spousal lifetime access trusts: income, gift, estate and

TRANSCRIPT

Spousal Lifetime Access Trusts: Income, Gift,

Estate and GST Tax, State Limitations,

Building in Powers and Options

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 1.

THURSDAY, JANUARY 14, 2021

Presenting a 90-minute encore presentation with live Q&A

Luke C. Bean, LLM, Partner, Rico Murphy Diamond & Bean, Natick, MA

Kenneth J. Crotty, J.D., LL.M., Partner, Gassman Crotty & Denicolo, Clearwater

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-877-447-0294 and enter your Conference ID and PIN when prompted.

Otherwise, please send us a chat or e-mail [email protected] immediately

so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the ‘Full Screen’ symbol located on the bottom

right of the slides. To exit full screen, press the Esc button.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 2.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the link to the PDF of the slides for today’s program, which is located

to the right of the slides, just above the Q&A box.

• The PDF will open a separate tab/window. Print the slides by clicking on the

printer icon.

FOR LIVE EVENT ONLY

Leveraging Spousal Lifetime Access Trusts

January 14, 2021

Presented By:

Luke C. Bean

Rico, Murphy, Diamond & Bean LLP190 N. Main Street, Suite 201

Natick, MA 01760

Phone: (617) 410-6890Email: [email protected]

www.rmdbllp.com

Strafford Webinars

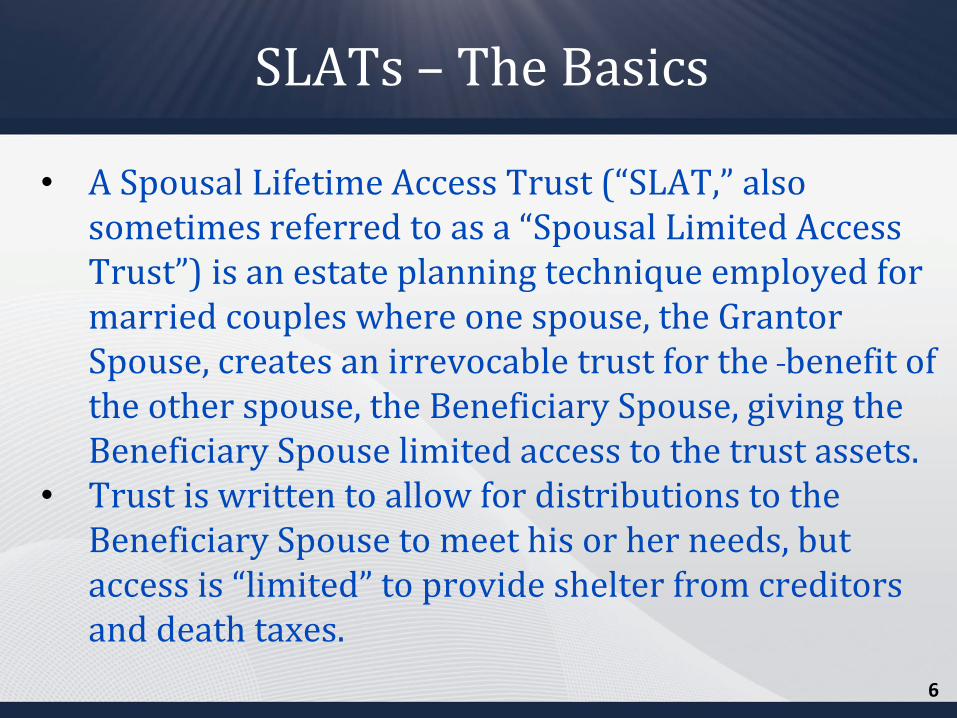

SLATs – The Basics

• A Spousal Lifetime Access Trust (“SLAT,” also sometimes referred to as a “Spousal Limited Access Trust”) is an estate planning technique employed for married couples where one spouse, the Grantor Spouse, creates an irrevocable trust for the benefit of the other spouse, the Beneficiary Spouse, giving the Beneficiary Spouse limited access to the trust assets.

• Trust is written to allow for distributions to the Beneficiary Spouse to meet his or her needs, but access is “limited” to provide shelter from creditors and death taxes.

6

SLATs – The Basics

• The transfer of assets by the Grantor Spouse is considered a gift and will use some or all of the Grantor Spouse’s gift tax exemption.

• The assets and their future appreciation can eventually pass to children, grandchildren, or future generations free of estate tax.

• A SLAT is essentially a Credit Shelter Trust or Bypass Trust set up during life rather than at death. The SLAT shelters the gifted assets plus growth from the date of the gift onwards rather than starting at death.

7

SLAT – The Benefits

• Asset protection (the amount of protection will depend on many things, including the trust’s terms and state law);

• Structured as a Grantor Trust, allowing the Grantor Spouse to pay the trust’s income taxes, gift tax-free;

• Avoid state estate taxes;• Reduce conflict in case of divorce by creating a pre-

existing asset division;• If the Grantor Spouse dies, SLAT assets are unable to

be directly accessed by the Beneficiary Spouse’s subsequent spouse;

8

SLAT – The Benefits

• Can provide income or principal not only to the Beneficiary Spouse but also descendants;

• At the Beneficiary Spouse’s death, the trust assets can immediately be available to provide care for descendants;

• Can be structured to avoid/minimize state income taxes;

• Can ensure bloodline protection;• Can be used as a Dynasty Trust, sheltering assets from

children and grandchildren’s divorces, creditors, and complications.

9

SLAT – The Drawbacks

• Once transferred, the SLAT assets cannot return to the Grantor Spouse (but, of course, the Beneficiary Spouse can always voluntarily share distributions with the Grantor Spouse);

• Divorce and access;• Reciprocal Trust Doctrine;• Death of the Beneficiary Spouse - Grantor Spouse

losing access to indirect benefit to the trust.

10

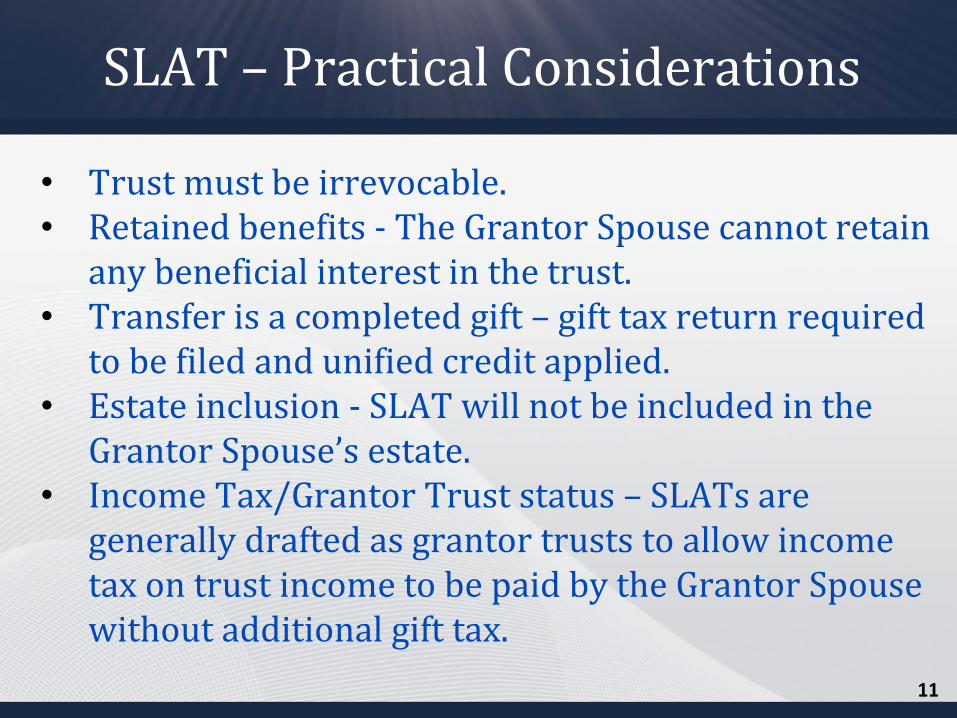

SLAT – Practical Considerations

• Trust must be irrevocable. • Retained benefits - The Grantor Spouse cannot retain

any beneficial interest in the trust. • Transfer is a completed gift – gift tax return required

to be filed and unified credit applied.• Estate inclusion - SLAT will not be included in the

Grantor Spouse’s estate.• Income Tax/Grantor Trust status – SLATs are

generally drafted as grantor trusts to allow income tax on trust income to be paid by the Grantor Spouse without additional gift tax.

11

• Trustee - The Grantor Spouse should not serve as trustee but the Beneficiary Spouse may, so long as the power to make distributions to him or herself is restricted by an “ascertainable standard.”

• Replacement Power - Either or both spouses (and current or future beneficiaries) can be given the ability to remove and replace a trustee.

• Beneficiaries - The primary beneficiary is the Beneficiary Spouse. Children, grandchildren, and more remote descendants may also be named as either current or remainder beneficiaries.

SLAT – Practical Considerations

12

• Flexibility – including limited or general power of appointment tax reimbursement clause, trust protector provisions, loan provisions, swap powers;

• Protection – drafting to anticipate divorce, death, etc., narrowing definition of surviving spouse, etc.

• Funding - a SLAT can be funded with a variety of assets. However, it is important for the Grantor Spouse to fund the SLAT with separate property only. Funding should also ensure sufficient assets remain outside of the trust.

