squre pharmaceuticals

TRANSCRIPT

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 121

1

Faculty of Business amp Economics

BBA Program

Sec ldquoBrdquo

Assignment on Impact of Direct and Indirect tax of

Bangladesh

Submitted to Farzana HudaLecturer

DIU

Submitted by

Student Name Student IDMdReazul Islam 073-11-2109Abu Bakar Siddiquez 09152-11-771Soyeb Mahmud 09152-11-746Sahadat Hossian 073-11-2112Md Mustafijur Rahman 073-11-2116

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 221

2

Submission Date 13th

April 2010

Farzana HudaLecturer

Faculty of business and economicsDaffodil International University

Dear Madam

Subject Letter of Transmittal

We are going to submit the report what we prepared on

Impact of Direct and Indirect tax of Bangladesh to you for further clarification The authority of this report is beingtransmitted to you as well Therefore we fervently hope that you would kindenough to let us inform the feedback regarding our report However if yourequire more information we will be very happy to provide that in future

Thank youSincerely yours

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 321

3

Executive summary

The term direct tax generally means a tax paid directly to the government by the persons

on whom it is imposed

A tax levied on goods or services rather than on persons or organizations is indirect tax

Income tax wealth tax is the direct tax and customs excise vat etc is the indirect tax

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 421

4

Introduction

Direct Tax

a tax paid directly by the person or organization on which it is leviedA tax demanded from the very persons who it is intended or desired should

pay it

The term direct tax generally means a tax paid directly to the government by the persons

on whom it is imposed

In the general sense a direct tax is one paid directly to the government by the persons(juristic or natural) on whom it is imposed (often accompanied by a tax return filed by thetaxpayer) Examples include some income taxes some corporate taxes and transfer taxessuch as estate (inheritance) tax and gift tax In this sense a direct tax is contrasted with anindirect tax or collected tax (such as sales tax or value added tax (VAT)) a collectedtax is one which is collected by intermediaries who turn over the proceeds to thegovernment and file the related tax return Some commentators have argued that a direct

tax is one that cannot be shifted by the taxpayer to someone else whereas an indirect taxcan be

The power of direct taxation applies to every individual as congress under thisgovernment is expressly vested with the authority of laying a capitation or poll-tax uponevery person to any amount This is a tax that however oppressive in its nature andunequal in its operation is certain as to its produce and simple in it collection it cannot be evaded like the objects of imposts or excise and will be paid because all that a manhath will he give for his head This tax is so congenial to the nature of despotism that it

has ever been a favorite under such governments Some of those who were in the lategeneral convention from this state have long labored to introduce a poll-tax among us

The power of direct taxation will further apply to every individual as congress may tax

land cattle trades occupations ampc to any amount and every object of internal taxation

is of that nature that however oppressive the people will have but this alternative either

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 521

5

Indirect Tax

a tax levied on goods or services rather than on persons or organizations

Tax - definition of tax - A fee charged (levied) by a government on a product on the price of a good or service then it is called an indirect tax

Charge levied by the State on consumption expenditure privilege or right but not on

income or property Customs duties levied on imports excise duties on production sales

tax or value added tax (VAT) at some stage in production-distribution process are

examples of indirect taxes because they are not levied directly on the income of the

consumer or earner Since they are less obvious than income tax (because they dont show

up on the wage slip) politicians are tempted to increase them to generate more state

revenue Also called consumption taxes they are regressive measures because they are

not based on the ability to pay principle

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 621

6

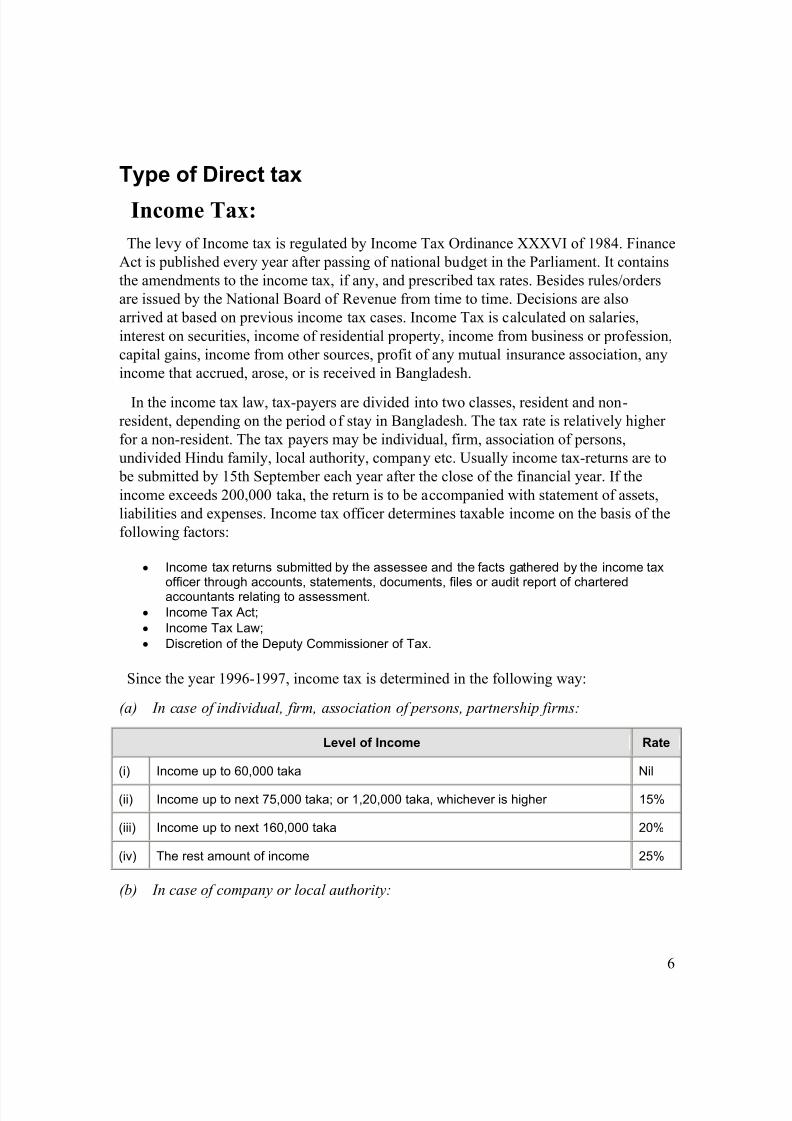

Type of Direct tax

Income Tax

The levy of Income tax is regulated by Income Tax Ordinance XXXVI of 1984 Finance

Act is published every year after passing of national budget in the Parliament It contains

the amendments to the income tax if any and prescribed tax rates Besides rulesorders

are issued by the National Board of Revenue from time to time Decisions are also

arrived at based on previous income tax cases Income Tax is calculated on salaries

interest on securities income of residential property income from business or profession

capital gains income from other sources profit of any mutual insurance association any

income that accrued arose or is received in Bangladesh

In the income tax law tax-payers are divided into two classes resident and non-

resident depending on the period of stay in Bangladesh The tax rate is relatively higher

for a non-resident The tax payers may be individual firm association of persons

undivided Hindu family local authority company etc Usually income tax-returns are to

be submitted by 15th September each year after the close of the financial year If the

income exceeds 200000 taka the return is to be accompanied with statement of assets

liabilities and expenses Income tax officer determines taxable income on the basis of the

following factors

Income tax returns submitted by the assessee and the facts gathered by the income taxofficer through accounts statements documents files or audit report of charteredaccountants relating to assessment

