state of the business - american logistics association (ala) · for deca shoppers as deca sow...

TRANSCRIPT

Copyright © 2017 The Nielsen Company. Confidential and proprietary.

July 2018

Andy HarbNadja Stein

STATE OF THE BUSINESS

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

2

AGENDA

Retail and Consumer Areas of Growth

DeCA Business Review

Appendix: Methodology

Economic Indicators

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

3

$791 $813 $832 $836 $845

253 254 254 253 252

52 weeks ending4/5/14

52 weeks ending4/4/15

52 weeks ending4/2/16

52 weeks ending4/1/17

52 weeks ending3/31/18

Billi

on

s Dollar Sales

Unit Volume

Source: Nielsen Answers, Total U.S. All Outlets Combined (plus Convenience), All Departments,

All Brands, “trend” means % change 52 weeks vs. year ago

All Departments

MODEST IMPROVEMENT IN U.S. RETAIL SALES

UPC-coded items

Dollar Trend (%) +2.7 +2.3 +0.5 +1.2

Unit Trend (%) +0.4 +0.2 -0.5 -0.3

Avg U Price Trend (%) +2.3 +2.1 +1.0 +1.5

% U sold on Promo 31.6 30.7 30.9 30.5

$ sales up 1.2%

as unit sales fell

0.3% with a price

increase of 1.5%

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

4

2.11.9

-0.4

0.7

2Q2015 3Q2015 4Q2015 1Q2016 2Q2016 3Q2016 4Q2016 1Q2017 2Q2017 3Q2017 4Q2017 1Q2018

DOLLARSUNITS

Source: Nielsen Answers, Total U.S. All Outlets Combined (plus Convenience), All Departments, All Brands, January 2015 – March 2018

All Departments sales growth vs. year ago quarter

U.S. FMCG MARKET – UPTICK IN DOLLARS AND UNITS IN Q1 2018

UPC-coded items

As we dissect these declines, it is clear

that changes afoot are not a slowdown,

but rather a shift in where growth is

occurring

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

5

WHERE ARE RETAILERS FINDING GROWTH?

Driving the health & wellness growth wave

Winning the eating occasion

Engaging in digital & e-commerce

Staying connected with the right assortment

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

6

31%

28%

14%

11%

9%

3%

2%

2%

1%

1%

1%

1%

Beauty Care

Pet Care

Health Care

Personal Care

Household Care

Packaged Grocery

Produce

Meat

Dairy

Bakery

Alcohol

Frozen Foods

26.9%

73.3%

27.3%

28.7%

17.8%

41.4%

18.4%

46.0%

67.4%

57.0%

0.8%

49.3%

NON-EDIBLE MOST COMMONLY PURCHASED ONLINE

E-COMM

E-COMMERCE – DEPARTMENT INSIGHTS

$ GROWTH

% OF ONLINE SHOPPERS PURCHASING THIS DEPT

Source: Nielsen Total Store Report, E-commerce measurement, 52 weeks ended Oct. 28, 2017 vs. year-ago

49% OF SHOPPERS

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

7

GENERATION X SPENDING HEAVILY ON MEAL KITS AND E-GROCERY

E-COMM

Source: Nielsen Buyer Insights, April 2016 – March 2017, Total U.S.; percentages may not total 100% due to rounding

28%

46%

33% 35%

47%

42%

52% 51%

25%

12% 14% 14%

U.S. Population Digital Meal Order &Delivery

E-Grocery Meal Kits

Baby Boomers

(55+)

Generation X

(35-54)

Millennials

(18-34)

DOLLAR SHARE BY GENERATIONAL COHORT

“Kroger’s newest

acquisition is a fast-

growing meal kit

company”Kroger will make Home

Chef meal kits available

online and in its storesCSA news, May 23 2018

“Ahold/Delhaize and

Giant Landover

partner with Hello

Fresh”CSA news, June 52018

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

8

CONSUMERS CONTINUING TO SPEND MORE AWAY FROM HOME

OCCASION

Source: U.S. Department of Agriculture – Economic Research Service (ERS), Food Expenditure Data *Preliminary 2017 results, dated to Nov. 2017

