strategic sourcing - · pdf filebest practice • strategic sourcing: from periphery to the...

TRANSCRIPT

BEST PRACTICE

Outsourcing has become strategic-yet many executives

remain unprepared. A new era of capability sourcing will

trigger organizational redesign and require a new set of

managerial skills.

Strategic SourcingFrom Peripheryto the Coreby Mark Gottfredson, Rudy Puryear, and Stephen Phillips

FOR YEAR5, "sourcing" has been justanother word for procurement - a

financially material, but strategicallyperipheral, corporate function. Now,globalization, aided by rapid technol-ogy innovation, is changing the basis ofcompetition. It's no longer a company'sownership of capabilities that mattersbut rather its ability to control and makethe most of critical capabilities, whetheror not they reside on the company's bal-ance sheet. Outsourcing is becoming sosophisticated that even core functionslike engineering, R&D, manufacturing,and marketing can -and often should-be moved outside. And that, in tum, ischanging the way firms think abouttheir organizations, their vaiue chains,and their competitive positions.

Forward-thinking companies are mak-ing their value chains more elastic andtheir organizations more flexible. Andwith the decline of the vertically inte-

grated business model, sourcing is evolv-ing into a strategic process for organiz-ing and fine-tuning the value chain.Thequestion is no longer whether to out-source a capability or activity but ratherhow to source every single activity in thevalue chain. This is the new discipline of"capability sourcing."

Perhaps the best window on the newsourciiig landscape is a handful of van-guard companies that are transform-ing what used to be purely internalcorporate functions into entirely newindustries. Firms like United Parcel Ser-vice in logistics management, Solectronin contract manufacturing, and HewittAssociates in human resource manage-ment have created new business modelsby concentrating scale and skill withina single function. As these and otherfunction-based companies grow, so doesthe potential value of outsourcingto ailcompanies.

132 HARVARD BUSINESS REVIEW

It's not always obvious which func-tions have the most potential for devel-oping scale and skill. Virgin, for instance,has successfully extended its brand man-agement capabilities from planes andtrains to music, mobile phones, personalfinance, and even bridal wear. And youmight still think of Nike as a sneakerand sportswear company. But as it lendsits brand and merchandising expertiseto an increasing array of products-fromgolf instruction centers to MP3 playersto eyewear- it's evolving into a focusedprovider of marketing services to othercompanies.

Migrating from avertically integratedcompany to a specialized provider ofa single function is not a winning strat-egy for everyone. But all companiesneed to rigorously assess each of theirfunctions to determine in which theyhave sufficient scale and differentiatedskills and in which they don't. Greater

focus on capability sourcing can im-prove a company's strategic position byreducing costs, streamlining the organi-zation, and improving quality. Findingmore-qualified partners to provide crit-ical functions usually allows companiesto enhance the core capabilities thatdrive competitive advantage in theirindustries.

Yet despite the enormous opportuni-ties available through capability sourc-ing, our research indicates that manyexecutives remain unprepared for thistransformation. A recent Bain surveyof large and medium-sized companiesreports that 82% of large firms in Eu-rope, Asia, and North America have out-sourcing arrangements of some kind,and 51% use offshore outsourcers. Butalmost half say their outsourcing pro-grams fall short of expectations, only10% are highly satisfied with the coststhey're saving, and a mere 6% are highly

satisfied with their offshore outsourc-ing overall.

The reason these efforts often fail tomeasure up to expectations, even purelyin terms of cost savings, is that mostcompanies continue to make sourcingdecisions on a piecemeal basis. Theyhave not put hard numbers against thepotential value of capability sourcing,and they've been slow to develop a com-prehensive sourcing strategy that wiilkeep them competitive in a global econ-omy. To realize the full potential ofsourcing, companies must forget the oldperipheral and tactical view and makeit a core strategic function.

In this article, we'll describe how andwhy the role of sourcing is changing inthe twenty-first-century economy andlay out a practical strategic framework toguide companiesthrough the transition.

