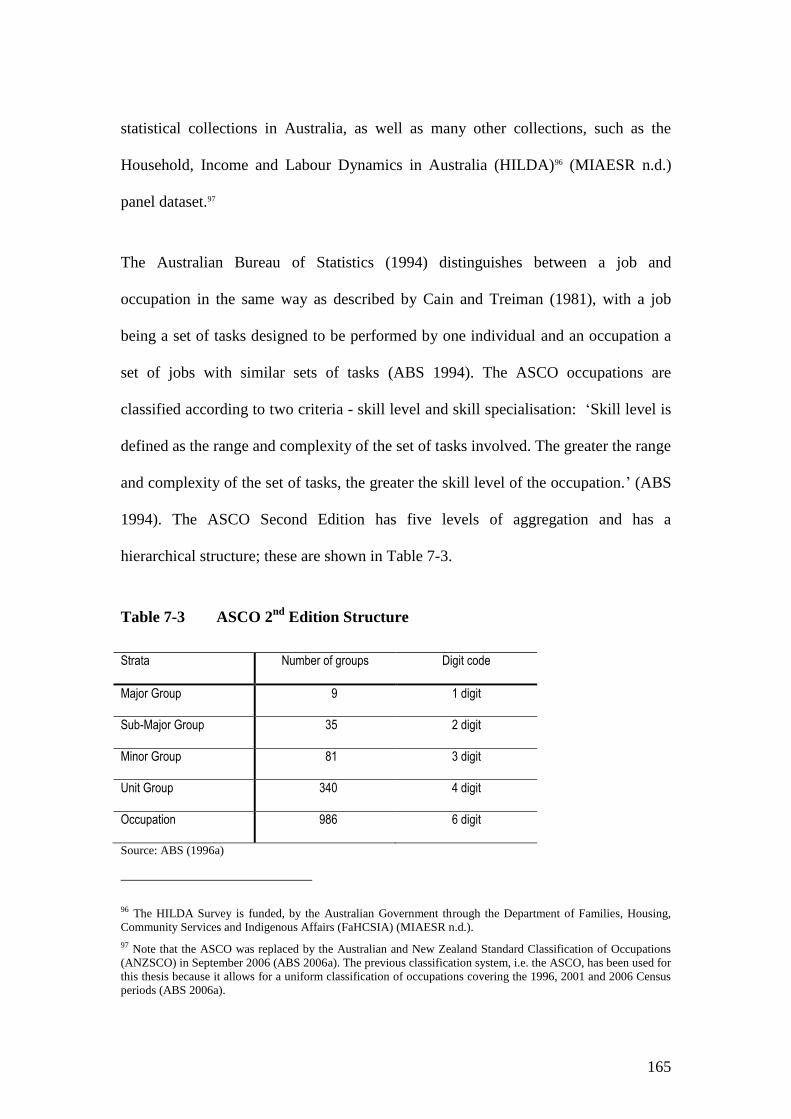

structural change and demand for skills in … · structural change and demand for skills in the...

TRANSCRIPT

STRUCTURAL CHANGE AND DEMAND

FOR SKILLS IN THE AUSTRALIAN

ECONOMY

A thesis submitted for the degree of Doctor of Philosophy

The University of Canberra

by

Ross Kelly

JUNE 2010

i

This thesis is the copyright © of Ross Kelly 2010.

ii

ABSTRACT

This thesis examines the effect that structural change and, in particular, information and

communication technologies (ICT) have had on skill demand, with the focus being on the

structure of skills in the economy and the way skills are defined and measured. A novel

approach to skill measurement is developed and used to determine the average skill level for

four skill dimensions: cognitive, education, interactive and motor skills. Shift-share analysis

covering between-industry and within-industry changes is undertaken for the period 1991 to

2006 using Census data. This is complemented by regression analysis to examine the

determinants of within-industry skill change. The thesis examines both the causes of change

and the distribution of change. That is, how skill changes have been distributed in terms of

industry, occupation, location and gender.

The main finding supports the central hypothesis of this thesis. That is, that there have been

significant changes to the composition of skills in the economy and that these changes were

substantially, but not solely, a result of technological change. Regression analyses were

undertaken for the various skill dimensions – cognitive, education, interactive and motor –

and provided further support to a vast body of international literature that ICT have been a

critical driver of skill change.

iii

Certificate of Authorship of Thesis

Except where clearly acknowledged in footnotes, quotations and the bibliography, I certify that I am

the sole author of the thesis submitted today entitled –

STRUCTURAL CHANGE AND DEMAND FOR SKILLS IN THE AUSTRALIAN ECONOMY

I further certify that to the best of my knowledge the thesis contains no material previously published

or written by another person except where due reference is made in the text of the thesis.

The material in the thesis has not been the basis of an award of any other degree or diploma except

where due reference is made in the text of the thesis.

The thesis complies with University requirements for a thesis as set out in Gold Book

Part 7: Examination of Higher Degree by Research Theses Policy, Schedule Two (S2).

Signature of Candidate

..........................................................................

Signature of chair of the supervisory panel

Date: ……………………………..

iv

ACKNOWLEDGEMENTS

I would like to express my gratitude to my supervisor, Professor Phil Lewis, for his excellent

supervision, encouragement, generosity and friendship. I am also indebted to Carrie, Hannah,

Jesse, Ruby and my parents for their enduring support, understanding and patience.

This thesis has benefited from professional editorial assistance for ‘Completeness and

Consistency’ adopted from the Australian Standards for Editing Practice (ASEP) in

accordance with the University Research Committee of the University of Canberra. I would

like to thank Lulu Turner from the University of Canberra for undertaking this task.

v

LIST OF ACRONYMS AND ABBREVIATIONS

ABS Australian Bureau of Statistics

ACCC Australian Consumer and Competition Commission

ACT Australian Capital Territory

ANZSCO Australian and New Zealand Standard Classification of Occupations

ANZSIC Australian and New Zealand Standard Industrial Classification

AQF Australian Qualifications Framework

ASCO Australian Standard Classification of Occupations

ASIC Australian Standard Industrial Classification

ATM Automatic Teller Machines

ATS Australian Traineeship System

B2B Business-to-Business

BIE Bounded Influence Estimates

BLMR Bureau of Labour Market Research

CBA Commonwealth Bank of Australia

CCLO Classification and Classified List of Occupations

CGT Capital Gains Tax

CPS Current Population Surveys

CR Concentration Ratio

DBCDE Department of Broadband, Communications and the Digital Economy

DCITA Department of Communications, Information Technology and the Arts

DIST Department of Industry, Science and Technology

DIW Deutsches Institut für Wirtschaftsforschung (German Institute for

Economic Research)

DOT Dictionary of Occupational Titles

vi

DVD Digital Video Disk

EDI Electronic Data Interchange Devices

EFTPOS Electronic Funds Transfer Point of Sale

EU European Union

FaHCSIA Department of Families, Housing, Community Services and Indigenous

Affairs

FWA Fair Work Australia

GDP Gross Domestic Product

GNP Gross National Product

GPS Global Positioning Systems

GSOEP German Socio-Economic Panel

GST Goods and Services Tax

GVA Gross Value Added

HECS Higher Education Contribution Scheme

HILDA Household, Income and Labour Dynamics in Australia

Kbs Kilobits per second

ICT Information and Communication Technology

IT Information Technology

ILO International Labor Organisation

IP Internet Protocol

IRC Industrial Relations Commission

ISCO International Standard Classification of Occupations

LTU Long-Term Unemployment

MIAESR Melbourne Institute of Applied Economic and Social Research

MIP-S Mannheim Innovation Panel in the Service Sector (survey)

vii

Mbs Megabits per second

NCVER National Centre for Vocational Education Research

NOIE National Office of the Information Economy

NSW New South Wales

NT Northern Territory

OBEC Oxford Business & Economics Conference

OECD Organisation for Economic Co-operation and Development

PC Productivity Commission

QLD Queensland

RBA Reserve Bank of Australia

R&D Research and Development

RULC Real Unit Labour Costs

SA South Australia

SBTC Skill-Biased Technological Change

SPIRT Strategic Partnerships with Industry- Research and Training Scheme

ST Stolper-Samuelson Theorem

TAFE Technical and Further Education

TAS Tasmania

TCFL Textile, Clothing, Footwear and Leather

TFP Total Factor Productivity

UK United Kingdom

US United States (of America)

USDOL United States Department of Labor

USO Universal Service Obligation

VET Vocational Education and Training

viii

VoIP Voice over Internet Protocol

WA Western Australia

WRA Workplace Relations Act (1996)

ix

CONTENTS

Abstract ii

Certificate of Authorship of Thesis iii

Acknowledgements iv

List of Acronyms and Abbreviations v

List of Tables xiii

List of Figures xv

1 INTRODUCTION 1

1.1 Change in the Australian Labour Market 2

1.2 Skills in the Australian Economy 3

1.3 Influence of ICT on Skill Change in Australia 4

1.4 Overview of Thesis 4

2 INFORMATION AND COMMUNICATION TECHNOLOGIES (ICT) AND THE

ECONOMY 7

2.1 Introduction 7

2.2 Growth of the Internet 8

2.2.1 Increase in Internet speeds 9

2.3 Household Access to the Internet 10

2.3.1 Current access levels in Australia 14 2.3.2 International comparison of broadband access 21

2.4 The Economics of eCommerce 22

2.4.1 eCommerce defined 22 2.4.2 Consumer behaviour 24 2.4.3 Contestability of markets 25 2.4.4 Market segmentation and consumer surplus 26 2.4.5 Transaction costs 27 2.4.6 Business-to-business (B2B) transactions 31

2.5 Growth of eCommerce 32

2.5.1 Growth of eCommerce in Australia 34

2.6 Summary 37

3 EMPLOYERS’ EARLY EXPECTATIONS OF IMPACTS FROM ICT 39

3.1 Survey of Firms 39

3.2 Potential Changes from ICT and eCommerce 40

3.3 Changing Skills Composition and Training Needs of the Workforce 41

3.4 Information Technology Staff, Quality and Supply 43

3.5 Impact of eCommerce on the Organisation 43

3.6 Does eCommerce Pose a Threat? 46

3.6.1 eCommerce poses no threat 46 3.6.2 Poses a threat to core business 46 3.6.3 eCommerce is a threat if not adopted 47

