stock liquidity and corporate tax avoidance: the tale of ... · stock liquidity and corporate tax...

TRANSCRIPT

1

Stock Liquidity and Corporate Tax Avoidance: The Tale of Two

Tails

Yangyang Chen

Department of Banking and Finance

Monash University

Leon Zolotoy*

Melbourne Business School

University of Melbourne

First draft: May 2013

Current version: January 2014

ABSTRACT

We examine the relation between stock liquidity and corporate tax avoidance.

Utilizing a quantile regression framework for the comprehensive sample of US firms,

we document the following key results: (i) stock liquidity is positively (negatively)

associated with the lower (upper) tail of the tax avoidance distribution; (ii) the effect

of stock liquidity on both tails of tax avoidance distribution is stronger for firms with

high levels of business uncertainty; and (iii) the effect of stock liquidity on the lower

(upper) tail of tax avoidance distribution is mitigated (magnified) for the financially

constrained firms. Our findings are consistent with the positive feedback channel

where, by making share prices more informative to managers, greater stock liquidity

affects firm’s tax planning.

JEL Classification: G10, G30, M40.

Keywords: Stock liquidity; Tax avoidance; Information asymmetry; Financial

constraints; Positive feedback.

* Corresponding author. Address: 200 Leicester Street, Carlton VIC 3053. Email:

[email protected]. Tel: +61 3 9349 8424.

2

I. INTRODUCTION

Corporate tax avoidance has become a substantial issue in both finance and

accounting research in recent years. The statutory corporate tax rate in the United

States is one of the highest in the world. At the same time, there is striking variation

in corporate tax payments among U.S. firms. At one extreme, a substantial share of

profitable U.S. corporations pay very little or even no corporate taxes, which makes

some observers view corporate tax avoidance as the most important compliance issue

in the U.S. tax system today (Desai and Dharmapala, 2006). At the other extreme,

approximately one-fourth of U.S. firms pay corporate taxes in excess of the statutory

tax rate (Dyreng, Hanlon, and Maydew, 2008), suggesting that these firms engage in

little or no tax avoidance. Why do some firms pay little corporate tax while others pay

excessive levels? The determinants of corporate tax avoidance are still far from being

well understood, and are a fertile ground for further research in this important area

(Shackelford and Shevlin, 2001; Hanlon and Heitzman, 2010).

We examine the effect of stock liquidity on corporate tax avoidance. Two strands

of the previous literature motivate our research question. The first strand examines the

determinants of tax avoidance and its implications for shareholder wealth. Studies in

this stream of research view tax avoidance as an investment decision along the

continuum of tax planning strategies available to managers, where in equilibrium a

value-maximizing firm should invest in tax avoidance as long as marginal benefits of

tax avoidance exceed its marginal costs (Hanlon and Heitzman, 2010; Edwards,

Schwab and Shevlin, 2013). However, similar to other investment decisions,

3

managers may deviate from the optimal level of investment in tax avoidance (from

the shareholders’ perspective) by investing either “too little” or “too much” in tax

planning (Armstrong et al., 2013). On the one hand, overly-conservative tax

avoidance (that is, being in the lower end of the continuum of tax planning strategies)

results in loss of potential cash-savings (Graham and Tucker, 2006; Cheng et al.,

2012). On the other hand, overly-aggressive tax avoidance (that is, being in the upper

end of the tax planning continuum) facilitates managerial rent extraction (Desai and

Dharmapala, 2006; Kim, Li and Zhang, 2011), and may also result in additional

auditor fees, legal fines and reputational costs (Mills, 1998; Wilson, 2009; Graham et

al., 2013), and thus will erode shareholder wealth1.

A second strand of related literature examines the effect of stock liquidity on

firm’s investment decisions. Prior studies suggest that firm managers make

investment decisions that are contingent on the information revealed by the firm’s

stock price (e.g., Subrahmanyam and Titman, 2001; and Khana and Sonti, 2004), and

that the sensitivity of firm’s investments to stock price is increasing in stock price

informativeness (Chen, Goldstein and Weng, 2007). Greater stock liquidity facilitates

trading by informed traders (Easley and O’Hara, 2004), thereby making share prices

1 Prior studies provide empirical evidence consistent with investors perceiving both overly-

conservative and overly-aggressive tax avoidance as the value-destroying activities. For the overly-

conservative tax avoidance, Cheng et al. (2012) find that, relative to matched firms, businesses targeted

by hedge fund activists exhibit lower tax avoidance levels prior to hedge fund intervention, but

experience increases in tax avoidance after the intervention. For the overly-aggressive tax avoidance,

Hanlon (2005) document that investors perceive large book-tax differences (book income greater than

taxable income) as a “red flag” and reduce their expectations of future earnings persistence for these

firms. In a similar context, Hanlon and Slemrod (2007) find that, on average, a company’s stock price

declines when there is news about its involvement in tax sheltering.

4

more informative to managers and allowing firm management to make better

investment decisions, a so-called “positive feedback” effect (Fang, Noe, and Tice,

2009).2

High stock liquidity may also improve firm’s investment decisions through the

corporate governance channel. For instance, Maug (1998) shows that stock liquidity

facilitates the formation of larger blockholdings and more liquid trading by these

blocks, thereby enhancing blockholders’ voice and their ability to intervene.

Alternatively, stock liquidity may discipline managers by enhancing the threat of

blockholder exit, when managerial compensation is closely tied to firm’s stock price

(Edmans, 2009; Edmans and Manso, 2011; and Bharath, Jayaraman, and Nagar,

2013).

Collectively, prior research suggests that (i) tax avoidance is a part of firm’s

overall investment strategy, (ii) there are beneficial effects of stock liquidity on firm’s

investment decisions, and (iii) there are adverse implications of both overly-

aggressive and overly-conservative tax avoidance strategies for shareholder wealth.

Integrating these three sets of results, we posit that firms with high stock liquidity will

engage less in both overly-conservative and overly-aggressive tax avoidance, ceteris

paribus.

2 A positive feedback perspective rests on the premise that the extent of share price informativeness is

determined by stock liquidity, and not the other way around, consistent with what prior studies suggest

(e.g., Grossman and Stiglitz, 1980; Kyle, 1985; Easley and O’Hara, 2004; Chordia et al., 2008; and

Jayaraman and Milbourne, 2012). In particular, Chordia et al. (2008) document that liquidity Granger-

causes stock price informativeness, but find no statistical evidence of reverse causality.

5

Consistent with our predictions, we document a positive association between

firm’s stock liquidity and the lower tail of the conditional tax avoidance distribution,

which is symptomatic of firm’s underinvestment in tax avoidance. We also document

a negative association between a firm’s stock liquidity and the upper tail of the

conditional tax avoidance distribution, which is symptomatic of firm’s

overinvestment in tax avoidance. The effect is economically significant and is robust

across different measures of tax avoidance and stock liquidity. We use stock splits as

a positive shock to stock liquidity and the instrumental variable method to address

potential endogeneity concerns, and obtain consistent results.

Next, we examine possible mechanisms for how stock liquidity may affect tax

avoidance. We find that the effect of stock liquidity on both tails of the tax avoidance

distribution is stronger for firms with high levels of business uncertainty. Further, the

effect of stock liquidity on the lower (upper) tail of tax avoidance distribution is

mitigated (magnified) for the financially constrained firms. These results provide

support for the existence of a positive feedback channel. On the other hand, we find

the effect of stock liquidity to be similar across firms with high versus low

shareholder rights, and across firms with high versus low managerial pay-for-

performance-sensitivities. These findings are inconsistent with either blockholder

intervention or blockholder exit channels.

Our paper contributes to the existing literature in several ways. First, at a broader

level, our paper can be viewed as a contribution to the tax avoidance research. Prior

studies on the determinants of tax avoidance mainly focus on firm fundamentals or

6

executive incentives (e.g., Desai and Dharmapala, 2006; Lisowsky, 2010; Armstrong,

Blouin and Larcker, 2012; and Rego and Wilson, 2012). Little is known, however,

about how stock market conditions, and in particular the liquidity of the firm's stock,

affect firm’s tax planning. To the best of our knowledge, our paper is the first to

document the effect of stock liquidity on tax avoidance, thereby establishing an

important link between corporate tax avoidance and firm’s stock market conditions.

Second, our paper also contributes to the corporate finance literature

documenting beneficial effects of stock liquidity on the value of the firm (e.g., Fang et

al., 2009; and Bharath et al., 2013). Our results suggest that greater stock liquidity

mitigates both overly-aggressive and overly-conservative tax planning, and thus

highlight a potential channel through which greater stock liquidity increases firm

value.

Finally, at a methodological level, our study contributes to the tax avoidance

literature by further emphasizing the importance of examining the whole distribution

of tax avoidance, instead of focusing on the mean effect; an essential point raised by

Armstrong et al. (2013).

The rest of the paper is organized as follows. In Section II we discuss the relevant

literature and develop our hypotheses. Section III describes the data. Section IV

outlines the methodology. In Sections V to VII, we report and discuss our empirical

findings. Concluding remarks are presented in Section VIII.

7

II. RELATED LITERATURE AND HYPOTHESES DEVELOPMENT

Corporate Tax Avoidance and Stock Liquidity

We posit that high liquidity firms engage less in both overly-aggressive and

overly-conservative tax avoidance. Our empirical predictions rest on the premise that

tax avoidance is viewed by managers as one of the many investment decisions

(Hanlon and Heitzman, 2010; Armstrong et al., 2013), and thus is considered as a part

of the overall investment strategy of the firm (McGuire, Omer, and Wilde, 2013).

Accordingly, factors that affect firm’s overall investment strategy should also affect

firm’s tax avoidance as shown by McGuire et al. (2013).

The above discussion suggests several causative mechanisms through which

stock liquidity may influence corporate tax avoidance. First, greater stock liquidity

may affect tax avoidance through the feedback channel from stock prices to firm’s tax

planning. Prior studies show that greater stock liquidity stimulates the entry of

informed traders (Grossman and Stiglitz, 1980; Kyle, 1985; and Easley and O’Hara,

2004). Informed investors factor the effect of their trades on firm’s investment

decisions, trade more aggressively, and consequently make stock prices more

informative to firm’s management (Subrahmanyam and Titman, 2001; Khana and

Sonti, 2004; Foucault and Gehrig, 2008; Fang et al., 2009). Information uncertainty

may cause managers to misestimate firm’s potential tax savings over the course of tax

avoidance investment, thereby resulting in over-or underinvestment in tax avoidance.

Thus, by increasing share price informativeness to managers, greater stock liquidity is

8

predicted to facilitate better informed tax planning decisions, and therefore will

influence firm’s tax avoidance.

