status and corporate illegality: illegal loan …

TRANSCRIPT

r Academy of Management Journal2015, Vol. 58, No. 5, 1287–1312.http://dx.doi.org/10.5465/amj.2012.0508

STATUS AND CORPORATE ILLEGALITY: ILLEGAL LOANRECOVERY PRACTICES OF COMMERCIAL BANKS IN INDIA

REKHA KRISHNANSimon Fraser University

RAJIV KRISHNAN KOZHIKODESimon Fraser University

Why might high-status organizations, presumably secure in their positions, resort toillegality? This study considers the possibility that status theory might have over-estimated the relative security of high-status organizations. We examine our theory thatan inability to meet associates’ expectations about quality might be the source of in-security, using data on the illegal loan recovery practices employed by commercialbanks in India between 2005 and 2009. High-status banks were found to be particularlylikely to engage in illegal recovery practices. This was especially true when a high-statusbank had experienced a decline in its financial asset quality or had fallen behind thefinancial asset quality of its peers. However, when a bank’s business partners placedgreater emphasis on corporate social responsibility (CSR), it minimized a bank’s ten-dency to resort to illegal loan recovery practices.

A key premise of status theory is that high-statusorganizations enjoy a sense of security resultingfrom the stability of the status order (Phillips &Zuckerman, 2001; Podolny, 1994; Sauder, Lynn, &Podolny, 2012), which sense of security shouldlimit their need to engage in questionable activities(Greve, Palmer, & Pozner, 2010). The stability in thestatus order is brought about by status homophily,

whereby high-status organizations carefully associ-ate only with others of high status and cautiouslyavoid associations with low-status organizations(Castellucci & Ertug, 2010; Podolny, 1994; Pollock,Chen, Jackson, & Hambrick, 2010). Occupying a po-sition higher up in the status hierarchy is known toattract disproportionate rewards. Research hasshown that high-status organizations are betterrewarded for a given level of quality (Benjamin &Podolny, 1999), enjoy cost advantages (Podolny,1993), and have better access to key resources andopportunities (Podolny & Phillips, 1996; Pollock &Rindova, 2003; Stuart, Hoang, & Hybels, 1999). Therelative security of their position and the dispro-portionate advantages that high-status organizationsenjoy should limit their motivation to engage incorporate illegality (Greve et al., 2010). However,scholarly work has shown that high-status organi-zations not only engage in illegality, but also sufferthe penalties of doing so (Greve et al., 2010; Jensen,2006). This gives rise to a puzzling question: Whatprompts high-status organizations to engage in riskyillegal acts?

In this study, we consider the possibility thatthe received wisdom in status research has over-estimated the relative security of a high-status po-sition and that high-status organizations mightactually be insecure. Recent research on the illegalacts of prominent firms supports this possibilityby suggesting that loss aversion could be a factor

Both authors contributed equally to this work. We aregrateful to the Associate Editor Tim Pollock and the threeanonymous reviewers for their insightful feedback duringthe review process. We also thank Tom Lawrence and theSFU Write Club for their constructive comments on earlierdrafts of the paper. We thank Chris Marquis for graciouslysharing the Karmayog data, which we used to construct oneof the variables in this paper. We thank Alex Epen for thetimely and insightful feedback on an earlier draft of thispaper. This paper has also benefited from the feedback ofseminar participants at Simon Fraser University, Acad-emy of Management’s PDW on Corporate Social Respon-sibility and Stakeholder Management in Emerging Marketsand David Lam Center’s Pacific Region Forum. We thankPUKrishnan, K PMeenakshi, Amruta Krishnan Srinivasanand Meena Rajiv Krishnan for their encouragement. Theresearch was funded by Social Sciences and Humanities Re-searchCouncil of Canada (Grant #: 410-2009-1607) andSimonFraser University (Endowed Fellowship #: 31-787191). Thefinal version of this paper was prepared while RekhaKrishnan was a visiting scholar at the Institute for Researchin the Social Sciences (IRiSS) of Stanford University.

1287

Copyright of the Academy of Management, all rights reserved. Contents may not be copied, emailed, posted to a listserv, or otherwise transmitted without the copyright holder’s expresswritten permission. Users may print, download, or email articles for individual use only.

motivating illegality. Mishina, Dykes, Block, andPollock (2010) suggest that firms with a record ofoutstanding performance may engage in corporateillegality to avoid the loss that they might incur ifthey were to fail to meet the unrealistic performanceexpectations of their audience. The authors find thatthis link between good performance and illegality isstronger for prominent firms. There are reasons toexpect that insecurity regarding status positionmight similarly trigger loss aversion among high-status organizations, motivating them to engage inillegality. Although not all prominent firms are ofhigh status, high-status firms tend to be prominent:“A firm’s prominence reflects the degree to whichexternal audiences are aware of its existence, as wellas the extent to which they view it as relevant andsalient” (Mishina et al., 2010: 706), which, fora high-status firm, is directly tied to its associationwith high-status others (Podolny, 1993). For a high-status organization, loss aversion may be triggeredby a fear of status loss should it fail to meet its as-sociates’ expectations about vital attributes of itsreputation. “Status loss” refers to a decline in thedeference formerly enjoyed by an organizationamong its associates, whereby its associates nolonger prioritize the organization as a preferredpartner (Neeley, 2013; Podolny & Phillips, 1996).

In developing our theory linking the insecurity ofhigh-status organizations with their motivation toengage in illegality, we consider (a) reputation forquality as the source of insecurity for high-statusorganizations, (b) why illegality might be adopted asa means of dealing with this insecurity, and (c)when illegality is less likely to be chosen as a rem-edy.1 Status homophily suggests that high-statusorganizations are careful about the status of thosewith whom they associate—avoiding associatingwith organizations of low status (Podolny, 1993).Indeed, high-status organizations are likely to ex-ercise such caution within their status class as well,basing associations with high-status others on thereputations of those others in terms of attributes thatthe organization deems relevant. Organizations canvary in terms of their reputations, and those repu-tations can vary across different attributes (Jensen &Roy, 2008; Jensen, Kim, & Kim, 2012). For instance,an organization might have a positive reputation interms of product quality and financial asset quality,but a negative reputation in terms of integrity

(Jensen & Roy, 2008). Jensen and Roy (2008) haveshown that high-status clients use status cues toscreen service providers and that clients sub-sequently tend to associate primarily with providerswithin their status class whose reputations meettheir expectations in terms of specific attributes thatthey care about: financial quality and integrity, forexample. To the extent that other firms with whoma high-status firm deals care about certain attributes,they may similarly be more likely to sever ties witha firm with a bad reputation along some importantdimension. An inability to meet associates’ expec-tations can thus threaten a firm with a loss of statusand induce insecurity; taking risks so as to preservea position in the status order may then seem at-tractive. This may be why high-status organizationsare willing to take risks to improve those aspects ofreputation that are most commensurate with a high-status position.

Quality, or the ability to consistently deliver highlevels of performance, is a prominent attribute oftenassociated with status, and it is salient for a firm’saffiliates (Ertug & Castellucci, 2013; Podolny, 1994),so high-status organizations tend to focus on main-taining or improving their reputations for quality.“Quality,” in this study, refers primarily to thequality of a firm’s financial assets: an importantmeasure of quality for the commercial banks thatwere the study’s focus (Beaver, Eger, Ryan, &Wolfson, 1989).2 Status theory posits that potentialassociates infer quality from an organization’s re-lationships with high-status others, which are oftenmore readily observable than its own underlyingquality. An organization’s status is then directlydetermined by its affiliations with high-statusothers, but indirectly determined by its prior dem-onstrations of quality (i.e., its reputation for quality)(Sauder et al., 2012). Although external audiencescan only imperfectly evaluate an organization’sunderlying quality and have to rely on observing itsrelationships with high-status others, its associatesare in a better position to evaluate the underlyingquality of the high-status organization owing to theirclose interactions with it. They have less need torely less on its position in the status hierarchy as

1 We thank the associate editor for helping us toclarify the structure of our theoretical mechanisms inthe introduction.

2 The proportion of nonperforming assets (NPAs) ina commercial bank’s portfolio largely determines its fi-nancial asset quality: The lower the NPA, the bettera bank’s financial asset quality (Beaver et al., 1989;Meeker & Gray, 1987). This is treated in the “Methods”section, but in our “Theory” section we refer to financialasset quality in general as “quality.”

1288 OctoberAcademy of Management Journal

a signal (Podolny, 2005: 38). This creates pressureon a high-status organization to continuously im-prove upon its own reputation for quality and toexceed, or at least keep up with, the reputations forquality of other high-status organizations if it is tomaintain its own high-status position (Park &Podolny, 2000: 380). To avoid status loss, a high-status firm may then be more willing to resort toillegal acts to enhance or maintain its reputation forquality. Discovery may, of course, contribute tostatus loss, but a high-status organization may as-sume that it will be able to divert its associates’ at-tention away from any illegal acts, because it usedthem only as a means of meeting expectations ofreputation for quality: an attribute highly relevant tothat audience (Bandura, Barbaranelli, Caprara, &Pastorelli, 1996; Greve et al., 2010).

