state of industry report 2015 - nepra.org.pk of industry... · 1 foreword the power sector is...

TRANSCRIPT

1

State of Industry Report 2015

STATE OF INDUSTRY REPORT

2015

v

CONTENTS

FOREWORD ........................................................................................................................................................ 1

1. OVERVIEW ............................................................................................................................................ 51.1 China-Pakistan Economic Corridor (C-PEC) Project ..................................................................................5

1.2 Donors’ Support ......................................................................................................................................................5

1.3 Load Shedding .........................................................................................................................................................5

1.4 Reduction in the Cost of Generation ..............................................................................................................5

1.5 Tariffs of Renewable Energy Projects ..............................................................................................................6

1.6 Performance of GENCOs ......................................................................................................................................6

1.7 Transmission Network NTDC .............................................................................................................................6

1.8 Projected Capacity and Power Balance of NTDC System ........................................................................7

1.9 Expansion Plan of NTDC ......................................................................................................................................7

1.10 Timely Completion of Upcoming Projects ....................................................................................................7

1.11 Power Balance of K-Electric System .................................................................................................................8

1.12 Environmental Impact of Coal Based Power Plants ...................................................................................8

1.13 Infrastructure Development ...............................................................................................................................8

1.14 Data Reporting ........................................................................................................................................................8

1.15 Power Market Reforms ..........................................................................................................................................8

1.16 Receivables of DISCOs ..........................................................................................................................................9

1.17 Transmission and Distribution (T&D) Losses of DISCOs .........................................................................9

1.18 Circular Debt .............................................................................................................................................................9

1.19 Tariff Differential Subsidy ...................................................................................................................................9

1.20 Multi-Year Tariff (MYT) Regime for DISCOs ...................................................................................................9

1.21 Generation Capacity of K-Electric .....................................................................................................................9

1.22 K-Electric Transmission and Distribution Systems ..................................................................................10

1.23 Upfront Tariffs.........................................................................................................................................................10

1.24 Net-Metering Regime..........................................................................................................................................10

1.25 Special Purpose Transmission Licence under Section 19 of NEPRA Act .........................................10

1.26 Recommendations ...............................................................................................................................................11

2. PERFORMANCE OF GENERATION SECTOR ...................................................................................... 152.1 General ......................................................................................................................................................................15

2.2 Source-wise Installed Capacity ........................................................................................................................15

2.3 Hydropower ............................................................................................................................................................15

2.4 Thermal .....................................................................................................................................................................15

2.4.1 Jamshoro Power Company Limited (GENCO-I) ........................................................................152.4.2 Central Power Generation Company Limited (GENCO-II) ....................................................162.4.3 Northern Power Generation Company Limited (GENCO-III) ...............................................162.4.4 Lakhra Power Generation Company Limited (GENCO-IV) ....................................................162.4.5 Overall Performance of GENCOs ....................................................................................................162.4.6 Independent Power Producers (IPPs) ...........................................................................................172.4.7 Installed versus Dependable Capacity .........................................................................................172.4.8 Manpower to MW Ratio .....................................................................................................................17

i

vi

2.5 Nuclear (CHASNUPP-I and II) ..........................................................................................................................18

2.6 Wind...........................................................................................................................................................................18

2.7 Bagasse .....................................................................................................................................................................18

2.8 Solar ...........................................................................................................................................................................18

2.9 K-Electric Limited ..................................................................................................................................................18

3. PERFORMANCE OF TRANSMISSION SECTOR .................................................................................. 233.1 General ......................................................................................................................................................................23

3.2 Overloading of Existing Power Transformers .............................................................................................23

3.3 Power Dispersal Constraints in Transmission Networks ........................................................................26

3.3.1 Uch-II Power (Pvt.) Limited ...............................................................................................................263.3.2 Engro Powergen Qadirpur Limited................................................................................................263.3.3 Altern Energy Limited .........................................................................................................................263.3.4 TNB Liberty Power Limited ...............................................................................................................263.3.5 Habibullah Coastal Power Company Limited ............................................................................263.3.6 Foundation Power Company (Daharki) Limited .......................................................................263.3.7 Nishat Power Limited and Nishat Chunian Power Limited ..................................................27

3.4 Induction of New Generation Power Plants ...............................................................................................27

3.5 Future NTDC Network.........................................................................................................................................29

3.6 NTDC Financial Plans ..........................................................................................................................................30

3.7 K-Electric Transmission System .......................................................................................................................30

4. PERFORMANCE OF DISTRIBUTION SECTOR ................................................................................... 354.1 Constraints in DISCOs’ System ........................................................................................................................35

4.2 Receivables of DISCOs ........................................................................................................................................35

4.3 Transmission and Distribution (T&D) Losses of DISCOs .......................................................................36

4.4 Circular Debt ...........................................................................................................................................................37

4.5 Tariff Differential Subsidy...................................................................................................................................37

4.6 Constraints in K-Electric System .....................................................................................................................37

4.7 Uploading of Performance Reports submitted by DISCOs and K-Electric on Quarterly

Basis on Website....................................................................................................................................................37

4.8 Legal Proceedings against DISCOs and K-Electric due to non-compliance of Performance Standards (Distribution) Rules, (PSDR) 2005 ..............................................................................................37

5. INITIATIVES BY NEPRA ...................................................................................................................... 415.1 Upfront Tariff for Wind Power Projects ........................................................................................................41

5.2 Upfront Tariff for New Bagasse based Co-Generation Power Projects ............................................41

5.3 Upfront Tariff for Coal Power Projects ..........................................................................................................41

5.4 Tariff for Conversion of Oil to Coal Projects ...............................................................................................42

5.5 Upfront Tariff for Solar Power Projects .........................................................................................................42

5.6 Upfront Tariff for Small Hydropower Projects ...........................................................................................42

5.7 Upfront Tariff for LNG based Power Projects .............................................................................................43

5.8 Tariff for Short-Term IPPs ...................................................................................................................................43

5.9 Development of NEPRA (Alternative and Renewable Energy) Distributed Generation and Net Metering Regulations, 2015 ..............................................................................................................................43

ii

vii

5.10 Integrated Generation, Transmission and Distribution Plans (IGTDPs) ...........................................43

5.10.1 Development of IGTDPs ...................................................................................................................435.10.2 Evaluation/Review of IGTDPs by NEPRA .....................................................................................445.10.3 Recommendations for Resubmission of IGTDPs ......................................................................445.10.4 Final Guidelines and Formats to Develop IGTDPs by NEPRA .............................................45

5.11 Special Purpose Transmission Licence (SPTL) under Section 19 of NEPRA Act ...........................45

5.12 Development of NEPRA Interconnection Guidelines, 2015 .................................................................45

6. MONITORING OF THE SECTOR ......................................................................................................... 496.1 Visits of DISCOs to Verify/Inspect the Sanctioned Load vis-a-vis Connected Load ...................49

6.2 Real Time Monitoring ..........................................................................................................................................49

6.3 Undue Scheduled/Unscheduled Load Shedding by K-Electric ...........................................................49

6.4 Safety Record of Distribution Companies ...................................................................................................49

6.5 Annual Performance Report (APR) of NTDC ..............................................................................................50

6.5.1 Number of Voltage Variations (Violating Prescribed Criteria) ............................................516.5.2 System Frequency ................................................................................................................................54

6.6 Annual Performance Report (APR) of K-Electric .......................................................................................55

6.7 Energy not served in KE System ......................................................................................................................57

6.8 Frequent Tripping of Transmission and Grid System in NTDC ............................................................58

6.9 Handing Over of Switchyards of GENCOs to NTDC ................................................................................59

6.10 Implementation of Performance Standards (Generation) Rules, (PSGR) 2009 .............................59

6.11 Implementation of Grid Code ..........................................................................................................................59

6.12 Implementation of Distribution Code ..........................................................................................................59

6.13 Development of Power Safety Code .............................................................................................................60

7. INITIATIVES BY STAKEHOLDERS ...................................................................................................... 637.1 Market Structure ....................................................................................................................................................63

7.2 Creation of Central Power Purchasing Agency - Guarantee Limited (CPPA-G) ............................63

7.3 ModificationinTransmissionLicenceofNTDC .........................................................................................63

7.4 Market Operator Registration (Standards and Procedure) Rules, 2015 ...........................................63

7.5 PPIB Policy for Private Sector Transmission Projects 2015 ...................................................................64

7.6 Central Asia-South Asia (CASA-1000) Project ..............................................................................................64

7.7 Import of Electricity from Iran .........................................................................................................................64

7.7.1 Import of 74 MW (Jackigur – Mand) .............................................................................................647.7.2 Import of 100 MW (Polan – Gawadar) .........................................................................................647.7.3 Import of 1000 MW (Zahedan – Quetta) ....................................................................................64

7.8 Alternative and Renewable Energy Developments .................................................................................65

7.8.1 Steps/initiatives for Development of ARE Sector ....................................................................657.8.2 On-Grid Projects ...................................................................................................................................667.8.3 Off-Grid Applications....... .....................................................................................................................66

8. MISCELLANEOUS ................................................................................................................................ 738.1 Promulgation of New Rules/Regulations ....................................................................................................73

8.2 Advisories issued by NEPRA to the Government of Pakistan ..............................................................73

8.3 Consumer Affairs ..................................................................................................................................................73

8.3.1 Achievements/Development ...........................................................................................................74

iii

viii

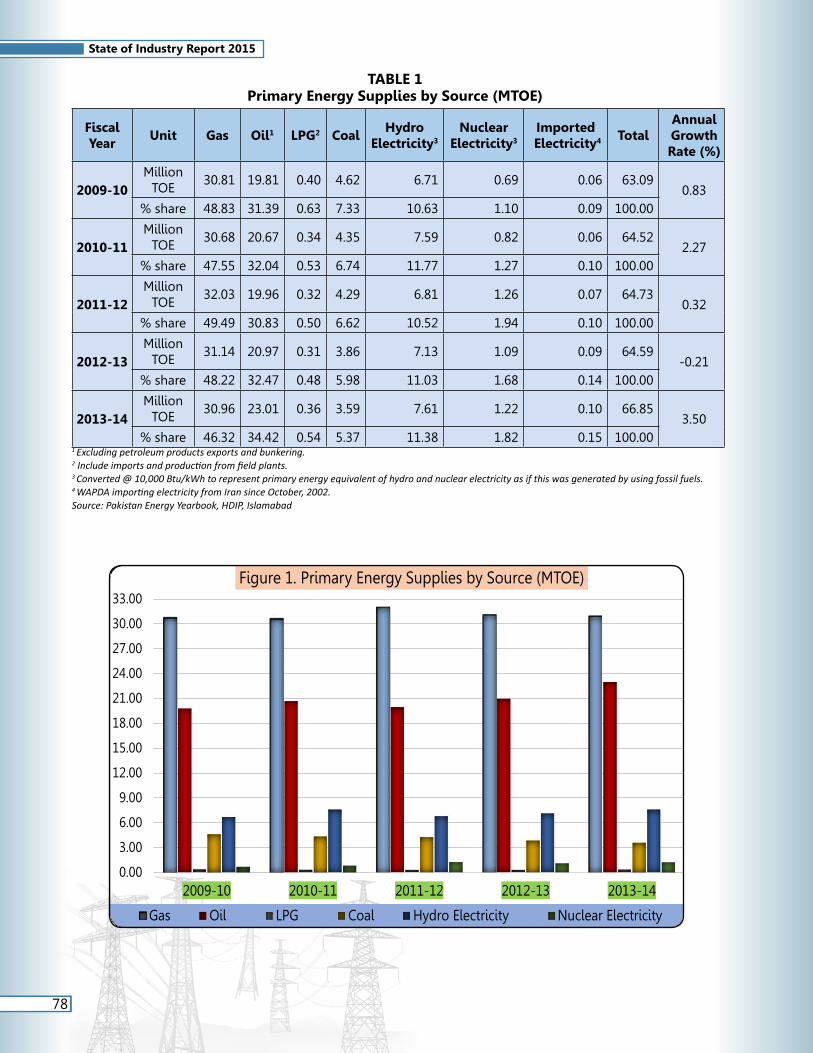

9. Energy Sector Overview .................................................................................................................... 779.1 Oil................................................................................................................................................................................77