Income Tax Act

Income Tax Law

Discretion of the Deputy Commissioner of Tax

Since the year 1996-1997 income tax is determined in the following way

(a) In case of individual firm association of persons partnership firms

Level of Income Rate

(i) Income up to 60000 taka Nil

(ii) Income up to next 75000 taka or 120000 taka whichever is higher 15

(iii) Income up to next 160000 taka 20

(iv) The rest amount of income 25

(b) In case of company or local authority

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 721

7

All income except dividend income of the Company that is registered in Bangladesh istaxable The rate is as follows-

Category Rate

(i) Income of Publicly Traded Company 35

(ii) Income of non-Publicly Traded Company 40

(iii) Bank Insurance or Investment Companies nonresident Companies 45

The rate of income tax will be 15 on the amount representing income from dividends

declared and paid by a company formed and registered in Bangladesh under companies

Act 1913 or a body corporate formed in pursuance of an Act of Parliament in respect of

the share capital issued subscribed and paid after 14th August 1947

In the case of a person not being a Company (non-resident) the rate of income tax will be

25 of income

Wealth Tax

Wealth tax is regulated by the provisions of Wealth Tax Act 1963 (Act No XV)

Wealth is assessed as per the prevailing market price in respect of the wealth of Hindu

undivided family or individual

Value of Wealth Rate

(i) First 25000000 taka net wealth Nil

(ii) Next 50000000 taka net wealth 12

(iii) Next 50000000 taka net wealth 34

(iv) For the balance amount of Value 1

If any tax payer pays income and wealth taxes in any year wealth tax plus income tax

must not exceed 30 of income

The number of wealth tax payers stood at 18350 in 1994-1995 943 Gift Tax

Gift tax Act 1963 was repealed in 1985 but came into force again in 1990 As per the

quoted Act gift means any transfer of ownership of movable or immovable property by

one person to another willingly and without any profit Property is evaluated at thecurrent market price

The following rates are applicable now

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 821

8

Value of property Rate

(i) 5000000 taka beyond exempted limit 5

(ii) On next 10000000 taka value 10

(iii) On next 10000000 taka value 15

(iv) On the balance amount of value 20

Indirect Taxes

The following are the main indirect taxes

Customs

Wester defines customs as duties tolls or imposts imposed by sovereign laws of a

country on imports and exports This duty is imposed as per Bangladesh Customs Act

1969 and as per the Customs Tariff As per the Customs Act banned and illegal items aresold on auction and sale-proceeds are deposited into government treasury Smuggled gold

seized at airsea ports are deposited into Central Bank

In order to hasten customs clearance and thereby encourage investment in the country

government has introduced Per-shipment Inspection (PSI) Scheme under which approved

internationally reputed inspection firms issue certificate regarding quality quantity price

classification of the imported items On the basis of that certificate (known as Clean

Report on Finding) goods are cleared without delay at sea or air ports But Revenue

Audit authorities have detected cases of under-invoicing and wrong classification by the

PSI agencies which deprive the government of large revenues

Moreover bonded ware houses get special duty privileges for imports There are 2956

bonded warehouses (private and special) in the country There are also privileges for

import under baggage rules

Excise

Excise duty is imposed on some items that are produced within Bangladesh Being an

indirect tax it is paid by the manufacturer who can pass its incidence to consumers This

is guided by Excises and Salt Act 1944 and Statutory Rules amp Order of 1984 At present

excise duty is charged on bidi (local cigarette) 25 taka per thousand on cotton Tk

150 per kilogram and cotton cloth Tk 150 per metre Excise duty is also imposed onBanking services

VAT

Value Added Tax is imposed on production wholesaling and retailing when value is

added This was introduced in 1991 Maximum limit of VAT is 15 on import and

home-made goods and services The number of registered firmscompanies under VAT

net is 100000 (approx)

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 921

9

Supplementary Duty This is imposed on luxury items and services like cigarette cinema alcohol etc in

addition to VAT The rate varies from 5 to 350

Turnover Tax

Those organisations whose annual sale is less than Taka 150000000 are to pay

turnover tax

Bangladesh Tax Information

I n Bangladesh the principal direct taxes are personal income taxes and corporateincome taxes and a value-added tax (VAT) of 15 levied on all important consumer

goods The top income tax rate for individuals is 25 For the 200405 tax year (July 1

2004 ndash June 30 2005) the top corporate rate was 45 However publicly tradedcompanies registered in Bangladesh are charged a lower rate of 30 Banks financial

institutions and insurance companies are charged the 45 rate All other companies are

taxed at the 375 rate Effective 1 July 2002 the VAT rate on computer hardware and

software was reduced to 75 and certain agricultural equipment and electricity supplied to the agricultural sector was exempted from VAT altogether VAT on the

transfer of land is also to be abolished Essential agricultural implements and irrigation pumps had previously been excluded from certain taxes

Corporate tax Corporate tax rates for industrial companies whose shares are publicly traded is 35 andthe rate of those whose shares are not publicly traded is 40

Tax rates on other companies Tax rates on income of all other companies including banks financial institutionsinsurance companies and local authorities is 45

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1021

10

Investment requirement by companies enjoying tax holiday Companies enjoying tax

holidays are required to invest only 25 to 30 of their income in other activities as perrule of NBR

Accepted of returns of public limited companies Returns filed by the public limited companies shall be accepted as correct if it isaccompanied by audited accounts and certified by a chartered accountant as to thecorrectness of the total income of the assessee

Salary of foreign technicians Salary income received by or due to a foreign technician under contract of serviceapproved by the National Board of Revenue is fully exempted from paying tax (subject to prescribed conditions and limitations) for a period of three years from the date of hisarrival in Bangladesh

Tax payable by employer on remuneration of foreign technician Expenditure incurred by an employer in respect of remuneration of a foreign technician isalso fully exempted from income tax (subject to the stipulated conditions)

the price of a good or service then it is called an indirect tax

Remuneration of foreign technicians employed by the firms of consultancy and

engineers

Expenditure incurred as remuneration payable to a foreign technicians by a Bangladeshifirm carrying on the business of consultant and engineers in Bangladesh is fullyexempted from tax (subject to prescribed conditions and limitations

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1121

11

Amount of TaxIf an individual has been in Bangladesh for a periodperiod totaling 182 days or more in

the income year heshe is considered a resident In case an individual has been in the

country for 90 days in the income year and 365 days in four years preceding this yearheshe will also be considered a resident

Each individual is entitled to an investment tax credit of 15 percent of the total income or

Tk 100000 whichever is less Incomes from small and cottage industries are entitled to a

5 to 10 per cent tax rebate depending on the production volume

On the first Tk 6000000 of total income - no tax obligation

On the next Tk 4000000 of total income - 10

On the next Tk 5000000 of total income - 15

On the next Tk 15000000 of total income - 20

On the balance of total income - 25

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1221

12

Effect of direct tax

The total effect on households of such taxes is assessed using input-output analysis Thus

both the direct effect of taxes through increased fuel prices and the indirect effect

through increased prices of other goods can be assessed simultaneously This input-

output approach allows the generation of direct plus indirect pollution intensities for all

household consumption categories for in principle a number of pollutants (CO2 SO2