3.7 Summary 48

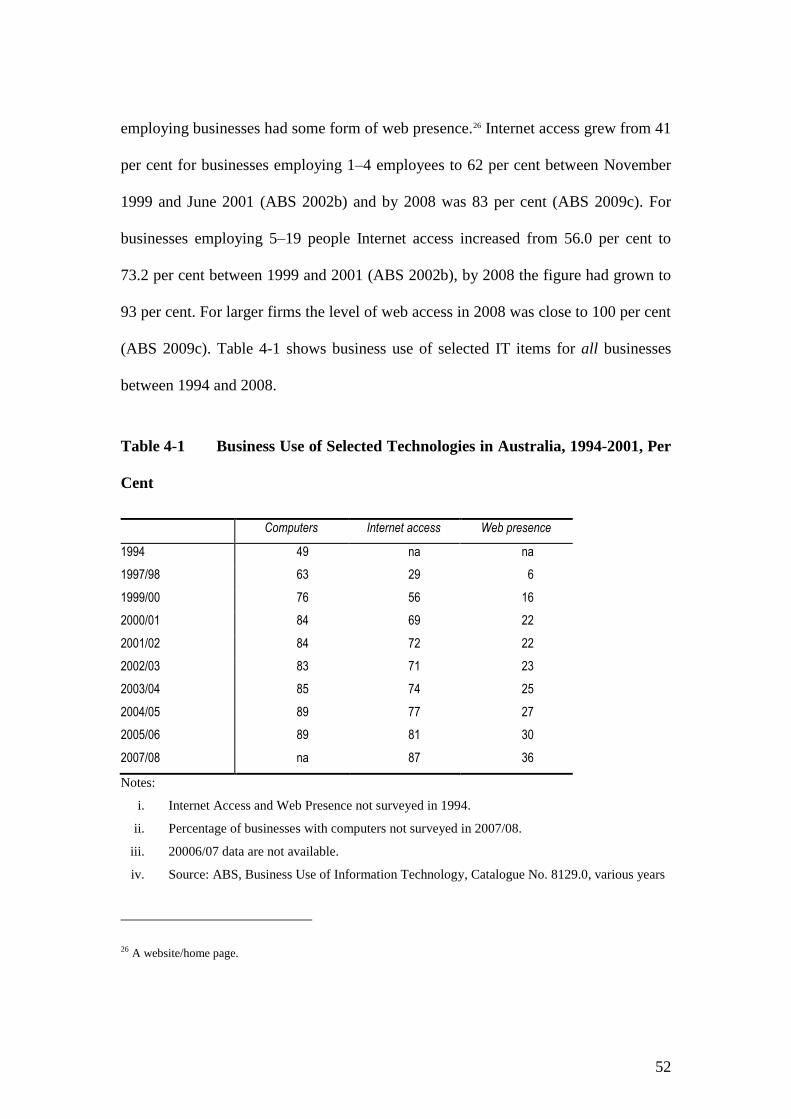

4 BUSINESS USE OF TECHNOLOGY 50

4.1 Overview 50

x

4.2 Computers in the Workplace, Network Access and Internet Usage 51

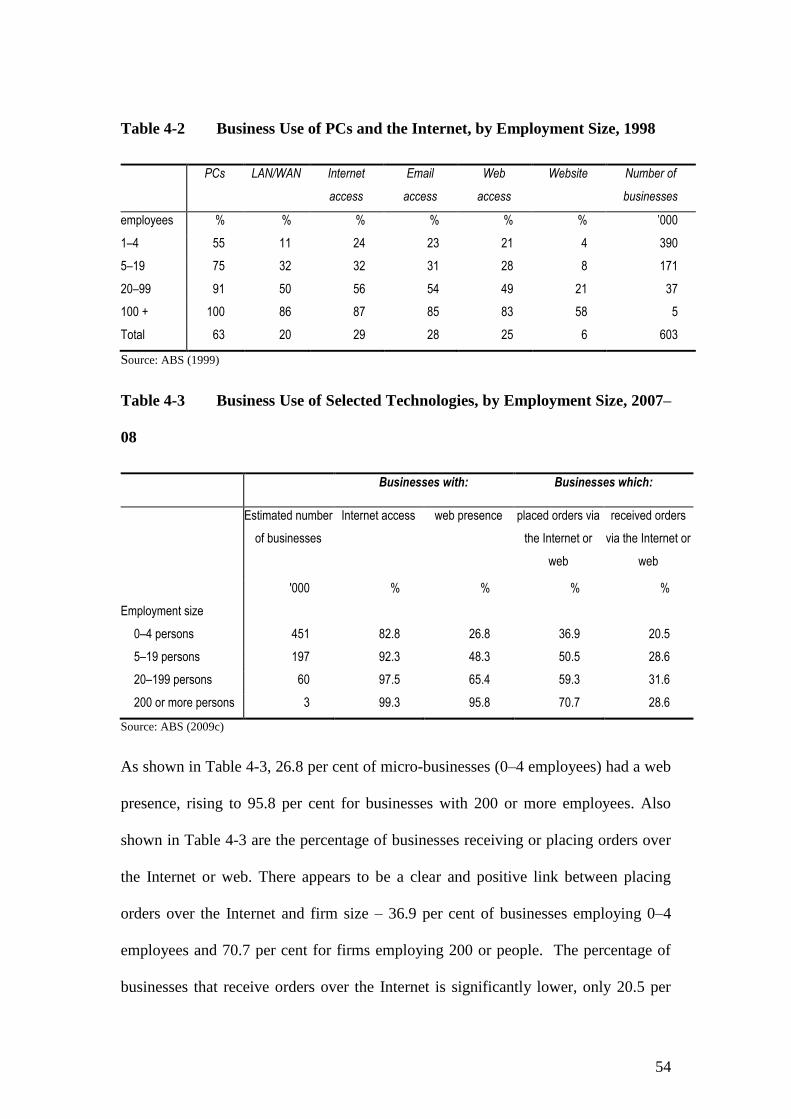

4.3 Application of the Internet by Businesses 53

4.4 Business Investment in ICT 57

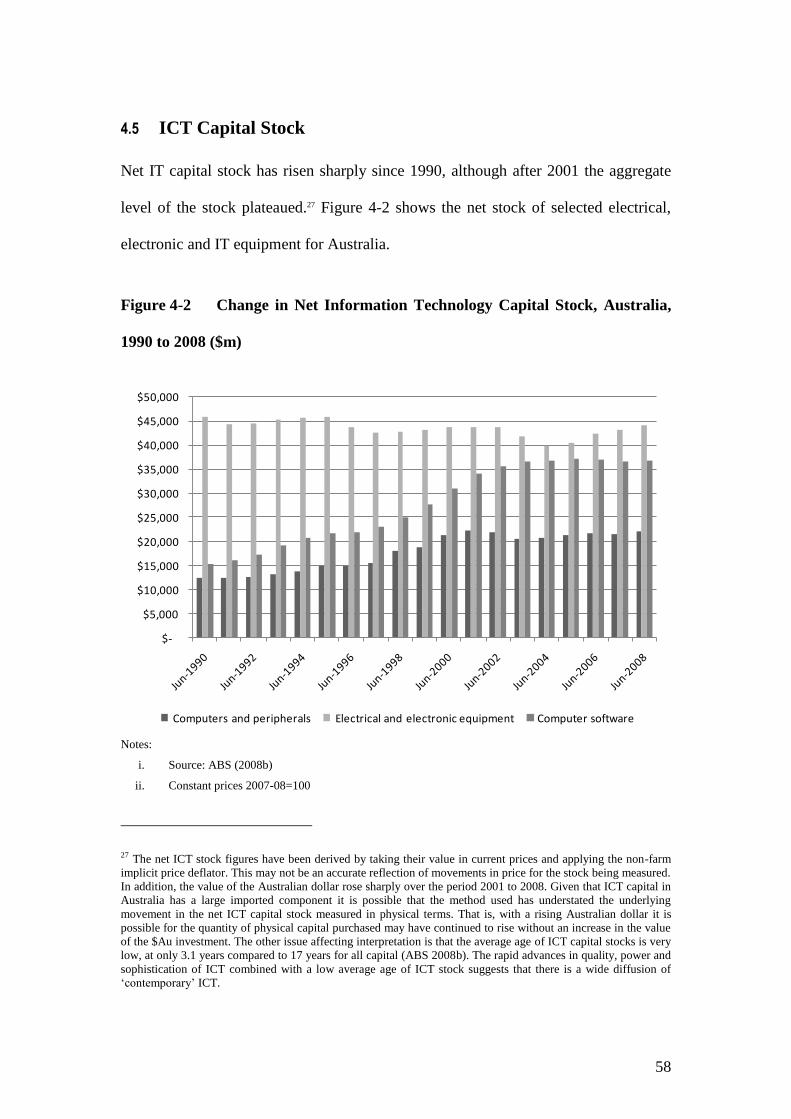

4.5 ICT Capital Stock 58

4.6 Examples of Investment in ICT by Firms 62

4.7 Summary 65

5 THE AUSTRALIAN LABOUR MARKET 66

5.1 Overview 66

5.2 Microeconomic Reform 68

5.2.1 Impact of microeconomic reform on the labour market 70

5.3 Industrial Relations 71

5.3.1 Unions, industrial relations and wage setting 73 5.3.2 Labour market flexibility, productivity & structural adjustment 74

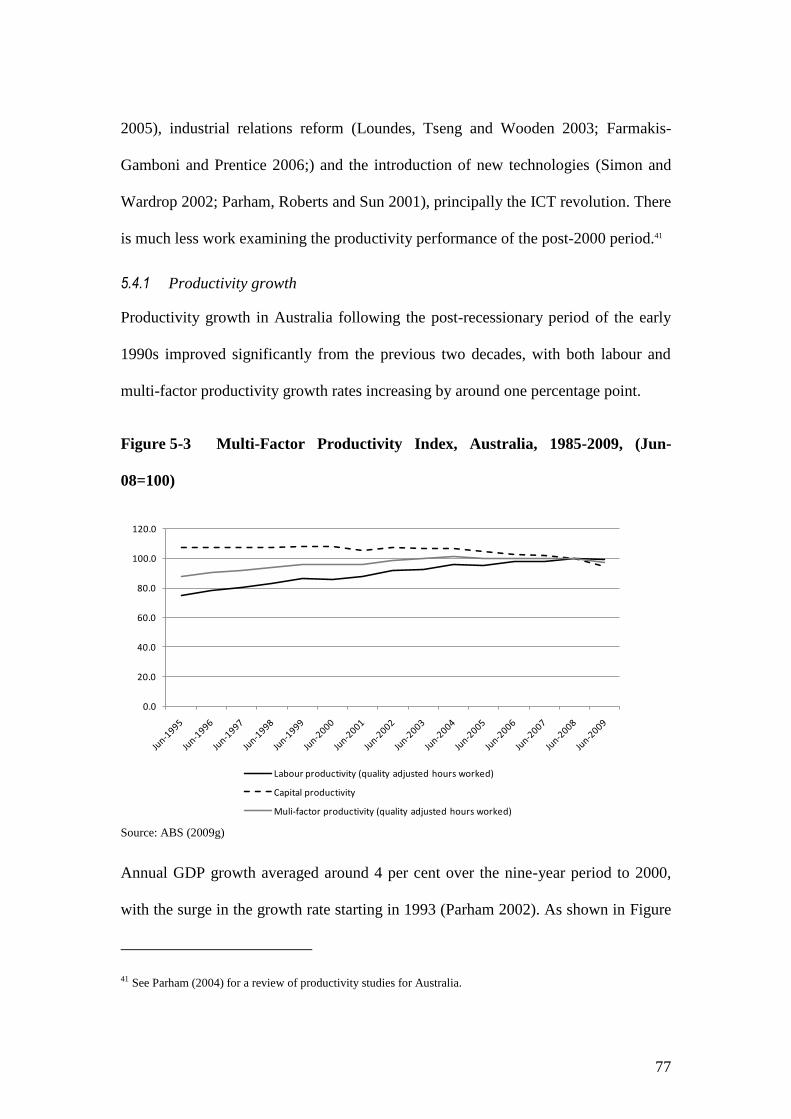

5.4 Productivity 76

5.4.1 Productivity growth 77 5.4.2 Real Unit Labour Cost 79

5.5 Education & Training 81

5.5.1 Human capital & the economy 81 5.5.2 High school retention 81 5.5.3 Vocational education and training (VET) 83 5.5.4 Apprentices 84 5.5.5 Higher education 87

