stronger… greener… bigger… e.i.d.- parry (india) limited · sugar based confectionery from...

TRANSCRIPT

0Making Sugar since 1842 0

E.I.D.- Parry (India) LimitedInvestor Presentation

Dec 2010

Stronger… Greener… Bigger…

Making Sugar since 1842 1

This presentation contains forward-looking statements which may be identified by their use of words like “plans,” “expects,” “will,” “anticipates,” “believes,” “intends,” “projects,”

“estimates” or other words of similar meaning. All statements that address expectations

or projections about the future, including, but not limited to, statements about the strategy for growth, product development, market position, expenditures, and financial results, are forward-looking statements.

Forward-looking statements are based on certain assumptions and expectations of future events. The companies referred to in this presentation cannot guarantee that these assumptions and expectations are accurate or will be realized. The actual results, performance or achievements, could thus differ materially from those projected in any such forward-looking statements. These companies assume no responsibility to publicly amend, modify or revise any forward looking statements, on the basis of any subsequent developments, information or events, or otherwise.

Disclaimer

2Making Sugar since 1842 2

Company Overview

Sugar Business ► World and Indian Sugar Balance► Closer look @ Sugar in South India► EID – Sugar Business

Bio Products Business► Nutraceuticals► Bio Pesticides

Consolidated Financials

Agenda

3Making Sugar since 1842 3

Company Overview

Sugar Business ► World and Indian Sugar Balance► Closer look @ Sugar in South India► EID – Sugar Business

Bio Products Business► Nutraceuticals► Bio Pesticides

Consolidated Financials

Agenda

4Making Sugar since 1842 4

E.I.D- PARRY (INDIA) LTD - OVERVIEWServing for more than 200 years….

Flagship company of Murugappa Group since 1981.

Pioneers in: ► Sugar from 1842► Distillery from 1848► Sanitaryware from 1906► Fertilisers from 1906 ► Sugar Based confectionery from 1914► Biogas and Bio earth 1987► Bio-pesticides from 1995► Co-generation- Exportable Power

from 1997► Algal Nutraceuticals from 1997► Branded Retail sugar from 2004

No.1 Sugar Producer in South India including Refinery

Second Largest Phosphatic Fertiliser producer in India

Enrich life by creating value from agriculture

“ Ranked 51 amongst the Top 200 Companies in India”- Economic Times 2009 survey

5Making Sugar since 1842 5

OVERVIEW

BUSINESS UNDER EID‟s FOLD

Sugar Bio – Products Farm Inputs

Sugar Cogeneration Distillery Refinery

TCD - 19000 84.5 MW 135 KLPD

TCD - 5000 16 MW 45 KLPD 2000 TPD 35 MW

TCD - 8500 45.5 MW 50 KLPD

Tamil Nadu & Puducherry

Andhra Pradesh

Karnataka

TCD - 32500 146 MW 230 KLPD 2000 TPD35 MW

Bio – Pesticides & Nutraceuticals

PhosphaticFertilisers 3.25 MMT

Specialty Nutrients & Compost

Pesticides

Retail

TCD – Tons crushed per dayMW - Mega Watt KLPD - Kilo Litres per day TPD - Tons per dayMMT - Million Metric Ton

6Making Sugar since 1842 6

85100

146

100

135

230

1900021500

32500

0

5000

10000

15000

20000

25000

30000

35000

0

50

100

150

200

250

2008-09 2009-10 2010-11

MW KLPD TCD

GROWING FACTS

Capacity - Sugar Power Distillery Production (in MMT) -Phosphatic Fertilisers

Production Capacity – 3.25 MMT

2.02 2.09

2.63

-

0.50

1.00

1.50

2.00

2.50

3.00

2007-08 2008-09 2009-10

7Making Sugar since 1842 7

Rs Million

Consolidated Gross Income Consolidated EBIT

FINANCIAL FACTS

EBIT includes Minority Interest

CAGR – Operating CAGR

Rs Million

0

20000

40000

60000

80000

100000

120000

05-06 06-07 07-08 08-09 09-10 10-11 H1

29218 2801546767

104246

77477

50264229 1181

9083

80

Gross Income Profit on Sale of Invest

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

05-06 06-07 07-08 08-09 09-10 10-11 H1

2564 2247 3914

8809 9694 6534 229 1181

9083

80

EBIT(operating) Profit on Sale of invest.