In particular, our empirical predictions are most closely related to the studies by

Khana and Sonti (2004), Chen et al. (2007), and Edwards et al. (2013). In Khana and

Sonti’s (2004) model higher share prices signal improved prospects to firm managers

and relax firm’s financial constraint. Informed traders factor this effect of share prices

on firm investment decisions and manipulate share prices to get firm to take certain

investments. Chen et al. (2007) show that the sensitivity of investment to share price

increases in the amount of private information in stock price, suggesting that

managers learn from the private information in stock price about their own firm’s

fundamentals (consistent with Khana and Sonti, 2004). Edwards et al. (2013) show

that financially constrained firms resort to a more aggressive tax planning.

Integrating these three sets of results, we posit that greater stock liquidity will

facilitate more informed trading to relax the level of financial constraints for the firms

whose tax avoidance strategies are considered by investors as overly-aggressive.

Similarly, greater stock liquidity will facilitate more informed trading to tighten

financial constraints for the firms whose investment in tax planning is perceived by

investors as overly-conservative. Accordingly, a positive feedback perspective

predicts that high liquidity firms will engage less in both overly-aggressive and

overly-conservative tax avoidance.

Second, a link between stock liquidity and tax avoidance can also be motivated

based on the corporate governance theories. Separation of ownership and control may

9

lead to corporate tax planning that reflects the private interests of the manager. The

resulting agency problems cause managers to engage in overly-aggressive or overly-

conservative tax avoidance (e.g., Chen and Chu, 2005; Desai and Dharmapala, 2006;

and Kim, Li and Zhang, 2011).

Prior research highlights two mechanisms for the beneficial role of stock liquidity

in corporate governance. One strand of literature in this vein suggests that stock

liquidity enhances blockholders’ incentives to intervene by allowing blockholders to

increase their stakes in the firm at lower cost (Maug, 1998). Another agency-based

causative mechanism suggests that liquidity improves corporate governance by

facilitating the threat of blockholder exit (Edmans 2009; and Edmans and Manso

2011). In these models, strategic dumping of firm shares by blockholders exerts a

downward pressure on share price, and thus penalizes management for actions that are

considered not to be in the best interests of blockholders.

Prior studies provide empirical evidence consistent with greater stock liquidity

improving corporate governance (e.g., Bharath et al., 2013; and Edmans et al., 2013).

More directly related to our hypothesis is the study by Armstrong et al. (2013) who

document that corporate governance increases extremely low levels of tax avoidance,

and decreases extremely high levels of tax avoidance. Thus, a corporate governance

perspective suggests that high stock liquidity will deter firm management from

engaging in both overly-aggressive and overly-conservative tax avoidance by either

enhancing blockholder intervention or amplifying the threat of blockholder exit.

10

To summarize, both the positive feedback and corporate governance perspectives

predict that high liquidity firms will engage less in both overly-aggressive and overly-

conservative tax avoidance. The above discussion leads to our main hypothesis.

lower (upper) tail of tax avoidance distribution.

Is There a Positive Feedback Effect?

Having established a link between stock liquidity and corporate tax avoidance,

our next step is to examine the causative mechanism of this relation. Positive

feedback perspective predicts that the effect of stock liquidity on firm’s investment

decisions will be stronger for the firms with high levels of business uncertainty

(Subrahmanyam and Titman, 2001; Fang et al., 2009). Further, since positive

feedback effect is predicted to relax financial constraints for the firms that engage in

overly-aggressive tax avoidance, the effect of liquidity on the upper tail of tax

avoidance is expected to be stronger for the financially constrained firms. On the

other hand, since positive feedback effect is predicted to tighten financial constraints

for the firms that engage in overly-conservative tax avoidance, the effect of liquidity

on the lower tail of tax avoidance distribution is predicted to be weaker for the firms

that already face financial constraints. This discussion leads to the following

hypotheses.

H1. Ceteris paribus, stock liquidity is positively (negatively)

associated with the lower (upper) tail of tax avoidance

distribution.

H1a: Ceteris paribus, the association between stock liquidity and

both tails of corporate tax avoidance distribution is stronger for the

firms with high levels of business uncertainty.

H1b: Ceteris paribus, the association between stock liquidity and

the upper (lower) tail of tax avoidance distribution is stronger

(weaker) for the financially constrained firms.

11

Is There Blockholder Intervention Effect?

The effect of blockholder intervention depends on the balance of power between

shareholders and managers. Therefore, if the association between stock liquidity and

tax avoidance occurs through blockholder intervention channel, the effect of liquidity

should be amplified for the firms with high shareholder rights (Fang et al., 2009; and

Bharath et al., 2013). This insight leads to the following hypothesis.

Is There Blockholder Exit Effect?

The disciplining effect of the threat of exit comes through managers' wealth

invested in firm’s stock. Accordingly, the implications of blockholder exit will be

more severe for managers, whose compensation is highly sensitive to changes in share

price (Bharath et al., 2013; and Edmans et al. 2013). Thus, blockholder exit

perspective predicts that the effect of stock liquidity will be magnified for the firms

with high pay-for-performance sensitivity. This discussion leads to the following

hypothesis.

H1c: Ceteris paribus, the association between stock liquidity and

both tails of corporate tax avoidance distribution is stronger for

the firms with high shareholder rights.

H1d: Ceteris paribus, the association between stock liquidity and

both tails of corporate tax avoidance distribution is stronger for the

firms with high managerial pay-for-performance sensitivity.

12

III. SAMPLE SELECTION AND VARIABLES

Sample Selection

Our main measure of stock liquidity is the relative effective spread, calculated

using intra-day data from the Trade and Quote database (TAQ). This measure comes

from Vanderbilt University's Financial Markets Research Centre (hereafter FMRC).3

Because TAQ only provides data since 1993, we restrict our sample period to 1993-

2010. We obtain firm financial information from Compustat fundamental annual files.

Our initial sample consists of all the firms in Compustat over the sample period of

1993-2010. We drop observations without sufficient information for construction of

the tax avoidance and /or stock liquidity measures, and those with negative pre-tax

income. We winsorize all the variables at both the 1st and 99

th percentiles to mitigate

the effect of outliers.

Variables

Tax Avoidance

In our analysis we adopt Hanlon and Heitzman’s (2010) broad definition of tax

avoidance as the reduction of explicit taxes that reflects all transactions that have any

effect on firm’s tax liability. Our primary measure of tax avoidance is GAAP

effective tax rate (GETR) which is computed as follows:

(1)

3 We are grateful to Hans Stoll and Christoph Schenzler from Vanderbilt University for providing the

effective spread data.

it

itit

PI

TXTGETR

13

where i denotes firm, t denotes year, is firm i’s total tax expenses and is firm

i’s pre-tax income. This measure has been extensively adopted by prior research (e.g.,

Dyreng, Hanlon and Maydew, 2010; Armstrong et al., 2012; and Cheng et al., 2012).

In particular, our choice of GETR as the primary measure of tax avoidance is

motivated by the results of Graham at al.’s (2013) survey, who find that management

at public companies places a higher weight on the GAAP effective tax rates compared

to other tax metrics, such as cash taxes paid. Further, Armstrong et al. (2012)

conclude that GETR is a more informative measure of tax director actions, compared

to other tax avoidance metrics. Lower values of GETR indicate more aggressive tax

avoidance.

Stock Liquidity

Our primary measure of stock liquidity (LIQ) is relative effective spread,

computed as the ratio of the difference between the trade price and the midpoint of the

bid-ask quote over the trade price. The relative effective spread is regarded as one of

the best measures of stock liquidity and has been extensively used by prior studies

(e.g., Fang et al., 2009; and Fang, Tian and Tice, 2013). FMRC computes daily

relative effective spread for the stock as the trade-weighted average of the relative

effective spread of all the trades during the day. To obtain the annual relative effective

spread, we take the arithmetic mean of the daily relative effective spreads over the

firm's fiscal year. Since relative effective spread is highly skewed and higher value

indicates lower liquidity, we take the natural logarithm of the ratio to correct for the

14

skewness following Fang et al. (2009) and then multiply it by minus one for ease of

interpretation. Accordingly, higher values of LIQ indicate higher stock liquidity.

Control Variables

The selection of control variables follows prior literature (e.g., Rego, 2003; and

Dyreng et al., 2010) and captures different aspects of firm operations. We include

return on assets (ROA) and ROA volatility (STDROA) to control for firm profitability

and the uncertainty of the firm's operation. PPE assets (PPE) and intangible assets

(INTANG) are included to control for the nature of the firm's business. We also

include leverage ratio (LEV), loss carry forward dummy (NOL) and change in loss

carry forward (DNOL_AT) to capture the debt and non-debt tax shields. Firm size

(SIZE) is included to control for “political costs” of tax avoidance (e.g., Rego, 2003).

Change in goodwill (POSGDWL) is included to capture the merger and acquisition

activities of the firm. Equity income in earnings (EQINC) and new investments

(NEWINV) are included to control for firm's investment activities. We also include

foreign assets (FRGNAT) to control for the economies of scale in tax planning. Last,

we include market-to-book (MB) to control for growth opportunities, cash holdings

(CASH) to control for financial conditions, and abnormal accruals (ABACC) to control

for earnings management. Detailed definitions of all the variables are presented in

Appendix A.

15

Descriptive Statistics

Table 1 presents the summary statistics of the data. The mean (median) GAAP

effective tax rate (GETR) of our sample firms is 0.296 (0.348) and the mean (median)

stock liquidity (LIQ) is 5.763 (5.724). These numbers are well in line with those

reported in prior studies (e.g., Fang et al., 2009; and Dyreng et al., 2010). As far as the

control variables are concerned, the mean cash holdings, ROA, and ROA volatility

are 0.186, 0.099, and 0.117, respectively. On average, our sample firms have change

in goodwill of 0.021, new investments of 0.085, leverage ratio of 0.172, foreign assets

of 0.44, equity income in earnings of 0.001, and change in loss carry forward of 0.005.

These firms also have PPE assets of 33.1% and intangible assets of 13.3% of total

assets. 29% of the firms have loss carry forward and 34% of them have foreign

income. Last, the sample firms have mean firm size of 6.182, mean market-to-book of

2.882, and mean abnormal accruals of 0.079.

