stirling abstract 2016-17 audited version · responsibilities of the chief finance officer for the...

TRANSCRIPT

Loch Dhu

STIRLING COUNCIL

ABSTRACT OF ACCOUNTS

2016-17

Page 2 of 75

Annual Accounts - Contents

Page Page

Independent Auditor’s Report 3 Note 14 Asset Revaluation Programme 45

Note 15 Capital Expenditure and Capital Financing 46

Management Commentary 5 Note 16 Heritage Assets 46

Note 17 Long Term Debtors 47

Explanatory & Assurance Statements Note 18 Short Term Debtors 47

Statement of Responsibilities 15 Note 19 Cash & Cash Equivalents 47

Annual Governance Statement 16 Note 20 Short Term Creditors 48

Remuneration Report 22 Note 21 PFI and PPP Contracts 48

Note 22 Pension Costs 49

Principal Financial Statements of the Single Entity Note 23 Unusable Reserves 52

Expenditure and Funding Analysis 28 Note 24 Leases 54

Comprehensive Income and Expenditure Statement 29 Note 25 Financial Instruments (FI) 55

Movement in Reserves Statement 30 Note 26 Nature and Extent of Risks Arising From

Financial Instruments 57

Balance Sheet 31 Note 27 Related Parties 58

Cash Flow Statement 32

Supplementary Financial Statements

Notes to the Single Entity Financial Statements Housing Revenue Account 59

General Accounting Policies & Assumptions Council Tax Income Account 61

Note 1 General Accounting Policies (where no

accompanying note) 33 Non Domestic Rates Income Account 62

Note 2 Accounting Standards Not Yet Adopted 34 Common Good Funds 63

Note 3 Critical Judgements Applied 34 Trust Funds 64

Note 4 Future Assumptions 35

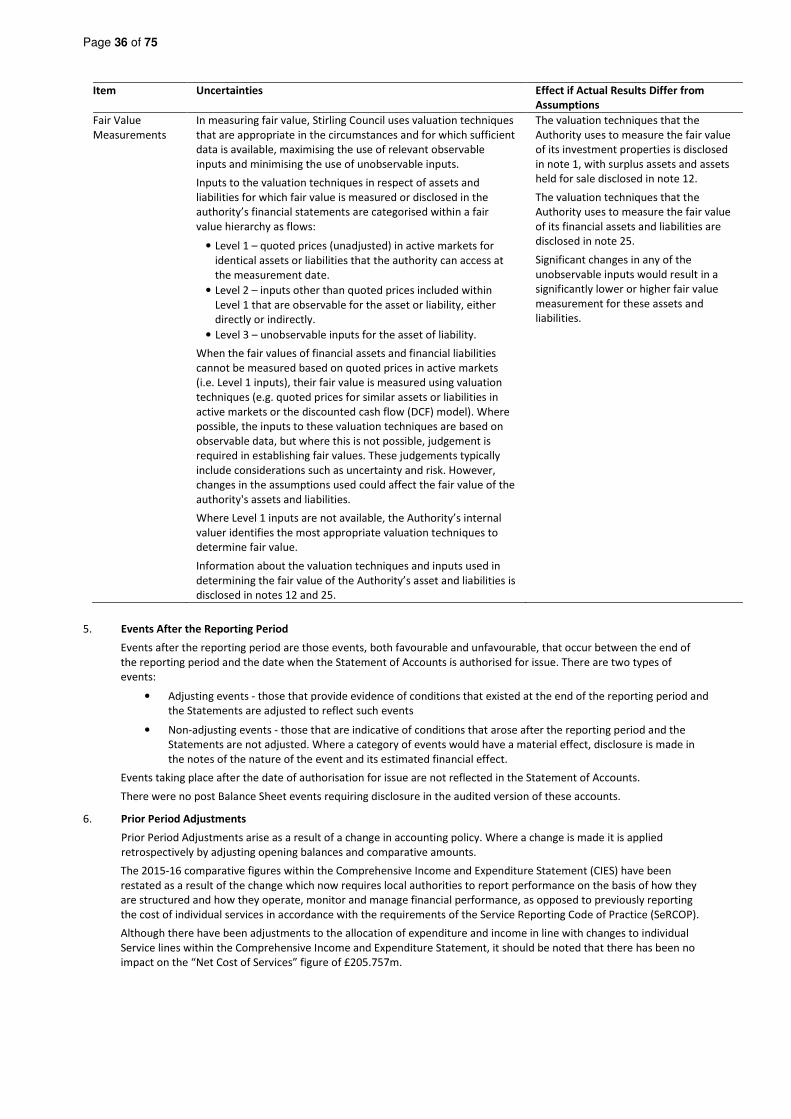

Note 5 Events After The Reporting Period 36 Principal Financial Statements of the Group

Note 6 Prior Year Adjustments 36 Group Comprehensive Income & Expenditure

Statement 65

Group Movement in Reserves Statement 66

Expenditure and Funding Analysis Group Balance Sheet 67

Note 7 Note to the Expenditure and Funding Analysis 37 Group Cash Flow Statement 68

Comprehensive Income and Expenditure Statement

Note 8 Grants and Taxation Income 38 Notes to the Group Financial Statements

Note 9 External Audit Costs 38 1. Group Accounting Policies 69

2. Non-Consolidation Interests in Other Entities 71

Statement of Movements in Reserves 3. Financial Results of Associates, Joint Ventures and

Joint Operations 71

Note 10 Adjustments Between Accounting Basis and

Funding Basis Under Regulations 39 4. Financial Impact of Group Consolidation 72

Note 11 General Fund Reserves 41

Glossary of Terms

Balance Sheet Glossary of Terms 73

Note 12 Property, Plant & Equipment 41

Note 13 Impairments/Downward Revaluations 44

Page 3 of 75

Independent Auditor’s Report

Independent auditor’s report to the members of Stirling Council and the Accounts Commission

This report is made solely to the parties to whom it is addressed in accordance with Part VII of the Local Government (Scotland)

Act 1973 and for no other purpose. In accordance with paragraph 120 of the Code of Audit Practice approved by the Accounts

Commission, I do not undertake to have responsibilities to members or officers, in their individual capacities, or to third parties.

Report on the audit of the financial statements

Opinion on financial statements

I certify that I have audited the financial statements in the annual accounts of Stirling Council and its group for the year ended

31 March 2017 under Part VII of the Local Government (Scotland) Act 1973. The financial statements comprise the Expenditure

and Funding Analysis, the group and council-only Comprehensive Income and Expenditure Statements, Movement in Reserves

Statements, Balance Sheets, and Cash-Flow Statements, the council-only Housing Revenue Account, the Council Tax Income

Account, and the Non-Domestic Rates Income Account and notes to the financial statements, including a summary of significant

accounting policies. The financial reporting framework that has been applied in their preparation is applicable law and

International Financial Reporting Standards (IFRSs) as adopted by the European Union, and as interpreted and adapted by the

Code of Practice on Local Authority Accounting in the United Kingdom 2016/17 (the 2016/17 Code).

In my opinion the accompanying financial statements:

• give a true and fair view in accordance with applicable law and the 2016/17 Code of the state of affairs of the council and

its group as at 31 March 2017 and of the deficit on the provision of services of the council and its group for the year then

ended;

• have been properly prepared in accordance with IFRSs as adopted by the European Union, as interpreted and adapted by

the 2016/17 Code; and

• have been prepared in accordance with the requirements of the Local Government (Scotland) Act 1973, The Local

Authority Accounts (Scotland) Regulations 2014, and the Local Government in Scotland Act 2003.

Basis of opinion

I conducted my audit in accordance with applicable law and International Standards on Auditing in the UK and Ireland (ISAs

(UK&I)). My responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the

Financial Statements section of my report. I am independent of the council and its group in accordance with the ethical

requirements that are relevant to my audit of the financial statements in the UK including the Financial Reporting Council’s

Ethical Standards for Auditors, and I have fulfilled my other ethical responsibilities in accordance with these requirements. I

believe that the audit evidence I have obtained is sufficient and appropriate to provide a basis for my opinion.

Responsibilities of the Chief Finance Officer for the financial statements

As explained more fully in the Statement of Responsibilities, the Chief Finance Officer is responsible for the preparation of

financial statements that give a true and fair view in accordance with the financial reporting framework, and for such internal

control as the Chief Finance Officer determines is necessary to enable the preparation of financial statements that are free from

material misstatement, whether due to fraud or error.

