strategist how regulation will reshape fx ... - deutsche bank · consequences for market structure...

TRANSCRIPT

Deutsche Bank Markets Research

Global

Special Report

Cross-Discipline

Date 24 July 2014

How Regulation Will Reshape FX and Rates Markets: Part 3

________________________________________________________________________________________________________________

Deutsche Bank AG/London

DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MCI (P) 148/04/2014.

Alexander Duering, CFA

Strategist

(+44) 20 754-55568

Oliver Harvey

Macro strategist

(+44) 20 754-51947

The process of reforming OTC derivative markets has moved on from rule-

making to implementation, allowing clients better understanding of the

consequences for market structure and their economic impact.

An understanding of the economics of central clearing is vital for client

decision making. Clearing houses provide benefits such as cross-party netting

and counterparty credit risk absorption, but require insurance against member

default in the form of margin, contributions to the default fund and bidding

obligations in post-default auctions. This is passed on to clients in the form of

indirect and direct costs.

On a macro level, collateral and capital requirements will be key determinants

of cost evolution. Collateral demand will itself be contingent on clearing

industry consolidation, extra-territorial rules and market behaviour. We

estimate peak collateral demand to be in the region of USD 700bn, lower than

some other estimates. Basel III capital and leverage ratio rules will drive the

costs of clearing services. We anticipate that the leverage ratio could be of

relatively greater importance in driving costs.

On a micro level, transaction costs will be path dependent. Our analysis

suggests that central clearing will raise costs for clients who currently trade

using PB in rates and FX. In FX, it may also raises costs for clients trading

uncollateralized in some circumstances. For those clients that are able to

choose between central clearing and bilateral trading, the trade-off between

liquidity risks and higher transaction costs will be crucial.

A key theme for the market will be the fragmentation of liquidity between the

cleared and non-cleared worlds. Variation margin requirements may leave real

money clients an uncomfortable choice between changing asset allocations or

suffering weighty capital charges. The approach of regulators to cross-border

recognition of clearing regimes raises the prospects of geographical

fragmentation. In any case, central clearing will necessarily only apply to the

more liquid financial instruments. Counterparties holding economically

equivalent bilaterally-settled and centrally cleared contracts may find them non-

fungible.

Following the introduction of mandatory electronic execution requirements in

the US, there has already been a substantial migration of USD denominated

swap liquidity to SEF. However, there is as yet little evidence the same is true

for other currencies. It remains to be seen whether liquidity will fragment

between different jurisdictions, or whether SEF liquidity pools become

sufficiently deep to attract voluntary participation.

One consequence of new regulations could be greater product standardization,

although so far there appears to be limited take-up of products like swap

futures. Ultimately standardization will depend on the trade off clients make

between transaction costs and basis risks. Client-dealer relationships will also

change as dealers adapt to the end of traditional business models based on

warehousing risk. There are reasons to believe that barriers to entry to the

dealer market may fall as balance sheet size and trading relationships become

of less importance. Regulations also may influence the underlying dynamics of

markets. For example, greater adoption of listed options could see gamma

concentrate at discrete points.

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Page 2 Deutsche Bank AG/London

Introduction

At the G20 summit in September 2009 global leaders set in motion the process for reforming global financial markets in the wake of the crisis of the previous year. Agreement was reached that all standardized OTC derivatives would be cleared through central counterparties where appropriate, executed on exchanges or electronic trading platforms and that all OTC transactions would be reported to central repositories.

Since then, US and EU regulators have been among the most active in finalizing their regulatory framework. Central clearing obligations and mandatory reporting requirements are in effect in both jurisdictions, and electronic execution requirements came into force in the US as of earlier this year.

The market’s understanding of the new regulations has moved on since we last published a study on the impact of these changes.1 From questions over the nature and implementation of the new rules, attention has shifted to their impact on trading costs, financial stability and market structure.

A core topic of this report is the choice of clearing mechanisms. The clearing of a trade is the settlement of all claims arising from the initial agreement on the trade. For spot-settled securities transactions or spot FX trades, this process usually takes the form of a delivery-versus-payment (DvP) transaction handled by a depositary institution. For derivatives or forward transactions, multiple pay legs and in the interest rate swap (IRS) world risk management of trades that can span decades make the process more complex. Consequently, multiple clearing models exist for long-dated transactions.

In a simple world where banks pose negligible credit risk to their non-bank counterparties, credit risk is one-sided on the client and handled by the bank via credit lines like any other loan exposure. This approach is known as bilateral trading. In the real world, banks are not risk-free counterparties and the ability to extend credit lines is rationed. Clearing structures that handle credit risk more symmetrically and minimise counterparty risk work by pooling exposures in central counterparties. This is central clearing. Historically, central clearing is older than bank credit risk concerns, just as derivatives trading preceded the modern banking system. Modern-day regulators have for a number of reasons decided to increase the incentives to use central clearing and in some cases make central clearing mandatory.

Some derivatives users have a degree of flexibility in their choice of clearing arrangements. This guide examines the trading cost impact of this choice. However, another aspect with no directly quantifiable cost is the split of liquidity between the cleared and non-cleared markets. The centrally cleared derivatives market is more liquid not only because by construction only the more liquid contracts are mandated for central clearing, but because centrally cleared derivatives can be assigned and novated without meaningful changes to their counterparty risk profile. Bilaterally settled and non-margined contracts, in contrast, are highly specific and less easily assignable. Entities that use both cleared and non-cleared contracts therefore may hold exposures that are economically offsetting but not fungible due to different clearing arrangements. This creates a strong incentive for derivatives users to move to central clearing even when regulation would nominally leave them a choice whether to take that step or not.

1 Exchange Rate Perspectives, How Regulations Will Reshape FX Markets, Part 2, July 2012

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Deutsche Bank AG/London Page 3

Collateral considerations will be a key concern for those clients that are able to choose between clearing and bilateral execution. The posting of variation margin creates liquidity risk for clients. This is particularly true for real money investors that require or prefer funds to be fully invested, meaning that access to cash collateral is limited. This effect could be compounded by the fact that these investors often engage in long-dated hedges, meaning that possible future variation margin requirements could be large or hedges need to be restructured occasionally. Clients will turn to dealers to provide collateral transformation services. However, these services could prove expensive as dealers’ ability to provide liquidity will also be constrained by Basel III capital and leverage ratio requirements.

The liquidity aspect to the use of central clearing only exists for users of standard derivatives contracts as non-standard contracts are ineligible for central clearing in any case (note, however, that bilateral margining can have a similar effects). Users of highly structured derivatives only have liquidity in the non-cleared market in any case. However, the increasing regulatory costs of bilateral derivatives provide a strong incentive to turn to more standard contracts that are eligible for clearing as discussed in the section ‘Hedge Effectiveness and Basis Risks’ below.

Clearing organizations (CCPs) are best understood as utilities that provide economic benefits such as cross party netting and absorbing default risks from other counterparties. Indeed, a key catalyst for the move to central clearing was the Lehman Brothers default in which the bank’s centrally cleared trades were quickly wound-up, while its bilateral transactions were seen as contributing meaningfully to wider risk contagion.2

However, clearing is not a risk free proposition and clearing organizations require insurance against counterparty default. This comes in the form of initial and variation margin, clearing members’ contributions to the default fund and auctions in which clearing members may bid to take on the defaulting member’s positions. In the event of default, clearing members face contingent liabilities which require capital to be set aside and thus absorb balance sheet. Moreover, the Basel III leverage ratio will require clearing agents to set aside equity against exposures to clients and CCPs. It will also rub against dealers’ provision of liquidity transformation services to clients. We anticipate that the leverage ratio will have a greater cost impact on clearing businesses than capital requirements, albeit this has to be set against its even greater impact on bilateral trades which do not benefit from the netting benefit of cleared trades.

For clients, mandatory clearing obligations will in general increase margin requirements and transaction costs. For both FX and interest rate products we find that central clearing will be more expensive for leveraged and real money clients than depositing portfolios with prime brokers, for example.

