steel long term final edited - karvy commodities

TRANSCRIPT

STEEL

DYNAMICS & OUTLOOK

COMMODITY DYNAMICS SUPPLY HIGH DEMAND HIGH INPUT COST HIGH OUTPUT PRICE STABLE

RESULT OPERATING MARGINS LOW

LIKELY OUTCOME PRICES HIGH

August 7, 2008

2

Table of Contents Steel ................................................................................................................................................................ 3

Classification of Steel .......................................................................................................................... 3

Methods of Production ................................................................................................................... 7

Steel Industry ‐ Global Scenario ......................................................................................................... 9

Indian Steel – Growth & Performance .......................................................................................... 12

Steel Industry Structure in India ................................................................................................. 15

Indian Sponge Iron Industry ..................................................................................................... 16

Indian Pig Iron Industry ......................................................................................................... 17

Induction Furnace Industry .............................................................................................. 18

Electric Arc Furnace Industry ...................................................................................... 18

Prospects of Indian Steel .................................................................................................................... 19

Demand‐Supply Dynamics ............................................................................................................. 20

Indian Economy Highlights ....................................................................................................... 22

Fundamental Outlook .......................................................................................................................... 23

Technical Outlook .................................................................................................................................. 27

3

Steel Steel is one such material that has played an important role in the development of mankind

in the last century. Today, it is difficult to imagine a world without steel. Steel has become

vital to our everyday life. It is at the root of the quality of life that each of us enjoys today,

helping to shelter us, to feed us and to facilitate both our working day and leisure activities.

We depend on steel for almost everything from our houses and buildings, the cars we drive,

roads, bridges, agricultural equipment, machines—the list is endless.

Steel is superior to others because of its versatility, its strength, and its recyclability. There

are few other materials that can be recycled over and over again without loss of properties.

Even steel created 150 years ago can be recycled today and used in new products and

applications. Steel has a very low production cost. If compared to its nearest competitor,

aluminium, steel requires only 25% of the energy for production. Steel is also been tagged

as an environment friendly metal due to its recyclable nature.

Steel is not a single product. There are currently more than 3,500 different grades of steel

with many different physical, chemical and environmental properties. Approximately, 75%

of modern steels have been developed in the last 20 years. If the Eiffel Tower was to be

rebuilt today, the engineers would only need one‐third of the amount of steel. Modern cars

are built with new steels that are stronger, but up to 25% lighter than in the past.

Today, consumption of steel is also regarded as an indicator of development of a nation. Per

capita steel consumption is now universally accepted as an index of economic development

of a nation. Given its role, steel has established itself as the backbone of any economy.

4

Classification of steel

Crude steel:

The term is internationally used to mean the first solid steel product upon solidification of

liquid steel. In other words, it includes ingots (in conventional mills) and semis (in modern

mills with continuous casting facility). According to International Iron & Steel Institute

(IISI), for statistical purpose, crude steel also includes liquid steel which goes into

production of steel castings.

Saleable steel:

The term is used to designate various types of solid steel products, which are sold to

outside customers for further processing or for direct use/consumption. Therefore, it

includes ingots and/or semis and/or finished steel products. (Liquid steel is normally not

traded).

As per form/shape/size:

a) Liquid steel:

Liquid steel is the immediate hot molten steel product from the steel melting shop (LD

converter/electric arc furnace/electric induction furnace/energy optimizing furnace). It is

further cast into ingots/semis. The by‐product from the steel melting shop is called SMS

slag.

b) Ingot steel (ingots):

Ingots are the primary solid product obtained upon solidification of liquid steel in

conventional, vertical, cast iron moulds, which are intended for rolling into

intermediate/semi‐finished products after re‐heating. Ingots are normally very large and

heavy weighing several tonnes (up to 15‐20 tonnes). Small ingots produced in mini‐steel

plants are called as pencil ingots.

c) Semifinished steel products (semis):

Intermediate solid steel products obtained by hot rolling/forging of ingots (in conventional

process) or by continuous casting of liquid steel are known as semis. These are so called

5

since they are intended for further rolling/forging to produce finished steel products.

Blooms, billets, and slabs are the kinds of semis existing in the industry.

As per finished steel:

Finished steel can be defined as products obtained upon hot rolling/forging of semi‐

finished steel. These cover two broad categories of products, namely, Long products and

Flat products:

a) Long products:

Longs are finished steel products produced normally by hot rolling/forging of

bloom/billets/pencil ingots into useable shape/sizes. These are normally supplied in

straight length/cut length except wire rods, which are supplied in irregularly wound coils.

The long products category mainly consists of bars and rods which form around 40% of the

structure of the steel long section. These are further divided into wire rods, reinforcing

rods, thermo mechanically treated (TMT) steel rebars, cold heading quality wire rods, and

tyre cord wire rods. Other sections of steel long consist of structural and railway materials.

b) Flat products (flat rolled products):

Finished steel thin flat products are produced from slabs/thin slabs in rolling mills using

flat rolls. These are supplied in hot rolled (HR), cold rolled (CR) or in coated condition,

depending on the requirement. Plates, sheets and strips are different types of flat products.

While plates are used for applications such as shipbuilding, etc., HR steel is the most widely

used variety of steel, and other downstream flat products such as CR steel and galvanized

steel are made from it.

HR steel has a variety of applications in the manufacturing sector. It is primarily used for

making pipes and has many direct industrial and manufacturing applications, including

construction of tanks, railway cars, bicycle frames, ships, engineering and military

equipment, automobile and truck wheels, and frames and body parts. Cold rolled steel is

used primarily for precision tubes, containers, bicycles, furniture and for use by the

automobile industry to produce car body panels. Galvanized steel is used for making roofs

in the housing and construction sector.

6

A specific variety of cold rolled sheets / strips with specific chemical composition comes

under the coated products category. Varieties of coated products are available around the

industry like galvanized sheets (coated with zinc metal), tin plate (coated with tin metal),

tin free steel (coated with chromium metal and oxide), etc. Among all the coated products,

galvanized sheets are most popular and are used mainly in roofing, panelling, automobile

bodies, trunks/boxes and others.

Steel as per composition:

a) Alloy steel:

Steel that is produced with intended amount of one or more alloying elements in specified

proportions to impart specific physical, mechanical, metallurgical and electrical properties.

Common alloying elements are manganese, silicon, nickel, lead, copper, chromium,

tungsten, molybdenum, niobium, vanadium, etc.

