stress test your portfolio. stress test your portfolio speakers: kevin gardiner, barclays wealth...

TRANSCRIPT

STRESS TEST YOUR PORTFOLIO

Stress Test Your Portfolio

Speakers:

• Kevin Gardiner, Barclays Wealth

• Jeff Johnson, Vanguard

• Joe LoPorto, Brown Brothers Harriman

• David Burns, Schroders

Moderator:

• Robert Paton, Aon Insurance Managers (Bermuda) Ltd.

Stress-testing portfolios: cash management

Kevin Gardiner, Head of Global Investment Strategy, Barclays Wealth

The stress test to end them all: 2008/9

• Counterparty risk – interbank freeze

• Breaking the buck

• Deflation risk

• Illiquidity

0

10

20

30

40

50

60

70

J un-00 J un-02 J un-04 J un-06 J un-08 J un-100

10

20

30

40

50

60

70

US Money Market Mutual Funds (as % of S&P market cap)Implied S&P volatility (VIX, %)

VIX and safe haven assets

Source: Datastream, Barclays Wealth Strategy

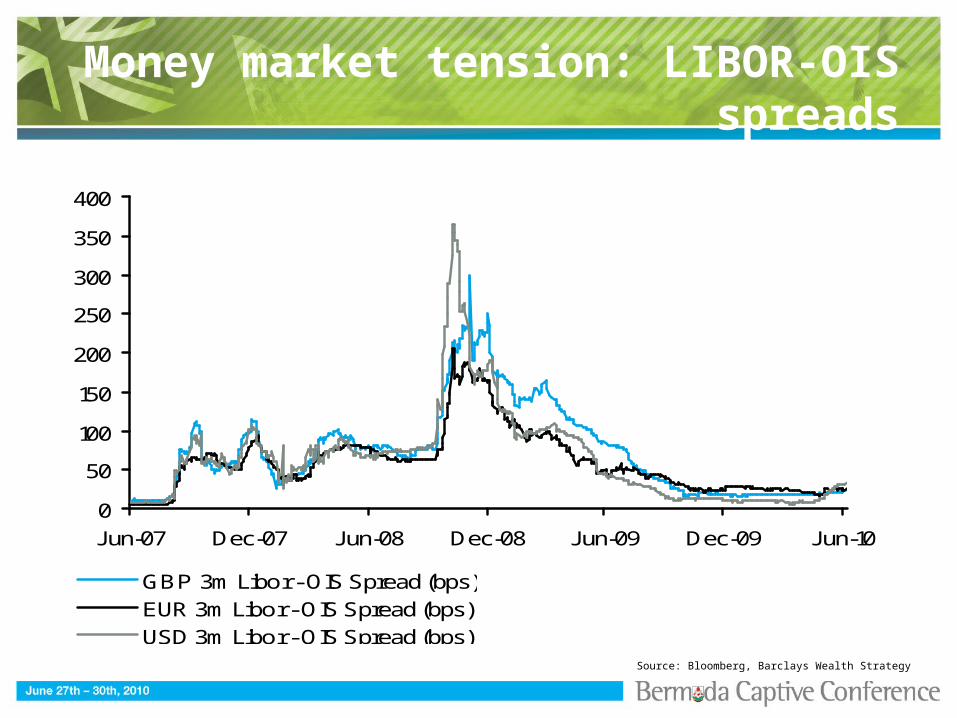

Money market tension: LIBOR-OIS spreads

0

50

100

150

200

250

300

350

400

J un-07 Dec-07 J un-08 Dec-08 J un-09 Dec-09 J un-10

GBP 3m Libor - OIS Spread (bps)EUR 3m Libor - OIS Spread (bps)USD 3m Libor - OIS Spread (bps)

