standard of the papers • the six-month rule • examination

TRANSCRIPT

-9-

SYLLABUSES AND READING LISTS FOR

THE ACCOUNTING TECHNICIAN EXAMINATIONS

• Standard of the Papers

• The Six-month Rule

• Examination Paper Structure

• Duration

• Syllabuses and Reading Lists

Appendices: 1 - 68

-Appendix 1-

SYLLABUSES AND READING LISTS FOR THE ACCOUNTING TECHNICIANEXAMINATIONS

Standard of the Papers

The papers are set at a level comparable with the level of skills and knowledge expected ofaccounting technicians. In terms of competency-based standards, the competency is level1 to 3 as indicated below:

Level 1 – Awareness

The candidate demonstrates familiarity with the concept in question; can define it in over-view terms; and can relate the importance or relevance of the concept to the activities of aprofessional accountant.

Level 2 – Knowledge

This builds upon awareness. Without necessarily being able to perform in the followingareas with professional skill, the candidate is able to explain the concept; describe anddiscriminate between its component parts and describe their inter-relationships; recogniseinstances of the concept; and describe processes, theories and judgement issues.

Level 3 – Skill

This builds upon knowledge. The candidate is able to execute or implement knowledge;and apply the knowledge to real world problems in real world situations. In so doing, thecandidate displays to a satisfactory degree the level of competence reasonably to be ex-pected of an Accounting Technician at career entrance level.

The Six-month Rule

Candidates have to respond to examination questions according to legislation andpronouncements of the Hong Kong Institute of Certified Public Accountants which arereleased six months prior to the examination date. It should be noted that the six-monthrule refers to the enactment date of the legislation and the release date of the pronouncements,not their effective date.

Examination Paper Structure

Paper

Paper 1FinancialAccounting

Paper 2BusinessCommunication

Paper 3Cost Accounting

Paper 4InformationTechnologyApplications inAccounting

Paper 5Hong KongTaxation

Paper 6Hong KongBusiness Law

Paper 7AdvancedAccounting

Paper 8Auditing

-Appendix 2-

Examination Format

Section A

10 – 25 multiplechoice questions

10 – 25 multiplechoice questions

10 – 25 multiplechoice questions

10 – 25 multiplechoice questions

10 – 25 multiplechoice questions

10 – 25 multiplechoice questions

10 – 25 multiplechoice questions

10 – 25 multiplechoice questions

Section B

3 out of 4questions

Not more than 5short questions

4 out of 5questions

2 questions onhands-on

computerisedaccounting

routines(i) System for

financialrecording

(ii) System foraccountingoperations,control anddecision-making

1 compulsoryquestion

Not more than10 short

questions

1 compulsoryquestion

4 out of 6questions

Section C

3 out of 4questions

3 out of 5questions

3 out of 5questions

(Questions onbills of

exchange willnot be asked in

this section)

2 out of 4questions

Remarks

Chart ofaccounts isappended

Tax rate andallowance tablesare available

Duration

All papers other than Paper 4 last for 3 hours. Paper 4 lasts for 31/2 hours, which includesthe time needed for basic data input and report printing.

-Appendix 3-

Paper 1 – Financial Accounting

Aim

This paper aims at testing students’ understanding of the basic accounting principles, andtheir ability to apply concepts of financial accounting and methods to record businesstransactions and to prepare and interpret financial statements.

Content

1. The role of financial accounting and reporting

CompetenceRequired

Understanding of the roleof financial accountingand reporting

Activity to Develop andDemonstrate Competence in

� Describe the nature, scope andpurposes of financial statements andtheir related records and accounts

� Identify and explain the qualitativecharacteristics of financialstatements

� Identify the users of financialaccounts and statements and explaintheir information needs

IndicativeLevel

1

2

2

2. The principles of financial accounting

CompetenceRequired

Understanding of theprinciples of financialaccounting

Activity to Develop andDemonstrate Competence in

� Explain and apply the followingaccounting concepts, principles andconventions:- going concern- accrual- consistency- materiality- prudence- business entity- accounting period- historic cost- money measurement- substance over form

� Describe the accounting standardsand guidelines and their applicationto external financial reports

� Explain the need for generallyaccepted accounting principles(GAAP) and apply them in thepractice of accounting

IndicativeLevel

2

2

2

-Appendix 4-

3. Recording, handling and summarising accounting data

CompetenceRequired

Understanding of thebooks of original entry

Understanding of thedouble entry accountingsystem

Skill in applying theaccounting equation anddouble entry accountingsystem to businesstransactions through topreparing a trial balance

Skill in keeping controlaccounts

Activity to Develop andDemonstrate Competence in

� Describe the functions of thefollowing books of original entry:- cash book- petty cash book- sales journal/book- purchases journal/book- returns inward journal/book- returns outward journal/book- general journal

� Explain the double entry accountingsystem

� Apply the accounting equation(Assets = Owner’s Equity +Liabilities)

� Classify and record businesstransactions in terms of theaccounting equation

� Prepare the following books oforiginal entry from source records:- cash book- petty cash book (including imprestsystem)

- sales journal/book- purchase journal/book- returns inward journal/book- returns outward journal/book- general journal

� Record the posting of journalentries to the following ledgeraccounts:- general ledger accounts- sales ledger accounts- purchases ledger accounts

� Extract a trial balance from theledger accounts

� Describe the functions of controlaccounts

� Prepare the following controlaccounts:- sales ledger control account- purchases ledger control account

� Reconcile control accounts withledger balances

IndicativeLevel

1

2

3

3

3

3

3

2

3

3

3. Recording, handling and summarising accounting data (continued)

CompetenceRequired

Skill in preparing a bankreconciliation statement

Understanding of thecorrection of errors andthe skill in preparingsuspense accounts

Activity to Develop andDemonstrate Competence in

� Explain the use of a bankreconciliation statement

� Prepare a bank reconciliationstatement

� Describe various types of errors

� Describe the purpose of a suspenseaccount

� Prepare journal entries to correcterrors and post the entries torespective ledger accounts,including the suspense account

IndicativeLevel

2

3

2

2

3

CompetenceRequired

Understanding of capitaland revenue expenditure

Knowledge of theaccounting treatment offixed assets

Knowledge of theaccounting treatment ofcurrent assets

Activity to Develop andDemonstrate Competence in

� Distinguish between capital andrevenue expenditure

� Define fixed assets

� Explain depreciation and thereasons for and methods ofproviding for it

� Describe the factors to beconsidered in formulating thedepreciation policy

� Record the accounting treatment forproviding depreciation for anddisposing of fixed assets

� Define and provide examples ofcurrent assets

� Define inventories and debtors

� Distinguish between perpetual andperiodic inventory systems

� Explain and justify the valuation ofinventories at the lower of cost andnet realisable value

� Explain bad debts and the provisionfor doubtful debts and prepare therelevant accounting entries

IndicativeLevel

3

2

3

2

3

2

2

2

3

3

-Appendix 5-

4. Fixed assets, current assets and pre-closing adjustments

-Appendix 6-

CompetenceRequired

Skill in handling pre-closing adjustments

Activity to Develop andDemonstrate Competence in

� Prepare the accounting treatment(journal entries and ledger posting)for pre-closing adjustmentsincluding:- accruals- prepayments- income in arrears- income in advance

IndicativeLevel

3

4. Fixed assets, current assets and pre-closing adjustments (continued)

CompetenceRequired

Skill in preparingfinancial statements forsole traders

Skill in preparingfinancial statements forclubs and societies

Skill in preparingfinancial statements forpartnerships

Activity to Develop andDemonstrate Competence in

� Prepare an income statement(trading and profit and lossaccount) and a balance sheet of asole trader from a trial balance orincomplete accounting records

� Prepare a receipts and paymentsaccount, an income and expenditureaccount and the correspondingbalance sheet for a club and society

� Prepare an income statement and anappropriation account and a balancesheet for a partnership,incorporating:- pre-closing adjustments- interest on capital- partners’ salary- interest on drawings- share of profits and losses

� Distinguish between partners’capital and current accounts

� Prepare capital and current accountsfor partners

� Record admission and retirement ofpartners and prepare the balancesheet for the new partnership

