south port annual report · south port annual report. ... liebherr hm 400 model at a $6 million ......

TRANSCRIPT

South Port annual report

Financial calendarInside front cover: Financial Calendar 1 Company Profile 2 Significant Events 3 Financial Results in Brief 4-10 Review of Operations 11 Directors’ Profiles and Photo 12,13 Corporate Governance 14 Statutory Report of Directors 15 Southern Region Production Locations 16,17 Mediterranean Shipping Company – Weekly

Container Line Servicing Bluff 18,19 Port Infrastructure 20-23 Profile – Ship Types through Bluff and their Cargoes 24 Auditor’s Report 25 Statement of Comprehensive Income / Statement of Movement in Equity 26 Statement of Financial Position 27 Statement of Cash Flows 28-46 Notes to the Financial Statements 47 Five Year Summary 48 Statutory Disclosure in Relation to ShareholdersInside back cover: Directory and Management Photo

2010 Full Year Profit Announcement Date 19 August 2010

Proxies must be lodged by 10.45 a.m. 28 September 2010

Annual Meeting – 10.45 a.m. 30 September 2010Venue: South Port Board Room, Island Harbour, Bluff

Close of Share Register for Entitlement to Final Dividend 24 September 2010

Final Dividend Payment mailed2 November 2010

2011 Interim Profit Announcement 10 February 2011

2011 Interim Dividend Payment March 2011

2011 Financial Year End 30 June 2011

contentS

Front cover: Export logs stored on Island Harbour leFt: Tanker Torea at the Tiwai Wharf with both South Port tugs in attendance

newzealand

SouthlandBluFF

CompanyPro ilef

South Port Facts

South Port new zealand ltd (South Port) is the southern most commercial port in new zealand, located at Bluff and operating on a year round, 24 hour basis. it is situated in the rich productive province of Southland which is responsible for generating a sizeable proportion of new zealand’s total exports by value. the region’s major cargo producing sites are situated within 30 to 80 km of the Port.

the Port of Bluff has been operating since 1877 while the company was formed in 1988 having taken over the assets and liabilities of the former Southland Harbour Board.

South Port was listed on the nz Stock exchange (nzX) in 1994 and has environment Southland, the region’s local government environmental agency, as its 66% majority shareholder.

owns and manages assets which have a book value of $34 million

directly employs more than 60 full time equivalent staff

is the only Southland based company listed on nzX – market capitalisation as at 30 June 2010 equates to $68 million

Handles in excess of 2 million tonnes of cargo in a normal trading year

offers full container, break-bulk and bulk cargo capability and services the following main cargoes:

import – alumina, petroleum products, fertiliser, acid, fish, stock food and cement

export – aluminium, timber, logs, dairy, meat by-products and woodchips

Has split its land-based operating resource into four main divisions – warehousing & packing, containers, cool & cold storage and dairy

Undertakes its primary port operation on a 40 ha man-made island Harbour situated at Bluff

operates a separate dedicated fuel berth at Bluff town wharf plus provides the tiwai wharf facility to nzaS under a long term licence

Services vessels carrying approx 1.0 million tonnes of cargo destined for movement across the tiwai wharf each year, of which 2/3 is raw material imports while 1/3 is finished aluminium product

Has approximately 9 ha of on-port land available for further port development or industry establishment

achieved $3.13 million profit result (2009 $4.12 million) after deducting several one-off, non-cash accounting adjustments. Underlying trading profit was favourable as a result of strong cargo and warehousing activity with pre-tax profit reflecting $7.45 million (2009: $5.68 million).

one-off deferred tax adjustments totalling $2.08 million reduced the 2010 reported profit but have no bearing on the underlying trading result of the business. these losses relate to taxation adjustments triggered by government changes to depreciation on buildings and corporate tax rates.

lifted total dividend to 17.00 cents per share (2009 – 13.50 cents) after adding back non-cash deferred tax charges recorded during the period. 2011 dividend level forecast at approximately 13.0 cents.

Cargo volume lifted by 14% or 306,000 tonnes (2009 – 1.86 million). this increase is largely attributable to uplifts in forestry sector and nzaS cargo.

t w o

Improved forestry demand driven by Chinese consumption meant that this cargo category recorded a volume gain of 182,000 tonnes (+ 177%). Forestry cargo grouping includes logs, woodchips and sawn timber.

nZaS, South Port’s single largest customer by volume, re-established its normal operating capability during the period resulting in a 104,000 tonne cargo increase (lower 2009 levels created by major transformer outage).

Containerised cargo lifted from 24,000 teU equivalents to 29,000 p.a. representing an increase of 21%. MSc weekly service continues to secure consistent support from regional importers and exporters.

upgrade of Company’s existing mobile crane committed to (June 2010) with ordering of larger capacity liebherr lHM 400 model at a $6 million cost.

new log export customer secured (nac Forest) and development of additional 1 hectare of log storage area commenced in May 2010.

Dairy warehousing volumes serviced for open Country Dairy and Fonterra, the former achieving increased production from its awarua plant.

South port and nZaS received interim arbitration award (June 2010) and proceeded to establish new terms for a licence agreement 35 year renewal period covering the provision of the tiwai wharf/access Bridge.

Cold storage division generated an improved contribution due to contracted year round utilisation plus increased storage demand.

exploration consortiums (led by exxon Mobil & oMv) obtained 12 month “drill or drop” deferrals from nz Government. Decisions on possible exploration campaigns are now expected in october 2010 & June 2011.

Solid energy / ravensdown undertook preliminary study into the potential establishment of a lignite-to-urea conversion process in Southland.

New Hyster forklift working the container pad

Signi icant Events 2009-10f

$5.2m*

80.9%

7.75c

$4.1m

$2.5m

$2.2m$2.4m

$m

5.0

4.0

3.0

2.0

1.0

0

16%

14%

12%

10%

8%

6%

4%

2%

0%

25%

20%

15%

10%

5%

0%

90%

85%

80%

75%

70%

65%

Financial Results in BriefSurpluS aFter tax

2006 2007 2008 2009 2010

t h r e e

18c

15c

12c

9c

6c

3c

0c

$m

6.0

5.0

4.0

3.0

2.0

1.0

0

$3.1m

$6.4m

$3.7m

$4.1m$4.4m

operatInG CaSH FloW

2006 2007 2008 2009 2010

$4.9m

87.8%

92.8%

88.5%

84.1%

eQuItY ratIo

2006 2007 2008 2009 2010

13.50c

9.50c

7.75c

DIVIDenDS per SHare

2006 2007 2008 2009 2010

17.00c

15.0%

9.4%

8.5%

9.4%

return on eQuItY

2006 2007 2008 2009 2010

11.4% 18.8%

14.0%

11.5%12.4%

return on aSSetS

2006 2007 2008 2009 2010

2006 2007 2008 2009 2010

23.1%

In Thousands of New Zealand dollars

2010 2009

revenue $22,937 $20,077

Surplus after tax

$3,129 $4,118

cashflow $4,942 $6,459

total assets $33,715 $31,539

total equity $27,287 $27,700

Shareholders’ equity ratio

80.9% 87.8%

earnings per Share

11.9c 15.7c

dividends declared 17.00c 13.50cper Share

net asset Backing $1.04 $1.06per Share

return on Shareholders’ 11.4% 15.0%Funds

cargo throughput 2,169 1,863(000’s tonnes)

* Restated profit with $2.08 million of one-off deferred tax adjustments added back

10,700

28,900

Mark O’Connor John Harrington

F o U r

oVerVIeW

the 2010 financial year delivered signs that the negative aspects of the Global Financial crisis were gradually subsiding. notwithstanding this assessment, South Port acknowledges that it has been a particularly testing period for a number of its customers and trading gains have been restricted to a narrow range of sectors. in South Port’s case strong cargo and warehousing activity plus the resolution of the new zealand aluminium Smelters (nzaS) licence arbitration meant that the company generated an improved pre-tax trading profit result of $7.45 million (2009 - $5.68 million).

the reported after tax profit of $3.13 million (2009 – $4.12 million) is a misleading indication of the strength of the company’s business during the past 12 months. this is due to recent Government tax changes relating to the removal of tax depreciation on buildings and the pending reduction of corporate tax rates. as a consequence of these changes South Port is required to reflect an additional $2.08 million tax charge in the 2010 year. this adjustment to profit is a one-off, non-cash accounting entry which has no impact on the company’s underlying profitability, cash flows or dividend policy.

other one-off factors reflected in the 2010 financial result include the following:

reaching a favourable agreement with nzaS over arrears and ongoing charges applicable to the tiwai wharf licence

an impairment adjustment (reduction in value) associated with the company’s existing mobile harbour crane

Foreign exchange losses linked to hedging contracts associated with the purchase of a replacement mobile harbour crane

continuing containerised cargo support by the region’s exporters and importers was evident on the MSc capricorn weekly service. cargo volume in containerised form grew by 21% increasing from 24,000 teU equivalents to 29,000 annually. recognising the need for reliable infrastructure to support this customer activity and taking into consideration that South Port operates a single mobile crane operation, in June 2010 the Board committed to replace the existing crane with a new and larger capacity liebherr lHM 400 model. a $6 million contract was entered into for this new plant and an additional heavy lift container forklift costing $700,000 was also ordered at the same time. this increased level of capital expenditure and resulting higher funding and depreciation expense will impact the company’s 2011 profit.

the other significant growth area for South Port’s business during 2010 was that of the forestry sector. tonnage in the logs/woodchips/sawn timber category lifted by 182,000 tonnes or +177% above the prior years volume.

other areas of the business which contributed positively to the bottom line included dry warehousing (dairy product) and cold storage (cheese/fish/pet food).

