stocks economics 71a: spring 2007 mayo, chapter 10 lecture notes 4.1

Post on 20-Dec-2015

219 views

TRANSCRIPT

Stocks

Economics 71a: Spring 2007

Mayo, chapter 10

Lecture notes 4.1

Goals

Stock basicsHistorical stock performance

Common Stock

Ownership of piece of a firm Key parts

Voting rights (control) Dividends Right to assets Limited liability

1. Voting and Control

Voting rights In proportion to share holdings Annual meetings Proxy

Firm control Shareholders elect Board of Directors Oversee management Sometimes difficult to remove

Voting Methods

Traditional Everyone votes on each candidate Like regular election

Cumulative One vote per board position

5 members - get 5 votes per share Can cast all votes for one candidate Increases power of minority voting blocks

Can group all votes for one candidate

2. Dividends

Payments to shareholders from firm Usually cash

Usually paid quarterlyFirm sets amountsDividends paid after all other obligations

are metAmount can be zero

Dividend Timing

Declaration date (June 3rd)Ex-dividend date (June 16)Date of record (June 18)Payment date (June 30)Key date: Ex-dividend date

Purchase before: get dividend Purchase after: no dividend

Dividend Decisions

Profits of the firm (earnings) Shareholders (dividends) Retained earnings (investment)

Payout ratio = (dividends)/earningsDividend yield =

(dividends per share)/(price per share)

Does Dividend Policy Matter?

Example: Assets - Liabilities = 100 = Shareholder equity Shares = 100, price per share = 100/100 = 1 Earnings = 10 1. Pay out earnings as dividends 10/100 = 0.1 per

share 2. Hold earnings as cash

Value of the firm goes from 100 to 110 (A-L) Price per share goes to 110/100 = 1.10 Shareholders gain 0.1 per share

Does Dividend Policy Matter?

In theory, No In real life, Yes

Worry about firm investing funds wisely Worry about firm running off with funds Stock may not be priced correctly

Dividend Reinvestment

Firm allows you to buy stock with dividends

No fees or commissionsSometimes below market prices

What is a Stock Return?

Stock held from time t to t+1Pays dividend during this time of d(t+1)

Why is this sensible? Increase of 1 dollar after investment t to

t+1€

Rt+1 =Pt+1 +dt+1 −Pt

Pt

Two Parts to a Stock Return

= (capital gain) + (dividend yield)€

Rt+1 =Pt+1 +dt+1 −Pt

Pt

Rt+1 =Pt+1 −PtPt

+dt+1

Pt

Numerical Example

Price(last year) = 100 (per share)Price(today) = 110Dividend = 3 (per share)

€

Rlastyear =110 + 3 −100

100= 13%

Rlastyear =110 −100

100+

3100

Rlastyear = 10% + 3% = 13%

3. Rights to Assets

Shareholders have rights to residual assets in a bankruptcy case

Value distributed after other obligations met Bills Tax payments Bond holders

Often this can be zero

4. Limited Liability

Liabilities of shareholders are limitedNot responsible for amounts firm owesOr lawsuits against the firmWhat does this mean?

If you buy a stock for $10, the most you can lose is $10

Preferred Stock(Debt like)

Fixed, promised dividend Similar to interest payments on debt Cumulative basis: missed dividends must

be paidNo voting rights (usually)Call option

Firm can buy back

Bankruptcy Priorities

Bills owed and tax paymentsDebt holdersPreferred stock holdersCommon stock holders

Issuing and Increasing Shares

Initial Public Offering (IPO) at start New issues (issue more shares)

“Dilution” Rights offering Stock options

Stock spin-offs Spin off subsidiaries

Stock splits 2 for 1 split

Stock dividends

Stock Splits

Example: 2-1 split Number of shares increases by 2 Price falls by 1/2 Dividend reduced by 1/2

No real impact Why?

Lower price, more investors Reverse split:

1-2 split Increase price, why??

Reducing Shares

Buy back shares (share repurchase) Treasury stock Reverse dilution

Stock Dividends

Pay dividends with shares of stockSimilar to stock splitNo change for investors

More shares Price goes down

Tax Treatments

Firm Interest payments on debt are tax deductible Dividend payments are not Example

(Profits – debt interest payments) Pay taxes on this amount

This gives a tax advantage to the firm for using debt financing

Tax Treatments

Individual Investors Capital gains (lower rates) Dividends (some at lower rates)

2003 tax law change Before 2003 dividends taxed at higher rates

Goals

Stock basicsHistorical stock performance

Goals

Stock basicsHistorical stock performance

Real Portfolio Values(Inflation Adjusted, dividends reinvested)

Total Portfolios (log scale)

Dividend Comparison

Real Portfolio Values(Inflation Adjusted)

Real Portfolio Values(Inflation Adjusted)

Real Portfolio Values(Inflation Adjusted)

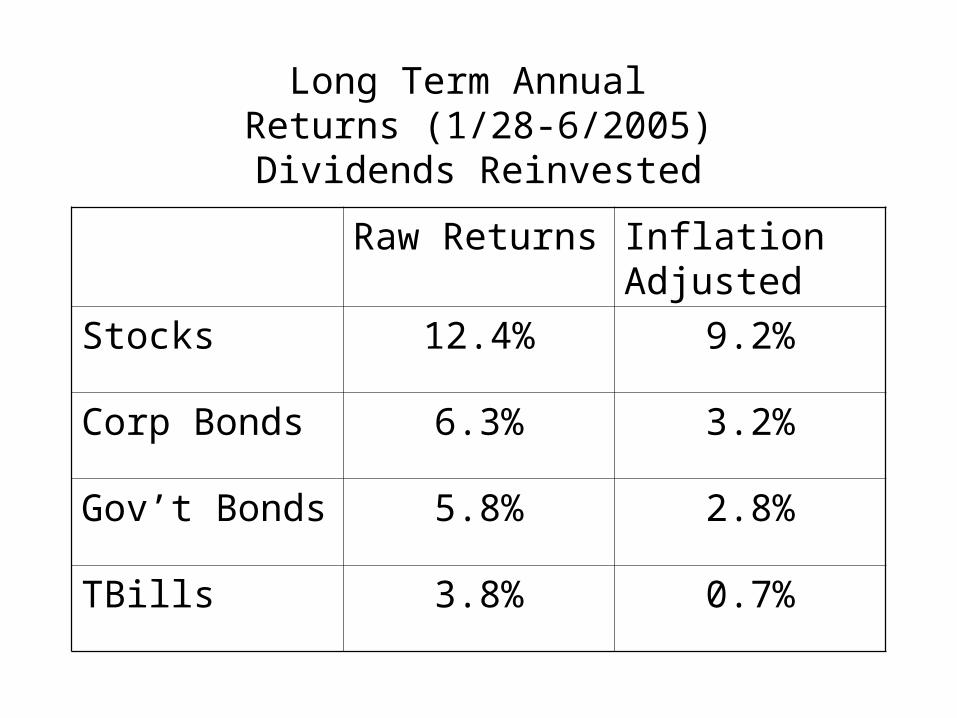

Long Term Annual Returns (1/28-6/2005)Dividends Reinvested

Raw Returns Inflation Adjusted

Stocks 12.4% 9.2%

Corp Bonds 6.3% 3.2%

Gov’t Bonds 5.8% 2.8%

TBills 3.8% 0.7%

Goals

Stock basicsHistorical stock performance