strategic plan 2018-2020 - bankia.com · 2016 - 2017 recapitalization and ... strategic plan...

TRANSCRIPT

1

STRATEGIC PLAN 2018-2020

Strategic Plan 2018-2020BankiaFebruary 2018

2

STRATEGIC PLAN 2018-2020

Disclaimer This document was originally prepared in Spanish. The English version published here is for information purposes only. In the event of any discrepancy

between the English and the Spanish version, the Spanish version will prevail.

This document has been prepared by Bankia, S.A. (“Bankia”) and is presented exclusively for information purposes. It is not a prospectus and does not constitute

an offer or recommendation to invest.

This document does not constitute a commitment to subscribe for, or an offer to finance, or an offer to sell, or a solicitation of offers to buy securities of Bankia,

all of which are subject to internal approval by Bankia.

Bankia does not guarantee the accuracy or completeness of the information contained in this document. The information contained herein has been obtained

from sources that Bankia considers reliable, but Bankia does not represent or warrant that the information is complete or accurate, in particular with respect to

data provided by third parties. This document may contain abridged or unaudited information and recipients are invited to consult the public documents and

information submitted by Bankia to the financial market supervisory authorities. All opinions and estimates are given as of the date stated in the document and

so may be subject to change. The value of any investment may fluctuate as a result of changes in the market. The information in this document is not intended

to predict future results and no guarantee is given in that respect.

This document includes, or may include, forward-looking information or statements. Such information or statements represent the opinion and expectations of

Bankia regarding the developmentof its business and revenue generation, but such development may be substantially affected in the future by certain risks,

uncertainties and other material factors that may cause the actual business development and revenue generation to differ substantially from our expectations.

These factors include i) market conditions, macroeconomic factors, government and supervisory guidelines, ii) movements in national and international

securities markets, exchange rates and interest rates and changes in market and operational risk, iii) the pressure of competition, iv) technological changes, v)

legal and arbitration proceedings, and vi) changes in the financial situation or solvency of our customers, debtors and counterparties. Additional information

about the risks that could affect Bankia’s financial position, may be consulted in the Registration Document approved and registered in the Official Register of

the CNMV.

Distribution of this document in other jurisdictions may be prohibited, therefore recipients of this document or any persons who may eventually obtain a copy of

it are responsible for being aware of and complying with said restrictions.

This document does not reveal all the risks or other material factors relating to investments in the securities/ transactions of Bankia. Before entering into any

transaction, potential investors must ensure that they fully understand the terms of the securities/ transactions and the risks inherent in them. This document is

not a prospectus for the securities described in it. Potential investors should only subscribe for securities of Bankia on the basis of the information published in

the appropriate Bankia prospectus, not on the basis of the information contained in this document

3

STRATEGIC PLAN 2018-2020

OUR STARTING POINT AND VISION FOR THE FUTURE1Mr. José Ignacio GoirigolzarriChairman

LINES OF ACTION OF THE NEW PLAN2Mr. José Sevilla Chief Executive Officer

STRATEGIC PLAN FINANCIAL BREAKDOWN3Mr. Leopoldo AlvearChief Financial Officer

CONCLUSIONS4Mr. José Ignacio GoirigolzarriChairman

STRATEGIC PLAN 2018-2020

4

STRATEGIC PLAN 2018-2020

OUR STARTING POINT AND VISION FOR THE FUTURE

1

5

STRATEGIC PLAN 2018-2020

Our path: 2012-2017

Strategic Plan

2012 - 2013

2014 - 2015

2016 - 2017

Recapitalization and Restructuring

Evolution of our business model

Positioning

STRATEGIC PLAN

2012-2015 RESTRUCTURING PLAN

2012-2017

✓✓

We have met the targets

Where do we come from?

6

STRATEGIC PLAN 2018-2020

Strategic Plan

Completion of the Restructuring Plan…

Well positioned for the new Strategic Plan

With strong commercial dynamics

Increase in high-value products market share: Consumer finance, Mutual funds, Pension funds

With a significant improvement in the level of non-performing assets

With a proven capacity to generate capital organically

+635bps of CET1 FL generated since 2013 and cumulative dividends of 1,160 million euros

Non-performing assets reduced by €11bn (-49%) since 2013

And the start of a new phase, consolidated as the fourth largest bank

7

STRATEGIC PLAN 2018-2020

• Capital (MREL, Basel IV, IFRS 9, SREP)

• Business Model (MiFID II, PSD2, GDPR)Regulation

• Technological developments (AI, Big Data, Digitalization)

• New competitors (Fintech and technology firms)Technology

• Relationship model

• More demanding customers (marketing-comparability)Customer habits

Strategic Plan

What has changed since 2012?

8

STRATEGIC PLAN 2018-2020

Strategic Plan

Corporate Governance

Independent Board

Professionalism

Dedication

Principles and Values

Professional and meritocratic project

Clearly defined values

Management Code and Style

Committed Teams Recognition from Society

What doesn’t change?

9

STRATEGIC PLAN 2018-2020

NUMBER OF DIRECTORS 11

% INDEPENDENT DIRECTORS 63.6%

EXECUTIVE CHAIRMANYes

Lead Director and CEO as counterbalance

LEAD DIRECTOR Yes

Maximum term 3 years

BOARD ASSESSMENT Yes

CHAIRMAN ASSESSMENTYes

Led by the Lead Director

Recognition by the market’s most influential proxy advisor

TARGET 2020: Maintain the score

Strategic Plan

Best practices in Corporate Governance

10

STRATEGIC PLAN 2018-2020

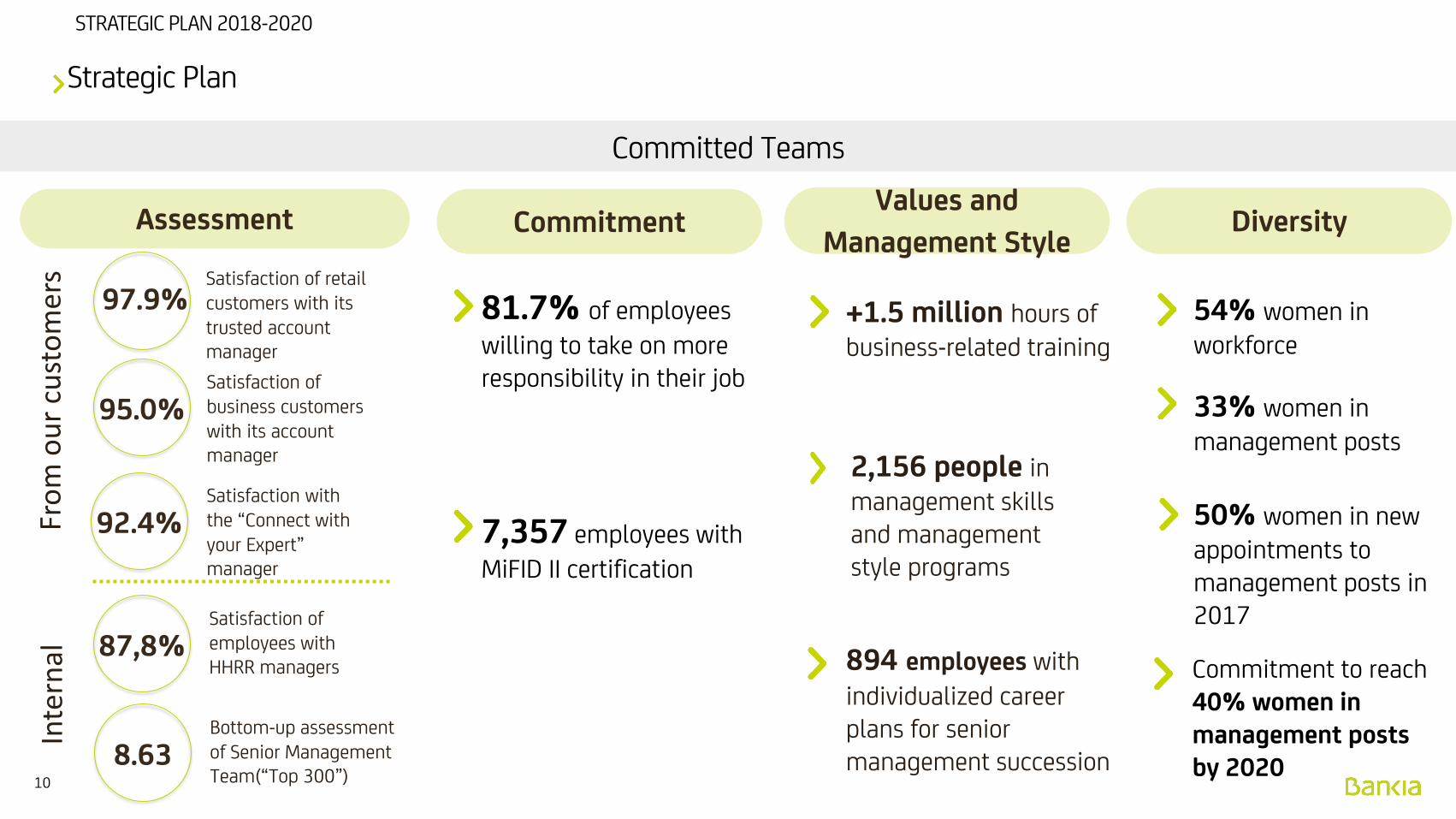

Assessment

Strategic Plan

Satisfaction of retail customers with its trusted account manager

97.9%

95.0%Satisfaction of business customers with its account manager

92.4%Satisfaction with the “Connect with your Expert” manager

87,8%Satisfaction of employees with HHRR managers

8.63Bottom-up assessment of Senior Management Team(“Top 300”)

Fro

m o

ur

cust

om

ers

Inte

rnal

CommitmentValues and

Management StyleDiversity

81.7% of employees

willing to take on more responsibility in their job

7,357 employees with

MiFID II certification

+1.5 million hours of business-related training

2,156 people in management skills and management style programs

894 employees with

individualized career plans for senior management succession

54% women in workforce

33% women in management posts

50% women in new appointments to management posts in 2017

Commitment to reach 40% women in management posts by 2020

Committed Teams

11

STRATEGIC PLAN 2018-2020

Education and employment Environment Responsible Digitalization

Privacy: Appointment of DataProtection and Privacy Director

Cyber security

Sustainable products:

“FP Dual” Foundation

In order to continue improving, we want to put the focus on the main challenges society faces today

“Empleo en Red” program to help unemployed customers

Education to help older people back into employment

100% of the energy consumed in Bankia is renewable

Consumer loan, sustainable investment fund, etc.