� Describe the nature of goodwill andexplain its accounting treatment

� Explain and record the revaluationof assets

� Record the dissolution ofpartnership

IndicativeLevel

3

3

3

2

3

3

3

3

3

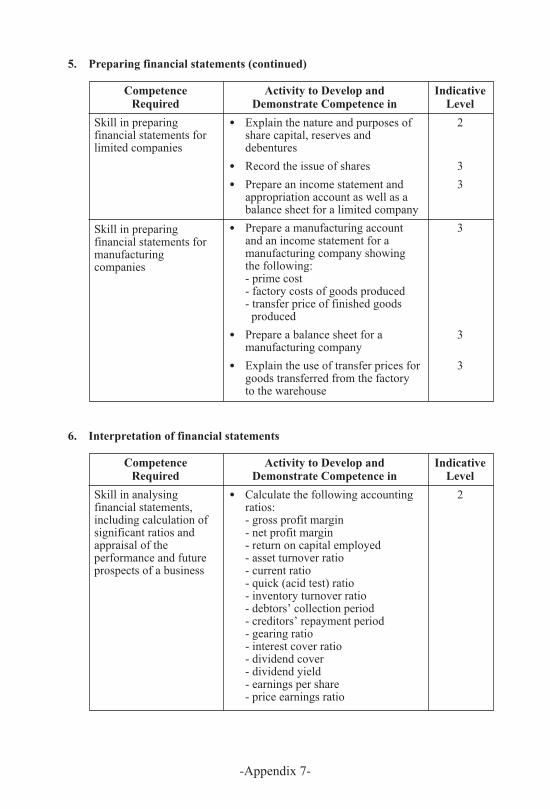

5. Preparing financial statements

-Appendix 7-

5. Preparing financial statements (continued)

CompetenceRequired

Skill in preparingfinancial statements forlimited companies

Skill in preparingfinancial statements formanufacturingcompanies

Activity to Develop andDemonstrate Competence in

� Explain the nature and purposes ofshare capital, reserves anddebentures

� Record the issue of shares

� Prepare an income statement andappropriation account as well as abalance sheet for a limited company

� Prepare a manufacturing accountand an income statement for amanufacturing company showingthe following:- prime cost- factory costs of goods produced- transfer price of finished goods

produced

� Prepare a balance sheet for amanufacturing company

� Explain the use of transfer prices forgoods transferred from the factoryto the warehouse

IndicativeLevel

2

3

3

3

3

3

6. Interpretation of financial statements

CompetenceRequired

Skill in analysingfinancial statements,including calculation ofsignificant ratios andappraisal of theperformance and futureprospects of a business

Activity to Develop andDemonstrate Competence in

� Calculate the following accountingratios:- gross profit margin- net profit margin- return on capital employed- asset turnover ratio- current ratio- quick (acid test) ratio- inventory turnover ratio- debtors’ collection period- creditors’ repayment period- gearing ratio- interest cover ratio- dividend cover- dividend yield- earnings per share- price earnings ratio

IndicativeLevel

2

-Appendix 8-

Examination format:

Section A 10 – 25 multiple choice questions 25 marks

Section B 3 out of 4 questions 75 marks

100 marks

Essential reading:

Author Title Publisher

Li, A. T. M. Financial Accounting HKAATand Ng, P. P. H. (New edition to be

published in 2005)

Additional reading:

Author Title Publisher

Wood, F., Sangster, A., Frank Wood’s Business LongmanYau, L., Yau, R. Accounting – Hong Kongand Yau, J. (Volumes 1 and 2) (2nd Edition)

Millichamp, A. H. Foundation Accounting Continuum(5th Edition)

6. Interpretation of financial statements (continued)

CompetenceRequired

Activity to Develop andDemonstrate Competence in

� Explain the significance of andreasons for changes in ratios overtime or differences in ratios betweentwo companies in terms of:- profitability and use of assets- short term liquidity- long term solvency- investment ratio

IndicativeLevel

3

-Appendix 9-

CompetenceRequired

Understanding of thebasic concepts ofcommunication

Activity to Develop andDemonstrate Competence in

� Define communication

� Identify the communication process

� Define the communication model:- sender- message- encoding- channel- receiver- decoding- feedback

� Recognise the importance of theyou-attitude:- differentiate between the you-

attitude and the I-attitude- describe how to develop the you-- attitude

IndicativeLevel

2

2

2

2

Paper 2 - Business Communication

Aim

This paper aims at assessing students’ ability to apply a broad range of language skills tocope with a variety of communication activities related to the accounting field. A skills-based approach to the examination of communication is adopted.

This paper also aims at testing students’ ability to communicate effectively and conciselywithin a business environment through accepted standard English.

Content

1. Introduction

2. Communication for career advancement

CompetenceRequired

Ability to applycommunication skills tocareer advancement

Activity to Develop andDemonstrate Competence in

� Understand the relationships betweenemployers and employees

� Describe the employment processand understand the requirementsfrom an employer’s perspective

� Apply communication skills to jobsearches and interviews

� Identify methods for self-analysis andplanning a career path

� Prepare an effective resume with aproper layout:- format- information required- style- tone

� Prepare a covering letter with astrategic purpose

� Outline the information and materialrequired for a job search:- reference- transcripts- portfolio- interview attire- organisational chart

� Prepare other employment relatedletters:- thank-you letter- letter to decline an offer of a

position- letter of resignation

� Understand the needs and reasons fora reference letter

� Outline the necessary informationincluded in a reference letter

� Prepare reference letters forsubordinates / friends / colleagues

IndicativeLevel

1

1

2

1

3

3

3

3

2

2

3

-Appendix 10-

-Appendix 11-

3. Communication skills

CompetenceRequired

Understanding of thedifferent means ofcommunication

Ability to solve businesscommunication problems

Recognition of thesource of writtenmaterial

Understanding about theforms of communicationwithin an organisation

Activity to Develop andDemonstrate Competence in

� Distinguish between the differentmeans of communication:- reading- written- oral- listening

� Compare the advantages andeffectiveness of the four types ofcommunication

� Identify the common barriers thatimpede communication:- barriers in the world around us- barriers between people- barriers made by words- barriers caused by cultural

differences

� Demonstrate how effectivecommunication can be achieved:- create a favourable environment- observe the dress code- use a proper channel- understand the audience’s

background- organise thoughts / ideas logically- focus on specific topics- encourage feedback from the

audience

� Discuss Maslow’s Hierarchy ofNeeds

� Identify the various sources ofwritten material

� Develop the ability to extractrelevant information from a widerange of documents and resources

� Prepare summary for businessmeetings and events

� Understand the different forms ofcommunication:- internal and external- verbal and written- upward and downward- vertical and lateral

IndicativeLevel

2

2

1

2

1

1

2

3

2

-Appendix 12-

4. Language proficiency

CompetenceRequired

Understanding of thewriting process

Ability to prepare andcompose businesswriting in a professionaltone

Activity to Develop andDemonstrate Competence in

� Identify the writing process:- brainstorming- defining goals and audience- doing research- planning- drafting- revising- proof-reading

� Be able to identify and eliminatecommon problems in writing:- wordiness- the overuse of passive sentences- excessive use of ‘s’ and commas- choppiness- subjectivity- negativity- clichés- lack of variety

� Use the four major techniques foremphasis in writing businessdocuments

� Use punctuation marks correctly

� Write complete, grammaticallycorrect sentences; avoid suchproblems as awkward construction,dangling modifiers, and misuse ofwords

� Apply unity and clarity in writingeffective sentences

� Understand the rules of paragraphingand use topic sentences in writingclear paragraphs

� Demonstrate knowledge of businessjargon and abbreviations

� Understand the advantages anddisadvantages of presentinginformation from diagrams, charts,tables and graphs in writing

� Use an appropriate tone:- The four Ps: personal / polite /

positive / professional

IndicativeLevel

2

2

3

3

3

3

3

2

1

2

-Appendix 13-

5. External written communication

CompetenceRequired

Ability to conveyaccurate and concreteinformation in writtenbusiness communication

Skill and ability to writedifferent forms ofexternal businesscommunicationeffectively

Activity to Develop andDemonstrate Competence in

� Discuss and distinguish thedifferences between the followingbusiness communication:- business letter- memo- agenda / minutes- report- proposal- e-mail- fax message

