits of public companies that are

subject to US security lawssubject to US security laws to establish auditing, quality control, ethics, to establish auditing, quality control, ethics,

independence and other standards relating to independence and other standards relating to the preparation of audit reportsthe preparation of audit reports

3 of the 5 PCAOB members cannot be and must 3 of the 5 PCAOB members cannot be and must not be CPA.not be CPA.

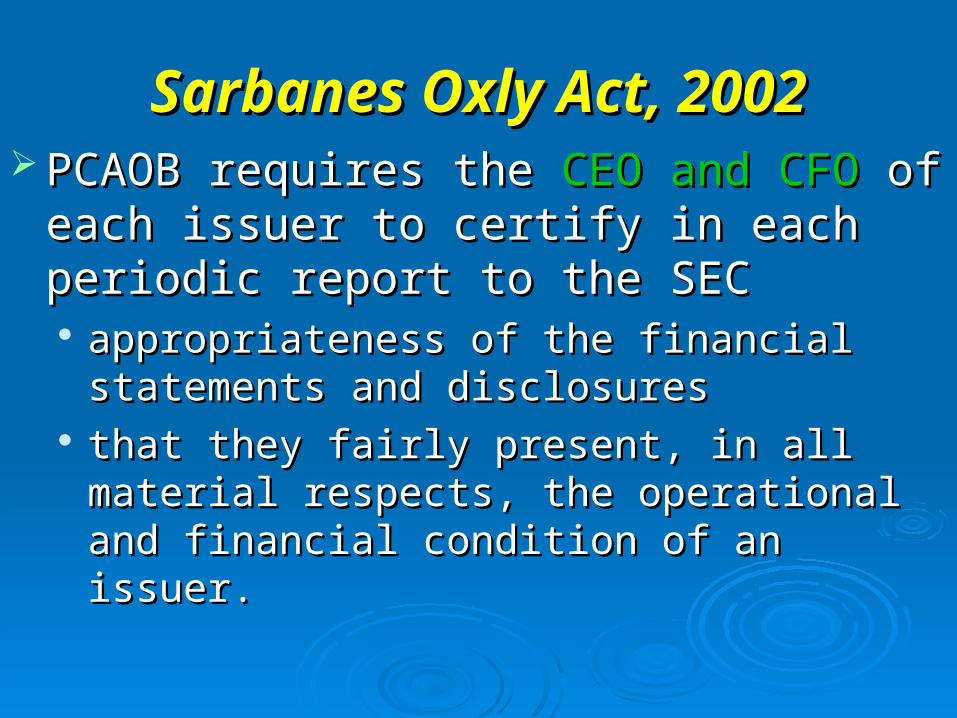

Sarbanes Oxly Act, 2002Sarbanes Oxly Act, 2002 PCAOB requires the PCAOB requires the CEO and CFOCEO and CFO of each of each

issuer to certify in each periodic report to the issuer to certify in each periodic report to the SECSEC appropriateness of the financial statements and appropriateness of the financial statements and

disclosuresdisclosures that they fairly present, in all material respects, that they fairly present, in all material respects,

the operational and financial condition of an the operational and financial condition of an issuer.issuer.

Sarbanes Oxly Act, 2002Sarbanes Oxly Act, 2002

PCAOB requires the SEC to conduct a study of PCAOB requires the SEC to conduct a study of off-balance sheet transactionsoff-balance sheet transactions and use of and use of spend-purpose-entities and reports to Congress spend-purpose-entities and reports to Congress its recommendations.its recommendations.

Section 404: Increases Corporate Section 404: Increases Corporate management’s responsibility for assessing its management’s responsibility for assessing its effectiveness of internal control over financial effectiveness of internal control over financial reporting.reporting.

Regulatory focus of SOX on auditors and Regulatory focus of SOX on auditors and corporate management.corporate management.

