stargazing: the effect of superstar ceos on competitors

TRANSCRIPT

1

Stargazing: The Effect of Superstar CEOs on Competitors’ Behavior

Anna Bergman Brown

School of Business

University of Connecticut

Viktoriya Zotova

R.H. Smith School of Business

University of Maryland

Emanuel Zur

R.H. Smith School of Business

University of Maryland

February 2018

2

Stargazing: The Effect of Superstar CEOs on Competitors’ Behavior

Abstract

U.S. corporate CEOs are rewarded by the media through a superstar system, whereby few CEOs

reap the majority of media awards and attention. Prior literature documents that the corporate

superstar system has a negative impact on the shareholders of superstar CEO firms, as superstar

CEOs tend to shift their focus toward lucrative personal interests after winning awards. This

study examines the effects of the corporate superstar system on competitors of superstar CEOs.

Consistent with social psychology’s upward social comparison theory, we document that

competing CEOs exhibit a more optimistic tone in conference calls and are more likely to

overinvest after superstar CEOs win awards. In addition, after superstar CEOs win awards,

competing CEOs engage in behaviors likely to attract media attention and/or temporarily boost

stock prices, to the detriment of long-term shareholder value. The results are strongest for CEOs

who share the most connections with superstar CEOs, and are weakest for firms with strong

corporate governance. Our findings provide new evidence of the costs to shareholders of a

competitive media-driven system of rewarding CEOs.

1

1. Introduction

Social comparison theory proposes that people tend to compare themselves to peers who

slightly outperform them. When comparing themselves to higher-performing peers (“upward

comparison”), people often group themselves in the same category as the higher-performing peer;

therefore considering themselves to be “almost as good” as the higher performer (Wheeler 1966).

In this way, upward comparison frequently results in improved self-evaluations, as people believe

themselves to be close to reaching the same level of achievement as the higher-performing peer

(Collins 1996). Further, upward comparison often induces competitive behavior, where people

strive to reach the same level of achievements as the higher-performing peer. Looking at how

CEOs react to competing CEOs receiving prestigious media-driven awards, we test these two

components of social comparison theory. Our empirical evidence suggests that CEOs react to

competing CEOs achieving superstar status by becoming more overconfident about their

performance as well as their firm’s performance and taking actions that likely harm shareholder

value.

First, we test whether CEOs react to competing CEOs achieving superstar status by

becoming more overconfident about their firm’s performance, consistent with upward comparison

leading to improved self-evaluation.1 We measure overconfidence using a proxy for managerial

optimism captured by the language tone in disclosures: a growing stream of literature finds that

managers’ optimistic language in firm disclosures is used to subtly convey value-relevant

information about future firm performance (Demers and Vega 2011; Davis et al. 2012; Price et al.

1 We use the term overconfidence to refer to a cognitive bias that leads to unrealistic positive beliefs about the

distribution of an uncertain outcome. We use the term optimism to refer to the degree of positive versus negative

language used in firm disclosures. Finance and accounting literature frequently uses the term overconfidence

interchangeably with optimism or optimistic bias (Ben-David et al. 2007; Schrand and Zechman 2012; Ahmed and

Duellman 2013; Davis et al. 2015).

2

2012; Demers and Vega 2014; Davis et al. 2015; Baginski et al. 2016). If CEOs react to competitor

CEOs achieving superstar status by becoming more overconfident about their firm’s performance

(because they are more optimistic about their own chances of winning an award), their disclosures

will be more optimistic after competitor CEOs win prestigious awards that elevate them to

superstar status. Further, we test for changes in CEO overconfidence using changes in the level of

industry-adjusted excess investment: overconfident CEOs tend to overinvest on average, because

they overestimate the cash flows and underestimate the risks associated with projects (Ben-David

et al. 2007; Schrand and Zechman 2012). If CEOs are more confident about their chances of

winning an award after competitor CEOs win awards, they will likely be overly confident about

the potential positive payoffs associated with investments.

We follow prior literature to construct a sample of shocks to CEOs’ status through a major

media award in order to proxy for the date that superstar CEOs “achieve” superstar status

(Malmendier and Tate 2009; Ammann et al. 2016). We examine changes in CEO tone in

conference calls for competitor vs. control firms (Bushee et al. 2011; Price et al. 2012; Brochet et

al. 2016; Levy et al. 2017) in a difference-in-differences analysis (hereafter, DID) using a sample

of the competitors of the superstar CEO firms and propensity score matched non-competitor

control firms, for the periods before and after superstar CEOs achieve superstar status (hereafter,

the “pre-award” and “post-award” periods).2 In a sample of conference call data for the four

quarters pre-award and post-award, we document that competitor CEOs employ a more optimistic

tone in conferences calls (measured using the number of optimistic vs. pessimistic words, as well

as the total number of words) compared to the changes for control firms over the same period. We

2 We propensity score match competitor CEO firms to non-competitor control firms based on the likelihood of

winning an award, which should control for the possibility that results are driven based on the likelihood of winning

an award, and not being a competitor of a superstar CEO (Ammann et al. 2016).

3

further show that competitor CEOs have a higher level of overinvestment post-award (measured

using industry-adjusted excess investments one year pre-award and post-award) compared to the

changes for control firms over the same period. The results are consistent with competitor CEOs

reacting to superstar CEOs winning awards with an improved self-evaluation and greater

confidence about their own chances of winning an award.

Next, we examine whether CEOs react competitively to peer CEOs achieving superstar

status by striving to win an award for themselves, and whether this competitive behavior is

beneficial or harmful to shareholder value. When CEOs achieve superstar status through

prestigious media awards, competitor CEOs may view themselves as being “almost as good” as

the superstar CEO and, therefore, close to winning an award. The competitor CEOs may therefore

try to achieve the same level of accomplishments and recognition as the superstar CEO through

competitive behaviors that are likely to improve their chances of winning an award.

Using a DID approach comparing competitor to control firms, pre- versus post-award, we

examine several mechanisms through which CEOs may increase their chances of winning an

award. Malmendier and Tate (2009) document that the stock returns in the 36 months leading up

to the award date are one of the primary predictors of winning an award; therefore, competitor

CEOs may engage in activities that are likely to increase firm stock returns, thus improving their

chances of winning an award. First, we examine changes in accounting choices, including changes

in accounting conservatism – measured using the firm-year conservatism measure from Khan and

Watts (2009) – and positive and negative disclosures – measured using the issuance of positive or

negative earnings guidance (i.e., earnings guidance or warning), following Levy et al. (2017).

Decreasing accounting conservatism and negative disclosures, and increasing positive disclosures

all likely provide a temporary boost in a firm’s stock price; however, manipulating the timing of

4

accounting recognition and disclosures to boost stock price is likely harmful to shareholder value

(Jin and Myers 2006; Chen et al. 2009).

Next, we examine changes in M&A activity and test whether CEOs engage in more

frequent and/or larger M&A transactions: successful M&A are likely to attract media attention,

enhance CEO social recognition, and increase long-term stock returns, and would therefore likely

increase a CEO’s chance of winning a media award. For this reason, overconfident CEOs may

engage in more/larger M&A because they are overconfident about the likelihood that investments

in M&A will yield positive payoffs and attract media attention. We further examine the quality of

M&A deals post-award versus pre-award to test whether CEOs are engaging in M&A that build

value for shareholders or are value-destroying: analyzing the change in the quality of M&A deals

post-award versus pre-award allows us to directly test the effect of competitor CEO activities on

shareholder value.

We document that both accounting conservatism and negative disclosures decrease at

competitor firms post-award, while positive disclosures increase, compared to the change for

control firms over the same period. Collectively, these results are consistent with competitor CEO

firms engaging in manipulation of accounting recognition and disclosures that may temporarily

boost stock price, but will likely harm long-term shareholder value. Next, we document that

competitor CEO firms increase both the number and size of M&A deals post-award and pay a

higher premium for targets: this behavior is consistent with competitor CEOs being overconfident

about the likelihood that an M&A deal will be successful, and therefore lead to positive returns,

improved social recognition, and media attention. However, we find that M&A deals for

competitor firms have lower abnormal returns around the M&A announcement date in the post-

award period, compared to control firms. This suggests that while competitor CEOs are trying to

5

improve their chances of winning an award by engaging in more frequent and visible M&A, the

M&A are relatively more value-destroying for shareholders.

