special topics chapter 7

DESCRIPTION

Special Topics chapter 7TRANSCRIPT

Rangarajan K. Sundaram Derivatives: Principles & Practice 1Copyright © 2011 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

Rangarajan K. Sundaram Derivatives: Principles & Practice 2

Chapter 7. Introduction to Options Rangarajan K. Sundaram

Stern School of Business New York University

Rangarajan K. Sundaram Derivatives: Principles & Practice 3

Outline

Introduction

Naked Option Positions

Options and Views on Direction

Options and Views on Volatility

Putting it Together ...

Summary

Rangarajan K. Sundaram Derivatives: Principles & Practice 4

Introduction

Rangarajan K. Sundaram Derivatives: Principles & Practice 5

Objectives

This segment is an introduction to options. It Examines "naked" option positions and their payoffs. Shows that every naked option position has an implicit view

on Direction. Volatility.

In particular, this segment introduces what is special about options compared to "linear" derivatives like forwards and futures.

Chapter 8 complements this material with a discussion of basic trading strategies using options.

Rangarajan K. Sundaram Derivatives: Principles & Practice 6

Options: Basic Definitions

An option is a financial security that gives the holder the right to buy or sell a specified quantity of a specified asset at a specified price on or before a specified date. Buy = Call option. Sell = Put option On/before: American. Only on: European Specified price = Strike or exercise price Specified date = Maturity or expiration date Specified asset = "underlying" Buyer = holder = long position Seller = writer = short position

Rangarajan K. Sundaram Derivatives: Principles & Practice 7

Broad Categories of Options

Exchange-traded options: Stocks (American). Futures (American). Indices (European & American) Currencies (European and American)

OTC options: Vanilla (standard calls/puts as defined above). Exotic (everything else—for example, Asians, barriers,

digitals, forward-starts, quant's). Others (e.g., embedded options).

Callable bonds. Convertible bonds.

Rangarajan K. Sundaram Derivatives: Principles & Practice 8

Options as Financial Insurance

Option provides financial insurance.The holder of the option has the right, but not

the obligation, to take part in the trade specified in the option.

This right will be exercised only if it is in the holder's interest to do so.

This means the holder can profit, but cannot lose, from the exercise decision.

Rangarajan K. Sundaram Derivatives: Principles & Practice 9

Put Options as Insurance: Example

Cisco stock is currently at $24.75. An investor plans to sell Cisco stock she holds in a month's time, and is concerned that the price could fall over that period.

Buying a one-month put option on Cisco with a strike of K will provide her with insurance against the price falling below K.

For example, suppose she buys a one-month put with a strike of K = 22.50.

If the price falls below $22.50, the put can be exercised and the stock sold for $22.50.

If the price increases beyond $22.50, the put can be allowed to lapse and the stock sold at the higher price.

In general, puts provide potential sellers of the underlying with insurance against declines in the underlying's price.

The higher the strike (or the longer the maturity), the greater the amount of insurance provided by the put.

Rangarajan K. Sundaram Derivatives: Principles & Practice 10

Call Options as Insurance: Example

Apple stock is currently trading at $218. An investor is planning to buy the stock in a month's time, and is concerned that the price could rise sharply over that period.

Buying a one-month call on Apple with a strike of K protects the investor from an increase in Apple's price above K.

For example, suppose he buys a one-month call with a strike of K = 225.

If the price increases beyond $225, the call can be exercised and the stock purchased for $225.

If the price falls below $225, the option can be allowed to lapse and the stock purchased at the lower price.

In general, calls provide potential buyers of the underlying with protection against increases in the underlying's price.

The lower the strike (or the longer the maturity), the greater the amount of insurance provided by the call.

Rangarajan K. Sundaram Derivatives: Principles & Practice 11

The Provider of this Insurance

The writer of the option provides this insurance to the holder.

The writer is obligated to take part in the trade if the holder should so decide.

In exchange, writer receives a fee called the option price or the option premium.

