stock transfer restrictions and the close corporation--a

TRANSCRIPT

Hastings Law Journal

Volume 17 | Issue 3 Article 9

1-1966

Stock Transfer Restrictions and the CloseCorporation--A Statutory ProposalGilbert N. Kruger

Follow this and additional works at: https://repository.uchastings.edu/hastings_law_journal

Part of the Law Commons

This Comment is brought to you for free and open access by the Law Journals at UC Hastings Scholarship Repository. It has been accepted forinclusion in Hastings Law Journal by an authorized editor of UC Hastings Scholarship Repository.

Recommended CitationGilbert N. Kruger, Stock Transfer Restrictions and the Close Corporation--A Statutory Proposal, 17 Hastings L.J. 583 (1966).Available at: https://repository.uchastings.edu/hastings_law_journal/vol17/iss3/9

COMMENTSSTOCK TRANSFER RESTRICTIONS AND THE

CLOSE CORPORATION-A STATUTORYPROPOSAL

By Gn.ERT N. KRUGER*

INTRODUCTION-THE CLOSE CORPORATION

THE importance of the closely held corporation (also known as thefamily corporation and the "incorporated partnership") seems tohave been obscured by the shadow of its big brother, the publiclyheld corporation. Although the earliest corporations were in reality"incorporated partnerships," formed to attain limited liability for theincorporators, it was the growth in stature of the larger, publicly heldcorporations at which legislation was directed.1 It was only naturalthat statutes were designed to protect the investing public as the gapbetween ownership and management in publicly held corporationsgrew wider.

Unfortunately however,

Statutes and judicial decisions, in laying down rules for the gov-ernance of corporations, have not distinguished between public issueand close corporations. As the nature and methods of operationsof publicly held and closely held corporations are utterly different,the result has been that many of the concepts and principles ofcorporate law (undoubtedly developed with public issue corpora-tions primarily in mind) are ill-adapted to closely held enterprises.In Great Britain and the countries of continental Europe, "private"companies are governed by special legislative rules; but in thiscountry, as a general proposition, the same rules are applied to allcorporations mdiscrmnnately 2

The close corporation is a highly desirable business form whichhas achieved widespread existence despite the comparative matten-tion paid to it by legislatures and courts. It is largely due to the inge-nuity of the corporate attorney that the close corporation has devel-oped and gamed acceptance. 3 Although divergent approaches have

*Member, Third Year Class.SO'NeaL Foreword to Note, A Plea for Separate Statutory Treatment of the Close

Corporation, 33 N.Y.U.L. Ev. 700 (1958).2Id. at 701.3 Ibid.

[5831

been used in attempts to define a close corporation, the singular intenthas been to differentiate it from the publicly held corporation.4

Although there are several distinguishing features of importance,two are most significant. A close corporation is generally character-ized by identity of ownership and management, as the shareholdershave a direct hand in corporate admimstration. In the publicly heldcorporation, on the other hand, the shareholders have practicallynothing to do with the management of corporate affairs. Managementis left to the board of directors, which is elected by the shareholdersfor this purpose. Additionally, since the "partners" work intimatelyin the daily operation of the business, they must be free to choosetheir own associates. It is a necessity in the close corporation thatthe parties mold themselves into a cohesive work group. Shares inthe publicly held corporation must be freely transferable becausethey are sold to the investing public. This requirement of free trans-ferability naturally eliminates the possibility of selecting one's co-owners in the publicly-held corporation. There would seem to be nogood reason why the shareholders of the publicly held corporationwould want to choose their co-shareholders, while in the close cor-poration the opportunity to choose is essential.

The striking resemblance between a partnership and a close cor-poration is the source of the phrase "incorporated partnership." Theclose corporation is a business form in which the participants acttowards each other as if they were partners, while adopting the cor-porate form to obtain its advantages. Once this corporate form hasbeen established the conduct of the associates between themselves,as distinguished from what the business entity looks like to third par-ties and the state, is what really concerns the "partners." Their desireis to have the close corporation remain close.5 Restricting the avail-ability of shares to outsiders is the most effective way to retain thiscloseness.

Use of the stock transfer restriction in the close corporation is

4 Winer, Proposing a New York "Close Corporation Law," 28 CORNELL L.Q. 313(1943), suggests that a close corporation be defined as one with one to five ultimateshareholders; The English Companies Act, 1948, 11 & 12 Geo. 6, c. 38, § 28(1)(b),defines a "private" company (close corporation) as one which 'limits the number ofits members to fifty ", Under the INT. REV. CODE OF 1954, § 1371(a)(1), "asmall business corporation" is defined as one "which does not have more than 10shareholders."

5 An early and classic statement to this effect is one by Holmes in Barrett v. King,181 Mass. 476, 479, 63 N.E. 934, 935 (1902)- "Stock in a corporation is not merelyproperty. It also creates a personal relation analogous otherwise than technically to apartnership. [T]here seems to be no greater objection to retaining the right ofchoosing one's associates in a corporation than in a firm."

6 A partial bibliography of materials dealing with stock transfer restrictions and

THE HASTINGS LAW JOURNAL [Vol. 17

indispensable for insuring continued closeness. It is the purpose ofthis comment to examine the stock transfer restriction in light of itsimportance to the close corporation, and to indicate the need forlegislative attention to the difficulties attorneys and courts encounterin working with stock transfer restrictions under present statutes andprecedents.

That the subject is of more than academic interest is underscoredby the fact that there are at present in excess of 18,000 new corporatefilings each year in California alone.7 Although separate figures forclose corporations are not available it is highly probable that the greatmajority of filings are for closely held corporations. 8

THE STOCK TRANSFER RESTRICTION IN RELATIONTO THE CLOSE CORPORATION

Stock transfer restrictions have been aptly referred to as "a sort ofpre-emptive right." Most commonly, either the existing stockholdersor the corporation or both in succession are given the first opportunityto purchase the shares offered by a selling shareholder. The effect ofthis first option or right of first purchase is to give the existing share-holders the power to "veto the admission of a new participant."10

close corporations includes: 1 HoNsTmN, CoRsonxoN LAw Aim PRACTCE §§ 191-210(1959); 2 O'NEA., CLOSE ConwoRa'xoNs 2-80 (1958); Cataldo, Stock TransferRestrictions and Closed Corporations, 37 VA. L. tnv. 229 (1951); Cower, SomeContrasts Between British and American Corporation Law, 69 HAmv. L. Rnv. 1369(1956); Hornstem, Judicial Tolerance of the Incorporated Partnership, 18 LAw &Corrmax. PRoB. 435 (1953); Hornstem, Stockholders' Agreements in the Closely HeldCorporation, 59 YALE L.J. 1040 (1950); Israels, The Close Corporation and the Law, 33CORNELL L.Q. 488 (1948); O'Neal, Developments in the Regulation of the CloseCorporation, 50 CoRNELL L.Q. 641 (1965); O'Neal, Restrictions on Transfer of Stockin Closely Held Corporations: Planning and Drafting, 65 H-Rv. L. tEv. 773 (1952);Oppenhem, The Close Corporation in California-Necessity of Separate Treatment, 12HAs=rns L.J. 227 (1961); Painter, Stock Transfer Restrictions: Continuing Uncertaintiesand a Legislative Proposal, 6 VmL. L. REv. 48 (1960); Winer, Proposing a New YorkClose Corporation Law, 28 CoRnNrz L.Q. 313 (1948); Annot., 2 A.L.R.2d 745 (1948);Annot., 61 A.L.R.2d 1318 (1958).