Eco-Efficiency and Climate Change Plan 2017–2020

Strategic Plan

Recognition from society

12

STRATEGIC PLAN 2018-2020

Processes improvement to serve our customers on an efficient and excellent manner

Permanently adapting our distribution model to better serve our customers

Positioning based on listening

Strategy

The CUSTOMER is at the center of our strategy

1

2

3

Business Pillars: PEOPLE and TECHNOLOGY

Bankia’s Strategic Priorities

13

STRATEGIC PLAN 2018-2020

1. Positioning

Strategy

86.2

81.3

79.3

77.3

79.2

80.2 80.4

1S12 2S12 1S13 2S13 1S14 2S14 1S15

Source Bankia. Quality Management. 68,388 retail customers surveyed in 2015

CLOSENESSPersonalized service

TRANSPARENCYCustomized products/services

Active listening to customers

SIMPLICITYSimple products

PositioningOur customer’s satisfaction was

insufficient

100,000 customers surveyed

100 focus groups

10,300 customer responses

Analysis of customer complaints

Is differentiation possible in the financial sector?

Strategic thought 2015: We were going to meet our goals, but…

1H12 2H12 1H13 2H13 1H14 2H14 1H15

%

14

STRATEGIC PLAN 2018-2020

Initiatives with customers Adaptation of our organisation

Positioning

Customer satisfaction is the key variable of our management

Strategy

1. Positioning

Goal: To be a Close, Simple and Transparent organisation“Cuenta SIN” account (+280,000 direct income deposits)

“Cuenta On” account (+230,000)

“Hipoteca SIN” mortgage (new mortgages 2.3x vs 2016)

Internal reorganisation

Action plans: +1,000 milestones committed

+27,000 internal satisfaction surveys

…new positioning launched in 2016…

15

STRATEGIC PLAN 2018-2020

86.2

81.3

79.3

77.3

79.280.2 80.4

82.4

86.387.3

89.390.0

1H12 2H12 1H13 2H13 1H14 2H14 1H15 2H15 1H16 2H16 1H17 2H17

Source Bankia. Quality Management. 58,388 retail customers surveyed in 2017

Net increase in customers

Strategy

1. Positioning. Retail Banking

Customer satisfaction

3,606 39,828

1H16 2H16

#

1H17

68,241

2H17

90,120

Increase of 280,000 direct income deposits in the last two years

We have achieved differentiation within the financial sector

16

STRATEGIC PLAN 2018-2020

Significant increase in our market shares in key products

CONSUMER CREDIT

+32.7%3.61% vs 4.79%

DEC 13 VS DEC 17

CREDIT CARDS

+28.8%5.48% vs 7.06%

DEC 13 VS DEC 17

MUTUAL FUNDS

+22.4%4.74% vs 5.80%

DEC 13 VS DEC 17

PENSION PLANS

+16.1%5.45% vs 6.33%

DEC 13 VS DEC 17

Source: BdE / Inverco

Strategy

1. Positioning. Retail Banking

Our customers’ satisfaction allow us to reach higher cross-sell levels

17

STRATEGIC PLAN 2018-2020

Strategy

1. Positioning. Business Banking

Increase in Business Banking customers

(>€50,000 investment)

2015-2017

+18.9%

% Businesses that work with Bankia

35.3%

2015 2017

37.5%

Net promoter score (NPS)

2015 2017

38.1% 52.2%

Source: Bankia

2,623 quality surveys to Business Banking customers in 2017

% Businesses with turnover in between €6mn and €300mn

Source: Bankia

95.2% level of satisfaction in 2017

We also started to transform the Business Banking activity…

18

STRATEGIC PLAN 2018-2020

REVERSE FACTORING

+115.3%3,67% vs 7,90%

DEC 14 vs DEC 17

COMMERCIALCREDIT

+49.4%6,90% vs 10,31% DEC14 vs DEC17

1. Positioning. Business Banking

Strategy

LOANS TO BUSINESSES

+4.2%5,74% vs 5,98%

DEC 14 vs DEC 17

LOANS TO BUSINESSES

normal sin inmobiliario

+8.4%5,94% vs 6,44%

DEC 14 vs DEC 17

25.1%

32.9%

Working capital as % of Total

2014 2017

Market share growth in working capital Businesses Market Shares

TRADE FINANCE

+91.2%4.89% vs 9.35%

DEC 14 vs Dec 17

Source: SWIFT Watch Insight / BdE / Bankia Research

Effort to change a very long-term oriented balance sheet: focus on working capital

19

STRATEGIC PLAN 2018-2020

Strategy

1. Positioning. Customers

Increase in number of customers

Customer’s satisfaction

+5%

92%

>7%Market shares

+20%

95%

~8%

Retail Banking Business Banking

Consumer, Funds and Insurance

2020 Targets

20

STRATEGIC PLAN 2018-2020

Strategy

Global view on the impact of technology

… which is only possible through technology

Efficiency in PROCESSESImproves CUSTOMER

experience

An excellent and sustainable service demands a high level of efficiency…

21

STRATEGIC PLAN 2018-2020

2. Processes improvement

Strategy

Impact on network staffTime saving in branches from processes

improvement

Opening a current account 55%

Granting and disbursing a

mortgage loan40%

Issuing a credit card 49%

+650Multichannel

-550Net reduction

2014-20172014-2017

Second processes review in 2018-2020: integration of BMN and artificial intelligence

-1.200Employees in branches-12%

Redesign of processes 2015-2017: multichannel, data capture and efficiency

22

STRATEGIC PLAN 2018-2020

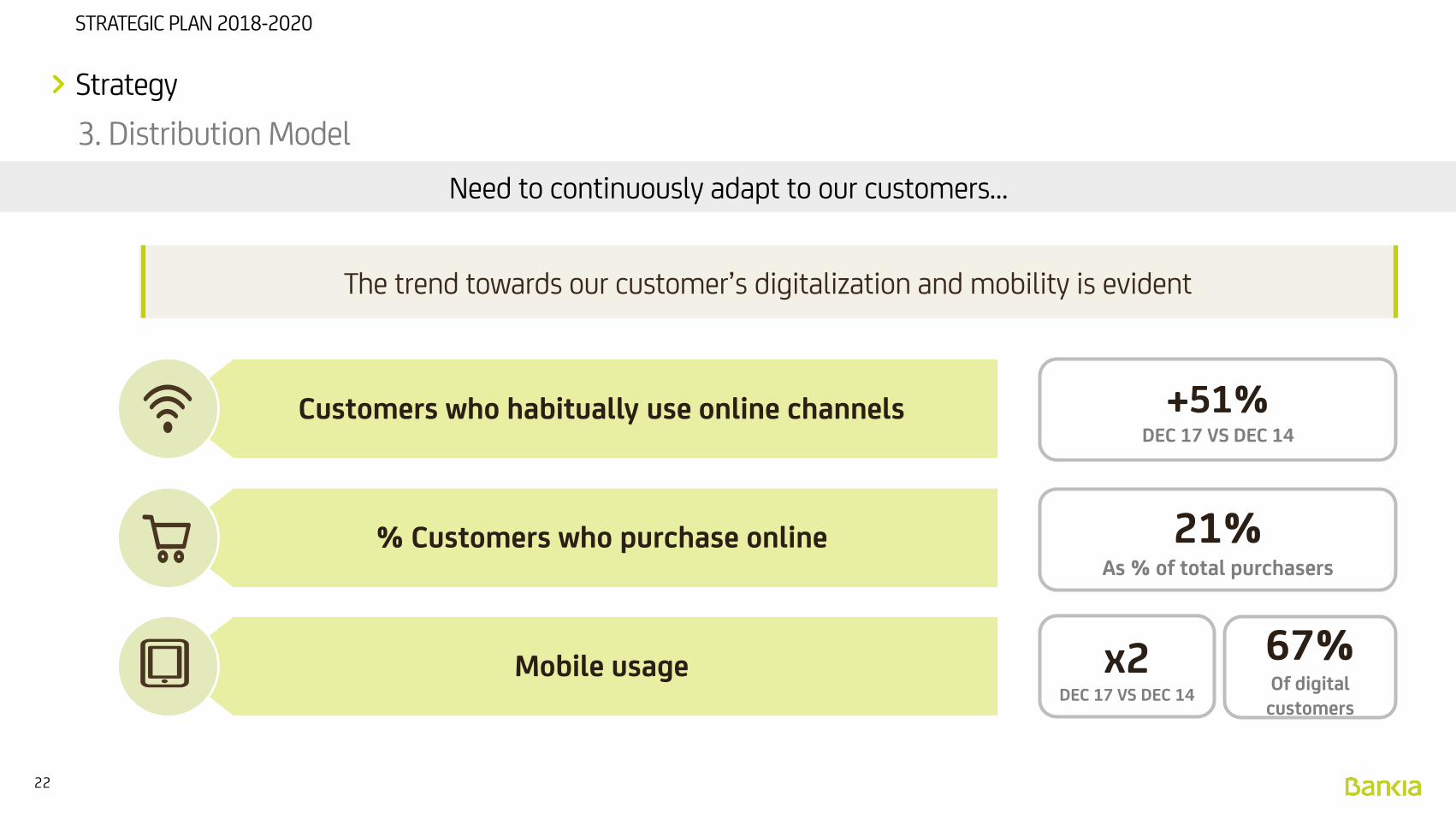

3. Distribution Model

Strategy

The trend towards our customer’s digitalization and mobility is evident

+51%DEC 17 VS DEC 14

x2DEC 17 VS DEC 14

67%Of digital

customers

21%As % of total purchasers

Customers who habitually use online channels

% Customers who purchase online

Mobile usage

Need to continuously adapt to our customers…

23

STRATEGIC PLAN 2018-2020

3. Distribution Model

Strategy

of our customers bank exclusively

through the branches

40%

of our customers banked through the branches as well as other channels

(last 12 months)

80%

of our customers who purchased digital

also made purchases in a branch

42%

* Inmark. Global Report September 2017

83.9%* of bank’s customers banked through a branch as well as other channels

…but this must not hide the fact that our reality is multichannel

24

STRATEGIC PLAN 2018-2020

3. Distribution Model

Strategy

Different customer groups with constant changes in behavior

Flexibility and responsiveness

…to which we need to adapt

Additionally, to have an assigned personal manager significantly increases the degree of satisfaction

Our customers demand a combination of models…

25

STRATEGIC PLAN 2018-2020

3. Distribution Model

Strategy

In-branchAdvisers

+-

+

-Personalisation

Dig

ital

izat

ion

How our model adapts in the future will depend on our customers

22%

2014 2017

50%

CUSTOMERS WITH ACCOUNT MANAGER

… Increasing personalisation

Source: Bankia

We are responding by adapting our model…

26

STRATEGIC PLAN 2018-2020

3. Distribution Model

Strategy

NPS – RETAIL BANKING

2014 2017

~ 870

# CUSTOMERS / IN-BRANCH MANAGER # CUSTOMERS / “CONNECT” MANAGER

NPS – CONNECT WITH YOUR EXPERT

2016 2017

56.9% 60.9%

~ 2,100 managers

~ 280

~ 500 managers

PRODUCT SALES / EMPLOYEE PER MONTH

2014 2017

25 41

Branch efficiency has improved, enhancing service quality

2016 2017

28.6% 40.1%

2015

9.6%

~ 90 managers

Source: BankiaSource:. 3,151 "Connect with your Expert" customers surveyed in 2017

Source: BankiaSource: Bankia

Source: 58,388 retail customers surveyed in 2017

2015 2017

~ 1,150

…and with an increasingly efficient management, which is a key factor for the future

27

STRATEGIC PLAN 2018-2020

3. Distribution Model

Strategy

Usage of Big Data

Contacts defined based on customer’s propensity

Leads prioritized by customer, manager and channel

Distribution of commercial action based on customer management instead of products

A

B Better tools for account managers

Better customer information, “Robo4Advisor”, etc.