8Making Sugar since 1842 8

Rs Million

Bio- Pesticides

Segmental Revenue and EBIT

Farm Inputs

Note: Revenue & EBIT of 2008-09 includes Rs. 159 Crs Business Assistance Agreement

18985 21178

38354

96140

64294

44003

12591741

3943

87057096 7337

0

2000

4000

6000

8000

10000

0

20000

40000

60000

80000

100000

120000

05-06 06-07 07-08 08-09 09-10 10-11 H1

SUGAR

8232

5559 64167596

11482

6199

935

308

-596

472

1682

-902

-1500

-1000

-500

0

500

1000

1500

2000

0

2000

4000

6000

8000

10000

12000

14000

05-06 06-07 07-08 08-09 09-10 10-11 H1

257263

306

364

363 25242

29

59

72

56

16

0

10

20

30

40

50

60

70

80

0

50

100

150

200

250

300

350

400

05-06 06-07 07-08 08-09 09-10 10-11 H1

Nutraceuticals

111 172

291

390 35313 14

1

19

-32 -40

-30

-20

-10

0

10

20

30

050

100150200250300350400450

06-07 07-08 08-09 09-10 10-11 H1

9Making Sugar since 1842 9

Company Overview

Sugar Business ► World and Indian Sugar Balance► Closer look @ Sugar in South India► EID – Sugar Business

Bio Products Business► Nutraceuticals► Bio Pesticides

Consolidated Financials

Agenda

10Making Sugar since 1842 10

Source: ISO Quarterly Market Outlook, Nov 2010 Source: ISMA – Oct 2010

Particulars

SS 2007-

08

SS 2008-

09

SS 2009-

10

Opening stock 11.0 10.5 4.4

Production 26.3 14.6 18.9

Imports 0 2.5 4.1

Consumption 21.9 23.0 21.5

Exports 4.9 0.2 0.2

Closing stock 10.5 4.4 5.7

Stock to Consumption Ratio % 48 20 27

India‟s Sugar Balance (mln t)World Sugar (mln t)

SUGAR – DEMAND & SUPPLY

Particulars2009/

102008/

09

Changes

in mln t in %

Production 160.5 151.8 8.7 5.7

Consumption 164.3 164.0 0.3 0.2

Surplus / Deficit -3.8 -12.2

Import demand 52.9 50.2 2.7 5.4

Export Availability 52.9 49.2 3.7 7.5

End Stocks 57.3 60.7 -3.4 -5.6

Stocks/ Consumptionratio in % 34.9 37.0

11Making Sugar since 1842 11

Company Overview

Sugar Business ► World and Indian Sugar Balance► Closer look @ Sugar in South India► EID – Sugar Business

Bio Products Business► Nutraceuticals► Bio Pesticides

Consolidated Financials

Agenda

12Making Sugar since 1842 12

South India is good….

Competitiveness in the Sugar Industry is driven by

► Mutual Inter-dependence between the Farmer & the Miller

Combined Productivity (Farm Yields and Factory Recoveries) is the key

Thus, Total Recovered Sugar as MT per Ha (ie Cane Yield in MT per Hectare times Recovery as Ton of Sugar per Ton of Cane) must be maximised

► Port Facilities

Freight cost for importing / exporting is Lower for South Indian Mills comparing to North Indian Mills.

► Tamil Nadu

Long crushing season being a plus

100% Drawal for Tamil Nadu Mills

No Poaching

► No Prior Period Liabilities for EID

Source: ISMA (5 Yrs average)

Total Sugar Recovered (MT/Ha)

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

11.00

12.00

Tam

ilnad

u

Karn

atak

a

Mah

aras

htra

And

ra P

rade

sh

Guj

arat UP

All

Indi

a

13Making Sugar since 1842 13

StateNo. of .

Operating DaysOff SeasonOperation

Tamil Nadu 210

Karnataka 160

Maharashtra 150

Uttar Pradesh 120

Andhra Pradesh 118

* Off Season Operation for running Power, Raw Sugar Processing

Source: ISMA (5 yrs Avg. No. of. Operating Days) Source: ISMA (5 Yrs Avg. of Yield and Recovery)

Operating days & Off Season Yield and Recovery

South India is good….

104.8 85.8 78.7 77.8 56.5

9.26

10.669.81

11.599.36

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

0.0

20.0

40.0

60.0

80.0

100.0

120.0

Yield (tonnes per hectare) Recovery

14Making Sugar since 1842 14

Long Duration Vs. High Recovery Mill areas

Long Duration

TCD - 3500

No. of working days - 240

Recovery - 9.5%

Investments - Rs.210 Crs.