9.2 Gas ..............................................................................................................................................................................77

9.3 Coal ............................................................................................................................................................................77

9.4 Primary Energy Supplies ....................................................................................................................................77

9.5 Final Energy Consumption ................................................................................................................................79

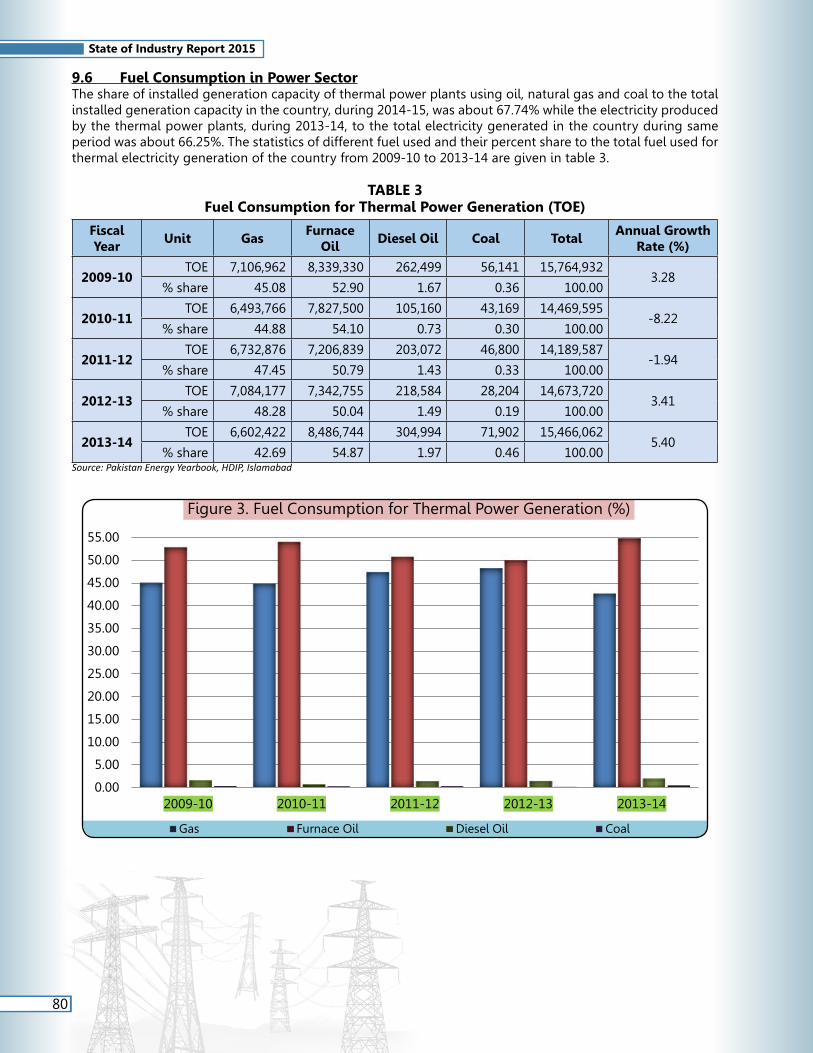

9.6 Fuel Consumption in Power Sector ...............................................................................................................80

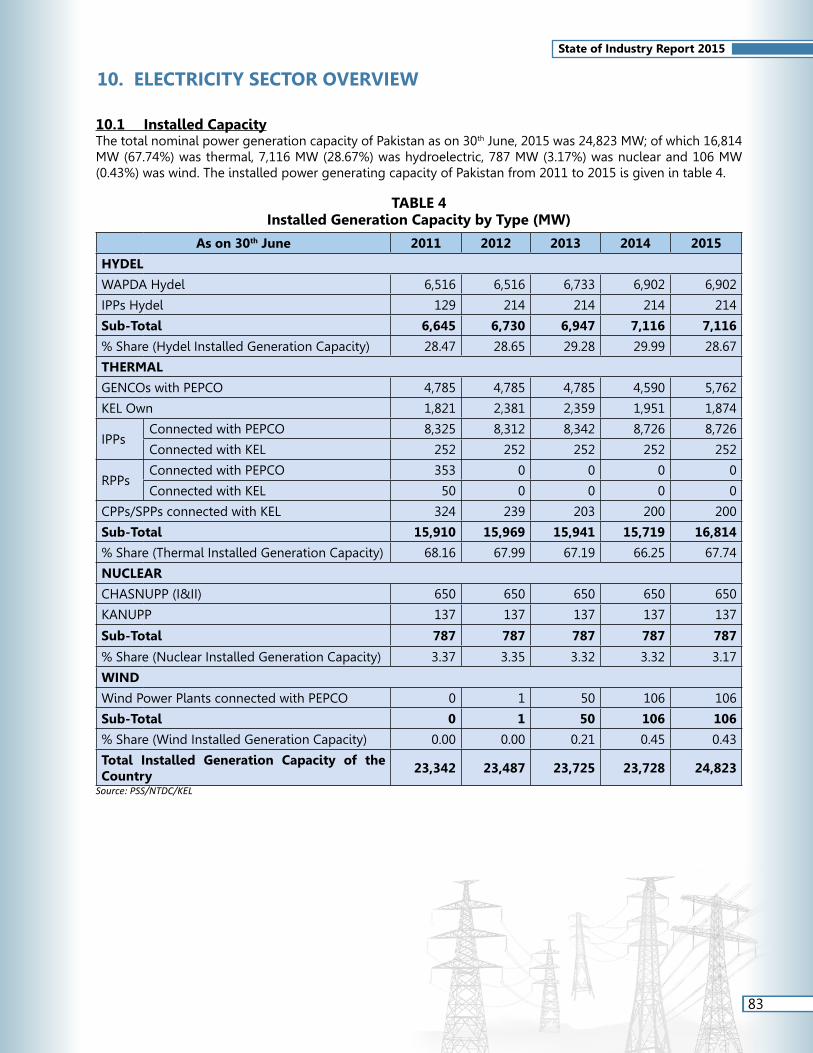

10. ELECTRICITY SECTOR OVERVIEW ..................................................................................................... 8310.1 Installed Capacity ..................................................................................................................................................83

10.2 Load Pattern and Peak Load Hours ............................................................................................................115

10.3 Maximum Demand ............................................................................................................................................117

10.4 Pattern of Electricity Consumption .............................................................................................................118

10.5 Surplus/DeficitinDemandandSupplyduringPeakHours(actualandprojected) ................ 119

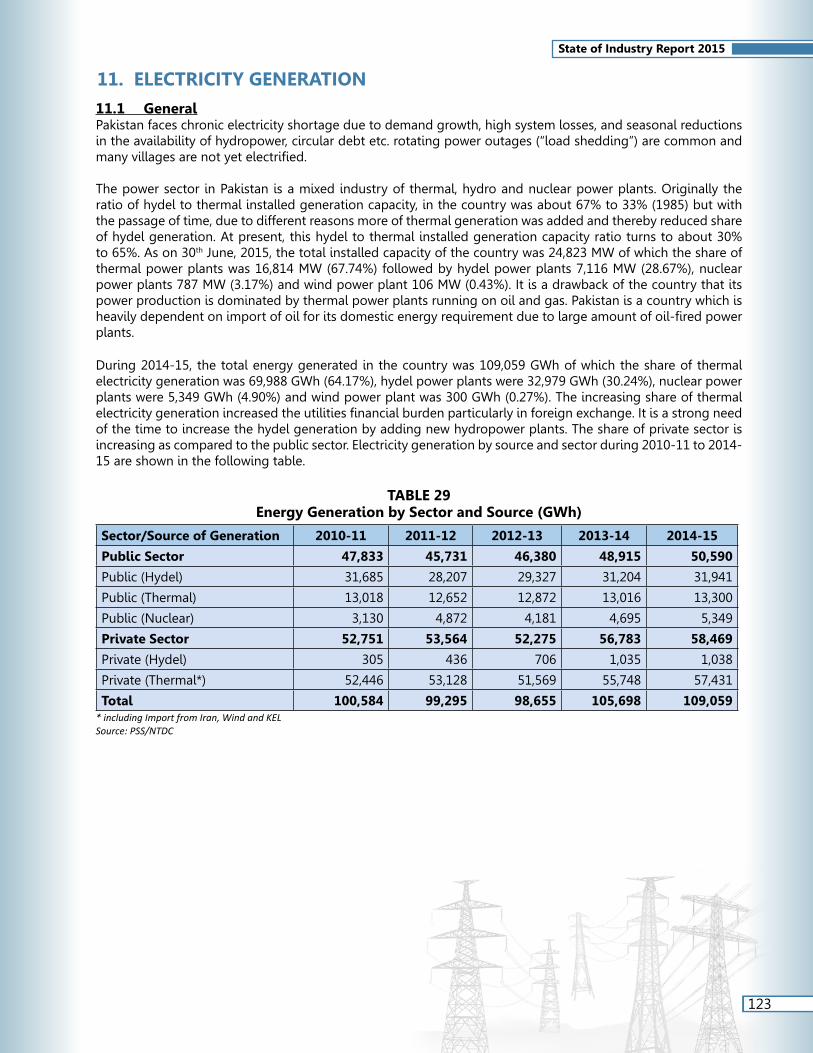

11. ELECTRICITY GENERATION ............................................................................................................. 12311.1 General ...................................................................................................................................................................123

11.2 Thermal Generation ..........................................................................................................................................124

11.3 Thermal Power Generation and Fuel Consumption .............................................................................124

11.4 Hydel Generation ...............................................................................................................................................125