Some of the common examples of alloy steels include stainless steel, silicon‐electrical steel

and high‐speed steel.

b) Nonalloy / carbon steel/ plain carbon / unalloyed steel:

These steels, by definition, do not contain any alloying element in specified proportions

(i.e., beyond those normally present in commercially produced steel in industry). Non‐

alloy steel is divided into three categories, namely:

Low carbon steel or mild steel (normally containing up to 0.3% carbon)

Medium carbon steel (normally containing 0.3 – 0.6% carbon)

High carbon steel (normally containing more than 0.6% carbon)

Non‐alloy steel constitutes approx. 90% of total steel production, of which mild steel takes

the lion’s share.

c) Special steel:

Steel which requires special care so as to attain the special/desired properties, such as

cleanliness, surface qualities and mechanical/metallurgical properties falls under the

7

special steel category. In layman’s language, all steel other than mild steel fall under the

category of special steel. However, metallurgically speaking, even mild steel/low carbon

steel, i.e., containing less than 0.25%/0.30% carbon may still fall under the category of

special steel if any special property is specified in the steel. Examples are DD / EDD steel,

Forging Quality steel, Free Cutting steel etc.

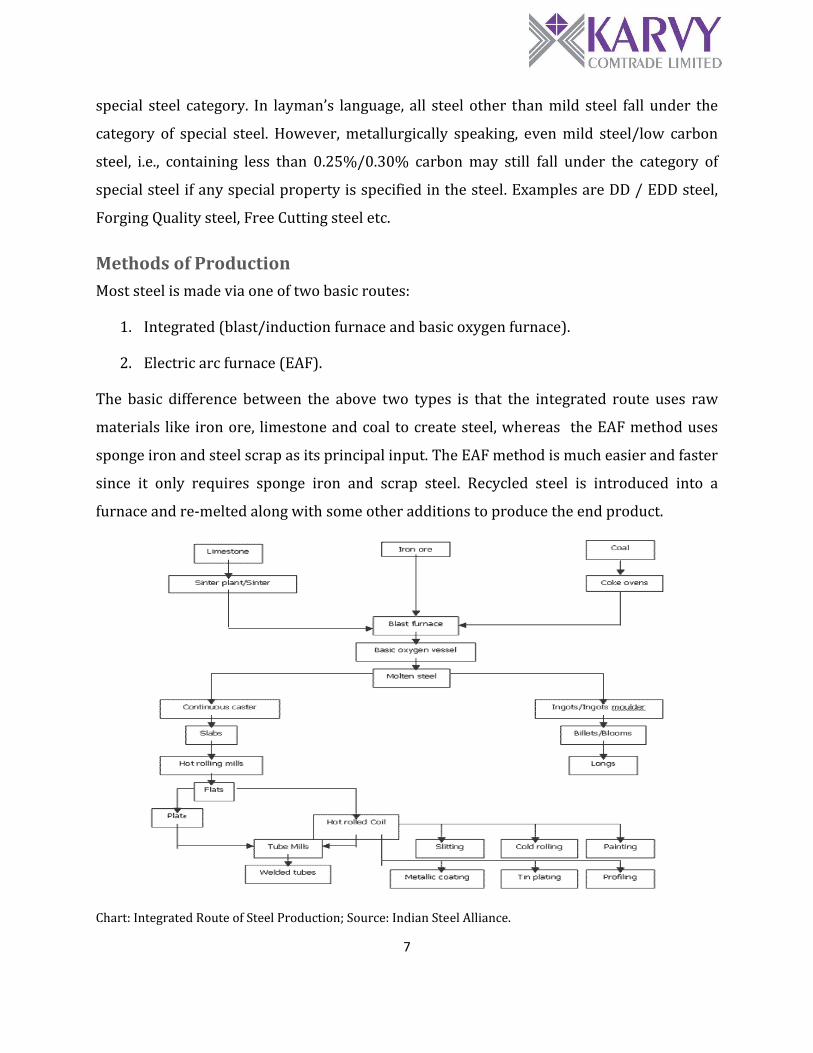

Methods of Production Most steel is made via one of two basic routes:

1. Integrated (blast/induction furnace and basic oxygen furnace).

2. Electric arc furnace (EAF).

The basic difference between the above two types is that the integrated route uses raw

materials like iron ore, limestone and coal to create steel, whereas the EAF method uses

sponge iron and steel scrap as its principal input. The EAF method is much easier and faster

since it only requires sponge iron and scrap steel. Recycled steel is introduced into a

furnace and re‐melted along with some other additions to produce the end product.

Chart: Integrated Route of Steel Production; Source: Indian Steel Alliance.

8

Chart: EAF Route of Steel Production; Source: Indian Steel Alliance.

9

Steel industry: Global scenario The world steel industry is currently going through an extraordinary phase of growth and

all‐round prosperity, fuelled primarily by the frenetic pace of growth in consumption and

production of steel in China. World crude steel production grew from 848 million tonnes in

2001 to approximately 1,344 million tonnes in 2007, recording a compounded annual

growth (CAGR) of 7.31% compared to a mere 2% CAGR recorded between 1995 and 2001.

It has been observed that the steel Industry has grown tremendously in the last one and a

half decade with a strong financial condition. The increasing demand for steel from

developing countries for its infrastructural projects has pushed the companies in this

industry near their operative capacity. The most significant growth in the steel industry

has been observed during the period 1960‐1974 when steel consumption globally doubled.

Between these years, the global steel industry grew at 5.5% per annum. This roaring

market saw a phase of deceleration from the year 1975 which continued until 1982. Post

this period, the continuous fall slowed down and the industry started its upward

movement again from the early 1990s.

The global steel industry is becoming increasingly competitive with every passing day.

From 1960s to late‐1980s, the steel market was dominated by OECD (Organization for

Economic Cooperation and Development) countries, but with the fast emergence of

developing countries like China, India and South Korea in this sector, the OECD countries’

market share has slipped. The main demand creators for the steel industry are

automobiles, construction, infrastructure, oil & gas and container sectors.

From 2001 to 2007, the world steel production and consumption has been growing at a

CAGR of 7.30% and 7.20%, respectively. In 2007, world crude steel output reached 1,344

million metric tonnes (mmt). This is an increase of 7.5% over 2006. The total represents

the highest level of crude steel output in history and it is the fifth consecutive year that

world crude steel production grew by more than 7%.

