stochastic modeling workshop —policyholder behavior · douglas l. robbins november 19, 2003. 2...

TRANSCRIPT

Stochastic Modeling Workshop

— Policyholder Behavior

Southeastern Actuaries Conference

Marc N. AltschullDouglas L. Robbins

November 19, 2003

2

IntroductionIntroduction

Agenda

GMDB ResultsGMDB Results

GMIB ResultsGMIB Results

ConclusionsConclusions

IntroductionIntroduction

3

Objective

The results presented in this paper will enable insurers to better understand that policyholder behaviors need to be modeled in order to evaluate the volatility of results, using variable annuity guarantees as an example.

The results presented in this paper will enable insurers to better understand that policyholder behaviors need to be modeled in order to evaluate the volatility of results, using variable annuity guarantees as an example.

4

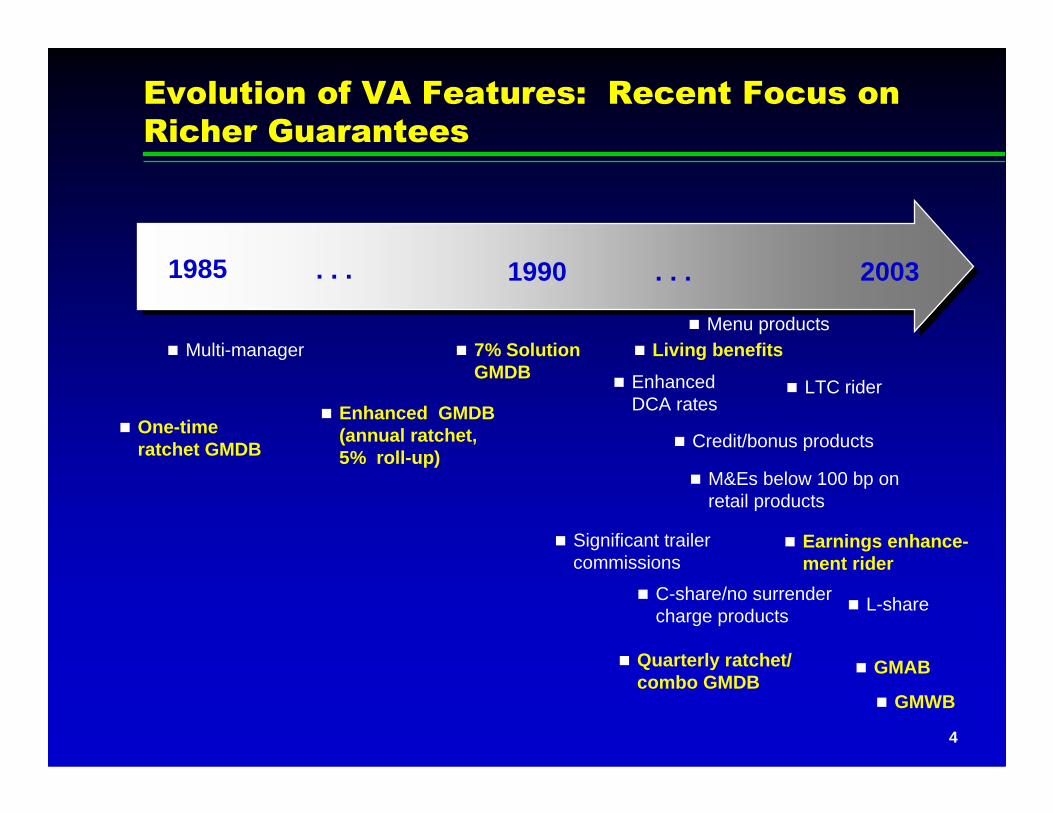

Evolution of VA Features: Recent Focus on

Richer Guarantees

� Multi-manager � 7% Solution GMDB

� Living benefits

� Credit/bonus products

� Significant trailer commissions

� Enhanced DCA rates

� LTC rider

� One-time ratchet GMDB

� M&Es below 100 bp on retail products

� C-share/no surrender charge products

� Enhanced GMDB (annual ratchet,5% roll-up)

1985 1990 2003. . . . . .

� Quarterly ratchet/ combo GMDB

� Menu products

� Earnings enhance-ment rider

� L-share

� GMAB

� GMWB

5

VA Sales Have Coincided with the Ebb and

Flow of the Equity Markets

400

600

800

1000

1200

1400

1600

1st Q

tr 9

5

1st Q

tr 9

6

1st Q

tr 9

7

1st Q

tr 9

8

1st Q

tr 9

9

1st Q

tr 0

0

1st Q

tr 0

1

1st Q

tr 0

2

1st Q

tr 0

3

S&

P 5

00

0

5

10

15

20

25

30

35

40

Qua

rter

ly G

ross

VA

Sal

es1

1 Annual sales for 1995 through 1999 distributed uniformly. Source: Variable sales from Tillinghast VALUE Survey, includes all non-pension variable annuitypremiums (first-year and renewal, separate account and fixed account).