SLAT – Practical Considerations

13

• SLATs can be used with a variety of other planning techniques including:o Family LLPs/LLCs, voting and non-voting shares,

discounting, formula clause gifts;o Sales in exchange for promissory note, SCIN or

private life annuity;

SLAT – An Integrated Strategy

14

• Grantor Trust status (easiest way is IRC 675(4)(c));• Funding – sourcing separate property;• Reciprocal Trust Doctrine; • Gift tax return – must be filed, GST elections, audit

risks, discounting, gift splitting;• Lost step-up in basis

SLAT – Traps

15

• SLATs do not work well for single persons – may consider DAPT instead;

• QPRTs, GRATs are still viable options;• Charitable giving vehicles – CRATs, CRUTs, CLATs and

CLUTs

SLAT – Alternatives?

16

SPOUSAL LIFETIME ACCESS TRUSTS:

INCOME, GIFT, ESTATE AND GST TAX, STATE

LIMITATIONS, BUILDING IN POWERS AND OPTIONS

A Strafford Webinar

Thursday, January 14, 2021 – 1:00 – 2:30 p.m. EDT(90 minutes)

Kenneth J. [email protected]

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Contingent Marital Devise Provision

In the highly unlikely event that the Grantor’s contributions to this Trust exceed the

maximum amount that can be gifted by the Grantor without incurring Federal Gift Tax, then the

Trustee shall divide the Trust estate into two separate shares, hereinafter designated as the

SMITH FAMILY TRUST SHARE and the SMITH MARITAL DEDUCTION TRUST SHARE.

The SMITH FAMILY TRUST SHARE shall be a fraction of the Trust estate of which (a) the

numerator shall be the largest amount that if allowed using the Grantor’s Federal Gift Tax

Exemption would result in no Federal Gift Tax being payable by the Grantor by reason of the

gift to this Trust, and (b) the denominator shall be the value as finally determined for Federal

Gift Tax purposes of the assets in the Trust estate immediately after such gift that would have

otherwise caused gift tax to be imposed has been made. The SMITH MARITAL DEDUCTION

TRUST SHARE shall be the remainder of the Trust estate. No property shall be allocated to the

SMITH MARITAL DEDUCTION TRUST SHARE that would not qualify for the Federal Gift

tax Marital Deduction and the Federal Estate Tax Marital Deduction. The SMITH FAMILY

TRUST SHARE shall be held pursuant to the terms of Section ____ and Article ____ of this

Trust. The SMITH MARITAL DEDUCTION SHARE shall be held for the benefit of the

Grantor’s spouse, pursuant to Section ____ below.

18

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Possible Impact of Divorce

In the highly unlikely event that either the Grantor or JANE SMITH has filed for a

dissolution of marriage, then at the time such dissolution is finalized (or sooner if determined

appropriate by the unanimous consent of all acting Trustees) the Trustee shall divide the assets of

this Trust and any separate trusts herein established, into separate equal trusts which will have

equivalent values. The Grantor shall have the authority to remove and replace the Trustee as

described above only with respect to one such described Trust (or Trusts equaling 50% of the

value of the assets of this Trust prior to division), and JANE SMITH shall have the authority to

remove and replace the Trustee as described above only with respect to the other Trust (or Trusts

equaling 50% of the value of the assets of this Trust prior to division). In such event, the Trust

Protectors of the separate trust that JANE SMITH will have the right to replace the Trusteeship of

shall be __________________, _________________ and ___________________, and the Trust

Protectors for the separate trust that the Grantor shall have the power to replace the Trusteeship

of shall be _____________________, ______________________ and

_______________________. Further, in such event, the Trust Protectors may name alternate

Trust Protectors to serve in lieu of one or more of the Trust Protectors then serving of each such

separate trust, but only with the advanced written approval of JANE SMITH, as to the separate

trust that she will have the power to replace the Trusteeship of, and only with the advanced

written approval of the Grantor, with respect to the separate trust that he will have the power to

replace the Trusteeship of.

19

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Invite Estate Tax Inclusion to Cause a Step-Up in IncomeTax Basis if the Clients Are Not Concerned with the Estate Tax

Utilize general powers of appointment to trigger estate tax

Joint trusts (i.e., community property trusts, JESTs, etc.) can help get a basis step-up on the

death of the first dying spouse

Amend irrevocable trusts to give the original grantor or grantors testamentary powers to appoint

trust assets to creditors of their estate

Also consider installing the Grantors as Trustees or Trust Protectors

Unwind previous estate tax avoidance transaction where the original purpose is no longer

applicable

Give senior family members put rights and use other mechanisms to reduce valuation discounts

Sell assets to a grantor trust established by the grantor, which affords a senior family member a

testamentary general power of appointment

20

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Sample Power of Appointment Language:

Each of ______________________and _________________ (“Parents”) shall have the right to direct how the ownership of the shares owned by each of _______________ and __________________ (“Children”) shall be devised, provided that (i) such power may only be exercised under the Last Will and Testament of each of Parents which specifically refers to this Agreement, (ii) the disposition of such shares must be solely to or in trust for the benefit of lineal descendants of Parents or to the creditors of Parents’ estate, and (iii) the exercise of such power must be approved by one (1) of the following individuals in the order named of ____________________, _________________ or TRUST COMPANY, and no approving party named above shall have any fiduciary duty to any descendant of parents.

Sample Put Right to Eliminate Discounts:

Each holder of shares that are owned by _____________ or _____________, or by them jointly, or by the ____________ LIVING TRUST as of the date of execution of this Agreement, shall have a “put right” which will entitle the holder of such share to be redeemed by the Company based upon the percentage of ownership represented by such share (one divided by the number of shares then issued and outstanding) multiplied by the Net Value of the Company. The Net Value of the Company will be based upon the Appraised Value of all assets of the Company, less the amount of all liabilities of the Company, with any contingent liabilities or contractual, legal, or tax obligations to be taken into account to the extent that a Valuation Expert would consider such items to reduce the value of the Company.

Using General Power of Appointment to Receive Step-Up In Basis

21

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Protect the Exercise of Powers of Appointment

Sample language:

The Primary Beneficiary shall have a limited Power of Appointment (as defined inSection ____ of this Trust Agreement) with respect to his or her separate trust, and uponthe Primary Beneficiary's death, the Trustee shall pay the remaining income andprincipal, or such portion thereof over which said Power is exercised, as the PrimaryBeneficiary directs pursuant to the exercise of such Power. Notwithstanding the above,and in order to assure that the Primary Beneficiary has been properly counseled withrespect to the advantages of keeping assets under trust for future generation, suchpower shall not be exercisable unless such Primary Beneficiary shall meet physically witha lawyer who is Board Certified in trusts and estates, taxation, or elder law, and has atleast ten (10) years’ experience to discuss the advantages of maintaining assets undertrust to facilitate protections of beneficiaries from creditors, divorce, estate taxes, andimprovidence, and no exercise of such power shall be considered to have occurredunless such qualified lawyer signs a letter contemporaneously with the executionthereof to confirm that the executions follows a consultation with such lawyer whichprovided input and advice with respect thereto.

Our trusts typically provide beneficiaries with powers of appointment to allow for flexibility.

However, we often require that any exercise of a power of appointment must first get the

consent of one or more independent parties, or that the powerholder consult with a law firm

who approves the exercise of the power.

22

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

THE REVERSIBLE EXEMPT ASSET PROTECTION (“REAP”) TRUST

23

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Steve Leimberg’s Estate Planning Newsletter:Excerpts from “The Reversible Exempt Asset Protection (“REAP”) Trust for 2017 Planning” by Alan Gassman, Christopher Denicolo, Kenneth Crotty & Brandon Ketron

THE ‘REVERSIBLE EXEMPT ASSET PROTECTION TRUST,’ ALSO KNOWN AS THE REVERSIBLE MIRROR TRUST, ALLOWS CLIENTS TO TAKE ADVANTAGE OF PRESENTLY AVAILABLE AND EFFECTIVE ESTATE TAX PLANNING OPPORTUNITIES, WHILE PROVIDING THE FLEXIBILITY NEEDED TO ADDRESS TO THE POSSIBLE UNCERTAINTIES THAT MIGHT EXIST THE HORIZON, WHILE ALSO PROVIDING ASSET PROTECTION THAT MAY GREATLY EXCEED WHAT IS NOW OTHERWISE IN PLACE.”

EXECUTIVE SUMMARY:

WHEN WE LOOK BACK IN A YEAR ON THE UNEXPECTED RESULTS OF THE 2016 PRESIDENTIAL ELECTION, AND THE TENDENCY FOR CLIENTS AND ADVISORS TO “WAIT AND SEE” WHAT HAPPENS WITH ESTATE AND GIFT TAXES, WE MAY FIND THAT THE MAJORITY OF PLANNERS AND DECISION MAKERS ERRED ON THE SIDE OF DOING NOTHING, COSTING FAMILIES SIGNIFICANT PORTIONS OF THEIR ASSETS UPON THE DEATH OF LOVED ONES IN THE FUTURE.

ALTERNATIVELY, WHEN WE LOOK BACK IN FIVE YEARS WE MAY FIND THAT THE ESTATE TAX “WENT AWAY” BUT CAME BACK IN HARSHER FORM, AFTER A PERIOD OF TIME DURING WHICH THOSE WHO PLANNED AHEAD CAME OUT MUCH BETTER THAN THOSE WHO DID NOT. WHILE SOME COMMENTATORS BELIEVE THAT REPEAL OF THE ESTATE TAX IS A STRONG POSSIBILITY, OTHERS HAVE POINTED OUT THE SEVERAL LIKELY ALTERNATIVES THAT MUST BE CONSIDERED TO STAY TWO OR MORE MOVE MOVES AHEAD ON THE CHESS BOARD OF FAMILY WEALTH PLANNING IN THIS DYNAMIC ENVIRONMENT.

