still bullish on smid energy, within e&p’s pulling off our

TRANSCRIPT

Lori Calvasina, Small/Mid Cap US Equity Strategist

212-538-6396/[email protected]

Sara Mahaffy, Associate Analyst

212-325-6824/[email protected]

Still Bullish On SMID Energy, Within E&P’s Pulling Off Our

Preference For Hybrids, Time For Oily & Gassy Names To

Take A Turn?

February 13th, 2013

Lauren Thompson, Research Analyst

212-325-1417/[email protected]

DISCLOSURE APPENDIX CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, INFORMATION ON TRADE ALERTS, ANALYST MODEL PORTFOLIOS AND THE STATUS OF NON-U.S ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/researchdisclosures or call +1 (877) 291-2683 US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION™

Client-Driven Solutions, Insights, and Access

Still Bullish On SMID Energy, Within E&P’s Pulling Off Our Preference For Hybrids, Time For Oily & Gassy Names To Take A Turn?

Updating Our Outlook For SMID E&P Groups: In this report we updated our analysis on the three SMID E&P baskets – “SMID Oily”, “SMID Hybrid” and “SMID Gassy” – that we began tracking in mid November. Names were classified with the help of CS Small/Mid Cap E&P analyst, Mark Lear, based on 2011 reserves data.

Our Bottom Line: We remain overweight Energy, and there are aspects we like about all three E&P groups, one the biggest weights within the sector. We no longer have a strong preference for SMID Hybrids as the group has run and valuations are no longer attractive. Our interest in the SMID Gassy group has picked up, at least in the short term, as investors have been more open to low quality/new ideas.

Hybrids Led in 2H12 & January, But Oily Names Leading In February: The SMID Hybrid group outperformed both the SMID Oily and SMID Gassy groups in the second half of last year. Outperformance continued into the first month of 2013, but the Hybrids have lagged both Oily & Gassy names in early Februrary.

No Longer Prefer SMID Hybrids, Valuations Have Run: We still can find several aspects that we like about this group. Beta is high and SMID investors dumped these names during 2Q12, but didn’t pile back into them in 3Q12 (though they may have started to during 4Q12/early 2013 when performance improved). The CS commodity team’s forecast for Oil is also constructive, and the performance of SMID Hybrid names has been closely correlated with WTI prices in the past. But we no longer have a preference for this group over the SMID Oily and Gassy baskets as valuations have run. This has been the best performing basket since mid-November, and valuations now look neutral on 2 of 4 metrics we track and expensive on the other 2. Earnings revisions trends also stalled last month, but we saw this happen across all three baskets. One of Mark Lear’s top picks (PDCE) is in this basket, plus four other Outperforms (ROSE, SFY, MHR and BCEI).

Intrigued By SMID Oily Valuations, But This Group Has Been Crowded: Valuations for SMID Oily names are now more attractive than what we’re seeing for SMID Hybrid names, with 3 out of 4 metrics below LT averages. This group has also had the strongest growth and trades closely with WTI prices. Crowding has been our main concern (several names are among the most popular in small cap funds across sectors, and crowded names have struggled to lead lately) and we would be selective within this group. Two of Mark Lear’s top ideas, GPOR and EXXI, are in the SMID Oily Basket.

SMID Gassy Names May Eventually Bounce From Interest In Lower Quality: We are getting more constructive on the SMID Gassy basket and think this group may benefit from its low quality bias in the short term as investors have become more open to the idea of moving into lower quality and are looking for new ideas. Valuations also remain deeply compelling, near historical lows. CS commodity analysts are worried about near term downside risks to US natural gas prices, which keeps us concerned. Mark Lear has Neutrals on three names in this group (REXX, CRK, PVA) and an Underperform rating on one name (FST). Note that most names on the Gassy list have been more lowly owned than Oily or Hybrid stocks in recent quarters.

2

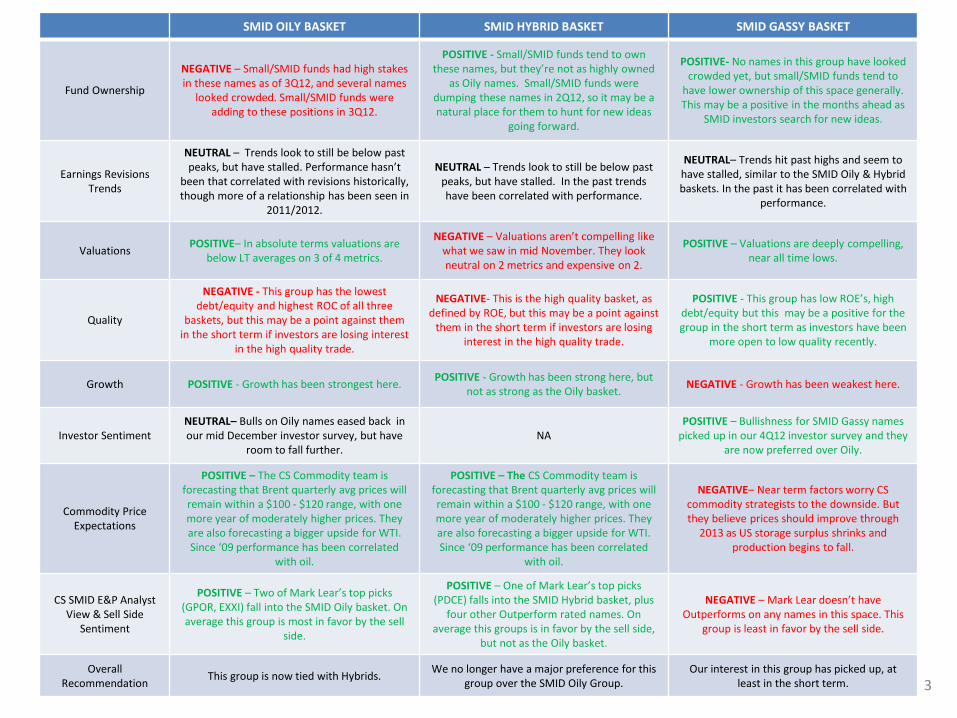

SMID OILY BASKET SMID HYBRID BASKET SMID GASSY BASKET

Fund Ownership

NEGATIVE – Small/SMID funds had high stakes in these names as of 3Q12, and several names

looked crowded. Small/SMID funds were adding to these positions in 3Q12.

POSITIVE - Small/SMID funds tend to own these names, but they’re not as highly owned

as Oily names. Small/SMID funds were dumping these names in 2Q12, so it may be a natural place for them to hunt for new ideas

going forward.

POSITIVE- No names in this group have looked crowded yet, but small/SMID funds tend to

have lower ownership of this space generally. This may be a positive in the months ahead as

SMID investors search for new ideas.

Earnings Revisions Trends

NEUTRAL – Trends look to still be below past peaks, but have stalled. Performance hasn’t

been that correlated with revisions historically, though more of a relationship has been seen in

2011/2012.

NEUTRAL – Trends look to still be below past peaks, but have stalled. In the past trends have been correlated with performance.

NEUTRAL– Trends hit past highs and seem to have stalled, similar to the SMID Oily & Hybrid baskets. In the past it has been correlated with

performance.

Valuations POSITIVE– In absolute terms valuations are

below LT averages on 3 of 4 metrics.

NEGATIVE – Valuations aren’t compelling like what we saw in mid November. They look neutral on 2 metrics and expensive on 2.

POSITIVE – Valuations are deeply compelling, near all time lows.

Quality

NEGATIVE - This group has the lowest debt/equity and highest ROC of all three

baskets, but this may be a point against them in the short term if investors are losing interest

in the high quality trade.

NEGATIVE- This is the high quality basket, as defined by ROE, but this may be a point against

them in the short term if investors are losing interest in the high quality trade.

POSITIVE - This group has low ROE’s, high debt/equity but this may be a positive for the group in the short term as investors have been

more open to low quality recently.

Growth POSITIVE - Growth has been strongest here. POSITIVE - Growth has been strong here, but

not as strong as the Oily basket. NEGATIVE - Growth has been weakest here.

Investor Sentiment NEUTRAL– Bulls on Oily names eased back in our mid December investor survey, but have

room to fall further. NA

POSITIVE – Bullishness for SMID Gassy names picked up in our 4Q12 investor survey and they

are now preferred over Oily.

Commodity Price Expectations

POSITIVE – The CS Commodity team is forecasting that Brent quarterly avg prices will remain within a $100 - $120 range, with one more year of moderately higher prices. They are also forecasting a bigger upside for WTI. Since ‘09 performance has been correlated

with oil.

POSITIVE – The CS Commodity team is forecasting that Brent quarterly avg prices will remain within a $100 - $120 range, with one more year of moderately higher prices. They are also forecasting a bigger upside for WTI. Since ‘09 performance has been correlated

with oil.

NEGATIVE– Near term factors worry CS commodity strategists to the downside. But they believe prices should improve through

2013 as US storage surplus shrinks and production begins to fall.

CS SMID E&P Analyst View & Sell Side

Sentiment

POSITIVE – Two of Mark Lear’s top picks (GPOR, EXXI) fall into the SMID Oily basket. On average this group is most in favor by the sell

side.

POSITIVE – One of Mark Lear’s top picks (PDCE) falls into the SMID Hybrid basket, plus

four other Outperform rated names. On average this groups is in favor by the sell side,

but not as the Oily basket.

NEGATIVE – Mark Lear doesn’t have Outperforms on any names in this space. This

group is least in favor by the sell side.

Overall Recommendation

This group is now tied with Hybrids. We no longer have a major preference for this

group over the SMID Oily Group. Our interest in this group has picked up, at

least in the short term. 3

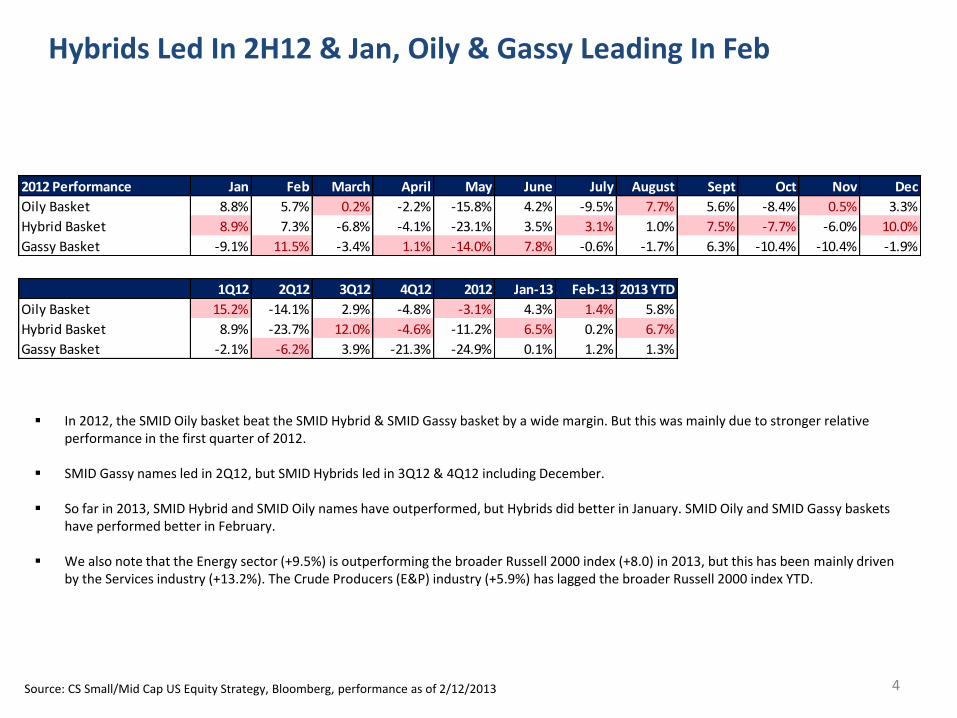

Hybrids Led In 2H12 & Jan, Oily & Gassy Leading In Feb

In 2012, the SMID Oily basket beat the SMID Hybrid & SMID Gassy basket by a wide margin. But this was mainly due to stronger relative performance in the first quarter of 2012.

SMID Gassy names led in 2Q12, but SMID Hybrids led in 3Q12 & 4Q12 including December.