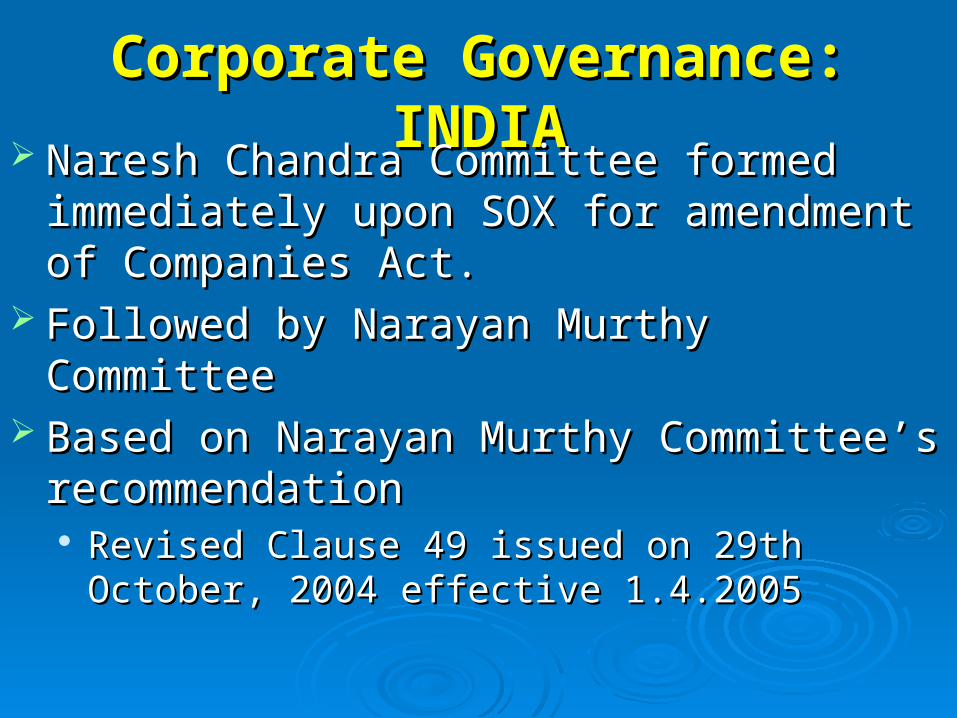

Corporate Governance: INDIACorporate Governance: INDIA Naresh Chandra Committee formed Naresh Chandra Committee formed

immediately upon SOX for amendment of immediately upon SOX for amendment of Companies Act.Companies Act.

Followed by Narayan Murthy CommitteeFollowed by Narayan Murthy Committee Based on Narayan Murthy Committee’s Based on Narayan Murthy Committee’s

recommendation recommendation Revised Clause 49 issued on 29th October, 2004 Revised Clause 49 issued on 29th October, 2004

effective 1.4.2005effective 1.4.2005

Corporate GovernanceCorporate Governance Mandatory Provision - Mandatory Provision - Audit CommitteeAudit Committee Comprising of at least 3 directors and two-third Comprising of at least 3 directors and two-third

being independent directors.being independent directors. All members shall be All members shall be financially literatefinancially literate (ability (ability

to read financial statements) and at least one to read financial statements) and at least one member shall have accounting or related member shall have accounting or related financial management expertise (experience in financial management expertise (experience in the area or professional qualification).the area or professional qualification).

CorporateCorporate GovernanceGovernance At least 4 meetings a year and not more than 4 At least 4 meetings a year and not more than 4

months shall elapse between 2 meetings.months shall elapse between 2 meetings. Audit CommitteeAudit Committee to mandatorily review : to mandatorily review :

M. D. & A. (Management Discussion & Analysis) of financial M. D. & A. (Management Discussion & Analysis) of financial conditions and resultsconditions and results

Statement of significant related party transactionsStatement of significant related party transactions Management letters / letters of internal control weaknesses Management letters / letters of internal control weaknesses

issued by statutory auditors.issued by statutory auditors. Internal audit reports relating to internal control weaknessesInternal audit reports relating to internal control weaknesses Appointment, removal, terms of remuneration of Chief Appointment, removal, terms of remuneration of Chief

Internal Auditors.Internal Auditors.

ACCOUNTING STANDARDSACCOUNTING STANDARDS

AS-1: DISCLOSURE OF AS-1: DISCLOSURE OF ACCOUNTING POLICIESACCOUNTING POLICIES

PURPOSEPURPOSE To promote better understandingTo promote better understanding To facilitate meaningful comparisonTo facilitate meaningful comparison

WHY AS-1WHY AS-1 Considerable variations existConsiderable variations exist P/L & state of affairs can be significantly P/L & state of affairs can be significantly

affected by APaffected by AP

FUNDAMENTAL ACCOUNTING FUNDAMENTAL ACCOUNTING ASSUMPTIONSASSUMPTIONS

Going concernGoing concernConsistencyConsistencyAccrualAccrual

ACCOUNTING POLICIESACCOUNTING POLICIES

Specific accounting principles Specific accounting principles and methods in the preparation and methods in the preparation & presentation of Fin. Sts.& presentation of Fin. Sts.