BY OUR VIEW IT IS CRUCIAL TO GIVE CLIENTS OPTIONS THAT INCLUDE FLEXIBLE METHODS OF TAKING ADVANTAGE OF PRESENT OPPORTUNITIES, WHILE BEING ABLE TO CHANGE OR REVERSE WHAT IS DONE, OR ASSURE THAT IT WOULD BE WANTED IN A NO ESTATE TAX WORLD, WHILE ALSO BEING AHEAD IN THE NON BASIS STEP UP ENVIRONMENT THAT MAY BE COMING.

THE “REVERSIBLE EXEMPT ASSET PROTECTION TRUST,” ALSO KNOWN AS THE REVERSIBLE MIRROR TRUST, ALLOWS CLIENTS TO TAKE ADVANTAGE OF PRESENTLY AVAILABLE AND EFFECTIVE ESTATE TAX PLANNING OPPORTUNITIES, WHILE PROVIDING THE FLEXIBILITY NEEDED TO ADDRESS TO THE POSSIBLE UNCERTAINTIES THAT MIGHT EXIST THE HORIZON, WHILE ALSO PROVIDING ASSET PROTECTION THAT MAY GREATLY EXCEED WHAT IS NOW OTHERWISE IN PLACE.

IN OTHER WORDS, WHILE SOME BELIEVE THAT THE ESTATE TAX IS FACING THE GHOULISH PROSPECT OF THE GRIM REAPER, WE THINK THAT KNOWLEDGEABLE ADVISORS SHOULD BE EMBRACING THE REAP TRUST.

24

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

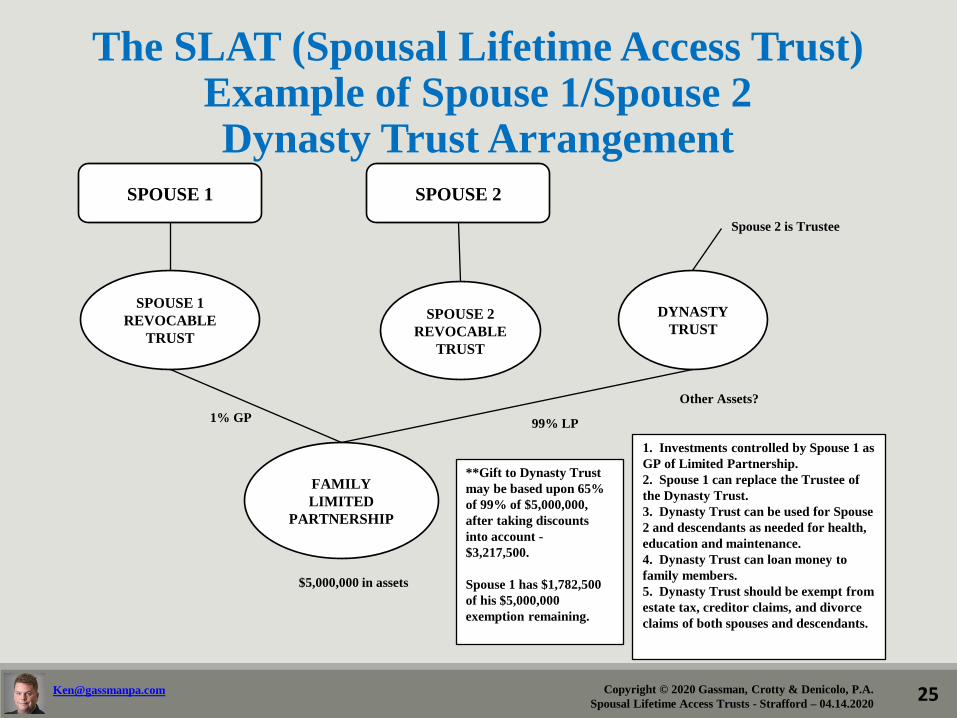

The SLAT (Spousal Lifetime Access Trust)Example of Spouse 1/Spouse 2Dynasty Trust Arrangement

1% GP

SPOUSE 1

REVOCABLE

TRUST

SPOUSE 2

REVOCABLE

TRUST

SPOUSE 1 SPOUSE 2

FAMILY

LIMITED

PARTNERSHIP

DYNASTY

TRUST

Spouse 2 is Trustee

Other Assets?

$5,000,000 in assets

99% LP

**Gift to Dynasty Trust

may be based upon 65%

of 99% of $5,000,000,

after taking discounts

into account -

$3,217,500.

Spouse 1 has $1,782,500

of his $5,000,000

exemption remaining.

1. Investments controlled by Spouse 1 as

GP of Limited Partnership.

2. Spouse 1 can replace the Trustee of

the Dynasty Trust.

3. Dynasty Trust can be used for Spouse

2 and descendants as needed for health,

education and maintenance.

4. Dynasty Trust can loan money to

family members.

5. Dynasty Trust should be exempt from

estate tax, creditor claims, and divorce

claims of both spouses and descendants.

25

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

GOOD REASONS TO USE FLORIDA AS

THE JURISDICTION OF AN

IRREVOCABLE TRUST

1. No income taxes on trust income.

2. No estate, inheritance or gift taxes.

3. A well-developed trust law and experienced probate court judiciary.

4. A 360-year Rule Against Perpetuities.

5. Ability to appoint a Designated Representative.

6. We need the business!

26

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

GOOD REASONS NOT TO USE FLORIDA AS THE

JURISDICTION OF AN IRREVOCABLE TRUST

1. The power of invasion by a beneficiary’s ex-spouse or unintended / undeserving

descendants.

2. Trustee’s obligation to make extensive disclosures to beneficiaries who the

settlor may not want to have annual reminders, plus related expenses.

3. Issues relating to clauses in trusts requiring beneficiaries to have certain religious

orientation, sexual orientation, or to be married, which may be viewed as repugnant to Florida

public policy but be upheld by a foreign jurisdiction.

4. Creditor access to non-lapsed withdrawal powers, child support, and alimony.

5. Concern as to “court of equity” interpretations.

6. Potential concern that federal legislation could cause domestic trusts to be subject to

governmental agency liability, which would not apply to international trusts.

27

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

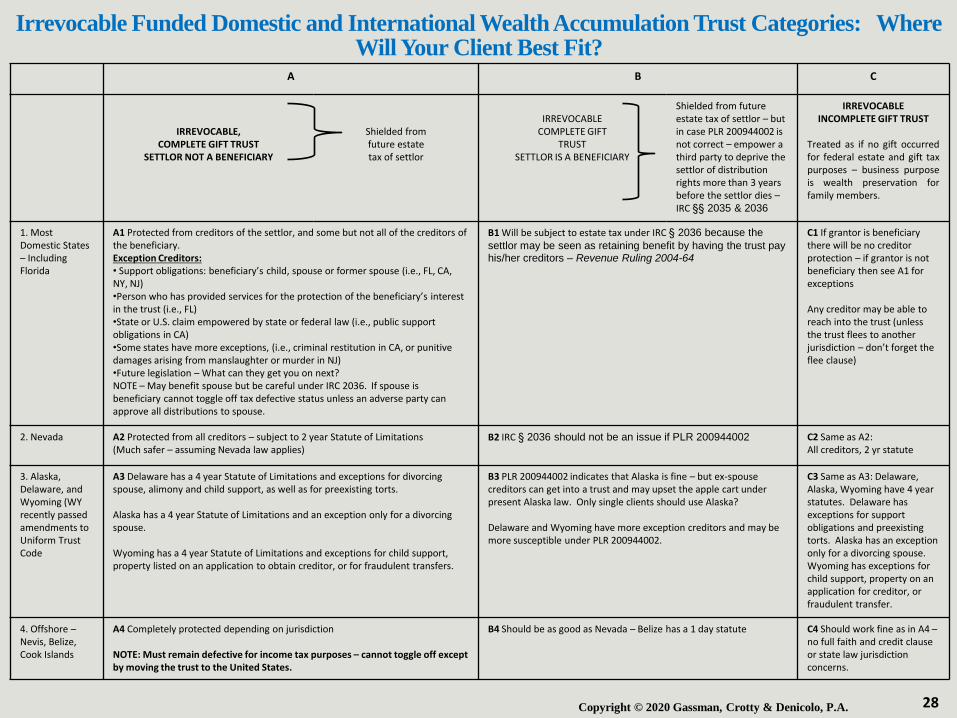

Irrevocable Funded Domestic and International Wealth Accumulation Trust Categories: Where Will Your Client Best Fit?

A B C

IRREVOCABLE,COMPLETE GIFT TRUST

SETTLOR NOT A BENEFICIARY

Shielded from future estate tax of settlor

IRREVOCABLECOMPLETE GIFT

TRUSTSETTLOR IS A BENEFICIARY

Shielded from future estate tax of settlor – but in case PLR 200944002 is not correct – empower a third party to deprive the settlor of distribution rights more than 3 years before the settlor dies –IRC §§ 2035 & 2036

IRREVOCABLE INCOMPLETE GIFT TRUST

Treated as if no gift occurredfor federal estate and gift taxpurposes – business purposeis wealth preservation forfamily members.

1. Most Domestic States – Including Florida

A1 Protected from creditors of the settlor, and some but not all of the creditors of the beneficiary.Exception Creditors:• Support obligations: beneficiary’s child, spouse or former spouse (i.e., FL, CA, NY, NJ)•Person who has provided services for the protection of the beneficiary’s interest in the trust (i.e., FL)•State or U.S. claim empowered by state or federal law (i.e., public support obligations in CA)•Some states have more exceptions, (i.e., criminal restitution in CA, or punitive damages arising from manslaughter or murder in NJ)•Future legislation – What can they get you on next?NOTE – May benefit spouse but be careful under IRC 2036. If spouse is beneficiary cannot toggle off tax defective status unless an adverse party can approve all distributions to spouse.