So far in 2013, SMID Hybrid and SMID Oily names have outperformed, but Hybrids did better in January. SMID Oily and SMID Gassy baskets have performed better in February.

We also note that the Energy sector (+9.5%) is outperforming the broader Russell 2000 index (+8.0) in 2013, but this has been mainly driven by the Services industry (+13.2%). The Crude Producers (E&P) industry (+5.9%) has lagged the broader Russell 2000 index YTD.

2012 Performance Jan Feb March April May June July August Sept Oct Nov Dec

Oily Basket 8.8% 5.7% 0.2% -2.2% -15.8% 4.2% -9.5% 7.7% 5.6% -8.4% 0.5% 3.3%

Hybrid Basket 8.9% 7.3% -6.8% -4.1% -23.1% 3.5% 3.1% 1.0% 7.5% -7.7% -6.0% 10.0%

Gassy Basket -9.1% 11.5% -3.4% 1.1% -14.0% 7.8% -0.6% -1.7% 6.3% -10.4% -10.4% -1.9%

Source: CS Small/Mid Cap US Equity Strategy, Bloomberg, performance as of 2/12/2013

1Q12 2Q12 3Q12 4Q12 2012 Jan-13 Feb-13 2013 YTD

Oily Basket 15.2% -14.1% 2.9% -4.8% -3.1% 4.3% 1.4% 5.8%

Hybrid Basket 8.9% -23.7% 12.0% -4.6% -11.2% 6.5% 0.2% 6.7%

Gassy Basket -2.1% -6.2% 3.9% -21.3% -24.9% 0.1% 1.2% 1.3%

4

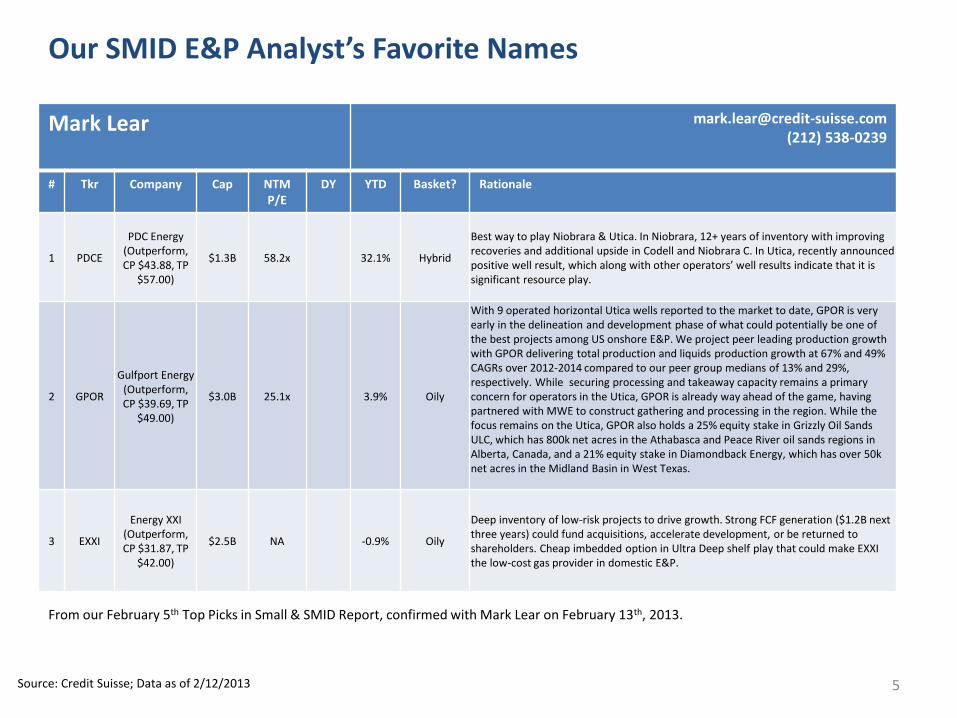

Our SMID E&P Analyst’s Favorite Names

Mark Lear [email protected] (212) 538-0239

# Tkr Company Cap NTM P/E

DY YTD Basket? Rationale

1 PDCE

PDC Energy (Outperform, CP $43.88, TP

$57.00)

$1.3B 58.2x 32.1% Hybrid

Best way to play Niobrara & Utica. In Niobrara, 12+ years of inventory with improving recoveries and additional upside in Codell and Niobrara C. In Utica, recently announced positive well result, which along with other operators’ well results indicate that it is significant resource play.

2 GPOR

Gulfport Energy (Outperform, CP $39.69, TP

$49.00)

$3.0B 25.1x 3.9% Oily

With 9 operated horizontal Utica wells reported to the market to date, GPOR is very early in the delineation and development phase of what could potentially be one of the best projects among US onshore E&P. We project peer leading production growth with GPOR delivering total production and liquids production growth at 67% and 49% CAGRs over 2012-2014 compared to our peer group medians of 13% and 29%, respectively. While securing processing and takeaway capacity remains a primary concern for operators in the Utica, GPOR is already way ahead of the game, having partnered with MWE to construct gathering and processing in the region. While the focus remains on the Utica, GPOR also holds a 25% equity stake in Grizzly Oil Sands ULC, which has 800k net acres in the Athabasca and Peace River oil sands regions in Alberta, Canada, and a 21% equity stake in Diamondback Energy, which has over 50k net acres in the Midland Basin in West Texas.

3 EXXI

Energy XXI (Outperform, CP $31.87, TP

$42.00)

$2.5B NA -0.9% Oily

Deep inventory of low-risk projects to drive growth. Strong FCF generation ($1.2B next three years) could fund acquisitions, accelerate development, or be returned to shareholders. Cheap imbedded option in Ultra Deep shelf play that could make EXXI the low-cost gas provider in domestic E&P.

Source: Credit Suisse; Data as of 2/12/2013

From our February 5th Top Picks in Small & SMID Report, confirmed with Mark Lear on February 13th, 2013.

5

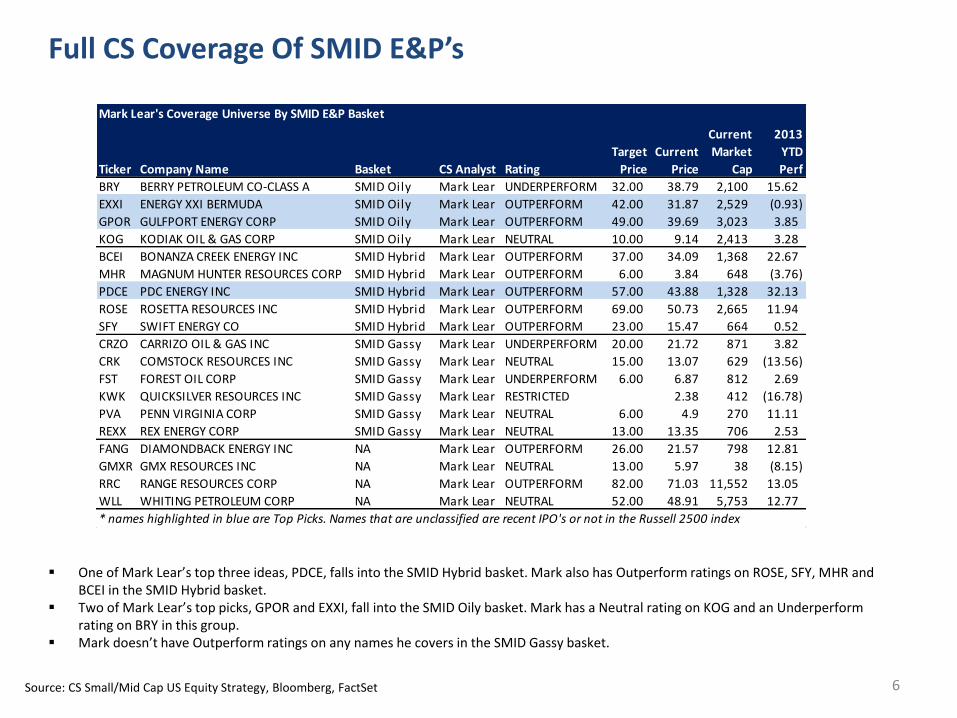

One of Mark Lear’s top three ideas, PDCE, falls into the SMID Hybrid basket. Mark also has Outperform ratings on ROSE, SFY, MHR and BCEI in the SMID Hybrid basket.

Two of Mark Lear’s top picks, GPOR and EXXI, fall into the SMID Oily basket. Mark has a Neutral rating on KOG and an Underperform rating on BRY in this group.

Mark doesn’t have Outperform ratings on any names he covers in the SMID Gassy basket.

Full CS Coverage Of SMID E&P’s

Source: CS Small/Mid Cap US Equity Strategy, Bloomberg, FactSet

Mark Lear's Coverage Universe By SMID E&P Basket

Ticker Company Name Basket CS Analyst Rating

Target

Price

Current

Price

Current

Market

Cap

2013

YTD

Perf

BRY BERRY PETROLEUM CO-CLASS A SMID Oily Mark Lear UNDERPERFORM 32.00 38.79 2,100 15.62

EXXI ENERGY XXI BERMUDA SMID Oily Mark Lear OUTPERFORM 42.00 31.87 2,529 (0.93)

GPOR GULFPORT ENERGY CORP SMID Oily Mark Lear OUTPERFORM 49.00 39.69 3,023 3.85

KOG KODIAK OIL & GAS CORP SMID Oily Mark Lear NEUTRAL 10.00 9.14 2,413 3.28

BCEI BONANZA CREEK ENERGY INC SMID Hybrid Mark Lear OUTPERFORM 37.00 34.09 1,368 22.67

MHR MAGNUM HUNTER RESOURCES CORP SMID Hybrid Mark Lear OUTPERFORM 6.00 3.84 648 (3.76)

PDCE PDC ENERGY INC SMID Hybrid Mark Lear OUTPERFORM 57.00 43.88 1,328 32.13

ROSE ROSETTA RESOURCES INC SMID Hybrid Mark Lear OUTPERFORM 69.00 50.73 2,665 11.94

SFY SWIFT ENERGY CO SMID Hybrid Mark Lear OUTPERFORM 23.00 15.47 664 0.52

CRZO CARRIZO OIL & GAS INC SMID Gassy Mark Lear UNDERPERFORM 20.00 21.72 871 3.82

CRK COMSTOCK RESOURCES INC SMID Gassy Mark Lear NEUTRAL 15.00 13.07 629 (13.56)

FST FOREST OIL CORP SMID Gassy Mark Lear UNDERPERFORM 6.00 6.87 812 2.69

KWK QUICKSILVER RESOURCES INC SMID Gassy Mark Lear RESTRICTED 2.38 412 (16.78)

PVA PENN VIRGINIA CORP SMID Gassy Mark Lear NEUTRAL 6.00 4.9 270 11.11

REXX REX ENERGY CORP SMID Gassy Mark Lear NEUTRAL 13.00 13.35 706 2.53

FANG DIAMONDBACK ENERGY INC NA Mark Lear OUTPERFORM 26.00 21.57 798 12.81

GMXR GMX RESOURCES INC NA Mark Lear NEUTRAL 13.00 5.97 38 (8.15)

RRC RANGE RESOURCES CORP NA Mark Lear OUTPERFORM 82.00 71.03 11,552 13.05

WLL WHITING PETROLEUM CORP NA Mark Lear NEUTRAL 52.00 48.91 5,753 12.77

* names highlighted in blue are Top Picks. Names that are unclassified are recent IPO's or not in the Russell 2500 index

6

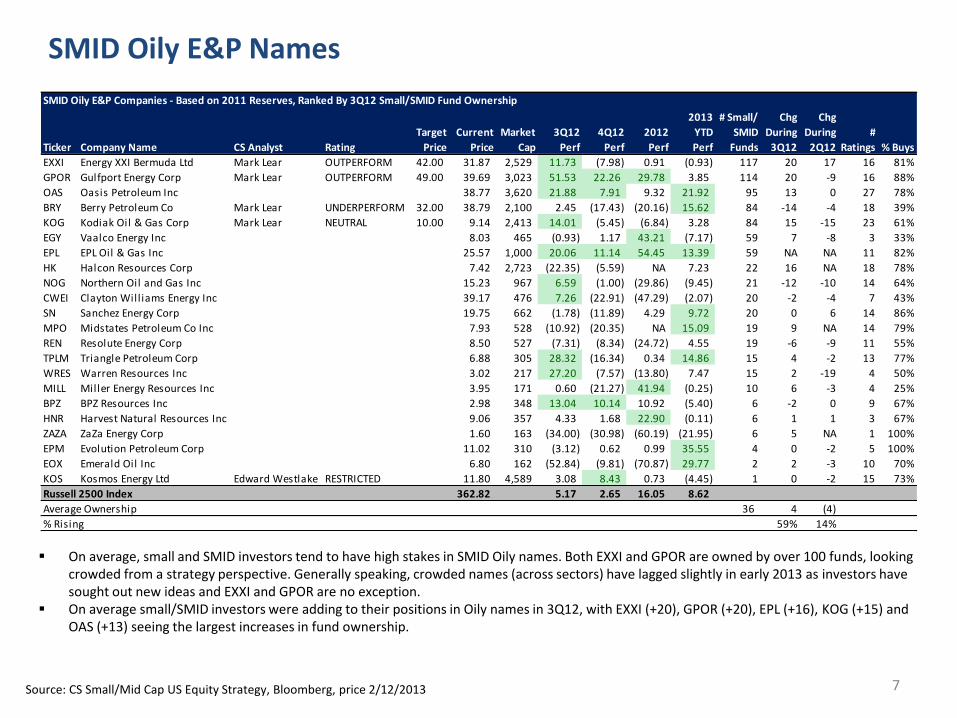

SMID Oily E&P Names

On average, small and SMID investors tend to have high stakes in SMID Oily names. Both EXXI and GPOR are owned by over 100 funds, looking crowded from a strategy perspective. Generally speaking, crowded names (across sectors) have lagged slightly in early 2013 as investors have sought out new ideas and EXXI and GPOR are no exception.

