statutory mergers: the us experience · pdf filecompany law symposium 1 march 20131 march 2013...

TRANSCRIPT

Company Law Symposium1 March 20131 March 2013

Statutory Mergers: the US experienceTREVOR S NORWITZTREVOR S. NORWITZ

Topics to Cover

• How Mergers Work in the U SHow Mergers Work in the U.S.• Benefits of the Merger Structure

H V i St k h ld A P t t d• How Various Stakeholders Are Protected

2

How Mergers Work in the U.S.

1 Principal Types of M&A Agreement1. Principal Types of M&A Agreement 2. Requirements for a Statutory Merger3 M St t3. Merger Structures4. State versus Federal Law5. One-Step and Two-Step Mergers

3

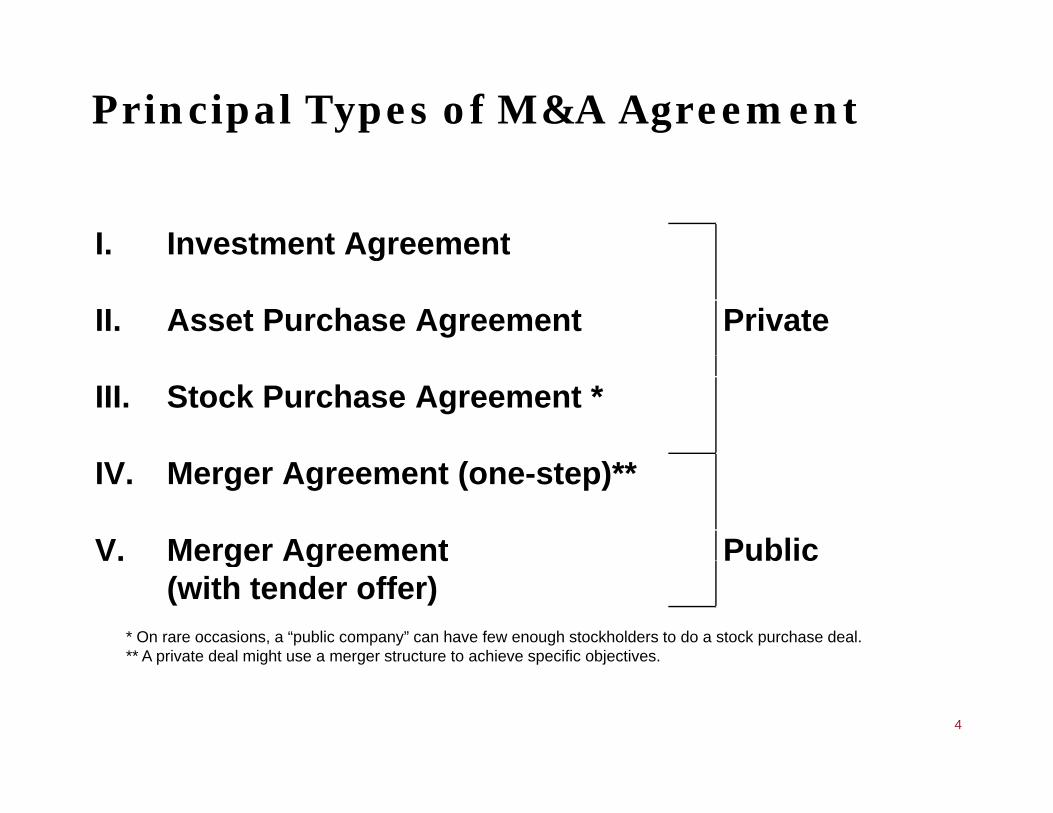

Principal Types of M&A Agreement

I. Investment AgreementI. Investment Agreement

II. Asset Purchase Agreement Private

III. Stock Purchase Agreement *

IV. Merger Agreement (one-step)**

V. Merger Agreement PublicV. Merger Agreement(with tender offer)

Public

* On rare occasions, a “public company” can have few enough stockholders to do a stock purchase deal.** A private deal might use a merger structure to achieve specific objectives.p g g p j