2008 2009 2010

bulk

number of Containers(teU equivalents)

23,800

2008 2009 2010

Breakdown of Cargo(Bulk/Break-bulk/Containers tonnage)

breAk-bulk

2008 2009 2010 2008 2009 2010

coNtAiNerS

1,200

4,900

2008 2009 2010

Containers(Vanned / Devanned)

4,900

Review of Operations

1,428,000

1,779,000

1,673,000

346,000

203,000

245,000

124,000

232,000250,000

NZASImports

34%

ForestProducts

19%

PetroleumProducts

11%Fertiliser

11%

Other 6%

Agricultu

ral

Products

4%

NZASExports

12%

ComparatIVe CarGo BreakDoWn

NZASImports

38%

ForestProducts

15%

PetroleumProducts

11%

Fertiliser12%

Other 6%

Acid 3%Agricultural Products 2%

NZASExports

13%

2009

2010

IMPORTS 62% EXPORTS 38%

IMPORTS 67% EXPORTS 33%

F i V e

Acid 3%

CarGo aCtIVItY

across all cargoes South Port registered an annual volume of 2.17 million tonnes (2009 – 1.86 million tonnes). Products to reflect volume increases included fertiliser, logs, petroleum and woodchips while improvement was recorded across a range of containerised cargo but especially in the dairy, sawn timber, fish food and general import/export categories. Smaller cargo declines occurred with stock food, molasses, pebbles and meat.

cargo volumes during the 12 months ended 30 June 2010 were also boosted by normal production capacity being re-established at the nzaS tiwai aluminium Smelter.

the nzaS capacity reduction in the prior year was caused by the substantial failure of a transformer in november 2008 which resulted in a “pot-line” having to be taken out of production. the net effect of this technical failure was a 30% reduction in nzaS’s output capability for almost 8 months of that financial year. as a consequence of nzaS reverting to normal production levels, the cargo tonnages generated by this customer increased by 104,000 tonnes during 2010.

af ter hav ing to manage severa l challenging years the forestry sector enjoyed a more buoyant trading period. logs and woodchips in particular registered sizeable volume increases. improved chinese demand for logs saw South Port’s existing storage areas fully utilised and the securing of a new export customer (nac Forest) meant that an extra 1.0 hectare of long term storage area had to be constructed on the island Harbour. in addition, eucalyptus trees planted in Southland in the early 1990’s are now available for harvest and this has boosted the volume of woodchip material being exported. Sawn

timber customers also experienced more consistent demand with this product being distributed in containerised form.

it is positive to see strong support from cargo providers who ship their goods via Bluff on the second largest container shipping operator in the world, Mediterranean Shipping company (MSc). the weekly capricorn service offers an “industry standard” frequency plus global linkages and will greatly assist South Port’s involvement and growth in the handling of containerised cargo. MSc continues to expand its presence in the new zealand market with both of its current shipping services experiencing robust demand.

open country dairy generated increased production of milk powder at its awarua plant (approximately 15 km from Bluff) during its second season of operation. this customer utilises South Port’s warehousing systems and a 4,500 m2 dedicated store located on the island Harbour to distribute its products to a variety of global markets.

Fonterra edendale marked the opening of the 2009/10 dairy season with the commissioning of the world’s largest milk powder drier. Known as ed4, the single drier can generate 27 tonnes of powder an hour when running at full capacity which translates to a seasonal production capability of 150,000 tonnes. the addition of this fourth drier means that the edendale site can now deliver a peak processing capacity of 15 million litres of milk per day. South Port continues to act as an overflow storage supplier for Fonterra in addition to providing year round cold storage for cheese product originating from the edendale plant.

the company’s cold storage division again produced an improved contribution. this was largely due to the contracted year round utilisation of the no. 2 cold store and increased storage demand arising from slower movement of consumer products such as salmon and other fish species.

InDuStrY ConSolIDatIon anD SHIppInG DeVelopmentS

Rationalisation of Shipping Services – ongoing shipping service rationalisation has been a feature of the international port landscape over the past 12 – 18 months. South Port has had discussions with several liner operators in an effort to develop additional shipping connections from Southern nz but the current economic environment is not necessarily conducive to creating such opportunities. notwithstanding this fact, nzaS has entered into a term contract with Se Shipping to distribute a manufacturing by-product to europe on a 6 weekly cycle. it is envisaged that this new service will connect with australia and South african markets before reaching europe and

thereby provide additional shipping links for Southern cargo.

LPC/Port Otago Merger Negotiations – in February 2010 lyttelton Port and Port otago announced publicly that they had committed to “detailed negotiations” on a merger opportunity. this possible action by the two port companies was first mooted as far back as late 2007. the more recent announcement marked the follow up to an initial evaluation report prepared by auckland based antipodes capital which explored the potential benefits and how a merger transaction might be structured. no further official commentary has been provided by the companies on the merger discussions although it is apparent that commerce commission approval will need to be sought if a merger transaction was to proceed.

Western Blue Highway Study – Shareholders may recall that one of the remaining funded projects under the now defunct domestic Sea-freight Fund (established by the labour Government to assist new projects involving the coastal shipping of cargo) was that of the western Blue Highway Study. initially

246

284

2008 2009 2010

Ship Calls

252

12.5

15.0

2008 2009 2010

Crane productivity(moves per hour)

15.6

S i X

two parties proceeded to negotiate an agreement relating to the ongoing provision of this infrastructure. a formal agreement was executed in august 2010 and this will serve as the charging basis for the 35 year renewal term of the licence. Both South Port and nzaS are pleased that certainty now exists over the future provision, funding and maintenance of the infrastructure covered by the long term licence.

Port Infrastructure Developments – Significant ‘capex’ outlays during the 2010 financial year related to:

the first stage of a two part paving upgrade of the container berth apron

other pav ing reconst ruc t ion associated with areas adjacent to the Marstel bulk-liquid storage terminal and warehouse no. 5

relocating the rail siding to the rear of the container pad

replacing the cooling towers in South Port’s cold storage complex

lodging a $2.2 million deposit for a larger capacity mobile crane.

the company has also continued to implement the requirements of the medium term focused asset Maintenance Plan which was developed for its major infrastructure in 2006/2007.

one additional coastal cargo rotation was potentially viable, that being a new Plymouth to nelson ro-ro shuttle concept. this scenario is being further investigated by the ports identified. the study understandably confirmed that the quantity of available coastal freight is a key determinant of viability but it also assisted the parties to better understand the costs associated with distributing coastal cargo.

otHer eVentS

NZAS/South Port Arbitration – South Port’s largest customer by volume, nzaS, receives and distributes the majority of its cargo across the dedicated tiwai wharf and access Bridge. these assets and associated port infrastructure are provided by South Port to nzaS under a long term licence (lease) agreement. this historic agreement expired in april 2008 and was renewed by nzaS for a further 35 year period effective from that date. as a result of being unable to reach agreement on an appropriate ongoing licence charge it was determined that the companies should revert to an arbitration process to resolve this impasse.

Following the receipt of the arbitrator’s interim award in early June 2010, the

driven by Port taranaki this exercise was expanded to also involve South Port, Port nelson, Ports of auckland (with emphasis on onehunga), Port of Greymouth and Port of westport.

the brief of the exercise was to capture and analyse data that may support a commercial shipping option based around cargo movements originating from or destined for the western Sea Board of new zealand. the output of the study reported during 2010 that only

Southwood Export’s wood chip stockpile on the Island Harbour

Recently purchased Hyster forklift in operation

S e V e N

$3.40

$3.30

$3.20

$3.10

$3.00

$2.90

$2.80

$2.70

$2.60

$2.50

$2.40

$2.30

$2.20

$2.10

$2.00

$1.90

$1.80

$1.70

$1.60

$1.50

SHare prICe from 1 July 2007 to 30 June 2010

200920082007 2010

SEP NOV JAN MAR MAY JUL SEP NOV JAN MAR MAY JUL SEP NOV JAN MAR MAY JUL

Hardwood Forests – as proposed in the 2009 annual report a final non-taxable distribution of approximately $91,000 was received from Hardwood Forests in the 2010 year. this payment concluded the distribution of assets and wind-up of this company.