NOx particulates) These intensities could then be used to assess the impact on

households of pollution taxes This paper concentrates on CO2 and energy performing a

static analysis of the effect of a tax on the carbon or energy content of goods using the

known consumption patterns for the various countries both in aggregate and for different

income groups This allows a first assessment of the regressiveprogressive effects of

such taxes and an indication of consumer welfare loss

The legal definition and the economic definition of taxes differ in that economists do not

consider many transfers to governments to be taxes For example some transfers to the

public sector are comparable to prices Examples include tuition at public universities and

fees for utilities provided by local governments Governments also obtain resources by

creating money (eg printing bills and minting coins) through voluntary gifts (eg

contributions to public universities and museums)by imposing penalties (eg trafficfines) by borrowing and by confiscating wealth From the view of economists a tax is a

non-penal yet compulsory transfer of resources from the private to the public sector

levied on a basis of predetermined criteria and without reference to specific benefit

received

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1321

13

Purposes and ef fects

Funds provided by taxation have been used by states and their functional equivalents

throughout history to carry out many functions Some of these include expenditures on

war the enforcement of law and public order protection of property economic

infrastructure (roads legal tender enforcement of contracts etc) public works social

engineering and the operation of government itself Governments also use taxes to fund

welfare and public services These services can include education systems health care

systems pensions for the elderly unemployment benefits and public transportation

Energy water and waste management systems are also common public utilities Colonial

and modernizing states have also used cash taxes to draw or force reluctant subsistence

producers into cash economies

Governments use different kinds of taxes and vary the tax rates This is done to distribute

the tax burden among individuals or classes of the population involved in taxable

activities such as business or to redistribute resources between individuals or classes in

the population Historically the nobility were supported by taxes on the poor modern

social security systems are intended to support the poor the disabled or the retired by

taxes on those who are still working In addition taxes are applied to fund foreign and

military aid to influence the macroeconomic performance of the economy (the

governments strategy for doing this is called its fiscal policy - see also tax exemption) or

to modify patterns of consumption or employment within an economy by making some

classes of transaction more or less attractive

A nations tax system is often a reflection of its communal values or the values of those in

power To create a system of taxation a nation must make choices regarding the

distribution of the tax burden mdash who will pay taxes and how much they will pay mdash and

how the taxes collected will be spent In democratic nations where the public elects those

in charge of establishing the tax system these choices reflect the type of community that

the public wishes to create In countries where the public does not have a significant

amount of influence over the system of taxation that system may be more of a reflection

on the values of those in power

The resource collected from the public through taxation is always greater than the amount

which can be used by the government The difference is called compliance cost and

includes for example the labour cost and other expenses incurred in complying with tax

laws and rules The collection of a tax in order to spend it on a specified purpose for

example collecting a tax on alcohol to pay directly for alcoholism rehabilitation centres

is called hypothecation This practice is often disliked by finance ministers since it

reduces their freedom of action Some economic theorists consider the concept to be

intellectually dishonest since (in reality) money is fungible

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1421

14

Effects of income taxation on division of labor

If a tax is paid on outsourced services that is not also charged on services performed foroneself then it may be cheaper to perform the services oneself than to pay someone

else mdash even considering losses in economic efficiency [37][38]

For example suppose jobs A and B are both valued at $1 on the market And suppose

that because of your unique abilities you can do job A twice over (100 extra output) in

the same effort as it would take you to do job B But job B is the one that you need done

right now Under perfect division of labor you would do job A and somebody else would

do job B Your unique abilities would always be rewarded

Income taxation has the worst effect on division of labor in the form of barter Suppose

that the person doing job B is actually interested in having job A done for him Now

suppose you could amazingly do job A four times over selling half your work on themarket for cash just to pay your tax bill The other half of the work you do for somebody

who does job B twice over but he has to sell off half to pay his tax bill Youre left with

one unit of job B but only if you were 400 as productive doing job A In this case of

50 tax on barter income anything less than 400 productivity will cause the division

of labor to fail

In summary depending on the situation a 50 tax rate can cause the division of labor to

fail even where productivity gains of up to 300 would have resulted Even a mere 30

tax rate can negate the advantage of a 100 productivity gain

Direct versus Indirect Taxation

o Direct taxes ndash are paid directly to the Exchequer by the individualtaxpayer ndash usually through ldquopay as you earnrdquo The same is true ofcorporation tax Tax liability cannot be passed onto someone else

o Indirect taxes ndash include VAT and a range of excise duties on oiltobacco alcohol The burden of an indirect tax can be passed on by thesupplier to the final consumer ndash depending on the price elasticity ofdemand and supply for the product

In the last twenty years there has been a shift towards indirect taxation ndash economists differ in their views about what is the optimum mix of taxationbetween indirect and direct taxes

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1521

15

Arguments For Using Indirect Taxation Arguments Against Using Indirect Taxation

Changes in indirect taxes are moreeffective in changing the overall pattern ofdemand for particular goods and servicesie in changing relative prices and therebyaffecting consumer demand (eg anincrease in the real duty on petrol)

Many indirect taxes make the distributionof income more unequal (less equitable)because indirect taxes are more regressive than direct taxes

They are a useful instrument in controllingand correcting for externalities ndash allgovernments have moved towards a morefrequent use of indirect taxes as a means ofmaking the polluter pay and ldquointernalizingthe external costsrdquo of production andconsumption

Higher indirect taxes can cause cost-pushinflation which can lead to a rise ininflation expectations

Indirect taxes are less likely to distort thechoices that people have to betweenwork and leisure and therefore have less ofa negative effect on work incentives

Higher indirect taxes allow a reduction indirect tax rates (eg lower starting rates ofincome tax)

There is no hard evidence that cuttingdirect tax rates has much of an incentiveeffect on peoplersquos decisions about whetheror not to work If indirect taxes are too high

ndash this creates an incentive to avoid taxesthrough ldquoboot-leggingrdquo ndash a good example ofthis would be attempts to evade the highlevels of duty on cigarettes

Indirect taxes can be changed more easilythan direct taxes ndash this gives economicpolicy-makers more flexibility when settingfiscal policy Direct taxes can only bechanged once a year at Budget time

Revenue from indirect taxes can beuncertain particularly when inflation is lowor there is a recession causing a fall inconsume spending

Indirect taxes are less easy to avoid by thefinal tax-payer who might be unaware ofhow much indirect tax they are paying

There is a potential loss of economicwelfare (taxes can create a deadweightloss of consumer and producers surplus)

Indirect taxes provide an incentive to save (and thereby avoid the tax)- a higher levelof savings might be used by the economy tofinance a higher level of capital investment

Higher indirect taxes affect households onlower incomes who are least able to save inthe first place

Indirect taxes leave people free to make achoice whereas direct taxes leave peoplewith less of their gross income in theirpockets

Many people are unaware of how much theyare paying in indirect taxes ndash this goesagainst one of the basic principles of a goodtax system ndash namely that taxes should betransparent

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1621

16

NBR Tax Revenue

In FY 2006-07 2007-08 and 2008-09 the growth of NBR Tax Revenue receipts stood at95 275 and 107 respectively

In FY 2009-10 the target for NBR Tax Revenue is TK 61000 cr (89 of GDP)whichis 119 higher than previous yearrsquos original estimate

During July-September quarter of the current fiscal year TK12 408 cr has beencollected which is 91 higher than previous years collection

In the current quarter growth of Import Duty and Value Added Tax (VAT) at import

levelhas declined by 23 and 87 respectively At the same time VAT at local levelSupplementary Duty at import level and Income Tax showed positive growth of 168203 and 259 respectively (Table 3)

ObservationsTaxGDP ratio (around 85) in Bangladesh is the lowest among the countries of Asian

region It is 4-percentage point lower than the regional average of 125 The ratio needto be increased to reduce our dependence on foreign aid as well as lessen the burden of loanon the future generation and to enhance the absorptive capacity of loan

Owing to increased import of high priced commodities like vehicles the 1st Quarter

Supplementary Duties at import level recorded growth of 203 This rate may declinetowards the end of the year