� Demonstrate clear understanding ofthe definition and application of thevarious jargon in the above businesscorrespondence

� Understand the nature and featuresof business letters:- enquiry letter- letter of request- letter placing an order- collection letter- sales and promotion letter- complaint letter- letter of recommendation- letter of appreciation- letter of congratulations- letter of condolence

� Distinguish the tone and format ofthe above types of letters

� Compose effective and concisewritten documents andcorrespondence

� Be able to prepare responses for thefollowing business correspondence:- enquiry letter- letter of request- letter placing an order- complaint letter

IndicativeLevel

2

2

2

2

3

3

-Appendix 14-

6. Internal written communication

CompetenceRequired

Skill and ability to writeeffective internalbusiness communication

Capability to produceshort reports that areinformative, accurate andtimely

Ability to applyappropriate style to shortreports for internalcommunication

Activity to Develop andDemonstrate Competence in

� Understand the nature and needs forwriting the various kinds ofdocuments for internalcommunication:- memorandum- agenda and minutes- report- proposal- notice

� Discuss the degree of formality usedin a memorandum

� Write clear and effectivememorandums for routine enquiries,responses, policies, directives andindirect messages

� Be able to convey facts and describeincidents concisely and clearly

� Define the purpose of a report

� Distinguish between the variouskinds of reports:- formal / informal report- long / short report- proposal- recommendation report- evaluation report

� Understand the report-writingprocess and explain the importanceof objectivity in report writing

� Prepare a complete report:- identify the different styles of

report and the features in a report- understand the pros and cons of

including diagrams, pictures, data,tables in a report

- discuss the importance of designand layout of a report

- gather and select information andsummarise relevant data fromresearch material

- evaluate the quality of the report

� Discuss the prefatory parts of areport in relation to length andformality

� Apply conventional organisation inwriting short reports, adapting thisfor writing reports such as staff, auditand technical reports

IndicativeLevel

2

2

3

2

2

2

2

3

2

3

7. Preparation for a meeting

CompetenceRequired

Understanding of thenature and requirementsfor a business meeting

Activity to Develop andDemonstrate Competence in

� Explain the functions of a meeting /conference

� Describe the process for calling aproductive and effective meeting

� Identify the features of a meeting:- people- purposes- venue

� Prepare an agenda and minutes

� Convey and consolidate materialsinto effective, concise presentationmaterials for the meeting

� Describe the problems of a meeting:- group-think- hidden agenda- interpersonal conflicts

� Evaluate the quality andeffectiveness of a meeting

IndicativeLevel

2

2

2

3

3

2

2

-Appendix 15-

-Appendix 16-

Examination format:

Section A 10 – 25 multiple choice questions 20 marks

Section B Not more than 5 short questions 20 marks

Section C 3 out of 4 questions 60 marks

100 marks

Essential reading:

Author Title Publisher

Heathman, G. and Business Communication HKAATLee, P. K. L. (2003 Edition)

Cullinan, M. Business Communication Harcourt Brace CollegePrinciples and Processes(2nd Edition)

Bilbow, G. T. Business Writing for LongmanHong Kong (3rd Edition)

Additional reading:

Author Title Publisher

Guffey, M. E. Business English South-Western(7th Edition)

Taylor, S. Communication for Business Longman(3rd Edition)

Brieger, N. and The Language of Business LongmanSweeney, S. English – Grammar and

Functions (1st Edition)

Aldred, D. and Written Business Communication: Hong Kong Institute ofOfford-Gray, C. A Course for Accountants Certified Public

Accountants (formerlyHong Kong Society ofAccountants),Hong KongUniversity Press

Macintosh, D. English for Business (6th Edition) Book Marketing Ltd

Paper 3 - Cost Accounting

Aim

This paper aims testing students’ ability to develop an understanding of the principles ofcost accounting and examining their knowledge of costing methods and techniques thatcan be applied to a variety of business situations.

Content

1. Framework of cost accounting

CompetenceRequired

Ability to compare cost,management andfinancial accounting

Knowledge of costclassification, conceptsand terminology

IndicativeLevel

1

1

1

1

1

1

2

3

1

1

Activity to Develop andDemonstrate Competence in

� Explain and differentiate thepurposes of cost accounting,management accounting andfinancial accounting

� Appreciate the role of costaccounting in a managementinformation system

� Appreciate the importance offinancial and non-financialinformation for planning, controland decision-making purposes

� Recognise the variety of cost units,cost centres and profit centres

� Understand the nature and purposeof cost classification

� Appreciate the importance of costcoding system and costaccumulation

� Differentiate between direct andindirect costs; fixed and variablecosts; period and product costs;controllable and uncontrollablecosts; avoidable and unavoidablecosts; etc.

� Identify cost classification fordecision-making and planning

� Appreciate cost behaviour patternsincluding linear, curvi-linear andstep functions

� Appreciate the importance of unitcosts to both financial andmanagement accountants

-Appendix 17-

1. Framework of cost accounting (continued)

2. Principles and practice of cost accounting

CompetenceRequired

Understanding ofintegrated andinter-locking costingsystem

Activity to Develop andDemonstrate Competence in

� Explain and illustrate the linkbetween cost accounting andfinancial accounting

� Explain and illustrate the working ofinterlocking accounts and integratedaccounts

� Prepare the accounting entries in ageneral ledger under an integratedcosting system

� Understand the reconciliation of costaccounts with financial accounts

IndicativeLevel

2

2

3

2

CompetenceRequired

Understanding ofmaterials cost as anelement of finishedgoods

Understanding of labourcost as an element offinished goods

Activity to Develop andDemonstrate Competence in

� Describe the methods and procedureof store-keeping, stock-taking andstock control

� Explain and illustrate the perpetualinventory system and its proceduresdocumentation

� Explain and illustrate the methodsavailable for pricing stores issuesand for stock valuation

� Appreciate the basic features andfunctions of direct and indirectlabour costs

� Use and contrast differentremuneration methods

� Appreciate the process of labourcost accounting

� Calculate and appreciate theimplications of labour turnover

IndicativeLevel

2

3

3

2

2

3

3

-Appendix 18-

2. Principles and practice of cost accounting (continued)

3. Application of cost accounting

CompetenceRequired

Understanding ofoverhead costs as anelement of finished goods

Activity to Develop andDemonstrate Competence in

� Appreciate the nature of overheadcosts

� Explain and illustrate the problemsand procedures of collection,analysis, allocation, apportionmentand absorption of overhead costs

� Ascertain the different bases foroverhead absorption rates

� Appreciate the use of and computethe predetermined overheadabsorption rate

� Differentiate and calculateplant-wide overhead rates anddepartmental overhead rates

� Explain and illustrate the principlesand methods of treatment of under-and over-absorption of overhead costs

IndicativeLevel

2

3

3

3

3

2

CompetenceRequired

Understanding of thenature and features of joband batch costing

Understanding of theprincipal features ofcontract costing

Activity to Develop andDemonstrate Competence in

� Describe the purpose and thecontent of a job cost sheet

� Account for the flow of costs whenusing job order costing

� Explain and illustrate the costaccounting methods used in costingthe products and services of abusiness

� Outline the characteristics,procedures and documentation ofjob-order costing and batch costing

� Explain and illustrate theapplications and identification ofcost units

� Appreciate the skill needed in thepreparation of a contract account

� Appreciate the treatment of profitand uncompleted contracts

� Explain and illustrate the ledgerentries relevant to contract costing

IndicativeLevel

3

2

3

2

2

3

3

2

-Appendix 19-

3. Application of cost accounting (continued)

CompetenceRequired

Knowledge of the natureand features of processcosting

Understanding of theprincipal features ofactivity based costing(ABC)

Activity to Develop andDemonstrate Competence in

� Explain and illustrate theapplications and identification ofcost units

� Illustrate the ledger entries andspecial features of process costaccounts

� Explain and compute the equivalentunits and cost per equivalent unit

� Demonstrate how costs are assignedto equivalent units using processcosting

� Explain and illustrate the costaccounting methods used in costprocesses, process losses and work-in-process

