south africa market overview

TRANSCRIPT

7/31/2019 South Africa Market Overview

http://slidepdf.com/reader/full/south-africa-market-overview 1/3

1

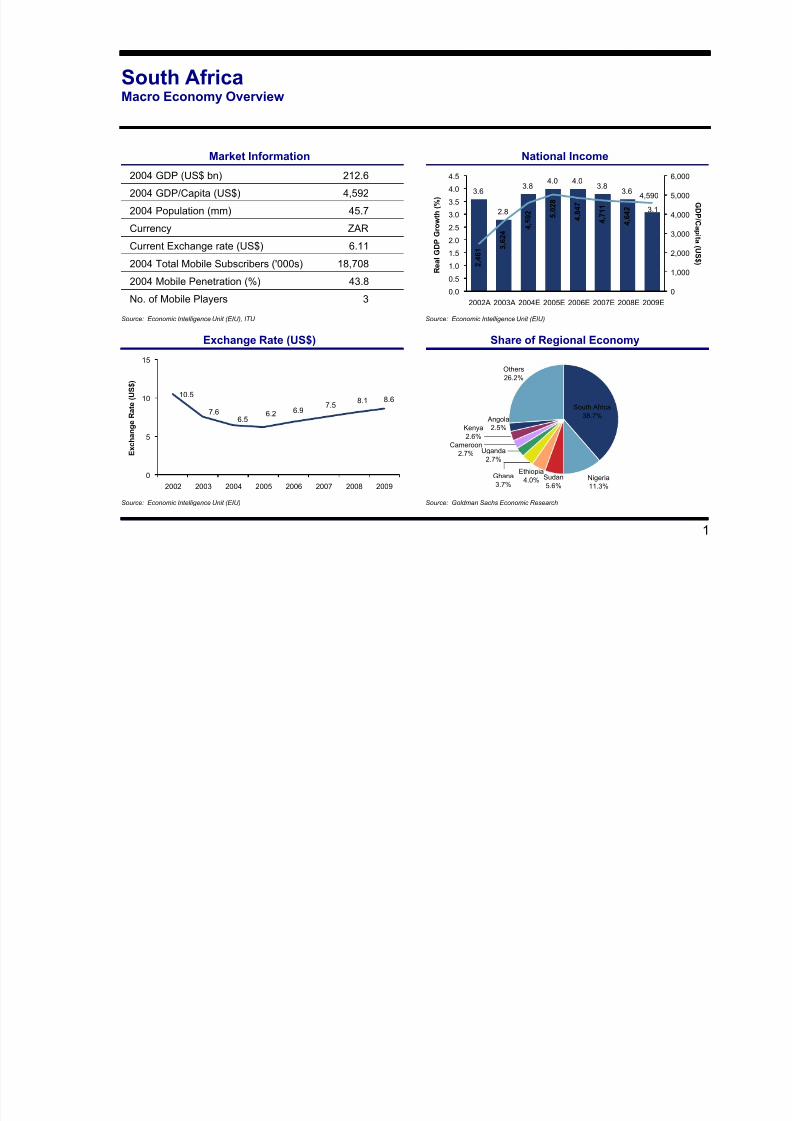

South AfricaMacro Economy Overview

Market Information National Income

2004 GDP (US$ bn) 212.6

2004 GDP/Capita (US$) 4,5922004 Population (mm) 45.7

Currency ZAR

Current Exchange rate (US$) 6.11

2004 Total Mobile Subscribers ('000s) 18,708

2004 Mobile Penetration (%) 43.8

No. of Mobile Players 3

3.6

2.8

3.84.0 4.0

3.83.6

3.1

4,590

4 , 6 4 2

4 , 7 1 1

4 , 8 4 7

5 , 0 2 8

4 , 5 9 2

3 , 6 2 4

2 , 4 6 1

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2002A 2003A 2004E 2005E 2006E 2007E 2008E 2009E

R e a l G D P G r o w t h ( % )

0

1,000

2,000

3,000

4,000

5,000

6,000

GDP / C a pi t a ( U S $ )

Source: Economic Intelligence Unit (EIU), ITU Source: Economic Intelligence Unit (EIU)