The next set of tests examine whether our results on CEO behaviors are mitigated by strong

corporate governance. We expect that firms with strong corporate governance may reign in CEOs’

value-destroying activities in the interest of shareholder value. Consistent with this prediction, we

find that in the post-award period, competitor CEO firms with weak (strong) corporate governance:

decrease accounting conservatism more (less), are less (more) likely to disclose bad news and more

(less) likely to disclose good news, complete more (fewer) M&A deals and of a larger (smaller)

amount, pay higher (lower) deal premiums, and have lower (higher) M&A announcement returns.3

In robustness tests, we examine the effects of upward comparison on competitor CEO

behavior using several additional cross-sectional analyses. First, we test whether our results are

strongest for CEOs who perceive themselves to be similar to the superstar CEO. Collins (1996)

argues that a person’s perceived similarity with a higher-achieving peer makes them more likely

to believe that they are in the “same group” as the higher achiever because they minimize the

significance of the differences in achievement between themselves and the higher achiever.4

Therefore, competitor CEOs who perceive themselves to be more similar to the superstar CEO

may be especially overconfident and competitive about their chances of winning an award. We

document that our results are strongest for firms where the CEOs have more connections with the

superstar CEO (measured using shared board seats), as well as firms that are closer competitors to

the superstar CEO firms (defined using the Hoberg and Phillips (2010, 2016) measure), consistent

3 We find no significant differences in CEO tone or overinvestments across firms with weak versus strong corporate

governance. This suggests that, on average, competitor CEOs are more overconfident about their chances of winning

an award after superstar CEOs win awards; however, our results show that competitor CEOs from firms with weak

corporate governance are more likely to engage in value-destroying activities to boost firm stock price. 4 In experiments, psychologists manipulate the condition of perceived similarity in a variety of ways, for example,

by telling subjects that they share a common birthday (Brown, Novick, Lord, and Richards 1992) or a common

group membership (Brewer and Weber 1994) with the higher achiever.

6

with these CEOs perceiving themselves to be more similar to the superstar, and, therefore, closer

to winning an award. We further document that our results are strongest for competitor CEOs who

are more likely to win an award, using the propensity score from a logit model predicting award

winners (Malmendier and Tate 2009). Overall these results provide additional evidence that our

findings are likely to be driven by changes in CEO behavior attributable to upward comparison.

Finally, we perform a falsification test examining changes in CFO tone and total words

used in conference calls at competitor versus control firms. This test allows us to isolate optimism

related to actual firm fundamentals – which should affect both CEO and CFO tone – from optimism

attributable to superstar awards – which should only affect CEO tone (Li et al. 2014). We find that

our results on tone and total words do not hold using changes in CFO tone, consistent with our

results being driven by changes in CEO optimism due to superstar awards, and not changes in firm

fundamentals.

Our results make several important contributions to the literature. First, we contribute to

the recent literature on superstar CEOs and their competitors. While the CEO is meant to serve

shareholders’ best interests, the superstar system is largely media-driven, and therefore

independent of shareholders. It is therefore important to note that this media-driven system could

negatively impact not only shareholders of firms for the few CEOs winning prestigious awards

(Malmendier and Tate 2009), but also, more broadly, the shareholders of their competitors. Next,

our results complement prior studies on the effects of the superstar system on competitor CEOs

(Ammann et al. 2016; Shi et al. 2017). Ammann et al. (2016) document positive long-term

abnormal stock returns (over one to three years) at competitor CEO firms when superstars win

awards, driven by competitor firms with strong corporate governance. The authors conclude that

the superstar system is in fact beneficial to shareholders, because it induces competitive behavior

7

at peer firms. Our empirical findings as a whole do not contradict the findings in Ammann et al.

(2016): our results for competitor CEO activities are strongest for firms with weak corporate

governance, a setting where Ammann et al. (2016) do not find results. However, our study suggests

that the corporate superstar system can have a negative effect on shareholders of competitor CEO

firms, as competitor CEO firms, on average, engage in value-destroying activities in the post-

award period.

Further, our results provide empirical support for upward social comparison theory in the

setting of superstar CEOs and their competitors; we provide evidence consistent with CEOs

comparing themselves to higher-achieving peers and behaving competitively in order to try to

reach the same level of achievements. Finally, our results contribute to the literature on peer

networks: our results suggest that peer CEOs with more connections compete more with one

another.

The remainder of the paper is organized as follows. Section 2 discusses prior literature and

motivates our hypotheses. Section 3 describes our measures of overconfidence and stock price-

boosting activities and section 4 presents our sample selection and research design. Section 5

discusses descriptive statistics and empirical results, section 6 presents additional and robustness

analyses, and section 7 concludes.

2. Prior Literature and Hypothesis Development

2.1 Superstar CEOs

The superstar CEO system refers to a media-driven practice of rewarding few CEOs with

prestigious awards and attention, and turning these few CEOs into “superstars” or celebrities of

8

the media world (Malmendier and Tate 2009).5 For example, in 2003, Amazon’s Jeff Bezos was

named the “Best Performing CEO of the Year” by Forbes magazine. This was the first of multiple

media awards for Bezos, and therefore, 2003 arguably marks the year that Bezos was catapulted

to media celebrity status. Similarly, Apple’s Tim Cook won his first major media award in 2011 –

the year he took over the position of CEO from Steve Jobs – being named on Fortune’s list of

“Businessperson of the Year.” The first time a CEO receives a major media award is a significant

media event for this CEO, and often marks the beginning of an elevated level of media-driven

attention, interviews, and further awards.

Malmendier and Tate (2009) examine the media-driven superstar CEO phenomenon, and

document that the most significant determinants of “becoming a superstar,” that is, winning the

first major media award, are firm size and stock returns in the 36 months leading up to the award

date. Next, Malmendier and Tate (2009) find evidence that superstar CEO firms underperform

after the award date: stock returns and ROA are lower in the three years following the award,

compared to a matched sample of predicted award winners. Despite this underperformance, there

is an increase in both cash- and equity-based compensation for superstar CEOs after the award

date, compared to a matched sample. In addition, after winning prominent awards, superstar CEOs

write more books, join more external boards, and improve their golf handicaps, consistent with

more time spent on lucrative and leisure activities. Therefore, although the media tends to reward

CEOs for their strong performance prior to the award, the corporate superstar system is associated

with negative effects for shareholders of superstar firms.

A number of related studies examine further consequences of the corporate superstar

system. Carlin et al. (2010, 2010a) propose a model in which greater competition for attention and

5 The superstar system in general was first defined by Rosen (1981) as a system in which few players reap the

majority of income, market share, and/or public attention.

9

prizes makes discretionary disclosures less likely. One implication of this model is that a superstar

system, in which competition is high and few CEOs win awards, should have the effect of reducing

voluntary disclosures among award competitors. Kubick and Lockhart (2017) document that

superstar CEOs exhibit greater tax aggressiveness after winning prominent awards. Next, in

contrast to Malmendier and Tate (2009), two studies provide evidence that superstar CEO firms in

fact improve their performance after winning an award: Koh (2011) finds that superstar CEOs

become more conservative and are less likely to manage earnings after winning an award, while

Shemesh (2017) finds that superstar CEO firms reduce idiosyncratic volatility, reduce R&D

spending, and increase investments in fixes assets after the award.

In a related study examining the effect of superstar CEOs’ award winning on competing

CEOs, Ammann et al. (2016) document positive long-term abnormal stock returns for competing

firms (over one to three years) when superstars win awards; the results are driven by firms with

strong corporate governance. The authors conclude that competing CEOs have incentives to

perform better when superstars win prominent awards, which has a positive effect on shareholders

of competing firms. In a final set of analyses, the authors also find that in the three years following

the awards, competing firms have a higher standard deviation of returns, higher ROA and markup

on sales, and issue more patents.

Finally, Shi et al. (2017) also examine competitors of superstar CEOs, and find that

competitors increase the number and size of M&A transactions after the superstar wins an award.

In addition, the authors find that post-award acquisitions by competitors are associated with poorer

announcement returns and lower ROA after the acquisitions are completed. The authors conclude

that competing CEOs seek to achieve social recognition and status and/or visibility, similar to the

superstar CEOs.

10

2.2 Social Comparison Theory and Competitor CEOs

Social comparison theory originates from social psychology research on how people

compare their own performance with that of their peers. Upward comparison theory argues that

people tend to compare their own performance with that of a peer who slightly outperforms them,

and that such a comparison motivates people to perform better in order to assimilate to the higher-

performing peer (Wheeler 1966). Further, upward comparison often leads to an enhanced self-

image, as people tend to minimize the significance of the differences in achievement between

themselves and the higher-performing peer. An example using academics is illustrated by Collins

(1996), who asks the reader to imagine a researcher with a vita with 10 publications comparing

herself to a peer with a vita with 12 publications (holding constant the quality of the publications).

The researcher with 10 publications likely minimizes the significance of these two additional

publications and places herself in the same category as the higher-achieving peer. The researcher’s

self-assessment is therefore enhanced because through this comparison she has changed her self-

evaluation from someone with a vita with 10 publications, to someone in a group of people with

vitas with “10 or 12” publications.