54.6%

49.7%

45.4%

50.3%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

At Home Away From Home

TOTAL FOOD EXPENDITURE - $ SHARE

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

9

HEALTH CLAIMS SEEING GROWTH IN U.S. FOOD – AND THERE IS

OPPORTUNITY IN COMMISSARIES

Source: Nielsen AOD H&W Characteristics; Fiscal 2018 - 52 Weeks Ending 05/19/18, UPC-Coded Items Only

-0.2

4.2

5.6

9.0

6.5

8.5

-5.9

-1.0

2.3

0.7

-0.9-0.1

TOTAL STORE GLUTEN FREE NATURAL GMO FREE NO ARTIFICIALCOLORS OR

FLAVORS

ORGANIC

Growth by Health Claim

Total U.S. Food DeCA

$40B $29B $20B $14B $13BTotal US Health

Claim Sales:

H&W

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

10

FREE FROM AND REDUCED CLAIMS STILL SHOWING LARGE GROWTH

H&W

FASTEST GROWING HEALTH & WELLNESS CLAIMS BY DOLLAR GROWTH

LATEST 52 WEEKS VS. YEAR-AGO

H&W Claim Dollars $ % Growth

Grain Free $795M 51.2%

Calorie Claim $1.12B 33.9%

Cruelty Free $925M 30.0%

Grass Fed $677M 27.6%

Corn Free $1.44B 22.1%

Source: Nielsen Retail Measurement Services, Core syndicated hierarchy, Total U.S., periods ended Dec. 30, 2017, UPC-coded

+27.2%

+19%

+13.3%

+23.3%

+9.3%

DeCA %$

growth

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

11

PRIVATE BRANDS RESURGENCE

PRIVATE BRANDS & SHARE – ALL DEPARTMENTS

Sources: Nielsen Strategic Planner (2009 data) & Nielsen Answers (2010-2017 data), Total U.S. – All Outlets Combined (xAOC), Total All Departments, * 52 weeks ending 3/31/2018

16.2%

16.8%

17.4% 17.4% 17.6%17.8% 17.8%

17.6%

18.1% 18.3%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018*

Dollar Sales Percent Change vs. Year Ago

Private Brand +4.9% +8.1% +3.0% +2.5% +2.8% +2.2% 0.0% +3.4% +4.5%

Branded +1.2% +3.3% +2.7% +1.6% +1.5% +2.6% +1.2% -0.4% +0.4%

UPC-coded items

ASSORTMENT

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

12

PREMIUM OFFERINGS ALSO SEEING GROWTH

ASSORTMENT

DOLLAR SHARE BY PRICE TIER

30%

11%

34%

27%

19%

26%

10%

19%

7%

17%

Private Label Branded

Tier 5 (Premium)

Tier 4

Tier 3

Tier 2

Tier 1 (Discount)

$ Growth

+6.3%

+1.8%

-0.7%

-1.6%

-7.4%

$ Growth

+10.6%

+4.1%

+3.7%

+1.6%

-2.3%

Source: Nielsen Analytic Product Attribute (APA) database by Nielsen Advanced Solutions Group, 52 weeks ended July 22, 2017 vs . year-ago

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

13

• Aldi’s SimplyNature

• CVS’s Gold Emblem Abound

• Food Lion’s Nature’s Place

• Giant Food’s Nature’s Promise Free from

• H-E-B’s Select Ingredients

• Kroger’s Simple Truth

• Meijer’s True Goodness

• Supervalu’s Wild Harvest

• Target’s Simply Balanced

• ShopRite’s Wholesome Pantry

• Stop & Shop’s Nature’s Promise Free from

Sources: cspinet.org and company websites

PRIVATE BRANDS ON BOARD WITH HEALTH & WELLNESS TRENDS

ASSORTMENT

Copyright © 2017 The Nielsen Company. Confidential and proprietary.