Rangarajan K. Sundaram Derivatives: Principles & Practice 12

Outline of Material

In this first segment on options, we: Review definitions in more detail. Examine payoff structures for "naked" option

positions. Identify why volatility is a primary determinant of

option values. Complementing this material, Chapter 8 looks at basic

trading strategies using options.

Rangarajan K. Sundaram Derivatives: Principles & Practice 13

Naked Option Positions

Rangarajan K. Sundaram Derivatives: Principles & Practice 14

"Naked" Option Positions

A "naked" option position is a portfolio consisting only of options of a given type (i.e., calls or puts).

There are four kinds of naked option positions: Long call. Short call. Long put. Short put.

We examine each in turn.

Rangarajan K. Sundaram Derivatives: Principles & Practice 15

Call Option Payoffs

Consider a call with a strike price of K = 100. Let ST denote the price of the underlying at maturity. Gross payoffs to long and short positions at maturity:

Rangarajan K. Sundaram Derivatives: Principles & Practice 16

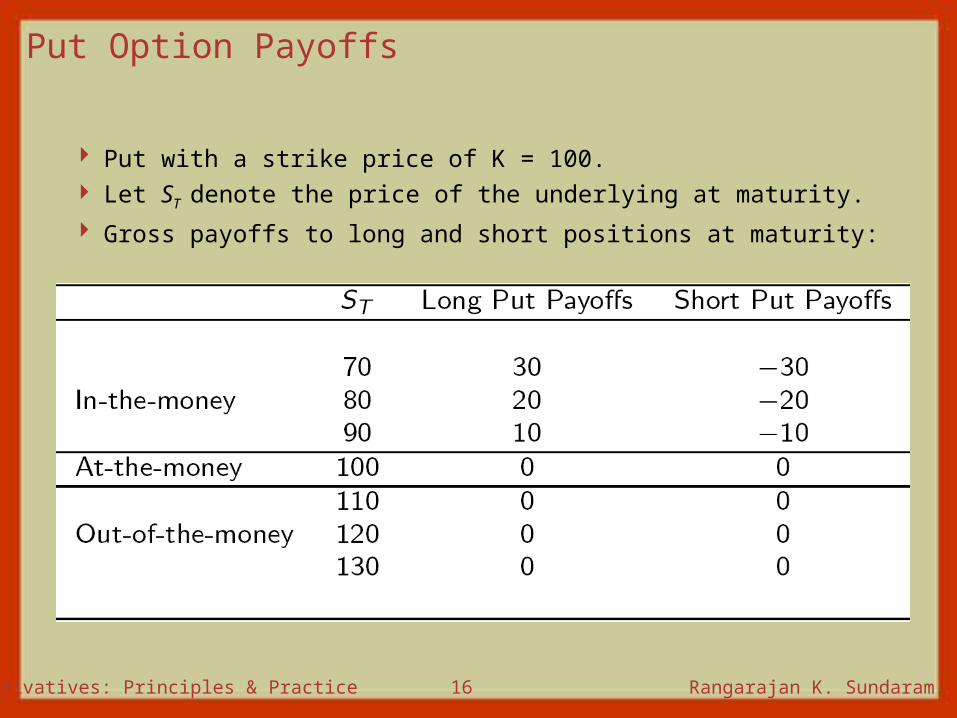

Put Option Payoffs

Put with a strike price of K = 100. Let ST denote the price of the underlying at maturity. Gross payoffs to long and short positions at maturity:

Rangarajan K. Sundaram Derivatives: Principles & Practice 17

Options and Views on Direction

Rangarajan K. Sundaram Derivatives: Principles & Practice 18

Options and Direction

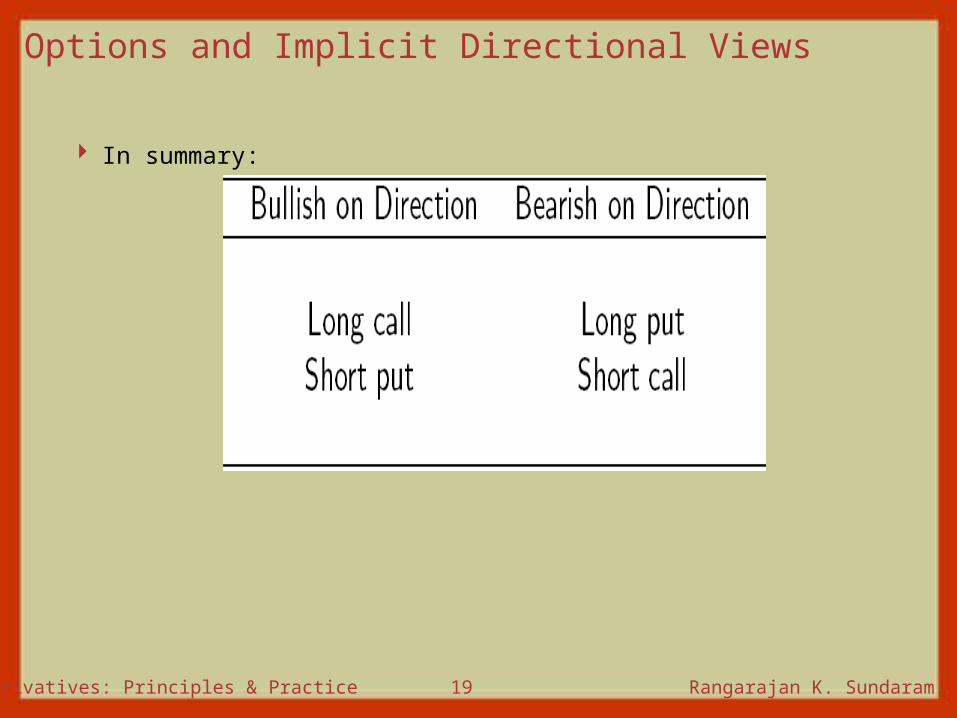

Every naked option position embodies a view on direction.

Long calls and short puts are both bullish positions. Both positions make money if markets go up. Neither is a sensible strategy if one anticipates

markets going down. Short calls and long puts are both bearish

positions. Both positions make money if markets go down. Neither is a sensible strategy if one anticipates

markets going up. Of course, there are important differences in the

nature of the cash flows from these strategies.

Rangarajan K. Sundaram Derivatives: Principles & Practice 19

Options and Implicit Directional Views

In summary:

Rangarajan K. Sundaram Derivatives: Principles & Practice 20

Options and Views on Volatility

Rangarajan K. Sundaram Derivatives: Principles & Practice 21

Options and Volatility

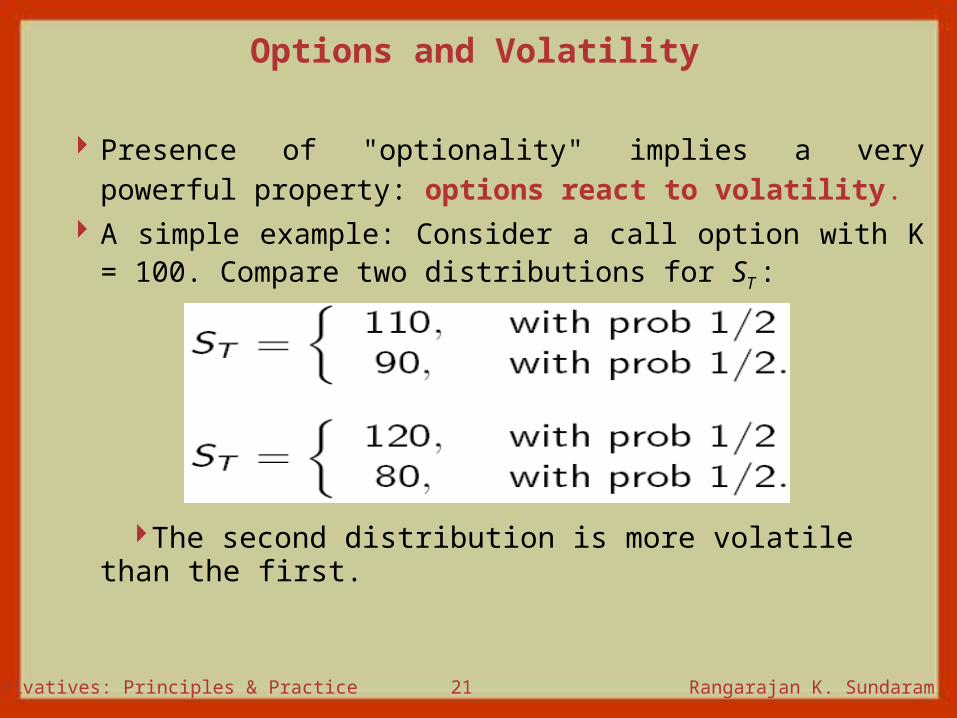

Presence of "optionality" implies a very powerful property: options react to volatility.

A simple example: Consider a call option with K = 100. Compare two distributions for ST :

The second distribution is more volatile than the first.

Rangarajan K. Sundaram Derivatives: Principles & Practice 22

Optionality + Volatility = Superior Payoffs

In the presence of optionality, the higher volatility translates to superior payoffs to the option holder:

Note the important role of "optionality:" without it, the second distribution is not necessarily better (think of a forward, for example).

Rangarajan K. Sundaram Derivatives: Principles & Practice 23

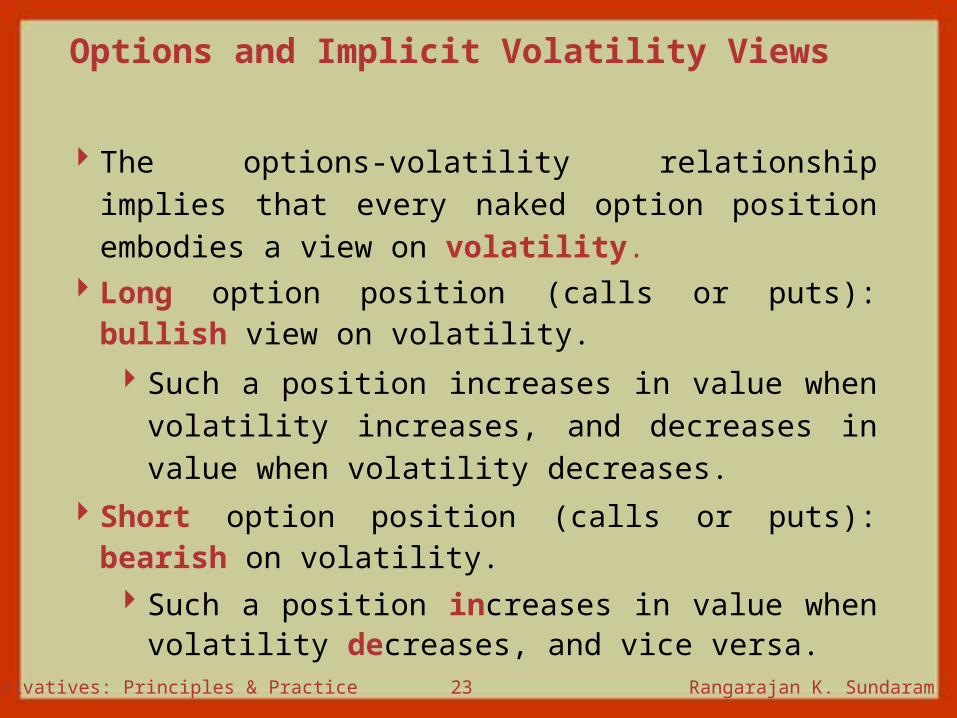

Options and Implicit Volatility Views

The options-volatility relationship implies that every naked option position embodies a view on volatility.