B1 Will be subject to estate tax under IRC § 2036 because the

settlor may be seen as retaining benefit by having the trust pay his/her creditors – Revenue Ruling 2004-64

C1 If grantor is beneficiary there will be no creditor protection – if grantor is not beneficiary then see A1 for exceptions

Any creditor may be able to reach into the trust (unless the trust flees to another jurisdiction – don’t forget the flee clause)

2. Nevada A2 Protected from all creditors – subject to 2 year Statute of Limitations (Much safer – assuming Nevada law applies)

B2 IRC § 2036 should not be an issue if PLR 200944002 C2 Same as A2:All creditors, 2 yr statute

3. Alaska, Delaware, and Wyoming (WY recently passed amendments to Uniform Trust Code

A3 Delaware has a 4 year Statute of Limitations and exceptions for divorcing spouse, alimony and child support, as well as for preexisting torts.

Alaska has a 4 year Statute of Limitations and an exception only for a divorcing spouse.

Wyoming has a 4 year Statute of Limitations and exceptions for child support, property listed on an application to obtain creditor, or for fraudulent transfers.

B3 PLR 200944002 indicates that Alaska is fine – but ex-spouse creditors can get into a trust and may upset the apple cart under present Alaska law. Only single clients should use Alaska?

Delaware and Wyoming have more exception creditors and may be more susceptible under PLR 200944002.

C3 Same as A3: Delaware, Alaska, Wyoming have 4 year statutes. Delaware has exceptions for support obligations and preexisting torts. Alaska has an exception only for a divorcing spouse. Wyoming has exceptions for child support, property on an application for creditor, or fraudulent transfer.

4. Offshore –Nevis, Belize, Cook Islands

A4 Completely protected depending on jurisdiction

NOTE: Must remain defective for income tax purposes – cannot toggle off except by moving the trust to the United States.

B4 Should be as good as Nevada – Belize has a 1 day statute C4 Should work fine as in A4 –no full faith and credit clause or state law jurisdiction concerns.

28

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

FLEE CLAUSE – SAMPLE FORM LANGUAGE

Flee Clause:In the event that there is a judgment against the Grantor or other imminent creditor circumstance, then the Trustee shall transfer all assets to the ___________ Trust Company in the jurisdiction of ___________, or such other trust company as may be directed by the Trust Protectors, provided that it shall be compulsory, and not within the discretion of any Trust Protector or Trustee to require such change in situs to a reputable trust company in Nevis, the Cook Islands, the Bahamas, the Isle of Man, or another jurisdiction outside of the United States, notwithstanding any provision herein to the contrary.

NOTE: The laws in most reputable asset protection jurisdictions will consider a trust that was settled in a U.S. jurisdiction to have been settled in the offshore jurisdiction when initially formed for statute of limitation purposes.

29

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

CREDITOR PROTECTION CONSIDERATIONS –

SAMPLE FORM LANGUAGE

Jones Clause:Notwithstanding anything herein to the contrary, in the event that XYZ obtains a judgment against __________, then the trustee shall satisfy such judgement with the Trust assets, when requested to do so.

DAPT where Grantor cannot be added back unless there is an act of independent significance:

The Trust Protectors may not add the Grantor as a beneficiary of this Trust unless or until the Grantor or the Grantor’s spouse has filed a petition for divorce, and the Grantor has been ordered to pay significant assets to the Grantor’s spouse, or the Grantor’s assets which are otherwise exempt from creditor claims are worth less than $1,000,000, and the Grantor is in need of financial support after taking into consideration sources of income and support of the Grantor, provided that no distributions may be made to the Grantor under such circumstances if any creditor would be able to seize assets from the Grantor, but instead, under such circumstances, the Trustee may pay for expenses of the Grantor, if the payment of such expenses would not be accessible of the Grantor under applicable law.

30

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Don’t Forget Possible Charitable Distributions from the Trust

The ability to pay otherwise taxable income to charity or private operating foundations from a complex trust.

Note – A private operating foundation can have almost all of the advantages of a public charity, plus the bigger advantage – complete control by the donor.

31

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

642(C) TRUST CHARITABLE DEDUCTION

In order to receive a charitable deduction, the following requirements of Section 642(c) must be

met:

1. The distribution must be made from gross income

2. The distribution must be made pursuant to the terms of the governing instrument.

If the above requirements are met, the trust is entitled to a charitable deduction without being

subject to the percentage of gross income limitations that apply to individuals.

As a result, charitable inclined individuals may want to consider making charitable

contributions from pre-existing complex trusts (if the terms of the trust allows for this) or

complex trusts that are created to plan for Section 199A so that the deduction is not limited

and/or possibly lost as a result of the taxpayer no longer itemizing deductions.

Planners should also consider specifically including in trust instruments that the trustee is

authorized to make distributions to one or more charitable organizations so that this option is

available.

As discussed in Slide 50, the charitable deduction for ESBTs is determined under the rules

applicable to individual taxpayers (Section 170) and not under the rules of Section 642(c).

32

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

HOW TO CHANGE TRUSTS

1. Changing asset composition (e.g. gift house in LLC to trust for SALT)

2. Using trust protector powers (changing trust situs)

3. Decanting

4. Non-judicial modification

5. Powers of Appointment within the terms of the instrument

6. Installing Trust Protectors

7. Section 2519

33

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Your Irrevocable Trust Can Be Modified

Many people assume that because their trust is irrevocable, that it is impossible to change any of its terms. In Florida, and in many other states around the country, an irrevocable trust can be changed through a method called decanting.

Decanting was first authorized in the state of Florida via case law. In the Florida Supreme Court Case, Phillips v. Palm Beach Trust Company, 196 So. 299 (Fla. 1940) the court allowed a trustee to transfer all of the assets from an existing trust into a new trust. The court held that this was permissible because the second trust did not include any beneficiaries who were not beneficiaries of the first trust and the trustee had the absolute power to invade trust assets.

In 2014 the Florida courts again approved the decanting of an irrevocable trust in Peck v. Peck, 133 So. 3d 587 (Fla. 2d DCA 2014). In this case, the court reasoned that all of the interested parties agreed to the decanting and that the trust’s terms did not prevent decanting in this specific instance.

The Florida Legislature did not codify this rule until 2007, when it enacted Fla. Stat. 736.04117. This statute required a trustee to have absolute discretion to invade the assets of the trust in order for the trust to be decanted. Although this statute may have been beneficial for a few irrevocable trusts, most trusts include language that restrict distributions to health, education, maintenance and support, or some other ascertainable standard. If such a standard was included in a trust (as it is in most trusts) the only option to decant that trust would be to rely on Florida common law.

34

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Your Irrevocable Trust Can Be Modified, Continued

In 2018, the Florida Senate approved House Bill 413, which modified Fla. Stat. 736.04117 to provide

much more flexibility in which trusts could be decanted. Virtually all Florida irrevocable trusts can now

be decanted, to varying degrees, without the need to rely on case law.

Updated Fla. Stat. 736.04117 now provides the ability to decant a trust when the trustee does not have

absolute power to invade trust assets as long as the new trust grants each beneficiary of the first trust

a substantially similar interests. “Substantially similar” is defined in the Statute as meaning “there is no

material change in a beneficiary’s beneficial interest or in the power to make distributions and that the

power to make a distribution under a second trust for the benefit of a beneficiary who is an individual is

substantially similar to the power under the first trust to make a distribution directly to the beneficiary.”

This is a powerful estate planning tool as it allows practitioners to modify irrevocable trusts that may

have tax inefficient provisions or to update the trust language to better suit the client’s desires. The

new trust cannot grant new powers of appointment, or make any substantial modifications to existing

powers of appointment.

If the trustee has an absolute power to invade the principal of the trust, the trust can be amended in

any fashion mentioned above, plus a power of appointment can be added or modified for any of the

current trust beneficiaries. Here again, only the beneficiaries of the first trust are allowed to be

beneficiaries of the new trust. If a beneficiary is not vested, that beneficiary could be completely

removed from the new trust.

35

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Your Irrevocable Trust Can Be Modified, Continued

Practitioners need to consider the effect of this statute when drafting trusts for their clients. If a client wants to make sure that the trust cannot be decanted, language can be added to the trust to prevent application of Fla. Stat. 736.04117. On the other hand, if the grantor of the trust wants to ensure that the terms of the trust can be changed going forward, language could be put in the trust to specify how, and to what extent, the trust may be decanted in the future.

Although the modifications that can be made to a trust through the Florida Decanting Statute are not unlimited, they do provide great flexibility in the modification of irrevocable trusts and give practitioners comfort in knowing that decanting has been blessed by the Florida Legislature.