4

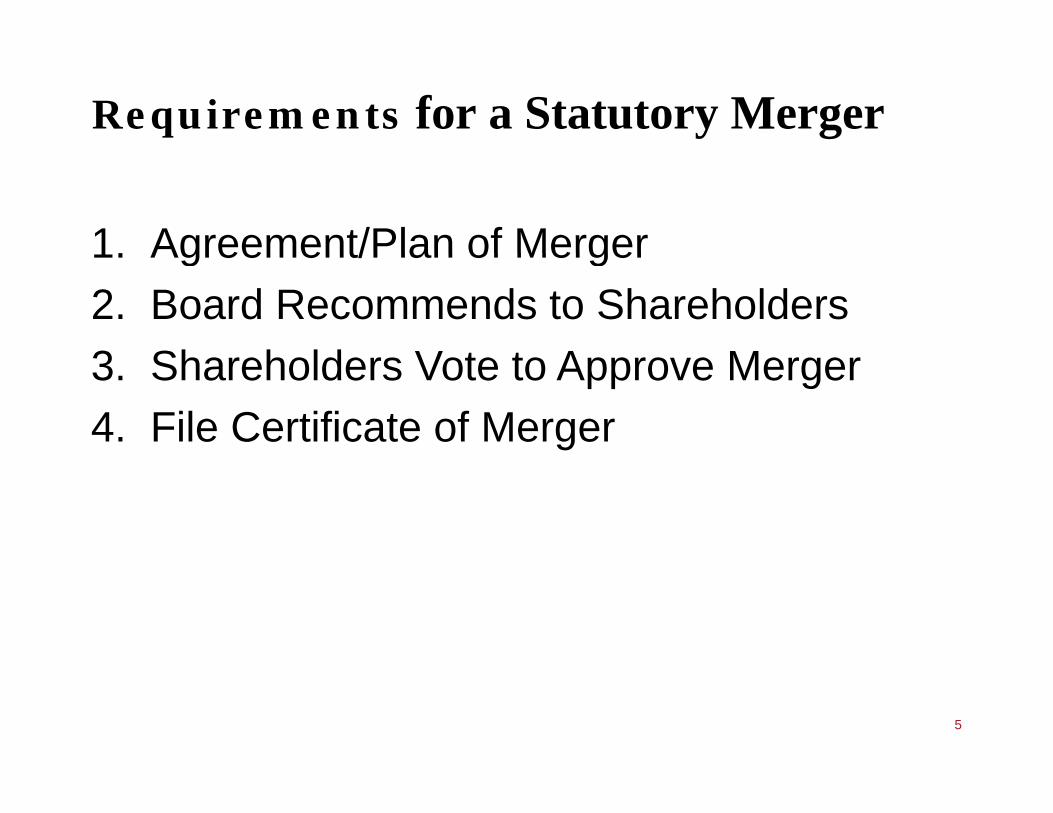

Requirements for a Statutory Merger

1 Agreement/Plan of Merger1. Agreement/Plan of Merger2. Board Recommends to Shareholders3 Sh h ld V t t A M3. Shareholders Vote to Approve Merger4. File Certificate of Merger

