south african cities green transport programme … · south african cities green transport...

TRANSCRIPT

SOUTH AFRICAN CITIES GREEN TRANSPORT

PROGRAMME

A BUSINESS CASE FOR CNG AND BIOGAS AS A GREEN TRANSPORT

FUEL

AUGUST 2015

Prepared by:

SOUTH AFRICAN CITIES NETWORK

SOUTH AFRICAN NATIONAL ENERGY DEVELOPMENT INSTITUTE

LINKD ENVIRONMENTAL SERVICES

Disclaimer:

THIS PAPER FORMS PART OF A RESEARCH PROJECT, ‘SOUTH AFRICAN CITIES GREEN TRANSPORT PROGRAMME’, FUNDED BY THE GREEN

FUND, AN ENVIRONMENTAL FINANCE MECHANISM IMPLEMENTED BY THE DEVELOPMENT BANK OF SOUTHERN AFRICA (DBSA) ON

BEHALF OF THE DEPARTMENT OF ENVIRONMENTAL AFFAIRS (DEA). OPINIONS EXPRESSED AND CONCLUSIONS ARRIVED AT ARE THOSE OF

THE AUTHOR(S) AND ARE NOT NECESSARILY TO BE ATTRIBUTED TO THE GREEN FUND OR DBSA

2

Contents

Acronyms ............................................................................................................ 3

1 Background ................................................................................................... 4

1.1.1 Text Box 1: What is Green Transport ................................................................................................

2 Business Case for CNG Conversion ......................................................... 6

1.1.2 Text Box 2: What is CNG ....................................................................................................................

2.1 2.1 The Business Concept ........................................................................................... 7

2.1.1 2.1.1 Gas availability .................................................................................................................... 9

2.1.2 2.1.2 Converting to natural gas ................................................................................................ 10

2.2 2.2 A case for minibus taxis conversions to CNG ................................................. 11

2.2.1 2.2.1 Financial Model ................................................................................................................. 13

2.2.2 2.2.2 Business Model Options .................................................................................................. 15

2.3 2.3 A case for converting buses and municipal fleets to CNG ............................. 16

2.3.1 2.3.1 Financial Model ................................................................................................................. 17

1.1.3 Text Box 3: Municipal vehicles going hybrid .....................................................................................

2.3.2 2.3.2 Business Model ................................................................................................................. 20

1.1.4 Text Box 4: Biogas and municipal waste ...........................................................................................

3 Way forward ................................................................................................ 23

4 Conclusion .................................................................................................. 25

5 Appendix ............................................................. Error! Bookmark not defined.

6 References ................................................................................................... 27

3

Acronyms

BRT Bus Rapid Transit

CBM Compressed bio-methane

CNG Compressed Natural Gas

CO2 Carbon dioxide

CoJ City of Johannesburg

CoT City of Tshwane

DBSA Development Bank of Southern Africa

DDF Diesel Dual Fuel

DEA Department of Environmental Affairs

DoE Department of Energy

DoT Department of Transport

GHG Green House Gas

IDC Industrial Development Corporation

Kfw Kreditanstalt für Wiederaufbau (German government-owned development bank)

LBM Liquid bio-methane

LNG Liquid Natural Gas

LPG Liquid Petroleum Gas

NGV Natural Gas Vehicles

NPV Net Present Value

NREL National Renewable Energy Lab

SACN South African Cities Network

SANEDI South African National Energy Development Institute

SUV Sports / Suburban Utility Vehicle

4

1 Background

The South African Cities Network (SACN), in partnership with Linkd Environmental Services and SANEDI,

with funding from the Green Fund, have undertaken to research and develop a business plan for a Green

Transport Programme for South African Cities. The Green Transport Programme seeks to give effect to

South Africa’s commitment to reduce national greenhouse gas (GHG) emissions by 34% by 2020 and 42%

by 2025 and forms part of the Transport Flagship Programme articulated in the National Climate Change

Response White Paper:

As part of the Transport Flagship Programme, the Department of Transport will facilitate the

development of an enhanced public transport programme to promote lower-carbon mobility in five

metros and in ten smaller cities and create an Efficient Vehicles Programme with interventions that

result in measurable improvements in the average efficiency of the South African vehicle fleet by

2020.

Transport and urban mobility represent one of the most pressing strategic and sustainability challenges

facing South African cities today. The transport sector is the largest greenhouse gas emissions contributor

in South African cities and contributes approximately 13% of the total national GHG emissions.

Furthermore the legacy of apartheid spatial planning perpetuates inequality in terms of affordable access

to the economic hubs in cities. Against this backdrop, cities are embarking on the daunting task of creating

a paradigm shift away from “one person, one car economic development” and towards eco-mobility,

freedom corridors for non-motorised/low-carbon transit, and urban mass transit systems. Achieving this

paradigm shift is a monumental task involving new thinking about spatial planning and spatial form,

rethinking commuting/transportation at a societal level, understanding the long-term public health impacts

of the diesel/petrol economy, and motivating for budget for a radical change in transportation

infrastructure planning and implementation.

1.1.1 Text Box 1: What is Green Transport

Green transport is transport that is environmentally, economically and socially sustainable.

“Greening” transport involves mitigating climate change and harmful health, social and economic

impacts by reducing GHG and particulate emissions from transport, reducing noise pollution,

reducing traffic congestion, and improving land use by reducing the physical footprint of

transportation systems. Measures to accomplish this range from technology improvements to

behaviour change and spatial planning interventions.

5

As part of the research to support the Green Transport Programme, the project team has engaged

extensively with stakeholders in cities, national departments and the private sector. Cities are already

embarking on a range of green transport initiatives, and have indicated an in principle willingness to

commit to aspirational emissions reduction targets for municipal transport. At the same time, cities have

articulated a clear need for technical support and exchange of information and ideas to support these

targets. There is a level of uncertainty about greening public transport in terms of both what cities should

be doing, and how they should be doing it. To this end, cities have proposed that a Green Transport

Working Group be established under the auspices of the SACN in order to guide the future development of

the Green Transport Programme.

Private sector technology providers have pointed to the fact that internationally, the public sector has often

been a key driver in establishing the market for green transport technologies, but that this has not yet

happened at suitable scale in South Africa. Despite this, a private sector company (CNG Holdings) has been

successfully working with taxi associations to drive the adoption of Compressed Natural Gas (CNG) as a

vehicle fuel.

There is a clear need to leverage cities’ willingness and need to make commitments to supporting and

procuring green transport in order to stimulate the market for green transport solutions. This document

seeks to present the business case for cities to support the conversion of municipal and public transport to

CNG in order to accomplish this.

There are of course other low carbon technologies (such as electric vehicles, biodiesel and bioethanol) and

a range of potential strategies for reducing emissions associated with transport, including promoting modal

shifts to rail and non-motorised options such as cycling. These are all important potential aspects of a green

transport programme, many of which are being pursued by South African Cities. In presenting the business

case for conversion of public transport to CNG it is in no way the intention to detract from the value and

importance of cities learning lessons and exchanging ideas about the other green transport initiatives being

pursued.

6

2 Business Case for CNG Conversion

The business case presented here is for fuel switching in taxis, municipal buses and municipal fleets from

petrol and diesel to Compressed Natural Gas (CNG).

Fuel switching is a proven strategy for reducing emissions. When undertaken with this end in mind, fuel

switching involves converting from a high emissions energy carrier such as petrol or diesel, to an energy

carrier with lower emissions such as CNG. To successfully accomplish this, the full value chain needs to be

established and understood, including:

The supply of fuel (in this Case CNG).

Fuel distribution infrastructure

The supply, manufacture and/or conversion of appropriate vehicles

Maintenance, support and training of vehicles and drivers

All these elements are already in place in South Africa for CNG – the challenge is one of scaling up. The

public sector, and in particular cities, can play a crucial role in driving the market for CNG as a vehicle fuel.