[Insert Table 1 about here]

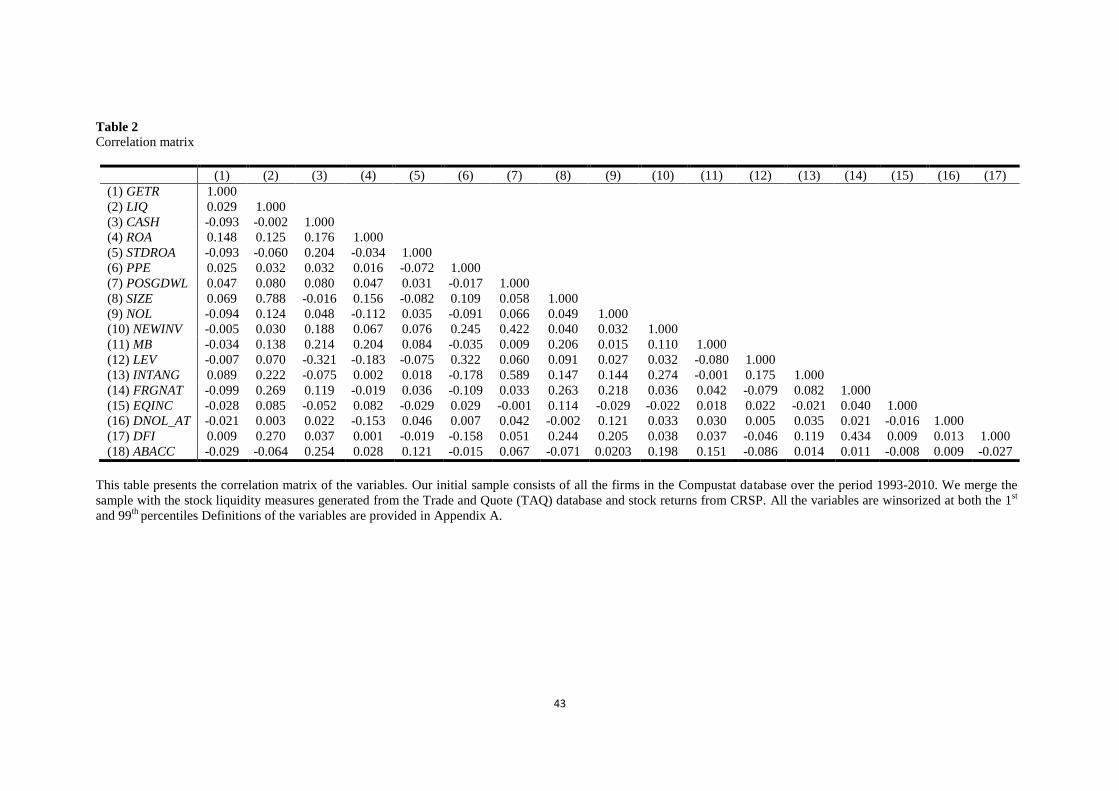

Table 2 presents the correlation matrix of the variables. The table shows that

GETR exhibits weak positive correlation with stock liquidity. GETR is also negatively

correlated with cash holdings, ROA volatility, loss carry forward dummy, new

investments, market-to-book, leverage, foreign assets, equity income in earnings,

change in loss carry forward, and abnormal accruals; while positively correlated with

return on assets, PPE assets, change in goodwill, firm size, intangible assets, and

foreign income dummy.

[Insert Table 2 about here]

16

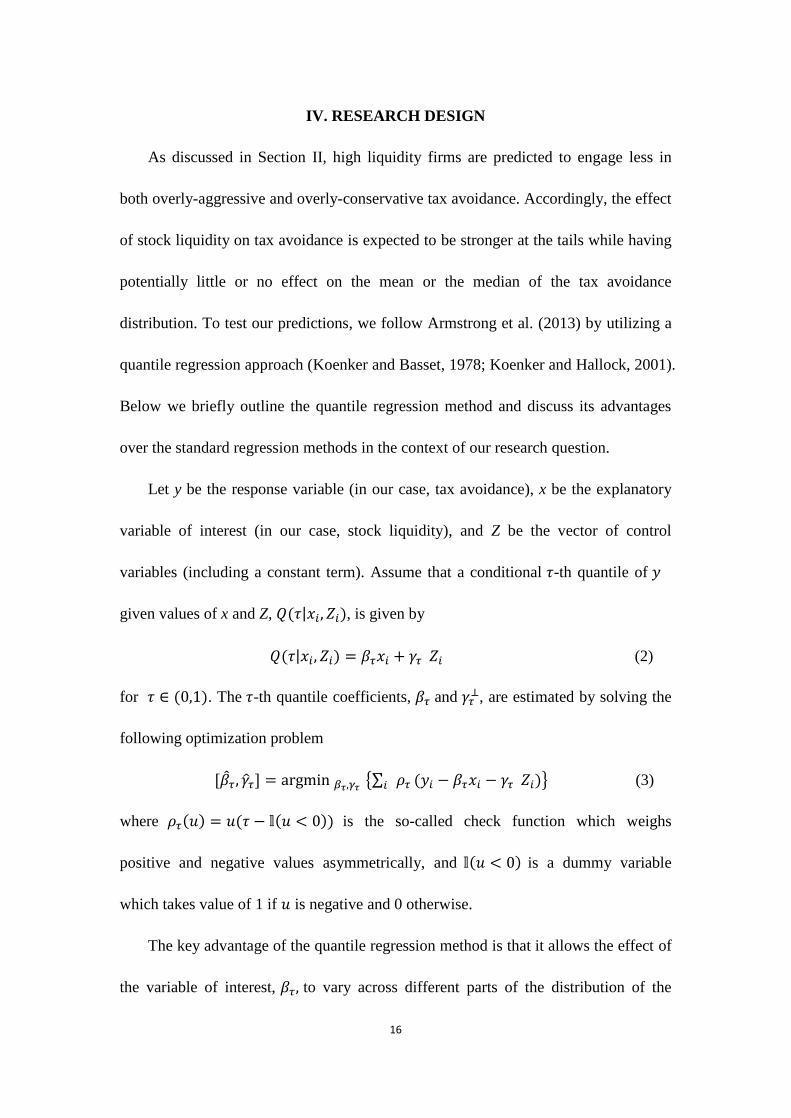

IV. RESEARCH DESIGN

As discussed in Section II, high liquidity firms are predicted to engage less in

both overly-aggressive and overly-conservative tax avoidance. Accordingly, the effect

of stock liquidity on tax avoidance is expected to be stronger at the tails while having

potentially little or no effect on the mean or the median of the tax avoidance

distribution. To test our predictions, we follow Armstrong et al. (2013) by utilizing a

quantile regression approach (Koenker and Basset, 1978; Koenker and Hallock, 2001).

Below we briefly outline the quantile regression method and discuss its advantages

over the standard regression methods in the context of our research question.

Let y be the response variable (in our case, tax avoidance), x be the explanatory

variable of interest (in our case, stock liquidity), and Z be the vector of control

variables (including a constant term). Assume that a conditional -th quantile of

given values of x and Z, | , is given by

| (2)

for . The -th quantile coefficients, and , are estimated by solving the

following optimization problem

{∑ } (3)

where is the so-called check function which weighs

positive and negative values asymmetrically, and is a dummy variable

which takes value of 1 if is negative and 0 otherwise.

The key advantage of the quantile regression method is that it allows the effect of

the variable of interest, to vary across different parts of the distribution of the

17

response variable, y. This feature is particularly important in the context of our study,

where greater stock liquidity is predicted to have a positive (negative) effect on the

lower (upper) tails of the tax avoidance distribution. This effect cannot be captured by

the standard ordinary least squares (OLS) regression method, which focuses solely on

the effect of the variable of interest on the mean of distribution of the response

variable. In contrast to the standard regression methods, quantile regression is

designed to characterize changes in both the location and shape of the distribution of

interest (Armstrong et al., 2013), and thus provides an appealing analytical framework

for our analysis. 4

V. STOCK LIQUIDITY AND CORPORATE TAX AVOIDANCE

Univariate Evidence

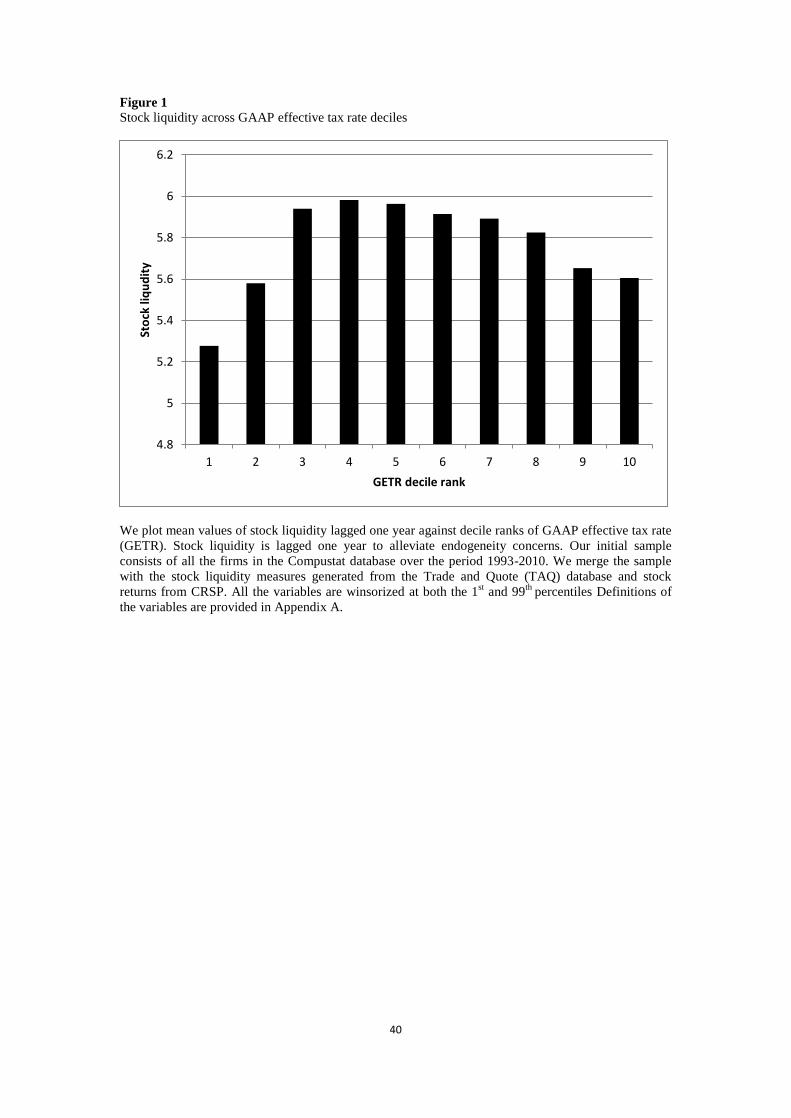

Figure 1 presents the univariate relation between stock liquidity and tax avoidance.

The x-axis plots decile ranks of GETR and y-axis plots mean values of stock liquidity

lagged one year that correspond to these deciles. The relation between the two

variables exhibits a distinct inverted U-shape, with firms in the centre (tails) of the

GETR distribution having higher (lower) stock liquidity. Specifically, the average

relative effective spreads for the firms in the highest and lowest deciles of GETR are

60 and 40 basis points, respectively. In contrast, the relative effective spread for the

firms in the 5-th decile of GETR is only 25 basis points. The difference is also

4

This important point is emphasized by Mosteller and Tukey (1977, p.266), who note that

“....regression often gives a rather incomplete picture. Just as the mean gives an incomplete picture of a

single distribution, so the regression curve gives a corresponding incomplete picture for a set of

distributions”

18

statistically significant. These results support H1, which predicts that high liquidity

firms will engage less in both overly-aggressive and overly-conservative tax

avoidance.