Achieving budget revenue target may be difficult

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1721

17

Actual Realisation of tax revenue vis-a-vis target

Financial Year Realisation of Target

1980-81 10179

1981 -82 9915

1982-83 9878

1983 -84 9748

1984-85 10292

1985-86 10197

1986-87 10101

1987-88 10101

1988-89 9854

1989-90 9887

1990-91 10235

1991 -92 10121

1992-93 10104

1993 - 94 9778

1994-95 10216

Source National Board of Revenue

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1821

18

Domination of Indirect Tax Over Direct Tax

Despite the progress for ensuring self-reliant development in a global climate of free

economy a major thrust of fiscal policy in Bangladesh has to be on raising the revenue-

GDP ratio Further there is an urgent need for shift in the composition of revenues away

from tax on international trade goods and services towards direct taxes on income and

profit whose share in total revenue in Bangladesh is appallingly low even compared to

other developing countries in Asia This can be seen from the following table

Position of Different Taxes in their share to total revenue () 1992

(Some Asian Examples)

Taxes On Income ampProfit

Taxes On Goodsamp Services

Taxes FromInternational Trade

Non-TaxRevenue

Singapore 270 228 22 335

Indonesia 580 263 51 78

Malaysia 342 200 149 269

Philippines 293 262 287 126

Thailand 275 416 167 99

Bangladesh 86 258 273 230

Bhutan 75 166 04 750

India 170 340 255 228

Myanmar 114 326 165 396

Nepal 99 367 308 171

Pakistan 100 322 302 272

Sri Lanka 112 478 276 98

Source IMF Government Finance Statistics Year Book (Various Issues)

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1921

19

Statistical figure of revenue collections under different heads of taxation and share of

each tax-revenue in total revenues is shown below (year 1994-95)

Heads of Taxation Total Amount(Crore Taka)

Percentage(Rounded Off)

Customs duties (Export import) 367694 34

VAT (Import) 221523 21

VAT (local production) 124834 12

Supplementary Duty (Luxury Items) 18761 15

Supplementary Duty (Luxury goods of local origin) 134412

Excise Duty 17782 2

Income Tax 149156 14

Other Taxes 18094 2

Total 1052256 100

Source National Board of Revenue

Exchange rate for different currencies vis-a-vis the US $ as on 31st March 1997 are

indicated in Appendix 1 (Pg 475)

This is depicted in the following pie diagram

It will be seen that major share of tax revenue is attributed to indirect taxes Out of the

indirect taxes share of import-based taxes was the highest Lack of progress in expanding

the base for direct taxes remains a major shortcoming of the tax reform agenda of

Bangladesh

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 2021

20

(f) Forecast of Tax-Revenue

The introduction of VAT in 1991 was a bold move It now covers manufacturing at the

wholesale and retail stage and some selected services Efforts are on to make VAT as

comprehensive as possible Though VAT is now recognised as an efficient and non-

distorting means of taxation by economists and policy makers alike its introduction in

many countries is held up due to political reasons Thus Bangladesh can take credit of

introduction of VAT within so short a period of time Due to computerization in progress

at NBR it is now possible to predict revenues and their composition with much more

precision than in the past

Tax revenues have recently shown unusual buoyancy and responsiveness to tax reforms

and rate adjustments Imports responded vigorously in 1994-95 to the sharp reductions in

tariffs yielding significantly higher revenues from import taxation with tariffs rates at an

all time low As most revenue targets except those of direct taxes were exceeded in

199495 it warranted upward revision of targets for the following year This optimistic

trend is expected to continue into the year 2000 with tax revenues posing a higher

trajectory than would have been the case without tax-reforms

Problems at the time of collecting tax

Lack o f information

Lack of equity

Lack of willingness of the taxpayers

High value added tax

Several imposition of taxes

Different

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 2121

CONCLUSION

Attaining an optimal tax system is a difficult and unenviable

task but nevertheless critical for revenue generation required

for accelerating growth and to improve the quality of life of thecitizens A long-term sustainable solution to enhance

transparency promote growth improve tax compliance and

thus to increase tax to GDP ratio is a much desirable issue in

the context of Bangladesh

To remove the distortions in the tax system and reduced the

base for tax Collection the treatment of tax exemption should

go to a desirable level

Agriculture is a largest sector in Bangladesh so for taxationneed to follow effective Agriculture Income Standard (AIS)

and need to expend in Agriculture sector

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 221

2

Submission Date 13th

April 2010

Farzana HudaLecturer

Faculty of business and economicsDaffodil International University

Dear Madam

Subject Letter of Transmittal

We are going to submit the report what we prepared on

Impact of Direct and Indirect tax of Bangladesh to you for further clarification The authority of this report is beingtransmitted to you as well Therefore we fervently hope that you would kindenough to let us inform the feedback regarding our report However if yourequire more information we will be very happy to provide that in future

Thank youSincerely yours

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 321

3

Executive summary

The term direct tax generally means a tax paid directly to the government by the persons

on whom it is imposed

A tax levied on goods or services rather than on persons or organizations is indirect tax

Income tax wealth tax is the direct tax and customs excise vat etc is the indirect tax

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 421

4

Introduction

Direct Tax

a tax paid directly by the person or organization on which it is leviedA tax demanded from the very persons who it is intended or desired should

pay it

The term direct tax generally means a tax paid directly to the government by the persons

on whom it is imposed

In the general sense a direct tax is one paid directly to the government by the persons(juristic or natural) on whom it is imposed (often accompanied by a tax return filed by thetaxpayer) Examples include some income taxes some corporate taxes and transfer taxessuch as estate (inheritance) tax and gift tax In this sense a direct tax is contrasted with anindirect tax or collected tax (such as sales tax or value added tax (VAT)) a collectedtax is one which is collected by intermediaries who turn over the proceeds to thegovernment and file the related tax return Some commentators have argued that a direct

tax is one that cannot be shifted by the taxpayer to someone else whereas an indirect taxcan be

The power of direct taxation applies to every individual as congress under thisgovernment is expressly vested with the authority of laying a capitation or poll-tax uponevery person to any amount This is a tax that however oppressive in its nature andunequal in its operation is certain as to its produce and simple in it collection it cannot be evaded like the objects of imposts or excise and will be paid because all that a manhath will he give for his head This tax is so congenial to the nature of despotism that it

has ever been a favorite under such governments Some of those who were in the lategeneral convention from this state have long labored to introduce a poll-tax among us

The power of direct taxation will further apply to every individual as congress may tax

land cattle trades occupations ampc to any amount and every object of internal taxation

is of that nature that however oppressive the people will have but this alternative either

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 521

5

Indirect Tax

a tax levied on goods or services rather than on persons or organizations

Tax - definition of tax - A fee charged (levied) by a government on a product on the price of a good or service then it is called an indirect tax

Charge levied by the State on consumption expenditure privilege or right but not on

income or property Customs duties levied on imports excise duties on production sales

tax or value added tax (VAT) at some stage in production-distribution process are

examples of indirect taxes because they are not levied directly on the income of the

consumer or earner Since they are less obvious than income tax (because they dont show

up on the wage slip) politicians are tempted to increase them to generate more state

revenue Also called consumption taxes they are regressive measures because they are

not based on the ability to pay principle

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 621

6

Type of Direct tax

Income Tax

The levy of Income tax is regulated by Income Tax Ordinance XXXVI of 1984 Finance

Act is published every year after passing of national budget in the Parliament It contains

the amendments to the income tax if any and prescribed tax rates Besides rulesorders

are issued by the National Board of Revenue from time to time Decisions are also

arrived at based on previous income tax cases Income Tax is calculated on salaries

interest on securities income of residential property income from business or profession

capital gains income from other sources profit of any mutual insurance association any

income that accrued arose or is received in Bangladesh

In the income tax law tax-payers are divided into two classes resident and non-

resident depending on the period of stay in Bangladesh The tax rate is relatively higher

for a non-resident The tax payers may be individual firm association of persons

undivided Hindu family local authority company etc Usually income tax-returns are to

be submitted by 15th September each year after the close of the financial year If the

income exceeds 200000 taka the return is to be accompanied with statement of assets

liabilities and expenses Income tax officer determines taxable income on the basis of the

following factors

Income tax returns submitted by the assessee and the facts gathered by the income taxofficer through accounts statements documents files or audit report of charteredaccountants relating to assessment