7 Letter from Ralph R. Martig, Semor Counsel and Deputy, Office of theCaliforma Secretary of State, to the Hastings Law Journal, December 10, 1965.

8 See Dykstra, Molding the Utah Corporation: Survey and Commentary, 7 UTwaL. REv. 1 (1960): "[Tlhe author undertook a study of fifty corporation charters toascertain the drafting practices followed by lawyers m respect to such documents. Whilethese charters were ified on behalf of Utah corporations, there is no reason to supposethat they are umque. In appraising these observations, it is unportant to note thatforty-two of the articles of incorporation were apparently drafted for small closely-heldenterprises."

9 Allen v. Biltmore Tissue Corp., 2 N.Y.2d 534, 543, 141 N.E.2d 812, 816, 161N.Y.S.2d 418, 424 (1957).

10 Ibid.

Marcha, 1966] COMMENTS

THE HASTINGS LAW JOURNAL

Such a restriction can be placed m the bylaws,"' the articles of mcor-poration,' s or a shareholders' agreement. 3

Although the phrase "preemptive right" is associated in corpora-tion law with the right of shareholders to have the first opportunityto buy new stock issued by the corporation, exercising rights undera stock transfer restriction is also a preemptive right. In the close cor-poration the right of first purchase is given to the corporation or theshareholders or both m succession and generally applies to shareswhich have already been issued. In the publicly held corporation, thepreemptive right (where it exists) invariably extends to new issues ofshares and runs only to the existing shareholders.' 4 Putting these dis-tinctions aside, it is clear that rights created by the stock transferrestriction are preemptive rights.' 5

Not all stock transfer restrictions are valid. The earliest cases con-cerning transfer restrictions in the United States held them invalid.16

The theory was that a share of stock is a property right and the re-striction amounts to an unreasonable restraint on the alienation ofproperty 17 On the other hand, 'English law has always regardedshares of stock as creatures of the company's constitution and there-fore as essentially contractual choses in action," 18 not subject to therules against restraints on alienation.

The present test for validity of a stock transfer restriction iswhether it is reasonable. It cannot amount to a total prohibitionagainst transfer because of the rule against restraints. Additionally,many courts hold unreasonable, on public policy grounds, stock trans-fer restrictions which give the present shareholders or the board ofdirectors the power to veto the admittance of a new shareholder.' 9

1 Tu-Vu Drive-In Corp. v. Ashkms, 61 Cal. 2d 283, 38 Cal. Rptr. 348, 391 P.2d828 (1964).

12 Monacan Hills v. Page, 203 Va. 110, 122 S.E.2d 654 (1961).13 Guaranty Laundry Co. v. Pulliam, 198 Okla. 667, 181 P.2d 1007 (1947).1 4

LATTn, ConPonrnoNs 424 (1959).15 According to Blackstone, the King "had the profitable prerogative of purveyance

and pre-emption: which was a right enjoyed by the crown of buying up provisions andother necessaries, by the intervention of the king's purveyors, for the use of his royalhousehold, at an appraised valuation, in preference to all others, and even withoutconsent of the owner " 1 JoNm' Br.cxsToNE 418 (1915).

16Victor J. Bloede Co. v. Bloede, 84 Md. 129, 34 Aft. 1127 (1896); Bunkerhoff-Farris Trust & Sav. Co. v. Home Lumber Co., 118 Mo. 447, 24 S.W 129 (1893);Ireland v. Globe Milling Co., 21 R.I. 9, 41 At. 258 (1898).

17 Tracey v. Franklin, 31 Del. Ch. 477, 67 A.2d 56 (Sup. Ct. 1949).18 Gower, Some Contrasts Between British and American Corporation Law, 69

HAv. L. REv. 1369, 1377 (1956).19 The American courts have been in conflict on this point, although the later cases

seem to sustain the validity of these "consent restraints." See O'Neal, Restrictions onthe Transfer of Stock in Closely Held Corporations: Planning and Drafting, 65 HAnv.L. REv. 773, 780 (1952).

[V9ol. 17

There is no doubt that today in the United States reasonable stocktransfer restrictions (such as rights of first purchase held by the cor-poration or the shareholders or both) are almost everywhere heldvalid.20 Now that the validity of reasonable restrictions has becomefirmly entrenched, recent cases indicate a shift of emphasis. Presentattention seems to be focusing on a determination as to whetheramendments to bylaws or articles of incorporation, either adoptingrestrictions for the first time or eliminating those already included,are valid. 1 A second broad area of difficulty is one that has been pre-sent from the beginning-judicial interpretation of the language usedin creating the restrictions. The material to follow will analyze each ofthese problem areas in trn, and a statutory solution will be suggested.

ADDING OR DELETING STOCK TRANSFERRESTRICTIONS BY AMENDMENT

An examination of some recent cases, principally cases from Cali-fornia, will illustrate the difficulty of adding or deleting stock transferrestrictions by amendment of the bylaws or articles.

Casady v. Modern Metal Spinning & Mfg Co.22 involved a closecorporation whose bylaws contained a typical right of first purchase.Plaintiff had brought a divorce proceeding against her husband, whoowned one half of the corporate stock. A property settlement agree-ment declared that plaintiff should be entitled to one half of theshares held by the husband. The corporation refused to issue theshares to plaintiff, pointing to the stock transfer restriction in thebylaws. The district court of appeal refused plaintiff's request for acourt order to force a meeting of the board of directors for the pur-pose of voting to delete the restriction. The court relied on an earlierline of cases23 winch also refused amendments of the bylaws eventhough a statute 4 explicitly permits amendment. The rationale wasthat some bylaws create contractual rights which cannot be destroyedwithout the consent of all the parties to the agreement.25

In Silva v. Coastal Plywood & Timber Co.2 6 the articles of incor-

20 Id. at 780-81.2 1 See, e.g., Tu-Vu Dnve-In Corp. v. Ashkms, 61 Cal. 2d 283, 38 Cal. Rptr. 348,

391 P.2d 828 (1964); Casady v. Modem Metal Spinning & Mfg. Co., 188 Cal. App. 2d728, 10 Cal. Rptr. 790 (1961); Silva v. Coastal Plywood & Timber Co., 124 Cal. App. 2d276, 268 P.2d 510 (1954); Bechtold v. Coleman Realty Co., 367 Pa. 208, 79 A.2d 661(1951); Sandor Petroleum Corp. v. Williams, 321 S.W.2d 614 (Tex. Civ. App. 1959).