[Insert Figure 1 about here]

Multivariate Evidence

Turning to our multivariate tests, we estimate a quantile regression with the

baseline model specification as follows

ititititit

itititit

ititititit

ititititit

INDYRABACCDFIDNOLAT

EQINCFRGNATINTANGLEV

NEWINVNOLSIZEPOSGDWLPPE

STDROAROACASHLIQGETR

116115114

113112111110

1918171615

141312110

(4)

where i denotes firm, t denotes year, and ε is the error term. GETR is GAAP effective

tax rate and LIQ is stock liquidity measured by negative log relative effective spread.

IND is the industry fixed effects based on two-digit SIC codes and YR is the year

fixed effects. All the independent variables are lagged one year to mitigate potential

endogeneity concerns following Fang et al. (2009). We estimate our baseline model

separately for the 10-th, 50-th (median) and 90-th GETR percentiles.

We present the regression results in Columns (1) - (3) of Table 3. The coefficient

for stock liquidity is positive and statistically significant for the 10-th GETR

percentile (z-statistic=6.26, p-value<0.01, two-tail) and is negative and statistically

significant for the 90-th GETR percentile (z-statistic=-7.94, p-value<0.01, two-tail).

These results suggest that stock liquidity is negatively associated with both overly-

aggressive and overly-conservative tax avoidance, thereby providing support for H1.

19

The coefficient for stock liquidity for the median GETR is positive and statistically

significant (z-statistic=3.98, p-value<0.01, two tail)5.

To facilitate economic interpretation of our results, we rank stock liquidity for

each year, and then partition the resulting ranks into deciles labelled from 1 (lowest

decile) to 10 (highest decile). Next, we estimate our baseline quantile regressions with

the decile ranking of stock liquidity and present the results in Columns (4) - (6) of

Table 3. The results further confirm the positive (negative) relation between the 10-th

(90-th) percentile of GETR and stock liquidity. Further, the coefficient for stock

liquidity in Column (4) suggests that moving from the lower to the upper decile of

stock liquidity increases 10-th percentile of GETR by 0.011*(10-1) = 0.099, or 9.9%

of pre-tax income. The coefficient for stock liquidity reported in Column (6) suggests

that moving from the lower to the upper decile of stock liquidity decreases 90-th

percentile of GETR by 0.004*(10-1) = 0.036, or 3.6% of pre-tax income. Therefore,

we conclude that the effect of stock liquidity on the tails of tax avoidance distribution

is not only statistically significant but is also economically meaningful. For

comparison, stock liquidity has a relatively moderate effect on the median GETR,

where moving from the lower to the upper decile of stock liquidity increases median

GETR by only 0.001*(10-1) =0.009 or 0.9% of pre-tax income.

[Insert Table 3 about here]

To further examine the relation between stock liquidity and tax avoidance, we re-

estimate our baseline model for the 10-th, 15-th, 20-th…, and 90-th percentiles of

5 For robustness purposes, we repeat our analyses with financial firms (SIC codes 6000-6799) excluded

from our sample. The results (untabulated) remain qualitatively similar to those reported in our paper.

20

GETR. Next, we plot in Figure 2 the estimated coefficients for stock liquidity along

with the 95% confidence intervals against the corresponding percentiles of GETR.

Figure 2 reveals several interesting findings. Stock liquidity associates positively with

GETR (i.e., associates negatively with tax avoidance) when moving from the centre to

the upper end of the tax avoidance distribution (i.e., lower percentiles of GETR) On

the other hand, stock liquidity associates negatively with GETR (i.e., associates

positively with tax avoidance) when moving from the centre to the lower end of the

tax avoidance distribution (i.e., upper percentiles of GETR). Furthermore, the

magnitude of the effect monotonously increases when moving from the centre of

distribution to the extreme percentiles of GETR. Overall, these results provide further

support for H1, suggesting that high liquidity firms engage less in both overly-

aggressive and overly-conservative tax avoidance.

[Insert Figure 2 about here]

As far as the control variables are concerned, since prior studies use least squares

regression method in their research design the results for the control variables are not

directly comparable to those reported in prior literature. Nonetheless, examination of

the coefficients for control variables reveals several interesting items. First, the effects

of control variables on the median GETR are largely in line with those reported in

prior studies (e.g., Rego, 2003; and Chen et al., 2010). Specifically, median GETR is

positively related to intangible assets (INTANG) and the return on assets (ROA), and

is negatively associated with equity in earnings (EQINC), proportion of foreign assets

(FRGNAT), loss carried forward (NOL), and firm size (SIZE). Second, while for some

21

variables the effect on GETR is uniformly positive or negative across different parts

of GETR distribution (e.g., EQINC and NOL), other variables, such as leverage

(LEV) and cash holdings (CASH), experience shifts in the coefficient sign as one

moves from the upper to lower tail of GETR distribution. While in-depth examination

of the effects of control variables is out of scope of a current study, these observations

further emphasize the importance of controlling for changes in both location and

shape of the tax-avoidance distribution.

VI. ROBUSTNESS TESTS

In this section, we conduct a variety of robustness checks to validate our main

findings. For the sake of brevity, we only report the coefficients for stock liquidity.

Alternative Measures of Tax Avoidance and Stock Liquidity

We commence by examining the robustness of our results to alternative measures

of tax avoidance. We use the following measures of tax avoidance employed in prior

studies (Desai and Dharmapala, 2006; Dyreng, 2008; Armstrong et al., 2012; and

Cheng et al., 2012): (1) annual effective cash tax rate, (2) long-term effective cash tax

rate, and (3) the residual book-tax difference6. The results are presented in Panel A of

Table 4. The coefficient for stock liquidity is positive and significant for the 10-th

percentile regression (smallest z-statistic=2.76, p-value<0.01, two-tail), and is

negative and significant for the 90-th percentile regression (smallest z-statistic=-2.23,

p-value<0.05, two-tail) for all three measures of tax avoidance.

6 For ease of interpretation we multiply residual book-tax difference by -1.

22

Next, we examine the sensitivity of our results to using alternative measures of

stock liquidity. We use the following stock liquidity measures: (1) the Amihud (2002)

measure, modified by Gopalan and Pevzner (2012), (2) implicit bid-ask spread

measure of Hasbrouck (2009), and (3) the percentage of zero returns measure of

Lesmond (2005). We take natural log of both Amihud (2002) and the Hasbrouck

(2009) measures, as these two measures are heavily skewed and multiply by the

minus one for ease of interpretation. Similarly, we use Lesmond (2005) measure as

one minus percentage of zero returns. Following Jayaraman and Milbourn (2012) we

combine these three measures into a composite measure using principal components.

The results are reported in Panel B of Table 4. The coefficient for stock liquidity

is positive and significant for the 10-th percentile of GETR (z-statistic=8.27, p-

value<0.01, two-tail), and is negative and significant for the 90-th percentile of GETR

(z-statistic=-5.95, p-value<0.01, two-tail) Hence, we conclude that our results are

robust to alternative measures of tax avoidance and stock liquidity.

Alternative Regression Specifications

Next, we examine the robustness of our results to alternative model specifications.

We conduct two analyses. In our first analysis, we consider the possibility that our

results are driven by the time-trends in tax-avoidance and/or stock liquidity. To

address this concern, we estimate our baseline model (Eq.4) cross-sectionally (year-

by-year) and report the time-series averages of the coefficients for stock liquidity. The

results are reported in Panel C of Table 4. The coefficient for stock liquidity is

positive and significant for the 10-th percentile of GETR (t-statistic=2.85, p-

23

value=0.01, two-tail), and is negative and significant for the 90-th percentile of GETR

(t-statistic=-2.39, p-value=0.03, two-tail). Hence, we conclude that our findings are

not likely to be driven by the time-trends in variables.

In our second analysis, we augment our baseline model with additional control

variables which were shown by prior literature to be correlated with stock liquidity

and which may also affect firm’s tax avoidance. Specifically, in addition to the

control variables specified in Section III we also include the following variables: (1)

institutional ownership, (2) analyst coverage, (3) board independence (proportion of

independent directors on the board), (4) CEO delta (sensitivity of CEO compensation

to changes in stock price), (5) CEO vega (sensitivity of CEO compensation to

changes in stock volatility), (6) implied firm’s cost of equity, and (7) probability of

informed trading (PIN). The results are reported in Panel C of Table 4. The

coefficient for stock liquidity remains positive and significant for the 10-th percentile

of GETR (z-statistic=4.14, p-value<0.01, two-tail), and negative and significant for

the 90-th percentile of GETR (z-statistic=-2.91, p-value<0.01, two-tail). Overall,

based on the results of these two analyses we conclude that our findings are robust to

alternative regression specifications.

[Insert Table 4 about here]

24

Endogeneity

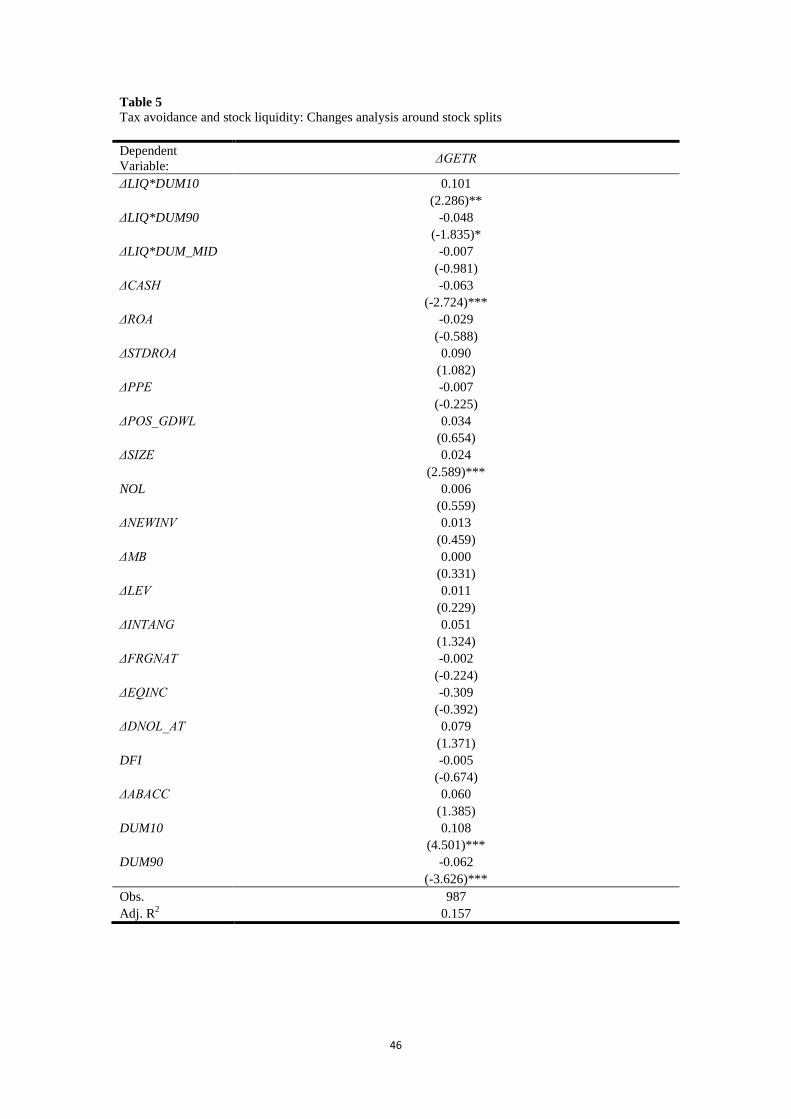

Stock Splits as a Shock to Stock Liquidity

Given the cross-sectional design of our analysis, our results may suffer from

endogeneity concerns. To address this issue, we conduct two analyses. First, we use

stock splits as a shock to stock liquidity and study its effect on tax avoidance. Prior

studies show that stock splits are associated with increases in stock liquidity (Lin et al.,

2009; Jayaraman and Milbourn, 2012). Furthermore, Chemmanur, Hu, and Huang

(2013) document that stock splits bring in more institutional trading and a consequent

reduction in information asymmetry (consistent with more informative share prices).