36

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

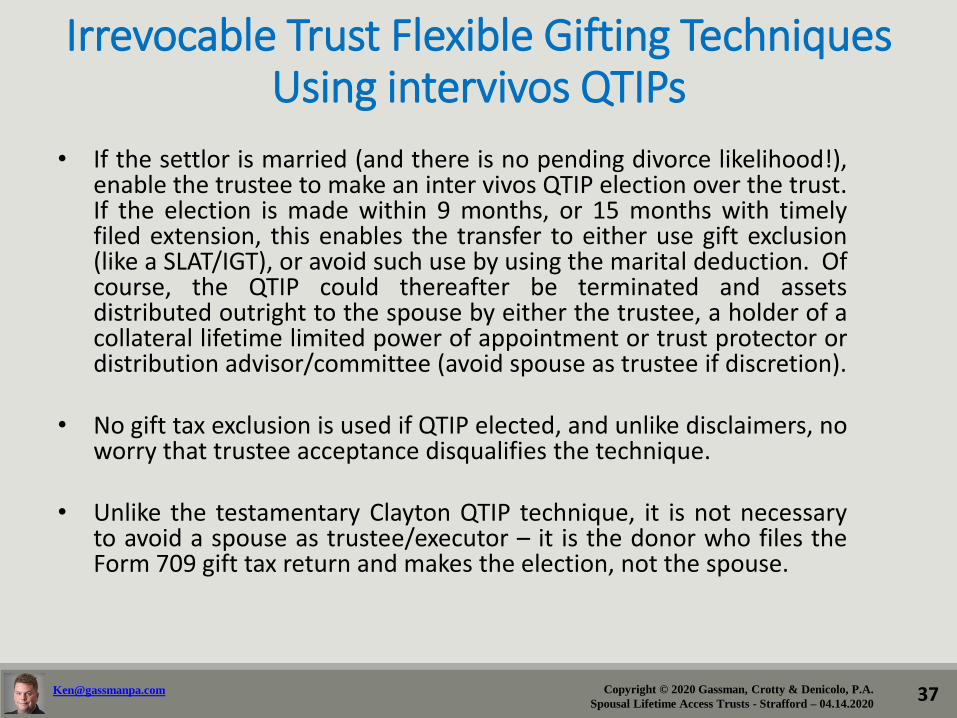

Irrevocable Trust Flexible Gifting Techniques Using intervivos QTIPs

• If the settlor is married (and there is no pending divorce likelihood!),enable the trustee to make an inter vivos QTIP election over the trust.If the election is made within 9 months, or 15 months with timelyfiled extension, this enables the transfer to either use gift exclusion(like a SLAT/IGT), or avoid such use by using the marital deduction. Ofcourse, the QTIP could thereafter be terminated and assetsdistributed outright to the spouse by either the trustee, a holder of acollateral lifetime limited power of appointment or trust protector ordistribution advisor/committee (avoid spouse as trustee if discretion).

• No gift tax exclusion is used if QTIP elected, and unlike disclaimers, noworry that trustee acceptance disqualifies the technique.

• Unlike the testamentary Clayton QTIP technique, it is not necessaryto avoid a spouse as trustee/executor – it is the donor who files theForm 709 gift tax return and makes the election, not the spouse.

37

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Irrevocable Trust Flexible Gifting TechniquesUse defined value formula gifting, w/charity

• The clauses with the most history/authority are defined value formula gifting clauses that pour any excess over to charity:

• See Estate of Christiansen v. Comm'r, 130 T.C. 1 (T.C. 2008), aff’d 586 F.3d 1061 (8th Cir. 2009)

• Succession of McCord v. Comm'r, 461 F.3d 614 (5th Cir. 2006)

• Estate of Petter v. Comm'r, T.C. Memo 2009-280 (T.C. 2009)

38

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Fractional Gift Transfer Arrangement from Petter, McCord, and Hendrix

HUSBAND

TRUST FOR

WIFE &

DESCENDANTS

CHARITABLE

ENTITY

It will be up to a fiduciary to

determine what portion goes to

the Trust and what portion goes

to the charity by formula in the

document.

Requirements:

1. An independent charity that the client has not been involved with in the past and does not sit on the board of.

2. A minimum of 1% or a greater overflow amount passing to the charity.

3. An independent representation by the charity and an independent deal worked out between the charity and the trustees

of the family’s recipient trust.

4. Paying the bills for all of the above.

39

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Irrevocable Trust Flexible Gifting TechniquesUse defined value formula gifting, w/marital

• There is no specific case using a marital pourover, but in theory it is logically no different from using a charitable pourover, and involves much fewer issues.

• Imagine the income tax filing headaches when you have to go back years later and amend entity tax returns, individual and/or trust tax returns because the ownership was improperly reported and none of the K-1s and other tax filings were correct due to incorrect allocation of ownership.

• If shares are reallocated from IGT to marital trust, both are grantor trusts and this largely goes away.

• If shares are reallocated outright to spouse, and spouses file jointly, this problem largely goes away as well.

40

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Irrevocable Trust Flexible Gifting TechniquesUse defined value formula gift, w/ no pourover

• There is no specific court case or ruling using an incomplete gift or a GRAT as the pourover, but in theory this should also be possible. The “public policy” in favor of charitable/marital deductions is not quite there.

• In lieu of pouring over into a GRAT or incomplete gift trust, such as a DAPT, you can simply copy the defined value gift in the Wandry case.

• Wandry simply used a defined value formula wherein any excess amount is deemed to have never been transferred in the first place. The IRS lost the case, but did not acquiesce in the decision. Unlike the Christiansen and McCord cases, which are at the appellate level and good authority in the 5th and 8th Circuit, Wandry is only a tax court memorandum decision – T.C. Memo 2012-88.

41

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Wandry v. Commissioner, T.C. Memo 2012-88 (2012)

PARENTS

LIMITED

LIABILITY

COMPANY

GRAND-

CHILDREN

CHILDREN

LLC units = lifetime gifting

exemption

LLC units = annual gift tax

exclusion

Language verbatim from Wandry: “Although the number of Units gifted is fixed on the date of the gift, that number is based on the

fair market value of the gifted Units, which cannot be known on the date of the gift but must be determined after such date based on

all relevant information as of that date. Furthermore, the value determined is subject to challenge by the Internal Revenue Service

(“IRS”). I intend to have a good-faith determination of such value made by an independent third-party professional experienced in

such matters and appropriately qualified to make such a determination. Nevertheless, if, after the number of gifted Units is

determined based on such valuation, the IRS challenges such valuation and a final determination of a different value is made by the

IRS or a court of law, the number of gifted Units shall be adjusted accordingly so that the value of the number of Units gifted to each

person equals the amount set forth above, in the same manner as a federal estate tax formula marital deduction amount would be

adjusted for a valuation redetermination by the IRS and/or a court of law.”

42

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Defined Valuation Allocation Formula Versus Defined Value Transfer Formula

Defined valuation allocation formula: allocates the transferred

assets among various transferees and defining the dollar amount

going to persons who would be treated as donees for gift tax

purposes, with any excess passing to charity.

-I give 100 shares of X stock to my child Sally, provided that if

the value of the shares is determined to exceed $1,000,000 then

the excess shall pass to My Favorite Charity.

Defined value transfer formula: defines the dollar amount of a

transfer that the transferor intends to make. If the value of the

assets is determined to be higher than the defined amount, the

assets will revert back to the transferor.

- I give 100 shares of X stock to my child Sally, provided that if

the value of the shares is determined to exceed $1,000,000, then

the number of shares given shall be reduced so that the total

shares given equal $1,000,000.

43

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Irrevocable Trust Flexible Gifting TechniquesUse a domestic asset protection trust (DAPT)

• Use a DE, OH, NV etc. domestic asset protection trust (DAPT) that enables settlor to remain as a beneficiary.

• Law is clear that the gift can still be complete – Rev. Rul. 77-378, but also PLR 9332006, PLR 9837007 and PLR 2009-44002

• Whether there is any Section 2036 retained interest is a fact-dependent question based on the circumstances of administration, upon which the IRS has declined to rule in PLRs.

• Another technique that might be safer (again, depending on how the trust is administered) is to omit the settlor as beneficiary, but permit a trust protector to add the settlor as beneficiary.

• However, this still uses gift tax exclusion even if it comes back to the settlor or spouse, unless one of the disclaimer/IV QTIP techniques discussed previously is exploited.

44

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Irrevocable Trust Flexible Gifting TechniquesUse Change of Situs Clauses

• Use change of situs clauses, especially if starting in non-DAPT state

• Enables later use of broad decanting powers in states like South Dakota, Nevada, etc. if your state does not have broad powers

• Enables change to a DAPT state/statute/trustee, if perhaps a trust protector contemplates adding a settlor as beneficiary.

• Enables change for state income tax law.

• Enables change for application of anti-lapse statute, no contest clauses, spendthrift trust protection, exception creditors and many more issues that may arise.

45

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

The Agency Tripwire

In some cases, such as Powell and Strangi, the courts have ruledthat the son, who may be sole GP in the example above is reallyacting as an agent for the principal, and in fact has a legal agencyrelationship and responsibility when he is also serving as the agentfor the principal under a durable power of attorney and/or astrustee under a Revocable Trust, so that the principal is consideredto have retained 2036(a) rights, even though the decedent doesnot own or hold them individually.

This seems unfair, because the fiduciary duty of a general partnerof a partnership to limited partners would seem to be no more orless of a duty regardless of whether the individual is acting as anagent for the limited partners or in another capacity. These TaxCourt decisions have not been appealed.

46

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

The Cahill Tripwire

This 2018 Tax Court Memo decision involved a Split Dollar Agreementwhere the decedent had the incidental and seemingly innocuouspower to agree that the split dollar agreement should be cancelled,allowing the decedent to receive the portion of the cash surrendervalue of the policy attributable to the loans that had been advancedby the decedent. The court found that this right to determine if andwhen there would be the equivalent of a liquidation or distributionconstituted a right to “designate persons who would enjoy theproperty” caused inclusion under 2036(a)(2) similar to the inclusion inPowell, where the decedent had the ability to terminate thepartnership.

Because the bona fide sale exception did not apply, 2036 would thenbring the value of these assets back into the gross estate of thedecedent.

47

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Thorns from Judge Thornton

Cahill is a Tax Court Memorandum case, so it has no precedential value, but itwas drafted by Judge Michael B. Thornton, who was one of the Tax Court judgesthat joined the Powell decision.

SOLUTION FOR ANY ARRANGEMENT WHERE THE OLDER FAMILY MEMBER WILLBE A PARTY TO ANY AGREEMENT RELATING TO ASSETS THAT HAVE BEEN SOLDOR GIFTED:

In light of Cahill, clients looking to create, sell or gift LLC or partnership interestsshould not retain any rights to participate in decisions concerning distributions,liquidations, or voting on amendments to an entity agreement that might givethem such rights, as they could possibly bestow a 2036(a) power upon thegrantor.

If there are only two parties to the Agreement, it will make sense to add at leastone other party, so that there are two parties that can vote to amend theAgreement in the future.

