southeast asia tech investment - cento ventures our inaugural southeast asia tech investment report,...

TRANSCRIPT

Southeast Asia tech investment

H1 2017

ABOUT CENTO VENTURES

2

Cento Ventures is a venture capital firm focused on technology startups

building products and services emerging from the digital transformation of

Southeast Asia.

We are based in Singapore and backed by a team well experienced in

internet business. We operate three funds that invest across industries

through a disciplined, well researched approach to locate talent and teams

concentrating on new opportunities sweeping through the ASEAN region.

Our investments are guided by these three principles:

Sectors ready for digital transformation

We believe that there is a great opportunity for technology to solve some of

the inefficiencies present in emerging markets. However, technology alone

does not digitise industries. Most of our investments apply innovative

business models to industries that are set in their ways, using technology as

an enabler.

Early stage, but with proof points

Cento Ventures aims to be the first institutional investor in most of our deals.

We believe this helps us establish a solid relationship with the founder, and

influence the strategic direction of the company. Our investments are most

frequently at Series A and we usually lead the round. We maintain a realistic

approach to investment and exit valuations, one that is driven by data we

gather on venture capital deals in Southeast Asia.

Expansion to multiple countries

Cento Ventures seeks to help our founders build large digital companies that

are leaders in their industry or category. In a fragmented region like

Southeast Asia, operating across multiple countries is almost inevitable. We

look for founding teams that share this ambition and focus our support on

making their expansion easier. We have a suspicion that great companies

born in one emerging market have an opportunity to replicate their success

across many others.

Cento Ventures is convinced that the opportunity exists for Southeast Asian

entrepreneurs to build transformational digital companies. Learn more about

us at digitalmedia.vc or our Facebook or Linkedin pages.

Introduction

INTRODUCTION

4

Cento Ventures has been tracking data on digital investment activity in Southeast Asia for a

number of years. In our inaugural Southeast Asia tech investment report, covering the first

half of 2017, we have decided to share some of the highlights of our data.

We hope this helps establish a clearer picture of how Southeast Asia’s tech ecosystem is

maturing, where investment is going, and where gaps still remain. We plan to update the

report on a regular basis to show how the landscape is changing over time. In future, it would

be interesting to extend the research to cover a variety of more qualitative matters, such as

the availability of talent, and we look forward to working with partners who can help us

achieve this.

The headline story of Southeast Asia is the continued growth in technology investment. A

record amount of $2.3B was invested during the first half 2017 over more than 140 deals,

compared to $2B in H2 2016 and $1.4B in H1 2017. This suggests a healthy, and growing,

interest in the potential for Southeast Asia’s tech startups. We estimate that this amount may

more than double for the second half, based on a number of large deals that were announced

in July.

A closer look at the data reveals key features, some of which have been present for a while,

that underlie the headline numbers:

- Concentration of capital in a few companies

2017 sees a continuation of ‘mega-deals’ as later stage companies capture ever larger

investments. Fully 81% of funding in H1 2017 was captured by just 3 investments (Go-Jek,

Garena and iFlix). This trend is expected to continue for the second half of 2017.

Interestingly, the earlier stages of capital raising look more stable. The number of deals in

earlier stage deals seems consistent with 2016. The amount invested at each stage is also

relative stable compared to the last couple of years.

Pre-Series A deals average out at US$0.5M per deal, Series A at slightly more than US$2M

per deal, and Series B at US$9M per deal.

- Diversification of capital by country

Excluding the mega-deals (since they skew the data), Indonesia and Singapore-based

startups account for about half of the capital invested in Southeast Asia. This is a decline

from earlier years when startups in these countries accounted for up to three quarters of

investment.

The same split is reflected in the number of deals done: 50% to Indonesia and Singapore

companies, 50% to the rest of the region. Of the rest, Vietnam and Malaysia appear to be

experiencing stable or growing interest, while investment has cooled off in Thailand and the

Philippines. However, a single half year period does not make a trend, so we will look again

once the rest of 2017 has played out.