On average small/SMID investors were adding to their positions in Oily names in 3Q12, with EXXI (+20), GPOR (+20), EPL (+16), KOG (+15) and OAS (+13) seeing the largest increases in fund ownership.

Source: CS Small/Mid Cap US Equity Strategy, Bloomberg, price 2/12/2013

SMID Oily E&P Companies - Based on 2011 Reserves, Ranked By 3Q12 Small/SMID Fund Ownership

Ticker Company Name CS Analyst Rating

Target

Price

Current

Price

Market

Cap

3Q12

Perf

4Q12

Perf

2012

Perf

2013

YTD

Perf

# Small/

SMID

Funds

Chg

During

3Q12

Chg

During

2Q12

#

Ratings % Buys

EXXI Energy XXI Bermuda Ltd Mark Lear OUTPERFORM 42.00 31.87 2,529 11.73 (7.98) 0.91 (0.93) 117 20 17 16 81%

GPOR Gulfport Energy Corp Mark Lear OUTPERFORM 49.00 39.69 3,023 51.53 22.26 29.78 3.85 114 20 -9 16 88%

OAS Oasis Petroleum Inc #N/A #N/A #N/A 38.77 3,620 21.88 7.91 9.32 21.92 95 13 0 27 78%

BRY Berry Petroleum Co Mark Lear UNDERPERFORM 32.00 38.79 2,100 2.45 (17.43) (20.16) 15.62 84 -14 -4 18 39%

KOG Kodiak Oil & Gas Corp Mark Lear NEUTRAL 10.00 9.14 2,413 14.01 (5.45) (6.84) 3.28 84 15 -15 23 61%

EGY Vaalco Energy Inc #N/A #N/A #N/A 8.03 465 (0.93) 1.17 43.21 (7.17) 59 7 -8 3 33%

EPL EPL Oil & Gas Inc #N/A #N/A #N/A 25.57 1,000 20.06 11.14 54.45 13.39 59 NA NA 11 82%

HK Halcon Resources Corp #N/A #N/A #N/A 7.42 2,723 (22.35) (5.59) NA 7.23 22 16 NA 18 78%

NOG Northern Oil and Gas Inc #N/A #N/A #N/A 15.23 967 6.59 (1.00) (29.86) (9.45) 21 -12 -10 14 64%

CWEI Clayton Williams Energy Inc #N/A #N/A #N/A 39.17 476 7.26 (22.91) (47.29) (2.07) 20 -2 -4 7 43%

SN Sanchez Energy Corp #N/A #N/A #N/A 19.75 662 (1.78) (11.89) 4.29 9.72 20 0 6 14 86%

MPO Midstates Petroleum Co Inc #N/A #N/A #N/A 7.93 528 (10.92) (20.35) NA 15.09 19 9 NA 14 79%

REN Resolute Energy Corp #N/A #N/A #N/A 8.50 527 (7.31) (8.34) (24.72) 4.55 19 -6 -9 11 55%

TPLM Triangle Petroleum Corp #N/A #N/A #N/A 6.88 305 28.32 (16.34) 0.34 14.86 15 4 -2 13 77%

WRES Warren Resources Inc #N/A #N/A #N/A 3.02 217 27.20 (7.57) (13.80) 7.47 15 2 -19 4 50%

MILL Miller Energy Resources Inc #N/A #N/A #N/A 3.95 171 0.60 (21.27) 41.94 (0.25) 10 6 -3 4 25%

BPZ BPZ Resources Inc #N/A #N/A #N/A 2.98 348 13.04 10.14 10.92 (5.40) 6 -2 0 9 67%

HNR Harvest Natural Resources Inc #N/A #N/A #N/A 9.06 357 4.33 1.68 22.90 (0.11) 6 1 1 3 67%

ZAZA ZaZa Energy Corp #N/A #N/A #N/A 1.60 163 (34.00) (30.98) (60.19) (21.95) 6 5 NA 1 100%

EPM Evolution Petroleum Corp #N/A #N/A #N/A 11.02 310 (3.12) 0.62 0.99 35.55 4 0 -2 5 100%

EOX Emerald Oil Inc #N/A #N/A #N/A 6.80 162 (52.84) (9.81) (70.87) 29.77 2 2 -3 10 70%

KOS Kosmos Energy Ltd Edward Westlake RESTRICTED 11.80 4,589 3.08 8.43 0.73 (4.45) 1 0 -2 15 73%

Russell 2500 Index 362.82 5.17 2.65 16.05 8.62

Average Ownership 36 4 (4)

% Rising 59% 14%

7

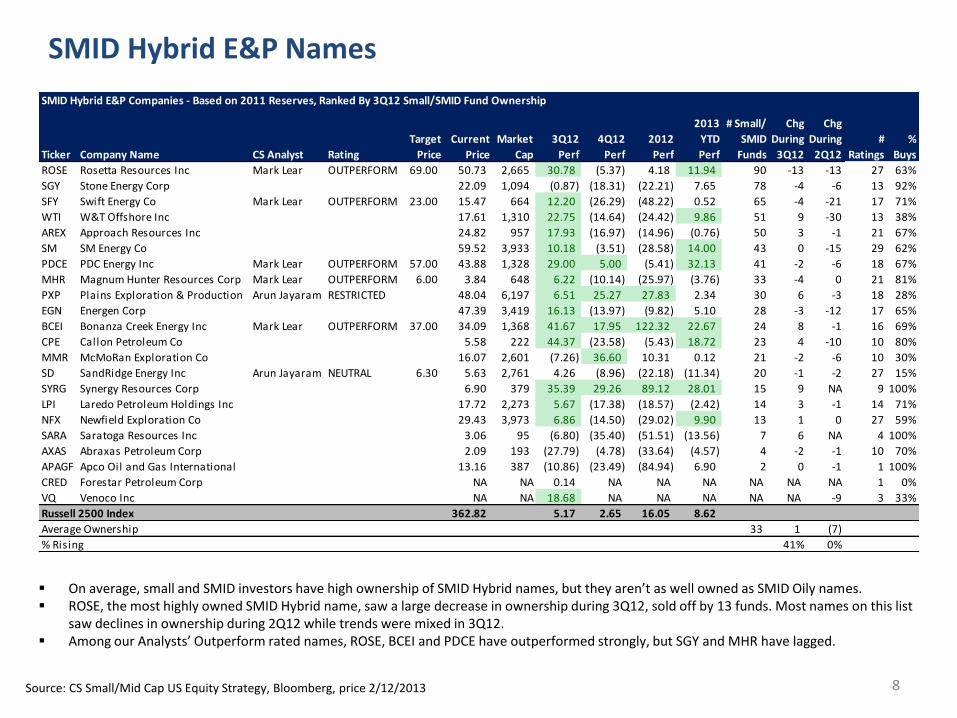

SMID Hybrid E&P Names

On average, small and SMID investors have high ownership of SMID Hybrid names, but they aren’t as well owned as SMID Oily names. ROSE, the most highly owned SMID Hybrid name, saw a large decrease in ownership during 3Q12, sold off by 13 funds. Most names on this list

saw declines in ownership during 2Q12 while trends were mixed in 3Q12. Among our Analysts’ Outperform rated names, ROSE, BCEI and PDCE have outperformed strongly, but SGY and MHR have lagged.

Source: CS Small/Mid Cap US Equity Strategy, Bloomberg, price 2/12/2013

SMID Hybrid E&P Companies - Based on 2011 Reserves, Ranked By 3Q12 Small/SMID Fund Ownership

Ticker Company Name CS Analyst Rating

Target

Price

Current

Price

Market

Cap

3Q12

Perf

4Q12

Perf

2012

Perf

2013

YTD

Perf

# Small/

SMID

Funds

Chg

During

3Q12

Chg

During

2Q12

#

Ratings

%

Buys

ROSE Rosetta Resources Inc Mark Lear OUTPERFORM 69.00 50.73 2,665 30.78 (5.37) 4.18 11.94 90 -13 -13 27 63%

SGY Stone Energy Corp #N/A #N/A #N/A 22.09 1,094 (0.87) (18.31) (22.21) 7.65 78 -4 -6 13 92%

SFY Swift Energy Co Mark Lear OUTPERFORM 23.00 15.47 664 12.20 (26.29) (48.22) 0.52 65 -4 -21 17 71%

WTI W&T Offshore Inc #N/A #N/A #N/A 17.61 1,310 22.75 (14.64) (24.42) 9.86 51 9 -30 13 38%

AREX Approach Resources Inc #N/A #N/A #N/A 24.82 957 17.93 (16.97) (14.96) (0.76) 50 3 -1 21 67%

SM SM Energy Co #N/A #N/A #N/A 59.52 3,933 10.18 (3.51) (28.58) 14.00 43 0 -15 29 62%

PDCE PDC Energy Inc Mark Lear OUTPERFORM 57.00 43.88 1,328 29.00 5.00 (5.41) 32.13 41 -2 -6 18 67%

MHR Magnum Hunter Resources Corp Mark Lear OUTPERFORM 6.00 3.84 648 6.22 (10.14) (25.97) (3.76) 33 -4 0 21 81%

PXP Plains Exploration & Production Arun Jayaram RESTRICTED 48.04 6,197 6.51 25.27 27.83 2.34 30 6 -3 18 28%

EGN Energen Corp #N/A #N/A #N/A 47.39 3,419 16.13 (13.97) (9.82) 5.10 28 -3 -12 17 65%

BCEI Bonanza Creek Energy Inc Mark Lear OUTPERFORM 37.00 34.09 1,368 41.67 17.95 122.32 22.67 24 8 -1 16 69%

CPE Callon Petroleum Co #N/A #N/A #N/A 5.58 222 44.37 (23.58) (5.43) 18.72 23 4 -10 10 80%

MMR McMoRan Exploration Co #N/A #N/A #N/A 16.07 2,601 (7.26) 36.60 10.31 0.12 21 -2 -6 10 30%

SD SandRidge Energy Inc Arun Jayaram NEUTRAL 6.30 5.63 2,761 4.26 (8.96) (22.18) (11.34) 20 -1 -2 27 15%

SYRG Synergy Resources Corp #N/A #N/A #N/A 6.90 379 35.39 29.26 89.12 28.01 15 9 NA 9 100%

LPI Laredo Petroleum Holdings Inc #N/A #N/A #N/A 17.72 2,273 5.67 (17.38) (18.57) (2.42) 14 3 -1 14 71%

NFX Newfield Exploration Co #N/A #N/A #N/A 29.43 3,973 6.86 (14.50) (29.02) 9.90 13 1 0 27 59%