Applied to the setting of superstar CEOs, upward social comparison theory predicts that

CEOs likely benchmark themselves against higher-performing peer CEOs. When superstar CEOs

win prestigious media awards, it is therefore likely that CEOs of competing firms may perceive

themselves to be “almost as good” as the superstar CEOs, and therefore, closer to winning an

award for themselves. In this way, competing CEOs will likely be overconfident about their own

firm’s performance, due to their improved self-evaluation. We therefore state our first hypothesis

as follows:

11

H1: Competitor CEOs experience an increase in overconfidence when superstar CEOs

receive prestigious media awards.

In addition, social comparison theory predicts that people react to upward comparison

through competitive behavior: because they perceive the accomplishments of the higher-achieving

peer as more accessible, or easier to achieve, people strive to reach the same level of

accomplishments by behaving competitively and/or assimilating to the higher-achieving peer’s

behavior (Wheeler 1966; Collins 1996).6 Following this theory, competitor CEOs likely react to

superstar CEOs achieving prestigious awards by trying to win an award for themselves through

competitive or assimilation behavior. Malmendier and Tate (2009) document that one of the

strongest predictors of winning an award are the stock returns in the 36 months leading up to the

award date. In addition, chances of winning an award should be higher when CEOs are engaging

in activities that enhance their social recognition, increase their firm’s visibility and attract media

attention. We therefore predict that competitor CEOs react to superstar CEOs achieving prestigious

awards by engaging in activities that are likely to boost stock prices and/or attract media attention.

We state our second hypothesis as follows:

H2: Competitor CEOs engage in activities that are likely to boost stock prices or attract

media attention when superstar CEOs receive prestigious media awards.

3. Measures of Overconfidence and Competitive Activities

3.1 Measures of Overconfidence

6 We use the term competitive behavior to refer to a person striving to reach the same level of accomplishments as a

higher-achieving peer. The term assimilation refers to directly emulating the higher achieving peer’s behavior, or, in

other words, doing what the higher achiever did to reach their level of accomplishments.

12

In order to measure CEO overconfidence, we use a measure of managerial optimism

captured by the language tone of disclosures, as well as a measure of industry-adjusted excess

investment. First, we measure managerial optimism as captured by the relative optimism of

language tone in quarterly earnings conference calls. Specifically, we use textual analysis to

calculate CEO_PosTone as the sum of optimistic words less the sum of pessimistic words spoken

by the CEO in the presentation section of each conference call, scaled by the total words spoken

by the CEO, following Loughran and McDonald (2011). Higher levels of CEO_PostTone therefore

reflect CEOs using relatively more optimistic versus pessimistic words during conference calls.

We also measure CEO_Words as the total number of words spoken by the CEO during the

presentation section of the conferences call, where using more words in total reflects a more

optimistic bias (DePaulo et al. 2003; Larcker and Zakolyukina 2012). Prior literature finds that

CEO optimism as measured by language tone reflects higher current and future performance, and

that the market reacts positively to optimistic tone (Davis et al. 2012; Price et al 2012; Demers and

Vega 2014). However, Davis et al. (2015) also find that optimistic tone is driven by a manager-

specific tendency to be optimistic versus pessimistic, consistent with tone optimism capturing a

managerial cognitive bias that reflects unrealistic positive beliefs about the distribution of an

uncertain outcome. If competitor CEOs are more overconfident about their firms’ performance

after superstars win awards, their overconfidence may be reflected in a more optimistic tone in

conference calls.

Next, we measure CEO overconfidence in investments using industry-adjusted excess

investments. Specifically, Over_Invest is an indicator variable equal to 1 if the residual of the

industry-year regression of total asset growth on sales growth is greater than zero, and 0 otherwise,

following Ahmed and Dullman (2013). Overconfident CEOs tend to overinvest, on average,

13

because they overestimate the positive cash flows and underestimate the risks associated with

investment projects (Ben-David et al. 2007; Schrand and Zechman 2012). If CEOs are more

overconfident about their firm’s performance after superstars win awards, we therefore predict that

they will be overly confident about the potential positive payoffs associated with investments.

3.2 Measures of Competitive Activities and the Effects on Shareholder Value

Our second hypothesis predicts that competitor CEOs will engage in competitive behavior

in order in increase their chances of winning an award after superstar CEOs win prominent awards.

These competitive activities may be activities likely to boost stock prices, enhance their social

recognition, increase their firm’s visibility and attract media attention. We first choose several

mechanisms through which CEOs may boost stock prices. First, we examine accounting

conservatism: C_Score is the firm-year measure of financial reporting conservatism estimated

following the model from Khan and Watts (2009). A higher value of C_Score reflects more

conservative financial reporting, defined as more timely recognition of losses versus gains.

Overconfident CEOs tend to report less conservatively, on average, because they are overconfident

about future returns, and therefore justify delaying loss recognition (or recognizing gains sooner)

on the basis that future returns will likely be higher (Ahmed and Duellman 2013). In addition,

decreasing accounting conservatism provides a temporary boost to stock prices, but likely harms

long-term shareholder value (Jin and Myers 2006; Chen et al. 2009). We therefore predict that if

competitor CEOs are more overconfident about their firm’s performance, they may report losses

on a less timely basis, therefore reporting less conservatively, on average, which should have a

negative effect on shareholder value.

Following this same argument, we use analysts’ forecasts and firms’ interim guidance to

measure positive and negative disclosures and predict that competitor CEOs will increase positive

14

disclosures and decrease negative disclosures if they are more overconfident after superstars win

prominent awards. We calculate Pos_Disclos (Neg_Disclos) for a subset of firms for which actual

earnings per share for period t exceeds (falls short of) analysts’ forecasts for period t that was

issued immediately after earnings announcement of period t-1. Next, we create an indicator

variable Pos_Disclos (Neg_Disclos) equal to 1 if the firm issues earnings guidance (warning) for

period t in the middle of period t, but before the earnings announcement of period t (and 0

otherwise). Pos_Disclos (Neg_Disclos) therefore captures cases where managers guide earnings

up (down) given a potential positive (negative) earnings surprise. Increasing positive disclosures

and decreasing negative disclosures likely provides a temporary boost to stock prices, but may

harm long-term shareholder value.

Finally, we measure M&A activity as a potential mechanism through which competitor

CEOs may seek to increase their chances of winning an award by attracting media attention and

enhancing CEO social recognition. First, contingent on H1, competitor CEOs are more likely to

be overly confident about the potential positive payoffs (and underestimate the potential risks)

associated with M&A investments. That is, if competitor CEOs are more overconfident post-

award, they will likely be overly confident about the potential success of M&A deals, and therefore

more likely to engage in M&A as an investment that will make their firm larger, and may boost

stock price. In addition, M&A deals likely lead to media attention and recognition; it is therefore

plausible that competitor CEOs engage in more and larger M&A deals as a means to attract media

attention and increase their chances of winning an award (Shi et al. 2017). We employ three

measures of the frequency and size of M&A deals: (1) Deal_Number measures the total number

of acquisitions of at least 50% of the target’s shares that were announced and completed; (2)

Deal_Value captures the total value (in $ Millions) of all acquisitions of at least 50% of the target’s

15

shares that were announced and completed; and (3) Deal_Prem measures the total value of all

premiums paid for acquisitions of at least 50% of the target’s shares that were announced and

completed, where the premium is calculated as the deal value, less the product of the target firm’s

equity value 42 days before the announcement and the % of the stock bought in the deal.

Last, we measure market-adjusted announcement returns in order to assess the effect of

M&A activity on shareholder value. If competitor CEOs are overconfident about the likely success

of M&A deals, and increase M&A activity in the post-award period, it may be that these deals are

relatively more value-destroying for shareholders, which would typically be reflected by lower

deal announcement returns. Ann_Returns measures the acquirer’s cumulative market adjusted

return over the three-day period (-1, +1), where day 0 is the merger announcement date.

4. Sample Selection and Research Design

4.1 Sample Selection

The sample originates from a list of 539 CEOs who won national media awards published

between 1996 to 2014.7 Business Week and Financial World are the two main publications that

granted awards to CEOs during the sample period. Other publications include Forbes, Chief

Executive, Harvard Business Review, Morningstar, Fortune, and Industry Week. Since some CEOs

receive multiple awards over multiple years, we only consider a superstar CEO’s first award – the

first award date therefore proxies for the date that the superstar is first elevated to celebrity status.

We also restrict our analysis to CEOs in the BoardEx universe. A total of 363 superstar CEOs are

included in our final sample of superstar CEOs.

7 We limit our sample to 1996-2013 because the Hoberg and Gordon (2016) database only covers the period

between 1996 and 2013.

