strategy& european banking outlook 2016 it’s time to ... · pdf fileit’s time...

TRANSCRIPT

It’s time to radically rethink business models

Strategy& European Banking Outlook 2016

2 Strategy&

Contacts About the authors

Düsseldorf

Peter Gassmann Partner, PwC Strategy& Germany +49-170-2238-470peter.gassmann @strategyand.de.pwc.com

Munich

Dr. Philipp WackerbeckPartner, PwC Strategy& Germany+49-170-2238-659philipp.wackerbeck @strategyand.de.pwc.com

Stuttgart

Dr. Sebastian MarekManager, PwC Strategy& Germany+49-170-2238-975sebastian.marek @strategyand.de.pwc.com

Dr. Philipp Wackerbeck is a partner in financial services with PwC Strategy& Germany. Based in Munich, he is a member of the financial-services team, where he is a leading practitioner in the area of risk, capital, and regulation for the banking and insurance industry.

Dr. Sebastian Marek is a manager with PwC Strategy& Germany. Based in Stuttgart, he is a leading financial-services practitioner. He has a strong track record in business strategy development and has led numerous engagements for financial institutions throughout Europe.

3Strategy&

Executive summaryAbout the authors

European banks need to drastically transform their business models to become sustainably profitable and earn their costs of equity. Our team recently studied 46 European banks and found that only 10 achieved a positive economic spread in 2015, thereby earning their costs of equity. The remaining banks in our study showed significant gaps in profitability. Overall, the European financial institutions we studied accumulated an earnings shortfall of €110 billion (US$125 billion).

Our study raises serious questions about the sustainability of current banking business models and offers three innovative strategic options for what traditional banks could become: platform banks, digital banks, or OEM banks — streamlined banks that emulate original equipment manufacturers such as carmakers.

Platform banks: This model would be marked by open infrastructures and the assimilation of products from competitors and financial technology companies into a bank’s own offerings. The core competencies of platform banks would include customer relationship management and the anticipation of client needs, along with the maintenance of open product infrastructures.

Digital banks: This model is characterized by extensive digitization of customer service as well as all downstream and back-office processes. Inspired by the product development approach of emerging technology companies, digital banks would be in a position to rapidly and efficiently respond to changes in customer or regulatory demands.

OEM banks: This model, inspired by automakers, calls for lean banks distinguished by a low degree of vertical integration. The traditional value chain would be dissolved and efficiency maximized by the integration of external vendors.

Although no traditional bank has yet made the full transition to any of these new models, there are signs that some institutions are moving in

4 Strategy&

that direction. Many startups that are disrupting traditional banks by heavily relying on technology to provide financial services are trying to establish themselves as platform providers for services such as payments, investing, or lending. Other banks are revamping their corporate strategies to shift toward becoming digital or open platform organizations. In addition, most banks have adopted elements of the OEM model by outsourcing part of their value chain, mainly to support such functions as information technology.

5Strategy&

Looking back to move forward

Within the last decade, European banks were hit by two grave events: the financial crisis of 2008, starting with the bankruptcy of Lehman Brothers, and the sustained European debt crisis beginning in 2010. Together these two events made evident the fragility and structural problems plaguing the global financial system.

In response to these serious threats, regulatory authorities around the globe, in Europe, and in the U.S. took serious actions to increase financial stability. Capital requirements have been significantly increased and are expected to increase further. Additionally, regulatory change reduced the possibilities for banks to earn money as they did in the old days.

New bank levies and compliance costs add further pressure on the profitability of the entire sector. To earn these additional costs in an ultra-low interest rate environment is a constant challenge for executives — especially since the full impact of the interest rate environment has yet to materialize, as banks usually can adjust margins on the liabilities side faster than on the assets side.

Banks also find themselves operating amid heavy market interventions by the European Central Bank and the European Stability Mechanism. Still, the European banking sector has not recovered fully from the crises, with the institutions’ market values stagnating below precrisis levels.

Our recent study of 46 major, exchange-listed European banks for the year 2015 shows that about 80 percent of these banks demonstrated significant profitability gaps and did not earn their costs of equity (CoE). Their total earnings shortfall amounted to €110 billion (US$125 billion) in 2015.