SARA Saratoga Resources Inc #N/A #N/A #N/A 3.06 95 (6.80) (35.40) (51.51) (13.56) 7 6 NA 4 100%

AXAS Abraxas Petroleum Corp #N/A #N/A #N/A 2.09 193 (27.79) (4.78) (33.64) (4.57) 4 -2 -1 10 70%

APAGF Apco Oil and Gas International #N/A #N/A #N/A 13.16 387 (10.86) (23.49) (84.94) 6.90 2 0 -1 1 100%

CRED Forestar Petroleum Corp #N/A #N/A #N/A NA NA 0.14 NA NA NA NA NA NA 1 0%

VQ Venoco Inc #N/A #N/A #N/A NA NA 18.68 NA NA NA NA NA -9 3 33%

Russell 2500 Index 362.82 5.17 2.65 16.05 8.62

Average Ownership 33 1 (7)

% Rising 41% 0%

8

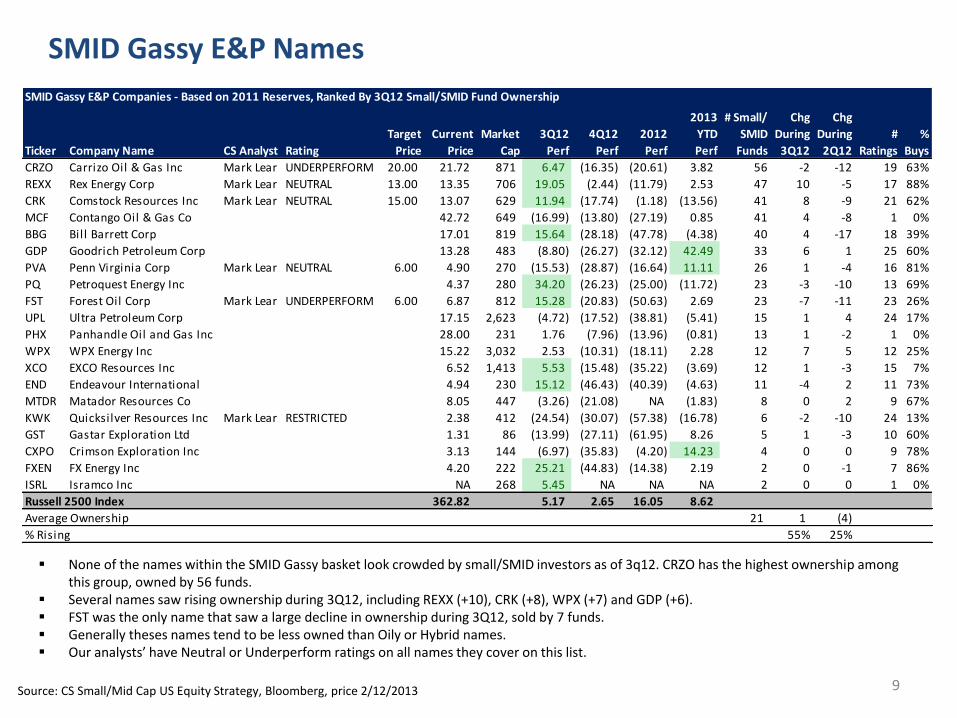

None of the names within the SMID Gassy basket look crowded by small/SMID investors as of 3q12. CRZO has the highest ownership among this group, owned by 56 funds.

Several names saw rising ownership during 3Q12, including REXX (+10), CRK (+8), WPX (+7) and GDP (+6). FST was the only name that saw a large decline in ownership during 3Q12, sold by 7 funds. Generally theses names tend to be less owned than Oily or Hybrid names. Our analysts’ have Neutral or Underperform ratings on all names they cover on this list.

SMID Gassy E&P Names

Source: CS Small/Mid Cap US Equity Strategy, Bloomberg, price 2/12/2013

SMID Gassy E&P Companies - Based on 2011 Reserves, Ranked By 3Q12 Small/SMID Fund Ownership

Ticker Company Name CS Analyst Rating

Target

Price

Current

Price

Market

Cap

3Q12

Perf

4Q12

Perf

2012

Perf

2013

YTD

Perf

# Small/

SMID

Funds

Chg

During

3Q12

Chg

During

2Q12

#

Ratings

%

Buys

CRZO Carrizo Oil & Gas Inc Mark Lear UNDERPERFORM 20.00 21.72 871 6.47 (16.35) (20.61) 3.82 56 -2 -12 19 63%

REXX Rex Energy Corp Mark Lear NEUTRAL 13.00 13.35 706 19.05 (2.44) (11.79) 2.53 47 10 -5 17 88%

CRK Comstock Resources Inc Mark Lear NEUTRAL 15.00 13.07 629 11.94 (17.74) (1.18) (13.56) 41 8 -9 21 62%

MCF Contango Oil & Gas Co #N/A #N/A #N/A 42.72 649 (16.99) (13.80) (27.19) 0.85 41 4 -8 1 0%

BBG Bill Barrett Corp #N/A #N/A #N/A 17.01 819 15.64 (28.18) (47.78) (4.38) 40 4 -17 18 39%

GDP Goodrich Petroleum Corp #N/A #N/A #N/A 13.28 483 (8.80) (26.27) (32.12) 42.49 33 6 1 25 60%

PVA Penn Virginia Corp Mark Lear NEUTRAL 6.00 4.90 270 (15.53) (28.87) (16.64) 11.11 26 1 -4 16 81%

PQ Petroquest Energy Inc #N/A #N/A #N/A 4.37 280 34.20 (26.23) (25.00) (11.72) 23 -3 -10 13 69%

FST Forest Oil Corp Mark Lear UNDERPERFORM 6.00 6.87 812 15.28 (20.83) (50.63) 2.69 23 -7 -11 23 26%

UPL Ultra Petroleum Corp #N/A #N/A #N/A 17.15 2,623 (4.72) (17.52) (38.81) (5.41) 15 1 4 24 17%

PHX Panhandle Oil and Gas Inc #N/A #N/A #N/A 28.00 231 1.76 (7.96) (13.96) (0.81) 13 1 -2 1 0%

WPX WPX Energy Inc #N/A #N/A #N/A 15.22 3,032 2.53 (10.31) (18.11) 2.28 12 7 5 12 25%

XCO EXCO Resources Inc #N/A #N/A #N/A 6.52 1,413 5.53 (15.48) (35.22) (3.69) 12 1 -3 15 7%

END Endeavour International #N/A #N/A #N/A 4.94 230 15.12 (46.43) (40.39) (4.63) 11 -4 2 11 73%

MTDR Matador Resources Co #N/A #N/A #N/A 8.05 447 (3.26) (21.08) NA (1.83) 8 0 2 9 67%

KWK Quicksilver Resources Inc Mark Lear RESTRICTED 2.38 412 (24.54) (30.07) (57.38) (16.78) 6 -2 -10 24 13%

GST Gastar Exploration Ltd #N/A #N/A #N/A 1.31 86 (13.99) (27.11) (61.95) 8.26 5 1 -3 10 60%

CXPO Crimson Exploration Inc #N/A #N/A #N/A 3.13 144 (6.97) (35.83) (4.20) 14.23 4 0 0 9 78%

FXEN FX Energy Inc #N/A #N/A #N/A 4.20 222 25.21 (44.83) (14.38) 2.19 2 0 -1 7 86%

ISRL Isramco Inc #N/A #N/A #N/A NA 268 5.45 NA NA NA 2 0 0 1 0%

Russell 2500 Index 362.82 5.17 2.65 16.05 8.62

Average Ownership 21 1 (4)

% Rising 55% 25%

9

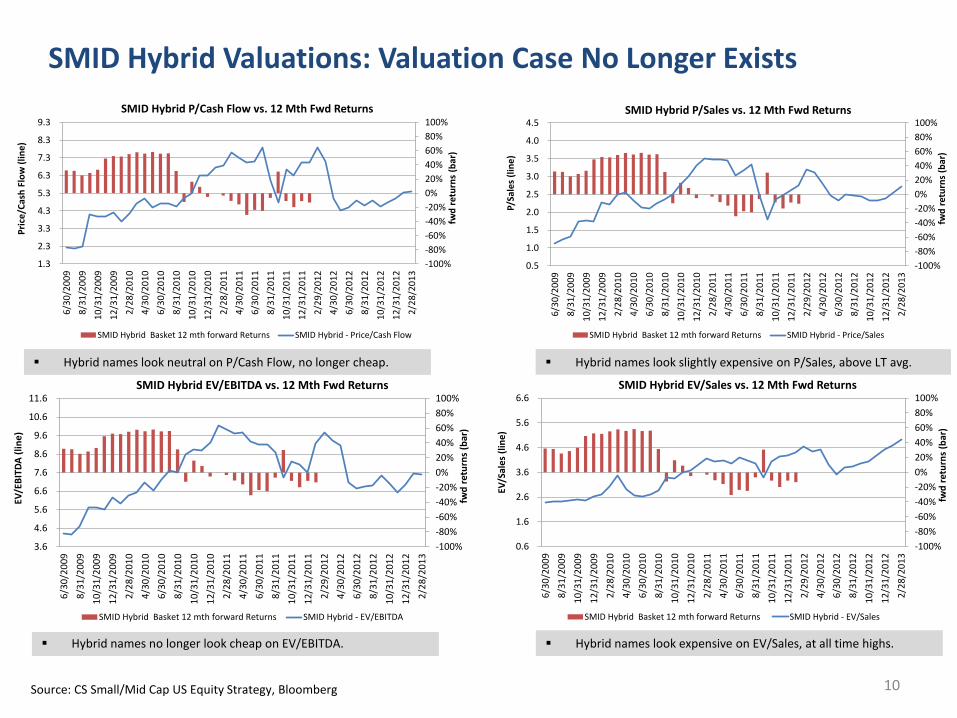

Hybrid names look neutral on P/Cash Flow, no longer cheap. Hybrid names look slightly expensive on P/Sales, above LT avg.

Hybrid names no longer look cheap on EV/EBITDA. Hybrid names look expensive on EV/Sales, at all time highs.

SMID Hybrid Valuations: Valuation Case No Longer Exists

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

1.3

2.3

3.3

4.3

5.3

6.3

7.3

8.3

9.3

6/3

0/2

00

9

8/3

1/2

00

9

10

/31

/20

09

12

/31

/20

09

2/2

8/2

01

0

4/3

0/2

01

0

6/3

0/2

01

0

8/3

1/2

01

0

10

/31

/20

10

12

/31

/20

10

2/2

8/2

01

1

4/3

0/2

01

1

6/3

0/2

01

1

8/3

1/2

01

1

10

/31

/20

11

12

/31

/20

11

2/2

9/2

01

2

4/3

0/2

01

2

6/3

0/2

01

2

8/3

1/2

01

2

10

/31

/20

12

12

/31

/20

12

2/2

8/2

01

3

fwd

ret

urn

s (b

ar)

Pri

ce/C

ash

Flo

w (

lin

e)

SMID Hybrid P/Cash Flow vs. 12 Mth Fwd Returns

SMID Hybrid Basket 12 mth forward Returns SMID Hybrid - Price/Cash Flow

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

6/3

0/2

00

9

8/3

1/2

00

9

10

/31

/20

09

12

/31

/20

09

2/2

8/2

01

0

4/3

0/2

01

0

6/3

0/2

01

0

8/3

1/2

01

0

10

/31

/20

10

12

/31

/20

10

2/2

8/2

01

1

4/3

0/2

01

1

6/3

0/2

01

1

8/3

1/2

01

1

10

/31

/20

11

12

/31

/20

11

2/2

9/2

01

2

4/3

0/2

01

2

6/3

0/2

01

2

8/3

1/2

01

2

10

/31

/20

12

12

/31

/20

12

2/2

8/2

01

3

fwd

ret

urn

s (b

ar)

P/Sa

les

(lin

e)