How to continue improving the Commercial Model?

28

STRATEGIC PLAN 2018-2020

3. Distribution Model

Strategy

We started in 2015…

New App

New portal Bankia.es

Redesign Bankia online

Our digital channels are the same level that those of our

competitors

There are no stable competitive advantages

At the same time, we are making progress in our digital channels

29

STRATEGIC PLAN 2018-2020

3. Distribution Model

Strategy

16%

2020

~ 35%

Targets for 2020…

DIGITAL SALES

Dec 2017

40%

2020

~ 65%

% DIGITAL CUSTOMERS

Dec 2017Dec 2015

7%

Dec 2015

33%

Target:+2mn digital

customers

BKIA+BMN 12.7% 38.5%BKIA+BMN

And we will continue investing to offer our customers the best

platforms

IT Investment 2018-2020

€1bn

Of which “change”

investment: 51.7%

Accompanying our customers on the process of digitalization of their relationship with the bank

30

STRATEGIC PLAN 2018-2020

3. Distribution Model

Strategy

We look at different time horizons…

Payment services

Open Business

New technologies

Competitive field in the next three years

Platform is under construction. Will be an important competitive factor for the next strategic plan

Monitoring and testing of progress in more mature technologies (artificial intelligence) and emerging technologies (blockchain)

Strategy of collaboration in FINTECH

2018

What do we expect in the future?

31

STRATEGIC PLAN 2018-2020

3. Distribution Model

Strategy

Strategic alliancesto lock in a dominant position

We start from a very good competitive position

Of total purchases with cards in Spain,

11.62% is with Bankia cards

12.22% of card collections in Spain are

through Bankia “Point of Sale” terminals

Provide our customers with all the payment services available in the market

Allow companies and retailers that are payment initiators to collect using any

payment method available in the market

(payment services and intermediaries)

Example in cards

The main challenge within the horizon of our Strategic Plan is PAYMENTS

32

STRATEGIC PLAN 2018-2020

Strategy

The CUSTOMER is at the center of our strategy

Strategic Priorities to better

serve our customers

Positioning

Processes improvement

Distribution Model

In order to execute anexcellent implementation…

Speed in deployment

Flexibility and capacity to adapt in a changing environment

We have a proven execution capacity

Bankia’s Strategic Priorities

33

STRATEGIC PLAN 2018-2020

Strategic Objectives 2020

Our goal: to be the best bank in Spain

Creating value for our shareholders

Satisfied customers

Committed teams

Recognitionfrom society

Sustainable profitability

Efficiency

Solvency

What is our aspiration?

34

STRATEGIC PLAN 2018-2020

Strategic Objectives 2020

Organic Capital Generation Model

2020E

<47%Efficiency Ratio

12%

ROE (1) 10.8%

Solvency CET1 FL

<6%NPAs

~ €1,3bnPAT

(1) Adjusted to 12% CET1 FL

Sustainable profitability

35

STRATEGIC PLAN 2018-2020

Strategic Objectives 2020

An ordinary cash pay out in the region of 45-50%

And the return of excess capitalabove 12% CET1 FL

(1) Includes cash pay out and y return of capital above 12% CET 1 FL

Fulfilling this Strategic Plan will allow us…

Capital distribution policy

Expected total remuneration > €2,500mn(1)

36

STRATEGIC PLAN 2018-2020

LINES OF ACTION OF THE NEW PLAN

2

37

STRATEGIC PLAN 2018-2020

MACROECONOMIC ENVIRONMENT1

MAIN THEMES OF OUR STRATEGIC PLAN2

38

STRATEGIC PLAN 2018-2020

General macro trends

Macroeconomic environment

GDPYear-on-year change

JOB CREATIONYear-on-year change in Social Security affiliates (thousands)

CREDIT PERFORMANCEHousehold and corporate credit in Spain – Year-on-year change

Source: Bankia Research

INTEREST RATES12-month Euribor – year-end data

2016

3.3%

2015

3.4%

2017

3.1%

2016

- 8 pbs

2015

6 pbs

2017

-19 pbs

2016

563

2015

530

2017

622

2016

-2,9%

2015

- 4,3%

2017

-2,0%

Main macroeconomic indicators performance

39

STRATEGIC PLAN 2018-2020

Credit performance in Spain

Macroeconomic environment

CREDIT TO BUSINESSES AND HOUSEHOLDS – EURO AREA / SPAIN

CREDIT PERFORMANCE

HOUSINGEURO AREA/SPAIN

Year-on-year change

Year-on-year change

2%

-1.8%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

dic1

2

mar

13

jun

13

sep1

3

dic1

3

mar

14

jun

14

sep1

4

dic1

4

mar

15

jun

15

sep1

5

dic1

5

mar

16

jun

16

sep1

6

dic1

6

mar

17

jun

17

sep1

7

dic1

7

%

UEM España

4.1%

-2,6%

-6%-5%-4%-3%-2%-1%0%1%2%3%4%5%

dic1

2

mar

13

jun1

3

sep1

3

dic1

3

mar

14

jun1

4

sep1

4

dic1

4

mar

15

jun1

5

sep1

5

dic1

5

mar

16

jun1

6

sep1

6

dic1

6

mar

17

jun1

7

sep1

7

dic1

7

%

CREDIT PERFORMANCE

BUSINESSESEURO AREA/SPAIN

Year-on-year change-25%

-20%

-15%

-10%

-5%

0%

5%

dic1

2

mar

13

jun1

3

sep1

3

dic1

3

mar

14

jun1

4

sep1

4

dic1

4

mar

15

jun1

5

sep1

5

dic1

5

mar

16

jun1

6

sep1

6

dic1

6

mar

17

jun1

7

sep1

7

dic1

7

%

0.1%

-2.9%

Source: Bankia Research

Credit growth in Spain below Euro Area average

dec1

2

mar

13

jun

13

sep1

3

dec1

3

mar

14

jun

14

sep1

4

dec1

4

mar

15

jun

15

sep1

5

dec1

5

mar

16

jun

16

sep1

6

dec1

6

mar

17

jun

17

sep1

7

dec1

7

dec1

2

mar

13

jun

13

sep1

3

dec1

3

mar

14

jun

14

sep1

4

dec1

4

mar

15

jun

15

sep1

5

dec1

5

mar

16

jun

16

sep1

6

dec1

6

mar

17

jun

17

sep1

7

dec1

7

dec1

2

mar

13

jun

13

sep1

3

dec1

3

mar

14

jun

14

sep1

4

dec1

4

mar

15

jun

15

sep1

5

dec1

5

mar

16

jun

16

sep1

6

dec1

6

mar

17

jun

17

sep1

7

dec1

7

40

STRATEGIC PLAN 2018-2020

43%

39%

88%

51%

España

UEM

Max histórico dic-17

Debt as % GDP

Macroeconomic environment

CREDIT TO BUSINESSES AND HOUSEHOLDS AS % GDP HOME LOANS AS % GDP

Debt as % GDP

Euro areaSPAIN

Debt as % GDP

46%

38%

62%

39%

España

UEM

Max histórico dic-17

CREDIT TO BUSINESSES AS % GDP

Debt as % GDP

Source: Bankia Research

DEC 03 DEC 10 DEC 17

GAP: 15 p.p.

84%

99%

GAP: 62 p.p.

104%

166%

GAP: 14 p.p.

90%

104%

The deleveraging process in Spain is almost complete

Spain

Spain

Historical max. Dec-17

Historical max. Dec-17

41

STRATEGIC PLAN 2018-2020

Source: Bankia Research

CREDIT PERFORMANCE

INTEREST RATE ASSUMPTION (%)

Macroeconomic trends favourable to banking business growthand asset quality improvement