16

Next, to identify the competitor CEOs for each superstar CEO, we use the Hoberg-Phillips

Text-based Network Industry Classification (TNIC-3), which builds on firms’ business and

product descriptions in 10-K annual filings, instead of the three-digit SIC grouping, to provide a

firm-by-firm similarity measure. The level of competitiveness between two firms is measured by

the relative number of words in common in the product description sections in the 10-k. A detailed

explanation of the TNIC-3 data can be found in Hoberg and Phillips (2010, 2016). We follow

Hoberg and Phillips (2016) and use a 21.32% threshold to define competitors. This procedure

yields a sample of the 1,857 competitors of the superstar CEO firms, or approximately five

competitors per superstar CEO (ranging from one to nine competitors). Finally, we construct a

sample of matched control firms using the propensity score from a logit model predicting award

winners (Malmendier and Tate 2009). For each of the 1,857 competitors of the superstar CEO

firms we choose, without replacement, another CEO who is not a direct competitor to the superstar

CEO, and has the propensity score closest to the score of the competitor CEO.

4.2 Research Design

Our empirical analyses are designed to test whether competitor CEOs react to superstar

CEOs winning awards with an improved self-evaluation and greater confidence about their own

chances of winning an award. To that end, we employ a DID approach comparing competitor CEO

firms to control firms, before and after the superstar CEO wins an award. We define the treatment

group as the sample of competitor CEO firms and the control group as the sample of matched

control firms. We expect CEOs in our treatment group to be influenced by the superstar CEO’s

win of a prestigious media award, and therefore experience an increase in overconfidence about

their firms’ performance in the year following the award. However, we do not expect the media

award to affect the CEOs and firms in the control group, as these CEOs are not direct competitors

17

of the superstar firms, and therefore are less likely to benchmark themselves against the superstar

CEOs. The basic regression we use in the analyses is as follows:

DEP_VARi,t = β0 + β1Posti,t + β2Competitori,t + β3Posti,t × Competitori,t

+ βControlsi,t + γt+λi+εi,t, (1)

where DEP_VAR is the dependent variable in each analysis. The dependent variables, which we

describe in detail in section 3, pertain to the measures of overconfidence and competitor firm

activities that we focus on in this study: the speech tone of the CEO (CEOPos_Tone and

CEO_Words), excess investments decision (Over_Invest), firms’ financial reporting conservatism

(C_Score), the provision of early disclosure of negative and positive news (Pos_Disclos and

Neg_Disclos), and merger and acquisition transactions (Deal_Number, Deal_Value, Deal_Prem,

and Ann_Returns).

Post is an indicator variable equal to one for the fiscal year(s) after the superstar CEO wins

a media award and zero otherwise. Competitor is an indicator variable equal to one for treatment

firms and zero for control firms. Post × Competitor is the variable of interest, an interaction

between the above-described variables. The interaction term Post x Competitor allows us to test

the difference in the change in the dependent variable across treatment and control samples. We

use the interaction of these variables throughout our analyses as the main explanatory variable.

We include the following variables to control for other firm characteristics that could

potentially affect CEO behavior and accounting and financial decisions: Log_MV, MTB, ROA,

Earnings_Growth, and Sales_Growth. In our tests using an M&A setting, we also control for the

following deal characteristics: RelativeSize, TargetPublic, TenderOffer, StockPercentage, and

Toehold (see Appendix A for variable definition).

18

Our analyses also include year and firm fixed effects. We chose to include firm fixed effects

to better gauge within-firm changes. Including firm and year fixed effects, however, renders

interpretation of the main effect in the analyses (Post and Competitor) meaningless. Therefore, we

ignore the main effects when reporting results. Finally, we calculate standard errors clustered by

firm and superstar CEO award.

5. Descriptive Statistics and Empirical Results

5.1 Descriptive Statistics

Table 1, Panel A, presents the descriptive statistics (mean, median and standard deviation)

for the dependent and independent variables for the full sample. The final sample consists of 1,857

competitors of the superstar CEO firms and a matched control sample of 1,857 non-competitor

control firms. To minimize the impact of outliers, we winsorize all variables at the 1st and 99th

percentile values.

We first examine the CEO overconfidence characteristics. As displayed in Panel A, a CEO

speaks an average of 1,497 words during conference calls (CEO_Words), and the CEO’s tone

during the conference call (CEO_PosTone) is slightly more positive than negative with

approximately 1.5 percent more positive words used by the CEO during the conference call than

negative ones. We also find that approximately 41 percent of the firms in our sample overinvest,

comparable to Schrand and Zechman (2012) and Ahmed and Dullman (2013). Next, we present

the disclosure characteristics of our sample. C_Score, Pos_Disclos and Neg_Disclos – measures

of conservatism and early disclosure of good and bad news – have mean values of 0.121, 0.158,

and 0.207, respectively; the values are comparable to Levy et al. (2017). We also describe the

acquisition activity in the one year before and after the competitor CEOs win prestigious awards

19

that elevate them to superstar status. Deal_Number is the total number of majority-ownership

acquisitions in a year announced in our sample and which will subsequently be completed, and

range from zero for firms that did not engage in any acquisition in the year to three deals at the

maximum. The firms in our sample announced an average of 0.415 majority-ownership

acquisitions in a year (and total of 3,083 deals during the period sample). The average total value

of these acquisition in a year is approximately 20 million dollars. The average total premium paid

by the firms in our sample each year for the acquisitions (Deal_Prem) is 13.5 percent. The acquirer

cumulative market-adjusted return over the three days spanning the deal announcement

(Ann_Returns) for the sample of 3,083 acquisitions is -2.24 percent, on average. Finally, Panel A

also provides the descriptive statistics for all the different control variables for our sample.

Table 1, Panel B, reports correlation coefficients between our variable pairs. The

correlation analyses demonstrate that most of the correlations are less than 0.5, which is

considerably less than the 0.8 threshold that would suggest multicollinearity (Gujarati 2003).

5.2 Empirical Results

Table 2 presents our tests of H1, the effect of superstars winning prestigious awards on the

overconfidence/optimism of competitor CEOs. Columns (1), (2), and (3) present regressions where

the dependent variables are CEO_PosTone, CEO_Words, and Over_Invest, respectively. The

independent variable of interest is the interaction term Competitor x Post, which indicates the

effect of the change in the dependent variable for competitors from the pre- to post-award periods,

compared to the change for control firms over the same period.8 In each of columns (1) through

(3), the coefficient on Competitor x Post is positive and significant: competitor CEOs employ a

more positive tone, use more words, and are more likely to overinvest in the post-award period,

8 Because our regressions include year and firm fixed effects, the coefficients on the standalone terms Post and

Competitor simply absorb the omitted year/firm term, and therefore cannot be interpreted meaningfully.

20

compared to the change for control firms over the same period. We also estimate the economic

significance of the interaction term Competitor x Post coefficients. We find that competitor CEOs

increase the positive tone in the post period by 0.3 percent, which is approximately one-third of

one standard deviation, and increase by an average of six percent of the number of words spoken

in the post period. Moreover, we show that competitor CEOs in the post period, on average, are

associated with a 5.5 percentage increase in over investment, representing a 13.3 percent increase

in the respective unconditional mean of Over_Invest. We therefore provide evidence supporting

H1, that competitor CEOs are more overconfident about their firms’ performance after superstars

win prominent awards.

Tables 3 and 4 presents our tests of H2, the effect of superstars winning prestigious awards

on competitor CEO behavior. Columns (1), (2), and (3) of Table 3 present regressions where the

dependent variables are C_Score, Pos_Disclos, and Neg_Disclos, respectively. The independent

variable of interest in each regression is the interaction term Competitor x Post. In column (1), the

coefficient on Competitor x Post is negative (-0.058) and significant (t-stat of -3.81): competitor

CEO firms therefore report less conservatively in the post-award period, compared to the change

for control firms. In column (2) (column (3)), the coefficient on Competitor x Post is positive

(negative) and significant, consistent with competitor CEOs providing more positive and less

negative disclosures in the post-award period, compared to the change for control firms. We find

the competitor CEOs in the post period are associated with a 4.7 (7.3) percentage increase

(decrease) in positive (negative) disclosure, representing a 29 (35) percent increase (decrease) on

the respective unconditional mean Pos_Disclos (Neg_Disclos). Overall, the results in Table 3 are

consistent with competitor CEOs manipulating the timing of accounting recognition and

21

disclosures in a way that may boost the firm’s stock price in the post-award period, an activity

which is likely harmful to shareholder value (Jin and Myers 2006; Chen et al. 2009).

Table 4 presents our tests of mergers and acquisitions activity, where the dependent

variables in columns (1), (2), (3), and (4), are Deal_Number, Deal_Value, Deal_Premium, and

Ann_Returns, respectively. The first three columns test whether competitor CEOs engage in more

and larger M&A deals in the post-award period. The coefficients on Competitor x Post in columns

(1) through (3) are positive and significant: competitor CEOs engage in more M&A deals, larger

deals, and pay a larger premium in the post-award period. These results are consistent with

competitor CEOs being overconfident about the probability that the M&A deals will be successful

and attract positive media attention. However, in column (4), the coefficient on Competitor x Post

is negative and significant: competitor CEO firms’ M&A deals have lower abnormal

announcement returns in the post-award period, consistent with these deals being relatively more

value-destroying for shareholders. Overall, the results in Table 4 are consistent with competitor

CEOs engaging in more M&A activity in the post-award period; however, shareholders perceive

these deals to be relatively more value-destroying.