5.6 Labour Force Participation, Employment and Unemployment 88

5.6.1 Labour force participation 88 5.6.2 Full-time and part-time employment 89 5.6.3 Disadvantaged groups 91 5.6.4 Long-term unemployment, mature-age unemployment 94

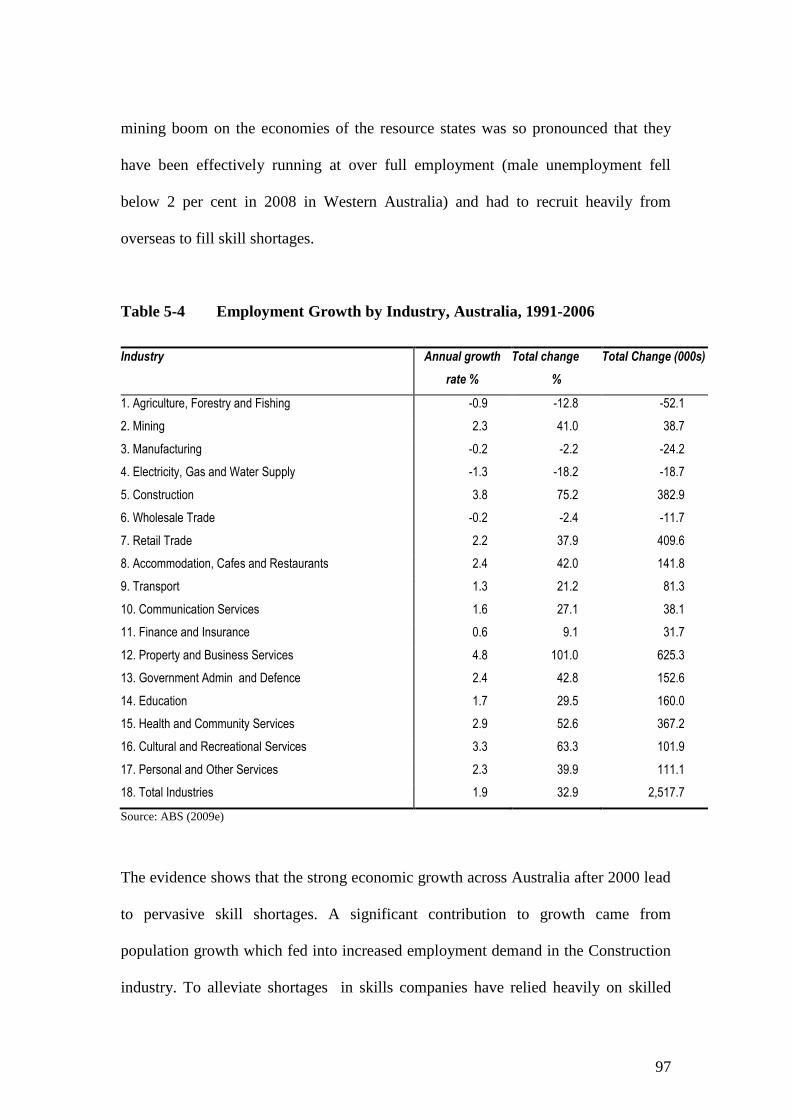

5.7 Employment Growth in the Australian Economy 95

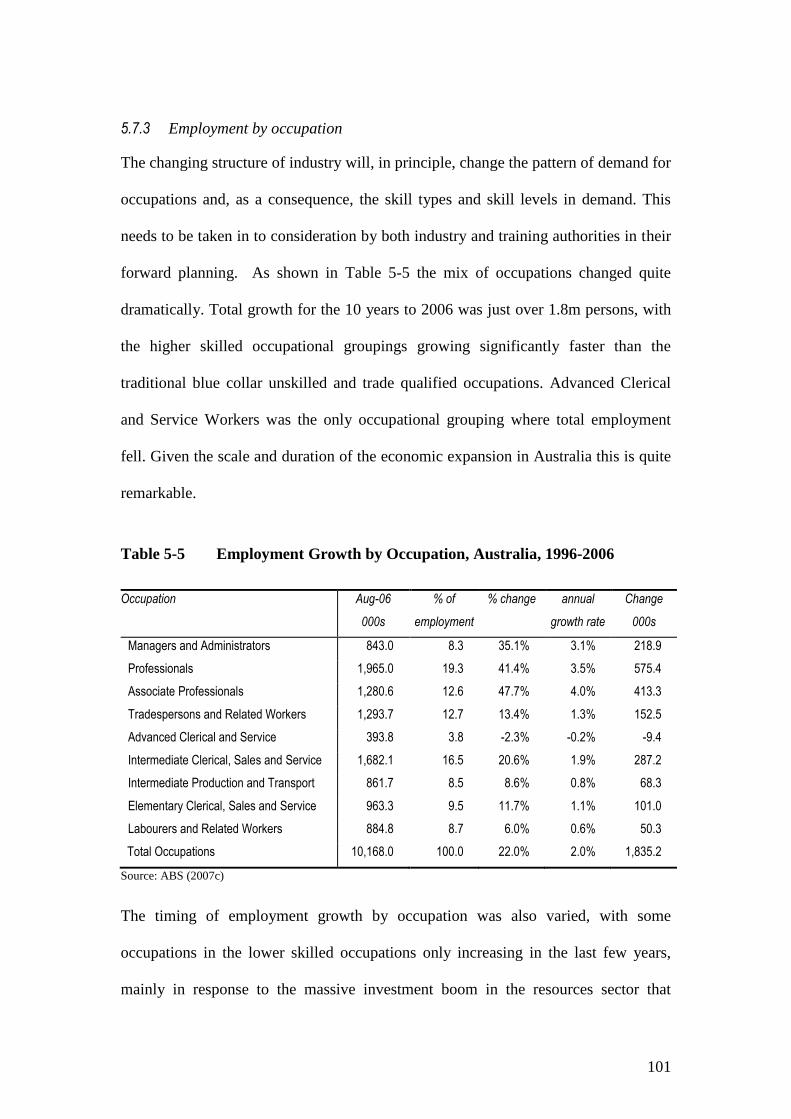

5.7.1 Overview 95 5.7.2 Employment by industry 96 5.7.3 Employment by occupation 101

5.8 Summary 104

6 SKILL BIASED TECHNOLOGICAL CHANGE 106

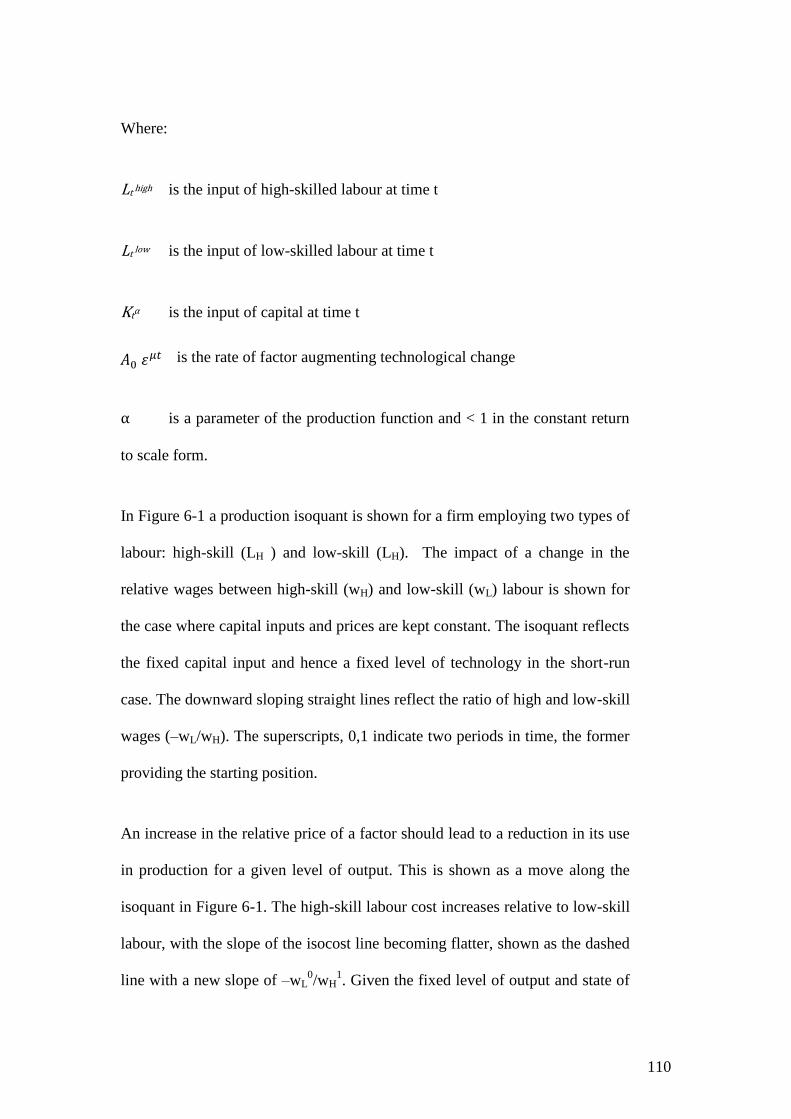

6.1 Overview 106

6.2 Skill Biased Technological Change (SBTC) Hypothesis 108

6.3 Evidence of SBTC 113

6.3.1 Firm level studies 114 6.3.2 Industry cross-section approaches 121 6.3.3 Cross country studies 126 6.3.4 Australian Studies 131