- Diversification of capital by sector

A few familiar sectors continue attract the most capital – of course these are the sectors in

which the mega-deals are occurring. These are online retail (e-commerce and C2C) and

local services (various on-demand services and urban transportation), along with ‘multi-

vertical’ companies (often a mix of the other two).

Other sectors in which multiple deals are happening and significant amounts of capital

flowing into include financial services, entertainment and travel. We see growing investor

interest in a range of industries such as real estate, healthcare, and enterprise software, as

startups emerge to address issues in many traditional, and still largely offline, parts of

Southeast Asia’s economy. We expect more attention to go toward B2B models as

entrepreneurs explore opportunities to apply technology throughout various industry value

chains.

INTRODUCTION

5

- Funding gaps and fund specialisation

The existence of gaps in the funding available for early stage startups has been observed by

others. It does seem to be the case that Southeast Asian startups raise Series B funding at a

lower rate than those based in the US or Europe. However, we are talking about a less

mature funding environment, and time will tell whether this ‘corrects’ itself over time. Certainly

we are seeing VC funds being raised that target this stage, and the availability of capital for

Series B rounds will likely improve.

We also see the emergence of sector specific funds, including our own new fund, called STV,

which invests exclusively in startups within the online fashion/apparel sector. The fund will

seek out ambitious founders who are using disruptive technology to build winners in this

exciting segment. To help realise this, we have partnered with Start Today, the US$10B

company behind Japan’s leading online branded fashion retailer Zozotown.

- Exits are by M&A

The majority of liquidity events for startups and early stage investors continue to come from

sale of shares either to later stage investors and/or to strategic acquirers, while liquidity

through IPOs remains a rarity. Despite a relatively small sample set (we don’t always know

the details of exit price or percentages liquidated), it seems that a ‘very good’ exit in the

region is priced somewhere in the region of US$200M.

Based on 2017 so far, that may well increase by the time we have a full year’s worth of data

to look at.

Acquirers generally fall into one of two buckets – either they are corporates (e.g. REA, Seek,

Telenor) or larger tech companies (e.g. Alibaba, Grab, Go-jek). In both cases their motivation

for buying Southeast Asia’s startups appear to include geographic extension (e.g. Alibaba) or

acquisition of complementary technology or teams (e.g. Go-jek).

Buyers are typically from within the wider APAC region, although there are isolated cases

from all parts of the world. The largest number of deals are made by Singapore-based

acquirers, while Chinese buyers have spent the most.

Overall it’s been an encouraging first half to 2017, and the outlook for the full year is very

healthy. Various challenges still remain: ensuring sufficient capital is available to high-quality

startups based in the less invested parts of Southeast Asia, and possibly also to startups

based beyond the region’s capital cities (we don’t have a breakdown of the data yet); bridging

funding gaps that still remain; building more successful exit stories that help inspire more

founders to start companies and attract more investors to the ASEAN region. And that’s only

on the financial side of things: better connectedness within the region and to other tech hubs;

more availability of talent; and more equality of opportunity are all topics that merit attention,

perhaps in future editions.

The aim of this report is to show how far Southeast Asia tech has developed during the time

that Cento Ventures has been investing, and perhaps to highlight some of the continuing

challenges. We hope it helps anyone, whether they are startup founders, investors, or

policymakers, achieve a better understanding of the landscape that we all operate within.

Thanks

Mark Suckling Laphat Thantiphipop

Investment landscape

RECORD INVESTMENT IN H1 2017. $7B FORECAST FOR FY 2017

7

Capital invested, US$M and deals done, #

2017 has seen record amounts of internet

technology related investment in Southeast

Asia. Investment activity measured by the

number of deals has declined since its peak in

2015.

We assume the amounts deployed in the

second half of the year will be significantly

higher due to already known large funding

rounds disclosed during July 2017. e.g Grab’s

US$2B, Tokopedia’s US$1.1B, and Traveloka

$500M round.

Notes:

The numbers include various events that while

count as investment in technology company,

are considered non-VC, e.g TenX ICO, Grab-

Honda project financing, Lippo Group funding

of Matahari Mall.