5

Mergers/Amalgamations Y (Al t) N SYou (Almost) Never See

Parent-to-Parent Merger Amalgamation

CompanyA

CompanyB

CompanyA

CompanyB

(New)Company

C

6

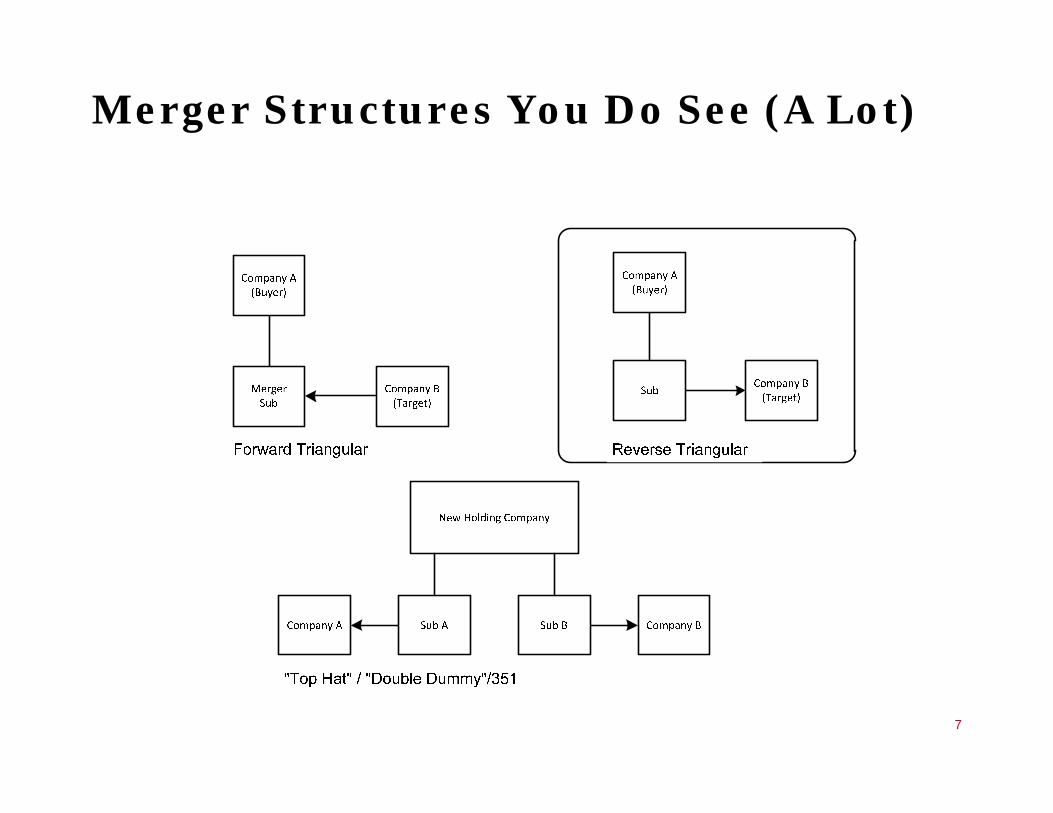

Merger Structures You Do See (A Lot)

7

A Two-Tiered System of Laws G US M&AGoverns US M&A

• State Law (statutes and courts) governs( ) g• Internal workings of companies• Duties of directors• Ability to adopt and maintain takeover defenses• Ability to adopt and maintain takeover defenses• Specific statutory takeover protections• Do consider fairness (especially in conflict situations)

• Federal Law (SEC) governs• Public offerings of securitiesPublic offerings of securities• Disclosure of information in public companies• Some substantive terms of tender offers

S li it ti f i f bli i• Solicitation of proxies for public companies• Not looking at fairness beyond disclosure

8

The 50 United States of America . . .5

9

d b l it. . . redrawn by popularity as a jurisdiction of incorporation.

10

Fortunately many of theFortunately, many of the “smaller” corporate jurisdictions follow thejurisdictions follow the Model Business Corporation Act