FInanCIal

2010 Financial result (comparatives shown in brackets)

revenue from port and warehousing operations increased by 18% from last year to $22.6 million ($19.1 million).

operating profit before financing costs and tax improved by 74% to $8.2 million ($4.7 million).

net financing costs for the Group reflected an expense of $723,000 ($719,000 credit/gain due to dividend distribution from Hardwood Forests). included in the financial expense is a $636,000 foreign exchange loss associated with hedging contracts taken out over the purchase of the replacement mobile harbour crane.

the Group’s overall result was a surplus of $3.13 million ($4.12 million), which equates to a 24% reduction on the previous year – note this surplus is calculated after deducting the one-off, non-cash deferred tax adjustment of $2.08 million.

Based on the reported result, earnings per share have decreased to 11.9 cents per share (15.7 cents per share).

total shareholders equity is $27.3 million ($27.7 million) after allowing

for dividend payments during the period of $3.54 million ($2.95 million).

Group equity includes issued capital of $9.4 million ($9.4 million), which is made up of 26,234,898 ordinary shares.

total Group assets stand at $33.7 million ($31.5 million).

net tangible asset backing per share equates to $1.04 ($1.06 per share).

current assets amount to $7.6 million ($4.8 million), whereas current liabilities stand at $4.6 million ($3.8 million). this creates a net working capital position of positive $3.0 million versus $1.0 million last year.

non-current assets excluding Property, Plant and equipment stood at $15,000 ($1.5 million).

term liabilities now total $1.8 million ($0.1 million).

Property, Plant and equipment stood at $26.1 million ($25.2 million).

Changes introduced in the taxation (Budget measures) act 2010

on 20 May 2010, the new zealand Government announced a number of tax changes and these were implemented in the taxation (Budget Measures) act 2010.

the changes that will directly impact the company included:

a reduction in the depreciation rate applicable to ‘building structures’ to 0%, with effect from 1 July 2011,and

the removal of a depreciation loading for assets acquired after 20 May 2010 (under the current rules a depreciation loading increases the depreciation rate by 20% for qualifying assets, such as certain plant and equipment).

the net result of these changes will be to increase the company’s effective tax rate however this impact will be more than offset by the Government’s programmed reduction in the corporate tax rate from 30% to 28% from 2012 onwards.

the change in the depreciation rate applicable to ‘building structures’ will however result in a reduction to the tax book value of items classified as ‘building structures’ to nil for financial reporting purposes because future tax deductions will no longer be available from the financial year commencing 1 July 2011. the reduction in the company’s tax rate from 30% to 28% will also affect deferred tax balances recorded by the company.

the net effect of these deferred tax adjustments is an estimated $2.08 million increase in net deferred tax liabilities and income tax expense, resulting in a reduction in both net Profit after tax and Shareholders’ Funds. Shareholders are reminded that the deferred tax adjustments will not affect underlying profitability, cash flows or dividend distributions.

DIVIDenDS

Shareholders will be aware directors have adopted an ongoing policy of aligning South Port’s dividend flow with both its Free cash Flows (FcF) and its reported profitability. For the purpose of this policy Free cash Flows is interpreted as being annual operating cash flow less net capital expenditure in the same period. when calculating 2010 FcF, an allowance was also made for the nzaS receivable at balance date which will be settled prior to the year end dividend payment date.

e i G h t

in assessing the level of dividend payment directors’ took heed of the company’s improved profitability plus the non-cash nature of the deferred tax charge recorded in the 2010 year. accordingly the Board elected to pay a final dividend of 12.5 cents. this translates to a full year dividend of 17.0 cents (2010 – 13.50 cents). note that in the current year dividend, 4.0 cents of the total distribution relates to arrears and interest due upon settlement of the nzaS licence dispute and should therefore be deducted when assessing potential future dividend streams.

Full imputation credits will be attached to all distributions. the dividend payment represents a gross return of 9.7% (net 6.5%) based on a share price of $2.60 as at 30 June 2010.

a dividend payout ratio of 86% results for 2010 (using nPat adjusted for the one-off deferred tax charge) and the company has assessed that a distribution of approximately 90% should be targeted in the foreseeable future. Based on current budget indications the forecast dividend level for 2011 is approximately 13.0 cents per share.

(millions)

net Surplus after income tax 3.1

one-off non-cash deferred tax adjustments 2.1

restated Profit upon which 2010 dividend distribution assessed $5.2

SaFetY

South Port’s commitment to workplace safety has been enhanced over the past 18 months through the appointment of a Health & Safety co-ordinator. the function of this new role is to more actively engage with the company’s staff and contractors in areas where workplace safety can be improved.

the company also gained secondary

level accreditation for the acc workplace Safety Management Programme (wSMP) in September 2009 and maintaining this accreditation further reinforces South Port’s intention to seek continuous improvement in Health in Safety.

in addition, elements of the company’s future capital expenditure programme will have a stronger linkage to achieving South Port’s health and safety targets.

StaFF ContrIButIon

the South Port Board and Management wish to recognise the positive contribution delivered by all staff throughout the 2010 financial year. South Port is fortunate to have a flexible and competent workforce which enhances the company’s ability to meet its customers’ requirements. thanks are extended to South Port’s personnel for their diligent and consistent work output.

BoarD CompoSItIon

Mr Graham Heenan retires this year by rotation and being eligible, offers himself for re-election. Mr Gary Kirk also retires this year and has elected to step down from the Board after 6 years service. the company thanks him for his input during a period when significant strategic gains have been achieved by the business.

the company has received one valid director nomination for Mr Philip cory-wright, who is an auckland based strategic adviser.

enVIronment

the company ’s operat ions were undertaken throughout the year in accordance with all existing resource consent conditions. South Port’s primary environmental responsibilities are subject to two different planning instruments; the invercargill district Plan administered by the invercargill city council and the Southland regional Plan which is administered by environment Southland.

in the past 12 months the company had no significant new capital projects that impacted on the environment.

CommunItY anD reGIonal aSSIStanCe

the sponsorship of a number of local sporting and cultural groups is part of a long-term commitment to support the community and region in which South Port operates. organisations that received sponsorship assistance over the past financial year included:

Bluff coastguard Bluff Hill/Motupohue environment

trust – pest eradication programme Bluff Maritime Museum Bluff oyster & Seafood Festival

Bluff rugby club Bluff Yacht club Bluff schools, Bluff Promotions and

various other sporting organisations rugby Southland

South Port continued its primary sponsorship of the Southland export Forum providing financial assistance to administer the forum and facilitate the holding of a number of events. in addition, the company will assist with the funding of the bi-annual Southland export awards dinner scheduled to be held in early September 2010.

Further, the company ’s ongoing scholarship assistance comprises both community and staff categories, with scholarship being awarded this year to tane campbell and thomas Hildebrand. tane is studying towards a certificate in Mechanical engineering (level 2) at Sit in invercargill and has a long term goal of becoming a Marine engineer. thomas is undertaking a Marine Biology degree at the University of canterbury.

enerGY SeCtor

Oil & Gas Exploration – Seismic activity was completed over the 2007/2008 summer months by the two largest consortiums who secured exploration licences in the Great South Basin. the consortium consisting of exxonMobil and todd energy engaged contractor westernGeco to undertake its seismic activity while the consortium headed up by oMv Group assigned wavefield inseis the responsibility of collecting its seismic information.

during the last quarter of calendar 2009 both the exxonMobil consortium and the oMv consortium sought and received from the new zealand Government 12 month deferrals to comply with their exploration licence conditions. what this means is that exxonMobil has until october 2010 to commit to an exploration campaign in Great South Basin while oMv has until July 2011 to do likewise.

exxonMobil said that it would be seeking interest from other potential partners. currently the exploration licence interest is held 90% by exxonMobil and 10% by todd energy. the main reason for deferral put forward by oMv was the additional time needed to gather and interpret extra seismic data plus plan a potential exploration campaign. linked to this statement was oMv’s action to engage Singapore-based reflect Geophysical to complete an additional 2,900 km of seismic mapping in January and February 2010.

whilst there are no assurances that South Port will secure future oil and gas industry activity, it is useful to restate several advantages that Bluff is able

Open Country Dairy’s Awarua Plant

N i N e

to provide over its competitors when it comes to meeting the requirements of an exploration base:

Bluff was selected as the base for previous Great South Basin exploration

South Port can offer extensive lay down storage areas directly on the port

the refuelling of support vessels and the provision of diesel supplies for rig operations are more easily accessible than other ports (note support vessels normally require draft of 7 – 8 metres which can be comfortably provided at Bluff Port)

a wide selection of dedicated service berths are available

South Port has established expertise handling project and break-bulk cargoes

the Southland region has a more extensive engineering resource as a result of companies servicing the nzaS aluminium smelter and the meat processing, dairy and forestry industries over several decades

local government in the region also has a reputation of being willing to try harder to address the needs of new commercial ventures while still meeting the requirements of their local stakeholders.

Stavanger, Norway Exercise – Shareholders may recollect that the formation of the Southland energy consortium (Sec) in 2007 was an initiative driven by South Port and venture Southland. this entity is made up of key regional businesses and organisations who could deliver services to those parties wishing to undertake sizeable energy projects in Southland.