Income Tax Act

Income Tax Law

Discretion of the Deputy Commissioner of Tax

Since the year 1996-1997 income tax is determined in the following way

(a) In case of individual firm association of persons partnership firms

Level of Income Rate

(i) Income up to 60000 taka Nil

(ii) Income up to next 75000 taka or 120000 taka whichever is higher 15

(iii) Income up to next 160000 taka 20

(iv) The rest amount of income 25

(b) In case of company or local authority

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 721

7

All income except dividend income of the Company that is registered in Bangladesh istaxable The rate is as follows-

Category Rate

(i) Income of Publicly Traded Company 35

(ii) Income of non-Publicly Traded Company 40

(iii) Bank Insurance or Investment Companies nonresident Companies 45

The rate of income tax will be 15 on the amount representing income from dividends

declared and paid by a company formed and registered in Bangladesh under companies

Act 1913 or a body corporate formed in pursuance of an Act of Parliament in respect of

the share capital issued subscribed and paid after 14th August 1947

In the case of a person not being a Company (non-resident) the rate of income tax will be

25 of income

Wealth Tax

Wealth tax is regulated by the provisions of Wealth Tax Act 1963 (Act No XV)

Wealth is assessed as per the prevailing market price in respect of the wealth of Hindu

undivided family or individual

Value of Wealth Rate

(i) First 25000000 taka net wealth Nil

(ii) Next 50000000 taka net wealth 12

(iii) Next 50000000 taka net wealth 34

(iv) For the balance amount of Value 1

If any tax payer pays income and wealth taxes in any year wealth tax plus income tax

must not exceed 30 of income

The number of wealth tax payers stood at 18350 in 1994-1995 943 Gift Tax

Gift tax Act 1963 was repealed in 1985 but came into force again in 1990 As per the

quoted Act gift means any transfer of ownership of movable or immovable property by

one person to another willingly and without any profit Property is evaluated at thecurrent market price

The following rates are applicable now

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 821

8

Value of property Rate

(i) 5000000 taka beyond exempted limit 5

(ii) On next 10000000 taka value 10

(iii) On next 10000000 taka value 15

(iv) On the balance amount of value 20

Indirect Taxes

The following are the main indirect taxes

Customs

Wester defines customs as duties tolls or imposts imposed by sovereign laws of a

country on imports and exports This duty is imposed as per Bangladesh Customs Act

1969 and as per the Customs Tariff As per the Customs Act banned and illegal items aresold on auction and sale-proceeds are deposited into government treasury Smuggled gold

seized at airsea ports are deposited into Central Bank

In order to hasten customs clearance and thereby encourage investment in the country

government has introduced Per-shipment Inspection (PSI) Scheme under which approved

internationally reputed inspection firms issue certificate regarding quality quantity price

classification of the imported items On the basis of that certificate (known as Clean

Report on Finding) goods are cleared without delay at sea or air ports But Revenue

Audit authorities have detected cases of under-invoicing and wrong classification by the

PSI agencies which deprive the government of large revenues

Moreover bonded ware houses get special duty privileges for imports There are 2956

bonded warehouses (private and special) in the country There are also privileges for

import under baggage rules

Excise

Excise duty is imposed on some items that are produced within Bangladesh Being an

indirect tax it is paid by the manufacturer who can pass its incidence to consumers This

is guided by Excises and Salt Act 1944 and Statutory Rules amp Order of 1984 At present

excise duty is charged on bidi (local cigarette) 25 taka per thousand on cotton Tk

150 per kilogram and cotton cloth Tk 150 per metre Excise duty is also imposed onBanking services

VAT

Value Added Tax is imposed on production wholesaling and retailing when value is

added This was introduced in 1991 Maximum limit of VAT is 15 on import and

home-made goods and services The number of registered firmscompanies under VAT

net is 100000 (approx)

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 921

9

Supplementary Duty This is imposed on luxury items and services like cigarette cinema alcohol etc in

addition to VAT The rate varies from 5 to 350

Turnover Tax

Those organisations whose annual sale is less than Taka 150000000 are to pay

turnover tax

Bangladesh Tax Information

I n Bangladesh the principal direct taxes are personal income taxes and corporateincome taxes and a value-added tax (VAT) of 15 levied on all important consumer

goods The top income tax rate for individuals is 25 For the 200405 tax year (July 1

2004 ndash June 30 2005) the top corporate rate was 45 However publicly tradedcompanies registered in Bangladesh are charged a lower rate of 30 Banks financial

institutions and insurance companies are charged the 45 rate All other companies are

taxed at the 375 rate Effective 1 July 2002 the VAT rate on computer hardware and

software was reduced to 75 and certain agricultural equipment and electricity supplied to the agricultural sector was exempted from VAT altogether VAT on the

transfer of land is also to be abolished Essential agricultural implements and irrigation pumps had previously been excluded from certain taxes

Corporate tax Corporate tax rates for industrial companies whose shares are publicly traded is 35 andthe rate of those whose shares are not publicly traded is 40

Tax rates on other companies Tax rates on income of all other companies including banks financial institutionsinsurance companies and local authorities is 45

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1021

10

Investment requirement by companies enjoying tax holiday Companies enjoying tax

holidays are required to invest only 25 to 30 of their income in other activities as perrule of NBR

Accepted of returns of public limited companies Returns filed by the public limited companies shall be accepted as correct if it isaccompanied by audited accounts and certified by a chartered accountant as to thecorrectness of the total income of the assessee

Salary of foreign technicians Salary income received by or due to a foreign technician under contract of serviceapproved by the National Board of Revenue is fully exempted from paying tax (subject to prescribed conditions and limitations) for a period of three years from the date of hisarrival in Bangladesh

Tax payable by employer on remuneration of foreign technician Expenditure incurred by an employer in respect of remuneration of a foreign technician isalso fully exempted from income tax (subject to the stipulated conditions)

the price of a good or service then it is called an indirect tax

Remuneration of foreign technicians employed by the firms of consultancy and

engineers

Expenditure incurred as remuneration payable to a foreign technicians by a Bangladeshifirm carrying on the business of consultant and engineers in Bangladesh is fullyexempted from tax (subject to prescribed conditions and limitations

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1121

11

Amount of TaxIf an individual has been in Bangladesh for a periodperiod totaling 182 days or more in

the income year heshe is considered a resident In case an individual has been in the

country for 90 days in the income year and 365 days in four years preceding this yearheshe will also be considered a resident

Each individual is entitled to an investment tax credit of 15 percent of the total income or

Tk 100000 whichever is less Incomes from small and cottage industries are entitled to a

5 to 10 per cent tax rebate depending on the production volume

On the first Tk 6000000 of total income - no tax obligation

On the next Tk 4000000 of total income - 10

On the next Tk 5000000 of total income - 15

On the next Tk 15000000 of total income - 20

On the balance of total income - 25

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1221

12

Effect of direct tax

The total effect on households of such taxes is assessed using input-output analysis Thus

both the direct effect of taxes through increased fuel prices and the indirect effect

through increased prices of other goods can be assessed simultaneously This input-

output approach allows the generation of direct plus indirect pollution intensities for all

household consumption categories for in principle a number of pollutants (CO2 SO2