� Differentiate joint product andby-product costing

� Define activity cost pools andprovide examples

� Compare and illustrate ABC andtraditional product costing systems

� Demonstrate how activity bases areused to assign cost pools to unitsproduced

� Outline the benefits and limitationsof ABC

� Explain the differences between,and the effect of, using fullabsorption costing, marginal costingand activity based costing for theallocation of costs to products

IndicativeLevel

2

2

3

3

3

3

1

3

3

2

3

-Appendix 20-

CompetenceRequired

Understanding of theneed for, and benefits of,budgeting and budgetarycontrol

Understanding ofstandard costing

Skill in analysingcost-volume-profit (CVP)relationships

Activity to Develop andDemonstrate Competence in

� Identify the objectives of budgetaryplanning and control systems

� Prepare functional, cash and masterbudgets

� Appreciate the differences betweenfixed and flexible budgets

� Calculate variances and identifytheir causes

� Explain and illustrate the concept ofzero-based budgeting

� Appreciate the uses and limitationsof standard costing

� Explain the importance of usingstandard costing to control costs

� Identify and determine differentstandards: basic, ideal, attainableand current standards

� Identify and calculate sales and costvariances

� Prepare standard product cost andanalyse different types of variancesbetween standard and actual productcosts

� Identify the significance of andinter-relationship between variances

� Prepare a CVP graph

� Calculate and explain the usefulnessof contribution margin andcontribution margin ratio

� Determine the sales volumerequired to earn a desired level ofoperating income

� Identify the purposes of break-evenanalysis

� Illustrate and determine the marginof safety

� Use CVP relationships to evaluate anew marketing strategy

� Identify assumptions underlyingCVP analysis

IndicativeLevel

2

3

3

3

2

2

1

2

3

3

3

1

3

3

2

2

3

1

-Appendix 21-

4. Information for planning and control

Examination format:

Section A 10 – 25 multiple choice questions 20 marks

Section B 4 out of 5 questions 80 marks

100 marks

Essential reading:

Author Title Publisher

Fong, S. C. C. and Cost Accounting HKAATKumar, N. K. (2002 Edition)

Drury, C. Cost & Management Accounting: Thomson LearningAn Introduction (5th Edition)

Lucey, T. Costing (6th Edition) Continuum

Additional reading:

Author Title Publisher

Garrison, R. H. and Managerial Accounting IRWIN/McGraw-HillNoreen, E. W. (10th Edition)

Drury, C. Management & Cost Accounting Thomson Learning(6th Edition)

Horngren, C. T. and Cost Accounting, Prentice HallFoster, G. A Managerial Emphasis

(11th Edition)

-Appendix 22-

Paper 4 – Information Technology Applications in Accounting

Aim

The aim of this paper is two-fold. The first is to assess students’ knowledge and skills inthe hands-on practice of computerised accounting work. The second is to assess theapplication of computer-based technologies for processing, presenting and managingaccounting data as well as documents.

Content

1. Selection and implementation of computerised accounting systems and software

2. Human information processing of computerised accounting systems

CompetenceRequired

Understanding of theselection andimplementation ofcomputerised accountingsystems and software

Activity to Develop andDemonstrate Competence in

� Understand organisational contextof systems development,conventional wisdom on systemsdevelopment lifecycle, developmentof prototype, and feasibility study

� Outline the accounting informationsystem development strategies: theselection of packaged software,customised software, and/ormodified software

� Understand the role of accountinginformation system in e-business

� Understand the needs, benefits andrisks of outsourcing computerisedaccounting work

IndicativeLevel

1

2

2

1

CompetenceRequired

Understanding of thehuman informationprocessing mechanism inhandling computerisedaccounting work

Activity to Develop andDemonstrate Competence in

� Describe the factors of humancomputer interaction: ergonomics,interaction styles, and the context ofinteraction

� Describe the uses of task analysis inhandling computerised accountingroutines: participation inrequirements capture, system designand interface design

� Understand the uses of the helpfunction and documentation of acomputerised accounting system

IndicativeLevel

1

1

1

-Appendix 23-

3. System for financial recording

CompetenceRequired

Skill in the application ofa computerised financialaccounting system forfinancial reporting

Activity to Develop andDemonstrate Competence in

� Demonstrate and apply skill in theoperation of the financial book-keeping system:

- create specific types of accountsunder the given structure ofchart of accounts

- conduct ledger transactions inthe general ledger, receivablesledger and payable ledger.Details include master filecreation, end of periodadjustments and closing

- create a customer file: handlebilling transactions for invoices,fill backorders and sales returnsprocessing

- create a vendor file: conducttransactions for purchase orders,merchandise received andpurchase returns processing

- handle cash transactions forreceipt and payment processing

- produce financial reports coveringchart of accounts, aging report,trial balance, profit and lossstatement, balance sheet

- perform periodic adjustmentsduring month-end and year-end,including entries for accruals,prepayment and depreciation

IndicativeLevel

2

3

3

3

3

3

2

-Appendix 24-

4. System for accounting operations, control and decision-making

CompetenceRequired

Skill in the application ofspreadsheet software forfinancial documentpreparation and costinganalysis

Activity to Develop andDemonstrate Competence in

� Demonstrate ability and skill inspreadsheet applications with Excelusing referenced cells, logicalfunctions, statistical functions,financial functions, and graphs to:

- perform financial result analysis inactual, static budgeted and flexiblebudgeted formats

- conduct financial statement analysis

- conduct profit volume analysisand pricing decision in variablecosting format

- perform discounted cash flowanalysis for financial management

- forecast inventory levels withmoving average analysis for stockcontrol

- compile operation and sales data

� Generate a PivotTable report invariable costing format foraccounting decision-making

IndicativeLevel

3

3

3

2

2

2

3

CompetenceRequired

Understanding of theconcepts of computerisedaccounting data controland security

Activity to Develop andDemonstrate Competence in

� Understand data security, natureand sources of threats to computersystems

� Outline the types of security design,contingency planning and operation

� Understand the types of computercrime

� Describe systems back-up proceduresfor disaster recovery

IndicativeLevel

2

2

2

2

-Appendix 25-

5. Control and security

Examination format:

Section A 10 – 25 multiple choice questions 25 marks

Section B 2 questions on hands-on computerised accounting routines 75 marks� System for financial recording� System for accounting operations, control and

decision-making

100 marks

The examination time is 31/2 hours, which includes the time needed for basic data input andreport printing. Students will use DacEasy Accounting for Windows and Microsoft Excelto answer two questions in the examination papers; in addition DacEasy will be used toanswer the “System for financial recording” question.

Essential reading:

Author Title Publisher

Lee, S. S. P. and Information Technology Applications HKAATLi, G. K. H. in Accounting (2004 Edition)

Smith, G. N. Excel Applications for Accounting South-WesternPrinciples (2nd Edition)

Fulford, James The Accountant’s Guide to Oak Tree PressAdvanced Excel (1st Edition)

Romney, M. B. and Accounting Information Systems Prentice HallSteinbart, P. J. (9th Edition)

Dix, A., Finlay, J., Human – Computer Interaction Pearon Education LtdArowd, G. and (3rd Edition)Beale, R.

Additional reading:

Author Title Publisher

Klooster, Dale H. and Integrated Accounting for South-WesternAllen, Warren W. Windows (4th Edition)

Smith, G. N. Excel Spreadsheet Applications South-WesternSeries for Cost Accounting(1st Edition)

-Appendix 26-

Paper 5 - Hong Kong Taxation

Aim

This paper aims at providing students with a general knowledge of the principles of taxationin Hong Kong and developing their ability to interpret and apply the taxing statutes topractical situations.