48

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

What About If The Taxpayer Has The Right To Replace Assetsof a Trust Which Owns The Liquidation/Distribution Interest

With Assets Of Equal Value?

Revenue Ruling 2008-22 states that a grantor of a trust who has retained thepower to substitute assets with the trust may exercise this right withouttriggering Sections 2036 or 2038. If the taxpayer is using an installment saleto a defective grantor trust, this is probably the safest power for the client tohave with respect to making the trust a defective grantor trust.

David Handler, David Herzig, and Naomita Yadav wrote that “if the grantor ofa trust has reserved a power to reacquire trust property by substituting otherproperty of equivalent value, the grantor may retain this power withouttriggering Section 2036. Specifically, Rev. Rul. 2008-22 held that a grantor’sretained power, exercisable in a nonfiduciary capacity, to acquire propertyheld in trust by substituting property of equivalent value will not, by itself,cause the value of the trust corpus to be includible in the grantor’s grossestate under Section 2036 or Section 2038.”

49

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Possible Solutions

50

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

ADVANTAGES DISADVANTAGES

Give General Partnership Interest Away

1. Simple 1. Lose control

2. 2704(b) issue

3. Still under three year rule

Give to Grantor Trust for Grandchildren, Etc.

OR Sell to Grantor Trust for Note or Cash in

“Bona-Fide Sale.”

1. Fairly simple

2. Indirect control by controlling the Trustee

3. Shows continuing desire to benefit family

1. Lose some degree of control

2. Expensive setting up a trust if it does not

already exist

3. Three year rule

Give to Lifetime Qualified Terminable Interest

Property Trust (Q-TIP Trust) for Spouse

1. 2036(a)(2) may not apply

2. Qualifies for marital deduction

1. Same as gift to Grantor Trust (above)

2. Same as gift to Grantor Trust (above)

3. Same as gift to Grantor Trust (above)

Give to Spouse1. Simple - should work if spouse did not

contribute to entity

1. Will spouse be considered a “deemed

agent” of the original contributor?

Appoint Fiduciary Officer with Exclusive

Distribution Liquidation Right in Partnership

or Operating Agreement

1. Simple to draft

2. Client may have the right to replace the

selected fiduciary with an alternate unrelated

qualified party

3. No transfers or new trusts needed

1. Unconventional to have segregation of

fiduciary duties and “trust-like provisions” in

an LLC or limited partnership agreement

2. Many clients will not have a list of non-

related parties that they would trust to be the

liquidation/distribution fiduciary

Liquidate the Entity

1. Simple and inexpensive, if it does not

trigger tax

2. Non-existent entity is less likely to be

audited or scrutinized

3. Distributed assets may be put to good use

if the children who are members/partners are

already at retirement age

1. Loss of control of the assets

2. Possible misuse or premature use or

spending by individual members/partners

3. Loss of discount for portion of entity

owned by contributor

STRATEGIES TO AVOID 2036(a)(2) INCLUSION – POWELL AND STRANGI AVOIDANCE TECHNIQUES

51

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

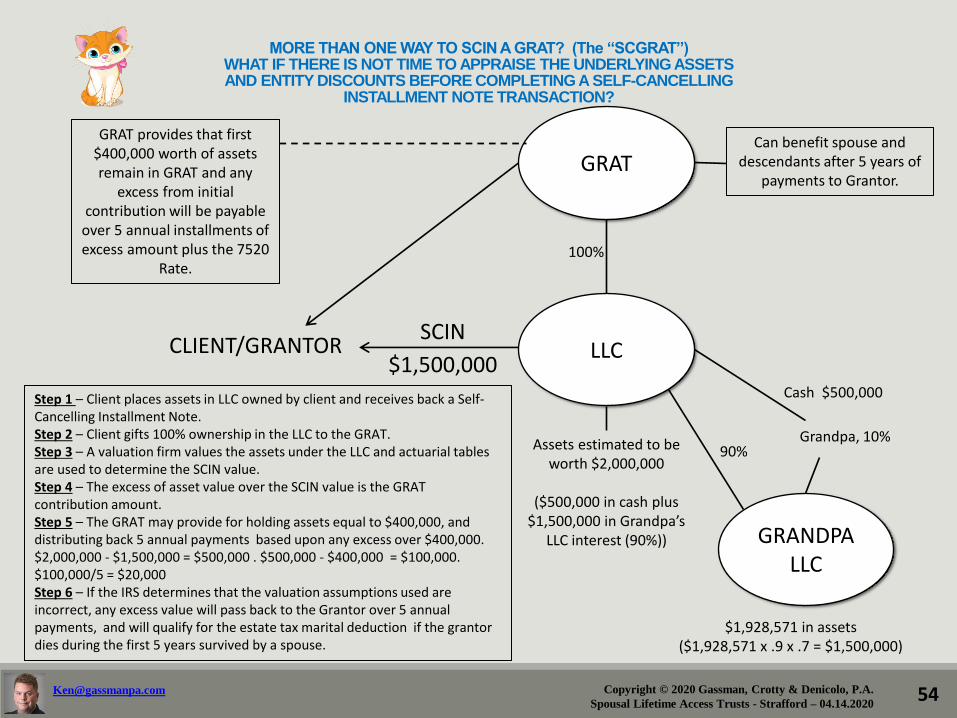

MORE THAN ONE WAY TO SCIN A GRAT? (The “SCGRAT”)WHAT IF THERE IS NOT TIME TO APPRAISE THE UNDERLYING ASSETS AND ENTITY DISCOUNTS BEFORE COMPLETING A SELF-CANCELLING

INSTALLMENT NOTE TRANSACTION?

GRAT

LLCSCIN

$1,500,000CLIENT/GRANTOR

Assets estimated to be worth $2,000,000

($500,000 in cash plus $1,500,000 in Grandpa’s

LLC interest (90%))

Cash $500,000

GRANDPALLC

$1,928,571 in assets($1,928,571 x .9 x .7 = $1,500,000)

Grandpa, 10%90%

Step 1 – Client places assets in LLC owned by client and receives back a Self-Cancelling Installment Note.Step 2 – Client gifts 100% ownership in the LLC to the GRAT.Step 3 – A valuation firm values the assets under the LLC and actuarial tables are used to determine the SCIN value.Step 4 – The excess of asset value over the SCIN value is the GRAT contribution amount.Step 5 – The GRAT may provide for holding assets equal to $400,000, and distributing back 5 annual payments based upon any excess over $400,000. $2,000,000 - $1,500,000 = $500,000 . $500,000 - $400,000 = $100,000. $100,000/5 = $20,000Step 6 – If the IRS determines that the valuation assumptions used are incorrect, any excess value will pass back to the Grantor over 5 annual payments, and will qualify for the estate tax marital deduction if the grantor dies during the first 5 years survived by a spouse.

GRAT provides that first $400,000 worth of assets remain in GRAT and any

excess from initial contribution will be payable

over 5 annual installments of excess amount plus the 7520

Rate.100%

Can benefit spouse and descendants after 5 years of

payments to Grantor.

54

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

BACKGROUND INFORMATION THAT IS PERTINENT TO THE CONSIDERATION OF THE SCGRAT

BY: ALAN S. GASSMAN, J.D., LL.M. AND KENNETH J. CROTTY, J.D., LL.M.

The use of a leveraged Grantor owned limited liability company, or limited partnership is the subject of extensive writings provided by S. Stacy Eastland, who is a well respected estate tax planning lawyer who presently works as a Managing Director for Goldman & Sachs.

Mr. Eastland’s Bloomberg BNA outline that was presented on March 23, 2012 entitled Two of our Favorite 2012 Gift Planning Ideas We See Out There; The Leveraged GRAT and the Remainder Purchase Marital Trust discusses the use of an LLC that can initially be owned by the Grantor to hold investments and can owe a note back to the Grantor to effectively leverage the contribution to a Grantor Retained Annuity Trust (“GRAT”).

These materials include an in depth discussion of the Step Transaction Doctrine at pages 23 through 26 indicating that “The creation of the family limited partnership, or Family Limited Liability Company should be designed to be sufficiently independent on its own, and as an a act that does not require a sale to that trust. There does not have to be a business purpose for the creation of the trust. It is difficult for this writer (Mr. Eastland) to understand the business purpose of any gift. As noted above, the Supreme Court has said on two separate occasions, estate and gift tax law should be applied in a manner that follows estate property law analysis. The outlined footnotes the US Supreme Court Cases of United States v. Bess (1958), Morgan v. Commissioner (1940), and the Ninth Circuit Case of Lindt v. US, which provides the following quote from Learned Hand’s decision “that anyone may so arrange his affairs that his taxes shall be as low as possible; he is not bound to choose that pattern which will best pay the Treasury” Helvering v. Gregory 69 F. 2d 809, 810-11 (2d Cir. 1934)?

Mr. Eastland’s outline provides further discussion on the ability to have a GRAT provide that a specified dollar of value in assets can be retained, with excess value being used to measure the GRAT’s payments back to the Grantor.Footnote 61 on page 57 of Mr. Eastland’s materials reads as follows:

For example, the formula might define the annuity as that percentage of the initial value of the trust assets (as finally determined for federal gift tax purposes) which will result in an annuity having a present value at the inception of the trust equal to the initial value of the trust assets (as so determined) less $4,800,000. A GRAT annuity defined in this way has not been passed upon by the IRS or the courts. It should meet the requirements of Treas. Reg. 25.2702-3(b)(i)(B), which permits the annuity to be “[a] fixed fraction or percentage of the initial fair market value of the property transferred to the trust, as finally determined for federal tax purposes, payable periodically but not less frequently than annually, but only to the extent the fraction or

percentage does not exceed 120 percent of the fixed fraction or percentage payable in the preceding year.” In order to freeze the remainder value at a constant dollar amount, such a formula definition generates a greater annuity percentage (not just a greater annuity amount) for a higher initial value. The percentage is dependent upon finally determined asset values and is fixed by them, since there is only one percentage corresponding to any given initial value of the trust. It therefore is hard to see in what sense this would not be a “fixed percentage,” and the regulatory definition, with its reference to values “as finally determined for federal tax purposes,” seems entirely consistent with defining the annuity percentage in this way. An initial annuity percentage defined in this way could then be made subject to the 20% annual increase permitted under the regulation, although that is not a feature of the technique under discussion.