No single list of AP which is No single list of AP which is applicable to all circumstancesapplicable to all circumstances

AREAS HAVING DIFFERENT APsAREAS HAVING DIFFERENT APs Methods of depreciation, depletion & amortisationMethods of depreciation, depletion & amortisation Treatment of expenditure during constructionTreatment of expenditure during construction Translation of foreign currency itemsTranslation of foreign currency items Valuation of InventoriesValuation of Inventories Treatment of GoodwillTreatment of Goodwill Valuation of InvestmentValuation of Investment Treatment of retirement benefitsTreatment of retirement benefits Recognition of profit on long-term contractsRecognition of profit on long-term contracts Valuation of FAValuation of FA Treatment of Contingent liabilitiesTreatment of Contingent liabilities

No exhaustive list of APsNo exhaustive list of APs

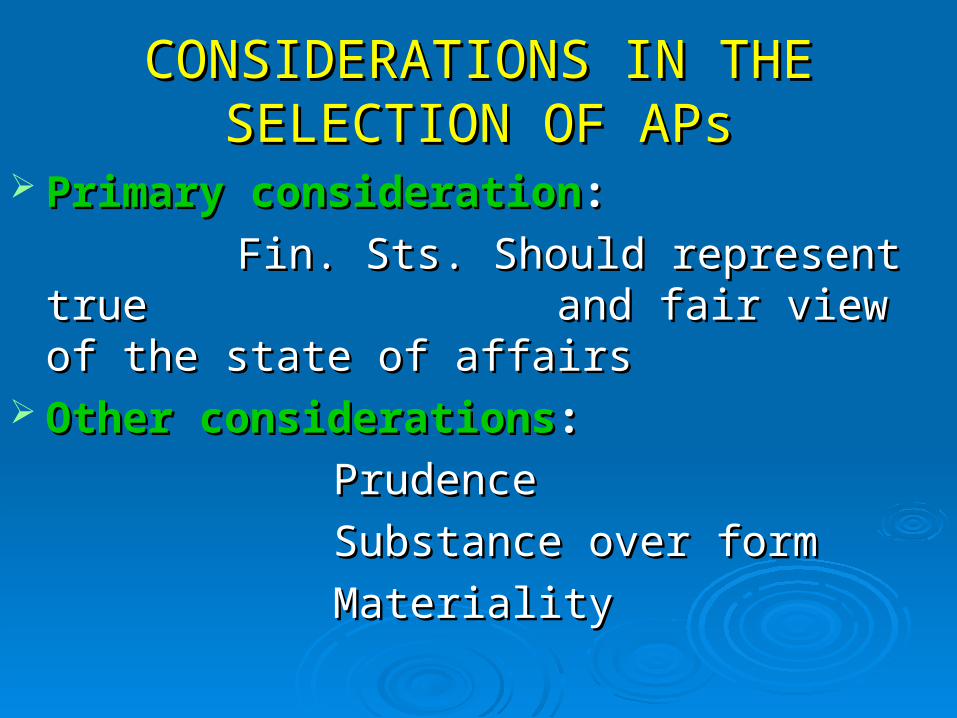

CONSIDERATIONS IN THE CONSIDERATIONS IN THE SELECTION OF APsSELECTION OF APs

Primary considerationPrimary consideration: :

Fin. Sts. Should represent true Fin. Sts. Should represent true and fair view of the state of affairs and fair view of the state of affairs

Other considerationsOther considerations::

PrudencePrudence

Substance over formSubstance over form

MaterialityMateriality

AS-1AS-1 24. All 24. All significantsignificant accounting policies accounting policies adopted in adopted in

the preparation and presentation of Financial the preparation and presentation of Financial Statement should be disclosed.Statement should be disclosed.

25. The Disclosure of significant APs should 25. The Disclosure of significant APs should form part of the Financial Statements and form part of the Financial Statements and should be disclosed in should be disclosed in one placeone place..

26.26. Any Any change in the APschange in the APs which has a which has a material material

effecteffect should be disclosed. should be disclosed. The The amountamount by which any item in the Financial by which any item in the Financial

Statement is Statement is affectedaffected by such change should by such change should be disclosed.be disclosed.

Where such amount is Where such amount is notnot ascertainableascertainable wholly wholly or in part, the fact should be disclosedor in part, the fact should be disclosed

27.27.

If the fundamental accounting If the fundamental accounting assumptionsassumptions (i.e.,3) are (i.e.,3) are followedfollowed- -

Specific disclosure is not required.Specific disclosure is not required. If If not followednot followed--

The fact should be disclosed. The fact should be disclosed.

AS- 2 RevisedAS- 2 Revised Mandatory: 01.04.1999Mandatory: 01.04.1999

OBJECTIVE:OBJECTIVE:

Determination of the value at which inventories Determination of the value at which inventories are carried in the Financial Statementare carried in the Financial Statement

VALUATION OF INVENTORIES

Inventories are assetsInventories are assets

a)a) Held for sale in the ordinary course of Held for sale in the ordinary course of business.business.

b)b) In the process of production for such In the process of production for such sale, or sale, or

c)c) In the form of materials or supplies to be In the form of materials or supplies to be consumed in the production process or in consumed in the production process or in the rendering of services.the rendering of services.