Avg. rates EUR 12-month forward curve, 26 January 2018

Macroeconomic environment

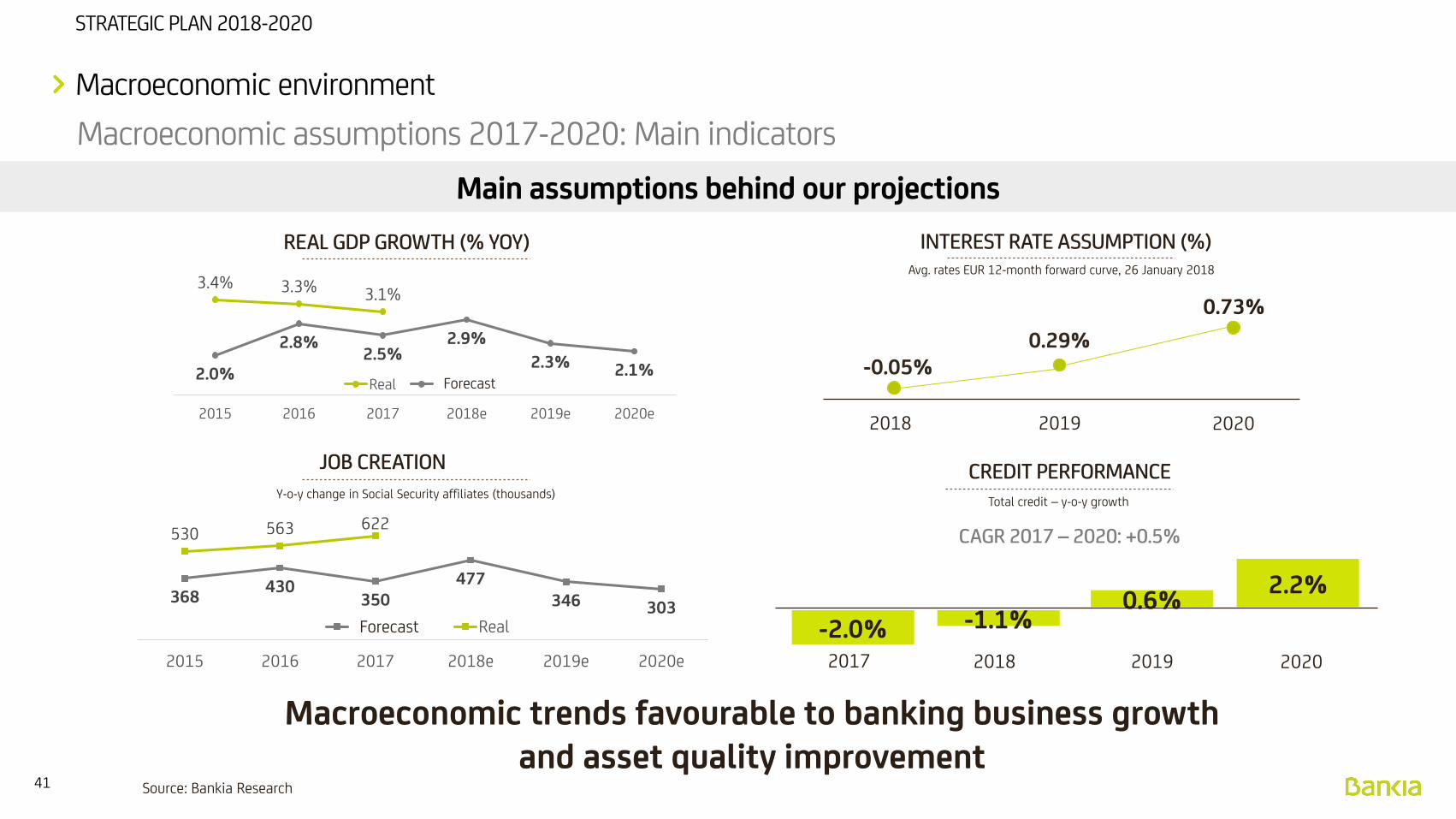

Macroeconomic assumptions 2017-2020: Main indicators

REAL GDP GROWTH (% YOY)

JOB CREATION

3.4% 3.3% 3.1%

2.0%

2.8%2.5%

2.9%

2.3% 2.1%

2015 2016 2017 2018e 2019e 2020e

Real Previsión

368430

350477

346 303

530 563 622

2015 2016 2017 2018e 2019e 2020e

Previsión Real

Y-o-y change in Social Security affiliates (thousands)Total credit – y-o-y growth

CAGR 2017 – 2020: +0.5%

-0.05%0.29%

0.73%

202020192018

2019

0.6%

2018

-1.1%

2020

2.2%

2017

-2.0%

Main assumptions behind our projections

Forecast

Forecast

42

STRATEGIC PLAN 2018-2020

Macroeconomic assumptions 2017-2020: Credit performance in Spain

Macroeconomic environment

CREDIT FORECASTS

HOUSING

CREDIT FORECASTS

BUSINESSES

CREDIT FORECASTS

CONSUMER FINANCE

TOTAL CREDIT FORECASTS - HOUSEHOLDS AND BUSINESSESHistoric and forecasted trends in Spain– €Thousand of millions

1,281

1,226

1,191

1,1671,154 1,160

1,185

2014 2015 2016 2017 2018e 2019e 2020e

In Spain €Thousands of millions

580552

536 522 512 508 510

2014 2015 2016 2017 2018e 2019e 2020e

545518 493 476 466 469 483

2014 2015 2016 2017 2018e 2019e 2020e

58 61 6979 87 92 98

2014 2015 2016 2017 2018e 2019e 2020e

Source: Bankia Research

CAGR 2017 – 2020: 0.5%

CAGR 2017 – 2020: - 0.8%

CAGR 2017 – 2020: 0.5%

CAGR 2017 – 2020: 7.4%

In Spain €Thousands of millions

In Spain €Thousands of millions

Sector credit growth trend

43

STRATEGIC PLAN 2018-2020

Macroeconomic assumptions 2017-2020: indebtedness levels

Macroeconomic environment

CREDIT TO COMPANIES AND HOUSEHOLDS AS % GDP

Debt as % GDP

Forecasted GDP growth and credit to businesses andhouseholds in Spain should cause the country to converge withthe euro area indebtedness levels

Source: Bankia Research

Euro areaSPAIN

CREDIT TO BUSINESSES AS % GDP

Debt as % GDP

HOME LOANS AS % GDP

Debt as % GDP

Euro areaSPAIN

DEC 17

GAP: 4 p.p.

39%

43%

DEC 20

36%

(7 p.p.)

DEC 17

GAP: 8 p.p.

38%

46%

DEC 20

38%

(8 p.p.)

DEC 17

GAP: 14 p.p.

90%

104%

DEC 20

89%

(15 p.p.)

Under the projected scenario we converge with the euro area in households and companies indebtedness

44

STRATEGIC PLAN 2018-2020

Macroeconomic assumptions 2017-2020: funds performance

Macroeconomic environment

Source: Bankia Research

CUSTOMER FUNDS PERFORMANCEHistoric and forecasted trend – €Thousands of millions

CAGR 2017 – 2020: 7.5%

1,1261,160

1,205

1,262

1,3151,356

1,393

2014 2015 2016 2017 2018e 2019e 2020e

Depósitos + Fondos de Inversión

CAGR 2017 – 2020: 3.3%

195220

235263

294315

327

2014 2015 2016 2017 2018e 2019e 2020e

FORECASTS

MUTUAL FUNDS

In Spain € Thousands of millions

CAGR 2017 – 2020: 2.2%

FORECASTS

DEPOSITS

In Spain € Thousands of millions

931 940970

9991,021

1,0411,066

2014 2015 2016 2017 2018e 2019e 2020eCAGR 2014 – 2017: 3.9%

Deposits + Mutual Funds

Customer funds will also trend upward over the next few years

45

STRATEGIC PLAN 2018-2020

MACROECONOMIC ENVIRONMENT1

MAIN THEMES OF OUR STRATEGIC PLAN2

46

STRATEGIC PLAN 2018-2020

1

2

3

4

Execution of BMN’s integration

Efficiency and cost control

Revenue growth via increased sale of high value products

Accelerated reduction of NPAs

Main themes of our Strategic Plan

Four main themes underpinning our Strategic Plan

47

STRATEGIC PLAN 2018-2020

PresentationBankia-BMN merger

plan

Regulatory authorizations

IT integrationAdmission to trading

of new shares

Execution of BMN’s integration

Challenges

1. Unify commercial management

• NEO operating system• Commercial systematic approach• Operational Management, processes & transactions• Sales team Management Styles

• Same culture and values• Same positioning• Same sales intensity and quality

• Positioning: Closeness, Simplicity and Transparency

IT integration in 3 months

Workforce adjustment plan agreement

2. Consolidate a single network

3. Integrate customers consistently

26 June 2017 28 December 2017 19 March 201812 January 2018 15 February 2018

Main themes of our Strategic Plan

Goal: Same Identity, Culture and Management Style

48

STRATEGIC PLAN 2018-2020

1

2

3

4

Execution of BMN’s integration

Efficiency and cost control

Revenue growth via increased sale of high value products

Accelerated reduction of NPAs

Main themes of our Strategic Plan

Four main themes underpinning our Strategic Plan

49

STRATEGIC PLAN 2018-2020

OPERATING EXPENSES (1)

2018E 2019E 2020E

SYNERGIES

€190mn€66mn €149mn

35% 78% 100%

Efficiency and cost control

PROJECTED ANNUAL INCREASE IN EXPENSES

BMN restructuring expenses already provisioned in 2017

2017

1.95 2.09

2020

~1.90

2020

Increase in expenses

2.25%

Synergies

Wage and overhead inflation

2018 2019

2.00 2.04

+ €0.14bn

€bn

Expenses and regulatory investment

Digitalization expenses and investment & others

Workforce adjustments

Branch closures

Processes improvement

(0.19)