1.1.2 Text Box 2: What is CNG

CNG (Compressed Natural Gas) is a practical alternative to petrol as a vehicle fuel. It is made by

compressing natural gas, which consists primarily of methane, to less than 1% of its volume at

standard atmospheric pressure. Natural gas occurs naturally as a fossil fuel, is a by-product of oil

refineries, and can be generated by purifying biogas from landfills or a bio digester. In all these

cases the active molecule is methane (CH4).

Natural gas can be further compressed into Liquid Natural Gas (LNG), which is often used for

transporting CNG due to its higher volumetric energy density, and is used as fuel in long haul

applications for the same reason.

7

2.1 2.1 The Business Concept

Emissions from petrol and diesel used on road transport (passenger vehicles, buses and trucks) have been

calculated as contributing 93.1% of the transport sectors overall emissions, which in turn amount for 13.1%

of the country’s total carbon emissions (DEA, 2013). Both local and global studies have established that

passenger cars are responsible for the majority of these emissions.

Cities, in conjunction with national and provincial government are already pursuing a range of strategies to

achieve model shifts in transport to reduce the impact of transport emissions. These target the shifting of

freight from road to rail, promoting mass public transport and non-motorised transport. In terms of urban

development and spatial planning, the underlying thrust is to transform the orientation of cities from the

passenger car to various forms of public transport and non-motorised transport, including cycling and

walking. The driving forces for this are not only climate change mitigation, but also to improve ambient air

quality – and therefore public health – in our urban centres, reduce traffic congestion and commuting

times, and to reduce the extent of urban space currently dedicated to parking. Most importantly,

considering that a high percentage of South Africa’s poor do not have access to private vehicles, achieving

equitable and accessible cities is predicated on these changes.

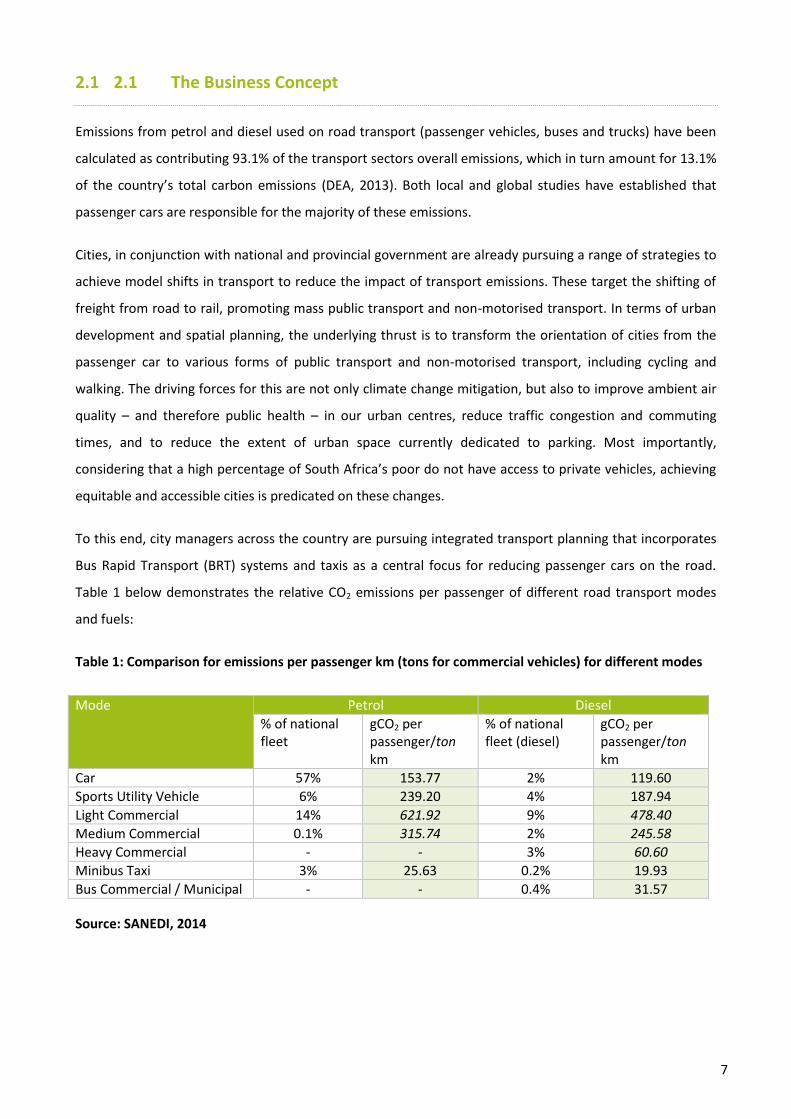

To this end, city managers across the country are pursuing integrated transport planning that incorporates

Bus Rapid Transport (BRT) systems and taxis as a central focus for reducing passenger cars on the road.

Table 1 below demonstrates the relative CO2 emissions per passenger of different road transport modes

and fuels:

Table 1: Comparison for emissions per passenger km (tons for commercial vehicles) for different modes

Mode Petrol Diesel

% of national fleet

gCO2 per passenger/ton km

% of national fleet (diesel)

gCO2 per passenger/ton km

Car 57% 153.77 2% 119.60

Sports Utility Vehicle 6% 239.20 4% 187.94

Light Commercial 14% 621.92 9% 478.40

Medium Commercial 0.1% 315.74 2% 245.58

Heavy Commercial - - 3% 60.60

Minibus Taxi 3% 25.63 0.2% 19.93

Bus Commercial / Municipal - - 0.4% 31.57

Source: SANEDI, 2014

8

The benefits in terms of reduced emissions per passenger per km (or per ton in the case of commercial

vehicles) of shifting passengers from private cars and SUVs to minibus taxis and buses are clearly

demonstrated.

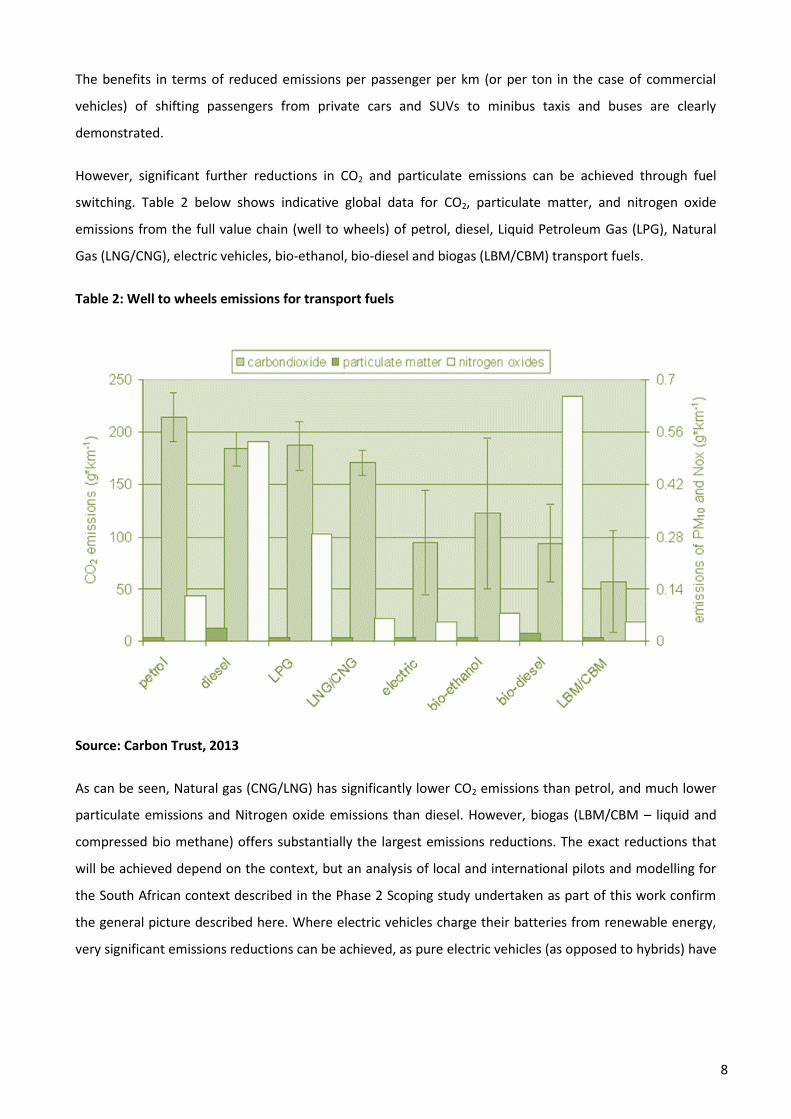

However, significant further reductions in CO2 and particulate emissions can be achieved through fuel

switching. Table 2 below shows indicative global data for CO2, particulate matter, and nitrogen oxide

emissions from the full value chain (well to wheels) of petrol, diesel, Liquid Petroleum Gas (LPG), Natural

Gas (LNG/CNG), electric vehicles, bio-ethanol, bio-diesel and biogas (LBM/CBM) transport fuels.