Some early stage incubator funded

companies are not yet included in 2017 H1

data

Source: Cento research

$251 $212 $218 $1,079 $1,172 $929 $1,418 $2,030 $2,267 $4,900

42

54

95

113

214

197192

140 143

160

2013 H1 2013 H2 2014 H1 2014 H2 2015 H1 2015 H2 2016 H1 2016 H2 2017 H1 2017 H2e

Capital invested # of deals

LARGEST DEALS GROW, SMALLEST DEALS COOLING OFF

8

US$0.5M or smaller deals** US$0.5M+ to $2M deals US$2M+ to $5M deals

US$5M+ to $10M deals US$10M+ to $50M deals US$50M+ deals

Source: Cento research

*Data only includes deals which are considered a VC investment

**Various incubator funded early stage companies are yet to be

included in 2017 H1 data

Capital invested, US$M

Deal #

$9 $25 $44 $30 $15

38

104

202

135

78

0

50

100

150

200

250

0.0

10.0

20.0

30.0

40.0

50.0

2013 2014 2015 2016 2017F

$31 $56 $143 $120 $109

29

51

112

9590

0

20

40

60

80

100

120

-

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

2013 2014 2015 2016 2017F

$41 $64 $130 $117 $166

12

17

40

33

46

0

10

20

30

40

50

-

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

180.00

2013 2014 2015 2016 2017F

$44 $109 $134 $204 $191

7

15

19

28 28

0

5

10

15

20

25

30

-

50.00

100.00

150.00

200.00

250.00

2013 2014 2015 2016 2017F

$87 $102 $443 $470 $238

4 4

1921

10

0

5

10

15

20

25

-

100.00

200.00

300.00

400.00

500.00

2013 2014 2015 2016 2017F

$415 $682$2,317 $5,440

3

4

6 6

0

1

2

3

4

5

6

7

-

1,000

2,000

3,000

4,000

5,000

6,000

2013 2014 2015 2016 2017F

AVERAGE INVESTMENT AT PRE-A IS $0.5M, A IS $2M, B IS $9M

9

Deals done by series, # Average deal size by series, $M

57

116

244

174

51

22

51

108

89

66 5

13

27

24

10

4

9

14

25

7

2013 2014 2015 2016 2017 H1

Pre-A A B C+

$0.7$0.5 $0.5 $0.7 $0.5

$2.7

$2.0

$2.8$2.3 $2.1

$4.2

$6.0

$11.5

$8.9 $8.8

2013 2014 2015 2016 2017

Pre-A A B

2017 H1

Source: Cento research

DEALS ARE SPREAD ACROSS THE REGION. 50% TO ID AND SG

10

Source: Cento research

Country of origin is defined as where the company was founded and where it is

believed to generate its core revenues

In 2017, companies based in Indonesia and

Singapore captured about half of investment

activity in Southeast Asia, both in terms of

proceeds and number of deals. The

remainder is split relatively evenly across the

rest of the region, with a slight skew towards

Malaysia.

On deals done, this is fairly consistent with

the last few years data. On capital invested,

the distribution is becoming less skewed to

Indonesia and Singapore-based companies.

The data excludes Garena (Sea), Go-jek,

Grab and Lazada investments since it heavily

skews the proceeds distribution. In the cases

of Garena, Grab and Lazada it is also rather

misleading to allocate their funding to a

particular country, since they are truly

regional.