6.4 Critique of SBTC 141

6.4.1 Critique of ICT linkages to skill change 141 6.4.2 Organisational and institutional change 143 6.4.3 Trade hypothesis and the structure of trade 146

6.5 Summary 150

7 MEASUREMENT OF TECHNOLOGY AND SKILLS 155

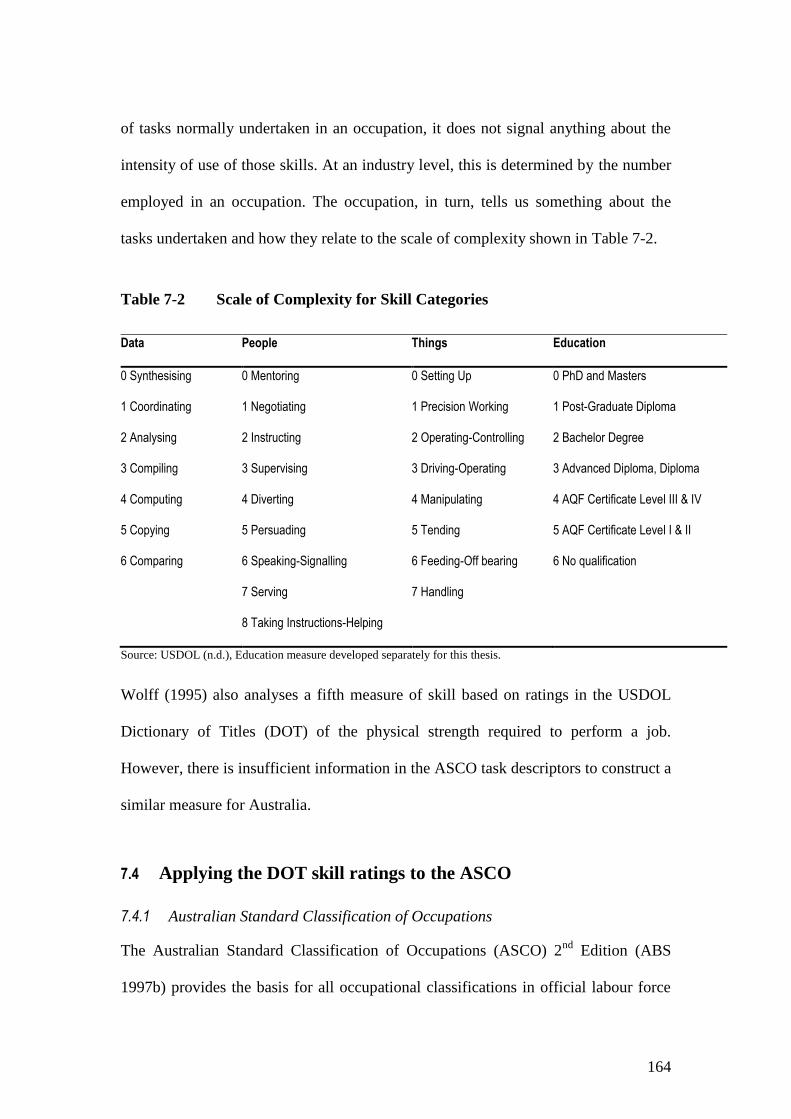

7.1 Measurement of Technology 155

7.2 Measurement of Skills 156

7.2.1 Defining skill 156

xi

7.2.2 Definitions and measures used in SBTC studies 157

7.3 US Department of Labor’s Dictionary of Occupational Titles (DOT) 162

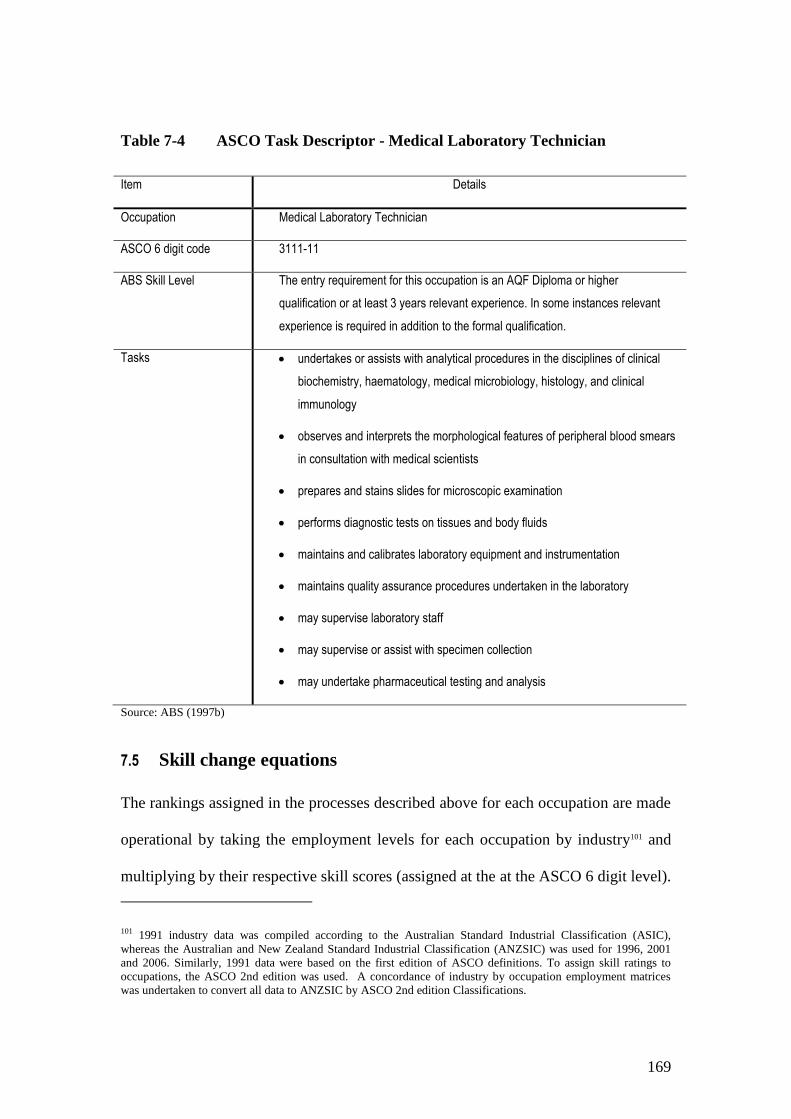

7.4 Applying the DOT skill ratings to the ASCO 164

7.4.1 Australian Standard Classification of Occupations 164 7.4.2 Rating skills 166

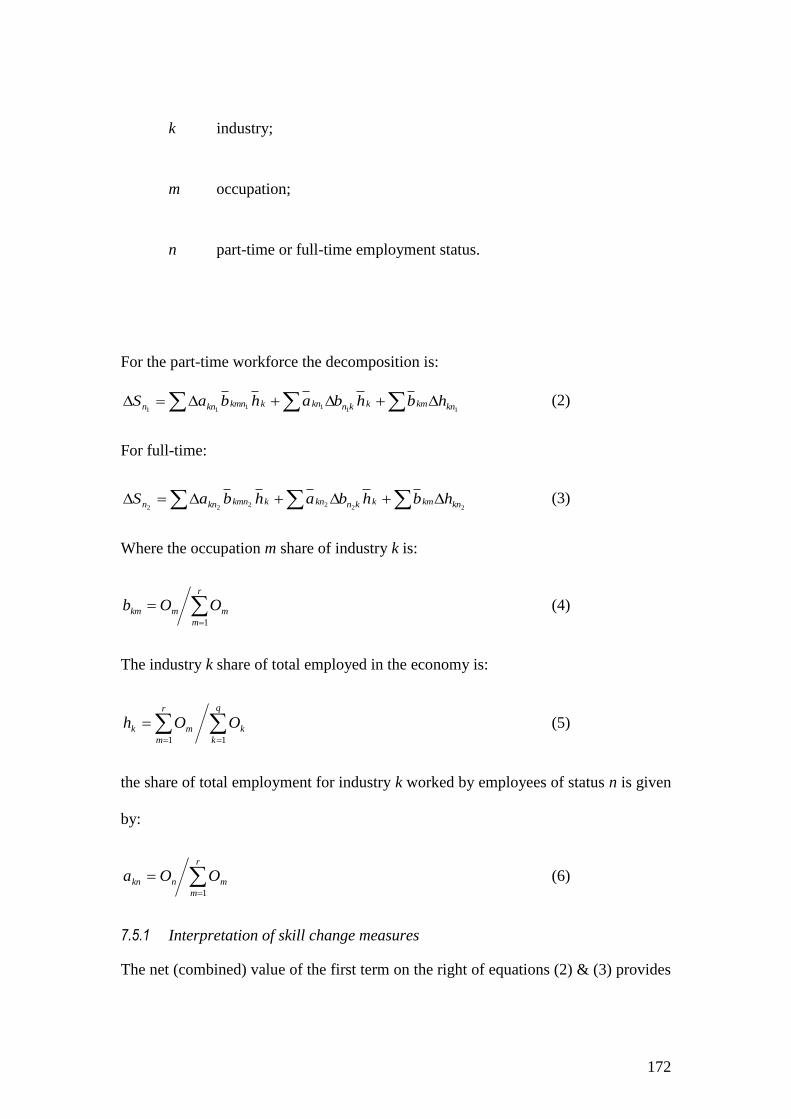

7.5 Skill change equations 169

7.5.1 Interpretation of skill change measures 172

7.6 Summary 173

8 CHANGES IN SKILL DEMAND 175

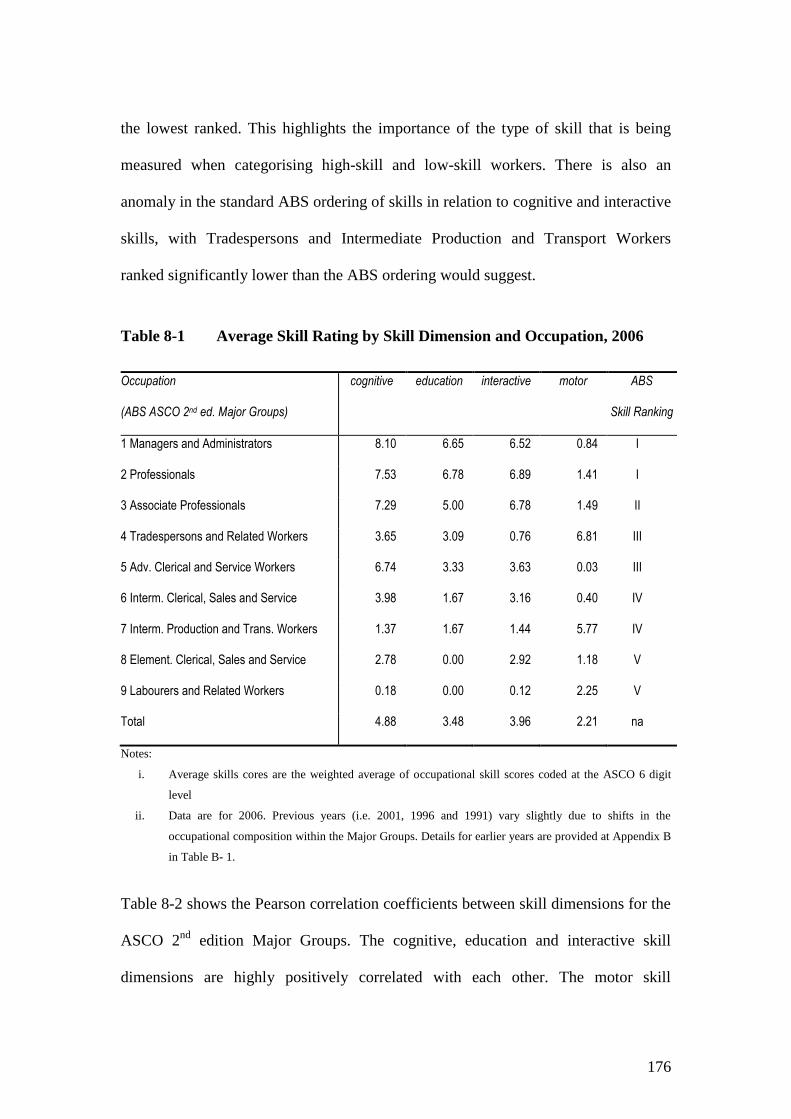

8.1 Occupational Skill Rankings 175

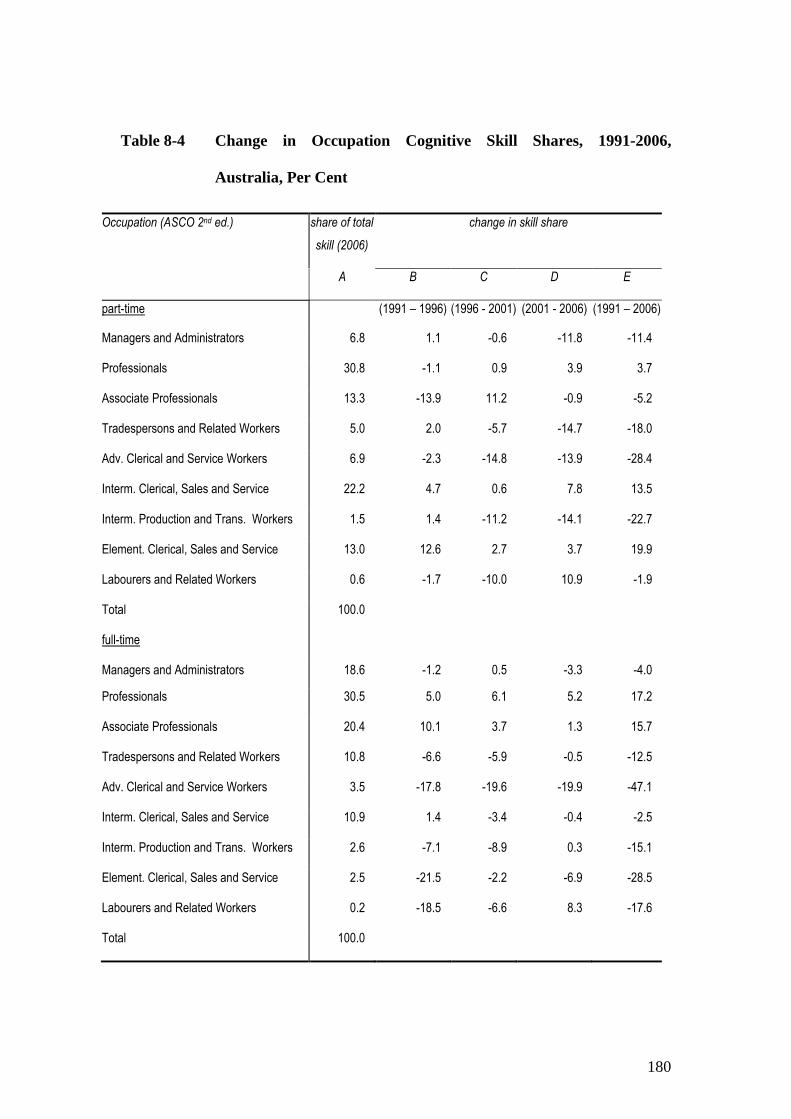

8.1.1 Occupational skill shares 178

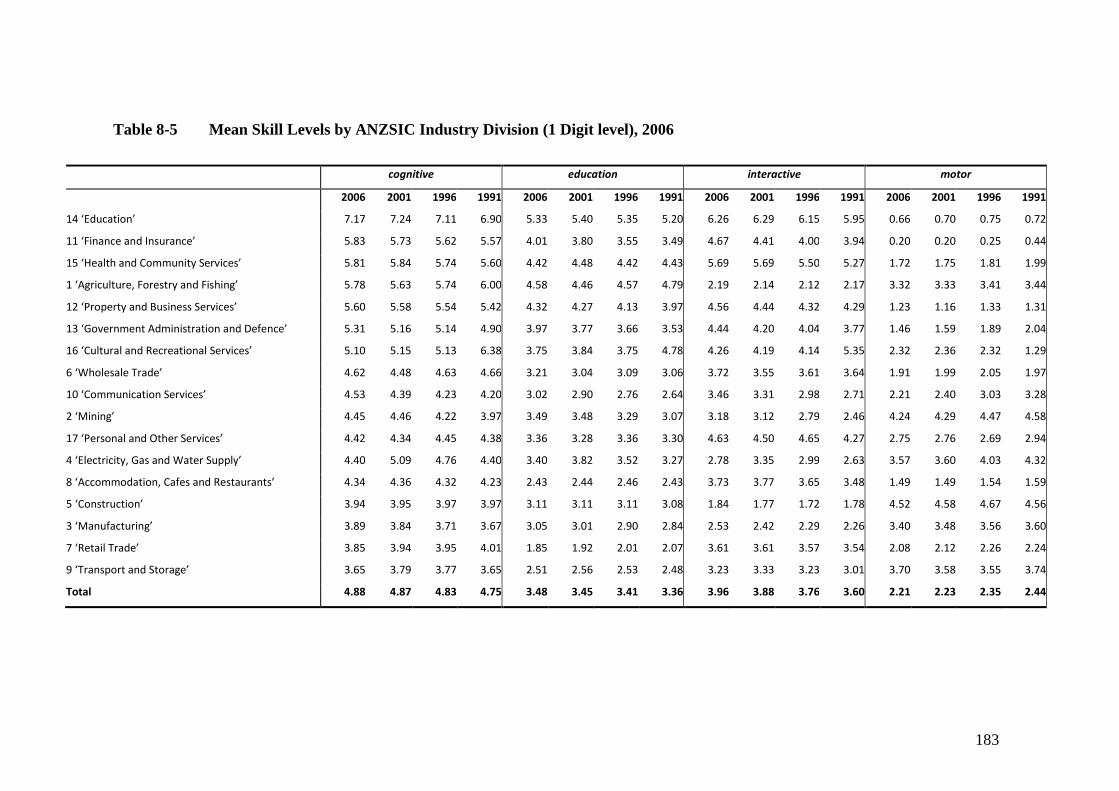

8.2 Industry Skill Structure 182

8.3 Skill Change 185

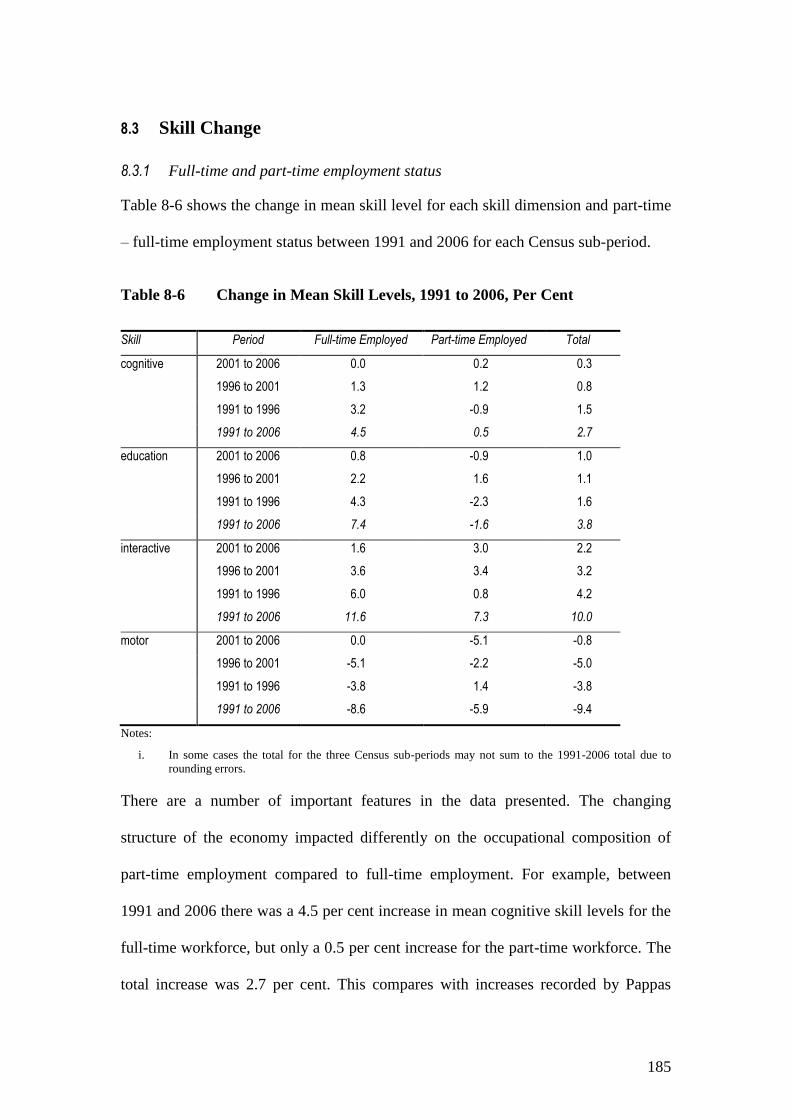

8.3.1 Full-time and part-time employment status 185

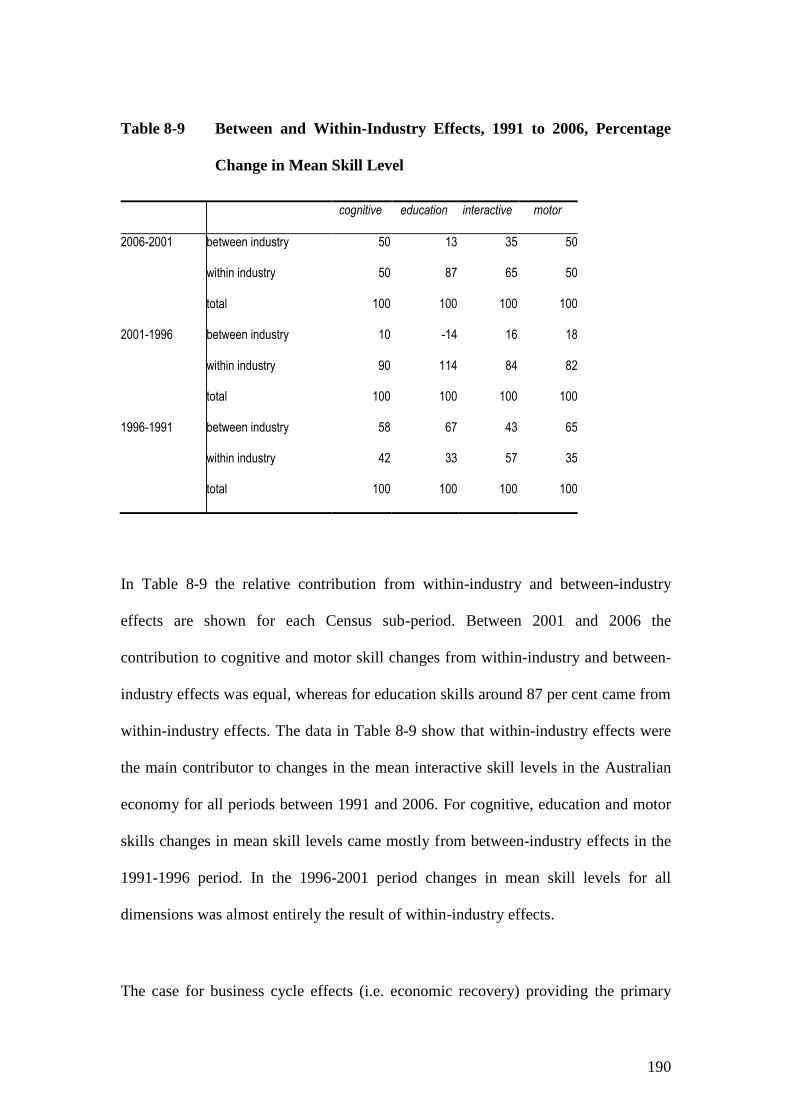

8.4 Shift-Share Analysis 188