Table 2: Well to wheels emissions for transport fuels

Source: Carbon Trust, 2013

As can be seen, Natural gas (CNG/LNG) has significantly lower CO2 emissions than petrol, and much lower

particulate emissions and Nitrogen oxide emissions than diesel. However, biogas (LBM/CBM – liquid and

compressed bio methane) offers substantially the largest emissions reductions. The exact reductions that

will be achieved depend on the context, but an analysis of local and international pilots and modelling for

the South African context described in the Phase 2 Scoping study undertaken as part of this work confirm

the general picture described here. Where electric vehicles charge their batteries from renewable energy,

very significant emissions reductions can be achieved, as pure electric vehicles (as opposed to hybrids) have

9

no tailpipe emissions. However, electric vehicles drawing their charge from the South African grid would

have emissions profiles determined by South African grid factors, which reflect the high proportion of coal-

powered electricity generation.

The research undertaken by SACN suggests that a municipal green transport programme should be based

on:

1. Promoting modal shifts from private cars to buses, minibus taxis, rail and non-motorised transport.

2. Converting minibus taxis and buses to run on cleaner fuels, in particular CNG and biogas.

The focus of this business case is on conversion of minibus taxis and buses to switch to cleaner and more

sustainable fuels, particularly CNG and biogas. It aims to contribute towards filling the gap identified in

making the rationale for, and an approach to accomplish it. In the following sections of this report, the

business models for converting minibus taxis and buses are unpacked in greater detail. The research

presented here suggests that in addition to reducing both harmful emissions, conversion of minibus taxis

(and municipal financing of such conversions with a cost recovery mechanism in place) and bus fleets to

CNG is likely to yield financial cost savings to municipalities in the medium to long term, particularly if

implemented at scale.

2.1.1 2.1.1 Gas availability

In South Africa, natural gas is piped from Mozambique and is a major source of energy used for stationary

applications and fuel production (gas to liquid petroleum). LNG import terminals have been considered but

not yet been built. In Gauteng Province, there is already an established natural gas distribution

infrastructure (Schmidt, et al., 2012).

Biogas can be produced from a variety of organic feedstock (household waste, agro-industry, grass cuttings,

etc.). South Africa disposes enormous quantities of waste to landfill. The third national waste baseline

shows that South Africa generated approximately 108 million tonnes of waste in 2011, of which 98 million

tonnes was disposed of at landfill (DEA, 2013). Landfills are overstressed, and some are under pressure to

close as a result (Jewaskiewitz 2008). Up to 40% of household waste is organic material, which when

landfilled slowly decomposes into various organic gases including the greenhouse gas methane. An IDC

pilot programme in Gauteng showed that converting buses to dual-fuel use of diesel and biogas saved

enough for the capital investment requirements to be reclaimed within about 3, 5 years (IDC, 2013). It is

estimated that around 7 100 dedicated CNG city buses could be supplied with compressed upgraded biogas

10

if the organic waste from households would be completely collected and fed into biogas plants for the

production of transportation fuel (Schmidt, et al., 2012).

South Africa consumed approximately 11.2 billion litres of petrol and 11.9 billion litres of diesel during

2013, showing a 4.8% decrease in petrol and a 5.6% decrease in diesel from the previous year. During 2013

there was a 2.1% decrease in petrol consumption and a 0.3% increase in diesel consumption from 2012

(SAPIA, 2015). South Africa has very limited oil reserves and no local source of oil, and therefore imports

95% of its crude oil requirements as well as finished petroleum products, primarily from Saudi Arabia,

Nigeria and Angola. Current development of regional gas-fields will lead to natural gas becoming a more

important fuel in South Africa. With the availability of natural gas in neighbouring countries, such as

Mozambique and Namibia, and the discovery of offshore gas reserves in South Africa, as well as the

potential for shale gas exploitation, the gas industry in South Africa is undergoing rapid expansion (DoE,

2015). Conversion to gas therefore also has the benefit of promoting greater energy independence, and

potentially improving the national balance of payments.

2.1.2 2.1.2 Converting to natural gas

Natural gas can be used as either in a dedicated CNG system or within a mixed-fuel, dual-fuel or bi-fuel

system.

A dedicated CNG vehicle runs completely (and only) on gas. This application is suitable for vehicles that

have a fixed route that guarantees them access to CNG refueling infrastructure. In the South African

context, this is a high-risk proposition, but could be considered in local applications – for instance, as an

option for powering on-site vehicles at a facility that generates, cleans and compresses biogas to the

requisite standard to be used interchangeably with CNG.

A mixed fuel bus uses a relatively small amount of diesel/petrol, but runs primarily on CNG and shares the

same limitations as a dedicated CNG vehicle.

A dual-fuel CNG/Diesel or CNG/petrol vehicle runs on both CNG and diesel/petrol, but is also capable of

running only on the petroleum-based fuel. In some dual fuel buses the petroleum and CNG are mixed in the

engine, in others the engine runs on either CNG or petrol/diesel by switching between two separate fueling

systems (these are sometimes called bi-fuel systems). Both forms of dual-fuel system can either be

retrofitted to an existing conventional diesel or petrol vehicle, or purchased as a new vehicle.

11

Johannesburg is converting its buses to dual fuel systems that can combine CNG and diesel, while the taxi

conversions being undertaken by CNG Holdings allows taxis to run on CNG or petrol. In the interests of

pursuing solutions that are practical with respect to the relative immaturity of CNG for transport in South

Africa, and reduce the risk associated with converting to CNG, this business case focuses on the two forms

of dual-fuel CNG conversions.

2.2 2.2 A case for minibus taxis conversions to CNG

In 2012, the German development bank KfW, initiated a study to test the viability of converting to natural

gas in South Africa. As explained by Schmidt, et al. (2012), the study outcomes suggested that a fuel switch

to CNG in transport makes sense as it increases energy diversification, improves the environment and living

conditions, builds on proven technology, and provides opportunities for industrialisation and job creation.

The study looks at conversion of taxis in terms of the impact on GHG emissions and financial costs (Schmidt,

et al., 2012).

With reference to GHG emissions, the study concluded that a fuel switch from petrol to CNG always results

in substantial GHG emission reductions (~25%). The following table from Schmidt, et al. (2012) shows the

GHG emissions ‘well-to-wheel’ of a CNG fueled Toyota Quantum (dual-fuel) compared with a petrol fueled

model.