The Changing Basis ofCompetitive AdvantageFor over a century, companies competedon the basis of the assets they owned.AT&T, with its direct control of theAmerican telephone network; Bethle-hem Steel, with its large-scale manufac-turing plants; and Exxon, with its vast oilreserves, each dominated its respectiveindustry. But in the 1980s, the basis ofcompetition began to shift from hardassets to intangible capabilities. Micro-soft, for example, became the de factostandard in the computing industrythrough its skill in writing and market-ing software. Wal-Mart transformed re-tailing through its proprietary approachto supply chain management and itsinformation-rich relationships with cus-tomers and suppliers.

FEBRUARY 2005 133

BEST PRACTICE • Strategic Sourcing: From Periphery to the Core

A similar shift occurred iti the world-wide auto industry. When U.S. auto-makers began losing market share toJapanese companies, they were forcedto confront a growing gap in both costand quality. Recognizing that upstreamcomponent quality was critical to theirend product and seeing the success ofthe Japanese keiretsu model of net-worked suppliers, the Big Three beganto move design, engineering, and man-ufacturing work to specialized partners.They hammered out strategic sourcingrelationships for complex subassemblies

orative sourcing relationships. That re-quired the company to train and pro-mote a different kind of manager whowas capable of understanding systemeconomics, not just one who knew howto nickel-and-dime the supplier base.

The same dynamics were also at workin the credit card industry, which re-structured in response to a dramaticchange in the basis of competition fu-eled by technological innovation, in the1970S, most banks that issued creditcards also processed their own transac-tions in a very labor-intensive manner.

It's no longer ownership of capabilities that mattersbut rather a company's ability to control and makethe most of critical capabilities.

such as seats, steering columns, andbraking systems. To win a significantshare of their business, chosen suppliershad to meet tough cost and quality spec-ifications. More important.to ensure thelong-term success of a partnership, bothparties had to open their books, sharingdetailed information that became thebasis for continual quality and cost im-provements over many years. Both par-ties shared in the savings generatedfrom improved efficiency, which pro-vided ongoing incentives to identify andremove unnecessary costs.

This new approach to sourcing hadprofound effects on the automakers'operations and management. For ex-ample, Chrysler established what itcalled "value managed relationships," inwhich it consolidated component pur-chases with the few suppliers it believedcould sustain competitive costs, highquality, and efficient delivery. The car-maker and its key suppliers set a com-mon goal of achieving the lowest totalsystems cost. Before it could reach thisgoal, however, Chrysler had to refocusits entire procurement function so thatit could manage the new, highly collab-

But as computers automated transac-tion processing, tbe economies of scalegrew significantly, and individual issu-ers started to pool their transactions todrive down costs. The industry beganto separate into those companies thatissued cards and managed customers,on the one hand, and those that pro-cessed transactions, on the other, astransaction-processing underwent rapidcommoditization.

For example, despite having enviablescale in its own transaction-processingoperations, American Express, in a pre-scient strategic move, spun off its trans-action-processing business in 1992. Thenthe company negotiated a long-termservice contract with the newly inde-pendent entity. First Data. AlthoughAmex executives considered transactionprocessing a strategic capability-with-out reliable and efficient processing, itwas very difficult to make money in thecredit card business-they also saw thatcommoditization was eliminating anyproprietary advantage. As a spin-off,First Data could aggregate Amex's vol-ume with that of other companies (is-suing banks would have been reluctant

Mark Gottfredson ([email protected]) in Dallas, Rudy Puryear ([email protected]) in Chicago, and Stephen Phillips ([email protected]) inLondon are partners in Bain & Company.

to outsource processing to Amex as acompetitor), in that way, American Ex-press could gain additional scale advan-tages while ensuring long-term cost ef-fectiveness. Going forward, Amex wasable to focus on the issuing side of thecredit card business and enhance itscore capabilities in marketing and riskmanagement.