NOx particulates) These intensities could then be used to assess the impact on

households of pollution taxes This paper concentrates on CO2 and energy performing a

static analysis of the effect of a tax on the carbon or energy content of goods using the

known consumption patterns for the various countries both in aggregate and for different

income groups This allows a first assessment of the regressiveprogressive effects of

such taxes and an indication of consumer welfare loss

The legal definition and the economic definition of taxes differ in that economists do not

consider many transfers to governments to be taxes For example some transfers to the

public sector are comparable to prices Examples include tuition at public universities and

fees for utilities provided by local governments Governments also obtain resources by

creating money (eg printing bills and minting coins) through voluntary gifts (eg

contributions to public universities and museums)by imposing penalties (eg trafficfines) by borrowing and by confiscating wealth From the view of economists a tax is a

non-penal yet compulsory transfer of resources from the private to the public sector

levied on a basis of predetermined criteria and without reference to specific benefit

received

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1321

13

Purposes and ef fects

Funds provided by taxation have been used by states and their functional equivalents

throughout history to carry out many functions Some of these include expenditures on

war the enforcement of law and public order protection of property economic

infrastructure (roads legal tender enforcement of contracts etc) public works social

engineering and the operation of government itself Governments also use taxes to fund

welfare and public services These services can include education systems health care

systems pensions for the elderly unemployment benefits and public transportation

Energy water and waste management systems are also common public utilities Colonial

and modernizing states have also used cash taxes to draw or force reluctant subsistence

producers into cash economies

Governments use different kinds of taxes and vary the tax rates This is done to distribute

the tax burden among individuals or classes of the population involved in taxable

activities such as business or to redistribute resources between individuals or classes in

the population Historically the nobility were supported by taxes on the poor modern

social security systems are intended to support the poor the disabled or the retired by

taxes on those who are still working In addition taxes are applied to fund foreign and

military aid to influence the macroeconomic performance of the economy (the

governments strategy for doing this is called its fiscal policy - see also tax exemption) or

to modify patterns of consumption or employment within an economy by making some

classes of transaction more or less attractive

A nations tax system is often a reflection of its communal values or the values of those in

power To create a system of taxation a nation must make choices regarding the

distribution of the tax burden mdash who will pay taxes and how much they will pay mdash and

how the taxes collected will be spent In democratic nations where the public elects those

in charge of establishing the tax system these choices reflect the type of community that

the public wishes to create In countries where the public does not have a significant

amount of influence over the system of taxation that system may be more of a reflection

on the values of those in power

The resource collected from the public through taxation is always greater than the amount

which can be used by the government The difference is called compliance cost and

includes for example the labour cost and other expenses incurred in complying with tax

laws and rules The collection of a tax in order to spend it on a specified purpose for

example collecting a tax on alcohol to pay directly for alcoholism rehabilitation centres

is called hypothecation This practice is often disliked by finance ministers since it

reduces their freedom of action Some economic theorists consider the concept to be

intellectually dishonest since (in reality) money is fungible

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1421

14

Effects of income taxation on division of labor

If a tax is paid on outsourced services that is not also charged on services performed foroneself then it may be cheaper to perform the services oneself than to pay someone

else mdash even considering losses in economic efficiency [37][38]

For example suppose jobs A and B are both valued at $1 on the market And suppose

that because of your unique abilities you can do job A twice over (100 extra output) in

the same effort as it would take you to do job B But job B is the one that you need done

right now Under perfect division of labor you would do job A and somebody else would

do job B Your unique abilities would always be rewarded

Income taxation has the worst effect on division of labor in the form of barter Suppose

that the person doing job B is actually interested in having job A done for him Now

suppose you could amazingly do job A four times over selling half your work on themarket for cash just to pay your tax bill The other half of the work you do for somebody

who does job B twice over but he has to sell off half to pay his tax bill Youre left with

one unit of job B but only if you were 400 as productive doing job A In this case of

50 tax on barter income anything less than 400 productivity will cause the division

of labor to fail

In summary depending on the situation a 50 tax rate can cause the division of labor to

fail even where productivity gains of up to 300 would have resulted Even a mere 30

tax rate can negate the advantage of a 100 productivity gain

Direct versus Indirect Taxation

o Direct taxes ndash are paid directly to the Exchequer by the individualtaxpayer ndash usually through ldquopay as you earnrdquo The same is true ofcorporation tax Tax liability cannot be passed onto someone else

o Indirect taxes ndash include VAT and a range of excise duties on oiltobacco alcohol The burden of an indirect tax can be passed on by thesupplier to the final consumer ndash depending on the price elasticity ofdemand and supply for the product

In the last twenty years there has been a shift towards indirect taxation ndash economists differ in their views about what is the optimum mix of taxationbetween indirect and direct taxes

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1521

15

Arguments For Using Indirect Taxation Arguments Against Using Indirect Taxation

Changes in indirect taxes are moreeffective in changing the overall pattern ofdemand for particular goods and servicesie in changing relative prices and therebyaffecting consumer demand (eg anincrease in the real duty on petrol)

Many indirect taxes make the distributionof income more unequal (less equitable)because indirect taxes are more regressive than direct taxes

They are a useful instrument in controllingand correcting for externalities ndash allgovernments have moved towards a morefrequent use of indirect taxes as a means ofmaking the polluter pay and ldquointernalizingthe external costsrdquo of production andconsumption

Higher indirect taxes can cause cost-pushinflation which can lead to a rise ininflation expectations

Indirect taxes are less likely to distort thechoices that people have to betweenwork and leisure and therefore have less ofa negative effect on work incentives

Higher indirect taxes allow a reduction indirect tax rates (eg lower starting rates ofincome tax)

There is no hard evidence that cuttingdirect tax rates has much of an incentiveeffect on peoplersquos decisions about whetheror not to work If indirect taxes are too high

ndash this creates an incentive to avoid taxesthrough ldquoboot-leggingrdquo ndash a good example ofthis would be attempts to evade the highlevels of duty on cigarettes

Indirect taxes can be changed more easilythan direct taxes ndash this gives economicpolicy-makers more flexibility when settingfiscal policy Direct taxes can only bechanged once a year at Budget time

Revenue from indirect taxes can beuncertain particularly when inflation is lowor there is a recession causing a fall inconsume spending

Indirect taxes are less easy to avoid by thefinal tax-payer who might be unaware ofhow much indirect tax they are paying

There is a potential loss of economicwelfare (taxes can create a deadweightloss of consumer and producers surplus)

Indirect taxes provide an incentive to save (and thereby avoid the tax)- a higher levelof savings might be used by the economy tofinance a higher level of capital investment

Higher indirect taxes affect households onlower incomes who are least able to save inthe first place

Indirect taxes leave people free to make achoice whereas direct taxes leave peoplewith less of their gross income in theirpockets

Many people are unaware of how much theyare paying in indirect taxes ndash this goesagainst one of the basic principles of a goodtax system ndash namely that taxes should betransparent

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1621

16

NBR Tax Revenue

In FY 2006-07 2007-08 and 2008-09 the growth of NBR Tax Revenue receipts stood at95 275 and 107 respectively

In FY 2009-10 the target for NBR Tax Revenue is TK 61000 cr (89 of GDP)whichis 119 higher than previous yearrsquos original estimate

During July-September quarter of the current fiscal year TK12 408 cr has beencollected which is 91 higher than previous years collection

In the current quarter growth of Import Duty and Value Added Tax (VAT) at import

levelhas declined by 23 and 87 respectively At the same time VAT at local levelSupplementary Duty at import level and Income Tax showed positive growth of 168203 and 259 respectively (Table 3)