ECONOMIC INDICATORS

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

15

INCREASED CONSUMER CONFIDENCE TRANSLATES INTO INCREASED

PERSONAL CONSUMPTION

Sources: https://fred.stlouisfed.orgThe Conference Board® Global Consumer Confidence™ Survey, in collaboration with Nielsen; Total U.S. responsesData through June 2018 unless noted otherwise

124

131

127128.7 128.8

126.4

Jan Feb Mar April May June

Consumer Confidence

0.8 vs LY

Personal Savings Rate

3.2%

• Consumer Confidence continues to

trend upward • Continued gains in Employment &

Wages that outpace Inflation

• Personal Savings Rate is down vs

LY

• Consumers are taking on more

revolving debt

Employment

0.5% vs LY

70.6%

2.7% vs LYWages$26.98

4.4% vs LY

Personal Consumption Expenditures

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

16

INCREASED DEMAND IS PUTTING PRESSURE ON PRICE

Source: https://fred.stlouisfed.orgData through June 2018

• Consumer Price Index continues to steadily increase vs LY

• At Home Food prices up slightly vs LY• Away From Home prices increase in

line with CPI

• Inflation is up vs. LY

• The Fed continues to raise the Federal Funds Rate with additional hikes planned in 2018

• Consumer revolving credit is up vs last year, as is student loan borrowing

Credit Card

Consumer Debt

5.2% vs LY

Student Loan5.6% vs LY

Consumer Price Indices (CPI)

All Items

2.8% vs LY

At Home0.4% vs LY

Away from Home2.8% vs LY

CPI - Food1.4% vs LY

76% vs LY

Inflation

2.87%

2.00%

Up +.50% since Jan

Fed. Funds TGT

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

17

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

Pri

ce %

Ch

g v

s LY

MORE CATEGORIES REFLECT AN INCREASE IN PRICE FOR DeCA AND

COMPETITORS

Source: Answers on Demand, DeCA RDH, (52 WE 4/28/2018)

DeCA has more categories raising prices by 5% or more than retailers outside the gate

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

Pri

ce %

Ch

g v

s LY

DeCA – Unit Price Trends xAOC – Unit Price Trends

L3 – Categories Experiencing a Price Increase >5%: 124

L3 – Categories Experiencing a Price Increase > 5%: 66

• 167 categories with negative price change• 259 categories with increases 0% to 4.9%• 37 categories with increases 5% to 9.9%• 10 categories with increases 10% to 14.9%• 19 categories with increases 15% and more

• 139 categories with negative price change• 204 categories with increases 0% to 4.9%• 75 categories with increases 5% to 9.9%• 24 categories with increases 10% to 14.9%• 25 categories with increases 15% and more

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

18

7 Predictions

Stars Aligned For Growth – Are you?

Clean Label, Ethnic, Comfort, & Convenience Innovation

Basket Building Personalized Marketing

Fresh Ideas For Center-Store

Department Trip Magnets

Private Brands Resurgence

Strange Bedfellows

Copyright © 2017 The Nielsen Company. Confidential and proprietary.

STATE OF THE BUSINESS

DeCA BUSINESS REVIEW

20

Co

pyr

igh

t ©

20

18

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

Walmart and Value Grocery remain top competitors for DeCA Shoppers as DeCA SOW declines

Leverage Private Label to improve buyer conversion and limit trips to Value Grocery and Walmart

Capitalize on growing importance of key Health & Wellness Claims within DeCA assortment to drive

buyer conversion across departments

SUMMARY

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

21

154

35 33 32 28 28 25 22 21 16 15 14 12 11 10

-5 -6 -6 -6 -7 -8 -9 -9 -12 -15 -16 -17 -23 -31 -34

variance Q1/18 vs Q1/17

Source: Retail ACView, Store Count Change Calendar Q1/18 vs Calendar Q1/17

AMONG GROCERS, ALDI LEADS THE EXPANSION IN THE U.S., FOLLOWED

BY WHOLE FOODS, SPROUTS AND PUBLIX

Top/Bottom 15 Food and Mass Retailer by store count change

Walmart and Target also added stores

Store count

chg. 837

FOOD 1

DRUG -383

MASS* -239

DOLLAR 1,458

*Mass: Closure of 304 Sears’ stores

Lidl operates now about 50 stores in the

U.S. (DE, GA, NJ, NC, SC and VA)

