special codes refusal -99 don’t know -66 not applicable...

TRANSCRIPT

1

THIRD WORLD BANK

GLOBAL PAYMENT SYSTEMS SURVEY

QUESTIONNAIRE FOR COLLECTING INFORMATION TO DEPICT THE SITUATION OF PAYMENT AND SETTLEMENT SYSTEMS WORLDWIDE The questionnaire set out in the subsequent pages of this note has been developed to collect information on the situation of national payment and settlement systems worldwide. The questionnaire is being sent to national central banks in their capacity of payment system overseers and (in many cases) payment system operators. This questionnaire has been developed by the World Bank’s Systems Development Group (PSDG)–Financial Infrastructure and Remittances Service Line, Financial Inclusion and Infrastructure Global Practice. The PSDG is aware that other surveys are conducted regularly, and some of the aspects contained in those surveys may also be covered herein. To the extent possible, there has been an effort to harmonize the approaches to these surveys.

IDENTIFICATION

Country country

Institution/Central Bank Information

Name of the institution instname

Address address

Phone Number phone1

Respondent Information

Name of the respondent resp

Position position

Email email

Direct line phone2

Fax number fax

Please find a list of acronyms and a glossary of the main terms used in this questionnaire at the end of it.

Special Codes

Refusal -99

Don’t know -66

Not applicable -77

Not available -33

Not significant -22

WORLD BANK GLOBAL SYSTEMS SURVEY A – LEGAL AND REGULATORY FRAMEWORK

2

A1)

What pieces of legislation have direct/explicit references to payment and securities settlement systems in the country? These include, for example, laws defining the powers and obligations of the Central Bank, main public policies in the area of payment and securities settlement systems, rights and obligations of other payment service providers, etc.

Yes No

a. Central Bank Law A1a

b. Banking Law A1b

c. Payment Systems Law A1c

d. Securities Markets Law A1d

e. Civil Code and/or Commerce Code A1e

f. Central Bank Regulations having the power of Law A1f

g. Consumer Protection Law A1g

h. Competition Law A1h

i. Anti-Money Laundering/Counter Financing of Terrorism (AML/CFT) Law A1i

j. Other. If other, please specify: A1jx A1j

A2)

Do legal provisions cover the following specific issues? Yes No

a. Clarity of timing of final settlement, especially when there is an insolvency A2a

b. Legal recognition of (bilateral and multilateral) netting arrangements A2b

c. Recognition of electronic processing of payments (for example, can electronic signatures/documents be used as evidence in the court of law?)

A2c

d. Non-existence of any zero hour rule or similar rules A2d

e. Enforceability of security interests provided under collateral arrangements and of any relevant repo agreements

A2e

f. Protection from third-party claims of securities and other collateral pledged in a payment system A2f

g. Consumer protection for retail payment services A2g

h. Fair and competitive practices in the provision of payment services A2h

i. Regulation allows correspondent banking arrangements (bank partnerships with non-banks, typically retail commercial outlets, in order for the latter to provide a range of banking and other financial services)

A2i

WORLD BANK GLOBAL SYSTEMS SURVEY A – LEGAL AND REGULATORY FRAMEWORK

3

A3)

Do the provisions in the previous questions apply to: (Select the answer that applies best from table A3 below): A3

Table A3

Only the payment systems operated by the Central Bank 1

All systemically important payment systems1 2

All payment systems in the country 3

A4)

Do legal provisions cover the following specific issues related to securities settlement? Yes No

a. Dematerialization of securities A4a

b. Immobilization of securities A4b

c. Securities ownership transfers through book entries A4c

d. Finality of settlement (securities and funds transfers) A4d

e. Protection of custody arrangements from third-party claims in the event of bankruptcy of the custodian – e.g., securities deposit accounts in the Central Securities Depositories (CSDs)

A4e

f. Securities lending arrangements A4f

g. Novation A4g

h. Open offer and other similar legal devices A4h

i. Protection of the operation of the securities settlement system in the event of the insolvency of a system participant

A4i

A5) Yes No

Has a court in the jurisdiction ever failed to uphold the legal basis of the activities or arrangements under A2 and A4 above?

A5

If Yes, for what reasons: A5x

1 Where they exist, statutory definitions of systemic importance may vary somewhat across jurisdictions, but in general a payment system is systemically

important if it has the potential to trigger or transmit systemic disruptions; this includes, among other things, systems that are the sole payment system in a

country or the principal system in terms of the aggregate value of payments; systems that mainly handle time-critical, high-value payments; and systems that

settle payments used to effect settlement in other systemically important FMIs.

WORLD BANK GLOBAL SYSTEMS SURVEY A – LEGAL AND REGULATORY FRAMEWORK

4

A6) Yes No

Does the Central Bank have any formal powers to perform payment system oversight? A6 If No skip to A7

If Yes, SEE TABLE A6 BELOW

a. Type of Empowerment? (Select the answer that applies best from table A6 below) A6a

Yes No

b. Oversight powers are to be found in the Central Bank Law A6b

c. Oversight powers are to be found in the Payment Systems Law A6c

d. Oversight powers are to be found in other laws A6d

e. Empowerment explicitly grants powers to oversee also other settlement systems such as securities settlement systems and/or central counterparties

A6e

Table A6

Empowerment is general, in the context of “ensuring the adequate and safe functioning of payment systems” in the country 1

Empowerment is explicit, granting it powers to operate, regulate, and oversee payment systems 2

WORLD BANK GLOBAL SYSTEMS SURVEY A – LEGAL AND REGULATORY FRAMEWORK

5

A7)

Please indicate the authorities that are legally empowered to regulate and supervise the following non-bank payment and settlement service providers.

CENTRAL

BANK

BANKING

SUPERVISION

AUTHORITY

SECURITIES

REGULATOR MINISTRY

OF FINANCE ANTI-TRUST

AUTHORITY

MINISTRY OF

INDUSTRY

AND

COMMERCE

OTHER.

Yes No Yes No Yes No Yes No Yes No Yes No Yes No If Yes to Other,

please specify

a. Clearinghouses A7a1 A7a2 A7a3 A7a4 A7a5 A7a6 A7a7 A7a7x

b. Entities operating payment card networks or switches

A7b1 A7b2 A7b3 A7b4 A7b5 A7b6 A7b7 A7b7x

c. MTOs (e.g., Western Union, Money Gram)

A7c1 A7c2 A7c3 A7c4 A7c5 A7c6 A7c7 A7c7x

d. CSD-SSSs A7d1 A7d2 A7d3 A7d4 A7d5 A7d6 A7d7 A7d7x

e. SSSs (non CSD-operated) A7e1 A7e2 A7e3 A7e4 A7e5 A7e6 A7e7 A7e7x

f. Derivatives CCPs A7f1 A7f2 A7f3 A7f4 A7f5 A7f6 A7f7 A7f7x

g. Other securities CCPs A7g1 A7g2 A7g3 A7g4 A7g5 A7g6 A7g7 A7g7x

h. Mobile phone operators2 A7h1 A7h2 A7h3 A7h4 A7h5 A7h6 A7h7 A7h7x

i. Supervised NBFIs3, please

specify the type of institutions: A7i1 A7i2 A7i3 A7i4 A7i5 A7i6 A7i7 A7i7x

A7ix

j. Any other entity that provides payment and/or securities settlement services to the public. If other, please specify: A7j1 A7j2 A7j3 A7j4 A7j5 A7j6 A7j7 A7j7x

A7jx

2 Applicable only if mobile phone operators in your country provide payment services.

3 Applicable only if supervised NBFIs in your country provide payment services.

WORLD BANK GLOBAL SYSTEMS SURVEY A – LEGAL AND REGULATORY FRAMEWORK

6

A8)

Are non-bank payment and settlement services providers required to be registered and/or to obtain a specific license from the relevant authority?

Select the answer that applies best from the

table A8 below

a. Clearinghouses A8a

b. Entities operating payment card networks or switches A8b

c. Money transfer operators (MTOs) - e.g. Western Union, Money Gram A8c

d. CSD-operated securities settlement systems (SSSs) A8d

e. SSSs (non-CSD-operated) A8e

f. Derivatives central counterparties (CCPs) A8f

g. Other securities CCPs A8g

h. Mobile phone operators4 A8h

i. Supervised non-bank financial institutions (NBFIs) 5.

Please specify type of institutions: A8ix A8i

j. Unsupervised non-bank financial institutions (NBFIs)

Please specify type of institutions: A8jx A8j

k. Any other entity that provides payment and/or securities settlement services to the public.

If other, please specify: A8kx A8k

Table A8

License only 1

Registration only 2

License and Registration 3

Neither a License nor any Registration 4

4 Applicable only if registration and/or license is required specifically for the provision of payment services (i.e. independently of any license that may have

obtained for providing regular mobile phone services). 5 Applicable only if registration and/or license is required specifically for the provision of payment services (i.e. in addition of any license that may have

obtained for acting as a NBFI).

WORLD BANK GLOBAL SYSTEMS SURVEY A – LEGAL AND REGULATORY FRAMEWORK

7

A9)

Which of the following payment service providers are subject to AML/CFT regulations? Yes No

a. Commercial banks A9a

b. Money transfer operators (MTOs) A9b

c. Exchange bureaus A9c

d. Credit unions A9d

e. Microfinance institutions (MFIs) A9e

f. Postal network A9f

g. Mobile phone operators A9g

h. Other. If Other, please specify: A9hx A9h

A10)

Consumer protection. Yes No

a. A general legislation on consumer protection is in place A10a

b. A specific legislation on consumer protection for financial services is in place A10b

c. Best practices code for the protection of financial services users is in place A10c

d. Best practices code is applicable also to remittance services A10d

e. There is a public authority (consumer protection agency, financial ombudsman, etc.) which oversees and implements the relative legislation

A10e

WORLD BANK GLOBAL SYSTEMS SURVEY B – LARGE-VALUE FUNDS TRANSFERS SYSTEMS

8

B1)

What is the main system used in the country for large-value funds transfers? If more than one payment system could be considered as systemically important,

6 please also indicate an approximate

percentage of the total volume of large-value payments that is channelled through each system.. %

a. Real-time gross settlement (RTGS) system B1a If =0% skip to B18

b. Cheque clearinghouse B1b If =100% skip to C1

c. Other B1c If =100% skip to B18

TOTAL 100%

Note to Central Bank: if there is more than one Real-Time Gross Settlement (RTGS7) system, please provide separate answers for each RTGS.

B2) RTGS – General Information RTGS 1 RTGS 2 RTGS 3

Names: RTGS1 RTGS2 RTGS3

a. Who is the Owner of the RTGS system? (See table B2) B2a1 B2a2 B2a3

b. Who is the Operator? (See table B2) B2b1 B2b2 B2b3

c. Who acts as Settlement Agent? (See table B2) B2c1 B2c2 B2c3

d. Please indicate the year in which the RTGS system began operations on a full scale?

B2d1 B2d2 B2d3

Table B2

Central Bank 1

Other Public-Sector 2

Private Sector 3

Other. If other please specify

RTGS 1 RTGS 2 RTGS 3

4 a. Owner B2a1x B2a2x B2a3x

b. Operator B2b1x B2b2x B2b3x

c. Settlement Agent B2c1x B2c2x B2c3x

6 Where they exist, statutory definitions of systemic importance may vary somewhat across jurisdictions, but in general a payment system is systemically

important if it has the potential to trigger or transmit systemic disruptions; this include, among other things, systems that are the sole payment system in a

country or the principal system in terms of the aggregate value of payments; systems that mainly handle time-critical, high-value payments; and systems that

settle payments used to effect settlement in other systemically important FMIs.

7 The real-time settlement of payments, transfer instructions, or other obligations individually on a transaction-by-transaction basis.