SMID Hybrid P/Sales vs. 12 Mth Fwd Returns

SMID Hybrid Basket 12 mth forward Returns SMID Hybrid - Price/Sales

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

3.6

4.6

5.6

6.6

7.6

8.6

9.6

10.6

11.6

6/3

0/2

00

9

8/3

1/2

00

9

10

/31

/20

09

12

/31

/20

09

2/2

8/2

01

0

4/3

0/2

01

0

6/3

0/2

01

0

8/3

1/2

01

0

10

/31

/20

10

12

/31

/20

10

2/2

8/2

01

1

4/3

0/2

01

1

6/3

0/2

01

1

8/3

1/2

01

1

10

/31

/20

11

12

/31

/20

11

2/2

9/2

01

2

4/3

0/2

01

2

6/3

0/2

01

2

8/3

1/2

01

2

10

/31

/20

12

12

/31

/20

12

2/2

8/2

01

3

fwd

ret

urn

s (b

ar)

EV/E

BIT

DA

(li

ne

)

SMID Hybrid EV/EBITDA vs. 12 Mth Fwd Returns

SMID Hybrid Basket 12 mth forward Returns SMID Hybrid - EV/EBITDA

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

0.6

1.6

2.6

3.6

4.6

5.6

6.6

6/3

0/2

00

9

8/3

1/2

00

9

10

/31

/20

09

12

/31

/20

09

2/2

8/2

01

0

4/3

0/2

01

0

6/3

0/2

01

0

8/3

1/2

01

0

10

/31

/20

10

12

/31

/20

10

2/2

8/2

01

1

4/3

0/2

01

1

6/3

0/2

01

1

8/3

1/2

01

1

10

/31

/20

11

12

/31

/20

11

2/2

9/2

01

2

4/3

0/2

01

2

6/3

0/2

01

2

8/3

1/2

01

2

10

/31

/20

12

12

/31

/20

12

2/2

8/2

01

3

fwd

ret

urn

s (b

ar)

EV/S

ales

(li

ne

)

SMID Hybrid EV/Sales vs. 12 Mth Fwd Returns

SMID Hybrid Basket 12 mth forward Returns SMID Hybrid - EV/Sales

Source: CS Small/Mid Cap US Equity Strategy, Bloomberg 10

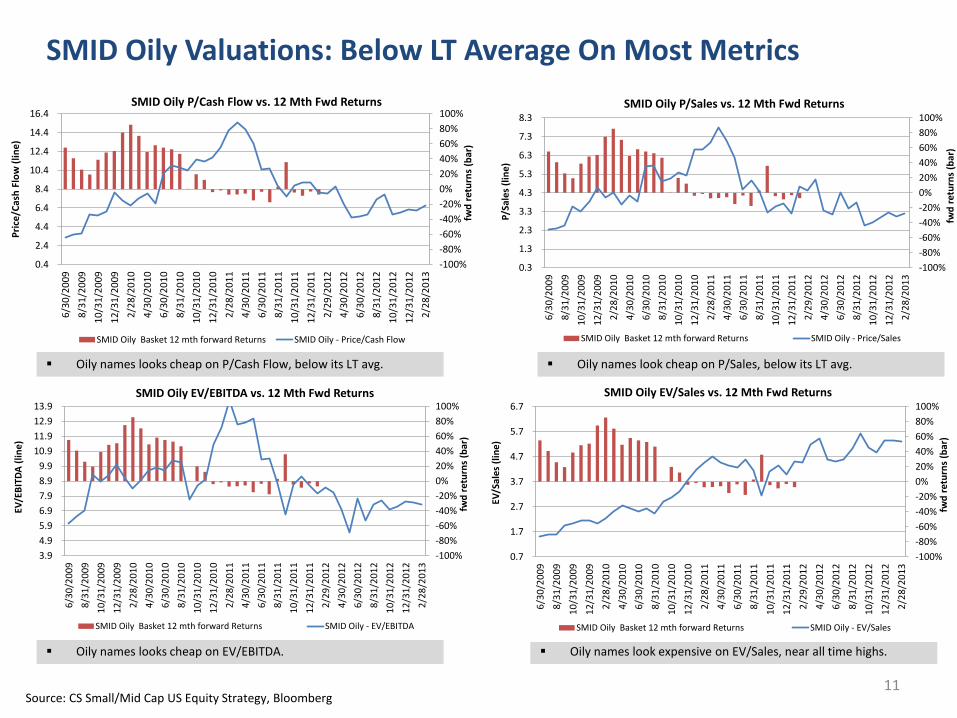

Oily names looks cheap on P/Cash Flow, below its LT avg. Oily names look cheap on P/Sales, below its LT avg.

Oily names looks cheap on EV/EBITDA. Oily names look expensive on EV/Sales, near all time highs.

SMID Oily Valuations: Below LT Average On Most Metrics

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

0.4

2.4

4.4

6.4

8.4

10.4

12.4

14.4

16.4

6/3

0/2

00

9

8/3

1/2

00

9

10

/31

/20

09

12

/31

/20

09

2/2

8/2

01

0

4/3

0/2

01

0

6/3

0/2

01

0

8/3

1/2

01

0

10

/31

/20

10

12

/31

/20

10

2/2

8/2

01

1

4/3

0/2

01

1

6/3

0/2

01

1

8/3

1/2

01

1

10

/31

/20

11

12

/31

/20

11

2/2

9/2

01

2

4/3

0/2

01

2

6/3

0/2

01

2

8/3

1/2

01

2

10

/31

/20

12

12

/31

/20

12

2/2

8/2

01

3

fwd

ret

urn

s (b

ar)

Pri

ce/C

ash

Flo

w (

lin

e)

SMID Oily P/Cash Flow vs. 12 Mth Fwd Returns

SMID Oily Basket 12 mth forward Returns SMID Oily - Price/Cash Flow

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

0.3

1.3

2.3

3.3

4.3

5.3

6.3

7.3

8.3

6/3

0/2

00

9

8/3

1/2

00

9

10

/31

/20

09

12

/31

/20

09

2/2

8/2

01

0

4/3

0/2

01

0

6/3

0/2

01

0

8/3

1/2

01

0

10

/31

/20

10

12

/31

/20

10

2/2

8/2

01

1

4/3

0/2

01

1

6/3

0/2

01

1

8/3

1/2

01

1

10

/31

/20

11

12

/31

/20

11

2/2

9/2

01

2

4/3

0/2

01

2

6/3

0/2

01

2

8/3

1/2

01

2

10

/31

/20

12

12

/31

/20

12

2/2

8/2

01

3

fwd

ret

urn

s (b

ar)

P/Sa

les

(lin

e)

SMID Oily P/Sales vs. 12 Mth Fwd Returns

SMID Oily Basket 12 mth forward Returns SMID Oily - Price/Sales

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

3.9

4.9

5.9

6.9

7.9

8.9

9.9

10.9

11.9

12.9

13.9

6/3

0/2

00

9

8/3

1/2

00

9

10

/31

/20

09

12

/31

/20

09

2/2

8/2

01

0

4/3

0/2

01

0

6/3

0/2

01

0

8/3

1/2

01

0

10

/31

/20

10

12

/31

/20

10

2/2

8/2

01

1

4/3

0/2

01

1

6/3

0/2

01

1

8/3

1/2

01

1

10

/31

/20

11

12

/31

/20

11

2/2

9/2

01

2

4/3

0/2

01

2

6/3

0/2

01

2

8/3

1/2

01

2

10

/31

/20

12

12

/31

/20

12

2/2

8/2

01

3

fwd

ret

urn

s (b

ar)

EV/E

BIT

DA

(li

ne

)

SMID Oily EV/EBITDA vs. 12 Mth Fwd Returns

SMID Oily Basket 12 mth forward Returns SMID Oily - EV/EBITDA

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

0.7

1.7

2.7

3.7

4.7

5.7

6.7

6/3

0/2

00

9

8/3

1/2

00

9

10

/31

/20

09

12

/31

/20

09

2/2

8/2

01

0

4/3

0/2

01

0

6/3

0/2

01

0

8/3

1/2

01

0

10

/31

/20

10

12

/31

/20

10

2/2

8/2

01

1

4/3

0/2

01

1

6/3

0/2

01

1

8/3

1/2

01

1

10

/31

/20

11

12

/31

/20

11

2/2

9/2

01

2

4/3

0/2

01

2

6/3

0/2

01

2

8/3

1/2

01

2

10

/31

/20

12

12

/31

/20

12

2/2

8/2

01

3

fwd

ret

urn

s (b

ar)

EV/S

ale

s (l

ine

)

SMID Oily EV/Sales vs. 12 Mth Fwd Returns

SMID Oily Basket 12 mth forward Returns SMID Oily - EV/Sales

Source: CS Small/Mid Cap US Equity Strategy, Bloomberg 11

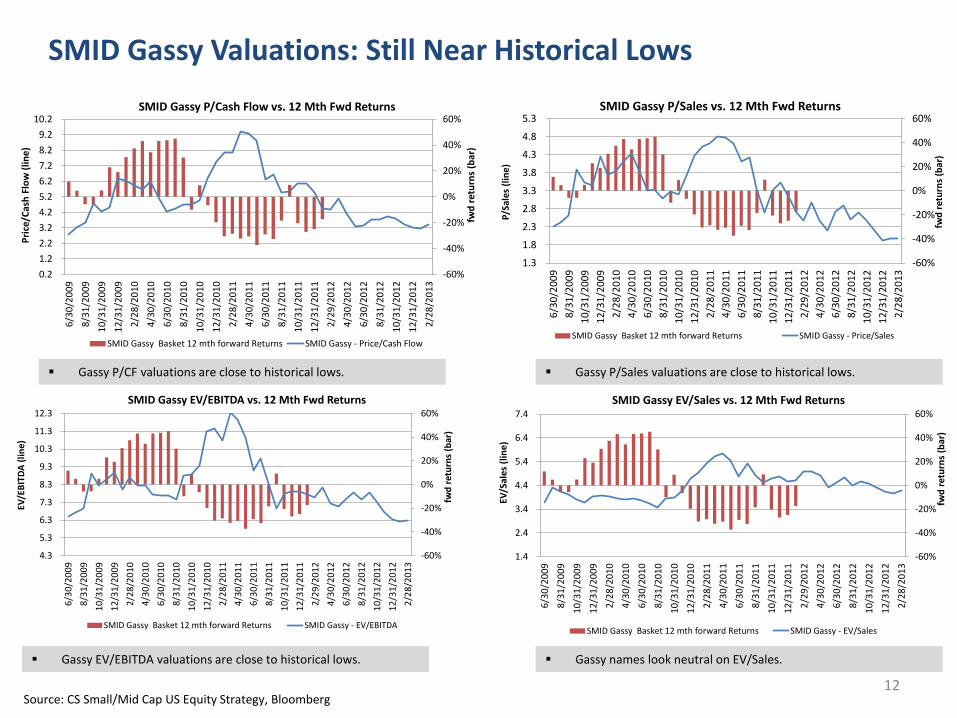

Gassy P/CF valuations are close to historical lows. Gassy P/Sales valuations are close to historical lows.

Gassy EV/EBITDA valuations are close to historical lows. Gassy names look neutral on EV/Sales.