10

On the other hand, world crude steel consumption for the year 2007 grew by 6.84% to

1,198 million tonnes. The gross surplus of crude steel (output usage) in 2007 accounted for

nearly 10% (146.4 million tonnes) of the total output.

848 850904

9701069

11421244

13441442

757 775815

895974

10261121

11981279

500600700800900100011001200130014001500

2000 2001 2002 2003 2004 2005 2006 2007 2008 (E)

In Million M

etric Tonnes

World Crude Steel Facts

Production Consumption Source: IISI

The major steel‐producing countries include China, Japan, United States, Russia and South

Korea. China remains the driving force behind the strong world production figures and

accounts for almost 36.4% of the total world crude steel output.

43%

19%

11%

9%

6%

5%4% 3%

Major Crude Steel Producers

China

EU

Japan

USA

Russia

India

South Korea

Source: IISI

11

Rank Company Name Production (mmt)1 Arcelor Mittal 116.42 Nippon Steel 35.73 JFE 344 POSCO 31.15 Baosteel 28.66 Tata Steel 26.57 Anshan‐Benxi 23.68 Jiangsu Shagang 22.99 Tangshan 22.810 US Steel 21.5

Top Crude Steel Producers in the World

Source: IISI

In 2007, ArcelorMittal was top ranked among the world’s major steel producers. India’s

Tata Steel emerged as the sixth‐largest steel company producer after it had acquired Corus.

Globally, steel prices have witnessed a sharp rise due to the increased demand and rising

raw material prices, especially for iron ore and coking coal. This, followed with higher

energy and freight charges, has resulted in sharp movement in steel prices. The long‐term

linear trend in steel prices is explained in the following chart.

0

100

200

300

400

500

600

8/12

/200

3

11/12/20

03

2/12

/200

4

5/12

/200

4

8/12

/200

4

11/12/20

04

2/12

/200

5

5/12

/200

5

8/12

/200

5

11/12/20

05

2/12

/200

6

5/12

/200

6

8/12

/200

6

11/12/20

06

2/12

/200

7

5/12

/200

7

8/12

/200

7

11/12/20

07

2/12

/200

8

5/12

/200

8Bloomberg World Iron & Steel Index

Source: Bloomberg

12

Indian steel: Growth and performance At the time of independence in 1947, India had only three steel plants: Tata Iron & Steel

Company, Indian Iron and Steel Company, and Visvesvaraya Iron & Steel, and a few electric

arc furnace based plants. The period until 1947 thus witnessed a small but viable steel

industry in the country, which operated with a capacity of about one million tonne, and was

completely in the private sector. From the fledgling one million tonne capacity status at the

time of independence, India has now risen to become the fifth‐largest crude steel producer

in the world and the largest producer of sponge iron. As per the official estimate, the iron

and steel industry contributes around 2% of the gross domestic product (GDP) and its

weight in the Index of Industrial Production (IIP) is 5.13%. From a negligible global

presence, the Indian steel industry is now acknowledged for its product quality, reflected

by trends of rising exports. Indian companies have also now made a mark in the global

mergers and acquisitions market.

As it traversed its long history during the past 60 years, the Indian steel industry has

responded to the challenges of the highs and lows of business cycles. The first major

change came during the first three Five Year Plans (1952‐1970), when in line with the

economic order of the day, the iron and steel industry was earmarked for state control.

From the mid‐50s to the early 1970s, the government thus set up large integrated steel

plants in the public sector at Bhilai, Durgapur, Rourkela and Bokaro. The policy regime

governing the industry during these years involved:

Licensing of capacity and reservation of large‐scale capacity creation for the

public sector units.

A dual pricing system, price and distribution control for the integrated large‐

scale producers in both private and public sectors, while the rest of the industry

operated in a free market.

Quantitative restrictions and high tariff barriers.

Railway freight equalization policy, to ensure balanced regional industrial

growth.

13

Controls on imports of inputs, including technology, capital goods, mobilization

of finances, and exports.

The large‐scale capacity creation in the public sector during these years contributed to

making India the 10th largest steel producer in the world as crude steel production grew

markedly to nearly 15 million tonnes in the span of a decade from a mere one million tonne

in 1947. But the trend could not be sustained from late‐1970 onwards, as the economic

slowdown adversely affected the pace of growth of the Indian steel industry. However, this

phase was reversed in 1991‐92, when the country replaced the control regime by

liberalization and deregulation in the context of globalization. The provisions of the New

Economic Policy initiated in the early‐1990s impacted the Indian steel industry in many

ways:

Large‐scale capacities were removed from the list of industries reserved for the

public sector.

Licensing requirement for additional capacities was also withdrawn subject to

locational restrictions.

Private sector came to play a prominent role in the overall set up.

Pricing and distribution control mechanisms were discontinued.

Iron and steel industry was included in the high priority list for foreign

investment, implying automatic approval for foreign equity participation up to

50%, subject to the foreign exchange and other stipulations governing such

investments in general. This limit has since been increased to 100%.

Freight equalization scheme was replaced by a system of freight ceiling.

Peak import tariff rates were reduced from more than 100% to about 30%

average, which is now reduced to nil.

Quantitative import restrictions were largely removed. Export restrictions were

withdrawn.

14

The system, therefore, underwent marked changes. For steel makers, opening up of the

economy opened up new channels of procuring their inputs at competitive rates from

overseas markets and also new markets for their products. It also led to greater access to

information on global operations/techniques in manufacturing. This, along with the

pressures of a competitive global market, increased the need to enhance efficiency levels so

as to become internationally competitive. The steel consumer, on the other hand, was now

able to choose items from an array of goods, be it indigenously manufactured or imported.

The National Steel Policy (NSP) was announced in November 2005 as a basic blueprint for

the growth of a self‐reliant and globally competitive steel sector. The Policy sought to

enhance the indigenous steel production to 110 million tonnes per annum by 2019‐20 from

the 2004‐05 level of 38 million tonnes, implying a compounded annual growth rate of

7.3%. The long‐term objective of the National Steel Policy is to ensure that India has a

modern and efficient steel industry of world standards, catering to diversified steel

demand. The focus of the policy is to attain levels of global competitiveness in terms of

global benchmarks of efficiency and productivity.

The National Policy seeks to facilitate the removal of procedural and policy bottlenecks that

affect the availability of production inputs, increased investment in research and

development, and the creation of road, railway and port infrastructure. The policy focuses

on the domestic sector, but also envisages a steel industry growing faster than domestic

consumption, which will enable export opportunities to be realized.

