spiceland, chapter 3 - texas tech universityqlynn.ba.ttu.edu/acct 3304/3304ch5kieso1… · ppt...

TRANSCRIPT

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-1

Balance Sheet and Statement of Cash Flows

Chapter 5

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-2

Evaluating the capital structure.Assess risk and future cash flows.Analyze the company’s: Liquidity, Solvency, and Financial flexibility.

Balance SheetUsefulness of the Balance Sheet

LO 1 Explain the uses and limitations of a balance sheet.

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-3

Most assets and liabilities are reported at historical cost.Use of judgments and estimates.Many items of financial value are omitted.

Limitations of the Balance Sheet

LO 1 Understand the uses and limitations of an income statement.

Balance Sheet

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-4

Resources (Assets)

Claims against resources (Liabilities)

Remaining claims accruing to owners

(Owners’ Equity)

Balance Sheet

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-5

Current AssetsCash

ReceivablesInventories

Prepayments

Will be converted to cash or

consumed within one year or the operating cycle,

whichever is longer.

Current Assets

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-6

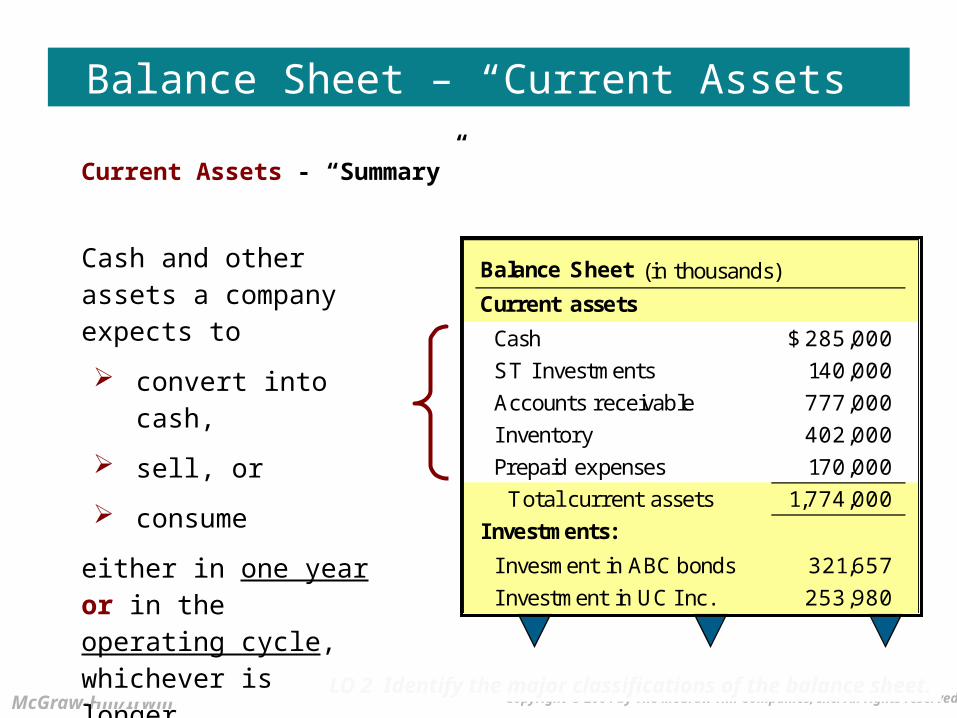

Current Assets - “Summary”

LO 2 Identify the major classifications of the balance sheet.

Balance Sheet (in thousands)Current assetsCash 285,000$ ST I nvestments 140,000 Accounts receivable 777,000 I nventory 402,000 Prepaid expenses 170,000 Total current assets 1,774,000

Investments:I nvesment in ABC bonds 321,657 I nvestment in UC I nc. 253,980

Balance Sheet – “Current Assets”

Cash and other assets a company expects to convert into cash, sell, or consume

either in one year or in the operating cycle, whichever is longer.

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-7

Claims held against customers and others for money, goods, or services.

Accounts receivable – oral promisesNotes receivable – written promises

Major categories of receivables should be shown in the balance sheet or the related notes.

Receivables

LO 2 Identify the major classifications of the balance sheet.