Auditor’s responsibilities for the audit of the financial statements

My responsibility is to audit and express an opinion on the financial statements in accordance with applicable legal

requirements and ISAs (UK&I) as required by the Code of Audit Practice approved by the Accounts Commission. Those standards

require me to comply with the Financial Reporting Council’s Ethical Standards for Auditors. An audit involves obtaining evidence

about the amounts and disclosures in the financial statements sufficient to give reasonable assurance that the financial

statements are free from material misstatement, whether caused by fraud or error. This includes an assessment of: whether the

accounting policies are appropriate to the circumstances of the council and its group and have been consistently applied and

adequately disclosed; the reasonableness of significant accounting estimates made by the Chief Finance Officer and the overall

presentation of the financial statements.

My objectives are to achieve reasonable assurance about whether the financial statements as a whole are free from material

misstatement, whether due to fraud or error, and to issue an auditor’s report that includes my opinion. Reasonable assurance is

a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs (UK&I) will always detect a

material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or

in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these

financial statements.

Other information in the annual accounts

The Chief Finance Officer is responsible for the other information in the annual accounts. The other information comprises the

information other than the financial statements and my auditor’s report thereon. My opinion on the financial statements does

not cover the other information and I do not express any form of assurance conclusion thereon except on matters prescribed by

the Accounts Commission to the extent explicitly stated later in this report.

Page 4 of 75

In connection with my audit of the financial statements in accordance with ISAs (UK&I), my responsibility is to read all the

financial and non-financial information in the annual accounts to identify material inconsistencies with the audited financial

statements and to identify any information that is apparently materially incorrect based on, or materially inconsistent with, the

knowledge acquired by me in the course of performing the audit. If I become aware of any apparent material misstatements or

inconsistencies I consider the implications for my report.

Report on other requirements

Opinions on other prescribed matters

I am required by the Accounts Commission to express an opinion on the following matters.

In my opinion, the auditable part of the Remuneration Report has been properly prepared in accordance with The Local

Authority Accounts (Scotland) Regulations 2014.

In my opinion, based on the work undertaken in the course of the audit

• the information given in the Management Commentary for the financial year for which the financial statements are

prepared is consistent with the financial statements and that report has been prepared in accordance with statutory

guidance issued under the Local Government in Scotland Act 2003; and

• the information given in the Annual Governance Statement for the financial year for which the financial statements are

prepared is consistent with the financial statements and that report has been prepared in accordance with the Delivering

Good Governance in Local Government: Framework (2016).

Matters on which I am required to report by exception

I am required by the Accounts Commission to report to you if, in my opinion:

• adequate accounting records have not been kept; or

• the financial statements and the auditable part of the Remuneration Report are not in agreement with the accounting

records; or

• I have not received all the information and explanations I require for my audit; or

• there has been a failure to achieve a prescribed financial objective.

I have nothing to report in respect of these matters.

David McConnell MA CPFA

Assistant Director

Audit Scotland

4th Floor, South Suite

8 Nelson Mandela Place

Glasgow

G2 1BT

Page 5 of 75

Management Commentary

1. Introduction

The purpose of the Management Commentary is to inform users of the Annual Accounts and help them assess how Stirling

Council has performed during 2016-17 and understand the year-end financial position as at 31 March 2017. It also provides a

narrative on the financial outlook and the complexities Stirling Council will have to deal with in the financial years 2017-18 and

beyond.

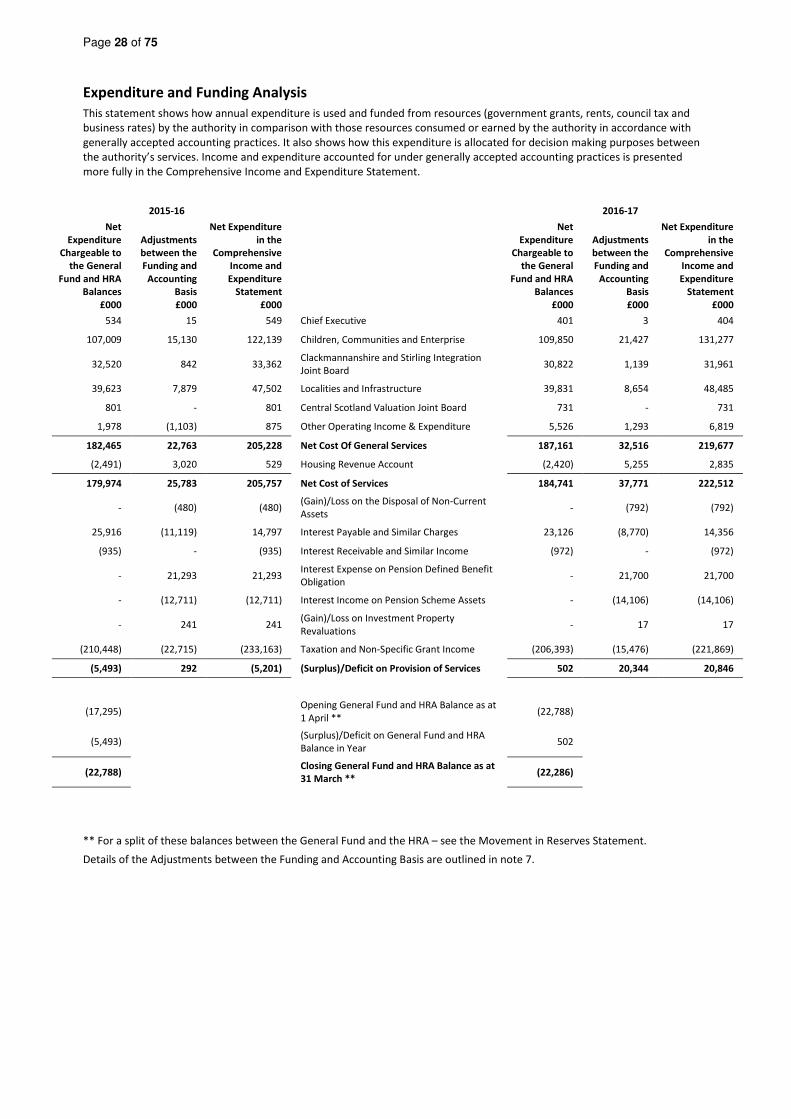

Stirling Council’s financial results are presented in five primary statements (pages 27 to 31): Expenditure and Funding Analysis;

Comprehensive Income and Expenditure Statement; Movement in Reserves Statement; Balance Sheet; Cash Flow Statement.

The accompanying notes to the financial statements set out the accounting policies adopted by Stirling Council to ensure that

the financial statements give a true and fair view of the Council’s financial position and transactions. The format and content of

local authorities’ Annual Accounts are governed by the The Code of Practice on Local Authority Accounting in the United

Kingdom (“the Code”).

2. About Stirling Council

Stirling Council is one of 32 Councils in Scotland established in 1996 as part of Local Government reorganisation. The Council

covers an area of around 850 square miles, and immediately prior to the recent Local Government Elections (May 2017), had 22

elected Members serving a population of approximately 92,000. The Stirling Council Administration prior to May 2017 was a

coalition of Labour and Conservative members as follows:

From May 2017, Stirling Council now has 23 elected members, with the Stirling Council Administration being a coalition of

Scottish National Party and Labour members.

A number of factors are impacting on Stirling Council and how it operates as an organisation. An increasing expectation amongst

citizens to have a say in how services are being delivered, a decrease in resources, localities becoming stronger and continued

financial challenges are all a catalyst for change.

As we have built up our relationships with communities, our understanding of their requirements has become better. The

integrated work we currently do in a range of areas, the new locality based approach, our organisational transformation and our

work on a City Region Deal, will mean significant changes in the way we deliver our services over the next five years.

These challenges which face Stirling Council over the next five years will be the focus of work in our two Service directorates -

‘Localities and Infrastructure’ and ‘Children, Communities and Enterprise’.

The remit for Localities and Infrastructure includes Waste, Integrated Facilities Management, Roads and Land, Business

Improvement and Compliance, Infrastructure, Planning and Building Standards Regulation, Sustainability, Finance, Governance

Page 6 of 75

and Technology, with corporate responsibility for Health and Safety, Fleet, Performance Management and Risk and Resilience.

The nature of these services means there will be a close relationship between their delivery and the locality approach and a

crossover with many aspects of Children, Communities and Enterprise.