bps

Source: Bloomberg, Barclays Wealth Strategy

0

100

200

300

400

500

600

700

800

900

1000

Jan-68 Jan-78 Jan-88 Jan-98 Jan-08

Real gold price, indexed

Source: Datastream, Barclays Wealth Strategy

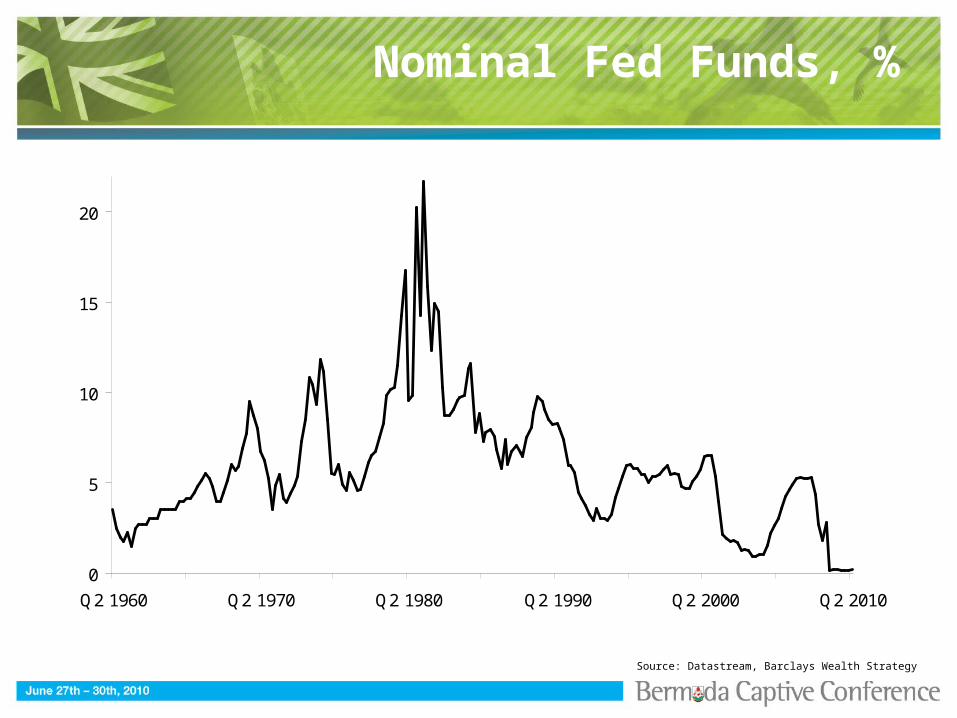

Nominal Fed Funds, %

Source: Datastream, Barclays Wealth Strategy

0

5

10

15

20

Q2 1960 Q2 1970 Q2 1980 Q2 1990 Q2 2000 Q2 2010

What stresses now?

• Banks broadly fixed

• Insurance enhanced

• Official rates on hold

• Look for high quality, low duration cash alternatives

Disclaimer

This document must not be regarded as independent research, which means that it has not been prepared in accordance with legal requirements designed to promote the independence of ‘investment research’, as defined in the UK FSA Handbook. As such, it has been signed off as a financial promotion. Investment ideas presented herein are not subject to any prohibition on dealing ahead of the dissemination of investment research, which applies only to independent research. Employees of Barclays Wealth are, however, subject to our internal Personal Account Dealing Policy and our Conflicts Management Policy.

This document has been prepared by Barclays Wealth, the wealth management division of Barclays Bank PLC ("Barclays"), for information purposes only. Barclays does not guarantee the accuracy or completeness of information which is contained in this document and which is stated to have been obtained from or is based upon trade and statistical services or other third party sources. Any data on past performance, modelling or back-testing contained herein is no indication as to future performance. No representation is made as to the reasonableness of the assumptions made within or the accuracy or completeness of any modelling or back-testing. All opinions and estimates are given as of the date hereof and are subject to change. The value of any investment may fluctuate as a result of market changes. The information in this document is not intended to predict actual results and no assurances are given with respect thereto.

The information contained herein is intended for general circulation. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The investments discussed in this publication may not be suitable for all investors. Advice should be sought from a financial adviser regarding the suitability of the investment products mentioned herein, taking into account your specific objectives, financial situation and particular needs before you make any commitment to purchase any such investment products. Barclays Wealth and its affiliates do not provide tax advice and nothing herein should be construed as such. Accordingly, you should seek advice based on your particular circumstances from an independent tax advisor. Neither Barclays Wealth, nor any affiliate, nor any of their respective officers, directors, partners, or employees accepts any liability whatsoever for any direct or consequential loss arising from any use of or reliance upon this publication or its contents, or for any omission. Past performance does not guarantee or predict future performance. The information herein is not intended to predict actual results, which may differ substantially from those reflected.

The products mentioned in this document may not be eligible for sale in some states or countries, nor suitable for all types of investors. This document shall not constitute an underwriting commitment, an offer of financing, an offer to sell, or the solicitation of an offer to buy any securities described herein, which shall be subject to Barclays’ internal approvals. No transaction or services related thereto is contemplated without Barclays' subsequent formal agreement.

Barclays Bank plc, Barclays Capital Inc., Member SIPC, and / or its affiliated companies may make a market or deal as principal in the securities mentioned in this document or in options or other derivatives based thereon. Barclays, its affiliates and the individuals associated therewith may (in various capacities) have positions or deal in transactions or securities (or related derivatives) identical or similar to those described herein. One or more directors, officers, and / or employees of Barclays Capital Inc. or its affiliated companies may be a director of the issuer of the securities mentioned in this document. Barclays Capital Inc. or its affiliated companies may have managed or co-managed a public offering of securities for any issuer mentioned in this document within the last three years.

"Barclays Wealth" is the wealth management division of Barclays and operates through Barclays Bank PLC and its subsidiaries. Barclays Bank PLC is authorised and regulated by the U.K. Financial Services Authority and is registered in England. Registered No: 1026167. Registered Office: 1 Churchill Place, London E14 5HP. This publication has been issued and approved by Barclays Bank PLC. Barclays Bank PLC is incorporated in England. Its members have limited liability.

