standard costing · pdf file · 2014-10-162014-10-16 · variance...

TRANSCRIPT

STANDARD COSTING

Samir K Mahajan

Standard Costing

Historical costs: Historical costing or actual costing is a system where costs are ascertained after they are incurred. Itis a post-mortem of the costs. When production is completed, i.e., products reached their final stage of finished status,costs are available and on that basis costs are ascertained. Historical costing does not help in finding mistakes andinefficiencies, which all lead to variation in profit.

o Standard costs: Due to these disadvantages and limitations of historical costing, the standard costing technique wasintroduced. A standard cost is a predetermined/estimated calculation of how much costs should be under specificworking conditions. It is a technique of cost control. Actual costs are compared with these standard costs. The objectof standard cost is to ascertain the quotation and determination of price policy. The other names for standard costsare, budgeted costs, projected costs, model costs, measured costs, specification costs etc.

STANDARD COSTING PROCEDURE

According to Wheldon "Standard costing is a method of ascertaining the costs whereby statistics are prepared to show (a)the standard cost (b) the actual cost (c) the difference between these costs, which is termed the variance". Thus thetechnique of standard cost study comprises of

Ascertainment and use of standard costs.

o Comparison of actual costs with standard costs (or budgeted cost) and measuring the variances.o Controlling costs by the variance analysis.o Reporting to management for taking proper action to maximize the efficiency

Standard cost forms a basis for future planning, preparation of tenders, fixation of price etc. Otherwise, or in the absenceof standard cost, decision will be based on actual cost.

VARIANCE ANALYSIS

In cost accounting, variance means deviation of the actual cost from the standard cost or budgeted cost. In standardcosting, standard costs are predetermined and refer to the amounts which ought to be incurred. These become theyardsticks against which actual costs can be compared.

Computation and analysis of variances is the main objective of standard costing. After the standard costs have been fixed,the next stage in the operation of standard costing is to ascertain the actual cost of each element and compare them withthe standard already set. It, thus, involves the measurement of the deviation of actual performance from the intendedperformance.The deviation of actual from the standard is called 'variance'.

Profitability of a business depends both on costs and sales. The variance may classified into two categories: costvariances and sales variances.

The difference between the actual cost (what is the cost ) and the standard cost (what should be the cost ) is known asthe 'cost variance'.

The sales variance is budgeted sales (or what should have ben the sales ) and actual sales (what have been the sales)

FAVOURABLE AND UNFAVOURABLE VARIANCES

Variances may be favourable (positive or credit) or unfavourable (negative or adverse or debit) depending upon whetherthe actual resulting cost is less or more than the standard cost.

Favourable Variance: When the actual cost incurred is less than the standard cost, the deviation is known as favourablevariance. The effect of favourable variance increases the profit. It is also known as positive or credit variance and viewedonly as savings.

Unfavourable Variance: When the actual cost incurred is more than the standard cost, there is a variance, known asunfavourable or adverse variance. Unfavourable variance refers to deviation to the loss of the business. It is also known asnegative or debit variance and viewed as additional costs or losses.

This favourable variance is a sign o r efficiency of the organization and the unfavourable variance is a sign of inefficiencyof the organisation.

CONTROLLABLE AND UNCONTROLLABLE VARIANCES

Variances may be controllable or uncontrollable, depending upon the controllability of the factors causing variances.

Controllable Variance: A variance is said to be controllable if a deviation caused by such factors which could be influencedby the executive action. For example excess usage of materials, excess time taken by a worker etc. is example forcontrollable variance. When compared to the standard cost it becomes controllable because the responsibility can befixed on the in-charge or foreman of the department.

Uncontrollable Variance: When variance is due to the factors beyond the control of the concerned person (ordepartment), it is said to be uncontrollable. Cost variance is due to outside factors, for example, the wage rate increasedon account of strike, Government restrictions, change in market price etc. No person or department can be heldresponsible for uncontrollable variances. Here revision of standards is required to remove such variances in future.

COMPUTATION OF COST VARIANCE VARIANCES

Variances can be found out with respect to all the elements of cost, i.e. direct material, direct labour and overheads. Inother words, the total cost variance is split into its component parts on the basis of elements, and each element isfurther subdivided to locate the responsibility of variance.

The cost variances can be studied in the following manner.A) Direct Material Cost VariancesB) Direct Labour Cost or wage VariancesC) Overhead Variances (i) Variable and (ii) Fixed

Direct expenses constitute an insignificant portion of total cost of the product. Hence direct expenses is generally notcalculated.