The remit for Children, Communities and Enterprise covers the spectrum from birth to older people, with an integrated

approach to the services that we provide to citizens, working in partnership with our communities, stakeholders, national

bodies, Community Planning Partners and the third sector. It includes Economic Development and Regeneration, Communities

and People (adult social care, housing, public transport, safer communities, enforcement and community planning), Schools,

Learning and Education, Children and Families, Human Resources, Organisational Development, Programme Management,

Customer Services and Complaints, Communications and Priority Based Budgeting (PBB).

Integration of Adult Health & Social Care Services

On 1 April 2016, Stirling Council, Clackmannanshire Council and NHS Forth Valley commenced a Health and Social Care

Partnership across the Stirling and Clackmannanshire Council areas to integrate the planning for and delivery of adult health and

social care services. The partnership has also been extended to third and independent sector colleagues.

The Integration Joint Board has representatives from Stirling and Clackmannanshire Councils, NHS Forth Valley Health Board, the

Third Sector, representatives of those who use health and social care services and unpaid carers. The Board, through the Chief

Officer, has responsibility for the planning, resourcing and operational oversight of integrated services within the Strategic Plan.

Further information on the Clackmannanshire and Stirling Health and Social Care Partnership can be found at the following

webpage: http://nhsforthvalley.com//about-us/health-and-social-care-integration/clackmannanshire-and-stirling/.

3. Council Performance 2016-17

Key Council Achievements 2016-17

• Completed new build construction of St Ninians and St Margaret’s Primary Schools;

• Continued with a replacement programme of energy efficient street lighting with funding secured for this from the UK

Green Investment Bank PLC;

• Built or purchased 66 new units of social housing;

• Supported development of Health & Social Care Integration; and

• Continued to progress proposals for the Stirling City Development Framework.

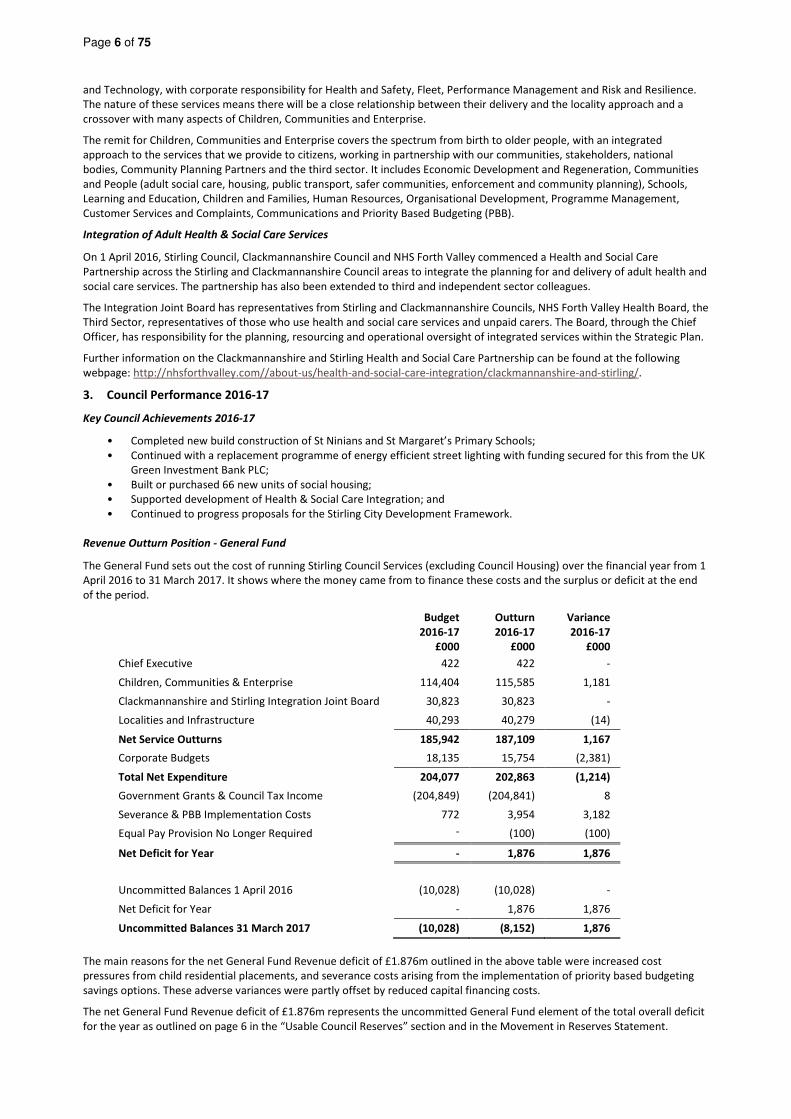

Revenue Outturn Position - General Fund

The General Fund sets out the cost of running Stirling Council Services (excluding Council Housing) over the financial year from 1

April 2016 to 31 March 2017. It shows where the money came from to finance these costs and the surplus or deficit at the end

of the period.

Budget

2016-17

£000

Outturn

2016-17

£000

Variance

2016-17

£000

Chief Executive 422 422 -

Children, Communities & Enterprise 114,404 115,585 1,181

Clackmannanshire and Stirling Integration Joint Board 30,823 30,823 -

Localities and Infrastructure 40,293 40,279 (14)

Net Service Outturns 185,942 187,109 1,167

Corporate Budgets 18,135 15,754 (2,381)

Total Net Expenditure 204,077 202,863 (1,214)

Government Grants & Council Tax Income (204,849) (204,841) 8

Severance & PBB Implementation Costs 772 3,954 3,182

Equal Pay Provision No Longer Required -

(100) (100)

Net Deficit for Year - 1,876 1,876

Uncommitted Balances 1 April 2016 (10,028) (10,028) -

Net Deficit for Year - 1,876 1,876

Uncommitted Balances 31 March 2017 (10,028) (8,152) 1,876

The main reasons for the net General Fund Revenue deficit of £1.876m outlined in the above table were increased cost

pressures from child residential placements, and severance costs arising from the implementation of priority based budgeting

savings options. These adverse variances were partly offset by reduced capital financing costs.

The net General Fund Revenue deficit of £1.876m represents the uncommitted General Fund element of the total overall deficit

for the year as outlined on page 6 in the “Usable Council Reserves” section and in the Movement in Reserves Statement.

Page 7 of 75

There was a surplus of £1.124m in the earmarked element of the General Fund income and expenditure. Overall, this resulted in

a deficit of £0.752m in the General Fund for 2016/17 which contributed to the decrease in usable reserves of £3.426m in

2016/17.

Council Housing (Housing Revenue Account)

Stirling Council owns 5,587 houses for which it charges rent. All expenditure associated with these houses must be funded from

the rental income generated. Any surplus or deficit at the end of the year is transferred into or out of the Housing Revenue

Account (HRA) balances. For 2016-17, the transfer of a net surplus of £0.250m resulted in HRA balances of £0.736m.

Capital Outturn Position

Capital expenditure represents money spent by the Council for buying, upgrading or improving assets such as buildings and

roads. The difference between capital and revenue expenditure is that the Council receives the benefit from capital expenditure

over a period exceeding one year. Stirling Council spent £40.688m during the year to finance various capital expenditure

programmes.

The General Fund Capital Programme reported expenditure of £28.127m against a full year budget of £32.106m representing

slippage of £3.979m. The most significant capital projects undertaken during the year included Sports Village – National Curling

Academy, Roads Improvements, Energy Efficient Street Lighting and St Margaret’s and St Ninians Primary School new builds.

The Housing Capital Programme reported expenditure of £12.561m, an overspend of £2.890m against a budget of £9.671m.

This overspend was due to the completion of previously slipped ‘New Build’ Programmes and additional spending on property

acquisitions which was offset by additional grant income and house sales of £2.057m. This resulted in borrowing of £0.955m in

the year against a budget of £0.122m.

Usable Council Reserves

The Movement in Reserves Statement shows an overall net increase in usable reserves of £3.426m for the year, which can be

analysed as follows:

Balances b/fwd

1 April 2016

£000

Movement in

Balances

£000

Balances c/fwd

31 March 2017

£000

Uncommitted Balances (10,028) 1,876 (8,152)

Earmarked Balances (12,274) (1,124) (13,398)

General Fund Balance (22,302) 752 (21,550)

Housing Revenue Account (486) (250) (736)

Repairs and Renewals Fund (1,605) (248) (1,853)

Insurance Fund (1,111) (660) (1,771)

Capital Receipts Reserve (3,739) 3,004 (735)

Capital Grants Unapplied Account (828) 828 -

Total Usable Reserves (30,071) 3,426 (26,645)

General Fund balances are split between uncommitted balances (the level of funding available to Stirling Council to manage

financial risks and unplanned expenditure) and balances which have been earmarked for specific purposes.