Balance Sheet – “Current Assets”

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-8

Accounts Receivable – Presentation Options

LO 2 Identify the major classifications of the balance sheet.

Balance Sheet – “Current Assets”

Current Assets:Cash $ 346Accounts receivable 500 Less allowance for doubtful accounts 25 475Inventory 812Total current assets $1,633

Current Assets:Cash $ 346Accounts receivable, net of $25 allowance 475 Inventory 812Total current assets $1,633

1

2

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-9

Non-Current AssetsInvestments and

FundsProperty, Plant, &

EquipmentIntangibles

OtherNot expected to be converted to cash

or consumed within one year or

the operating cycle, whichever is

longer

Noncurrent Assets

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-10

Long-Term Investments

Securities I nvestments:

I nvesment in ABC bonds 321,657 I nvestment in UC I nc. 253,980 Notes receivable 150,000 Land held f or speculation 550,000 Sinking f und 225,000 Pension f und 653,798 Cash surrender value 84,321 I nvestment in Uncon. Sub. 457,836

Total investments 2,696,592 Property, Plant, and Equip.

Building 1,375,778 Land 975,000

LO 2 Identify the major classifications of the balance sheet.

Balance Sheet – “Noncurrent Assets”

bonds, stock, and long-term notesFor marketable securities,

management’s intent determines current or noncurrent classification.

Balance Sheet (in thousands)Current assets

Cash 285,000$

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-11

Fixed Assets I nvestments:

I nvesment in ABC bonds 321,657 I nvestment in UC I nc. 253,980 Notes receivable 150,000 Land held f or speculation 550,000 Sinking f und 225,000 Pension f und 653,798 Cash surrender value 84,321 I nvestment in Uncon. Sub. 457,836

Total investments 2,696,592 Property, Plant, and Equip.

Building 1,375,778 Land 975,000

LO 2 Identify the major classifications of the balance sheet.

Balance Sheet – “Noncurrent Assets”

Land held for speculation

Long-Term Investments Balance Sheet (in thousands)Current assets

Cash 285,000$

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-12

Special Funds I nvestments:

I nvesment in ABC bonds 321,657 I nvestment in UC I nc. 253,980 Notes receivable 150,000 Land held f or speculation 550,000 Sinking f und 225,000 Pension f und 653,798 Cash surrender value 84,321 I nvestment in Uncon. Sub. 457,836

Total investments 2,696,592 Property, Plant, and Equip.

Building 1,375,778 Land 975,000

LO 2 Identify the major classifications of the balance sheet.

Balance Sheet – “Noncurrent Assets”

Sinking fundPensions fundCash surrender value of life insurance

Long-Term Investments Balance Sheet (in thousands)Current assets

Cash 285,000$

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-13

Nonconsolidated Subsidiaries or Affiliated Companies

I nvestments:I nvesment in ABC bonds 321,657 I nvestment in UC I nc. 253,980 Notes receivable 150,000 Land held f or speculation 550,000 Sinking f und 225,000 Pension f und 653,798 Cash surrender value 84,321 I nvestment in Uncon. Sub. 457,836

Total investments 2,696,592 Property, Plant, and Equip.

Building 1,375,778 Land 975,000

LO 2 Identify the major classifications of the balance sheet.

Balance Sheet – “Noncurrent Assets”

Long-Term Investments Balance Sheet (in thousands)Current assets

Cash 285,000$

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-14

Property, Plant, and Equipment

Total investments 2,696,592 Property, Plant, and Equip.

Building 1,375,778 Land 975,000 Machinery and equipment 234,958 Capital leases 384,650 Leasehold improvements 175,000 Accumulated depreciation (975,000)

Total PP&E 2,170,386 I ntangibles

Goodwill 3,000,000 Patents 177,000 Trademarks 40,000

LO 2 Identify the major classifications of the balance sheet.

Balance Sheet – “Noncurrent Assets”

Assets of a durable nature used in the regular operations of the business.

Balance Sheet (in thousands)Current assets

Cash 285,000$

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-15

Intangibles

Accumulated depreciation (975,000) Total PP&E 2,170,386

I ntangiblesGoodwill 2,000,000 Patents 177,000 Trademark 40,000 Franchises 125,000 Copyright 55,000

Total intangibles 2,397,000 Other assets

Prepaid pension costs 133,000 Def erred income tax 40,000

Total other 173,000

LO 2 Identify the major classifications of the balance sheet.