Long option position (calls or puts): bullish view on volatility. Such a position increases in value when

volatility increases, and decreases in value when volatility decreases.

Short option position (calls or puts): bearish on volatility. Such a position increases in value when

volatility decreases, and vice versa.

Rangarajan K. Sundaram Derivatives: Principles & Practice 24

Putting it Together …

Rangarajan K. Sundaram Derivatives: Principles & Practice 25

Options, Direction, and Volatility

► Combining these observations, every naked option position can be seen to be a unique combination of views on direction and volatility.

Rangarajan K. Sundaram Derivatives: Principles & Practice 26

The "Specialness" of Options

These observations highlight a fundamental difference between options and spot/futures/forwards.

We can exploit views on direction with spot/futures/forwards also. Bullish on direction Long spot/futures/forwards. Bearish on direction Short

spot/futures/forwards. However, there is no obvious way to exploit views on

volatility using spot or futures/forwards. Options even permit pure volatility plays where there

is no view on direction but there is a view on volatility.

Rangarajan K. Sundaram Derivatives: Principles & Practice 27

Summary

Rangarajan K. Sundaram Derivatives: Principles & Practice 28

Summary

This chapter has looked at naked option positions and their implied views on market direction and market volatility.

Main observation: each naked option position is a unique combination of views of market direction and market volatility. Long calls: Bullish on direction and volatility. Long puts: Bearish on direction, bullish on volatility. Short calls: Bearish on direction and volatility. Short puts: Bullish on direction, bearish on volatility.

In the next chapter, we examine a range of "trading strategies" using options. Each of these strategies exploits these implied views to set up a portfolio that reflects a specific view on direction and volatility.

Rangarajan K. Sundaram Derivatives: Principles & Practice 29

ExamplesStock XYZ is trading at $47.89 per share DEC 50 Call is

trading at $1.25 premium Investor A ("A") forecasts that XYZ will not trade above $50 per share before December, so A sells the 10 DEC 50 Calls for $1,250 (each option contract controls 100 shares). A doesn't buy the stock, therefore A's investment is considered naked.

Meanwhile, Investor B ("B") forecasts that XYZ will go above $50 per share before December, so B purchases those 10 calls from A for $1,250. At expiration of the option, consider 4 different scenarios where the share price drops, stays the same, rises moderately or surges.

Assuming there are no other costs or taxes affecting the contract, when A) the date is December 1 or B) prices rise above $50, one of two general things happen: 1) B makes a 100% loss, 2) B profits by the same amount of A's net loss.

The following are four scenarios for the example:

Rangarajan K. Sundaram Derivatives: Principles & Practice 30

ExamplesScenario 1Stock drops to $43.25 DEC 50 Call expires worthless A

keeps the entire premium of $1,250.00 B makes a 100% loss

Scenario 2Stock stays at $47.89 DEC 50 Call expires worthless A

keeps the entire premium of $1,250.00 B makes a 100% loss

Scenario 3Stock rises to $52.45 DEC 50 Call is exercised A is forced

to buy 1,000 shares of XYZ for $52,450 and immediately sell them at $50,000 for a loss of $2,450. Since A received the premium of $1,250 before, A's net loss is $1,200. B buys 1,000 shares of XYZ for $50,000 and now is able to sell them at open market for $52.45 per share, if B so chooses. B's net gain is $1,200.00 (same as A's loss excluding commission costs)

Rangarajan K. Sundaram Derivatives: Principles & Practice 31

Scenario 4Stock surges to $75.00 on a news announcement. DEC

50 Call is exercised. A is forced to buy 1,000 shares of XYZ for $75,000 and immediately sell them at $50,000 for a loss of $25,000. Since A received the premium of $1,250 before, A's net loss is $23,750. B buys 1,000 shares for $50,000 and paid the premium of $1,250 before. These shares are now worth $75,000 on the open market. B's net gain is $23,750 (same as A's loss, if commission costs are omitted)