Inventories encompass:Inventories encompass: Goods purchased and held for resaleGoods purchased and held for resale Computer software held for resaleComputer software held for resale Land and other property held for resaleLand and other property held for resale Finished goods, Work-in-progress, Finished goods, Work-in-progress,

Materials, Maintenance Supplies, Materials, Maintenance Supplies, Consumables & Loose tools.Consumables & Loose tools.

Inventories do not include

Machinery spares

AS 2 will not apply to:AS 2 will not apply to:

a)a) WIP under construction contractsWIP under construction contracts

b)b) WIP of service providerWIP of service provider

c)c) Shares, debentures and other financial Shares, debentures and other financial instrumentsinstruments

d)d) Producer inventories of live stock, Producer inventories of live stock, agricultural and forest products and agricultural and forest products and mineral oils, ores and gasesmineral oils, ores and gases

MEASUREMENT OF INVENTORIESMEASUREMENT OF INVENTORIES

Inventories should be valued at the Inventories should be valued at the lower of cost and net realisable valuelower of cost and net realisable value

COSTThe cost of inventories should comprise (1) Cost of purchase (2) Cost of conversion (3) Other cost incured in bringing the inventories to there present location and condition

Exclusion from the cost of inventory: Abnormal amounts, Storage cost, administrative overhead, selling & distribution overhead

COST FORMULACOST FORMULA (1)Specific identification of cost(1)Specific identification of cost

Items not ordinarily interchangeable Items not ordinarily interchangeable Goods & Services for specific Goods & Services for specific projectsprojects

(2) FIFO or Weighted Average cost(2) FIFO or Weighted Average cost

TECHNIQUES FOR MEASUREMENT OF COST

(1)Standard Cost(2) Retail Method

NET REALISABLE VALUENET REALISABLE VALUE(Estimated selling price (Estimated selling price lessless Estimated cost of Estimated cost of

completion)completion)

Damaged Wholly or partially obsoleteSelling prices have declinedIncrease in estimated cost of completion

CASH FLOW STATEMENTCASH FLOW STATEMENT AS 3 RevisedAS 3 Revised

Objective:Objective:

Shows the historical changes in cash Shows the historical changes in cash

and cash equivalents during the and cash equivalents during the period from operating, investing & period from operating, investing & financing activities.financing activities.

CashCash C.E.C.E. ActivitiesActivities

BenefitsBenefits(1)(1) Shows the ability to generate cash & cash equivalentShows the ability to generate cash & cash equivalent

(2)(2) Shows the need to utilise these cash flowsShows the need to utilise these cash flows

(3)(3) Helps to assess liquidity & solvencyHelps to assess liquidity & solvency

(4)(4) Indicate the amount, timing & certainty of future Indicate the amount, timing & certainty of future cash flowscash flows

(5)(5) Shows relationship between Shows relationship between profit & net cash profit & net cash flowsflows

(6)(6) Useful in checking accuracy of past assessmentUseful in checking accuracy of past assessment

Cash Flow StatementCash Flow Statement

Cash flow from operating activities ------------Cash flow from operating activities ------------Cash flow from investing activities ------------Cash flow from investing activities ------------Cash flow from financing activities ------------Cash flow from financing activities ------------______________________________________________________________________________________________Net cash increase (decrease) in Net cash increase (decrease) in

cash & cash eq. ------------ cash & cash eq. ------------ Cash &cash eq. at the beginning Cash &cash eq. at the beginning

of the period ------------of the period ------------______________________________________________________________________________________________Cash & cash eq. at the end of theCash & cash eq. at the end of the

Period ------------Period ------------

AS-4: CONTINGENCIES AND AS-4: CONTINGENCIES AND EVENTS OCCURING AFTER EVENTS OCCURING AFTER THE BALANCE SHEET DATETHE BALANCE SHEET DATE

Deals withDeals with::Contingencies Contingencies Events occurring after the Events occurring after the

Balance Sheet dateBalance Sheet date

AS-4 does not apply:AS-4 does not apply:

Liabilities of life assurance and general Liabilities of life assurance and general insuranceinsurance

Obligation under retirement benefit plansObligation under retirement benefit plans Commitments arising from long-term lease Commitments arising from long-term lease

contractscontracts

Contingencies refers to-Contingencies refers to-

Existing conditions or situation.Existing conditions or situation. Result of which is not known on the Result of which is not known on the

balance sheet date.balance sheet date. Result of which would be known only Result of which would be known only

happening or non-happening of certain happening or non-happening of certain events in future.events in future.