We argue, however, that this tendency will bemitigated when the associates of a high-status or-ganization also care about reputation for integrity(i.e., the use of ethical means to deliver a givenlevel of quality). Reputation for quality may bea baseline role expectation for occupying a high-status position, but some associates might alsocare about whether or not the means used to de-liver that high quality are ethical. If so, they arelikely to be hypervigilant in their evaluation ofa high-status organization’s actions in an attemptto avoid any negative contagion (Boivie, Graffin, &Pollock, 2012; Jensen, 2006). That should dis-courage a high-status organization from resortingto illegality to meet expectations about reputationfor quality. In this study, we find support for thesearguments in an examination of illegal loan re-covery practices among commercial banks in Indiabetween 2005 and 2009.

The present study offers the following contribu-tions to status theory. First, it emphasizes the needto reconsider the conventional assumption in statustheory that high-status organizations enjoy relativesecurity (Phillips & Zuckerman, 2001; Sauder et al.,2012): It shows, in fact, that the fear of potentialstatus loss can prompt high-status organizations toresort to corporate illegality.

Second, status theory not only considers the linkbetween reputation for quality and status to be in-direct, but also considers this link to be less relevantfor status once an organization establishes its posi-tion higher up in the status hierarchy. Our studycontributes to this stream of research by showinghow reputation for quality might be highly relevant,to the extent that it might be a source of insecurityfor high-status organizations.

Third, and relatedly, whereas quality is the onlyattribute of reputation that is highlighted in statustheory, recent status research shows that reputationfor other attributes, when considered relevant toa focal exchange, may also affect partner choicedecisions (Jensen & Roy, 2008). Our study adds tothis recent stream of research by showing that af-filiates’ reputation expectations can also affect thebehavior of high-status organizations: In additionto the associates’ generalized expectations abouta high-status organization’s reputation for quality,heterogeneity in their expectations about reputationfor integrity can also heavily condition a high-statusorganization’s behavior.

Finally, while prior research has emphasizedonly the many benefits of occupying a high-statusposition, this study draws attention to the burdensof occupying a high-status position and its detrimentaleffect on organizational actions.

THEORY AND HYPOTHESES

Status and Reputation

Status is an organization’s relative position ina hierarchical social order. It is directly tied to thefirm’s pattern of affiliations and indirectly tied to itspast behavior (Podolny, 2005: 13). An organization’sstatus influences others’ behavioral expectations ofit (Podolny, 2005). “Reputation,” in a general sense,has been used to describe behavioral expectationsabout an organization based on its actual past be-havior (Lee, Pollock, & Jin, 2011; Pfarrer, Pollock, &Rindova, 2010). Thus status is indirectly tied to pastbehaviors, while reputation is directly tied, sug-gesting an imperfect correlation between an orga-nization’s reputation and its status (Barron & Rolfe,2012; Podolny, 2005: 13). Status is actor-specificbecause it is conferred on an organization as awhole; reputation is attribute-specific because anorganization’s reputation can be different with re-spect to different attributes. The firm might, forexample, have a positive reputation for productquality and financial asset quality, but a negativereputation with respect to other attributes, such asintegrity (Jensen & Roy, 2008; Jensen et al., 2012).Similarly, in citing the usefulness of the reputationconstruct in status research, Podolny (2005) arguesthat reputation can be more useful as a stratifyingconstruct if it is followed by a “for.” According toPodolny (2005), unlike status, which is an overallassessment, reputation might more usefully beconsidered an attribute-specific assessment such as

2015 1289Krishnan and Kozhikode

a “reputation for quality” or a “reputation forintegrity.”

Although status and reputation are clearly dis-tinct constructs, research has sometimes conflatedthe two (Barron & Rolfe, 2012; Jensen et al., 2012;Washington & Zajac, 2005). This has to do pri-marily with how reputation has been defined inmanagement research (Lange, Lee, & Dai, 2011).Scholars have used integrative definitions of rep-utation that center on overall, organization-levelassessments of a firm’s ability to consistently de-liver value to multiple audiences judged on mul-tiple attributes (e.g., Fomburn, 2012; Rindova &Martins, 2012). Such integrative definitions makeit difficult to distinguish reputation from status, sotheorizing about and measuring them individuallybecomes difficult. Reputation is best treated asattribute- and audience-specific (Jensen et al., 2012).Some attributes will usually be more importantthan others for assigning status, and this can bea deciding factor in determining on which attri-butes an organization will focus. An organizationtends to focus on the attributes that its target au-dience considers most relevant. Reputation thenserves to predict future behavior based on whetheror not the organization’s past behavior has met theexpectations involved with occupying a certainsocial status (Ertug & Castellucci, 2013; Jensenet al., 2012).

Status research, for the most part, contends thatstatus is a relationally based signal of quality andso is indirectly tied to an organization’s past dem-onstrations of quality (Lynn, Podolny, & Tao, 2009;Podolny, 2005). Because an organization’s affilia-tions are more readily observable than its actualquality, potential exchange partners are morelikely to rely on an organization’s status to infer itsunderlying quality (Ertug & Castellucci, 2013).That makes a reputation for quality highly relevantto meeting the role expectations of occupyinga high-status position (Ertug & Castellucci, 2013;Jensen et al., 2012). Of course, some associatesmight also consider other attributes of reputationimportant (Jensen et al., 2012). For instance, asso-ciates expect a high-status organization such asStarbucks to use good-quality coffee beans, butsome might also be very concerned that the beansare ethically sourced and Fair Trade certified. Inorder to gain and retain franchises on universitycampuses in the United States and Canada, Star-bucks offers a Fair Trade certified espresso optionin addition to its standard range (Newswire, 2013).So associates will generally expect a high-status

organization to maintain a high reputation forquality, but they are likely to differ in terms of theirexpectations about a reputation for integrity (i.e., theuse of ethical means to deliver a given level ofquality).

Status and Corporate Illegality

Status order stability. Viewing status as a re-lationally based signal of quality, status theoryemphasizes how status flows through a firm’sassociations and why organizations tend to becautious in choosing their associates. High-statusorganizations will try to refrain from associatingwith those of lower status, and low-status organi-zations will find it hard to associate with thoseenjoying higher status (Podolny, 2005). This leadsto status homophily, whereby organizations asso-ciate most frequently with other organizations ofcomparable status (Castellucci & Ertug, 2010;Podolny, 1994; Pollock et al., 2010). Status homo-phily tends to stabilize the status ordering (Podolny,1994), giving firms of high status a sense of secu-rity in their positions (Phillips & Zuckerman,2001; Sauder et al., 2012). Extant status researchargues that, once established, status positions canbecome so rigidified that an organization’s statusbecomes more salient than its prior demonstra-tions of quality, and status becomes self-perpetuating(Phillips & Zuckerman, 2001). For instance, intheir analysis of California wineries, Benjaminand Podolny (1999) showed that high-status win-eries were able to charge more than those of lowstatus for wine of the same quality. Research hasshown that high-status organizations are evenfree to stray from maintaining a reputation forhigh quality without being penalized (Phillips &Zuckerman, 2001). Phillips and Zuckerman (2001)showed that high-status Silicon Valley law firmscould afford to enter the less-admired family lawpractice without diluting their high-quality imagebecause of the security of their position within thestatus hierarchy. Overall, the emphasis on statusorder stability in extant status research seems tosuggest that once an organization establishes itsposition as a high-status player, its reputation forquality becomes less relevant for maintaining thatposition.

Reputation for quality as a source of statusinsecurity. There are, however, reasons to suspectthat high-status organizations need not be as securein their position as portrayed in prior research. Al-though potential associates infer an organization’s

1290 OctoberAcademy of Management Journal

reputation for quality from its position in the statushierarchy, this may not be equally true for an orga-nization’s current associates. Their ongoing associ-ation may enable them to more accurately evaluatethe validity of the firm’s reputation for quality(Podolny, 2005: 38). Organizations must thereforeconstantly strive to meet their associates’ expecta-tions of reputation for quality. Moreover, an asso-ciate is also better placed and more likely to comparean organization’s reputation for quality with thereputations of other organizations with which itassociates. So, to maintain or improve its position inthe status hierarchy, an organization must constantlystrive to outperform its status bracket peers, main-taining or improving upon prior quality levels (Park &Podolny, 2000: 380). Such pressure is likely tocreate insecurity, especially among high-status or-ganizations of whom expectations are dispropor-tionately high. Should a high-status firm not striveto maintain or improve its reputation for quality, itwill violate its associates’ expectations and risklosing its status.

Status insecurity, loss aversion, and illegality.Ahigh-status organization cannot risk losing defer-ence from high-status associates because that mightsend unfavorable signals to potential associates whomay prefer not to associate with it (Podolny, 1993).Compared to a low-status organization, a high-statusone has more to lose from status loss, consideringthe amount of premium that a high-status positionfetches (Jonsson, Greve, & Greve, 2009). Poor qualityfrom a low-status organization is not very in-formative: It is in line with expectations. But ahigh-status organization’s failure to maintain itsreputation for quality is unexpected and thereforehighly informative (Jonsson et al., 2009: 210).Once expectations about a high-status organization’squality are revised downward, it must expect to loseits position in the status hierarchy and the dispro-portionate rewards to cease to exist. The value atstake in losing a high-status position should triggerloss aversion.