ObservationsTaxGDP ratio (around 85) in Bangladesh is the lowest among the countries of Asian

region It is 4-percentage point lower than the regional average of 125 The ratio needto be increased to reduce our dependence on foreign aid as well as lessen the burden of loanon the future generation and to enhance the absorptive capacity of loan

Owing to increased import of high priced commodities like vehicles the 1st Quarter

Supplementary Duties at import level recorded growth of 203 This rate may declinetowards the end of the year

Achieving budget revenue target may be difficult

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1721

17

Actual Realisation of tax revenue vis-a-vis target

Financial Year Realisation of Target

1980-81 10179

1981 -82 9915

1982-83 9878

1983 -84 9748

1984-85 10292

1985-86 10197

1986-87 10101

1987-88 10101

1988-89 9854

1989-90 9887

1990-91 10235

1991 -92 10121

1992-93 10104

1993 - 94 9778

1994-95 10216

Source National Board of Revenue

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1821

18

Domination of Indirect Tax Over Direct Tax

Despite the progress for ensuring self-reliant development in a global climate of free

economy a major thrust of fiscal policy in Bangladesh has to be on raising the revenue-

GDP ratio Further there is an urgent need for shift in the composition of revenues away

from tax on international trade goods and services towards direct taxes on income and

profit whose share in total revenue in Bangladesh is appallingly low even compared to

other developing countries in Asia This can be seen from the following table

Position of Different Taxes in their share to total revenue () 1992

(Some Asian Examples)

Taxes On Income ampProfit

Taxes On Goodsamp Services

Taxes FromInternational Trade

Non-TaxRevenue

Singapore 270 228 22 335

Indonesia 580 263 51 78

Malaysia 342 200 149 269

Philippines 293 262 287 126

Thailand 275 416 167 99

Bangladesh 86 258 273 230

Bhutan 75 166 04 750

India 170 340 255 228

Myanmar 114 326 165 396

Nepal 99 367 308 171

Pakistan 100 322 302 272

Sri Lanka 112 478 276 98

Source IMF Government Finance Statistics Year Book (Various Issues)

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1921

19

Statistical figure of revenue collections under different heads of taxation and share of

each tax-revenue in total revenues is shown below (year 1994-95)

Heads of Taxation Total Amount(Crore Taka)

Percentage(Rounded Off)

Customs duties (Export import) 367694 34

VAT (Import) 221523 21

VAT (local production) 124834 12

Supplementary Duty (Luxury Items) 18761 15

Supplementary Duty (Luxury goods of local origin) 134412

Excise Duty 17782 2

Income Tax 149156 14

Other Taxes 18094 2

Total 1052256 100

Source National Board of Revenue

Exchange rate for different currencies vis-a-vis the US $ as on 31st March 1997 are

indicated in Appendix 1 (Pg 475)

This is depicted in the following pie diagram

It will be seen that major share of tax revenue is attributed to indirect taxes Out of the

indirect taxes share of import-based taxes was the highest Lack of progress in expanding

the base for direct taxes remains a major shortcoming of the tax reform agenda of

Bangladesh

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 2021

20

(f) Forecast of Tax-Revenue

The introduction of VAT in 1991 was a bold move It now covers manufacturing at the

wholesale and retail stage and some selected services Efforts are on to make VAT as

comprehensive as possible Though VAT is now recognised as an efficient and non-

distorting means of taxation by economists and policy makers alike its introduction in

many countries is held up due to political reasons Thus Bangladesh can take credit of

introduction of VAT within so short a period of time Due to computerization in progress

at NBR it is now possible to predict revenues and their composition with much more

precision than in the past

Tax revenues have recently shown unusual buoyancy and responsiveness to tax reforms

and rate adjustments Imports responded vigorously in 1994-95 to the sharp reductions in

tariffs yielding significantly higher revenues from import taxation with tariffs rates at an

all time low As most revenue targets except those of direct taxes were exceeded in

199495 it warranted upward revision of targets for the following year This optimistic

trend is expected to continue into the year 2000 with tax revenues posing a higher

trajectory than would have been the case without tax-reforms

Problems at the time of collecting tax

Lack o f information

Lack of equity

Lack of willingness of the taxpayers

High value added tax

Several imposition of taxes

Different

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 2121

CONCLUSION

Attaining an optimal tax system is a difficult and unenviable

task but nevertheless critical for revenue generation required

for accelerating growth and to improve the quality of life of thecitizens A long-term sustainable solution to enhance

transparency promote growth improve tax compliance and

thus to increase tax to GDP ratio is a much desirable issue in

the context of Bangladesh

To remove the distortions in the tax system and reduced the

base for tax Collection the treatment of tax exemption should

go to a desirable level

Agriculture is a largest sector in Bangladesh so for taxationneed to follow effective Agriculture Income Standard (AIS)

and need to expend in Agriculture sector

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 321

3

Executive summary

The term direct tax generally means a tax paid directly to the government by the persons

on whom it is imposed

A tax levied on goods or services rather than on persons or organizations is indirect tax

Income tax wealth tax is the direct tax and customs excise vat etc is the indirect tax

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 421

4

Introduction

Direct Tax

a tax paid directly by the person or organization on which it is leviedA tax demanded from the very persons who it is intended or desired should

pay it

The term direct tax generally means a tax paid directly to the government by the persons

on whom it is imposed

In the general sense a direct tax is one paid directly to the government by the persons(juristic or natural) on whom it is imposed (often accompanied by a tax return filed by thetaxpayer) Examples include some income taxes some corporate taxes and transfer taxessuch as estate (inheritance) tax and gift tax In this sense a direct tax is contrasted with anindirect tax or collected tax (such as sales tax or value added tax (VAT)) a collectedtax is one which is collected by intermediaries who turn over the proceeds to thegovernment and file the related tax return Some commentators have argued that a direct

tax is one that cannot be shifted by the taxpayer to someone else whereas an indirect taxcan be

The power of direct taxation applies to every individual as congress under thisgovernment is expressly vested with the authority of laying a capitation or poll-tax uponevery person to any amount This is a tax that however oppressive in its nature andunequal in its operation is certain as to its produce and simple in it collection it cannot be evaded like the objects of imposts or excise and will be paid because all that a manhath will he give for his head This tax is so congenial to the nature of despotism that it

has ever been a favorite under such governments Some of those who were in the lategeneral convention from this state have long labored to introduce a poll-tax among us

The power of direct taxation will further apply to every individual as congress may tax

land cattle trades occupations ampc to any amount and every object of internal taxation

is of that nature that however oppressive the people will have but this alternative either

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 521

5

Indirect Tax

a tax levied on goods or services rather than on persons or organizations

Tax - definition of tax - A fee charged (levied) by a government on a product on the price of a good or service then it is called an indirect tax

Charge levied by the State on consumption expenditure privilege or right but not on

income or property Customs duties levied on imports excise duties on production sales

tax or value added tax (VAT) at some stage in production-distribution process are

examples of indirect taxes because they are not levied directly on the income of the

consumer or earner Since they are less obvious than income tax (because they dont show

up on the wage slip) politicians are tempted to increase them to generate more state

revenue Also called consumption taxes they are regressive measures because they are

not based on the ability to pay principle

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 621

6

Type of Direct tax

Income Tax

The levy of Income tax is regulated by Income Tax Ordinance XXXVI of 1984 Finance