22 188 Cal. App. 2d 728, 10 Cal. Rptr. 790 (1961).2 3 Bennett v. Hiberia Bank, 47 Cal. 2d 540, 305 P.2d 20 (1956); State v. San

Francisco Say. Etc. Soc., 66 Cal. App. 53, 225 Pao. 309 (1924); Bornstein v. DistrictGrand Lodge No. 4, 2 Cal. App. 624, 84 Pac. 271 (1906).

24 CAL. Conp. CODE § 501(g).25 188 Cal. App. 2d 728, 734, 10 Cal. Rptr. 790, 794 (1961).26 124 Cal. App. 2d 276, 268 P.2d 510 (1954).

March, 1966] COMMENTS

THE HASTINGS LAW JOURNAL

poration provided that only one share of stock could be issued to orowned by any stockholder. The corporation had financial difficultiesand filed for reorgamzation under Chapter X of the Bankruptcy Act.27

Plaintiffs, the minority shareholders, sought an injunction against pro-posed majority-shareholder action eliminating the restrictions. Thecorporation was organized under the laws of Nevada. The districtcourt of appeal upheld the majority's action in amending the articlesto eliminate the restriction. Under the Nevada statute, which is to thesame effect as that of California, amendments to the articles are per-mitted.2 8 Since the amendment fell within the scope of the statute itwas held valid, notwithstanding the minority's clai that they had avested contractual right in retaining the restriction.2 9

As stated by the court in Tu-Vu Drtve-In Corp. v. Ashkrns,30 "Thiscase presents the issue of whether a corporation may enforce a bylawrestricting the alienation of stock against a non-consenting shareholderwho acquired his stock prior to the enactment of the bylaw "3 ' Neitherthe original articles nor bylaws contained any stock transfer restric-tions. The supreme court upheld the action of the board of directorsin amending the bylaws to include a restriction after the minorityshareholder, defendant in this declaratory judgment action, had at-tempted to sell the shares to a business competitor. The court basedits decision on two sections of the California Corporations Code.Section 500 permits amendments of the bylaws32 and section 5 01(g)permits "reasonable restraints upon the right to transfer or hypothe-cate shares" in the bylaws.38 Most of the opinion was devoted to deter-mining whether the restriction was "reasonable" as required by sec-tion 501(g) A two-pronged test was set forth: first, whether therestriction would be a prohibitive restraint on the right of alienationand second, whether the restriction would "unreasonably deprive theshareholder of 'substantial rights.'-34 Both tests were resolved in

27 52 Stat. 883 (1938), 11 U.S.C. § 501-676 (1964).28 NE v. REv. STAT. § 78.385(1) (c) (1957) provides that a corporation may amend

its articles of incorporation by "increasing, decreasing or reclassifying its authorizedcapital stock by changing the number, par value, designations, preferences or thequalifications, limitations or restrictions of its shares

29 Silva v. Coastal Plywood & Timber Co., 124 Cal. App. 2d 276, 279, 268 P.2d510, 512 (1954).

30 61 Cal. 2d 283, 38 Cal. Rptr. 348, 391 P.2d 828 (1964), noted, 53 CALI. L.REv. 692 (1964).

31 Id. at 284, 38 Cal. Rptr. at 349, 319 P.2d at 829.3 2 CAL. Cor,. CODE § 500 provides in part: "By-laws may be adopted, amended

or repealed by the vote or the written assent of shareholders entitled to exercise amajority of the voting power of the corporation.

33 CAL. CoRn,. CoDE § 501 provides: "The by-laws of a corporation may makeprovisions not in conflict with law or its articles for: (g) Special qualifications ofpersons who may be shareholders, and reasonable restrictions on the right to transfer orhypothecate shares."

34 61 Cal. 2d at 286, 38 Cal. Rptr. at 350, 391 P.2d at 830 (1964).

[Vol. 17

favor of the action which had been taken by the board of directors-the first because a right of first purchase is not "unreasonably restric-tive"35 and the second because the purpose or benefit to the corpora-tion (preventing the sale of shares to a business competitor) out-weighed the impairment of the rights of the complaining shareholderto hold his shares free of the restriction .3

Each of these cases involved a determination as to whether, at adate subsequent to incorporation, the bylaws or articles could beamended either to delete or add stock transfer restrictions. It hasbeen found difficult to reconcile the opinions in these decisions. As amatter of generalization it seems safe to say that the Califorma courtshave attempted to reach desirable results by choosing from amongseveral available approaches, none of which is directly applicable. 7

In Casady, the court refused to order the deletion of the stocktransfer restriction from the bylaws, apparently feeling no compellingneed to disrupt the corporate structure in order to satisfy the termsof a property settlement agreement. The court emphasized the con-tractual nature of stock transfer restrictions. Where an amendment ofarticles to eliminate a stock transfer restriction was necessary to ef-fectuate a program of corporate reorgamzation, as in Silva, the courtupheld the deleting amendment. Here reliance was placed on statutorylanguage permitting amendment of the articles. In Tu-Vu, the courtupheld an amendment of the bylaws creating a stock transfer restric-tion not found in the original bylaws. In so doing, it forestalled a po-tential transfer of a minority shareholder's interest to a business com-petitor. Here, as in Silva, stress was put on the language of the statutepermitting amendment.

It is interesting to note that the court in Casady failed to cite theSilva case, while the court in Tu-Vu relied on Silva, but omitted anyreference to Casady. It would appear that these cases were all similarenough to merit at least a distinguishing discussion.

In the light of the Tu-Vu decision, would the Califorma SupremeCourt reach the same result where the bylaw amendment induced bythe majority shareholder was designed to prevent a transfer of sharesto a fellow shareholder rather than a business competitor? The courtin Tu-Vu stated that

Bylaws restricting transfer in closed corporations are frequentlyessential to a successful enterprise; they perform an important func-tion in precluding unwanted intrusions by outsiders; they preservethe integrity of the functionmg entity Such bylaws are "necessary

85 Ibid.35 Id. at 287, 38 Cal. Rptr. at 350, 391 '.2d at 830. Contra, Sandor Petroleum

Corp. v. Williams, 321 S.W.2d 614 (Tex. Civ. App. 1959).37 CAL. CoPX. CODE § 501(g) provides that stock transfer restrictions may appear

in the bylaws, but there is no specific indication that they may be adopted byamendment at a date subsequent to incorporation.