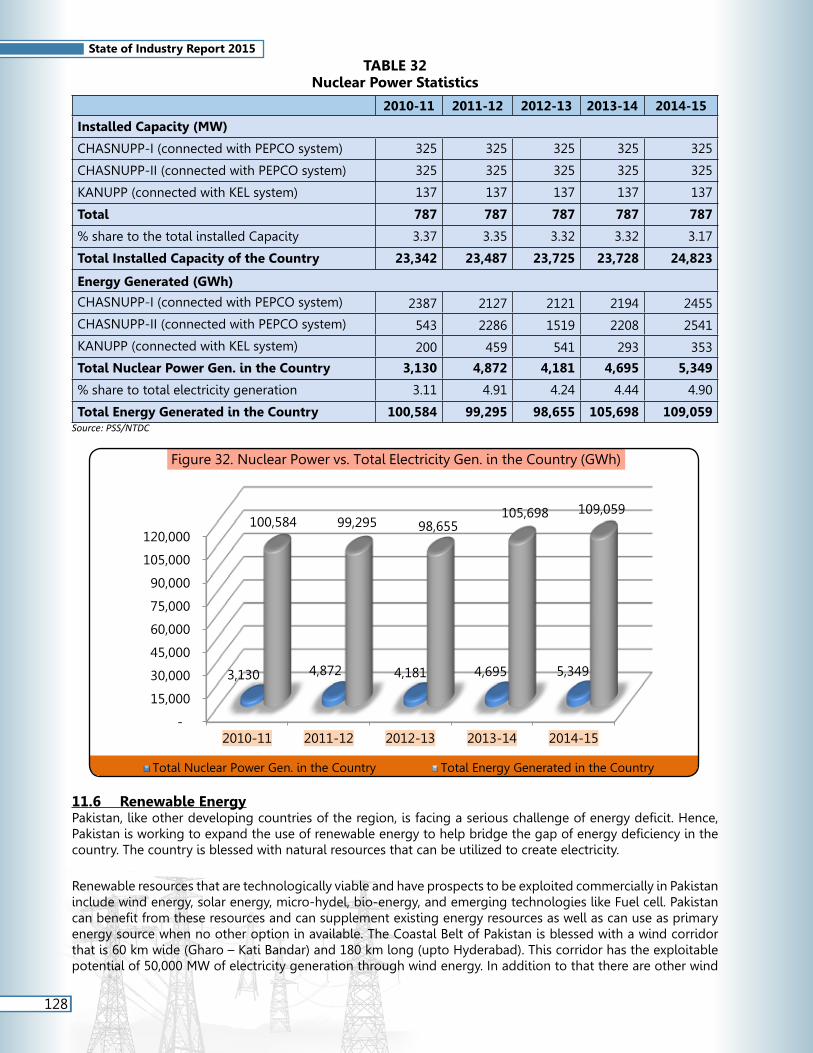

11.5 Nuclear Power Plants .......................................................................................................................................127

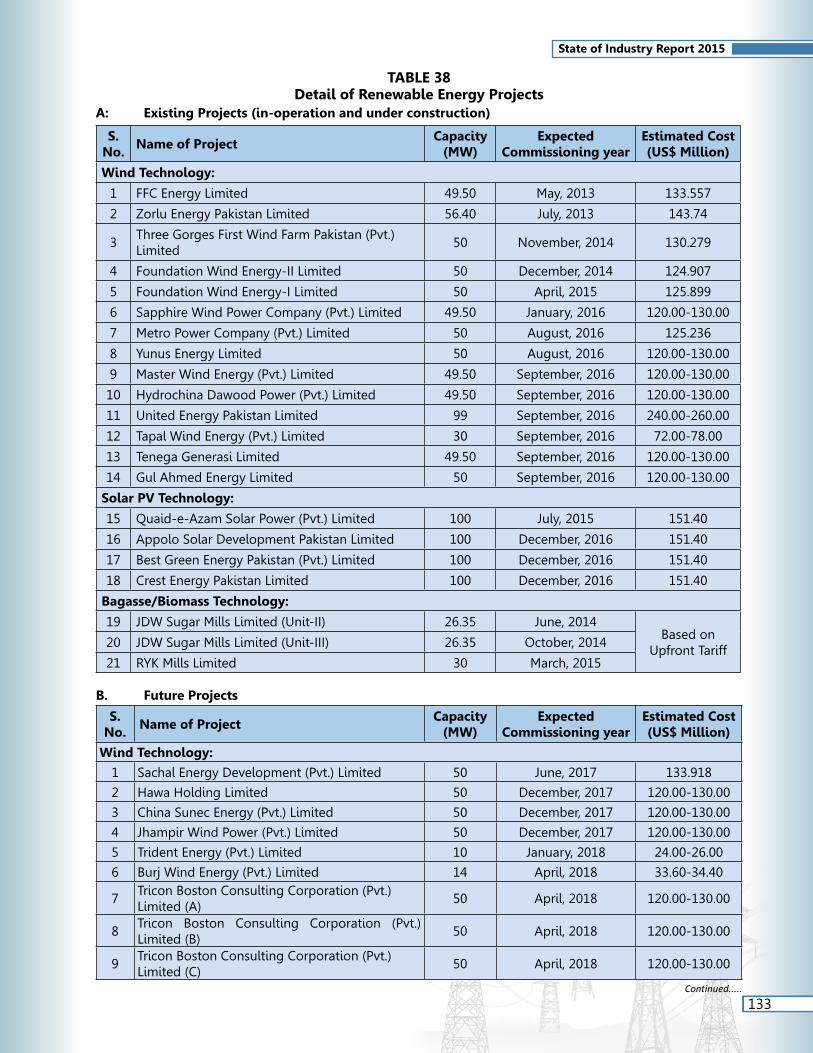

11.6 Renewable Energy .............................................................................................................................................128

11.7 Available Power Generation Capacity ........................................................................................................129

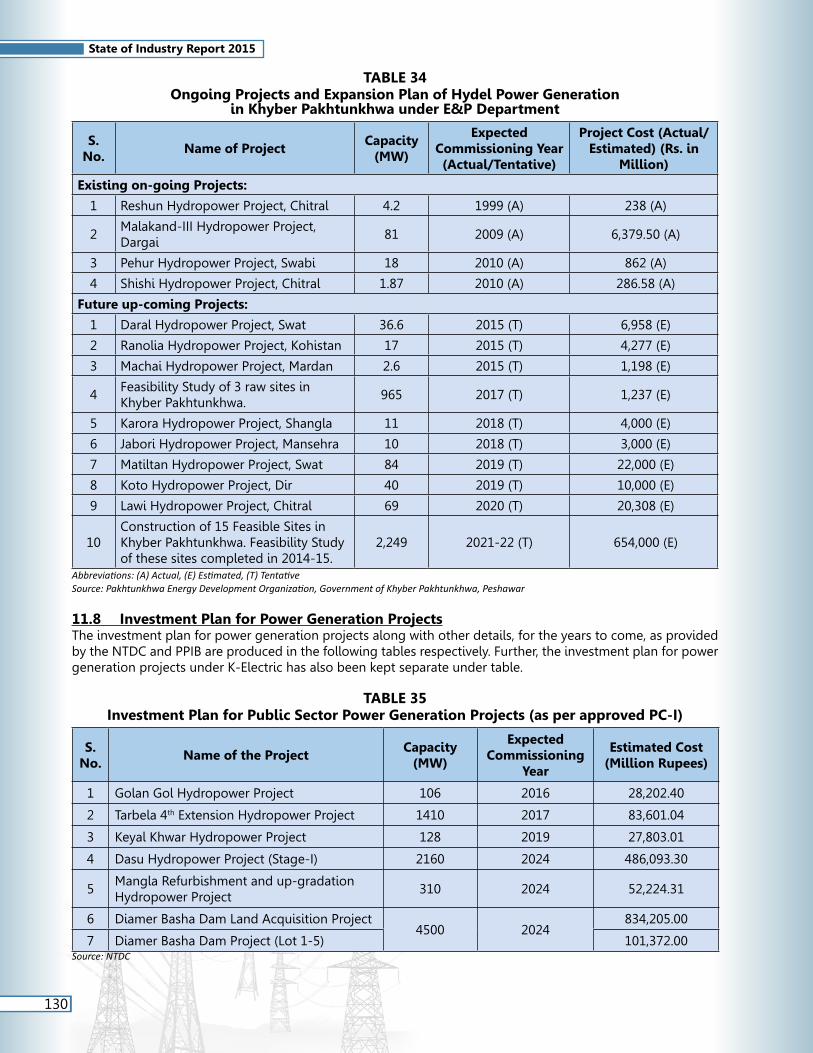

11.8 Investment Plan for Power Generation Projects ....................................................................................130

11.9 Economic Load Dispatch System .................................................................................................................136

11.10 Generation Licenses Granted ........................................................................................................................139

12. ELECTRICITY TRANSMISSION ......................................................................................................... 15112.1 General ...................................................................................................................................................................151

12.2 Transmission Lines and Grid Stations with NTDC .................................................................................151

12.3 Transmission Losses ..........................................................................................................................................152

12.4 Utilization of Transmission Lines and Power Transformers ...............................................................153

12.5 Investment Plan - NTDC System ..................................................................................................................154

12.6 Transmission Lines and Grid Stations with K-Electric ..........................................................................157

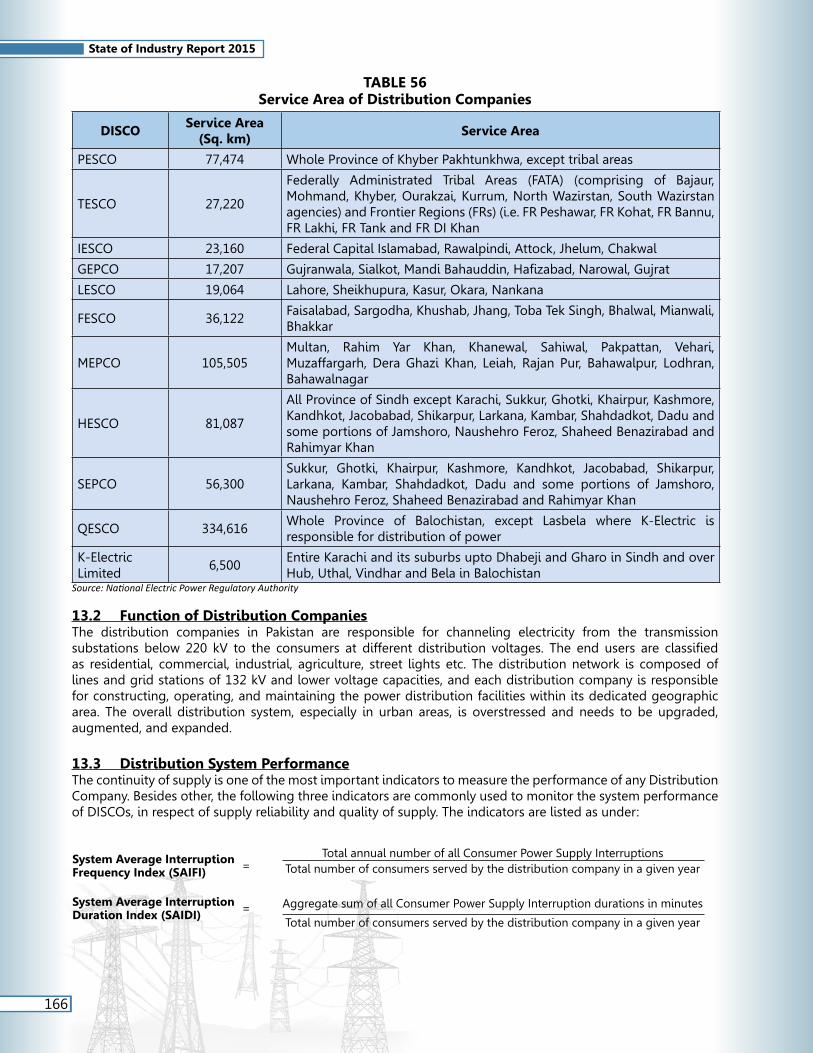

13. ELECTRICITY DISTRIBUTION ........................................................................................................... 16513.1 General ...................................................................................................................................................................165