11

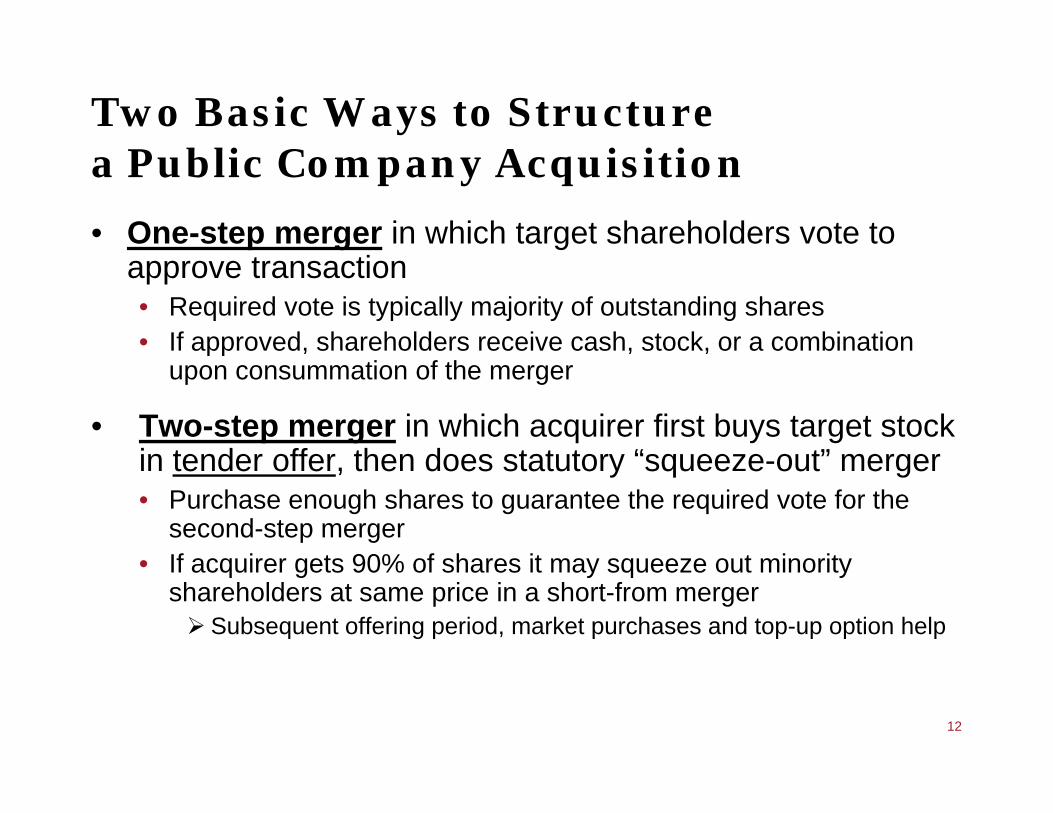

Two Basic Ways to Structure P bli C A i itia Public Company Acquisition

• One-step merger in which target shareholders vote to approve transaction• Required vote is typically majority of outstanding shares• If approved, shareholders receive cash, stock, or a combination pp

upon consummation of the merger

• Two-step merger in which acquirer first buys target stock in tender offer then does statutory “squeeze out” mergerin tender offer, then does statutory squeeze-out merger• Purchase enough shares to guarantee the required vote for the

second-step merger• If acquirer gets 90% of shares it may squeeze out minority• If acquirer gets 90% of shares it may squeeze out minority

shareholders at same price in a short-from merger Subsequent offering period, market purchases and top-up option help

12

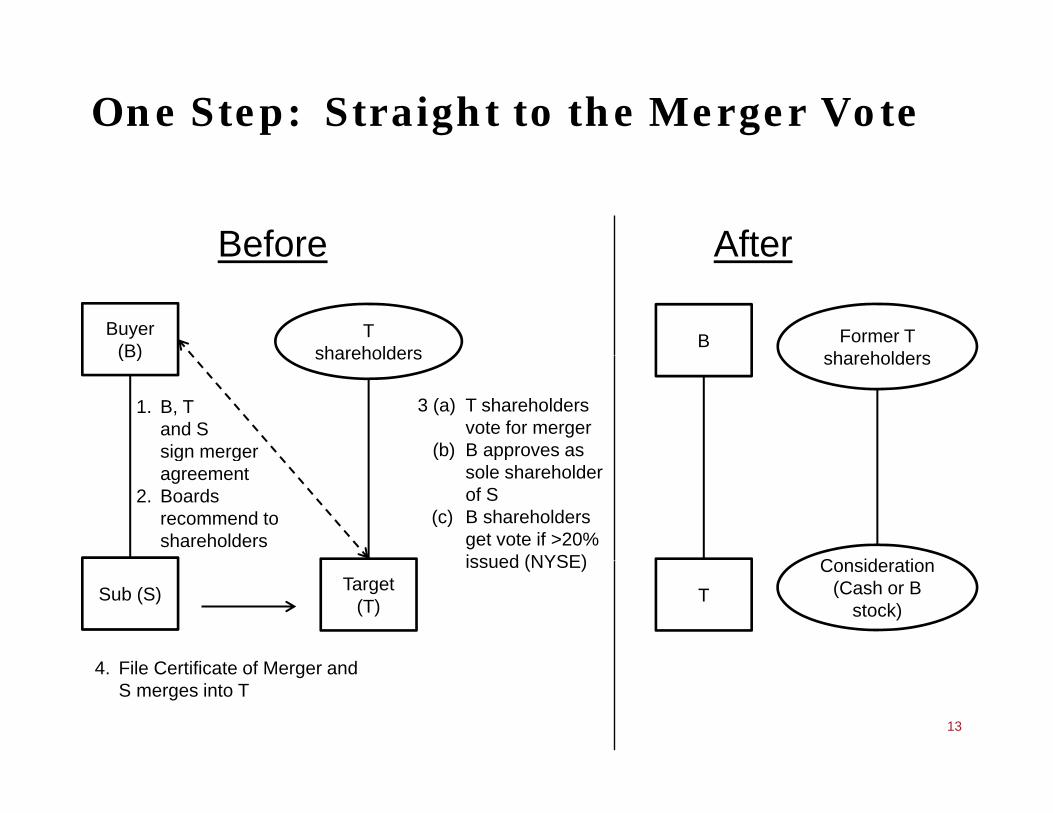

One Step: Straight to the Merger Vote

Before AfterBefore

Buyer (B)