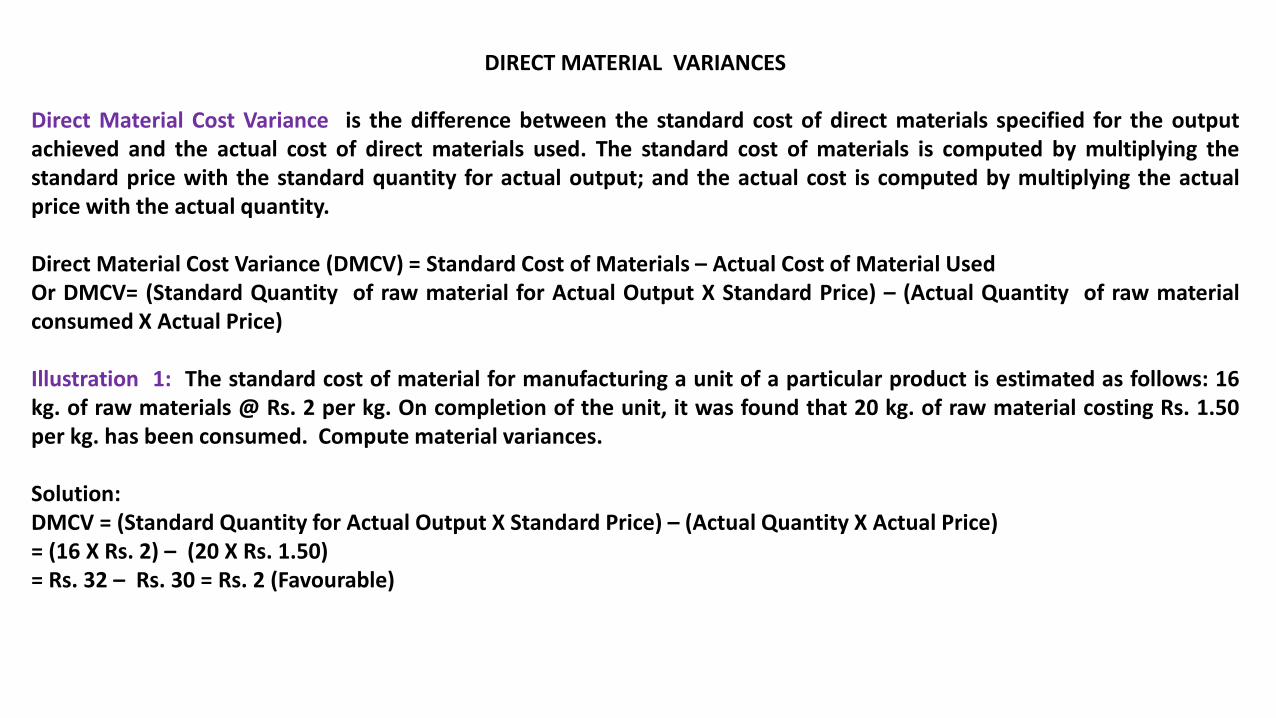

DIRECT MATERIAL VARIANCES

Direct Material Cost Variance is the difference between the standard cost of direct materials specified for the outputachieved and the actual cost of direct materials used. The standard cost of materials is computed by multiplying thestandard price with the standard quantity for actual output; and the actual cost is computed by multiplying the actualprice with the actual quantity.

Direct Material Cost Variance (DMCV) = Standard Cost of Materials – Actual Cost of Material UsedOr DMCV= (Standard Quantity of raw material for Actual Output X Standard Price) – (Actual Quantity of raw materialconsumed X Actual Price)

Illustration 1: The standard cost of material for manufacturing a unit of a particular product is estimated as follows: 16kg. of raw materials @ Rs. 2 per kg. On completion of the unit, it was found that 20 kg. of raw material costing Rs. 1.50per kg. has been consumed. Compute material variances.

Solution:DMCV = (Standard Quantity for Actual Output X Standard Price) – (Actual Quantity X Actual Price)= (16 X Rs. 2) – (20 X Rs. 1.50)= Rs. 32 – Rs. 30 = Rs. 2 (Favourable)

DIRECT MATERIAL VARIANCES contd.