Share of capital invested by country

Share of deals done by country

20%

39%

30%

50%

29%

54%

34%

35%

25%

29%

9%

8%

12%

10%

30%

2%

8%

14%

8%

4%

10%

8%

4%

4%

6%

5%

3%

5%

3%

3%

2013

2014

2015

2016

2017H1

23%

24%

23%

27%

24%

35%

41%

29%

31%

31%

14%

9%

20%

13%

14%

9%

10%

10%

12%

10%

10%

7%

10%

8%

14%

9%

8%

8%

9%

6%

2013

2014

2015

2016

2017H1

Indonesia Singapore Malaysia Thailand Vietnam Philippines

DEALS IN MY & VN ARE SOLID. TH & PH COOLED OFF

11

Capital invested and deals done in Malaysia

Capital invested and deals done in Vietnam

Capital invested and deals done in Thailand

Capital invested and deals done in Philippines

$18 $31 $110 $118 $253

1216

75

3936

$-

$50

$100

$150

$200

$250

$300

2013 2014 2015 2016 2017F

0

10

20

30

40

50

60

70

80

$4 $28 $125 $90 $34

8

18

37 36

26

$-

$50

$100

$150

$200

$250

$300

2013 2014 2015 2016 2017F

0

10

20

30

40

50

60

70

80

$20 $31 $39 $54 $34

913

39

25

36

$-

$50

$100

$150

$200

$250

$300

2013 2014 2015 2016 2017F

0

10

20

30

40

50

60

70

80

$10 $10 $45 $37 $21

8

15

3227

16

$-

$50

$100

$150

$200

$250

$300

2013 2014 2015 2016 2017F

0

10

20

30

40

50

60

70

80

Source: Cento research

THERE IS DIVERSIFICATION ACROSS INDUSTRY SECTORS

12

Deals done by sector, US$M

While online retail (e-commerce and

C2C) and local services (on-demand

services and urban transportation),

along with ‘multi-vertical’ companies

(often a mix of the two), remain most

heavily funded categories. other

categories are attracting more attention.

Financial services, entertainment and

travel sectors have for some time, and

are continuing to attract investment.

There is also emerging interest in other

categories like real estate, healthcare,

and enterprise software.

2013 2014 2015 2016 2017H1

Multi-vertical $53 $270 $770 $1,750

Local services $1 $328 $372 $776 $9

Retail $71 $175 $219 $814 $75

Travel $34 $12 $78 $238 $13

Financial Services $37 $7 $127 $67 $37

Payments and Remittances $19 $26 $86 $114 $18

Entertainment / Non-Gaming $1 $4 $52 $83 $95

Food $8 $32 $69 $48 $6

Retail backend & infrastructure $0 $6 $27 $38 $67

Comms & communities $4 $23 $16 $80 $0

Healthcare $0 $12 $24 $43 $36

Demand management $2 $6 $85 $12 $3

Logistics $1 $13 $33 $53 $6

Enterprise software & services $6 $13 $28 $29 $19

Advertising $6 $15 $26 $17 $3

Real estate $4 $2 $9 $15 $26

Education $0 $7 $12 $7 $10

Employment $3 $4 $11 $10 $4

Entertainment / Gaming $4 $8 $11 $7 $0

Others $0 $1 $0 $0

Source: Cento research

% of companies raising seed round that raised follow-on rounds

13

Source: Cento research

https://www.cbinsights.com/research/venture-capital-funnel-2/

http://www.atomico.com/news/the-state-of-european-tech-2016

IS THERE A SERIES B GAP?

We tracked Southeast Asian startups

that announced seed funding between

2013-2015 and compare the rate of

follow-on fundraising with data from the

US and Europe. It appears that startups

in Southeast Asia have been able to

attract Series A funding at a broadly

similar rate to more mature

ecosystems.

A funding ‘gap’ seems to remain at

Series B however, where follow-on

rates are lower. However our cohort

data on Southeast Asia is more recent,

and therefore there is potential for rates

of follow-on funding to increase.0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Seed Follow-on round 1 Follow-on round 2 Follow-on round 3

SE Asia 2013 SE Asia 2014 SE Asia 2015 US 2008-2010 Europe 2010

FUND FORMATION APPEARS TO SLOW IN 2016

14

Southeast Asia focused funds formed and AUM*, US$M

Source: Cento research

*in cases using best estimates

$561 $814 $1,752 $588

25

35

52

34

0

10

20

30

40

50

60

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2013 2014 2015 2016

AUM Number of funds formed

$357

$210

$30 $28$20 $18 $12 $10 $10 $5

Formation Group Vertex Ventures Beacon Ventures (K-Bank)