Tshareholders

After

B Former T shareholders

1. B, Tand Ssign merger

3 (a) T shareholders vote for merger

(b) B approves as

(B) shareholders shareholders

g gagreement

2. Boards recommend to shareholders

( ) ppsole shareholder of S

(c) B shareholders get vote if >20% issued (NYSE) C id ti

4 Fil C tifi t f M d

issued (NYSE)

Sub (S) Target (T) T

Consideration (Cash or B

stock)

4. File Certificate of Merger and S merges into T

13

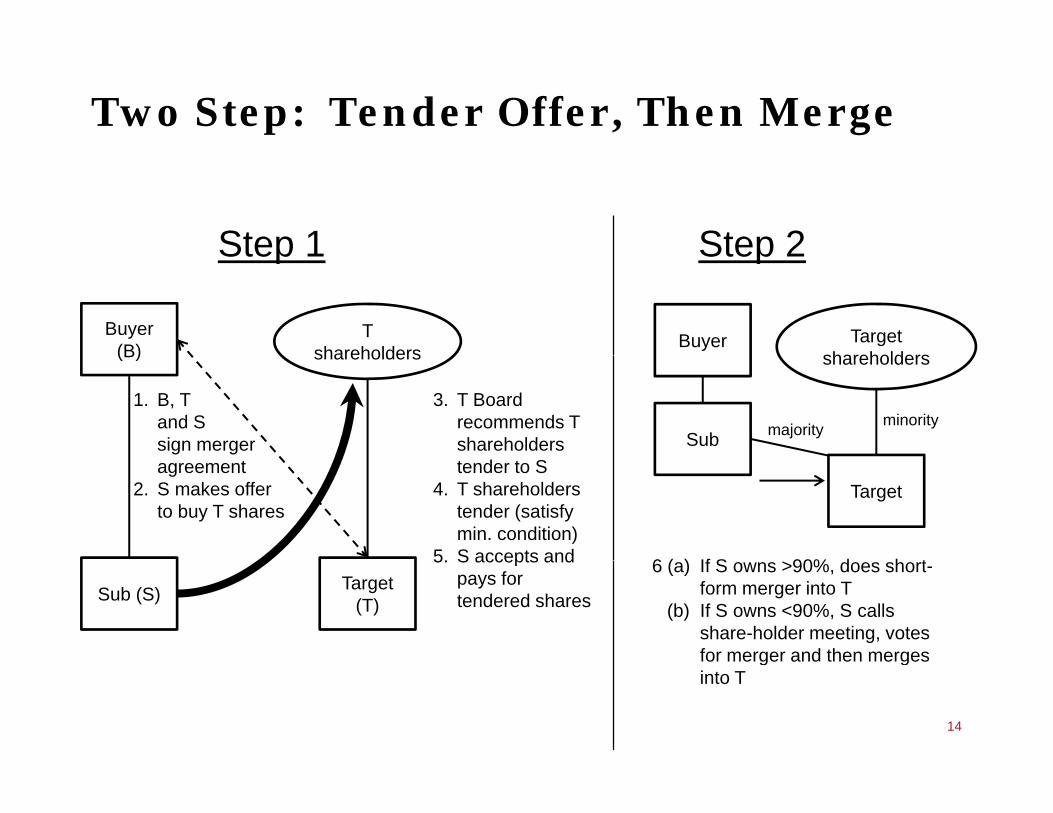

Two Step: Tender Offer, Then Merge

Step 1 Step 2Step 1

Buyer (B)

T shareholders

Step 2

Buyer Targetshareholders

1. B, Tand Ssign merger

3. T Board recommends T shareholders

(B) shareholders

Sub

shareholders

minoritymajority

agreement2. S makes offer

to buy T shares

tender to S4. T shareholders

tender (satisfy min. condition)