Since stock splits are not clustered in calendar time and have no effect on the

underlying firm fundamentals (e.g., Easley et al., 2001), they provide an appealing

framework to examine the causal effect of stock liquidity on corporate tax avoidance.

We collect the data on stock splits from CRSP database. Excluding stock splits

with missing data on GAAP effective tax rate, stock liquidity and control variables

leaves us with a sample of 987 stock split events. We proceed as follows. First, we

estimate our baseline model (Eq.4) excluding stock liquidity (that is, with control

variables only) for the 10-th and 90-th percentiles of GETR. Next, we construct a

dummy variable, DUM1, which takes value of one if firm i’s GETR was below the

estimated conditional 10-th percentile of GETR for the firm i in the year prior to stock

split. We construct a second dummy variable, DUM10, which takes value of one if

firm i’s GETR was above the estimated conditional 90-th percentile of GETR for the

firm i in the year prior to stock split and zero otherwise. Last, we construct a dummy

25

variable, DUM_MID, which equals to one minus the sum of DUM1 and DUM10. Our

prediction is that changes in liquidity around stock splits will be positively (negatively)

associated with changes in GETR for the firms that engaged in overly-aggressive

(overly-conservative) tax avoidance prior to stock split, that is, the firms with

DUM1=1 (DUM10=1).

To test our prediction, we perform regression analysis on the changes in the

effective tax rate against changes in stock liquidity around the stock splits. The

dependent variable is the change in GETR over the two years around the stock split

event and the independent variables are the change in stock liquidity, interacted with

DUM1, DUM10 and DUM_MID dummy variables, and the changes in the control

variables7.

The results are presented in Table 5. Consistent with our prediction, the

coefficient for the interaction term of stock liquidity with DUM1 dummy is positive

and significant (t-statistic=2.29, p-value<0.05, two-tail), and the coefficient for the

interaction term of stock liquidity with DUM10 dummy is negative and significant (t-

statistic=-1.84, p-value=0.066, two-tail). These results are consistent with greater

stock liquidity resulting in less overly-aggressive and overly-conservative tax

avoidance.

[Insert Table 5 about here]

7 The advantage of using firm-specific changes regression is that it provides time-series evidence of the

link between the effective tax rate and stock liquidity as well as alleviates concerns about firm-specific

omitted correlated variables (Jayaraman and Milbourn, 2012).

26

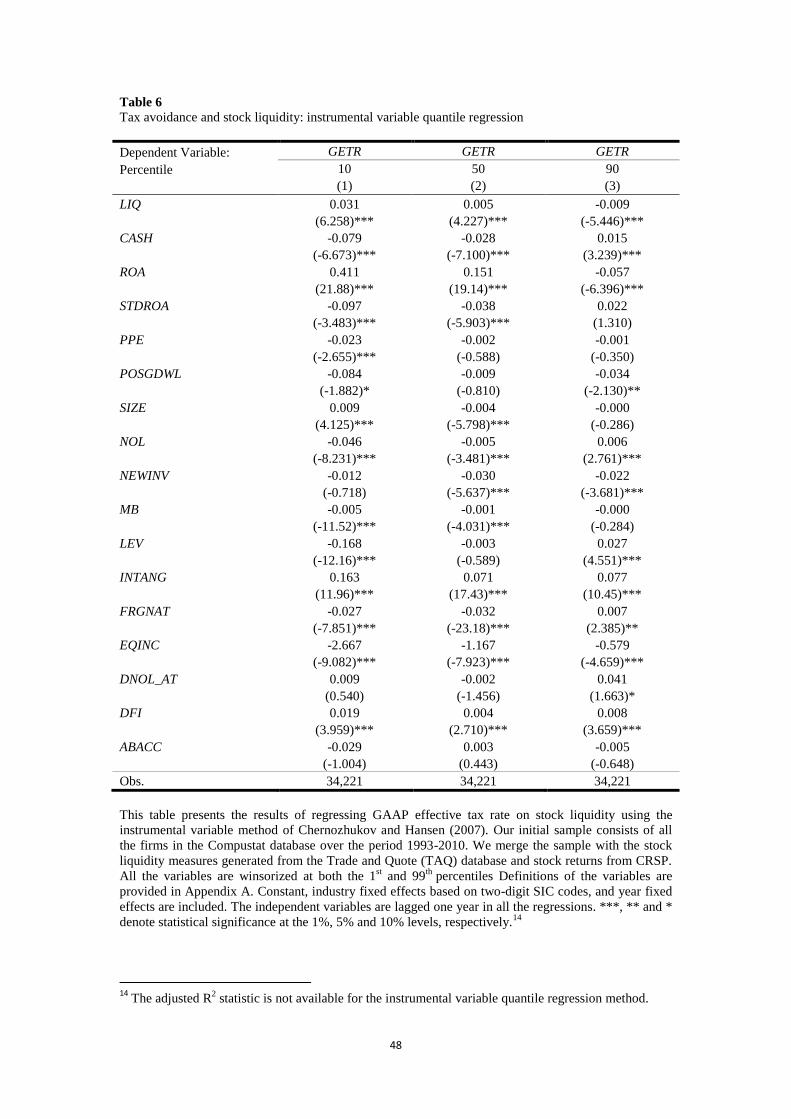

Instrumental Variable Quantile Regression

In our second analysis, we employ the instrumental variable quantile regression

method of Chernozhukov and Hansen (2007). Following Fang et al. (2009) and

Jayaraman and Milbourn (2012) we use stock liquidity lagged two years and mean

stock liquidity for the industry as the instruments. The use of stock liquidity lagged

two years further helps mitigate concerns that our results are driven by the omitted

variable correlated with both effective tax rate and stock liquidity in fiscal year t. As

for the industry liquidity, the portion of firm i’s liquidity that is correlated with the

liquidity of its industry is less likely to be correlated with potential firm-specific

omitted variables (Jayaraman and Milbourne, 2012).

The results are reported in Table 6. The coefficient for stock liquidity for the 10-

th percentile of GETR remains positive and significant (z-statistic=6.26, p-

value<0.01, two-tail). The coefficient for stock liquidity for the 90-th percentile of

GETR remains negative and significant (z-statistic=-5.45, p-value<0.01, two-tail).

Overall, based on the results of these two analyses we conclude that our findings are

robust to potential endogenous effects.

[Insert Table 6 about here]

VII. HOW DOES STOCK LIQUIDITY AFFECT TAX AVOIDANCE?

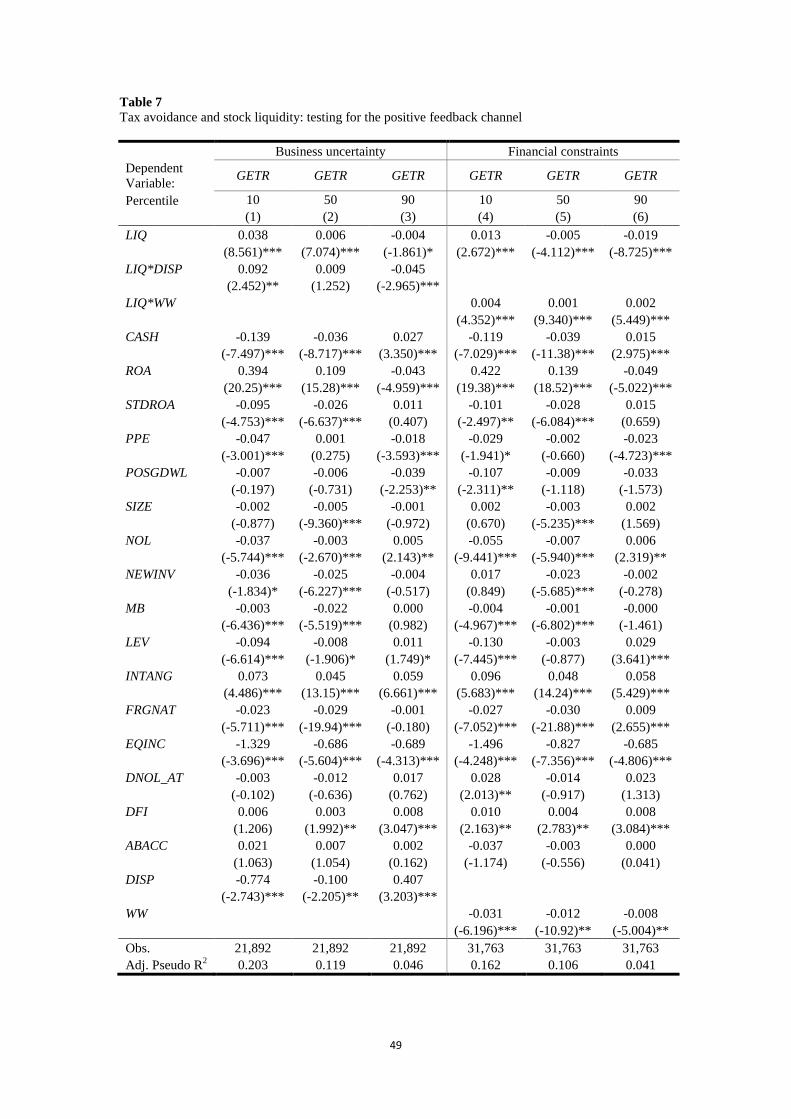

Is There a Positive Feedback Effect?

To test for the positive feedback channel, we examine the effects of business

uncertainty and financial constraints on the association between stock liquidity and

tax avoidance. Specifically, H1a and H1b predict that (1) the effect of stock liquidity

27

on both tails of tax avoidance distribution is stronger for the firms with high levels of

business uncertainty, and (2) the effect of stock liquidity on the upper (lower) tail of

tax avoidance distribution is magnified (mitigated) for the financially constrained

firms.