Act is published every year after passing of national budget in the Parliament It contains

the amendments to the income tax if any and prescribed tax rates Besides rulesorders

are issued by the National Board of Revenue from time to time Decisions are also

arrived at based on previous income tax cases Income Tax is calculated on salaries

interest on securities income of residential property income from business or profession

capital gains income from other sources profit of any mutual insurance association any

income that accrued arose or is received in Bangladesh

In the income tax law tax-payers are divided into two classes resident and non-

resident depending on the period of stay in Bangladesh The tax rate is relatively higher

for a non-resident The tax payers may be individual firm association of persons

undivided Hindu family local authority company etc Usually income tax-returns are to

be submitted by 15th September each year after the close of the financial year If the

income exceeds 200000 taka the return is to be accompanied with statement of assets

liabilities and expenses Income tax officer determines taxable income on the basis of the

following factors

Income tax returns submitted by the assessee and the facts gathered by the income taxofficer through accounts statements documents files or audit report of charteredaccountants relating to assessment

Income Tax Act

Income Tax Law

Discretion of the Deputy Commissioner of Tax

Since the year 1996-1997 income tax is determined in the following way

(a) In case of individual firm association of persons partnership firms

Level of Income Rate

(i) Income up to 60000 taka Nil

(ii) Income up to next 75000 taka or 120000 taka whichever is higher 15

(iii) Income up to next 160000 taka 20

(iv) The rest amount of income 25

(b) In case of company or local authority

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 721

7

All income except dividend income of the Company that is registered in Bangladesh istaxable The rate is as follows-

Category Rate

(i) Income of Publicly Traded Company 35

(ii) Income of non-Publicly Traded Company 40

(iii) Bank Insurance or Investment Companies nonresident Companies 45

The rate of income tax will be 15 on the amount representing income from dividends

declared and paid by a company formed and registered in Bangladesh under companies

Act 1913 or a body corporate formed in pursuance of an Act of Parliament in respect of

the share capital issued subscribed and paid after 14th August 1947

In the case of a person not being a Company (non-resident) the rate of income tax will be

25 of income

Wealth Tax

Wealth tax is regulated by the provisions of Wealth Tax Act 1963 (Act No XV)

Wealth is assessed as per the prevailing market price in respect of the wealth of Hindu

undivided family or individual

Value of Wealth Rate

(i) First 25000000 taka net wealth Nil

(ii) Next 50000000 taka net wealth 12

(iii) Next 50000000 taka net wealth 34

(iv) For the balance amount of Value 1

If any tax payer pays income and wealth taxes in any year wealth tax plus income tax

must not exceed 30 of income

The number of wealth tax payers stood at 18350 in 1994-1995 943 Gift Tax

Gift tax Act 1963 was repealed in 1985 but came into force again in 1990 As per the

quoted Act gift means any transfer of ownership of movable or immovable property by

one person to another willingly and without any profit Property is evaluated at thecurrent market price

The following rates are applicable now

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 821

8

Value of property Rate

(i) 5000000 taka beyond exempted limit 5

(ii) On next 10000000 taka value 10

(iii) On next 10000000 taka value 15

(iv) On the balance amount of value 20

Indirect Taxes

The following are the main indirect taxes

Customs

Wester defines customs as duties tolls or imposts imposed by sovereign laws of a

country on imports and exports This duty is imposed as per Bangladesh Customs Act

1969 and as per the Customs Tariff As per the Customs Act banned and illegal items aresold on auction and sale-proceeds are deposited into government treasury Smuggled gold

seized at airsea ports are deposited into Central Bank

In order to hasten customs clearance and thereby encourage investment in the country

government has introduced Per-shipment Inspection (PSI) Scheme under which approved

internationally reputed inspection firms issue certificate regarding quality quantity price

classification of the imported items On the basis of that certificate (known as Clean

Report on Finding) goods are cleared without delay at sea or air ports But Revenue

Audit authorities have detected cases of under-invoicing and wrong classification by the

PSI agencies which deprive the government of large revenues

Moreover bonded ware houses get special duty privileges for imports There are 2956

bonded warehouses (private and special) in the country There are also privileges for

import under baggage rules

Excise

Excise duty is imposed on some items that are produced within Bangladesh Being an

indirect tax it is paid by the manufacturer who can pass its incidence to consumers This

is guided by Excises and Salt Act 1944 and Statutory Rules amp Order of 1984 At present

excise duty is charged on bidi (local cigarette) 25 taka per thousand on cotton Tk

150 per kilogram and cotton cloth Tk 150 per metre Excise duty is also imposed onBanking services

VAT

Value Added Tax is imposed on production wholesaling and retailing when value is

added This was introduced in 1991 Maximum limit of VAT is 15 on import and

home-made goods and services The number of registered firmscompanies under VAT

net is 100000 (approx)

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 921

9

Supplementary Duty This is imposed on luxury items and services like cigarette cinema alcohol etc in

addition to VAT The rate varies from 5 to 350

Turnover Tax

Those organisations whose annual sale is less than Taka 150000000 are to pay

turnover tax

Bangladesh Tax Information

I n Bangladesh the principal direct taxes are personal income taxes and corporateincome taxes and a value-added tax (VAT) of 15 levied on all important consumer

goods The top income tax rate for individuals is 25 For the 200405 tax year (July 1

2004 ndash June 30 2005) the top corporate rate was 45 However publicly tradedcompanies registered in Bangladesh are charged a lower rate of 30 Banks financial

institutions and insurance companies are charged the 45 rate All other companies are

taxed at the 375 rate Effective 1 July 2002 the VAT rate on computer hardware and

software was reduced to 75 and certain agricultural equipment and electricity supplied to the agricultural sector was exempted from VAT altogether VAT on the

transfer of land is also to be abolished Essential agricultural implements and irrigation pumps had previously been excluded from certain taxes

Corporate tax Corporate tax rates for industrial companies whose shares are publicly traded is 35 andthe rate of those whose shares are not publicly traded is 40

Tax rates on other companies Tax rates on income of all other companies including banks financial institutionsinsurance companies and local authorities is 45

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1021

10

Investment requirement by companies enjoying tax holiday Companies enjoying tax

holidays are required to invest only 25 to 30 of their income in other activities as perrule of NBR

Accepted of returns of public limited companies Returns filed by the public limited companies shall be accepted as correct if it isaccompanied by audited accounts and certified by a chartered accountant as to thecorrectness of the total income of the assessee

Salary of foreign technicians Salary income received by or due to a foreign technician under contract of serviceapproved by the National Board of Revenue is fully exempted from paying tax (subject to prescribed conditions and limitations) for a period of three years from the date of hisarrival in Bangladesh

Tax payable by employer on remuneration of foreign technician Expenditure incurred by an employer in respect of remuneration of a foreign technician isalso fully exempted from income tax (subject to the stipulated conditions)

the price of a good or service then it is called an indirect tax

Remuneration of foreign technicians employed by the firms of consultancy and

engineers

Expenditure incurred as remuneration payable to a foreign technicians by a Bangladeshifirm carrying on the business of consultant and engineers in Bangladesh is fullyexempted from tax (subject to prescribed conditions and limitations

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1121

11

Amount of TaxIf an individual has been in Bangladesh for a periodperiod totaling 182 days or more in

the income year heshe is considered a resident In case an individual has been in the

country for 90 days in the income year and 365 days in four years preceding this yearheshe will also be considered a resident

Each individual is entitled to an investment tax credit of 15 percent of the total income or

Tk 100000 whichever is less Incomes from small and cottage industries are entitled to a

5 to 10 per cent tax rebate depending on the production volume

On the first Tk 6000000 of total income - no tax obligation

On the next Tk 4000000 of total income - 10

On the next Tk 5000000 of total income - 15

On the next Tk 15000000 of total income - 20

On the balance of total income - 25

8132019 Squre Pharmaceuticals

httpslidepdfcomreaderfullsqure-pharmaceuticals 1221

12

Effect of direct tax

The total effect on households of such taxes is assessed using input-output analysis Thus

both the direct effect of taxes through increased fuel prices and the indirect effect