That precarious situation is not fully reflected in their capital market valuations: Nearly 45 percent of the institutions have an average price-to-book ratio of greater than one. Thus, these banks are trading for more than their book value even though half of them failed to cover their CoE.

6 Strategy&

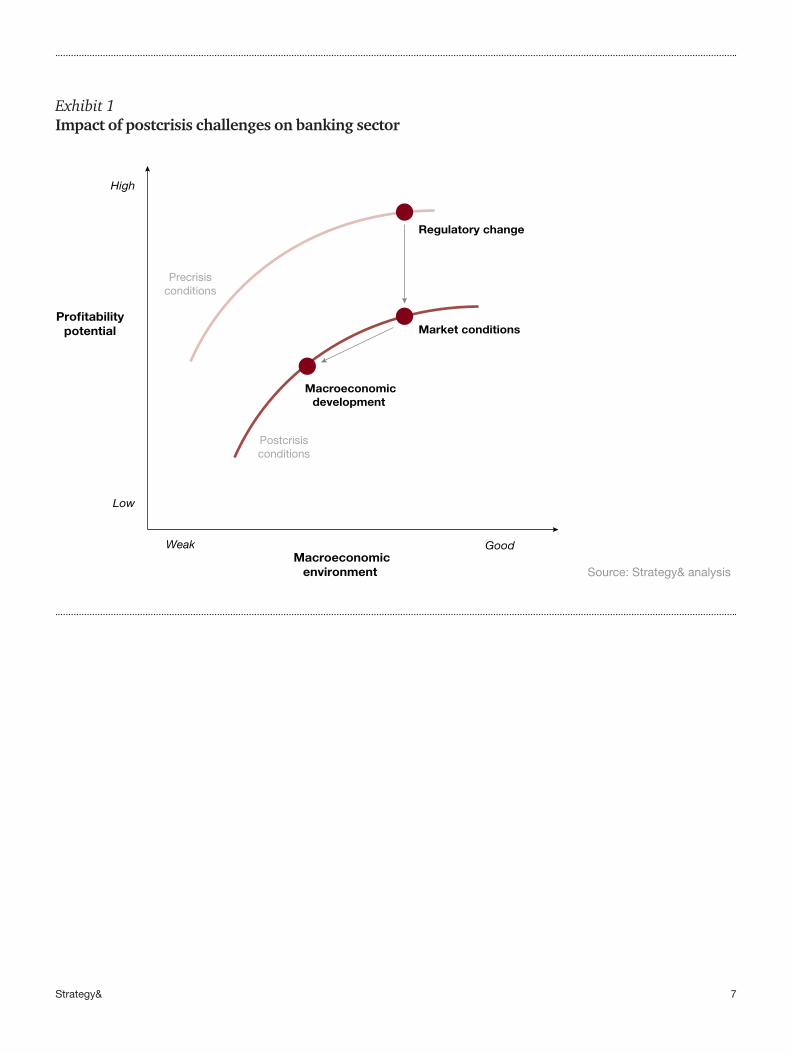

In this fragile environment, additional challenges have arisen for banks as they face a structural downward shift in their profit pools (see Exhibit 1, next page), driven by the following:

• Regulatory change: Increasing regulatory requirements are raising the cost of business for banks, as additional resources are required to ensure regulatory compliance.

• Market conditions: New market conditions are creating further pressure — including changes in customer behavior, emergence of new competitors, and shadow banks.

• Macroeconomic development: The macroeconomic environment, characterized by sustained low interest rates and high nonperforming loan ratios in Southern European countries, remains another big challenge cutting into overall margins and further limiting banks’ profitability potential.

The far-reaching implications and complexity of these postcrisis challenges are raising fresh doubts about whether a wait-and-see approach by European banks is sufficient to meet the expectations of both investors and regulators.