12

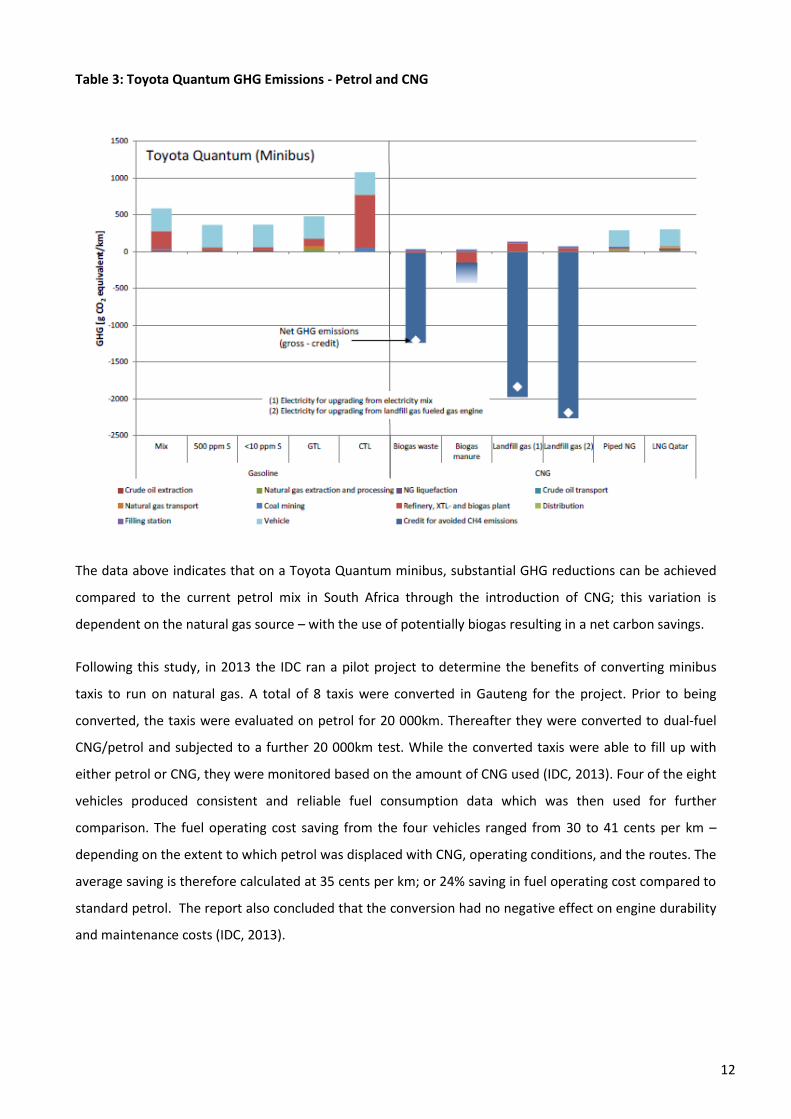

Table 3: Toyota Quantum GHG Emissions - Petrol and CNG

The data above indicates that on a Toyota Quantum minibus, substantial GHG reductions can be achieved

compared to the current petrol mix in South Africa through the introduction of CNG; this variation is

dependent on the natural gas source – with the use of potentially biogas resulting in a net carbon savings.

Following this study, in 2013 the IDC ran a pilot project to determine the benefits of converting minibus

taxis to run on natural gas. A total of 8 taxis were converted in Gauteng for the project. Prior to being

converted, the taxis were evaluated on petrol for 20 000km. Thereafter they were converted to dual-fuel

CNG/petrol and subjected to a further 20 000km test. While the converted taxis were able to fill up with

either petrol or CNG, they were monitored based on the amount of CNG used (IDC, 2013). Four of the eight

vehicles produced consistent and reliable fuel consumption data which was then used for further

comparison. The fuel operating cost saving from the four vehicles ranged from 30 to 41 cents per km –

depending on the extent to which petrol was displaced with CNG, operating conditions, and the routes. The

average saving is therefore calculated at 35 cents per km; or 24% saving in fuel operating cost compared to

standard petrol. The report also concluded that the conversion had no negative effect on engine durability

and maintenance costs (IDC, 2013).

13

Following the results of these studies, the conversion of taxis to CNG has increased rapidly in Gauteng. In

March 2014, Stephen Rothman of CNG Holdings stated that they were servicing 110 taxis at their flagship

station in Johannesburg and by October 2014 the station was servicing around 412 taxis daily, with an

additional 180 at their Dobsonville station. One of the main reason for this, as stated by Rothman, is due to

the IDC (which owns around 38% of CNG Holdings) deciding to invest in the industry as it sees the potential

of natural gas to reduce the country’s carbon footprint (Lamprecht, 2014). While an accurate number of

converted taxis does not exist at this point, it is estimated that in the Cities of Johannesburg, Tshwane and

Ekurhuleni combined there are approximately 1,000 CNG taxis.

2.2.1 2.2.1 Financial Model

The table below describes the gas pricing model used by CNG Holdings, incorporating incentives to taxi-

owners and associations in the form of commissions as well as the cost of gas with and without a margin to

recover the costs of CNG conversion. The pricing is for a volume of gas that is equivalent to one litre of

petrol. CNG Holdings regard its core business as being a gas retailer. In order to stimulate the market for

CNG as a vehicle fuel, the company funds the conversion of minibus taxis and recovers the cost from gas

sales, at a rate of R1.26 per litre equivalent sold. Even with cost recovery built in, this results in a

significantly lower fuel price for taxi operators.