However, the migration of transaction costs is best understood as a path dependent process which is highly contingent on client and market-specific variables. For example, higher rated entities may find that the cost of clearing is relatively higher than choosing to trade bilaterally via a credit support annex (CSA) or credit value adjustment arrangement (CVA), while lower rated entities may find the reverse. This is because new regulations impact bilateral trading relationships through extra capital charges like the Basel III CVA-add on charge and higher risk weightings for uncollateralized trades. Nor will clients trading bilaterally be fully insulated from the economics of central clearing. A dealer

2 See, for example, Reserve Bank of Australia, Financial Stability Review, March 2009

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Page 4 Deutsche Bank AG/London

will typically hedge any bilateral trade which will itself be subject to mandatory clearing. Dealers are likely to pass on the costs of this hedge via the pricing of bilateral trades.

Mandatory electronic execution requirements are changing market liquidity. A significant proportion of USD denominated IRS volumes has already migrated to electronic platforms. However, this is not the case for other currencies, potentially opening up a bifurcated market between the US and Europe. New regulations may influence market liquidity in other ways. For example, a greater use of listed options could mean that gamma becomes concentrated at particular points, influencing the underlying market.

New regulations have fundamental implications for hedging decisions and client-dealer relationships. Corporate clients will have to weigh the higher transaction costs arising from bilaterally traded, bespoke hedges, against the basis risk arising from more standardised contracts. For their part, dealers will find that electronic execution and product standardisation pose risks to existing business models. How far banks are able to adapt to this world will depend on their ability to create comparative advantage as gatekeepers to new liquidity pools. New regulations may also lower the barriers to entry for new participants in the dealer market.

Our paper is organized as follows. First, we assess the economics of clearing through a CCP and how collateral demand and cross-border regulations will influence the development of central clearing globally, and the costs of clearing. We then examine from a bottom-up perspective the cost of central clearing for clients as against other forms of trading arrangements, and discuss the impact of new regulations on bilaterally executed trades. Next we look at how US electronic execution requirements are influencing market liquidity. In the last two sections, we discuss the potential implications of new regulations for market structure, such as the impact on hedging efficacy and sales relationships. In this paper, we concentrate on the impact of OTC regulations on IRS and FX markets. However, we also touch on some of the main issues concerning CDS markets on page 21.

Figure 1: We are well travelled down the regulatory road

Source: Deutsche Bank

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Deutsche Bank AG/London Page 5

Central Clearing Mechanics

Agent and principal clearing models

Two different models exist for the relationship between clearing agents, the CCP and the end customer.

In the agent model (used in the US), the customer has a direct relationship with the CCP and books trades directly against the CCP. The role of the clearing agent is to handle the mechanics of margin transfers and (potentially) collateral transformation. The disadvantage of this model is higher operational complexity for customer and CCP. The advantage is that it is comparatively easy to change clearing agents for existing trade portfolios. Existing prime brokers will also generally find it easy to integrate the new clearing business into prime brokerage. For a bank acting as clearing agent, capital charges and leverage ratio concerns are also relatively light, with the exception of collateral transformation services.

In the principal clearing model, used extensively in Europe, the client does not face the CCP directly, instead the clearing agent is legal counterparty of the cleared trades for the customer. The clearing agent has identical back-to-back trades against CCP and customer, potentially with differing margining. The advantage of the principal model is that under certain account types, the clearing agent may be able to net trades against the CCP across customers, posting less margin to the CCP.

However, while back-to-back trades of the agent have no market risk, they carry credit risk because they are against different counterparties. OTC exposures to clearing houses carry a preferential risk weighting of 2%. However, there is currently no preferential treatment for exposures under the calculation of the leverage ratio. Banks may therefore have to set aside significant additional equity to meet leverage ratio requirements under a principal based model.

Regulatory treatment of the clearing business is therefore not free from aspects of competition policy. Even uniform global rules on capital and leverage treatment of certain clearing services have a differential impact on trading costs different jurisdictions.

Figure 2: Agent and principal clearing models

CCP

Customer

ClearingAgent

Traderelationship

Collateral

MarginCCP

Customer

ClearingAgent

Collateral

Margin

Trade

Tradeback-to-back

Source: Deutsche Bank

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Page 6 Deutsche Bank AG/London

Risk management by central counterparties

Central counterparties provide two kinds of economic benefits. The first is that they enable netting of all trades of a single entity across all ultimate counterparties. This effect is more significant for dealers who tend to have balanced books of offsetting trades. End clients on the other hand tend to use derivatives to offset business-specific risks and therefore have more one-sided exposures that offer less scope for netting benefits. Unsurprisingly, therefore, CCPs have historically been set up by dealer communities. The economic cost of the netting benefit is very low because it amounts to essentially operational issues.

The second benefit of central clearing is that the central counterparty absorbs the default risk of individual clearing members. Aside from the immediate risk of a failure to post variation margin (which would affect the ability of the CCP to post margin to the holders of the opposite position), CCPs also require mechanisms to deal with the residual risk left after a member default. While the loss mitigation aspect of central clearing is the most interesting for financial stability, it is useful to look in more detail at what it means in practice.

It should be clear that central clearing brings no benefits in strongly one-sided market where either a single counterparty or a group of similar companies is dominating one side of the trades cleared. In such situations, netting benefits are limited and credit risk is also essentially unchanged versus bilateral clearing.

CCPs are essentially utilities with a strong focus on operational efficiency. As such, there is usually little economic incentive to tie up capital in these entities. Instead, the loss absorption is implemented via a chain of loss buffers in which CCP equity is the last component. The figure below shows this structure. In particular, it should be noted that a substantial part of the risk buffers of a central counterparty actually take the form of contingent liabilities of the clearing members.

Because an insufficiently capitalised CCP would be dysfunctional, CCP capital is indeed the last resource to be affected by counterparty losses. Ahead of CCP capital, the resources generally available to absorb losses are margin posted by the defaulting member, pre-paid default funds, and additional default fund

Figure 3: Structure of risk-absorption of a central counterpary

CCPequity

Defa

ult

fu

nd

Bid

din

g o

blig

atio

n

MarginClearingmembers

Source: Deutsche Bank

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Deutsche Bank AG/London Page 7

contributions by other clearing members. The specific sizes and precedence of these resources are specific to each CCP.

The Basel Committee has, jointly with IOSCO, set out some basic principles for the operation of CCPs in the form of ‘Principles of Financial Market Infrastructures’ (PFMI)3. As a minimum, they require that a CCP can withstand the default of its largest member, and that there are clearly defined mechanisms to handle member defaults. In this context, it should be noted that CCPs generally face wrong-way risk on member defaults in the sense that they are left with a net risk position that will move against the CCP as a result of the member default.

Until a CCP member defaults, the CCP has a perfectly balanced position in every contract cleared on that CCP. At the moment of default, this balance disappears because the defaulting member (member L in the chart above) will no longer be able to fulfil its obligations. The CCP therefore has an outright position corresponding to the net positions of the defaulting member (the column chart next to L). To return to a balanced position, the CCP must execute offsetting trades that bring its own net position back to zero. In the example of swaps, it has to receive where the defaulted member was paying, and pay where that member was receiving. Depending on the size of the position of that member, the market pricing will move against the CCP given that the trading interest is likely to be fairly transparent (the curve changes are symbolised in the line chart next to L).

In general, the default of a large clearing member will lead to a market dislocation, and resulting market value change in the CCP net position that is large compared to the variation margin obligation of the defaulting member. Clearing houses therefore need to not only be able to seize available margin collateral from defaulting members, but need to have mechanisms in place to ensure a fast close-out of net positions, and to allocate losses to the remaining members. The success of the close-out process depends on the willingness of other market participants to trade with the CCP. Consequently, CCPs conduct auctions of net positions among clearing members with economic incentives that reward aggressive bidding. Losses of the CCP as a result of the default are allocated to the non-defaulting members. The choice of auction mechanism and bidding incentives are essentially a game-theoretical exercise. The

3 BIS Committee on Payment and Settlement Systems, Technical Committee of IOSCO, Principles for

financial market infrastructures, April 2012

Figure 4: CCP counterparty positions following a member default

G

CCP

A

C

B

D

L

K

E

FH

I

J

Source: Deutsche Bank

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Page 8 Deutsche Bank AG/London

management of a CCP must predict the behaviour of the non-defaulting clearing members in a variety of crisis scenarios and design incentives in such a way as to obtain the desired response.