East Ventures VSV Fund SeedPlus (JungleVentures)

STV (Cento) Intudo Ventures Shiftventure Innovatube

15

SOME NEW (AND FAMILIAR) NAMES WITH NEW FUNDS IN 2017

Southeast Asia focused funds launched during 2017 by AUM, US$M

Source: Cento research

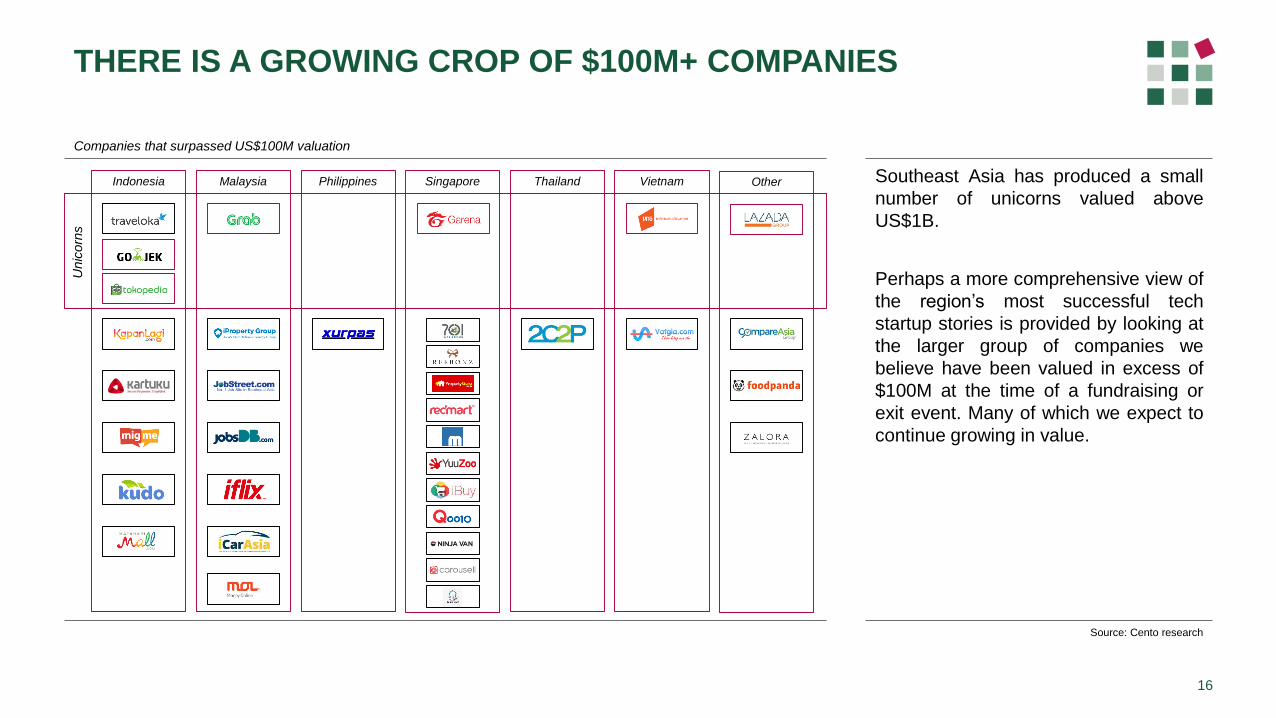

THERE IS A GROWING CROP OF $100M+ COMPANIES

16

Companies that surpassed US$100M valuation

Source: Cento research

Southeast Asia has produced a small

number of unicorns valued above

US$1B.

Perhaps a more comprehensive view of

the region’s most successful tech

startup stories is provided by looking at

the larger group of companies we

believe have been valued in excess of

$100M at the time of a fundraising or

exit event. Many of which we expect to

continue growing in value.