Content

1. Hong Kong taxation system

CompetenceRequired

Understanding of theoperation of the HongKong taxation systemand the chargeability toHong Kong income tax

Activity to Develop andDemonstrate Competence in

� Distinguish between differentclassifications of taxes

� Describe the characteristics of theHong Kong taxation system

� Describe the sources of Hong Kongtax law and how the tax statutes areinterpreted

� Describe the functions of differentunits of the Inland RevenueDepartment

� Describe the appointment andpowers of the Commissioner ofInland Revenue

� Describe the structure, powers andfunctions of the Board of InlandRevenue

� Describe the structure, powers andfunctions of the Board of Review

� Describe and distinguish the scopeof charge of different sources ofincome tax:- property tax- salaries tax- profits tax

IndicativeLevel

1

1

1

1

2

2

2

2

-Appendix 27-

2. Property tax

3. Salaries tax

CompetenceRequired

Understanding of thecomputation of propertytax liabilities of ownersof land/buildings situatedin Hong Kong

Activity to Develop andDemonstrate Competence in

� Identify the persons and propertieschargeable to property tax

� Compute the assessable value andnet assessable value

� Explain the treatment of theirrecoverable consideration

� Explain the treatment of lump sumpayment

� Compute the amount of property taxand provisional property tax

� Describe the requirements andconditions for hold over of paymentof provisional property tax

� Distinguish the circumstances whereincome from letting of property issubject to property tax or profits tax

� Explain the conditions forexemption of property tax forcorporations and set-off of propertytax against profits tax

� Explain the statutory requirementsof retention of rent records

IndicativeLevel

1

3

3

3

3

2

2

2

2

CompetenceRequired

Understanding of thecomputation of salariestax liabilities ofindividuals

Activity to Develop andDemonstrate Competence in

� Describe the factors to beconsidered in the determining thelocality of income of:- employment- office- pension

� Distinguish between employmentand profession

� Explain the differences between thetreatment of:- Hong Kong offices and foreign

offices- Hong Kong employment and

foreign employment

� Explain the tax treatment of incomeof Hong Kong employment whereforeign tax has been paid

IndicativeLevel

3

1

3

2

-Appendix 28-

CompetenceRequired

Activity to Develop andDemonstrate Competence in

� Explain the tax treatment of theincome received by aircrew andseamen

� Identify the different types ofincome exempt from salaries tax

� Identify the basis period

� Explain the meaning of accrual ofincome and determine the date ofaccrual of different kinds of income

� Explain the procedures andtreatment for relating back lumpsum receipts

� Describe different kinds of incometo be included as income fromemployment or office

� Describe and compute taxablebenefits, including:- accommodation benefit- holiday warrant- share options- education expenses of a child of

an employee- benefits-in-kind

� Compute assessable income, netassessable income and netchargeable income

� Explain the conditions for anyexpenditure to be deducted from theassessable income

� Describe the conditions for thededuction of concessionarydeductions

� Explain the conditions for thededuction of personal allowances

� Compute salaries tax payable withreference to the lower of tax atprogressive rate on net chargeableincome or tax at standard rate on netassessable income as reduced byconcessionary deductions

� Compute provisional salaries taxpayable

� Describe the requirements andconditions for hold over of paymentof provisional salaries tax

IndicativeLevel

3

1

2

2

2

2

3

3

2

2

2

3

3

2

3. Salaries tax (continued)

-Appendix 29-

3. Salaries tax (continued)

4. Profits tax

CompetenceRequired

Activity to Develop andDemonstrate Competence in

� Explain the meaning of “husband”,“wife” and “husband and wifeliving apart”

� Distinguish between the tax treatmentof a husband and wife under separatetaxation and under joint assessment

� Explain the procedures and time limitfor the election of joint assessment

� Explain the tax treatment of a husbandand wife in the year of marriage,separation, divorce and death

IndicativeLevel

1

2

2

1

CompetenceRequired

Understanding of thecomputation of profits taxliabilities of businesses ofan individual, partnershipand corporation

Activity to Develop andDemonstrate Competence in

� Define the meanings of persons,trade and business

� Describe the badges of trade

� Define the meaning of profitsarising in or derived from HongKong and identify the factors to beconsidered in determining thesource of profit

� Distinguish between capital andrevenue receipts and capital andrevenue expenditure

� Explain different kind of deemedtrading receipts chargeable toprofits tax

� Identify different kinds of income tobe excluded from the charge toprofits tax

� Explain the conditions for thededuction of various types ofexpenses under profits tax in general

� Explain the conditions for thededuction of specific expensesunder profits tax, including:- special contributions to recognised

occupational retirement schemes- expenditure on scientific research- expenditure on refurbishment of

building- expenditure on prescribed fixed

assets- technical education payment- patent and know-how purchase costs

IndicativeLevel

1

2

2

2

1

1

2

2

-Appendix 30-

CompetenceRequired

Activity to Develop andDemonstrate Competence in

� Identify the various types of non-deductible expenditure under profitstax

� Recognise the presentation of aproper format in the computation ofassessable profits

� Determine when income frombusiness should be assessed

� Identify different acceptablemethods of the valuation of stock

� Explain the principle of Sharkey v.Wernher

� Determine the basis period fordifferent circumstances

� Compute the amount of profits taxand provisional profits tax

� Explain the requirements andconditions for hold over of paymentof provisional profits tax

� Explain the treatment of losses fordifferent kinds of businesses

� Explain the meaning of partnershipand illegal partnership

� Compute the profit/loss shared byeach partner

� Explain the person who is liable topay the tax under partnership

� Explain the treatment of share ofprofit/loss where there is a changein a partnership

� Explain the treatment of losses of apartnership

IndicativeLevel

2

3

1

1

1

2

2

2

3

1

3

1

3

3

4. Profits tax (continued)

-Appendix 31-

5. Depreciation allowances

CompetenceRequired

Understanding of thecomputation ofdepreciation allowances

Activity to Develop andDemonstrate Competence in

� Explain the meaning of plant andmachinery and identify items whichare plant and machinery

� Identify the persons who areentitled to claim depreciationallowances on plant and machinery

� Identify the qualifying expenditurefor depreciation allowances on plantand machinery

� Compute depreciation allowancesunder the pooling system andnon-pooling system

� Explain the meaning of an industrialbuilding and identify a building/structure which is treated as anindustrial building

� Identify the persons who areentitled to claim the industrialbuilding allowance

� Identify the qualifying expenditurefor an industrial building allowance

� Compute the industrial buildingallowance

� Explain the meaning of commercialbuilding and identify a building/structure which is treated as acommercial building

� Identify the persons who areentitled to claim the commercialbuilding allowance

� Identify the qualifying expenditurefor a commercial buildingallowance

� Compute the commercial buildingallowance

IndicativeLevel

1

1

3

3

1

1

3

3

1

1

3

3

-Appendix 32-

6. Personal assessment

7. Administration of taxes

CompetenceRequired

Understanding of thecomputation of taxpayable under personalassessment

Activity to Develop andDemonstrate Competence in

� Explain the persons who are eligibleto elect for personal assessment

� Explain the requirements andconditions for electing personalassessment

� Compute the tax payable underpersonal assessment in respect of:- an individual- husband and wife

IndicativeLevel

1

2

3

CompetenceRequired

Understanding of theadministration of taxesunder the InlandRevenue Ordinance

Activity to Develop andDemonstrate Competence in

� Explain the powers of the assessorto obtain returns

� Explain the powers of the followingofficers of the Inland RevenueDepartment to obtain information:- assessor- inspector- assistant commissioner- commissioner

� Explain the obligations of ataxpayer and an employer

� Explain the powers of an assessor inraising an assessment

� Identify the persons responsible forcompliance with the InlandRevenue Ordinance

� Explain how notices issued by theInland Revenue Department shouldbe served

� Explain the requirements andprocedures for lodging a validobjection by a taxpayer

� Explain the procedures at the InlandRevenue Department upon receiptof a valid objection

� Explain the requirements of a validappeal against the Commissioner ofInland Revenue’s determination tothe Board of Review

� Explain how the Board of Reviewhears and disposes of an appeal

IndicativeLevel

1

1

2

2

1

1

3

3

3

1

-Appendix 33-

CompetenceRequired

Activity to Develop andDemonstrate Competence in

� Explain the procedures required tolodge an appeal to the:- Court of First Instance- Court of Appeal- Court of Final Appeal

� Explain the right of a taxpayer tomake an error or omission claim

� Explain the powers of the InlandRevenue Department in respect ofthe demand of payment of tax underobjection or appeal

� Explain the powers of the InlandRevenue Department in therecovery of tax

� Explain the procedures for claimingrepayment of tax

� Explain the penalties to be imposedby the Inland Revenue Departmentin respect of an offence committedby the taxpayer

� Explain the procedures for raisingan assessment to additional taxunder section 82A

� Explain the requirements of a validappeal against the assessment toadditional tax under section 82A

IndicativeLevel

1

1

1

1

1

1

2

2

7. Administration of taxes (continued)

-Appendix 34-

Examination format:

Section A 10 – 25 multiple choice questions 20 marks

Section B 1 compulsory question 26 marks

Section C 3 out of 5 questions 54 marks

100 marks

Essential reading:

Author Title Publisher

Lee, D. L. Y. Hong Kong Taxation HKAAT(2004 Edition)

Inland Revenue Ordinance, HKSARChapter 112

Additional reading:

Author Title Publisher

Smith, D. Hong Kong Taxation: The Chinese UniversityLaw & Practice Press(2004 – 05 Edition)

Departmental Interpretation and Inland Revenue DepartmentPractice Notes

Inland Revenue Rules HKSAR

Hong Kong Tax Cases HKSAR

Hong Kong Board of Review HKSARDecisions

-Appendix 35-

Paper 6 - Hong Kong Business Law

Aim

This paper aims at providing students with an awareness of the overall legal framework inwhich business in Hong Kong operates and at enabling them to apply the relevant legalrules and practices to business problems and practical situations.