WORLD BANK GLOBAL SYSTEMS SURVEY B – LARGE-VALUE FUNDS TRANSFERS SYSTEMS

9

B3a1) For RTGS 1, NUMBER/VOLUME of transactions/settled payments (in thousands)

Specify currency:

2012 2011 2010 2009 2008 2007

a. Number of local currency transactions / settled payments. Local currency, please specify:

B3a1x B3a1_12 B3a1_11 B3a1_10 B3a1_09 B3a1_08 B3a1_07 If No Other currency, skip to B3b1

If the RTGS system handles foreign currency transactions, Number of transactions / settled payments for each foreign currency:

b. Foreign currency, please specify: B3a11x B3a11_12 B3a11_11 B3a11_10 B3a11_09 B3a11_08 B3a11_07 If No Other currency, skip to B3b1

c. Foreign currency, please specify: B3a12x B3a12_12 B3a12_11 B3a12_10 B3a12_09 B3a12_08 B3a12_07 If No Other currency, skip to B3b1

d. Foreign currency, please specify: B3a13x B3a13_12 B3a13_11 B3a13_10 B3a13_09 B3a13_08 B3a13_07 If No Other currency, skip to B3b1

B3b1) For RTGS 1, VALUE settled (in thousands)

Specify currency:

2012 2011 2010 2009 2008 2007

a. Value of local currency transactions / settled payments. Local currency, please specify:

B3b1x B3b1_12 B3b1_11 B3b1_10 B3b1_09 B3b1_08 B3b1_07 If No Other currency, skip to B3a2

If the RTGS system handles foreign currency transactions, Value of transactions / settled payments for each foreign currency:

b. Foreign currency, please specify: B3b11x B3b11_12 B3b11_11 B3b11_10 B3b11_09 B3b11_08 B3b11_07 If No Other currency, skip to B3a2

c. Foreign currency, please specify: B3b12x B3b12_12 B3b12_11 B3b12_10 B3b12_09 B3b12_08 B3b12_07 If No Other currency, skip to B3a2

d. Foreign currency, please specify: B3b13x B3b13_12 B3b13_11 B3b13_10 B3b13_09 B3b13_08 B3b13_07 If No Other currency, skip to B3a2

WORLD BANK GLOBAL SYSTEMS SURVEY B – LARGE-VALUE FUNDS TRANSFERS SYSTEMS

10

B3a2) For RTGS 2, NUMBER/VOLUME of transactions/settled payments (in thousands)

Specify currency:

2012 2011 2010 2009 2008 2007

a. Number of local currency transactions / settled payments. Local currency, please specify:

B3a2x B3a2_12 B3a2_11 B3a2_10 B3a2_09 B3a2_08 B3a2_07 If No Other currency, skip to B3b1

If the RTGS system handles foreign currency transactions, Number of foreign currency transactions / settled payments for each foreign currency:

b. Foreign currency, please specify: B3a21x B3a21_12 B3a21_11 B3a21_10 B3a21_09 B3a21_08 B3a21_07 If No Other currency, skip to B3b1

c. Foreign currency, please specify: B3a22x B3a22_12 B3a22_11 B3a22_10 B3a22_09 B3a22_08 B3a22_07 If No Other currency, skip to B3b1

d. Foreign currency, please specify: B3a23x B3a23_12 B3a23_11 B3a23_10 B3a23_09 B3a23_08 B3a23_07 If No Other currency, skip to B3b1

B3b2) For RTGS 2, VALUE settled (in thousands)

Specify currency:

2012 2011 2010 2009 2008 2007

a. Value of local currency transactions / settled payments. Local currency, please specify:

B3b2x B3b2_12 B3b2_11 B3b2_10 B3b2_09 B3b2_08 B3b2_07 If No Other currency, skip to B3a2

If the RTGS system handles foreign currency transactions, Value of foreign currency transactions / settled payments for each foreign currency:

b. Foreign currency, please specify: B3b21x B3b21_12 B3b21_11 B3b21_10 B3b21_09 B3b21_08 B3b21_07 If No Other currency, skip to B3a2

c. Foreign currency, please specify: B3b22x B3b22_12 B3b22_11 B3b22_10 B3b22_09 B3b22_08 B3b22_07 If No Other currency, skip to B3a2

d. Foreign currency, please specify: B3b23x B3b23_12 B3b23_11 B3b23_10 B3b23_09 B3b23_08 B3b23_07 If No Other currency, skip to B3a2

WORLD BANK GLOBAL SYSTEMS SURVEY B – LARGE-VALUE FUNDS TRANSFERS SYSTEMS

11

B3a3) For RTGS 3, NUMBER/VOLUME of transactions/settled payments (in thousands)

Specify currency:

2012 2011 2010 2009 2008 2007

a. Number of local currency transactions / settled payments. Local currency, please specify:

B3a3x B3a3_12 B3a3_11 B3a3_10 B3a3_09 B3a3_08 B3a3_07 If No Other currency, skip to B3b1

If the RTGS system handles foreign currency transactions, Number of foreign currency transactions / settled payments for each foreign currency:

b. Foreign currency, please specify: B3a31x B3a31_12 B3a31_11 B3a31_10 B3a31_09 B3a31_08 B3a31_07 If No Other currency, skip to B3b1

c. Foreign currency, please specify: B3a32x B3a32_12 B3a32_11 B3a32_10 B3a32_09 B3a32_08 B3a32_07 If No Other currency, skip to B3b1

d. Foreign currency, please specify: B3a33x B3a33_12 B3a33_11 B3a33_10 B3a33_09 B3a33_08 B3a33_07 If No Other currency, skip to B3b1

B3b3) For RTGS 3, VALUE settled (in thousands)

Specify currency:

2012 2011 2010 2009 2008 2007

a. Value of local currency transactions / settled payments. Local currency, please specify:

B3b3x B3b3_12 B3b3_11 B3b3_10 B3b3_09 B3b3_08 B3b3_07 If No Other currency, skip to B3a2

If the RTGS system handles foreign currency transactions, Value of foreign currency transactions / settled payments for each foreign currency:

b. Foreign currency, please specify: B3b31x B3b31_12 B3b31_11 B3b31_10 B3b31_09 B3b31_08 B3b31_07 If No Other currency, skip to B3a2

c. Foreign currency, please specify: B3b32x B3b32_12 B3b32_11 B3b32_10 B3b32_09 B3b32_08 B3b32_07 If No Other currency, skip to B3a2

d. Foreign currency, please specify: B3b33x B3b33_12 B3b33_11 B3b33_10 B3b33_09 B3b33_08 B3b33_07 If No Other currency, skip to B3a2

WORLD BANK GLOBAL SYSTEMS SURVEY B – LARGE-VALUE FUNDS TRANSFERS SYSTEMS

12

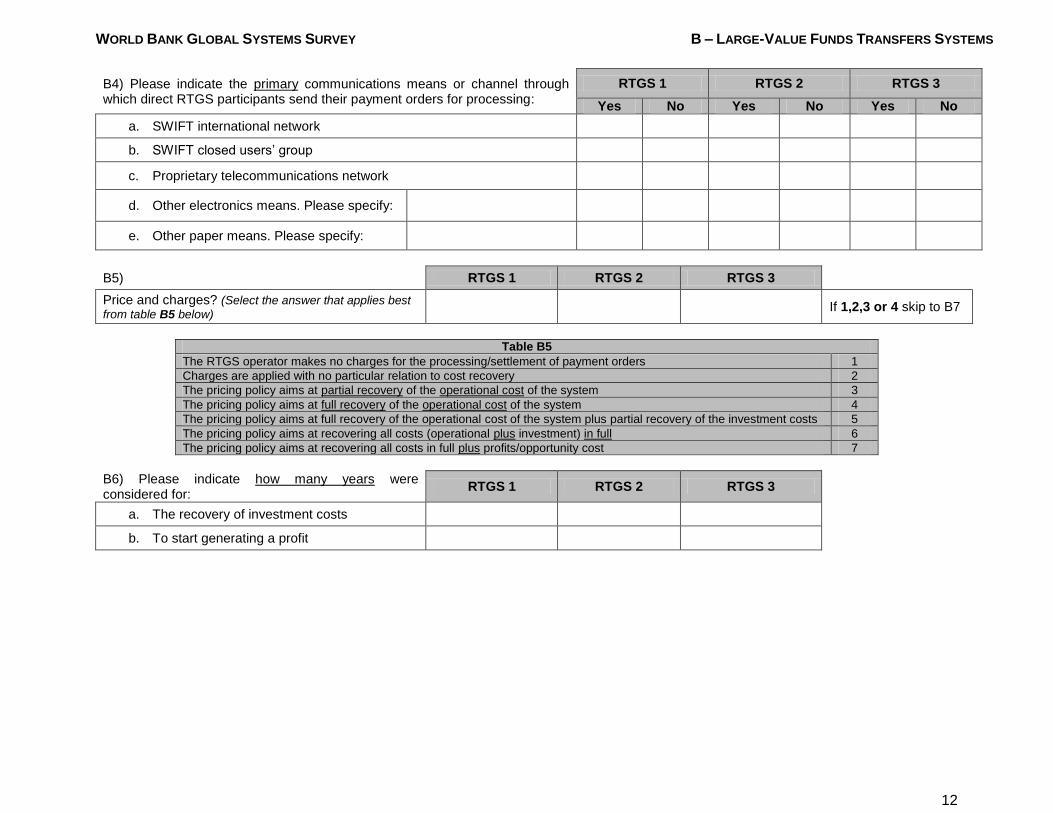

B4) Please indicate the primary communications means or channel through which direct RTGS participants send their payment orders for processing:

RTGS 1 RTGS 2 RTGS 3

Yes No Yes No Yes No

a. SWIFT international network B4a1 B4a2 B4a3

b. SWIFT closed users’ group B4b1 B4b2 B4b3

c. Proprietary telecommunications network B4c1 B4c2 B4c3

d. Other electronics means. Please specify: B4d1x, B4d2x, B4d3x B4d1 B4d2 B4d3

e. Other paper means. Please specify: B4e1x, B4e2x, B4e2x B4e1 B4e2 B4e3

B5) RTGS 1 RTGS 2 RTGS 3

Price and charges? (Select the answer that applies best

from table B5 below) B51 B52 B53 If 1,2,3 or 4 skip to B7

Table B5

The RTGS operator makes no charges for the processing/settlement of payment orders 1

Charges are applied with no particular relation to cost recovery 2

The pricing policy aims at partial recovery of the operational cost of the system 3

The pricing policy aims at full recovery of the operational cost of the system 4

The pricing policy aims at full recovery of the operational cost of the system plus partial recovery of the investment costs 5

The pricing policy aims at recovering all costs (operational plus investment) in full 6

The pricing policy aims at recovering all costs in full plus profits/opportunity cost 7

B6) Please indicate how many years were considered for:

RTGS 1 RTGS 2 RTGS 3

a. The recovery of investment costs B6a1 B6a2 B6a3

b. To start generating a profit B6b1 B6b2 B6b3

WORLD BANK GLOBAL SYSTEMS SURVEY B – LARGE-VALUE FUNDS TRANSFERS SYSTEMS

13

B7) What are the main sources of liquidity during the day? RTGS 1 RTGS 2 RTGS 3

Yes No Yes No Yes No

a. Opening balances and funds received from other participants during the day

B7a1 B7a2 B7a3

b. Participants can use all their reserve requirements balance during the day

B7b1 B7b2 B7b3 If Yes, skip to c

If No, Participants can use a part of their reserve requirements during the day

B7b1a B7b2a B7b3a

c. Lines of credit between banks B7c1 B7c2 B7c3

d. The RTGS operator allows uncollateralized current account overdrafts

B7d1 B7d2 B7d3 If Yes, skip to e

If No, The RTGS operator allows collateralized: (Select

the answer that applies best from table B7) B7d1a B7d2a B7d3a

e. Other sources of liquidity during the day. B7h1 B7h2 B7h3

If Other sources of liquidity during the day, Please specify: B7h1x B7h2x B7h3x

Table B7. The RTGS operator allows collateralized:

Current account overdrafts 1

Credit, either in the form of a loan or a repo 2

Both current account overdrafts and credit, either in the form of a loan or a repo 3

B8) RTGS 1 RTGS 2 RTGS 3

How does the RTGS operator manage the credit risk that may arise as a result of applying some of the mechanisms discussed in the previous question? (Select the answer that applies best from table

B8) B81 B82 B83

Table B8

Suitable collateral8 is required in all cases 1

Collateral is required in all cases, but collateral does not always have suitable quality 2

There are limits to the amount of current account overdrafts/credit, but no collateralization is required 3

There are no limits or collateralization requirements for account overdrafts/credit 4

8 In this context, suitable collateral should be interpreted as having low credit, liquidity and market risks. It also implies that the value of such collateral is

marked to market on a daily basis and haircuts applied where appropriate.