7Strategy&

Exhibit 1Impact of postcrisis challenges on banking sector

Source: Strategy& analysis

High

Low

Macroeconomicenvironment

Profitabilitypotential

Good Weak

Regulatory change

Macroeconomicdevelopment

Market conditions

Precrisisconditions

Postcrisisconditions

8 Strategy&

New business models for a sustainable and viable future

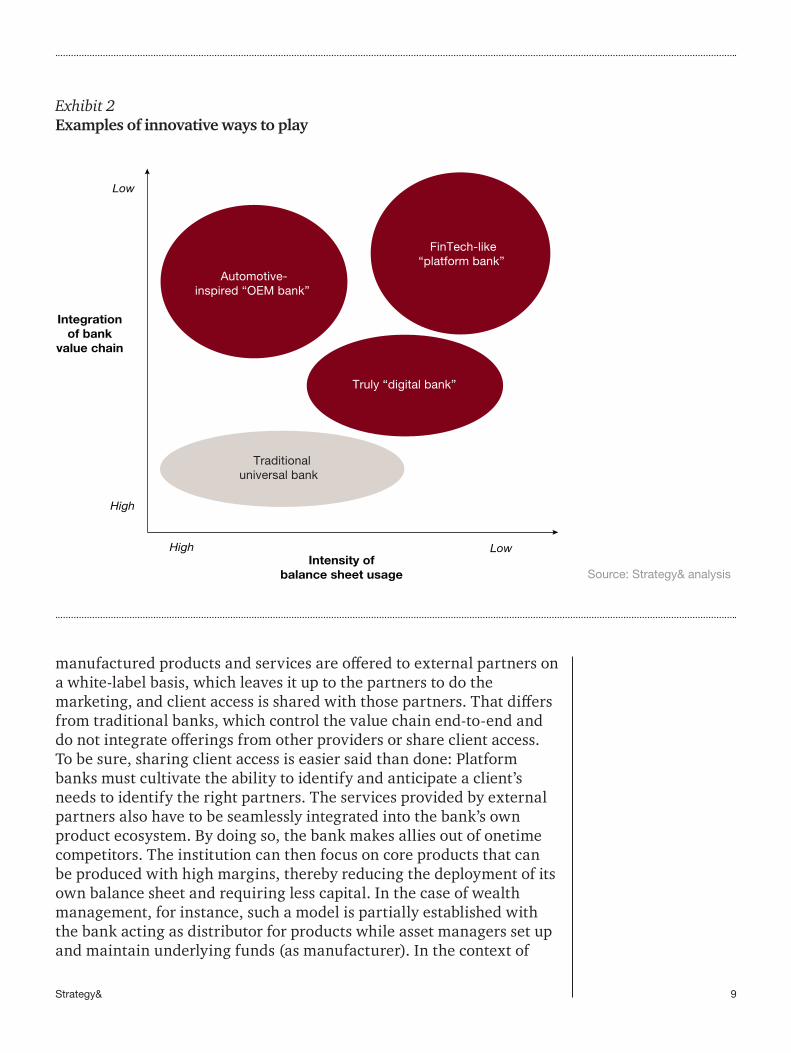

As European banks face the need for fundamental changes, traditional measures such as cost cutting, adapting operations and business to new regulations, or streamlining product portfolios are not enough to tackle their structural problems. The institutions need to go beyond that and transform their business models by embracing the opportunities of digitization and deleveraging their balance sheets. The three main strategic options that we have identified — platform banks seamlessly integrating products of external partners, digital banks fully embracing technologies, and lean OEM banks, which emulate original equipment manufacturers such as carmakers, focusing on core competencies — can bring about a sustainable and profitability-oriented transformation of the industry (see Exhibit 2, next page).

To become sustainably profitable the banks need to drastically transform their business models. To succeed in the transformation, legacy banks need to spread the message for change throughout their organizations, and they might meet resistance from a conservative corporate culture, especially since the transition requires adaptations to the established service offerings, processes, and infrastructure. The foremost task of executives, therefore, is to build a clear vision of the new model and the adaptations required to actively manage change from a top-down perspective — also against internal resistance. Not all of the institutions are likely to succeed in making the shift, and the European banking industry will experience further consolidation. The current models are not sustainable.

Strategy& has identified three innovative strategic options for what traditional banks could become (see Exhibit 3, page 10).