Table 4: Financial model for CNG Fuel

GAS PRICE KIT FUNDED GAS PRICE KIT OWNED

Rand price per L/Eq Rand price per L/Eq

Details L/Eq L/Eq

Retail selling price including VAT 8.99 7.56

VAT 1.10 0.93

Retail selling price excluding VAT 7.89 6.63

CNG kit recovery cost 1.26 0.00

Selling price excluding VAT & kit recovery cost 6.63 6.63

Commissions taxi owner 0.07 0.07

Commission taxi association 0.07 0.07

Total commissions 0.14 0.14

14

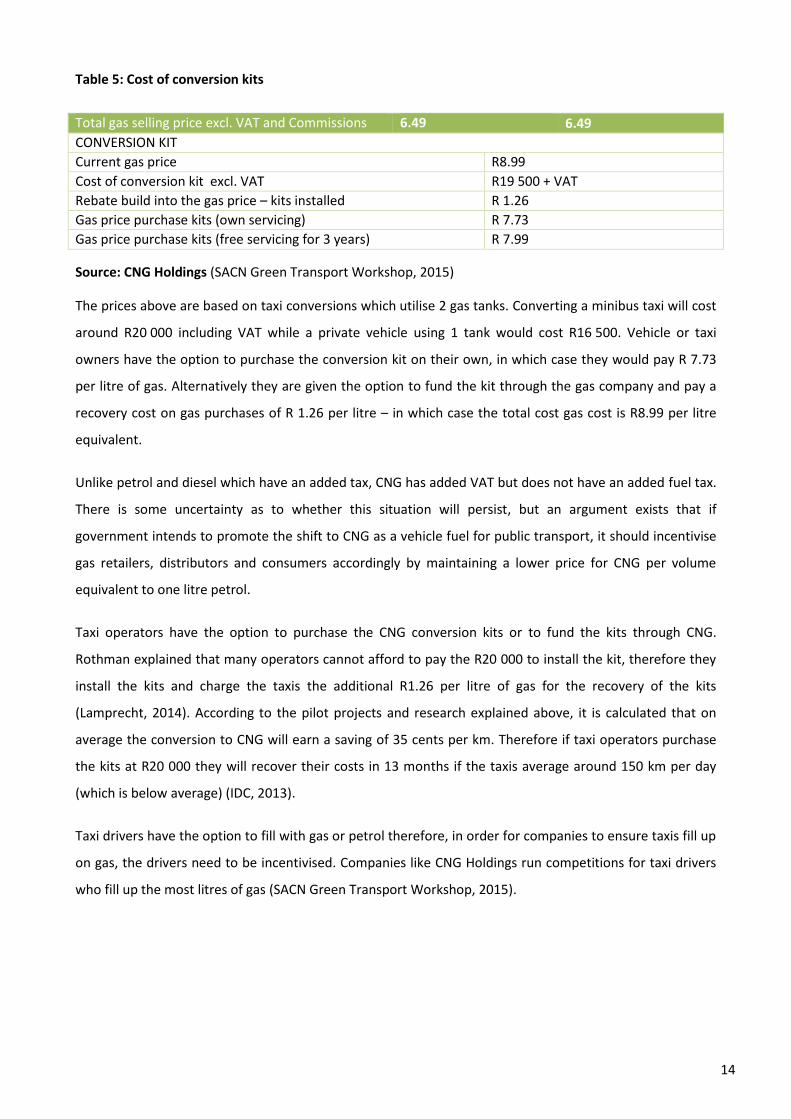

Table 5: Cost of conversion kits

Total gas selling price excl. VAT and Commissions 6.49 6.49

CONVERSION KIT

Current gas price R8.99

Cost of conversion kit excl. VAT R19 500 + VAT

Rebate build into the gas price – kits installed R 1.26

Gas price purchase kits (own servicing) R 7.73

Gas price purchase kits (free servicing for 3 years) R 7.99

Source: CNG Holdings (SACN Green Transport Workshop, 2015)

The prices above are based on taxi conversions which utilise 2 gas tanks. Converting a minibus taxi will cost

around R20 000 including VAT while a private vehicle using 1 tank would cost R16 500. Vehicle or taxi

owners have the option to purchase the conversion kit on their own, in which case they would pay R 7.73

per litre of gas. Alternatively they are given the option to fund the kit through the gas company and pay a

recovery cost on gas purchases of R 1.26 per litre – in which case the total cost gas cost is R8.99 per litre

equivalent.

Unlike petrol and diesel which have an added tax, CNG has added VAT but does not have an added fuel tax.

There is some uncertainty as to whether this situation will persist, but an argument exists that if

government intends to promote the shift to CNG as a vehicle fuel for public transport, it should incentivise

gas retailers, distributors and consumers accordingly by maintaining a lower price for CNG per volume

equivalent to one litre petrol.

Taxi operators have the option to purchase the CNG conversion kits or to fund the kits through CNG.

Rothman explained that many operators cannot afford to pay the R20 000 to install the kit, therefore they

install the kits and charge the taxis the additional R1.26 per litre of gas for the recovery of the kits

(Lamprecht, 2014). According to the pilot projects and research explained above, it is calculated that on

average the conversion to CNG will earn a saving of 35 cents per km. Therefore if taxi operators purchase

the kits at R20 000 they will recover their costs in 13 months if the taxis average around 150 km per day

(which is below average) (IDC, 2013).

Taxi drivers have the option to fill with gas or petrol therefore, in order for companies to ensure taxis fill up

on gas, the drivers need to be incentivised. Companies like CNG Holdings run competitions for taxi drivers

who fill up the most litres of gas (SACN Green Transport Workshop, 2015).

15

As can be seen from the above model, an opportunity exists to achieve a return on investment in

conversion kits, while at the same time delivering savings to taxi operators due to the lower per km cost of

gas relative to petrol, even with the cost recovery and servicing built into the gas price. Furthermore, the

financial analysis conducted by the IDC (2013) concludes that purchasing new dual-fuel (CNG) taxis is a

more attractive option for the operator compared to petrol powered taxis, and that the conversion of a 5

year old taxi to CNG yields the highest cash flow savings for the operator compared to new petrol taxis.

With regards to municipalities, there is a strong case for municipalities to get actively involved in the

conversion of taxis. The main outcome of the above mentioned data is that the conversion of taxis to

natural gas is a sustainable option – both financially and environmentally. Municipalities essentially need

to kick start the process through engaging local taxi operators to incentivize the conversion. They could

either offer to fund the conversion kits – in which case municipalities will enter into an agreement with gas

companies wherein they receive a percentage of the R1.26/litre recovery cost or they could direct taxi

operators to the gas companies in which case municipality’s returns would be based on health benefits

from decreased GHG emissions in their cities. With regards to the first option of municipalities funding the

kits to taxi operators, municipalities will incur the initial cost of R20 000, and they could receive a return on

investment within 6 to 12 months, following which they will earn on every kilometer travelled. This is based

on the following assumptions:

Cost of kit = R20,000 (CNG Holdings)

Payback for funded kit = R1.26/litre (CNG Holdings)

Taxis average 200 to 300km/day (IDC, 2013, p. 63)

This provides a viable case for municipalities to approach the taxi industry, either to get actively involved

and invest in the conversion kits or to build a relation between the taxi industry and the gas companies.

There is a clear incentive for taxi owners to use gas rather than petrol, as they will save on fuel prices and

maintenance as well as earn a commission on every litre of gas filled (based on the CNG Holdings model

explained above).

2.2.2 2.2.2 Business Model Options

Where suitable CNG gas supply infrastructure exists – currently the N3 corridor – there are a range of

opportunities for municipalities to support the conversion of minibus taxis to CNG:

16

Municipalities can support the establishment through fuel distribution infrastructure along the

established taxi-corridors by identifying suitable land and fast tracking the provision of utilities for

gas refilling stations. This should be made available to private sector gas retailers at competitive

rates using a concession model. This is a relatively low risk option for municipalities but relies on

the private sector – both taxi associations and gas retailers – to drive the market for CNG taxi

conversions. Municipalities will remain as facilitators between the taxi industry and gas service

providers. Depending on the opportunity cost associated with making land available for refilling

stations as opposed to other purposes, the financial investment required is likely to be small, while

returns are likely to be in social outcomes rather than financial.

Municipalities may also choose to play a more direct role in driving the market, by investing in the

conversion of taxis. As has been demonstrated, a financial model exists that suggests that such an

investment can yield both a social and financial return. One possible route is for CNG refueling

infrastructure and taxi conversions to CNG to be undertaken as a public-private joint venture

between the municipality and gas retailers, with taxi associations as empowerment partners.

o The gas retailer would undertake to provide CNG at a defined profit margin.

o The municipality would raise development finance to fund the conversion of taxis, with the

return on investment being realised through the gas price to taxi-owners.

o Taxi associations could potentially receive a dividend based on volumes of gas sold that

could be reinvested in their members and in incentives for individual taxi-operators.

To realise this, it would probably be necessary to appoint a transaction advisor who would facilitate a

detailed feasibility study, culminating in a request for proposals issued by the municipality in partnership

with a taxi association to potential private sector partners in the gas industry.

2.3 2.3 A case for converting buses and municipal fleets to CNG

During a pilot project, an ethanol bus (Metrobus), a gas bus (Metrobus), and a diesel/gas dual fuel bus (IDC

Gas Vehicle Pilot Project) operated on urban drive cycles for over a year providing some valuable data

points for decision-makers. The focus of the pilot project was to determine the payback period and

financial viability of converting diesel buses to dual-fuel buses, rather than to analyse the lifecycle

environmental, operations, maintenance, and fuel costs of municipal buses compared to other propulsion

technology choices (IDC, 2013). The findings from this initial pilot suggested that both operational costs and

GHG emissions for dual-fuel buses are reduced.

17

Following the results of the IDC study and other studies, the cities of Johannesburg and Tshwane have

begun pilots on their municipal bus fleets. In 2014/15 Tshwane procured 40 dedicated CNG buses for the “A

Re Yeng” bus rapid transit (BRT) fleet which are due for delivery in the last quarter of 2015 calendar year.

These buses will be operating on gas and the gas tanks will be placed/ installed on the front end of the roof

for safety reasons. The overall target is to operate 30% of the entire fleet on gas as part of the City’s gas-to-

energy portfolio) (SACN Green Transport Workshop, 2015).