13.2 Function of Distribution Companies ..........................................................................................................166

13.3 Distribution System Performance ................................................................................................................166

14. ELECTRICITY TARIFF......................................................................................................................... 19114.1 Tariff Setting .........................................................................................................................................................191

14.2 Tariff Standards ...................................................................................................................................................191

LIST OF TABLES .............................................................................................................................................. 213

ACRONYMS AND ABBREVIATIONS ............................................................................................................. 215

SOURCE OF INFORMATION .......................................................................................................................... 217

iv

1

FOREWORD

The power sector is presently undergoing a major transformation where the Federal and Provincial Governments have aligned their priorities for overcoming the energy crises which have been adversely affecting the social, economicandfinancialprogressofthecountryforthepastmanyyears.TheGovernmentofPakistan’s(GoP)efforts for bringing new power generation plants through China-Pakistan Economic Corridor (C-PEC) Agreement reflectstherealizationthatthecountryisindireneedofenergyresourcestosatisfybaseloadrequirements.Similarly, overall generation mix is also planned to have renewable energy projects which will provide necessary diversificationandincreasedenergysecuritytothesector.TheintroductionofRe-GasifiedLiquidNaturalGas(R-LNG) Projects is also a step towards adding relatively clean and cheaper energy generation resources.

According to the available plans, more than 17,200 MW are expected to be added to the system. In order to meet peak time demand about 8,000 MW will be inducted by the end of June, 2017. Although such a target by June, 2017 is quite ambitious yet this is achievable, as this planned capacity includes Solar and Wind Projects, 3,600 MW R-LNG based Projects, and under-construction hydropower projects at Tarbela and Neelum-Jhelum. Sustained efforts are, however, required at all levels so that smooth and transparent implementation of these projects is achieved within the target dates.

While it is satisfying to note that the generation sector has been drawing all the due attention, strengthening of the transmission and distribution sectors is equally critical. One of the problems faced by these sectors is their overloaded networks which not only hinder their power transfer capability but also add to wastage of electricity through increased losses. The constraints on transmission networks have also led to severe power evacuationproblemswiththeresultthatthecapacitiesofsomeofthemostefficientplantscannotbeutilizedto their optimum level. Therefore, addition of new generation facilities of around 8,000 MW by June, 2017 and strengthening of existing transmission system requires large scale investment in this area, besides hugely improved managerial performance by NTDC, in order to ensure availability of a reliable transmission system well before the completion of generation facilities.

In addition to funding constraints, the Distribution Companies (DISCOs) are required to enhance their ability and competence especially in the areas of designing, specifying and constructing 132 kV facilities which shall complement the additional energy referred to above.

It is noted that due to better load management policies, fewer agitations and protests were witnessed during 2014-15, especially in the later part of the year. Not only, improvement in uninterrupted supply to the industrial sector has been ensured, load shedding in the domestic and commercial sectors remained somewhat predictable whereas unscheduled load shedding hours have been considerably reduced. The improved continued electricity supply to the industrial sector is expected to help increase the industrial production besides creating more employment opportunities.

The ability of DISCOs to have accommodated and distributed more than 16,000 MW this year shows an improvement over the previous year.

The DISCOs did not show any noticeable improvement in their performance and continued with the business as usual in the areas of T&D losses, recoveries and technical operations. While overall averages for the year in the above areas remained almost the same as for 2013-14, the second half of the current year (January to June) showed slight improvements in the above areas relative to corresponding period of 2013-14. The safety aspect deterioratedwhichisreflectedintheincreasednumberoffatalincidentsoverthepreviousyearinmostoftheDISCOs.

The receivables of distribution sector increased by more than Rs. 120 billion during 2014-15, which on 30th June, 2015 stood at Rs. 633.119 billion. Out of Rs. 120 billion, Rs. 75 billion increase is due to the receivables from private sector, whereas Rs. 15 billion increase stood against AJK share. Another Rs. 13 billion increase is due to the Provincial Governments (especially Government of Sindh’s receivables). The Federal Government needs to

State of Industry Report 2015

2

pay attention to creating a smooth payment mechanism from the government connections especially in Sindh andAJK.Therecoveriesfromagricultureconnectionsalsoremainasourceofconstantinflowintothecirculardebt and cannot be resolved unless the provincial governments lend their active support to DISCOs.

K-Electric, despite having the generation capacity, is continuously carrying out load shedding for certain categories of its consumers. Although K-Electric has been reporting satisfactory performance in relation to NEPRAperformancestandards,thecrisesinK-ElectricterritoryinJune,2015haveprovedotherwise.ThefindingsofNEPRA’sfactfindingteamhavebroughtoutsomerealconcernsaboutthehealthofK-Electricsystem,theseissuesarerequiredtobeaddressedimmediatelywhichneedreasonableinvestmentspecificallyintransmissionand distribution networks.

Although no major steps were taken for the past many years to move towards a competitive market, despite NEPRA having indicated about the slow pace of reform process initiated in 1992, recent changes by creating a Central Power Purchasing Agency - Guarantee Limited (CPPA-G) out of the umbrella of NTDC are encouraging as these changes aimed at not only bringing transparency in the operations of power procurement agency, but also helping in smooth transition towards market based operations in the power sector.

During the year, the Authority has introduced up-front tariff regimes, in technologies of Solar, Wind, Bagasse, Small Hydro, R-LNG and Coal. The Authority also announced a number of land mark decisions including grant of “Special Purpose Transmission Licence” (SPTL) to a private entity, regulations on sale of power by renewable energy sources and regulations on net-metering regime. It is believed that the above decisions especially about SPTL and net-metering would prove to be the game-changer in the areas of transmission and distribution sectors. NEPRA expects that the GoP would also incentivize solar industry so that consumers are encouraged to participate not only in net-metering regime but also in off-grid application of solar power. Availability of funds would not only facilitate consumers to install solar panels but will also help in meeting supply-demand gap.

It has been observed that the targets set for the sector are reasonably ambitious but critical at the same time. It is, therefore, desired that coherent efforts are made in the sector with continuous vigor and zeal. Continuous monitoring ensuring transparency for timely completion of all envisaged projects is equally important.

The detailed statistics and data provided on the power sector in the State of Industry Report 2015, besides being a source of information, would also be helpful and useful for the decision makers.

State of Industry Report 2015

OVERVIEW 1

5

State of Industry Report 2015

1. OVERVIEW

Notwithstanding the issues and shortcomings in the power sector, some of the following factors during the year 2014-15 have shown positive developments as a result of various steps taken by the Federal and Provincial Governments coupled with international trends in the capital and fuel markets.

1.1 China-Pakistan Economic Corridor (C-PEC) ProjectThe US$ 46 billion Agreement under China-Pakistan Economic Corridor (C-PEC) Project between the Governments of China and Pakistan includes around US$ 33.8 billion for various energy projects. Under the C-PEC agreement, US$ 15.5 billion worth of coal, wind, solar and hydropower projects will add 10,400 MW of energy to the National Grid. C-PEC also foresees cooperation between the two countries in developing nuclear energy based projects. It is expected that the development of nuclear and coal projects would meet the necessary base load requirementsintheoveralldemandprofileofthecountryinthelongrun.Expensiveenergymixhasremainedone of the major contributors to relatively higher tariffs for the end-consumers. Coal power plants operating at high utilization levels will help in bringing down the cost of energy generation.

1.2 Donors’ SupportThe support of donor agencies in the infrastructure development and capacity building has resulted in some noticeable improvement. In the generation sector, refurbishment through USAID funding in public sector generation companies (GENCOs) has led to recovery of additional useful capacities at relatively better operational efficiencies. GENCOs were also helped by USAID in carrying out performance testing of their generationfacilities. Through JICA and USAID support, detailed studies for National Transmission and Dispatch Company Limited (NTDC) have been initiated, including preparation of a National Least Cost Expansion Plan and studies for absorption levels of renewable energy projects in the National Grid. The World Bank has been providing assistance for improving the functioning of Central Power Purchasing Agency (CPPA). Similarly, infrastructure improvement of SCADA system is being contemplated at National Power Control Centre (NPCC), through JICA support. USAID, World Bank and Asian Development Bank are also helping in importing power from Central Asian States.

1.3 Load SheddingOwingtooverallmonitoringbytheMinistryofWaterandPowerandrealtimemonitoringofpowerflowsatthefeeder level, the DISCOs have been able to achieve marked improvement in demand management. Reportedly, the load shedding duration has been reduced from 12 hours in 2013 to 6 hours in 2015 in the urban areas. Similarly, load shedding in the industrial sector has been reduced from 12 hours to 4 hours over the same period. Rural areas have also witnessed relative reduction in their load shedding hours.

1.4 Reduction in the Cost of GenerationDue to reduction in oil prices in the international market, the cost of generation declined in the year 2014-15, compared to the last year. A comparison of the two years is shown in the following table:

Source-wise Fuel Cost (Rs./kWh)

Source Hydel Coal HSD RFO Gas Nuclear Import Iran Mixed Wind Solar Average

Basket Price2013-14 - 4.05 21.85 15.97 4.81 1.32 9.35 9.31 - - 10.592014-15 - 4.50 17.14 12.54 4.81 1.19 10.03 8.23 - - 9.84

Source: NEPRA

It may be noted that up to June 2015, except for coal and import from Iran, which constitute only 0.11% and 0.46% respectively of the overall energy generated, the cost of generating a unit of energy through major fuels declined. Generation on furnace oil made up 32.66% of total energy. The unit cost of energy on furnace oil reduced by Rs. 3.43 per kWh. Similarly, the cost of generation on high speed diesel (HSD) which provided 3.01% of total generation reduced by Rs. 4.71 from 2013-14. The cost of generation on gas remained almost the same. The reduction in cost of generation was passed on to the consumers for the respective months of 2014-15 as tabulated herein. An overall impact of the reduction in cost has been noted as Rs. 87.97 billion during the year:

6

State of Industry Report 2015

Increase/(Decrease) Rs./kWh

July Aug. Sept. Oct. Nov. Dec. Jan. Feb. March April May June

0.43 (0.30) 0.52 (0.48) (2.97) (3.24) (2.08) (4.43) (3.62) (1.86) (2.68) (2.19)Source: NEPRA

1.5 Tariffs of Renewable Energy ProjectsThereductionincapitalcostsandtechnological improvementsinrenewableenergyhasreaffirmedNEPRA'sstance that such projects should be inducted with due consideration to these factors. NEPRA, in order to provide incentivestoinvestors,andtobuildtheirconfidenceandwithaviewtointroducingwindtechnologyinthecountry, determined an upfront levelized tariff of Rs. 13.1998 per kWh, for wind power projects in 2013. In view of the improvement in technology and overall decline in project costs, the tariff was revised at Rs. 10.6048 in 2015. Similarly, in order to introduce solar technology in the country, NEPRA determined an upfront levelized tariff of Rs. 17.1216 per kWh in 2014 and the same was capped at a maximum of 50 MW, out of which 46.5 MW tariff was secured, which in 2015 has been determined at the rate of Rs. 14.8591 per kWh. Renewable energy not only provides energy security but is also instrumental in saving foreign exchange, guarantees predictability and is environment friendly. In view of the continuous improvements in technology, reduction in prices and the grid stability, renewable energy has to be inducted gradually in the system. For creating more space for renewable energy projects, detailed studies need to be carried out to identify short term and long term expansion plans for strengthening the grid system.