Marcha, 1966] COMMENTS

for the protection of the corporation and its stockholders againstrivals in business or others who might purchase its shares for the pur-pose of acquiring information which might thereafter by used againstthe interest of the company "38

A court faced with this variation of the Tu-Vu situation would haveto decide whether a transfer to another stockholder, rather than abusiness competitor (as in Tu-Vu), was sufficiently harmful to thecorporation to justify the bylaw amendment. Such a determinationmight present a difficult factual problem for the court. An alternativeapproach would be to hold the bylaw amendment sanctioned bystatute and dispense with the case on this ground, as was done inSilva and Tu-Vu.

A second modification of the Tu-Vu fact pattern would appear topresent an even greater potential problem. In Bechtold v. ColemanRealty Co.3 9 the court was faced with the question of determiningwhether a majority shareholder could induce an amendment to thebylaws which would delete a stock transfer restriction. The majorityshareholder's purpose in doing this was to sell to an outsider who wasnot a business competitor of the corporation. The court m Bechtolddivided corporate bylaws into two classes, (a) those that are merelyregulatory and (b) those that are in the nature of a contract whichvests property rights in all the shareholders. 40 The stock transfer re-striction was placed m the second class, thereby preventing its dele-tion without the consent of all the other stockholders whose rightswere affected 41 Would the Califorma supreme court reach the sameresult? It will be remembered that in Silva the court upheld an amend-ment of the articles eliminating a stock transfer restriction becausesuch an amendment was sanctioned by statute as a regulatory matter.Although that decision would be good case law precedent for the sameresult here, it is doubtful whether the Califorma supreme court wouldfollow the rationale of Silva in this situation. In Silva the corporationwas reorganizing under the Bankruptcy Act and it was essential thatnew stockholders with fresh capital be admitted. No correspondingneed is present under these facts.

A possible basis for rejecting the amendment deleting the restric-tion would be to hold, as did Bechtold, that the minority shareholdershad a contractual or "vested" right to hold their shares with the restric-tion intact. The district court of appeal upheld the minority share-holder's "vested right" contention in Tu-Vu.42 The California supreme

38 61 Cal. 2d at 287, 38 Cal. Rptr. at 350, 391 P.2d at 830. (Emphasis added.)39 367 Pa. 208, 79 A.2d 661 (1951). Accord, Cowles v. Cowles Realty Co., 201 App.

Div. 460, 194 N.Y.S. 546 (1922).40 367 Pa. at 213, 79 A.2d at 663 (1951).41 Tbd.42The trial court found that the minority shareholder had a vested right to hold

[VoL. 17THE HASTINGS LAW JOURNAL

court reversed the district court of appeal, holding that "The share-holder thus acquires his shares subject to the power of the corpora-tion to alter its contract with hzm pursuant to statutory authority 4 sThis broad statement rejecting the argument that certain bylawscreate contractual rights would apparently foreclose the supremecourt from protecting the minority shareholders on this basis, shouldthe Bechtold case arise in California.

The court's strongest position in refusing the proposed amend-ment ught be to hold that the majority shareholder owes a fiduciaryduty to the minority shareholders. The ivocation of this equitableprmciple in many analogous cases represents a growing trend in cor-poration law44 Using tis approach, the court would look to the goodfaith of the majority shareholder and could set aside the attemptedelimination of the stock transfer restriction on the basis of a findingof unfair dealing for personal gain. "But fraud and fair dealing areunfortunately not self-explanatory; even sensitive consciences willvary in their reaction to a given situation."45 In other words, here toothe court would be faced with a difficult factual determination.

The element common to each of the above fact situations was theabsence of statutory language which definitively dealt with all of thefacts. The courts were forced to deal with corporation statutes satis-factory for handling ordinary amendments of bylaws or articles butentirely inadequate in coping with the particular problem of amend-ments concering stock transfer restrictions. One might ask at tispoint, in light of the importance of stock transfer restrictions, whystatutes bearing on the problem have not been enacted. The answersimply is that this phase of corporation law is in its rudimentary stage.

It has only been in the last twenty years or so that the close cor-porations plight has been noticed to any appreciable extent in theUnited States.46 The initiative was taken by scholars who brought theproblem to light with the intention of effecting corrective legislation.4rThey must be given credit for some of the recent enactments aimedat aiding the close corporation. Suggested drafts of comprehensiveclose corporation statutes, however, have usually been rejected be-

her shares free of the restriction mposed by the amended bylaws. This position wasupheld by the district court of appeal m Tu-Vu Dnve-In Corp. v. Ashkins, 34 Cal.Rptr. 622 (1963).

43 Tu-Vu Drive-In Corp. v. Ashkins, 61 Cal. 2d 283, 288, 38 Cal. Rptr. 348, 351,

391 P.2d 828, 831 (1964). (Emphasis added.)4 4 See, e.g., Schwab v. Schwab-Wilson Mach. Corp., 13 Cal. App. 2d 1, 55 P.2d

1268 (1936); LATri, CoponATIoNs 267-72, 511-15.45 Frey, Shareholder's Pre-Emptive Rights, 38 YAxE L.J. 563, 583 (1929).46 O'Neal, Developments %n the Regulation of the Close Corporation, 50 Coiumu

L.Q. 641 (1965).47 hId.

March, 1966] COMMENTS

THE HASTINGS LAW JOURNAL

cause of a single factor-the perplexing problem of defining a closecorporation .4 North Carolina has met this difficulty by defining aclose corporation as being one whose shares are not "generally tradedin the markets maintained by securities dealers or brokers "49

Florida has followed suit,50 but the rest of the states have not, prob-ably because they are not convinced that this approach is satisfactory

It is submitted that an alternative approach to the problem ofamendments of bylaws or articles affecting stock transfer restrictionsis possible. As is the case in other situations where piecemeal legis-lation has been directed at the close corporation, it is feasible to worda statute so that only a close corporation could avail itself of its terms.5

Thus, a statute could be drawn whose language simply states thatif those formig a corporation desire stock transfer restrictions as partof the corporate form, they must provide for the restrictions m thearticles of incorporation. 2 The proposed statute would state that onlyrestrictions found in the articles, either as originally drawn or asamended, will be valid. If a corporation desires to make use of thestock transfer restriction, it must do so by following the statute'sdirections. Provisions for stock transfer restrictions in any other man-ner will not suffice. It should be stressed that choosing to includestock transfer restrictions is a completely elective process. Obviously,only a close corporation could (or would) avail itself of this procedure.Yet a close corporation never has to be defined. Those states whichhave sympathized with the close corporations' predicament, but havenot taken action because of the definitional problem, could readilyadopt the proposed statute.