Direct Material Cost Variance may

o Direct Material Price Varianceo Direct Material Usage (Quantity) Variance

Direct Material Price Variance: Material price variance is that portion of the direct material cost variance which is thedifference between the standard price specified and the actual price paid for the direct materials used. The formula is:

Material Price Variance (DMPV) = (Actual quantity consumed X Standard Price) - (Actual quantity consumed X Actual Price)

Or MPV = Actual quantity consumed X(Standard Rate - Actual Rate)

Reasons for price variance may be due to:o Buying efficiency or inefficiencyo High or low costs of transportation and carriage goodso Changes in or laxity in perusing purchase policy for instance purchase of superior or inferior materials etc.o Fraud in purchase or loss of discountso Incorrect setting of standards

DIRECT MATERIAL VARIANCES contd.

Illustration 2: The standard cost of material for manufacturing a unit of a particular product is estimated as follo ws: 20 kgof raw materials @ Rs. 2 per kg. On completion of the unit, it was found that 25 kg. of raw material costingRs. 3 per kg. has been consumed.Solution:DMPV = Actual quantity consumed (Standard Rate - Actual Rate)= 25 (Rs. 2 - Rs. 3) = Rs. 25 (Adverse)

DIRECT MATERIAL VARIANCES contd.

Direct Material Usage ( or Quantity) Variance: It is the deviation caused by the standards due to the difference inquantity used. It is calculated by multiplying the difference between the standard quantity specified and the actualquantity used by the standard price.

Direct Material Usage Variance (DMUV) = Standard Rate (Standard Quantity to be consumed - Actual Quantityconsumed)

Reasons for direct material usage variances:

o Inefficiency, lack of skill or faulty workmanship resulting in more consumption of raw materialso Lack of proper maintenance of plant and equipment and frequent break down during production process leading to

wastage of materialso Non-consideration of product design and method of processing etc while fixing standardso Incorrect using processing of materials resulting in wastageso Improper inspection of and supervision of workmen resulting in careless handling and processingo Too strict supervisions or inspection resulting excessive rejection of materials

DIRECT MATERIAL VARIANCES contd.

Illustration3: From the following data, you are required to material usage variance.Standard - 20 kg. at Rs. 5.50 per kg.Actual - 25 kg. at Rs. 6 per kg.

Solution:

MUV = Standard Rate (Standard Quantity - Actual Quantity)= Rs. 5.50 (20 -25) = Rs. 27.50 (Adverse)

DIRECT MATERIAL VARIANCES contd.

Illustration 4 : It is estimated that a product requires 50 units of material at the rate of Rs. 3 perunit. The actual consumption of material for manufacturing the same product came to 60 units atthe rate of Rs. 2.9 per unit. Calculate

1. Material cost variance2. Material price variance3. Material usage variance

Solution:1. Material cost variance = Std cost – Actual costStd cost = Std qty x Std price per unit = 50 x 3 = 150Actual cost = Actual qty x Actual price per unit = 60 x 2.90 =174

Material Cost Variance = 150 – 174 = 24 (unfavourable)

2. Material Price Variance = Actual qty x (Std price – actual price)60 x (3 – 2.90) = 6 favourable

3. Material usage variance = Std price x (Std qty – Actual qty)3x (50 -60 ) = Rs. 30 unfavourable

DIRECT LABOUR VARIANCE OR DIRECT WAGE VARIANCE

DIRECT LABOUR COST VARIANCE OR LABOUR WAGE VARIANCE (LCV OR LWV) represents the difference between thestandard labour cost and the actual labour costs for actual output. That is, it is the difference between standard direct wagesspecified for the activity achieved and the actual direct wages paid. Labour costs may be considered wages including pay,allowances and other expenses on labour. If the standard cost is higher, the variation is favourable and vice versa. Thisvariance can be calculated with the help of the following formulae:

Direct Labour Cost Variance (DLCV) = Standard Cost of Labour - Actual Cost of LabourDLCV = (Standard Hour X Standard Rate) - (Actual Hour X Actual Rate)

Direct labour cost variance arises on account variance in either rates of wags or time. It may further analysed as i. ratevariance and ii. Time or efficiency variance. Thus Direct labour cost variance may be further subdivided into Direct Labour Rate Variance (DLRV) Direct labour Efficiency Variance (DLEV).

DIRECT LABOUR VARIANCE OR DIRECT WAGE VARIANCE

Direct Labour (or Wage) Rate Variance (L or WRV): This variance is the direct result of the wages paid at a rate different fromthe standard rate. That is, it is the difference between the standard rate of pay specified and the actual rate paid. If thestandard rate is higher then the variance is favourable and vice versa.