However, while the National Steel Policy indicated production and consumption targets for

2019‐20 at 110 million tonnes and 90 million tonnes, respectively, the Working Group on

Steel Industry set up by the Planning Commission for the 11th Five Year Plan (2007‐12)

has projected a total demand of 70.34 million tonnes for finished steel and a total

production of 80.23 million tonnes of crude steel by the end of the 11th Plan, i.e., 2011‐12.

15

Steel Industry Structure in India The Indian steel industry can be divided into two distinct producer groups:

1. Main/Major producers: Main producers group includes large steel producers with

high levels of backward integration and capacities. Steel Authority of India Limited

(SAIL), Tata Steel Ltd (TSL) and Rashtriya Ispat Nigam Limited (RINL) form this group.

These companies produce steel using the blast furnace/basic oxygen furnace (BF/BOF)

route that uses iron ore, coal/coke as the basic input mix for producing finished steel.

Other major producers such as Essar Steel, Ispat Industries, Jindal Vijaynagar Steel Ltd.

use routes other than BF/BOF for producing steel. Essar Steel and Ispat Industries

employ the electric arc furnace (EAF) route that uses sponge iron, melting scrap or a

mix of both as input. JVSL uses COREX, a revolutionary technology for making steel

using basically iron‐ore and coal.

2. Other producers: This group consists of smaller stand‐alone steel plants that include

producers and processors of steel.

Processors/Re‐rollers: Units producing small quantities of steel (flat/long products)

from materials procured from the market or through their own backward

integration system.

Stand‐alone units making pig iron and sponge iron.

Small producers using scrap‐sponge iron‐pig iron combination produce steel ingots

(for long products) using the electric arc furnace (EAF) or the induction arc furnace

(IAF) route.

The major producers are strategic in nature and account for most of the mild steel

production in the country. The group produces most of the flat steel products in the

country, including hot rolled, cold rolled and galvanised steel. The majors also produce a

small proportion of long products and other special steel being produced in the country.

Other producers account for a majority of long products being produced in the country,

and some of the value‐added flat steel products like cold rolled steel and galvanized steel.

16

Indian sponge iron industry Sponge iron/direct reduced iron/hot briquetted iron is the solid metallic iron product

obtained upon direct reduction of high‐grade iron ore in solid state itself without being

converted into liquid form like that in a blast furnace.

India is the world’s largest producer of sponge iron. The growth of sponge iron, especially

during the last 5‐6 years in terms of capacity and production has been substantial. The

installed capacity of sponge iron increased from 1.52 million tonnes per annum in 1990‐91

to 26.39 million tonnes in 2004‐05. Sponge iron production grew at a CAGR of 22% to

reach a level of 18.35 million tonnes in 2006‐07 compared to 7.86 million tonnes in 2002‐

03. At present, there are 324 sponge iron units installed in the country having a capacity of

26.39 million tonnes per annum. Out of these, there are 321 coal‐based units in operation

with a capacity of 18.40 million tonnes per annum. There are three gas‐based units

covering a capacity of 7.99 million tonnes per annum. The production of sponge iron units

during the last few years is shown as under:

9.8712.53

14.82

18.34

13.9

02468

101214161820

2003‐04 2004‐05 2005‐06 2006‐07 2007‐08 (Apr‐Dec)

In Million Tonnes

India ‐ Sponge Iron Production

5.9

7.89

10.28

13.08

9.88

3.97 4.64 4.54 5.264.02

0

2

4

6

8

10

12

14

2003‐04 2004‐05 2005‐06 2006‐07 2007‐08 (Apr‐Dec)

In Million Tonnes

Sources of Sponge Iron Production

Coal Based Gas Based

5000

10000

15000

20000

25000

30000

12/6/200

51/6/20

062/6/20

063/6/20

064/6/20

065/6/20

066/6/20

067/6/20

068/6/20

069/6/20

0610

/6/200

611

/6/200

612

/6/200

61/6/20

072/6/20

073/6/20

074/6/20

075/6/20

076/6/20

077/6/20

078/6/20

079/6/20

0710

/6/200

711

/6/200

712

/6/200

71/6/20

082/6/20

083/6/20

084/6/20

085/6/20

086/6/20

087/6/20

08

Rupe

es per to

nne

MCX Sponge Iron Prices

0

50

100

150

200

250

USD

/Metric ton

China Import Indian Iron Ore Price

Source: Steel Ministry & Bloomberg

17

Indian pig iron industry Pig iron is the product in solid (lumpy) form obtained upon solidification of hot metal

(liquid iron) in Pig Casting Machine. It is called “pig” or “pig iron” because of its typical

humpy shape. It is one of the basic raw materials required by the foundry and casting

industry for manufacture of various types of castings for the engineering sector. Usha

Martin Industries, Jindal Steel & Power and Ispat Industries have integrated the mini blast

furnace (MBF) and are using the hot metal in the charge‐mix directly for manufacture of

steel through the electric arc furnace. Hospet Steel, a joint venture of Kalyani and Mukand

and Southern Iron and Steel Company (now a part of JSW Steel) have integrated their MBF

with energy optimising furnace for manufacture of steel. The excess hot metal produced by

them supplements the pig iron production. Besides MBF, a COREX plant (alternative to

conventional MBF/ BF) along with downstream steel‐making through basic oxygen furnace

(BOF), which has been commissioned in Karnataka by JSW Steel, also supplements the

production of pig iron. The production of pig iron during the past few years is shown in the

chart below.

3.7643.228

4.6954.993

3.901

0

1

2

3

4

5

6

2003‐04 2004‐05 2005‐06 2006‐07 2007‐08 (Apr‐Dec)

In Million Tonnes

India ‐ Pig Iron Production

Source: Steel Ministry

18

Induction furnace industry India is the first country using “induction melting furnaces” for making mild steel. As a

matter of fact, EAFs are not making mild steel of structural quality for over a decade now.

The bulk of structural quality mild steel for long products is manufactured by induction

melting furnaces. There are several reasons for the popularity of induction melting

furnaces for making steel. They consume less power compared to EAFs; expenditure on

electrode is nil; they use lesser quantity of refractory; and initial investment is less on plant

and equipment. Thus, there are economic advantages in making steel through the induction

furnaces route. During 2006–07, it is estimated that 970 units with a capacity of 19.50

million tonnes were in operation. The total production of induction furnace units

registered a growth of 14% during 2006‐07, producing 15.39 million tonnes against a

production of 13.49 million tonnes in 2005–06, as reported to the Joint Plant Committee.