First, consider the effect of business uncertainty. Following prior studies (e.g.,

Lang and Lundholm, 1996; Diether, Maloy and Scherbina, 2002; and Zhang, 2006)

we employ the dispersion in analyst earnings forecasts (DISP) as a proxy for business

uncertainty. The results are reported in Columns (1) - (3) of Table 7. The coefficient

for the interaction term of stock liquidity with the analyst forecast dispersion is

positive and significant for the 10-th percentile of GETR (z-statistic=2.45, p-

value<0.05, two-tail), and is negative and significant for the 90-the percentile of

GETR (z-statistic=2.96, p-value=0.01, two-tail). Since stock liquidity is positively

(negatively) associated with the 10-th (90-th) percentile of GETR, these results

suggest that the effect of liquidity on both tails of tax avoidance distribution is

stronger for the firms with high levels of business uncertainty, thereby supporting H1a.

Next, consider the effect of financial constraints. We use the Whited-Wu index

(WW) proposed by Whited and Wu (2006) as the proxy for firm financial constraints.

Higher values of the Whited-Wu index indicate firms that are more financially

constrained. The results are reported in Columns (4) - (6) of Table 7. The coefficient

for the interaction term of stock liquidity with the Whited-Wu index is positive and

significant for both 10-th and 90-th percentiles of GETR (smallest z-statistic=4.35, p-

28

value<0.01, two-tail).8 Since stock liquidity is positively (negatively) associated with

the 10-th (90-th) percentile of GETR, these findings imply that the effect of stock

liquidity on the upper (lower) tail of the tax avoidance distribution is magnified

(mitigated) for the financially constrained firms, and thus provide support for

hypothesis H1b9. Overall, we conclude that our findings are consistent with the

positive feedback channel.

[Insert Table 7 about here]

Is There Blockholder Intervention Effect?

To test for the blockholder intervention channel, we examine the effect of

shareholder rights on the association between stock liquidity and tax avoidance.

Specifically, H1c predicts that the effect of stock liquidity on both tails of the tax

avoidance distribution is stronger for the firms with high shareholder rights.

We consider two measures of shareholder rights. Our first measure is the

governance index (GINDEX) of Gompers, Ishii, and Metrick (2003). Following

Gompers et al. (2003) we classify firms with GINDEX<=5 (GINDEX>=14) as the

firms with high (low) shareholder rights. Our second measure is CEO power

(CEO_POWER) which is the principal component of three board governance

measures suggested by prior literature (Jensen, 1993; Mehran, 1995; and Core,

8 For robustness purposes we also try a principal component of the three financial constraints measures

suggested by prior literature: Kaplan-Zingales index (Kaplan and Zingales, 1997), Whited-Wu index

(Whited and Wu, 2006), and Hadlock-Pierce index (Hadlock and Pierce, 2010). The results are

qualitatively similar to those reported for the Whited-Wu index measure. 9 The coefficient for the Whited-Wu index is negative and significant for all three regression models

(smallest z-statistic=-5.00, p-value<0.01, two-tail). These results suggest that financially constrained

firms, on average, engage more in tax avoidance, consistent with Edwards et al’s. (2013) results.

29

Holthausen and Larcker, 1999). These measures include board size, CEO-Chairman

duality, and board independence. Higher values of CEO_POWER indicate lower

shareholder ability to influence CEO decision making. The data used to construct

these measures were obtained from RiskMetrics.10

First, consider the results using GINDEX as a proxy for shareholder rights. The

results are reported in Columns (1) - (3) of Table 8. For the 10-th percentile of GETR

the coefficient for the interaction term of stock liquidity with the LOW_GINDEX

dummy (GINDEX<=5) is negative and significant (z-statistic=-1.94, p-value=0.053,

two-tail). The coefficient for the interaction term of stock liquidity with the

HIGH_GINDEX dummy (GINDEX>=14) is not significant (z-statistic=-0.34, p-

value=0.73, two-tail). The difference between the two coefficients is not significant

(z-statistic=-1.03, p-value=0.30, two-tail). For the 90-th percentile of GETR the

coefficient for the interaction term of stock liquidity with the LOW_GINDEX dummy

is negative and marginally significant (z-statistic=-1.74, p-value=0.08, two-tail). The

coefficient for the interaction term of stock liquidity with the HIGH_GINDEX dummy

is not significant (z-statistic=0.29, p-value=0.76, two-tail), and so is the difference

between the two coefficients (z-statistic=-1.36, p-value=0.18, two-tail).

Next, consider the results for the CEO_POWER measure. The results are reported

in Columns (4) - (6) of Table 8. The coefficient for the interaction term of stock

liquidity with CEO_POWER is not significant for both 10-th and 90-th percentiles of

GETR (largest z-statistic=-1.60, p-value=0.11, two-tail). Overall, since the

10

The RiskMetrics database covers S&P 1500 firms and contains information of the governance index

since 1990 and the board of directors since 1996.

30

blockholder intervention channel predicts the effect of liquidity to be stronger for the

firms with high shareholder rights, the results reported in Table 8 do not support H1c.

[Insert Table 8 about here]

Is There Blockholder Exit Effect?

To test for blockholder exit channel, we examine the effect of pay-for-

performance sensitivity on the association between stock liquidity and tax avoidance.

Specifically, H1d predicts that the effect of stock liquidity on both tails of tax

avoidance distribution is stronger for the firms with high pay-for-performance

sensitivity.

We employ two measures of pay-for-performance sensitivity. The first measure,

outlined in Core and Guay (2002) (PPS_CG), is computed as the natural logarithm of

the dollar value change in managers' stock and option holdings with respect to 1%

change in the firm's stock price. We obtain the data used to construct this measure

from the ExecuComp database.11

The second measure, outlined in Edmans, Gabaix

and Landier (2009) (PPS_EGL), is defined as the dollar change in the CEO wealth for

a one hundred-percentage point change in firm value divided by annual flow

compensation. We obtain the data from Alex Edmans’ website.12

The results are reported in Table 9. Columns (1) to (3) report the results for

PPS_CG. The coefficient for the interaction term of stock liquidity with the pay-for

11

The ExecuComp database covers the stock and option compensation information of the management

of S&P 1500 firms since 1992. 12

http://finance.wharton.upenn.edu/~aedmans/data.html

31

performance sensitivity is negative and significant (z-statistic=-2.14, p-value<0.05,

two-tail) for the 10-th percentile of GETR, and is not significant for the 90-th

percentile of GETR (z-statistic=1.14, p-value=0.25, two-tail).13

Columns (4) to (6)

report the results for the same sample when using scaled pay-for-performance

sensitivity, PPS_EGL. The coefficient for the interaction term of stock liquidity with

scaled pay-for-performance sensitivity is not significant for both the 10-th and 90-th

percentiles of GETR (largest z-statistic=-0.58, p-value=0.59, two-tail). These results

do not support H1d which predicts that the effect of stock liquidity on tax avoidance

is stronger for the firms with high pay-for-performance sensitivity, and thus are

inconsistent with the threat of exit channel.

[Insert Table 9 about here]

VIII. SUMMARY AND CONCLUSIONS

In this study, we investigate the effect of stock liquidity on corporate tax

avoidance. Greater stock liquidity makes share prices more informative to managers,

and thus allows managers to make better informed tax planning decisions. Greater

stock liquidity may also affect tax avoidance through the corporate governance

channel by enhancing blockholders’ voice or amplifying the threat of blockholder exit.

We document a positive (negative) effect of stock liquidity on the lower (upper)

tails of the (conditional) tax avoidance distribution, suggesting that high liquidity

13

Given that PPS_CG is significantly correlated with firm size (Edmans et al., 2009), it is possible that

the negative coefficient for the interaction term of PPS_CG with stock liquidity for the 10-th percentile

of GETR captures the effect of firm size. In our sample the Pearson correlation coefficient between

PPS_CG and firm size is 0.58 while that between PPS_EGL and firm size is only 0.05.

32

firms engage less in both overly-aggressive and overly-conservative tax avoidance.

The effect of stock liquidity on both tails of tax avoidance distribution is stronger for

firms with high level of business uncertainty. Also, the effect of stock liquidity on the

lower (upper) tail of tax avoidance distribution is mitigated (magnified) for the

financially constrained firms. Our findings are consistent with the positive feedback

channel where, by making share prices more informative to managers, greater stock

liquidity improves firm’s tax planning decisions.

Corporate tax avoidance raises substantial interests among both academics and

regulators in recent years. There is also a growing consensus that firm’s stock

liquidity plays a substantial role in corporate governance and firm’s investment

decisions. Nevertheless, the relation between stock liquidity and tax avoidance insofar

remained an uncharted territory. Our paper makes a significant contribution to the

literature by being the first to document an effect of stock liquidity on corporate tax

avoidance, thereby carrying potential implications for further academic research and

stock market legislations.

33

References

Armstrong, C., Blouin, J., and D. Larcker. 2012. The Incentives for Tax Planning.

Journal of Accounting and Economics 53: 391 – 411

Armstrong, C., Blouin, J., Jagonlizer, A., and D. Larcker. 2013. Corporate

Governance, Incentives, and Tax Avoidance. Rock Center for Corporate

Governance working paper series.

Bebchuk, L., Cohen, A., and A. Ferrell. 2009. What Matters in Corporate

Governance? Review of Financial Studies 22: 783:827.

Bharath, T., S. Jayaraman, and V. Nagar. 2013. Exit as Governance: An Empirical

Analysis. Journal of Finance, forthcoming.

Chemmanur, T., Hu, G., and J. Huang. 2013. Institutional Investors and the

Information Production Theory of Stock Splits. Journal of Financial and

Quantitative Analysis, forthcoming

Chen, K.-P., Chu, C., 2005. Internal Control vs. External Manipulation: A Model of

Corporate Income Tax Evasion. RAND Journal of Economics 36, 151–164.

Chen, Q., Goldstein, I., and W. Jiang. 2007. Price Informativeness and Investment

Sensitivity to Stock Price. The Review of Financial Studies 20: 619-650

Chen, S., Chen, X., Cheng, Q., and T. Shevlin, 2010. Are Family Firms More Tax

Aggressive than Non-Family Firms? Journal of Financial Economics 95: 41-61.

Cheng, C.S.A., Huang, H., Li. Y., and J. Stanfield. 2012. The Effect of Hedge Fund

Activism on Corporate Tax Avoidance. The Accounting Review 87: 1493-1526.

Chernozhukov, V., and C. Hansen. 2007. Instrumental Variable Quantile Regression:

A Robust Inference Approach. Journal of Econometrics 142: 379:398.

Chordia, T., Roll, R., and A. Subrahmanyam. 2008. Liquidity and Market Efficiency.

Journal of Financial Economics 87: 249-268.

Core, J. E., Holthausen, R.W., and D. F. Larcker. 1999. Corporate Governance, Chief

Executive Officer Compensation, and Firm Performance, Journal of Financial

Economics 51, 371-406.

34

Core, J. E, and W. Guay. 2002. Estimating the Value of Employee Stock Option

Portfolios and Their Sensitivities to Price and Volatility. Journal of Accounting

Research 40: 613-630.

