star conference london october 5, 2010 - eems.it · 05 oct 10 3 group structure eems italia s.p.a....

TRANSCRIPT

Star Conference

London

October 5, 2010

EEMS Key Notes

Not only semiconductor, but ……..

A fast growing Photovoltaic business

Fully recovered from loss of Qimonda

With a much stronger financial position

Back on fast growing track

Moving for leadership in PV

05 Oct 103

Group Structure

EEMS Italia S.p.A.

EEMS TechnologySuzhou Co Ltd.

(China)

EEMS Singapore Pte. Ltd

(Singapore)Solsonica S.p.A.

EEMS Asia EEMS Asia PtePte. Ltd. Ltd

(Singapore)(Singapore)

EEMS China Pte. Ltd.(Singapore)

100%

100%

100%

100% 100%

100%

Listed Co Semiconductor Photovoltaic Dormient Holding

EEMS SuzhouCo. Ltd.(China)

05 Oct 104

Shareholders

Mutti family

D’Antonio *

Management *

Market

Total

9.208.316

2.950.975

709.828

30.728.001

43.597.120

21.1

6.8

1.6

70.5

100.0

Nbr of shares %

* Mr. D’Antonio and others have exercised their warrants

option for a total of 1.094.275 shares and injecting in the

Company a total consideration of 1.356.901 €

5 Oct 105

• Anticipated the opportunities in the Photovoltaic business sometime in 2007

• Shut down the semiconductor operations in Italy in 2008 to improve our overall competitiveness

• Consolidated all our semiconductor business in our existing operations in China

• Invested about 50 M€ for our start up in the Photovoltaic business

• Won a major contract to supply Dram back end services to Qimonda

• Invested in China specifically for Qimonda and started to ramp to volume

• Qimonda became insolvent as a company in early 2009 and went outof business

• We became financially stressed by lack of planned cash flow to be generated in China by the Qimonda business

Lots of changes in the past two years

5 Oct 106

What did we do

• Started our negotiations with Bank Pool to restructure the debt

• Successfully acquired more Dram volume from an existing customer

• Successfully completed our debt restructuring in early 2010

• Managed to sell out our non Dram test operation in Singapore

• The proceeds were used to pay off about 36 % of the 74 M€ debt with Bank Pool

• As result, we are approaching a more affordable NFP of slightly above 40 M€

• In the mean time we did develop substantial Photovoltaic business and properly positioned our Solsonica brand

5 Oct 107

The two legs strategy - Executed

EEMS Italia S.p.A.

EEMS AsiaSemiconductors

SolsonicaPhotovoltaic

Revenues in US $ currency

High Capex

Moderate growth

Fully integrated

One of few

Revenues in € currency

Low Capex

Very high growth

Partially integrated

One of many

05 Oct 108

Business and Factories

EEMS Italia S.p.A.