WORLD BANK GLOBAL SYSTEMS SURVEY B – LARGE-VALUE FUNDS TRANSFERS SYSTEMS

14

B9) How does the RTGS operator deal with intraday liquidity that is not repaid by the end of the system’s operating day?

RTGS 1 RTGS 2 RTGS 3

Yes No Yes No Yes No

a. The RTGS operator liquidates the collateral immediately thereafter B9a1 B9a2 B9a3

b. The RTGS operator transforms the intraday credit into overnight at market rates

B9b1 B9b2 B9b3

c. The RTGS operator transforms the intraday credit into overnight at penalty rates

B9c1 B9c2 B9c3

d. Other. Please specify: B9d1x, B9d2x, B9d3x B9d1 B9d2 B9d3

B10) RTGS 1 RTGS 2 RTGS 3

If a participant does not have enough balance (and/or credit) in its current account with the RTGS operator to process new payments, what mechanism becomes applicable? (Select the answer that

applies best from table B10) B101 B102 B103

Table B10

The payment order is rejected immediately 1

The payment order goes into a queue for later processing 2

Other. Please specify: B101x, B102x, B103x 3

WORLD BANK GLOBAL SYSTEMS SURVEY B – LARGE-VALUE FUNDS TRANSFERS SYSTEMS

15

B11) Queuing arrangements, payment order prioritization and settlement optimization?

RTGS 1 RTGS 2 RTGS 3

Yes No Yes No Yes No

a. A centralized queuing mechanism is used B11a1 B11a2 B11a3

b. A first in, first out (FIFO) resolution algorithm is used B11b1 B11b2 B11b3

SEE TABLE BELOW SEE TABLE BELOW SEE TABLE BELOW

c. Offsetting used as resolution algorithm? (See table B11a) B11c1 B11c2 B11c3

d. How is the offsetting mechanism triggered? (See table B11b) B11d1 B11d2 B11d3

Yes No Yes No Yes No

e. Participants can set priorities to their payment orders B11e1 B11e2 B11e3

f. Participants can change the priorities to their payment orders once these orders are in a queue waiting to be settled

B11f1 B11f2 B11f3

Table B11a. Bilateral vs Multilateral? Table B11b. Trigger?

Bilateral offsetting only is used as resolution algorithm 1 The offsetting mechanism is triggered automatically every certain period of time 1

Multilateral offsetting only is used as resolution algorithm 2 The offsetting mechanism is triggered automatically by other, non-time-related

parameters such as accumulated volumes pending settlement or other measures 2

Both bilateral and multilateral offsetting is used 3 The offsetting mechanism can be triggered manually by the RTGS operator at any

time 3

RTGS 1 RTGS 2 RTGS 3

Yes No Yes No Yes No

B12) Is the pricing policy used to incentivize the smooth flow of payment orders through the system, e.g. are participants charged different prices based on the time of the day when their payments are processed?

B12_1 B12_2 B12_3

RTGS 1 RTGS 2 RTGS 3

Yes No Yes No Yes No

B13) Do participants have access to real-time information on their settlement balances and available credit/overdrafts during the day?

B13_1 B13_2 B13_3

WORLD BANK GLOBAL SYSTEMS SURVEY B – LARGE-VALUE FUNDS TRANSFERS SYSTEMS

16

B14) Operational risk management RTGS 1 RTGS 2 RTGS 3

Yes No Yes No Yes No

a. The roles and responsibilities for addressing operational risk are explicitly defined by the Board (or equivalent) of the organization operating the RTGS system

B14a1 B14a2 B14a3

b. The operational risk-management framework has been endorsed by the Board (or equivalent)

B14b1 B14b2 B14b3

c. The overall operational risk management framework is periodically reviewed and tested

B14c1 B14c2 B14c3

d. Routine procedures are in place for periodical data back-ups B14d1 B14d2 B14d3

e. Tapes and other storage media are kept in sites other than the main processing site

B14e1 B14e2 B14e3

f. Back-up servers have been deployed at the main processing site B14f1 B14f2 B14f3

g. A fully equipped alternate processing site exists B14g1 B14g2 B14g3

h. The RTGS operator has a documented, formal business continuity plan B14h1 B14h2 B14h3

i. Business continuity arrangements include procedures for crisis management and information dissemination

B14i1 B14i2 B14i3

j. Business continuity arrangements are regularly reviewed and tested B14j1 B14j2 B14j3

k. The RTGS operator coordinates business continuity arrangements with interdependent financial market infrastructures (FMIs). Please specify what other FMIs are included in these arrangements: B14kx B14k1 B14k2 B14k3

B15) What is the targeted performance level for full system recovery / recovery time objective?

RTGS 1 RTGS 2 RTGS 3

B15_1 minutes B15_2 minutes B15_3 minutes

RTGS 1 RTGS 2 RTGS 3

Yes No Yes No Yes No

B16) Is there a specific RTGS users’ group in place for the RTGS operator to better address participants’ needs?

B16_1 B16_2 B16_3

WORLD BANK GLOBAL SYSTEMS SURVEY B – LARGE-VALUE FUNDS TRANSFERS SYSTEMS

17

B17) Please indicate which of the following dependencies are applicable to the RTGS system

RTGS 1 RTGS 2 RTGS 3

Yes No Yes No Yes No

a. The system is dependent on another system for final settlement9 B17a1 B17a2 B17a3

b. The system is dependent on a SSS (e.g. for collateralized intraday credit)

B17b1 B17b2 B17b3

c. The system is dependent on a third-party service provider B17c1 B17c2 B17c3

d. The system is dependent on liquidity provision by the Central Bank or another system

B17d1 B17d2 B17d3

If B1c=0% (i.e. The Central Bank have indicated above that there is no other Large Value payment systems apart from RTGS and / or Cheque Clearinghouse as the main payment systems for Large Value Transactions) then SKIP TO Part C.

Answer Only if B1c>0%

B18) Features of the main settlement system for large-value payments SEE TABLE BELOW

a. Gross versus net settlement? (Select the answer that applies best from table B18a below) B18a

b. Where does the final settlement take place? (Select the answer that applies best from B18b below) B18b

Yes No

c. The payment system explicitly guarantees settlement B18c

Table B18a. Gross versus Net settlement Table B18b. Takes place

Settlement of payments is executed on a gross basis but not in real time 1 Final settlement takes place in Central Bank money but not through

RTGS (e.g. in the deposit accounts or current accounts participants hold at the Central Bank)

1

Settlement of payments is processed on a net basis at the end of the day 2 Final settlement takes place through a RTGS system 2

Payments are settled in multiple clearing sessions during the day 3 Final settlement takes place in commercial bank money 3

9 Such as the General Ledger or other system that holds the current accounts of RTGS participants.

WORLD BANK GLOBAL SYSTEMS SURVEY B – LARGE-VALUE FUNDS TRANSFERS SYSTEMS

18

B19) Please indicate the primary means through which participants send their payment orders for processing: Yes No

a. SWIFT International Network B19a

b. SWIFT closed users’ group B19b

c. Proprietary telecommunications network B19c

d. Other electronic means (e.g. e-mail, etc.). Please specify: B19dx B19d

e. Other paper means. Please specify: B19ex B19e

B20) If a participant does not have enough balance (and/or credit) in its settlement account to process new payments, what mechanism becomes applicable?

Yes No

a. The payment order is rejected immediately B20a If Yes, skip to B21

b. The payment order is delayed until funds are available B20b

c. The settlement institution / system operator extends immediate credit B20c If No, skip to d

If Yes, credit provided by the operator collateralized or not? (Select the answer that applies

best from B20 below) B20c1

Yes No

d. Other. Please specify: B20dx B20d

Table B20

Credit provided by the operator is collateralized 1

Credit provided by the operator without requiring collateral, but there are limits 2

B21) Please indicate which of the following dependencies are applicable to the system indicated above: Yes No

a. The system is dependent on another system for final settlement B21a

b. The system is dependent on a SSS (e.g. for collateralized intraday credit) B21b

c. The system is dependent on a third-party service provider B21c

d. The system is dependent on liquidity provision by the Central Bank or another system B21d

WORLD BANK GLOBAL SYSTEMS SURVEY C – RETAIL PAYMENT SYSTEMS

19

C1a) Please provide the following statistical data: (if data is not available please indicate -33; if an item is not applicable please indicate -77; if figures are not significant please indicate -22)

2012 2011 2010 2009 2008 2007

a. Total number of ATMS in the country C1a1_12 C1a1_11 C1a1_10 C1a1_09 C1a1_08 C1a1_07

b. Total number of POS terminals in the country C1a2_12 C1a2_11 C1a2_10 C1a2_09 C1a2_08 C1a2_07

c. Total number of checking accounts C1a3_12 C1a3_11 C1a3_10 C1a3_09 C1a3_08 C1a3_07

d. Total number of debit cards C1a4_12 C1a4_11 C1a4_10 C1a4_09 C1a4_08 C1a4_07

e. Total number of credit cards C1a5_12 C1a5_11 C1a5_10 C1a5_09 C1a5_08 C1a5_07

f. … of which, total number of credit cards not linked to a bank account

C1a6_12 C1a6_11 C1a6_10 C1a6_09 C1a6_08 C1a6_07

g. Total number of prepaid and stored-value cards (general-purpose cards only)

C1a7_12 C1a7_11 C1a7_10 C1a7_09 C1a7_08 C1a7_07

h. … of which, total number of prepaid and stored-value cards not linked to a bank account

C1a8_12 C1a8_11 C1a8_10 C1a8_09 C1a8_08 C1a8_07

i. Total number of e-money accounts for mobile payments (please do not include traditional bank accounts that can be operated also with a mobile phone)

C1a9_12 C1a9_11 C1a9_10 C1a9_09 C1a9_08 C1a9_07

j. Total number of ATM networks10 C1a10_12 C1a10_11 C1a10_10 C1a10_09 C1a10_08 C1a10_07

k. Total number of POS networks11 C1a11_12 C1a11_11 C1a11_10 C1a11_09 C1a11_08 C1a11_07

Please use the following codes in the

following cases:

Not applicable -77

Not available -33

Not significant -22

10

Involving at least two banks and/or other payment service providers. 11

Involving at least two banks and/or other payment service providers.

WORLD BANK GLOBAL SYSTEMS SURVEY C – RETAIL PAYMENT SYSTEMS

20

C1b) For the following table, please include information on both intrabank and

interbank transactions12

. (If data is not available please indicate -33; if an item is

not applicable please indicate -77; if figures are not significant please indicate -22)

2012 2011 2010 2009 2008 2007

Number of transactions (in thousands)

a. Cheques C1b1_12 C1b1_11 C1b1_10 C1b1_09 C1b1_08 C1b1_07

b. Direct credits/credit transfers C1b2_12 C1b2_11 C1b2_10 C1b2_09 C1b2_08 C1b2_07

c. Direct debits C1b3_12 C1b3_11 C1b3_10 C1b3_09 C1b3_08 C1b3_07

d. Payments by debit card C1b4_12 C1b4_11 C1b4_10 C1b4_09 C1b4_08 C1b4_07

e. Payments by credit card C1b5_12 C1b5_11 C1b5_10 C1b5_09 C1b5_08 C1b5_07

f. Payments by prepaid and stored-value cards (general-purpose cards only)

C1b6_12 C1b6_11 C1b6_10 C1b6_09 C1b6_08 C1b6_07

g. Internet payments C1b7_12 C1b7_11 C1b7_10 C1b7_09 C1b7_08 C1b7_07

h. Mobile payments C1b8_12 C1b8_11 C1b8_10 C1b8_09 C1b8_08 C1b8_07

Please use the following codes in the

following cases:

Not applicable -77

Not available -33

Not significant -22

12

If only interbank transaction information is available, please indicate so in the comments, and fill table C1b with available information.