Desai, M., Dharmapala, D., 2006. Corporate Tax Avoidance and High-Powered

Incentives. Journal of Financial Economics 79, 145–179.

Diether, K. B., Malloy, C.J., and A. Scherbina. 2002. Difference of Opinion and the

Cross Section of Stock Returns. The Journal of Finance 57: 2113–2141.

Dyreng, S. D., Hanlon, M., Maydew, E., 2008. Long-run Corporate Tax Avoidance.

The Accounting Review 83, 61–82.

Dyreng, S., Hanlon, M., and E. L. Maydew. 2010. The Effect of Executives on

Corporate Tax Avoidance. The Accounting Review 85:1163-1189.

Easley, D., and M. O’Hara. 2004. Information and the Cost of Capital. Journal of

Finance 59: 1553-1583.

Edmans, A. 2009. Blockholder Trading, Market Efficiency, and Managerial Myopia.

Journal of Finance 64: 2481-2513.

Edmans, A., X. Gabaix, and A. Landier. 2009. A Multiplicative Model of Optimal

CEO Incentives in Market Equilibrium. Review of Financial Studies 22: 4881-

4917.

Edmans, A., and G. Manso. 2011. Governance through Trading and Intervention: A

Theory of Multiple Blockholders. Review of Financial Studies 24: 2395-2428.

Edmans, A., V. Fang, and E. Zur. 2013. The Effect of Liquidity on Governance.

Review of Financial Studies, forthcoming.

Edwards, A., Schwab, C., and T. Shevlin. 2013. Financial Constraints and The

Incentives for Tax Planning, 2013 American Taxation Association Midyear

Meeting. Available at SSRN: http://ssrn.com/abstract=2216875

Fang, V., T. Noe, and S. Tice. 2009. Stock Market Liquidity and Firm Value. Journal

of Financial Economics 94: 150 – 169.

Fang, V., Tian, X., and S. Tice. 2013. Does Stock Liquidity Enhance or Impede Firm

Innovation? Journal of Finance, forthcoming

35

Foucault, T., and T. Gehrig. 2008. Stock Price Informativeness, Cross-Listings, and

Investment Decisions. Journal of Financial Economics 88: 146-168

Gompers, P., Ishii, J., and A. Metrick. 2003. Corporate Governance and Equity

Prices. Quarterly Journal of Economics 118: 107:156.

Gopalan, R., O. Kadan, and M. Pevzner. 2012. Asset Liquidity and Stock Liquidity.

Journal of Financial and Quantitative Analysis 47: 333-364.

Graham, J., and A. Tucker. 2006. Tax Shelters and Corporate Debt Policy. Journal of

Financial Economics 81: 563-594.

Graham, J.R., Hanlon, M., Shevlin, T., and N. Shroff. 2013. Incentives for Tax

Planning and Avoidance: Evidence from the Field. MIT Sloan Research Paper

No. 4990-12. Available at SSRN: http://ssrn.com/abstract=2148407

Grossman, S., and J. Stiglitz. 1980. On the Impossibility of Informationally Efficient

Markets. American Economic Review 70: 393:408

Hadlock, C.J., and J.R. Pierce. 2010. New Evidence on Measuring Financial

Constraints: Moving Beyond the KZ Index. Review of Financial Studies 23:1909-

1940.

Hanlon, M. 2005. The Persistence and Pricing of Earnings, Accruals, and Cash-Flows

When Firms Have Large Book-Tax Differences. The Accounting Review 80: 137-

166.

Hanlon, M., and S. Heitzman. 2010. A Review of Tax Research. Journal of

Accounting and Economics 50, 127-178.

Hasbrouck, J. 2009. Trading Costs and Returns for U.S. Equities: Estimating

Effective Costs from Daily Data. Journal of Finance 64: 1445-1477.

Jayaraman, S., and T. Milbourn. 2012. The Role of Stock Liquidity in Executive

Compensation. The Accounting Review 87: 537-563.

Jensen, M. C.1993. The Modern Industrial Revolution, Exit, and the Failure of

Internal Control Systems. Journal of Finance 48: 831-880.

36

Kaplan, S., and L. Zingales. 1997. Do Investment-cash flow Sensitivities Provide

Useful Measures of Financing Constraints? Quarterly Journal of Economics 112:

169-215.

Khana, N. and R. Sonti. 2004. Value Creating Stock Manipulation: Feedback Effect

of Stock Prices on Firm Value. Journal of Financial Markets 7: 237–270.

Kim, J-B., Li, Y., and L.Zhang. 2011. Corporate Tax Avoidance and Stock Price

Crash-a Firm-Level Analysis. Journal of Financial Economics 100: 639-662

Koenker, R., and G. Bassett. 1978. Regression Quantiles. Econometrica. 46: 33–50.

Koenker, R., and K.F. Hallock. 2001. Quantile Regression. Journal of Economic

Perspectives 15:143-156

Kyle, A. 1985. Continuous Auctions and Insider Trading. Econometrica 53: 1315-

1336

Lang, M. H., and R. J. Lundholm. 1996. Corporate Disclosure Policy and Analyst

Behaviour. The Accounting Review 71: 467-492.

Lesmond, D., 2005. Liquidity of emerging markets. Journal of Financial Economics

77: 411-452.

Lin, J.C., Singh, A.K., and W. Yu. 2009. Stock Splits, Trading Continuity, and the

Cost of Equity Capital. Journal of Financial Economics 93: 474-489.

Lisowsky, P. 2010. Seeking Shelter: Empirically Modeling Tax Shelters Using

Financial Statement Information. The Accounting Review 85, 1693-1720.

Maug, E. 1998. Large Shareholders as Monitors: Is There a Trade-Off between

Liquidity and Control? Journal of Finance 53: 65-98.

McGuire, S.T., Omer, T.C., and J.H. Wilde. 2013. Investment Opportunity Sets,

Operating Uncertainty and Capital Market Pressure: Determinants of Investments

in Tax Shelter Activities? The Journal of American Taxation Association,

forthcoming

Mehran, H. 1995. Executive Compensation Structure, Ownership, and Firm

Performance. Journal of Financial Economics 38: 163-84.

37

Mills, L., Erickson, M., and E. Maydew. 1998. Investments in tax planning. Journal

of the American Taxation Association. 20: 1-20.

Mosteller, F., and J. Tukey. 1977. Data Analysis and Regression: A Second Course in

Statistics. Reading, Mass.: Addison-Wesley.

Powell, J. 1989. Estimation of Monotonic Regression Models Under Quantile

Restrictions, in Non-parametric and Semiparametric Methods in Econometrics,

W. Barnett, J. Powell, and G. Tauchen, eds., Cambridge: Cambridge University

Press.

Rego, S.O., 2003. Tax-Avoidance Activities of US Multinational Corporations.

Contemporary Accounting Research 20: 805:833.

Rego, S. O., and R. Wilson, 2012. Equity Risk Incentives and Corporate Tax

Aggressiveness. Journal of Accounting Research 50: 775-810.

Shackelford, D. A., and T. Shevlin. 2001. Empirical Tax Research in Accounting.

Journal of Accounting and Economics 31: 312-387.

Subrahmanyam, A. and S. Titman. 2001. Feedback from Stock Prices to Cash Flows.

Journal of Finance 56: 2389–2413.

Whited, T., and G. Wu. 2006. Financial Constraints Risk. Review of Financial Studies

19: 531-559.

Wilson, R. 2009. An examination of corporate tax shelter participants. The

Accounting Review 84: 969-999.

Zhang, X. F. 2006. Information Uncertainty and Stock Returns. The Journal of

Finance 61: 105-137.

38

Appendix A. Variables and Definitions

Characters in parentheses refer to the item name in the Compustat database.

Abnormal accruals

(ABACC)

Absolute value of abnormal accruals, estimated following Kothari et

al. (2005).

Cash effective cash rate

(CETR)

Taxes paid in cash (TXPD) plus tax benefits of stock options

(TXBCO+TXBCOF) scaled by pretax income (PI).

Cash holdings

(CASH) Cash and cash equivalents (CHE) scaled by lagged total assets (AT).

CEO Power

(CEO_POWER)

Principal component of boar size, CEO-Chairman duality, and board

independence. Board size is the natural log of the number of

directors in the board. CEO-Chairman duality is a dummy variable

equal to one if the CEO and the Chairman of the board is the same

person and zero otherwise. Board independence is the proportion of

independent directors in the board.

Change in goodwill

(POSGDWL)

Change in goodwill (GDWL) scaled by lagged total assets (AT). If

the value is negative, then it is set to zero.

Change in loss carryforward

(DNOL_AT)

Change in net operating loss carry forwards (TLCF) over year t

scaled by lagged total assets (AT).

Core-Guay Pay-for-

performance sensitivity

(PPS_CG)

Dollar change in CEO stock and option compensation with respect

to 1% change in share price, estimated following Core and Guay

(2002).

Dispersion of analyst forecasts

(DISP) Standard deviation of analyst earnings forecasts.

Edmans-Gabaix-Landier Pay-

for-performance sensitivity

(PPS_EGL)

Dollar change in CEO wealth for a one hundred-percentage point

change in firm value divided by annual flow compensation,

estimated following Edmans et al. (2009).

Equity income in earnings

(EQINC)

Equity income in earnings (ESUB) scaled by lagged total assets

(AT).

Firm size

(SIZE) Log of market value of equity (PRCC_F×CSHO).

Foreign assets

(FRGNAT) Proportion of foreign assets, estimated following Oler et al. (2007).

Foreign income dummy

(DFI)

An indicator variable set equal to 1 for firm observations reporting

foreign income (PIFO) in year t and zero otherwise;

Governance index

(GINDEX) Governance index of Gompers et al. (2003)

GAAP effective tax rate

(GETR) Income taxes (TXT) scaled by pretax income (PI).

Intangible assets

(INTANG) Intangible assets (INTAN) scaled by lagged total assets (AT).

Leverage

(LEV) Long term debt (DLTT) scaled by total assets (AT).

Long-run cash effective tax rate

(LCETR)

Sum of taxes paid in cash (TXPD) over the last three years scaled

by the sum of pretax income (PI) over the same period.

Loss carryforward dummy

(NOL)

An indicator variable that equals one if net operating loss carry

forwards (TLCF) is positive for year t-1.

Market-to-book

(MB)

Market value of equity (PRCC_F×CSHO) divided by book value of

equity (CEQ).

New Investments

(NEWINV)

New investment, calculated as Compustat (XRD+CAPX+AQC-

SPPE -DPC) scaled by lagged total assets (AT).

PPE assets

(PPE)

Net property, plant and equipement (PPENT) scaled by lagged total

assets (AT).

Residual book-tax difference

(RBTD)

The residual from regression of book-tax difference on firm’s total

accruals (Desai and Dharmapala, 2006). Regression is performed

cross-sectionally for each year and 2-digit SIC code.

39

ROA volatility

(STDROA) Standard deviation of ROA over the past five years.

Return on assets

(ROA) Pre-tax income (PI) divided by lagged total assets (AT).