This means that the economic cost of risk absorption by the CCP is in fact a shared contingent liability of the clearing members. From a regulatory point of view, this means that clearing members need to have capital reserves to cover potential claims from this contingent liability. Calibrating the required reserve level is complicated. If the reserve requirement against CCP obligations is set too high, it becomes more economical to clear bilaterally where such a choice exists for market participants, thwarting the G20 objective of encouraging central clearing. If the requirement is set too low, clearing members might be insufficiently prepared for default events. At the same time, the interests of CCP operators are not necessarily aligned with those of clearing members. In particular, higher capitalisation of the CCP and lower priority of CCP capital in the loss absorption waterfall would, for equal risk, reduce the capital required on part of the clearing members.

The Basel rules for CCP capital requirements are still in flux as the BCBS is proposing to move from a simple current exposure-based method (CEM). The two options under consideration are based on the actual level of CCP risk-absorption resources (including pre-paid default funds) versus the potentially required amount of resources.4

We note that comprehensive capital requirements for CCP members are difficult to estimate because the risk faced by a clearing member is not just limited to the obligation to replenish a default fund. Aside from that obligation, clearing members may also end up holding the erstwhile risk positions of the defaulted member which will then require capital reserves against market risk. Contingent market risk is not a concern under the Basel II/III framework but does of course affect the economic analysis of the clearing business for the institutions concerned.

Because CCP membership entails capital requirements, clearing is not a pure agency business. The clearing member acting as agent for non-member users of the CCP accepts contingent liabilities under the default mechanism that are linked to the amount of agency business conducted. Clearing therefore consumes balance sheet of the clearing agent.

Clearing also affects the leverage ratio of the clearing agent via exposures to clients and CCPs. Capital requirements held against cleared derivative exposures are relatively low because of collateralization and the preferential Basel treatment of exposures to clearing houses. However, there is currently no such treatment for cleared derivative exposures under the leverage ratio calculation.

Additionally, because CCPs typically settle variation margin in cash (preferably central bank cash) while clearing clients are not operationally set up to provide cash in the required time scale, clearing banks tend to offer the service of funding variation margin against collateral. Such arrangements enter the leverage ratio calculation. Clearing agents close to a leverage ratio constraint need therefore take into account contingent increases in the balance sheet size as a result of market moves that require financing for clients when estimating the equity capital required to underwrite the clearing agency business.

4 BIS Committee on Payment and Settlement Systems, Technical Committee of IOSCO, Principles for

financial market infrastructures, April 2012

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Deutsche Bank AG/London Page 9

Principle 9 of the PFMI specifies a preference for settlement in central bank money by CCPs (as opposed to commercial bank monies). While this isolates the clearing at CCPs from the credit risk of the banking system, it also creates the risk of liquidity shortfalls at the CCP resulting from settlement failures (technical or default-related) by some of its users. CCPs therefore need to arrange for standby liquidity lines from commercial banks which are separate from the default fund arrangements, or for direct liquidity support from central banks. While some central banks, including the Bank of England, have declared themselves ready in principle to provide such liquidity support, and some CCPs, like Eurex Clearing, are themselves banks with automatic access to their central bank, there are principal reasons why such direct central bank access is undesirable. From the central bank point of view, support of derivatives markets is ancillary to the more fundamental tasks of monetary policy and contingent claims from a CCP could create conflicts of interest. To enforce a last resort nature of direct central bank access, regulators do not include such facilities in the assessment of the liquidity provisions of a CCP.

Collateral demand

Various studies exist that estimate the likely demand for collateral as a result of mandatory clearing. An essential problem with all such studies is that trading itself will be affected by regulatory changes and historical trading and margining patterns are therefore unreliable guides to future margin requirements. It is quite likely that OTC trading activity will be substantially reduced and risk-taking shifted to public exchanges. More regular rolls of positions should reduce potential future exposures and therefore variation margin required, similar to periodic re-couponing/re-striking of trades. An additional factor that will affect collateral demand is ongoing optimisation of clearing strategies and consolidation of clearing houses. While fair value drift of mandatorily cleared derivatives will initially lead to a steep increase of collateral demand, optimisation of CCP usage will counteract that trend over time.

We estimate with a very wide confidence interval that collateral demand could peak around USD 700bn, corresponding to 1/5th of what would be the case if the complete portfolio of currently existing derivatives were to be centrally cleared.5 While this number is lower than estimates based on an essentially unchanged market behaviour, the cost is still substantial. Funding costs of banks and corporates are substantially higher than the overnight rates accruing on posted collateral, and the new Basel III liquidity rules require some degree of term funding. Assuming a funding spread of 50bp on USD 700bn of collateral would translate into an annual cost of USD 3.75bn to the derivatives industry. Unlike Tobin-style taxes on turnover, this cost would be borne against the stock of portfolios but it would have the characteristics of a tax. The benefits accrue to the issuers of high-grade collateral (largely government bonds) and the common good provided in return for the tax is a more stable financial market.

Collateral demand is also likely to vary considerably across client type, however. While some clients will find eligible collateral relatively easy to source, others will require liquidity transformation services from banks. We anticipate that certain kinds of real money clients, such as pension funds, may find it particularly difficult to source and post variation margin. We explore this issue in more detail in the section ‘The cost of clearing for clients.’

5 See Fixed Income Special Report: Central Clearing, 6th February 2012

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Page 10 Deutsche Bank AG/London

Jurisdictional issues

Given the non-zero correlation of asset prices across markets, the economically optimal number of central counterparties globally is one. Using a single CCP for all trades creates the maximal benefit of netting. Put differently, adding one more CCP to an existing set makes it possible that two trades that were partially netted on a single CCP are split across two CCPs and have no netting. This increases the amount of required collateral.

The idea of a single global CCP for all trades is of course unrealistic. Any such CCP would necessarily be subject to the supervision of one country, or small group of countries. Inevitable conflicts of interest would arise between the country or countries acting as supervisors and other countries whose financial markets would depend on the functioning of this CCP. It is therefore more likely that regulators will insist on on-shoring systemically important CCPs. Additionally, regulators are reluctant to pick winners in the transition to central clearing and will encourage the parallel existence of CCPs clearing the same trades in the same jurisdiction.

As a result, the consolidation process in the CCP industry will take some time and collateral usage across the financial system will be sub-optimal. For large users of derivatives, deliberate trade allocation across multiple CCPs can reduce collateral demand under some circumstances, but for smaller users, particularly with one-sided exposures, the scope for doing so is limited. Reduction of collateral use by these derivatives users instead depends on CCP consolidation which will take several years.

The EU is fairly open in its approach and the implementing Regulatory Standard for EMIR allows appropriately regulated third-country CCPs to operate in the EU.6 This is in line with the EU’s goal of preserving business opportunities for EU-based CCPs outside the EU by way of reciprocity in the recognition of regulatory oversight. EMIR therefore requires that a third-country CCP shows that it is adequately supervised rather than that it directly satisfies EU standards. While this approach suggests a high degree of cross-border clearing, at the time of writing, three cases related to oversight of CCPs are pending before the European Court of Justice where the United Kingdom objects to clearing infrastructure opinions of the ECB. 7

In the US, foreign clearers can obtain Designated Clearing Organisation status subject to registration at the CFTC. However, CFTC registration requires a full assessment by the CFTC, not merely proof of adequate home country supervision. This sets a higher standard because a foreign CCP has to satisfy both home and US supervisory standards to operate in the US.