SMID Gassy Valuations: Still Near Historical Lows

-60%

-40%

-20%

0%

20%

40%

60%

0.2

1.2

2.2

3.2

4.2

5.2

6.2

7.2

8.2

9.2

10.2

6/3

0/2

00

9

8/3

1/2

00

9

10

/31

/20

09

12

/31

/20

09

2/2

8/2

01

0

4/3

0/2

01

0

6/3

0/2

01

0

8/3

1/2

01

0

10

/31

/20

10

12

/31

/20

10

2/2

8/2

01

1

4/3

0/2

01

1

6/3

0/2

01

1

8/3

1/2

01

1

10

/31

/20

11

12

/31

/20

11

2/2

9/2

01

2

4/3

0/2

01

2

6/3

0/2

01

2

8/3

1/2

01

2

10

/31

/20

12

12

/31

/20

12

2/2

8/2

01

3

fwd

ret

urn

s (b

ar)

Pri

ce/C

ash

Flo

w (

lin

e)

SMID Gassy P/Cash Flow vs. 12 Mth Fwd Returns

SMID Gassy Basket 12 mth forward Returns SMID Gassy - Price/Cash Flow

-60%

-40%

-20%

0%

20%

40%

60%

1.3

1.8

2.3

2.8

3.3

3.8

4.3

4.8

5.3

6/3

0/2

00

9

8/3

1/2

00

9

10

/31

/20

09

12

/31

/20

09

2/2

8/2

01

0

4/3

0/2

01

0

6/3

0/2

01

0

8/3

1/2

01

0

10

/31

/20

10

12

/31

/20

10

2/2

8/2

01

1

4/3

0/2

01

1

6/3

0/2

01

1

8/3

1/2

01

1

10

/31

/20

11

12

/31

/20

11

2/2

9/2

01

2

4/3

0/2

01

2

6/3

0/2

01

2

8/3

1/2

01

2

10

/31

/20

12

12

/31

/20

12

2/2

8/2

01

3

fwd

ret

urn

s (b

ar)

P/Sa

les

(lin

e)

SMID Gassy P/Sales vs. 12 Mth Fwd Returns

SMID Gassy Basket 12 mth forward Returns SMID Gassy - Price/Sales

-60%

-40%

-20%

0%

20%

40%

60%

4.3

5.3

6.3

7.3

8.3

9.3

10.3

11.3

12.3

6/3

0/2

00

9

8/3

1/2

00

9

10

/31

/20

09

12

/31

/20

09

2/2

8/2

01

0

4/3

0/2

01

0

6/3

0/2

01

0

8/3

1/2

01

0

10

/31

/20

10

12

/31

/20

10

2/2

8/2

01

1

4/3

0/2

01

1

6/3

0/2

01

1

8/3

1/2

01

1

10

/31

/20

11

12

/31

/20

11

2/2

9/2

01

2

4/3

0/2

01

2

6/3

0/2

01

2

8/3

1/2

01

2

10

/31

/20

12

12

/31

/20

12

2/2

8/2

01

3

fwd

ret

urn

s (b

ar)

EV/E

BIT

DA

(lin

e)

SMID Gassy EV/EBITDA vs. 12 Mth Fwd Returns

SMID Gassy Basket 12 mth forward Returns SMID Gassy - EV/EBITDA

-60%

-40%

-20%

0%

20%

40%

60%

1.4

2.4

3.4

4.4

5.4

6.4

7.4

6/3

0/2

00

9

8/3

1/2

00

9

10

/31

/20

09

12

/31

/20

09

2/2

8/2

01

0

4/3

0/2

01

0

6/3

0/2

01

0

8/3

1/2

01

0

10

/31

/20

10

12

/31

/20

10

2/2

8/2

01

1

4/3

0/2

01

1

6/3

0/2

01

1

8/3

1/2

01

1

10

/31

/20

11

12

/31

/20

11

2/2

9/2

01

2

4/3

0/2

01

2

6/3

0/2

01

2

8/3

1/2

01

2

10

/31

/20

12

12

/31

/20

12

2/2

8/2

01

3

fwd

ret

urn

s (b

ar)

EV/S

ales

(li

ne

)

SMID Gassy EV/Sales vs. 12 Mth Fwd Returns

SMID Gassy Basket 12 mth forward Returns SMID Gassy - EV/Sales

Source: CS Small/Mid Cap US Equity Strategy, Bloomberg 12

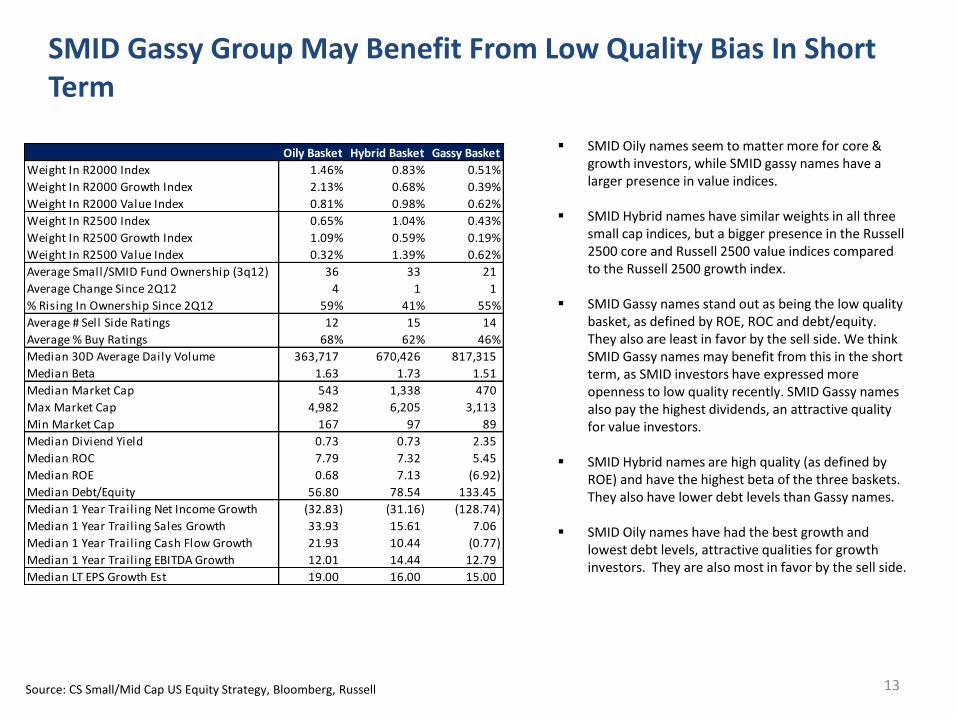

SMID Gassy Group May Benefit From Low Quality Bias In Short Term

SMID Oily names seem to matter more for core &

growth investors, while SMID gassy names have a larger presence in value indices.

SMID Hybrid names have similar weights in all three small cap indices, but a bigger presence in the Russell 2500 core and Russell 2500 value indices compared to the Russell 2500 growth index.

SMID Gassy names stand out as being the low quality basket, as defined by ROE, ROC and debt/equity. They also are least in favor by the sell side. We think SMID Gassy names may benefit from this in the short term, as SMID investors have expressed more openness to low quality recently. SMID Gassy names also pay the highest dividends, an attractive quality for value investors.

SMID Hybrid names are high quality (as defined by

ROE) and have the highest beta of the three baskets. They also have lower debt levels than Gassy names.

SMID Oily names have had the best growth and lowest debt levels, attractive qualities for growth investors. They are also most in favor by the sell side.

Source: CS Small/Mid Cap US Equity Strategy, Bloomberg, Russell

Oily Basket Hybrid Basket Gassy Basket

Weight In R2000 Index 1.46% 0.83% 0.51%

Weight In R2000 Growth Index 2.13% 0.68% 0.39%

Weight In R2000 Value Index 0.81% 0.98% 0.62%

Weight In R2500 Index 0.65% 1.04% 0.43%

Weight In R2500 Growth Index 1.09% 0.59% 0.19%

Weight In R2500 Value Index 0.32% 1.39% 0.62%

Average Small/SMID Fund Ownership (3q12) 36 33 21

Average Change Since 2Q12 4 1 1

% Rising In Ownership Since 2Q12 59% 41% 55%

Average # Sell Side Ratings 12 15 14

Average % Buy Ratings 68% 62% 46%

Median 30D Average Daily Volume 363,717 670,426 817,315

Median Beta 1.63 1.73 1.51

Median Market Cap 543 1,338 470

Max Market Cap 4,982 6,205 3,113

Min Market Cap 167 97 89

Median Diviend Yield 0.73 0.73 2.35

Median ROC 7.79 7.32 5.45

Median ROE 0.68 7.13 (6.92)

Median Debt/Equity 56.80 78.54 133.45

Median 1 Year Trailing Net Income Growth (32.83) (31.16) (128.74)

Median 1 Year Trailing Sales Growth 33.93 15.61 7.06

Median 1 Year Trailing Cash Flow Growth 21.93 10.44 (0.77)

Median 1 Year Trailing EBITDA Growth 12.01 14.44 12.79

Median LT EPS Growth Est 19.00 16.00 15.00

13

18%

41% 39%36%

41%

23%

41%

34%

26%

43%

35%

22%

0%

10%

20%

30%

40%

50%

Outperform Market Perform Underperform

What is your expectation for Gassy names (within small/mid

cap) over the next 6-12 months?

1Q12 2Q12 3Q12 4Q12

46%

34%

16%

26%

44%

30%

45%

35%

20%

36%

43%

21%

0%

10%

20%

30%

40%

50%

Outperform Market Perform Underperform

What is your expectation for Oily names (within small/mid

cap) over the next 6-12 months?

1Q12 2Q12 3Q12 4Q12

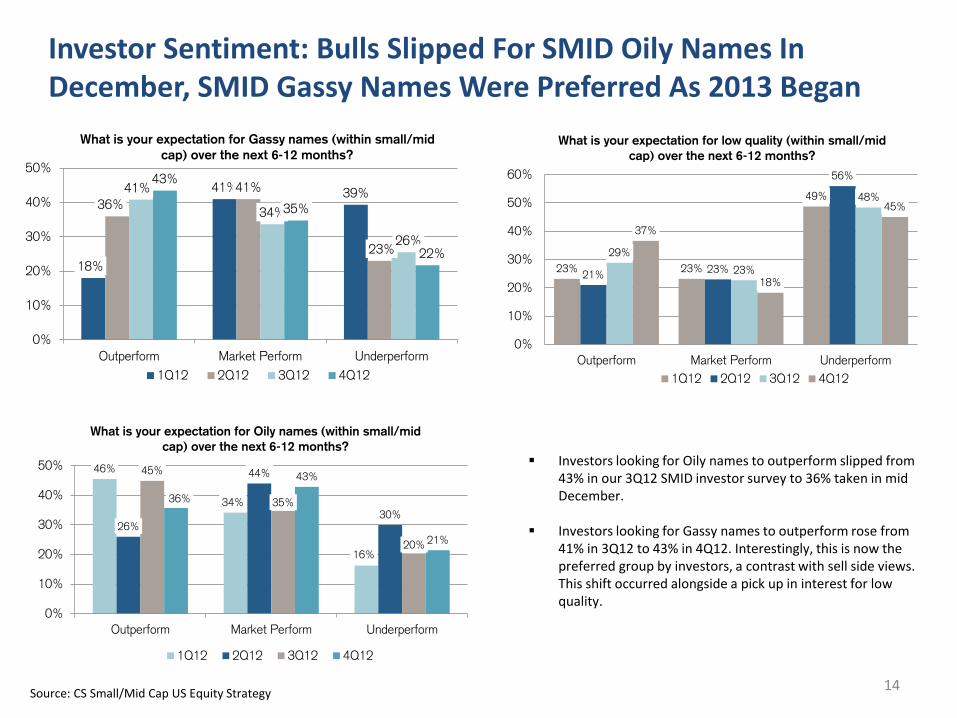

Investor Sentiment: Bulls Slipped For SMID Oily Names In December, SMID Gassy Names Were Preferred As 2013 Began

Investors looking for Oily names to outperform slipped from 43% in our 3Q12 SMID investor survey to 36% taken in mid December.

Investors looking for Gassy names to outperform rose from 41% in 3Q12 to 43% in 4Q12. Interestingly, this is now the preferred group by investors, a contrast with sell side views. This shift occurred alongside a pick up in interest for low quality.

Source: CS Small/Mid Cap US Equity Strategy

23% 23%

49%

21%23%

56%

29%

23%

48%

37%

18%

45%

0%

10%

20%

30%

40%

50%

60%

Outperform Market Perform Underperform

What is your expectation for low quality (within small/mid

cap) over the next 6-12 months?