Platform banks

Platform banks distinguish themselves by open product infrastructures and the integration of offerings from FinTechs — startups that are disrupting traditional banks by heavily relying on technology to provide financial services — and other competitors. In addition,

9Strategy&

manufactured products and services are offered to external partners on a white-label basis, which leaves it up to the partners to do the marketing, and client access is shared with those partners. That differs from traditional banks, which control the value chain end-to-end and do not integrate offerings from other providers or share client access. To be sure, sharing client access is easier said than done: Platform banks must cultivate the ability to identify and anticipate a client’s needs to identify the right partners. The services provided by external partners also have to be seamlessly integrated into the bank’s own product ecosystem. By doing so, the bank makes allies out of onetime competitors. The institution can then focus on core products that can be produced with high margins, thereby reducing the deployment of its own balance sheet and requiring less capital. In the case of wealth management, for instance, such a model is partially established with the bank acting as distributor for products while asset managers set up and maintain underlying funds (as manufacturer). In the context of

Exhibit 2Examples of innovative ways to play

Source: Strategy& analysis

Low

High

Intensity ofbalance sheet usage

Integrationof bank

value chain

LowHigh

Automotive-inspired “OEM bank”

Truly “digital bank”

Traditionaluniversal bank

FinTech-like“platform bank”

10 Strategy&

Exhibit 3Business models

Source: Strategy& analysis

Platform bankSpecialized partnerswith different sizes

and offerings

Digital bank

Lean andcost-ef�cient

cross-country, cross-divisional

in-house structures

Back-enddigitization

Front-enddigitization

Client involvement inproduct and service

development

OEM bank

In-house

All other processes/products

Client front-end

Financial-services value chain

Core processes/products

Outsourced to specialists

11Strategy&

FinTechs and new offerings, such a setup provides excellent new business opportunities.

The most important step is the initial setup of the platform infrastructure and relationships since that is the very basis of the business model. The second step is the maintenance and seamless integration of external offerings into the bank’s own universe of products, which requires consolidated IT and application infrastructure. Moreover, internal risk and compliance management of external products and services must be set up.

Platform banks operate as an interface between clients, products, and external service providers, thus offering the clients broad but highly specialized services. The ability to manage this interface will be a key factor differentiating one bank from another within the industry. A well-functioning platform will enable banks to quickly offer new innovative products and services, which will extend their customer base to previously untapped segments of the market.

Digital banks

These banks distinguish themselves by extensive digitization of customer service as well as all downstream and back-office processes. End-to-end digitization is essential as banks compete against agile and disruptive market players. Inspired by the product development approach of emerging technology companies, digital banks are in a position to quickly and efficiently react to changes in customer or regulatory requirements. At the same time, highly scalable infrastructure services, such as B2B transactions, as well as the integration of clients in product development have to be supported by a digital business model. Full system data integration ensures that less time will be needed to market new products.

Although traditional banks have increased their digital offerings for the client, the back-end infrastructure is rarely digitized. What’s more, traditional banks rely on outdated software development and data concepts, making it hard to adapt to new digital technologies such as analytics.

Thus, the full implementation of digital opportunities can put banks in a much better position to respond to future market developments, since it will enable them to address the needs of upcoming generations of digital natives. Furthermore, banks can reap a competitive advantage and more easily fulfill future regulatory demands. Traditionally opaque processes become transparent due to digitization and standardization,

12 Strategy&

facilitating internal risk management as well as data reporting for regulators.

Vital for digital banks will be the full integration and digitization of back-office processes, as well as the elimination of redundant interfaces to reduce operating costs and increase the business’s agility. It will also be essential to cultivate strong banking capabilities to reap the benefits from low-cost products and services.

The execution of the digital bank business model might require significant up-front investment for the transformation or buildup of the system infrastructure. Since market developments in the digital world occur rapidly and companies can become no-names in the blink of an eye, it is important for any bank to integrate the latest technology and anticipate market trends. Hence, the development of products and the ecosystem needs to be flexible but standardized.

OEM banks

OEM banks, like the carmakers from which their nickname derives, focus on doing what they do best and leverage external providers to maintain a streamlined setup. They have a low degree of vertical integration and break down the traditional value chain, especially in areas not covered by classical outsourcing or offshoring. To maximize production efficiency, external vendors must be integrated. These external and specialized providers can take over non-differentiating and non-client-relevant processes such as the day-to-day servicing of loans, leaving in-house only core competencies that distinguish the bank from its competitors. External vendors therefore act as suppliers, especially in back- and middle-office processes.