8.4.1 Changes over time 188 8.4.2 Within- and between-industry effects 189 8.4.3 Industry structure of skill change 191

8.5 Distribution of skill change 195

8.5.1 Region 195 8.5.2 Gender 198

8.6 Summary of findings 201

8.6.1 Summary of industry changes 201

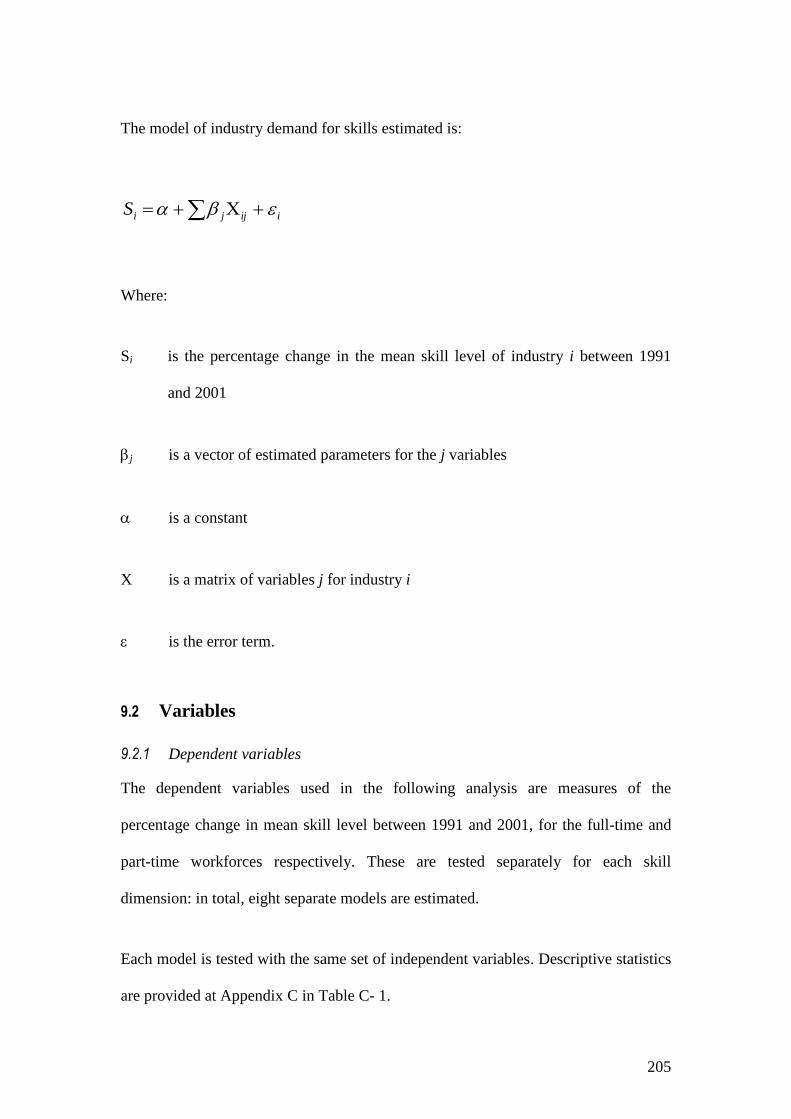

9 DETERMINANTS OF SKILL CHANGE IN AUSTRALIA 204

9.1 Model of Skill Change 204

9.2 Variables 205

9.2.1 Dependent variables 205 9.2.2 Independent variables 206

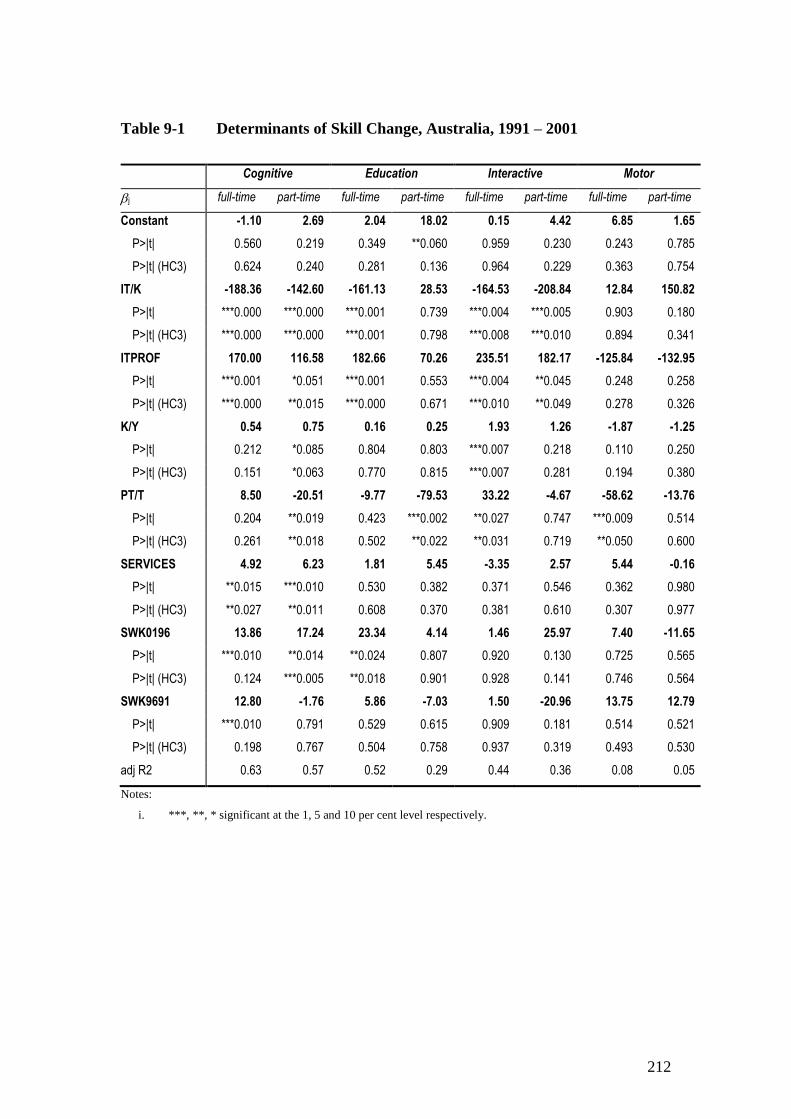

9.3 Results 209

9.4 Summary 216

10 CONCLUSION 219

10.1 Main findings 220

10.1.1 Diffusion of ICT 220 10.1.2 The Australian labour market 222 10.1.3 Previous research into Australian skill change 223 10.1.4 Skill definition and measurement 223 10.1.5 Shift-share analysis 224 10.1.6 Determinants of skill change 225

10.2 Implications 225

10.2.1 Further ICT development – how much left to go? 225 10.2.2 Groups at risk 226 10.2.3 Gender earnings differentials 227

10.3 Policy Response 228

10.3.1 Labour market flexibility 228 10.3.2 Training market responsiveness 229

10.4 Future Research 231

10.4.1 Investment in education and returns to skill 231 10.4.2 Gender 231 10.4.3 Jobs and regions at risk 232

xii

10.5 Conclusion 232

11 REFERENCES 233

12 APPENDIX A 252

13 APPENDIX B 255

14 APPENDIX C 259

xiii

LIST OF TABLES

Table 2-1 World Internet Usage and Population by Region, June 2009 ............................................................................. 8

Table 2-2 Internet Access Statistics for Australia, 1998 to 2007-08 ................................................................................ 15

Table 2-3 Computer and Internet Access by Household Equivalised Income, Australia, 2007-08 .................................. 16

Table 2-4 Impact of Income on Computer and Internet Access Rates, Australia, 2007-08 .............................................. 17

Table 2-5 Annual Equivalised Income, Australia, 2007-08, ($A, current prices) ............................................................. 20

Table 2-6 Income Elasticity of Demand for Selected Household ICT, Australia, 2007-08 .............................................. 21

Table 2-7 Information Product Versioning Enabled by the Internet ................................................................................. 27

Table 2-8 Customers Accessing Banking Services by Medium, Canada, 1999 to 2006, Per Cent ................................... 33

Table 2-9 Share of Banking Transactions by Access Medium, Canada, 1999 to 2006, Per Cent ..................................... 34

Table 2-10 Number of Banks and Credit Unions Offering On-Line Services .................................................................... 34