Main themes of our Strategic Plan

(1) Includes amortizations

Synergies derived from the integration with BMN exceed the announced €155mn

50

STRATEGIC PLAN 2018-2020

1

2

3

4

Execution of BMN’s integration

Efficiency and cost control

Revenue growth via increased sale of high value products

Accelerated reduction of NPAs

Main themes of our Strategic Plan

Four main themes underpinning our Strategic Plan

51

STRATEGIC PLAN 2018-2020

Lending to businesses

Consumer loans

Revenue growth

Mortgages

Payment services

Insurance

Mutual funds

A BImpulse to new lending Fees from high value products

Main themes of our Strategic Plan

52

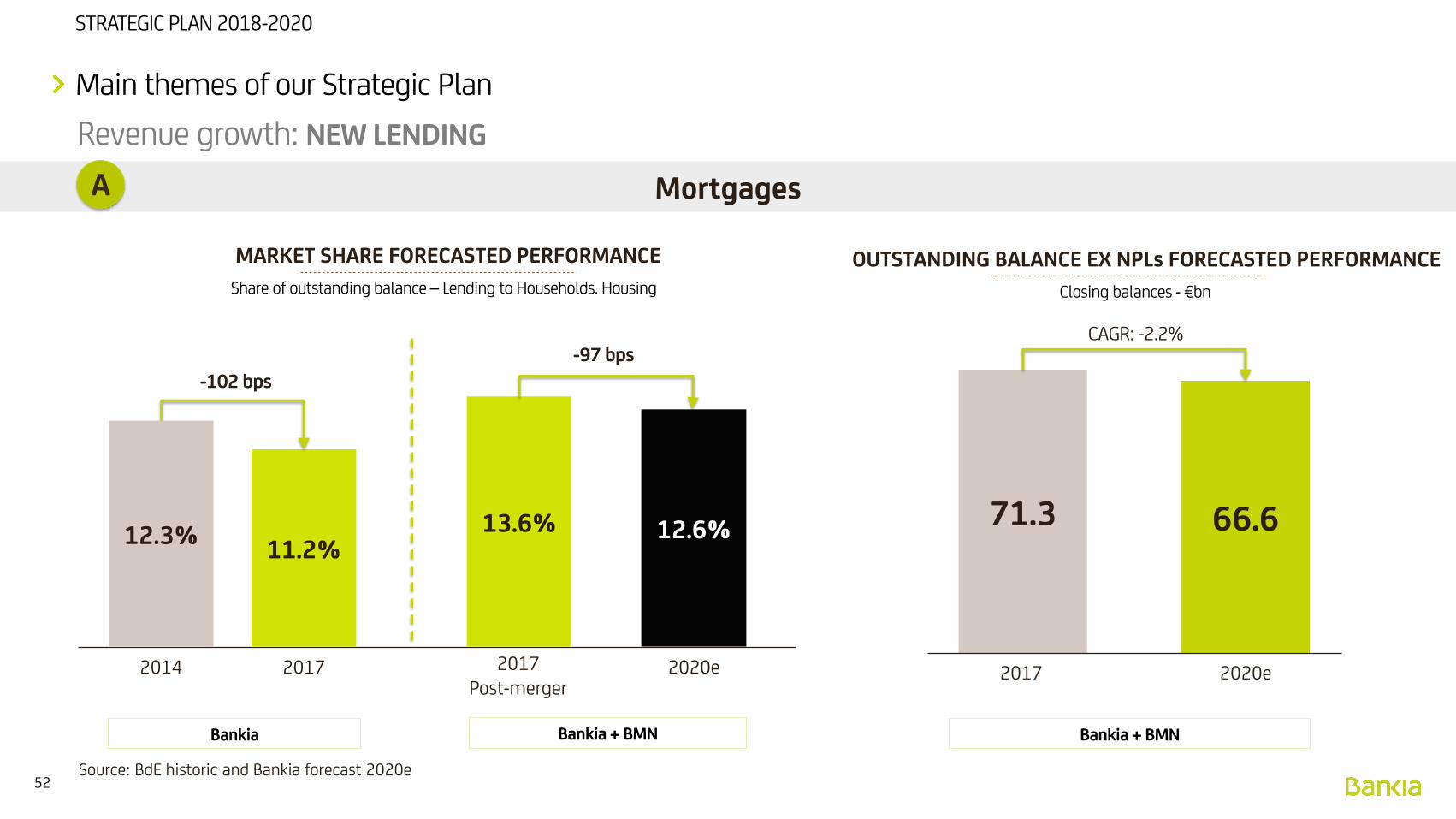

STRATEGIC PLAN 2018-2020

Revenue growth: NEW LENDING

Share of outstanding balance – Lending to Households. Housing

CAGR: -2.2%

-102 bps

MARKET SHARE FORECASTED PERFORMANCE

Closing balances - €bn

OUTSTANDING BALANCE EX NPLs FORECASTED PERFORMANCE

Bankia Bankia + BMN

-97 bps

Bankia + BMN

Source: BdE historic and Bankia forecast 2020e

11.2%

2017

13.6% 12.6%

2020e

71.3 66.6

2017 2020e2017Post-merger

12.3%

2014

Main themes of our Strategic Plan

MortgagesA

53

STRATEGIC PLAN 2018-2020

>70% of new loans are attributable to the market performance

Strong growth of real estate activity in regions where the Group is present(2)

“Hipoteca SIN Comisiones” (mortgage without fees)

Selective approach to the business

LTV <= 65% in new loans

Note (1): originations as % of new loans, not including renegotiated loansNote (2): real estate activity growth measured as home purchase and sale agreements per 100,000 inhabitants

+202 bps

+351 bps

Share of new loans 2018 – 2020

NEW LOANS

Bankia Bankia + BMN

GROWTH LEVERS

Focus on quality of new loans

5.2%

2017 (1)

7.3%10.8%

Average2018-2020e

2017 (1)

Post-merger

3.2%

2015 (1)

Main themes of our Strategic Plan

Source: BdE historic and Bankia forecast 2020e

MortgagesA

Revenue growth: NEW LENDING

54

STRATEGIC PLAN 2018-2020

Share of outstanding balance – Lending to Businesses

CAGR: 7.9%

+24 bps

Closing balances - €bn

Bankia Bankia + BMN

+77 bps

Note: balances for the businesses segment including RED

Bankia + BMN

6.0%

2017

6.9% 7.7%33.0 41.5

2017 2020e2017Post-merger

5.7%

2014 2020e

Main themes of our Strategic Plan

MARKET SHARE FORECASTED PERFORMANCE OUTSTANDING BALANCE EX NPLs FORECASTED PERFORMANCE

Source: BdE historic and Bankia forecast 2020e

Revenue growth: NEW LENDING

BusinessesA

55

STRATEGIC PLAN 2018-2020

85% of new loans are attributable to the market performance

Businesses model developed in the last few years

24bps gain in the period 2014-17 despite deleveraging in the legacy business

BMN allows us to grow in new regions

The return to new products in which the bank has experience will help capture market share

Core Business ex NPLs

CAGR: 5.6%

Note: Only Bankia data (does not include BMN)

Legacy Business ex NPLs

CAGR: -15.3%

GROWTH LEVERS

24.2 28.4

2014 2017

5.5 3.3

2014 2017

Main themes of our Strategic Plan

Revenue growth: NEW LENDING

Lending to businessesA

56

STRATEGIC PLAN 2018-2020

Real estate development

Syndicated lending

Other products, other

customers

Participation in syndicated loans and capital market operations with customers, previously restricted because of the Restructuring Plan

Gradual recovery of the real estate developer financing activity

Development of other fee-generating products (project finance, acquisition finance, etc.), as well as lending to non-resident companies

Market Size 2017(2)

109.7bn

Note (1): originations in period 2014 – 2017. Euro bn. The market in which the bank has been unable to operate includes investment grade rated customers, customers who had issued bonds in the last 12 months, who went public or had raised capital on the stock market, financing of transactions outside Spain, project finance (>8 years) and acquisition finance through SPVs

Ranking 2017

#4

Restricted Market (1)

€77.4bn

Note (2): market as of September 2017, latest figures available

Main themes of our Strategic Plan

Revenue growth: NEW LENDING

Lending to Businesses: Development of new productsA

57

STRATEGIC PLAN 2018-2020

Share of outstanding balance – Consumer Loans

CAGR: 16.2%

+81 bps

Closing balances - €bn

Bankia Bankia + BMN

+118 bps

Note (1): organic performance

CAGR 15 – 17: 16.6%Bankia ex BMN

Bankia + BMN

Source: dE

4.8%

2017

5.5%6.6%

4.46.8

2017 2020e

4.0%

2014

Main themes of our Strategic Plan

MARKET SHARE FORECASTED PERFORMANCE OUTSTANDING BALANCE EX NPLs FORECASTED PERFORMANCE

Source: BdE historic and Bankia forecast 2020e

Revenue growth: NEW LENDING

Consumer loansA

58

STRATEGIC PLAN 2018-2020

75% of estimated new loans are attributable to the market performance

Pre-approved credit lines (>85% of new loans) tested and with low CoR

Bankia has 2.5 million of pre-approved credit lines

BMN contributes 0.5 million customers with direct income deposits

Study of possible alliances in consumer finance

New loans

Pre-approved lines

Point of sale

Main themes of our Strategic Plan

Revenue growth: NEW LENDING

Consumer loans – business leversA

59

STRATEGIC PLAN 2018-2020

Revenue growth: FEE AND COMMISSION INCOME

Goal: to repeat the increase in market share achieved in the period 2014 - 2017

Bankia potential: disintermediation ratio (11% vs. 15% sector)(1)

BMN potential: lower penetration rate (3.9% vs 7.5%)

Share of outstanding balance – Mutual Funds

+82 bps

Bankia Bankia + BMN

+82 bps

GROWTH LEVERS

Note (1): Mutual funds / Customer funds + Mutual funds

Source: Inverco historic and Bankia forecast 2020e

5.8%

2017

6.4% 7.2%

2017Post-merger

5.0%

2014 2020e

Main themes of our Strategic Plan

MARKET SHARE FORECASTED PERFORMANCE

Mutual fundsB

60

STRATEGIC PLAN 2018-2020

# Credit cards

+89 bps

Bankia Bankia + BMN

+90 bps

GROWTH LEVERS

No. of POS terminals

+97 bps

+81 bps

Commercial positioning (Dec17 vs Dec15)Credit cards

+490,000 cards (+19.8%) +22.8% in debit and credit cards turnover

Point of Sale terminals

+19,300 customers (+32.9%) +46.7% in turnover

BMN customers: (credit card penetration rate in Bankia 30.20% of customers vs. 18.59% in BMN)

Opportunity to grow in retail establishments in BMN

Source: BdE historic and Bankia forecast 2020e(1) Latest share available: Sep 17 (2) Source: Servired Dec 17

7.1%

2017(1)

8.1%9%

2017Post-merger(1)

6.2%

2014 2020e

7.1%

2017(2)

8.2% 9%

2017Post-merger(2)

6.1%

2014 2020e

Main themes of our Strategic Plan

MARKET SHARE FORECASTED PERFORMANCE

Revenue growth: FEE AND COMMISSION INCOME

Payment servicesB

61

STRATEGIC PLAN 2018-2020

Bancassurance

GROWTH LEVERS

Newly created Bancassurance unit supporting the Retail Network and Business Banking

Specialized teams in Marketing and Channels

BMN contributes a higher penetration rate (22.3%) than Bankia (17.7%)

Retail Network

(Individuals and SMEs)

Business Banking

Marketing Channels

Main themes of our Strategic Plan

Revenue growth: FEE AND COMMISSION INCOME

InsuranceB

62

STRATEGIC PLAN 2018-2020

1

2

3

4

Execution of BMN’s integration

Efficiency and cost control

Revenue growth via increased sale of high value products

Accelerated reduction of NPAs

Main themes of our Strategic Plan

Four main themes underpinning our Strategic Plan

63

STRATEGIC PLAN 2018-2020

NPLS AND NPL RATIO PERFORMANCE

13.016.5

11.5

12.9% 10.8% 9.8%

DEC 14 DEC 15 DEC 16

20.0

14.7%

DEC 13

€Bn

9.7

DEC 17Bankia

8.5%

12.1

8.9%

Accelerated reduction of NPAs

Main themes of our Strategic Plan

DEC 17Bankia + BMN

€bn – net balances

FORECLOSED ASSETS PERFORMANCE

1.922.25

DEC 16

3.282.69

DEC 15 DEC 17Bankia

DEC 17Bankia + BMN

Average reduction per year: €2.6bn

Performance from peak

2.88

DEC 14

Average reduction per year: €0.3bn

We have achieved a major reduction in non-performing loans and foreclosed assets…