“Loss aversion” describes an attitude to riskwhereby the consequences of potential loss loomlarger than the consequences of potential gains forthe decision maker, even if they are in fact of thesame magnitude. It increases a decision maker’swillingness to make risky decisions (Kahneman &Tversky, 1979). In a series of social psychology ex-periments, Pettit, Yong, and Spataro (2010) showedthat individuals value their current status morewhen they envision a potential loss in status thanwhen they imagine a potential gain. Also, individuals

who face a potential loss of status strive harder toavoid it than they would to achieve a similar statusgain (Pettit et al., 2010). Applying these argumentsto organizations, high-status organizations are likelyto weigh the disadvantages of a possible status lossmore heavily than the advantages derived froma current high-status position. A high-status firm isalso likely to strive harder to maintain its statusposition than would a low-status firm, because thehigh-status firm has more to lose. Pettit and col-leagues (2010) have also shown that when theirstatus is at stake, individuals are willing to risk thebest interests of the group to avoid losing status.Faced with a potential loss of status, high-statusorganizations will similarly be more willing to takerisks—and the risky decisions triggered by lossaversion may even take the form of corporate ille-gality (Harris & Bromiley, 2007; Mishina et al.,2010).

Being discovered acting illegally is also likely toresult in a loss of status, but the immediacy of a po-tential decline in reputation for quality may loomlarger than the more distant prospect of gettingcaught; hence unethical, or even illegal, actions mayseem tempting. Research on moral disengagementshows that disengaging moral self-regulation froman illegal act allows individuals to engage inillegality (Bandura, 1986; Bandura et al., 1996).Bandura and colleagues (1996) show that, of all of themoral disengagement mechanisms, moral justifica-tion, whereby an illegal conduct is morally re-constructed by connecting it to worthy purposes,contributed highly to engagement in illegality. In itsattempt to avoid status loss by improving its repu-tation for quality, a high-status organization mayalso assume that it will be able to divert its associ-ates’ attention away from any illegal acts, because itused them only as a means to meet expectation onreputation for quality: an attribute highly relevant tothat audience (Greve et al., 2010). Apple, for exam-ple, is reputed to produce consistently high-qualityproducts. News reports suggest, however, that theyare produced by Chinese suppliers who allegedlyemploy questionable labor practices and environ-mentally unfriendly production processes (Larson,2011). A high-status organization might evenassume that meeting, or exceeding, expectationson reputation for quality—a highly relevantattribute—might be noticed more and rewarded byits audience, or might “represent acceptable com-promises” (Jensen et al., 2012: 150; Rhee & Valdez,2009). Such supplier practices seem to be accept-able compromises for Apple’s key audience: They

2015 1291Krishnan and Kozhikode

have not hurt its sales. Hence a high-status organi-zation might assume that a certain amount of illegalactivity might go unnoticed, or at least unpenalized,especially if the illegality does not affect its associ-ates directly (Greve et al., 2010):

Hypothesis 1. The higher an organization’sstatus, the more likely it is to engage in corpo-rate illegality.

Status and Damage to Reputation for Quality andIllegality

Behavioral theory of the firm identifies that or-ganizations evaluate their current organizationaloutcomes vis-a-vis their own historical organiza-tional outcomes (Cyert & March, 1963). When theyfall short, firms will tend to take risks to remedy thesituation (Cyert & March, 1963; Greve, 1998; Iyer &Miller, 2008; Miller & Chen, 2004). A key finding ofthis research is that when organizational outcomesfall below historical aspirations, organizations arereluctant to adjust their aspirations downward(Greve, 2002; Lant, 1992); instead, they may takerisks to make good the shortfall (Greve, 1998;March & Shapira, 1987, 1992). Since a high-statusorganization is expected to have a high absolutereputation for quality, it has to improve, or at leastmaintain, that reputation if it is to maintain itsposition.

In addition to their own historical organizationaloutcomes, organizations also evaluate themselvesvis-a-vis the organizational outcomes of relevantothers (Cyert & March 1963). Research shows thatthe “relevant others” for a high-status organizationare likely to be other organizations within its statusbracket (e.g., Festinger, 1954; Park & Podolny, 2000).Specifically, status theory posits that high-statusorganizations will avoid competing with low-statusorganizations for fear of losing deference from au-diences within their own status bracket. Park andPodolny (2000: 386) explain that, in the sports carsegment for example, the high-status producer Fer-rari would compete more intensely with Lambor-ghini, which is within its status bracket, than itwould with Mazda, which belongs to a lower statusbracket. Status competition is thus localized (Park &Podolny, 2000), affecting how organizations evalu-ate their organizational outcomes vis-a-vis the or-ganizational outcomes of others within their statusbracket. In his work on the social comparison pro-cess, Festinger (1954) has shown that, when evalu-ating their abilities, individuals tend to compare

themselves with those whose abilities are perceivedto be close to their own. When abilities differmarkedly, individuals categorize those whom theyconsider noncomparable as either higher status orlower status players. It is only within their ownstatus group that individuals aspire to superiorability and strive to raise their ability vis-a-vis othersin that group (Dreyer, 1953; Festinger, 1954). Con-sistent with this, in their work on managerial riskpreferences, March and Shapira (1987, 1992) haveshown that organizations take risks when their or-ganizational outcomes fall below those of otherswhom they consider relevant. Such risky behaviorcan even extend to corporate illegality (Harris &Bromiley, 2007; Mishina et al., 2010).

When a high-status organization experiencesa decline in its reputation for quality in comparisonwith its historical or social aspirations, the highexpectations of its associates make it even moredifficult to revise aspirations downward. Instead,the decline generates enormous pressure for theorganization to regain its reputation for quality(Podolny & Phillips, 1996). A high-status firm thatperceives status loss to be imminent may experi-ence intense loss aversion. Hence we expect that, incomparison to those high-status organizations thathave improved, or at least maintained, their repu-tations for quality vis-a-vis their own historicalreputations or relative to those of their high-statuspeers, a high-status organization that has failed to doso will be tempted to resort to illegality:

Hypothesis 2. Any positive association betweenan organization’s status and its level of illegalactivity will be stronger when the organizationfalls short of its historical reputation for quality.

Hypothesis 3. Any positive association betweenan organization’s status and its level of illegalactivity will be stronger when the organization’sreputation for quality falls short of those of itspeers.

Status and Reputation for Integrity of Associatesand Illegality

Because it is primarily evaluated in terms of itsreputation for quality, a high-status organizationmay come to believe that associates will reward it aslong as it meets or exceeds quality expectations,regardless of the means adopted. Greve and colleagues(2010) have argued that since a high-status orga-nization is generally considered to be compe-tent and credible, audiences do not pay much

1292 OctoberAcademy of Management Journal

attention to reports of its illegal acts that are notdirectly relevant to their own exchanges with thehigh-status organization. High-status organizationsare thus less likely to be negatively affected by al-legations of illegal acts if those acts are not directlypertinent to their focal exchange. Rhee and Valdez(2009) argue that organizations suffer irreparabledamage to their images in the eyes of their targetaudience only if they violate audience expectationson a dimension of reputation that the audiencevalues highly, but not if the damaging event is un-related to the dimensions of reputation that thetarget audience values.

These arguments suggest that a high-status orga-nization might expect to divert its associates’ at-tention away from its illegal acts as long as thoseacts are not very relevant to the exchanges involved.However, some of those associates might them-selves be rated high on integrity: For them, a firm’sreputation for integrity may matter as much as itsreputation for quality; and for them, any act of ille-gality is highly relevant. Indeed, such associates arelikely to be hypervigilant about the high-status or-ganization’s actions and may not hesitate to disas-sociate themselves if they even suspect illegalactivity. For example, research shows that outsidedirectors are more likely to leave a firm’s boardfollowing negative events such as a financial re-statement or a shareholder lawsuit (Arthaud-Day,Certo, Dalton, & Dalton, 2006; Boivie et al., 2012;Cowen & Marcel, 2011; Srinivasan, 2005). Boivieand colleagues (2012) have shown that such de-partures are voluntary: the director’s attempt toavoid tainting his or her own reputation for in-tegrity. After all, outside directors tend themselvesto have an elite background.

Overall, associates who are themselves ratedhighly for integrity are less likely to tolerate corpo-rate illegality from a high-status organization andare more likely to avoid damage to their own repu-tations for integrity by distancing themselves fromthe high-status organization should corporate ille-gality occur. This should discourage a high-statusorganization whose associates care about their rep-utations for integrity from resorting to illegality asa means of meeting expectations pertaining to itsreputation for quality:

Hypothesis 4. Any positive association betweenan organization’s status and its level of illegalactivity will be weaker when the organization’sassociates are rated higher in terms of reputa-tion for integrity.

METHODS

Data and Sample

We tested our hypotheses using data on the illegalloan recovery practices of commercial banks in In-dia. While employing illegal means to recover baddebts is a practice typically associated with the“loan sharks” of the underworld (Haller & Alvitti,1977), there are indications that it has becomewidespread even among high-status commercialbanks the world over (Chicago Sun Times, 2011;Klan, 2008; Raja, 2007; Rowley, 2011). Such dubi-ous practices have been rampant in Indian bankingsince at least 2004.