Return on Investment *- 20%

Only Colombia

Short Duration No Interest

TCD - 5000

No. of working days - 168

Recovery - 10.5%

Investments - Rs.326 Crs.

Return on Investment - 16%

Low Recovery High Recovery

Key Assumptions

Cane Crushing = 8.4 Lakh MTs

Sugar Price = Rs.26000

Cane Price = Rs.2000/MT

Cane Crushing = 8.4 Lakh MTs

Sugar Price = Rs.26000

Cane Price = Rs.2200/MT

15Making Sugar since 1842 15

Recent AcquisitionsLocation Advantage

Recent Acquisitions - Karnataka / AP

High Recovery Zone of NW Karnataka Bagalkot, Haliyal & Ramdurg

Closer to major Indian sugar markets

Less controls on Molasses and Alcohol than TN

Proximity to Silkroad minimise the freight cost

Larger power shortage than TN for Cogen

I) Sadashiva – Bagalkot (Karnataka)

Date of Acquisition : 7-10-2009

Capacity - 2500 TCD , 15.5 MW

76% Shareholding, Investment Rs. 496 Mn

Present Debt - Rs. 930 Mn

II) Parrys Sugars Industries Ltd (PSIL*) –(Haliyal, Ramdurg, Sankili) (Karnataka & Andhra)

Date of Acquisition : 27-08-2010

Capacity - 11000 TCD ,46 MW , 95 KLPD

65% Shareholding, Investment Rs. 988 Mn

Open offer for 20% shareholding at Rs.110.69 (12.18% Subscribed)

Present Debt – Rs. 3720 Mn* GMR Industries Ltd name has been changed into Parrys Sugar Industries Ltd

Sadashiva / Parrys Sugar Industries Ltd

Making Sugar since 1842 16

Experienced Management Strong track record of turning around poorly performing sugar mills Additional benefits from use of Coromandel International’s expertise

Extending EID practices in Sadashiva / Parrys Sugar- Farmer relations , Agricultural depots- Building Trust with Farmers, Govt, Bankers etc.- Tie up with Harvesting & Transport Gangs

Cane development initiatives across Command area

Working with Bank/Farm equipment suppliers for introducing Best practices including Drip irrigation , Borewells for increase in Acreage & Yield - Significant cane planting ensuring cane availability for next season

Debottlenecking at all factories to achieve 100% capacity utilisation

Restructure debt – Substitution of high cost debt with low cost debt

17Making Sugar since 1842 17

Agenda

Company Overview

Sugar Business ► World and Indian Sugar Balance► Closer look @ Sugar in South India► EID – Sugar Business