The decisions Chrysler and AmericanExpress made required them to chal-lenge one of the basic tenets of businessstrategy: that you should always keepstrategic capabilities within your walls.As globalization and technology trans-form more industries, all companies willeventually have to let go of that com-fortable but simplistic guideline. A se-ries of geopwlitical, macroeconomic, andtechnological trends has opened theworld's markets, made business capa-bilities much more portable, and pro-duced a level of discontinuity that hasno precedent in modern economic his-tory. These events include the fall of theBerlin wall, China's embrace of capital-ism, the advent of worldwide tariff re-duction agreements, and the spread ofcheap, accessible telecommunicationsinfrastructure. In the new era of capa-bility sourcing, companies' value chaindecisions will increasingly shape theirorganizations and determine the kindsof managerial skills they need to acquireand develop in order to survive amidincreasingly fluid industry boundaries.

Capability Sourcingat 7-ElevenTo illustrate the power of capabilitysourcing, let's take a detailed look atone dramatically successful practitioner,which began as a most traditional, ver-tically integrated company.

Back in 1991, when 7 Eleven's currentCEO Jim Keyes was named vice presi-dent of planning and chairman of tbeexecutive committee, the retailer waslosing both money and market share.As the major oil companies added mini-marts to more and more of their gasstations, the convenience store indus-try was becoming crowded and cut-throat, putting both revenue and mar-gins under intense pressure. To attract

134 HARVARD BUSINESS REVIEW

strategic Sourcing: From Periphery to the Core • BEST PRACTICE

more customers, 7-Eleven needed to cutits operating costs substantially, expandthe range of its products and services,and increase the freshness of food items.

Keyes launched a business reviewaimed at tightening operations, re-building competitive advantage, andperhaps divesting a few noncore busi-nesses. The deeper he and his team got,however, the more apparent it becamethat 7-Eleven was trying to do too manythings and was not good enough at anyof them. The core of the business, Keyesbelieved, was merchandising skill-thepricing, positioning, and promotion ofgasoline, ready-to-eat food, and sundriesfor consumers driving cars. But 7-Eievenhad always been vertically integrated,controlling most of the activities in itsvalue chain. The company operated itsown distribution network, deliveredits own gasoline, made its own candyand ice. It even owned the cows that pro-duced the milk it sold. Managers wererequired to do lots of things other thanmerchandising - store maintenance,credit card processing, payroll, and ITsystems management. Keyes found ithard to believe that the company couldbe best-in-class in every one of thosefunctions.

As part ofhis initial assessment, Keyesstudied the company's bighly successfulJapanese unit, whose keiretsu modelof tight partnerships with supplierswas unique within 7-Eieven. By relyingon an extensive and carefully managedweb of suppliers to carry out many day-to-day functions, the Japanese storeswere able to reduce their costs and en-hance the quality of tbeir operations,spurring rapid growth and strong prof-its. After considering many options,Keyes concluded that the best way tosave the U.S. company was to adopt theJapanese model. The goal he set was to"outsource everything not mission crit-ical." This marked an abrupt and delib-erate break with the company's verti-cally integrated past.

All activities were on the table. Keyes'steam even evaluated strategic functionssuch as product distribution, advertis-ing, and procurement, attempting toidentify outside partners with greater

expertise and scale. Simply put, if a part-ner could provide a capability moreeffectively than 7-Eleven could itself,then that capability became a candidatefor outsourcing. Over time, the com-pany relinquished direct ownership ofmany parts of its business, includingHR, finance, IT management, logistics,distribution, product development, andpackaging. Yet despite moving at a rapidpace, Keyes remained cautious aboutlosing control and avoided the tempta-tion to take a one-size-fits-all approachto outsourcing.

The way 7-Eleven has structured eachpartnership depends on how importanteach function is to the company's com-petitive distinctiveness. For routine ca-pabilities like benefits administrationand accounts payable, 7-Eleven picksproviders that can consistently fulfill

cost and quality requirements. Morestrategic capabilities require more com-plex arrangements. Gasoline retailing,for example, represents an Importantsource of revenue tor many 7-Elevens, asgas is often the reason customers cometo the stores. So while the firm out-sources gasoline distribution to Citgo, itmaintains proprietary control over gaspricing and promotion - activities thatcould differentiate its stores if done well.