The more exacting US standards raise a problem for the cross-border recognition of US and European CCPs by their respective authorities. This is because article 25 of EMIR states that cross-border recognition will only apply where non-EU regulatory regimes have an equivalent regime of foreign CCP recognition. The CFTC is currently working on rules that would allow non-US CPPs to clear US persons without full compliance with US supervisory standards. However, if US rules were not deemed equivalent by the European Commission, this would raise the prospect of European banks being unable to act as clearing agents to US CCPs. As well as hindering clearing house consolidation, such an outcome could result in a fragmentation of liquidity across European and US markets.

6 (Delegated Regulation 153/2013)

7 (T-496/11, T-45/12, T-93/13)

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Deutsche Bank AG/London Page 11

Cost of centrally cleared derivatives

FX, rates and central clearing

The Dodd-Frank Act mandates the clearing of all swaps via CCPs, with an exemption for ‘end users’ who use swap contracts for commercial hedging purposes. The European Market Infrastructure Regulation (EMIR) also mandates clearing derivatives for all financial counterparties and certain non-financial counterparties, with a temporary exemption for pension funds.

Central clearing is not a new concept for FX or rates markets. The BIS estimates that 57% of FRAs and 35% of all swaps are cleared, although this is significantly lower for FX products.8 However, central clearing has so far been primarily dealer to dealer. Buy-side participants will therefore be approaching questions of the costs and risks of central clearing for the first time.

Not all rate and FX products will be mandated to clear. The US Treasury has granted an exemption for FX forwards and swaps to be treated as ‘swaps’, recognizing their different risk profile from other OTC instruments. In Europe, ESMA is currently seeking guidance from the European Commission over the definition of currency derivatives. We anticipate that ultimately ESMA will exempt forwards and swaps from mandatory clearing.

The CFTC has already provided final clearing determinations for certain IRS and CDS contracts, meaning these products are mandated to clear. It has yet to do so for FX products. We expect the CFTC to mandate some NDF contracts

8 BIS, The OTC interest rate derivatives market in 2013. By contrast, only 10% of NDF contracts are

currently centrally cleared.

Figure 5:To clear or not to clear?

Source: Deutsche Bank

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Page 12 Deutsche Bank AG/London

shortly. Clearing houses are already offering clearing services for NDFs in several tenors and currency pairs.

Clearing of FX options have proved more complex. BCBS and IOSCO principals require that clearing houses should guarantee full and final settlement of FX options. Because the FX market relies on full settlement of fixed notional amounts, clearing houses would face very high liquidity demands if major clearing members were to default. In a recent study, the GFMA estimated that the same day liquidity shortfall resulting from the failure of two clearing members representing the largest settlement obligation could be as high as USD 161bn on a gross basis and USD 44bn on a net basis, if mandatory clearing was extended to both dealers and clients.9 The FX industry is working with CCPs and regulators to mitigate the replacement risks associated with the clearing of FX options. The clearing of FX options will also imply the clearing of those FX forwards and swaps part of delta-hedges to prevent bifurcated pricing.

Some of the more structured and/or less liquid OTC derivatives will likely not be subjected to clearing. We outline which products are, will be and likely will not be subject to mandatory clearing in the matrix above.

Not all counterparties will clear derivatives. US and European authorities have distinguished derivatives used for commercial hedging purposes from those used by financial institutions. Most non-financial institutions will not be mandated to clear derivative products.

In addition, ESMA has provided pension funds with an exemption from clearing until August 2015. This exemption is extendable potentially until 2018 depending on a number of factors, such as progress made on clearing houses accepting non-cash collateral for variation margin. This followed concerns over fund performance if fully invested funds were required to use collateral generation services to meet variation margin requirements.

The cost of clearing for clients

The cost of central clearing for end users of derivatives is not straightforward. In general, transaction costs and margin requirements will rise. However, this is best seen as a path dependent process, contingent on both client-specific and market-specific variables.

Trading models Financial institutions will have to clear mandated interest rate and FX products via CCPs. Certain clients, for example pension funds, may in the short term at least, elect to trade products bilaterally via a CSA. Corporate clients will choose between trading bilaterally (typically without a CSA) and clearing with a CCP.

Central clearing involves the posting of initial and variation margin by both counterparties to a clearing house. The clearing house sets thresholds above which initial margin needs to be maintained based on the expected volatility of future returns. The direct cost of clearing is therefore the cost of funding the initial and variation margin. In general, for all but the largest clients, banks will sit between individual counterparties to a trade and the clearing house. This might be on a use style FCM (agent) model or European style matched principal (principal) model. Clients also pay additional charges for clearing services, generally a percentage of IM and a ticket fee. Where trades are also subject to mandatory electronic execution requirements, SEF fees may also apply.

9 GFMA, Briefing Note, OTC FX Options Analysis Results, November 18th 2013

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Deutsche Bank AG/London Page 13

Cost evolution for clients Building on previous analysis, we have built sample rates and FX portfolios to examine how transaction costs will evolve for clients under the new regulatory regime.10 We have also analyzed the composition of transaction costs for clients to better understand how these change under different trading arrangements.

For rates, uncollateralized trading is the least economically attractive option. CVA credit charges and the extra capital charges incurred by dealers because of higher risk weightings under Basel III make uncollateralized trades more expensive than CSA, PB or central clearing.

By bilaterally margining trades with their counterparties, A-rated entities reduce transaction costs by 64%, and BBB-rated entities by 68% relative to trading via CVA. The larger savings for lower rated entities reflects the importance of counterparty’s credit risk in the CVA calculation.

For clients that PB their portfolio, costs fall further still (96% for an A rated entity and 97% for a BBB rated entity). This is due to the extra netting benefit provided by PB relative to splitting the portfolio into individual bilateral accounts.

10 See Exchange Rate Perspectives, How Regulation Will Reshape FX Markets, Part II

Figure 6: Cost composition and migration for a ‘typical’ interest rate portfolio*

A rated BBB rated A rated BBB rated A rated BBB rated

Uncollateralized CVA Credit Charge 43% 45%

Capital Costs 57% 55%

Bilateral CSA Cost of Margin 20% 14%

Capital costs 80% 86%

PB Cost of Margin 44%

PB Fees 21%

Maintence Fee 35%

PB + Clearing Cost of Margin 45%

PB Fees 36%

Clearing Fees 12%

SEF Fees 6%

PORTFOLIO SUMMARY ASSUMPTIONS

Gross notional(mn) # Trades 1) Standardized FIPB Booking fee structure applied in calculation of PB booking and maintainence fee

Share of clearing volume 0 1155 2) Standardized LCH - CCP margin methodology and fee structure applied in calculation of margin and fee

Swaptions 831,577 23 3) Standard internal funding costs taken to be the same across all trading relationships

4) SEF fee applies to only those trades which are mandated to be cleared

Clearing Mandatory 5,616 186 5) Portfolio is a weighted sample of trades from FIPB and clearing books

Clearing Eligible but non Mandatory 90,118 969 6) Variation margin is not used in the analysis

Clearing Ineligible (PB Only) 831,577 23 7) PB and Clearing fees have been duration weighted

8) CVA spread/mark-up required by banks is calculated as:

# RoC = 25%, ## Capital Ratio = 10%

Cost Composition Cost Migration

No CSA Bilateral CSA PB

-64% -68%

Previous model

-96% -97%

-91% -94%

-88% -92%

-75% -82% 111%

Previous model

Previous model

Return on Capital = # (Mark-up + At Risk Table – CVA) * Variable costs

max (RWA* Capital Ratio, CRD4 Balance Sheet * Leverage Ratio)##

Source: Deutsche Bank, *Note: this cost analysis is for illustrative purposes only and dependent on a number of regulatory, market and client specific variables. Actual pricing may differ

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Page 14 Deutsche Bank AG/London

Centrally clearing eligible products is less expensive than uncollateralized trading, but more expensive than PB for A and BBB-rated counterparties and more expensive than bilaterally margining the trades for A-rated counterparties. Some of the cross-netting benefit for trades is lost as there is no cross margining between non-cleared and cleared trades.

By contrast in the FX portfolio, we find that uncollateralized trading is a more economically attractive option for an A rated entity than CSA, PB or central clearing. While the Basel III CVA add-on is intended to discourage uncollateralized trading arrangements, the predominantly short dated nature of the instruments in the FX portfolio mean that credit charges are lower than margin funding costs and other associated fees.