64

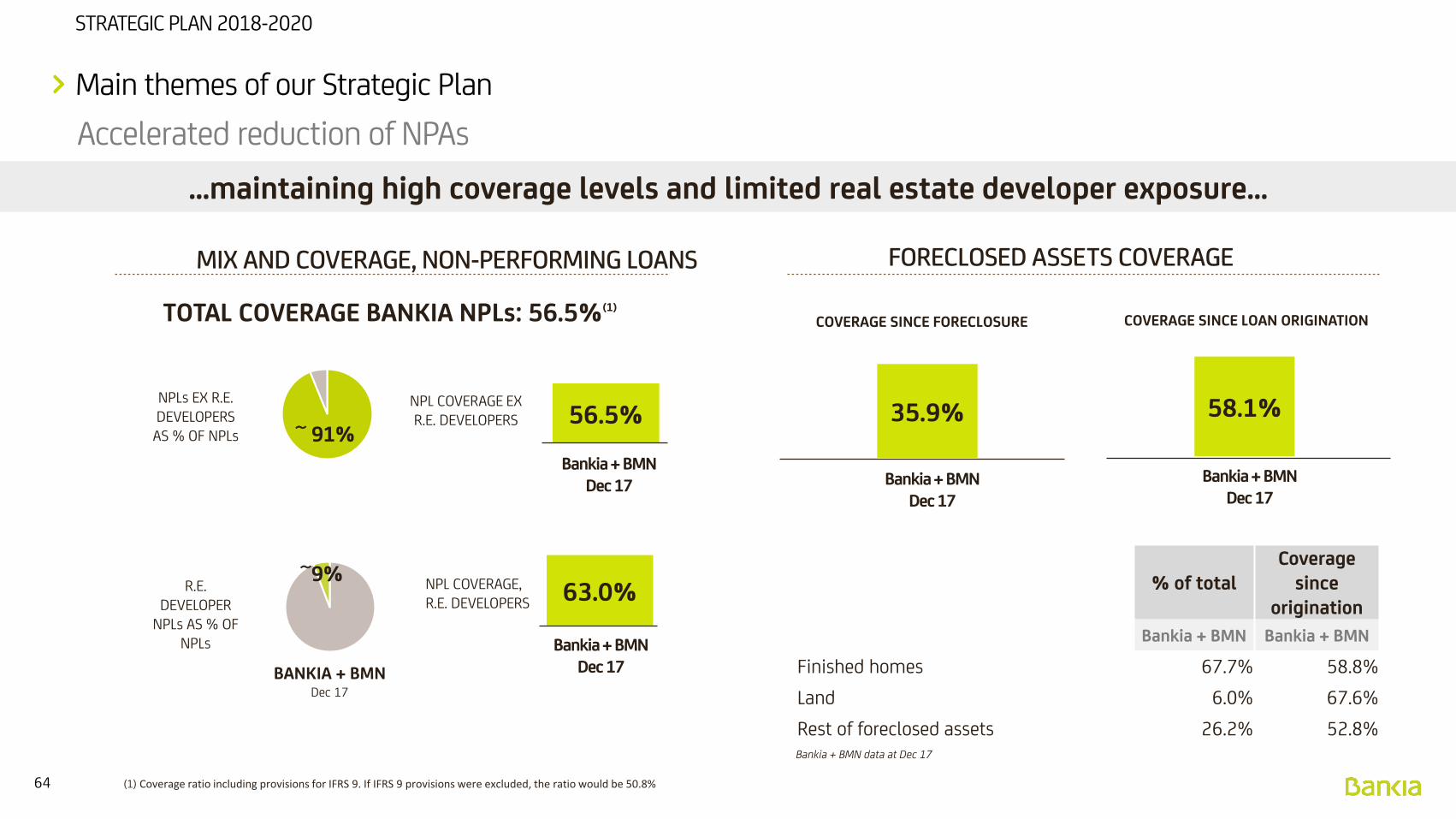

STRATEGIC PLAN 2018-2020

FORECLOSED ASSETS COVERAGE

Bankia + BMN Dec 17

~ 91%

MIX AND COVERAGE, NON-PERFORMING LOANS

NPL COVERAGE EX R.E. DEVELOPERS

Bankia + BMN Dec 17

NPL COVERAGE, R.E. DEVELOPERS

BANKIA + BMNDec 17

TOTAL COVERAGE BANKIA NPLs: 56.5%(1)

NPLs EX R.E. DEVELOPERS AS % OF NPLs

R.E. DEVELOPER

NPLs AS % OF NPLs

~9%

(1) Coverage ratio including provisions for IFRS 9. If IFRS 9 provisions were excluded, the ratio would be 50.8%

% of totalCoverage

since origination

Bankia + BMN Bankia + BMN

Finished homes 67.7% 58.8%

Land 6.0% 67.6%

Rest of foreclosed assets 26.2% 52.8%Bankia + BMN data at Dec 17

Bankia + BMN Dec 17

Bankia + BMN Dec 17

35.9% 58.1%56.5%

63.0%

COVERAGE SINCE FORECLOSURE COVERAGE SINCE LOAN ORIGINATION

Main themes of our Strategic Plan

…maintaining high coverage levels and limited real estate developer exposure…

Accelerated reduction of NPAs

65

STRATEGIC PLAN 2018-2020

(1) NPA ratio gross: Gross NPAs + Gross Foreclosed Assets / Total Risks + Gross Foreclosed AssetsNPA ratio net: Net NPAs + Net Foreclosed Assets / Total Risks + Gross Foreclosed Assets

(2) Coverage ratio including IFRS 9 provisions. If IFRS 9 provisions were excluded, the ratio would be 50.8%(3) 2017 data for Bankia not including BMN

PERFORMANCENON-PERFORMING

ASSETS

24 bps

NPA ratio (1)

NPL ratio

NPL coverage(2)

Cost of Risk(3)

2020e2017

12.5%

8.9%

56.5%

24 bps

<6.0%

<4.0%

~56%RATE OF REDUCTION NON-PERFORMING

ASSETS

€bn – gross amounts

€bn – gross amounts

Rise in home prices Employment recovery

Note: 2013, peak NPAs

24.1

2013

17.2

2017Bankia + BMN

8.412.8

2017Bankia

ANNUAL AVERAGE 2013 - 2017

2.8 2.9

BANKIA BANKIA + BMN

2020e

Main themes of our Strategic Plan

ANNUAL AVERAGE 2018e – 2020e

NPA ratio net 6.1% <3.0%

Accelerated reduction of NPAs

…trends that we maintain in our Strategic Plan…

66

STRATEGIC PLAN 2018-2020

51.2%

58.5%

24 bps

6.8%

Summary of targets

€0.8bn

2020e2017(1)

€0.26/share

<47%

<48%

24 bps

11.0%

€1.3bn

€0.43/share

Efficiency Ratio

Cost-to-income Ratio ex NTI

Cost of Risk

ROTE (2020 adjusted to CET1 FL of 12%)

Net Profit

Earnings per share

(1) Data for Bankia without BMN as of 31 December

+62%

+62%

Main themes of our Strategic Plan

6.7% 10.8%ROE (2020 adjusted to CET1 FL of 12%)

Increase in sustainable profitability

67

STRATEGIC PLAN 2018-2020

STRATEGIC PLAN 2018-2020FINANCIAL BREAKDOWN

3

68

STRATEGIC PLAN 2018-2020

Main assumptions of the Financial Plan

Financial breakdown

2018 2019 2020

Eur 3m -0.30% -0.01% 0.44%

Eur 1 year -0.05% 0.29% 0.73%

IRR 1yr Spain -0.28% 0.11% 0.58%

Average spread on new lending (1):

New lending:

• 82% of new loans attributable to market performance

• 18% due to market share gain

Average rates for the period. Source: Bloomberg

Average rate on new retail deposits:

The Plan includes wholesale debt issues that allow to reach an MREL ratio of 20% by 2020

CAGR 2017 – 2020e

Total portfolio: +1.7%Housing : -2.2%

Businesses: 7.9%Consumer finance 16.2%

LOANS AND RECEIVABLES EX NPLS PERFORMANCE (€BN)The plan assumptions are based on the forward curve of 26 January 2018:

Yield curve Spreads Volumes

(1) Ex public sector

2.6%

2017 Average 2018e – 2020e

2.5%

0.06%

2017

0.12%

2020e

Scenario 2018-2020

69

STRATEGIC PLAN 2018-2020

Interest Margin

Financial breakdown

Positive performance of interest margin due to rise in interest rates and mix improvement

0.3

2.3

2020e

2.9

2017Bankia + BMN

Volume +credit mix

€bn

INTEREST MARGIN

0.3

Rates impact:(+) credit book

(-) Funding and MREL(-) Income from Fixed

Income portfolio

CREDIT YIELD

2018e

1.7%1.7%

2020e

RatesVolume

Mix

30%

70%

2.4%

2017

1.03% 1.79%Yield mortgages

2.70% 3.11%Yield other credit (1)

2017 2020

(1) Consumer Finance, Businesses and other

122bn 125bnNet total loans and advances

Avg. balance122bn

87% of the book varies with euribor

Change in mix: weight of Businesses and Consumer Finance over total credit book changes from 32% in 2017 to 40% in 2020

70

STRATEGIC PLAN 2018-2020

Fee and commission income

Financial breakdown

FEE AND COMMISSION INCOME GROWTH DRIVERS

Lending products: performance linked to new lending

Saving products: increased disintermediation towards mutual funds and pension funds

Payment Services: increased penetration in cards and point of sale terminals

Insurance: new bancassurance unit with specialized teams

~ €0.2bnFee and commission

income growth2020e vs 2017

~ 7% CAGR2018e – 2020e

One single franchise and commercial management boosts fee and commission income

71

STRATEGIC PLAN 2018-2020

Gross income and loan portfolio composition

Financial breakdown

LOAN PORTFOLIO EX NPLs

Credit portfolio by segment

61% 54%Mortgages

Businesses 28% 34%

Consumer finance 4% 6%

2020e2017

Other* 7% 7%

*Public Sector and others

Net interest income and fee and commission income as the main components of gross income

COMPOSITION OF GROSS INCOMENet interest income, Fee and commission income and Net trading

income as % of Gross income

(1) Bankia + BMN full year data

2020e

63% 8 p.p.

29%

12%

Net interest income Fee & c. income NTI

71%

30%

2%

1 p.p.

10 p.p.