Bio Products Business► Nutraceuticals► Bio Pesticides

Consolidated Financials

18Making Sugar since 1842 18

TiruvallurChennai

Vellore

KanchipuramTiruvannamalai

Dharmapuri

VilupuramSalem

NamakkalErodeNilgiris

Kanyakumari

Tirunelveli Tuticorin

Ramanathapuram

Sivaganga

PudukkottaiDindigul

Madurai

Virudunagar

Teni

Thanjavur Tiruvarur

Cuddalore

Trichirappalli

Perambalur

Karur

Puduchery

Nagappattinum

Krishnagiri

Coimbatore

Bidar

Gulbarga

Bijapur

BagalkotBelgaum

Kappal

Raichur

Bellary

DharwadGadag

Uttar kannad Davengere

Shimoga

Udupi

Tumkur

KolarBangaloreChikmangalur

Hassan

Mandya

Mysore

Koorag

Chamrajnagar

Adllabad

Nizamabad Karimnagar

Chitoor

Khammam

SrikakulamVizianagaram

East Godavari

Warangal Vishakhapatnam

West Godavari

Guntur

MedakSangareddi

NalgondaRangareddi

Mahbubnagar

Ongole

NelloreCuddapah

Kurnool

Anantapur

PugalurTCD – 4000

Cogen – 22 MW

Salem

NamakkalErodeNilgiris

KarurKarurCoimbatoreCoimbatoreCoimbatoreCoimbatore

PettavaithalaiTCD – 3000

Cogen – 20 MW

ChennaiChennaiChennaiChennaiChennai

Kanchipuram

PuducheryPuducheryPuduchery

PuducheryTCD – 2000

PudukkottaiPudukkottai

Thanjavur TiruvarurTiruvarurTiruvarurTiruvarur

Cuddalore

Perambalur

NagappattinumNagappattinumNagappattinum

NellikuppamTCD – 6000

Cogen – 24.5 MWDistillery – 75 KLPD

PudukottaiTCD – 4000Cogen – 18Tuticorin

Ramanathapuram

Sivaganga

Ramanathapuram

Sivaganga

PudukottaiTCD – 4000Cogen – 18

SivagangaDistillery – 60 KLPD

Uttar kannad DavengereDavengere

Shimoga

Udupi

KooragKooragKoorag

RamdurgTCD – 2500

Cogen – 6 MW

Bijapur

BagalkotBelgaum

BagalkotTCD – 2500

Cogen – 15.5 MW

BelgaumBelgaum

HaliyalTCD – 3500

Cogen – 24 MWDistillery –50 KLPD

SrikakulamSrikakulamSrikakulam

SankiliTCD – 5000

Cogen – 16 MWDistillery – 45 KLPD

West GodavariGodavariGodavariGodavariGodavari

Silkroad Refinery2000 TPD

35MW

Tamil Nadu

Andra Pradesh

Karnataka

SOUTH INDIA PRESENCE

19Making Sugar since 1842 19

Sugar – 32500 TCD

2006-07 2007-08 2008-09 2009-10 2010-11 (Est)

Nellikuppam 5000 5000 6000 6000 6000

Pugalur 4000 4000 4000 4000 4000

Pettavaithalai 2500 2500 3000 3000 3000

Pudukottai 3000 4000 4000 4000 4000

Puducherry 2000 2000 2000 2000 2000

Tamil Nadu & Puducherry 16500 17500 19000 19000 19000

Sankili 5000

Andhra Pradesh 5000

Bagalkot 2500 2500

Haliyal 3500

Ramdurg 2500

Karnataka 2500 8500

Capacities and Operating Parameters

20Making Sugar since 1842 20

Particulars 2006-07 2007-08 2008-09 2009-10 2010-11(Est)

Cane Registration(in acres) 107782 92261 97147 94553 173000

Cane Crushed(Mn MT) * 4.10 4.23 3.37 2.55 5.30

Recovery % 8.93 9.06 9.52 8.89 10.30

Process Loss 1.92 1.91 1.89 1.89 1.85

No. of. Operating days

in Season 273 278 204 158 150-230

off Season(Power, Raw Sugar) 40 45-50

Estimates for 2010-11

Cane Crushing (Mn MT)