It is important to note that this is not the case for the BBB rated entity, which sees costs fall by -8% and -25% respectively for CSA and PB, although rise by 6% when clearing eligible trades.

Similar to rates, clients that choose to move from CSA to PB see savings of -8% and -18% respectively for A and BBB-rated entities. Clearing eligible trades is the most expensive option for clients. Fees make up a substantial proportion of total costs (PB and clearing fees make up over 40% of total).

This analysis illustrates how cost outcomes are closely related to client-specific variables. These numbers do not take account of costs of back-to-back trades made by dealers on uncollateralized trades, which will typically be cleared. This cost will be passed onto clients in the form of a funding value adjustment (FVA), discussed in more detail below. Ultimately, this could mean that both uncollateralized and CSA trading becomes less economically attractive. We have also excluded variation margin from our calculations. For many clients, however, variation margin requirements will be of key concern. We discuss this in more detail in the section below.

Figure 7: Cost composition and migration for a ‘typical’ FX portfolio*

A rated BBB rated A rated BBB rated A rated BBB rated

Uncollateralized CVA Credit Charge 38% 38%

Capital Costs 62% 63%

Bilateral CSA Cost of Margin 75% 66% 24% -8%

Capital Costs 25% 34%

PB Cost of Margin 74%

PB Fees 26%

PB + Clearing Cost of Margin 58%

PB Fees 19% 43% 6% 15% 2%

Clearing Fees 12%

Maintenence Fee 11%

PORTFOLIO SUMMARY ASSUMPTIONS

Gross Notional (mn) # Trades 1) LCH margin simulator for house margin, standard multiplier SQRT (7/5) converts to client margin

FORWARD 1,076 256 2) Standard internal funding costs taken to be the same across all trading relationships

NON DELIVERABLE FORWARD 155 34 3) No SEF fees, no charge for RFQ as per Reuters termsheet

SPOT 409 486 4) FXPB and Clearing Fees duration weighted

5) Varion margin is not used in the analysis

Share of clearing volume 10% 6) PB and clearing fees duration weighted

7) CVA spread/mark-up required by banks is calculated as:

# RoC = 25%, ##Capital Ratio = 10%

Cost Composition

Previous model

Previous model

Cost Migration

14%

No CSA Bilateral CSA PB

Previous model

25%

-25% -8% -18%

Return on Capital = #(Mark-up + At Risk Table – CVA) * Variable costs

(Basel II RWA + Basel III RWA)* Tier 1 Capital Target ##

Source: Deutsche Bank, *Note: this cost analysis is for illustrative purposes only and dependent on a number of regulatory, market and client specific variables. Actual pricing may differ

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Deutsche Bank AG/London Page 15

Collateral considerations

The posting of initial and variation margin presents its own costs and risks. Some entities may not have ready access to high quality non-cash or cash collateral with which to post as initial or variation margin. This will mean that collateral transformation services are required.

Collateral transformation involves the upgrading of collateral to meet CCP-eligible margin. As clearing houses are unable to transform collateral, clearing brokers will typically fund clients’ cash margin requirements in exchange for lower quality collateral such as corporate bonds where a haircut is applied. Clearing brokers source the cash themselves through the repo market.

Basel treatment of derivatives However, this may prove expensive for clients. In the first place, Basel III requires banks to hold capital against client and CCP exposures (although the latter enjoys a preferential RWA of 2%). Repo financing for collateral transformation will further require capital to be set aside. With banks therefore becoming more conscious of return on equity, some may be reluctant to extend this service.

The Basel III leverage ratio may have an even higher impact on equity costs. As well as the more limited ability for banks to offset exposures using collateral, the ambivalent nature of the leverage ratio to the risk profile of assets will have a proportionately larger impact on clearing banks exposures to clients and CCPs. It will also encourage banks to shed low risk assets like repos, which could impact collateral transformation.

Market fragmentation Questions of collateral sourcing are likely to be particularly acute for certain kinds of clients. In particular, collateral transformation will be costly for clients will near-fully or fully-invested portfolios such as asset managers or pension funds.

Clearing houses accept variation margin in cash only. This is because they are obliged to pass on cash margin to counterparties whose trades are in the money. Clearing houses are not themselves able to transform non-cash collateral. At an aggregate level the requirement for counterparties to post

Figure 8: Cost/liquidity trade off for real money Figure 9: Cost/liquidity trade off for hedge funds

Source: Deutsche Bank Source: Deutsche Bank

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Page 16 Deutsche Bank AG/London

variation margin does not contribute to global collateral demand as the in and out of the moneyness of trades net out. However, they do pose substantial liquidity risks for clients that require the full investment of available assets to ensure liabilities are met and are not generally able to deploy significant leverage.

The effect of variation margin requirements for real money clients can be compounded by the fact that they typically engage in long-dated hedges. This increases potential future exposures and therefore the demand for variation margin.

Variation margin requirements could also be acute in times of market stress. A market dislocation may see haircuts on illegible collateral increased, requiring funds to set aside additional securities from their portfolios, or resort to the more expensive option of unsecured funding. The potential correlation between haircuts on collateral and clients’ positions could compound this effect, as could the decreased willingness of clearing-brokers to provide liquidity to clients.

An alternative is that funds move to bilateral clearing. However, Basel III rules will increase the costs for uncleared trades. This could again disproportionately impact real money clients that transact long-dated trades, as capital costs increase for transactions of a longer duration.

The combined impact of OTC rules and banking regulation therefore raises the prospect of market fragmentation. Real money will choose between liquidity risk under central clearing, or higher hedging costs if trades remain uncollateralized. This is illustrated by the left hand diagram above. As collateral transformation services may add to transaction costs, the shape of the liquidity-cost curve also flattens. It may be that real money investors choose to split portfolios by centrally clearing more actively managed instruments where tighter bid-ask spreads are required, while leaving passive buy-and-hold investments to be traded on a bilateral basis, absorbing extra cost but avoiding major changes in asset allocation.

Leveraged investors are already used to posting variation margin and will see little additional liquidity risk from existing arrangements, although costs will rise due to higher initial margin requirements and the lower netting provided by central clearing (shown by the diagram on the right). Ironically, central clearing requirements may therefore have a greater impact in terms of cost and liquidity risk on less risky clients that are less prone to leverage.

In Europe, ESMA has provided a temporary exemption for pension funds from mandatory clearing requirements, recognizing the particular challenges these counterparties face. In spite of this, there is evidence that some funds may be already migrating to central clearing. One reason may be that firms are taking into accounts risks associated with EMIR frontloading requirements (see below).

Other collateral issues Clients may also find eligible collateral for initial margin hard to come by. Estimates of future collateral demand under mandatory clearing and bilateral margin rules vary considerably. Some estimate that the under-collateralization of the OTC market is between USD 2-3 trillion.11 Our considerably lower estimate is that demand for collateral will peak at around USD 700bn (see section 1). However, this will still have a marked impact on costs for the OTC market.

11 See, for example, IMF Working Paper, The Changing Collateral Space, Singh, January 2013

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Deutsche Bank AG/London Page 17

Risks to collateral availability range from central bank policy (e.g. the willingness of central banks to provide eligible collateral through the wind down of asset purchase programs), the development of CCPs (in particular the availability of cross-netting), the evolution of trading relationships and how far clearing rules are harmonized across borders.

Collateral segregation will play another important role in trading arrangements. In the US, the CFTC have approved one model of collateral segregation model from CCPs - legally segregated operationally comingled (LSOC). This model requires FCMs and DCOs to keep clients’ collateral separate from their own and other clients’ assets.

By contrast, in Europe ESMA requires clearing houses to provide a minimum of two collateral segregation models: individual and omnibus accounts. In individually segregated accounts, the value and type of assets are attached to individual clients, cannot be used to cover losses connected to fellow client positions and excess assets are held by the clearing member not the FCM. In omnibus accounts, the gross margin posted by clients in the same omnibus account is passed on by the FCM to the clearing house on a net basis. Client assets can be used to cover losses connected to fellow clients within the account (although not across accounts) and excess collateral can be held at the clearing member level.