Result may be either gain or loss.Result may be either gain or loss.

Examples of Contingencies:Examples of Contingencies:

Collectibility of recoverable/debtorsCollectibility of recoverable/debtors Litigation, claims and assessments for Litigation, claims and assessments for

recovery of assets.recovery of assets.

Events after Balance Sheet date:Events after Balance Sheet date:Events which occur between the Events which occur between the

balance sheet datebalance sheet date and date on which and date on which financial statements are financial statements are approved by approved by competent authoritycompetent authority..

The events are significant event and The events are significant event and may be favourable and unfavourable.may be favourable and unfavourable.

DISCLOSUREDISCLOSURE If material contingent loss is If material contingent loss is not provided not provided

forfor, its nature and an estimate of financial , its nature and an estimate of financial effect should be disclosed by way of note.effect should be disclosed by way of note.

If estimate of financial If estimate of financial effect can not be effect can not be mademade, the fact should be disclosed., the fact should be disclosed.

AS 5-AS 5-Net profit or loss for the Net profit or loss for the period, prior period items & period, prior period items & change in accounting policieschange in accounting policies

OBJECTIVE:OBJECTIVE: To prescribe the criteria for certain items in the P&L To prescribe the criteria for certain items in the P&L

a/c to enhance comparabilitya/c to enhance comparability To suggest the accounting treatment & presentations To suggest the accounting treatment & presentations

of the items not relating to the period.of the items not relating to the period. To deal with the change in accounting policy, To deal with the change in accounting policy,

accounting estimates & extraordinary itemsaccounting estimates & extraordinary items

COMPONENTS OF NET PROFITCOMPONENTS OF NET PROFIT

P&L from ordinary activitiesP&L from ordinary activitiesExtraordinary itemsExtraordinary items

To be disclosed on the face To be disclosed on the face of statement of P&L accountof statement of P&L account

DISCLOSE SEPARATELY : DISCLOSE SEPARATELY : If RelevantIf Relevant

Write down of inventory to NRV or reversal of Write down of inventory to NRV or reversal of such write downsuch write down

Restructuring costRestructuring cost Profit or loss on disposal of F.A.Profit or loss on disposal of F.A. Profit or loss on disposal of long term Profit or loss on disposal of long term

investmentinvestment Litigation settlementsLitigation settlements Reversal of provisionsReversal of provisions

EXTRAORDINARY ITEMSEXTRAORDINARY ITEMS

Clearly distinct from ordinary activitiesClearly distinct from ordinary activities Not occurring frequently or regularlyNot occurring frequently or regularly Nature and amount : Disclosed separately Nature and amount : Disclosed separately

in P&L accountin P&L account

PRIOR PERIOD ITEMPRIOR PERIOD ITEM Incomes or expenses arising in current period as Incomes or expenses arising in current period as

a result of a result of error or omissionerror or omission in the preparation of in the preparation of Financial Statements of one or more prior periodsFinancial Statements of one or more prior periods

Nature and amount : Disclosed separately in Nature and amount : Disclosed separately in P&LP&L

Ex. Salary A/CEx. Salary A/C Dr. Dr.

Prior period expense (Salary) Dr.Prior period expense (Salary) Dr.

To Bank A/CTo Bank A/C

Note: Note: Payment of prior period expense by court orderPayment of prior period expense by court order

CHANGE IN ACCOUNTING CHANGE IN ACCOUNTING ESTIMATESESTIMATES

Estimation of provision of sundry debtorsEstimation of provision of sundry debtors Estimation of provision for any liabilityEstimation of provision for any liability Computing income tax provisionComputing income tax provision Estimating the useful life of F.A.Estimating the useful life of F.A.

To classify as ordinary & To classify as ordinary & extraordinary & disclose the effectextraordinary & disclose the effect