The above discussion indicates that a uniform method of adopting48 The New York Law Revision -Commssion debated the matter of defining a close

corporation for the purpose of enacting a close corporation law but decided againstsuch a measure. As stated in the report, "no satisfactory way of defining the genuineclose corporation for purposes of a statute has been found. Economcally, the distinctionbetween a close corporation and any other is that in the close corporation managementand ownership are substantially identical, but the only way in which it appeared tothe Commission that a definition could be embodied in a statute would be to limit theamendment to corporations having not more than a stated number of shareholders, ornot more than a stated amount of capital. This would necessarily be arbitrary, mightnot provide an answer to the economic problem, and would possibly permit a singleshareholder by splitting up of his shareholding to break up the arrangement at willunless the remaining shareholders or the corporation bought him out." 1948 N.Y. LAwREvlsION Comi2X'N Rsa'. 386 (1948).

49 N.C. Gm. STAT. § 55-73(b) (1965).50 FLA. STAT. § 608.0100(2) (1963).51 See, e.g., N.Y. Bus. Corp. LAw § 616, growing out of the famous case of

Benmtendi v. Kenton Hotel, 294 N.Y. 112, 60 N.E.2d 829 (1945), and CAL. CoRP. CODE§ 500, which allow the incorporators to provide for more than a bare majority voteto transact corporate business.

52 See Appendix for § 1 of the proposed statute.

[Vol. 17

and eliminating stock transfer restrictions is needed. Corporate at-torneys drafting stock transfer restrictions are entitled to know before-hand, with some degree of certainty, the basis on which the courtswill ]udge the restrictions. Courts, on the other hand, need explicitstatutory guidance. Applying this principle to the cases discussed,the court would merely have to determine whether the adoption orelimination of the stock transfer restriction complied with the pro-posed statute's instructions.5 3

There is no magic in including stock transfer restrictions in thearticles of incorporation rather than the bylaws. The desired uniform-ity could be achieved by inclusion in either place. But greater solem-nity is generally required to amend the articles and the proposedstatute would properly take advantage of this requirement. 4 Sincemaintaining the closeness of the close corporation is a major premiseupon which the corporation is formed, the articles, either as originallydrawn or as amended, should reflect this intention.

Another section of the proposed statute indicates the method bywhich an amendment of the articles either to include stock transferrestrictions not found therein originally, or to eliminate restrictionsoriginally included, shall be made.5 If the corporation is composed offour or fewer shareholders, a unammous vote of all voting shareswould be required. In a corporation with five or more shareholders, atwo-thirds vote of the voting shares would be required. The numberof shareholders delimiting each group was chosen arbitrarily, butwith a definite intention. If the corporation is really small (four orfewer shareholders), it closely resembles the typical partnership, andit is therefore fair to require unammous action to include or eliminatestock transfer restrictions. When the corporation becomes larger, theprocess of unanimous vote becomes unwieldly because the whinof a single shareholder could block action. Thus the unammous voterequirement is dropped. But to prevent action by a bare majority (aswas the case in Tu-Vu) a two-thirds vote is necessary 58

Any statute directed at stock transfer restrictions should indicatewhat types of restrictions are approved. The proposed statute sanc-

53 Aside from this determination, the court would also have to pass upon thereasonableness of the restriction. This is to make sure that it does not amount to anunreasonable restraint on alienation.

54 Usually statutes require filing of amendments to the articles of incorporation.There is no corresponding rule for amendments to the bylaws. In addition, amending thearticles usually requires action by the board of directors and by the shareholders. Bylawsmay often be amended by the shareholders or the board of directors. Compare CAL.Coiu'. CODE § 3632 with DEL. CODE ANN. tit. 8, § 109 (1953).

55 See Appendix for § 1(b) of the proposed statute.56 See note 51 supra for examples of statutes with analogous more-than-majority

voting requirements.

March, 1966] COMMENTS

tions typical rights of first purchase running to the benefit of theshareholders or the corporation or both in succession, restrictionsgiving the corporation the right to purchase the shares of a share-holder-employee whose employment is terminated, and restrictionswhich give the shareholders the right of first purchase of shares heldby the corporation and subsequently offered for sale.57 The languageof the proposed statute indicates that the restrictions listed are notintended to be exclusive.

The right of first purchase enjoyed by the corporation or the share-holders or both in succession is the most commonly used and accepted.Whether the prospective purchase is occasioned by a shareholder'sfortuitous present intent to sell his shares, or occasioned by a salepursuant to his retirement, death, or incapacity to participate in thebusiness, the purpose to be served by the restriction is the same-toretain the original closeness and balance of power. In practice thecorporation is usually given the first option to purchase. The practicaleffect of this provision is that the remaining stockholders retain theirpercentage of control, pay no money personally, and have the stockretired. If the corporation is unable to make the purchase, the share-holders are given the second option.

Where the corporation purchases its own shares, two points shouldbe kept in mind, although they are not dealt with in the proposedstatute. First of all, corporation statutes often provide that a corpora-tion may purchase its own shares only out of earned surplus.5 8 Thereis a strong legislative policy behind this requirement 9 which the pro-posed statute does not attempt to override. Those drafting stocktransfer restrictions under the proposed statute would find it necessaryto research the other corporations statutes on this point.

The second point is closely akin to the first. It is sometimes pro-vided by statute that if a corporation desires to purchase its ownshares it must make provision for this in the articles of incorporation.60

Here again, it would be necessary to research the other corporationsstatutes to verify the applicable law

The purchase (by the corporation or the shareholders) of theshares of a shareholder-employee whose employment is terminatedserves ]ust as useful a purpose as that described immediately above.The associates in the close corporation will usually want to "restrictemployee shareholdings to those currently employed (to protect the

57 See Appendix for § 2 of the proposed statute.5 8 See, e.g., CAL. CoRP. CODE § 1707(c).59 "The purchase or redemption of its shares by a corporation constitutes a with-

drawal of assets and should be restricted to some reasonable limits of safety forthe protection of creditors and other shareholders. " LAT=r & JENNwNcs, CASES ONCoEPonATioNs 1211 (3d ed. 1959). See also CAL. CORP. CODE §§ 1705-08.