Individual accounts will offer clients greater protection but will be more expensive, as they are operationally more difficult for dealers to implement and prevent them from cross netting margin from different clients. Clients may require the highest level of protection over their assets, however. For example, in the case of pension funds which have defined liabilities to meet, receiving back assets different to those originally pledged could be problematic.

Frontloading EMIR mandates that trades executed between the authorization of a CCP and the start date of the clearing obligation will be retrospectively shifted to central clearing. This raises the possibility that bilateral trades executed after the authorization of the first clearing house on 18th of March this year could be moved to CCPs prior to the expiry of the trade. As bilateral and centrally cleared trades operate under different pricing structures, the efficacy of hedges could be impacted.

On the 8th of May this year, ESMA addressed this issue by suggesting that it would interpret EMIR frontloading requirements to mean that trades executed between the entry into force of the regulatory technical standards (RTS) and the date of the clearing obligation itself would be subject to frontloading. This would give clients greater legal certainty which classes of derivatives will be retrospectively subject to the clearing obligation, when the obligation would take effect and which clearing houses will be available. ESMA also suggested it would introduce a minimum maturity cap which would exclude a large proportion of trades from the requirement.

As yet, however, there is no certainty on whether pension funds will be immune from front-loading requirements when their exemption from central clearing expires in August 2015.

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Page 18 Deutsche Bank AG/London

Figure 10: Sources of clearing costs

Source: Deutsche Bank

Collateral transformation by clearing agents The core task of a clearing agent is to handle the process of daily or intraday margin transfer to and from the clearing house. While it would technically be possible to use a cash account of the client at the agent for that purpose, the normal case is that the client deposits a mix of cash and securities with the agent. The agent then uses repo transactions to transform securities into CCP-eligible cash.

This liquidity transformation consumes balance sheet and liquidity at the agent. The agent therefore needs to have (and fund) equity to underwrite the residual risks, as well as sourcing term liquidity to satisfy regulatory liquidity constraints. Mandatory segregation of client accounts reduces the scope for collateral reuse, or the offsetting of margin flows from the agent’s own trading activities. Capital and liquidity constraints apply independently but at the same time. Whether the liquidity constraint is the binding one on the activities of a clearing agent therefore depends on the capital situation. A well-diversified universal bank with a large loan book may be capital-constrained but find it relatively easy to add zero-risk weighted exposures that increase the (non-binding) liquidity ratio. Conversely, a more dealer-focused institution with a high proportion of zero-risk-weight exposures might instead find itself constrained by liquidity alone.

Leverage ratio impact on clearing agents Clearing banks’ exposures to their clients and CCPs will be included under the Basel III leverage ratio. Under the BCBS leverage ratio framework outlined in January this year, banks must calculate these exposures as the replacement cost of the contract plus an add-on that reflects the potential future exposure (PFE) of the contract. Bilateral netting is permitted across clients but not across accounts subject to netting agreements. Clearing banks may not use IM to net off exposures and variation margin may only be used to net off exposures insofar as it is cash in the currency of the underlying derivative and exchanged daily. It is important to note that there is currently

no preferential treatment of OTC exposures to clearing houses under the leverage ratio calculation, in contrast to the capital requirements. Additionally, the existence of margin cash and repo collateral on the balance sheet of the clearing agent as a result of the clearing banks collateral transformation services will be included in the leverage ratio exposure.

Because of this, the leverage ratio is likely to impose greater equity costs for clearing businesses than capital requirements which provide a preferential risk weight for exposures to CCPs as well as taking into account IM and the risk profile of assets.

Contingent market risk Although regulators do not enforce this, clearing agents will at least internally set aside risk capital against the potential obligation to bid for, and acquire, market risk as result of the failure of another clearing agent. As this capital is caused by the agency business, it is funded from clearing fees.

Cost of infrastructure Establishing clearing infrastructure for FCMs and on-boarding clients is an expensive process that carries fixed costs. Clearing business therefore works to economies of scale insofar as client business is concerned. While costs are not directly passed on to clients, dealers may be reluctant to onboard clients with low turnover.

Client Clearin

g bank CCP

Repo

Market

Capital

charges Leverage ratio

exposure

Default fund capital

Counterparty RWA same

as bilateral exposures,

IM and VM reduces LGD 2% preferential RWA treatment

Principal model

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Deutsche Bank AG/London Page 19

Cost of bilaterally cleared derivatives

Forms of bilateral clearing

While central clearing is highly standardised by construction, bilateral arrangements can in principle take any form. In practice, derivatives users and dealers find it convenient to reduce basis risks between trades with different counterparties by adhering to standard arrangements. These are the ISDA Master agreement and optionally a Credit Support Annex (CSA) to the ISDA Master.

The essential choice in bilateral clearing is whether or not to collateralise credit exposure arising from mark-to-market changes in valuations. This decision usually translates into the use or not of a CSA. A collateralised trade reduces counterparty risk but requires extra operational effort. Regulatory pressure means that uncollateralised bilateral clearing is confined to corporate derivatives users.

CSA agreements CSA agreements involve the posting of initial and variation margin, generally with minimum thresholds set for the posting of variation margin. Variation margin will be transferred regularly depending on the extent to which the threshold is exceeded. Initial margin may be required, depending on the creditworthiness of the counterparty. CSA agreements will therefore pose similar liquidity demands on clients to clearing as well as costs associated with funding the margin.

Regulatory risk charges on bilaterally cleared trades Bilateral clearing without margining eliminates the liquidity risks associated with margin calls as well as pricing and margin management costs. However, uncollateralized trades will be subject to the new CVA charge introduced by Basel III legislation as well as increased risk weights for financial institutions. European lawmakers agreed an exemption for corporates, pension funds and sovereigns from the regulatory CVA add-on. However, there are signs that domestic regulators may seek to compensate for this exemption through an additional capital add-ons. There is no such exemption in the US and the economic cost of carrying uncollateralised bilateral exposure exists independently of the regulatory treatment.

While clients clearing bilaterally will not be subject to the stringent liquidity demands of clearing houses, neither will they be fully insulated from the economics of central clearing. As we note below, a dealer will typically back-to-back any bilateral trade with a hedge which will itself be subject to mandatory clearing. Dealers are likely to pass on the costs of this hedge via the pricing of bilateral trades. For clients trading on a CSA, segregated margin (i.e. restricting dealers’ ability to use bilateral margin for their cleared back-to-back trades) will increase costs.

CVA, FVA and DVA

The benchmark for derivatives trading is the centrally cleared market where customer trades are hedged. Consequently, bilateral trades are priced largely relative to centrally cleared trades, exposing clients who do not use CCPs to the economics of central clearing. A bilaterally cleared trade puts the dealer into a position where the client trade is cleared bilaterally while the hedge is cleared centrally, and the full hedge costs are passed on to the client via the pricing of the bilateral trade.

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Page 20 Deutsche Bank AG/London

The additional costs associated with bilateral clearing can be split into two groups. The first are costs arising from the management of bilateral counterparty risk, the second are costs stemming from the liquidity requirements of central clearing. We refer to these as credit and funding adjustments, respectively, and explain them briefly below.

Credit and funding charges even on plain vanilla trades are themselves complex financial derivatives. Their complexity arises from their dependency on two sets of stochastic processes: the market value of the underlying transaction on one hand, and the cost of funding, collateral, or credit risk of both counterparties on the other. Unlike the underlying derivative, these costs are not zero sum processes; an increase in implied volatility for instance can impose costs on both counterparties.

Credit value adjustment The CVA represents the cost of counterparty risk arising from a derivative contract in the event of a default. It is a function of the expected market value of the counterparty’s derivates portfolio (which would be lost should the counterparty default), the probability of default and the recovery value of default. Calculating the CVA is complex. Inputs into the calculation depend on a number of proprietary variables, including the banks’ required return on capital, its Tier 1 capital target ratio and its proprietary VaR model which calculates the Risk Weighted Assets (RWAs) against which the bank holds capital.