Electric arc furnace industry Currently, there are 36 electric arc furnace based steel plants operating in the country with

an aggregate capacity of 13.80 million tonnes per annum. Apart from the operating units,

there are around three units that are closed. Production of ingots/concast billets by EAF

units, which have been reporting their production to the Joint Plant Committee, during

2006‐07, was 9.88 million tonnes as compared to 8.43 million tonnes during 2005‐06,

registering a growth of 17%. This sector continues to face challenges of rising cost of

inputs, increasing power tariffs, shortage of power and resource crunch.

19

Prospects of Indian steel The Indian steel industry is on an upswing the world over. Indian steel‐making units, both

in the private and public sectors, remain upbeat about their improved volume of turnover,

capacity utilization, sales and profit margins. A number of MOUs have been signed by major

steel producers, both domestic and international, with the mineral rich states signifying

possibilities of marked increase in both Greenfield and Brownfield production capacities.

While private steel majors like Tata Steel have moved towards a globalised growth strategy

based on mergers and foreign acquisitions, the public sector majors like Steel Authority of

India Limited (SAIL) or Rashtriya lspat Nigam Limited (RINL) have eliminated huge

accumulated losses and become commercially buoyant.

In India, the steel sector is growing at a robust rate with significant increases in both

production and consumption. Crude steel production grew more than 10% annually from

34.71 million tonnes in 2002‐03 to 50.82 million tonnes in 2006‐07. This growth was

driven by both capacity expansion (from 40.41 million tonnes in 2002‐03 to 56.84 million

tonnes in 2006‐07) and improved capacity utilization (from 86% in 2002‐03 to 89% in

2006‐07).

34.71

38.73

43.44

46.46

50.82

39.61

0 10 20 30 40 50 60

2002‐03

2003‐04

2004‐05

2005‐06

2006‐07

2007‐08 (Apr‐Dec)

Units in million tonnes

Crude Steel Production

Source: Steel Ministry

India emerged as the 5th largest crude steel producing country in the world as against 8th

position in 2003. It is expected to become the second‐largest producer of steel in the world

by 2015. The present per capita consumption in the country is only around 35kg against

20

the world average of 150kg, and 400 kg in developed countries, and this reflects the growth

potential the steel industry has in India.

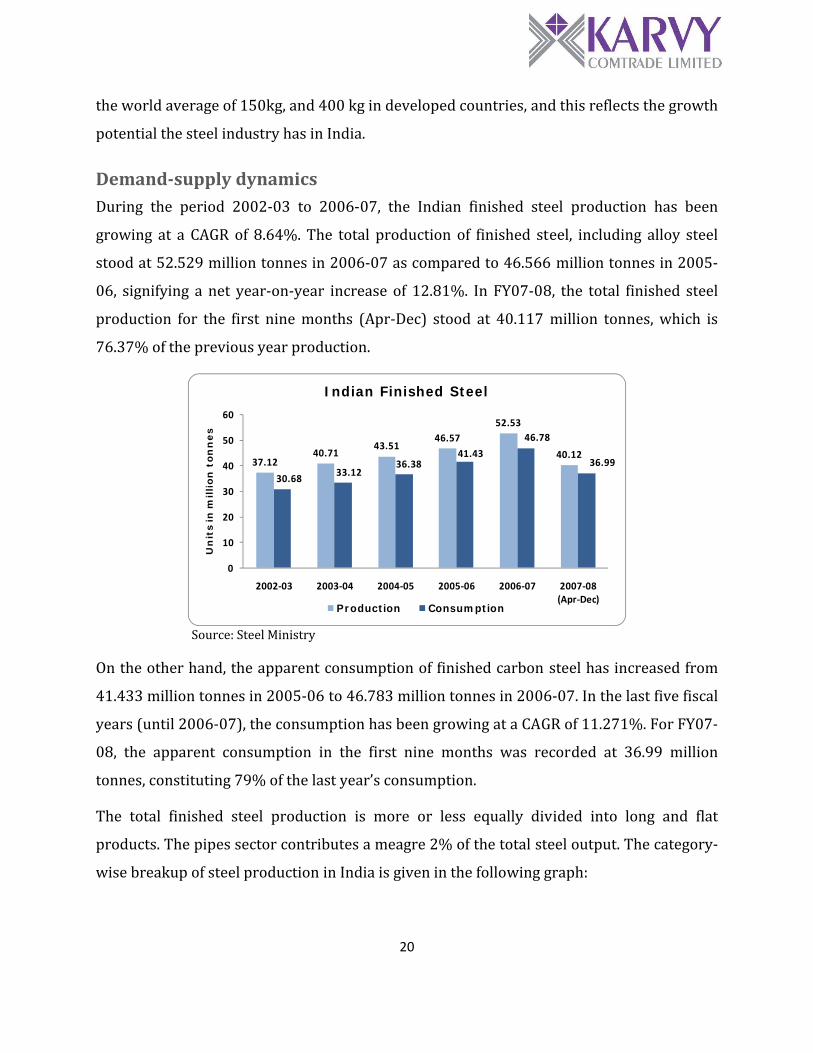

Demandsupply dynamics During the period 2002‐03 to 2006‐07, the Indian finished steel production has been

growing at a CAGR of 8.64%. The total production of finished steel, including alloy steel

stood at 52.529 million tonnes in 2006‐07 as compared to 46.566 million tonnes in 2005‐

06, signifying a net year‐on‐year increase of 12.81%. In FY07‐08, the total finished steel

production for the first nine months (Apr‐Dec) stood at 40.117 million tonnes, which is

76.37% of the previous year production.

37.1240.71

43.5146.57

52.53

40.12

30.6833.12

36.3841.43

46.78

36.99

0

10

20

30

40

50

60

2002‐03 2003‐04 2004‐05 2005‐06 2006‐07 2007‐08 (Apr‐Dec)

Un

its in

million

ton

nes

Indian Finished Steel

Production Consumption

Source: Steel Ministry

On the other hand, the apparent consumption of finished carbon steel has increased from

41.433 million tonnes in 2005‐06 to 46.783 million tonnes in 2006‐07. In the last five fiscal

years (until 2006‐07), the consumption has been growing at a CAGR of 11.271%. For FY07‐

08, the apparent consumption in the first nine months was recorded at 36.99 million

tonnes, constituting 79% of the last year’s consumption.