In July 2015, Johannesburg launched its green Metrobus fleet with 70 dual-fuel CNG buses; 40 new buses

and 30 rehabilitated and converted buses. The City announced that by June 2016 there will be 190 new

green buses on the streets of Johannesburg. This shows a commitment from municipalities to go green; to

decrease operational costs as well as GHG emissions.

With regards to municipal fleet vehicles, a study was done by SANERI in 2011 on the Toyota Hilux (pickup),

the results of which were reported by Schmidt, et.al (2012). During the study, various dual-fuel CNG

vehicles were tested and the emissions and fuel consumption in real operation on the street evaluated. The

study shows that the GHG emission savings of a converting Toyota Hilux is 47 to 50% compared to the

gasoline mix in South Africa (Schmidt, et al., 2012)

2.3.1 2.3.1 Financial Model

2.3.1.1 Municipal Bus conversions

Based on the information shared through phase 1 and 2 of this project, it was explained that the National

Renewable Energy Lab of the US Department of Energy (NREL) built the CNG model to demonstrate the

relationship between project profitability (the purchase of gas buses, gas refueling infrastructure and gas

fuel); fleet operating and fleet size parameters. The business case targets municipal governments which

operate fleets well suited to CNG vehicles, namely because they run circular routes that enable refueling

from the same station, including transit buses, school buses, an refuse trucks.

NREL also targeted municipal governments because they are well suited to take advantage of all the proven

advantages of CNG including: long-term cost effectiveness, more consistent operational costs, increased

energy security, reduced greenhouse gas emissions, reduced local air pollution, and reduced noise

pollution.

18

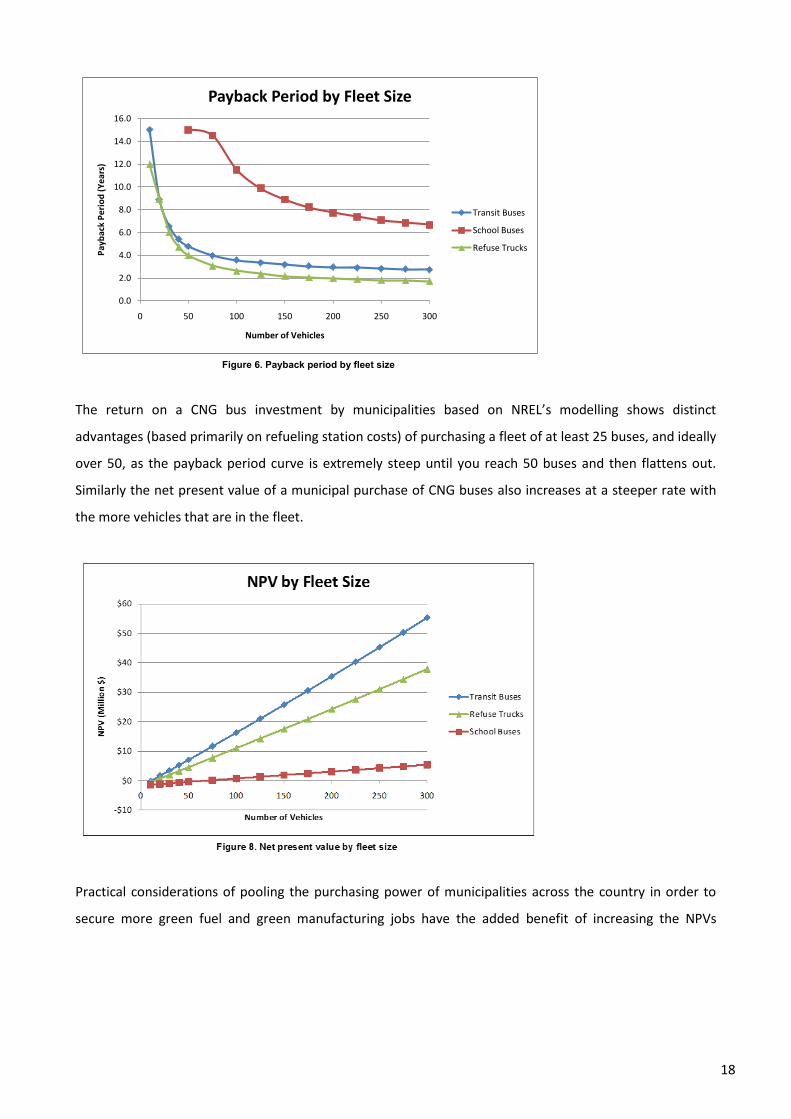

The return on a CNG bus investment by municipalities based on NREL’s modelling shows distinct

advantages (based primarily on refueling station costs) of purchasing a fleet of at least 25 buses, and ideally

over 50, as the payback period curve is extremely steep until you reach 50 buses and then flattens out.

Similarly the net present value of a municipal purchase of CNG buses also increases at a steeper rate with

the more vehicles that are in the fleet.

Practical considerations of pooling the purchasing power of municipalities across the country in order to

secure more green fuel and green manufacturing jobs have the added benefit of increasing the NPVs

12

Figure 6. Payback period by fleet size

What will my ROR be? Base-case refuse and transit projects look very profitable when judged on the basis of ROR. With

fleets as small as 25 buses, they can provide returns that are deemed acceptable by any

organization, and large fleets yield extraordinary returns. Refuse projects become more

profitable than transit projects as the fleet size increases—probably because the larger refueling

window allows increased vehicle usage without increasing fueling capacity.

School bus projects require large fleets to provide a good ROR. The ROR surpasses 6% with a

75-vehicle fleet and 10% with a 100-vehicle fleet. It then maxes out at 21% ROR, which is quite

a good investment for a municipal government.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

0 50 100 150 200 250 300

Pay

bac

k P

eri

od

(Y

ear

s)

Number of Vehicles

Payback Period by Fleet Size

Transit Buses

School Buses

Refuse Trucks

19

significantly and decreasing the payback periods of the projects. It also encourages the major metros to go

big – an approach that has higher political, financial, and operating returns.

During a pilot project prepared for the IDC (2013), the operating cost of running diesel dual fuel (DDF)

buses was compared to standard diesel buses. The project used R11.06 per litre of diesel, which was the

average diesel price for the evaluation period (August 2012 – May 2013), and R7.74 per litre equivalent

petrol as the price for the CNG, available from the Langlaagte NGV Gas filling station. The diesel equivalent

price for CNG is calculated at R 8.13.

The fuel running cost, based on the accumulated fuel consumption, for the diesel (standard) bus arrived at

was R3.97 per kilometer versus R3.19 per kilometer for the DDF bus, which indicates a saving of 78c per

kilometer. The lower cost amounts to a 19.6% reduction in the fuel running cost for the DDF bus compared

to the diesel (standard) bus. These results provide a clear business case for the conversion of municipal

buses to CNG (either dedicated or dual-fuel) and recognizes the benefits of procurement at scale.

2.3.1.2 Municipal vehicle conversion

The findings presented here are based on the SANERI 2011 test as reported by Schmidt, et.al (2012). The

following table shows the results of the tests that were conducted on a 2005 Toyota Hilux pick-up vehicle

converted to dual-fuel (the vehicle used in the trials was a carburetor feed 4-cyclinder engine):

Table 6: Fuel Consumption and CO2 emissions of the CNG pickup ‘Toyota Hilux’

Operation Cycle Fuel consumption CO2

Nm³/(100 km) l/(100 km) kWh/km g/km CNG Vehicle operation/

SANERI 11.19 - 1.11 220

Gasoline * Vehicle operation/ SANERI

- 12.65 1.13 301

Gasoline * Manufacturer data - 12.0 1.07 287

Gasoline * Vehicle operation/ Australia

- 12.34 1.10 294

Source: (Schmidt, et al., 2012)

Based on these tests, the report concluded that the fuel saving on this specific engine model is about 20%

lower that of a gasoline fueled variant. In terms of the conversion, the price of converting fleet vehicles to

CNG is R16 500. Based on this costing and the statistics provided by CNG Holdings, the payback period for

the conversion is estimated around 13 months - the same as a minibus taxi (SACN Green Transport

Workshop, 2015). Even though the cost of converting is less, because the driver averages a lot less

kilometers in a day, the payback period is still 13 months. Additionally, the pilot projects have shown that

20

converting vehicles to natural gas reduces maintenance cost and service intervals as there is no lead or

benzene content to foul the spark plugs (CNG Holdings, date unknown).