1.6 Performance of GENCOsThe performance of GENCOs has been a matter of concern for the regulator and an aggressive monitoring programhasbeeninitiatedforoverseeingGENCOs'regulatoryaffairs.Earlier,alltheGENCOswereadvisedbytheAuthoritytocarryoutperformancetestssothatdegradationintheiroperationalcapabilities,efficienciesand administrative factors like manpower, timely overhauling and maintenance are set afresh. Particularly, the surplus human resource which is sitting idle due to closure and non-operational plants and over employment are major factors contributing towards higher cost of generation. NEPRA during forthcoming tariff determinations for GENCOs will keep these factors in view in order to rationalize their tariff. The surplus and skilled human resource of these GENCOs can be absorbed and utilized in the upcoming power generation projects.

1.7 Transmission Network NTDCUnder its transmission license, NTDC is required to play a number of roles. As a network operator, it is required to construct and operate Extra High Voltage transmission lines and grid stations for transporting power from the existing and new generation facilities to the DISCOs. NTDC has a critical role in the sense that it has to match not only the availability of its transmission facilities with the timing of new power generation plants, but also to periodically refurbish and upgrade its existing system to cater for the increased load demand put on by the DISCOs, besides managing transmission losses. The transmission network of NTDC includes 5,197 km long transmission lines operating at 500 kV level and 9,814 km long 220 kV lines.

As of 30th June 2015, NTDC is maintaining 13 No. 500 kV grid stations with a transformation capacity of 18,624 MVA. There are 33 No. 500/220 kV transformers and 28 No. 220/132 kV transformers installed at these grid stations. At 220 kV level, there are 37 grid stations with a transformation capacity of 24,063 MVA. There are 101No. 220/132 kV transformers installed at 220 kV and after inclusion of 28 No. 220/132 kV transformers installed at 500 kV grid stations, total 220/132 kV transformers come to 129. An overview of the existing transmission capacity shows that EHV network is barely enough to cater for the present generation capacity. It has been noted that out of 33, 500/220 kV transformers, 8 are overloaded. Similarly, out of 129 No. 220/132 kVtransformers,90areoverloaded,whichifnotrectifiedareapotentialthreattothereliableoperationofthesystem. It is imperative that NTDC besides strengthening of existing transmission network should ensure timely completionoftheplannedtransmissionrequirementsidentifiedforevacuationofpowerfromtheupcominggeneration projects.

7

State of Industry Report 2015

1.8 Projected Capacity and Power Balance of NTDC SystemThe following table provides peak time demand in NTDC system, year-wise capacity additions and resulting installed capacity till 2020-21:

Financial Year ending 30th June

NTDC Peak Demand (MW)

Capacity Addition per yearin NTDC System (MW)

Total Installed Capacityper year (MW)

2015 21,701 1,504 22,9282016 23,711 689 23,6172017 24,871 6,643 30,2602018 26,105 9,961 40,2212019 27,408 1,279 41,5002020 28,773 4,580 46,0802021 30,156 2,200 48,280

Source: NTDC

Ifnewgenerationasnotedaboveisaddedtothesystem,itisexpectedthatby2017,negligibledeficitwillbefaced at the peak time only, while no load shedding during other times be required. However, for this to happen, not only the generation but the transmission and distribution systems must be strengthened so that constraints in the existing system are completely removed.

1.9 Expansion Plan of NTDCTo cater for the needs for transmission of power from upcoming generation power plants and strengthening of existing system, grid station expansion plan of NTDC over the next two years is shown in the following table, which provides that by the end of 2017, 3 new grid stations at 500 kV level will be added which will add 3750 MVA in transformation capacity in the system, the fourth 500 kV grid station will be complete by the end of 2020 adding additional 1500 MVA to the system. At 220 kV level, 8 new grid stations with a cumulative transformation capacity of 5750 MVA will be added in the system. Similarly, one overloaded 500 kV grid station will be strengthened, while six such grid station at 220 kV level be improved by 2019-20. The adequacy of NTDC system is discussed further in the later sections of the report.

Grid Station Expansion Plan of NTDC

Period of Report

500/220 kV Grids 220/132 kV Grids

Nos. MVA Capacity

Expected COD

*Estimated Cost (Rs. Million) Nos. MVA

CapacityExpected

CODEstimated Cost

(Rs. Million)New Grid Station

2015-16 3 3750 2016-17 20,399 8 5750 2016-17 26,2332016-17 1 1500 2019-20 3,500 - - - -

Extension2015-16 1 430 2016-17 697 - - - -

Addition/Reinforcement of Transformers at Overloaded Grid Stations2015-16 1 0 2016-17 1,413 - - - -2016-17 - - - - - - - -2017-18 - - - - 6 3000 2019-20 16,400

* The cost of 500/220 kV Grid Stations also include the cost of 220/132 kV Transformers.Source: NTDC

1.10 Timely Completion of Upcoming ProjectsIt is noted that by June 2017, a large generation capacity has been planned to be added which is expected to reduce the gap between supply and demand. Similarly, transmission system is required to be strengthened for evacuation of power from these generation facilities. However, it is noted that to meet these targets, timely completion of projects is critical and of paramount importance. From the above tables it is also evident that more than 10,000 MW will be surplus to the demand requirements by 2021, which will essentially be required to maintain necessary reserve and operating margins in the system as per international practices.

8

State of Industry Report 2015

1.11 Power Balance of K-Electric SystemThefollowingtableshowsyear-wiseprojectedfiguresofpowerbalancesinrespectofK-Electrici.e.plannedgenerationcapability,projecteddemandgrowthrate,projecteddemandduringpeakhoursandsurplus/deficit:

Financial Year ending

30th June

Generation* Capability as per

K-EL (MW)

KEL's Projected Demand Growth

Rate (%)

KEL's Projected Demand during

Peak hours (MW)

Surplus/ (Deficit) (MW)

2015 2,632 - 3,056 -424

2016 2,752 (including 20 + 100 MW SNPC) 5.00 3,209 -457

2017 2,804 (including 52 MW FPCL) 5.00 3,369 -565

20183,674

(including 450 LNG + 420 Coal Conversion)

5.00 3,538 136

2019 4,374 (including 700 MW Coal)** 5.00 3,715 659

2020 4,374 5.00 3,900 474* includes 650 MW from NTDC** Subject to approval of acceptable tariff by NEPRA and other regulatory approvals.Source: K-Electric Limited

It may be noted that the above generation capability data as reported by K-Electric includes 650 MW from NTDC implying thereby that K-Electric will barely meet its requirements by 2019 provided that additional generation capacity is timely achieved.

1.12 Environmental Impact of Coal Based Power PlantsInduction of coal based power plants at a large scale would affect the environmental balance due to various issues related to coal power. These include increased emission levels, particulate matter and disposal of ash. Similarly, the coal-based power plants proposed to be constructed in mid-country would also require a robust transportation system for a continued supply of coal. The environmental issues put a huge responsibility on the relevant environmental agencies for monitoring coal based projects during their planning, construction and operation stages.

1.13 Infrastructure DevelopmentThe Federal Government is also required to ensure availability of infrastructure i.e. road/rail facilities before the completion of coal-based projects for transportation of coal from the port to project sites without interruption. Efforts on war footing are also required for the development of infrastructure at port and transmission lines for R-LNG supply to upcountry power plants.

1.14 Data ReportingThe DISCOs have been continuing with manual record keeping and its functionaries are prone to in-accurate reporting as well as human errors and discretion, which distort reported data leading to skewed decisions, not reflectingthetruepicture.Inviewthereof,itisreiteratedandemphasizedthatallpowersectorentitiesshouldimmediately explore and adopt automation to have system generated reports to minimize the human factor thus forming the basis for informed and real time decisions.

1.15 Power Market ReformsThe Authority granted transmission license to NTDC in 2002, which required NTDC to create a number of entities within its setup. In this respect, CPPA was also created which was responsible for procurement of power on behalf of DISCOs. Similarly, an independent system operator, a network operator and a contract registrar were also to be created. The operations of the sector were expected to move forward from a single-buyer mode tosingle-buyer-plusmodeandfinallytoabilateralcontractmarket.Underthestructureofbilateralmarket,theCPPA and the contract registrar were to be taken out of the NTDC umbrella for the transparency of functions. Over the years, however, the power sector structure could not make progress as stipulated in the transmission license as the single-buyer mode has continued. Almost all of the major contracts by IPPs have been entered

9

State of Industry Report 2015

into on long terms with CPPA/NTDC through sovereign guarantees of the GoP. During the year, the Authority consideredaLicenseeProposedModification(LPM)byNTDCforrevisioninitstransmissionlicenseandcreationofanewentityasCPPA-G.NEPRAhasapprovedsuchmodification.CreationofCPPA-Gwillhelpprovidingenablingenvironmenttomovefromsinglebuyermodeltosinglebuyerplusmodelandfinallytothebilateralcontract mode.

1.16 Receivables of DISCOsThe overall receivables of DISCOs at the end of June, 2015 increased by Rs. 120 billion over the previous year. it is noted that apart from Federal Government and agriculture tube wells in Balochistan which show a reduction of around Rs. 0.7 billion and Rs. 0.2 billion respectively, receivables from other areas increased. As on 30th June, 2015 the overall distribution sector receivables stood at Rs. 633 billion (including Rs. 43.97 billion pertaining to K-Electric).

1.17 Transmission and Distribution (T&D) Losses of DISCOsDISCOs' performance in the area of losses, has been mixed. Certain DISCOs have reported very slightimprovement; others have maintained the same level of losses, whereas a number of DISCOs have reported higher losses than they had reported to NEPRA during earlier years. In this respect, PESCO and SEPCO have shown increase in losses. Adding further to T&D losses is the low recovery ratio of DISCOs. The Authority assessed a recovery target of 100% while setting the consumer tariff for DISCOs, however according to the information provided by DISCOs, the actual level of recovery remained around 89.16% for the year 2014-15.

1.18 Circular DebtCircular debt is still a major issue confronting power sector. One of the contributors of circular debt remained hightransmissionanddistributionlossesinDISCOs.Basedonthecurrentlynotifiedconsumer-endtariffof10th June, 2015, if DISCOs fail to show any improvement in their actual level of losses, the impact of missing the Authority’s set T&D loss target would result in an annual gap of Rs. 41 billion. It is pertinent to mention that the authorityhassetanaveragelosstargetof15.29%for2014-15,whereasDISCOs'reportedlossesforthesameperiod remained around 18.73%.