WORLD BANK GLOBAL SYSTEMS SURVEY C – RETAIL PAYMENT SYSTEMS

21

C1c) For the following table, please include information

on both intrabank and interbank transactions13

. (If data is

not available please indicate -33; if an item is not applicable please indicate -77; if figures are not significant please indicate -22)

2012 2011 2010 2009 2008 2007

Value settled (in local currency. In thousands).

Please specify the local currency: C1cx

a. Cheques C1c1_12 C1c1_11 C1c1_10 C1c1_09 C1c1_08 C1c1_07

b. Direct credits/credit transfers C1c2_12 C1c2_11 C1c2_10 C1c2_09 C1c2_08 C1c2_07

c. Direct debits C1c3_12 C1c3_11 C1c3_10 C1c3_09 C1c3_08 C1c3_07

d. Payments by debit card C1c4_12 C1c4_11 C1c4_10 C1c4_09 C1c4_08 C1c4_07

e. Payments by credit card C1c5_12 C1c5_11 C1c5_10 C1c5_09 C1c5_08 C1c5_07

f. Payments by prepaid and stored-value cards (general-purpose cards only)

C1c6_12 C1c6_11 C1c6_10 C1c6_09 C1c6_08 C1c6_07

g. Internet payments C1c7_12 C1c7_11 C1c7_10 C1c7_09 C1c7_08 C1c7_07

h. Mobile payments C1c8_12 C1c8_11 C1c8_10 C1c8_09 C1c8_08 C1c8_07

Please use the following codes in the

following cases:

Not applicable -77

Not available -33

Not significant -22

13

If only interbank transaction information is available, please indicate so in the comments, and fill table C1c with available information.

WORLD BANK GLOBAL SYSTEMS SURVEY C – RETAIL PAYMENT SYSTEMS

22

C2) Cheque clearinghouse main features Yes No

Is a cheque clearinghouse available in the country? C2 If No, skip to C5

If Yes, Yes No

a. Cheque clearinghouse is operated by the Central Bank C2a

b. Cheques are standardized C2b

c. Cheque processing? (Select the answer that applies best from C2a below) C2c

Yes No

d. Multilateral net balances are calculated C2d

e. Net balances are calculated and settled at what frequency? (Select the answer that applies best from

C2b below) C2e1

f. Where does final settlement of net positions take place? (Select the answer that applies best from C2c

below) C2f

Yes No

g. Customer accounts are credited no later than T+2 C2g

Table C2a. Cheque processing

Processing of cheques is automated, but physical exchange is required 1

Processing of cheques is automated, and cheque truncation is used 2

Table C2b. Settlement of net balances Table C2c. Final settlement of net positions takes place:

Once a day 1 Final settlement takes place through a RTGS system 1

More than once each day 2 Final settlement takes place in Central Bank money, but not through a RTGS system 2

C3) Large-value cheques Yes No

Has a special procedure for large-value cheques been implemented? C3 If No, Skip to C4

If Yes, Yes No

a. As part of this procedure, large-value cheques can be settled with same-day value C3a

b. As part of this procedure, large-value cheques are processed on a gross basis C3b

c. As part of this procedure, net balances are calculated and settled more than once a day C3c

d. There is a settlement guarantee fund for large-value cheques processed under this procedure (on a net basis)

C3d

WORLD BANK GLOBAL SYSTEMS SURVEY C – RETAIL PAYMENT SYSTEMS

23

C4) Cheque clearinghouse settlement risk controls Yes No

Does the cheque clearinghouse have a specific settlement risk management framework? C4 If No, skip to C5

If Yes, Yes No

a. In the event a participant is unable to settle its debit position, an unwinding procedure would be initiated

C4a

b. Participants have access to information during the day on their preliminary position in the clearinghouse

C4b

c. There are limits in place to protect netting systems from significant exposures C4c

d. There is a specific guarantee fund in place for the system C4d

e. Risk management mechanisms in place ensure completion of daily settlements in case of the inability to settle by the participant with the largest single settlement obligation

C4e

f. The Central Bank or the operator ultimately provides liquidity to the system C4f

WORLD BANK GLOBAL SYSTEMS SURVEY C – RETAIL PAYMENT SYSTEMS

24

Note to Central Bank: if there is more than one Automated Clearing House (ACH14), please provide separate answers for each ACH.

C5) ACH for direct credits and/or direct debits main features ACH 1 ACH 2 ACH 3

Yes No Yes No Yes No

Is an ACH for direct credits and/or direct debits available in the country? C5_1 C5_2 C5_3 If No, skip to C7

If Yes, Yes No Yes No Yes No

a. The ACH is operated by the Central Bank C5a1 C5a2 C5a3

b. The ACH allows the processing of both direct credits and direct debits

C5b1 C5b2 C5b3

c. Net balances are calculated and settled at least once a day C5c1 C5c2 C5c3

d. Final settlement of net positions takes place through a RTGS system

C5d1 C5d2 C5d3

e. Final settlement takes place in Central Bank money, but not through a RTGS

C5e1 C5e2 C5e3

C6) ACH settlement risk controls ACH 1 ACH 2 ACH 3

Yes No Yes No Yes No

Does the ACH have a specific settlement risk management framework? C6_1 C6_2 C6_3 If No, skip to C7

If Yes, Yes No Yes No Yes No

a. In the event a participant is unable to settle its debit position, an unwinding procedure would be initiated

C6a1 C6a2 C6a3

b. Participants have access to information during the day on their preliminary positions in the clearinghouse

C6b1 C6b2 C6b3

c. There are limits in place to protect netting systems from excessive exposures

C6c1 C6c2 C6c3

d. There is a specific guarantee fund in place for the system C6d1 C6d2 C6d3

e. The guarantee fund ensures completion of the daily settlement in case of inability to settle by the participant with the largest single settlement obligation

C6e1 C6e2 C6e3

f. The Central Bank or the operator provides ultimately liquidity to the system C6f1 C6f2 C6f3

14 An electronic clearing system in which payment orders are exchanged among financial institutions, primarily via magnetic media or telecommunications

networks, and then cleared amongst the participants. All operations are handled by a data processing center. An ACH typically clears credit transfers and

debit transfers, and in some cases also cheques. See also clearing/clearance.

WORLD BANK GLOBAL SYSTEMS SURVEY C – RETAIL PAYMENT SYSTEMS

25

C7) Payment card systems main features SEE TABLE BELOW

a. Which brands dominate the marketplace for payment cards? (Select the answer that applies best from table C7 below) C7a

Yes No

b. There is at least one payment card switch operating in the country? C7b

Table C7. Brands

Local brands dominate the marketplace for payment cards 1

International brands (e.g. Visa, Mastercard) dominate the marketplace 2

C8) Payment card systems: interoperability of ATMs and POS Note: please rank each of the following according to the corresponding table

SEE TABLE BELOW

a. Interoperability15 of ATM systems in the country (Select the answer that applies best from table C8a) C8a

b. Interoperability16 of POS terminals in the country (Select the answer that applies best from table C8a) C8b

c. Payment cards are actually used as payment instruments (and not only for cash withdrawals at ATMs) (Select the

answer that applies the best to your situation from table C8b) C8c

Table C8a. Interoperability Table C8b. Payment cards

Full interoperability 1 Extensively 1

Good interoperability 2 Sometimes 2

Low interoperability 3 Rarely 3

C9) Please indicate which of the following services are provided through ATMs in the country in addition to cash withdrawals Yes No

a. Bill payments C9a

b. Cash deposits C9b

c. Purchases (e.g. tickets, airtime) C9c

d. Credit transfers to other accounts within the same bank C9d

e. Credit transfer to accounts at any other bank C9e

f. Other. Please specify: C9fx C9f

15

In the context of this survey, “full interoperability of ATMs” means that all payment and cash withdrawal cards issued by banks in the country can be used

seamlessly (though probably at a cost) at all ATMs in the country. 16

In the context of this survey, “full interoperability of POS terminals” means that all payment cards issued by banks in the country can be used seamlessly in

any POS terminal in the country.

WORLD BANK GLOBAL SYSTEMS SURVEY C – RETAIL PAYMENT SYSTEMS

26

C10)

How are domestic ATM transactions processed in the country? (Select the answer that applies best from table C10 below) C10

Table C10

Most ATM networks are interconnected, enabling inter-network customer transactions which result in inter-network clearing and settlement 1

All ATM networks are interconnected, enabling inter-network customer transactions which result in inter-network clearing and settlement 2

ATM networks are not interconnected 3

C11)

How are domestic POS transactions processed in the country? (Select the answer that applies best from table C11 below) C11

Table C11

Most POS networks are interconnected, enabling inter-network customer transactions which result in inter-network clearing and settlement 1

All POS networks are interconnected, enabling inter-network customer transactions which result in inter-network clearing and settlement 2

POS networks are not interconnected 3

C12) Interchange fees for payment cards Yes No

a. Authorities consider interchange fees prevailing in the card industry to be high C12a

b. Authorities have taken actions, or are considering taking action to address this issue C12b

c. Authorities have no jurisdiction over interchange fees C12c

d. There have been instances of litigation on interchange fees brought: Yes No

by the government C12d

by merchants C12e

WORLD BANK GLOBAL SYSTEMS SURVEY C – RETAIL PAYMENT SYSTEMS

27

C13) For the three main payment card switches in the country (in terms of volume of transactions) complete the table below

Switch 1 Switch 2 Switch 3

Names: Switch1 Switch2 Switch3

Are the following Transactions supported (authorization, clearing, and settlement)?

Yes No Yes No Yes No

a. POS transactions C13a1 C13a2 C13a3

b. ATM transactions C13b1 C13b2 C13b3

c. Transactions initiated via the internet C13c1 C13c2 C13c3

d. Transactions initiated through other remote channels like mobile phones

C13d1 C13d2 C13d3

e. Funds transfer transactions C13e1 C13e2 C13e3

f. Other. C13f1 C13f2 C13f3

If Other, Please specify: C13f1x C13f2x C13f3x

Which of the following best describes the Ownership Structure? Yes No Yes No Yes No

a. Consortium of a few large banks C13g1 C13g2 C13g3

b. Consortium of a most banks in the country (say 80% of all banks) C13h1 C13h2 C13h3

c. Central Bank C13i1 C13i2 C13i3

d. Other Government bodies. C13j1 C13j2 C13j3

If Other Government bodies, Please specify: C13j1x C13j2x C13j3x

e. Other private sector entities. C13k1 C13k2 C13k3

If Other private sector entities, Please specify: C13k1x C13k2x C13k3x

WORLD BANK GLOBAL SYSTEMS SURVEY C – RETAIL PAYMENT SYSTEMS

28

C13) For the three main payment switches in the country (in terms of volume of transactions) complete the table below

Switch 1 Switch 2 Switch 3

Which of the following best describes the Settlement Features? Yes No Yes No Yes No

a. Final settlement of net positions takes place through a RTGS system C13l1 C13l2 C13l3

b. Final settlement takes place in Central Bank money, but not through a RTGS

C13m1 C13m2 C13m3

c. Final settlement takes place in commercial bank money inside the country

C13n1 C13n2 C13n3

d. Final settlement takes place in another country C13o1 C13o2 C13o3

Which of the following best reflects the Pricing Model? Yes No Yes No Yes No

a. Free of charge C13p1 C13p2 C13p3

b. Partial cost recovery C13q1 C13q2 C13q3

c. Full cost recovery C13r1 C13r2 C13r3

d. Full cost recovery in addition to building a surplus C13s1 C13s2 C13s3

e. Other. C13t1 C13t2 C13t3

If Other, Please specify: C13t1x C13t2x C13t3x

Please indicate if the following Other Services are provided? Yes No Yes No Yes No

a. Gateway for foreign transactions on domestic cards and foreign cards used in the country