2.3.2 2.3.2 Business Model

As has been established through research undertaken during the scoping phase of the Cities Green

Transport project, most bus manufacturers are willing to set up new manufacturing plants for either

CNG/Biogas, ethanol or electric buses in South Africa for committed orders (across municipalities) of

approximately 300 buses over 3 years ramping up to at least 300 buses per year for a negotiated period of

time. During the project team’s engagement with cities, the following projections for planned orders of

new CNG/biogas buses over the next 5 to 7 years were indicated:

Table 7: Indicative targets for planned CNG/biogas bus procurement

Municipality Total 5-7 year Planned Order

Johannesburg BRT/ Metrobus 402

Cape Town BRT 320

Tshwane BRT 130

Ekurhuleni BRT 50

eThekwini BRT 60

Rustenberg BRT 25

Total 977

Source: Project Team Cities’ Consultation

It must be noted that the above planned orders only relate to direct purchases by some of the metros. It

doesn’t include the fleet replenishment plans of private bus companies, many of whom have contracts with

1.1.3 Text Box 3: Municipal vehicles going hybrid

During the SACN Green Transport Workshop, both CoT and CoJ mentioned that they are investing in

a new hybrid vehicle fleet. CoJ launched the City’s Green Fleet Programme on 19 June with 34 hybrid

vehicles. As part of the programme, the city plans to replace half of its 3 500 vehicle fleet with hybrid

and dual-fuel vehicles (City of Joburg, 2015), 35% of the fleet is planned to be converted by 2016.

CoT has as well procured 10 electric fleet vehicles which serves as the corporate fleet for City

messengers. They are now looking to partner with the private sector to implement charging points

around the City.

21

the cities. It is clear that there is a potential to justify local manufacturing of green buses thus contributing

towards job creation and skills development.

The project team have investigated the potential for the application of a transversal procurement

mechanism to which cities could sign up to, thereby aggregating demand to achieve benefits of scale and

drive down costs. An in-principle support was reached for such a mechanism from National Treasury,

Department of Transport and Department of Environmental Affairs. However, cities opted to be cautious

towards a transversal procurement citing concerns around governance and potential implications for local

accountability in relation to municipal procurement, as well as divergent technical requirements and

perspectives on appropriate technology.

While there is little cooperation between cities in terms of aggregating demand, the lead taken by Tshwane

and Johannesburg in introducing CNG into their bus fleets is commendable. It is worth replication and

expansion in support of the establishment of a green industry. There are also compelling reasons for

municipalities to consider biogas (methane from biological origins) as a potential source for gas powered

municipal vehicles. It is a local cleaner fuel with a potential to sustain the industry momentum in the

medium to long term that would have been created through CNG.

With regards to municipal fleet vehicles, the pilot projects show that municipalities would make a saving of

20% on fuel if they convert to CNG fleets, additionally, vehicle maintenance costs will be reduced and GHG

emissions decreased. We note that are purchasing new hybrid fleets, given that this report is focusing on

the conversion to natural gas, the results of the hybrid vehicle fleets were not shared, however, it is useful

to note that both CoT and CoJ have taken on hybrid vehicle fleets. While CNG tank to wheels reduce GHG

emissions by a certain percentage, electric hybrid vehicles reduce the emissions to zero – therefore, electric

hybrid vehicles would be the most environmentally sustainable option for municipal fleet.

22

1.1.4 Text Box 4: Biogas and municipal waste

Biogas, which has methane as the active component, is derived from anaerobic digestion

(decomposition in the absence of oxygen) either in landfills or in specially constructed

anaerobic digesters which can produce biogas from a wide range of organic inputs including

domestic waste, human and animal effluent, agricultural waste, as well as dedicated

feedstock crops. In the absence of biogas capture, methane vented into the atmosphere is a

significantly more potent greenhouse gas than CO2. For this reason, even where landfill gas is

not captured for use in energy and heating applications, it is flared to reduce the impact of

its emissions.

The use of landfill gas in energy applications is a key directive from the National Waste

Management Strategy, as well as being an established methodology for emissions reduction

and the generation of carbon credits.

Currently, many South African municipalities have yet to make productive use of the energy

potential of landfill gas and experience severe challenges in the treatment of human effluent

in wastewater. Both landfills and wastewater treatment plants are potentially important

sources of biogas.

Significant potential synergy exists between conversion of municipal vehicles to run on gas

and the development of a biogas industry in South Africa. Despite well-established

opportunities for biogas in the country, investment in a biogas industry has been slow to

gather momentum in the absence of guaranteed off-take agreements. Biogas as a vehicle

fuel compares favourably financially with use for electricity generation and heating where

physically proximate take-up is possible – for this reason, in many parts of the world waste

management vehicles are powered by biogas.

While small-scale biogas production is already well established through a number of pilot

and demonstration projects in South Africa, often at a household or community scale, there

is no production on an industrial scale. A large scale project that will generate 4MW of

electricity is under development at Bronkhorstpruit in Tshwane municipality, drawing on

biomass from one of the country’s largest feedlots.

23

Based on the existing momentum around CNG as a fuel for municipal buses, the synergies that exist with

biogas for municipalities in relation to waste management, and the need to achieve scale in both these

sectors to make a significant impact on GHG emissions and unlock industry value chains around green

transport, it is suggested that:

1. The SACN Green Transport Working Group continue to share information and experiences on the

rollout of gas powered buses and engage with private sector transport companies to progressively

promote opportunities for localisation of green transport technologies – including continuing to

explore the potential for cooperation between cities in aggregating demand to drive down costs.

2. In the context of the above, and taking into account the mandate of cities in relation to waste

management, it is suggested that SACN in partnership with SANEDI, DEA, DoE and the DoT seek to

develop opportunities for donor and concessional finance to support project development of a

demonstration project that makes use of biogas from municipal waste sources as a vehicle fuel,

initially for selected municipal waste vehicles as the scale of biogas production allows.

3 Way forward

Based on the results of the above business case it is evident that a case exists for the conversion of taxis to

dual-fuel, the conversion of municipal fleet vehicles to dual-fuel, and the conversion of municipal buses to

dedicated CNG or dual-fuel. This section aims to explain how municipalities can take the process forward. In

any of these cases, municipalities need to engage gas companies to understand the conditions for setting

up municipal gas pumps – as done by CoJ and CoT – or to setup general gas stations within the city. Most

gas companies have indicated that if municipalities can assist with the procurement of land on major

transport routes they would be willing to setup stations in those cities. However, for this to happen, there

needs to be an order in place for the conversion of mass taxis / vehicles / buses to CNG.

3.1 Taxi conversions

To achieve genuine scale in the conversion of taxi to dual-fuel CNG/petrol, municipalities will need to:

(1.) Work with taxi associations, private sector companies in the gas industry, and financial institutions

to raise awareness of the business case for conversion and facilitate the investments in gas

refuelling infrastructure and financing of taxi conversions needed to execute the business case.

(2.) Work with national government and municipal stakeholders to facilitate the development of an

enabling regulatory environment – in particular, ensuring that regulation is not at the expense of

24

the competitiveness of the gas price as an alternative to petrol. Currently, CNG sales to taxi

operators incur VAT, but do not have a transport fuel levy (currently R1.54 per litre) or petroleum

pipelines levy (currently R0.19 per litre) imposed on them. Introducing fuel levies of a similar size

on CNG would significantly reduce its attractiveness as an alternative to petrol.