Balance Sheet – “Noncurrent Assets”

Lack physical substance and are not financial instruments.

Limited life intangibles amortized.Indefinite-life intangibles tested for impairment.

Balance Sheet (in thousands)Current assets

Cash 285,000$

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-16

Other Assets

I ntangiblesGoodwill 2,000,000 Patents 177,000 Trademark 40,000 Franchises 125,000 Copyright 55,000

Total intangibles 2,397,000 Other assets

Prepaid pension costs 133,000 Def erred income tax 40,000

Total other 173,000 Total Assets 9,210,978$

LO 2 Identify the major classifications of the balance sheet.

Balance Sheet – “Noncurrent Assets”

This section should include only unusual items sufficiently different from assets in the other categories.

Balance Sheet (in thousands)Current assets

Cash 285,000$

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-17

Current LiabilitiesAccounts Payable

Notes PayableAccrued Liabilities

Current Maturities of Long-Term Debt

Obligations expected to be

satisfied through current assets or creation of other current liabilities

Current Liabilities

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-18

“Obligations that a company reasonably expects to liquidate either through the use of current assets or the creation of other current liabilities.”

LO 2 Identify the major classifications of the balance sheet.

Balance Sheet

Current Liabilities Balance Sheet (in thousands)Current liabilitiesAccounts payable 233,450$ Notes payable 131,800 Accrued compensation 43,000 Unearned revenue 17,000 I ncome tax payable 23,400 Current maturities LT debt 121,000 Total current liabilities 569,650

Long- term liabilitiesLong-term debt 979,500 Obligations capital lease 345,800 Def erred income taxes 77,909 Total long-term liabilities 1,403,209

Stockholders' equity

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-19

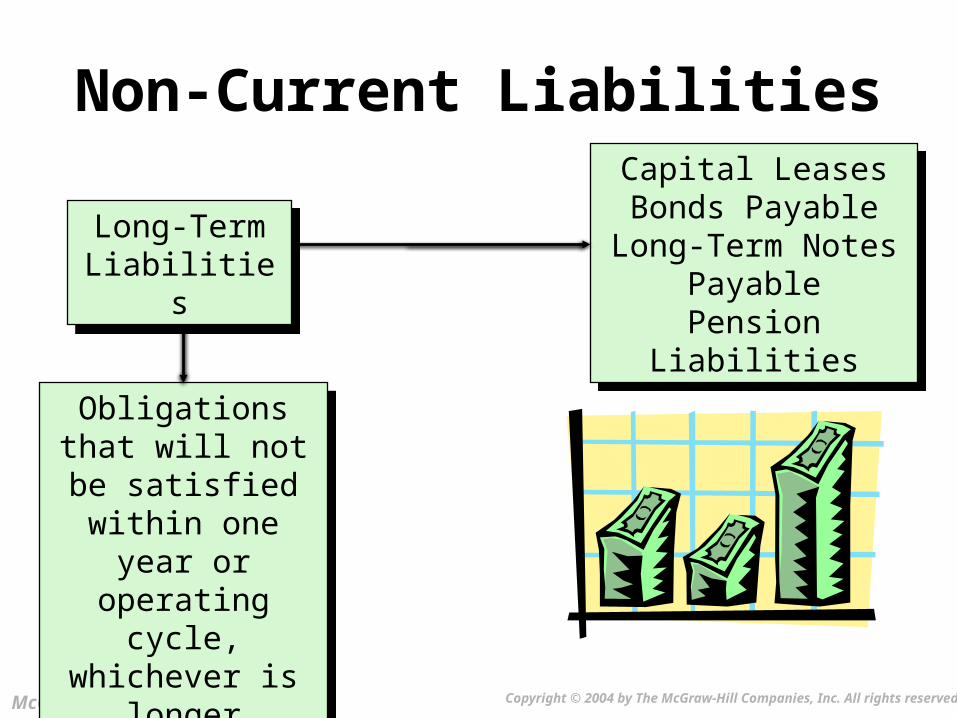

Non-Current LiabilitiesCapital LeasesBonds Payable

Long-Term Notes Payable

Pension Liabilities

Obligations that will not be satisfied within one year or operating cycle,

whichever is longer

Long-Term Liabilities

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-20

LO 2 Identify the major classifications of the balance sheet.