In Table 5, we test whether our results for H2 are mitigated by firms with strong corporate

governance. Tables 3 and 4 provide evidence consistent with competitor CEOs engaging in

activities in the post-award period that overconfident CEOs believe are likely to increase the

chances of winning an award; however, these activities come at the expense of long-term

shareholder value. We therefore predict that competitor CEO firms with weak corporate

governance will be relatively more likely to engage in such activities, while competitor CEO firms

with strong corporate governance will be more likely to reign in the CEOs’ value-destroying

activities. For these and all subsequent tests, we omit control firms, and instead examine cross-

22

sectional results for competitor firms only. First, in Panel A of Table 5, we compare accounting

choices for competitor firms with weaker corporate governance (HighG-Index=1) compared to

competitor firms with stronger corporate governance (HighG-Index=0). The coefficient on

HighG-Index x Post is negative in column (1): competitor CEO firms with weaker corporate

governance therefore decrease accounting conservatism more than firms with stronger corporate

governance, although the results are only marginally significant. The coefficient on the interaction

term is insignificant in column (2), but in column (3) it is negative and significant, consistent with

competitor CEO firms with weaker corporate governance decreasing negative disclosures more

than those with stronger corporate governance in the post-award period.

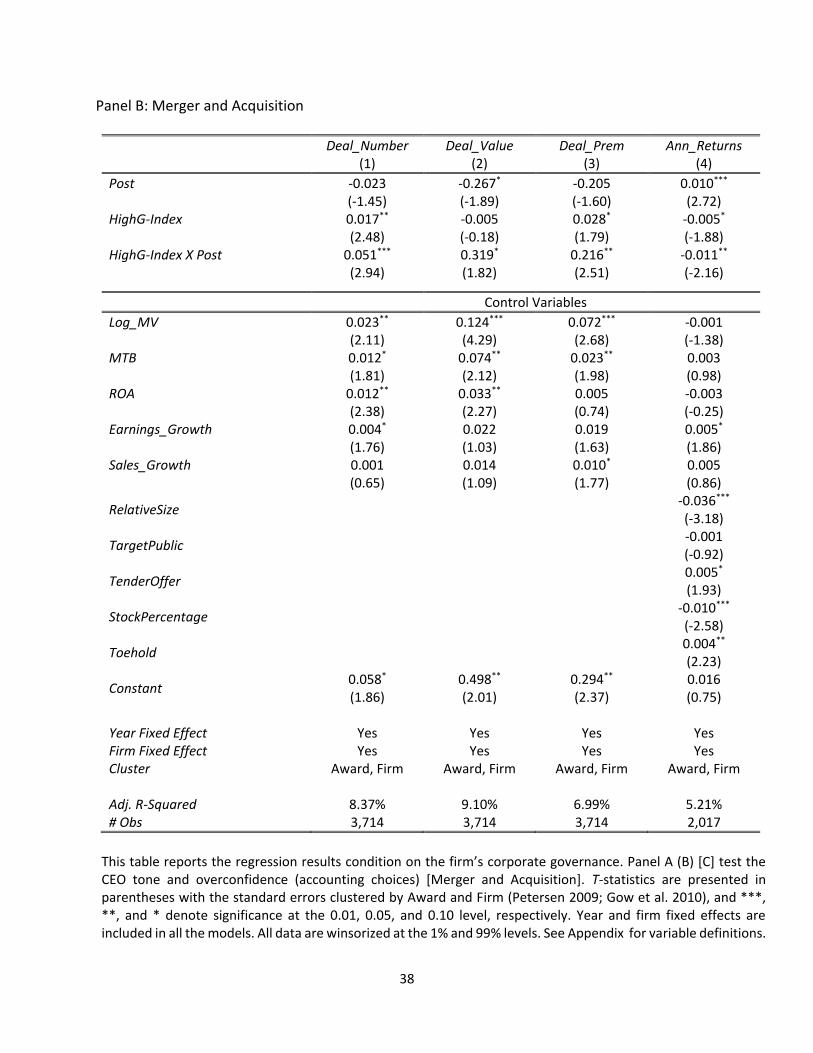

Next, in Panel B of Table 5, we test for the effects of competitor firms with weaker/stronger

corporate governance on M&A activity. We document that competitor CEO firms with weaker

corporate governance complete more M&A deals of a larger value and pay a higher premium, but

have lower announcement returns in the post-award period, compared to firms with stronger

corporate governance. Overall, the results in Table 5 support the prediction that competitor CEO

firms with weaker corporate governance engage in activities that are detrimental to shareholder

value; competitor CEO firms with stronger corporate governance are more likely to reign in CEOs’

value-destroying activities.

6. Additional Analyses and Falsification Test

6.1 Additional Analyses

In additional analyses, we test whether our results vary cross-sectionally across CEOs who

share more connections with the superstar or are more likely to win an award. Specifically, we

divide our sample of competitor CEOs at the median across three dimensions: (1) the level of

connections with the superstar CEO, defined using shared board seats between the competitor and

23

superstar firms (Cai and Sevilir 2012; Larcker, So, and Wang 2013); (2) whether the competitor

firm is the closest competitor with the superstar, defined using the Hoberg and Phillips (2010,

2016) text-based competitor classification; and (3) whether the competitor has a relatively higher

chance of winning an award, using the logit model predicting award winners from Malmendier

and Tate (2009).

In Table 6, we test our cross-sectional predictions for H1. We document that competitor

CEOs exhibit a more optimistic tone in conferences calls and are more likely to overinvest when

they share more connections with the superstar CEOs, are the closest competitors to superstar

CEOs (marginally significant), and are more likely to win awards. These findings provide

additional evidence that our primary results are driven by competitor CEOs engaging in upward

comparison with higher-achieving peers, and being driven by a desire to win an award.

Next, in Tables 7 and 8, we test our cross-sectional predictions for H2. In Table 7, we

document that competitor CEOs decrease accounting conservatism more when they are more

connected with the superstar CEO, or the closest competitor to the superstar CEO. In addition,

competitor CEOs increase (decrease) positive (negative) disclosures when they share more

connections with the superstar, are the closest competitor to the superstar, and have a higher chance

of winning an award. In Table 8, we similarly document that competitor CEOs increase the

number, size, and premium of M&A deals, but experience lower announcement returns, when they

share more connections with the superstar CEO, are the closest competitor to the superstar CEO,

and have a higher chance of winning an award. Overall, the results in Tables 7 and 8 provide

evidence that competitor CEOs are most likely to engage in activities they believe will boost stock

prices and/or attract media attention when they are a closer peer to the superstar, and when their

ex ante chances of winning an award are higher.

24

6.2 Falsification Test

Our results for CEO overconfidence/optimism document that CEOs employ a more

optimistic tone in earnings conference calls when their competitors win prestigious awards. We

propose that these results suggest an increase in CEO overconfidence, consistent with upward

social comparison leading to improved self-evaluation. However, one concern arising from these

analyses is that our results could be driven by shared characteristics of the competing firms, and

not a CEO’s personal overconfidence.

To address this concern, in Table 9, we test whether competitor firm CFOs also exhibit a

more optimistic tone in conference calls in the post-award period (Li et al. 2014). Competitor

CEOs and CFOs would likely share in any optimistic bias/overconfidence driven by firm

fundamentals; however, competitor CFOs should not share in the optimism/overconfidence driven

by CEOs’ personal biases and comparison to their peers. In Table 9, we document that competitor

CFOs do not exhibit a more optimistic tone/number of words in conference calls in the post-award

period, consistent with the primary results for H1 being driven by competitor CEOs’ improved

self-evaluation after upward comparison with superstars.

7. Conclusion

This study examines how CEOs react to competing CEOs winning prestigious media

awards. Social comparison theory proposes that people tend to compare themselves to higher-

performing peers (upward comparison); upward comparison often leads to improved self-

evaluation, because people think they are closer to reaching the same level of achievements as the

higher-performing peer. In addition, upward comparison often results in competitive/assimilation

behavior, where people strive to reach the same level of achievements as the higher-performing

peer. Applying social comparison theory to CEO behavior, we therefore predict that CEOs will

25

react to peer CEOs winning prestigious awards by becoming more overconfident and engaging in

activities likely to boost their chances of winning an award.