Being mindful of the opportunity that energy resources represent for the region, a Sec delegation, which included South Port management, visited the norwegian oil and gas service hub of Stavanger in late november 2009. the delegation was hosted by the Greater Stavanger economic development Unit and gained a valuable insight into the main strategies deployed to attract oil/gas participants to that region plus the infrastructure necessary to support the resulting activity.

Following the Stavanger exercise, Sec concluded that Southland must continue to plan for development of potentially significant energy reserves located within the province or immediately offshore. active promotion to international oil/gas companies and central government will continue to be a feature of this planning work.

Development of Southland’s Lignite Resource – Solid energy and ravensdown announced in late September 2009 that the two companies would undertake a joint study into the viability of establishing a lignite-to-fertiliser conversion plant in Southland. with an estimated establishment cost of $1.5 billion such a plant would be capable of producing up to 1.2 million tonnes of nitrogen fertiliser (urea) annually. the 2 million tonnes of lignite material for this annual production would be sourced from Solid energy’s large lignite resources in eastern Southland.

if it is determined that such a process is viable the development could result in export of urea fertiliser as well as supplying domestic farming needs. this type of development could also be the

forerunner to a much larger project to produce synthetic diesel from the same extensive lignite resources.

Solid energy and ravensdown expect to complete the initial study later in 2010 when they will decide whether to proceed to the next stage of a feasibility exercise. Following engineering design, and subject to consenting and financing, construction could start by 2014, and the plant could be operational by late 2016.

in addition to evaluating the merits of a lignite-to-fertiliser plant, Solid energy is also trialling the manufacture of coal briquettes in Southland. it has recently shipped 500 tonnes of Southland lignite to the USa for commercial trials at a colorado based drying plant. Solid energy has entered into a joint venture with USa based Gtl energy ltd, to investigate the feasibility of building a briquette plant in eastern Southland. the briquette system involves a mechanical process to extract moisture from the coal thereby enhancing the thermal value.

Should the briquette plant proceed, it would be the first of its kind in new zealand and process an estimated 100,000 tonnes of lignite a year. a decision to advance the briquette development would be partly based on the likely demand from Solid energy’s South island industrial and commercial customers. a viable process could also create potential export opportunities for the briquette product in the future.

Coal Seam Gas – l&M energy (previously l&M Petroleum) continue to actively develop coal seam gas opportunities in Southland. in June 2010 the company announced an agreement with H w richardson Group to investigate

Longest vessel to visit the Port, MSC Brasilia

t e N

pricing, potential new industry establishment and electricity demand in the region

wind Prospect cwP nz ltd is also working up a proposal to develop a wind farm at Slopedown 15 Km east of wyndham. the site would consist of 50 towers with a maximum generation of 150 Mw of electricity. a resource application is expected to be lodged in late 2011 with construction potentially targeted for 2012.

outlook

the company highlighted in its interim report that the new zealand economy contained a sense of fragility and that it was likely to take some time before full confidence is restored to international markets . th is pos i t ion remains unchanged and will have a bearing on the primary industry exports generated in Southland. the domestic marketplace is also beginning to show greater signs of strain that were not necessarily apparent during the height of the Global Financial crisis.

it would be fair to say that at this time it is difficult for any commentator to accurately predict the likely direction of global economic activity in the medium term. what is clear is that new zealand, particularly the Southern part of the country, remains in a more favourable position then many other regions around the world. demand for forestry, dairy and other agricultural goods is still relatively strong and this coupled with nzaS production should underpin the cargo levels passing through the Port of Bluff.

despite the challenging global conditions that presently exist the company looks forward to providing appropriate distribution infrastructure and to being of service to both existing and future customers. South Port will continue to

work with various companies connected with potential energy related projects including the targeted conversion of Southland’s 6 billion tonnes of recoverable lignite reserves into other more viable products. the company’s directors and Management maintain the view that the Port of Bluff is located in a unique part of the world and that the future still offers considerable upside for the increased storage and movement of cargo.

all known factors and assumptions suggest an estimated tax-paid profit range of $3.50 million to $3.90 million is a probable outcome for the 2011 financial year. this profitability estimate takes into account the increased funding and depreciation expenses associated with the $6 million replacement of the mobile harbour crane. assuming that the above profit level is achieved, shareholders should expect a total dividend payout level in the order of approximately 13.0 cents. as in the past an update of the earnings outlook will be provided by the company at the time of releasing its interim result.

J.a. HarrinGton

Chairman

M.P. o’connor

Chief Executive

2,500,000

2,000,000

1,500,000

1,000,000

500,000

0

1 – 1993 9 month period due to change in financial year end2 – 2009 drop in tonnage due to 30% decrease in NZAS throughput attributable to a pot-line outage

1

2

1922 1925 1928 1931 1934 1937 1940 1943 1946 1949 1952 1955 1958 1961 1964 1967 1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009

HIStorIC traDe FIGureS (tonneS) 1922-2010

the feasibility of delivering automotive lnG. in addition, industry analysts are suggesting that the dairy sector could potentially utilise this energy source either as industrial heat/electricity or automotive fuel.

l&M energy also holds several sizeable coal and lignite extraction licences in Southern nz and remains interested in the potential that exists to convert lignite into synthetic diesel.

Wind-farm Project Timing – Previous shareholder communications have outlined that there are two regional wind-farm projects currently in the planning stage.

trustPower ltd has obtained resource consents from the Gore district council to build a wind farm at Kaiwera downs, east of Gore. the consents allow for the installation of up to 240 Mw of electricity or a maximum of 83 towers. it is expected that this wind farm would be developed over a 2 to 3 year period should the project become viable.

Factors impacting viability (and therefore timing) include exchange rates, wind turbine availability, sector

HMNZS otago on maiden voyage arrives at Bluff

e l e V e Ne l e V e N

Directors' ProfJoHn artHur HarrInGton c.a., aFinstdChairman

Mr Harrington is a company director, Business consultant and trustee. He provides business and financial advice to a number of companies, and also acts as a director for a number of South island based private companies. Previously he was a practicing chartered accountant for a period of 40 years.

rex tHomaS CHapman llB

Mr chapman is a Senior litigation and commercial Partner in invercargill law Firm cruickshank Pryde.

rICk CHrIStIe crSnz, MSc (Hons), aFinstd

Mr christie is a company director based in wellington. He is currently a director and chairman of a number of public and private companies. He has also held a number of government appointments and was a chief executive for many years prior to becoming a professional director. He was recently made a companion of the royal Society of new zealand.

tHomaS mcCuISH FoGGo

Mr Foggo is based in invercargill and is the Southland Manager for Sanford ltd. He has held senior management positions and directorships in the Seafood industry for over 27 years and has for the past 13 years been a director of live lobster Southland 1995 ltd. He is also a Government appointed director of invercargill airport ltd.

GraHam DouGlaS Heenan B.com, aFinstd, FnziM

Based in christchurch, Mr Heenan is chairman of dB South island Brewery ltd, Heller tasty ltd, dairyworks ltd and Hanmer Springs thermal Pools & Spa. He is a director of intercity Group ltd and is a past director of the Port of timaru ltd, canterbury district Health Board, and the taB. Mr Heenan also acts as a consultant to several companies.

GarY JoHn kIrk

Mr Kirk, who resides in riversdale, Southland is currently involved in property development and building industry consulting. in addition to agri-cultural sector experience, his previous professional associations include involvement on the Southland education Property Board and Southland Business development Board and as a director of invercargill airport ltd.

Directors and Chief Executive with the Ranfurly Shield, from left:

• thomas Foggo• rex chapman• John Harrington• Gary Kirk• Mark o'connor• rick christie• Graham Heenan

iles

t w e l V e

the Board of South Port new zealand limited is committed to ensuring that the company adheres to best practice governance principles and maintains the highest ethical standards. the Board believes that good governance is based on a set of principles and behaviours that provide a clear basis for the company’s everyday activities to ensure transparency, fairness and recognition of the interests of South Port’s stakeholders.

Following a review of its governance practices the Board adopted a code of corporate Governance. the code has been developed after considering contemporary best practice and principles contained in the new zealand Stock exchange corporate Governance Best Practice code issued in october 2003 and the Port companies act 1988.

CoDe oF etHICS

the company expects its employees and directors to maintain high ethical standards. a code of ethics has been adopted as part of the corporate governance framework and is monitored by the Board. the company’s code of ethics has been published and made available to all directors and staff. this key corporate governance document is available on the company’s website (www.southport.co.nz).

the code of ethics addresses, amongst other things:

conflicts of interest; receipt of gifts; corporate opportunities; confidentiality; expected behaviours; delegated authority; director responsibilities; and reporting issues regarding

breaches of the code of ethics, legal obligations and other policies of the company.

reSponSIBIlItIeS oF tHe BoarD

the business and affairs of the company are managed under the direction of the Board of directors. the South Port Board is collectively accountable to shareholders for the performance of the company. directors, in carrying out their

responsibilities, undertake to act in the best interests of the company, its shareholders and its other stakeholders in accordance with applicable law.