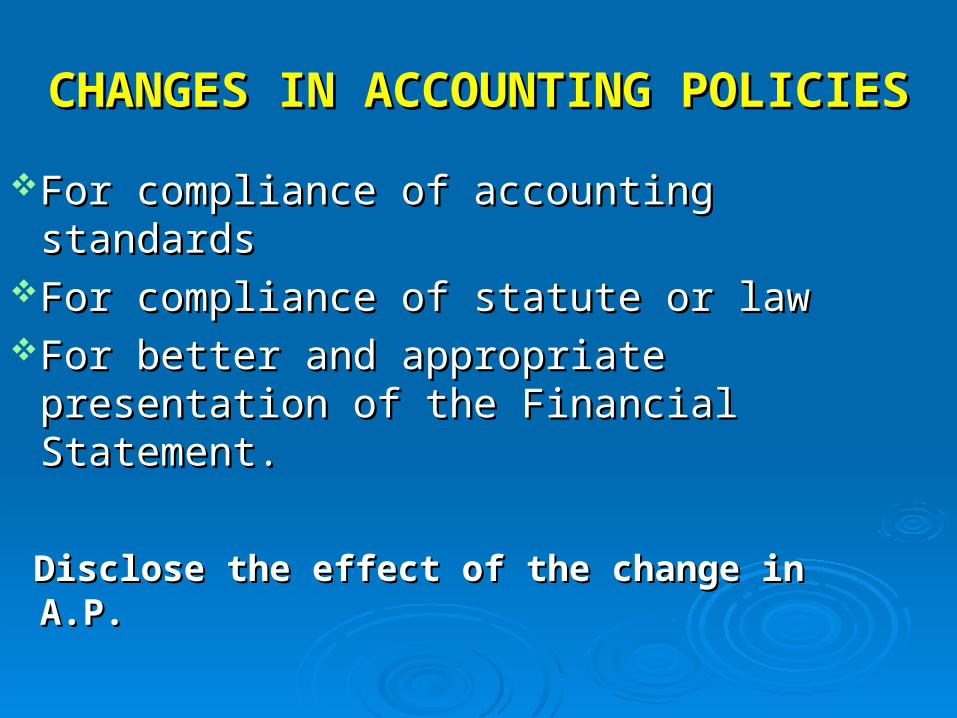

CHANGES IN ACCOUNTING POLICIESCHANGES IN ACCOUNTING POLICIES

For compliance of accounting standardsFor compliance of accounting standardsFor compliance of statute or lawFor compliance of statute or lawFor better and appropriate presentation For better and appropriate presentation

of the Financial Statement.of the Financial Statement.

Disclose the effect of the change in A.P.Disclose the effect of the change in A.P.

ACCOUNTING STANDARD - 6ACCOUNTING STANDARD - 6DEPRECIATION ACCOUNTINGDEPRECIATION ACCOUNTING

Applies to all depreciable assets except:Applies to all depreciable assets except:

1.1. Forests, plantations and similar regenerative natural Forests, plantations and similar regenerative natural resources.resources.

2.2. Wasting assets: minerals, oils, natural gas and Wasting assets: minerals, oils, natural gas and similar non-generative resources.similar non-generative resources.

3.3. Expenditure on R & D.Expenditure on R & D.

4.4. GoodwillGoodwill

5.5. Live stockLive stock

It also does not apply to land unless it has a It also does not apply to land unless it has a limited useful life for the organisation.limited useful life for the organisation.

Why AS for Depreciation Accounting?Why AS for Depreciation Accounting?

DEPRECIATION:DEPRECIATION: A measure of the wearing out, A measure of the wearing out, consumption or other loss of value arising from use, consumption or other loss of value arising from use, effluxion of time or obsolescence through technology effluxion of time or obsolescence through technology and market changes.and market changes.

DEPRECIABLE ASSETSDEPRECIABLE ASSETS are assets which: are assets which: 1. are used during more than one accounting period.1. are used during more than one accounting period.2. have a limited useful life.2. have a limited useful life.3. are held for use in the production or supply of 3. are held for use in the production or supply of goods goods and services.and services.

USEFUL LIFEUSEFUL LIFE

i.i. The period over which a depreciable asset is The period over which a depreciable asset is expected to be used, orexpected to be used, or

ii.ii. The number of production or similar units The number of production or similar units expected to be obtained for the asset.expected to be obtained for the asset.

DEPRECIABLE AMOUNTDEPRECIABLE AMOUNT

Historical cost or other amount substituted for Historical cost or other amount substituted for historical cost historical cost

LessLess the estimated residual value. the estimated residual value.

AMOUNTAMOUNT OF DEPRECIATIONOF DEPRECIATION

Based on:Based on:

i. Historical cost i. Historical cost

or other amount substituted.or other amount substituted.

ii. Expected useful life.ii. Expected useful life.

iii. Estimated residual valueiii. Estimated residual value

HISTORICAL COSTHISTORICAL COST Represents its money outlay for acquisition, Represents its money outlay for acquisition,

installation & commissioning as well as for installation & commissioning as well as for additions to or improvement thereof.additions to or improvement thereof.

H.C. may undergo changes arising as a result H.C. may undergo changes arising as a result of increase or decrease in long term liability on of increase or decrease in long term liability on account of exchange fluctuations, price account of exchange fluctuations, price adjustments, changes in duties or similar adjustments, changes in duties or similar factors.factors.

The The quantum of depreciationquantum of depreciation to be to be provided in an accounting period involves provided in an accounting period involves the exercise of judgement by mgt. in the the exercise of judgement by mgt. in the light of technical, commercial, accounting light of technical, commercial, accounting and legal requirements and may need and legal requirements and may need periodical review.periodical review.