• Uncommitted balances of £8.152m as at 31 March 2017 represent 4.0% of the General Fund Budget for 2016-17 and

exceed the target level of balances (between 2% and 2.5% of revenue budget over the medium term).

• The movement in Uncommitted General Fund Balances of £1.876m during 2016-17 represents a net deficit for the

year when compared to the approved budget as shown above.

• The movement in Earmarked General Fund balances of £1.124m during 2016-17 is outlined in note 11.

The Housing Revenue Account balances represent the accumulation of surpluses, deficits and appropriation over past years in

relation to Council Houses. The Housing Revenue Account achieved a surplus of £0.250m during 2016-17.

The Repairs and Renewals Fund provides for major repairs to the Lower Polmaise Waste Transfer Station and Stirling Council’s

sports facilities. Reserves at 31 March 2017 represent £0.2m (Waste Transfer Station) and £1.653m (Sports Facilities).

The Insurance Fund covers the main classes of insurance and is specifically earmarked for possible future insurance claims.

The Capital Receipts Reserve represents the proceeds from non-current asset disposals not yet used and which are available to

meet future capital investment.

The Capital Grants Unapplied Account holds those grants and contributions received towards capital projects where Stirling

Council has met the conditions that would otherwise require repayment of the monies, but the monies have yet to be applied to

meet expenditure.

Balance Sheet

The Balance Sheet represents a snapshot of Stirling Council’s overall financial position as at 31 March 2017. It brings together

the year-end balances of all Stirling Council's accounts and presents money owed to and by the Council, assets owned and the

Page 8 of 75

balances and reserves at the Council's disposal. The overall net assets of Stirling Council reduced by £88.1m from £263.6m to

£175.5m in 2016-17.

The significant changes in the Balance Sheet were a £13.9m increase in the value of Property, Plant & Equipment (PPE) assets, a

£5.1m decrease in cash and cash equivalents and an increase in the local government pension scheme liability of £99.6m.

Pension Liability

Under International Accounting Standard 19 (IAS19), Stirling Council is required to disclose information regarding the pension

fund assets and liabilities of the Local Government Pension Scheme. Hymans Robertson, an independent firm of actuaries, has

calculated a net liability position on the Scheme as at 31 March 2017, with Stirling Council’s share being £315.821m. This

represents an increase of £99.592m when compared with the net liability position of £216.229m as at 31 March 2016.

The increase in the net liability position is principally due to an decrease in the net discount rate for the year to 31 March 2017,

which is used to place a value on the pension fund liabilities. The negative impact of the decreased discount rate on pension

fund liabilities however, has been partially offset by an increase in pension fund assets.

Employer’s contributions to the pension fund during 2016-17 were charged at 21% of total pensionable employee pay in line

with actuarial advice. The actuary has recommended an annual increase of 0.5% for 2017/18 following the most recent formal

fund valuation at 31 March 2014.

Borrowing

During 2016-17, the level of short-term temporary borrowing undertaken by Stirling Council reduced by £4.9m from the

previous year. New long-term borrowing of £12.0m (average rate 1.97%) was undertaken from the Public Works Loan Board

(PWLB) to replenish maturing loans and support the Council’s capital financing requirement. New loans of £3.119m were also

drawn from the UK Green Investment Bank Ltd arrangement to support energy efficient street lighting projects.

Overall, Stirling Council maintained its under-borrowed position and, consistent with the approved strategy for the year,

achieved this by giving priority to internal borrowing and short-term temporary borrowing. The strategy of effectively delaying

new long-term borrowing by prioritising internal and temporary borrowing has served well at a time when comparatively

cheaper temporary borrowing is readily available, counterparties meeting the investment criteria are limited and historically low

investment returns generate potentially significant carrying costs for any new long-term borrowing undertaken.

The Local Authority (Capital Finance & Accounting) (Scotland) Regulations 2016 came into force on 1 April 2016 to replace the

statutory provisions for local authority borrowing, lending and loans fund as set out in Schedule 3 of the Local Authority

(Scotland) Act 1965 and Finance Circular 29/1975. The change in legislative basis from the prescriptive approach of the 1975 Act

to a general power to borrow and a requirement maintain a statutory loans fund in accordance with proper accounting practices

and prudent financial management represents a change in accounting policy. The Council’s Treasury Management Financial

Strategy 2017/18 set out the Council’s intention to continue to use the Statutory Method during the transition period.

Property, Plant & Equipment Assets

During 2016-17, the overall valuation of Property, Plant & Equipment assets owned by Stirling Council increased by £13.9m.

Expenditure of £39.7m on new assets was partially offset by an annual depreciation charge of £27.8m.

The Council had anticipated the introduction of the Highways Network Asset Code on 1 April 2016, the provisions of which

required the Highways Network Asset to be measured at current value i.e. depreciated replacement cost instead of historic cost.

However, at it’s meeting on 8th March 2017, the CIPFA/LASAAC Board decided not to proceed with the introduction of this code

into the financial reporting requirements for local authorities. The Board decided that in the absence of central support for key

elements of the valuation, the costs of implementation outweighted the benefits and determined that further consideration to

this issue would be subject to clear evidence that benefits outweighted costs for local authorities.

Group Accounts

Stirling Council has a controlling interest in a number of companies and joint ventures, which were set up to promote

partnerships between the public and private sectors. After consolidation, the Group Balance Sheet shows a reduction in reserves

and net assets (excluding minority interests) of £5.949m or 3.39% from those reported in Stirling Council’s Balance Sheet (2015-

16, £5.179m, 1.96%). Details of the consolidated Group Accounts of Stirling Council can be found on pages 64 to 71.

Financial Indicators

The Chartered Institute of Public Finance and Accountancy (CIPFA) Directors of Finance Section recommends the inclusion of

certain “financial ratios” in the Management Commentary to assist the reader to assess the performance of Stirling Council over

the financial year and the affordability of its ongoing commitments. The following table provides the indicators with an

explanation of each, grouped into CIPFA categories for the various areas of financial activity.

Financial Indicator Commentary Restated 2015-16 2016-17

Uncommitted general fund

reserve as a % of annual net

budget

Reflects the amount of funding available to

manage unplanned events.

4.9% 4.0%

In year council tax collection Reflects Stirling Council’s effectiveness in

collecting council tax debt.

97.69% 97.75%

Page 9 of 75

Financial Indicator Commentary Restated 2015-16 2016-17

Council Tax funding to overall

level of funding

Reflects to overall percentage of Stirling Council

funding from local taxation.

19.8% 20.0%

Actual outturn compared to

budgeted expenditure

How closely expenditure compares to the

budget is a reflection of the effectiveness of

financial management.

98.96% 100.9%

Capital financing requirement Reflects Stirling Council’s underlying need to

borrow.

£256.948m £256.955m

External debt levels The actual external debt and long term liabilities

of Stirling Council. This should never exceed

Stirling Council’s authorised limit.

£215.976m £217.385m

Ratio of finance costs to net

revenue stream

This is a measure of how affordable Stirling

Council’s capital plans are. It takes actual finance

costs as a % of net revenue spend.

GF

10%

GF

10%

HRA

18%

HRA

17%

Impact of capital investment

on council tax and housing

rents

This measures the impact of capital investment

decisions on Stirling Council’s bottom line. The

figures shown are council tax per band D

household and housing rents per week/per

house.

Council Tax

£11.59

Council Tax

£9.97

Housing Rent

£11.86

Housing Rent

£11.67

4. Looking Forward - Five Year Business Plan

Executive Summary

Stirling Council’s vision is to be bold, ambitious and community led, delivering quality services with customer focus, tailored to

the different needs of our communities.

Overall, the Council will invest in the region of £200m per annum across services throughout urban and rural Stirling.

The rolling Five Year Business Plan identifies the different factors that impact on the development and delivery of services. It

outlines the activities and initiatives the Council plans to undertake to achieve our strategic vision for the Stirling area.

The Council has put in place a number of strategies and plans designed to support sustainable growth and diversification of

Stirling’s economy and deliver high-impact projects. Key to this will be building on the City Region Deal which will position

Stirling as a vibrant economic centre benefiting the whole of the region.

The Council continues to be committed to improving the way it engages with employees, residents and other key stakeholders

from the public, private and voluntary sectors and to developing and modernising the way we deliver services to better meet

the needs of our communities. To achieve this, we will develop with communities a different approach to delivering services

which are closer to the needs of localities, with 2017 seeing us embark on the next phase of our work to support communities to

test out new ways of moulding the delivery of their services per the priorities of those living and working within the area.