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

22

CHANNEL PERFORMANCE

UNDERSTANDING TOTAL US SHOPPER BEHAVIOR

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

23

92.1

25.3 $43.60

Penetration Frequency Basket Size

Commissary Conventional Premier Value Walmart Target Club Online

$ Share 0.5% 39.2% 1.3% 4.3% 22.8% 3.8% 11.3% 2.0%

Pt Chg. NC 0.2 0.2 0.2 0.4 NC -0.1 0.2

% Penetration 2.3% 96.8% 21.2% 39.0% 81.5% 50.6% 52.3% 34.8%

Pt Chg. -0.1 -0.1 1.1 1.1 0.4 0.5 0.0 1.3

Item Buy Rate ($) $821 $1,522 $235 $416 $1,056 $280 $810 $221

Absolute Chg. -$29 NC $16 $1 $5 -$7 -$12 $15

Frequency 14.1 42.8 9.6 14.2 22.9 7.8 11.4 5.6

Absolute Chg. 0.1 -0.3 0.2 -0.2 0.4 0.1 -0.1 0.4

Basket Size $58.08 $35.60 $24.40 $29.36 $46.12 $36.01 $71.02 $39.57

Absolute Chg. -$2.26 $0.29 $1.12 $0.45 -$0.50 -$1.22 -$0.20 -$0.05

COMMISSARIES MAINTAINED SHARE IN A CHALLENGING RETAIL

ENVIRONMENT

131.4%

Source: Nielsen Homescan Panel; US Total TA, 52 weeks ending 03/31/18 v YAG

98.1

49.9 $34.43

Penetration Frequency Basket Size

Grocery Channel – Total USNC

-0.1 trip+$0.54 +0.2 trips

-$0.28

Mass w/ Super – Total US+0.4 pts

All Shoppers in All Outlets

Q2 2018 TOTAL US SHOPPERS: Purchase Behaviors

Premier: Whole Foods, Wegmans, etc

Value: Aldi, Lidl, Save-a-Lot, etc

Limited share changes occurred amongst retailers/channels with only Club declining

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

24

SHOPPER PERFORMANCE

UNDERSTANDING COMMISSARY SHOPPER BEHAVIOR

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

25

96.0

+0.2 Pt chg

52 W/E 03/31/18% of Military Commissary

Shoppers in Grocery

131.4%

Source: Nielsen Homescan Panel, Total Outlets, Military Commissary Shoppers, L52W/E 03/31/18 v YAGO

Military Commissary

HOUSEHOLDS IN…Military

CommissaryConv. Premier Value Wal-Mart Target Club Online

% of Shoppers 100.0% 94.8% 19.1% 35.7% 90.3% 57.3% 63.8% 34.9%

Pt Chg. -0.3 -1.6 2.0 1.3 1.4 0.6 2.3

Share of Wallet 19.3% 22.9% 0.7% 2.8% 19.2% 2.8% 13.0% 1.8%

Pt Chg. -0.3 0.4 0.1 0.3 0.4 -0.2 0.7 0.2

Item Buy Rate ($) $821 $1,053 $156 $337 $908 $210 $869 $227

Absolute Chg -$28.77 $28.52 $28.61 $16.21 -$10.35 -$26.78 $23.97 $10.38

Frequency 14.1 36.4 6.3 13.2 24.4 6.5 12.5 5.1

Absolute Chg. 0.1 0.4 -0.3 0.7 0.1 -0.4 0.2 -0.1

Basket Size $58.08 $28.95 $24.73 $25.58 $37.18 $32.07 $69.77 $44.37

Absolute Chg. -$2.26 $0.44 $5.56 -$0.12 -$0.64 -$2.23 $0.79 $2.81

27.3$36.06

Frequency Basket Size

131.4%42.1

$28.43

Frequency Basket Size

+0.6 trip-$0.67

+$0.54

Military Commissary Shoppers in All Outlets Combined (Leakage)