6

Methodology

� Projected inforce deferred VA

� Issue date = one month prior to model start date

� Initial surplus = 0

� Annual surplus projected 20 years

� 500 stochastic scenarios

� Discount at after-tax, general account earned rate

� Total Capital Requirement = CTE 90

7

Guaranteed Benefits Considered

� GMDB� Greater of annual ratchet to age 80 and 5% premium

roll-up to age 80� Cost included in base product asset charges

� GMIB� 5% roll-up to age 80� 10-year waiting period for annuitization � 35 bps additional asset fee

8

Summary of Base Results

Guaranteed Benefits C3 Capital Requirement

GMDB Only 88 bps

GMDB and GMIB 91

9

Scenario Calibration Modifications

� Purpose: to determine sensitivity of results to scenario calibration

� 1% reduction in annual expected returns

� 120% multiplier on annual return volatility

10

Summary of Scenario Calibration Results

(Change from Base)

Guaranteed Benefits (Base)

1% Reduction in Expected Returns

120% Multiplier on Return Volatility

GMDB only (88 bps)

30 bps 27 bps

GMDB and GMIB (91 bps)

97 39

11

IntroductionIntroduction

Agenda

GMDB ResultsGMDB Results

GMIB ResultsGMIB Results

ConclusionsConclusions

12

GMDB Behavioral Assumptions

� Lapses

� Partial withdrawals� Dollar-for-dollar� Proportionate

� Transfers to the fixed account

� Transfers to a “safer” separate account fund

13

Assumption Change in C3 Requirement

Dynamic increasedlapsation in down markets

(13) bps

GMDB Dynamic Lapse Results (Changes from

base C3 requirement of 88 bps)

Dynamic lapse reductionover 20% of GMDB

25

Dynamic lapse reductionover 40% of GMDB

20

14

GMDB Deterministic Lapse Results (Changes

from base C3 requirement of 88 bps)

Assumption Change in C3 Requirement

200% lapse rates in allyears

(32) bps

50% lapse rates in allyears

31

200% lapse rates aftersurrender charge period

(4)

50% lapse rates aftersurrender charge period

9

15

Dollar-for-Dollar with Dynamic Partial

Withdrawals Increase C3 Requirement 217 bps

Base Dollar-for-Dollar

88 bps

305 bps

217

bps

Incr

ease

16

Dynamic lapses with transfers from SA to GA and 0% guarantee on GA

15

Dynamic lapses only 25

Assumption Change in C3 Requirement

Transfers from SA to GA (no dynamic lapses)

3 bps

Dynamic lapses with transfers from SA to GA

33

GMDB Transfers to Fixed Account Results

(Changes from base C3 requirement of 88 bps)

17

IntroductionIntroduction

Agenda

GMDB ResultsGMDB Results

GMIB ResultsGMIB Results

ConclusionsConclusions

18

GMIB Behavioral Assumptions

� GMIB utilization

� Lapses

� Transfers to the fixed account

� Transfers to a safer separate account fund

19

GMIB Utilization Assumption (Changes from

base C3 requirement of 91 bps)

12 bps

22 bps67 bps

vs.

Combination: Electionrate of 100% with max of 50%

Maximum annual GMIB election rate increased from25% to 50%

GMIB election rateincreased from50% to 100% of“in-the-moneyness”

20

Assumption Change in C3 Requirement

Dynamic Lapse Tests

Dynamic lapse reductionover 20% of GMIB

224 bps

Dynamic lapse reductionover 40% of GMIB

164

Deterministic Lapse Tests

200% lapse rates in all years (80)

50% lapse rates in all years 281

GMIB Lapse Assumption Results (Changes

from base C3 requirement of 91 bps)

21

Dynamic Lapses Amplify C3 Requirement

Sensitivity to GMIB Utilization

91 bps Base

22 bps

Maximum annual GMIB election rate increased to 50%12 bps

GMIB election rate increased to 100% of “in-the-moneyness”

No DynamicNo DynamicLapsesLapses

DynamicDynamicLapsesLapses

91 bps

224 bps Dynamic lapses

52 bps

36 bps

33 bps

Combination: Election rate of 100%

with max of 50%

60 bps

22

Negligible Impact of Transfers to the Fixed

Account: GMDB vs. GMIB

88 bps 91 bps

3 bps8 bps

GMDB GMIB

Base

Transfers fromSA to GA

(no dynamic lapses)

23

Transfers to a Safer Separate Account Provide

Counterintuitive Results

88 bps 91 bps

GMDB GMIB

(46) bps

Net C3Requirement

with No Dynamic Lapses42 bps 44 bps

Net C3Requirement

with No Dynamic Lapses135 bps

25 bps

224 bps

(42) bps

207 bps

Net C3Requirement

with Dynamic Lapses71 bps

Net C3Requirement

with Dynamic Lapses522 bps

Base

Transfersfrom

large cap to bonds

(no dynamiclapses)

Dynamiclapses

turned on,but no

transfers

Transferfrom large

cap tobonds

24

IntroductionIntroduction

Agenda

GMDB ResultsGMDB Results

GMIB ResultsGMIB Results

ConclusionsConclusions

25

GMDB Observations

� Certain behaviors can be comparable to moderate changes in economic scenarios for average issue ages

� Partial withdrawals on products with dollar-for-dollar GMDB reductions can be significant

� Behavioral changes in early policy durations dominate later durations for average issue age

� Moderate scenario changes dominate most behavioral changes for older issue ages

26

GMIB Observations

� Many behaviors influence C3 much more than moderate changes in economic scenarios

� Impact of behaviors compounds

� Late duration behaviors more important than with GMDB only