The Five-Year Business Plan will be reviewed every year and updated in line with changes in the Council’s priorities and any

relevant external factors. It is supported by our priority-based approach to budgeting and a five year strategic workforce plan.

Strategic Priorities

Stirling Council is committed to ensuring the best possible outcomes for everyone who lives, works and visits the Stirling area. By

October 2017, Stirling Council and our community planning partners need to have a Local Outcome Improvement Plan (LOIP) in

place which will set out a clear and ambitious vision for the Stirling area, identifying how we will work to support communities

who are experiencing the poorest outcomes through locality plans.

The LOIP will build on our Single Outcome Agreement (SOA) 2013-23, which developed seven outcomes based on evidence and

priorities gathered from consultation with communities and partners:

• Improved outcomes in children’s early years;

• Improved support for disadvantaged and vulnerable families and individuals;

• Communities are well served, better connected and safe;

• Reduced risk factors that lead to health and other inequalities;

• Improved opportunities for learning, training and work;

• A diverse economy that delivers quality local jobs; and

• Improved supply of social and affordable housing.

Page 10 of 75

Key Priorities

To deliver the seven strategic outcomes, the Council has set out the following key priorities:

• Partnership - building a Community Planning Partnership that is democratically led with an engaged community and

works towards positive outcomes for Stirling;

• Welfare Reform - developing advice services that are fit to support people through the current round of welfare

changes by establishing an integrated service with voluntary sector leadership;

• Families - increasing the focus on early intervention to help families in need;

• Service Delivery - Examining and delivering more opportunities for improved models of service delivery;

• Regeneration - regenerating our most in-need communities to deliver a full range of positive social, environmental

and economic outcomes;

• Environment - adopting a pragmatic approach to sustainability that protects and enhances the local environment;

• Education - improving the outcomes for the lowest performing 20 per cent of children in nurseries and schools and

providing additional nursery and out of school care places throughout the Stirling area to support working families;

• Roads - making resurfacing roads, paths and pavements the service priority across the whole Stirling area;

• Housing - building more socially rented housing;

• Corporate Parenting - being a good corporate parent;

• Digital Connectivity - delivering and improving upon access to and speed of, internet access across the Stirling area;

• Older People - improving care for our vulnerable people at home;

• Economy - streamlining business support under the leadership of the business community;

• Sport - promoting opportunities and supporting access to physical activity and sport for all;

• Business - pursuing a diverse high wage economy that delivers local jobs for people across Stirling and a procurement

policy that supports this;

• Enforcement - ensuring enforcement action is taken across all areas of Council activity and making full use of Council

policy to combat anti-social behaviour;

• Finance - our financial strategy will reflect the current economic challenges by making savings while ensuring the

delivery of quality services.

The Next Five Years

Stirling has a bold ambition and a once-in-a-generation opportunity to reposition itself as an economic and cultural powerhouse.

We are ready to do this, with the backing of our local communities, elected representatives, City Commissioners and Community

Planning Partners. Our unique, collaborative and evidence-based approach has identified the programmes to support us to do

this, including our approach to organisational transformation, our City Region Deal and our localities programmes.

Stirling Council will face significant changes and challenges over the next five years that will impact on the way we operate.

These changes are being driven by policy and financial, legislative and demographic factors.

The Council will continue to respond to an increasingly challenging economic environment by seeking innovative and effective

ways of delivering high-value services in partnership with our residents and communities.

There are also opportunities, particularly around sustainability, reducing carbon and the use of smart technology - in the next

five years we can expect to see better use of renewables for heat and energy and greater use of technology to make our services

more efficient and help inform our future decision making.

Genuine partnership lies at the heart of our people and place plans in the City Region Deal programme. This sets out a robust

and compelling case for transformative and sustainable economic growth that benefits everyone across the area and closes the

gap between the most advantaged and disadvantaged in our communities. Spanning skills and employability, social innovation,

marketing, inward investment and infrastructure projects, the programme aims to create local jobs and a stronger economy

across urban and rural areas, while promoting health and attainment and driving growth in key areas of the economy.

Capital investment by the Council is important in facilitating further investment in the area, thereby contributing to economic

growth. The Council intends to broaden its outlook on alternative means of financing and funding investment and leverage

additional investment where appropriate.

Stirling Council will be refining our ten-year Capital Programming to align it with the City Region Deal negotiations and to ensure

that asset management, infrastructure planning and the Council’s key priorities tie together within a sustainable and affordable

capital programme.

It is important that the Council is clear about how services will be structured and managed. Alternative models of service

delivery may emerge which complement and enhance what we currently do. Any developments will be considered in the

context of current service provision and delivery, the requirements of the people who use the services and the changing

expectations of the wider public.

The Council also recognises the different roles that our urban and rural communities play, acknowledging that there isn’t a “one

size fits all” approach. In line with the Community Empowerment (Scotland) Act 2015, the development of a localities based

approach to service delivery will allow the Council and partners to deliver alternative ways of working which complement the

needs and priorities of different communities.

Page 11 of 75

The Council needs a more tailored approach to deliver this opportunity, acknowledging that the scope for refining services may

be more limited for some than others. The Council will be structured and managed accordingly and will operate with a new set

of values and ways of working and our employees will play a key part in this.

The rolling five-year plan allows us the flexibility to adapt to these changes and taking this strategic approach enables us to

continue to deliver high quality services and ensure that only the most appropriate savings are made.

How we deliver this plan reflects the Council’s priorities, political imperatives and local circumstances. Councilors will determine

the principles and direction of this plan and the Chief Executive and Corporate Management Team are accountable for its detail

and delivery.

To meet the agreed priorities of Stirling Council, we have created a set of key messages and goals to focus our work as follows:

• Be Community Led - design and deliver services that respond to the needs and priorities of our diverse communities

and empower them to play a greater role in service delivery.

• Be One Council: One Team - address service provision in a collaborative manner, with no artificial or perceived

boundaries.

• Be a Learning Council - work with and learn from each other and our partners, sharing knowledge and best practice to

meet current and future challenges.

• Be Risk Aware: Not Risk Averse - take innovative and new approaches to service delivery, being aware of risks rather

than being risk averse.

• Be Open and Responsive - engage and communicate effectively and meaningfully with communities, employees and

partners.

Influences Over The Next Five Years

Stirling Council will continue to face significant changes and challenges over the next five years that will impact the way the

Council operates. These changes will be driven by economic, financial, technological, political direction and public policy factors.

Economic Influences

• Stirling has lower levels of unemployment than Scotland as a whole, however 2,200 people in the area are looking for,

but cannot find a job at any one time.

• Stirling has lower rates of economic activity, higher rates of economic inactivity and lower rates of employment than

Scotland as a whole.

• The numbers of people of working age in Stirling whose long term conditions affect their lives are almost as great, as

those over the age of 65 with similar conditions.

• Resident earnings are higher than workplace earnings.

• Business birth rates are still relatively high compared to Scotland, but other cities are catching up and overtaking

Stirling.

• The ratio of jobs to working population is falling.

• Retail spend is falling - 40% of resident spend is outside of Stirling.

• Gross value added (GVA) per head is behind Scotland, Glasgow and Edinburgh.

• A successful City Region Deal will see us gain the financial investment necessary to deliver a programme of change for

Stirling that will unlock our full potential and result in a healthier, wealthier, greener and better connected future for

Stirling, Scotland and the UK. The programme will benefit everyone who lives, visits, works and invests in Stirling and

beyond by permanently boosting GVA, creating 3,000 additional jobs, ensuring sustainable growth across all areas,

closing gaps in attainment and health inequalities, increasing Foreign Direct Investment, increasing overseas exports,

benefitting all citizens through work and skills programmes and increasing tourism by 25 per cent.

Financial Influences

• It is anticipated that there will be continued financial pressure on our government grant.

• Councils will have the ability to increase council tax, following a nine-year period of council tax freeze.

• There will be increasing service delivery costs.

• Pension and salary costs will increase.

• Localities financing has still to be addressed.

The Council will also be considering how we can involve local communities in our budgeting processes and notes the success of

participatory budgeting elsewhere in the world.

Technological Influences

• Stirling has one of the highest levels of internet connectivity in Scotland, but investment in broadband infrastructure is

required to enable communities and business across the area.