We conduct difference-in-differences analyses comparing a sample of firms with CEOs

who are competitors of superstar CEOs (“competitor CEOs”) to matched control firms, before and

after superstar CEOs first win prestigious media awards. We first document that competitor CEOs

employ a more optimistic tone in earnings conference calls after superstars win awards, compared

to the change for control firms. In addition, competitor CEOs are more likely to overinvest in the

post-award period, consistent with an increase in CEO overconfidence after peer CEOs win

awards. Next, in our test of competitive behaviors, we document that after superstar CEOs win

awards, competitor CEOs: (1) report less conservatively, (2) increase positive disclosures, (3)

decrease negative disclosures, (4) engage in more M&A, of a larger amount, and pay a higher

premium, and (5) experience lower M&A announcement returns. These activities all suggest that

overconfident competitor CEOs are engaging in activities likely to boost stock price and/or attract

media attention, and therefore increase their chances of winning an award. However, these

activities are value-destroying for shareholders. We find that our results are strongest (weakest)

for firms with weak (strong) corporate governance, consistent with firms with strong corporate

governance reigning in CEOs’ value-destroying activities. In additional analyses, we document

that our results are strongest when competitor CEOs share more board connections with the

superstar CEO, are closer competitors to the superstar CEO, and have a higher chance of winning

an award. In a falsification test, we document that competitor CFOs do not exhibit a more positive

tone in conference calls after superstars win awards, consistent with the primary results being

driven by CEO upward comparison, and not competitor firm characteristics.

26

This study makes several contributions to the literature. First, we complement Malmendier

and Tate’s (2009) findings that the media-driven corporate superstar system has a negative impact

on shareholders of superstar firms; we provide evidence that the superstar system also negatively

impacts the shareholders of competing firms. Next, our results provide empirical support for

upward social comparison theory among CEO: our findings suggest that CEOs compare

themselves to higher-performing peers, and strive to reach the same level of achievements as these

peers by engaging in activities that are likely detrimental to shareholders. Further, we contribute

to the literature on peer networks by documenting that CEOs react more to one another’s behavior

when they share more boardroom connections. Finally, we contribute to a limited literature on

competitors of superstar CEOs; in contrast to the findings of Amman et al. (2016), our results

suggest that shareholders of competitor firms are negatively impacted by the corporate superstar

system.

27

Appendix - Variable Definitions

Dependent Variables

CEO_PosTone The difference between the positive words and the negative words spoken by the CEO during the presentation section of the conference call, scaled by the total words spoken by the CEO during the presentation section. The positive and negative words are based on the list from Loughran and McDonald (2011).

CEO_Words Total number of words spoken by the CEO during the presentation section Over_Invest An indicator variable equals to 1 if the residual of regression of total asset

growth on sales growth run by industry-year is greater than zero, and 0 otherwise.

C_Score The firm-year conservatism measure estimated from the model by Khan and Watts (2009).

Pos_Disclos Potentially positive surprise—For the subset of firms for which actual earnings per share for period t exceeds analysts’ forecasts for period t that was issued immediately after earnings announcement of period t-1: Indicator variable equals to 1 if the firm issued earning guidance for period t in the middle of period t but before the earnings announcement of period t, and 0 otherwise.

Neg_Disclos Potentially negative surprise—For the subset of firms for which actual earnings per share for period t falls short of analysts’ forecasts for period t that was issued immediately after earnings announcement of period t-1, we create an indicator variable coded 1 if the firm issued earning guidance (warning) for period t in the middle of period t but before the earnings announcement of period t, and 0 otherwise.

Deal_Number The total number of acquisitions of at least 50% of the target’s shares which were announced in a year by each acquirer firm. If a firm did not engage in any acquisition during the year the total number of acquisitions is zero.

Deal_Value The total value of all the acquisition of at least 50% of the target’s shares which were announced in a year by each acquirer firm. If a firm did not engage in any acquisition during the year the total value of acquisitions is zero.

Deal_Prem The total value of all the premium paid for acquisitions which were announced in a year by each acquirer firm. If a firm did not engage in any acquisition during the year the total deal premium is zero. Premium is calculated as (Deal Value-(Target Equity Value 42 days before announcement* % of stock bought in the deal)).

Ann_Returns The acquirer cumulative market adjusted return over the three days spanning day -1 to day +1, where day 0 is the merger announcement date.

Variables of Interests

Post An indicator variable equals to 1 for the period post superstar award and 0 otherwise.

Competitor An indicator variable equals to 1 when the observation is superstar CEO competitor firm and 0 otherwise.

Connectedness The degree of connection between competitor’s board of directors and CEO superstar’s board of director from Cai and Sevilir (2012) and Larker, So, and

28

Wang (2013), which is measured as how easily or quickly a board can reach an outside board through interlocking directorates. For example if both firms share a common director the connectedness is equal 1, and if one director from the competitor and one director from the superstar CEO have been serving on the board of a third firm the connectedness is equal 2.

HighConnectedness An indicator variable equals to 1 when Connectedness is below the median value and 0 otherwise.

CloseCompetitor An indicator variable equals to 1 for the closest competitor for each superstar CEO (base on the text-bases competitor classification developed by Hoberg and Phillips (2010, 2016)) and 0 otherwise.

HigherChanceWin An indicator variable equals to 1 when competitor propensity score for probability of winning an award is above median and 0 otherwise.

G-Index The governance index developed by Gompers et al. (2003). HighG-Index An indicator variable equals to 1 when G-Index is above nine and 0 otherwise.

Control Variables

Log_MV Log market value of equity (COMPUSTAT CSHO×PRCC_F). MTB Market value of equity / book value of equity (COMPUSTAT

(CSHO×PRCC_F)/CEQ). ROA Return on assets (COMPUSTAT EBIT/AT). Earnings_Growth Change in earnings in quarter q relative to quarter q-4 scaled by total assets

(COMPUSTAT (IBQq-IBQq-4)/ATQ). Sales_Growth Growth in sales in quarter q relative to quarter q-4 (COMPUSTAT

SALESQq/SALESQq-4-1) RelativeSize The ratio of deal value over acquirers’ market value.

TargetPublic An indicator variable equals to 1 when the target is a public traded company and 0 otherwise.

TenderOffer An indicator variable that equals to 1 when the acquisition involves a tender offer and 0 otherwise.

StockPercentage The percentage of the transactions financed with common stock.

Toehold The percentage of target firm’s outstanding shares held by the bidder prior to the current deal.

Other Variables

CFO_PosTone The difference between the positive words and the negative words spoken by the CFO during the presentation section of the conference call, scaled by the total words spoken by the CFO during the presentation section. The positive and negative words are based on the list from Loughran and McDonald (2011).

CFO_Words Total number of words spoken by the CFO during the presentation section Rel_Words Relative words of CEO to CFO calculated as CEO_Words- CFO_Words. Rel_Tone Relative positive tone of CEO to CFO calculated as CEO_PosTone -

CFO_PosTone.

29

References

Ammann, M., Horsch, P., & Oesch, D. (2016). Competing with Superstars. Management Science,

62(10), 2842-2858.

Ahmed, A., & Duellman, S. (2013). Managerial overconfidence and accounting

conservatism. Journal of Accounting Research, 51(1), 1-30.

Baginski, S., Demers, E., Wang, C., & Yu, J. (2016). Contemporaneous verification of language:

Evidence from management earnings forecasts. Review of Accounting Studies, 21(1), 165-197.

Ben-David, I., Graham, J., & Harvey, C. (2007). Managerial overconfidence and corporate

policies (NBER working paper series, no. 13711). Cambridge, Mass.: National Bureau of

Economic Research.

Brewer, M. B., & Weber, J. G. (1994). Self-evaluation effects of interpersonal versus intergroup

social comparison. Journal of Personality and Social Psychology, 66(2), 268-75.

Brochet, F., Naranjo, P., & Yu, G. (2016). The capital market consequences of language barriers

in the conference calls of non-U.S. firms. The Accounting Review, 91(4), 1023-1049.

Brown, J., Novick, N., Lord, K., & Richards, J. (1992). When Gulliver travels: Social context,

psychological closeness, and self-appraisals. Journal of Personality and Social Psychology, 62(5),

717-727.

Bushee, B., Jung, M., & Miller, G. (2011). Conference presentations and the disclosure

milieu. Journal of Accounting Research, 49(5), 1163-1192.

Cai, Y., & Sevilir, M. (2012). Board connections and M&A transactions. Journal of Financial

Economics, 103(2), 327-349.

Carlin, B., Davies, S., & Iannaccone, A. (2010). Competing for attention in financial

markets (NBER working paper series, no. 16085). Cambridge, Mass.: National Bureau of

Economic Research.

Carlin, B. I., Davies, S., & Iannaccone, A. (2010). Competition and transparency in financial

markets. AFA 2012 Chicago Meetings Paper. Available at

SSRN: https://ssrn.com/abstract=1778262.