Grocery Channel – Total US Mass w/ Super – Total US

-0.5 trips

The Club Channel increased household penetration and SOW of Military Commissary Shoppers through higher annual

spend

Premier: Whole Foods, Wegmans, etc

Value: Aldi, Lidl, Save-a-Lot, etc

DeCA STRUGGLES TO MAINTAIN SHARE DUE TO SMALLER BASKETS AS

MORE SHOPPERS GO TO VALUE GROCERY, WALMART, & CLUB

2018 Q2 COMMISSARY SHOPPERS – PURCHASE BEHAVIORS

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

26

Commissary Shopper% Share of Wallet

19.3%

80.7%

-0.3pts

COMMISSARY SHOPPERS’ SHARE OF WALLET TO MILITARY BASES

DECREASED SLIGHTLY IN Q2 2018Walmart is DeCA’s #1 competitor while Grocery is #2 but fragmented Share of

WalletPt Chg vs YA

+0.3pts

Nielsen Homescan,, Household Projected, L52W/E 3/31/18 v YAG

Military

Commissary

Rest of Market

Military Commissary 19.3% -0.3

Walmart 19.2% 0.4

Kroger 6.0% 0.2

Costco 5.6% 0.1

Sams 5.6% 0.3

Exchanges 3.0% -0.5

Target 2.8% -0.2

Dollar Stores* 2.1% 0.2

Walmart NHD 2.0% 0.4

Online 1.8% 0.2

Aldi 1.7% 0.3

HEB 1.6% 0.6

Walgreens 1.6% 0.3

Bj's 1.6% 0.2

Publix 1.6% 0.1

Food Lion 1.4% 0.0

Safeway 1.2% -0.4

Rem. Market 19.5% -1.7

Grocery Military Mass Clubs Drug Online Dollar

*Added since 6-12 meeting

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

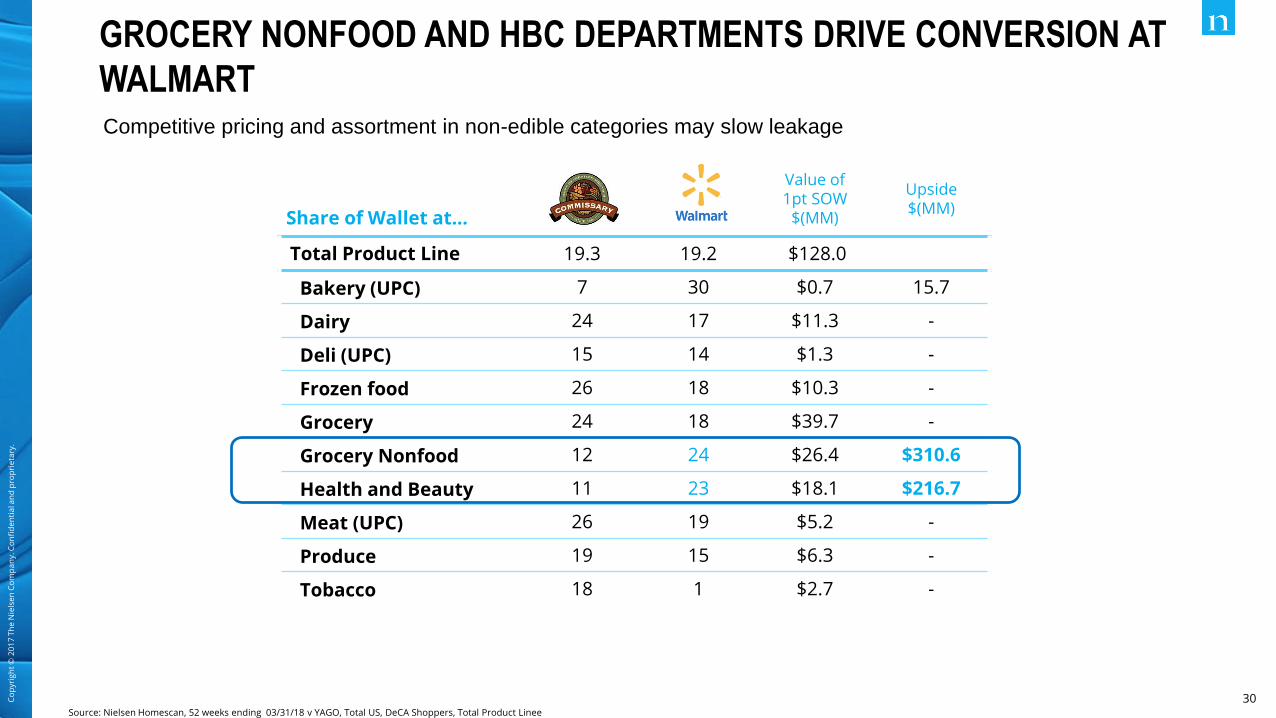

30Source: Nielsen Homescan, 52 weeks ending 03/31/18 v YAGO, Total US, DeCA Shoppers, Total Product Linee