EEMS AsiaSemiconductors

SolsonicaPhotovoltaic

FreeZone

23,000 SQM1179 People

Dram-Dimm

No FreeZone

43,000 SQM339 People

Dram

Headquarter

23,000 SQM269 People

Cells & Modules

EEMS Suzhou EEMS Tech Solsonica

05 Oct 109

Semiconductor

5 Oct 1010

Eems China – Financial Performance – M$

0

20

40

60

80

100

120

140

2005 2006 2007 2008 2009 1H10

M$

Revenues Ebitda

Revenues

Ebitda

Ebitda %

4.6 70

30

43

111

42

38

123

46

38

90

24

27

63

17

28

Source : Company data

5 Oct 1011

Eems China - Financials – M$

1H09 1H10 2Q09 2Q10 1Q10 2Q10

31.7 63.5 16.4 34.0 29.5 34.0

100% 107% 15%

1H09 1H10 2Q09 2Q10 1Q10 2Q10

6.3 17.5 3.3 8.9 8.6 8.9

178% 170% 3%

Ebitda Ebitda Ebitda

Yr on Yr Qtr on Qtr Sequential

Yr on Yr Qtr on Qtr Sequential

Revenues Revenues Revenues

5 Oct 1012

Dram – Market evolution – Value & Volume

0

5

10

15

20

25

30

35

40

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

B$

0

5

10

15

20

25

30

35

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

BU

- 28 19 50 18 -1 26 12 27 19 3

High volatility

Significant swings

No substantial growth

Continuous growth

Year on year > 20%

Need for 14BU capacity in

2014

(*) Our Suzhou factory has a capacity for about 300 MU/Yr

Market Value – B$ Market Volume - BU

Source : Gartner 2010

5 Oct 1013

Dram – EEMS China Versus Market - History

0

5

10

15

20

25

30

35

40

2005 2006 2007 2008 2009

B$

0

2

4

6

8

10

12

14

16

2005 2006 2007 2008 2009

BU

0

20

40

60

80

100

120

140

2005 2006 2007 2008 2009

M$

0

50

100

150

200

250

300

350

2005 2006 2007 2008 2009

MU

Market Value

EEMS China Revenues EEMS China Volume

Market Volume

Sometime anti cyclical

Following and exceeding market volume

2009 affected by Qimonda default

Source : Gartner 2010 and Company data

5 Oct 1014

Dram – Market Share – B Units

2008 2009 2010 2011 Rank 2010

Elite B Units 0.2 0.2 0.2 0.2

Elpida B Units 2.1 2.4 3.1 3.9 3

Etron B Units 0.2 0.2 0.2 0.2

Hynix B Units 3.1 3.3 4.0 4.5 2

Iss B Units 0.1 0.1 0.1 0.2

Micron B Units 1.0 1.4 2.0 2.3 4

Nanya B Units 0.7 0.8 0.9 1.1 5

Oki B Units 0.1 0.1 0.0 0.0

Powerchip B Units 0.6 0.4 0.8 1.1 6

Promos B Units 0.9 0.4 0.4 0.3

Qimonda B Units 1.5 0.1 0.0 0.0

Samsung B Units 3.3 3.8 5.1 6.0 1

Toshiba B Units 0.0 0.0 0.0 0.0

Winbond B Units 0.2 0.5 0.6 0.5

All Others B Units 0.2 0.2 0.2 0.2

Totale B Units 14.2 14.0 17.6 20.6 15.9 Top 6

90.3%

Source : Gartner 2010

Our current customers

5 Oct 1015

Dram – Top 6 Dram manufacturers by volume – Who is outsourcing ?

♦ Samsung

♦ Hynix

♦ Elpida

♦ Micron

♦ Nanya

♦ Powerchip

Total

EEMS estimated volume

EEMS estimated penetration %

1

2

3

4

5

6

5.1

4.0

3.1

2.0

.9

.8

15.9

.3

1.9

Rank BU

Estimated% Outsourcing

-

1.1

3.1

.5

.9

.8

6.4

.3

4.7

BU

Outsourced

In house

Captive subcontractors network

Source : Gartner 2010 and Company estimates

5 Oct 1016

Dram – Market Share – B Units – Our Customers

Source : Gartner 2010

♦ Our customers own 18% of total Dram market

♦ Our customers will grow by 2.5 B units by 2014

♦ DDR3 products with higher density should increase our value added

2010 2011 2012 2013 2014

Micron B Units 2.0 2.3 3.0 3.5 3.6

Nanya B Units 0.9 1.1 1.4 1.7 1.8

Etron B Units 0.2 0.2 0.2 0.2 0.2

Total B Units 3.1 3.6 4.6 5.5 5.6

Total Market B Units 17.6 19.7 25.0 29.7 30.6

Share % 18% 18% 18% 18% 18%

5 Oct 1017

Dram – Market Share – B Units – Additional Potential Opportunities

♦ Two key Dram players make 40% of market

♦ Elpida is said to be planning a new wafer fab close to EEMS factories in China

♦ Hynix has already a wafer fab near by the EEMS factories and is considering to grow its outsourcing

Source : Gartner 2010

2010 2011 2012 2013 2014

Elpida B Units 3.1 3.9 5.0 5.9 6.1

Hynix B Units 4.0 4.5 5.8 6.8 7.0

Total B Units 7.0 8.5 10.8 12.8 13.2

Total Market B Units 17.6 19.7 25.0 29.7 30.6

Share % 40% 43% 43% 43% 43%

5 Oct 1018

Dram Business - Summary

Dram volume continuously and significantly growing

EEMS well positioned logistically in China

State of the art technology available

Already fully operational on DDR3 technology

Opportunity to increase capacity on marginal Capex

Generating Ebitda margin from 25% to 35%

5 Oct 1019

Photovoltaic

5 Oct 1020

BoomingBooming marketmarket

From Semiconductor to PV in Italy - Natural development

IndustrialIndustrial strenghtstrenght

♦ Strong industrial background

♦ Used to face high tech challenges

♦ Well established “silicon culture”

♦ Leveraging on EEMS existing assets

♦ Building on an educated work force

♦ Sky-rocketing demand

♦ High sun hours

♦ Increasing green awareness

♦ PV prices close to Grid parity

♦ Best feed in tariff in Europe

5 Oct 1021

PV business – Italian PV market: Trend

Cumulated PV power(MW)