60 See, e.g., ABA-ALI MODEL Bus. Cors'. ACT § 5 (1953).

[Vol. 17THE HASTINGS LAW JOURNAL

corporation from disgruntled former employees) ,,oi This desirehas been given effect by the courts and is entitled to legislative sanc-tion.62

The third approved restriction in the proposed statute is that whichgives the existing shareholders the first opportunity to buy shareswinch the corporation has reacquired and later intends to sell. Sincethe sale of shares to outsiders by the corporation is just as destructiveas sales by the shareholders, careful draftsmen will often insert sucha restriction.

A notable exception to these sanctioned stock transfer restrictionsis the "consent restraint." The consent restraint is a method by whichthe shareholders or the board of directors are given the power to vetoa proposed transfer of shares to a third party Usually, the restraintspecifies that the veto must be exercised on reasonable grounds. Thereare three reasons why the consent restraint was omitted from the pro-posed statute: (1) There are strong policy arguments against consentrestraints and these arguments have prevailed in many jurisdictions;-"(2) requiring courts to determine whether the veto was "reasonably"exercised creates a litigation-breeding situation; (3) a right-of-first-purchase restriction is all the protection the shareholders need any-way 6

4

PROBLEMS OF JUDICIAL INTERPRETATION OF STOCKTRANSFER RESTRICTIONS

It is probable that the great majority of cases involving stocktransfer restrictions entail judicial construction of the language used

61 1 HonNsmTn, ConoRAnoN LAw AND PRcs'Tc. 248 (1959).02 Ibzd.6 3 The older cases took the position that consent restraints were unreasonable

restraints on the right of alienation of personal property. See, e.g., Morrs v. HussongDyeing Mach. Co., 81 N.J. Eq. 256, 86 Ad. 1026 (Ch. 1913); In re Klaus, 67 Wis. 401,29 N.W 582 (1886). Most of the recent cases uphold consent restraints, althoughtheir validity is still in doubt in many jurisdictions. See O'Neal, Restrictions on Transferof Shares in Closely Held Corporations: Planning and Drafting, 65 HAIv. L. REV. 773,780 (1952).

04 A right of first purchase is often provided for in situations where a judgmentcreditor of a shareholder seeks to levy execution on the shares in satisfaction of thejudgment. This type of restriction was not included in the statute as an example of asanctioned restriction even though it is generally held valid. The diMculty involves adetermination of the price to be paid to the judgment creditor to prevent his getting holdof the shares. It is anticipated that the requisite statutory language would becumbersome and, since these restrictions are commonly upheld by the courts whenproperly drafted, no real hardships should result from their omission from the proposedstatute. The list of restrictions in the proposed statute Is expressly stated to beillustrative and not inclusive.

Marcha, 1966] COMMENTS

m creating the restrictions.6 5 The proposed statute attempts to dealwith these problems.

The stock transfer restriction agreement will state the time limitwithin which the stockholders or the corporation must elect whetheror not to exercise this right of first purchase. Confusion sometimesoccurs because of the failure to specify the date upon which the periodbegins to run. Allen v. Biltmore Tissue Corp.66 illustrates the judicialapproach to this situation. The bylaws provided for a right of firstpurchase both during the life of the stockholder and in case of deathas follows: "'Should the option provided for in this section not beexercised, then, after the lapse of ninety days, the legal representativemay dispose of said stock as he sees fit."' 67

As stated by the court, "the section is patently deficient m omittingto specify the date upon which the 90-day period is to commence."68

Decedent died on October 25, 1953. In February of 1954 the corpora-tion was informed of his death. Biltmore's board of directors votedto exercise the option on March 4, 1954 and notified the executor'sattorney of their action on March 23, 1954, nearly five months afterdecedent's death. The court held the corporation acted within thepermitted ninety-day period since it could act only after receivingnotice and this occurred in February, 1954.69

Section 3(a) of the proposed statute70 attempts to anticipate thesesituations by providing that the option period begins to run upon thereceipt of written notice. Since small corporations may not ask forthe advice of counsel in all instances, it was considered better not toburden the transferor with the techicalities of registered or certifiedmail. Certainly this latter method is more desirable as providing morereliable proof, but the proposed statutory procedure should suffice.

Every stock transfer restriction agreement specifies a time limitwithin which the right of first purchase must be exercised. The periodschosen vary according to the individual situation. Section 3 of theproposed statuter l provides for this factor by enabling the draftsmanto select the limitation suitable to his client's needs. If no periodis provided, the proposed statute sets an outer limit of forty-five dayswhere the corporation is the potential transferee and thirty days wherethe shareholder is in this position. The purpose in choosing twodifferent periods recognizes the greater amount of tume corporate ac-

65 For a collection of cases dealing with the construction and application of stocktransfer restrictions see Annot., 2 A.L.R.2d 745 (1948).

66 2 N.Y.2d 534, 141 N.E.2d 812, 161 N.Y.S.2d 418 (1957).67 Id. at 538, 141 N.E.2d at 813, 161 N.Y.S.2d at 419.68 Id. at 544, 141 N.E.2d at 817, 161 N.Y.S.2d at 424.69 Id. at 544, 141- N.E.2d at 817, 161 N.Y.S.2d at 425.70 See Appendix.71 Ibid.

THE HASTINGS LAW JOURNAL [Vol. 17

tion requires. Since the most common stock transfer restriction pro-vides for alternative rights of first purchase in the corporation and theshareholders, section 3(b) of the proposed statute provides for twostatutory periods. 72 If the first potential transferee exercises the pur-chase right, there is no need for the second period to run. Where thefirst potential transferee does not exercise the purchase right, thesecond period begins to run the day after the first period expires.

Questions sometimes arise as to who will be bound by the stocktransfer restriction agreement. Where, for example, shares come intothe hands of an executor or pledgee, judicial construction of theagreement's terms is necessary if the language is not explicit. Theproposed statute assumes that draftsmen always intend that the broad-est possible scope be given stock transfer restrictions. Section 4 of theproposed statute makes it clear that, unless provided otherwise, thestock transfer restriction adheres to every share of stock of the corpora-tion.73 Whether the shares are in the hands of the shareholders, thecorporation, or third parties, the stock transfer restriction binds theshares. The broad language is intended to fasten to shares in anystatus. Thus treasury shares, authorized but unissued shares, issuedshares, and new issues are all subject to the restrictions.