EID – 3.6, Sadashiva – 0.4, PSIL – 1.4

Operating Parameters

*

21Making Sugar since 1842 21

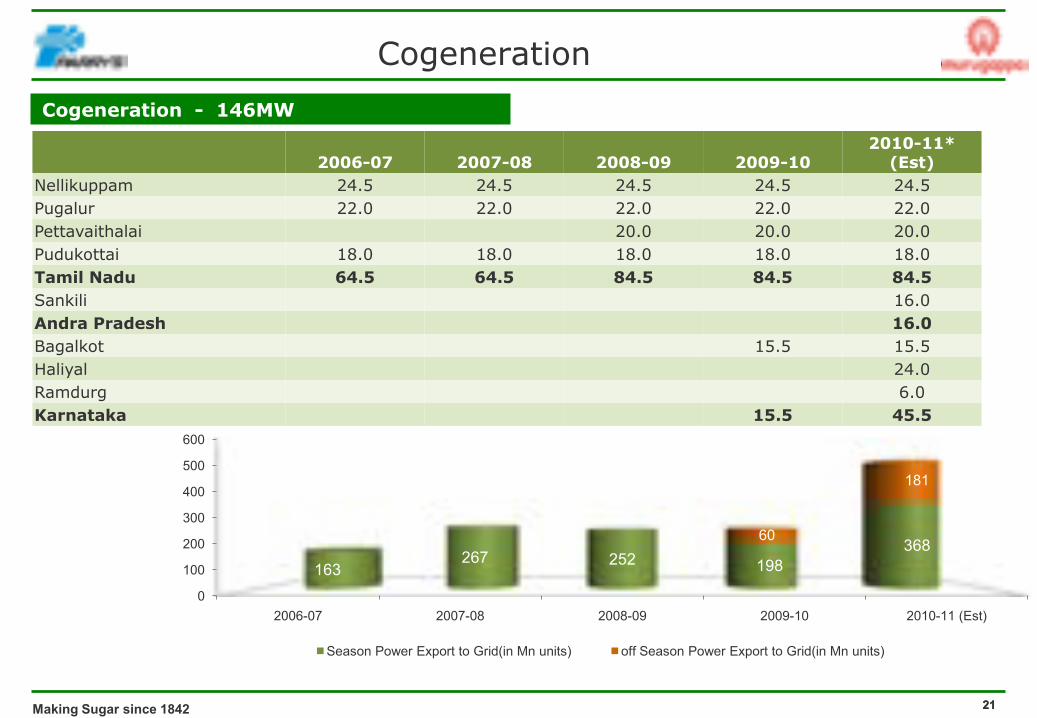

Cogeneration - 146MW

Cogeneration

2006-07 2007-08 2008-09 2009-102010-11*

(Est)Nellikuppam 24.5 24.5 24.5 24.5 24.5Pugalur 22.0 22.0 22.0 22.0 22.0Pettavaithalai 20.0 20.0 20.0Pudukottai 18.0 18.0 18.0 18.0 18.0Tamil Nadu 64.5 64.5 84.5 84.5 84.5Sankili 16.0Andra Pradesh 16.0Bagalkot 15.5 15.5Haliyal 24.0Ramdurg 6.0Karnataka 15.5 45.5

0

100

200

300

400

500

600

2006-07 2007-08 2008-09 2009-10 2010-11 (Est)

163267 252 198

36860

181

Season Power Export to Grid(in Mn units) off Season Power Export to Grid(in Mn units)

22Making Sugar since 1842 22

Distillery – 230 KLPD

Distillery

2006-07 2007-08 2008-09 2009-10 2010-11* (Est)Nellikuppam 40 40 40 75 75

Sivaganga 60 60 60

Tamil Nadu 40 40 100 135 135

Sankili 45

Andra Pradesh 45

Haliyal 50

Karnataka 50

11 10 1017

54

1822

2634

34

0

5

10

15

20

25

30

35

40

0

10

20

30

40

50

60

2006-07 2007-08 2008-09 2009-10 2010-11 (Est)

Sales(Mn Ltrs) Avg Realisation

23Making Sugar since 1842 23

52%

72%

79%

89%92%

40%

50%

60%

70%

80%

90%

100%

2006-07 2007-08 2008-09 2009-10 2010-11 E

22% 31%

69%

100%

0%

20%

40%

60%

80%

100%

120%

2007-08 2008-09 2009-10 2010-11 E

Level of Value Addition

Bagasse utilisation (%) for Value Addition

Molasses utilisation (%) for Value Addition

Bagasse to Power

Molasses to Alcohol

24Making Sugar since 1842 24

Increasing the coverage of HSV by introducing of Parry India (PI) Cane Variety through Parry's

breeding program

LogisticsManagement

Optimum Utilization during Peak recovery by balancing the Cane supply and Operating Days, capacity expansion, modernization, efficiency improvement( Total Loss).

Ensuring application of fertilizer for improving quality of cane through soil analysis, input supplies on right time

by Parry Mayyams ,extension and farmer training programs

.

Recovery Improvement – Actions Taken

Unique – Agri services

Making Sugar since 1842 25

Cane Development

Linkages Govt..Institutions

Information IndiaAgriline.com

Kiosk

Payments On timeBanks/SAP

Harvest LogisticsTransport

Crop Insurance

Bio controlAgents Production

/Supply

MonitoringDiagnostics

Control

RegistrationCrop schedule

Technology transferKnowledge sharing

Training

Infrastructure& Crop loans

Soil analysisNutrient scheduleRemote sensing

Agri -inputs

MachineryImplements

Tissue culturePlants

Nursery setts

PI – Parry Varieties

Co – Benchmark Varieties

The only sugar company in India & perhaps one of the five in the world who practice sugar cane

varietal development

9.67

10.17

10.8710.58 10.71 10.50

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

11.00

Co 86032 PI 96 1946 PI 96 843 PI 95 151 PI 98 1160 PI 99 1750

Sug

ar y

ield

Mt/h

a

Average Sucrose yield (MT/Ha)

26Making Sugar since 1842 26

Higher Crushing & Higher Recovery

Recent Investments in Sugar will enable Crushing during peak period

8.529.04

10.8711.25

10.54

9.26

8.68

9.5610.07

0

2

4

6

8

10

12

0

20000

40000

60000

80000

100000

120000

140000

OCT NOV DEC JAN FEB MAR APR MAY JUN JUL AUG SEP

Cane Crushed (MTs) Recovery (%)