Direct Labour Rate Variance = Actual Hour X (Standard Rate – Actual Rate)

Reasons for direct labour rate variance:o Deployment of more efficient and skilled workers giving rise to higher paymento Higher payment due to shortage of availability of labouro Lesser payment due to abundant availability of labour or high consumption among them for employmento Employment of unskilled labourers causing lower actual rates of payo Extra shift allowance to workers or overtime allowances leading to high wageso Changes in wage rate higher wage rates during seasonal or emergency operations

DIRECT LABOUR VARIANCE OR Direct WAGE VARIANCE contd.

Direct Labour Efficiency Variance (DLEV): Direct Labour Efficiency Variance (DLEV): 'the difference between the standardhours specified for the actual production achieved and the hours actually worked, valued at the standard labour rate.' Whenthe workers finish the specific job in less than the standard time, the variance is favourable. It is important to note that theactual time should be taken after deducting abnormal idle time if any.

Direct Labour Efficiency Variance (DLEV) = Standard Rate X (Standard Hour - Actual Hour)

Reasons for labour efficiency varianceo Use of incorrect grade of labouro Insufficient trainingo Bad supervisiono Incorrect instructionso Bad working conditionso Worker’s dissatisfactiono Defective equipment and machineryo Wrong item of equipmentso Excessive labour turn over, ando Fixation of incorrect standards

Illustration 6: The standard and actual figures of a firm are asunderStandard time for the job : 1000 hrsStandard rate per hour : Re.0.50Actual time taken : 900 hoursActual wages paid : Rs.360Compute labour variances.

Solution:Labour Cost Variance:= Standard cost of labour – Actual cost of labour= (1000x0.50) – (900 x 0.40)=500 – 360= Rs. 140 Favourable Labour Mix Variance = Actual time x (Standard rate – Actual rate)= 900x (0.50 – 0.40)Favourable Labour efficiency Variance = Standard rate x (Standard time for actual output – Actual time)=0.50 x (1000 – 900)= Rs. 50 Favourable

Illustration 5: Calculate labour cost variance fromthe following data:Standard hours: 40Rate : Rs. 3 per hourActual hours : 60Rate : Rs. 4 per hour

Solution:Labour cost Variance = Standard cost of labour –Actual cost of labour= (40x3) – (60x4)=120 – 240 =Rs. 120 Adverse

DIRECT LABOUR VARIANCE OR Direct WAGE VARIANCE contd.

DIRECT LABOUR VARIANCE OR Direct WAGE VARIANCE contd.

Illustration 7:Standard labour hours and rate of production of Article A are given below:Skilled Worker- 5 hours @ Rs. 1.50 per hour Total Rs. 7.50Unskilled Worker- 8 hours @ Rs. .50 per hour Total Rs. 4.00Semi-skilled Worker- 4 hours @ Rs. .75 per hour Total Rs. 3.00Grand Total Rs.14.50

Actual Data are as follows:Article produced- 1000 unitsSkilled Worker- 4500 hours, Rate Rs. 2.00 per hour Total Rs. 9000Unskilled Worker- 10000 hours, Rate Rs. 0.45 per hour Total Rs. 4500Semi-skilled Worker- 4200 hours, Rate Rs. 0.75 per hour Total Rs. 3150Grand Total Rs. 16650

Calculate a) Labour Cost Variance b) Labour Rate Variance c) Labour efficiency Variance

DIRECT LABOUR VARIANCE OR Direct WAGE VARIANCE contd.

Solution: a) Labour Cost Variance (LCV) = (Standard Hour for Actual Production X Standard Rate) – (Actual Hour X ActualRate)

Computation of Standard Hour for Actual Production:

Skilled Worker- 1000 X 5 = 5000 HoursUnskilled Worker- 1000 X 8 = 8000 HoursSemi-skilled Worker- 1000 X 4 = 4000 Hours

Labour Cost Variance (LCV):Skilled Worker = (5000 X Rs. 1.50) - (4500 X Rs. 2) = Rs. 1500 (A)Unskilled Worker = (8000 X Rs. 0.50) - (10000 X Rs. 0.45) = Rs. 500 (A)Semi-skilled Worker = (4000 X Rs. 0.75) - (4200 X Rs. 0.75) = Rs. 150 (A)

Total Labour Cost Variance = Rs. 2150 (A)

DIRECT LABOUR VARIANCE OR Direct WAGE VARIANCE contd.

b) Labour Rate Variance (LRV) = Actual Hour x (Std. Rate – Actual Rate)

Skilled Worker = 4500 (1.50 - 2) = Rs. 2250 (Adverse)Unskilled Worker = 4200 ( 0.75 - 0.75) = Nil

