southern employee benefits conference beyond stock options long-term incentives in a volatile or...

Post on 19-Dec-2015

214 views

TRANSCRIPT

Southern Employee Benefits Conference

Beyond Stock Options

Long-Term Incentives in a Volatile or Protracted Bear Market

Copyright © May 7, 1998

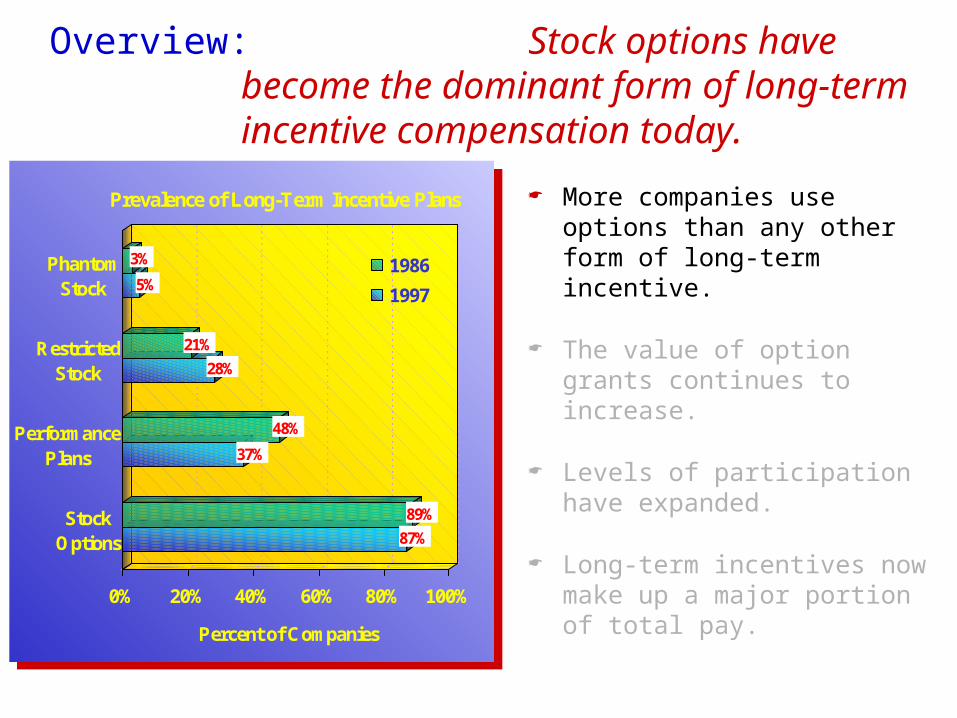

Overview: Stock options have become the dominant form of long-term incentive compensation today.

More companies use options than any other form of long-term incentive.

The value of option grants continues to increase.

Levels of participation have expanded.

Long-term incentives now make up a major portion of total pay.

87%

89%

37%

48%

28%

21%

5%

3%

0% 20% 40% 60% 80% 100%

Percent of Companies

StockOptions

PerformancePlans

RestrictedStock

PhantomStock

Prevalence of Long-Term Incentive Plans

1986

1997

Overview: Stock options have become the dominant form of long-term incentive compensation today.

More companies use options than any other form of long-term incentive.

The value of option grants continues to increase.

Levels of participation have expanded.

Long-term incentives now make up a major portion of total pay.

Overview: Stock options have become the dominant form of long-term incentive compensation today.

More companies use options than any other form of long-term incentive.

The value of option grants continues to increase.

Levels of participation have expanded.

Long-term incentives now make up a major portion of total pay.

313,500

262,500

222,000

0 100,000 200,000 300,000 400,000

1997

1995

1993

Median Expected Value of Long-Term Incentives($300,000 Base Salary)

2.4%

1.8%

1.69%

1.27%

0.0% 0.5% 1.0% 1.5% 2.0% 2.5%

Workforce Eligibility

1997

1994

1991

1988

Prevalence of Long-Term Incentive Plans

Overview: Stock options have become the dominant form of long-term incentive compensation today.

More companies use options than any other form of long-term incentive.

The value of option grants continues to increase.

Levels of participation have expanded.

Long-term incentives now make up a major portion of total pay.

26% 21% 46% 7%

37% 24% 31% 8%

0% 20% 40% 60% 80% 100%

Percent of Companies

1997

1989

Prevalence of Long-Term Incentive Plans

Base Bonus LTI Benefits

Overview: Stock options have become the dominant form of long-term incentive compensation today.