1.19 Tariff Differential Subsidy GoP is providing Tariff Differential Subsidy (TDS), primarily to the agriculture and residential class of consumers, having consumption of up to 300 units. The GoP intends to decrease the gap between NEPRA determined consumer-endtariffandtheGoPnotifiedtariffthroughimpositionofTariffRationalizationSurchargeonsomecategories of consumers of different DISCOs so that its burden in the shape of TDS is reduced from Rs. 135 billion to Rs. 65 billion.

1.20 Multi-Year Tariff (MYT) Regime for DISCOsAccordingtoNEPRATariffStandardsandProcedureRules,1998determinationofDISCOs'tariffrequiresaveryelaborate procedure to be followed. DISCOs are required to provide extensive information which is generally delayed. Furtherdelaysmayoccurduringnotificationof tariff.Conducting suchproceedingsannuallyhavebeenprovingtobeinefficient.Therefore,tostreamlinetheprocessandtoregulatetherevenuestreamsfortheentitiesinvolvedandfurthertobringin-builtincentivesandefficiency,NEPRAhasdecidedtore-introduceMYTregime. MYT being a performance based tariff will require DISCOs to achieve certain targets of performance over the control period to receive revenue streams based on known tariffs.

1.21 Generation Capacity of K-ElectricIt is noted that K-Electric was required to enhance its generation capacity by 1000 MW over the capacity indicated in its Generation License. K-Electric has added 1034 MW in the system however it has decommissioned or permanently closed 685 MW of its existing generation capacity. Therefore, effectively about 349 MW has been added by K-Electric considering retirement and permanent closure of its generation facilities. Inability of K-Electric to effectively increase its generation capacity has made it dependent on external power sources, including the import from NTDC system. To meet its demand, it has to operate its generation facilities and other resources specifically650MW fromNTDCat theirmaximum. It isobserved that reservemarginsperinternational standards are required in order to avert any breakdown in the system.

10

State of Industry Report 2015

The contract of power supply between NTDC and K-Electric has already expired, however, the power is still being imported out of necessity. The Authority has advised K-Electric and NTDC to enter into a contract if such arrangement is to continue, without which import of 650 MW will be ostensibly illegal and unlawful.

1.22 K-Electric Transmission and Distribution Systems The Authority has noted that recently with increase in load demand, the tripping on Extra High Voltage Transmission (EHT) network has increased. Normally, EHT is considered the strongest link between power generation and consumers as it is used only for transporting electricity, therefore, increased tripping indicates weakness in K-Electric system.

TheloadingprofileofEHTnetworkduringJune2015,showsthatoutofatotal129powertransformers,45are overloaded. Out of these, 16 are overloaded between 90% and 100% whereas a number of transformers are noted to be operating at more than 100% of their rated capacity. It is also noted that in order to ensure that power transformers are loaded within their limits, feeders are isolated by K-Electric as a routine, so that overloading can be avoided. The Authority has noted that EHT system of K-Electric lacks enough capacity to transmit power to the underlying network. NEPRA has taken cognizance of this unwarranted situation and is proceeding as per law.

1.23 Upfront TariffsUnder NEPRA Tariff (Standards and Procedure) Rules 1998, it takes around four months to determine tariff of a facility. Taking cognizance of the electricity shortage in the country, which has direct bearing on the social and economic health of consumers besides GDP, NEPRA under its Up-front Tariff (Approval & Procedure) Regulations, 2011 has decided to introduce the regime of up-front tariff. Under this regime, the time has been reduced to 10 days for determination by the Authority in case the investors decide to opt for the respective upfront tariff for thattechnology.Theregime,besidesprovidingpredictabilityandlevelplayingfieldforallinvestors,willalsoallow inbuilt incentives for early completion of the projects. Accordingly, up-front tariffs for all technologies i.e. small hydropower, wind, solar, bagasse, R-LNG and coal have been announced by NEPRA. The up-front tariff for coal is basically structured on using local coal, which will reduce the import of oil and save from shocks of volatile oil market, which can rebound any time as has been experienced by power sector in the past. It is to be noted that the up-front tariffs announced by NEPRA are periodically revised in view of introduction of new technologies and international market trends.

1.24 Net-Metering RegimePakistan has a huge potential for solar-based energy. In order to make optimum use of this potential, NEPRA, besides announcing up-front tariff for solar technology, has also decided to introduce net-metering regime.

The regime will enable commercial units, industry and household consumers to install solar PV panels on their roof tops who will be able to sell surplus electricity in the national grid through the mechanism provided in net-metering regulations. This will not only provide an opportunity for the common man to earn energy based income but will also mitigate the shortfall of energy, bringing stability in the system. It is expected that GoP will introduceafinancialpackagetofacilitatehouseholdconsumersashasbeendoneinthecaseofsolartubewellschemes.

The introduction of this regime will encourage the investors to setup necessary solar panel and allied equipment manufacturing facilities in the country to further reduce its cost. Such facilities will help in generation of employment opportunities throughout the country. Solar panels and net-metering are also expected to encourage provision of electricity in remote areas through off-grid solutions.

1.25 Special Purpose Transmission Licence under Section 19 of NEPRA Act (Special Transmission Facilities for Private Entities)Only a distribution licensee has an exclusive right to construct, own, maintain and operate the 132 kV and 11 kVlines/networksinthespecifiedserviceterritoryofthatDISCOasperprovisionsunderSection20and21ofthe Act. Therefore, no entity can engage in the distribution regime except a DISCO. However, under Section 19

11

State of Industry Report 2015

of the Act, the Authority granted a Special Purpose Transmission Licence (SPTL) to a private entity to engage in construction,ownership,maintenanceandoperationofspecifictransmissionfacilities(66kVandabove)builtfor provision of transmission and interconnection services to NTDC and others by connecting its facilities at transmission and distribution networks.

SPTL regime will not only open the sector, it will reduce response time for attending faults, restoration of system and increase reliability of transmission and distribution networks. Due to this regime, the opportunities for the private sector for investment in generation and transmission facilities within reasonable resources will increase. It is expected that introduction of SPTL regime will facilitate off-grid solutions for supplying electricity through the technologies like solar and small hydropower plants.

1.26 RecommendationsIn view of the above, following recommendations are made:

1.26.1 For the power sector to come out of the existing crises, it is critical that timely completion of planned powergenerationprojects,specificallythroughChina-PakistanEconomicCorridorisensured.

1.26.2 For the protection of environment from the emissions by coal power projects, the relevant agencies must adopt an aggressive monitoring regime before and during operation of such power plants.

1.26.3 Infrastructure for coal transportation and R-LNG are potential hotspots on which the operation of the mid country coal power plants and R-LNG based power plants is dependent. In view thereof, it shall be ensured that infrastructure for coal transportation and R-LNG meet the timeline envisaged for respective projects.

1.26.4 Transmission and distribution are hardly adequate to meet the existing requirements and have little or no potential to absorb planned generation in the South. In view thereof, it is imperative that transmission and distribution systems may be strengthened and stabilized besides completion of new transmission and distribution systems planned to transmit electricity generated by upcoming projects.

1.26.5 The Federal Government may provide incentives to the households intending to enter into net-metering regime on the lines already announced for solar tube well schemes.

1.26.6 In order to reduce losses, control theft and improve the service delivery to consumers and effective revenue recording, use of technology i.e. smart meters/prepaid meters may be immediately introduced in all DISCOs.

1.26.7 Out-sourcingofinefficientserviceindistributionsystemmaybeexploredandconsidered by theDISCOs.

12

State of Industry Report 2015

PERFORMANCE OF GENERATION SECTOR 2

15

State of Industry Report 2015

2. PERFORMANCE OF GENERATION SECTOR

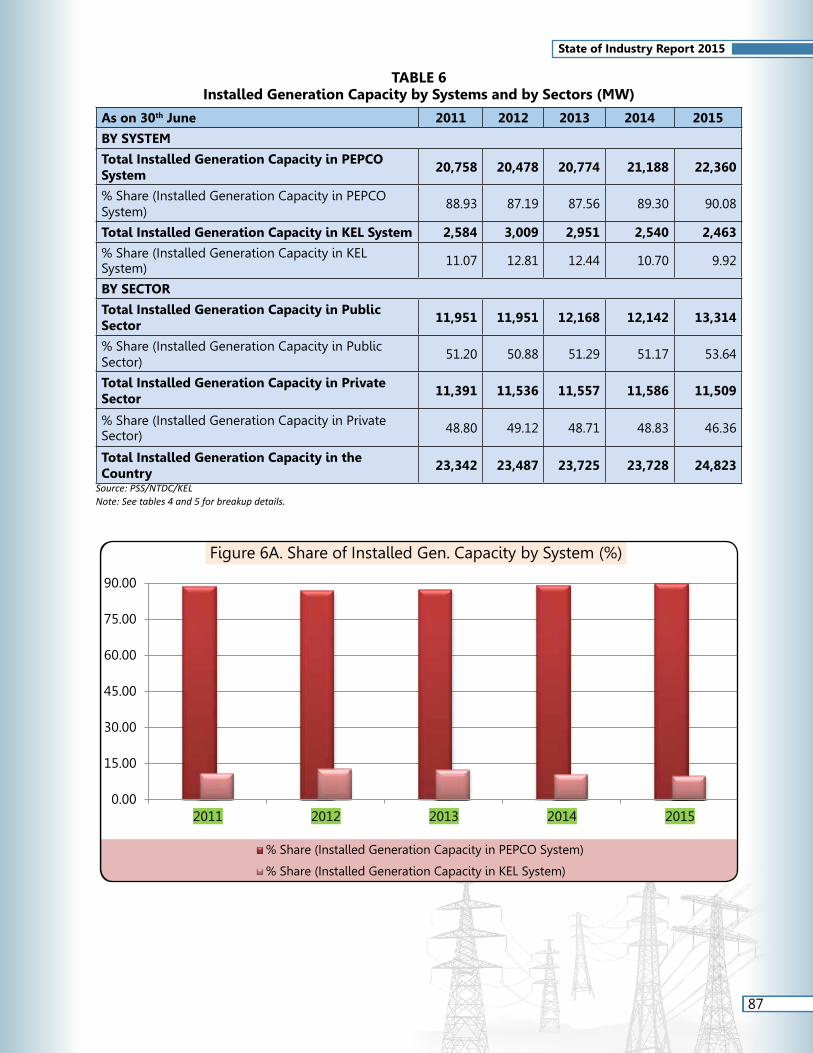

2.1 GeneralTheinstalledgenerationcapacityoftheNTDC'ssystemon30th June, 2015 stands at 22,928 MW, against 21,424 MW on 30th June, 2014 recording an increase of 1,504 MW or 7.02% over the last year. The power plants connectedwithNTDC'ssystemgenerated97,284GWhofenergyduringtheyear2014-15,whileoverthesameperiod during 2013-14, 93,903 GWh were produced; an increase by 3,381 GWh or 3.60%. During July, 2014 to June2015,themajoradditionstoinstalledcapacityofNTDC'ssystemareGuddu(747MW)andNandipur(425MW)thermalpowerplants.Inaddition,320MWhavebeenaddedtoNTDC'ssystemthroughrenewableandalternative energy (Solar, Wind and Bagasse) based power plants during 2014-15.