As the following extract attests, banks and theirloan recovery agents have been found jointly guiltyof imposing mental distress and physical abuse onborrowers, much like underworld loan sharks. Suchharassment has targeted not only the defaultersthemselves, but also those close to them, to addpressure for repayment:

It was not the inability to repay their debts thatpushed them over the edge, it was the verbal, andsometimes, physical abuse, public humiliation attheir places of residence and work, threats and theintimidating behavior that did it. Petrified whengoons called their Mulund house the day before andthreatened to abduct his sister and take away all thebelongings if the family did not come up with thedues immediately, Nikhil Prabhakar killed himselfover just Rs4,000. He consumed pesticide. Therehave been suicides over defaults where the entireloan amount has been under Rs20,000. . . The list ofcomplaints against leading private sector banks likeICICI, HDFC and Citibank run into the thousands. . .[This is despite the fact that] the [Reserve Bank ofIndia] has clearly laid down guidelines for loan re-covery methods and reserves the right to impose anypenalty on a bank under the provisions of theBanking Regulation Act, 1949, for violation.

(The Statesman, 2007: 1)

This extract is from a front-page story reported inTheStatesman, an Indian newspaper, on November 18,2007. Recovery agents arrived unannounced ata borrower’s workplace and residence, deliveringverbal abuse, threats, and even physical torture notonly to the borrower, but also to his friends andfamily. There have also been instances of kidnappingand detention of credit card defaulters at a bank’spremises until the borrower made arrangements forrepayment (e.g., Special Correspondent, 2005).

2015 1293Krishnan and Kozhikode

Interestingly, in India, it is the high-status com-mercial banks such as State Bank of India, ICICIBank, HDFC Bank, and Citibank that have gener-ated the greatest number of loan recovery harass-ment complaints to the Banking Ombudsman. Infact, between 2005 and 2009, 15 of the banks withthe highest status scores (based on Bonacich cen-trality scores in preferred banker networks amongBSE500 firms) also figured prominently amongthe banks that were subject of the largest numberof loan recovery harassment complaints. Indianbanks’ illegal loan recovery practices thus lendthemselves well to testing hypotheses about therelationship between organizational status andcorporate illegality.

We examined the illegal loan recovery practicesof all 82 commercial banks that operated in Indiabetween 2004 and 2009. Since the analysis involveda time-lagged design, the complaints spanned2005–09 and the independent variables were ob-served between 2004 and 2008. Of the 82 banks inthe sample, 77 operated throughout the studyperiod and five others entered or exited duringthe period, resulting in a total of 396 bank-yearobservations.

We collected data on illegal loan recovery prac-tices from the published reports of India’s BankingOmbudsman. The Banking Ombudsman is an ap-pellate authority appointed by the Reserve Bank ofIndia (RBI) to resolve consumer complaints againstbanks and their affiliates. It has been in operationsince 1995; since 2005, the RBI has been publishinga breakdown of the various complaints made againsteach bank.

We constructed a status measure using data fromthe Prowess database. This is a popular businessresearch database for Indian companies, developedand maintained by the Center for Monitoring theIndian Economy (CMIE). The database is publiclyavailable, and is often used in studies of corporatefinance and management involving Indian organi-zations (see Bertrand, Mehta, & Mullainathan, 2002;Gopalan, Nanda, & Seru, 2007; Khanna & Palepu,2000). We used information from the database totabulate the affiliations of each bank with the top500 firms by market capitalization listed on theBombay Stock Exchange (BSE), India’s leading ex-change. Shares in those 500 firms are often consid-ered to be India’s “blue chips.”

We obtained financial data for each bank, such asits ratio of nonperforming assets to total assets,return on assets (ROA), and amount of bad loanssecuritized, from the annual reports available in the

RBI’s statistical archives. This source also provideddemographic data on each, such as its age, numberof employees, and the number and profile of its newbranches each year.

We obtained data on corporate social responsi-bility (CSR) for the BSE500 firms from the publica-tions of Karmayog, a nonprofit organization that,like Kinder, Lydenberg, and Domini in the UnitedStates, records the socially responsible activities ofIndia’s 500 largest companies (i.e., those includedin the BSE500 index).

Variables

Corporate illegality. The illegal act examinedwas the use of illegal loan recovery practices by thecommercial banks and their agents. We coded thedata from the Banking Ombudsman’s annual re-ports, which categorize the complaints lodgedagainst each bank. The categories include failureto fulfill commitments, credit card issues, housingloan issues, loan recovery harassment, deposit-related issues, and others. The RBI clarifies thatthe harassment category pertains to “non-observanceof Reserve Bank guidelines on engagement of re-covery agents by banks” (Thorat, 2009). The RBI re-quires each bank to complete a thorough backgroundcheck on its agents and to appoint loan recoveryofficers to monitor their actions. The RBI and thecourts hold banks vicariously liable for any of theiragents’ transgression (Associated Press, 2007).

Ample research on negative reputation spill-overs has established that stakeholders and law-makers do hold a firm responsible for the illegalbehavior of its agents (Barnett & Hoffman, 2008;Jonsson et al., 2009). Hence firms tend to regulatethe behavior of their agents to avoid any negativespillover from any illegal acts in which their agentsmight engage (Barnett & King, 2008; Jonsson et al.,2009). Of course, if the illegal acts directly or in-directly benefit the focal firm, the focal firm isindeed an accomplice. For example, when an ac-counting firm endorses accounts that prove to con-tain accounting irregularities, the courts hold thefirm and its accounting firm jointly responsible(Allen, 1990; Dodd, 1992). Therefore any illegalloan recovery practices that a bank’s loan recoveryagents might adopt are clearly attributed to thebanks themselves.

We quantified corporate illegality for each bank ineach year as the number of harassment complaintsagainst the bank, as reported by the Banking Om-budsman. This measure of corporate illegality is

1294 OctoberAcademy of Management Journal

consistent with one used by Simpson and Koper(1997) in a prior study of corporate crime.

It is, of course, well known that crime statisticsare, at best, an approximation of actual crime rates(Simpson, 1986; Simpson & Koper, 1997). In addi-tion to the usual underreporting, there may actuallybe over-reporting of crimes committed by firms, andsuch reporting errors may not be randomly distrib-uted across firms (Simpson, 1986). In this study,however, we can be reasonably confident that thereis not much over-reporting because of the stringentcriteria that the Ombudsman uses when registeringcomplaints against banks. A complainant must ap-proach the bank first and give it sufficient time inwhich to respond before filing a complaint with theOmbudsman. The Ombudsman then verifies thatthe complaint is not frivolous or vexatious, that itis not a duplicate, and that the complaint is notpending or resolved in the courts or other avenuesfor consumer redress.

However, it is difficult to rule out underreporting.The prime cause of underreporting is probably thatthe victim is either shy or unaware of the redressmechanism. We therefore controlled for under-reporting in the analyses by using control variables.Further, to establish the robustness for the findings,additional analyses tested whether or not the resultsstill held after accounting for each bank’s baselinecomplaint frequency (i.e., the number of otherconcurrent and previous complaints unrelated toloan recovery). Further, in one of our robustnesstests, we quantified the dependent variable as thenumber of loan recovery harassment complaintsnormalized by bank size (the natural logarithmof the number of employees). We discuss theseadditional analyses in detail under the heading“Robustness Checks”.

Status. A bank’s status was the key independentvariable in our modeling. An organization’s status iswell represented by the status of the other organi-zations with which it is connected. Bonacich’s(1987) centrality score is a well-established networkmeasure of status often used in prior studies(Podolny, 2001; Podolny & Phillips, 1996; Jensen,2003). It computes an actor’s power in its networkby taking into account not only the actor’s central-ity, but also the centrality of those connected with it(Bonacich, 1987). The network that we used tocompute the Bonacich centrality score for each bankwas an affiliation network based on the preferredbanker relationships of the 500 largest firms listedon the BSE. Many of the BSE500 list their preferredbankers in their annual reports. This is voluntary

disclosure, but it signals their endorsement of thebanks and presumably shows that they are confi-dent about those banks’ conduct. On average, eachfirm in the BSE500 lists 3.5 banks as preferredbankers. Preferred bankers often share banking re-sponsibilities, acting as co-lenders on commercialloans to the firm, jointly promoting its share anddebenture issues, and so on. Thus banks intersectwith each other when they jointly service a corpo-rate client that lists them as “preferred.” This ap-proach to constructing networks of banks throughtheir joint affiliations with corporate clients is con-sistent with the methods of prior research on socialnetworks, in which networks of venture capitalistshave been constructed using their affiliations withstart-up firms that they jointly funded (e.g., Rider,2009; Sorenson & Stuart, 2001). Based on this affil-iation network, we computed each bank’s Bonacichcentrality score in each year and used this as themeasure of its status. We used alternative proxiesfor status in the robustness testing, and we discussthese in our section on “Robustness Checks”.

Decline in reputation for quality. Financial assetquality is an important measure of quality for com-mercial banks (Beaver et al., 1989). The proportionof nonperforming assets (NPA) in a commercialbank’s asset portfolio largely determines its finan-cial asset quality: The lower the NPA proportion,the better is a bank’s financial asset quality (Beaveret al., 1989; Meeker & Gray, 1987). Regulators, cor-porate clients, analysts, and other key audiencesplace substantial importance on a bank’s financialasset quality. When it deteriorates, the risk ofbankruptcy increases (Cole & Gunther, 1995), thestock market tends to react negatively (Beaver et al.,1989), and its key associates tend to withdrawfrom their associations (Brewer, Genay, Hunter, &Kaufman, 2003).