Content

1. Hong Kong legal system

CompetenceRequired

Knowledge of:- the historical and

formal sources of HongKong law

- the system of courtsand administration ofjustice

- legislation and statutoryinterpretation

- the work of solicitorsand barristers

Activity to Develop andDemonstrate Competence in

� Describe the different categories oflaw

� Demonstrate an awareness of why itis essential for business people tohave a knowledge of law

� Describe the origin and developmentof the Hong Kong SAR legal system

� Describe the relationship betweenthe constitution of the PRC, BasicLaw and Hong Kong SAR law

� Describe the main provisions of theHong Kong SAR Basic Law

� Distinguish between common lawrules and rules of equity

� Outline the main sources of law andshow how each operate

� Explain the doctrine of precedentand the role of the courts in thedevelopment of the common law

� Identify the unique nature of case law

� Describe the structure and jurisdictionof the courts and tribunals and explainthe way disputes are resolved throughthe courts and through alternativemeans

� Outline how appeals may progressfrom one court to another

� Explain how the principles ofinterpretation apply to statutes

� Describe the main rules of statutoryinterpretation

� Describe the work of solicitors andbarristers

IndicativeLevel

1

1

1

1

1

1

1

2

2

1

1

2

2

2

-Appendix 36-

2. General principles of contract law

CompetenceRequired

Understanding of:- the essentials for the

formation of a contract- formality and terms of a

contract- exemption clauses- the vitiating factors

affecting the validityand formality of acontract

- the discharge of acontract

- the remedies for breachof contract

Ability to apply theabove principles toproblem situations

Activity to Develop andDemonstrate Competence in

� List the requirements for a simplevalid contract

� Differentiate between valid, void,voidable and unenforceablecontracts

� Define offer and distinguish it fromother similar statements

� Describe and analyse when an offercomes to an end

� Define acceptance and identifywhether an acceptance is valid

� Describe the effects of differentmeans of communications ofacceptance

� Explain battle of forms

� Distinguish between simple contractand specialty contract

� Define consideration and apply therules in relation to consideration

� Differentiate between past, executedand executory consideration

� Explain the equitable doctrine ofpromissory estoppel

� Describe the meaning and effect ofprivity of contract

� Explain the meaning of intention toenter into legal relations and applythe various presumptions relating tointention

� Explain and analyse the effect ofincapacity on contracts

� Distinguish between arepresentation and a term

� Recognise an express term of acontract

� Describe how terms may be impliedin a contract

� Distinguish between conditions andwarranties

� Describe innominate terms

IndicativeLevel

1

2

3

3

3

3

2

2

3

3

2

3

2

3

3

2

2

3

2

-Appendix 37-

2. General principles of contract law (continued)

CompetenceRequired

Activity to Develop andDemonstrate Competence in

� Define an exclusion clause

� Describe how the courts and statuterestrict the use of exclusion clauses

� Define an unconscionable contract

� Define actionable misrepresentations

� Distinguish between the differenttypes of misrepresentation

� Describe the different remedies forthe various types of misrepresentation

� Explain the different types ofmistake and the defences available

� Identify duress and describe itseffect in a contract

� Explain undue influence

� Explain contract in restraint of tradeand the circumstances under whichsuch a contract will be enforceable

� Describe the effect of illegality

� Explain when a contract isdischarged by performance

� Identify the requirements that arenecessary to terminate a contract byagreement

� Explain frustration and its effects

� Explain the nature of breach ofcontract

� Identify the various remediesavailable for breach

� Explain the principles in assessingdamages

� Distinguish between liquidateddamages and a penalty clause

� Explain specific performance andinjunction

� Identify those situations where anequitable remedy is applicable

IndicativeLevel

2

3

2

2

3

3

3

3

2

3

2

2

2

3

2

2

2

3

3

2

-Appendix 38-

2. General principles of contract law (continued)

3. Bills of exchange

CompetenceRequired

Activity to Develop andDemonstrate Competence in

� Understand rescission and restitution

� Demonstrate an awareness of thegeneral principles in relation toSales of Goods Ordinance

� Demonstrate an awareness of thegeneral principles in relation toagency law

IndicativeLevel

2

1

1

CompetenceRequired

Understanding of:- the nature, definition

and purpose of a bill ofexchange

- the concept ofnegotiability of bills ofexchange

- the duties and liabilitiesof the parties concerned

Activity to Develop andDemonstrate Competence in

� Define a bill of exchange and anegotiable instrument anddemonstrate awareness of thepurpose of a bill of exchange

� Define a cheque and distinguish itfrom other bills of exchange

� Identify the parties to a bill ofexchange and a cheque

� Explain the concept of negotiabilityand describe the process ofnegotiation

� Outline the different types ofindorsement

� Describe how a bill of exchange anda cheque can be dishonoured

� Explain the liabilities of parties to adishonoured bill of exchange and adishonoured cheque

� Explain the effect of a forged orunauthorised signature of a bill ofexchange

� Explain the purpose and describe thedifferent types of crossing in cheques

� Outline the duties and liabilities of abank with respect to cheques

� List the statutory protectionavailable to the paying bank andcollecting bank with respect tocheques

IndicativeLevel

1

1

1

1

1

1

1

1

1

1

1

-Appendix 39-

4. Legal personality and the nature of limited company

CompetenceRequired

Understanding of:- the differences between

a limited company anda partnership

- the consequences ofseparate legalpersonality

- the relationship of legalpersonality to limitedliability and itsimplications in thebusiness world

and ability to apply theabove principles toproblem situations.

Activity to Develop andDemonstrate Competence in

� Define partnership

� Describe the nature andcharacteristics of partnership

� Explain the advantages anddisadvantages of forming apartnership

� Compare a partnership with acompany

� Explain the advantages anddisadvantages of incorporation

� Recognise the different types ofregistered company

� Explain the veil of incorporationand the circumstances when the veilwill be lifted

� Explain the concept and the purposeof limited liability

IndicativeLevel

2

2

3

3

3

2

3

3

-Appendix 40-

5. Company law

CompetenceRequired

Knowledge of:- the formation of a

company and itsconstitution

- the formalities and therole of the Registrar

- the registration ofshares, charges,directors and theirshareholdings

- the contractual capacityof a company

- the statutory books,records and returns

Activity to Develop andDemonstrate Competence in

� Describe the procedures in theformation of a registered company

� Describe a promoter and list his duties

� Describe what is meant by a pre-incorporation contract and explainthe problems of such a contract

� Describe the memorandum ofassociation and articles ofassociation and explain their effects

� List the typical contents of thememorandum of association andarticles of association

� Identify the restriction on its articleswhich a company can choose

� Explain what is meant by Table A

� State how articles and memorandummay be changed

� Understand the functions andresponsibilities of the Registrar ofCompanies

� State the requirements for theregistration of shares, charges,directors and their shareholdings