More companies use options than any other form of long-term incentive.

The value of option grants continues to increase.

Levels of participation have expanded.

Long-term incentives now make up a major portion of total pay.

Overview: Stock options have become the dominant form of long-term incentive compensation today.

Impact:

Heightened scrutiny by shareholder groups and the press.

Heightened interest in LTI alternatives.

“[T]he proliferation of stock-option grants, combined with the rise of cushy retirement deals, sign-on bonuses, and ironclad severance packages for CEOs, have made a mockery out of many attempts to truly link pay to performance.

“The upshot: Good, bad, or indifferent, virtually anyone who spent time in the corner office of a large public company in 1997 saw his or her net worth rise by at least several million.”

Source: Business Week, April 20, 1998.

Overview: The pros and cons of management stock options.

Pros Direct alignment of management

and shareholder interests.

A truly long-term perspective.

Better appreciation and understanding of value drivers.

Cons Not line-of-sight.

Can’t differentiate management performance from industry fortune.

Lack stimulus during economic downturns.

Perceived internally and externally as a game of chance.

The Challenge: Making long-term incentives work in a volatile or a protracted down market.

The Prevailing Methods

Design cash-based long-term incentives to address stock option deficiencies.

Design better stock options.

The Challenge: Making long-term incentives work in a volatile or a protracted down market.

The Prevailing Methods

Design cash-based long-term incentives to address stock option deficiencies.

Improved metrics.

Almost all metrics are variations on the same theme...

The Challenge: Making long-term incentives work in a volatile or a protracted down market.

RI = Operating Profit - Opportunity Cost of Running the Business

The return (or expectation) foregone by not investing in a comparably risky portfolio of projects—the weighted cost of debt and equity capital.

Opp. Cost = Cost of Capitalx Beg. Capital

Sales– Cost of Sales– Overhead EBIT– Tax on Operations NOPAT

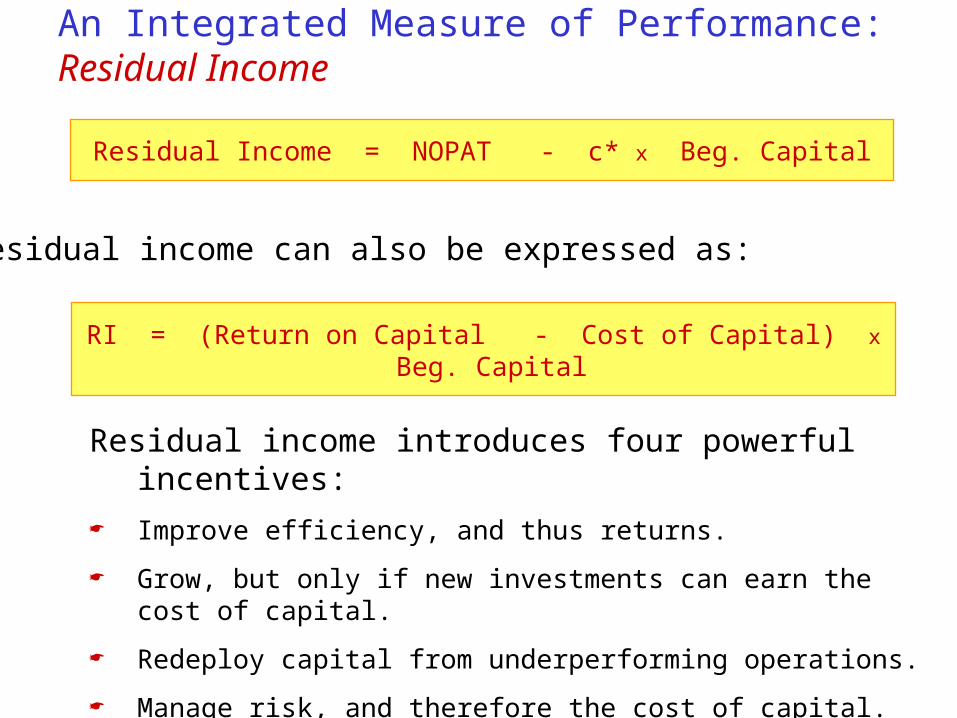

Residual Income = NOPAT - c* x Beg. Capital

An Integrated Measure of Performance: Residual Income

Residual income can also be expressed as:

RI = (Return on Capital - Cost of Capital) x Beg. Capital

Residual income introduces four powerful incentives: Improve efficiency, and thus returns.

Grow, but only if new investments can earn the cost of capital.