The company has paid similarly closeattention to its relationship with Frito-Lay, since snack foods are one of themost important product tines for con-venience stores. By allowing Frito-Layto distribute its products directly to thestores, 7 Eleven has been able to takeadvantage of the chip maker's vast ware-housing and transport system. But un-like other convenience store companies.

The Endgame: Dynamic Sourcing

%

GIVEN rHE RAPIDLY SHIFTING coNrouRS of the global

economy, companies need to be able to anticipate changes

in the economics and geography of outsourcing. It wasn't

long ago, for example, that most big companies had to own

their own warehouses and operate their own distribution systems. Third-

party logistics specialists had neither the skill nor the scale to handle

those functions. But today, suppliers like UP5 and FedEx are competing

fiercely to offer full-service logistics networks, and even the largest com-

panies can now outsource warehousing, distribution, and related activi-

ties. Such trends will only accelerate in the future, and those companies

that have recognized and prepared for them will be the first to capitalize

on them.

So, to ensure that it doesn't quickly become obsolete, a sourcing strat-

egy needs to consider not only present circumstances but aiso future

alternative scenarios. What trends will influence the sourcing options

available for each key capability? Is the supplier base growing rapidly,

and are innovative new outsourcers emerging? Are different regions of

the world investing heavily in particular capabilities-like contract man-

ufacturing or customer service-and will they offer greater cost or qual-

ity advantages in the future? The answers to such questions may encour-

age a company to pursue certain sourcing opportunities that might not

be highly attractive based on current numbers but could offer dramatic

benefits in the coming months and years. Or they may lead a company

to negotiate short-term sourcing contracts to keep options open, rather

than enter into long-term relationships. Ultimately, a company's skill

in quickly remolding its sourcing arrangements in response to market

conditions and rivals' moves may be its strongest competitive advantage,

FEBRUARY 2005 135

BEST PRACTICE • Strategic Sourcing: From Periphery to the Core

7'Eleven doesn't allow Frito-Lay to makecritical decisions about order quantitiesor shelf placement. Instead, the retailermines its e.xtensive data on local cus-tomer purchasing patterns to makethose decisions on a store-by-store basis.

The choice 7-Eleven has made to main-tain control over product selection andstocking illustrates a critical issue instrategic sourcing partnerships: when tokeep vital data confidential and whento share them with a partner. Similarlykey was 7-Eleven's decision to rely onan outside vendor, IRI, to maintainand format detailed customer purchas-ing behavior data while keeping thedata themselves proprietary. This gives7-Eleven a picture ofthe mix of productsits customers want indifferent locationswithout relying on outside decisionmakers like Frito-Lay for such informa-tion. In this way, 7-Eleven is able to struc-ture its supplier relationships to gain acapability without relinquishing controlover decisions that could make or breakits business.

For a few targeted product segments,7-Eleven has Identified opportunities

The Measure of Success

that call for an even deeper level of col-laboration. Company executives figuredout that their traditional, do-it-yourselfapproach to creating branded productswas cutting the company otf from thesuperior scale, resources, and creativityof major food suppliers. So they begansharing information with a select groupofmanufacturers, allowing them to cre-ate custom products for 7-Eleven stores.For example, 7-Eleven worked with Her-shey to develop an edible straw basedon the candy maker's popular TWizzlertreat. In retum, Hershey gave 7-Eleventhe exclusive right to sell the strawfor its first 90 days on the market. Tofurther promote the unique product,7-Eleven ioined with its syrup supplier,Coca-Cola, to come up with a Twizzler-flavored version of its proprietary Slur-pee drink. Such exclusive arrangementsreduce the strategic risk of sharing cus-tomer information while greatly ex-panding the set of unique products7-Eleven can offer.