Balance Sheet

Balance Sheet (in thousands)Current liabilitiesAccounts payable 233,450$ Notes payable 131,800 Accrued compensation 43,000 Unearned revenue 17,000 I ncome tax payable 23,400 Current maturities LT debt 121,000 Total current liabilities 569,650

Long- term liabilitiesLong-term debt 979,500 Obligations capital lease 345,800 Def erred income taxes 77,909 Total long-term liabilities 1,403,209

Stockholders' equity

“Obligations that a company does not reasonably expect to liquidate within the normal operating cycle.”

All covenants and restrictions must be disclosed.

Long-Term Liabilities

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-21

Shareholders’ Equity

Capital Stock

Retained Earnings

Treasury Stock

Other Contributed

Capital

Accumulated Other Comprehensive Income

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-22

Now, let’s look at some ratios!

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-23

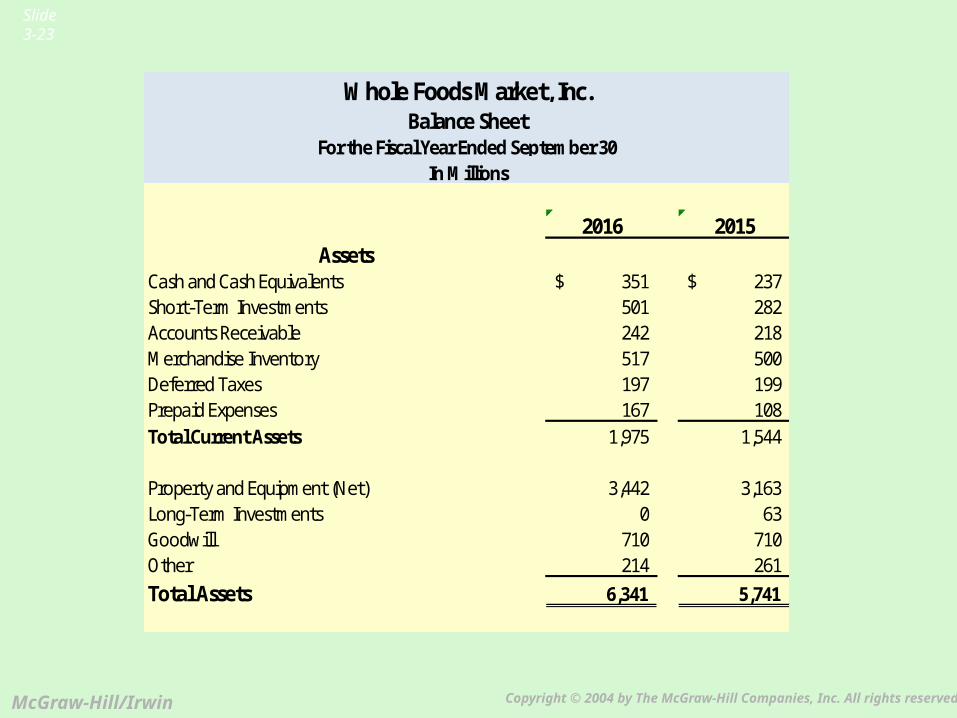

2016 2015Assets

Cash and Cash Equivalents 351$ 237$ Short-Term Investments 501 282Accounts Receivable 242 218Merchandise Inventory 517 500Deferred Taxes 197 199Prepaid Expenses 167 108Total Current Assets 1,975 1,544

Property and Equipment (Net) 3,442 3,163Long-Term Investments 0 63Goodwill 710 710Other 214 261Total Assets 6,341 5,741

Whole Foods Market, Inc.Balance Sheet

For the Fiscal Year Ended September 30In Millions

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-24

2016 2015Liabilities

Accounts Payable 307 295Other Accrued Liabilities 1,031 954Current Portion of Long Term Debt 3 3Total Current Liabilities 1,341 1,252

Long-Term Debt 1,048 62Deferred Lease Liabilities 640 587Other Liabilities 88 71Total Liabilities 3,117 1,972

EquityCommon Stock 2,933 2,904Additional Paid in Capital 0 0Treasury Stock (2,026) (1,124)Retained Earnings 2,349 2,017Accumulated Other Comprehensive Income/(Loss) (32) (28)Total Stockholders' Equity 3,224 3,769Total Liabilities and Stockholders' Equity 6,341$ 5,741$

Balance SheetFor the Fiscal Year Ended September 30

In Millions

Whole Foods Market, Inc.