Redeploy capital from underperforming operations.

Manage risk, and therefore the cost of capital.

Value Proposition: Residual Income Drives MVA

PV CF1

Value

PV CF3

PV CF2

PV

NOPATC

Discounted Free Cash Flow

Capital

Discounted Residual Income

PV RI1

PV RI2

PV RI3

PV RIC

Value

MVA

The discounted present value of a company’s expected residual income is its market value premium or discount to book value (“MVA”).

A company’s discounted residual income plus its level of capital employed will always equal the discounted present value of expected Free Cash Flow.

Residual income is the only integrated measure of growth and profitability which relates directly to stock value.

The Challenge: Making long-term incentives work in a volatile or a protracted down market.

The Prevailing Methods

Design cash-based long-term incentives to address stock option deficiencies.

Improved metrics.

It all boils down to...

Adopting a metric which works well with your company.

Conceptually simple.

Difficult to manipulate.

Economically rigorous.

The Challenge: Making long-term incentives work in a volatile or a protracted down market.

The Prevailing Methods

Design cash-based long-term incentives to address stock option deficiencies.

Improved metrics.

Improved implementation.

Focus on controllable, company-specific value drivers. Line-of-sight.

Improved Implementation:Making performance measures “line-of-sight”

Raw Materials

Labor

Other

Plant & Equipment

Property

Inventory

Receivables

Payables

Good Will

Intangibles

Revenue

Tax

Operating Expenses

Cost of Capital

Capital Employed

Capital Charge

NOPAT

EVA

Legend:

High Impact Medium Impact Low Impact

Legend:

High Impact Medium Impact Low Impact

Volume

Cost of Goods Sold

SG&A

Cost of Debt

Cost of Equity

Fixed Capital

Working Capital

Other

Price

The Challenge: Making long-term incentives work in a volatile or a protracted down market.

The Prevailing Methods

Design cash-based long-term incentives to address stock option deficiencies.

Improved metrics.

Improved implementation.

Focus on controllable, company-specific value drivers. Line-of-sight.

Make calibration and target-setting truly long-term.

Understand corporate culture and “process.” Help build value-creation coaches.

The Challenge: Making long-term incentives work in a volatile or a protracted down market.

Design cash-based long-term incentives to address stock option deficiencies.

Design better stock options.

What would we like to see?

Real capital at risk. Management rewarded for its

distinctive contribution to share value. Meaningful incentives during

downturns. A strong aversion to repricing.

The Prevailing Methods

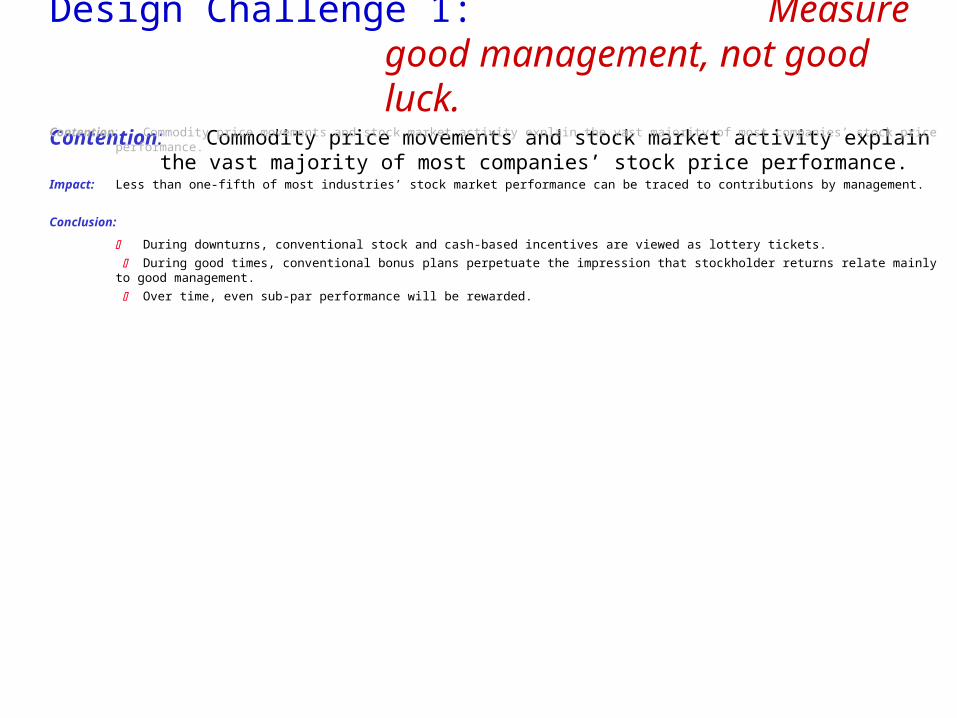

Design Challenge 1: Measure good management, not good luck.