27Making Sugar since 1842 27

On time Payment –All the Time

Command Area100% Drawal

Cane weighment & payment alertThrough SMS

Integrated System from Cane Registration to Payment at Rural banks

No prior period Liabilities for EID

Farmer Loyalty

Parrys corner(Knowledge sharing )

Crop information & InsuranceTissue culture, Parry Varieties

Crop LoansFarmers Accidental

Insurance & Hospitalisation

Centralised, Web based , online

Automated display Cane weighment

system On factory gate

Hassle free cash delivery through

Online baking at his rural back yard

Cane Management System, SAP

wireless online

connectivity

In House ERP solution

Farmer

Cane harvester

Transporter

Farmer Relations – leverage IT

28Making Sugar since 1842 28

Parry Service Kiosks (PARRY MAYYAM)

Harvesting / Transport Labourers Insurance

Mechanisation of Cane harvesting

Centralised cane payment by e-mode… payment lead time reduced by 3 days

Higher Yield

Timely Supply of Cane

Farm Labour Relations

BrokersSugar Mills

Bulk Users

WholesalersRetailers

Industrial Users

Traditional

Disadvantages

- Pricing determined by few brokers

-End consumer needs not addressed

- Pricing is the “sole purchase criteria”

- No scope for Customization / Value addition

Brokers

Sugar Mills

EID

Sugar Sales value chain

Advantages

- Derisking – Reduced channel dependency

- Customisation and Value addition.

Authorized Distributers

Industrial Users Retailers100%

Making Sugar since 1842

Making Sugar since 1842 30

Sugar Sales Segment wise – Last 6 Years

Institutional Customers 250

Retail Outlets 19000

Achieved through

- Moving from Standards to Specifications

- Customised solutions for Industrial customers

Grades, Packing, Pricing modes, Service parameters.

- Retail Brand – Large Sales Network

Sugar Sales value chain

Reduced dependency on Traditional Channels

0.59 0.69 0.80 1.00 0.85 1.000.02 0.05 0.080.15 0.25 0.20

4.49

2.69

3.803.67

3.09 2.47

0.00

1.00

2.00

3.00

4.00

5.00

6.00

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11(Est)

Institution Retail Trade

In Lac MT

Institutional Segment …………

Making Sugar since 1842 31

Beverage sugarConfectioner’s sugar BiscuitsBaker’s sugar

Pharma sugarSugar for Indian Sweets

32Making Sugar since 1842 32

Halal

Indian Pharmacopoeia

Our Certifications

British Pharmacopoeia

Kosher

US Pharmacopoeia

ISO 9001-2008

Japanese Pharmacopoeia European Pharmacopoeia

33Making Sugar since 1842 33

SPRI – USA

SRI – Australia

Mitr Phol – Thailand

TLPT – UK

Honeywell Tech.

IPRO – Germany

ISSCT

Mitr Phol – Thailand

CTC – Brazil

ICSB

ISSCT

Milling MarketingCane Growing

Cargill

Sucden

Czarnikow

Working with

34Making Sugar since 1842 34

REACHING OUT BEYOND TRADITIONAL FRONTIERS………..

Silkroad Sugar… An Innovative Business Model

35Making Sugar since 1842 35

Destination Refinery concept

► Logistical Advantage in transportation of Raws and refining at destination

Locational Advantage

► East Coast Advantage, proximity to Kakinada Port

► Sugar Consumption /demand strongly correlated , future growth in countries like China, India

Cargill backing, largest Sugar trader accounting 25% of global trade

SEZ Advantage

► Duty , Tax concessions

Power Plant

► Integrated for energy, thus low cost

Silkroad Sugar Pvt Ltd

Unit in Parry Infra SEZ , Kakinada (Andhra Pradesh)

Joint Venture company of - EID Parry India Ltd (50%)- Cargill Asia Pacific Private Ltd (49%) - New Ambadi Estates Private Ltd (1%)

Capacity levels► Refined Sugar – 2000 TPD(Annual

capacity of 0.60 mn MT)► Power – 35 MW► Exportable Power – 25 – 27 MW

Investment – Rs 4300 Mn

Why Refinery in India? Capacity & Investments

Why Silkroad ?

Making Sugar since 1842 36

Concept -- Refinery + Power plant

Model -- India + Overseas…..

• Pioneering technology

Integration of Gas Turbine Power Plant with Refinery is Globally UNIQUE

• Strategic Location

Landfall point of India’s largest Natural Gas find

All weather deep draught Private port

Deficit sugar geography

Above all …..