Chen, S., Chen, X., Cheng, Q., Hutton, A. (2009). Accounting conservatism and large

shareholders. Working Paper. University of Texas, Austin.

Collins, R. L. (1996). For better or worse: The impact of upward social comparison on self-

evaluations. Psychological Bulletin, 119(1), 51-69.

30

Davis, A. K., Piger, J. M., & Sedor, L. M. (2012). Beyond the Numbers: Measuring the Information

Content of Earnings Press Release Language. Contemporary Accounting Research, 29: 845–868.

Davis, A., Ge, W., Matsumoto, D., & Zhang, J. (2015). The effect of manager-specific optimism

on the tone of earnings conference calls. Review of Accounting Studies, 20(2), 639-673.

Demers, E., & Vega, C. (2011). Linguistic Tone in Earnings Announcements: News Or Noise?.

(INSEAD working paper series). Fontainebleau, France: INSEAD.

Demers, E., & Vega, C. (2014). Understanding the role of managerial optimism and uncertainty

in the price formation process: evidence from the textual content of earnings announcements.

Working paper, Univeristy of Virginia.

DePaulo, B., & Malone, B. (2003). Cues to deception. Psychological Bulletin, Vol. 129 No. 1 (ene.

2003), P74-118.

Gujarati, D.N. (2003). Basic Econometrics. New York: McGraw Hill Book Co.

Hoberg G., & Phillips, G. (2010) Product market synergies and competition in mergers and

acquisitions: A text-based analysis. Review of Financial Studies, 23(10):3773–3811.

Hoberg G., & Phillips, G. (2016). Text-based network industries and endogenous product

differentiation. Journal of Political Economy, 124(5), 1423-1465.

Jin, L. & Myers, S. (2004). R-squared around the world: New theory and new tests (NBER

working paper series, no. 10453). Cambridge, Mass.: National Bureau of Economic Research.

Khan, M., & Watts, R. L. (2009). Estimation and empirical properties of a firm-year measure of

accounting conservatism. Journal of accounting and Economics, 48(2-3), 132-150.

Koh, K. (2011). Value or glamour? An empirical investigation of the effect of celebrity CEOs on

financial reporting practices and firm performance. Accounting & Finance, 51(2), 517-547.

Kubick, T. R., & Lockhart, G. B. (2017). Overconfidence, CEO Awards, and Corporate Tax

Aggressiveness. Journal of Business Finance & Accounting, 44(5-6), 728-754.

Larcker, D. F., So, E. C., & Wang, C. C. (2013). Boardroom centrality and firm

performance. Journal of Accounting and Economics, 55(2-3), 225-250.

Larcker, D. F., & Zakolyukina, A. A. (2012). Detecting deceptive discussions in conference

calls. Journal of Accounting Research, 50(2), 495-540.

Levy, H., Shalev, R., & Zur, E. (2018). The effect of CFO personal litigation risk on firms’

disclosure and accounting choices. Contemporary Accounting Research, forthcoming.

31

Li, F., Minnis, M., Nagar, V., & Rajan, M. (2014). Knowledge, compensation, and firm value: An

empirical analysis of firm communication. Journal of Accounting and Economics, 58(1), 96-116.

Loughran, T., & McDonald, B. (2011). When is a liability not a liability? Textual analysis,

dictionaries, and 10‐Ks. The Journal of Finance, 66(1), 35-65.

Malmendier, U., & Tate, G. (2005). CEO overconfidence and corporate performance. Journal of

Finance 60(6): 2661–2700.

Price, S. M., Doran, J. S., Peterson, D. R., & Bliss, B. A. (2012). Earnings conference calls and

stock returns: The incremental informativeness of textual tone. Journal of Banking &

Finance, 36(4), 992-1011.

Rosen, S. (1981). The economics of superstars. The American Economic Review, 71(5), 845-858.

Schrand, C. M., & Zechman, S. L. (2012). Executive overconfidence and the slippery slope to

financial misreporting. Journal of Accounting and Economics, 53(1-2), 311-329.

Shemesh, J. (2017). CEO social status and risk-taking. Quarterly Journal of Finance, 7(02).

Shi, W., Zhang, Y., & Hoskisson, R. E. (2017). Ripple effects of CEO awards: Investigating the

acquisition activities of superstar CEOs' competitors. Strategic Management Journal, 38(10),

2080-2102.

Wheeler, L. (1966). Motivation as a determinant of upward comparison. Journal of Experimental

Social Psychology, 1, 27-31.

32

Table 1: Sample Panel A: Descriptive Statistics

#Obs Mean Median Std Dev (1) (2) (3) (4)

Dependent Variables

CEO_PosTone 29,712 0.015 0.014 0.010 CEO_Words 29,712 1496.900 1315.000 946.805 Over_Invest (0/1) 29,712 0.412 0.000 C_Score 7,428 0.121 0.112 0.137 Pos_Disclos (0/1) 18,372 0.158 0.000 Neg_Disclos (0/1) 9,126 0.207 0.000 Deal_Number 7,428 0.415 0.000 0.905 Deal_Value 7,428 20.053 0.000 133.352 Deal_Prem 7,428 13.501% 0.000 17.195% Ann_Returns 3,083 -2.248% -1.103% 6.385%

Control Variables

Log_MV 7,428 7.851 7.442 1.583 MTB 7,428 2.811 2.142 2.095 ROA 7,428 0.095 0.083 0.074 Earnings_Growth 7,428 0.001 0.001 0.008 Sales_Growth 7,428 0.096 0.070 0.083 RelativeSize 2,692 0.095 0.067 0.174 TargetPublic (0/1) 2,692 0.410 0.000 TenderOffer (0/1) 2,692 0.045 0.019 StockPercentage 2,692 0.228 0.158 0.369 Toehold 2,692 0.020 0.000 0.016

Other Variables

CFO_PosTone 29,712 0.003 0.003 0.009 CFO_Words 29,712 1301.677 1140.000 820.210 Rel_Words 29,712 195.223 112.000 948.322 Rel_Tone 29,712 0.011 0.010 0.012

33

Panel B: Correlation Table

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11) (12) (13) (14) (15) (16) (17) (18) (19)

1.CEO_PosTone 1.00

2.CEO_Words 0.13 1.00

3.Over_Invest 0.19 0.11 1.00

4.C_Score -0.02 -0.04 -0.12 1.00

5.Pos_Disclos 0.03 0.01 0.01 -0.09 1.00

6.Neg_Disclos -0.01 0.00 -0.04 0.26 -0.31 1.00

7.Deal_Number -0.00 -0.01 -0.02 0.01 -0.05 0.03 1.00

8.Deal_Value 0.03 0.04 0.06 -0.03 0.01 -0.02 0.69 1.00

9.Deal_Prem 0.07 0.10 0.03 -0.14 0.06 -0.16 0.45 0.08 1.00

10.Ann_Returns -0.06 -0.03 -0.01 0.02 0.01 0.05 -0.26 -0.10 -0.23 1.00

11.Log_MV 0.20 0.17 0.12 -0.03 0.06 -0.01 0.04 0.05 0.03 -0.06 1.00

12.MTB 0.09 0.02 0.05 -0.09 0.14 -0.12 0.02 0.03 0.01 -0.02 0.14 1.00

13.ROA 0.16 0.23 0.17 -0.02 0.05 -0.01 0.01 0.01 0.06 -0.09 0.23 0.17 1.00

14.Earnings_Growth 0.13 0.10 0.12 -0.08 0.02 -0.05 -0.00 -0.02 -0.01 0.03 0.10 0.13 0.15 1.00

15.Sales_Growth 0.19 0.16 0.09 -0.05 0.07 -0.12 0.03 0.01 0.03 0.00 0.07 0.08 0.11 0.18 1.00

16.RelativeSize -0.02 0.00 -0.01 0.02 -0.04 0.01 -0.03 -0.05 -0.03 -0.01 -0.04 -0.01 0.02 0.01 0.02 1.00

17.TargetPublic -0.00 -0.01 0.03 0.01 -0.00 0.01 -0.01 -0.01 -0.00 0.01 -0.02 -0.01 -0.01 -0.03 -0.00 0.09 1.00

18.TenderOffer 0.03 0.04 0.13 -0.16 0.10 -0.21 -0.01 0.01 0.02 -0.04 0.03 0.03 0.01 0.05 0.02 0.11 0.05 1.00

19.StockPercentage 0.05 0.08 -0.01 -0.09 0.04 -0.16 0.08 0.05 0.01 -0.06 0.01 0.01 0.00 -0.01 -0.03 0.08 0.10 0.18 1.00

20.Toehold 0.00 -0.01 0.03 0.14 -0.15 0.05 -0.02 -0.03 -0.00 0.01 0.03 0.05 0.02 0.01 0.00 0.01 0.07 0.03 0.03

This table describe the sample. Panel A provides the descriptive statistics (mean, median, and standard deviation) for all of our variables. Panel B presents sample Spearman’s correlations. Correlations that are significantly different from zero at the p<0.05 level are in bold. All data are winsorized at the 1% and 99% levels. See Appendix for variable definitions.