Contention: Commodity price movements and stock market activity explain the vast majority of most companies’ stock price performance.

Example: The Specialty Chemical Industry

20% 10% 0% (10%) (20%)% Change in S&P 500

(10%)

(5%)

0%

5%

10%

% Change inMethanol Prices

(15%) (10%) (5%) 0% 5% 10% 15%

% Change in Market Value

(20%) 0% 20%% Change in Ethylene Prices

Sample:

Georgia Gulf CorpLyondell Petrochemical Co

Dow Chem Co

Union Carbide Corp

Olin Corp

R 2

0 637

80 0%

.

.

Design Challenge 1: Measure good management, not good luck.

Contention: Commodity price movements and stock market activity explain the vast majority of most companies’ stock price performance.

Contention: Commodity price movements and stock market activity explain the vast majority of most companies’ stock price performance.

Impact: Less than one-fifth of most industries’ stock market performance can be traced to contributions by management.

Conclusion:

During downturns, conventional stock and cash-based incentives are viewed as lottery tickets.

During good times, conventional bonus plans perpetuate the impression that stockholder returns relate mainly to good management.

Over time, even sub-par performance will be rewarded.

Design Challenge 2: Eliminate the Perception Gap in Bear Markets.

Contention: Conventional stock options lose much of their power to motivate if the stock is under water, despite retaining significant economic value.

($10)

$0

$10

$20

$30

$40

$40 $50 $60 $70 $80 $90 $100Underlying Stock Price

Value ofStock Option

Option ValueExercise Value

Option Value at Grant

Option Value Today

Perceived Value at Grant

Perceived Value Today

Design Challenge 2: Eliminate the Perception Gap in Bear Markets.

Contention: Conventional stock options lose much of their power to motivate if the stock is under water, despite retaining significant economic value.

Implication:

1. There is often a wide gap between management’s perception of a stock option’s value and its economic substance. This is especially true for companies beset by industry cycles.

Reason: Managers focus on exercise or conversion value, not option value.

2. During downturns, stockholders receive a severely diluted motivational return on the high cost of previously granted options.

Design Approach 1: Tinker with the options themselves...

1. Index against industry performance.

Specifically: Exclude value gains (or losses) attributable to the S&P or industry.

Impact: Creates options where the difference between option value and exercise value (and thus the perception gap) is small.

Justifies issuing more options as a consequence.

but don’t confuse this with repricing.

($40)

($20)

$0

$20

$40

$60

$80

$100

$120

$40 $60 $80 $100 $120 $140

1 Standard Option 1 Indexed Option 5.6 Indexed Options

1.0 Slope:

Slope: 5.4

Slope: 0.97

Portfolio of 5.6 at-the-money indexed options is worth just one out-of-the-money option, but ...

The difference in upside (and downside) potential is enormous, thus greatly amplifying incentives.

Opti

on V

alu

e

Stock Value

($10)

$0

$10

$20

$30

$40

$40 $50 $60 $70 $80 $90 $100 $110 $120

1 Standard Option 1 Indexed Option

1.0 Slope:

1.0 Slope:

High covariance with index means much closer relationship between option value and conversion value.

Unchanging strike price and longer term to maturity makes conventional option more valuable than indexed option, despite higher starting point..

Design Approach 1: Tinker with the options themselves...

Indexing options exploits the perception gap to comparative advantage.

Perception Reality

($10)

$0

$10

$20

$30

$40

$40 $50 $60 $70 $80 $90 $100 $110 $120

1 Standard Option 1 Indexed Option

1.0 Slope:

1.0 Slope:

At-the-money option considerably more valuable than out-of-the-money option.

Indexing means more control over destiny—thus greater option value.

Op

tion

Valu

e

($40)

($20)

$0

$20

$40

$60

$80

$100

$120

$40 $60 $80 $100 $120 $140

1 Standard Option

1 Leveraged Option

8.4 Leveraged Options

1.0 Slope:

Slope: 3.7

Slope: 0.4

Design Approach 1: Tinker with the options themselves...

1. Index against industry performance

2. Reward performance, not longevity.

Consider performance options—options which raise the exercise price over time.