Table 4-1 Business Use of Selected Technologies in Australia, 1994-2001, Per Cent ..................................................... 52

Table 4-2 Business Use of PCs and the Internet, by Employment Size, 1998 .................................................................. 54

Table 4-3 Business Use of Selected Technologies, by Employment Size, 2007–08 ........................................................ 54

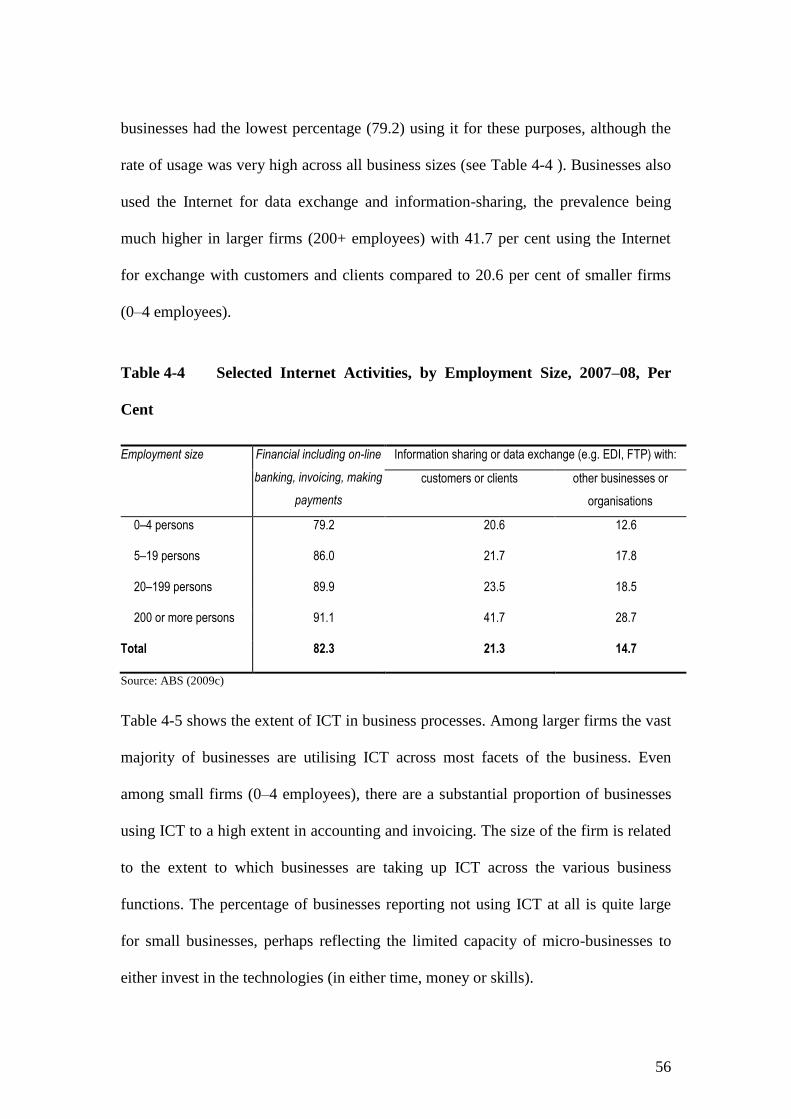

Table 4-4 Selected Internet Activities, by Employment Size, 2007–08, Per Cent ............................................................ 56

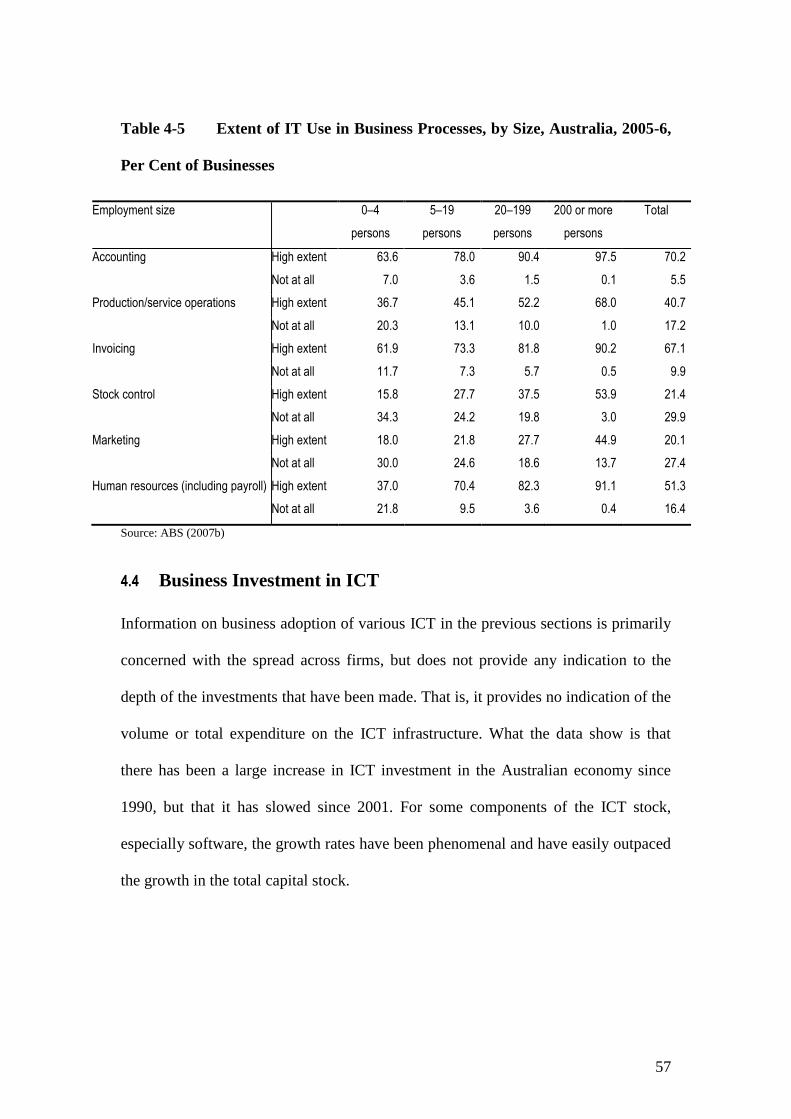

Table 4-5 Extent of IT Use in Business Processes, by Size, Australia, 2005-6, Per Cent of Businesses .......................... 57

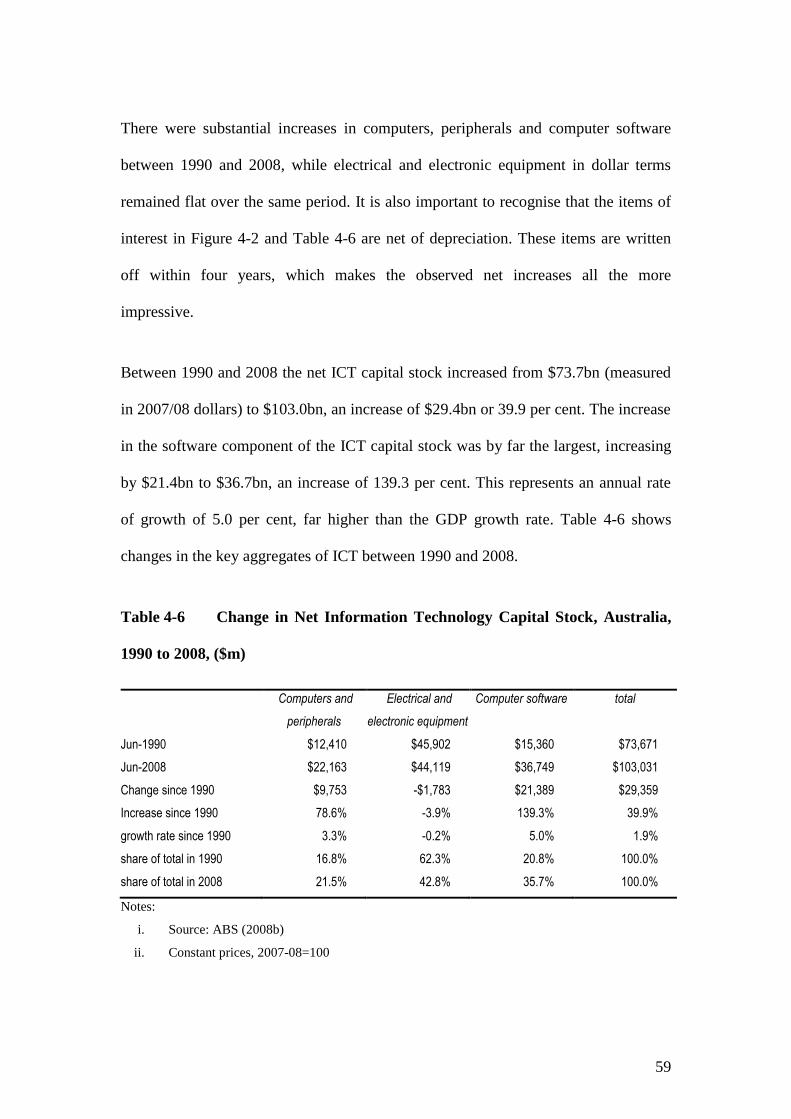

Table 4-6 Change in Net Information Technology Capital Stock, Australia, 1990 to 2008, ($m) .................................... 59