• Approximately 20% of households do not have access to superfast broadband and are relying on slower services. The

Government’s broadband scheme is targeted to reduce this to 6% of households by 2018 and further investment is

required beyond this programme.

• Many rural properties and those not included in the first phase of the Government programme do not have any access

to broadband connections. The next phase is targeted to be completed by 2021.

Page 12 of 75

• In early 2017, Stirling became Scotland’s fourth Gigabit City in order to deliver high speed connectivity which will

encourage economic growth and inward investment within the City. Construction will commence in June 2017.

• Improving digital engagement with our citizens, businesses and visitors through a new website offering an enhanced

range of online services transforming the way we do business.

• By pursuing a cloud-based strategy for our business systems we will ensure that our staff are able to work in a more

mobile and flexible manner, as well as improve information sharing to better equip and support our staff in their work.

• Developing more joined up technologies to validate and quality check we have the correct and most up-to-date

information on all our communities.

• Stirling is developing its smart capability through the Smart Cities programme with other Scottish cities. Over the next

two years, Stirling will develop solutions around smart energy systems, smart waste, mobility, intelligent street lighting

and greatly enhance not only our data capability but how we use that data.

Political Direction and Public Policy

• A new administration following the Scottish local government elections in May 2017. A snap General Election in June

2017.

• Public service reform will place expectations on the public sector to share budget and resources.

• The Community Empowerment (Scotland) Act 2015 was issued by the Scottish Government on 25th October 2016.

This replaces the current Single Outcome Agreement with the expectation that a Local Outcome Improvement Plan

(LOIP) will be in place for October 2017.

• Community Justice (Scotland) Act 2016 was passed by the Scottish Parliament on 11th February 2016 and sees the

establishment of a national body - Community Justice Scotland - on 31st March 2017. The arrangements for local

strategic planning and delivery of community justice will be undertaken with local community planning partners.

• The Integration Joint Board (IJB) responsible for the delivery of adult health and social care services was implemented

from 1st April 2016. The Chief Officer is in post and has financial responsibility for the joint budgets across the three

partners - Clackmannanshire Council, Stirling Council and NHS Forth Valley. The Partnership approach also includes

third and independent sectors.

• Effective community planning arrangements are at the heart of public service reform and Single Outcome Agreements

will be replaced by Local Outcome Improvement Plans (LOIP) and Locality Plans. This will commit our community

planning partners to an evidence-based approach to determining priorities and tackling inequalities, which will focus

on putting communities at the heart of everything we do and provide clearer focus on early intervention and

prevention to achieve both financial stability and improve outcomes.

Community Engagement

The Scottish Government introduced new revised national standards for community engagement which were launched in

September 2016. These are good practice principles designed to support and inform the process of community engagement and

improve what happens as a result.

The Community Empowerment (Scotland) Act 2015 has a specific focus on promoting effective engagement and participation to

help communities achieve greater control and influence in the decisions and circumstances that affect their lives. The national

standards for community engagement are important in supporting organisations in putting the Act into practice , they can be

used to shape the participation process used by public bodies as well as shape how community organisations can involve wider

communities of interest.

The key aspects of the national standards are inclusion, support, planning, working together, methods and communication.

These will allow us to assess the impact of engagement and use what has been learned to improve our future community

engagement.

Priority Based Budgeting

Over the last few years Stirling Council has been developing and strengthening its approach to Priority Based Budgeting (PBB).

The five year budget that supports this business plan takes account of extensive communication and community engagement,

including:

• The publication of a draft report with an improved format based on Engagement Sounding Board input which allowed

greater time for comment and feedback.

• Whole Council and service-led workforce briefings, informal drop-in sessions and colleague conversations.

• Five community conversations in November and December 2016 to share options and gather comments, questions

and suggestions.

• A public survey held in January/February 2017 asking people what they think the Council could do differently.

• A contact point at [email protected] where people could provide comment, questions and

suggestions on the process.

• The publication of a priority based budgeting report outlining proposals for PBB4 (2017/18).

Our aim throughout the community engagement exercises has been to connect with communities and ensure they have

sufficient opportunity to influence the budget process. The Council will continue to have open and meaningful dialogue with

employees, residents and key stakeholders throughout this process.

Page 13 of 75

We will also work hard to improve awareness and understanding of all the Council’s activities and services and encourage

increased participation and engagement across the board. We will then build on this engagement with urban and rural

communities, our partner organisations and staff.

Stirling Council is also currently developing an approach which will help it move towards much more participatory budgeting.

Management of Risks

Risk Management processes have been embedded across Stirling Council to manage risks that might impact on the delivery of

the Five Year Business Plan.

The Service Risk Registers contain operational risks and are managed by each Service Management Team. The Resilience and

Risk Team and Corporate Risk Group provide further scrutiny of Service Risks. Service risks with a score above 15 (red) are

reported to Audit Committee. Significant Service risks can be escalated to the Strategic Risk Register.

The Strategic Risk Register is managed by the Corporate Management Team which provides assurance through scrutiny and

challenge at a senior level and ensures that the significant risks facing the Council have been identified and effective treatment

actions implemented that reduce these risks to acceptable levels. It is maintained by the Resilience and Risk Team Leader and

submitted to the Corporate Management Team, prior to Audit Committee, for discussion and monitoring. The Strategic Risk

Register is reported to each Audit Committee which provides effective scrutiny and challenge as part of the Council’s corporate

governance arrangements.

Strategic Workforce Plan

The Strategic Workforce Plan is strategically aligned to the Council’s Five Year Business Plan and the Priority Based Budgeting

(PBB) process. The Plan captures the implications of the Council’s ongoing process of transformation, while providing

information on the current workforce and setting out a strategy to ensure the Council’s outcomes and priorities are delivered.

Taking into consideration the common themes emerging from individual service and corporate business plans and with regard

to the financial landscape, the following strategic workforce priorities are proposed for the period 2017 to 2022:

• Strengthen the linkage between business, financial and strategic workforce planning.

• Continue to embed a culture of customer-focused, high performance across the Council.

• Maximise employee engagement, creating a working environment where everyone can have a rewarding and

enjoyable working life.

• Work together with our trades unions, striving for positive industrial and employee relations.

• Develop the working environment and the promotion of a health, safety and wellbeing culture.

• Manage required changes to the workforce in a structured, planned and fully consultative basis.

• Ensure that the Council’s status as an ‘employer of choice’ is enhanced and that the principle of equal opportunities is

evident in all aspects of the Council’s employment processes.

• Focus on increasing the diversity of the workforce over the next five years.

• Increase the number of training, apprentice, graduate and talent management opportunities and help everyone to

develop skills to excel in their performance and move towards their life and career goals. This includes supporting the

Corporate Parenting and employability pipeline.

• Ensure attendance management levels equate to upper quartile performance standards.

• Ensure high level management performance across the Council through robust selection processes and tailored

development programmes.

• Measures will be developed as part of the Organisational Change programme to align major strategies, including

digital, customer and technology and locality programmes.

Delivering on these priorities will contribute significantly to fulfilling the Five Year Business Plan aspiration to have a “flexible,

skilled and motivated workforce”. Staff will operate effectively if they feel valued, have a clear role to play and can see the

results of their efforts. Workforce planning is an on-going process and the Plan will continue to evolve to match the objectives

and aspirations of Stirling Council.

Council Performance Management Framework

Stirling Council's Performance Management Framework is the method by which the Council plans and prioritises, monitors and

manages performance and undertakes reviews and improvement activities as part of the Five Year Business Plan. The

Framework is shown in the diagram that follows and includes the following sections:

• Planning and Prioritising - details of Stirling Council's main strategic plans and priorities.

• Reporting and Managing - the latest performance information and analysis showing Stirling Council's performance

over time and in comparison with other local authorities.

• Reviewing and Improving - details of how Stirling Council reviews progress and identifies its strengths and areas for

improvement.

Page 14 of 75

Jim Boyle CPFA

Chief Finance Officer

31 August 2017

Stewart Carruth

Chief Executive

31 August 2017

Scott Farmer

Leader of the Council

31 August 2017

Page 15 of 75

Statement of Responsibilities

The Authority’s Responsibilities

The authority is required to:

- Make arrangements for the proper administration of its financial affairs and to secure that the proper officer of the

authority has responsibility for the administration of those affairs (section 95 of the Local Government (Scotland)

Act 1973). In this authority, that officer is the Chief Finance Officer, Corporate Operations.

- Manage its affairs to secure economic, efficient and effective use of resources and safeguard its assets.