Because performance options are worth less than conventional options, managers can be offered more such options without diluting the value of stockholders’ investment.

Design Approach 2: Tinker with capital structure...

1. Make capital structure line-of-sight.

Create equity in the business units themselves.

Partial public offerings.

Spinoffs and split-ups.

Letter stock.

Restructure business portfolio to reflect core competencies.

Design Approach 2: Tinker with capital structure...

1. Make capital structure line-of-sight.

Create equity in the business units themselves.

Partial public offerings.

Spinoffs and split-ups.

Letter stock.

Restructure business portfolio to reflect core competencies.

28 Large Corporate Split-Ups10-Day Gain

5%25%

50%

100%

Hanson PLC

W.R. GraceNat'l Medical

MarriottHost

KodakEastman Chemical

AllegisHertz

D&BAnheuser Busch

Campbell Taggart

Quaker OatsFisher-Price

SearsDean Witter

General MillsDarden

Eli LillyGuidant

James RiverCrown

RoadwayCaliber

GMEDS

Am. CyanamidCytec

BaxterAHS

ITTHartford

Am. ExpressLehman

Cooper IndustriesCooper Cameron

CoorsATX

AT&TLucent,NCR

Morrisoncafeterias, hospitals

MarriottMarriott Int'l

LittonWestern Atlas Union Carbide

Praxair

DoleCastle & Cooke

The LimitedIntibrands

CeridianControl Data

De-Conglomeratization De-Integration

Proactive

Reactive/Defensive

Positive

Negative

17 Large Corporate Split-Ups365-Day Gain

100%

5%25%

50%

Union CarbidePraxair

MarriottMarriott Int'l

CeridianControl Data

Eli LillyGuidant

CoorsATX

SearsDean Witter

KodakEastman Chemical

LittonWestern Atlas

AllegisHertz

Am. ExpressLehman

James RiverCrown

DoleCastle & Cooke

General MillsDarden

Am. CyanamidCytec

The LimitedIntibrands

Cooper IndustriesCooper Cameron

Quaker OatsFisher-Price

De-Conglomeratization De-Integration

Proactive

Reactive/Defensive

Positive

Negative

Design Approach 2: Tinker with capital structure...

1. Make capital structure line-of-sight.

Create equity in the business units themselves.

Partial public offerings.

Spinoffs and split-ups.

Letter stock.

Restructure business portfolio to reflect core competencies.

Design Approach 2: Tinker with capital structure...

1. Make capital structure line-of-sight.

2. Make the stock a management play rather than an industry play.

Issue equity-linked debt—pegged to the stock price of competitors.

Design Approach 2: Tinker with capital structure...

Specifics: DECS or Prides issued against competitors.

Hybrid debt instruments whose interest payments are linked to the performance of a particular stock—in this case, a market-weighted or equally-weighted portfolio of competitors.

Examples: Lyondell, Enron, NationsBank, Netscape, Nextel, Telecom Argentina, plus seven others—each issued for tax reasons, not business reasons. Issuance relatively low-cost and routine.

1. Make capital structure line-of-sight.

2. Make the stock a management play rather than an industry play.

Design Approach 2: Tinker with capital structure...

1. Make capital structure line-of-sight.

2. Make the stock a management play rather than an industry play.

Issue equity-linked debt—pegged to the stock price of competitors.

Issue commodity-linked debt—pegged to the price of raw materials.

The Common Theme: Pay for Performance, Not Luck

Inexpensive way for company, and thus its shareholders, to place an extended bet against the competition while investing long in management.

Lessens industry risk (and thus beta). Effectively hedges a portion of the equity against all risk except that of lagging behind the industry.

Lowers the cost of capital. Although risk reduction for stockholders would be offset by increased risk (and reward) for creditors, the transferred return would be tax deductible.

Improves cash flow. Debt service would decline when the market anticipated an industry downswing, and would rise in anticipation of an upswing.

Transforms investing in company from an industry play into a management play without shuffling investors.

Summary: Getting the most out of long-term incentives.

Equity is still the most powerful long-term motivator.

Real long-term incentives require real at-risk capital.

LTI’s are more effective if made line-of-sight—whether through cash-based incentives, changes in capital structure, portfolio management or better analysis of value drivers.

LTI’s are more effective if they differentiate management performance from the economy’s.

Summary: Getting the most out of long-term incentives.

Bottom Line

Long-term incentives are most effective when part of a comprehensive financial and strategic value-based initiative to make managers think and behave like diversified owners.