# PVinstallations

Note: Data from GSE report

So far a fast growing market …

30,3687,678 63,742 ~130,000

Tot Power1,600 MW@ Sept 2010

Tot Installations100,200@ Sept 2010

408

1,057

2,200

80

2007 2008 2009 2010

5 Oct 1022

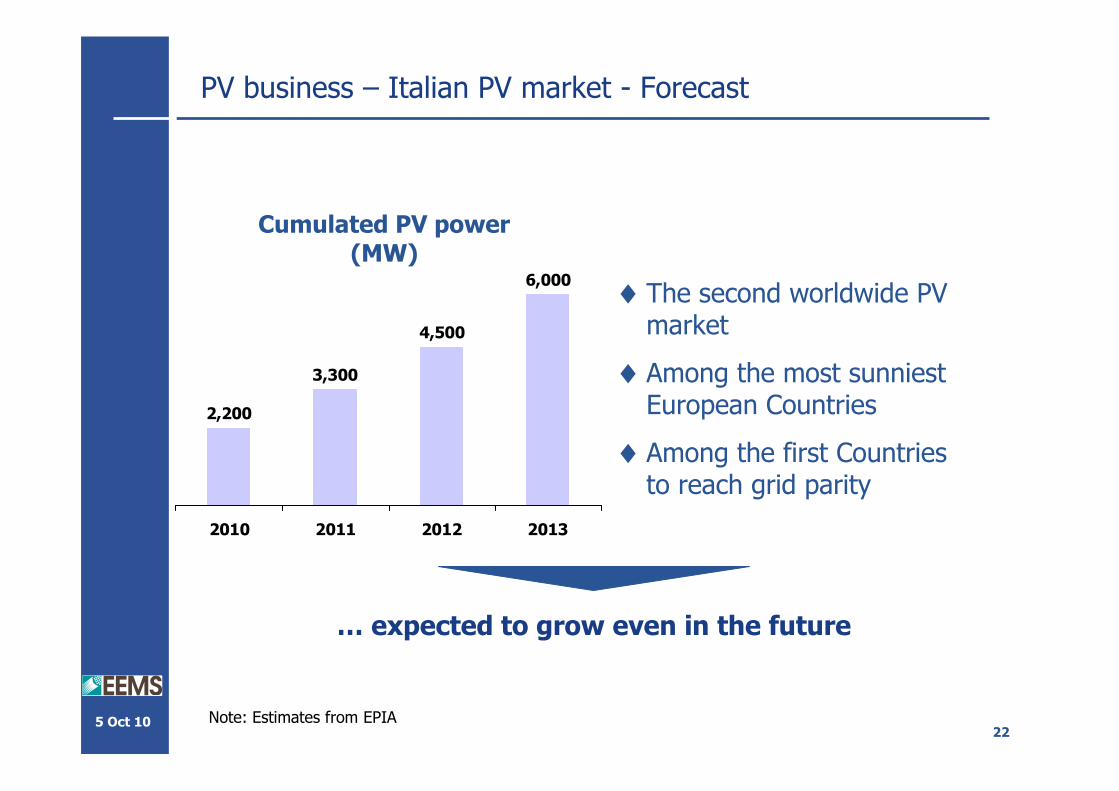

PV business – Italian PV market - Forecast

Cumulated PV power(MW)

Note: Estimates from EPIA

3,300

4,500

6,000

2,200

2010 2011 2012 2013

♦ The second worldwide PV market

♦ Among the most sunniest European Countries

♦ Among the first Countries to reach grid parity

… expected to grow even in the future

5 Oct 1023

PV business – Italian PV market - New opportunities

Note: Data from GSE Report

In addition:

♦ 56 Millions population

♦ 20 Millions houses

♦ 2 Millions firms

Rooftop installations

Total Available Market

100 GW (estimate)

… with a major opportunity in rooftop installations for residential and small business

Share of PVinstallations

5 Oct 1024

Solsonica – Achievements

Solsonica achieved the following objectives :

1. Completion of the industrial turnaround from DRAM to photovoltaic cells and module manufacturing

2. The planned cell and module lines are up and running achieving state of the art manufacturing

3. Established as one of the major Italian PV manufacturers achieving an increasing market share in the Italian market

4. Gaining reputation among Italian key customersdelivering high performing products and a total quality service

5 Oct 1025

Solsonica – Strategy

Improve cost competitiveness through value chain integration, excellence in manufacturing process and a better economy of scale

Leadership in the segment of residential and small/medium business rooftop installations

Consolidate positioning in the Italian market and expand toward new geographic areas

Strategic partnership across the value chain to consolidate and expand business

1.

2.

3.

4.