2.2 Source-wise Installed CapacityThe following table gives additional details of installed capacity and energy generation by different power plantsconnectedwithNTDC'ssystemandcomparisonoflasttwoyears:

SourceInstalled Capacity

(MW)Generation

(GWh)Variation

Capacity Generation

2013-14 2014-15 2013-14 2014-15 MW % GWh %

WAPDA Hydel 6,902 6,902 31,656 31,877 0 -- 221 0.70

IPPs Hydel 214 214 1,015 1,070 0 -- 55 5.43

Total Hydel 7,116 7,116 32,671 32,947 0 -- 276 0.84

GENCO-I 1,024 1,024 3,152 3,320 0 -- 168 5.32

GENCO-II 1,690 2,437 4,484 5,541 747 44.20 1,057 23.56

GENCO-III 1,965 2,390 5,307 5,203 425 21.63 -104 -1.96

GENCO-IV 150 150 112 141 0 -- 29 26.21

Total GENCOs 4,829 6,001 13,055 14,205 1,172 24.27 1,150 8.81

Thermal IPPs 8,723 8,735 43,706 44,332 12 0.14 626 1.43

Nuclear 650 650 4,208 5,006 0 -- 798 18.97

Wind 106 256 263 459 150 141.50 196 74.58

Bagasse 0 70 0 308 70 -- 308 --

Solar 0 100 0 28 100 -- 28 --

GRAND TOTAL 21,424 22,928 *93,903 *97,284 1,504 7.02 3,381 3.60* The generation from SPPs/CPPs and energy import from Iran have not been included.Source: NEPRA

2.3 HydropowerIt may be noted that the installed capacity of WAPDA Hydropower remaining at 6,902 MW in 2014 and 2015, the 31,877 GWh generated in 2014-15 shows an increase of 221 GWh from the last year. Similarly, the IPP (hydel) also contributed 55 GWh more in the system during 2014-15 with the same installed capacity as in 2013-14. The hydropower production pattern over the year remained consistent with the historical trends. The availability and overall performance of hydropower plants has also remained satisfactory during the 2014-15.

2.4 ThermalOn the thermal side, overview of the public sector GENCOs is as follows:

2.4.1 Jamshoro Power Company Limited (GENCO-I)There has been no increase in the installed capacity of 1,024 MW of GENCO-I Power Stations at the end of June, 2015 over that of 2014. The GENCO-I has a dependable capacity of 830 MW. The energy generated by GENCO-I during the 2014-15 was 2,961 GWh, while, it was 3,153 GWh in 2013-14; a decrease of 192 GWh or 6.09%, over lastyear.NetelectricalefficiencyofGENCO-Iduring2014-15stoodat28.30%.Withacapacityutilizationof

16

State of Industry Report 2015

45.66% due to forced outages and various maintenance issues, the overall performance of GENCO-I has not been satisfactory.

2.4.2 Central Power Generation Company Limited (GENCO-II)Total installed capacity of GENCO-II, up to 30th June, 2015 has been noted as 2,437 MW, while the capacity available for generation i.e. the dependable capacity is observed as 1,952 MW. The installed and dependable capacities of GENCO-II were 1,690 MW and 1,180 MW respectively at the end of June, 2014. During the 2014-15, the installed capacity of GENCO-II has increased by 747 MW or 44.20%, as compared to 2013-14, due to the addition of Guddu 747 power plant. The energy generated by GENCO-II during the 2014-15 has been recorded at 5,610 GWh, while, it was 4,444 GWh during the 2013-14. The energy generated by GENCO-II during the 2014-15, has increased by 1,166 GWh or 26.24%, compared with that of the last year.

It is observed that various units of GENCO-II have been off-bar for more than two years due to various maintenance issues, forced outages, fuel constraints and rehabilitation activities etc. and are not being fully utilized. With annualefficiencyof33.95%andcapacityutilizationofonly32.43%,theoverallperformanceofGENCO-IIhasbeen unsatisfactory.

2.4.3 Northern Power Generation Company Limited (GENCO-III)Total installed capacity of GENCO-III, up to 30th June, 2015 has been noted as 2,151 MW, while the capacity available for generation i.e. the dependable capacity is observed as 1,925 MW. The installed and dependable capacities of GENCO-III were 1,726 MW and 1,530 MW respectively at the end of June, 2014. During the 2014-15, the installed capacity of GENCO-III has increased by 425 MW or 21.63%, as compared with that of the year 2013-14, due to the addition of Nandipur power plant. The energy generated by GENCO-III during the 2014-15 was 4,627 GWh, while it was 5,307 GWh during the 2013-14 showing a decline of 680 GWh or 12.81%, compared with the last year.

ItisobservedthatvariousunitsofGENCO-IIIhaveremainedoff-barsincelongduetotheirpoorefficiencylevels.TheoverallnetefficiencyofGENCO-III isalsovery lowat24.84%.Furthermore,duetovariousmaintenanceissues, forced outages and fuel constraints etc. resulting in annual capacity utilization of 38.44%, the overall performance of GENCO-III cannot be termed as satisfactory.

2.4.4 Lakhra Power Generation Company Limited (GENCO-IV)Total installed capacity of GENCO-IV, up to 30th June, 2015 has been noted as 150 MW, while the capacity available for generation i.e. the dependable capacity is observed as 30 MW. GENCO-IV had three units of 50 MW, however, due to lack of proper maintenance and cannibalization, only one unit is in working condition though at a reduced level for the past number of years. GENCO-IV during 2014-15 generated 102 GWh.

It may be noted that, against the installed capacity of 150 MW, approximately, one third capacity of GENCO-IV isavailableforgeneration,whichalsoisnotbeingfullyutilizedduetoforcedoutagesetc.Withnetefficiencyof17.74%, the overall performance of GENCO-IV has not remained satisfactory.

2.4.5 Overall Performance of GENCOsItisnotedthat,althoughthetotalinstalledcapacityofGENCOs'powerplantshasincreasedby1,172MWduringthe2014-15(includingefficientmachinesatGuddu),ascomparedwiththecapacityof thesepowerstationsduring theyear2013-14, the impactof increasedcapacityofGENCOspowerplants isyet tobe reflected inthe performance of these power stations. It is noted that overall non-availability of GENCOs on account of fuel constraints reduced in 2014-15 due to better availability of fuel at all the GENCO power plants. The overall furnaceoilinventoryatthefiveplantssuppliedbyPSO(Muzaffargarh,Jamshoro,KAPCO,HUBCOandNandipur)was only 49,123 metric tons in June 2014, which increased to 223,819 metric tons in June 2015.

It is also observed that other than fuel, GENCOs power plants remained off bar, due to various maintenance issues, forced outages, and rehabilitation activities etc. and their available capacity has not been fully utilized. The prevailing situation warrants maximum generation from public sector thermal power plants to cater for the dire need of the system.

17

State of Industry Report 2015

2.4.6 Independent Power Producers (IPPs)Total installed and dependable capacities of thermal IPPs at the end of June, 2015 are noted as 8,735 MW and 7,935 MW respectively, representing a ratio between dependable and installed capacities of 0.91. These capacities were 8,723 MW and 7,960 MW during June, 2014 representing a ratio of dependable and installed capacities as 0.912. The energy generated by thermal IPPs during the year 2014-15 is noted as 45,369 GWh, against 44,809 GWh during the year 2013-14.

It is also noted that due to certain disputes with NTDC/WAPDA, two IPPs namely Japan Power and SEPCOL are not contributing power to the grid and if these issues are properly addressed, approximately 270 MW will be added to the National Grid, which will help reduce the demand and supply gap of the system.

2.4.7 Installed versus Dependable CapacityThe ratios between the dependable capacity and the installed capacity of the four GENCOs are also noted here:

Ratio of Dependable Capacityand Installed Capacity

GENCO-I(JPCL)

GENCO-II(CPGCL)

GENCO-III(NPGCL)

GENCO-IV(LPGCL)

2013-14 0.81 0.70 0.78 0.20

2014-15 0.81 0.80 0.80 0.20Source: NEPRA

The ratios of dependable capacity and installed capacity for GENCOs and IPPs (indicated earlier) provide clear evidence about the manner in which the private and public sectors have been able to maintain their power plants. Whereas such ratios are more than 90% in both the years for IPPs, GENCO-I has a ratio of slightly more than 0.8, whereas ratios close to 0.8 have been achieved by GENCO-II and GENCO-III, only after new plants were added (Guddu 747 and Nandipur 425). The present state of GENCO-IV is evidence of typical public sector management failure, which has deprived the sector of a source of cheap power.

2.4.8 Manpower to MW RatioThe following table compares the ratio between the number of employees and MW installed in different power plants in Pakistan and other countries. It may be noted that only one plant in Bangladesh has comparable ratio with GENCO-II, whereas all other power plants have very low ratios of manpower per MW.

S.No.

Power Plant LocationInstalled Capacity

(MW)No. of

EmployeesManpower

to MW ratio

Capacity Utilization

(%)

1 HUBCO Pakistan 1,292 300 0.232 64.48

2 KAPCO Pakistan 1,345 588 0.437 58.81

3 Lal Pir Power Pakistan 362 110 0.303 54.29

4 Pak. Gen. Power Pakistan 365 110 0.301 40.29

5 Tongi Power Bangladesh 105 98 0.933 ---

6 NTPC India 652 295 0.452 ---

7 MSEB India 912 277 0.303 ---

8 Power Gen. UK 700 33 0.047 ---

9 GENCO-I Pakistan 1,054 1,578 1.490 45.66

10 GENCO-II Pakistan 2,431 1,977 0.813 32.43

11 GENCO-III* Pakistan 1,921 2,634 1.370 38.44

12 GENCO-IV Pakistan 150 546 3.640 53.33* Excluding Nandipur and Shahdara Power Plant and including NGPS Multan.Source: NEPRA, GENCOs

18

State of Industry Report 2015

2.5 Nuclear (CHASNUPP-I and II)During the year 2014-15, total installed and dependable capacity of Nuclear power plants connected with NTDC'ssystem,arenotedas650MWand615MWrespectively,whicharethesamefortheyear2013-14.Theenergy generated by Nuclear power plants during the year 2014-15 stands at 5,006 GWh, which is an increase of 798 GWh over the energy during the year 2013-14. The overall performance of Nuclear power plants connected withNTDC'ssystemhasremainedsatisfactoryduringtheyear2014-15asnomajoroutageisnoted.

2.6 WindDuring2014-15,totalinstalledcapacityofwindpowerplantsconnectedwithNTDC'ssystem,isnotedas256MW, while, it was 106 MW during the year 2013-14. The installed capacity of wind power plants has increased by 150 MW during the year 2014-15 due to the addition of three wind based power plants (FWEL-I, FWEL-II and TGF) having capacity of 50 MW each. 459 GWh of energy has been generated by wind power plants during the 2014-15 against 263 GWh during the 2013-14.