GROCERY NONFOOD AND HBC DEPARTMENTS DRIVE CONVERSION AT

WALMARTCompetitive pricing and assortment in non-edible categories may slow leakage

Commissary

Walmart Value of 1pt SOW

$(MM)

Upside $(MM)

Total Product Line 19.3 19.2 $128.0

Bakery (UPC) 7 30 $0.7 15.7

Dairy 24 17 $11.3 -

Deli (UPC) 15 14 $1.3 -

Frozen food 26 18 $10.3 -

Grocery 24 18 $39.7 -

Grocery Nonfood 12 24 $26.4 $310.6

Health and Beauty 11 23 $18.1 $216.7

Meat (UPC) 26 19 $5.2 -

Produce 19 15 $6.3 -

Tobacco 18 1 $2.7 -

Share of Wallet at…

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

31Source: Nielsen Homescan, 52 weeks ending 03/31/18, Total US, DeCA Shoppers, Total Product Line, UPC Coded Items

COMMISSARY SHOPPERS INCREASED SPEND ACROSS ALL

CATEGORIES AT VALUE GROCERYWhile the Commissary retains highest Share of Wallet across categories, competitive pricing and assortment

reviews will be necessary to halt grocery growth within conventional and value grocery retailers

Commissary

Premier Grocery

PT ChgConventional

GroceryPT Chg Value Grocery PT Chg

Total Product Line 19 1 0.1 23 0.7 3 0.5

Bakery (UPC) 7 2 0.1 34 -2.4 5 1.6

Dairy 24 1 0.2 36 -0.6 5 0.7

Deli (UPC) 15 2 -0.3 38 2.2 4 0.9

Frozen food 26 1 NC 33 -0.1 4 0.3

Grocery 24 1 NC 28 0.1 4 0.7

Grocery Nonfood 12 0.2 NC 10 0.9 1 0.2

Health and Beauty 11 1 NC 11 0.2 0.4 0.0

Meat (UPC) 26 1 0.1 34 0.9 1 0.9

Produce 19 2 -0.1 31 0.7 8 1.6

Share of Wallet at…

32Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

PRIVATE & BRANDED LABELS ATTRACTING DeCA SHOPPERS IN VALUE

GROCERY DRIVEN BY FREQUENCY & BASKET SIZE

PRIVATE

BRANDS

NATIONAL

BRANDS

PRIVATE

BRANDS

NATIONAL

BRANDS

PRIVATE

BRANDS

NATIONAL

BRANDS

PRIVATE

BRANDS

NATIONAL

BRANDS

1.5M 2.8M 2.5M 2.6M 1.0M 1.1M 2.7M 2.8M

$15 $820 $204 $738 $186 $178 $226 $835

5.2 14.2 17.8 23.0 12.3 12.1 23.8 33.9

$4.43 $57.85 $11.47 $32.05 $15.17 $14.67 $9.52 $24.63

+9% +6%+129% -4%

+56% -4% +16% +4% 0%

-1%

-5% +10% +2%+52%

+6%

0%

+2%

-7%

0%

-2% -3%

Source: Nielsen Homescan Panel; All Shoppers Total US RTA, 52 weeks ending 03/31/18 v YAG

Commissary WalmartDiv1+Super Value GroceryConventional Grocery

Aldi, Save A Lot, Lidl

Sho

pper

s$

Bas

ket

Fre

quen

cyA

vg $

Spe

nd

Military Commissary Shoppers in …

+4%

-1%

+8% -4%

+1% +2%

-3%

+12% +2%

+6%

-1%

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

33Source: Nielsen Homescan, 52 weeks ending 03/31/18, Total US, DeCA Shoppers, Total Product Line, UPC Coded Items