Likewise, when the data on beersales showed that certain packaghigoptions were more successful than oth-

For 7-Eleven, strategic sourcing has translated into industry dominance. In the

past two years, the mini-mart retailer has led all major rivals in same-store

merchandise growth, inventory turn rate, and revenue per employee.

Same-StoreMerchandise Sales Growth(first half 2004 overfirst half 2003)

MerchandiseInventory TurnsOune 2003 tojune 2004)

22.2

3.5%

Merchandise SalesPer Employee(June 3003 tojune 2004)

$239K

7-Eleven Rest ofIndustry

7-Eleven Rest oftndustry

7-Eleven Rest ofIndustry

Sources: Annuat and quarterly SEC filings

ers, 7-Eleven forged a tight partnershipwith Anheuser-Busch to build sales inthose categories. Anheuser-Busch helped7-Eieven develop a product assortmentand establish merchandising standardsfor a new display. The beer giant alsoagreed to give 7-Eleven first-look op-portunities at new products. In retum,7-Eieven shares its customer informa-tion so together the two companiescan develop innovative marketing pro-grams, such as a cobranded NASCARpromotion targeting 7-Eleven's core cus-tomers and a Major League Baseballpromotion campaign. Anheuser-Buschis also using 7-Eleven store data, pro-vided daily by IRI, to test a new order-forecasting system that would link theretailer's orders more tightly with de-liveries from the brewer's wholesalers.

In addition to restructuring and en-hancing existing activities, 7-Eleven hasused creative sourcing partnerships topioneer entirely new capabilities. It re-alized, for example, that by being a one-stop source for a broad range of prod-ucts and services, it could gain a leg upon more narrowly focused competitors.So it has set up a consortium to providemultipurpose kiosks in its stores. Amer-ican Express supplies ATM functions,Western Union handles money wires,and CashWorks furnishes check-cashingcapabilities, while EDS integrates thetechnical functions ofthe kiosks. Here,too, 7-Eleven maintains control over thedata-in this case, information on howcustomers use the kiosks-which it viewsas critical to its competitive edge.

Some of 7-Eleven's outsourcing rela-tionships tie suppliers' financial inter-ests to its own. The company took anequity stake in Affiliated Computer Ser-vices, for instance, one of its major IToutsourcers. 7-Eleven also agreed toshare productivity gains from a servicesagreement with Hewlett-Packard. In aneven deeper collaboration, the companycreated a joint venture with prepared-foods distributor E.A. Sween: CombinedDistribution Centers (CDC) is a direct-store delivery operation that supplies7-Elevens with sandwiches and otherfresh goods. By drawing on the skills andscale of a specialist, 7-Eleven was able to

136 HARVARD BUSINESS REVIEW

Strategic Sourcing: From Periphery to the Core • BEST PRACTICE

cut its distribution costs from more than15% of revenues to 10% and eventuallyhopes to cut that figure in half again.But cost reduction is only a secondarybenefit. The real gains have come in ser-vice. When it owned its own distribu-tion network, 7-Eleven delivered freshgoods to its stores only a couple of timesa week. CDC now makes deliveties tostores once, and soon twice, a day. Morefrequent deliveries mean fresher prod-ucts, which draw more customers intothe stores.

By almost any measure, 7-Eleven'ssourcing strategy has transformed thecompany. In narrowing its focus to asmall, strategically vital set of capabili-ties-in-store merchandising, pricing, or-dering, and customer data anaiysis-the

company has reduced its capital assetsand overhead while streamlining itsorganization. It reduced head count 28%from 43.000 in 1991 to 31,000 in 2003and fiattened its organizational struc-ture, cutting managerial levels in halffrom 12 to six.