C13u1 C13u2 C13u3

b. Operate ATM terminals C13v1 C13v2 C13v3

c. Operate POS terminals C13w1 C13w2 C13w3

d. Manage merchant relationships C13x1 C13x2 C13x3

e. ATM cash management C13y1 C13y2 C13y3

f. Act as counterparty for transactions cleared through the network C13z1 C13z2 C13z3

g. Provide settlement guarantee to merchants C13aa1 C13aa2 C13aa3

h. Provide transaction statistics and related analytical reports C13ab1 C13ab2 C13ab3

i. Conduct market research C13ac1 C13ac2 C13ac3

j. Other. C13ad1 C13ad2 C13ad3

If Other, Please specify: C13ad1x C13ad2x C13ad3x

WORLD BANK GLOBAL SYSTEMS SURVEY C – RETAIL PAYMENT SYSTEMS

29

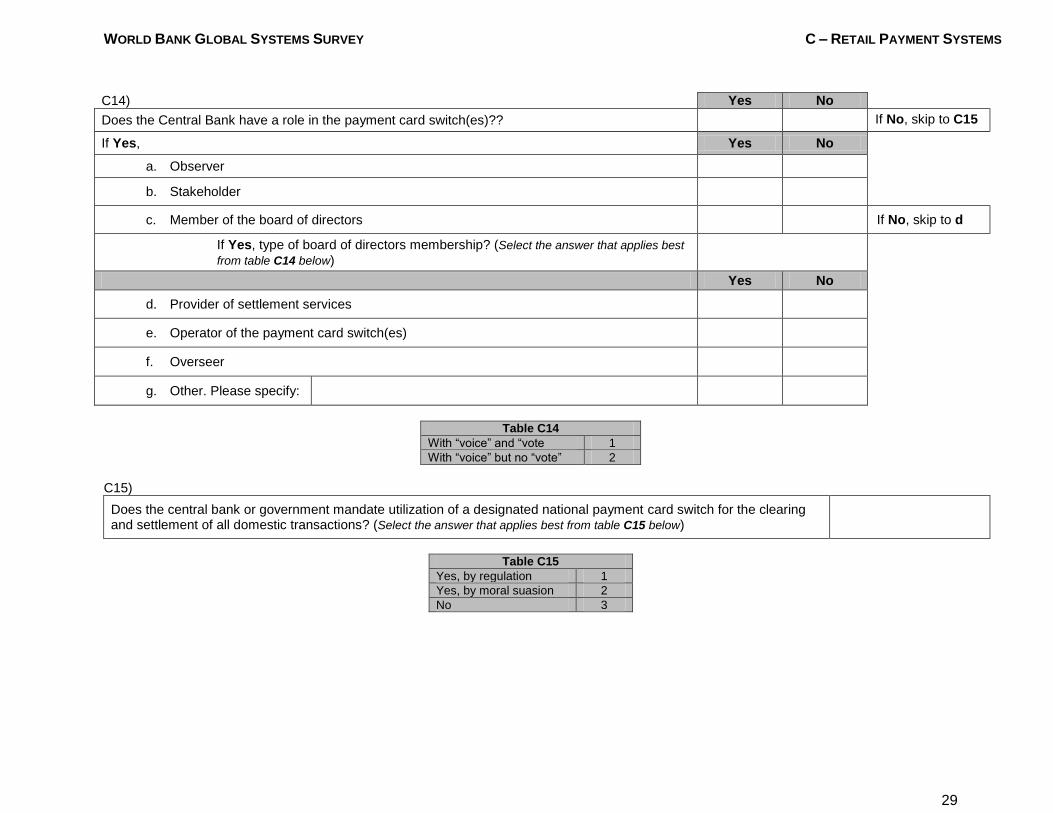

C14) Yes No

Does the Central Bank have a role in the payment card switch(es)?? C14 If No, skip to C15

If Yes, Yes No

a. Observer C14a

b. Stakeholder C14b

c. Member of the board of directors C14c If No, skip to d

If Yes, type of board of directors membership? (Select the answer that applies best

from table C14 below) C14c1

Yes No

d. Provider of settlement services C14d

e. Operator of the payment card switch(es) C14e

f. Overseer C14f

g. Other. Please specify: C14hx C14g

Table C14

With “voice” and “vote 1

With “voice” but no “vote” 2

C15)

Does the central bank or government mandate utilization of a designated national payment card switch for the clearing and settlement of all domestic transactions? (Select the answer that applies best from table C15 below)

C15

Table C15

Yes, by regulation 1

Yes, by moral suasion 2

No 3

WORLD BANK GLOBAL SYSTEMS SURVEY C – RETAIL PAYMENT SYSTEMS

30

C16) Which of the following non-bank institutions issue non-cash payment instruments? Yes No

a. Microfinance institutions C16a If No, skip to b

If Yes, Only supervised microfinance institutions? C16a1

b. Credit cooperatives C16b If No, skip to c

If Yes, Only supervised credit cooperatives? C16b1

c. Savings & loans associations C16c If No, skip to d

If Yes, Only supervised savings & loans associations? C16c1

d. Other financial institutions C16d

e. Postal network C16e

f. Mobile phone operators C16f

g. Other non-financial institutions C16g

h. Other. Please specify: C16hx C16h

WORLD BANK GLOBAL SYSTEMS SURVEY C – RETAIL PAYMENT SYSTEMS

31

C17a)

Provide the average cost in local currency of the following non-cash payment instruments and services for individuals, preferably for the market as a whole, or for the two largest banks/payment service providers? If data on costs is not available please indicate -33; if an item is not applicable please indicate -77; if cost is not significant please indicate -22). Please also indicate the source of information on costs. Select the answer that applies best from table C17 below in order to indicate the source.

AVERAGE COST IN LOCAL

CURRENCY

SOURCE

(see table C17 below) Please specify the local currency: C17x

a. Opening a basic bank current account C17a1 C17a2

b. Maintaining a basic bank current account (annual fees) C17b1 C17b2

c. Direct credits (e.g. wire transfers) C17c1 C17c2

d. Direct debits C17d1 C17d2

e. Cheques C17e1 C17e2

f. Non-reward credit cards: Annual fee C17f1 C17f2

g. Non-reward credit cards: Individual payment transaction C17g1 C17g2

h. Debit cards: Annual fee (if any) C17h1 C17h2

i. Debit cards: Individual payment transaction C17i1 C17i2

j. Pre-paid cards: Purchase fee (if any) C17j1 C17j2

k. Pre-paid cards: Individual payment transaction C17k1 C17k2

l. Pre-paid cards: Re-load (Top-up) C17l1 C17l2

m. ATM cash withdrawals fees: Own bank ATM C17m1 C17m2

n. ATM cash withdrawals fees: Other bank ATM C17n1 C17n2

o. Other ATM services fees: Own bank ATM C17o1 C17o2

p. Other ATM services fees: Other bank ATM C17p1 C17p2

q. Mobile payments: Service subscription fee or equivalent (if any) C17q1 C17q2

r. Mobile payments: Individual payment transactions C17r1 C17r2

s. Mobile payments: Re-load (top-up) C17s1 C17s2

Table C17

Regularly collected data on pricing of payment services for the whole market 1

Average of two largest banks/payment service providers 2

Anecdotal evidence 3

WORLD BANK GLOBAL SYSTEMS SURVEY C – RETAIL PAYMENT SYSTEMS

32

C17b)

What is the lowest available cost of person to person transfers (domestic remittances) in the country? For the purposes of this question, please consider only cash-to-cash services (Select the answer that applies best from table C17b below)

C17b

Table C17b

Between 0% and 1% of the value 1

Between 1% and 2% of the value 2

Between 2% and 5% of the value 3

More than 5% of the value 4

Not applicable -77

C18) Which of the following measures are in place to prevent fraud in payment card systems? Yes No

a. Industry-led standards C18a

b. Common efforts by the banking industry and merchants’ associations C18b

c. Legal requirements applicable to payment service providers/users C18c

d. Other. Please specify: C18dx C18d

WORLD BANK GLOBAL SYSTEMS SURVEY C – RETAIL PAYMENT SYSTEMS

33

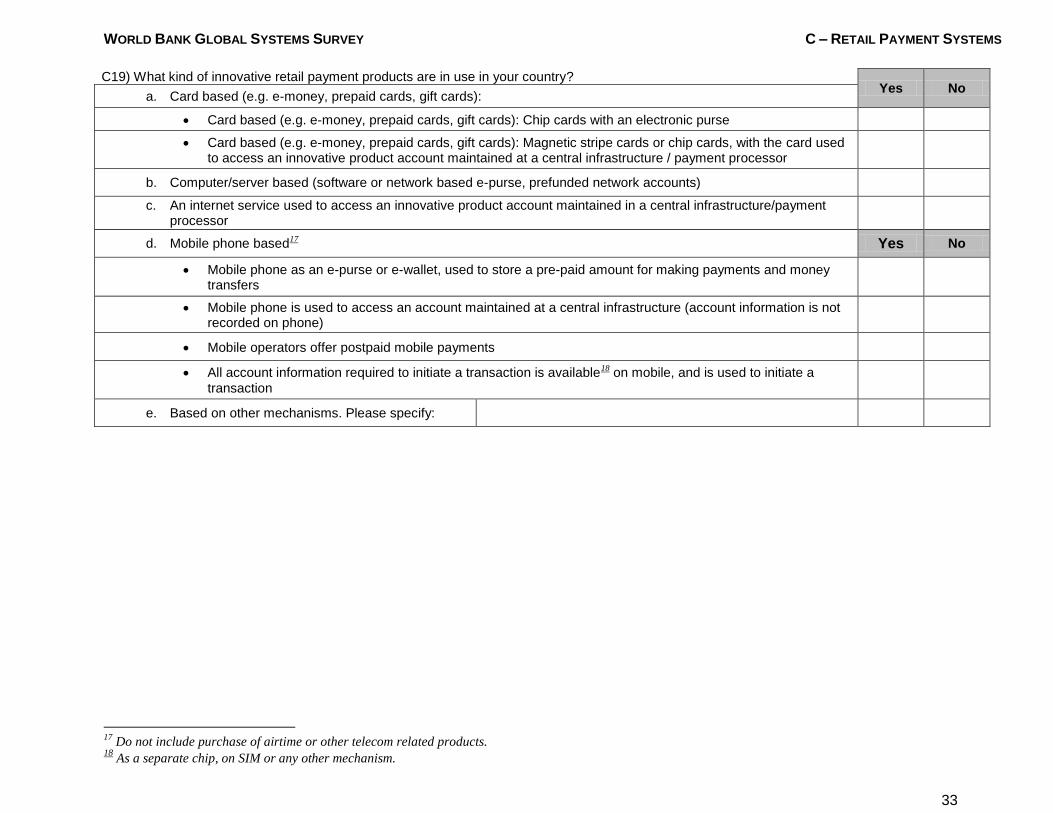

C19) What kind of innovative retail payment products are in use in your country? Yes No

a. Card based (e.g. e-money, prepaid cards, gift cards):

Card based (e.g. e-money, prepaid cards, gift cards): Chip cards with an electronic purse C19a

Card based (e.g. e-money, prepaid cards, gift cards): Magnetic stripe cards or chip cards, with the card used to access an innovative product account maintained at a central infrastructure / payment processor

C19b

b. Computer/server based (software or network based e-purse, prefunded network accounts) C19c

c. An internet service used to access an innovative product account maintained in a central infrastructure/payment processor

C19d

d. Mobile phone based17 Yes No

Mobile phone as an e-purse or e-wallet, used to store a pre-paid amount for making payments and money transfers

C19e

Mobile phone is used to access an account maintained at a central infrastructure (account information is not recorded on phone)

C19f

Mobile operators offer postpaid mobile payments C19g

All account information required to initiate a transaction is available18 on mobile, and is used to initiate a

transaction C19h

e. Based on other mechanisms. Please specify: C19ix C19i

17

Do not include purchase of airtime or other telecom related products. 18

As a separate chip, on SIM or any other mechanism.

WORLD BANK GLOBAL SYSTEMS SURVEY C – RETAIL PAYMENT SYSTEMS

34

C20) Which of the following innovative access channels to a bank account for payment19

purposes (in addition to the traditional use of debit/credit cards) are in use in your country?

Yes No

a. Mobile banking (mobile phone is used to access a bank account) C20a

b. Internet banking (an internet web-site offering certain banking transactions to authenticated customers, enabling them to operate their bank accounts using a computer device connected to internet)

C20b

c. ATM for remote access to operate the bank account (in addition to cash withdrawals or balance enquiries) C20c

d. POS terminals that are magnetic stripe, biometric and chip enabled C20d

e. Other non-bank remote access payment mechanisms – TV based, kiosk, telephone, interactive voice response (IVR) etc.