Silkroad Sugar Pvt Ltd

Opportunistically can source from

OR supply into India

37

EID - Investment Trend in Sugar

Making Sugar since 1842 37

Rs. Million

Note:

Benefits to accure from following investment from 2010-11:

► Inv (Silkroad, Sadashiva & Parrys Sugar) - Rs. 2477 Mn

► Cogen CAPEX - Rs. 1050 Mn

► Distillery CAPEX - Rs. 1340 Mn

Investment 05-06 06-07 07-08 08-09 09-10 10-11 (Est) Total

Existing Facilities 1019 1158 909 2975 816 400 7276

Puducherry Unit 563 563

Silkroad Sugar 36 459 355 143 993

Sadashiva 496 496

GMR 988 988

Total 1019 1756 1369 3330 1455 1388 10316

Low Cane High sugar price

Mid - Base 100 Peak/Trough - Represented in %age terms of Mid

80

55

23

36

49

39

14

0

20

40

60

80

100

120

Peak Mid Trough

Sugar Cogen Distillery

107100

63

Consolidated Operation – Minimise Cyclicality

High Cane Low sugar price

38Making Sugar since 1842

in Terms of PBIT

39

Agenda

Making Sugar since 1842 39

Company Overview

Sugar Business

► World and Indian Sugar Balance

► Closer look @ Sugar in South India

► EID – Sugar Business

Bio Products Business

► Nutraceuticals

► Bio Pesticides

Consolidated Financials

40

NutraceuticalsGlobal Nutraceutical Segments Parry Nutraceuticals “Product portfolio”

NutraceuticalsParry

Nutraceuticals

Herbal formulations

Organic Spirulina

AstaxanthinBeta caroteneLycopeneLutein

EPA /DHA

FenugreekGalactomanon

Existing ProductsPipeline Products

Global Ingredient market size - $ 27 Billions

Global Nutritional products (formulated) Industry size - $ 236 Billions

Making Sugar since 1842

41

Products and Opportunities…..

Making Sugar since 1842 41

Organic Spirulina

Current market - $ 7.5 Mi.

Parry share - $ 3.35 Mi.

CAGR - 2%

Astaxanthin

Current market - $ 35 Mi.

Parry share - $ 2.46 Mi.

CAGR - 7%

Lutein

Current market - $ 150 Mi.

Parry share - $ 1.47 Mi.

CAGR - 9%

Lycopene

Current market - $ 55 Mi.

Parry share - $ 1.25 Mi.

CAGR - 6%

42

Life Sciences – Business Model

Making Sugar since 1842 42

Biomass

Oleoresins

Pre-Mixes

Formulations

Ingredient Supplier

Valensa

IP / Science based products

Life Science

Health condition products backed by

IP / Science

Enhancing value of existing ingredients

Dietary Supplements

Food & Beverage

Cosmeceutical

Brand / Retail

Health solution provider

Participation in this segment will multiply the Value of the business

43

Nutraceuticals - Financials

Making Sugar since 1842 43

Description 06-07 07-08 08-09 09-10

SALES 112.0 171.9 291.4 374.7

PBIT 13.0 13.7 1.3 20.5

CAPITAL EMPLOYED 243.4 327.6 490.9 474.6

INVESTMENTS

PHTYO REMEDIES (2007-2010) 21.3

VALENSA (2008-2011) 481.0

TOTAL 502.3

Rs. Mn

44

Agenda

Making Sugar since 1842 44

Company Overview

Sugar Business

► World and Indian Sugar Balance

► Closer look @ Sugar in South India

► EID – Sugar Business

Bio Products Business

► Nutraceuticals

► Bio Pesticides

Consolidated Financials

45Making Sugar since 1842 45

Multi discipline R&D

Product development

Registration

India/Abroad

Raw material –Neem Seed

MarketDemonstration

Test Marketing

Concept selling

Exports

1994

28 countries

Main Plant

Bio - Business

46Making Sugar since 1842 46

Market Est. for Bio pesticides

The global pesticide market was valued at approximately $40 billion in 2008. This figure increased to nearly $43 billion in 2009 and is expected to grow at a compound annual growth rate (CAGR) of 3.6% to reach $51 billion in 2014.

Biopesticides represent a strong growth area in the global pesticide market. This segment is expected to grow at a 15.6% compound annual growth rate (CAGR) from $1.6 billion in 2009 to $3.3 billion in 2014.