� Explain the contractual capacity ofa company

� State the requirements for statutorybooks, records and annual return

IndicativeLevel

2

2

2

2

2

2

2

2

1

2

2

2

-Appendix 41-

CompetenceRequired

Knowledge of:- share capital of

companies- loan capital of

companies

Ability to apply theabove knowledge toproblem situations

Activity to Develop andDemonstrate Competence in

� Explain the meaning and purpose ofcapital and the nature of shares

� Differentiate between the differentclasses of share capital

� Explain class rights and explain howa company can change its class rights

� Distinguish between the transferand transmission of shares

� Explain how shares might betransferred from one person toanother and how a company canrestrict the free transferability ofshares

� Explain the nature of dividends andthe rules on their distribution

� Describe how a company can alterits share capital

� Define a debenture and describedifferent types of debenture

� Explain the company’s power toborrow

� Contrast the position of ashareholder with the position of adebenture holder

� Contrast the position of a securedcreditor with that of an unsecuredcreditor

� Distinguish between a fixed and afloating charge

� Explain the registration requirementfor company charges

� Outline the effect of a failure toregister a charge

� Explain the priority of differenttypes of charges on a winding up ofa company

� List the remedies available to loancreditors

IndicativeLevel

2

3

3

1

2

3

2

1

2

3

3

2

2

2

2

2

-Appendix 42-

6. Capital and financing of companies

CompetenceRequired

Knowledge of:- company directors- company secretary- auditors- companies meetings

Ability to apply the aboveknowledge to problemsituations.

Activity to Develop andDemonstrate Competence in

� Identify a director and explain whata shadow director is

� Describe how directors areappointed and removed

� Explain the powers and duties ofdirectors

� Explain conflict of interests and therules applicable when directors dealwith their own company

� Explain how directors may avoidliability for breach of duty andoutline the remedies available whena director breaches his duty

� Explain the various forms ofprotection available to minorityshareholders

� Explain the role and duties of acompany secretary and describehow a company secretary isappointed and how his contract maybe terminated

� Explain the role and duties of anauditor and describe how an auditoris appointed and re-appointed andhow his contract may be terminated

� Explain the differences between anannual general meeting and anextraordinary general meeting

� Distinguish between an ordinaryresolution and a special resolution

� State the rules and procedures as tothe voting rights of membersincluding proxy voting

� State the quorum requirements ingeneral meetings

IndicativeLevel

2

3

3

3

2

3

3

3

2

3

3

2

-Appendix 43-

7. Management and administration of a company

Examination format:

Section A 10 – 25 multiple choice questions 20 marks

Section B Not more than 10 short questions 20 marks

Section C 3 out of 5 questions 60 marks(Questions on bills of exchange will not be asked in this section)

100 marks

Essential reading:

Author Title Publisher

Cheng, P. W., Hong Kong Business Law HKAATClementson, I., (New edition to be publishedSaunders, J. R. and in 2005)Scott, P.

Stott, V. Hong Kong Company Law Longman(10th Edition)

Additional reading:

Author Title Publisher

Stott, V. An Introduction to LongmanHong Kong Business Law(3rd Edition)

Dobinson, I. and Introduction to Law Sweet & MaxwellRoebuck, D. of HKSAR (2nd Edition)

Shum, C. General Principles of LongmanHong Kong Law (3rd Edition)

Srivastava, D. K. (ed.) Business Law in Hong Kong Sweet & Maxwell(1st Edition) Asia

Arjunan, K. and Business Law in Hong Kong LexisNexisMajid, A. (1st Edition)

Cheng, P. W., The Hong Kong Company LongmanSum, H. S. and Secretary’s Handbook, PracticeYuen, K. T. Francis and Procedure (7th Edition)

Legislation in various areas: HKSAR- The Basic Law of the Hong

Kong Special AdministrativeRegion of the People’sRepublic of China

- Companies Ordinance

- Control of ExemptionClauses Ordinance

- Misrepresentation Ordinance

- Partnership Ordinance

- Sale of Goods Ordinance

- Unconscionable Contracts

Ordinance

-Appendix 44-

Paper 7 - Advanced Accounting

Aim

This paper aims at developing an understanding of the principles and practices of financialaccounting and the practical skills and professional competence of an accounting technician.

Content

1. The principles of financial accounting and reporting

CompetenceRequired

Knowledge of theregulatory framework

Knowledge of account-ing theories and prin-ciples

Understanding of theframework for thepreparation andpresentation of financialstatements

Understanding of theimportance ofmaintaining professionalethics and independenceof the accounting andauditing professions

Activity to Develop andDemonstrate Competence in

� Describe the structure of theregulatory system and itsrelationship to financial accountsand statements

� Identify the nature and role ofbodies which set the accountingstandards and guidelines

� Identify the nature, role andsignificance of accounting theoriesand principles, accountingconventions, accounting standardsand guidelines, legislative andquasi-legislative requirements inpreparing financial accounts andreports

� Demonstrate awareness of theconcepts that underlie thepreparation and presentation offinancial statements under generallyaccepted accounting principles

� Understand the conceptualframework for financial reporting

� Demonstrate awareness of theguidance given in the relevantaccounting standards regarding theframework for financial statementspresentation

� Outline the requirements of theProfessional Accountants Ordinance

� Demonstrate awareness of theguidance with respect toprofessional ethics given in theFundamental Principles, Statementsand Guidelines

IndicativeLevel

1

1

2

1

2

1

1

1

-Appendix 45-

2. Applications of accounting conventions and accounting practice as specified inthe Companies Ordinance and Accounting Standards

CompetenceRequired

Understanding of thebasis for presentation offinancial statements

Understanding of theclassification, disclosureand accounting treatmentof certain items infinancial statements

Understanding of theprinciples for thedetermination andpresentation of earningsper share

Understanding of theaccounting treatment forgroup companies

Activity to Develop andDemonstrate Competence in

� Specify the underlying accountingprinciples and rules for offsettingassets and liabilities

� Define current assets and currentliabilities

� Specify the requirements of relevantaccounting standard in relation tothe minimum content and layout forprimary financial statements, anddisclosures for the incomestatements

� Specify the treatment and disclosureof changes in accounting policies,changes in accounting estimates andcorrection of errors and otherrequirements of relevant accountingstandard

� Explain the need to discloseearnings per share

� Compute the basic and dilutedearnings per share

� Describe the disclosurerequirements under relevantaccounting standard

� Explain the reasons for differentforms of business combinations

� Define a parent, a subsidiary, agroup, minority interests andconsolidated financial statements

� Discuss the legal requirements ofconsolidated financial statementsand the relevant requirements ofrelevant accounting standard

� Explain the disclosure requirementsof consolidated financial statementsunder relevant accounting standard

IndicativeLevel

2

2

1

2

1

3

1

1

2

2

1

-Appendix 46-

2. Applications of accounting conventions and accounting practice as specified inthe Companies Ordinance and Accounting Standards (continued)

CompetenceRequired

Understanding of thesignificance ofprovisions, contingentliabilities and contingentassets, and events afterthe balance sheet date inthe ascertainment of acompany’s net profit orloss for a period

Understanding of theaccounting treatment tobe adopted by aninvestor for investmentsin associates

Activity to Develop andDemonstrate Competence in

� Define and identify provisions,contingent liabilities and contingentassets

� Explain the requirements of relevantaccounting standard in relation tothe accounting treatment ofprovisions, contingent liabilities andcontingent assets in the financialstatements and their disclosures

� Define events after the balancesheet date

� Identify adjusting and non-adjustingevents after the balance sheet date

� Explain the requirements of relevantaccounting standard in relation towhen an entity should adjust itsfinancial statements for events afterthe balance sheet and theirdisclosures

� Explain the requirements of relevantaccounting standard in relation toaccounting for events after thebalance sheet date and theirdisclosures

� Define an associate

� Explain the meaning of significantinfluence

� Explain the equity method ofaccounting for investments inassociates in the consolidatedfinancial statements

� Explain the requirements of relevantaccounting standard in relation toaccounting for investments inassociates in an investor’s ownfinancial statements

� Prepare consolidated financialstatements for a group incorporatingthe results of associates

� Describe the disclosurerequirements under relevantaccounting standard

IndicativeLevel

2

2

2

2

2

2

2

2

2

2

3

1

-Appendix 47-

2. Applications of accounting conventions and accounting practice as specified inthe Companies Ordinance and Accounting Standards (continued)