C20e

C21) Please indicate the trends for innovative retail payment products20

? Yes No

a. Innovative product transactions are growing C21a

b. Innovative product transactions account for more than 5% of traditional electronic retail payments C21b

c. Innovative product transactions are growing at a faster rate than traditional electronic retail payments C21c

d. Innovative product transactions are being used for payments, and not just for safekeeping of money C21d

e. For the majority of innovative product users, the innovative product is the only electronic payment instrument they have access to

C21e

19

For the purpose of this survey, payment – the payer’s transfer of a monetary claim on a party acceptable to the payee – is also used to refer to a transfer e.g.

person-to-person (P2P). 20

For the purposes of this survey, “innovative products” are defined as products that are not based on cheques, traditional credit and debit cards, or

traditional direct credit and debit services. This definition, therefore, captures: prepaid cards, card-based e-money products, and other types of e-money

products including those developed around mobile phones and mobile technology, among others.

WORLD BANK GLOBAL SYSTEMS SURVEY C – RETAIL PAYMENT SYSTEMS

35

C22) Government payments For each category of government payments, please indicate the percentage transmitted via each of the specified instruments? (The total of percentages for each category should sum up to 100%) OR If percentages are not available, kindly rank the payment instruments used for each category of government payments (1 being the most used in terms of number of transactions and 3 being the least used in terms of number of transactions)

PAYMENT INSTRUMENTS

CASH PAPER BASED PAYMENT

INSTRUMENTS-CHEQUES, PAYMENT ORDERS

ELECTRONIC PAYMENT

INSTRUMENTS-PAYMENT

CARDS, EFT, AND OTHER

E-PAYMENT SCHEMES

Government to person payments % Ranking % Ranking % Ranking

a. Public sector salaries C22a1p % C22a1r C22a2p % C22a2r C22a3p % C22a3r =100%

b. Pensions and transfer payments C22b1 p % C22b1r C22b2p % C22b2r C22b3p % C22b3r =100%

c. Cash transfers and social benefits C22c1p % C22c1r C22c2p % C22c2r C22c3p % C22c3r =100%

Person to government payments % Ranking % Ranking % Ranking

d. Taxes C22d1p % C22d1r C22d2p % C22d2r C22d3p % C22d3r =100%

e. Utility payments C22e1p % C22e1r C22e2p % C22e2r C22e3p % C22e3r =100%

f. Payment for services (like driving license, parking

fees, fines, etc.) C22f1p % C22f1r C22f2p % C22f2r C22f3p % C22f3r =100%

Government to business payments % Ranking % Ranking % Ranking

g. Procurement of goods and services C22g1p % C22g1r C22g2p % C22g2r C22g3p % C22g3r =100%

h. Tax refunds C22h1p % C22h1r C22h2p % C22h2r C22h3p % C22h3r =100%

Business to government payments % Ranking % Ranking % Ranking

i. Taxes C22i1p % C22i1r C22i2p % C22i2r C22i3p % C22i3r =100%

j. Utilities C22j1p % C22j1r C22j2p % C22j2r C22j3p % C22j3r =100%

k. Payment for services (like fees for services like

business registration, social security contributions, etc.)

C22k1p % C22k1r C22k2p % C22k2r C22k3p % C22k3r =100%

WORLD BANK GLOBAL SYSTEMS SURVEY C – RETAIL PAYMENT SYSTEMS

36

C23) If government payments are handled mainly through cash or paper-based payment instruments, are there plans to migrate these to electronic payments in the near term? Yes No

a. Government-to-person payments will be migrated to prepaid cards within a year

Public sector salaries C23a

Pensions and transfer payments C23b

Cash transfers and social benefits C23c

b. Government-to-person payments will be migrated within a year to direct deposit to the account of the beneficiary Yes No

Public sector salaries C23d

Pensions and transfer payments C23e

Cash transfers and social benefits C23f

c. For items “a” and “b” of this question, please indicate if the plans to migrate these payments are related to one of the following objectives:

Yes No

the main objective underlying the migration of government-to-person payments to electronic payments is an explicit financial inclusion objective

C23g

the main objective underlying the migration of government-to-person payments to electronic payments is to increase the efficiency of the National Treasury and/or reduce operational costs

C23h

d. Government- to-business payments will be migrated within a year to direct deposit to the account of the beneficiary C23i

e. Payments to the government will be required to be done mostly or solely through the banks (and/or other deposit institutions)

C23j

C24)

Which of the following best describes the processes underlying the disbursement of government payments? (Select the answer

that applies best from table C24 below) C24

Table C24

The Ministry of Finance (through the National Treasury or equivalent) deposits funds to the accounts of the various government agencies, which in turn make the payment to the intended beneficiary

1

The Ministry of Finance (through the National Treasury or equivalent) makes all payments directly to the beneficiary upon request by the executing agency, at least for what concerns payments of the central government

2

C25) Yes No

With regard to collections of the central government (taxes, duties, rights, etc.), are the funds transferred directly to, and concentrated/consolidated at the account of the National Treasury (or equivalent)?

C25

WORLD BANK GLOBAL SYSTEMS SURVEY D – FOREIGN EXCHANGE SETTLEMENT SYSTEMS

37

D1) General Yes No

a. One foreign currency accounts for 90% or more of total Foreign Exchange (FX) transactions D1a

b. The Central Bank offers current account services to banks and/or other institutions in at least one major foreign currency

D1b

c. There are restrictions on FX dealings, and the FX market is not very active D1c

D2) Please provide the following statistical data for the main foreign currency that is traded in the interbank/wholesale market in your country

Traded amounts (in thousands, in the applicable currency)

2012 2011 2010 2009 2008 2007

Please specify the currency: D2x

a. Over the Counter (OTC) market D2a_12 D2a _11 D2a _10 D2a _09 D2a _08 D2a _07

b. Exchange-traded D2b_12 D2b _11 D2b _10 D2b _09 D2b _08 D2b _07

D3) Yes No

Does a centralized21

foreign currency market exist in the country? D3 If No, skip to D4

If Yes, Yes No

a. One foreign currency accounts for 90 % or more of total transactions D3a

b. The Exchange has organized the settlement arrangements for foreign currency deals made at the Exchange

D3b If No, skip to c

If Yes, PVP? (Select the answer that applies best from table D3 below) D3b1 Skip to D4

c. Settlement arrangements are organized bilaterally between the counterparties of a FX deal D3c

Table D3

Settlement of FX deals occurs on a PVP basis solely through settlement accounts at the Central Bank 1

Settlement of FX deals occurs on a PVP basis through a combination of Central Bank (domestic leg) and foreign correspondent banks 2

Settlement of FX deals occurs on a PVP basis solely through local commercial banks and foreign correspondent banks 3

There is no PVP procedure in place 4

21

A centralized market is intended to be a structured arrangement for trading at a central location e.g. an Exchange.

WORLD BANK GLOBAL SYSTEMS SURVEY D – FOREIGN EXCHANGE SETTLEMENT SYSTEMS

38

D4) OTC markets Yes No

a. There is an organized mechanism or procedure for FX trades to be settled on a PVP basis (e.g. a common foreign correspondent bank)

D4a

b. No significant information is available on the risks in the foreign currency market D3b

c. The time lag between the confirmation of settlement of the foreign currency leg and the domestic currency leg? (Select the answer that applies best from table D4 below)

D3c

Table D4. Time lag

Does not exceed 2 hours 1

Exceeds 2 hours but is less than 24 hours 2

Exceeds 24 hours 3

WORLD BANK GLOBAL SYSTEMS SURVEY E – CROSS-BORDER PAYMENTS AND INTERNATIONAL REMITTANCES

39

CROSS-BORDER PAYMENTS

E1) Apart from payment card systems, are there any direct (operational) links between payment systems in your country and payments systems in other countries?

Yes No

a. Local ACH interconnected with ACH in other country/ies. E1a If Yes, Please specify country/ies: E1ax

b. Local ACH interconnected with RTGS in other country/ies. E1b If Yes, Please specify country/ies: E1bx

c. Local RGTS interconnected with RTGS in other country/ies. E1c If Yes, Please specify country/ies: E1cx

d. Other. E1d

If Yes, Please specify payment systems that are interconnected and the country/ies: E1dx

E2) Are there any plans in the pipeline for developing an interconnection of the kinds described above?

Yes No If Yes, Please specify the

kind of interconnection using the table below

If Yes, Please specify

country/ies:

a. Within two years E2a E2a1 E2a1x

b. In more than two years E2b E2b1 E2b1x

Table E2

Local ACH is interconnected with ACH in other country/ies 1

Local ACH is interconnected with RTGS in other country/ies. 2

Local RGTS is interconnected with RTGS in other country/ies 3

Other Please specify payment systems that are interconnected: E2a2x, E2b2x

4

E3)

Use of the international SWIFT network? (Select the answer that applies best from table E3 below) E3

Table E3

90% or more of commercial banks in your country are connected to SWIFT 1

Less than 90% but at least 50% of commercial banks are connected to SWIFT 2

Some banks or other financial institutions can use SWIFT through the Central Bank’s own connection to SWIFT 3

Some banks or other financial institutions can use SWIFT through a SWIFT Service Bureau operated by the Central Bank or another institution 4

WORLD BANK GLOBAL SYSTEMS SURVEY E – CROSS-BORDER PAYMENTS AND INTERNATIONAL REMITTANCES

40

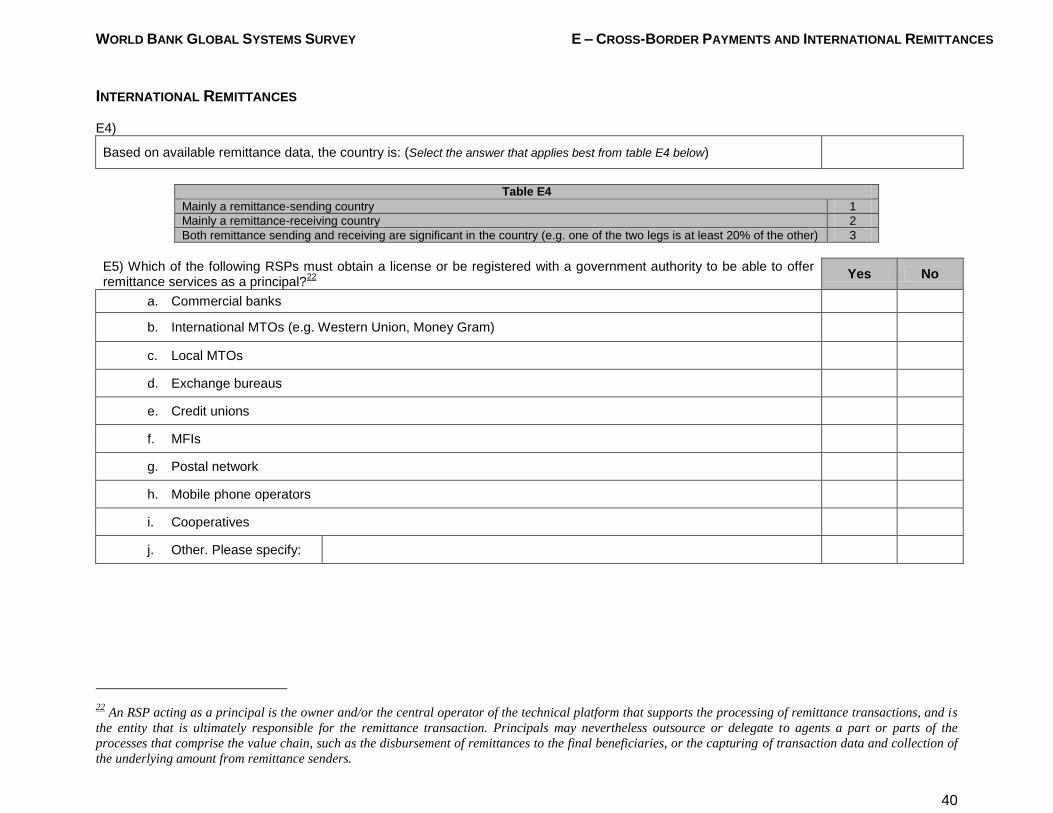

INTERNATIONAL REMITTANCES E4)

Based on available remittance data, the country is: (Select the answer that applies best from table E4 below) E4

Table E4

Mainly a remittance-sending country 1

Mainly a remittance-receiving country 2

Both remittance sending and receiving are significant in the country (e.g. one of the two legs is at least 20% of the other) 3

E5) Which of the following RSPs must obtain a license or be registered with a government authority to be able to offer remittance services as a principal?