Today, 7-Eleven consistently outper-forms competitors. Same-store saleshave grown in four out of the last fiveyears. In the past two years, it has dom-inated the industry's vital statistics, withsame-store merchandise growth at al-most twice the industry average, reve-nue per employee at just about two-and-a-half times higher, and inventoryturns at 72% more than the industry av-erage. (See the exhibit "The Measureof Success") Furthermore, after its ac-

Should you always keep strategic capabilitieswithin your walls? As globalization and technologytransform more industries, all companies willeventually have to let go of that comfortable butsimplistic guideline.

quisition of two regional U.S. chains(Christy's Markets in the Northeast andRed D Mart in the Midwest), the firm'snew business model helped grow salesby more than 30% and increase grossprofit margins by 2%. 7-Eleven's stockappreciation over the past five years hasoutpaced all major competitors, includ-ing Casey's General Stores, the Pantry,and Uni-Mart.

A Frameworkfor Capability SourcingAs companies like Chrysler, AmericanExpress, and 7-Eleven have discovered,a strategic approach to sourcing can dra-matically improve your company's com-petitive position. So how do you makesomething that's always been tacticalmore strategic? You need to stop focus-ing on incremental cost improvementtargets, step back, and reevaluate yourstrategy and your capabilities. In work-ing through this process with clients,we've found that three steps can ensurethat decisions are made objectively andare based on facts.

The first step is to identify the com-ponents of your business that representthe core of the core. These are the activ-ities that your company does better andcheaper than its rivals. For 7-Eleven, thecore of the core is in-store merchandis-ing and product ordering. For drugmaker Pfizer, it's developing and mar-keting pharmaceutical compounds. ForAmerican Express, it's identifying cus-tomer segments and creating card of-ferings tailored to them. Everything elseexists to support the core of the core.

in deciding what to outsource andwhat to keep inside, 7-Eleven consideredtwo factors: whether a capability wasproprietary and whether it was com-mon enough that outside supplierscould achieve scale or other advantagesby supplying it to multiple companies.To determine proprietary value, execu-tives asked themselves two questions:Did 7-Eieven carry out the capability ina way that generated measurably morevalue than its competitors could deliver?And would the company suffer a highdegree of strategic damage if rivalscould imitate that capability? To deter-