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-25

2016 2015

Net Sales 15,724$ 15,389$ Cost of Goods Sold 10,313 9,973Gross Profit 5,411 5,416

General and Administrative Expenses 4,477 4,472Pre-Opening Expenses 64 67Restructuring Costs 13 16Operating Income/(Loss) 857 861

Interest Expense (41) 0Interest Revenue 11 17Income/(Loss) before Income Taxes 827 878

Income Tax Expense/(Benefit) 320 342Net Income/(Loss) 507$ 536$

Whole Foods Market, Inc.Income Statement

For the Fiscal Year Ended September 30In Millions

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-26

Liquidity Ratios

=Current ratioCurrent assets

Current liabilitiesMeasures a company’s ability to satisfy its short-

term liabilities

=1.47$1,975$1,341

Current ratio

=1.23$1,544$1,252

2016 2015

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-27

Liquidity Ratios

=.82 $1,094$1,341

Acid-test ratio

=Acid-test ratioQuick assets

Current liabilitiesProvides a more stringent indication of a company’s

ability to pay its current liabilities

=.60$737

$1,252

2016 2015

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-28

Financing Ratios

=Debt to equity ratio

Total liabilitiesShareholders’ equity

Indicates the extent of reliance on creditors, rather than owners, in providing resources

=.97$3,117$3,224

Debt to equity ratio

=.52$1,972$3,769

2016 2015

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-29

Financing Ratios

=21.2$868$41

Times interest earned ratio

=Times interest earned ratio

Net income + Interest expense + TaxesInterest expense

Indicates the margin of safety provided to creditors

=N/A$878

0

2016 2015

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-30

Now, let’s move on to a new topic.

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-31

Statement of Cash Flows

The Statement of Cash Flows provides relevant information about the cash receipts and cash payments of an enterprise during a period. It provides answers to questions:

1. Where did the cash come from during the period?2. What was the cash used for during the period?3. What was the change in the cash balance during the

period?

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-32

Three different activities:Operating,

Content and Format

The Statement of Cash Flows

LO 7 Identify the content of the statement of cash flows.

Investing, Financing

Illustration 5-24

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-33

Statement of Cash Flows

Cash Flows from Operating ActivitiesReports the cash effects of transactions that enter into

the determination of net income.The direct method and indirect method are two different approaches to report cash flows from operations. Each has its advantages and disadvantages, but each reconciles to the same number for total cash flows from operating activities.

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-34

Statement of Cash Flows

Cash Flows from Investing Activities

Reports cash effects of transactions that result in a change in long-term assets. For example:

Buying or selling property, plant, or equipment

Buying or selling financial investment instruments

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-35

Statement of Cash Flows

Cash Flows from Financing Activities

Reports cash effects of transactions that result in a change in long-term liabilities and stockholder’s equity. For example:

Acquiring or paying down borrowingsIssuing capital stockPaying dividends to stockholders

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-36

Cash flows from operating activities: $$

Cash flows from investing activities: $$

Cash flows from financing activities: $$

Net increase in cash $$Cash at beginning of year $$Cash at end of year $$

Basic Format for theStatement of Cash Flows

Involve the purchase and sale of products or services

Involve the acquisition and saleof long-term assets

Involve the issuance and paymentof long-term liabilities and stock

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Slide3-38

ReviewIn preparing a statement of cash flows, which of the following transactions would be considered an investing activity? a. Sale of equipment at book value b. Sale of merchandise on credit c. Declaration of a cash dividend d. Issuance of bonds payable at a discountreceivable.

The Statement of Cash Flows

LO 8 Prepare a statement of cash flows.