Original estimate of Original estimate of useful lifeuseful life may be may be revised.revised.

METHODSMETHODSStraight line methodStraight line methodReducing balance methodReducing balance method

The Companies Act 1956 lays The Companies Act 1956 lays down the rates of depreciation for down the rates of depreciation for various assets.various assets.

DISCLOSUREDISCLOSURE

The depreciation methods used.The depreciation methods used. The total depreciation for each class of The total depreciation for each class of

assets.assets. The gross amount of each class of assetThe gross amount of each class of asset The accumulated depreciation.The accumulated depreciation. Revaluation of depreciable asset.Revaluation of depreciable asset. Change in the method of depreciationChange in the method of depreciation

AS (Paragraphs 20-29) AS (Paragraphs 20-29) 20. The 20. The depreciable amountdepreciable amount should be allocated on a should be allocated on a

systematic basis to each accounting period during the systematic basis to each accounting period during the useful lifeuseful life..

21. The 21. The depreciation methoddepreciation method selected should be selected should be applied consistently from period to period.applied consistently from period to period.

A change in method should be made only if:A change in method should be made only if: The adoption of new method is required by statute.The adoption of new method is required by statute. For compliance with an accounting standard.For compliance with an accounting standard. Change would result in a more appropriate Change would result in a more appropriate

preparation or presentation of financial statistics.preparation or presentation of financial statistics.Retrospective recomputation of depreciationRetrospective recomputation of depreciation Deficiency/Surplus adjusted in St. of profit and loss.Deficiency/Surplus adjusted in St. of profit and loss.

22. 22. Useful lifeUseful life should be estimated after should be estimated after considering:considering:

i.i. Expected physical wear and tear.Expected physical wear and tear.

ii.ii. ObsolescenceObsolescence

iii.iii. Legal or other limits on the use of the asset.Legal or other limits on the use of the asset.

23. 23. Useful livesUseful lives may be reviewed periodically. may be reviewed periodically. The unamortized depreciable amount should The unamortized depreciable amount should be charged over the revised remaining useful be charged over the revised remaining useful life.life.

24. Any 24. Any addition or extensionaddition or extension should be should be depreciated over the remaining useful life of depreciated over the remaining useful life of that asset.that asset.

25. 25. Change in H.C.:Change in H.C.: Due to exchange fluctuation Due to exchange fluctuation price adjustments, changes in duties etc.price adjustments, changes in duties etc.

Depreciation on revised amount should be Depreciation on revised amount should be provided prospectively over the residual provided prospectively over the residual useful life.useful life.

26. 26. Revaluation of asset:Revaluation of asset: Depreciation on Depreciation on revalued amount. revalued amount.

Disclosed separately if revaluation has Disclosed separately if revaluation has material effect on the amount of material effect on the amount of depreciation.depreciation.

27. If the asset is disposed of, discarded, 27. If the asset is disposed of, discarded, demolished or destroyed, the net surplus of demolished or destroyed, the net surplus of deficiency; if material , should be disclosed.deficiency; if material , should be disclosed.

28. Disclose:28. Disclose: i.i. H.C. or other amount substituted for H.C.H.C. or other amount substituted for H.C.ii.ii. Depreciation for the period for each class.Depreciation for the period for each class.iii.iii. The related accumulated depreciation.The related accumulated depreciation.

29. Disclose29. Disclose: along with other accounting : along with other accounting policiespolicies

i.i. Depreciation methods used Depreciation methods used ii.ii. Depreciation rates or the useful lives if Depreciation rates or the useful lives if

they are different from statute.they are different from statute.

ACOUNTING FOR FIXED ASSETS ACOUNTING FOR FIXED ASSETS (AS-10)(AS-10)

This statement does not deal with:This statement does not deal with:

i.i. Forest plantations & similar regenerative Forest plantations & similar regenerative natural resources.natural resources.

ii.ii. Wasting assetsWasting assets

iii.iii. Expenditure on real estate developmentExpenditure on real estate development

iv.iv. LivestockLivestock

Applies to Financial statements prepared Applies to Financial statements prepared on H.C. basis.on H.C. basis.

FIXED ASSET: DefinitionFIXED ASSET: DefinitionFixed asset is an asset held Fixed asset is an asset held

with the intention of being used with the intention of being used for the purpose of producing or for the purpose of producing or providing goods or services and providing goods or services and is not held for sale in the is not held for sale in the normal course of business. normal course of business. (para 6.1)(para 6.1)

GROSS BOOK VALUE GROSS BOOK VALUE of a of a fixed asset is its historical cost fixed asset is its historical cost or other amount substituted for or other amount substituted for historical cost.historical cost.