Synthetic pesticides represent the greatest market share, valued at $41 billion in 2009. This market will be worth an estimated $48 billion in 2014, a compound annual growth rate (CAGR) of 3%

Source:* http://www.bccresearch.com/chem/C204R.html

47Making Sugar since 1842 47

Bio biz…so far

Achieved maximum production of 7450 Kg and sale of 5300 kg so far in a year.

Obtained product registration in over 32 countries with Brazil, S Korea, Australia and Japan developing into new high volume potential markets.

Received 3 different patents for product and process across 10 countries.

Year 09-10 was an aberation(due to recession)

Launched a plant extract based Plant Growth Regulator granule, achieved a sale of about 500 MT in 2009-10. plan in place to double the volume in 10-11

Plan to increase sale by 60% during 2010-11

48Making Sugar since 1842 48

Description 06-07 07-08 08-09 09-10

Sales Quantities

Total Technical(in Kgs) 3928 5129 4900 4319

Abda MT 30 147 509

Sales Value (Rs. Mn) 262.7 306.0 363.6 362.6

PBIT(Rs. Mn) 29.3 59.2 71.7 56.1

Capital Employed(Rs. Mn) 368.9 363.7 463.9 505.6

Bio – Pesticides Financials

49

Agenda

Making Sugar since 1842 49

Company Overview

Sugar Business ► World and Indian Sugar Balance► Closer look @ Sugar in South India► EID – Sugar Business

Bio Products Business► Nutraceuticals► Bio Pesticides

Consolidated Financials

50Making Sugar since 1842 50

FINANCIALS SNAP SHOT: CONSOLIDATED

Revenue

EBT PAT

Rs. Million

0

20000

40000

60000

80000

100000

120000

FY 07-08 FY 08-09 FY 09-10 H1 10-11

44090

101584 75508

49359

Sales incl Govt. …

0

5000

10000

15000

20000

FY07-08 FY 08-09 FY09-10 H1 10-11

28907660 8420 5662

908380

EBT(excl. Profit on Sale of Invest) Profit on Sale of Investments

16745

8502

2890

5662

0

2000

4000

6000

8000

10000

FY07-08 FY 08-09 FY09-10 H1 10-11

10473878 3866 3460

5670

70

Net Profit excl Sale of Invest. Profit on Sale of Invest. after Tax

9548

39361047

3460

51Making Sugar since 1842 51

Average Payout over last 5 Years – 32%, Rs. 3571 Million(Group Dividend Policy – 30% of PAT )

Operating Margin % Return on Equity

Long Term Debt : Equity Return on Capital Employed

FINANCIALS SNAP SHOT: CONSOLIDATED

10%

24%

22%

16.15%

0% 10% 20% 30%

FY 07-08

FY 08-09

FY 09-10

HY 10-11

8%

8%

13%

13%

0% 5% 10% 15%

FY 07-08

FY 08-09

FY 09-10

HY 10-11

0.43

0.27

0.32

0.46

0 0.1 0.2 0.3 0.4 0.5

FY 07-08

FY 08-09

FY 09-10

HY 10-11

13%

19%

17%

10%

0% 5% 10% 15% 20%

FY 07-08

FY 08-09

FY 09-10

HY 10-11

Making Sugar since 1842 52

OTHER FINANCIAL INFORMATION

Share Holding Pattern as on 30th Sep, 2010Free Cash Flow (in MN)

4248

551

6582

3896

01000200030004000500060007000

FY 07-08 FY 08-09 FY 09-10 HY 10-11

Rating

CRISIL upgraded

- Long Term Debt rating to AA/Stable outlook from AA-/Stable outlook.

- Short Term Debt rating to P1+

- same ratings also been assigned by CRISIL as Bank Loan rating as per BASEL II requirement for the existing and proposed Bank Facilities.

47.17%

13.58%

9.61%

4.58%0.85%3.59% 19.70%

0.92%

Period ending 30-9-2010 Promoters

Mutual Funds

Banks/FI

FII

NRIs

Bodies Corporate

Indian Public

Trusts

53Making Sugar since 1842 53

Quartely ResultsLast week of January „2011 and April „2011, July „2011, October „2011

For further information, please contact:

P. Gopalakrishnan,

Vice-President (Finance)

E.I.D. - Parry (India) Limited,

Dare House, 234 NSC Bose Road,

Chennai – 600 001.

Tel: +44 – 2530-6789

Email: [email protected]

Website: www.eidparry.com

Investor Co-ordinator

54Making Sugar since 1846 54

Stronger… Greener… Bigger…