Stock liquidity

(LIQ)

Minus one times natural logarithm of the relative effective spread.

Relative effective spread is calculated as the difference between the

trade price and the midpoint of the bid-ask quote divided by the

trade price.

Stock liquidity composite

measure

(LIQ_PC)

A principal component of the Amihud (2002) illiquidity measure,

Hasbrouck (2009) implicit bid-ask spread and Lesmond (2005)

percentage of zero-returns

Whited-Wu index

(WW) Financial constraint index proposed by Whited and Wu (2006).

40

Figure 1

Stock liquidity across GAAP effective tax rate deciles

We plot mean values of stock liquidity lagged one year against decile ranks of GAAP effective tax rate

(GETR). Stock liquidity is lagged one year to alleviate endogeneity concerns. Our initial sample

consists of all the firms in the Compustat database over the period 1993-2010. We merge the sample

with the stock liquidity measures generated from the Trade and Quote (TAQ) database and stock

returns from CRSP. All the variables are winsorized at both the 1st and 99

th percentiles Definitions of

the variables are provided in Appendix A.

4.8

5

5.2

5.4

5.6

5.8

6

6.2

1 2 3 4 5 6 7 8 9 10

Sto

ck li

qu

dit

y

GETR decile rank

41

Figure 2

Stock liquidity coefficients for various percentiles of the GAAP effective tax rate

We estimate quantile regressions of GAAP effective tax rate on stock liquidity and control variables

for 10-th, 15-th…90-th percentile of GAAP ETR. The estimated coefficients for stock liquidity (solid

line) and the 95% confidence intervals (dashed lines) are plotted against the estimation quantiles. Our

initial sample consists of all the firms in the Compustat database over the period 1993-2010. We merge

the sample with the stock liquidity measures generated from the Trade and Quote (TAQ) database and

stock returns from CRSP. All the variables are winsorized at both the 1st and 99

th percentiles

Definitions of the variables are provided in Appendix A.

-0.02

-0.01

0

0.01

0.02

0.03

0.04

10 20 30 40 50 60 70 80 90Sto

ck L

iqu

idit

y C

oe

ffic

ien

t

GETR percentile

42

Table 1

Summary statistics

Mean S.D. 10% Median 90%

GETR 0.296 0.185 0.024 0.348 0.427

LIQ 5.763 1.302 4.069 5.724 7.555

CASH 0.186 0.267 0.008 0.088 0.486

ROA 0.099 0.154 -0.015 0.088 0.249

STDROA 0.117 0.351 0.014 0.053 0.206

PPE 0.331 0.294 0.036 0.247 0.759

POSGDWL 0.021 0.065 0.000 0.000 0.055

SIZE 6.182 2.008 3.546 6.158 8.965

NOL 0.290 0.454 0.000 0.000 1.000

NEWINV 0.085 0.165 -0.019 0.038 0.233

MB 2.882 3.950 0.859 2.039 5.636

LEV 0.172 0.180 0.000 0.129 0.412

INTANG 0.133 0.196 0.000 0.043 0.405

FRGNAT 0.440 0.694 0.000 0.000 1.000

EQINC 0.001 0.006 0.000 0.000 0.003

DNOL_AT 0.005 0.122 -0.011 0.000 0.016

DFI 0.340 0.474 0.000 0.000 1.000

ABACC 0.079 0.094 0.009 0.053 0.172

Obs. 34,221

This table presents the mean, standard deviation (S.D.), 10th percentile (10%), median, and 90th

percentile (90%) of the variables. Our initial sample consists of all the firms in the Compustat database

over the period 1993-2010. We merge the sample with the stock liquidity measures generated from the

Trade and Quote (TAQ) database and stock returns from CRSP. All the variables are winsorized at

both the 1st and 99

th percentiles Definitions of the variables are provided in Appendix A.

43

Table 2

Correlation matrix

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11) (12) (13) (14) (15) (16) (17)

(1) GETR 1.000

(2) LIQ 0.029 1.000

(3) CASH -0.093 -0.002 1.000

(4) ROA 0.148 0.125 0.176 1.000

(5) STDROA -0.093 -0.060 0.204 -0.034 1.000

(6) PPE 0.025 0.032 0.032 0.016 -0.072 1.000

(7) POSGDWL 0.047 0.080 0.080 0.047 0.031 -0.017 1.000

(8) SIZE 0.069 0.788 -0.016 0.156 -0.082 0.109 0.058 1.000

(9) NOL -0.094 0.124 0.048 -0.112 0.035 -0.091 0.066 0.049 1.000

(10) NEWINV -0.005 0.030 0.188 0.067 0.076 0.245 0.422 0.040 0.032 1.000

(11) MB -0.034 0.138 0.214 0.204 0.084 -0.035 0.009 0.206 0.015 0.110 1.000

(12) LEV -0.007 0.070 -0.321 -0.183 -0.075 0.322 0.060 0.091 0.027 0.032 -0.080 1.000

(13) INTANG 0.089 0.222 -0.075 0.002 0.018 -0.178 0.589 0.147 0.144 0.274 -0.001 0.175 1.000

(14) FRGNAT -0.099 0.269 0.119 -0.019 0.036 -0.109 0.033 0.263 0.218 0.036 0.042 -0.079 0.082 1.000

(15) EQINC -0.028 0.085 -0.052 0.082 -0.029 0.029 -0.001 0.114 -0.029 -0.022 0.018 0.022 -0.021 0.040 1.000

(16) DNOL_AT -0.021 0.003 0.022 -0.153 0.046 0.007 0.042 -0.002 0.121 0.033 0.030 0.005 0.035 0.021 -0.016 1.000

(17) DFI 0.009 0.270 0.037 0.001 -0.019 -0.158 0.051 0.244 0.205 0.038 0.037 -0.046 0.119 0.434 0.009 0.013 1.000

(18) ABACC -0.029 -0.064 0.254 0.028 0.121 -0.015 0.067 -0.071 0.0203 0.198 0.151 -0.086 0.014 0.011 -0.008 0.009 -0.027

This table presents the correlation matrix of the variables. Our initial sample consists of all the firms in the Compustat database over the period 1993-2010. We merge the

sample with the stock liquidity measures generated from the Trade and Quote (TAQ) database and stock returns from CRSP. All the variables are winsorized at both the 1st

and 99th

percentiles Definitions of the variables are provided in Appendix A.

44

Table 3

Tax avoidance and stock liquidity: main results

This table presents the results of regressing GAAP effective tax rate (GETR) on stock liquidity. Our

initial sample consists of all the firms in the Compustat database over the period 1993-2010. We merge

the sample with the stock liquidity measures generated from the Trade and Quote (TAQ) database and

stock returns from CRSP. All the variables are winsorized at both the 1st and 99

th percentiles

Definitions of the variables are provided in Appendix A. Constant, industry fixed effects based on two-

digit SIC codes, and year fixed effects are included in all regressions. The regressions are performed by

quantile regression method, with the z-statistics (in parentheses) computed using Powel (1989)

standard errors. The independent variables are lagged one year in all the regressions. ***, ** and *

denote statistical significance at the 1%, 5% and 10% levels, respectively

Raw liquidity Decimalized liquidity

Dependent

Variable: GETR GETR GETR GETR GETR GETR

Percentile 10 50 90 10 50 90

(1) (2) (3) (4) (5) (6)

LIQ 0.028 0.003 -0.013 0.011 0.001 -0.004

(6.258)*** (3.976)*** (-7.941)*** (7.016)*** (5.074)** (-5.981)***

CASH -0.118 -0.039 0.019 -0.118 -0.039 0.018

(-7.319)*** (-10.31)*** (3.406)*** (-7.217)*** (-10.47)*** (3.186)***

ROA 0.414 0.138 -0.045 0.404 0.137 -0.049

(18.01)*** (17.71)*** (-4.858)*** (17.39)*** (17.72)*** (-4.898)***

STDROA -0.108 -0.028 0.014 -0.102 -0.028 0.015

(-5.834)*** (-8.152)*** (0.692) (-2.469)** (-8.307)*** (0.771)

PPE -0.035 0.001 -0.019 -0.028 0.000 -0.021

(-2.935)*** (0.356) (-4.245)*** (-2.297)** (0.241) (-4.704)***

POSGDWL -0.067 -0.011 -0.038 -0.077 -0.009 -0.042

(-1.625) (-1.403) (-2.064)** (-1.897)* (-1.152) (-2.292)**

SIZE 0.011 -0.002 0.002 0.011 -0.002 0.000

(5.095)*** (-4.045)*** (2.243)** (5.301)*** (-4.852)*** (0.439)

NOL -0.058 -0.006 0.007 -0.058 -0.006 0.007

(-10.60)*** (-4.899)*** (2.689)*** (-10.32)*** (-5.039)*** (2.705)***

NEWINV 0.014 -0.025 -0.008 0.011 -0.026 -0.005

(0.869) (-6.227)*** (-1.179) (0.594) (-6.314)*** (-0.691)

MB -0.004 -0.001 -0.000 -0.004 -0.001 -0.000

(-7.071)*** (-6.480)*** (-1.106) (-6.906)*** (-6.484)*** (-0.853)

LEV -0.113 0.001 0.031 -0.114 0.002 0.030

(-7.299)*** (0.322) (4.309)*** (-7.466)*** (0.414) (4.291)***

INTANG 0.077 0.049 0.065 0.085 0.049 0.063

(4.034)*** (15.01)*** (6.682)*** (4.519)*** (14.86)*** (6.494)***

FRGNAT -0.028 -0.031 0.009 -0.028 -0.031 0.009

(-7.832)*** (-23.36)*** (2.697)*** (-7.808)*** (-23.35)*** (2.582)***

EQINC -1.625 -0.787 -0.830 -1.588 -0.786 -0.791

(-5.193)*** (-7.953)*** (-7.305)*** (-5.433)*** (-7.897)*** (-6.286)***

DNOL_AT 0.033 -0.002 0.034 0.029 -0.002 0.034

(2.212)** (-0.135) (2.016)** (2.188)** (-0.116) (2.031)**

DFI 0.016 0.003 0.008 0.017 0.003 0.009

(3.230)*** (2.676)*** (3.180)*** (3.567)*** (2.573)*** (3.395)***

ABACC -0.048 0.001 0.015 -0.043 0.000 0.015

(-1.567) (0.197) (1.309) (-1.499) (0.042) (1.303)

Obs. 34,221 34,221 34,221 34,221 34,221 34,221

Adj. Pseudo R2 0.156 0.107 0.042 0.157 0.106 0.041

45

Table 4

Tax avoidance and stock liquidity: robustness tests

Dependent variable: Tax Avoidance

Percentile: 10 50 90

Panel A. Alternative tax avoidance measures (1) Annual effective cash tax-rate 0.006 0.004 -0.013

(2.755)*** (2.029)** (-2.299)**

(2) Long-term effective cash tax-rate 0.008 0.004 -0.016

(3.115)*** (2.244)** (-3.003)***