- Ensure the Annual Accounts are prepared in accordance with legislation (The Local Authority Accounts (Scotland)

Regulations 2014) and so far as is compatible with that legislation, in accordance with proper accounting practices

(section 12 of the Local Government in Scotland Act 2003).

- Approve the Annual Accounts for signature.

I confirm that these Annual Accounts were approved for signature by the Audit Committee at its meeting on 31 August 2017.

Signed on behalf of Stirling Council.

Scott Farmer

Leader of the Council

31 August 2017

The Chief Financial Officer’s Responsibilities

The Chief Finance Officer is responsible for the preparation of the authority’s Annual Accounts in accordance with proper

practices as required by legislation and as set out in the CIPFA/LASAAC Code of Practice on Local Authority Accounting in the

United Kingdom (the Accounting Code).

In preparing the Annual Accounts, the Chief Finance Officer has:

- Selected suitable accounting policies and then applied them consistently.

- Made judgements and estimates that were reasonable and prudent.

- Complied with legislation.

- Complied with the local authority Accounting Code (in so far as it is compatible with legislation).

The Chief Finance Officer has also:

- Kept adequate accounting records which were up to date.

- Taken reasonable steps for the prevention and detection of fraud and other irregularities.

I certify that the financial statements give a true and fair view of the financial position of the local authority and its group at the

reporting date and the transactions of the local authority and its group for the year ended 31 March 2017.

Jim Boyle CPFA

Chief Finance Officer

31 August 2017

Page 16 of 75

Annual Governance Statement

Scope of Responsibility

Stirling Council is responsible for ensuring that its business is conducted in accordance with the law and proper standards, and

that public money is safeguarded, properly accounted for, and used economically, efficiently and effectively. The Council also

has a statutory duty, under the Local Government in Scotland Act 2003, to make arrangements to secure best value through

continuous improvement in performance of its functions. Elected Members and the Corporate Management Team are

responsible, in discharging those responsibilities, for putting proper arrangements in place for the governance of the Council’s

affairs, and for facilitating the effective exercise of its functions, including risk management arrangements.

This assurance statement relates to the governance framework in place within the Council for the year ended 31 March 2017,

and up to the date of signature of the Council’s Annual Accounts for 2016-17.

The Council approved and adopted its Local Code of Corporate Governance (‘the Code’) in December 2013. The Code is

consistent with the six principles of the CIPFA and SOLACE Delivering Good Governance in Local Government Framework. It also

incorporates the requirements of CIPFA’s Statement on The Role of the Chief Financial Officer in Local Government. A copy of

the Code is on our website at www.stirling.gov.uk, or can be obtained by writing to: The Chief Governance Officer, Stirling

Council, Old Viewforth, Stirling FK8 2ET.

This Annual Governance Statement explains how the Council has complied with the Code and complies with the CIPFA Code of

Practice on Local Authority Accounting in the United Kingdom: Guidance Notes for Practitioners 2016-17, which details the

requirements for an Annual Governance Statement. It also complies with the Delivering Good Governance in Local Government

Framework and Guidance Notes, and the Local Authority Accounts (Scotland) Regulations 2014, both of which require the

Council to conduct an annual review of the effectiveness of its system of internal control, to consider and report the findings of

that review, and to approve an Annual Governance Statement, signed by the Chief Executive and Council Leader.

The Governance Framework

The governance framework comprises the systems, processes, culture and values by which the Council is directed and

controlled, and the activities through which it accounts to, engages with, and leads its communities. It enables the Council to

monitor achievement of its eighteen key priorities, published in the Council’s Five-year Business Plan. It also enables the Council

to consider whether those objectives have led to the delivery of appropriate value for money.

The Council’s system of internal control is a significant part of the governance framework and is designed to manage risk to a

reasonable level. Internal control cannot eliminate all risk of failure to achieve policies, aims and objectives, and can therefore

only provide reasonable and not absolute assurance of effectiveness. The system of internal control is based on an ongoing

process designed to identify and prioritise the risks to the achievement of policies, aims and objectives; to evaluate the

likelihood of those risks being realised and the impact should they be realised; and, to manage those risks efficiently, effectively

and economically.

The Council’s governance framework is set out in the Local Code of Corporate Governance, which aims to:

• give an overview of the governance arrangements in operation within the Council;

• provide assurance that the Council’s business is run lawfully, accountably and openly; and,

• provide the Council with a focus for self-assessment of its governance arrangements.

The Council maintains organisational and management structures to ensure it has the right capacity, competencies, behaviours

and governance arrangements to address future opportunities and challenges, including a greater emphasis on: community

planning and engagement; health and social care integration; a strategic infrastructure plan; changing customer demands; and,

ongoing financial challenges.

The Council structure underpins a flexible partnership delivery approach based on community priorities and outcomes. The

Council keeps its decision-making and delegation arrangements, and its organisational structure, under regular review to

support the delivery of its key priorities and objectives. The Council endorsed a revised organisational and management

structure on 19 May 2016, in line with earlier Council decisions, and delegated authority to the Chief Executive to implement the

approved structure.

The Council’s current decision-making structures include:

• a Community Planning & Regeneration Committee • an Education Committee

• an Environment & Housing Committee • a Finance & Economy Committee

• a Public Safety Committee • a Social Care & Health Committee

Page 17 of 75

The Council also has an Audit Committee that is chaired by the Leader of the Opposition.

The Council considers that the senior management, decision-making and scrutiny arrangements are aligned appropriately to its

eighteen key priorities, and provide an effective framework through which it can direct and control its activities, and scrutinise

its performance in delivering these. The other key elements of the corporate governance framework are:

• a Five-year Business Plan that sets out The Council’s vision and key corporate priorities and supports the actions required to

deliver the agreed priorities under the Single Outcome Agreement. The Single Outcome Agreement and Five-year Business

Plan are published on the Council’s website;

• Outcomes for Stirling, the Single Outcome Agreement for 2013-2023, was agreed by the Council, Community Planning

Partners and the Scottish Government. It sets out the shared objectives of the Council and its Community Planning Partners,

and details their vision, strategic priorities and intended outcomes for the Stirling area, its citizens and service users;

• governance arrangements for the Single Outcome Agreement during 2016/17 included a Leadership Group to perform the

functions of the Community Planning Partnership (CPP) Board, to lead the Partnership and be responsible for its

effectiveness, and sub-groups responsible to the Leadership Group for delivery of specified priorities;

• the Priority Based Budgeting (PBB) process, which underpins the Five-year Business Plan and Strategic Workforce Plan,

enabling the Council to manage expected future costs and service demands, aligning service delivery and transformation to

address those demands and deliver best value from available resources;

• governance arrangements for Strategic Transformation and Priority Based Budgeting (PBB) savings options, including

Thematic and Subsidiary Boards to oversee the co-ordination, prioritisation and delivery of PBB projects;

• formal arrangements to support and engage with Local and Area Community Planning Groups through the three Area

Community Planning Forums, and to support and engage with Community Councils, ensuring that the service needs and

priorities of local communities are identified and can influence Council policy and services;

• a performance management framework, incorporating internal and public performance reporting, that enables the Council

to regularly report performance in achieving its key objectives. Performance reports include the Annual Report and

Accounts, and Performance and Strategic Priorities Progress Reports: these are published on the Council’s website and in

Council or Committee agenda papers;

• presentation of reports, including findings and recommendations, to the Corporate Management Team, Audit Committee

and Council, where appropriate, by Internal Audit, external audit, and other inspectorates;

• Standing Orders, Contract Standing Orders, Schemes of Delegation and Financial Regulations, which define the roles and

responsibilities of Elected Members and officers, and are subject to regular review

• the overall responsibilities of:

• the Chief Executive, as the Head of Paid Service, for all aspects of operational management;

• the Chief Finance Officer for keeping proper financial records, maintaining an effective system of internal financial

control, and ensuring appropriate advice is given to the Council on all financial matters;

• the Chief Governance Officer, as statutory Monitoring Officer, for ensuring appropriate advice is given to the Council

on corporate governance arrangements, and for ensuring compliance with relevant legislation and procedure;

• the Audit Manager, as set out in the Internal Audit Charter, to review, appraise and report to management, the Audit

Committee and the Council on the adequacy of internal control and corporate governance arrangements and on risks

relating to approved policies, programmes and projects;

• an Audit Committee that provides the Council with independent assurance of the adequacy of the governance and risk

management frameworks and the internal control environment, including through an annual report;

• an approved Risk Management Policy and Procedures that sets out the responsibilities of Elected Members, the Audit