34

Table 2: Change in CEO’s Tone and Overconfidence

CEO_PosTone CEO_Words Over_Invest (1) (2) (3)

Post -0.003 (-1.60)

186.022*** (3.09)

0.025 (1.21)

Competitor -0.001* (-1.76)

-22.989 (-0.95)

0.013 (0.75)

Competitor X Post 0.003*** (3.21)

95.186* (1.94)

0.055** (2.01)

Control Variables

Log_MV -0.001*** (-4.37)

103.577** (2.01)

0.069** (2.34)

MTB -0.001** (-2.16)

-17.998 (-1.51)

-0.011* (-1.88)

ROA 0.003 (0.95)

1054.117** (2.11)

0.011 (0.31)

Earnings_Growth -0.009*** (-3.83)

-937.194 (-1.05)

0.100** (2.51)

Sales_Growth -0.002*** (-3.68)

-46.925 (-1.28)

0.021*** (3.01)

Constant -0.016*** (-6.54)

1437.476*** (5.90)

Year Fixed Effect Yes Yes Yes Firm Fixed Effect Yes Yes Yes Cluster Award, Firm Award, Firm Award, Firm Adj. R-Squared 34.35% 2.05% 13.12% # Obs 29,712 29,712 29,712

This table reports the regression results where the dependent variables are CEO_PosTone, CEO_Words, and Over_Invest in columns 1, 2 and 3, respectively. T-statistics are presented in parentheses with the standard errors clustered by Award and Firm (Petersen 2009; Gow et al. 2010), and ***, **, and * denote significance at the 0.01, 0.05, and 0.10 level, respectively. Year and firm fixed effects are included in all the models. All data are winsorized at the 1% and 99% levels. See Appendix for variable definitions.

35

Table 3: Accounting Choices

C_Score Pos_Disclos Neg_Disclos (1) (2) (3)

Post -0.016 (-0.45)

-0.124** (-2.41)

-0.264 *** (-3.81)

Competitor 0.021* (1.71)

0.031 (1.10)

-0.025 (-0.85)

Competitor X Post -0.058*** (-3.81)

0.047* (1.90)

-0.073** (-2.25)

Control Variables

Log_MV -0.036*** (-8.46)

0.105* (1.88)

0.121*** (2.82)

MTB -0.025*** (-5.28)

-0.005 (-0.35)

-0.014 (-1.15)

ROA -0.368*** (-7.32)

-0.041* (-1.88)

-0.046 (-1.04)

Earnings_Growth -0.047 (-1.39)

0.011* (1.81)

-0.017 (-0.93)

Sales_Growth -0.026* (-1.80)

0.003 (-0.26)

0.001 (0.52)

Constant 1.132*** (3.89)

Year Fixed Effect Yes Yes Yes Firm Fixed Effect Yes Yes Yes Cluster Award, Firm Award, Firm Award, Firm Adj. R-Squared 11.52% 3.85% 4.27% # Obs 7,428 18,372 9,126

This table reports the regression results where the dependent variables are C_Score, Pos_Disclos, and Neg_Disclos in columns 1, 2 and 3, respectively. T-statistics are presented in parentheses with the standard errors clustered by Award and Firm (Petersen 2009; Gow et al. 2010), and ***, **, and * denote significance at the 0.01, 0.05, and 0.10 level, respectively. Year and firm fixed effects are included in all the models. All data are winsorized at the 1% and 99% levels. See Appendix for variable definitions.

36

Table 4: Merger and Acquisition

Deal_Number Deal_Value Deal_Prem Ann_Returns (1) (2) (3) (4)

Post -0.041** (-1.97)

-0.319** (-2.10)

-0.195 (-1.48)

0.011** (2.12)

Competitor 0.006 (1.09)

-0.058 (-1.02)

-0.016 (-0.17)

0.001 (0.49)

Competitor X Post 0.066** (2.33)

0.438*** (3.11)

0.285*** (5.03)

-0.019*** (-3.76)

Control Variables

Log_MV 0.032*** (3.18)

0.136*** (5.39)

0.065* (1.92)

-0.002* (-1.73)

MTB 0.010* (1.68)

0.085*** (2.72)

0.019** (2.13)

0.005 (1.38)

ROA 0.018* (1.84)

0.035** (2.11)

0.010 (1.34)

-0.005 (-0.68)

Earnings_Growth 0.006* (1.73)

0.025 (1.06)

0.018** (2.31)

0.005* (1.72)

Sales_Growth 0.003 (1.18)

0.013 (0.62)

0.013* (1.70)

0.003 (0.37)

RelativeSize -0.039***

(-3.10)

TargetPublic -0.001

(-0.49)

TenderOffer 0.003*

(1.68)

StockPercentage -0.011***

(-2.83)

Toehold 0.005*

(1.93)

Constant 0.053*** (2.28)

0.538* (1.92)

0.329** (2.41)

0.019 (1.12)

Year Fixed Effect Yes Yes Yes Yes Firm Fixed Effect Yes Yes Yes Yes Cluster Award, Firm Award, Firm Award, Firm Award, Firm Adj. R-Squared 9.83% 10.15% 7.52% 5.81% # Obs 7,428 7,428 7,428 3,083

This table reports the regression results where the dependent variables are Deal_Number, Deal_Value, Deal_Prem, and Ann_Returns in columns 1, 2, 3 and 4, respectively. T-statistics are presented in parentheses with the standard errors clustered by Award and Firm (Petersen 2009; Gow et al. 2010), and ***, **, and * denote significance at the 0.01, 0.05, and 0.10 level, respectively. Year and firm fixed effects are included in all the models. All data are winsorized at the 1% and 99% levels. See Appendix for variable definitions.

37

Table 5: Corporate Governance Panel A: Accounting Choices

C_Score Pos_Disclos Neg_Disclos (1) (2) (3)

Post 0.008 (1.39)

0.157 (1.51)

-0.238** (-2.45)

HighG-Index -0.022** (-2.25)

0.057 (1.29)

-0.091* (-1.85)

HighG-Index X Post -0.018* (-1.84)

0.089 (1.01)

-0.129*** (3.16)

Control Variables

Log_MV -0.040*** (-4.59)

0.155* (1.79)

0.330*** (3.27)

MTB -0.020*** (-3.10)

-0.011 (-0.58)

-0.011 (-0.73)

ROA -0.334*** (-5.17)

-0.041** (-2.01)

-0.055 (-1.28)

Earnings_Growth -0.056 (-0.88)

0.003 (0.78)

-0.022 (-1.48)

Sales_Growth -0.020** (-2.03)

0.001 (-0.32)

0.001 (0.55)

Constant 1.173*** (2.79)

Year Fixed Effect Yes Yes Yes Firm Fixed Effect Yes Yes Yes Cluster Award, Firm Award, Firm Award, Firm Adj. R-Squared 10.23% 3.52% 4.42% # Obs 14,856 10,104 3,461

38

Panel B: Merger and Acquisition

Deal_Number Deal_Value Deal_Prem Ann_Returns (1) (2) (3) (4)

Post -0.023 (-1.45)

-0.267* (-1.89)

-0.205 (-1.60)

0.010*** (2.72)

HighG-Index 0.017** (2.48)

-0.005 (-0.18)

0.028* (1.79)

-0.005* (-1.88)

HighG-Index X Post 0.051*** (2.94)

0.319* (1.82)

0.216** (2.51)

-0.011** (-2.16)

Control Variables

Log_MV 0.023** (2.11)

0.124*** (4.29)

0.072*** (2.68)

-0.001 (-1.38)

MTB 0.012* (1.81)

0.074** (2.12)

0.023** (1.98)

0.003 (0.98)

ROA 0.012** (2.38)

0.033** (2.27)

0.005 (0.74)

-0.003 (-0.25)

Earnings_Growth 0.004* (1.76)

0.022 (1.03)

0.019 (1.63)

0.005* (1.86)

Sales_Growth 0.001 (0.65)

0.014 (1.09)

0.010* (1.77)

0.005 (0.86)

RelativeSize -0.036***

(-3.18)

TargetPublic -0.001

(-0.92)

TenderOffer 0.005*

(1.93)

StockPercentage -0.010***

(-2.58)

Toehold 0.004**

(2.23)

Constant 0.058* (1.86)

0.498** (2.01)

0.294** (2.37)

0.016 (0.75)

Year Fixed Effect Yes Yes Yes Yes Firm Fixed Effect Yes Yes Yes Yes Cluster Award, Firm Award, Firm Award, Firm Award, Firm Adj. R-Squared 8.37% 9.10% 6.99% 5.21% # Obs 3,714 3,714 3,714 2,017