5. S accepts and

Target

6 ( ) If S 90% d h t5. S accepts and pays for tendered sharesSub (S) Target

(T)

6 (a) If S owns >90%, does short-form merger into T

(b) If S owns <90%, S calls share-holder meeting, votes for merger and then merges

14

g ginto T

Timing to Acquire a Public Company

Short Form Acquisition 4-8 weeks

Timing

90%* Filing of Certificate of MergerShort-Form Merger

Long-Form Merger

Acquisition Completed

Acquisition Completed

4-8 weeks

< 40 business days

3-5 months

100% Cash

90%

< 90%

(but more than 50%)

g o Ce ca e o e ge

> 50% vote

of all shareholders

Short-Form Merger

Acquisition Completed 5-12 weeks

Tender Offer/ Share Exchange

Offer

Part Cash/

than 50%)

90%* Filing of Certificate of Merger

Long-Form Merger

Acquisition Completed 3-6 months

Part Cash/Part Stock

< 90%

(but more than 50%)

> 50% vote

of all shareholders

Acquisition Completed

Acquisition

2-3 months (all cash)

3-4 months (part/all stock)Merger

(any form of consideration)

Post Proxy

SECReview > 50% shareholder vote

> 50% shareholder vote Acquisition Completed 4-8 weeks

NoSEC

Review

Post Proxy

* Including after Subsequent Offering Period and Top-Up Option, if applicable.15

Benefits of Tender Offer:T St O St MTwo-Step vs. a One-Step Merger

• No Pre-Clearance: SEC pre-clearance of cash tender offer pmaterials is not required

• Speed: a cash tender offer can be completed relatively i kl 20 b i d i th f f i dl d lquickly – 20 business days in the case of a friendly deal

not involving any regulatory issues• Direct: a tender offer is made directly to shareholders andDirect: a tender offer is made directly to shareholders and

does not require a shareholder meeting or board approval (so useful/necessary for a hostile takeover bid)

• Freeze-out: a tender offer between parent/subsidiary can avoid entire-fairness heightened review so long as certain conditions (e.g., majority of minority) are metconditions (e.g., majority of minority) are met

16

Benefits of One-Step Merger vs.T d Off (T St M )Tender Offer (Two-Step Merger)

• 100% Ownership: get to 100% ownership in a single step, p g p g pwhich may be important for financing the transaction.

• Possible Timing Advantage: if regulatory or other conditions d l l i t d ff f th th t fdelay closing tender offer for more than three to four months, the interloper risk can be eliminated (by securing shareholder approval) more quickly in a one-step merger than in a two-step tender offer.

• Flexibility in Structuring Consideration: Simpler to provide f h t k l ti ll tfor cash-stock elections, collars, etc.

• Flexibility to Buy Target Shares in the Market: Can buy target shares during deal pendency (subject to anytarget shares during deal pendency (subject to any applicable restrictions), which cannot in a tender offer.