Committee, management and staff for the identification and management of risks to the key corporate priorities;

• a Council-wide Strategic Risk Register and Service Risk Registers, which identify risks and treatment actions, are regularly

reviewed, updated and reported to the Audit Committee and the Corporate Management Team

• Business Impact Assessment & Recovery Plans are in place to set out arrangements for service continuity in the event of an

emergency or other disruption to critical services;

• formal objectives for staff, including senior management, which are subject to review through the Council-wide Personal

Review & Development (PRD) process;

• a Register of Members’ Interests and a Register of Officers’ Interests (for senior officers) are maintained and made available

for public inspection;

• a ‘Members’ Remuneration and Expenses Scheme’ which is consistent with Scottish Government– guidance. Information on

the amounts and composition of Elected Members’ salaries, allowances and expenses is published on the Council website;

Page 18 of 75

• induction training on roles and responsibilities, and ongoing development opportunities, are provided for Elected Members;

• codes of conduct that set out the standards of behaviour expected from Elected Members and officers, including the

Councillors’ Code of Conduct and the Code of Ethical Standards for officers;

• an Anti-Fraud & Corruption Strategy sets out the responsibilities of officers and Elected Members in relation to fraud and

corruption, and is reinforced by the Public Interest Disclosure (‘Whistleblowing’) Policy, the codes of conduct and the

Financial Regulations;

• an Integrity Group, which manages and co-ordinates the corporate response to the Scottish Government’s Serious

Organised Crime Strategy and national Prevent Duty guidance;

• an Information Management Group contributes to, and has oversight of, strategy, policy and procedures to promote the

effective management of information throughout its lifecycle; and,

• a Local Code of Practice on Following the Public Pound & Funding External Bodies, and arrangements for appointments of

Members and Officers to Boards or management groups of group entities, to ensure proper accountability for Council funds

used in the external delivery of services to meet strategic priorities and objectives.

Review of Effectiveness

The Council is responsible for conducting, at least once in each financial year, a review of the effectiveness of its governance

framework, including the system of internal financial control. The review of the effectiveness of the Council governance

framework is informed by:

• the work of the Corporate Management Team, which develops and maintains the governance environment;

• the work of Council managers and finance staff;

• the annual assurance statements on governance arrangements that are provided by Directors;

• an annual review, by Internal Audit, of compliance with the Council’s Local Code of Corporate Governance;

• the Audit Manager’s annual report and internal audit reports across the range of Council services;

• reports from the Council’s external auditor; and,

• reports from other external review bodies, agencies and inspectorates.

The annual review of effectiveness is supported by a process of self-assessment and assurance certification by Directors and

Senior Managers, including completion of an Assurance Checklist covering the key elements of the governance framework. As

part of this process, they were asked to identify progress on implementing improvement actions identified as part of the 2016-

17 assessments, and to identify actions they proposed to take during 2017-18.

The Audit Manager considered the completed assurance checklists, certifications and improvement action plans from each

Service, and concluded that:

• these did not highlight any issues that would impact on the level of assurance over the effectiveness of the Council’s

governance framework;

• Services had identified areas for improvements to the current governance framework, focussing on:

� strengthening Service planning, data management, risk management, and performance management;

� improving procurement capacity and capability, and cyber threat arrangements;

� undertaking training on key financial responsibilities and corporate fraud awareness;

� improving monitoring and management of the Council’s arms’ length organisations and partnerships; and,

� strengthening operational procedures to ensure these meet requirements of new legislation, in relation to privacy

impact assessments in particular.

• the proposed improvements did not indicate any significant gaps or weaknesses in the existing governance framework that

should have been addressed by Services.

Internal Audit has performed an annual review on the existence, appropriateness and application of the key elements of the

Local Code of Corporate Governance during the year to 31 March 2017, concluding that:

• the Code is consistent with CIPFA and SOLACE guidance on the Delivering Good Governance in Local Government

Framework and with the International Framework Good Governance in the Public Sector;

• the key governance arrangements and controls are clearly set out in the Code, and there is sufficient, clear, reliable and

objective evidence to provide assurance that these exist and are being applied in practice; and,

• there is scope to continue to develop and refine corporate governance arrangements. Internal Audit has made a small

number of recommendations for improvement, agreed with the Chief Governance Officer.

Page 19 of 75

In order to comply with the group accounting requirements of the Code of Practice on Local Authority Accounting in the United

Kingdom: Guidance Notes for Practitioners 2016-17, this Statement incorporates assurance on the governance arrangements

and systems of internal financial controls within the consolidated group entities of Stirling Council. The review of the

effectiveness of those arrangements for the year to 31 March 2017 is informed by:

• the work of those bodies’ respective external auditors (and, where relevant, internal auditors); and,

• the Annual Governance Statement included within the Statement of Accounts of Central Scotland Valuation Joint Board.

Roles and Responsibilities of the Audit Committee and the Head of Internal Audit

The Audit Committee is chaired by the Leader of the Opposition and operates in accordance with CIPFA’s Audit Committee

Principles in Local Authorities in Scotland and Audit Committees: Practical Guidance for Local Authorities. Its role includes:

• to review internal and external audit reports and the main issues arising, and seek assurance that action has been taken

where necessary;

• to receive and consider the Audit Manager’s annual report, summarising internal audit activity and the level of assurance

this provides over the arrangements for risk management, governance and internal financial control within the Council and

its group entities;

• to satisfy itself that the Council’s assurance statements, including the Annual Governance Statement, properly reflect the

risk environment and any actions required to improve it;

• to keep the Local Code of Corporate Governance under review and ensure arrangements for the publication of a statement

in the Council’s Annual Accounts confirming compliance with the Code; and,

• to review the Annual Accounts and to consider the external auditor’s report to those charged with governance on issues

arising from the audit of the accounts.

As required by the Public Sector Internal Audit Standards, the Audit Manager (as Head of Internal Audit) prepares an annual

Internal Audit Risk Assessment & Plan, and undertakes a programme of internal audit reviews that takes account of the risks

identified in the Council’s risk registers and Internal Audit’s own assessment of risk.

The Audit Committee approves Internal Audit’s planned programme of work and regularly monitors the performance of the

service. The Audit Manager provides an annual Statement of Assurance to the Audit Committee, containing his independent

opinion on the adequacy and effectiveness of the Council’s risk management, internal control and corporate governance

arrangements.

Internal Audit reports are provided to Elected Members, to management and to the external auditor. The reports include

improvement recommendations and agreed action plans to address these. Management is responsible for responding to those

reports and ensuring that appropriate action is taken. Significant matters, including any non-compliance with recommendations

arising from Internal Audit work, are reported to the Audit Committee.

Compliance with Best Practice

The Council complies with the requirements in CIPFA’s The Role of the Chief Financial Officer in Local Government. The Chief

Finance Officer has overall responsibility for the Council’s financial arrangements, and is professionally qualified and suitably

experienced to lead the Council’s finance function and to direct finance staff.

The Council complies with the requirements in CIPFA’s The Role of the Head of Internal Audit in Public Service Organisations

The Audit Manager has responsibility for the Council’s Internal Audit service, and is professionally qualified and suitably

experienced to lead and direct the Internal Audit team. The Internal Audit service operates in accordance with the Public Sector

Internal Audit Standards. The Council’s external auditor conducts an annual review of the effectiveness of the Council’s Internal

Audit Service and arrangements, and reports its findings to the Council within its Annual Audit Report.

Health & Social Care Integration: Clackmannanshire and Stirling Health & Social Care Partnership

The Public Bodies (Joint Working) (Scotland) Act 2014 (the Act) requires Local Authorities and Health Boards to integrate

planning and delivery of certain adult health and social care services. Stirling and Clackmannanshire Councils elected to form a

single body corporate with NHS Forth Valley. The Clackmannanshire and Stirling Health & Social Care Partnership was

established and became operational on 1 April 2016.

The Act required that each Health & Social Care Integration Joint Board (IJB) establish adequate internal audit arrangements to

support independent review of the adequacy of risk management, governance and control arrangements for the delegated

resources, including the appointment of a Chief Internal Auditor.

Page 20 of 75

The Clackmannanshire and Stirling IJB has agreed a rotational appointment across constituent bodies, and appointed Stirling

Council’s Audit Manager as the Chief Internal Auditor for the period up to 31 March 2019. The IJB has also approved the

establishment, membership and remit of its Audit Committee.

The Audit Manager, in his capacity as Chief Internal Auditor, provided information and reports to the IJB Audit Committee at