Semi-skilled Worker = 1000 (0.50 - 0.45) = Rs. 500 (Favourable)

Total Labour Rate Variance = Skilled Worker + Unskilled Worker + Semi-skilled worker=Rs. 2250 (Adverse) + Nil+ Rs. 500 (Favourable)= Rs. 1750 (A)

c) Labour Efficiency Variance (LEV) = Standard Rate X (Standard Hour for Actual Production – Actual Hour for Actualproduction )Skilled Worker = 1.50 X(5000 - 5500) = Rs. 750 (A)Unskilled Worker = 0.50 X( 8000 - 8800) = Rs.400 (A)Semi-skilled Worker = 0.75 X(4000 - 4400) = Rs. 300 (A)Total Labour Efficiency Variance = Rs. 1450 (A)

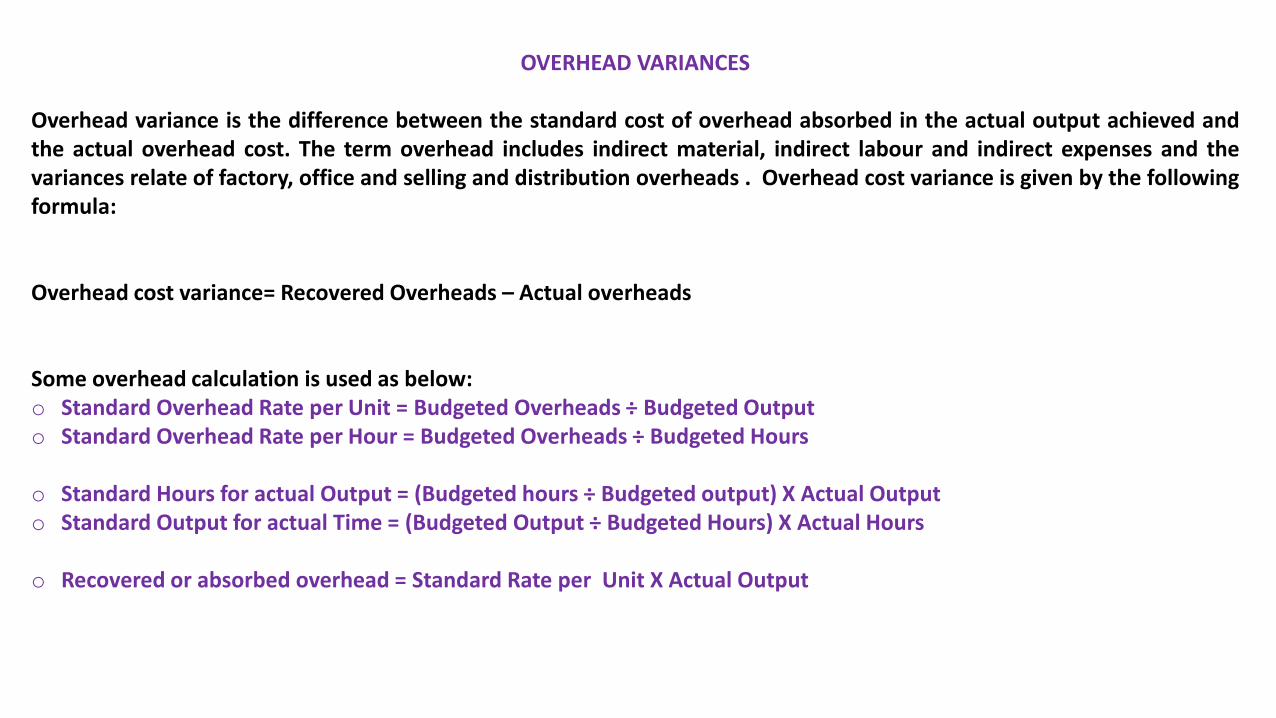

OVERHEAD VARIANCES

Overhead variance is the difference between the standard cost of overhead absorbed in the actual output achieved andthe actual overhead cost. The term overhead includes indirect material, indirect labour and indirect expenses and thevariances relate of factory, office and selling and distribution overheads . Overhead cost variance is given by the followingformula:

Overhead cost variance= Recovered Overheads – Actual overheads

Some overhead calculation is used as below:o Standard Overhead Rate per Unit = Budgeted Overheads ÷ Budgeted Outputo Standard Overhead Rate per Hour = Budgeted Overheads ÷ Budgeted Hours

o Standard Hours for actual Output = (Budgeted hours ÷ Budgeted output) X Actual Outputo Standard Output for actual Time = (Budgeted Output ÷ Budgeted Hours) X Actual Hours

o Recovered or absorbed overhead = Standard Rate per Unit X Actual Output

OVERHEAD VARIANCES contd.