Vanguard’s Approach to Manager Oversight & Selection

Jeffrey A. Johnson, CFA

Agenda

• Vanguard Overview

• Internal vs. External Management

• Manager Search & Oversight Process

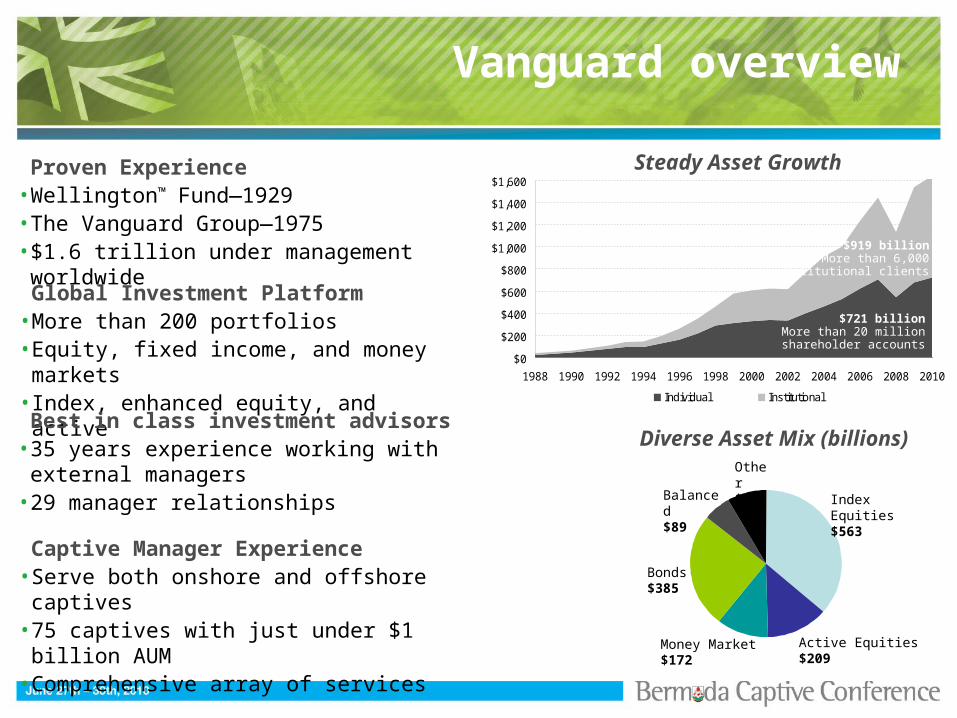

Proven Experience• Wellington™ Fund—1929• The Vanguard Group—1975• $1.6 trillion under management worldwide

Global Investment Platform• More than 200 portfolios• Equity, fixed income, and money markets• Index, enhanced equity, and active

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Individual Institutional

$919 billionMore than 6,000

institutional clients

$721 billionMore than 20 million

shareholder accounts

Best in class investment advisors • 35 years experience working with external

managers• 29 manager relationships

Vanguard overview

Diverse Asset Mix (billions)

Index Equities$563

Active Equities$209

Bonds$385

Balanced$89

Money Market$172

Other$131

Steady Asset Growth

Captive Manager Experience• Serve both onshore and offshore captives• 75 captives with just under $1 billion AUM• Comprehensive array of services

46%Externally managed

54%Internallymanaged

50%Actively Managed

50%Indexed

There are benefits to usinginternal and external managers

Diversity and Specialization

• Index and fixed income assets managed internally

– Cost-effectiveness

– Disciplined execution

• External active managers selected for specialized expertise

• No dominant approach or management “group think”

Discipline and Risk Control

• Tightly defined investment mandates

• Clear and style-consistent investment processes

• Rigorous selection and monitoring process for portfolio managers

• Experienced portfolio managers with track records in all market cycles

People Philosophy

Process PerformancePortfolio

People Philosophy

Process PerformancePortfolio

• Ownership structure• Business viability• Investment culture• Fiduciaries

Firm

Blend of qualitative and quantitativecriteria for manager selection

• Perspective• Experience• Depth• Stability

• Unwavering• Coherent• Rooted in research• Aligns with our beliefs

• Consistent with philosophy

• Transparent• Disciplined• Repeatable

• Reflects philosophy and process

• High conviction• Aware of risks

• Outcome of other elements• Various perspectives

– Risk-adjusted– Time periods– Benchmarks

Results

Vanguard’s low costs, which allows investors to keep more of a fund’s return

Select talented

managers

Combine managers effectively

Provide rigorous oversight+ +

Closing Thoughts

We believe manager oversight, selection, and risk management combines art and science

Fixed Income

Joseph LoPortoVice PresidentBrown Brothers Harriman & Co.Insurance Asset Management

Normal Probability DistributionWhat are common risk measures telling us?