In India, it was only in 2004 that the RBI began torequire all commercial banks to disclose periodi-cally the level of NPA in their loan portfolios. Thenew regulatory requirement soon started to impacton how banks in India were evaluated. Banks cameunder tremendous pressure from their key associ-ates to improve their financial asset quality. High-status banks such as ICICI Bank and HDFC Bankeither discussed, in their quarterly shareholdermeetings, their intention to reduce their NPA in thenext quarter or highlighted their NPA reductions inthe current quarter. By early 2005, banks that hadimproved their financial asset quality were alsoviewed favorably by the media. For example, Busi-ness Today, a popular Indian business magazine,

2015 1295Krishnan and Kozhikode

now uses financial asset quality as an importantmetric to rank the best banks in India annually. TheRBI also rewarded banks with excellent loan re-covery rates. Hence maintaining a good reputationfor financial asset quality became a highly desiredgoal for Indian banks.

The hypotheses predict a moderating role fora bank’s decline in reputation for quality on anyobserved status–illegality relationship. Testing forsuch moderating effects requires us first to definethe effects of a decline in reputation on the tworeference points (i.e., a bank’s own reputation andthose of its peers). Spline functions are suitable forthis purpose (Mishina et al., 2010). Specifyinga spline function of the difference between a bank’sreputation for quality and its own past reputationand the reputations of its social reference pointscreates two separate variables from each splinefunction: (1a) decline in historically referencedreputation for quality; (1b) increase in historically

referenced reputation for quality; (2a) decline insocially referenced reputation for quality; and (2b)increase in socially referenced reputation for qual-ity. Although we are particularly interested inmoderating effects 1a and 2a, 1b and 2b do help usto distinguish the effects of a decline in reputationfor quality from those of an improvement.

To code the two spline functions, we firstcoded the financial asset quality of a bank ina given year using the NPA percentage in its loanportfolio in that year (Cole & Gunther, 1995).Higher values indicated poorer financial assetquality. We computed the difference in NPApercentage between year t and year t–1 for eachbank-year. Values above 0 indicated that the bank’sfinancial asset quality had deteriorated; valuesbelow 0 indicated that it had improved. We com-puted two variables to quantify the historicallyreferenced change in reputation for quality in eachbank-year:

Decline in historically referenced reputation for quality at time t5 ðNPA percentage in year t �NPA percentage in year t � 1Þ; ifðNPA percentagein year t.NPA percentage in year t � 1Þ;5 0; ifðNPA percentage in year t<NPA percentage in year t � 1Þ

and

Increase in historically referenced reputation for quality at time t5 ðNPA percentage in year t � 1-NPA percentage in year tÞ; ifðNPA percentage inyear t,NPA percentage in year t � 1Þ5 0; ifðNPA percentage in year t>NPA percentage in year t � 1Þ

We used the second spline function to examine theannual difference in a bank’s NPA from that of itspeers in that year. We theorized that the most rel-evant social reference in a study of status-basedmotivations for corporate illegality would be thosepeers with which a bank is affiliated. In particular,we expect that a BSE500 firm will have privateinformation about all of its preferred bankers;hence it will be more able and likely to accuratelycompare the reputations for quality of all of itspreferred bankers. Each bank might thereforeevaluate its own performance vis-a-vis that of otherbanks with which it is directly affiliated in a pre-ferred banker network. When a focal bank waslisted as a preferred banker by more than oneBSE500 firm, it implied that the focal bank was incompetition with all of the other banks listed as

preferred by all of its BSE500 clients. We consid-ered a bank not listed by any BSE500 firm to below-status bank competing primarily with otherlow-status banks.

We coded two variables representing sociallyreferenced change in a bank’s reputation for quality.As a first step, we computed annual change in NPAfor each bank-year as:NPA percentage in year t – NPA percentage in yeart–1We then computed the mean annual change in NPAof peers as the average of the annual changes in NPAof all the other banks in a focal bank’s peer group, aspreviously defined.

With these two values, we coded two variablesrepresenting socially referenced change in reputa-tion for quality:

1296 OctoberAcademy of Management Journal

Decline in socially referenced reputation for quality at time t5 ðAnnual change in NPA of focal bank-Mean annual change in NPA of peersÞ; ifðAnnual change in NPA of focal bank.Mean annual change in NPA of peersÞ;5 0; ifðAnnual change in NPA of focal bank<Mean annual change in NPA of peersÞ

and

Increase in socially referenced reputation for quality at time t5 ðMean annual change in NPA of peers-Annual change in NPA of focal bankÞ; ifðAnnual change in NPA of focal bank,Mean annual change in NPA of peersÞ5 0; ifðAnnual change in NPA of focal bank>Mean annual change in NPA of peersÞ

Integrity expectations. Hypothesis 4 proposesthat high-status organizations will be deterred fromillegality if their associates care about their reputa-tion for integrity. To test this hypothesis, we con-structed a measure for reputation for integrityexpectations of associates based on the reputationfor integrity of each bank’s associated BSE500 firms.A BSE500 firm’s own reputation for integrity wasassumed to signal its expectations about the integrityof its preferred bankers. Thus we first coded thereputations for integrity of all of the BSE500 firmsthat disclosed their preferred bankers using the Kar-mayog data. Karmayog’s ratings are based on themandatory sustainability reporting that each BSE500firm must include in its annual report.

A bank’s associates can be assumed to differ interms their expectations about integrity: Somemight have very high expectations and others, verylow. If the expectations of associates are to have animpact on the behavior of a bank, however, theyshould be widely shared bymany of its associates. Agood way of quantifying the level of agreement inrelation to the integrity expectations variable is tocompute a signal to noise ratio, which is the inverseof the coefficient of variation. We therefore dividedthe mean Karmayog score of all of a bank’s BSE500associates by the standard deviation of the scores toconstruct the variable. Larger values indicatedhigher integrity expectations and greater agreementamong a bank’s BSE500 associates. In additionalanalysis, we coded this variable more conserva-tively as the lowest Karmayog score among a bank’sBSE500 clients. In a third analysis, we used themean CSR score of all of the bank’s BSE500 clients.Both additional approaches yielded results qualita-tively similar to those of the main analysis.

Control variables. We also included a set of firm-level control variables in the regressions. We includedage and size because younger banks might suffer from

the liability of newness, which would mandate theirsticking to legally acceptable behavior, while youngerbanks also tend to be of lower status. Age was mea-sured as the natural logarithm of the number of yearssince each bank’s incorporation. Larger banks willtend to have more complaints lodged against thembecause of their larger consumer base, but larger bankscan be of higher status, so, consistent with the con-ventions of prior research (e.g., Ettlie, Bridges, &O’Keefe, 1984; Mishina et al., 2010), size was quanti-fied as the natural logarithm of the number of em-ployees. Those size and status measures were highlycorrelated (.47), so it was important to isolate the trueeffect of status from that of size. Based on techniquesapplied in prior research (e.g., Brown & Perry, 1994;Mishina et al., 2010), we consequently partialled outthe common variance between the two by regressingthe status measure (the Bonacich centrality scores)against the size measure (the natural logarithm of thenumber of employees) and using the residual fromthat model as a true measure of size uncorrelated withstatus. In an additional analysis, we regressed sizeagainst status and used that residual as an indicator ofstatus uncorrelated with size. The results of the twoapproaches were consistent.

Prior financial performance could also influencethe number of complaints if a bank were to feelcompelled to improve its ROA by recovering NPAthrough illegal means. Indeed, Indian firms withbetter performance can better afford to pay theirrecovery agents well, promoting illegality. We in-cluded ROA in the analysis to control for eachbank’s prior financial performance.

The Banking Ombudsman’s stringent complaintreporting standards minimize over-reporting, butunderreporting is more likely for some organizationsthan for others. Media attention to a bank’s illegality isthe primary mechanism minimizing underreporting.The findings of prior research on the relationship

2015 1297Krishnan and Kozhikode

between media attention and corporate illegality(Greve et al., 2010) suggest that media reporting ofa bank’s illegal loan recovery practices should en-courage victims to complain and force the authoritiesto be more alert about that bank’s behavior. One dif-ficulty in coding media attention in India is that thereare 22 official languages and none has national stature.The only language with a wider presence is English,and only English newspapers have nationwide circu-lation. We therefore searched the archives of all of thepopular English-language newspapers for mentions ofbanks’ illegal loan recovery practices using theLexisNexis Academic database. We identified all of thenews reports for each bank, and three coders searchedthe reports independently using the key words “ha-rassment” (and various synonyms such as “torment,”“torture,” “intimidate,” etc.), “loan recovery” (in-cluding “NPA recovery,” “asset recovery,” “seize,”etc.), and “agents” (including “agency,” “agent,” “as-sociates,” “allies,” etc.). Each coder performed thissearch for each bank in the sample for each financialyear, then read each article to ascertain that it wasindeed a negative report relating to loan recoveryagents’ harassment of the bank’s consumers. Fleiss’s(1971) k value was calculated to estimate interraterreliability, yielding a value (k5 .84) that signified highinterrater agreement (Landis & Koch, 1977). We re-solved any disagreements by considering only thosecases in which at least two of the raters agreed.

We defined the variable negative media attentionas the number of negative news reports abouta particular bank as a proportion of the total numberof news reports published about that bank. Themaximum number of negative news reports was 59for the Bank of India, followed by 50 for ICICI Bankand 17 for HDFC Bank.

Another factor that could potentially influencethe level of a bank’s illegal loan recovery practicesmight be its success in using legal recovery methods.Securitization is still little used in Indian bankingbecause the regulatory costs are crippling and themarket for such securities is not well developed.Nevertheless, some banks continue to experimentwith this, although with limited success. We there-fore also included in the analysis the natural loga-rithm of the total amount of substandard anddoubtful loans that a bank securitized in a particularyear (bad assets securitized), to control for success inrecovering poor loans legally.