Two crucial parameters of the CVAs are the credit rating of the counterparty, and the duration of the transaction. Clients with less favourable credit rating wishing to execute transactions of longer duration are likely to find costs rise.

Posting collateral under a CSA, including initial margin (also known as independent amount), drastically reduces but does not eliminate credit risk. There is a residual risk that the market value of the derivatives position moves between the detection of a counterparty default and the hedging of the transaction risk including the realisation of the collateral. However, this market risk exists only for a number of days whereas it can span years for the underlying derivative transactions.

Just as under central clearing, so banks’ bilateral exposures will be subject to the Basel III leverage ratio. However, the scope for netting is significantly reduced under bilateral trading, relative to central clearing. In this sense, on a relative basis, the leverage ratio is set to be an even greater driver of transaction costs under bilateral trading than central clearing.

Debit value adjustment Credit costs can be reflexive when pre-default arrangements exist that mitigate credit risk deterioration. A clearing arrangement may for instance call for collateralisation of trades when the credit rating of the counterparty with negative mark-to-market is downgraded below a certain threshold. Such an arrangement is in effect a conditional liability that needs to be valued in the form of a debit value adjustment.

The cost of credit risk management of collateralised trades depends also on the cost of funding future collateral in the bilaterally cleared leg of the transaction. The associated cost is known as the funding value adjustment (FVA).

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Deutsche Bank AG/London Page 21

Funding adjustment The requirement to post margin, usually cash, to a CCP in the process of clearing the hedge leg of a bilaterally cleared trade creates a contingent obligation on the dealer to fund margin in response to market moves. The dealer may be able to do so in the repo market against collateral received on the bilaterally cleared trade unless client asset segregation applies and the appropriate funding benchmark is unsecured. The type of collateral posted will be an important driver of costs. Non-standard bonds will incur greater charges. The cost of liquidity transformation for core government bonds is less clear, however. For example, the fact that under current market conditions some government bonds repo cheaper than overnight unsecured funding rates could make these a relatively more attractive option.

The correct valuation of the cost of funding margin also depends on the margin rules of the CCP. Multi-currency margin at CCPs further complicate the calculation of the fair value of funding charges because the term structure of basis swap spreads between the currency of the derivative and the possible margin currencies can offer switch options that are contingent on the market value of the hedge trade.

An important aspect of the cost of credit risk management is the segregation of client assets in the context of leverage ratio and liquidity requirements. Segregated client collateral consumes balance sheet but cannot be used to post collateral to the CCP on the hedge leg of the trade. The dealer therefore has to reserve and fund balance sheet capacity for the trade collateral.

Figure 11: Central clearing and CDS markets

Source: Deutsche Bank

CDS are an outlier in the context of mandatory central clearing because regulatory attention on the clearing of these contracts predates the financial crisis response of the G20. In the US, the Federal Reserve had faulted the industry for excessive delays in final confirmation of trades which created pressure on dealers to move to a centralised clearing solution. In the EU, CDS referencing European entities moved to central clearing of inter-dealer trades on 31 July 2009 under pressure from the Markets Directorate of the EU Commission. In both the US and the EU, therefore, operational concerns prompted regulatory intervention. The nature of credit risk, which is characterised by infrequent but rapid large changes in valuations, also provides a strong incentive for market participants to have solid mechanisms for the management of counterparty risk.

At the same time, the experience in the CDS market during the crisis provides an important example of the limits of risk reduction by central clearing. When AIG required government support, the main trigger for this intervention was margin calls on CDS contracts. In a hypothetical scenario where all these contracts had been cleared through a CCP, it is unlikely that the CCP would have survived a default of AIG simply because AIG was completely one-sided as a protection seller. In other words, the default events of AIG and the CCP would have been fully correlated and systemic support for AIG or the CCP would have been economically equivalent as far as the CDS market was concerned. In contrast, the authoritative study on collateral demand by the BIS ('Collateral requirements for mandatory central clearing of over-the-counter derivatives', working paper 373) does not account for two-sided risk in dealers arbitraging between the single name and index CDS market (this shortcoming is acknowledged in footnote 16) and therefore over-estimates the amount of margin calls and hence the risk absorption of CCPs under a central clearing scenario.

Central clearing of customer trades is as yet incomplete. ESMA has proposed in July 2014 to mandate central clearing of un-tranched index CDS but would leave tranche CDS and single names cleared on a bilateral basis, reflecting the less standardised nature of such contracts. In the US, clearing of most index CDS has been mandatory since March 2013. Again, the often bespoke nature of single name CDS makes them less suitable for central clearing.

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Page 22 Deutsche Bank AG/London

Trade facilities and reporting

CFTC final rules

The Dodd-Frank Act requires mandated swaps to be executed on a designated contract market (DCM) or swap execution facility (SEF).

In May 2013, the CFTC adopted final rules concerning SEFs. SEF trading became operational in October 2013 and mandatory execution requirements for certain interest rate and credit derivatives came into force on February 15th this year.

The CFTC’s final rules clarified what transactions and which participants would be exempt from mandatory SEF or DCM execution. Non-financial end-users who use trades to mitigate commercial risk may choose not to execute trades on SEFs or DCMs. Swaps that are not mandated to be cleared by the CFTC will not be subject to electronic execution. Finally, swaps that are not Made Available to Trade (MAT) by SEFs will be exempt.

To be MAT, a swap or a category of swap must first be submitted by a SEF or DCM to the CFTC. In determining whether to submit the swap, the SEF or DCM must take into account whether there are sufficiently deep and liquid markets for the product, including whether there are ready and willing buyers and sellers, the frequency or size of transactions, the trading volume and the typical bid-ask spread. The CFTC will subsequently review and choose to confirm or reject the submission.

Once the MAT determination is confirmed by the CFTC, all other DCMs and SEFs that offer that swap for trading must do so in accordance with the trade execution requirement and market participants are obliged to trade that swap on a SEF. There had been concerns that the MAT rule provided SEFs with too much latitude over which products would be traded electronically, particularly as there existed a possible economic incentive from listing as many products as possible. However, so far these fears have proved unfounded.

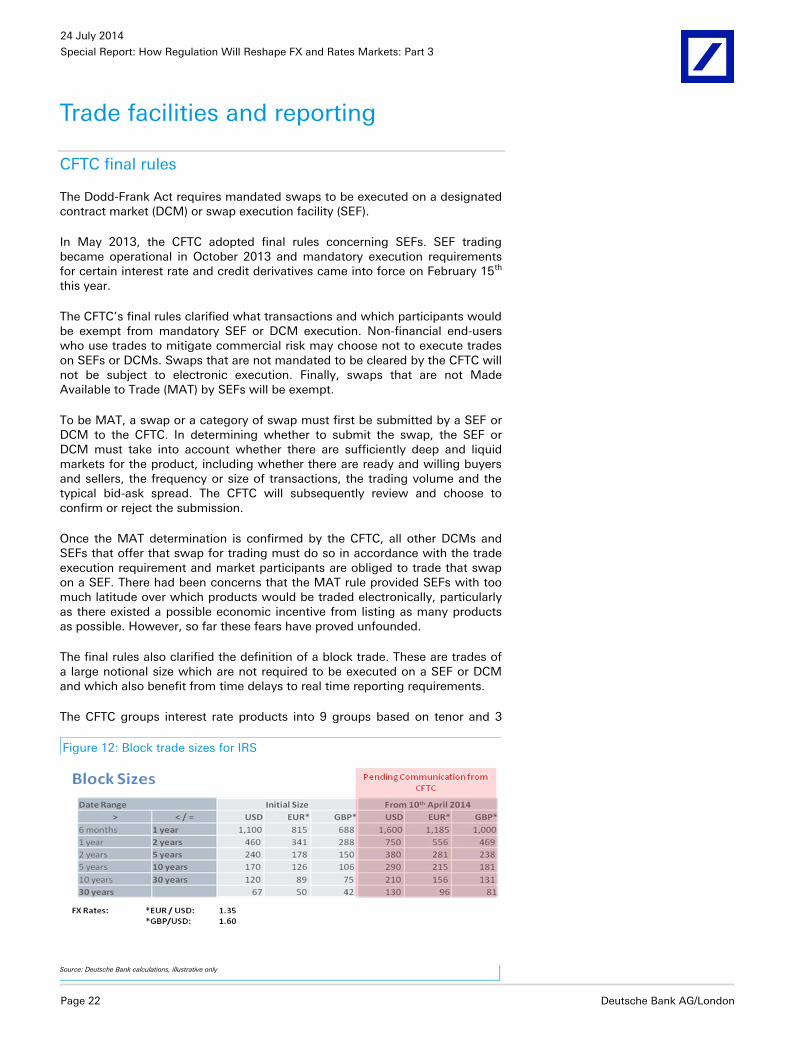

The final rules also clarified the definition of a block trade. These are trades of a large notional size which are not required to be executed on a SEF or DCM and which also benefit from time delays to real time reporting requirements.