1Q12 2Q12 3Q12 4Q12

14

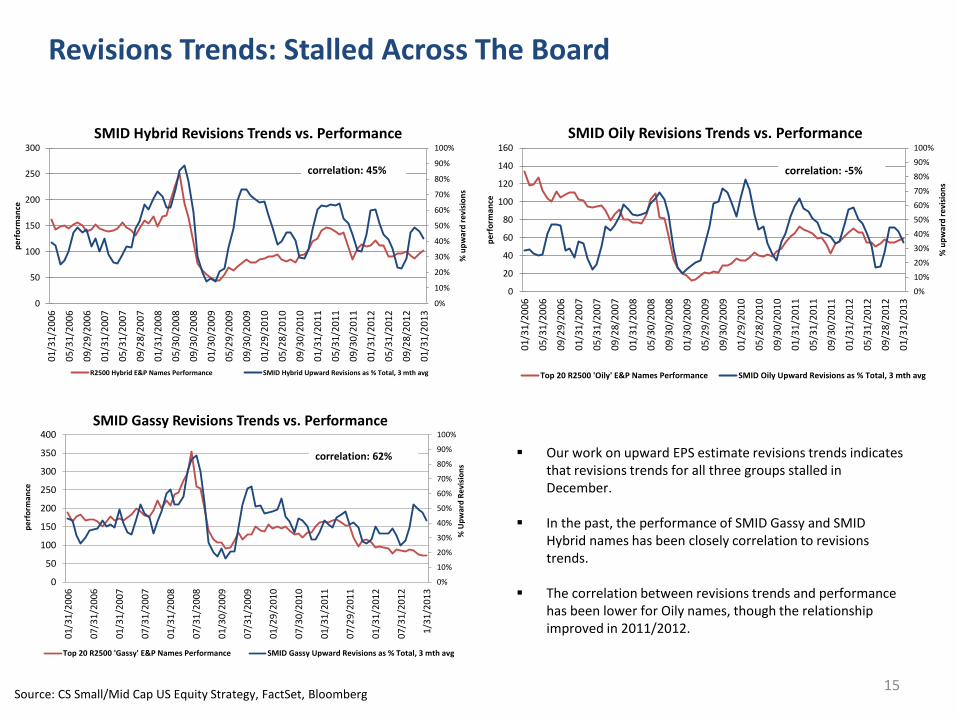

Revisions Trends: Stalled Across The Board

Our work on upward EPS estimate revisions trends indicates that revisions trends for all three groups stalled in December.

In the past, the performance of SMID Gassy and SMID Hybrid names has been closely correlation to revisions trends.

The correlation between revisions trends and performance has been lower for Oily names, though the relationship improved in 2011/2012.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

50

100

150

200

250

300

350

400

01

/31

/20

06

07

/31

/20

06

01

/31

/20

07

07

/31

/20

07

01

/31

/20

08

07

/31

/20

08

01

/30

/20

09

07

/31

/20

09

01

/29

/20

10

07

/30

/20

10

01

/31

/20

11

07

/29

/20

11

01

/31

/20

12

07

/31

/20

12

1/3

1/2

01

3

% U

pw

ard

Re

visi

on

s

pe

rfo

rman

ce

SMID Gassy Revisions Trends vs. Performance

Top 20 R2500 'Gassy' E&P Names Performance SMID Gassy Upward Revisions as % Total, 3 mth avg

correlation: 62%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

20

40

60

80

100

120

140

160

01

/31

/20

06

05

/31

/20

06

09

/29

/20

06

01

/31

/20

07

05

/31

/20

07

09

/28

/20

07

01

/31

/20

08

05

/30

/20

08

09

/30

/20

08

01

/30

/20

09

05

/29

/20

09

09

/30

/20

09

01

/29

/20

10

05

/28

/20

10

09

/30

/20

10

01

/31

/20

11

05

/31

/20

11

09

/30

/20

11

01

/31

/20

12

05

/31

/20

12

09

/28

/20

12

01

/31

/20

13

% u

pw

ard

re

visi

on

s

pe

rfo

rman

ce

SMID Oily Revisions Trends vs. Performance

Top 20 R2500 'Oily' E&P Names Performance SMID Oily Upward Revisions as % Total, 3 mth avg

correlation: -5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

50

100

150

200

250

300

01

/31

/20

06

05

/31

/20

06

09

/29

/20

06

01

/31

/20

07

05

/31

/20

07

09

/28

/20

07

01

/31

/20

08

05

/30

/20

08

09

/30

/20

08

01

/30

/20

09

05

/29

/20

09

09

/30

/20

09

01

/29

/20

10

05

/28

/20

10

09

/30

/20

10

01

/31

/20

11

05

/31

/20

11

09

/30

/20

11

01

/31

/20

12

05

/31

/20

12

09

/28

/20

12

01

/31

/20

13

% u

pw

ard

re

visi

on

s

pe

rfo

rman

ce

SMID Hybrid Revisions Trends vs. Performance

R2500 Hybrid E&P Names Performance SMID Hybrid Upward Revisions as % Total, 3 mth avg

correlation: 45%

Source: CS Small/Mid Cap US Equity Strategy, FactSet, Bloomberg 15

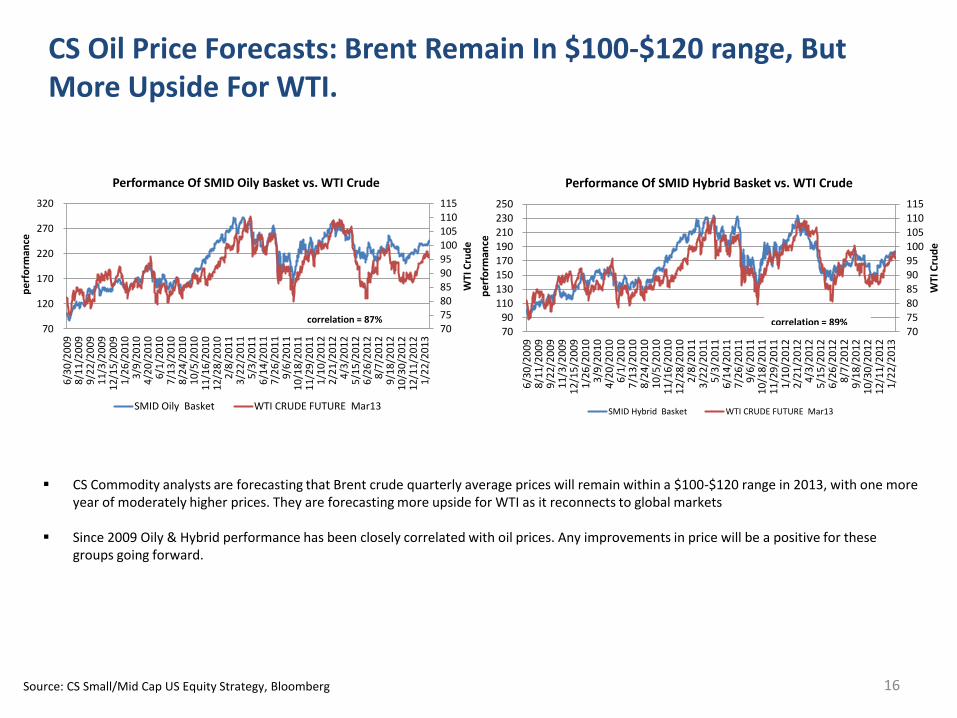

CS Oil Price Forecasts: Brent Remain In $100-$120 range, But More Upside For WTI.

CS Commodity analysts are forecasting that Brent crude quarterly average prices will remain within a $100-$120 range in 2013, with one more year of moderately higher prices. They are forecasting more upside for WTI as it reconnects to global markets

Since 2009 Oily & Hybrid performance has been closely correlated with oil prices. Any improvements in price will be a positive for these

groups going forward.

707580859095100105110115

70 90

110 130 150 170 190 210 230 250

6/3

0/2

009

8/1

1/2

009

9/2

2/2

009

11

/3/2

009

12

/15

/20

09

1/2

6/2

010

3/9

/20

10

4/2

0/2

010

6/1

/20

10

7/1

3/2

010

8/2

4/2

010

10

/5/2

010

11

/16

/20

10

12

/28

/20

10

2/8

/20

11

3/2

2/2

011

5/3

/20

11

6/1

4/2

011

7/2

6/2

011

9/6

/20

11

10

/18

/20

11

11

/29

/20

11

1/1

0/2

012

2/2

1/2

012

4/3

/20

12

5/1

5/2

012

6/2

6/2

012

8/7

/20

12

9/1

8/2

012

10

/30

/20

12

12

/11

/20

12

1/2

2/2

013

WTI

Cru

de

per

form

ance

Performance Of SMID Hybrid Basket vs. WTI Crude

SMID Hybrid Basket WTI CRUDE FUTURE Mar13

correlation = 89%707580859095100105110115

70

120

170

220

270

320

6/3

0/2

00

98

/11

/20

09

9/2

2/2

00

91

1/3

/20

09

12

/15

/20

09

1/2

6/2

01

03

/9/2

01

04

/20

/20

10

6/1

/20

10

7/1

3/2

01

08

/24

/20

10

10

/5/2

01

01

1/1

6/2

01

01

2/2

8/2

01

02

/8/2

01

13

/22

/20

11

5/3

/20

11

6/1

4/2

01

17

/26

/20

11

9/6

/20

11

10

/18

/20

11

11

/29

/20

11

1/1

0/2

01

22

/21

/20

12

4/3

/20

12

5/1

5/2

01

26

/26

/20

12

8/7

/20

12

9/1

8/2

01

21

0/3

0/2

01

21

2/1

1/2

01

21

/22

/20

13

WTI

Cru

de

pe

rfo

rman

ce

Performance Of SMID Oily Basket vs. WTI Crude

SMID Oily Basket WTI CRUDE FUTURE Mar13

correlation = 87%

Source: CS Small/Mid Cap US Equity Strategy, Bloomberg 16

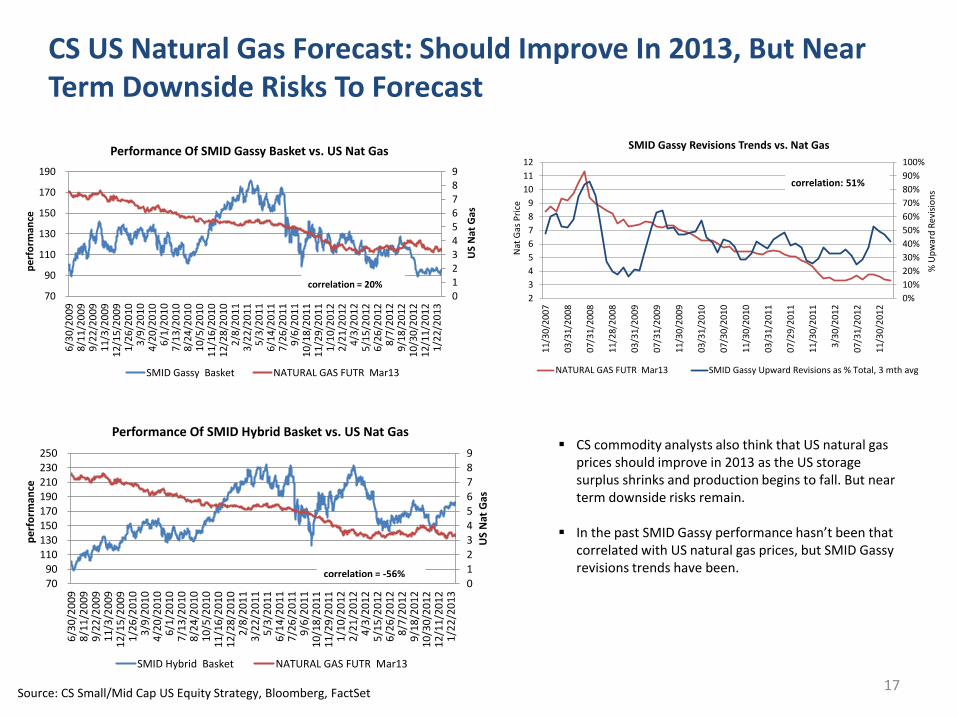

CS commodity analysts also think that US natural gas prices should improve in 2013 as the US storage surplus shrinks and production begins to fall. But near term downside risks remain.

In the past SMID Gassy performance hasn’t been that correlated with US natural gas prices, but SMID Gassy revisions trends have been.