A bank’s reputation for socially responsible be-havior was another control, since a good reputationmight increase the riskiness of illegal loan recoverypractices. In India, a bank’s commitment to rural

areas can signal its social responsibility (Burgess &Pande, 2005; Burgess, Pande, & Wong, 2005). Open-ing rural branches (which tend to be relatively un-profitable) is an important indicator in that respect(Kozhikode & Li, 2012). We therefore coded sociallyresponsible banking practices using the proportion ofnew rural branches in a bank’s branch portfolioscaled by the proportion of new rural branches of allother banks in that year. We took a higher value torepresent a better reputation for socially responsiblebehavior than that of a bank’s peers. In additionalanalysis, we used a simpler measure of rural com-mitment: the proportion of rural branches in a bank’sportfolio. This measure produced a similar outcome.

Finally, we included indicator variables to con-trol for year fixed effects, with 2004 as the referencecategory.

Modeling

The dependent variable was an event count ob-served annually. Poisson regression is normally usedto model such count data. A Poisson model generatesconsistent coefficient estimates under a wide range ofassumptions (Wooldridge, 1997), but when the dataare overdispersed it can generate a downwardly bi-ased covariance matrix, leading to small, incorrectlyestimated standard errors (Haynes, Thompson, &Wright, 2003). We therefore used negative binomialmodels, because these can accommodate over-dispersion in the dependent variable (Barron, 1992)and have often been used in prior research to ana-lyze overdispersed count data (e.g., Dobbin & Dowd,1997; Kozhikode & Li, 2012; Zelner, Henisz, &Holburn, 2009).

Generalized estimating equations (GEEs) were theprimary specification as a result of their inherentadvantages over random effects and fixed effectsspecifications. Random effects estimators use all ofthe observations, but they do not account well forunobserved heterogeneity at the group level (i.e.,among banks). Fixed effects estimators are bettersuited to dealing with unobserved heterogeneity atthe group level, but at the expense of dropping allobservations from groups with no events. In thissample, that would mean dropping more than 120bank-year combinations (of the total of 396 observa-tions) for which there was not a single complaintduring the study period. Generalized estimatingequations overcome these limitations: The method isboth efficient and accounts for unobserved heteroge-neity (Hardin & Hilbe, 2003; Katila & Ahuja, 2002;Liang & Zeger, 1986). Further, standard errors robust

1298 OctoberAcademy of Management Journal

to group-level heteroskedasticity in negative binomialmodels are available only from GEE specifications(Zelner et al., 2009). Finally, GEEs allow for autocor-relation. We therefore applied a GEE negative bi-nomial estimator with a first-order autoregressivecorrelation structure (AR1) and heteroskedasticity-consistent standard errors.

RESULTS

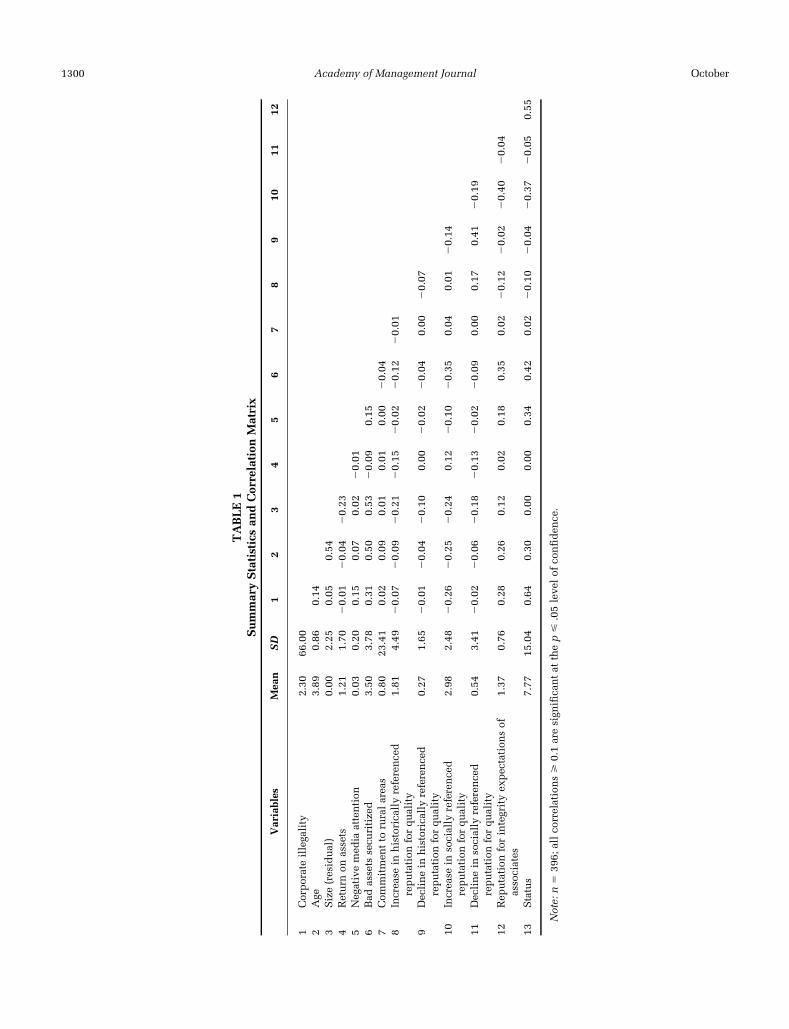

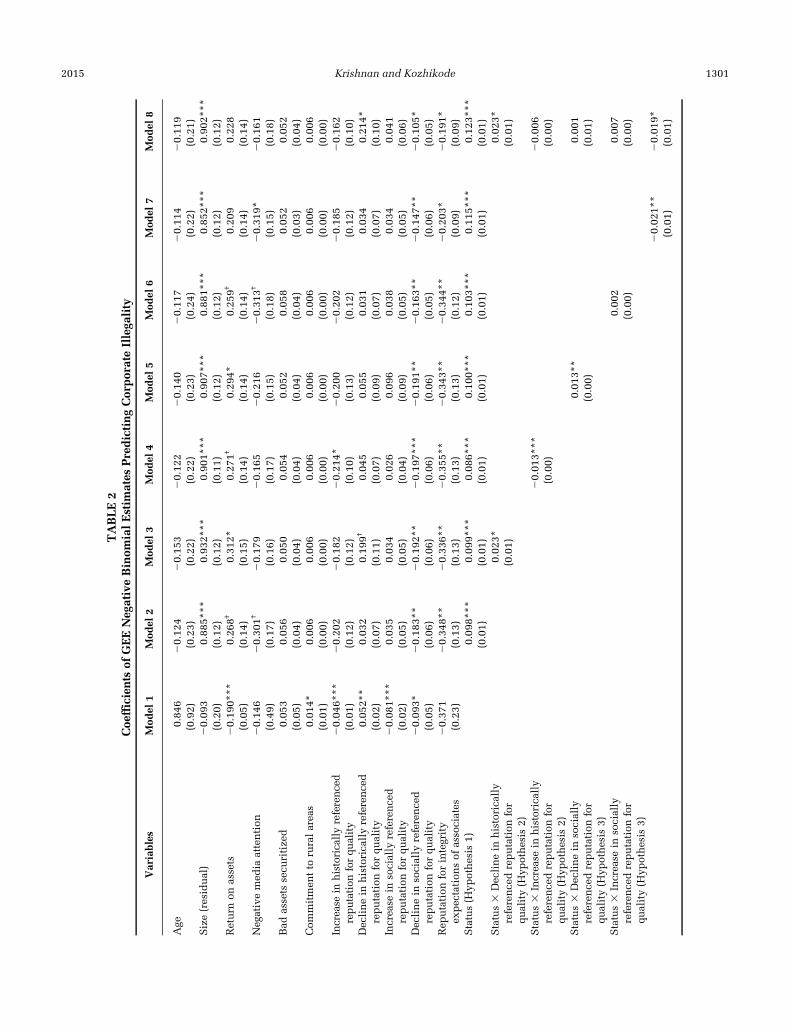

Table 1 reports summary statistics and correlationsfor the study variables. Because a few of the predictorvariables were highly intercorrelated, collinearitywas a potential problem, especially in the analysis ofinteraction effects. Applying Cohen, Cohen,West andAiken’s (2003) suggestion, we first mean-centered thevariables used in the interactions. Further, we con-ducted the analysis hierarchically. Finally, we com-puted collinearity diagnostics for all of the modelsusing the “Collin” routine in the Stata 12 softwarepackage. Table 2 reports the mean variance inflationfactors (VIFs) for all of the models. In Models 1–7, theVIF was less than 4, which is well below the meanVIF threshold of 10 suggested in prior research (e.g.,Netter, Wasserman, & Kutner, 1985; Pollock, Rindova,& Maggitti, 2008). But in Model 8, the full model, themean VIF was 10.94, which is slightly above the ac-ceptable threshold. This may be the result of thepresence of multiple interactions with the status var-iable. Hence we interpreted only the coefficients ofModels 1–7.

Table 2 also presents the coefficients of the GEEnegative binomial models with AR1 error structureand heteroskedasticity-consistent standard errors.Model 1 is the baseline formulation with the controland moderating variables. Models 2–7 test hierar-chically the relationships predicted in Hypotheses1–4. Model 8 is the full model, which includes all ofthe hypothesized effects.