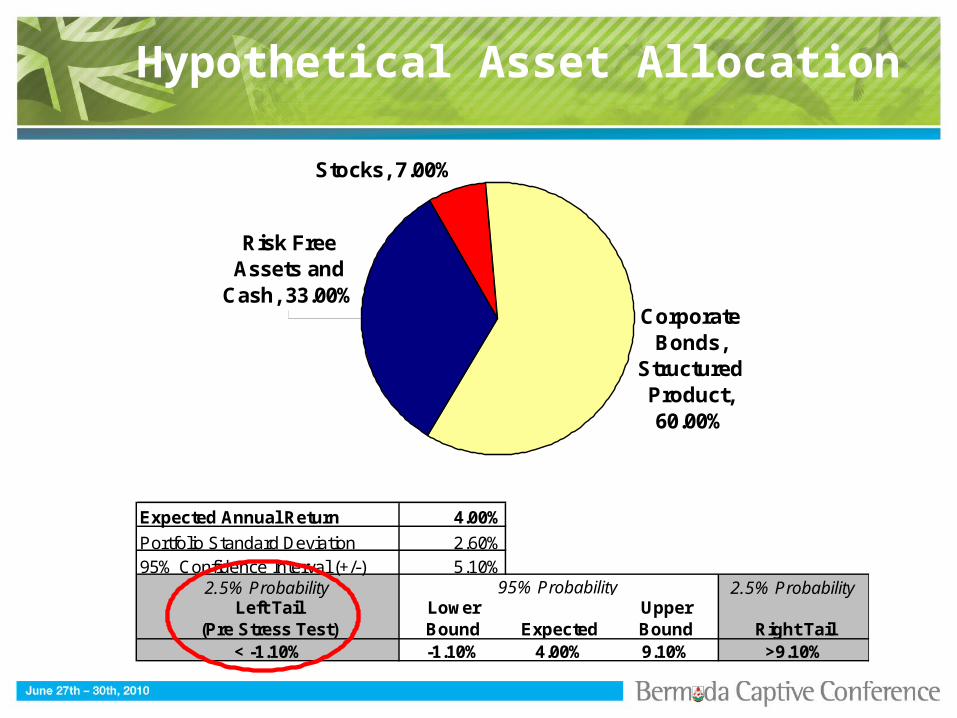

Hypothetical Asset Allocation

Expected Annual Return 4.00%

Portfolio Standard Deviation 2.60%95% Confidence Interval (+/-) 5.10%

2.5% Probability 2.5% ProbabilityLeft Tail

(Pre Stress Test)LowerBound Expected

UpperBound Right Tail

< -1.10% -1.10% 4.00% 9.10% >9.10%

95% Probability

Stocks, 7.00%

Corporate Bonds,

Structured Product, 60.00%

Risk Free Assets and

Cash, 33.00%

The Black Swan of 2008The Subprime Chickens Come Home to Roost

Investment Grade Bond Spreads rise by over 200 basis pointsStocks fall by more than 50%

June 2008 to March 200980

130

180

230

280

65

75

85

95

105

115

125

135

145

155

5yr IG CDS Spread (Left Hand Scale Reversed)

S&P 500 (Right Hand Scale)

Source: Bloomberg and BBH Analysis

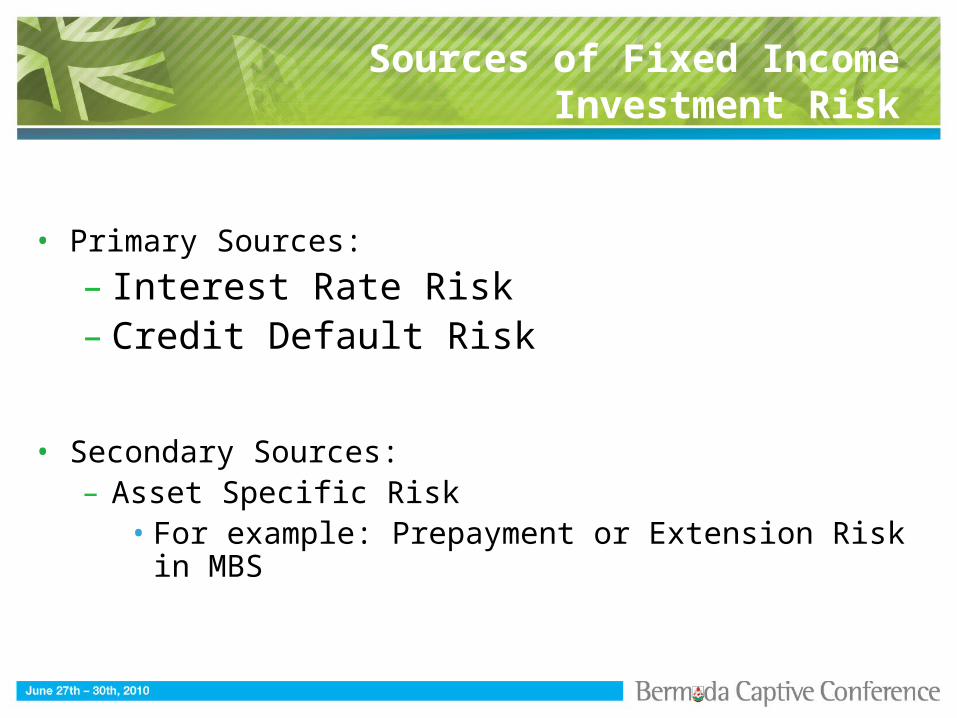

Sources of Fixed Income Investment Risk

• Primary Sources:

– Interest Rate Risk– Credit Default Risk

• Secondary Sources:– Asset Specific Risk

• For example: Prepayment or Extension Risk in MBS

Interest Rate RiskDuration

800

850

900

950

1000

1050

1100

1150

1200

-2.00% -1% 0.00% 1% 2.00%

Effective Duration Slope10 Year Treasury3.2% CouponDuration = 8.5 yrs

Bonds

How risky are bonds?