I-FIBRUARY 2005 137

BEST PRACTICE • Strategic Sourcing: From Periphery to the Core

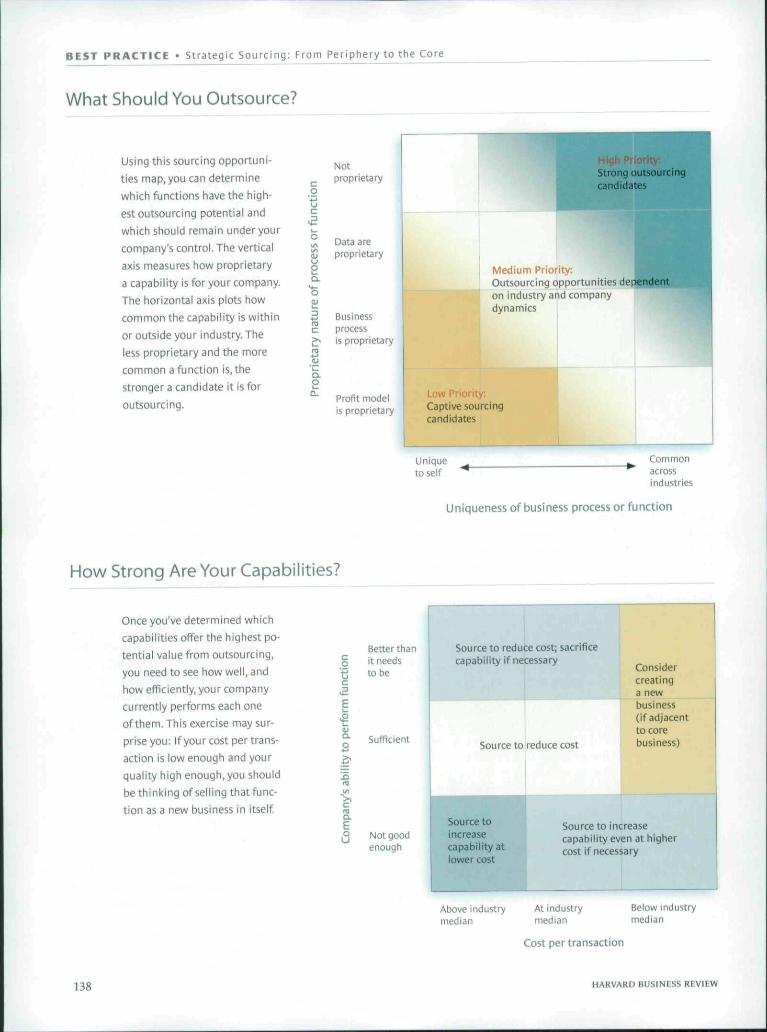

What Should You Outsource?

Using this sourcing opportuni-

ties map, you can determine

which functions have the high-

est outsourcing potential and

which should remain under your

company's control. The vertical

axis measures how proprietary

a capability is for your company.

The horizontal axis plots how

common the capability is within

or outside your industry. The

less proprietary and the more

common a function is, the

stronger a candidate it is for

outsourcing,

o

icti'

ao

a.

"Siturt

c>.

ieta

a.o

1 ^

proprietary

Data areproprietary

Businessprocessis proprietary

Profit modelis proprietary

High Priortty:^ Strong outsourcingl l candidates

Medium Priority:Outsourcing opportunities deiiendenton industry and companydynamics

Low Priority: " ^Captive soucandidates

Uniqueto self

rcmg "

Common* across

industries

Uniqueness of business process or function

How Strong Are Your Capabilities?

Once you've determined which

capabilities offer the highest po-

tential value from outsourcing,

you need to see how well, and

how efficiently, your company

currently performs each one

of them. This exercise may sur-

prise you: If your cost per trans-

action is low enough and your

quality high enough, you should

be thinking of selling that func-

tion as a new business in itself

I

Better thanit needsto be

Sufficient

Q Not goodenough

Source to reduce cost; sacrificecapability if necessary

Source to reduce cost

Source toincreasecapability atlower cost

Abovemedian

Considercreatinga newbusiness(if adjacentto corebusiness)

Source to increasecapability even at highercost if necessary

At industrymedian

Cost per transaction

Below industrymedian

138 HARVARD BUSINESS REVIEW

strategic Sourcing: From Periphery to the Core • BEST PRACTICE

mine commonality, they had to lookoutside their company - even outsidetheir industry. They tried to identifycapabilities in which outside supplierswere building scale across their indus-try, or across several industries, becausethese common business processes or ca-pabilities could pose an immediate orfuture threat to 7-Eleven's cost position.

By plotting each of your required ca-pabilities on a 5Owra>3̂ opportt(n/f/e5;Tjnplike the one in the exhibit "What ShouldYou Outsource?" you can judge the rela-tive merits of your company's outsourc-ing possibilities. The vertical axis of themap measures how proprietary a pro-cess or function is; the horizontal di-mension assesses the degree of com-monality, both within and outside yourindustry. Capabilities that fall in theupper right portion of the map arestrong candidates for outsourcing. Thosethat appear in the lower left section arepotential prospects for captive sourcing.Such capabilities may even be candi-dates for"insourcing"-that is, if you de-termine that your company is really thebest at a given function, you may havean opportunity to perform this functionfor other companies. One example ofsuccessful insourcing is FedEx, whichplans and manages inbound transpor-tation for more than 1,500 product sup-pliers into 26 General Motors powertrain facilities.Thiscapability puts FedExat the leading edge of the $225 billionlogistics-outsourcing industry.

Opportunities that fall in the middleof the sourcing opportunities map gen-erally require more detailed analysis ofboth your company and your industry.You will need to consider such factors asregulation, standards, and alternativeproducts to figure out what will happento those capabilities in the future. Toprovide a quick sense of the relative fi-nancial stakes involved, and highlightthe biggest opportunities, the sourcingopportunities map should be populatedwith bubbles scaled to represent the costdollars at stake for each capability.