17

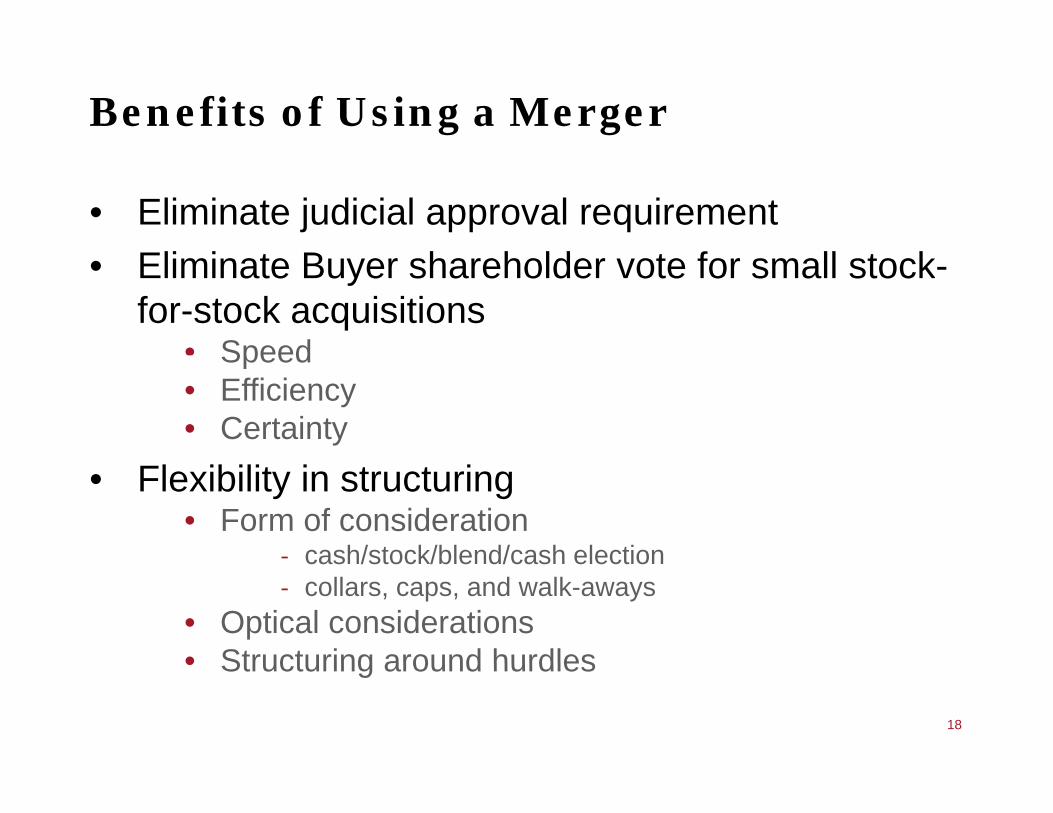

Benefits of Using a Merger

• Eliminate judicial approval requirementEli i t B h h ld t f ll t k• Eliminate Buyer shareholder vote for small stock-for-stock acquisitions

• SpeedSpeed• Efficiency• Certainty

• Flexibility in structuring• Form of consideration

‐ cash/stock/blend/cash electioncash/stock/blend/cash election‐ collars, caps, and walk-aways

• Optical considerations• Structuring around hurdles• Structuring around hurdles

18

Example: The Merck/Schering-Plough Merger“M difi d T H t/D bl D ”“Modified Top-Hat/Double Dummy”

AfterBefore

Schering-Plough(renamed Merck)Schering-Plough

1

Old MerckSub 2 Merck2

Sub 1

Merger 2:Sub 2 merges into Merck (1:1 basis)

Merger 1:Sub 1 merges into Schering-Plough(1:0 57 exchange ratio)(1:0.57 exchange ratio)

How Are All Stakeholders Protected?

CustomersGovernmentalEntities/Regulators

• Antitrust laws• Other regulatory regimes

(utility, telecom, financials)• Contract

• CFIUS (if applicable)• Antitrust and other

regulatory regimes

S li

• Antitrust law• Contract

• Approval right• Fiduciary

duties of

Company

SuppliersStockholdersBoard(litigation)

• Appraisalrights

• State anti-takeover laws

Other Companies

Employees,.

takeover laws• “Wall Street

walk”

Creditors

Other Companies(joint venturers,

M&A parties)Executives

• Contract• Contract

(benefit plans,

20• Contract• Fraudulent Conveyance law

• Contract( p ,union contracts, parachutes)

• Other legal regimes

How Are Shareholders Protected?

• Shareholder vote requirementT t ’ h h ld t• Target company’s shareholders must approve a merger

• SEC polices disclosure (also state courts)

• Strongest protection is directors’ fiduciary duties• Strongest protection is directors fiduciary duties • Actively policed by litigious plaintiffs bar and

sophisticated judiciary (especially in Delaware)sophisticated judiciary (especially in Delaware)

• State law anti-takeover statutes• Business Combination; Control Share Acquisition• Business Combination; Control Share Acquisition

statutes• Dissenters’ Appraisal RightsDissenters Appraisal Rights

21

Appraisal Rights

• Important theoretical protection for minority shareholders (given the law’s deference to majority shareholders) but(given the law s deference to majority shareholders) but not often invoked in practice

• How do buyers achieve certainty?y y• Statute specifies fair value is standalone and without synergies• Judges recognize value of arm’s-length sale process

Ri k f l l l it d l l f d t t i• Risk of lower value, long wait and legal fees deter opportunism• Buyers can also build in self-help (5% assertion condition)

• Potential risks under Section 164:Potential risks under Section 164:• Judge interpreting “fair value” could consider sale premium• What is a “reasonable interest rate”?