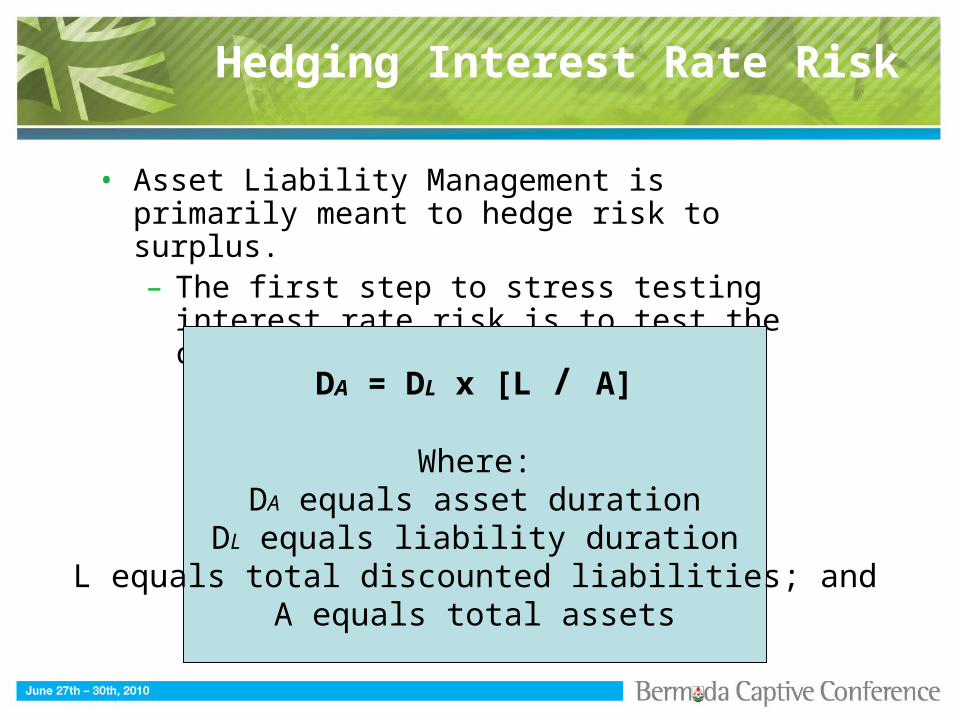

Hedging Interest Rate Risk

• Asset Liability Management is primarily meant to hedge risk to surplus.– The first step to stress testing interest rate risk

is to test the captive’s ALM approach.

DA = DL x [L / A]

Where:DA equals asset duration

DL equals liability durationL equals total discounted liabilities; and

A equals total assets

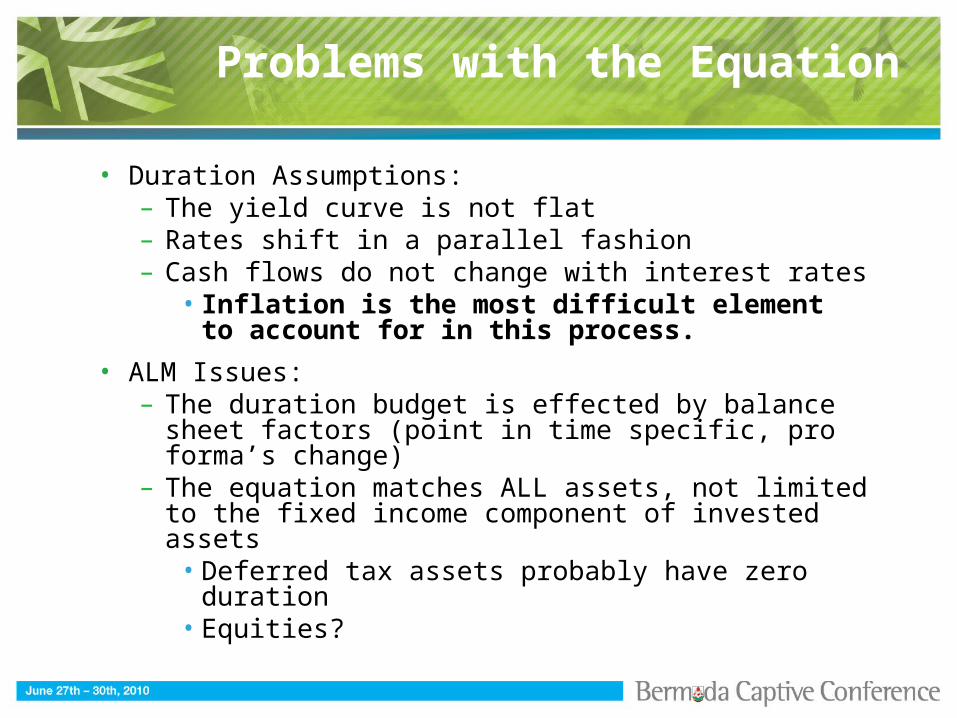

Problems with the Equation

• Duration Assumptions:– The yield curve is not flat– Rates shift in a parallel fashion– Cash flows do not change with interest rates

• Inflation is the most difficult element to account for in this process.

• ALM Issues:– The duration budget is effected by balance sheet

factors (point in time specific, pro forma’s change)– The equation matches ALL assets, not limited to

the fixed income component of invested assets• Deferred tax assets probably have zero

duration• Equities?