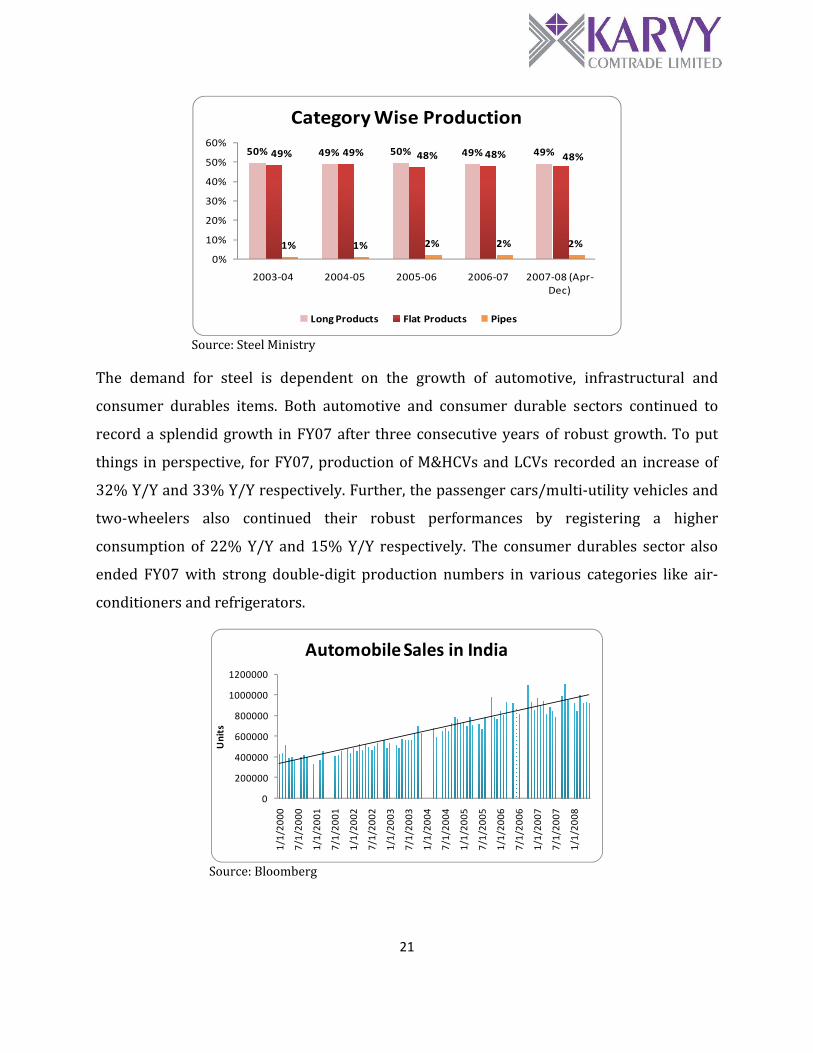

The total finished steel production is more or less equally divided into long and flat

products. The pipes sector contributes a meagre 2% of the total steel output. The category‐

wise breakup of steel production in India is given in the following graph:

21

50% 49% 50% 49% 49%49% 49% 48% 48% 48%

1% 1% 2% 2% 2%

0%

10%

20%

30%

40%

50%

60%

2003‐04 2004‐05 2005‐06 2006‐07 2007‐08 (Apr‐Dec)

Category Wise Production

Long Products Flat Products Pipes

Source: Steel Ministry

The demand for steel is dependent on the growth of automotive, infrastructural and

consumer durables items. Both automotive and consumer durable sectors continued to

record a splendid growth in FY07 after three consecutive years of robust growth. To put

things in perspective, for FY07, production of M&HCVs and LCVs recorded an increase of

32% Y/Y and 33% Y/Y respectively. Further, the passenger cars/multi‐utility vehicles and

two‐wheelers also continued their robust performances by registering a higher

consumption of 22% Y/Y and 15% Y/Y respectively. The consumer durables sector also

ended FY07 with strong double‐digit production numbers in various categories like air‐

conditioners and refrigerators.

0

200000

400000

600000

800000

1000000

1200000

1/1/20

00

7/1/20

00

1/1/20

01

7/1/20

01

1/1/20

02

7/1/20

02

1/1/20

03

7/1/20

03

1/1/20

04

7/1/20

04

1/1/20

05

7/1/20

05

1/1/20

06

7/1/20

06

1/1/20

07

7/1/20

07

1/1/20

08

Units

Automobile Sales in India

Source: Bloomberg

22

In FY07‐08, India has become a net importer of finished steel. In the first nine months (Apr‐

Dec) the imports and exports of finished steel were recorded at 5.32 tonnes and 3.85

million tonnes respectively. From 2002‐03 to 2006‐07, compounded annual growth rate in

steel imports stood at 35.94% and that of exports was at 2.19%.

1.663 1.753

2.293

4.305 4.927

5.3254.5175.207

4.705 4.801 5.242

3.85

0

1

2

3

4

5

6

2002‐03 2003‐04 2004‐05 2005‐06 2006‐07 2007‐08 (Apr‐Dec)

Un

its in

mil

lion t

on

nes

Import & Export - Finished Steel

Import Export

Source: Steel Ministry

Indian economy highlights

Gross domestic production continued to record a growth of 8.8% in the first quarter

of 2008.

Total automobile sales in H1 2008 stood at 5.5 million units compared to the last

year’s figure of 5.39 million units (a gain of 3.47%).

The core industry sector represented by the Finished Steel Production Index has

reported a growth of 5.20% in May (Y/Y). The index carries a weight of 5.13 in

India’s core infrastructure index.

At the same time, coal production index has shown an increase of 8.38% from the

previous year’s figures.

Index of Industrial Production (IIP) recorded a 3.84% growth in May 2008

compared to 10.59% growth in the same period last year.

Construction spending during the quarter ended March 2008 grew 12.6% against

the last year’s figure of 12.2%.