A key to success is for the banks to take a broader view of what services external partners could provide, beyond what is typically the case today when the focus is on information technology and other supporting areas such as human resources or real estate management. Banks need to think bigger. In the credit business, for example, many tasks could be taken over by external partners, such as digitizing client data or using data providers. Today, for example, market data is often collected, aggregated, and analyzed in-house or not available in machine-usable formats.

The OEM strategy can lead to cost reductions and increased margins because of selective outsourcing of noncore processes. Because external partners can better focus on what they are good at, service quality can be enhanced in comparison with what we see now in the more complex and opaque legacy organizations. Consequently, the leaner and more

13Strategy&

flexible OEM infrastructure can make the banks more resilient and increase their ability to react faster to current and future market disruptions.

The main challenge of this model will be to identify the core capabilities that set the bank apart from its rivals and should be done in-house. (See “Make, buy, or cooperate: Right-sourcing the value chain in banking,” Strategy&, May 2015.) To build a sustainable business model, OEM banks also have to effectively manage their external providers during and beyond the integration process to ensure the quality of their work. Adopting this model could be a real test for traditional banks because they typically try to handle most things in-house, in contrast to car manufacturers, which constantly work with external suppliers to improve products and reduce costs. By strictly focusing on core functions and deploying service providers along the entire value chain, banks can achieve cost savings of as much as 40 percent.

14 Strategy&

Profitability gap in the European banking sector

Although the transition to these business models will not be easy, the downward shift in profitability potential is significantly affecting banks’ activities, calling into question the viability of their current business models. From an economic perspective, it is crucial to meet investors’ demands for returns and to achieve satisfactory distributions to shareholders. With shrinking profit pools, banks may fall short in meeting these demands and capital markets are likely to put additional pressure on institutions that fail to adequately compensate investors for their risk.

Also, the viability of traditional business models will be a key priority for authorities in this year’s supervisory review and evaluation process (SREP), an examination carried out by the European Central Bank and national authorities to gauge the banks’ ability to manage risks. One focal point will be the relationship between profits and costs of equity, which we have analyzed in this study as well. Financial institutions have to build up the capacity to generate acceptable short- and long-term returns while balancing their exposure to market risk.

In our study, we analyzed the European banking sector from a profitability perspective. Specifically, we took into consideration the so-called economic spread (ES), which measures the gap between actual return on equity and the bank-specific costs of equity. By applying this method, we addressed a fundamental pitfall of traditional performance and profitability measurement, which assumes constant CoE. The bank-specific CoE were approximated by the well-established capital asset pricing model and based on a market risk premium, the institution’s measure for systemic risk as well as a country-specific, risk-free interest rate. All data was compiled from publicly available information — e.g., balance sheet data and stock price information.

We studied 46 banks that are listed on the STOXX Europe 600 in order to evaluate the profitability of the European banking sector. The analysis shows that the vast majority of the banks — about 85 percent — generated a positive return on equity in 2015 (see Exhibit 4, next page).

15Strategy&

Yet only 10 of the banks we studied achieved a positive economic spread that year (see Exhibit 5). That means about 80 percent of the banks showed significant profitability gaps and did not earn their CoE.

Exhibit 4Return on equity of 46 analyzed banks (2015)

Exhibit 5Economic spread of 46 analyzed banks (2015)

Source: Strategy& analysis

Source: Strategy& analysis

–10%

5%

–50%

15%

–15%

–5%

10%

0%

Median

Median

–10%

10%

0%

–20%

–30%

–70%

Positive economicspread: 7 out of 10banks are Nordic

16 Strategy&

These figures imply that banks generally do not meet their investors’ expectations, so our study generates serious doubts about the sustainability of current business models. This picture is consistent over time with basically identical results for 2014.

Low earnings performance is a Europe-wide phenomenon. We were unable to identify a concentration of troubled banks in any particular country, finding instead that institutions are equally affected across regions. Of the 20 percent of banks with positive economic spreads, we discovered a cluster among Nordic institutions. This might be a result of individual factors such as strong competitive positions or leaner cost structures, as well as distinct market characteristics, even though these countries are also facing historically low interest rates.