Stress Testing Parameters

• The residual duration budget is an important factor when evaluating the fixed income component of the captive’s investment strategy.

• The probability that the target duration is incorrectly estimated is important

• The ultimate parameters should incorporate the manager’s risk management processes and reflect empirical and hypothetical scenarios.

• If we can be fairly confident in our ALM study, stress testing should focus on the risk of permanent impairments.

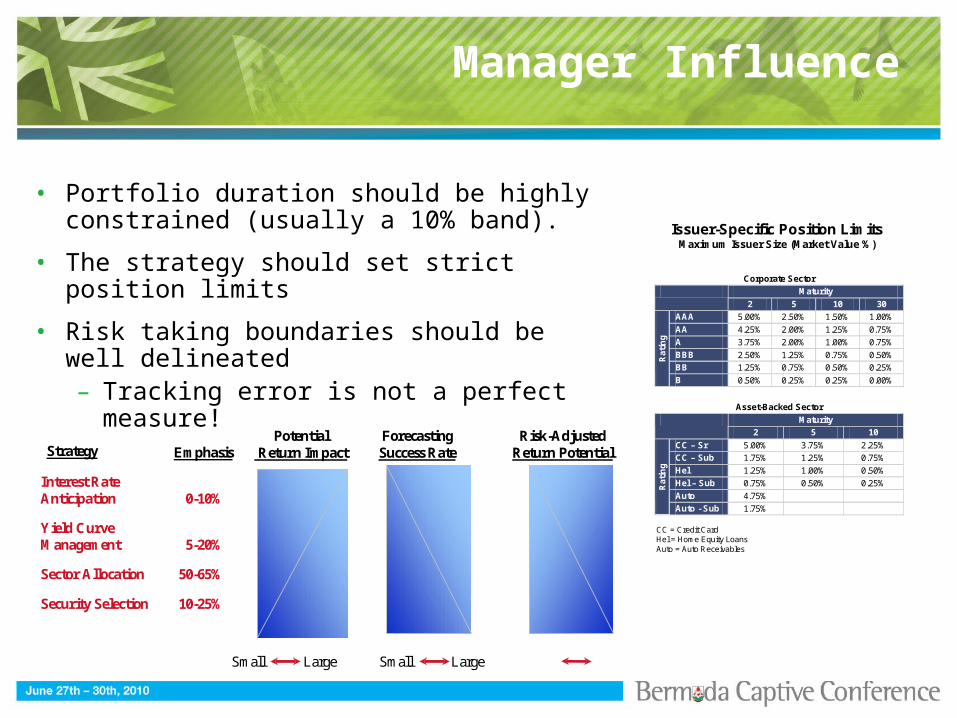

Manager Influence

Interest RateAnticipation 0-10%

Yield CurveManagement 5-20%

Sector Allocation 50-65%

Security Selection 10-25%

PotentialReturn Impact

ForecastingSuccess Rate

Risk-AdjustedReturn Potential

Small LargeSmall Large

EmphasisStrategy

Corporate Sector

Maturity

2 5 10 30

AAA 5.00% 2.50% 1.50% 1.00%

AA 4.25% 2.00% 1.25% 0.75%

A 3.75% 2.00% 1.00% 0.75%

BBB 2.50% 1.25% 0.75% 0.50%

BB 1.25% 0.75% 0.50% 0.25%

Rat

ing

B 0.50% 0.25% 0.25% 0.00%

Asset-Backed Sector

Maturity

2 5 10

CC – Sr 5.00% 3.75% 2.25%

CC – Sub 1.75% 1.25% 0.75%

Hel 1.25% 1.00% 0.50%

Hel – Sub 0.75% 0.50% 0.25%

Auto 4.75%

Rat

ing

Auto - Sub 1.75%

Issuer-Specific Position LimitsMaximum Issuer Size (Market Value %)

CC = Credit CardHel = Home Equity LoansAuto = Auto Receivables

• Portfolio duration should be highly constrained (usually a 10% band).

• The strategy should set strict position limits

• Risk taking boundaries should be well delineated– Tracking error is not a perfect measure!

Conclusion

Some Final Thoughts

Hypothetical Result

Expected Annual Return 4.00%

Portfolio Standard Deviation 2.60%95% Confidence Interval (+/-) 5.10%

2.5% Probability 2.5% ProbabilityLeft Tail

(Stress Test)LowerBound Expected

UpperBound Right Tail

-3.00% -1.10% 4.00% 9.10% >9.10%

4.0%

95% Probability

Adjusted Expected Return

Stocks, 7.00%

Corporate Bonds,

Structured Product, 60.00%

Risk Free Assets and

Cash, 33.00%

4% is a safeestimate.