WALMART LOST SHARE OF WALLET ACROSS ALL CATEGORIES

WHERE DeCA LAUNCHED PRIVATE LABEL

These launches, however, did not reverse negative share of wallet trends for those categories at DeCA

Commissary

PT Chg Total Grocery PT Chg Walmart PT Chg

Cheese 28 -0.4 39 0.4 17 -1.3

Private Label Cheese 7 - 55 -9.2 21 -0.4

Water 17 -3.3 30 5.1 16 -0.8

Private Label Water 10 - 40 8.4 18 -5.0

Disposable Bags 15 -1.3 19 0.4 19 -1.0

Private Label Disposable Bags 10 - 19 0.6 15 -2.3

Share of Wallet at…

Cheese: -1.4 Pt Chg 2YAGO

Water: +5.1 Pt Chg 2YAGO

Disposable Bags: -4.0 Pt. Chg 2YAGO

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

34Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

CHEESE SHOPPER ACTIVITY AT WALMART IS DOWN

Decline due to fewer trips

Walmart Cheese Sales

Buyer Penetration

$33 (-$2)

$6 ($0.24)X

X1.2% (NC)

Dollars per HH per year

5.5 (-0.3)

Trips per HH Dollars Per Trip

Q1 2018 (Chg vs. YA)

Source: Nielsen Homescan XOF, 52 weeks ending 12/31/16, Total US, DeCA Shoppers, Total Product Line, UPC Coded Items

Co

pyr

igh

t ©

20

17

Th

e N

iels

en

Co

mp

an

y. C

on

fid

en

tia

l an

d p

rop

rie

tary

.

35

HEALTH & WELLNESS

OPPORTUNITIES

36

Co

pyr

igh

t ©

20

18

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

-15.0 -10.0 -5.0 0.0 5.0 10.0 15.0

LOW SALT OR SODIUM

VITAMIN PRESENCE

NATURALLY NO CAFFEINE

LOW FAT

HIGH FRUCTOSE CORN SYRUP FREE

CHOLESTEROL FREE

Total Store

NO ARTIFICIAL FLAVOR

PRESERVATIVE FREE

WHOLE GRAIN

KOSHER

NO TRANS FAT

SOY

NATURAL PRESENCE

GLUTEN FREE

NO ARTIFICIAL COLORS OR FLAVORS

ORGANIC

ORGANIC CONTENT 95-100 PERCENT

GMO FREE

NO ARTIFICIAL PRESERVATIVES

NATURAL

Top 20 H&W Label by $ Sales

DeCA $ % Chg YA xAOC $ % Chg YA

MOST HEALTH & WELLNESS CLAIMS DISPLAY DECLINING SALES AT

DeCA AND ARE NOT KEEPING PACE WITH TOTAL MARKET

Source: Nielsen RWS, 52 weeks ending 04/28/18 v YAG, Total US Source: Nielsen Homescan, 52 weeks ending 03/31/18 v YAG, Total US, DeCA Shoppers, Total Product Line, UPC Coded Items

-80.0 -60.0 -40.0 -20.0 0.0 20.0 40.0 60.0

Total Convenience / Gas

Whole Foods Market

Safeway

Target

Premiere Fresh Grocery

Sams

Dollar Stores

Trader Joe's

Publix

Warehouse Club

All Outlets

Conventional Grocery

Walmart

Food Lion

BJ's

Costco

Kroger

Military Commissary

Value Grocery

Aldi Discount

Wegmans

Drug Store

H-E-B

NATURAL CLAIM $ % Chg for DeCA Shoppers

Natural claim products in Panel for DeCA Shoppers show that Value Grocery retailers are winning ahead of Military

Commissaries

37

Co

pyr

igh

t ©

20

18

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

As Private Label resurge, continue to expand own brands to improve buyer conversion and limit trips to Value

Grocery and Walmart

Value Grocery expands and continues to engage Commissary shoppers. Competitive pricing will be key

to win.

SUMMARY

Capitalize on the H&W opportunity across national and own brands.

Copyright © 2018 The Nielsen Company. Confidential and proprietary.