Overhead variances are divided into two broad categories

i) Variable Overhead Cost variances and ii) Fixed Overhead Cost variances.

Variable Overhead Variance: Variable cost varies in proportion to the level of output, where the cost is fixed per unit. Assuch the standard cost per unit of these overheads remains the same irrespective of the level of output attained. As thevolume does not affect the variable cost per unit or per hour, the only factor leading to difference is price.

Variable Overhead Cost Variance (VOCV): Variable Overhead Cost Variance (VOCV): is the difference between standardoverheads for actual output i.e. Recovered Overhead and actual variable overheads.

VOCV = Variable Recovered Overhead – Actual Variable Overhead

Where Variable Recovered Overhead = ( Standard Variable Overhead ÷ Variable Standard Output) X Variable ActualOutput

OVERHEAD VARIANCES contd.

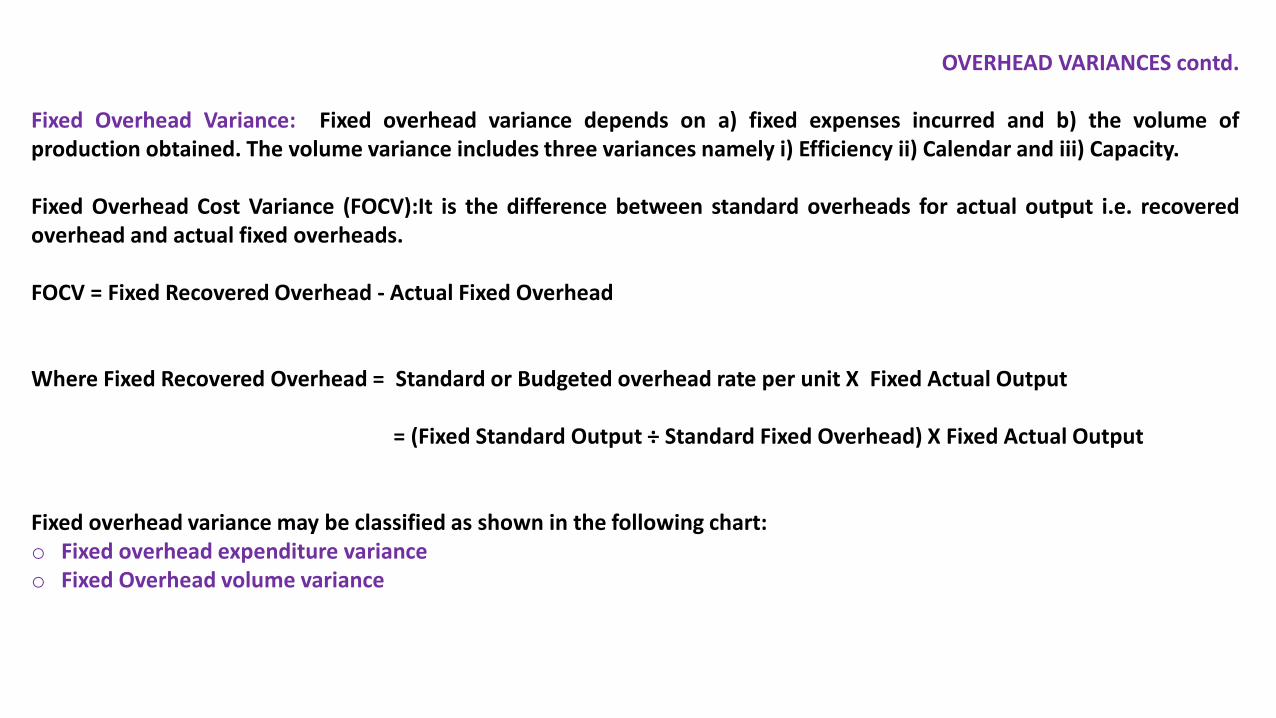

Fixed Overhead Variance: Fixed overhead variance depends on a) fixed expenses incurred and b) the volume ofproduction obtained. The volume variance includes three variances namely i) Efficiency ii) Calendar and iii) Capacity.

Fixed Overhead Cost Variance (FOCV):It is the difference between standard overheads for actual output i.e. recoveredoverhead and actual fixed overheads.