Key responsibilities of the Board include:

to review and approve the strategic, business and financial plans prepared by management and to develop a depth of knowledge of the company’s business so as to understand and question the assumptions upon which such plans are based;

to monitor the company’s performance against its approved strategic, business and financial plans;

to review the company’s code of ethics from time to time;

to select and appoint (and, if appropriate, remove from office) the chief executive, determine his/her conditions of service and monitor his/her performance against established objectives;

to review the company’s remuneration policy at least annually; and

to monitor South Port’s regulatory and legislative compliance and risk management processes.

the Board delegates management of the day-to-day affairs and management responsibilities of the company to achieve the strategic direction and goals determined by the Board.

BoarD CompoSItIon

at present, there are six independent directors on the Board including a non executive chairman. the biography of each Board member is set out in the “directors’ Profiles” section of this annual report.

the size and composition of the Board is subject to the limits imposed by South Port’s constitution and in accordance with the provisions of the Port companies act 1988. the constitution requires the Board to comprise of a minimum number of six directors. Under the nzX listing rules the Board is required to maintain at least two independent directors.

Pursuant to the company’s constitution, one third of the

Corporate Governancedirectors retire by rotation at each annual Meeting, but are eligible for reappointment by shareholders.

the Board conducts regular performance reviews to consider the appropriate mix of skills required by the Board to maximise its effectiveness and its contribution to the company.

auDIt CommIttee

the audit committee provides the Board with assistance in fulfilling their responsibilities to shareholders, the investment community and others for overseeing the company’s financial statements, financial reporting pro-cesses, internal accounting systems, financial controls and South Port’s relationship with its independent au-ditors.

the committee is governed by an audit committee charter adopted by the Board in august 2004. the Board regularly reviews the performance of the committee in accordance with the charter.

the committee comprises of three independent members of the Board of directors.

the committee chairman, also appointed by the Board, cannot also be the chairman of the company. rex chapman, a commercial lawyer is the audit committee chairman. at least one member of the committee must have an accounting or financial background; both John Harrington and Graham Heenan are or have been members of the new zealand institute of chartered accountants.

directors’ attendance at Meetings – 1 July 2009 to 30 June 2010

total Meetings 1 10 2

r.G. Bettle – 1 –

r.t. chapman 1 10 2

r.G. M. christie – 8 –

t. M. Foggo 1 9 –

J. a. Harrington 1 10 2

G. d. Heenan 1 9 2

G. J. Kirk 1 10 -

ann

ual

Mee

ting

Boa

rd

Mee

ting

aud

itc

omm

ittee

t h i r e e N

SHareHolDer CommunICatIon

South Port seeks to ensure its shareholders are appropriately informed on its operations and results, with the delivery of timely and focused communication, and the holding of shareholder meetings in a manner conducive to achieving shareholder participation.

to ensure shareholders have access to relevant information the company:

Provides a website which contains media releases, current and past annual reports, dividend histories, notices of meeting and other information about the company,

Makes available printed half year and annual reports and encourages shareholders to access these documents on the website and to receive advice of their availability by email,

Publishes press releases on issues/events that may have material information content that could impact on the price of its traded securities,

issues additional explanatory memoranda where circumstances require, such as explanations of dividend changes and other explanatory memoranda as may be required by law,

Maintains regular contact with leading analysts and brokers who monitor the company’s activities.

Shareholder meetings are generally held at the company’s place of business (Bluff) at a time which best ensures full participation by shareholders.

Full participation of shareholders at the annual Meeting is encouraged to ensure a high level of accountability and identification with the company’s strategies and goals. Shareholders have the opportunity to submit questions prior to each meeting and senior management and auditors are present to assist in answering any specific queries raised. there is also an opportunity for informal discussion with directors and senior management for a period after the meeting concludes.

SenIor manaGement remuneratIon

the Board is responsible for reviewing the remuneration of the company’s senior management in consultation with the chief executive of the company.

the remuneration packages of senior management consist of a mixture of a base remuneration package and a variable remuneration component based on relevant performance measures.

the remuneration policy for senior management is designed to attract, motivate and retain high quality employees who will enable the company to achieve its short and long term objectives.

a general and wider disclosure of senior management and other staff remuneration is included in the “employee remuneration” section set-out in the Statutory information section of this annual report, where the company has disclosed in various escalating remuneration bands the number of employees and former employees whose remuneration, including benefits, exceeds $100,000.

rISk manaGement

effective management of all types of risk (financial and non-financial) is a fundamental part of the company’s business strategy. the audit committee is responsible for overseeing risk management practices and works closely with Management, external advisors and the company’s auditors to ensure that risk management issues are properly identified and addressed.

the company has a separate risk Management committee which meets annually to review changes to the risk profile of the business and to consider ways of mitigating additional risks identified. a director currently sitting on the audit committee is appointed to the risk Management committee as a Board representative.

ContInuouS DISCloSure

in accordance with the nzX listing rules, the company is required to disclose to the market matters which could be expected to have a material effect on the price or value of the company’s shares. Management processes are in place to ensure that all material matters which may require disclosure are promptly reported to the Board through established reporting lines. Matters reported are assessed as and when required by the nzX listing rules, advised to the market. the chairman and chief executive are responsible for communications with nzX and for ensuring that such information is not provided to any person or organisation until nzX has confirmed its release to the market.

all material announcements are posted on the company’s website www.southport.co.nz.

Ultimate Goal “South Port

New Zealand limited will be the best

distribution cost option for all Southern region importers and exporters

through the delivery of innovative solutions.”

Key Objectives To increase customer usage of South Port and

improve customer satisfaction. To make the best use of South Port’s resources

and develop the assets of Bluff Harbour. To improve returns to shareholders and create

positive value. To achieve differentiation in the market

and gain competitive advantage over other operators in the transport sector.

To assist the establishment of new industry and the growth of existing businesses in the southern region.

F o U r e e N

Statutory Report of Directorsthe directors have pleasure in submitting their 2010 report and Financial Statements.

principal activities the company is primarily engaged in the commercial operation of the Port of Bluff. there has been no significant change in the nature of the company’s business during the year.

accounting period the financial statements are for the 12 month period from 1 July 2009 to 30 June 2010.

resultsthe company recorded a surplus for the period of $3,129,000.

Disclosure of Share Dealing by Directors directors acquired no additional equity securities in the company since the date of the last annual Meeting.

Dividend the directors have declared an ordinary dividend of $4,460,000 for the period ended 30 June 2010 including the final dividend amount of $3,279,000 payable in november 2010.

Directors and officers liability Insurance the company has arranged directors and officers’ liability insurance with vero liability insurance ltd. this cover insures directors against liabilities to other parties that may arise from their positions as directors. the insurance does not cover liabilities arising from criminal actions or any legal action brought by the company’s majority shareholder.

remuneration of Directorsdirectors’ remuneration for the 12 month period ended 30 June 2010 was as follows:

J.a. Harrington $47,500r.G. Bettle* $16,850(resigned October 2009)r.t. chapman $26,500r.G.M. christie $20,000(appointed October 2009)t.M. Foggo $26,500G.d. Heenan $26,500G.J. Kirk $26,500

*includes retiring allowance

no other benefits have been provided by the company to a director or in any other capacity. no loans have been made by the company to a director nor has the

company guaranteed any debts incurred by a director.

Directors’ Shareholdingcurrent beneficial shareholding held by directors:

J.a. Harrington 2,333G.J. Kirk 1,000

remuneration of employeesSection 211(1)(g) of the new zealand companies act 1993 requires disclosure of remuneration and other benefits, including redundancy and other payments made on termination of employment, in excess of $100,000 per year, paid in respect of the current year by the company to any employees who are not directors of the company.

Number ofRemuneration Employees

$100,000 - $110,000 1$141,000 - $150,000 1$161,000 - $170,000 2$191,000 - $200,000 3$261,000 - $270,000 1

the chief executive officer’s employment contract is reviewed annually by the Board. it is not a fixed term contract.the remuneration of senior management is reviewed annually and is determined in a transparent, deliberate and objective manner.

notice and pause provisionsthe company has adopted “notice and pause” provisions in its constitution.

accounting policiesthere were no changes in accounting policies during the period. all policies are consistent with those applied in the previous year.

audit Committeethe company has a formally constituted audit committee comprising Messrs r.t. chapman (chairman), J.a. Harrington and G.d. Heenan.

it is the role of the audit committee to review the company’s financial statements and announcements, liaise directly with the company’s auditors and review the company’s accounting policies, practices and related matters.

auditor’s remunerationduring the year $35,616 was paid to the company’s auditors, wHK, for audit services carried out as agent for the controller and auditor-General.

the company also paid $3,813 to the auditors for advice and guidance on other matters. this did not compromise the independence of the auditors.

Interest registerthe company maintains an interest register in which particulars of certain transactions and matters involving the directors are recorded. entries in the interests register must in turn be disclosed in the annual report. no material transaction entries were recorded in the interests register for the period 1 July 2009 to 30 June 2010.