2017(1)

72

STRATEGIC PLAN 2018-2020

Operating expenses

Financial breakdown

OPERATING EXPENSES€bn

2020e

1.95 1.90

+ 0.14

2.09

- 0.19

Expense glide

Synergies2020e

COST TO INCOME RATIO

2020e

<47%56%

Restructuring expenses already provisioned

Ratio ex NTI: <48%

2017 (1)2017

(1)

(1) Bankia + BMN full year data

Strict cost control discipline improving our efficiency level

-2,5%

73

STRATEGIC PLAN 2018-2020

Cost of risk

Financial breakdown

Initial high coverage levels:

NPLs: ˜56%

Foreclosed assets: 58.1%

RED balance (1.1% of total portfolio)

Reduced exposure to land

Rating improvements at Businesses conforming the credit stock

€8.8bn reduction in NPAs expected in 2018 – 2020e (51% of 2017 closing stock)

Track record in NPLs sales: €4.2bn of sales in 2014-2017 without impact on P&L

Capacity to mitigate impact of new loans (businesses and consumer finance) on CoR

IFRS 9 impact in 1Q 2018

Reduction of refinanced loans “on watch” >€300mn in 2H17

Well provisioned balance sheet Reduction of NPAs Limited impact of IFRS 9

Cost of risk close to current levels (24 bps)

74

STRATEGIC PLAN 2018-2020

Financial breakdown

Improvement in CORE businessNet Interest Inc. + Fee income

Operating expenses -2.5%

StableCost of risk

Profitability

€0.8bn

2020e

+62%

€1.3bn

2017(1)

(1) Bankia ex BMN

Increase in profit: CORE business improvement and cost control due to cost of risk

75

STRATEGIC PLAN 2018-2020

Funding and liquidity

Financial breakdown

FUNDING STRUCTURE

<100%LTD 2020E

>100%NSFR 2020E

<150%LCR 2020E

20%MREL 2020E

MAIN TARGETS

WHOLESALE DEBT MATURITIES

40%

9%24%

19%

8%

DECEMBER 2014 DECEMBER 2017

58%

10%

17%

9%8%

63%10%

16%

12%

DECEMBER 2020

Retail deposits Issues and Treasury other ECB Wholesale deposits Repos

€BN

RATINGS

BBB-Positive outlook

BBB-Positive outlook

BBB (HIGH)

Stable outlook

12.91.0

2.8

1.4

0.4

0.4

3.2 4.8 0.4 1.5 14.4

2018 2019 2020 2021 > 2021

1.5

0.1

1.0

2.8

Covered BondsSubordinated Debt

Senior Debt

Solid liquidity position

76

STRATEGIC PLAN 2018-2020

Capital - MREL

Financial breakdown

MREL REQUIREMENTS

The cost of issuing an additional 1.0% of “Senior Non-Preferred” debt is estimated at €1.7mn per year

ISSUANCE PLAN 2018 – 2020E

a. Debt maturities 8.4

b. Planned debt issuances ~8.9

AT1 + T2 ~1.6

SNP + Covered bonds ~7.3

a – b = Net issuances +0.5

€BN

MREL 2020e

CET 1

~12%

AT1: 1.5%

T2: 2%

SNP: <4.5%

~20%

MREL 2017

CET 1

12.3%

AT1: 0.9%

T2: 1.9%

15.1%

Issuance plan focused on compliance with MREL requirements by 2020

77

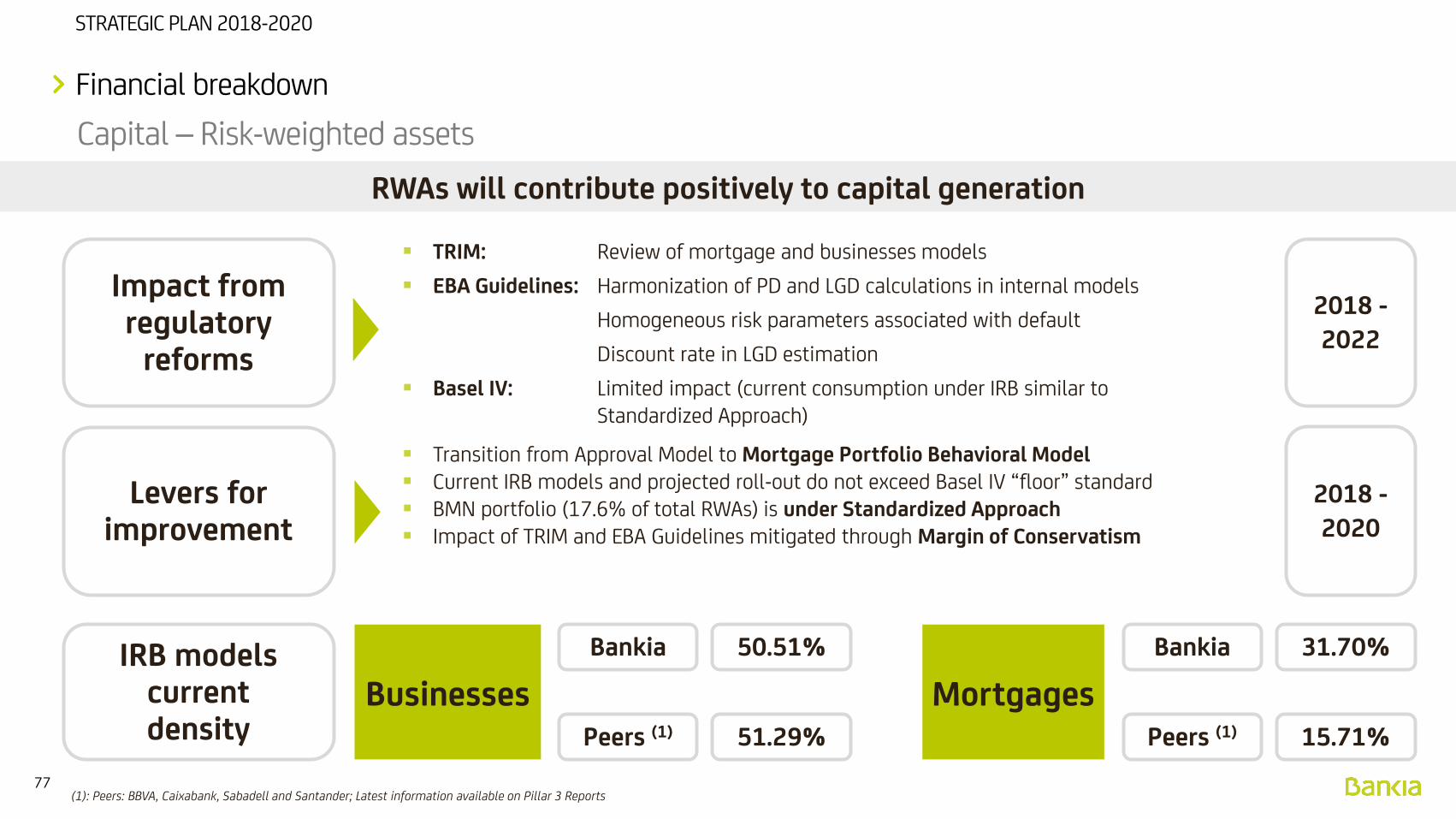

STRATEGIC PLAN 2018-2020

Financial breakdown

2018 -

2022

TRIM: Review of mortgage and businesses models

EBA Guidelines: Harmonization of PD and LGD calculations in internal models

Homogeneous risk parameters associated with default

Discount rate in LGD estimation

Basel IV: Limited impact (current consumption under IRB similar toStandardized Approach)

Transition from Approval Model to Mortgage Portfolio Behavioral Model Current IRB models and projected roll-out do not exceed Basel IV “floor” standard BMN portfolio (17.6% of total RWAs) is under Standardized Approach Impact of TRIM and EBA Guidelines mitigated through Margin of Conservatism

2018 -2020

Capital – Risk-weighted assets

Impact from regulatory

reforms

Levers for improvement

RWAs will contribute positively to capital generation

IRB modelscurrentdensity

Businesses Mortgages

Bankia

Peers (1)

Bankia

Peers (1)

50.51%

51.29%

31.70%

15.71%

(1): Peers: BBVA, Caixabank, Sabadell and Santander; Latest information available on Pillar 3 Reports

78

STRATEGIC PLAN 2018-2020

Capital

Financial breakdown

MREL LEVEL

Substantial organic capital generation through profit growth and RWAs optimization

Payout ratio of 45-50%

Issuance plan to achieve a MREL of 20%

Return of capital above 12% CET1 FL

CET1 FULLY LOADED

(1): Ratio without sovereign gains and including the impact of IFRS 9 (ratio with sovereign gains 14.46%)

2020e

20%15%

2020e

12%

2017 (2)

12%

2017 (1)

High organic capital generation

79

STRATEGIC PLAN 2018-2020

Main levers for ROTE growth

6.8%

Interest Margin

~1.6%

~1.0%

Fees & Com.

11%

~(1.5%)

NTI andOther gross

margin

Costs & Synergies

~0.2%~0.4%

~0.7%

NPAs

(1) Data Bankia + BMNAdjusted ROTE to 12% CET 1Levers net of taxes, assuming tax rate of ~27%

RoTE 2017 (1) RoTE 2020e

Adjusted to 12% CET1

Rate Volumen / Mix

~1.2%

10%

ROTE 2020e

~1.0%

Excess capital

Other

~(0.3%)

Cost of Risk

Profitability

Financial breakdown

80

STRATEGIC PLAN 2018-2020

Financial breakdown

Summary of targets

2020e

€1.3bn

45 - 50%

€0.43

<47%

<6% / 24 bps

12%

PAT

Cash dividend Pay Out

Efficiency Ratio

NPA ratio / CoR

CET 1 FL

Profitability

Efficiency

Asset quality and Solvency

2020ewith forward curve to 2021 (1)

EPS

ROTE adjusted to CET1 FL of 12% 11.0%

€1.5bn

€0.51

12.5%

2020 Targets

ROE adjusted to CET1 FL of 12% 10.8% 12.2%

(1) 2020 metrics with 2021 forward curve rates(2) Includes cash pay out and return of capital above 12% CET1 FL

Return of capital > €2,500mn (2)