It is important to note that even under such a statutory provision,the intent of the incorporators may be defeated unless additionalsafeguards are provided. If the corporation has a number of author-ized but umssued shares, the majority shareholders may be able todilute the percentage ownership of the minority by voting to issuethese shares at a time when the minority is not m a financial positionto purchase. The majority may purchase the shares themselves andthereby increase their percentage ownership at the expense of theminority Section 4 of the proposed statute would be of no help to theminority group. The provision states that when authorized but un-issued shares are subsequently issued, the stock transfer restrictionwill attach automatically to these shares-but there is no require-ment restricting the majority from causing the shares to be issuedat any time it decides is appropriate. In other words, although thetransfer restrictions will attach to these shares there is nothing in thestatute which prevents the majority from effectively insuring, by tak-ing advantage of economic circumstances and its voting power, thatthese shares go only to majority shareholders. 74

To protect against issuance of shares which would alter corporatecontrol, the draftsman should give the shareholders an opportunity to

72 Ibid.73 Ibid.7 4 Here, too, the court might hold the majority shareholders to a fiduciary duty to

the minority.

March, 1966] COMMENTS

reject the issuance of previously authorized, but as yet unissued,shares. This could be accomplished by a provision in the articles ofincorporation which requires, perhaps, a two-thirds vote for approvalof the issuance.75 Since treasury shares can also be sold to outsiders,the same procedure would be applicable here.

Another way for the majority shareholders to disrupt the originalbalance of power would be to authorize a new issue of shares. Asthe judge-made equitable doctrine of shareholders preemptive rightsevolved, the existing shareholders had a preemptive right to purchaseany new issue of shares on a pro rata basis, and, therefore, under thisrule there would be no difficulty 76 There is a dangerous pitfall inCaliforma, however, because under the Corporations Code there areno preemptive rights unless provided for in the articles of incorpora-tion.77 Thus, as in the case of authorized but umssued shares, themajority could dilute the minority's interest by authorizing the newissue at a time which is financially inconvement for the minority 7 1

To carry out the associates' intent, two provisions should be made inthe articles: (1) by analogy to the authorized-but-umssued situation,the shareholders should be given the opportunity to vote down a pro-posed new issue and (2) the existing shareholders should be givena preemptive right to purchase newly issued shares.

One of the main objectives of the proposed statute is to have thestock transfer restriction become a part of every share of stock of theclose corporation. This objective is designed to help achieve the ulti-mate goals of keeping the close corporation close and maintaining thebalance of power. The corporate draftsman should take complementaryaction by protecting against the foreseeable problems of authorizedbut unissued shares, treasury shares, and new issues.

It has already been indicated that maintaining the original balanceof power is often as inportant to the associates as preventing mtru-sions by outsiders. This objective attained by a clause which givesthe shareholders the right of first purchase on a pro rata basis; i.e., aright exercisable in proportion to their existing interests.79 The ruleof narrow construction of stock transfer restrictions, however, has ledto defeat of the parties' intent where the wording of the restrictionhas been subject to doubt.80

75 On veto rights m the minority shareholders see O'Neal, Giving Shareholders Powerto Veto Corporate Decisions: Use of Special Charter and By-law Provisions, 18 LAw& CoNTEm. PoB. 451 (1953).

76 LAT N, Con'oRATnoNs 424-31 (1959).77 CoiRp. CODE § 1106 provides: "Unless the articles provide otherwise, the

board of directors may issue shares, option rights, or securities having conversion oroption rights, without first offering them to shareholders of any class."

78 Although again the majority nght be held to a fiduciary duty.79 See Appendix for § 5 of the proposed statute.8 0 See, e.g., Carlson v. Ringgold County Mutual Telephone Co., 252 Iowa 478, 108

THE HASTINGS LAW JOURNAL FVol. 17

Guaranty Laundry Co. v. Pulliam81 is illustrative of the-problem.The stock transfer restriction was included in a shareholders' agree-ment which provided that in the event one shareholder should con-sider selling his shares, he would "'give the remaining stockholdersor stockholder, the first and last chance to purchase his stock."' 82 Theissue was whether a sale of all the shares to one shareholder satisfiedthe terms of the agreement. Following the rule of narrow construction,the court held that "we conclude that it may reasonably be construed

that the agreement was satisfied by sale to a remaining stock-holder, as well as to all of the remaining stockholders."83

Because of the rule of narrow construction typified by the Pulliamcase and because it must be presumed that the draftsman's intent isto maintain the original balance of power, a pro rata exercise of theright of first purchase is the rule under section 5 of the proposedstatute, unless provided otherwise.

Section 15 of the Uniform Stock Transfer Act,84 which is intendedto be superseded by section 8-204 of the Uniform Commercial Code,85

requires a notation on the face of the stock certificate that the sharesare subject to transfer restrictions. The Uniform Commercial Codechanges the old rule m two respects: (1) a transferee with actualknowledge of the restriction will be bound by it even in the absence ofnotation on the shares and (2) the notation must be conspicuous.86

Section 6 of the proposed statute, which refers to the Uniform Com-mercial Code, is intended merely as a reminder that these rules mustbe compiled with.8 7

The proposed statute does not indicate any method by which theprice to be paid for the transfer of shares under a stock transfer re-striction shall be determined. Fixing the value of shares of a closecorporation has been a continuing, thorny problem.8 8 The difficulty

N.W.2d 478 (1961); Sands Point Land Co. v. Rossmore, 43 Misc. 2d 368, 251 N.Y.S.2d197 (Sup. Ct. 1964); Dorby v. Dorby, 262 P.2d 691 (Okla. 1953); Guaranty LaundryCo. v. Puliam, 198 Okla. 667, 181 P.2d 1007 (1947). The Massachusetts decisions, how-ever, take a contrary position: Boston Safe Dep. & Tr. Co. v. North Attleborough Chapter,American Red Cross, 330 Mass. 114, 111 N.E.2d 447 (1953); Monotype CompositionCo. v. Kiernan, 319 Mass. 456, 66 N.E.2d 565 (1946).

81 198 Okla. 667, 181 P.2d 1007 (1947).82 Id. at 670, 181 P.2d at 1009.83Id. at 670, 181 P.2d at 1009.84 UNoRM STocK TRANsTEa AcT § 15 reads: "[TIhere shall be no restriction upon

the transfer of shares unless the restriction is stated upon the certificate."8S'TNIFoM CoMrMcIAL CODE § 8-204 reads: "Unless noted conspicuously on the

security a restriction on transfer imposed by the issuer even though otherwise lawful isineffective except against a person with actual knowledge of it."

86 Ibid.87 If, for any reason, a state which adopts the Uniform Commercial Code elects

not to adopt § 8-204 and repeals the Uniform Stock Transfer Act, then § 6 of theproposed statute would not have to be complied with.88 See Forster, Valuing a Business Interest for the Purposes of a Purchase and Sale

March, 1966] COMMENTS

THE HASTINGS LAW JOURNAL

arises because the shares of a close corporation are not traded in themarket and therefore their fair market value cannot be readily ascer-tamed. As a result, various formulae have been devised to arrive at aproper valuation; these include book value (either inclusive or ex-clusive of good will), fixed price, par value, and appraisal.89 Un-fortunately, none of these approaches has produced a satisfactoryresult in all situations because each method has its shortcomngs 0

Although fixing the price of shares subject to stock transfer restric-tions is most inportant in drafting effective restrictions, it was con-sidered best to omit any reference to valuation in the proposedstatute. Instead of adhering to one particular valuation method pre-scribed by the statute the draftsman will be free to choose the priceformula best suited to the particular situation.