NET BOOK VALUE:NET BOOK VALUE: Net of Net of accumulated depreciationaccumulated depreciation

WHY THIS STANDARD?WHY THIS STANDARD?Expenditure:Expenditure: An asset or An asset or

an expensean expenseAn enterprise may decide to An enterprise may decide to

expense an item which could expense an item which could otherwise have been included as otherwise have been included as fixed assets, because the amount fixed assets, because the amount of the expenditure is not material.of the expenditure is not material.

COMPONENTS OF COSTCOMPONENTS OF COST Purchase pricePurchase price including import duties & including import duties &

other non-refundable taxes or levies & any other non-refundable taxes or levies & any directly attributable cost.directly attributable cost.

ExamplesExamples

i.i. Site preparationSite preparation

ii.ii. Initial delivery & handling costs Initial delivery & handling costs

iii.iii. Installation costInstallation cost

iv.iv. Professional feesProfessional fees

AS (Paragraphs 18-39)AS (Paragraphs 18-39)

18. Items included under F.A. : Para 6.118. Items included under F.A. : Para 6.1

19. Gross Book Value: Historical cost or 19. Gross Book Value: Historical cost or Revaluation. Revaluation.

20. Cost of a F.A. : Purchase price20. Cost of a F.A. : Purchase price

Attributable costAttributable cost

Financing cost up to completion of F.A.Financing cost up to completion of F.A.

21. 21. Cost of a Self-constructed F.A.:Cost of a Self-constructed F.A.:Direct costsDirect costsAttributable costsAttributable costs

22. 22. F.A. acquired in exchange for another F.A.F.A. acquired in exchange for another F.A. Recorded at fair market value or, net book Recorded at fair market value or, net book valuevalueAdjusted for balancing payment/receipt.Adjusted for balancing payment/receipt.

FMV:FMV: Price agreed to in an open and unrestricted Price agreed to in an open and unrestricted market between knowledgeable & willing market between knowledgeable & willing parties.parties.

23. 23. Subsequent expendituresSubsequent expenditures

Added if they increase future benefits.Added if they increase future benefits.

24. 24. Material items retired from active use Material items retired from active use & & held for disposalheld for disposal

Stated at the lower of their net book value & net Stated at the lower of their net book value & net realizable value: Shown separately.realizable value: Shown separately.

25. 25. F.A. eliminatedF.A. eliminated from Financial Statements: from Financial Statements:

On disposal or no further benefit is On disposal or no further benefit is expected from its use.expected from its use.

26. 26. LossesLosses arising from retirement or, arising from retirement or,

gainsgains or or losseslosses arising from disposal: arising from disposal:

Recognised in P & L A/C.Recognised in P & L A/C.

27. 27. Revaluation of F.A.Revaluation of F.A.

An entire class of assets to be revalued or, An entire class of assets to be revalued or, systematic selection of assets for revaluation.systematic selection of assets for revaluation.

Basis of selection should be disclosedBasis of selection should be disclosed..

28. 28. Revaluation of a class of assetsRevaluation of a class of assets

Net book value Net book value ≤ Recoverable amount≤ Recoverable amount

29. 29. F.A. revalued upwardsF.A. revalued upwards

Accumulated depreciation not credited to Accumulated depreciation not credited to

P & L A/CP & L A/C

30. 30. Increase in net book value on revaluationIncrease in net book value on revaluation

Credited to Revaluation ReserveCredited to Revaluation Reserve

P/L: Increase P/L: Increase ≤decrease on previous revaluation≤decrease on previous revaluation

Decrease in net book value on revaluationDecrease in net book value on revaluation - Charged to P/L- Charged to P/L

- Charged to Revaluation Reserve: if previously - Charged to Revaluation Reserve: if previously increased increased

31. 31. F.A. at revaluationF.A. at revaluation: Para 23,24 &25 : Para 23,24 &25 applicable.applicable.

32. 32. Disposal of revalued F.A.:Disposal of revalued F.A.:

- Difference charged or credited to P/L- Difference charged or credited to P/L

- Revaluation Reserve: If loss relates to - Revaluation Reserve: If loss relates to previous increase & RR is not utilisedprevious increase & RR is not utilised

33. 33. F.A. on hire purchaseF.A. on hire purchase: At cash value : At cash value Shown in Balance Sheet with narration.Shown in Balance Sheet with narration.

34. 34. Joint ownership of F.A.Joint ownership of F.A.

Proportion of original cost, accumulated Proportion of original cost, accumulated depreciation & written down value: depreciation & written down value:

Shown in Balance SheetShown in Balance Sheet