22

Yes No

a. Commercial banks E5a

b. International MTOs (e.g. Western Union, Money Gram) E5b

c. Local MTOs E5c

d. Exchange bureaus E5d

e. Credit unions E5e

f. MFIs E5f

g. Postal network E5g

h. Mobile phone operators E5h

i. Cooperatives E5i

j. Other. Please specify: E5jx E5j

22 An RSP acting as a principal is the owner and/or the central operator of the technical platform that supports the processing of remittance transactions, and is

the entity that is ultimately responsible for the remittance transaction. Principals may nevertheless outsource or delegate to agents a part or parts of the

processes that comprise the value chain, such as the disbursement of remittances to the final beneficiaries, or the capturing of transaction data and collection of

the underlying amount from remittance senders.

WORLD BANK GLOBAL SYSTEMS SURVEY E – CROSS-BORDER PAYMENTS AND INTERNATIONAL REMITTANCES

41

E6) Yes No

Is the use of agents of RSPs permitted (e.g. for initiating remittance transactions in case of remittance sending countries or for disbursements to final beneficiaries in case of remittance receiving countries)?

E6 If No, skip to E7

If Yes, which of the following institutions can perform the role of agents of RSPs? Yes No

a. Commercial banks E6a

b. Local MTOs (acting also as agents of international MTOs) E6b

c. Exchange bureaus E6c

d. Credit unions E6d

e. MFIs E6e

f. Postal network E6f

g. Mobile phone operators E6g

h. Retail outlets (supermarket, pharmacies, gas stations) E6h

i. Cooperatives E6i

j. Other. Please specify: E6jx E6j

E7) MOST

IMPORTANT SECOND MOST

IMPORTANT THIRD MOST

IMPORTANT

Please rank the three most important RSPs in your country in terms of market share for initiation of remittance transactions (for remittance sending countries) or disbursement of remittance transactions (for remittance receiving countries) among those listed in the table below. (Select the answer that applies best from table E7 below)

E7a E7b E7c

Table E7

Commercial banks 1

International MTOs (e.g. Western Union, Money Gram) 2

Local MTOs 3

Exchange bureaus 4

Credit unions 5

MFIs 6

Postal network 7

Mobile phone operators 8

Cooperatives 9

Other. Please specify MOST IMPORTANT

SECOND MOST

IMPORTANT THIRD MOST

IMPORTANT 10

E7ax E7bx E7cx

WORLD BANK GLOBAL SYSTEMS SURVEY E – CROSS-BORDER PAYMENTS AND INTERNATIONAL REMITTANCES

42

E8) MOST USED SECOND MOST

USED THIRD MOST

USED

Please indicate the three most used payment mechanisms and instruments (most used, second most used, and third most used) for sending and/or receiving remittances in your country among those listed in the table below. (Select the answer that applies best from table E8 below)

E8a E8b E8c

Table E8

Cash (including via MTOs, banks or other service providers) 1

Cheque or similar payment instrument (e.g. bank drafts, money orders) 2

Account-to-account funds transfers 3

Payment cards linked to a current account in the sending country but which enable the recipient to withdraw cash locally at ATMs 4

Prepaid cards (not linked to a current account) that enable the recipient to withdraw cash locally at ATMs 5

Mobile phone-based payment mechanisms (e.g. m-wallet or mobile phone as access channel to a bank account) 6

Other. Please specify MOST USED SECOND MOST USED THIRD MOST USED

7 E8ax E8bx E8cx

E9) Transparency of remittance services? Yes No

a. RSPs are required by law to disclose fees applied E9a

b. RSPs are subject to different legal requirements as to fees disclosed, depending on the destination country E9b

c. RSPs are required by law to disclose FX rate applied E9c

d. RSPs are required by law to disclose taxes applied E9d

e. RSPs are required by law to disclose speed of the transfer E9e

f. RSPs are required by law to disclose available complaint mechanisms E9f

g. RSPs must inform customers on the details of the transaction before they perform it E9g

h. RSPs must provide customers with receipt containing the details of the transaction E9h

i. A national remittance prices database is available on the internet E9i

E10) Competition environment? Yes No

a. Exclusivity agreements23 are present in the national market for international remittance services E10a

b. Legislation/regulation exists that specifically bans exclusivity agreements in the international remittance market. E10b

c. Legislation exists to address other types of anti-competitive or monopolistic behaviors E10c

d. RSPs have to be incorporated as banks E10d

e. RSPs have to meet stipulated minimum capital requirements E10e

f. Agents are allowed to disburse funds in foreign currency E10f

23 Exclusivity conditions are where an RSP allows its agents or other RSPs to offer its remittance service only on condition that they do not offer

any other remittance service.

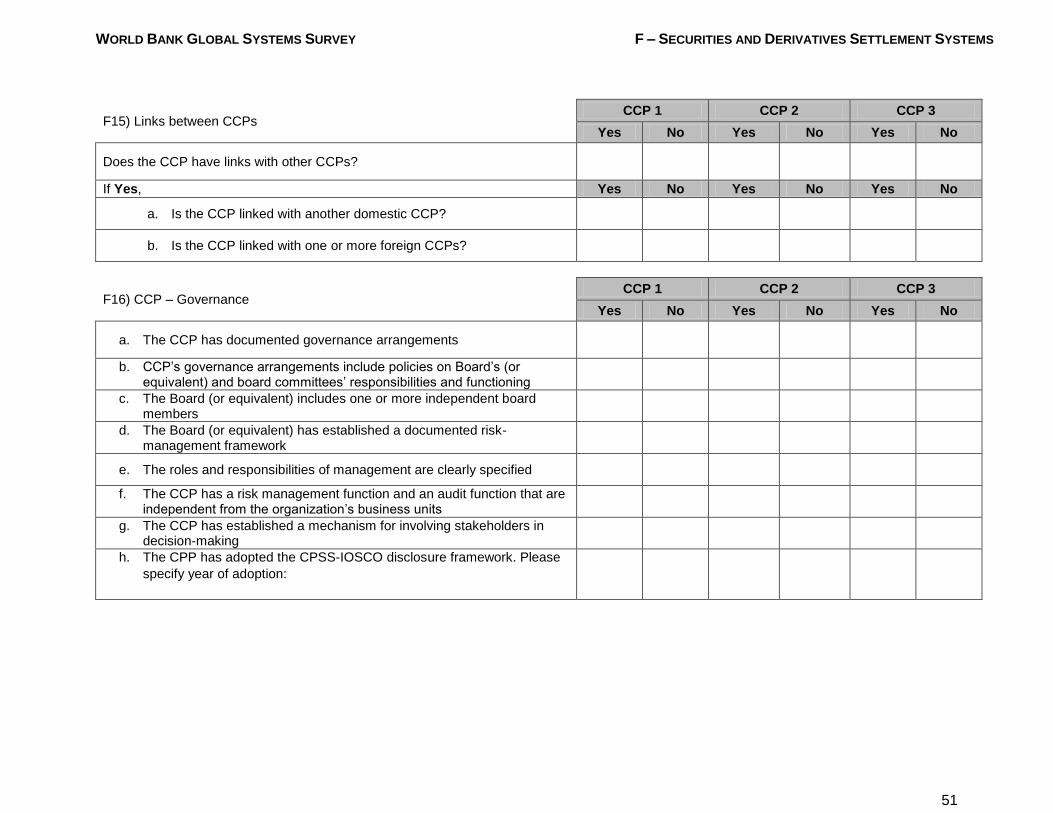

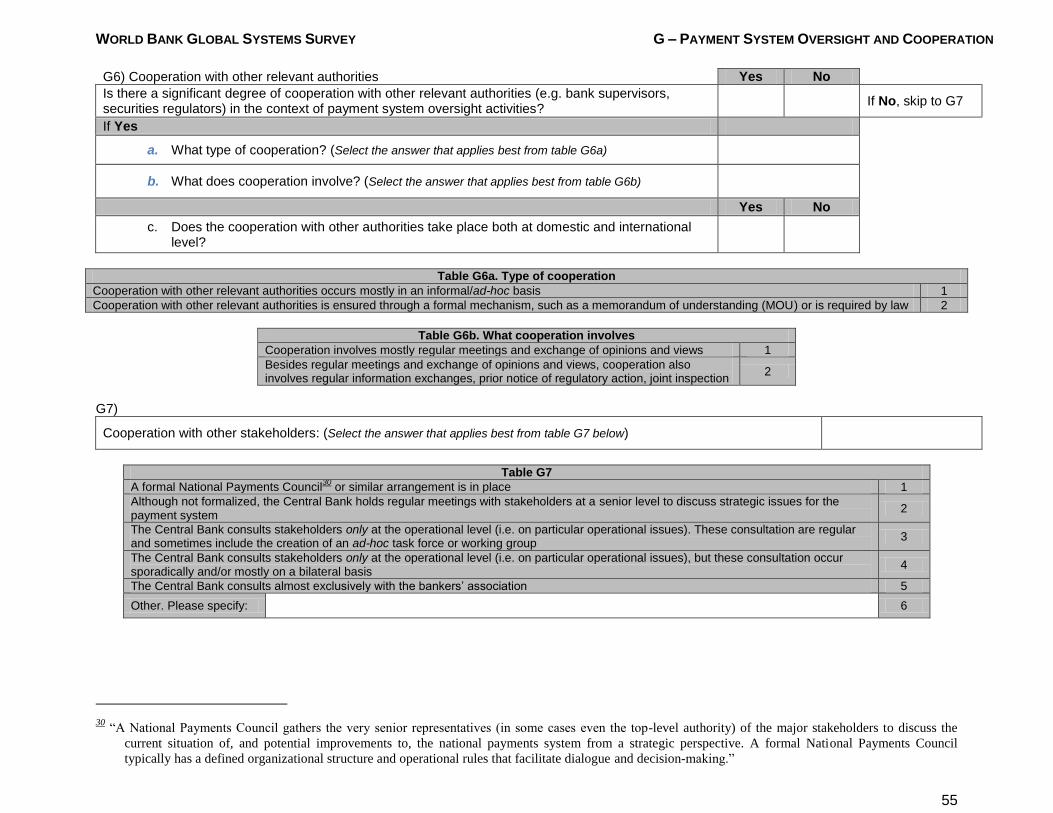

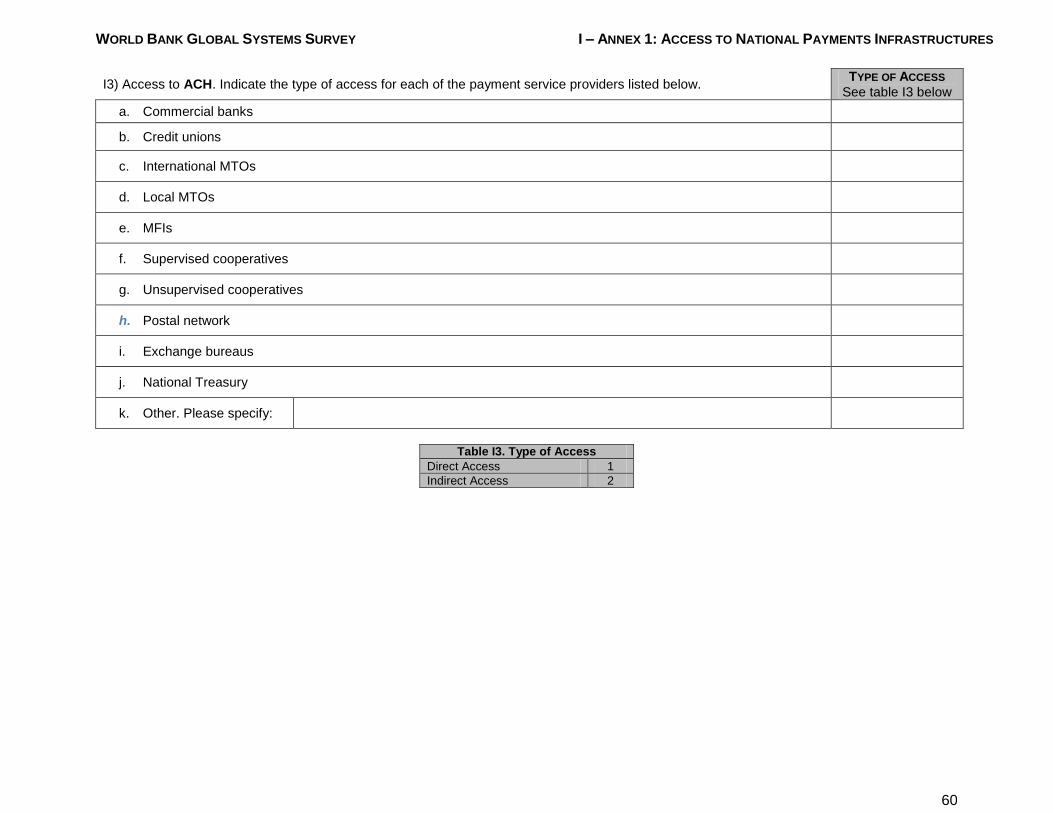

WORLD BANK GLOBAL SYSTEMS SURVEY F – SECURITIES AND DERIVATIVES SETTLEMENT SYSTEMS

43

F1) General features of the securities market Yes No

a. The securities market (government securities, equities, corporate bonds and derivatives) is at a nascent stage, characterized by only a few or none primary issuances, and few or none secondary market trades