Once you've discovered which capa-bilities promise high potential for alter-native sourcing, the next question is:How should you source them? You need

to figure out how your capabilities stackup to what's required. Do you meet,exceed, or fall short of cost and qualityrequirements? A capability assessmentmap like the one in the exhibit "HowStrong Are Your Capabilities?" plotseach capability according to its cost andquality relative to top-performing com-petitors or suppliers. This map will helpyou determine which key capabilitygaps your company needs to fill. Per-haps equally important, it will identifyany current activities that you couldperform with less rigor without incur-ring any strategic penal^.

7-Eleven had alwaysbeen a verticallyintegrated company,delivering its owngasoline, making itsown candy and ice.It even owned thecows that producedthe milk it sold.

Where capabilities fall on this gridestablishes appropriate goals for an out-sourcing relationship. Functions thatfall, for instance, in the upper left (rela-tively high-cost functions whose qualitylevels exceed requirements) should beoutsourced to low-cost providers-evenif it means a reduction in quality. Capa-bilities that fall in the lower left (high-cost functions performed relativelypoorly) require outsourcing partnersthat can both reduce costs and improvequality. The capability assessment mapalso gives you another way to identifyinsourcing opportunities. Capabilitiesthat fall in the upper right (low-cost,high-quality functions) could becomethe basis for attractive new businesses.

Following the first two steps of ourframework can help you determinewhat type of control you need over eachof your capabilities. The third step is akind of reality check in which you de-

termine whether a capability that is astrong candidate for strategic sourcingcan be carried out at a distance withoutany loss of quality.

The issue of physical proximity maynot seem very strategic, but globaliza-tion and advances in technology ensurethat it's a constantly moving target. Formany functions, including transactionprocessing, design, engineering, and cus-tomer service, the Internet and an in-creasingly sophisticated telephone infra-structure have made physical proximitymuch less relevant, at least from a costperspective. The necessary infonnationand outputs can be transferred elec-tronically at high speed and low cost.For tangible products that must beshipped, however, proximity plays alarge role in both cost and timelinessconsiderations; it may not be feasible tomanage the movement of such prod-ucts from afar. There may also be cus-tomer service constraints. Certain prod-uct development, sales, and servicetasks, for example, may require local in-teractions. Capabilities that do not re-quire physical proximity are good can-didates for offshoring, whether througha traditional outsourcing arrangementor, for proprietary capabilities, througha captive operation.

If you go through this three-stepanalysis, your company should have theoutline of a comprehensive capabilitysourcing strategy. You will know whichcapabilities you need to own and pro-tect, which can be best performed bywhat kind of partners, and how to struc-ture a productive relationship. Formu-lating the strategy is, of course, only thefirst stage of a sourcing effort: Partnersthen have to be chosen, contracts nego-tiated, and management structures es-tablished and monitored. As 7-Elevenfound, the success of the strategy oftenhingeson the creativity with which part-nerships are organized and managed.But only by first taking a broad, strate-gic view of capability sourcing can yourcompany make the most of its sourcingchoices. ^

Reprint R0502J; HBR OnPoint 8878To order, see page 151.

FEBRUARY 2005 139

Harvard Business Review Notice of Use Restrictions, May 2009

Harvard Business Review and Harvard Business Publishing Newsletter content on EBSCOhost is licensed for

the private individual use of authorized EBSCOhost users. It is not intended for use as assigned course material

in academic institutions nor as corporate learning or training materials in businesses. Academic licensees may

not use this content in electronic reserves, electronic course packs, persistent linking from syllabi or by any

other means of incorporating the content into course resources. Business licensees may not host this content on

learning management systems or use persistent linking or other means to incorporate the content into learning

management systems. Harvard Business Publishing will be pleased to grant permission to make this content

available through such means. For rates and permission, contact [email protected].