FOCV = Fixed Recovered Overhead - Actual Fixed Overhead

Where Fixed Recovered Overhead = Standard or Budgeted overhead rate per unit X Fixed Actual Output

= (Fixed Standard Output ÷ Standard Fixed Overhead) X Fixed Actual Output

Fixed overhead variance may be classified as shown in the following chart:o Fixed overhead expenditure varianceo Fixed Overhead volume variance

OVERHEAD VARIANCES contd.

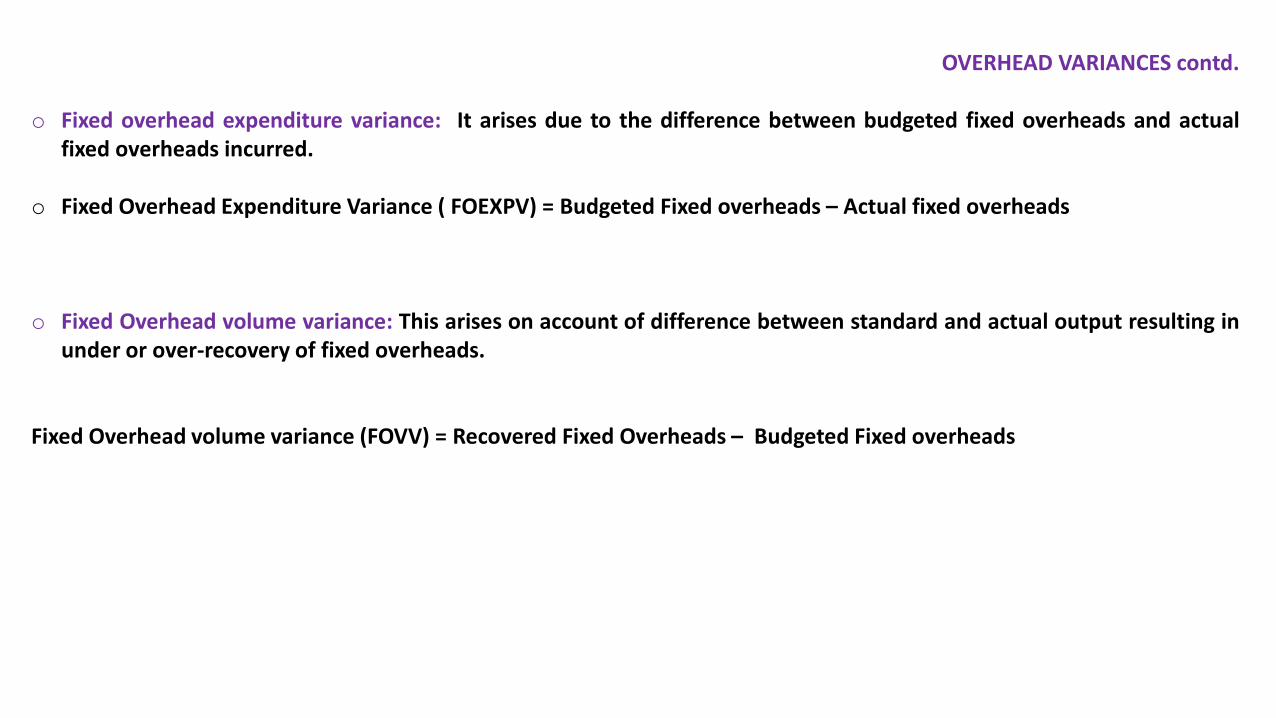

o Fixed overhead expenditure variance: It arises due to the difference between budgeted fixed overheads and actualfixed overheads incurred.

o Fixed Overhead Expenditure Variance ( FOEXPV) = Budgeted Fixed overheads – Actual fixed overheads

o Fixed Overhead volume variance: This arises on account of difference between standard and actual output resulting inunder or over-recovery of fixed overheads.

Fixed Overhead volume variance (FOVV) = Recovered Fixed Overheads – Budgeted Fixed overheads