CS US Natural Gas Forecast: Should Improve In 2013, But Near Term Downside Risks To Forecast

0123456789

70 90

110 130 150 170 190 210 230 250

6/3

0/2

00

98

/11

/20

09

9/2

2/2

00

91

1/3

/20

09

12

/15

/20

09

1/2

6/2

01

03

/9/2

01

04

/20

/20

10

6/1

/20

10

7/1

3/2

01

08

/24

/20

10

10

/5/2

01

01

1/1

6/2

01

01

2/2

8/2

01

02

/8/2

01

13

/22

/20

11

5/3

/20

11

6/1

4/2

01

17

/26

/20

11

9/6

/20

11

10

/18

/20

11

11

/29

/20

11

1/1

0/2

01

22

/21

/20

12

4/3

/20

12

5/1

5/2

01

26

/26

/20

12

8/7

/20

12

9/1

8/2

01

21

0/3

0/2

01

21

2/1

1/2

01

21

/22

/20

13

US

Nat

Gas

pe

rfo

rman

ce

Performance Of SMID Hybrid Basket vs. US Nat Gas

SMID Hybrid Basket NATURAL GAS FUTR Mar13

correlation = -56%

0123456789

70

90

110

130

150

170

190

6/3

0/2

00

98

/11

/20

09

9/2

2/2

00

91

1/3

/20

09

12

/15

/20

09

1/2

6/2

01

03

/9/2

01

04

/20

/20

10

6/1

/20

10

7/1

3/2

01

08

/24

/20

10

10

/5/2

01

01

1/1

6/2

01

01

2/2

8/2

01

02

/8/2

01

13

/22

/20

11

5/3

/20

11

6/1

4/2

011

7/2

6/2

01

19

/6/2

01

11

0/1

8/2

01

11

1/2

9/2

01

11

/10

/20

12

2/2

1/2

01

24

/3/2

01

25

/15

/20

12

6/2

6/2

012

8/7

/20

12

9/1

8/2

01

21

0/3

0/2

01

21

2/1

1/2

01

21

/22

/20

13

US

Nat

Gas

pe

rfo

rman

ce

Performance Of SMID Gassy Basket vs. US Nat Gas

SMID Gassy Basket NATURAL GAS FUTR Mar13

correlation = 20%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2

3

4

5

6

7

8

9

10

11

12

11

/30

/20

07

03

/31

/20

08

07

/31

/20

08

11

/28

/20

08

03

/31

/20

09

07

/31

/20

09

11

/30

/20

09

03

/31

/20

10

07

/30

/20

10

11

/30

/20

10

03

/31

/20

11

07

/29

/20

11

11

/30

/20

11

3/3

0/2

01

2

07

/31

/20

12

11

/30

/20

12

% U

pw

ard

Re

visi

on

s

Nat

Gas

Pri

ce

SMID Gassy Revisions Trends vs. Nat Gas

NATURAL GAS FUTR Mar13 SMID Gassy Upward Revisions as % Total, 3 mth avg

correlation: 51%

Source: CS Small/Mid Cap US Equity Strategy, Bloomberg, FactSet 17

-100%

-75%

-50%

-25%

0%

25%

50%

75%

100%

(4)

(3)

(2)

(1)

-

1

2

3

4

Dec

-86

Dec

-88

Dec

-90

Dec

-92

Dec

-94

Dec

-96

Dec

-98

Dec

-00

Dec

-02

Dec

-04

Dec

-06

Dec

-08

Dec

-10

Dec

-12

Ret

urn

Val

uat

ion

Small Cap Energy Relative Valuation

Energy 12 Mth Relative Forward Return

Energy Relative Valuation Model - P/B, P/S

Still Overweight Energy & E&P’s Are The Biggest Weight

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

01

/30

/19

87

01

/31

/19

89

01

/31

/19

91

01

/29

/19

93

01

/31

/19

95

01

/31

/19

97

01

/29

/19

99

01

/31

/20

01

01

/31

/20

03

01

/31

/20

05

01

/31

/20

07

01

/30

/20

09

1/3

1/2

011

1/3

1/2

013

Energy Upward Revisions Trends

Russell 2500 Energy Sector Up Revisions as % of Total

Russell 2500 Energy Sector 3 mo avg

0%

2%

4%

6%

8%

10%

Dec

-03

Mar

-04

Jun

-04

Sep

-04

Dec

-04

Mar

-05

Jun

-05

Sep

-05

Dec

-05

Mar

-06

Jun

-06

Sep

-06

Dec

-06

Mar

-07

Jun

-07

Sep

-07

Dec

-07

Mar

-08

Jun

-08

Sep

-08

Dec

-08

Mar

-09

Jun

-09

Sep

-09

Dec

-09

Mar

-10

Jun

-10

Sep

-10

Dec

-10

Mar

-11

Jun

-11

Sep

-11

Dec

-11

Mar

-12

Jun

-12

Sep

-12

Dec

-12

Energy Allocation in R2000 Value Funds vs Sector Weight In R2000 Value Index

R2000 Value Benchmarked Funds Energy Allocation

Energy Weight In R2000 Value Index

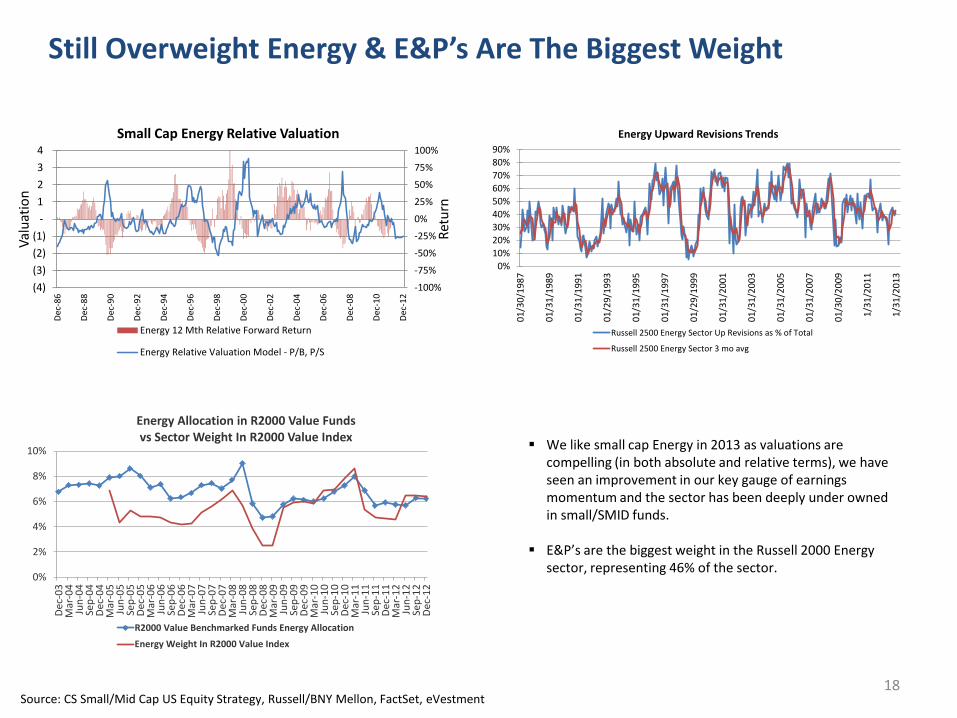

We like small cap Energy in 2013 as valuations are compelling (in both absolute and relative terms), we have seen an improvement in our key gauge of earnings momentum and the sector has been deeply under owned in small/SMID funds.

E&P’s are the biggest weight in the Russell 2000 Energy sector, representing 46% of the sector.

Source: CS Small/Mid Cap US Equity Strategy, Russell/BNY Mellon, FactSet, eVestment 18

Please see slides 5-9 for a full list of companies mentioned

DISCLOSURE APPENDIX CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, INFORMATION ON TRADE ALERTS, ANALYST MODEL

PORTFOLIOS AND THE STATUS OF NON-U.S ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

Disclosure Appendix

Important Global Disclosures

I, Lori Calvasina, certify that (1) the views expressed in this report accurately reflect my personal views about all of the subject companies and securities and (2) no part of my compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

The analyst(s) responsible for preparing this research report received Compensation that is based upon various factors including Credit Suisse's total revenues, a portion of which are generated by Credit Suisse's investment banking activities

As of December 10, 2012 Analysts’ stock rating are defined as follows:

Outperform (O) : The stock’s total return is expected to outperform the relevant benchmark*over the next 12 months.

Neutral (N) : The stock’s total return is expected to be in line with the relevant benchmark* over the next 12 months.

Underperform (U) : The stock’s total return is expected to underperform the relevant benchmark* over the next 12 months.

*Relevant benchmark by region: As of 10th December 2012, Japanese ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. As of 2nd October 2012, U.S. and Canadian as well as European ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms represe nting the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. For Latin American and non -Japan Asia stocks, ratings are based on a stock’s total return relative to the average total return of the relevant country or regional benchmark; Australia, New Zealand are, and prior to 2nd October 2012 U.S. and Canadian ratings were based on (1) a stock’s absolute total return potential to its current share price and (2) the relative attractiveness of a stock’s total return potential within an analyst’s coverage universe. For Australian and New Zealand stocks, 12-month rolling yield is incorporated in the absolute total return calculation and a 15% and a 7.5% threshold replace the 10-15% level in the Outperform and Underperform stock rating definitions, respectively. The 15% and 7.5% thresholds replace the +10-15% and -10-15% levels in the Neutral stock rating definition, respectively. Prior to 10th December 2012, Japanese ratings were based on a stock’s total return rel ative to the average total return of the relevant country or regional benchmark.

Restricted (R) : In certain circumstances, Credit Suisse policy and/or applicable law and regulations preclude certain types of communications, including an investment recommendation, during the course of Credit Suisse's engagement in an investment banking transaction and in certain other circumstances.

Volatility Indicator [V] : A stock is defined as volatile if the stock price has moved up or down by 20% or more in a month in at least 8 of the past 24 months or the analyst expects significant volatility going forward.

Analysts’ sector weightings are distinct from analysts’ stock ratings and are based on the analyst’s expectations for the fundamentals and/or valuation of the sector* relative to the group’s historic fundamentals and/or valuation:

Overweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is favorable over the next 12 months.

Market Weight : The analyst’s expectation for the sector’s fundamentals and/or valuation is neutral over the next 12 months.

Underweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is cautious over the next 12 months.

*An analyst’s coverage sector consists of all companies covered by the analyst within the relevant sector. An analyst may cover multiple sectors.

Credit Suisse's distribution of stock ratings (and banking clients) is:

Global Ratings Distribution

Rating Versus universe (%) Of which banking clients (%)

Outperform/Buy* 42% (53% banking clients)

Neutral/Hold* 38% (47% banking clients)

Underperform/Sell* 16% (40% banking clients)

Restricted 3%

*For purposes of the NYSE and NASD ratings distribution disclosure requirements, our stock ratings of Outperform, Neutral, an d Underperform most closely correspond to Buy, Hold, and Sell, respectively; however, the meanings are not the same, as our stock ratings are determined on a relative basis. (Please refer to definitions above.) An investor's decision to buy or sell a security should be based on investment objectives, current holdings, and other individua l factors.

Credit Suisse’s policy is to update research reports as it deems appropriate, based on developments with the subject company, the sector or the market that may have a material impact on the research views or opinions stated herein.

Credit Suisse's policy is only to publish investment research that is impartial, independent, clear, fair and not misleading. For more detail please refer to Credit Suisse's Policies for Managing Conflicts of Interest in connection with Investment Research: http://www.csfb.com/research and analytics/disclaimer/managing_conflicts_disclaimer.html

Credit Suisse does not provide any tax advice. Any statement herein regarding any US federal tax is not intended or

written to be used, and cannot be used, by any taxpayer for the purposes of avoiding any penalties.

Please refer to the firm's disclosure website at www.credit-suisse.com/researchdisclosures for the definitions of abbreviations typically used in the target price method and risk sections.

Important Regional Disclosures

Singapore recipients should contact Credit Suisse AG, Singapore Branch for any matters arising from this research report.

Restrictions on certain Canadian securities are indicated by the following abbreviations: NVS--Non-Voting shares; RVS--Restricted Voting Shares; SVS--Subordinate Voting Shares.

Individuals receiving this report from a Canadian investment dealer that is not affiliated with Credit Suisse should be advised that this report may not contain regulatory disclosures the non-affiliated Canadian investment dealer would be required to make if this were its own report.

For Credit Suisse Securities (Canada), Inc.'s policies and procedures regarding the dissemination of equity research, please visit http://www.csfb.com/legal_terms/canada_research_policy.shtml.

As of the date of this report, Credit Suisse acts as a market maker or liquidity provider in the equities securities that are the subject of this report.

Principal is not guaranteed in the case of equities because equity prices are variable.

Commission is the commission rate or the amount agreed with a customer when setting up an account or at any time after that.

For Credit Suisse disclosure information on other companies mentioned in this report, please visit the website at www.credit-suisse.com/researchdisclosures or call +1 (877) 291-2683.

19