Schroders Investment Management

Stressing equity portfolios and managing risk

trusted heritageadvanced thinking

IntroductionStressing equity portfolios and managing risk

• Stressing portfolios

• Cyclical market forum (CMF) presents economic scenarios used to shape equity portfolio positioning

• Portfolio managers use proprietary software (SMART) to stress portfolios

• Regulatory influence on risk analysis and capital requirements

• Managing risk

• Diversification reduces specific risk

• Active positioning according to market view

• Portfolio managers can use equity index futures or option strategies

IntroductionThe need to hedge risk

Volatility and downside risk put pressure on earnings and balance sheets

Cyclical market forum

Determining Schroders portfolio positioning

Quarterly Monthly Daily

Equity

Determine Investment Policy

– Asset class preferences

– Conviction & Accountability

– Set stop-loss/take-profit

Global Asset Allocation Committee

Gather Information

– Outlook for asset classes

– Specialist views

– Discuss economic scenarios

Cyclical Market Forum

InvestmentStrategy

Individual Fund Managers & Analysts

Construct

Portfolios

– Sizing positions

– Fund / Vehicle selection

– Monitor risk & return

Fund Management

& Analysis

Alternatives

5 Independent Specialists

40+ Senior Investment Specialists

53

162

68

Fund Managers

& Analysts

Fixed Income

Models & economic cycle analysis

Models & economic cycle analysis

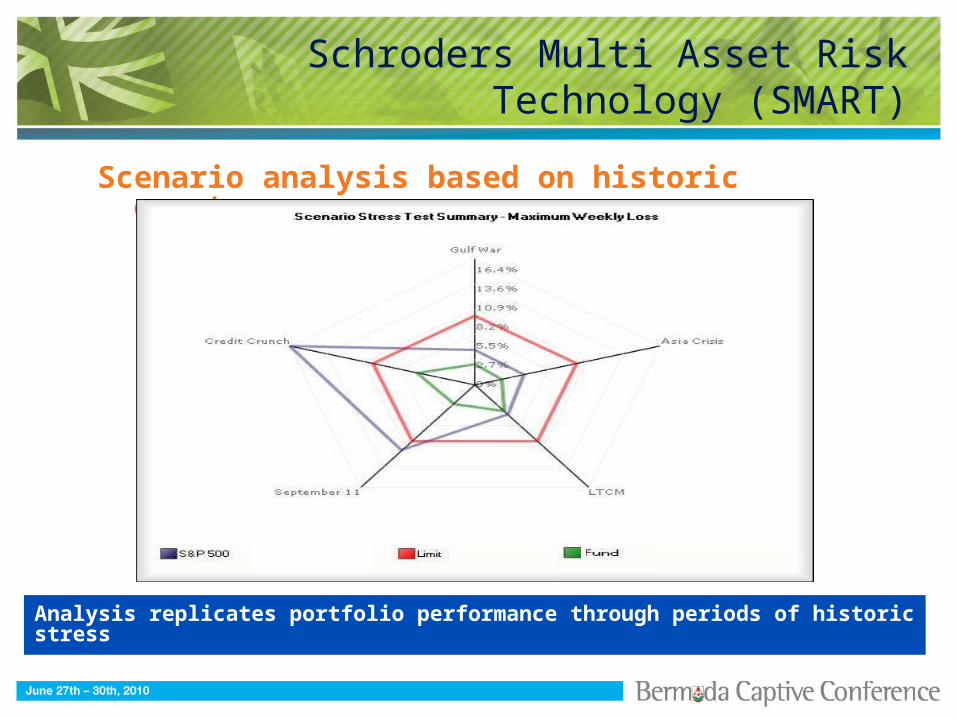

Schroders Multi Asset Risk Technology (SMART)

Allows us to analyse:– Alpha and Beta separately– VaR and CVaR – Non-normality i.e. extreme events– Stress tests for any asset class /

market scenario– Changes in correlations between

assets– Cyclical views on assets and

economic cycle– Regulatory constraints can be

imposed

This allows us to construct more robust portfolios, optimised from multiple risk return perspectives, and which therefore deal with volatile markets better.

Proprietary third generation portfolio risk analytics

Schroders Multi Asset Risk Technology (SMART)