Exchange Rate (US$) Share of Regional Economy

10.58.68.1

7.5

6.2 6.97.66.5

0

5

10

15

2002 2003 2004 2005 2006 2007 2008 2009

E x c h a n g e R a t e ( U S

$ )

South Africa

38.7%

Nigeria

11.3%

Sudan

5.6%

Ethiopia

4.0%Ghana

3.7%

Uganda

2.7%

Cameroon

2.7%

Kenya

2.6%

Angola

2.5%

Others

26.2%

Source: Economic Intelligence Unit (EIU) Source: Goldman Sachs Economic Research

7/31/2019 South Africa Market Overview

http://slidepdf.com/reader/full/south-africa-market-overview 2/3

2

South AfricaMobile Market Overview

Mobile Subscribers ARPU

18,708

22,544

26,248

29,200 31,313

32,658

43.9

79.9

75.7

69.9

62.3

53.1

0

10,000

20,000

30,000

40,000

2004E 2005E 2006E 2007E 2008E 2009E

S u b s c r i b e r s ( ' 0 0 0 )

0

20

40

60

80

100

P en e t r a t i on ( % )

CA G R ( 0 4 - 0 9 )

= 1 2. 7 %

48.645.8

40.741.8

0

10

20

30

40

50

Mar-2004 Jun-2004 Sep-2004 Dec-2004

A R P U ( U S $ )

% C hange = 16. 2 %

Source: EMC Worldwide Source: EMC Worldwide

Mobile Players – Subscribers Mobile Players – Market Share

2,050

7,113

9,545

11,624

13,39514,598

15,26915,518

4,6304,0283,4042,8152,344

8,57610,038

11,19812,016 12,510

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Dec-2004 Dec-2005 Dec-2006 Dec-2007 Dec-2008 Dec-2009

S u b s c r i b e r s ( ' 0

0 0 )

3C Telecommunications MTN Vodacom

18,708

22,544

26,248

29,20031,313 32,658

14.2%12.9%11.7%10.7%10.4%11.0%

38.3%38.4%38.3%38.2%38.0%38.0%

51.0% 51.6% 51.0%50.0% 48.8% 47.5%

0%

10%

20%

30%

40%

50%

60%

2004E 2005E 2006E 2007E 2008E 2009E

M a r k e t S h a r e ( % )

3C Telecommunications MTN Vodacom

Source: EMC Worldwide Source: EMC Worldwide

7/31/2019 South Africa Market Overview

http://slidepdf.com/reader/full/south-africa-market-overview 3/3

3

South AfricaPolitical and Regulatory Overview

Regulators & Key Regulations update

Independent Communications Authority South Africa - www.icasa.org.za

Department of Communications - www.gov.za

ICASA's key functions are to implement regulations and policies, issue licenses, monitor the environment and enforce compliance withrules, regulations and policies. It also acts as an adjudicator in disputes and for complaints brought by the industry or members of thepublic against licensees, and is responsible for the planning and control of the frequency spectrum and protecting consumers from unfair business practices

It promotes the attainment of universal service and access by issuing licenses requiring operator to roll out services in under-servicedareas and ensuring that they contribute to the Universal Service Fund

In May/June 2004 ICASA awarded temporary 3G concessions to Vodacom and MTN. Vodacom may convert this to a permanent license

for ZAR 6 million per annum, while MTN is for now testing, evaluating and demonstrating UMTS and EDGE on a live pilot network

Political Overview

South Africa is a republic with a bicameral parliament and an indirectly elected president as its executive. The constitution of 1997established a parliamentary political system with three tiers of government: national, provincial and local. Each of the nine provinces hasits own government, separate executive, judiciary and legislature

In the latest elections of April 2004, Mbeki was re-elected for a second five-year term following a landslide victory for the ANC. He haspromised to continue the state's market-oriented policies and has begun to introduce more concrete plans for privatization, public sector

restructuring and economic growth

South Africa has the largest economy in Africa and has an abundance of natural resources, well-developed financial, legal, commercialand communications sectors, and a modern infrastructure which, though at capacity, supports the efficient distribution of goods andservices throughout the country