Disclosure of InterestPursuant to Section 140 of the companies act 1993, directors have disclosed interests in the following entities with which the company conducts or may conduct business from time to time:

Mr R.T. Chapman PositionBright wood nz ltd SolicitorJ. crooks & Sons ltd SolicitorPrime range Meats ltd SolicitorSouthland veneers ltd Solicitortransport rentals ltd Solicitor

Mr R.G.M. ChristieSolnet Solutions ltd adviser

Mr T.M. FoggoBarnes oysters ltd directorBluff oyster Management co. ltd directorinvercargill airport ltd directorlive lobster Southland 1995 ltd directorSanford ltd Branch Manager

Mr J.A. HarringtonBrazier Scaffolding ltd directorPrint central ltd director

Mr G.D. Heenanintercity Group ltd director

Mr G.J. Kirk nil

J.A. HARRINGTONChairman of Directors

G.D. HEENANDirector

Dated 19 August 2010

F i F e e N

9

13

8

2

KilOMetRes fROM Bluff

1 Craigpine timber . . . . . . . . . . . . . . . . . . 60 NZ Growing Media . . . . . . . . . . . . . . . . 60 Winton stock feed . . . . . . . . . . . . . . . . 60 2 Quality foods . . . . . . . . . . . . . . . . . . . . . 30 stabicraft Marine . . . . . . . . . . . . . . . . . 30 Prime Range Meats . . . . . . . . . . . . . . . 33 3 Ballance Agri Nutrients . . . . . . . . . . . . 15 south Wood export . . . . . . . . . . . . . . . . 15 south Pacific Meats . . . . . . . . . . . . . . . 15 Open Country Dairy . . . . . . . . . . . . . . . . 15 4 NZ & Aus. Pet food ingredients . . . . . . . . . . . . . . . . . . . . . . . 0 Dynes stockfood . . . . . . . . . . . . . . . . . . . 0 sanford Bluff . . . . . . . . . . . . . . . . . . . . . . 0 southfish . . . . . . . . . . . . . . . . . . . . . . . . . 0 NZAs tiwai smelter . . . . . . . . . . . . . . . 30 5 Dongwha Patinna NZ . . . . . . . . . . . . . . 70 Alliance Mataura Plant . . . . . . . . . . . . 75 6 Pyper’s Produce. . . . . . . . . . . . . . . . . . . 45 Alliance lorneville Plant . . . . . . . . . . . 40 Alliance Makarewa Plant . . . . . . . . . . 45 7 silver fern farms Kennington Plant . . 38 Blue sky Meats . . . . . . . . . . . . . . . . . . . 55 southland Veneers . . . . . . . . . . . . . . . . 38 Niagara sawmilling . . . . . . . . . . . . . . . . 38 8 fonterra edendale . . . . . . . . . . . . . . . . . 65 9 silver fern farms Gore Plant . . . . . . . . 80 10 lindsay & Dixon . . . . . . . . . . . . . . . . . . . 88 11 silver fern farms Balclutha Plant . . 145 12 fonterra stirling . . . . . . . . . . . . . . . . . . 145 13 silver fern farms Mossburn Plant . . 118 14 Procure Cement . . . . . . . . . . . . . . . . . . 195

4

2

15

10

14

1

4

5

6Balclutha

lumsden

Winton

te Anau

Queenstown

Mossburn

tuatapere

invercargill

GoreMataura

edendale

bluff

stewartisland

73

tapanui

1112

Southern Region Production Locations

naPa Service vessel, Positive Passion, at the South Port-owned tiwai wharf.

F i F e e N

Sines

Trans-shipment to USA

Jebel Ali

Ad Dammam Bandar Abbas

Durban

Capetown

Mediterranean Shipping Company - Weekly Container Line Servicing Bluff

S i X e e N

SERVICE OVERVIEWNOUMEASydney–Brisbane–Noumea–Sydney

CHEETAHSingapore–Port Louis–Durban–Capetown

FALCONSingapore–Bandar Abbas–Jebel Ali–Ad Dammam

kiwi Sydney–Melbourne–Nelson–Auckland–Tauranga–Lyttelton–Wellington–New Plymouth–Sydneyl

PANDA Melbourne–Sydney–Brisbane–Kaohsiung–Chiwan–Hong Kong–Melbourne

CAPRiCORN Sydney–Bluff–PortChalmers–Lyttelton–wellington–Napier–Tauranga–Brisbane–Singapore–Jakarta–Fremantle–Melbourne–Sydney

EURO Sydney–Melbourne–Adelaide–Fremantle–Singapore–Colombo–Jeddah–Gioia Tauro–La Spezia–Felixstowe–Antwerp–Le Havre–Montoir–Valencia–Fos–La Spezia–Naples–Pointe de Galets (Reunion)–Port Louis–SydneywALLAByFremantle–Melbourne–Sydney–Brisbane–Yokohama–Osaka–Busan–Qingdao–Shanghai–Ningbo–Fremantle

Valencia

Montoir

Felixstowe Antwerp

La Spezia Naples

Gioia Tauro

Jeddah

Port Louis Pointe de Galets

(Reunion)

Colombo

Le Havre

Fos

Bluff

Noumea

Trans-shipment to USA and

South America

Napier

Mediterranean Shipping Company - Weekly Container Line Servicing Bluff

S e V e N e e NS e V e N e e N

Ningbo

Shanghai

Qingdao

Busan Yokohama

Osaka

Port Chalmers

NewPlymouth

Lyttelton

Wellington

Tauranga Auckland

Nelson

Chiwan Hong Kong Kaohsiung

TrAnS-ShipmenT porTSTo USA/SoUTh AmericA• Sines • chiwan

Colombo

Singapore

Jakarta

Adelaide

Melbourne

Sydney

Brisbane Fremantle

3

4

8

910

11

12

13

14 15

16

1819

20

24

21

port infrastructure7

21

e i G h e e N

1 island Harbour – comprises 40 ha, 10 shipping berths

2 Vacant land for Development – available for future growth

3 town Wharf – petroleum product discharge, bunkering

4 Fishing boat Piers – 72 inshore fishing boat berths

5 r&D office

6 Administration building

7 log Storage

8 cold Stores complex – 39,000m3 of storage capacity in 3 cold/cool stores

9 Wood chip Stockpile10 Syncrolift Dry Docking for

Vessels – boat construction and repair facility11 Mobile Harbour crane – liebherr lHM 320 (heavy lift capacity 100

tonnes) Dry Warehouses:12 No.1 — 2,000m2 sanford Bluff13 No.2 — 1,400m2 Cement storage14 No.3 — 3,300m2 Packing and

devanning store15 No.3A — 4,500m2 Open Country Dairy

product storage16 No.3B — 3,300m2 transit and dairy

storage17 No.4 — 5,900m2 Dynes stockfood

product storage18 No.5 — 5,500m2 fonterra product

storage19 No.6 — 1,500m2 NZ & Australian Pet food ingredients20 Dedicated container Servicing

Pad21 bulk Storage Facilities –

storing caustic soda, sulphuric acid, molasses and tallow

22 rail Marshalling Yard23 island Harbour Access bridge24 entrance channel

1

5

6

7

17

22

port infrastructure2

23

N i N e e e N

CEMENT MILk POWDER

SAWN TIMBER ALuMINIuM INGOT

FISH

containers are a metal box structure of standard design in which cargo

can be stowed, coming in many forms, including: ventilated,

insulated, refrigerated, flat rack, open top, bulk liquid, dry bulk and

typically in either 20 or 40 foot lengths.

Mediterranean Shipping company's vessel MSc Nederland entering Port

containerShip types through bluff and their cargoes

PEBBLES

t w e N t y

cargoes carried on a ship constructed to transport liquids, such as petroleum, in bulk.

coastal oil logistics chartered vessel, Torea, berthed at Bluff

WORkS INFRASTRuCTuRE TANk(BITuMEN)

Ballance Agri-Nutrients Tank Farm(SuLPHuRIC ACID)

Pacific Terminals Tank Farm(TALLOW AND MOLASSES)

MOBIL OIL TANk FARM(JET, DIESEL, PMS RMS)

GREENSTONE BuNkER TANkS(MARINE GAS OIL)

Mobil Oil Tank Farm(JET, DIESEL, PREMIuM/REGuLAR MOTOR SPIRIT)

Greenstone Bunker Tank Farm(MARINE GAS OIL)

tankerWorks Infrastructure Tank

(BITuMEN)

Ship types through bluff and their cargoes

t w e N t y o N e

Marstel Terminals Tank Farm(CAuSTIC SODA)

cargo moved in bulk form, such as alumina (dry bulk) or

diesel (bulk liquid).

LOGS (RADIATA PINE AND DOuGLAS FIR) FERTILISER

STOCk FOOD ALuMINA

bulkShip types through bluff and their cargoes

Pacific Basin's bulk carrier, Tiwai Point arriving at Bluff

(RADIATA PINE AND EuCALYPTuS)WOOD CHIPS

t w e N t y t w o

SCRAP METAL

General cargo, as opposed to cargo in containers. also referred to as conventional cargo. can include cargo in packages, pallets or bulk form (dry or liquid). large objects, such as those shown and project cargo for the Province also fall into this category.