Mr. Eastland’s materials further discuss whether generation skipping tax exemption can be allocated to a GRAT where there is less than a 5% chance that the Grantor will die before receiving all GRAT payments.

Mr. Eastland states that based upon the rates in effect at the time of publication in 2012 that a two year GRAT payable to a Grantor under age 70 would satisfy the 5% maximum life expectancy requirement and that it should therefore be possible to allocate GST exemption to the GRAT under the ETIP (“Estate Tax Inclusion Period”) rules. The ETIP rules prevent allocation of GST exemption to a GRAT in many circumstances. This discussion begins at page 55 of those materials.

It would be safest to wait until the GRAT term ends before allocating GST exemption to the GRAT.

Stacy [email protected]

55

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

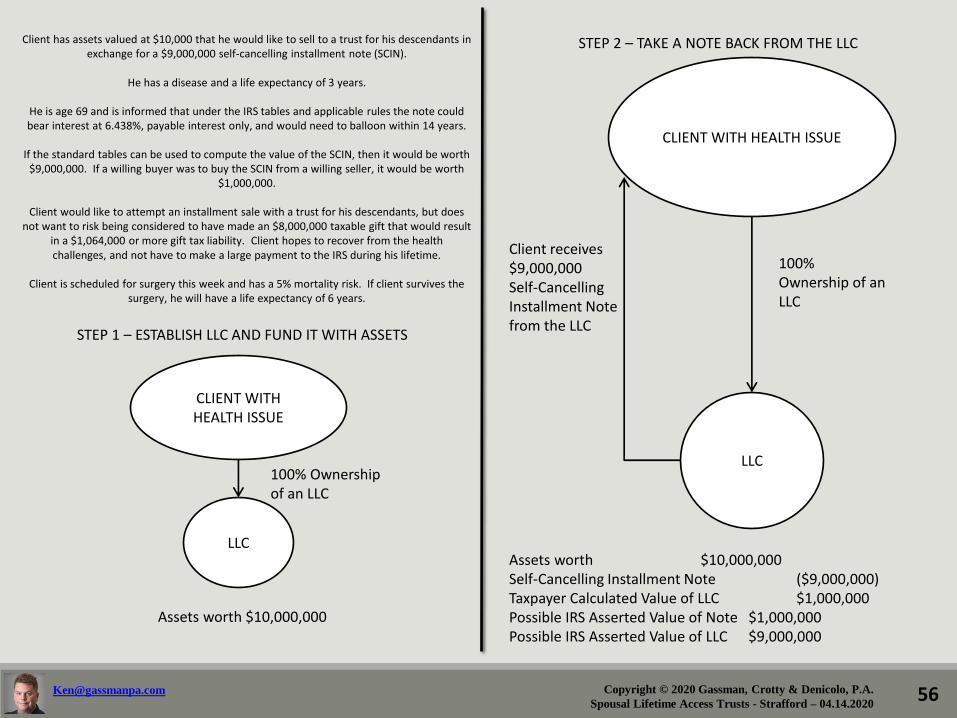

Client has assets valued at $10,000 that he would like to sell to a trust for his descendants in exchange for a $9,000,000 self-cancelling installment note (SCIN).

He has a disease and a life expectancy of 3 years.

He is age 69 and is informed that under the IRS tables and applicable rules the note could bear interest at 6.438%, payable interest only, and would need to balloon within 14 years.

If the standard tables can be used to compute the value of the SCIN, then it would be worth $9,000,000. If a willing buyer was to buy the SCIN from a willing seller, it would be worth

$1,000,000.

Client would like to attempt an installment sale with a trust for his descendants, but does not want to risk being considered to have made an $8,000,000 taxable gift that would result

in a $1,064,000 or more gift tax liability. Client hopes to recover from the health challenges, and not have to make a large payment to the IRS during his lifetime.

Client is scheduled for surgery this week and has a 5% mortality risk. If client survives the surgery, he will have a life expectancy of 6 years.

STEP 1 – ESTABLISH LLC AND FUND IT WITH ASSETS

CLIENT WITH HEALTH ISSUE

LLC

100% Ownership of an LLC

Assets worth $10,000,000

STEP 2 – TAKE A NOTE BACK FROM THE LLC

CLIENT WITH HEALTH ISSUE

LLC

100% Ownership of an LLC

Assets worth $10,000,000Self-Cancelling Installment Note ($9,000,000)Taxpayer Calculated Value of LLC $1,000,000Possible IRS Asserted Value of Note $1,000,000Possible IRS Asserted Value of LLC $9,000,000

Client receives $9,000,000Self-Cancelling Installment Note from the LLC

56

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

STEP 3

Client establishes a Grantor Retained Annuity Trust (GRAT) which provides

that the value of assets contributed to it will be multiplied by 27%, and that

dollar amount will be paid to client each year for four (4) consecutive years.

CLIENT GRAT

LLC

CLIENT CONTRIBUTES

LLC TO THE GRAT

GRAT makes 4 annual paymentsof 27% of the value of the LLC

back to the client.

STEP 4 – HOPED FOR OUTCOME

Client transfers 100% ownership of the LLC to the GRAT and payments of $270,000 per year

are scheduled to be made.

LLC

100%

4 annual payments of $270,000

CLIENT

GRAT

Self-cancellingInstallment Note

The client also receives annual interest payments of $579,420 a year from the LLC under the SCIN.

STEP 5 – OUTCOME IF NOTE IS WORTH ONLY $1,000,000

In the unlikely event that the IRS were to succeed in claiming that the promissory

note is worth only $1,000,000, then there would be no gift tax due, and

because under the GRAT formula payment clause client would have the

right to receive $2,430,000 per year worth of assets from the GRAT. This

generally places the family back to where they would be.

LLC

100%

4 annual payments of $2,430,000

CLIENT

GRAT

Self-cancellingInstallment Note

The client also receives annual interest payments of $64,380 a year from the LLC under the SCIN

57

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Transfer

Subject to

Additional

Gift Tax?

Language of Valuation Adjustment

Analyzed by the Court

Proctor1

(4th Cir. 1944)Yes

"The Grantor is advised by counsel and satisfied that the present transfer is not subject to Federal gift

tax. However, in the event it should be determined by final judgment or order of a competent federal

court of last resort that any part of the transfer in trust hereunder is subject to gift tax, it is agreed by all

the parties hereto that in that event the excess property hereby transferred which is decreed by such court

to be subject to gift tax, shall automatically be deemed not to be included in the conveyance in trust

hereunder and shall remain the sole property of Frederic W. Procter free from the trust hereby created.“2

King3

(10th Cir. 1976)

Taxpayer resided in

Colorado

Taxpayer victory

No

"However, if the fair market value of The Colorado Corporation stock as of the date of this letter is ever

determined by the Internal Revenue Service to be greater or less than the fair market value determined in

the same manner described above, the purchase price shall be adjusted to the fair market value

determined by the Internal Revenue Service.“4

Harwood5

(Tax Court, 1984)Yes

“In the event that the value of the partnership interest listed in Schedule "A" shall be finally determined

to exceed $ 400,000 for purposes of computing the California or United States Gift Tax, and in the

opinion of the Attorney for the trustee a lower value is not reasonably defendable, the trustee shall

immediately execute a promissory note to the trustors in the usual form at 6 percent interest in a

principal amount equal to the difference between the value of such gift and $ 400,000. “

58

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Transfer

Subject to

Additional

Gift Tax?

Language of Valuation Adjustment

Analyzed by the Court

Ward6

(Tax Court, 1986)Yes

“In consideration of love and affection, each Donor does hereby assign to each Donee all of the Donor's

right, title and interest in and to twenty-five (25) shares of the capital stock of J-SEVEN RANCH, INC.,

a Florida corporation, hereinafter called the "Corporation". The parties acknowledge that the

computation of the number of shares constituting each gift has been based upon their mutual

understanding and belief that the fair market value of each share is $ 2,000.00, resulting in tax liability

for each Donor less than the amount of unified credit against gift tax to which the Donor is entitled at

this time under applicable provisions of law.

Each party hereto agrees that if it should be finally determined for Federal gift tax purposes that the fair

market value of each share of capital stock of the Corporation exceeds or is less than $ 2,000.00 an

adjustment will be made in the number of shares constituting each gift so that each Donor will give to

each Donee the maximum number of full shares of capital stock of the Corporation, the total value of

which will be $ 50,000.00 from each Donor to each Donee and a total of $ 150,000 from each Donor to

all Donees. Any adjustment so made which results in an increase or decrease in the number of shares

held by a stockholder of the Corporation will be made effective as of the same date as this Agreement,

and any dividends paid thereafter shall be recomputed and reimbursed as necessary to give effect to the

intent of this Agreement.”

Knight7

(Tax Court, 2001)Yes

“Transferor irrevocably transfers and assigns to each Transferee above identified, as a gift, that number

of limited partnership units in Herbert D. Knight Limited Partnership which is equal in

value, on the effective date of this transfer, to $ 600,000.”

59

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Transfer

Subject to

Additional

Gift Tax?