81

STRATEGIC PLAN 2018-2020

CONCLUSIONS

4

82

STRATEGIC PLAN 2018-2020

Conclusions

We have successfully ended our Restructuring Plan…

… fulfilling the targets set in 2012

We have an excellent starting point…

… to initiate a Growth stage

We count on a well defined Strategic Plan…

… and with a proven execution capacity

1

2

3

83

STRATEGIC PLAN 2018-2020

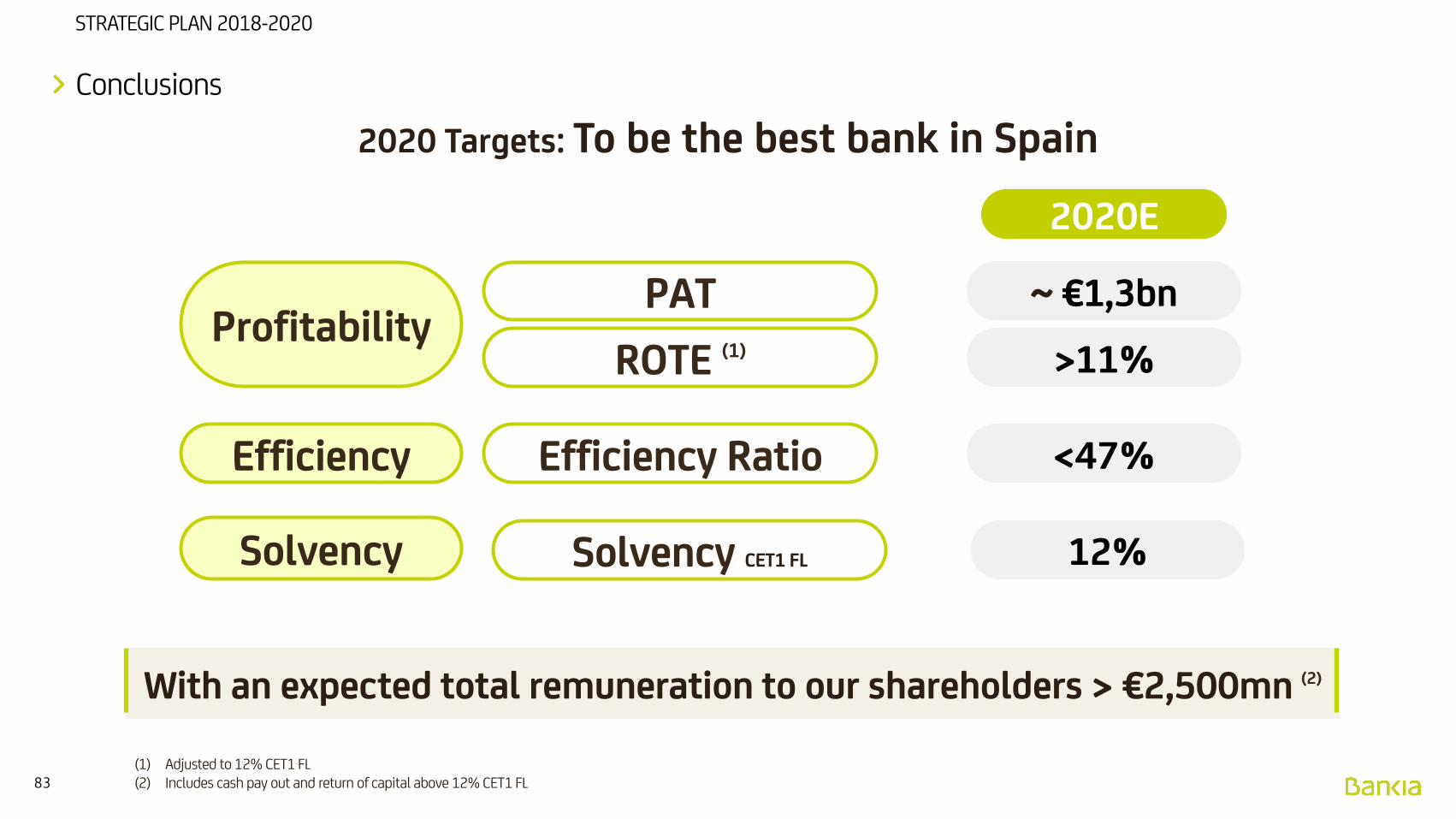

Conclusions

2020 Targets: To be the best bank in Spain

2020E

<47%Efficiency Ratio

12%

ROTE (1) >11%

Solvency CET1 FL

With an expected total remuneration to our shareholders > €2,500mn (2)

~ €1,3bnPAT

(1) Adjusted to 12% CET1 FL(2) Includes cash pay out and return of capital above 12% CET1 FL

Profitability

Efficiency

Solvency

84

STRATEGIC PLAN 2018-2020

Anexo

ANNEX

85

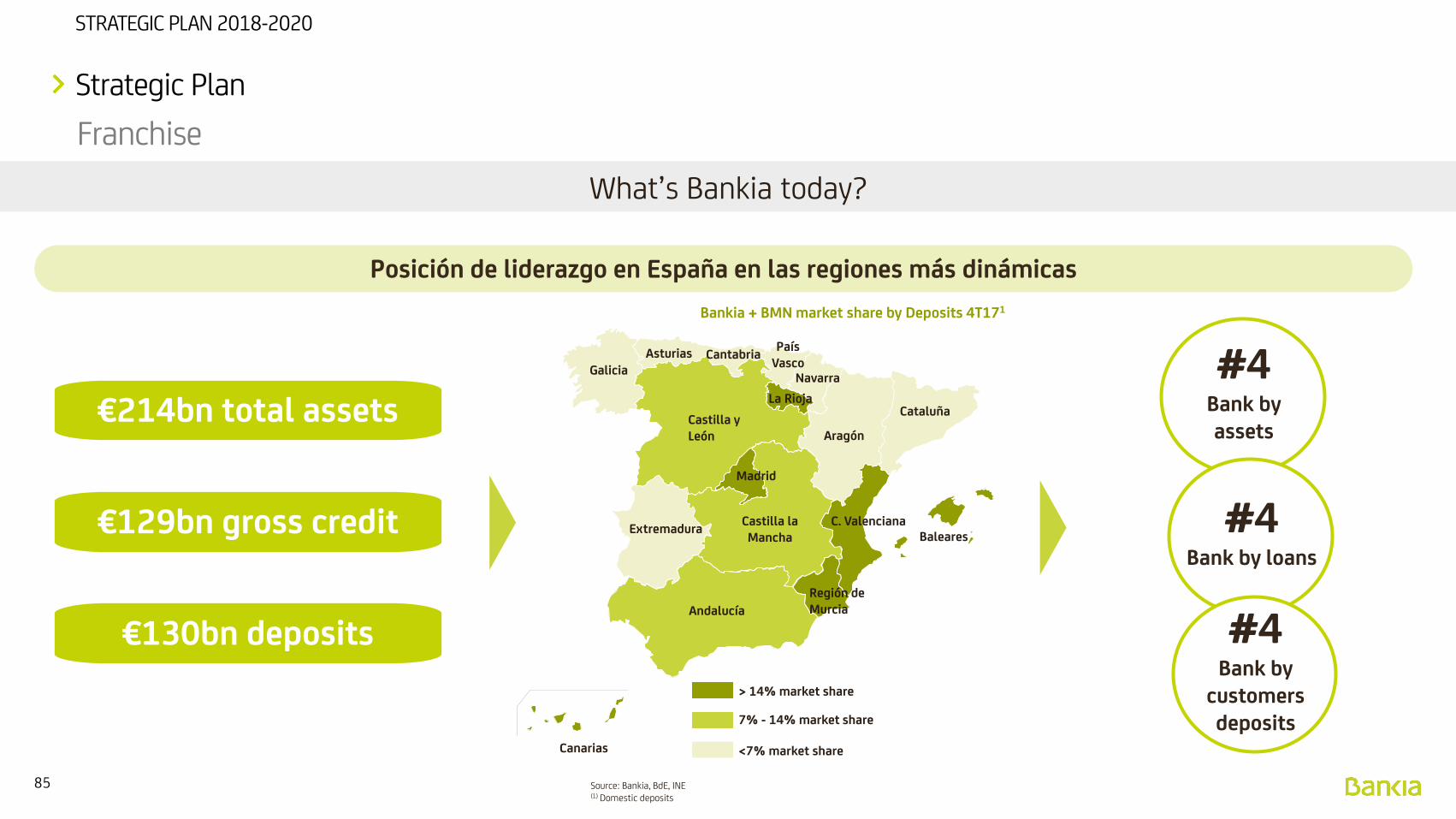

STRATEGIC PLAN 2018-2020

Extremadura

Madrid

Andalucía

Castilla la Mancha

Castilla y León

C. ValencianaBaleares

Región deMurcia

Galicia

Aragón

CataluñaLa Rioja

Navarra

Asturias CantabriaPaís

Vasco

> 14% market share

7% - 14% market share

<7% market share

Bankia + BMN market share by Deposits 4T171

Source: Bankia, BdE, INE(1) Domestic deposits

Canarias

Posición de liderazgo en España en las regiones más dinámicas

€214bn total assets

€129bn gross credit

€130bn deposits

#4Bank byassets

#4Bank by loans

#4Bank by

customersdeposits

Strategic Plan

Franchise

What’s Bankia today?

86

STRATEGIC PLAN 2018-2020

Microcredits

Volunteering

Engaged with local development

“Red Solidaria” Project

Additionally, in 2017 we financed Spanish businesses and households with €18bn

Boost to employment/employability

Environment

Sustainability

Education support

Sponsorships

252 projects and y 167,000 beneficiaries

First Spanish micro-finance institution with European structure

584 volunteers with a focus on Financial Education

Supporting 341 local NGO

Close to 5,000 beneficiaries

Permanent Improvement Plan and relevant results (DJSI and Footsie4Good)

Coefficiency Plan, maximum score on fight against climate change, A (CDP)

“FP Dual” Bankia Foundation

Cultural institutions with local roots

Recognition from Society

Contribution to society

We are engaged with society

87

STRATEGIC PLAN 2018-2020

Want to protect their personaldata better but don’t know how

73%consumers

Consider banks as aguarantee of data security(second only to hospitals)

64% consumers

think that their personaldata are valuable

87%consumers

GOVERNANCE & POLICY

• Appointment of Data Protection &

Privacy Officer (DPO)

• Training and awareness building in

employees, suppliers and other

responsible parties

RIGHTS MANAGEMENT

• Development of personal data

catalogue

• Data identification for exercise of

Portability Right

INFORMATION

• Adapt the legal drafting of

disclaimers

PROCESSES &

TECHNOLOGY

• Identification

and inventory of

personal data

SECURITY

• Security PIAs*

PRIVACY

Privacy Impact Assessment: a process for identifying and correcting or mitigating any security problems concerning an organisation’s personal data privacy policy.

*

Recognition from Society

Privacy

Create a secure and private digital environment for our customers