CONCLUSIONAs long as legislatures consider that it is not possible adequately

to define the close corporation, comprehensive closely-held corpora-tion statutes will not be enacted. Yet present statutes do not suffici-ently provide for the needs of the close corporation. The courts andclose corporation draftsmen have attempted to reach satisfactoryresults under these adverse conditions. When the adoption or elimi-nation of stock transfer restrictions at a date subsequent to organrza-tion is in issue, the outcome is often speculative. The courts, in at-tempting to reach desirable results, are free to choose from amongseveral available approaches. Usually, none of these is expresslyadapted to stock transfer restrictions in the close corporation, andthe results are exemplified in the vacillations of the Caifforma courts.When interpretation of the language creating stock transfer restric-tions is in issue, many courts feel bound to a rule of narrow con-struction because of the policy against restraints on alienation.

The proposed statute is directed specifically at stock transferrestrictions in the close corporation. It is intended as a basis for in-termediate legislation-somewhere between comprehensive close cor-poration statutes (which are not too likely to be enacted) and existingstatutes (which are not satisfactory). Such intermediate legislationshould alleviate some of the existing uncertainties regarding stocktransfer restrictions, which are essential elements to the success ofthe close corporation.91

Agreement, 4 STAN. L. REv. 325 (1952); O'Neal, Restrictions on Transfer of Stock inClosely Held Corporations: Planning and Drafting, 65 HARv. L. REv. 773, 797-807(1952).

89 See authorities cited note 88 supra.90 See authorities cited note 88 supra.91 It should be stressed that the proposed statute is not intended to be all-inclusive.

It is not a panacea for all the ills involving stock transfer restrictions. The prnmary

[Vol. 17

COMMENTS

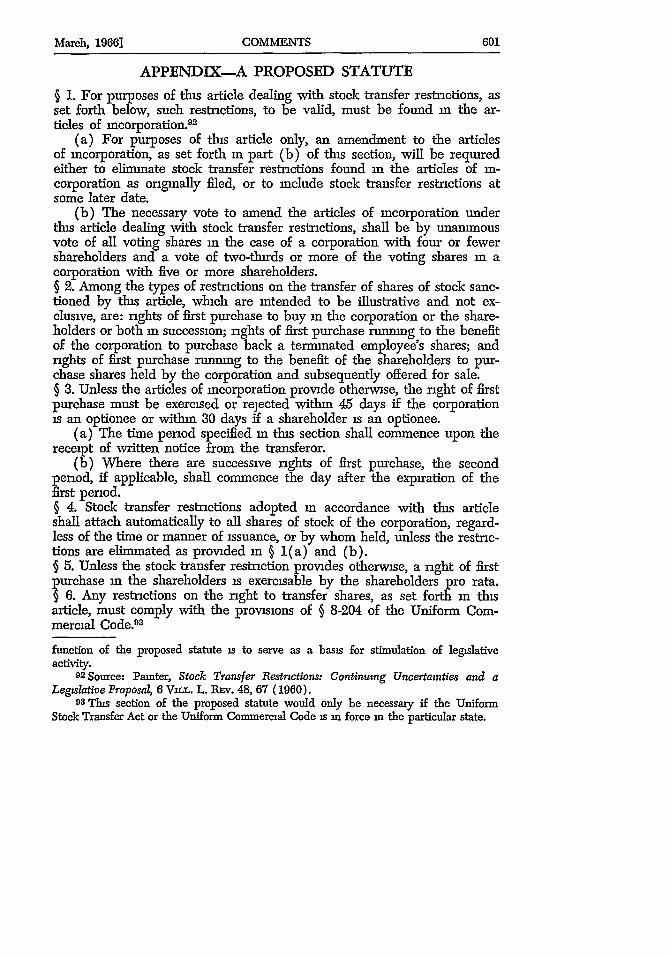

APPENDIX-A PROPOSED STATUTE

§ 1. For purposes of this article dealing with stock transfer restrictions, asset forth below, such restrictions, to be valid, must be found in the ar-ticles of incorporation. 92

(a) For purposes of this article only, an amendment to the articlesof incorporation, as set forth in part (b) of this section, will be requiredeither to eliminate stock transfer restrictions found in the articles of in-corporation as originally filed, or to include stock transfer restrictions atsome later date.

(b) The necessary vote to amend the articles of incorporation underthis article dealing with stock transfer restrictions, shall be by unanmousvote of all voting shares in the case of a corporation with four or fewershareholders and a vote of two-thirds or more of the voting shares in acorporation with five or more shareholders.§ 2. Among the types of restrictions on the transfer of shares of stock sanc-tioned by this article, which are intended to be illustrative and not ex-clusive, are: rights of first purchase to buy in the corporation or the share-holders or both in succession; rights of first purchase running to the benefitof the corporation to purchase back a terminated employee's shares; andrights of first purchase running to the benefit of the shareholders to pur-chase shares held by the corporation and subsequently offered for sale.§ 3. Unless the articles of incorporation provide otherwise, the right of firstpurchase must be exercised or rejected within 45 days if the corporationis an optionee or within 30 days if a shareholder is an optionee.

(a) The time period specified n this section shall commence upon thereceipt of written notice from the transferor.

(b) Where there are successive rights of first purchase, the secondperiod, if applicable, shall commence the day after the expiration of thefirst period.§ 4. Stock transfer restrictions adopted in accordance with this articleshall attach automatically to all shares of stock of the corporation, regard-less of the time or manner of issuance, or by whom held, unless the restric-tions are eliminated as provided in § 1(a) and (b).§ 5. Unless the stock transfer restriction provides otherwise, a right of firstpurchase in the shareholders is exercisable by the shareholders pro rata.§ 6. Any restrictions on the right to transfer shares, as set forth in thisarticle, must comply with the provisions of § 8-204 of the Uniform Com-mercial Code.93

function of the proposed statute is to serve as a basis for stimulation of legislativeactivity.

92 Source: Painter, Stock Transfer Restrictions: Continuing Uncertainties and aLegislative Proposal, 6 VmL. L. REv. 48, 67 (1960).

93 Tis section of the proposed statute would only be necessary if the UniformStock Transfer Act or the Uniform Commercial Code is in force in the particular state.

March, 1966]