CompetenceRequired

Understanding of theaccounting treatment forinvestment properties

Understanding of theaccounting treatment forleases

Understanding of therequirements for cashflow statements

Understanding of theaccounting treatment forintangible assets,including research anddevelopment expenditureand goodwill

Activity to Develop andDemonstrate Competence in

� Define an investment property

� Explain the accounting treatmentrequired by relevant accountingstandard in respect of investmentproperties and the necessarydisclosures

� Comment on the prescribed practicefor depreciation on investmentproperties

� Demonstrate awareness of theaccounting issues concerned withexpensing versus capitalising forleases

� Explain the nature and classificationof leases

� Apply the required accountingtreatment to operating leases andfinance leases in the financialstatements of the lessee and lessor

� Describe the disclosure requirementsunder relevant accounting standardfor both lessees and lessors

� Explain the purpose of preparing acash flow statement

� Define cash, cash equivalents andcash flows

� Evaluate the usefulness of a cashflow statement

� Prepare a cash flow statement for asingle company and a group usingthe direct and indirect methods withsupporting notes in the format asspecified in relevant accountingstandard

� Define intangible assets

� Outline the problems relating toaccounting for intangible assets

� Comment on the controversysurrounding the treatment ofintangible assets

� Describe the requirements ofrelevant accounting standard inrespect of intangible assets that are:

IndicativeLevel

2

2

2

2

2

3

1

2

2

2

3

1

2

1

2

-Appendix 48-

2. Applications of accounting conventions and accounting practice as specified inthe Companies Ordinance and Accounting Standards (continued)

CompetenceRequired

Understanding of theaccounting treatment forproperty, plant andequipment

Understanding of incomemeasurement andrevenue recognition

Activity to Develop andDemonstrate Competence in

- acquired from a separateacquisition

- acquired from an acquisition aspart of a business combination

- internally generated

� Define research and development

� Describe the requirements ofrelevant accounting standard inrespect of research and developmentexpenditure and the necessarydiscloures

� Distinguish between internallygenerated goodwill and goodwill ornegative goodwill arising onacquisition

� Explain the requirements of relevantaccounting standard in respect ofaccounting for internally generatedgoodwill and goodwill or negativegoodwill arising on acquisition

� Discuss the requirements of relevantaccounting standard in respect ofthe recognition criteria for property,plant and equipment

� Discuss the accounting treatment ofthe determination of carryingamounts and the depreciationcharges and impairment losses ofproperty, plant and equipment

� Describe the disclosurerequirements under relevantaccounting standard

� Demonstrate awareness of theissues in revenue recognition

� Determine the measurement ofrevenue

� Discuss the revenue recognitioncriteria for sale of goods

� Explain the various types of servicetransactions and their criteria forrevenue recognition

� Discuss the revenue recognitioncriteria for interest, royalties anddividends

� Describe the disclosurerequirements under relevantaccounting standard

IndicativeLevel

1

2

1

2

2

3

1

1

3

2

2

2

1

-Appendix 49-

2. Applications of accounting conventions and accounting practice as specified inthe Companies Ordinance and Accounting Standards (continued)

CompetenceRequired

Understanding of theaccounting treatment forborrowing costs

Understanding of thedisclosure requirementsfor related partytransactions

Understanding of theclassification, disclosureand accounting treatmentrequired for interests injoint ventures

Activity to Develop andDemonstrate Competence in

� Discuss the criteria forcapitalisation of borrowing costs

� Determine when should theborrowing costs be capitalised

� Determine the commencement,suspension and cessation ofcapitalisation of borrowing costs

� Explain the accounting treatmentfor borrowing costs

� Describe the disclosurerequirements under relevantaccounting standard

� Explain the significance ofsufficient disclosure of related partytransactions

� Define a related party relationshipand identify the key elements indetermining related partyrelationships

� Describe situations where twoparties are possibly related

� Describe the disclosurerequirements of relevant accountingstandard in respect of related partytransactions

� Differentiate between investmentsin a joint venture and other types ofinvestments

� Identify the major types of jointventure:- jointly controlled operations- jointly controlled assets- jointly controlled entities

� Apply the required accountingtreatment to investments in differenttypes of joint venture

� Describe the disclosurerequirements for interests in a jointventure under relevant accountingstandard

IndicativeLevel

2

3

3

2

1

2

2

2

1

2

2

3

1

-Appendix 50-

2. Applications of accounting conventions and accounting practice as specified inthe Companies Ordinance and Accounting Standards (continued)

CompetenceRequired

Understanding of theaccounting treatment forinventories under thehistorical cost system

Understanding of theaccounting treatment ofrevenue and costsassociated withconstruction contracts

Activity to Develop andDemonstrate Competence in

� Define inventories

� Explain the appropriate accountingpractice with respect to thevaluation of inventories andsubsequent recognition as anexpense, including any write-downto net realisable value

� Compute the value of inventoriesfor inclusion in periodic financialstatements

� Describe the requirements ofrelevant accounting standard inrelation to the disclosure ofinformation regarding inventories infinancial statements

� Define construction contracts

� Discuss appropriate accountingpractice with respect to thevaluation of construction contracts

� Compute the value of constructioncontracts for inclusion in periodicfinancial statements

� Explain how the profit or loss on aconstruction contract is recognised

� Describe the requirements ofrelevant accounting standard inrelation to the disclosure ofinformation regarding constructioncontracts in financial statements

IndicativeLevel

2

2

3

1

2

2

3

2

1

-Appendix 51-

CompetenceRequired

Skill in preparingfinancial statements forpartnerships

Activity to Develop andDemonstrate Competence in

� Record the admission and retirementof partners and prepare a balancesheet for the new partnership

� Discuss the nature of internallygenerated goodwill

� Ascertain the value of and recordinternally generated goodwill

� Explain and record asset revaluation

IndicativeLevel

2

2

3

3

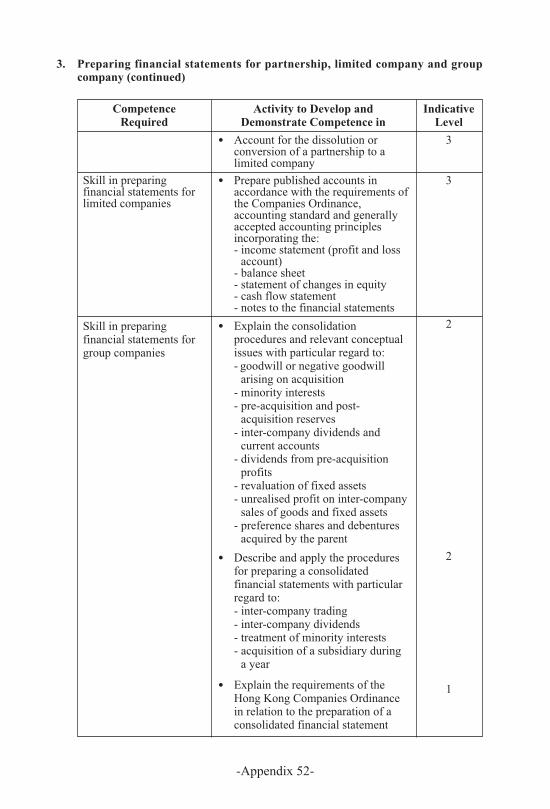

3. Preparing financial statements for partnership, limited company and groupcompany

-Appendix 52-

3. Preparing financial statements for partnership, limited company and groupcompany (continued)

CompetenceRequired

Skill in preparingfinancial statements forlimited companies

Skill in preparingfinancial statements forgroup companies

Activity to Develop andDemonstrate Competence in

� Account for the dissolution orconversion of a partnership to alimited company

� Prepare published accounts inaccordance with the requirements ofthe Companies Ordinance,accounting standard and generallyaccepted accounting principlesincorporating the:- income statement (profit and loss

account)- balance sheet- statement of changes in equity- cash flow statement- notes to the financial statements

� Explain the consolidationprocedures and relevant conceptualissues with particular regard to:- goodwill or negative goodwill

arising on acquisition- minority interests- pre-acquisition and post-

acquisition reserves- inter-company dividends and