Unic

orn

s

Indonesia Malaysia Philippines Singapore Thailand Vietnam Other

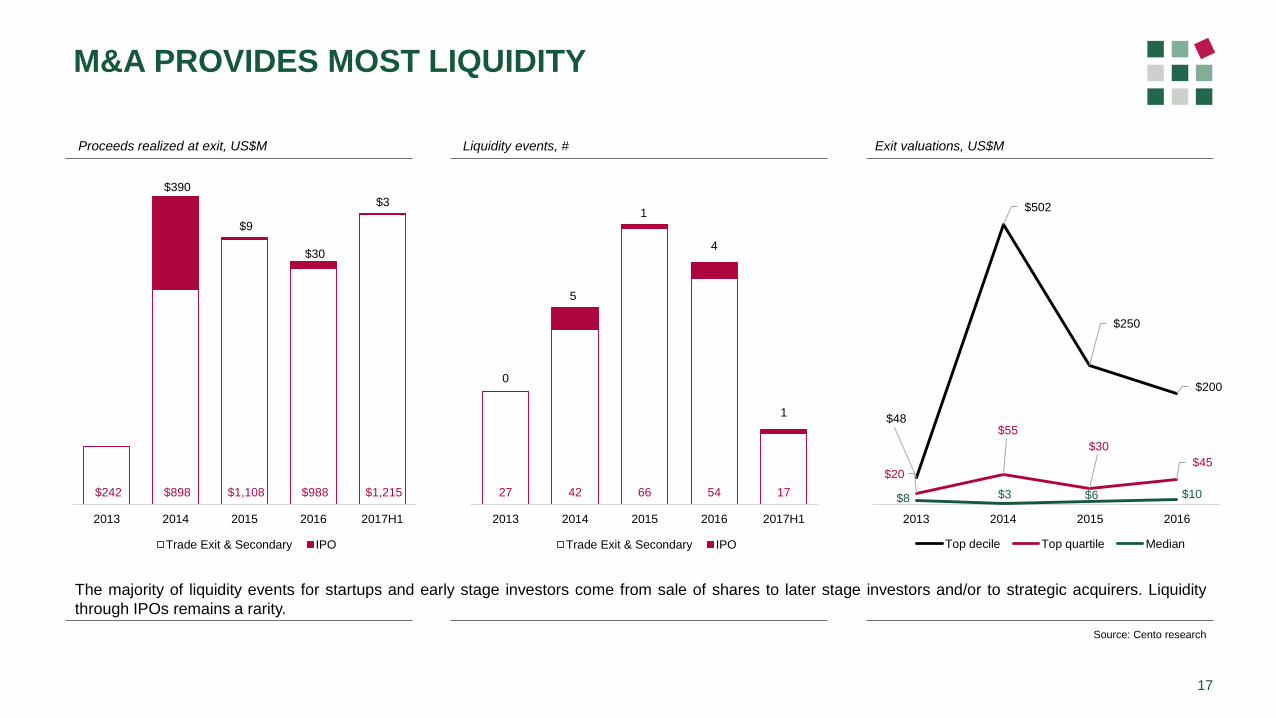

M&A PROVIDES MOST LIQUIDITY

17

Source: Cento research

Liquidity events, #Proceeds realized at exit, US$M

The majority of liquidity events for startups and early stage investors come from sale of shares to later stage investors and/or to strategic acquirers. Liquidity

through IPOs remains a rarity.