Language of Valuation Adjustment

Analyzed by the Court

McCord8

(5th Cir. 2006)

Taxpayers resided

in Louisiana

Taxpayer victory

No

"[T]he fair market value of the Assigned Partnership Interest as of the date of this

Assignment Agreement shall be the price at which the Assigned Partnership Interest would

change hands as of the date of this Assignment Agreement between a hypothetical willing

buyer and a hypothetical willing seller, neither being under any compulsion to buy or sell

and both having reasonable knowledge of relevant facts.”9

In re Christiansen

(8th Cir. 2009)10

Taxpayer resided

in South Dakota

Taxpayer victory

No

"Partial Disclaimer of the Gift: Intending to disclaim a fractional portion of the Gift,

Christine Christiansen Hamilton hereby disclaims that portion of the Gift determined by

reference to a fraction, the numerator of which is the fair market value of the Gift (before

payment of debts, expenses and taxes) on April 17, 2001, less Six Million Three Hundred

Fifty Thousand and No/100 Dollars ($6,350,000.00) and the denominator of which is the fair

market value of the Gift (before payment of debts, expenses and taxes) on April 17, 2001

("the Disclaimed Portion"). For purposes of this paragraph, the fair market value of the Gift

(before payment of debts, expenses and taxes) on April 17, 2001, shall be the price at which

the Gift (before payment of debts, expenses and taxes) would have changed hands on April

17, 2001, between a hypothetical willing buyer and a hypothetical willing seller, neither

being under any compulsion to buy or sell and both having reasonable knowledge of relevant

facts for purposes of Chapter 11 of the [Internal Revenue] Code, as such value is finally

determined for federal estate tax purposes."

60

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Transfer

Subject to

Additional

Gift Tax?

Language of Valuation Adjustment

Analyzed by the Court

Petter11

(9th Cir. 2011)

Taxpayer resided in

Washington

Taxpayer victory

No

Transferor wishes to assign X number of Units in the Company (the "Units") including all of the

Transferor's right, title and interest in the economic, management and voting rights in the Units as a gift

to the Transferees.

1. Subject to the terms and conditions of this Agreement, Transferor:

1. assigns to the Trust as a gift the number of Units described in the Recital above that

equals X dollar amount that can pass free of federal gift tax by reason of

Transferor's applicable exclusion amount allowed by Internal Revenue Code

Section 2010(c). Transferor currently understands her unused applicable exclusion

amount to be X dollars, so that the amount of this gift should be X dollars; and

2. assigns to The Charity as a gift . . . the difference between the total number of Units

described in the Recital above and the number of Units assigned to the Trust in

Section 1.1.1.

The Trust agrees that, if the value of the Units it initially receives is finally determined for federal gift tax purposes to exceed the amount described in Section 1.1.1, Trustee will, on behalf of the Trust and as a condition of the gift to it, transfer the excess Units to The Charity as soon as practicable.1.3 The Charity agrees that, if the value of the Units the Trust initially receives is finally determined for federal gift tax purposes to be less than the amount described in Section 1.1.1, The Charity will, as a condition of the gift to it, transfer the excess Units to the Trust as soon as practicable."

61

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Transfer

Subject

to

Addition

al

Gift Tax?

Language of Valuation Adjustment

Analyzed by the Court

Hendrix12

( Tax Court,

2011)

Taxpayers

resided in Texas

Taxpayer victory

No

"Each agreement effected the transfer pursuant to a formula under which: (1) A

portion of the assigned shares having a fair market value as of the effective date

equal to $10,519,136.12 was assigned to the trustees to be held in equal shares for

the benefit of the daughters, and (2) any remaining portion of the assigned shares

was assigned to the Foundation for the benefit of the donor-advised fund. The

assignment agreements defined fair market value as the price at which those shares

would change hands as of the effective date between a hypothetical willing buyer

and a hypothetical willing seller, neither under any compulsion to buy or to sell and

both having reasonable knowledge of relevant facts." 13

62

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Summary of cases where courts have addressed the step transaction doctrine by analyzing the close proximity between date of funding of entity and date of transfer of entity interests.

Case Name/Court

Deci-sion Date

DateEntity

Formed

Date AssetsTransf-erred

Date InterestGifted

# of days in between

Court Found

For

Type of Assets

Invested

Court Held Court’s Dicta Special notes

Holman v.

Comr. (U.S.

Tax Ct.)

5/27/08 11/3/99 11/2/99 11/8/99 6 Taxpayer Shares of

Dell stock

The limited

partnership was

formed and the

shares of Dell

stock were

transferred to it

almost 1 week in

advance of the

gift, so that on

the facts before

us, the transfer

cannot be viewed

as an indirect gift

of the shares to

the donees.

Furthermore, the

gift may not be

viewed as an

indirect gift of the

shares to the

donees under the

step transaction

doctrine.

This case is distinguishable

from Senda because

petitioners did not contribute

the Dell shares to the

partnership on the same day

they made the 1999 gift;

indeed, almost 1 week passed

between petitioners' formation

and funding of the partnership

and the 1999 gift. Petitioners

bore the risk that the value of

an LP unit could change

between the time they formed

and funded the partnership and

the times they chose to

transfer the LP units.

Therefore, the Court decided

not to disregard the passage of

time and treat the formation

and funding of the partnership

and the subsequent gifts as

occurring simultaneously under

the step transaction doctrine.

Also, in this case, the IRS

conceded that a 2-month

separation is sufficient to give

independent significance to the

funding of a partnership and a

subsequent gift of LP units.

There were

other gifts and

transfers, but

the Court was

only

concerned

with the

November set

of

transactions.

63

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Summary of cases where courts have addressed the step transaction doctrine byanalyzing the close proximity between date of funding of entity and date of transfer

of entity interests.

Case Name/Court

Deci-sion Date

DateEntity

Formed

Date AssetsTransf-erred

Date InterestGifted

# of days in

between

Court Found

For

Type of Assets

Invested Court Held Court’s DictaSpecial notes

Senda v.

Comr.

(U.S. Tax

Ct.)

7/12/04 6/3/98

(SFLP I)

12/2/99

(SFLP II)

12/28/98

12/20/99

12/28/98

12/20/99

0

0

IRS Shares of

stock

Shares of

stock

The

taxpayers'

transfers of

stock to

partnerships,

coupled with

transfer of

limited

partnership

interests to

their children,

were indirect

gifts of stock

to children,

and thus,

stock and not

partnership

interests,

would be

valued for gift

tax purposes.

Petitioners presented no

reliable evidence that

they contributed the stock

to the partnerships before

they transferred the

partnership interests to

the children. It is unclear

whether petitioners'

contributions of stock

were ever reflected in

their capital accounts. At

best, the transactions

were integrated and, in

effect, simultaneous.

Therefore, the Court

concluded that the value

of the children's

partnership interests was

enhanced upon

petitioners' contributions

of stock to the

partnerships and were

indirect gifts.

On January

31, 2000,

petitioner

gave to

each child

an

additional

4.5-percent

limited

partnership

interest in

SFLP II.

64

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Summary of cases where courts have addressed the step transaction doctrine by analyzing the close proximity between date of funding of entity and date of

transfer of entity interests.

Case Name/Court

Deci-sion Date

DateEntity

Formed

Date AssetsTransf-erred

Date InterestGifted

# of days in

between

Court Found

For

Type of Assets

Invested Court Held Court’s DictaSpecial notes

Estate of

Jones v.

Comr.

(U.S. Tax

Ct.)

3/6/01 1/1/95

(JBLP)

1/1/95

(AVLP)

1/1/95

1/1/95

1/1/95

1/1/95

0

0

Tax-

payer

Assets

including

real

property

Transfers of

property to

partnerships

were not

taxable gifts.

All of the contributions of

property were properly

reflected in the capital

accounts of the taxpayer,

and the value of the other

partners' interests was

not enhanced by the

contributions of decedent.

Therefore, the

contributions do not

reflect taxable gifts.

65

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

Summary of cases where courts have addressed the step transaction doctrine by analyzing the close proximity between date of funding of entity and date of transfer of entity interests.

Case Name/Court

Deci-sion Date

DateEntity

Formed

Date AssetsTransf-erred

Date InterestGifted

# of days in between

Court Found

For

Type of Assets

Invested Court Held Court’s DictaSpecial notes

Shepherd

v. Comr.

(U.S. Tax

Ct.)

10/26/00 8/2/91 Leased

Land

(8/1/91) ;

Bank

Stock

(9/9/91)

8/2/91 Varies IRS Fee

interest in

timberland

subject to

a long-

term

timber

lease and

stocks in

three

banks

Transfers

represent

separate

indirect gifts to

his sons of

25% undivided

interests in the

leased

timberland and

stocks.

Not every capital

contribution to a

partnership results in a gift

to the other partners,

particularly where the

contributing partner's

capital account is increased

by the amount of his

contribution, thus entitling

him to recoup the same

amount upon liquidation of

the partnership. Here,

however, petitioner's

contributions of the leased

land and bank stock were

allocated to his and his

sons' capital accounts

according to their

respective partnership

shares. Upon dissolution of

the partnership, each son

was entitled to receive

payment of the balance in

his capital account.

66

Copyright © 2020 Gassman, Crotty & Denicolo, P.A.

Spousal Lifetime Access Trusts - Strafford – 04.14.2020

WHAT IS THE RECIPROCAL TRUST DOCTRINE?

Many married couples will make use of the $11,580,000 lifetime gifting exclusion by having each spouse create a dynasty trust that would preferably benefit both the other spouse and their descendants. Unfortunately, when two people establish trusts that benefit each other, each person might become considered as the constructive Grantor as to the trust assets that he or she can benefit from, and thus the assets of the trust that he or she can benefit from would be subject to federal estate tax on his or her death under Internal Revenue Code Section 2036(a). The reciprocal trust doctrine is the judicial recognition of this phenomenon.