2.7 BagasseDuring 2014-15, three new bagasse based power plants (JDW-II, JDW-III and RYKML) have been connected withtheNTDC'ssystemhavingtotalinstalledcapacityof70MW,while,therewasnobagassebasedgeneratingfacility during the year 2013-14. The energy generated by these power plants, during the 2014-15 is noted as 308 GWh.

2.8 SolarDuring2014-15, 100MWoffirst solarpowerproject (Quaid-e-AzamSolar)hasbeenadded to theNTDC'ssystem, contributing 28 GWh.

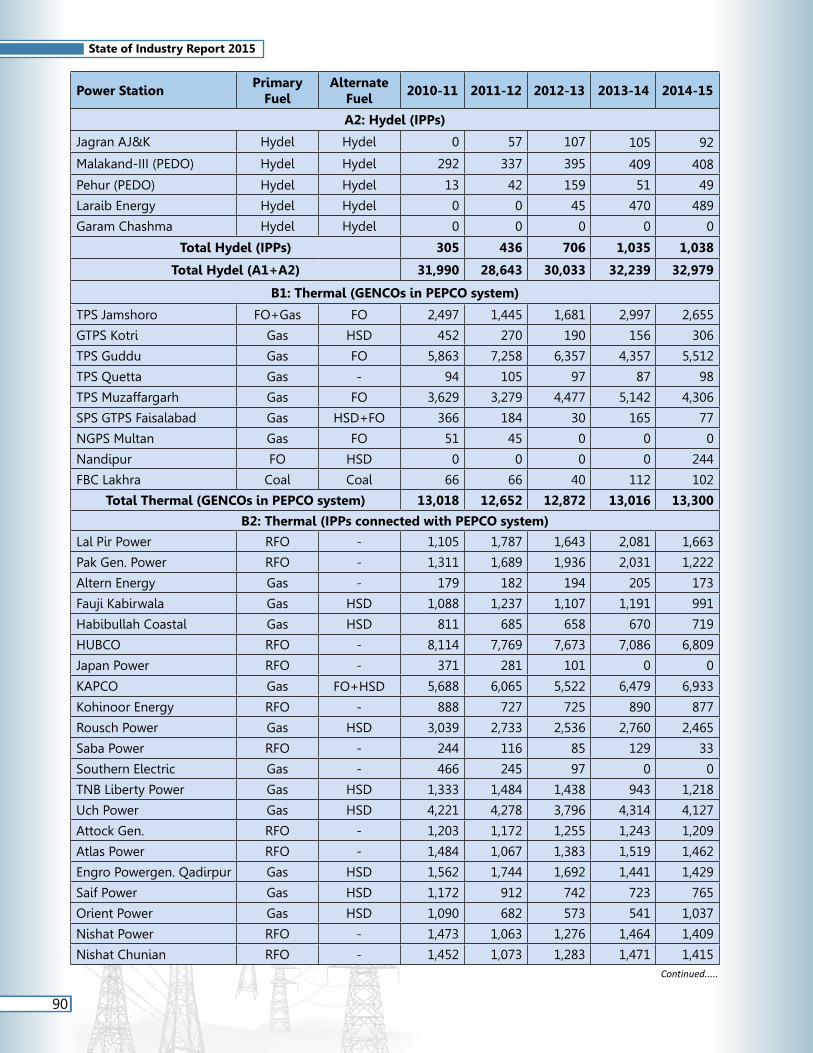

2.9 K-Electric LimitedAs for K-Electric Limited, the Implementation Agreement (IA) and the Amended Implementation Agreement (AIA) put binding requirements on it to make certain investment for refurbishment and development of generation, transmission and distribution sectors. It is noted that K-Electric was required to enhance its generation capacity by 1000 MW over the capacity indicated in its Generation Licence. K-Electric has added the following facilities to its Generation capacity:

Name of Commissioned Plants Capacity (MW) Year

Korangi Combined Cycle Power Plant (KCCPP) 220.00 2009

Gas Engines at Korangi 97.31 2013

Gas Engines at SITE 97.31 2013

CCPP at Bin Qasim 572.67 2013

Steam Turbine at KCCPP 27.50 2015

Steam Turbine at Gas Engines at Korangi 10.00 2015

Steam Turbine at Gas Engines at SITE 10.00 2015

Total 1,034.79Source: K-Electric Limited

19

State of Industry Report 2015

However, at the same time, K-Electric also retired or permanently closed following power plants:

Name of Retired or Closed Plants Capacity (MW) Year

Korangi Thermal Power Station (Unit 4) 125 2013

Korangi Town Gas Turbines Power Station (Units 1, 2 & 4) 75 2013

SITE Gas Turbines Power Station (Units 1, 3, 4 & 5) 100 2013

Korangi Thermal Power Station (Unit 3) 125 2015

Korangi Town Gas Turbines Power Station (Unit 3) 25 2015

SITE Gas Turbine Power Station (Unit 2) 25 2015

Bin Qaim Unit 4 (closed) 210 2012

Total 685Source: K-Electric Limited

Therefore, effectively about 349 MW has been added by K-Electric considering retirement and permanent closure of its generation facilities. Since K-Electric is responsible for maintaining integrated systems of generation, transmission and distribution, therefore shortage of generation capacity is not helpful in overcoming supply and demand gap. Inability of K-Electric to effectively increase its generation capacity has made it dependent on external power sources, including the import from NTDC system. To meet demand, it has to operate its generationfacilitiesandotherresourcesspecifically650MWfromNTDCattheirmaximum.Itmayalsobenotedthat the contract of power supply between NTDC and K-Electric has already expired, however, the power is still being imported out of necessity.

20

State of Industry Report 2015

PERFORMANCE OF TRANSMISSION SECTOR

PERFORMANCE OF TRANSMISSION SECTOR 3

23

State of Industry Report 2015

3. PERFORMANCE OF TRANSMISSION SECTOR

3.1 GeneralThe transmission line network of NTDC includes 5,197 km long transmission lines operating at 500 kV level and 9,814 km long 220 kV lines. The power generation plants connected at high voltage levels are summarized here:

Voltage Level 500 kV 220 kV 132 kV Total

Installed Capacity (MW) 6,948 9,625 6,172 22,745Source: NTDC

As of 30th June 2015, NTDC is maintaining 13 No. 500 kV grid stations with a transformation capacity of 18,624 MVA. There are 33 No. 500/ 220 kV transformers and 28 No. 220/132 kV transformers installed at these grid stations. At 220 kV level there are 37 grid stations with a transformation capacity of 24,063 MVA. There are 101 No. 220/132 kV transformers installed at 220 kV and after inclusion of 28 No. 220/132 kV transformers installed at 500 kV grid stations, total 220/132 kV transformers come to 129.

3.2 Overloading of Existing Power TransformersAs discussed earlier, the transmission system is critical for a reliable power supply to DISCOs. The following table showsoverloaded(above80%)transformersat500kVand220kVgridstationsindifferentregionsdefinedbyNTDC. It is also noted that on average around 11,000 MW to 15,000 MW have been transmitted through these transformers in different months depending on the generation and electricity load demand. With increasing demand and more generation expected in the system as a result of upcoming projects, the overloading of below noted transformers would also increase in future years.

A. Over Loading of 500 kV and 220 kV Transformers at 500 kV Grid Stations:

(above 80%)

Continued.....

24

State of Industry Report 2015

(above 80%)

(above 80%)

Source: NTDC

B. Over Loading of 220 kV Transformers at 220 kV Grid Stations

Continued.....

25

State of Industry Report 2015

(above 80%)

Continued.....

26

State of Industry Report 2015

Shikarpur

T-1 220/132 160 700 660 94.29 T-2 220/132 160 700 640 91.43 T-3 220/132 160 700 640 91.43

T.M.K. Road

T-1 220/132 160 700 690 98.57 T-2 220/132 160 700 680 97.14

Khuzdar T-1 220/132 160 700 680 97.14

(above 80%)

There are 13 No. 500 kV Grid Stations with 33 transformers at 500/220 kV level. Out of these 8 transformers are loaded above 80% of their rated capacity. Similarly, out of total 129 No. 220/132 kV transformers 90 transformers are overloaded representing around 70% overloading in the system.

3.3 Power Dispersal Constraints in Transmission NetworksIn addition to overloading of EHV transformers, constraints in power dispersal from certain major power plants andqualityissuesinNTDC'ssystemhavealsobeenreported.AsperinformationanddatareportedtoNEPRA,following power plants faced evacuation problems due to transmission constraints.

3.3.1 Uch-II Power (Pvt.) LimitedUch-IIisalowBTUGasfiredpowerplanthavinggrosscapacityof404MWandnetcapacityof375.2MWlocatedat Dera Murad Jamali, District Naseerabad, Balochistan. It was planned to construct a 125 km long 220 kV double circuit twin bundle transmission line form Uch-II power plant to Sibbi substation for evacuation of power. The proposed transmission line was to pass through three (03) Districts of Balochistan Province (a) Naseerabad (b) Kachi and (c) Sibbi. In addition, a 500 kV grid station at Shikarpur was also to be constructed.

Due to non-fulfillment of contractual obligations by NTDC, Uch-II power plant is facing power dispersalproblems, transmission system constraints and frequent tripping on EHV networks. The reasons for delay in completion of the transmission projects by NTDC are reportedly: (a) Late retendering, (b) Bad law and order situation in the area, (c) Security threats to Supervisory Engineers, Revenue Staff and Construction Crews and (d) Failure to start major construction activity on time.

3.3.2 Engro Powergen Qadirpur LimitedEngro Powergen Qadirpur Limited (EPQL) is a combined cycle power plant having installed capacity of 226.52 MW with derated capacity of 223.8 MW located at Qadirpur, District Ghotki, Sindh. This plant is also facing the problem of low dispatch/part load operation due to limitation and constraints of auto-transformer at 500 kV Guddu Grid Station, which is reportedly resulting in a revenue loss of Rs. 80 million per year to the GoP.

3.3.3 Altern Energy LimitedAltern Energy Limited (AEL) complex is facing frequent tripping due to over/under voltage from 66 kV WAPDA grid. Further during the year 2012-13 and 2013-14, AEL has experienced tripping 63 and 99 times respectively due to WAPDA grid failure resulting in generation loss of 1459.25 MWh and 1309.57 MWh respectively.

3.3.4 TNB Liberty Power LimitedThe power evacuation constraints confronted by the company are due to the tripping of grid system and other technical reasons of transmission lines.

3.3.5 Habibullah Coastal Power Company LimitedThe two major issues which have been faced by the generation facility resulting in non-optimal power evacuation are, gas curtailment during the winter months and low voltage on the power system.

3.3.6 Foundation Power Company (Daharki) LimitedAs per PPA signed between NTDC and FPCDL, the plant was to be connected with 220 kV New Rohri Grid, but due to delay in construction of 220 kV grid and transmission lines, the Daharki power complex was temporarily connected with 132 kV grid station Sadiqabad. NTDC constructed a temporary grid of 220/132 kV adjacent to

27

State of Industry Report 2015

FPCDL. FPCDL has experienced many tripping since commissioning due to the problems in transmission lines between Guddu and Sadiqabad. Later on, 220 kV New Rohri grid was commissioned and power dispersal was provided on both end, but still major part of power dispersal is through 132 kV Sadiqabad which is not an efficientsolution.