Banks with a higher economic spread tend to have a higher valuation, reflecting a certain degree of market efficiency. The analysis shows that all banks with positive economic spreads have been traded with a price/book (P/B) ratio greater than one — without any discount to their book value. What’s more, a substantial number of banks recorded both very weak economic spreads and P/B ratios, so the profitability gap does not seem to be fully reflected in capital market valuations (see Exhibit 6, next page). Almost one-fourth of the banks we examined had a P/B ratio above one despite a negative ES. Overall, shareholders seem not to have yet fully priced in the lack of sufficient returns (adjusted for CoE) in banks’ valuations. Alternatively, but less likely, markets might expect that the negative economic spread will be equalized and turned into a positive spread, and have already priced this in.

17Strategy&

Exhibit 6Profitability vs. valuation of 46 analyzed banks (2015)

1. Average of weekly P/B ratios in 2015.

2. Although 11 banks have a negative ES but a P/B ratio above 1, one bank was excluded for clearer presentation (P/B: 0.33x, ES: -69%)

Source: Bloomberg; Strategy& analysis

Trend lineR2 = 0.39

11 banks with negative ESbut P/B ratio above 1

Price/bookratio

Economic spread

–35% –30% –25% –20% –15% –10% –5% 0% 5% 10%

2.5x

0.0x

1.5x

2.0x

1.0x

0.5x

18 Strategy&

A turning point for European banks

The market turbulence of the past decade and the significant regulatory challenges that have resulted are taking a heavy toll on European banks. Clearly, the industry has reached the point where vital decisions must be made. To become a sustainably profitable market earning its costs of equity, it must rethink its approach to business. We have offered a road map by identifying three potential alternative approaches. The corporate cultures in many legacy banks may stand in the way of this necessary change. Yet we have seen signs that some banks are gradually heading in the right direction.

For their part, regulators have already developed initiatives to influence how banks conduct business in the future. These include, for example, the Markets in Financial Instruments Directive and Regulation (MiFID II/MiFIR) and the European Market Infrastructure Regulation (EMIR), which actively influence the market structure and how business is conducted. Furthermore, supervisors are increasing their pressure on the banks from multiple angles.

The assessment of the viability of the business models will be a key priority for the European Central Bank in its annual review process. Additionally, the 2016 European Banking Authority stress test is expected to reveal a significant capital impact, which was analyzed in a recent Strategy& study, “Sneak preview: European banks and the 2016 stress test” (May 2016). Supervisors have developed a stricter approach that is creating further transparency on the pain points of the sector.

For banks, the first step is recognizing the need for change and acknowledging that the market environment has been radically altered. Not all executives have fully considered this. Some still believe that there will be a shift back to the old, more stable times or that their bank will not be affected by the market shifts, but they are wrong.

19Strategy&

Conclusion

Following a crisis-ridden decade, European banks are struggling to stabilize their industry and comply with new, stricter regulations in an environment of historically low interest rates. Regulatory authorities are increasingly concerned about the sustainability and viability of their business models and are launching a comprehensive review of the banks as a top priority for 2016. Still, too few banks are engaging actively with the business and market challenges on the horizon. Many are taking a dangerous wait-and-see approach with focus on traditional optimization measures, but shying away from more radical change. However, it’s exactly that more radical change that is needed to structurally address the profitability dilemma and adjust banks’ business models to the new regulatory and macroeconomic reality.

© 2016 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details. Mentions of Strategy& refer to the global team of practical strategists that is integrated within the PwC network of firms. For more about Strategy&, see www.strategyand.pwc.com. No reproduction is permitted in whole or part without written permission of PwC. Disclaimer: This content is for general purposes only, and should not be used as a substitute for consultation with professional advisors.

www.strategyand.pwc.com

Strategy& is a global team of practical strategists committed to helping you seize essential advantage.

We do that by working alongside you to solve your toughest problems and helping you capture your greatest opportunities.

These are complex and high-stakes undertakings — often game-changing transformations. We bring 100 years of strategy consulting experience and the unrivaled industry and functional capabilities of the PwC network to the task. Whether you’re

charting your corporate strategy, transforming a function or business unit, or building critical capabilities, we’ll help you create the value you’re looking for with speed, confidence, and impact.

We are part of the PwC network of firms in 157 countries with more than 208,000 people committed to delivering quality in assurance, tax, and advisory services. Tell us what matters to you and find out more by visiting us at strategyand.pwc.com.