Solsonica strategy is based on four key elements

5 Oct 1026

Solsonica – Our new vision

A complete and truly distinctive turn key system for residential customers and small industries based on:

• Guarantee the economic return

• Distinctive and performing product features

• Energy monitoring and after sales services

• Easy and industrialized installation

An aggressive approach to sales based on:

• The set up of a network model for sales and installations

• New location in Milan to be closer to the core market

• New managers hired with strong marketing expertise

• Strategic partnership to fuel the project pipeline

To become the Leader in PV solutions for residential and small businesses

5 Oct 1027

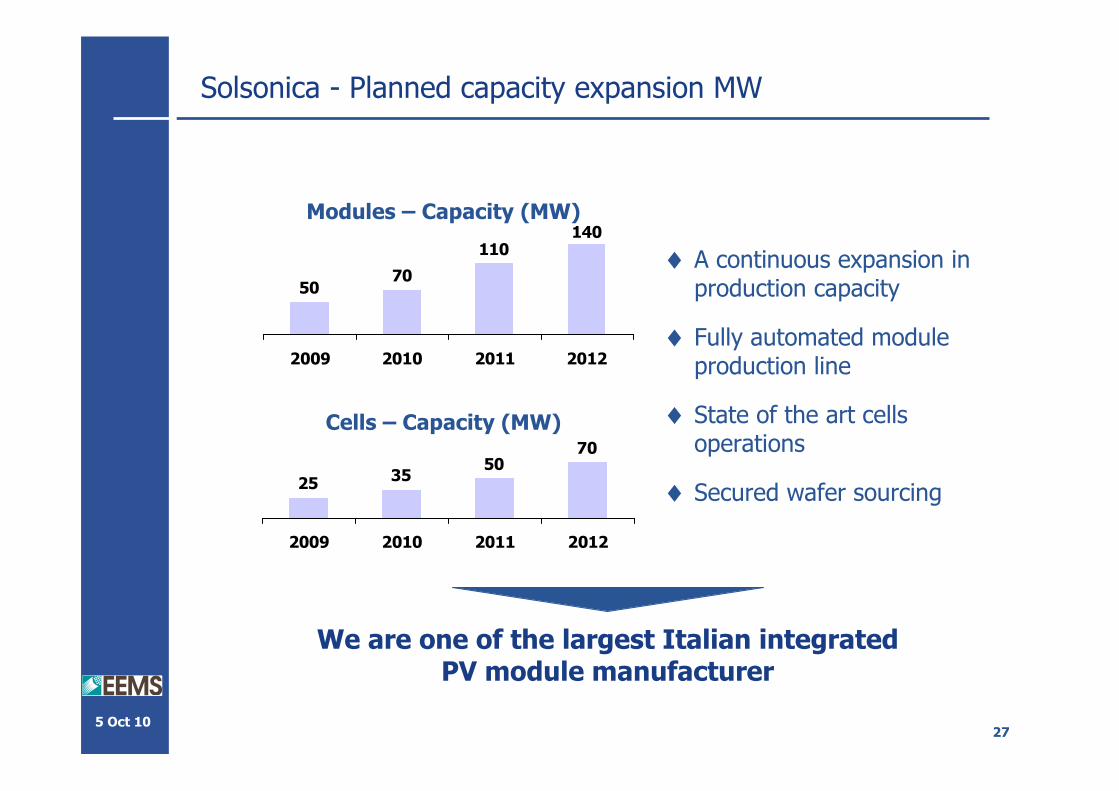

Solsonica - Planned capacity expansion MW

70

110140

50

2009 2010 2011 2012

Modules – Capacity (MW)

♦ A continuous expansion in production capacity

♦ Fully automated module production line

♦ State of the art cells operations

♦ Secured wafer sourcing35

5070

25

2009 2010 2011 2012

Cells – Capacity (MW)

We are one of the largest Italian integrated PV module manufacturer

5 Oct 1028

Solsonica - Financials M€

37

100

19

2008 2009 2010 E

Revenues (M€)

Continuous growth in revenues

5 Oct 1029

Solsonica - Summary

A path to grow ….

A market in constant expansion

New opportunities in rooftop installations

Extremely well positioned in the Italian market

An excellent product well perceived by the market

… and a vision to attain

Leadership in PV solutions to residential and small/medium enterprises

5 Oct 1030

Group Financial Projections

5 Oct 1031

EEMS Group (*) Consolidated - Projections M€

♦ Revenues

♦ Ebitda

♦ Ebit

♦ NFP

133.5

25.5

-14.5

80.9

99.5

25.3

3.8

86.8

200 - 210

41 - 43

5 - 7

41 - 43

2009Actual

20101st Half

2010 YearGuidance

♦ Hitting barrier of 200 M€ revenues

♦ Return to black

♦ Approaching to halve NFP

(*) Including 7 months of EEMS Test financials