The CFTC groups interest rate products into 9 groups based on tenor and 3

Figure 12: Block trade sizes for IRS

Source: Deutsche Bank calculations, illustrative only

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Deutsche Bank AG/London Page 23

groups based on currency. Currently, a 50% notional methodology determines which IRS transactions qualify as block trades. The methodology is designed to ensure that 50% of the total notional amounts of all swaps are traded on SEF and publically disseminated on a real time basis. Ultimately a 67% notional methodology will apply following CFTC confirmation. We outline the current block size trades for IRS in the information box above.

For FX products, block trade sizes are currently set with reference to futures contracts. Ultimately, the CFTC will split currencies into super majors and non-super majors. For super major currencies, the 67% notional methodology will be applied, while all non-super major currency swaps will be considered block trades.

SEF models

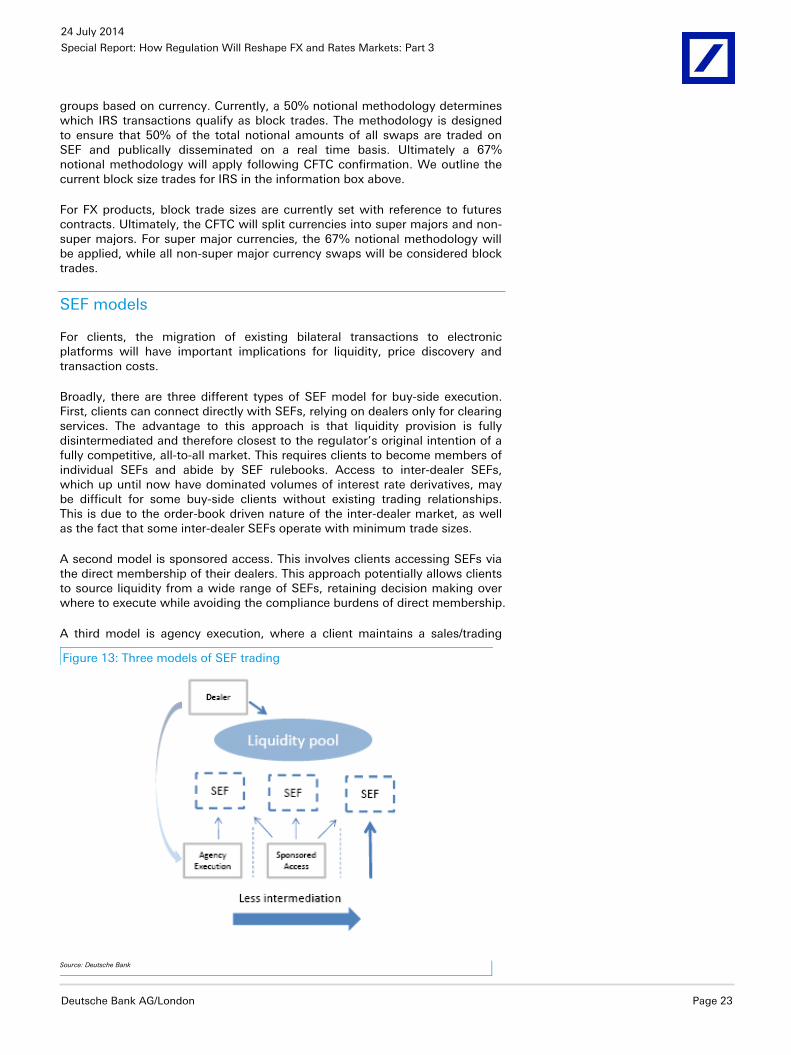

For clients, the migration of existing bilateral transactions to electronic platforms will have important implications for liquidity, price discovery and transaction costs.

Broadly, there are three different types of SEF model for buy-side execution. First, clients can connect directly with SEFs, relying on dealers only for clearing services. The advantage to this approach is that liquidity provision is fully disintermediated and therefore closest to the regulator’s original intention of a fully competitive, all-to-all market. This requires clients to become members of individual SEFs and abide by SEF rulebooks. Access to inter-dealer SEFs, which up until now have dominated volumes of interest rate derivatives, may be difficult for some buy-side clients without existing trading relationships. This is due to the order-book driven nature of the inter-dealer market, as well as the fact that some inter-dealer SEFs operate with minimum trade sizes.

A second model is sponsored access. This involves clients accessing SEFs via the direct membership of their dealers. This approach potentially allows clients to source liquidity from a wide range of SEFs, retaining decision making over where to execute while avoiding the compliance burdens of direct membership.

A third model is agency execution, where a client maintains a sales/trading

Figure 13: Three models of SEF trading

Source: Deutsche Bank

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Page 24 Deutsche Bank AG/London

relationship with a dealer, which takes responsibility for executing the trade on SEF. Dealers could provide extra services as part of this model, such as liquidity aggregation. By connecting to multiple SEFs dealers may be able to harness multiple liquidity pools, providing the client with a better price and arbitraging away liquidity fragmentation in the process. However, aggregation is only likely to be practical for products trading under a central limit order book (CLOB) model.

It remains to be seen whether volumes will be sufficient to support the number of SEFs that have registered with the CFTC. It may be that industry consolidation occurs due to the economies of scale latent in the cost per lot fees SEFs make from trades. This may in turn be advantageous for greater liquidity and price transparency.

On the other hand, individual SEFs may develop comparative advantages in certain products and for certain client types. As well as liquidity, operational costs, fees and the ability to efficiently connect to clearing houses and guarantee clearing will be foremost in the minds of clients when choosing SEFs.

Cross-border coordination of electronic execution rules will be crucial in determining the evolution of liquidity. Currently, CFTC rules mean US persons are required to trade mandated products on a CFTC-approved SEF. This may restrict their access to European trading platforms that are unwilling or unable to qualify for relief from CFTC rules. For their part, European clients that deal with US dealers may not wish to be subject to mandatory SEF execution and clearing requirements. There is a danger that liquidity is therefore fragmented across borders for similar products, leading to lower client choice and raising risks of regulatory arbitrage from dealers able to access both liquidity pools. 12

For their part, dealers are facing up to the consequences for traditional business models of electronic execution requirements, as well as more stringent capital and leverage rules. As we discuss below, the main obstacle

12 ISDA Research Note, Cross Border Fragmentation of Global OTC Derivatives: An Empirical Analysis

January 2014

Figure 14: Swap futures volumes are growing but still small

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

Mar-13 May-13 Jul-13 Sep-13 Nov-13 Jan-14 Mar-14 May-14

Swap futures open interest on CME, % 10 year US treasury note open interest

5 year deliverable USD IRS

10 year deliverable USD IRS

Source: Deutsche Bank, CFTC

24 July 2014

Special Report: How Regulation Will Reshape FX and Rates Markets: Part 3

Deutsche Bank AG/London Page 25

for dealers to shift from warehousing risk to an agency model is the absence of centralized liquidity pools to which they can act as gatekeepers. Developing SEF aggregation services is a possible response to this issue. However, the success of this approach will depend on liquidity fragmentation, as well as the extent to which CLOB trading takes off.