Scenario analysis based on historic events

Analysis replicates portfolio performance through periods of historic stress

Mitigating short term equity risk

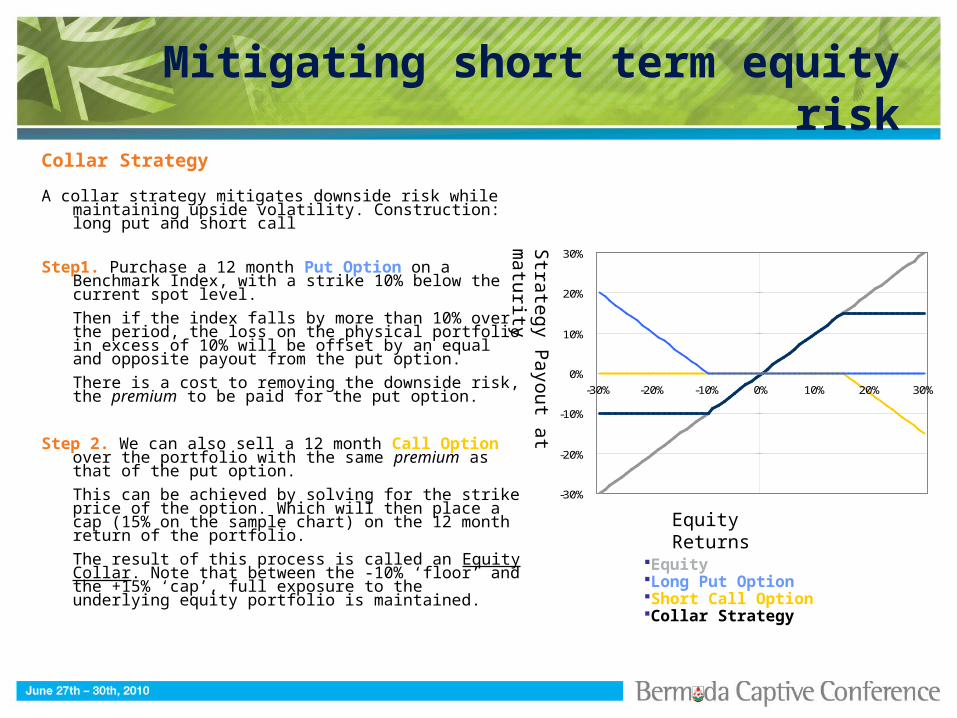

Collar Strategy

A collar strategy mitigates downside risk while maintaining upside volatility. Construction: long put and short call

Step1. Purchase a 12 month Put Option on a Benchmark Index, with a strike 10% below the current spot level.

Then if the index falls by more than 10% over the period, the loss on the physical portfolio in excess of 10% will be offset by an equal and opposite payout from the put option.

There is a cost to removing the downside risk, the premium to be paid for the put option.

Step 2. We can also sell a 12 month Call Option over the portfolio with the same premium as that of the put option.

This can be achieved by solving for the strike price of the option. Which will then place a cap (15% on the sample chart) on the 12 month return of the portfolio.

The result of this process is called an Equity Collar. Note that between the -10% ‘floor’ and the +15% ‘cap’, full exposure to the underlying equity portfolio is maintained.

-30%

-20%

-10%

0%

10%

20%

30%

-30% -20% -10% 0% 10% 20% 30%

EquityLong Put OptionShort Call OptionCollar Strategy

Equity ReturnsS

trat

egy

Pay

out a

t mat

urit

y

Mitigating short term equity risk

Implement the collar as an individual overlay on the physical portfolio• Fund manager can set a different strike price and maturity date for each option in line with

target ‘take profit’ level for the corresponding underlying stock• More value can be generated by selling calls on each of the individual stock components of

an index than by selling a single call on the index itself Replicate the put option strategy• Dynamically hedging the option position within the equity portfolio, using the tried and trusted

techniques that investment banks have always employed to hedge their exposure to the options they provide

• Eliminates both the cost and the counterparty risk of having a ‘middle man’ and able to choose the level of volatility of the market at which to implement the replication

Price transparency• Should be improved through the best execution process. In this process a panel of

counterparties is made to compete head to head for the best price on each leg of the collar strategy

Index futures

• Fund manager can reduce market exposure by selling index futures instead of selling holdings thus hedging market risk and reducing transaction costs

Improving on the collar strategy

Regulatory requirements

Increasing granularity of assessment necessary to capture risk profile

Solvency II equivalence• Stress test formulae calibrated to 99.5% VaR• ‘Global’ equities (listed in OECD or EEA) 30% market level shock, ‘Other’ 40% shock• Correlations • 1st June BMA announced pilot risk analysis study of Class 3 insurers – future extension

to Class 1 and 2?

Capital assessment• Interaction with liabilities • Interaction with other assets• Whole balance sheet approach

Important information

For Professional Investors only. Not suitable for Private Customers

This presentation contains indicative terms for discussion purposes only and is not intended to provide the solebasis for evaluation of the instruments described. It is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment recommendations. Schroders has expressed its own views and these may change. Information herein is believed to be reliable but Schroder Investment Management Ltd (Schroders) does not warrant its completeness or accuracy. No responsibility can be accepted for error of fact or opinion. This does not exclude or restrict any duty or liability that Schroders has to its customers under the Financial Services and Markets Act 2000 (as amended from time to time) or any other regulatory system.

For the purposes of the Data Protection Act 1998, the data controller in respect of any personal data you supply is Schroder Investment Management Limited (SIM). Personal information you supply may be processed for the purposes of investment administration by the Schroders Group which may include the transfer of data outside of the European Economic Area. SIM may also use such information to advise you of other services or products offered by the Schroder Group unless you notify it otherwise in writing.

Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them can go down as well as up and investors may not get back the amounts originally invested. As a result of the annual management fee being charged wholly to capital, the distributable income of the fund may be higher, but the capital value of the fund may be eroded

The hypothetical results shown in the presentation must be considered as no more than an approximate representation of the portfolios’ performance, not as indicative of how it would have performed in the past. It is the result of statistical modelling, based on a number of assumptions and there are a number of material limitations on the retroactive reconstruction of any performance results from performance records. For example, it does not take into account any dealing costs or liquidity issues which would have affected a real investment's performance. This data is provided to you for information purposes only as at today's date and should not be relied on to predict possible future performance.

Exchange rates may cause the value of overseas investments and the income from them to rise or fall. Funds may make use of derivatives which involve a higher degree of risk and can be more volatile

For your security, communications may be taped or monitored.

Issued by:

Schroder Investment Management Limited31 Gresham StreetLondon, EC2V 7QA

Registered no. 2015527 England. Authorised and regulated by the Financial Services Authority. April 2009