27 42 66 54 17

0

5

1

4

1

$-

$10

$20

$30

$40

$50

$60

$70

$80

2013 2014 2015 2016 2017H1

Trade Exit & Secondary IPO

$242 $898 $1,108 $988 $1,215

$390

$9

$30

$3

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

2013 2014 2015 2016 2017H1

Trade Exit & Secondary IPO

$48

$502

$250

$200

$20

$55

$30

$45

$8 $3 $6 $10

2013 2014 2015 2016

Top decile Top quartile Median

Exit valuations, US$M

EXITS ARE HAPPENING, BUT STILL RELATIVELY FEW IN NUMBER

18

Source: Cento research

$790 $543 $700 $2,200

3

2 2

4

2013 2014 2015 2016 2017F

$67 $239 $220 $80 $100

1

3 3

1 1

2013 2014 2015 2016 2017F

$90 $162 $209 $110 $144

3

5

6

3

4

2013 2014 2015 2016 2017F

$87 $63 $110 $95 $40

7

4

10 10

4

0

2

4

6

8

10

12

0

20

40

60

80

100

120

2013 2014 2015 2016 2017F

$11 $26 $38 $24 $29

4

9

13

98

0

2

4

6

8

10

12

14

0

5

10

15

20

25

30

35

40

45

2013 2014 2015 2016 2017F

$7 $9 $15 $10 $5

12

22

31

25

13

2013 2014 2015 2016 2017F

Amount, US$M

Events, #

Liquidity events and proceeds, <US$1M Liquidity events and proceeds, US$1M+ to $5M Liquidity events and proceeds, US$5M+ to $20M

Liquidity events and proceeds, US$20M+ to $50M Liquidity events and proceeds, US$50M+ to $100M Liquidity events and proceeds, >US$100M

19

Source: Cento research

ACQUIRERS ARE FROM WITHIN SE ASIA & APAC REGION

Country of origin of acquirer, by deals done, 2013-2017 Country of origin of acquirer, by capital invested, 2013-2017, US$M

35

15

98

7

54

2 2

$1,500

$917

$331

$244$176

$86 $84 $72 $55 $51 $50 $47 $40

Methodology

METHODOLOGY

21

Data sources:

Our data is compiled from a number of sources, although we primarily rely on public press

announcements from companies and investors. Our team researches the validity of claims and

supplements incomplete information with our insights. Our data passes through a number of quality

control checks. Inevitably data is incomplete and in some cases we use best estimates to assess a

particular deal.

Deal definitions

Stage:

Each series definition is determined as follows:

- Pre-Series A: amounts from $10K-1M. Purpose of investment tends to be building the idea/team, in

some cases the company generates revenue.

- Series A: amounts from $500K-2M. Product has been built and proven initial/repeatable revenue.

Investment tends to be establishes domestic position, and sometimes scaling regionally.

- Series B: amounts from $2M-10M. Investment tends to be increases scale, either domestically or

regionally.

- Series C+: any amount invested later than Series B. Series C, Series D, later series investments,

pre-IPO, mezzanine.

Deal type:

We focus mainly on venture capital deals – investments made by fund entities into early stage startups,

whether they are from independent funds of corporate venture capital entities. This is subset of the

total number of early stage tech deals in the region.

We separate the following from most of our data, apart from the ‘total capital invested and total deals

done’ chart:

- Corporate transfers: events where a corporate entity funds an entity in the region in which it owns a

majority or significant minority stake (e.g. Rocket Internet, Lippo Group)

- Project financing: A deal which was a partnership for an identified purpose – e.g. Grab-Honda.

- Non-Southeast Asia deals: e.g. India and China focused companies that happen to use Singapore for

their corporate domicile.

Country of origin:

Determined by the country in which the company was founded, and has its primary base of operation

(defined in terms of revenue, if known). At the (subjective) point where the company has both operations

in multiple countries in Southeast Asia and substantial revenues generated in multiple countries, then is

may be classified as Southeast Asia in country of origin.

Sector classification:

Cento’s definition of the industry segment in which the company’s primary business focus sits. A full

taxonomy of sector allocation is available. In cases where a company has multiple sector focus with

different units generating thought to generate substantial revenue, then multi-vertical category is used.

Fund definitions

Mapping fund allocations is an inexact science. We count the number of funds that have been observed

doing early stage tech investment in Southeast Asia. We also try to assess the allocation of those funds

to the region. In some cases (e.g. Cento Ventures) that is equivalent to 100% of their AUM. In many

others with a broader, or no particular, geographic focus, allocation is an estimate based on information

received from the fund manager, or the relative number of deals that they have done within the region

compared to elsewhere.

www.cento.vc

+65 6816 2810

Office address: 56B Pagoda Street, Singapore

059215

Mailing address: Cento Ventures, 3 Church Street,

Level 8, Singapore 049483

Co

nta

ct

22