F1a

b. One or more stock exchanges are currently operating in the country F1b

c. The great majority (90% or more) of negotiable securities in the country are immobilized or dematerialized in one or more Central Securities Depositories (CSDs)

F1c

SEE TABLE BELOW

d. How many Central Securities Depositories (CSDs) are there in the country? (Select the answer that applies best from table F1 below)

F1d If one or more CSD, answer F2-F5

Yes No

e. There is one or more Central Counterparties (CCPs) operating in the country F1e If one or more CCP, answer F11-F16

f. At least one Securities Settlement System (SSS) does not settle in Central Bank money F1f

g. There is one or more Trade Repositories (TRs) operating in the country F1g If one or more TR, answer F17

Table F1. CSD(s)

None – Not Applicable -77

There is a single CSD for all types of securities in the country 1

There are two or more CSDs, each handling only certain types of securities (e.g. one CSD for securities issued by the private sector, another CSD for government securities, etc.)

2

There are two or more CSDs, each handling all types of securities 3

Note to Central Bank: if there is more than one Central Securities Depositories, please provide separate answers for each CSD

F2) CSD - General Information

CSD 1 CSD 2 CSD 3

Name of CSD: CSD1 CSD2 CSD3

SEE TABLE BELOW SEE TABLE BELOW SEE TABLE BELOW

a. Which type of securities is handled by the CSD? (Select the answer

that applies best from table F2 below) F2a1 F2a2 F2a3

Yes No Yes No Yes No

b. There is more than one SSS for the securities handled by this CSD F2b1 F2b2 F2b3

Table F2. Securities handled

The CSD handles only government securities 1

The CSD handles only corporate securities 2

The CSD handles both government and corporate securities 3

WORLD BANK GLOBAL SYSTEMS SURVEY F – SECURITIES AND DERIVATIVES SETTLEMENT SYSTEMS

44

F3) CSD – Main features CSD 1 CSD 2 CSD 3

Yes No Yes No Yes No

a. Securities are held in physical but immobilized/dematerialized form

F3a1 F3a2 F3a3

b. The CSD is also the official securities registrar F3b1 F3b2 F3b3 If Yes,

skip to c

If No, is daily reconciliation conducted in coordination with other relevant entities?

F3c1 F3b2 F3b3

c. The CSD conducts at least daily reconciliation of the totals of securities issues in the CSD for each issuer (or issuing agent)

F3d1 F3d2 F3d3

d. The CSD prohibits overdrafts and debit balances in securities accounts

F3e1 F3e2 F3e3

e. The CSD ensures segregation between its own assets and the securities of its participants

F3f1 F3f2 F3f3

f. The CSD ensures segregation between the securities belonging to the CSD participants and those belonging to its clients

F3g1 F3g2 F3g3

g. Beneficial owners24 are identified at the individual level in the

CSD (i.e. there are sub-accounts for each individual holding securities operated by the CSD)

F3h1 F3h2 F3h3

F4) Participation in the CSD – Please indicate the types of institutions that can be direct participants in the CSD

CSD 1 CSD 2 CSD 3

Yes No Yes No Yes No

a. Commercial banks F4a1 F4a2 F4a3

b. Brokers-dealers F4b1 F4b2 F4b3

c. Other financial institutions (e.g. mutual fund operators, pension fund operators)

F4c1 F4c2 F4c3

d. Some non-financial institutions F4d1 F4d2 F4d3

24

Beneficial owners refer to the real owners of the securities and include individuals and institutional investors.

WORLD BANK GLOBAL SYSTEMS SURVEY F – SECURITIES AND DERIVATIVES SETTLEMENT SYSTEMS

45

F5) Links between CSDs CSD 1 CSD 2 CSD 3

Yes No Yes No Yes No

Does the CSD have operational links with other CSDs? F51 F52 F53

If Yes, Yes No Yes No Yes No

a. The CSD is linked with another domestic CSD F5a1 F5a2 F5a3

b. The CSD is linked with one or more foreign CSDs F5b1 F5b2 F5b3

Note to Central Bank: if there is more than one Securities Settlement System - SSS25, please provide separate answers for each

SSS

F6) SSS – Main features SSS 1 SSS 2 SSS 3

Name of SSS: SS1 SS2 SSS3

SEE TABLE BELOW SEE TABLE BELOW SEE TABLE BELOW

a. Which type of securities is handled by the SSS? (Select the answer

that applies best from table F6a below) F6a1 F6a2 F6a3

b. The SSS is operated by? (Select the answer that applies best from table

F6b below) F6b1 F6b2 F6b2

Please specify the CSD or Other entity: F6b1x F6b2x F6b2x

Yes No Yes No Yes No

c. The SSS is used regularly to facilitate ownership transfers stemming from secondary market transactions

F6c1 F6c2 F6c3

d. The SSS is used for the clearing and settlement of securities traded at the stock exchange only

F6d1 F6d2 F6d3

e. The SSS is used also for the clearing and settlement of OTC transactions

F6e1 F6e2 F6e3

Table F6a. Securities handled Table F6b. Operated by

The SSS handles only government securities 1 The CSD 1

The SSS handles only corporate securities 2 Other entity 2

The SSS handles both government and corporate securities 3

25 A Securities Settlement System (SSS) enables securities to be transferred and settled by book entry according to a set of predetermined multilateral rules. Such

systems allow transfers of securities either free of payment or against payment. An SSS may be organized to provide additional securities clearing and

settlement functions, such as the confirmation of trade and settlement instructions.

WORLD BANK GLOBAL SYSTEMS SURVEY F – SECURITIES AND DERIVATIVES SETTLEMENT SYSTEMS

46

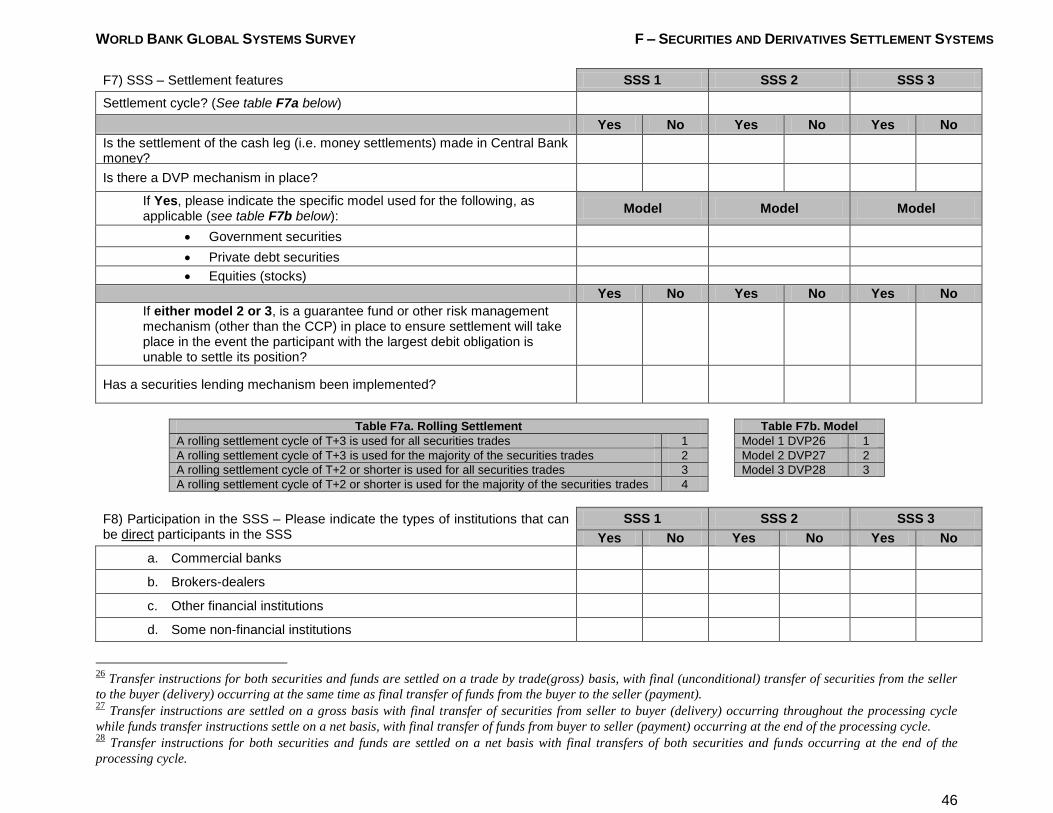

F7) SSS – Settlement features SSS 1 SSS 2 SSS 3

Settlement cycle? (See table F7a below) F7a1 F7a2 F7a3

Yes No Yes No Yes No

Is the settlement of the cash leg (i.e. money settlements) made in Central Bank money?

F7b1 F7b2 F7b3

Is there a DVP mechanism in place? F7c1 F7c2 F7c3

If Yes, please indicate the specific model used for the following, as applicable (see table F7b below):

Model Model Model

Government securities F7d1 F7d2 F7d3

Private debt securities F7e1 F7e2 F7e3

Equities (stocks) F7f1 F7f2 F7f3

Yes No Yes No Yes No

If either model 2 or 3, is a guarantee fund or other risk management mechanism (other than the CCP) in place to ensure settlement will take place in the event the participant with the largest debit obligation is unable to settle its position?

F7g1 F7g2 F7g3

Has a securities lending mechanism been implemented? F7h1 F7h2 F7h3

Table F7a. Rolling Settlement Table F7b. Model

A rolling settlement cycle of T+3 is used for all securities trades 1 Model 1 DVP26 1

A rolling settlement cycle of T+3 is used for the majority of the securities trades 2 Model 2 DVP27 2

A rolling settlement cycle of T+2 or shorter is used for all securities trades 3 Model 3 DVP28 3

A rolling settlement cycle of T+2 or shorter is used for the majority of the securities trades 4

F8) Participation in the SSS – Please indicate the types of institutions that can be direct participants in the SSS

SSS 1 SSS 2 SSS 3

Yes No Yes No Yes No

a. Commercial banks F8a1 F8a2 F8a3

b. Brokers-dealers F8b1 F8b2 F8b3

c. Other financial institutions F8c1 F8c2 F8c3

d. Some non-financial institutions F8d1 F8d2 F8d3

26

Transfer instructions for both securities and funds are settled on a trade by trade(gross) basis, with final (unconditional) transfer of securities from the seller

to the buyer (delivery) occurring at the same time as final transfer of funds from the buyer to the seller (payment). 27

Transfer instructions are settled on a gross basis with final transfer of securities from seller to buyer (delivery) occurring throughout the processing cycle