22

State Law on Takeover Bids

• Directors owe shareholders duties of care and loyalty• Three standards of judicial review• Three standards of judicial review

• Business Judgment Rule generally recognizes Board’s prerogative to manage the company acting loyally and with due care

• Enhanced Scrutiny in takeover defenses– Unocal – reasonable response to perceived threat to company– Unitrin – defense must not be preclusive– Household to Airgas – upholds “poison pill” defense

• Entire Fairness Standard applies if conflict of interests– Increasing reliance on Special Committees/Majority-of-Minority

• Revlon Rule – If selling control, get best available price• Blasius Rule – May not mess with the shareholder franchise• Specific state takeover statutes apply

23

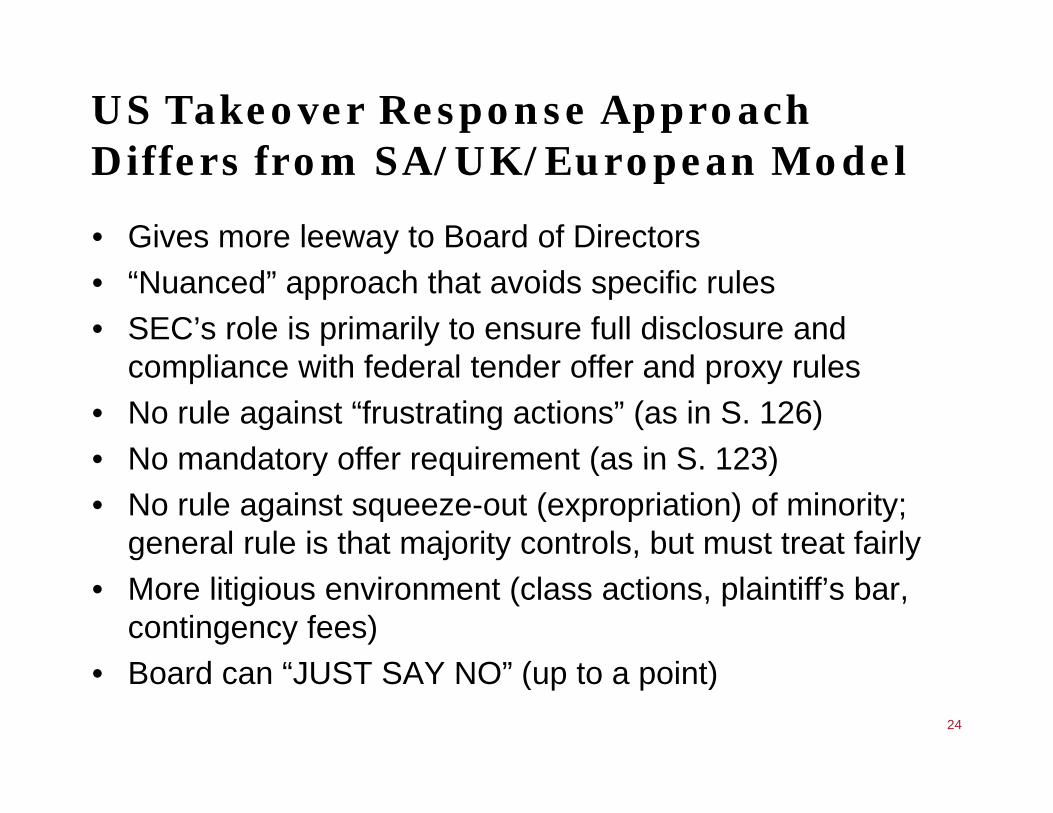

US Takeover Response Approach Diff f SA/UK/E M d lDiffers from SA/UK/European Model

• Gives more leeway to Board of Directors y• “Nuanced” approach that avoids specific rules• SEC’s role is primarily to ensure full disclosure and

li ith f d l t d ff d lcompliance with federal tender offer and proxy rules• No rule against “frustrating actions” (as in S. 126)• No mandatory offer requirement (as in S 123)• No mandatory offer requirement (as in S. 123)• No rule against squeeze-out (expropriation) of minority;

general rule is that majority controls, but must treat fairly• More litigious environment (class actions, plaintiff’s bar,

contingency fees) B d “JUST SAY NO” ( t i t)• Board can “JUST SAY NO” (up to a point)

24

25