In Model 1, several of the control variables provedsignificant. As expected, ROA, increase in histori-cally referenced reputation for quality, and increasein socially referenced reputation for quality allshowed significant negative relationships with cor-porate illegality. Decline in historically referencedreputation for quality had a significant positive cor-relation with corporate illegality, while decline insocially referenced reputation for quality showeda significant negative correlation. Commitment torural areas had significant positive predictive power.In that model, the years 2007, 2008, and 2009 hadpositive and significant coefficients, but the co-efficient for 2006 was not significant. Since 2005 was

the reference category, this implies that, comparedwith 2005, significantly more complaints were reg-istered in 2007, 2008, and 2009.

The coefficient for status in Model 2 was highlysignificant and positive (p < .001). This result sup-ports the contention of Hypothesis 1 that the likeli-hood of corporate illegality increases with status. Aone-unit increase in the status measure predicteda 10% increase in the incidence of harassmentcomplaints against a bank (Exp[.098] 5 1.10). Thisprovides strong support for Hypothesis 1.

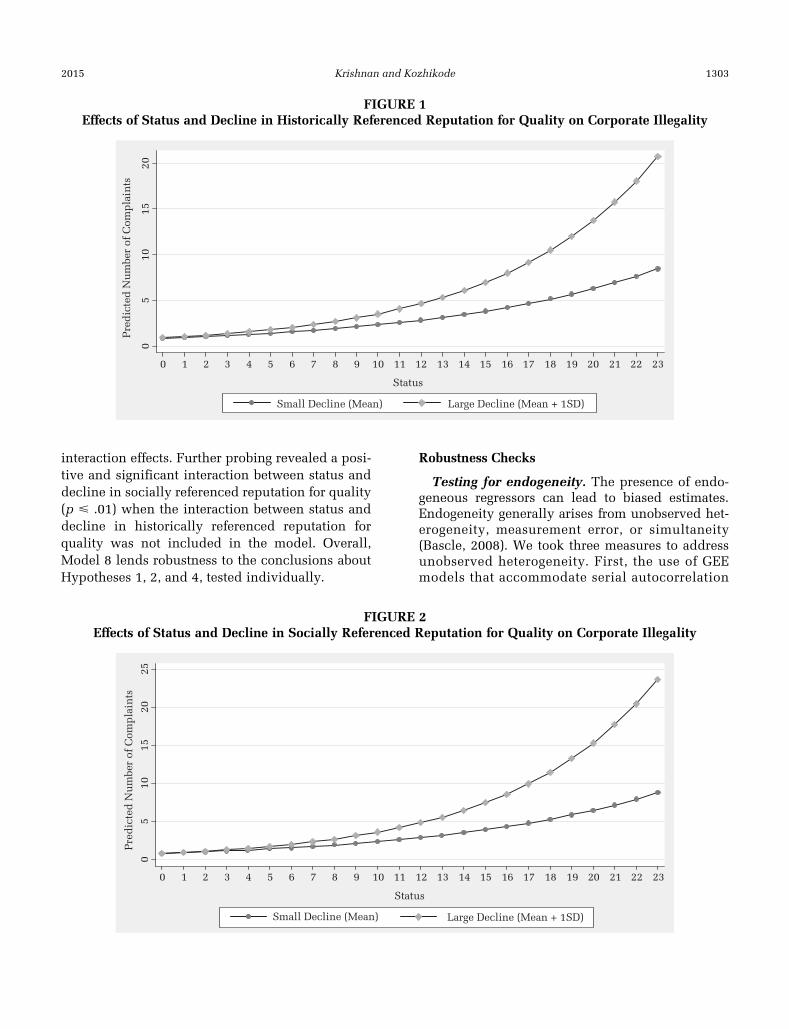

Hypothesis 2 predicted that any positive re-lationship between status and corporate illegalitywill strengthen when an organization experiencesa steeper decline in its historically referenced repu-tation for quality. Model 3 tests that hypothesis. Inthat model, the coefficient of the term representingthe interaction between status and decline in his-torically referenced reputation for quality was posi-tive and significant (p < .05). We assessed themoderating effect of decline in historically refer-enced reputation for quality on the relationship be-tween status and corporate illegality ([Exp(.099 3status 1 .023 3 status 3 decline in historically ref-erenced reputation for quality)]). When decline inhistorically referenced reputation for quality was .27(the mean), a one-unit increase in status increasedcorporate illegality by about 11%. When decline inhistorically referenced reputation for quality tookthe value 1.92 (1SD above the mean), a one-unit in-crease in status increased corporate illegality byabout 15% (a net increase of about 4.21 percentagepoints). Figure 1 illustrates this effect.3

Model 4 included a term representing the in-teraction between status and increase in historically

3 This figure was produced using the “margins” and“marginsplot” commands in Stata 12. In this approach,using the “margins” command, we first obtained pre-dictive margins for theoretically interesting values of theinteracting variables with all other variables held at theirmean value. In our case, the values that we used for thethree moderators were their mean (for low) and 1SD abovetheir mean (for high), and the range of values we used forstatus were from a low of 0 to a high of 1SD above themean (23) in one-unit increments. We then use the“marginsplot” command to graph these predictive mar-gins (predicted number of complaints) from fitted nega-tive binomial models. This technique is ideal to interpretinteraction effects in nonlinear regressions such as nega-tive binomial, Poisson, logit, and hazard rate models(Mitchell, 2012). Because these two commands are inbuiltin Stata 12 and above, they are more reliable than otheruser-written Stata commands.

2015 1299Krishnan and Kozhikode

TABLE1

SummaryStatisticsan

dCorrelation

Matrix

Variables

Mea

nSD

12

34

56

78

910

1112

1Corporateillegality

2.30

66.00

2Age

3.89

0.86

0.14

3Size(residual)

0.00

2.25

0.05

0.54

4Return

onassets

1.21

1.70

20.01

20.04

20.23

5Negativemed

iaattention

0.03

0.20

0.15

0.07

0.02

20.01

6Bad

assets

secu

ritize

d3.50

3.78

0.31

0.50

0.53

20.09

0.15

7Com

mitmen

tto

ruralareas

0.80

23.41

0.02

0.09

0.01

0.01

0.00

20.04

8Increase

inhistoricallyreferenced

reputation

forqu

ality

1.81

4.49

20.07

20.09

20.21

20.15

20.02

20.12

20.01

9Declinein

historicallyreferenced

reputation

forqu

ality

0.27

1.65

20.01

20.04

20.10

0.00

20.02

20.04

0.00

20.07

10Increase

insocially

reference

dreputation

forqu

ality

2.98

2.48

20.26

20.25

20.24

0.12

20.10

20.35

0.04

0.01

20.14

11Dec

linein

socially

referenced

reputation

forqu

ality

0.54

3.41

20.02

20.06

20.18

20.13

20.02

20.09

0.00

0.17

0.41

20.19

12Rep

utation

forintegrityex

pectation

sof

associates

1.37

0.76

0.28

0.26

0.12

0.02

0.18

0.35

0.02

20.12

20.02

20.40

20.04

13Status

7.77

15.04

0.64

0.30

0.00

0.00

0.34

0.42

0.02

20.10

20.04

20.37

20.05

0.55

Note:

n5

396;

allco

rrelations>

0.1aresign

ifican

tat

thep<

.05leve

lof

confiden

ce.

1300 OctoberAcademy of Management Journal

TABLE2

Coe

fficients

ofGEENeg

ativeBinom

ialEstim

ates

PredictingCorporateIllega

lity

Variables

Mod

el1

Mod

el2

Mod

el3

Mod

el4

Mod

el5

Mod

el6

Mod

el7

Mod

el8

Age

0.84

620.12

420.15

320.12

220.14

020.11

720.11

420.11

9(0.92)

(0.23)

(0.22)

(0.22)

(0.23)

(0.24)

(0.22)

(0.21)

Size(residual)

20.09

30.88

5***

0.93

2***

0.90

1***

0.90

7***

0.88

1***

0.85

2***

0.90

2***

(0.20)

(0.12)

(0.12)

(0.11)

(0.12)

(0.12)

(0.12)

(0.12)

Return

onassets

20.19

0***

0.26

8†0.31

2*0.27

1†0.29

4*0.25

9†0.20

90.22

8(0.05)

(0.14)

(0.15)

(0.14)

(0.14)

(0.14)

(0.14)

(0.14)

Neg

ativemed

iaattention

20.14

620.30

1†20.17

920.16

520.21

620.31

3†20.31

9*20.16

1(0.49)

(0.17)

(0.16)

(0.17)

(0.15)

(0.18)

(0.15)

(0.18)

Bad

assets

secu

ritize

d0.05

30.05

60.05

00.05

40.05

20.05

80.05

20.05

2(0.05)

(0.04)

(0.04)

(0.04)

(0.04)

(0.04)

(0.03)

(0.04)

Com

mitmen

tto

ruralareas

0.01

4*0.00

60.00

60.00

60.00

60.00

60.00

60.00

6(0.01)

(0.00)

(0.00)

(0.00)

(0.00)

(0.00)

(0.00)

(0.00)

Increase

inhistoricallyreferenced

reputationforqu

ality

20.04

6***

20.20

220.18

220.21

4*20.20

020.20

220.18

520.16

2(0.01)