23

0

2

4

6

8

10

12

6/1/20

00

11/1/200

0

4/1/20

01

9/1/20

01

2/1/20

02

7/1/20

02

12/1/200

2

5/1/20

03

10/1/200

3

3/1/20

04

8/1/20

04

1/1/20

05

6/1/20

05

11/1/200

5

4/1/20

06

9/1/20

06

2/1/20

07

7/1/20

07

12/1/200

7

India's Real GDP Growth (%)

‐5

0

5

10

15

20

25

6/1/2000

11/1/2000

4/1/2001

9/1/2001

2/1/2002

7/1/2002

12/1/2002

5/1/2003

10/1/2003

3/1/2004

8/1/2004

1/1/2005

6/1/2005

11/1/2005

4/1/2006

9/1/2006

2/1/2007

7/1/2007

12/1/2007

Indian Construction Sector Growth

100

150

200

250

300

350

4/1/19

94

1/1/19

95

10/1/199

5

7/1/19

96

4/1/19

97

1/1/19

98

10/1/199

8

7/1/19

99

4/1/20

00

1/1/20

01

10/1/200

1

7/1/20

02

4/1/20

03

1/1/20

04

10/1/200

4

7/1/20

05

4/1/20

06

1/1/20

07

10/1/200

7

Industrial Production Index

0

1000

2000

3000

4000

5000

6000

4/1/19

99

10/1/199

9

4/1/20

00

10/1/200

0

4/1/20

01

10/1/200

1

4/1/20

02

10/1/200

2

4/1/20

03

10/1/200

3

4/1/20

04

10/1/200

4

4/1/20

05

10/1/200

5

4/1/20

06

10/1/200

6

4/1/20

07

10/1/200

7

4/1/20

08

Finished Steel Intrastructure Index

Source: Bloomberg

Fundamental outlook The steel industry plays an important role in the economic development of a country. India,

being the 5th largest steel producer in the world, has a share of around 4 percent in world

steel production of 1,344 million metric tonnes. Despite this, the per capita steel

consumption in India is one of the lowest, thus providing the domestic industry with a huge

potential to scale greater heights. The per capita steel consumption in India is around 35kg

as compared to the world average of 150kg, and 300kg and 400kg for China and the US,

respectively.

Strong infrastructure development and economic indicators reflects robust demand for

steel in India. During the 11th Plan (2007‐08 to 2011‐12), the projected investment

towards infrastructure is likely to be Rs20,27,000 crore, an increase of 180% over the 10th

Plan.

International iron ore prices have climbed by 100% and coking coal prices have almost

tripled this year. The effect of this has been observed in both global and domestic markets.

The Indian domestic steel ingot prices have jumped over 50% this year mainly attributed

24

to the spiralling prices of raw materials. The wholesale price index of iron and steel has

jumped by 29.92% this year (until week ended July 5) and inflation soared to a 13‐year

high of 11.91%.

A double‐digit inflation figure has been causing panic in the market as the government

continuously keeps taking measures to calm down prices. A number of fiscal steps have

been taken, such as exempting pig iron, non‐alloy steel, and steel‐making inputs like zinc,

ferro‐alloys and met coke from customs duty; withdrawing DEPB benefits on export of

various categories of steel products; and bringing back railway freight on iron ore from

classification 180 to 170 for domestic steel produce. Moreover, a 15% export duty on long

products and iron ore exports have been imposed and a commitment from primary steel

manufacturers have been taken to hold prices for a period of three months ending July. As a

result, steel producers had rolled back prices of flat products by Rs4,000 per tonne and

Rs2,000 per tonne for structural steel. Most recently, they also agreed to cut down the

prices for steel pipes by 10% after the government agreed to rollback the 15% export duty

on flat products.

However, even after implementing these steps, the government failed to control the prices

as dealers and retail sellers of steel continued to pass on the higher input costs to the final

consumer. An example of this is the rise in mild steel ingot prices which moved to

Rs.37,500 per tonne from its April month lowest level of Rs28,300 per tonne levels.

Following is the outline on trend in steel input costs in 2008 (until July):

Domestic sponge iron (ex‐Raipur) is exchanging hands at Rs28,705 per tonne,

signifying a net gain of 69.7%.

Currently, contract coking coal price is reigning at $300 per tonne, an increase of

200% from $98 per tonne in March and spot prices are hovering at $350 per tonne.

NMDC had raised iron ore prices by 47.5 % with retrospective effect from October 1,

2007. Currently, iron ore prices in the spot market are $110 per tonne FOB India.

China’s import prices (CFR) of Indian iron ore (63% iron content) has moved

slightly lower by 2.63% to US$185 per tonne levels.

25

Baosteel, China’s largest steel maker, have agreed for a hike of 79.88% and 95% on

their long‐term iron ore fines and lumps prices, respectively, thus clearly pointing

out the supply tightness in the iron ore market.

Benchmark Australian Newcastle spot thermal coal prices are quoting at US$181.30

per metric tonne, up 103% in 2008.

The Baltic Dry Index (BDI), which is the main indicator for commodity freight rates,

has averaged at 8556 levels in 1H 2008, up 61% compared to the figures in 1H

2007.

Baseload German Power has increased by 42% to over 88 euros per mega watt hour

(MWH).

The robust demand for steel in India followed with the rising input costs is likely to

pressurize the steel companies to pass on the additional costs to the consumers. This is the

likely scenario once the steel company’s voluntary commitment to hold prices ends in July.

Rising input costs is adversely impacting the operating margins of steel companies. Though

primary steel producers have better margins on account of larger capacities, it will be

difficult for secondary and smaller players to hold the prices. Meanwhile, Steel Authority of

India Limited (SAIL) issued a written advisory to its dealers and long‐term contract

customers and warned of punitive action in case of any violation of its stipulations. In its

advisory, SAIL has asked its MoU dealership customers to limit their retail margins to

within Rs1,200 a tonne over the price at which they have procured the products from it.

To add, following were the statements made by major steel giants:

SAIL Chairman, SK Roongta ‐ “We have been able to register growth because we

increased output of value‐added steel and improved efficiencies. But fixed costs are

increasing. We need to raise prices to maintain margins.''

Tata Steel Managing Director, B Muthuraman ‐ “There is every justification to increase

steel prices since the industry cannot go for capacity expansion at the current profit

margins.”

26

Tata Steel Managing Director, B Muthuraman ‐ “Domestic steel prices are Rs15, 000 to

Rs20, 000 lower than international prices.”

JSW Steel Director (Finance), Sheshagiri Rao ‐ "Price movements are a result of

movements in companies’ cost structure. We are surely going to review steel prices in

August. But we are yet to decide whether the price movement would be upwards or

downwards."