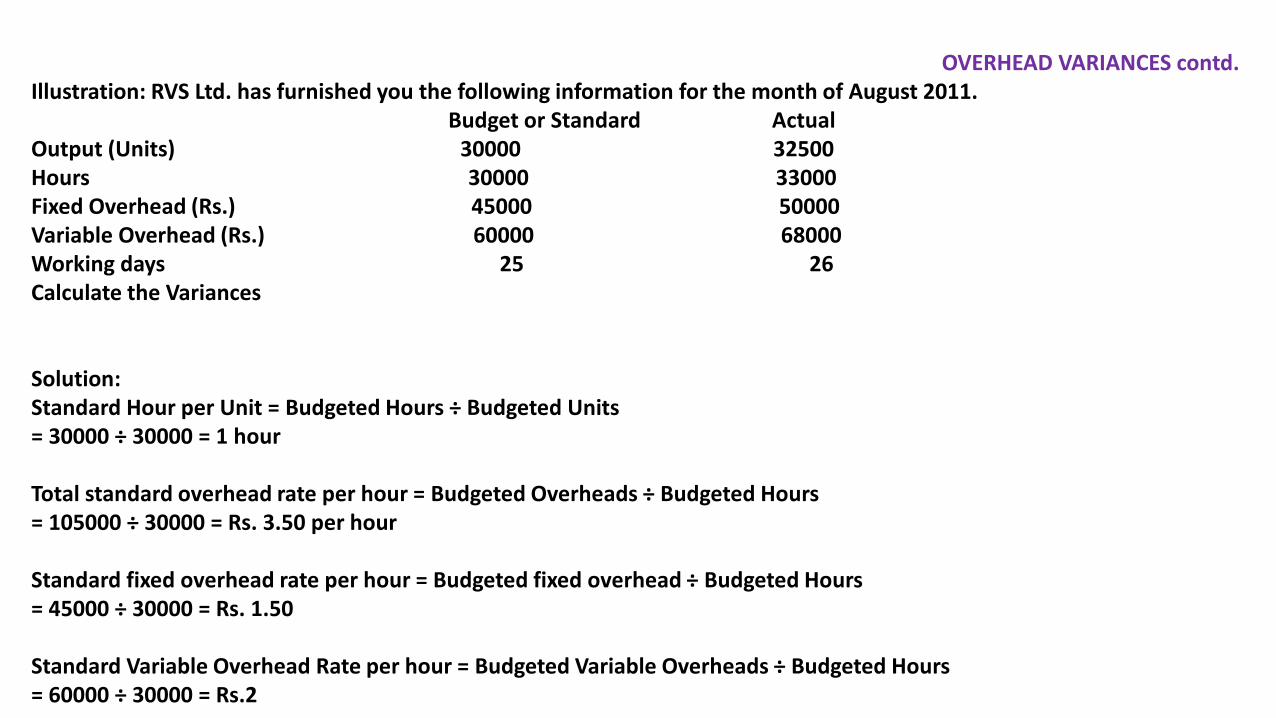

OVERHEAD VARIANCES contd.Illustration: RVS Ltd. has furnished you the following information for the month of August 2011.

Budget or Standard ActualOutput (Units) 30000 32500Hours 30000 33000Fixed Overhead (Rs.) 45000 50000Variable Overhead (Rs.) 60000 68000Working days 25 26Calculate the Variances

Solution:Standard Hour per Unit = Budgeted Hours ÷ Budgeted Units= 30000 ÷ 30000 = 1 hour

Total standard overhead rate per hour = Budgeted Overheads ÷ Budgeted Hours= 105000 ÷ 30000 = Rs. 3.50 per hour

Standard fixed overhead rate per hour = Budgeted fixed overhead ÷ Budgeted Hours= 45000 ÷ 30000 = Rs. 1.50

Standard Variable Overhead Rate per hour = Budgeted Variable Overheads ÷ Budgeted Hours= 60000 ÷ 30000 = Rs.2

OVERHEAD VARIANCES contd.

Overhead Cost Variance = Recovered Overheads - Actual Overheads

Total Recovered Overheads = Standard Rate per Unit X Actual Output= ( Budgeted overhead ÷ budgeted output )X Actual Output

= (105000 ÷ 30000) X 325,00 = 3.5 X Rs. 113750

Total Overhead Cost Variance = total overhead recovered – actual overheads= Rs. 113750 – Rs. 118000 = Rs. 4250 (Adverse)

Recovered Variable overheads = Variable Standard Rate per Unit X Actual Output = ?

Recovered Fixed overheads = Fixed Standard Rate per Unit X Actual Output = ?

Variable Overhead Cost Variance = Rs. 65000 - Rs. 68000 = Rs. 3000 (A) = how?

Fixed Overhead Cost Variance = Rs. 48750 - Rs. 50000 = Rs. 1250 (A) = how?

OVERHEAD VARIANCES contd.

Calculate different overheads variances from the following standard and actual data

Standard Overheads Rate per unit

Variable Rs. 3.00Fixed (Rs 36000 ÷ 3000) Rs. 12.00

Rs. 15.00

Actual Data during the period:

Output 2400 unitsOverheadVariable Rs. 6000Fixed Rs. 28000 Rs 34000