Taxi associations are clearly the core stakeholders that need to be won over to converting to CNG. Through

the SACN platform, municipalities can arrange site visits to the Langlaagte CNG filling station with members

of their local taxi associations, and learn first-hand from taxi operators about the benefits of CNG

conversion, as well as feasibility of technology transfer to their respective areas.

Before interest is generated, municipalities must be prepared to follow through in facilitating the requisite

infrastructure. The SACN can facilitate introductions to private companies with the requisite technical

capacity, but municipalities will need to decide on their approach to the business model options outlined

earlier i.e. do they want to:

a) Play a facilitating role in an informal cross sector partnership with taxi associations and gas

companies, for instance by acting as a neutral broker and platform convenor between gas

companies and taxi associations, making suitably located land available for CNG filling stations and

fast-tracking supporting utilities; or

b) Actively drive the creation of refuelling infrastructure and financing of taxi conversions by entering

into a formal joint venture in the form of either a public private partnership (PPP) or a special

purpose vehicle (SPV) in which one or more municipalities are shareholders.

If a municipality is of the view that CNG filling stations should be regarded as municipal infrastructure – for

instance where CNG forms a significant part of the greening of municipal fleets and buses – a municipal

infrastructure PPP is a practical way of accomplishing this, and there are clear Treasury guidelines and

technical support for accomplishing these types of projects.

However, in general it is likely to be more appropriate in the long term for filling stations of privately owned

vehicles such as taxis to be privately owned and taxi conversions to be commercially financed.

Municipalities can drive the initial investment by forming a SPV with stakeholders in the gas and taxi

industries to secure the project finance for filling stations and taxi conversions. An SPV in the context of this

Business Case (rather than in context of financial securities industry) is an instrument for raising equity

finance (through shareholders) and debt finance (through loan agreements) to deliver projects – in this

case, it would likely be registered as a “Not for Profit Company – with members (NPC)”. A potential avenue

25

for pursuing initial grant funding would be registering such an SPV as a cluster with the Department of

Trade and Industries Manufacturing Competitiveness Enhancement Programme (MCEP): Cluster

Competitiveness Improvement initiative. Amongst the qualifying activities costs that are eligible for funding

and likely to be relevant are costs of developing shared infrastructure, process improvement costs, and

market research.

3.2 Vehicle conversions

Based on municipalities transport visions as laid out in their 20 to 25 year plans, transport department

would need to approach fleet management with the abovementioned vehicle fleet conversion. The

conversion will not only decrease emissions, but it will decrease municipal fuel and servicing costs. The

most feasible option would be for municipalities to add gas fuel pumps at current municipal fleet stations,

thereby decreasing the costs of implementation. Due to the work done by pilot projects explained above,

as well as by CoJ and CoT on vehicle fleet conversion, municipalities have the option of converting to hybrid

or CNG.

3.2.1 Bus conversions

The conversion of buses to CNG as has been explained becomes more efficient if the number of converted

buses is larger. This mainly is due to the cost of converting and the installing of the pumps at fleet stations.

Buses can either be converted to dedicated CNG or to dual-fuel. As both CoT and CoJ have adopted both

these conversions, it is recommended that the conversion should be based on what is the most feasible for

municipalities in the long run. Many municipalities are initiating their BRT projects and are still in the

process of ordering the buses, therefore it would be more feasible to order dedicated CNG buses from

manufacturers as is being done in Tshwane, than to convert the fleet once it arrives. It should be noted

however, that even if conversion is done on current fleets, it is still a more attractive option for

municipalities than to run on conventional petroleum fuels.

4 Conclusion

Greening transport infrastructure and services in cities is a complex enterprise, requiring strategic vision

and the application of multi-disciplinary skills and experience in an integrated approach to transport

planning. Engagement with cities confirmed existence of political will in support of green transport. The

drive behind this support is to reduce GHG emissions, improve air quality as well as to promote safe and

equitable mobility within cities. On the other hand, there is still less confidence about the technology

26

decisions in relation to greening the transport sector for maximum impact on GHG emissions and human

health.

This Business Case demonstrates that converting to natural gas will not only reduce GHG and carbon

emissions, but it will reduce municipal operational spending. The payback period for a bulk order of 50

buses or more is 5 years or less – depending on the size of the order – following which municipalities will

incur savings and healthier buses which require less maintenance. Investing in taxis which is clearly the

quickest win for municipalities, will earn returns within a year – if municipalities fund conversion kits to

taxis. Conversion of municipal fleet vehicles will earn cities direct saving on both fuel and vehicle

maintenance, and the payback period for the initial investment would be 13 months – similar to that of

taxis.

Additionally, the stakeholder engagement revealed an overall consensus that integrated planning is key to

achieving the important modal shifts from private cars to public transport and non-motorised transport.

Cities have some leverage in relation to procurement of buses and municipal fleets. The minibus taxi

industry remains a critical area for fuel switching in order to achieve significant improvements in air quality.

Private car use and minibus taxis indeed beg for immediate attention as a starting point in creating the

green industry given that they represent 57% and 3% of national fleet.

Municipalities must play a supportive and facilitating role in relation to green transport industry. There is

also an opportunity to play a proactive role by actively investing in taxi conversions to greener fuel – with

CNG, possibly supplemented by biogas, representing a market that already has significant momentum.

27

5 References

Carbon Trust, 2013?

City of Joburg, 2015. Metrobus Unveils Eco-Friendly Bus Fleet. [Online]

Available at: http://www.reavaya.org.za/news-archive/july-2015/1200-metrobus-new-green-bus-

fleet-unveiled

[Accessed 9 August 2015].

City of Joburg, 2015. Mayor Tau takes delivery of green cars. [Online]

Available at:

http://www.joburg.org.za/index.php?option=com_content&view=article&id=9802:mayor-tau-

takes-delivery-of-green-cars&catid=88:news-update&Itemid=266 [Accessed 19 August 2015]

CNG Holdings (date unknown) Accessed online at: http://www.cngholdings.co.za/faq/taxi-industry/

[Accessed 19 August 2015]

DEA. 2006. South Africa Environment Outlook: A Report on the State of the Environment. Pretoria.

Greben, H., L. M. Burke, and S. Szewczuk. 2009. Biogas, as a Renewable Energy Source, Produced

during the Anaerobic Digestion of Human Waste. Johannesburg

DEA. 2013. GHG Inventory for South Africa. Pretoria.

DoE, 2015?

IDC, 2013. Gas Vehicle Pilot Project FInal Report, Atlantis: Cape Advanced Engineering (CAE).

Jewaskiewitz, S. 2008. “Waste to Energy: Are We Ready for It in South Africa?” Waste

Management, February, 69–77.

Lamprecht, I., 2014. An alternative to rising petrol prices. [Online]

Available at: http://today.moneyweb.co.za/article?id=732231#.VcycPvmqpBd

[Accessed 9 August 2015].

Linkd, 2014. Phase 1: Local and International Status Quo report, prepared as part of the SACN

Green Transport Programme, Johannesburg, Linkd Environmental Services, Release Date: August

2014

Linkd, 2015. Phase 2: Accelerating the Transition to Green Municipal Fleets, prepared as part of the

SACN Green Transport Programme, Johannesburg, South Linkd Environmental Services, Release

date: March 2015

Linkd, 2015. Phase 3: Stakeholder Engagement Report, prepared as part of the SACN Green

Transport Programme, Johannesburg, South Linkd Environmental Services, Release date: June 2015

28

SACN Green Transport Workshop, 2015. Towards the Establsihment of a Cities Green Transport

Programmed. Johannesburg, Linkd Environmental Services.

SANEDI, 2014?

SAPIA, 2015

Schmidt, P., Weindorf, W., Wurster, R. & Zittel, W., 2012. Climate Friendly Mobility in South Africa,

Munich: Ludwig-Boljow-Systemtechnik GmbH (LBST) - an expertise for KfW.