FISH

TRANSFORMER

TANkS

Ship types through bluff and their cargoes

Mitsui oSK lines vessel, Rakiura Maru, at Bluff

break-bulkALuMINIuM BuLk BAG CARGOES

GREEN SAWN TIMBER & BILLET

t w e N t y t h r e e

t w e N t y F o U r

AUDIT REPORTTO THE READERS OF SOUTH PORT NEW ZEALAND LIMITED AND GROUP’SFINANCIAL STATEMENTS FOR THE YEAR ENDED 30 JUNE 2010

the Auditor-General is the auditor of South Port New Zealand limited (the company) and group. the Auditor-General has appointed me, Kenneth Gordon Sandri, using the staff and resources of whK South NZ, to carry out the audit of the financial statements of the company and group, on her behalf, for the year ended 30 June 2010.

Unqualified Opinionin our opinion: − the financial statements of the company and group on pages 25 to 46:

− comply with generally accepted accounting practice in New Zealand; − comply with international Financial reporting Standards; and− give a true and fair view of:

− the company and group’s financial position as at 30 June 2010; and− the results of operations and cash flows for the year ended on that date.

− Based on our examination the company and group kept proper accounting records.the audit was completed on 19 August 2010, and is the date at which our opinion is expressed.the basis of our opinion is explained below. in addition, we outline the responsibilities of the Board of Directors and the Auditor, and explain our independence.

Basis of Opinionwe carried out the audit in accordance with the Auditor-General’s Auditing Standards, which incorporate the New Zealand Auditing Standards.we planned and performed the audit to obtain all the information and explanations we considered necessary in order to obtain reasonable assurance that the financial statements did not have material misstatements, whether caused by fraud or error.Material misstatements are differences or omissions of amounts and disclosures that would affect a reader’s overall understanding of the financial statements. if we had found material misstatements that were not corrected, we would have referred to them in our opinion.the audit involved performing procedures to test the information presented in the financial statements. we assessed the results of those procedures in forming our opinion.Audit procedures generally include:— determining whether significant financial and management controls are working and can be relied on to produce complete and

accurate data;— verifying samples of transactions and account balances;— performing analyses to identify anomalies in the reported data;— reviewing significant estimates and judgements made by the Board of Directors;— confirming year-end balances;— determining whether accounting policies are appropriate and consistently applied; and— determining whether all financial statement disclosures are adequate.we did not examine every transaction, nor do we guarantee complete accuracy of the financial statements.we evaluated the overall adequacy of the presentation of information in the financial statements. we obtained all the information and explanations we required to support our opinion above.Provision for unforeseen repairs and maintenancein forming our unqualified opinion, we considered the recognition, presentation and disclosure of the provision for unforeseen repairs and maintenance in the statement of financial position and note 20 in our view, the provision does not meet the definition of a liability and it should not be recognised as such. rather, equity should be increased by the amount of the provision. however, the amount involved is not material to the financial statements as a whole.

Responsibilities of the Board of Directors and the Auditorthe Board of Directors is responsible for preparing the financial statements in accordance with generally accepted accounting practice in New Zealand. the financial statements must give a true and fair view of the financial position of the company and group as at 30 June 2010 and the results of operations and cash flows for the year ended on that date. the Board of Directors’ responsibilities arise from the Port Companies Act 1988 and the Financial reporting Act 1993. we are responsible for expressing an independent opinion on the financial statements and reporting that opinion to you. this responsibility arises from section 15 of the Public Audit Act 2001 and section 19 of the Port Companies Act 1988.

Independencewhen carrying out the audit we followed the independence requirements of the Auditor-General, which incorporate the independence requirements of the institute of Chartered Accountants of New Zealand.whK South NZ has provided other guidance to the value of $3813 and also through an associated entity, Janet Copeland law, for employment law Services to the value of $372. other than this, and in our capacity as auditors, we have no relationship with or interests in the company or any of its subsidiaries.

Kenneth Gordon SandriwhK South NZon behalf of the Auditor-Generalwellington, New Zealand

WHK South NZ

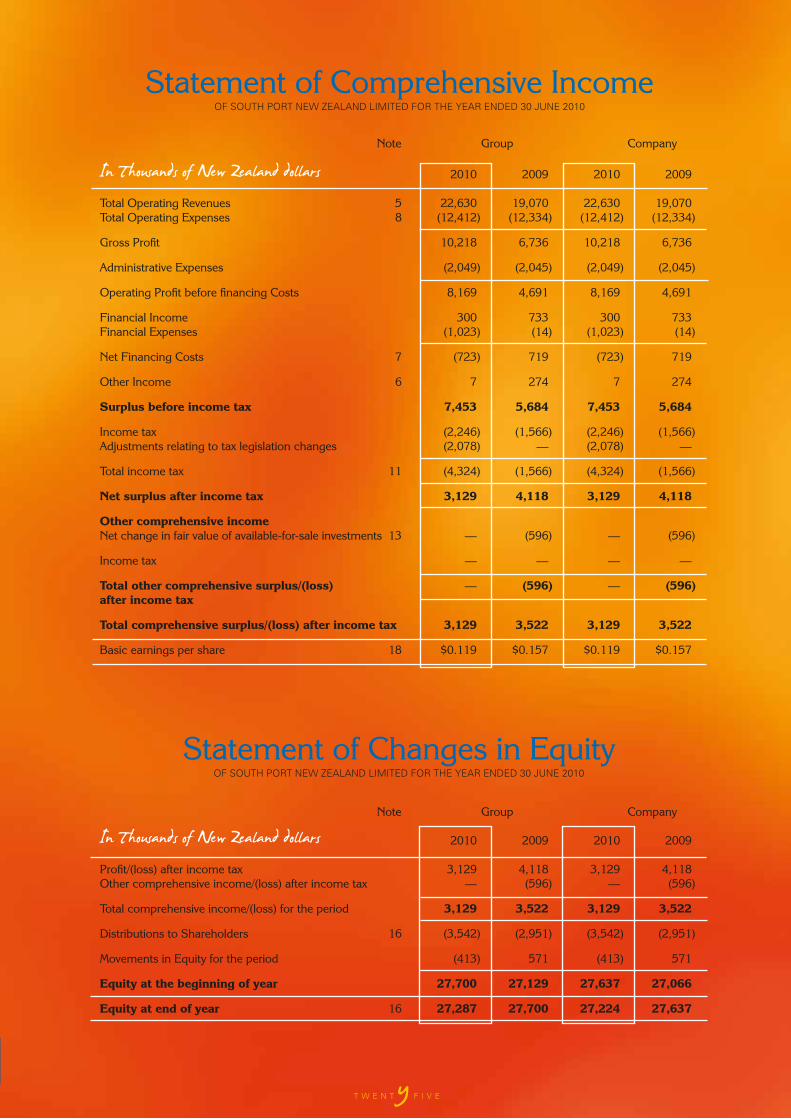

Statement of comprehensive incomeoF SoUth Port New ZeAlAND liMiteD For the yeAr eNDeD 30 JUNe 2010

note Group company

In Thousands of New Zealand dollars 2010 2009 2010 2009

total operating revenues 5 22,630 19,070 22,630 19,070total operating expenses 8 (12,412) (12,334) (12,412) (12,334)

Gross Profit 10,218 6,736 10,218 6,736

administrative expenses (2,049) (2,045) (2,049) (2,045)

operating Profit before financing costs 8,169 4,691 8,169 4,691

Financial income 300 733 300 733 Financial expenses (1,023) (14) (1,023) (14)

net Financing costs 7 (723) 719 (723) 719

other income 6 7 274 7 274

Surplus before income tax 7,453 5,684 7,453 5,684

income tax (2,246) (1,566) (2,246) (1,566)adjustments relating to tax legislation changes (2,078) — (2,078) —

total income tax 11 (4,324) (1,566) (4,324) (1,566)

net surplus after income tax 3,129 4,118 3,129 4,118

other comprehensive income net change in fair value of available-for-sale investments 13 — (596) — (596)

income tax — — — —

total other comprehensive surplus/(loss) — (596) — (596) after income tax

total comprehensive surplus/(loss) after income tax 3,129 3,522 3,129 3,522

Basic earnings per share 18 $0.119 $0.157 $0.119 $0.157

Statement of changes in equityoF SoUth Port New ZeAlAND liMiteD For the yeAr eNDeD 30 JUNe 2010

note Group company

In Thousands of New Zealand dollars 2010 2009 2010 2009

Profit/(loss) after income tax 3,129 4,118 3,129 4,118other comprehensive income/(loss) after income tax — (596) — (596)

total comprehensive income/(loss) for the period 3,129 3,522 3,129 3,522

distributions to Shareholders 16 (3,542) (2,951) (3,542) (2,951)