(0.12)

(0.12)

(0.10)

(0.13)

(0.12)

(0.12)

(0.10)

Declinein

historicallyreferenced

reputation

forqu

ality

0.05

2**

0.03

20.19

9†0.04

50.05

50.03

10.03

40.21

4*(0.02)

(0.07)

(0.11)

(0.07)

(0.09)

(0.07)

(0.07)

(0.10)

Increase

insocially

reference

dreputation

forqu

ality

20.08

1***

0.03

50.03

40.02

60.09

60.03

80.03

40.04

1(0.02)

(0.05)

(0.05)

(0.04)

(0.09)

(0.05)

(0.05)

(0.06)

Dec

linein

socially

reference

dreputation

forqu

ality

20.09

3*20.18

3**

20.19

2**

20.19

7***

20.19

1**

20.16

3**

20.14

7**

20.10

5*(0.05)

(0.06)

(0.06)

(0.06)

(0.06)

(0.05)

(0.06)

(0.05)

Rep

utation

forintegrity

expectation

sof

associates

20.37

120.34

8**

20.33

6**

20.35

5**

20.34

3**

20.34

4**

20.20

3*20.19

1*(0.23)

(0.13)

(0.13)

(0.13)

(0.13)

(0.12)

(0.09)

(0.09)

Status(H

ypothesis

1)0.09

8***

0.09

9***

0.08

6***

0.10

0***

0.10

3***

0.11

5***

0.12

3***

(0.01)

(0.01)

(0.01)

(0.01)

(0.01)

(0.01)

(0.01)

Status3

Declinein

historically

reference

dreputation

for

quality(H

ypothesis

2)

0.02

3*0.02

3*(0.01)

(0.01)

Status3

Increase

inhistorica

lly

reference

dreputation

for

quality(H

ypothesis

2)

20.01

3***

20.00

6(0.00)

(0.00)

Status3

Dec

linein

socially

reference

dreputation

for

quality(H

ypothesis

3)

0.01

3**

0.00

1(0.00)

(0.01)

Status3

Increase

insocially

reference

dreputation

for

quality(H

ypothesis

3)

0.00

20.00

7(0.00)

(0.00)

20.02

1**

20.01

9*(0.01)

(0.01)

2015 1301Krishnan and Kozhikode

referenced reputation for quality. This term’s co-efficient was negative and highly significant (p< .001).So, while a historically referenced decrease in a bank’sfinancial asset quality predicted an increased tendencyto collect its debts illegally, a historically referencedincrease in financial asset quality predicted a decreasein that tendency.

Hypothesis 3 predicted that any positive re-lationship between status and corporate illegalityshould strengthen when an organization’s reputa-tion for quality falls behind those of its peers. Model5 tests that hypothesis. The coefficient for the in-teraction between status and decrease in sociallyreferenced reputation for quality was positive andsignificant (p < .01). This lends strong support toHypothesis 3. Figure 2 illustrates this effect. Whendecline in historically referenced reputation forquality was .54 (the mean), a one-unit increase instatus predicted an 11.33% increase in the illegalityvariable. When decline in historically referencedreputation for quality was 1SD above the mean(3.95), a one-unit increase in status predicted a 16.25%increase in corporate illegality (a net increase ofabout 5 percentage points).

Model 6 generated a coefficient for a term repre-senting an interaction between status and increasein socially referenced reputation for quality, but itwas not statistically significant.

Model 7 tested Hypothesis 4, which predictedthat the criminal acts of high-status banks shouldbe less frequent if the banks’ associates were tovalue a reputation for integrity. In support of thathypothesis, the coefficient for a term representingthe interaction between status and reputation forintegrity expectations of associates was negativeand significant (p < .01). A high-status bank willindeed tend to rein in illegal loan recovery prac-tices if its high-status associates value a reputationfor integrity. Figure 3 illustrates this effect. Whenreputation for integrity expectations of associateswas 1.37 (the mean), a one-unit increase in statusincreased corporate illegality by about 12.17%.When the integrity expectations variable tooka value 1SD above the mean (2.13), a one-unit in-crease in status increased corporate illegality byabout 10.39% (a net decrease of about 1.78 per-centage points).

Model 8 is the full model. In that model, the hy-pothesized effects of Hypotheses 1, 2, and 4 allproved significant and as predicted, but the effect ofHypothesis 3 was not significant. This should beinterpreted in light of the multicollinearity in thefull model introduced by the inclusion of five

TABLE2

(Con

tinued

)

Variables

Mod

el1

Mod

el2

Mod

el3

Mod

el4

Mod

el5

Mod

el6

Mod

el7

Mod

el8

Status3

Rep

utation

forintegrity

expectation

sof

associates

(Hyp

othesis

4)Con

stan

t20.87

01.06

31.07

6†1.21

1*1.09

4†0.94

00.72

20.41

0(3.81)

(0.67)

(0.64)

(0.61)

(0.65)

(0.71)

(0.67)

(0.65)

x2

1,18

6.88

551.21

577.30

672.37

623.34

551.79

601.49

1,26

7.75

MeanVIF

1.62

1.84

2.34

2.77

3.78

2.28

2.10

1.94

Note:

n5

393ba

nk-ye

arob

servations;

year

fixe

deffectsincluded

inallmod

els;

AR1errorstructure;rob

ust

stan

darderrors

inparen

theses.

†p<

.1*

p<

.05

**p<.01

***

p<

.001

(two-tailed

tests)

1302 OctoberAcademy of Management Journal

interaction effects. Further probing revealed a posi-tive and significant interaction between status anddecline in socially referenced reputation for quality(p < .01) when the interaction between status anddecline in historically referenced reputation forquality was not included in the model. Overall,Model 8 lends robustness to the conclusions aboutHypotheses 1, 2, and 4, tested individually.

Robustness Checks

Testing for endogeneity. The presence of endo-geneous regressors can lead to biased estimates.Endogeneity generally arises from unobserved het-erogeneity, measurement error, or simultaneity(Bascle, 2008). We took three measures to addressunobserved heterogeneity. First, the use of GEEmodels that accommodate serial autocorrelation

FIGURE 1Effects of Status and Decline in Historically Referenced Reputation for Quality on Corporate Illegality

05

1015

20

Pre

dic

ted

Nu

mbe

r of

Com

pla

ints

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23

Status

Small Decline (Mean) Large Decline (Mean + 1SD)

FIGURE 2Effects of Status and Decline in Socially Referenced Reputation for Quality on Corporate Illegality

05

1015

2025

Pre

dic

ted

Nu

mbe

r of

Com

pla

ints

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23

Status

Small Decline (Mean) Large Decline (Mean + 1SD)

2015 1303Krishnan and Kozhikode

and produce heteroskedasticity-consistent standarderrors to a great extent reduces endogeneity concernsarising from unobserved group-level heterogeneity(Katila & Ahuja, 2002). Second, including severalcontrols for alternative explanations addressedendogeneity concerns arising from omitted variables.For example, if both status and illegality are drivenby size, not including size as a control can lead toomitted variable bias, but including it limits thisproblem. Finally, we evaluated additional modelsthat included a lagged dependent variable as an ad-ditional regressor. Including lagged dependent vari-ables can limit concerns about endogeneity arisingfrom unobserved heterogeneity (Heckman & Borjas,1980; Katila & Ahuja, 2002). Because no data on il-legal loan recovery practices were available prior to2005, including a lagged dependent variable reducedthe sample to 314 bank-year observations. Theseanalyses are available from the authors on request.The lagged dependent variable was significant inseveral models, but it did not affect the results. Allfour hypothesized effects were significant and alongthe predicted directions. Hence those analyses lentadditional robustness to the findings.

Errors in measuring status or the controls for al-ternate explanations might also generate endoge-neity. In this study, status was quantified usingBonacich centrality, a well-established measure forstatus, but in additional analyses we tested the totalnumber of BSE500 firms listing a focal bank amongtheir preferred bankers each year as an alternative

(Phillips & Zuckerman, 2001). A second measurewas the residual from a regression of size againststatus. That measure was intended to help to iso-late the effect of status uninfluenced by size. Theresults with both of these alternative status mea-sures were consistent with those reported. Detailsof these analyses are also available on request.

The third concern is about endogeneity resultingfrom simultaneity: status influencing illegality, butalso illegality influencing status. We evaluated two-stage least squares (2SLS) instrumental variableregressions to address this concern. With five in-teraction effects, however, if status is endogenous,those interaction effects also become endogenous.This necessitates using as many instruments. Theproducts of the instrument for status and the mod-erating variables can serve as instruments, but itwill result in substantial efficiency loss. Econome-tricians suggest first testing whether a variable be-ing considered endogenous actually is endogenous(cf. Wooldridge, 2003: 527). Accordingly, we eval-uated a 2SLS regression using the number of yearsfor which a bank had been operating in Mumbaiand whether a bank was listed on the BSE as in-struments. A valid instrument is one that is stronglyrelated to the endogenous variables, but weaklyrelated (only through the instrumented variable) orunrelated to the dependent variable (Murray, 2006).Mumbai is considered to be the corporate capital ofIndia: Over a third of the BSE500 firms are head-quartered there. A bank that had been operating for

FIGURE 3Effects of Status and Associates’ Integrity Expectations on Corporate Illegality

05

1015

Pre

dic

ted

Nu

mbe

r of

Com

pla

ints

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23

Status