Bhushan Steel Director (Finance), Nitin Johri ‐ "If primary steel firms go ahead with a

price increase, we will also raise prices of our products as we will be under pressure with

mounting price of everything from crude oil to iron ore, coking coal and electricity,"

Steel Secretary, R.S. Pandey ‐ "As long as inflation is high, as long as steel's contribution to

inflation is high, the government will deliberate and find out what best could be done."

Considering all the factors, prices are likely to move higher in the medium to long

term (from end of Q3 08). In the near short term, there are chances of price

correction, in anticipation of the government taking a few measures to control the

spiralling prices. Reports show that the government is already considering imposing an

extra export duty on both long and flat products. It is also evaluating a decision of 20%

export duty on sponge iron (currently 15%). There is a speculation in the market that the

steel industry may face a price band, which, we think, will not happen so as to develop the

industry over a period of time.

27

Technical outlook Mild Steel Ingots prices are taking correction after witnessing a sharp rally which

catapulted prices from 17000 to 37500 levels. The RSI indicator is treading near the

overbought conditions in monthly charts, suggesting that prices may be due for a

correction. The decline in volumes during the recent rally and increasing volumes during

the current fall is giving support to the bearish view in the short term. Lower volumes

usually reflect weak market sentiment for the prevailing trend and the opposite is true for

strong market sentiment.

The daily chart is also looking weak as prices are moving lower after testing the trend

channel resistance at 37,500 levels and failing to breach the same. Prices find first major

support at 30,000 levels, which is the trend channel support. A close below the same may

take prices to 27,800 levels, which is previous swing low. These levels can be a good entry

point for long term buying for targets of 45,000.

Though the long term trend continues to be bullish, we expect prices to take good

correction before continuing the journey northwards.

28

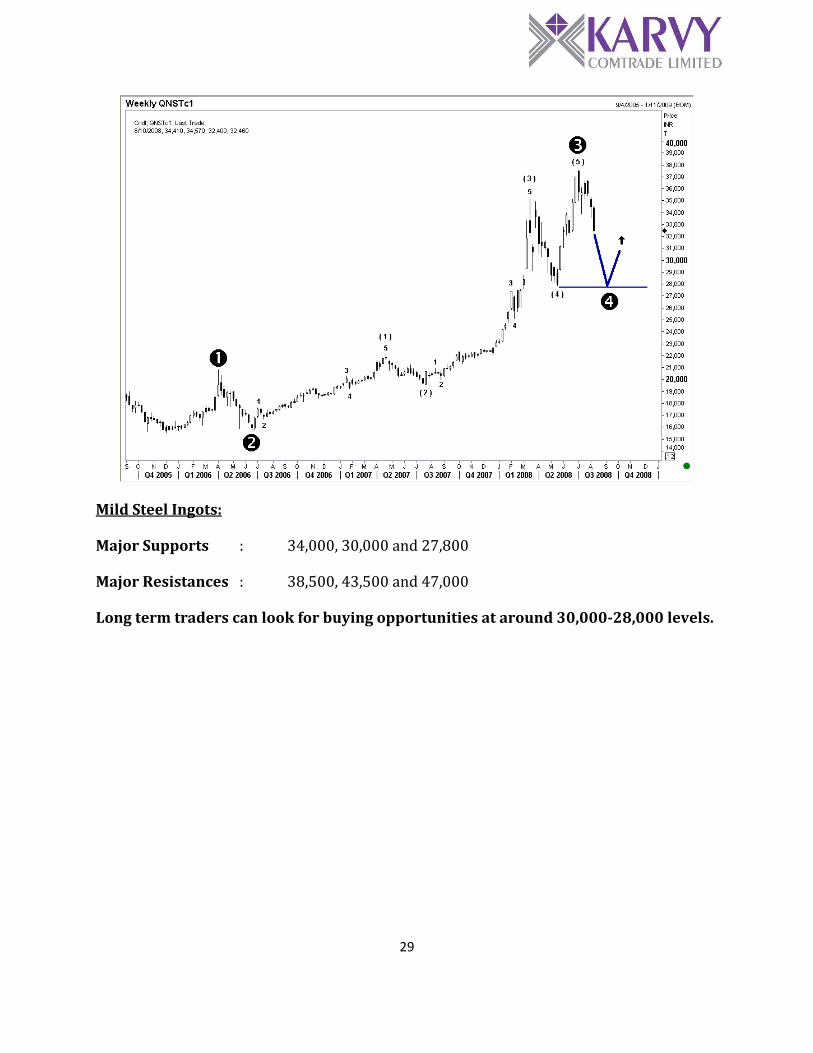

Elliot Wave Count

Primary Wave 3 – The primary wave 3 seems to have completed its move higher and we

feel that primary wave 4 is in formation. Generally the target for wave 4 of a greater degree

is considered to be the bottom made by wave 4 of immediately lesser degree. So in this case

the probable target for primary wave 4 can be the bottom made by intermediate wave 4 i.e.

27,800 levels. However this is only a guiding principle to assess the probable target, but not

a hard and fast rule.

29

Mild Steel Ingots:

Major Supports : 34,000, 30,000 and 27,800

Major Resistances : 38,500, 43,500 and 47,000

Long term traders can look for buying opportunities at around 30,00028,000 levels.

30

To unsubscribe please mail us at [email protected]

Disclaimer

The report contains the opinions of the author that are not to be construed as investment advice. The author, directors and other employees of Karvy, and its affiliates, cannot be held responsible for the accuracy of the information presented herein or for the results of the positions taken based on the opinions expressed above. The above‐mentioned opinions are based on the information which is believed to be accurate and no assurance can be given for the accuracy of this information. There is risk of loss in trading in derivatives. The author, directors and other employees of Karvy and its affiliates cannot be held responsible for any losses in trading.

Commodity derivatives trading involve substantial risk. The valuation of the underlying may fluctuate, and as a result, clients may lose their entire original investment. In no event should the content of this research report be construed as an express or an implied promise, guarantee or implication by, or from, Karvy Comtrade that you will profit or that losses can, or will be, limited in any manner whatsoever. Past results are no indication of future performance. The information provided in this report is intended solely for informative purposes and is obtained from sources believed to be reliable. Information is in no way guaranteed. No guarantee of any kind is implied or possible where projections of future conditions are attempted.

We do not offer any sort of portfolio advisory, portfolio management, or investment advisory services. The reports are only for information purposes and not to be construed as investment advice.

For a detailed disclaimer please go to following URLs:

http://www.karvycomtrade.com/disclaimer.asp

http://www.karvycomtrade.com/riskDisclaimer.asp