Movements in equity for the period (413) 571 (413) 571

equity at the beginning of year 27,700 27,129 27,637 27,066

equity at end of year 16 27,287 27,700 27,224 27,637

t w e N t y F i V e

Statement of Financial PositionoF SoUth Port New ZeAlAND liMiteD AS At 30 JUNe 2010

t w e N t y S i X

note Group company

In Thousands of New Zealand dollars 2010 2009 2010 2009

total eQUitY 16 27,287 27,700 27,224 27,637

non-cUrrent aSSetS Property, plant and equipment 12 26,068 25,226 26,068 25,226 investments 13 15 15 15 15 deferred tax asset 11(d) — 1,522 — 1,503

total non-current assets 26,083 26,763 26,083 26,744

cUrrent aSSetS cash 14 696 1,780 664 1,755 trade and other receivables 15 6,936 2,996 6,936 2,996

total current assets 7,632 4,776 7,600 4,751

total assets 33,715 31,539 33,683 31,495

non-cUrrent liaBilitieS employee provisions 20 56 51 40 36 deferred tax liability 11(d) 1,456 — 1,475 — other 23 300 — 300 —

total non-current liabilities 1,812 51 1,815 36

cUrrent liaBilitieS current borrowings 19 1,950 — 1,950 — trade and other payables 22 1,613 2,511 1,707 2,602 Provisions 20 692 633 628 578 other 23 361 644 359 642

total current liabilities 4,616 3,788 4,644 3,822

total liabilities 6,428 3,839 6,459 3,858

total net aSSetS 27,287 27,700 27,224 27,637

net asset backing per share $1.04 $1.06 $1.04 $1.05

on behalf of the BoardDated 19 August 2010

chairman of directors director

note Group company

In Thousands of New Zealand dollars 2010 2009 2010 2009

caSH FlowS FroM oPeratinG activitieScash was provided by (applied to): receipts from customers 18,887 18,778 18,887 18,778 Payments to suppliers and employees (12,273) (12,006) (12,282) (12,006) dividends received 92 557 92 557 interest received 10 87 10 87 interest paid (79) (14) (79) (14) income taxes paid (1,765) (969) (1,763) (968) net goods and services tax paid 70 26 70 23

net cash flow from operating activities 26 4,942 6,459 4,935 6,457

caSH FlowS FroM inveStinG activitieScash was provided by (applied to): Proceeds from disposal of other investments — 200 — 200 Proceeds from disposal of non-current assets 26 2,073 26 2,073 acquisition of other non-current assets (3,958) (4,095) (3,958) (4,095) Foreign exchange Gains/(losses) (501) 148 (501) 148 acquisition of shares/investments (1) — (1) — net cash used in investing activities (4,434) (1,674) (4,434) (1,674)

caSH FlowS FroM FinancinG activitieScash was provided by (applied to): dividend paid (3,542) (2,951) (3,542) (2,951) drawdown/(repayment) of borrowings 1,950 (150) 1,950 (150)

net cash used in financing activities (1,592) (3,101) (1,592) (3,101)

net increaSe (decreaSe) in caSH Held (1,084) 1,684 (1,091) 1,682 add cash at beginning of year 1,780 96 1,755 73

total CaSH at enD oF Year 14 696 1,780 664 1,755

Statement of cash FlowsoF SoUth Port New ZeAlAND liMiteD For the yeAr eNDeD 30 JUNe 2010

t w e N t y S e V e N

1 reportInG entItY

South Port new zealand limited (the “company”) is a company domiciled in new zealand, registered under the companies act 1993 and listed on the new zealand Stock exchange (“nzX”). the company is an issuer in terms of the Financial reporting act 1993.

the consolidated financial statements of South Port new zealand limited as at and for the period ended 30 June 2010 comprise the company and its subsidiary awarua Holdings ltd (together referred to as the “Group”).

South Port new zealand ltd is primarily involved in providing and managing port services and warehousing services.

2 BaSIS oF preparatIon

(a) Statement of Compliance

the financial statements have been prepared in accordance with new zealand Generally accepted accounting Practice (GaaP). they comply with new zealand equivalents to international Financial reporting Standards (nz iFrS), and other applicable Financial reporting Standards, as appropriate for profit-oriented entities. these financial statements comply with international Financial reporting Standards (iFrS).

the financial statements were approved by the Board of directors on 19 august 2010.

(b) Basis of measurement

the financial statements have been prepared on the historical cost basis except for the following:

• f i nanc ia l i ns t ruments a re measured at fair value

the methods used to measure fair values are discussed further in note 4.

(c) Functional and presentation Currency

these financial statements are presented in new zealand dollars ($), which is the company’s functional currency. all financial information presented in new zealand dollars has been rounded to the nearest thousand.

(d) Use of Estimates and Judgements

the preparat ion o f f inanc ia l statements requires management to make judgements, estimates

and assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses. actual results may differ from these estimates.

estimates and underlying assumptions are reviewed on an ongoing basis. revisions to accounting estimates are recognised in the period in which the estimate is revised and in any future periods affected.

there were no est imates and assumptions that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year.

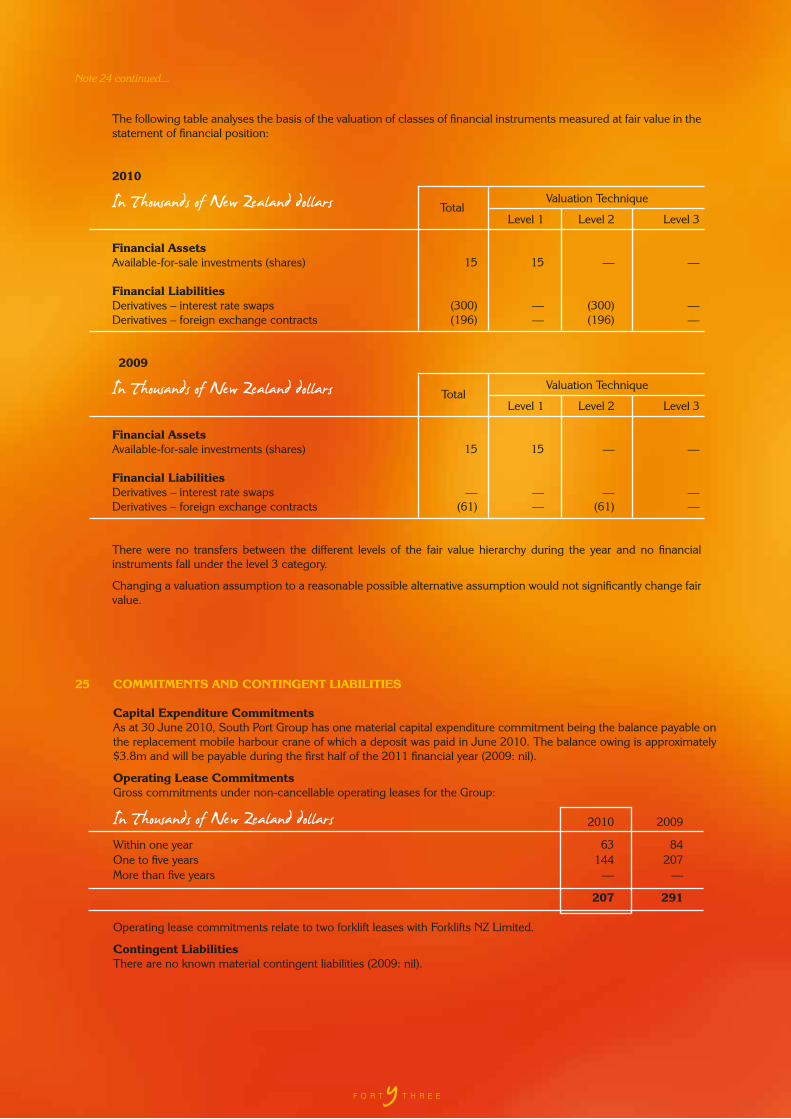

in particular, information about significant areas of estimation uncertainty and critical judgements in applying accounting policies that have the most significant effect on amounts recognised in the financial statements are as detailed below:

• Provisions (note 20)

• commitments and contingent liabilities (note 25)

• Financial instruments (note 24)

3 SIGnIFICant aCCountInG polICIeS

the accounting policies set out below have been applied consistently to all periods presented in these financial statements, and have been applied consistently by Group entities.

certain comparative amounts have been reclassified to conform with the current year’s presentation.

(a) Basis of preparing Group Financial Statements

the Group financial statements include the parent company and its subsidiary accounted for using the purchase method. all significant inter-company items and transactions are eliminated on consolidation. in the parent company financial statements, investments in subsidiaries are stated at cost.

on acquisition of a subsidiary, fair values are assigned to their assets and liabilities. any excess of cost of acquisition of a subsidiary over the fair values assigned (being goodwill) is written off in the year of acquisition or amortised over the period to benefit from the investment.

where the cost of acquisition of a subsidiary is less than the fair values assigned (being a discount) this discount is applied to the reduction of the fair value of the non-monetary assets of the acquired company. Such a discount is then reflected in the Group income statement when non-monetary assets (property, plant and equipment) are realised through reduced depreciation charges.

(b) Foreign Currency