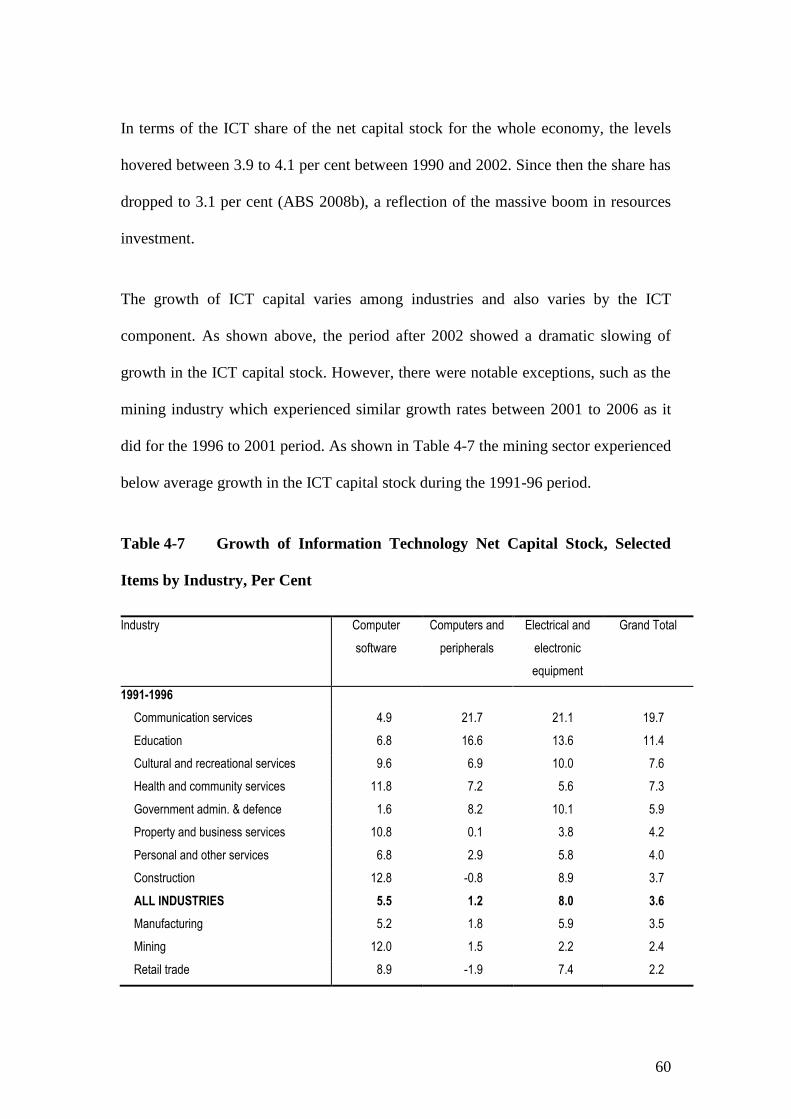

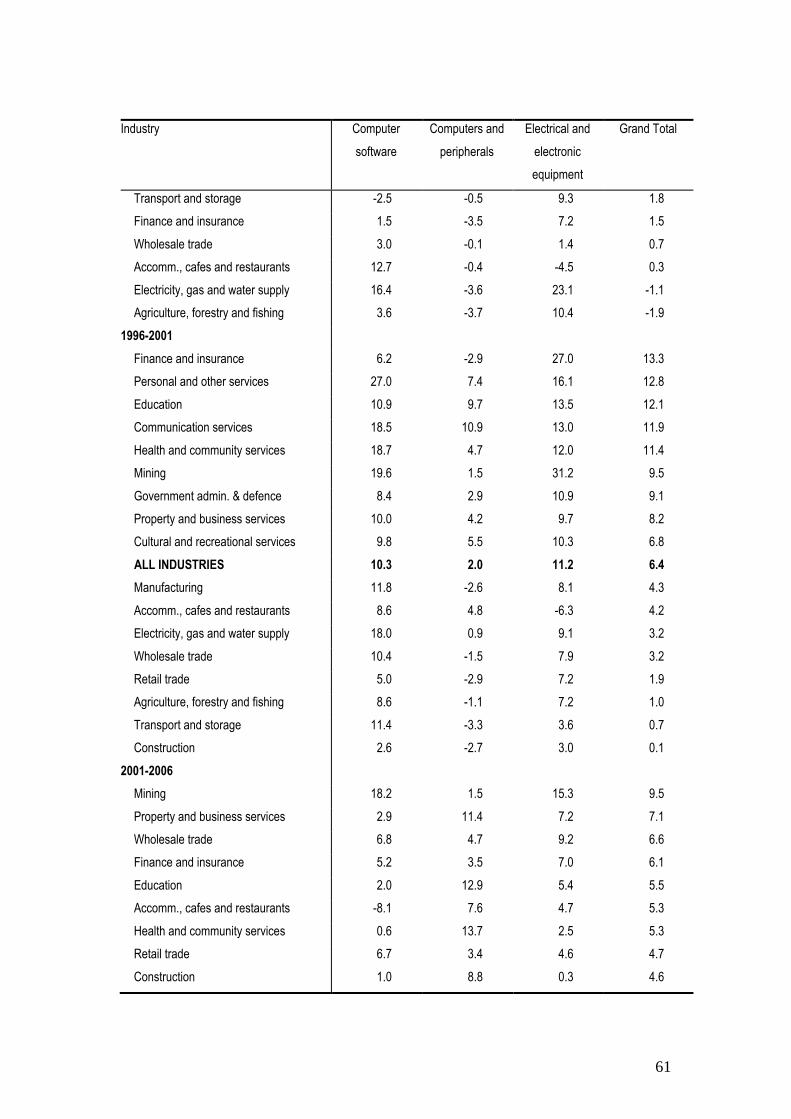

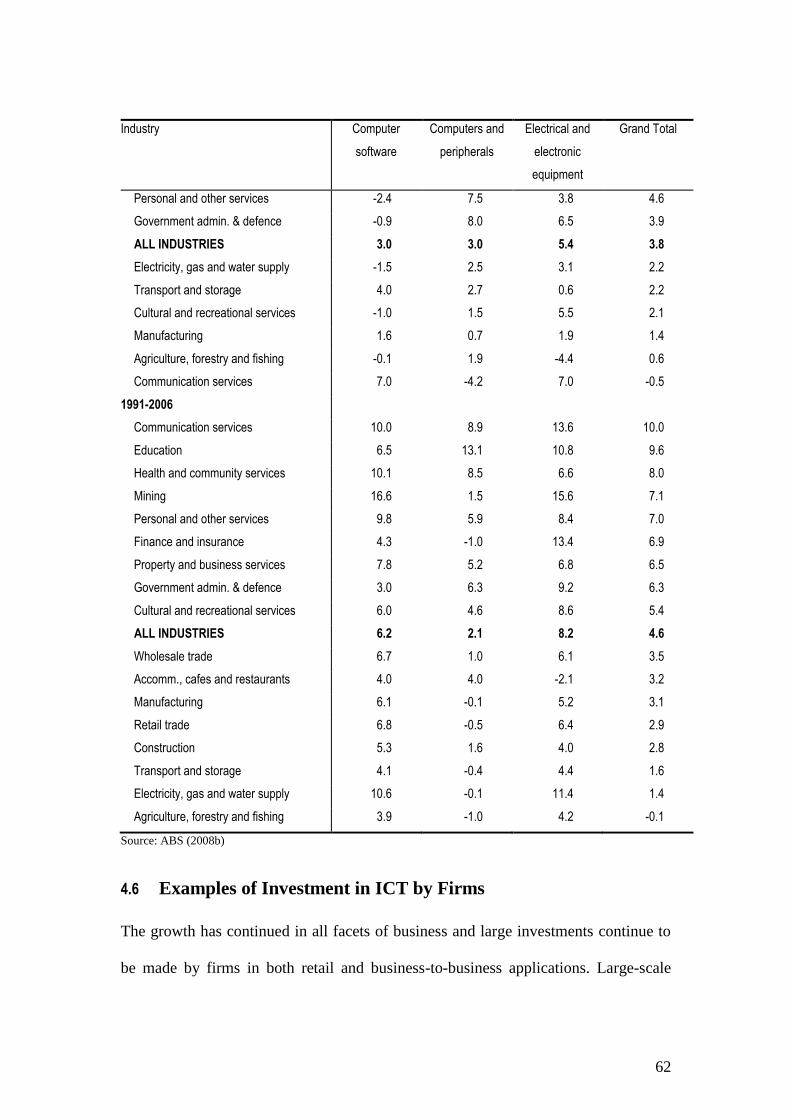

Table 4-7 Growth of Information Technology Net Capital Stock, Selected Items by Industry, Per Cent ........................ 60

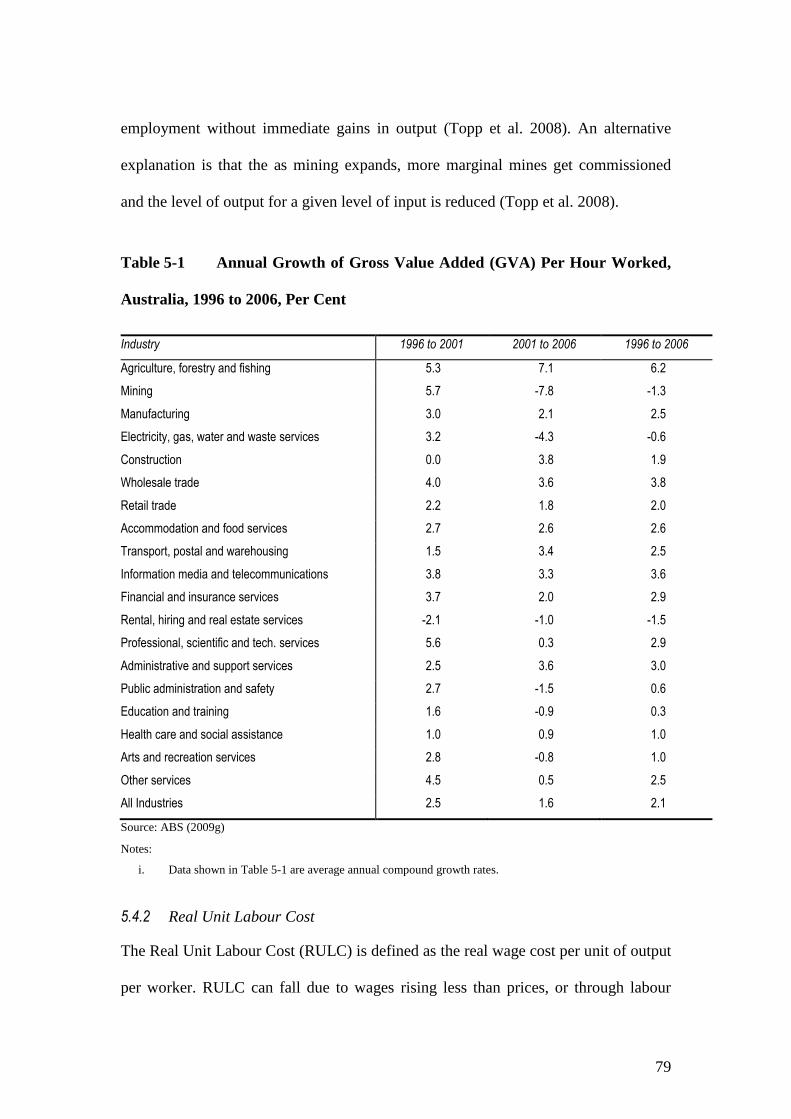

Table 5-1 Annual Growth of Gross Value Added (GVA) Per Hour Worked, Australia, 1996 to 2006, Per Cent ............ 79

Table 5-2 Graduate Completions in VET, 2000 to 2009, Australia, Persons, 000s .......................................................... 84

Table 5-3 Percentage of Working-Age Population with Bachelor Degree or Above, 1991 to 2006, Australia ................ 88

Table 5-4 Employment Growth by Industry, Australia, 1991-2006 ................................................................................. 97

Table 5-5 Employment Growth by Occupation, Australia, 1996-2006 .......................................................................... 101

Table 6-1 Harrod, Hicks and Solow Technological Change ........................................................................................... 109

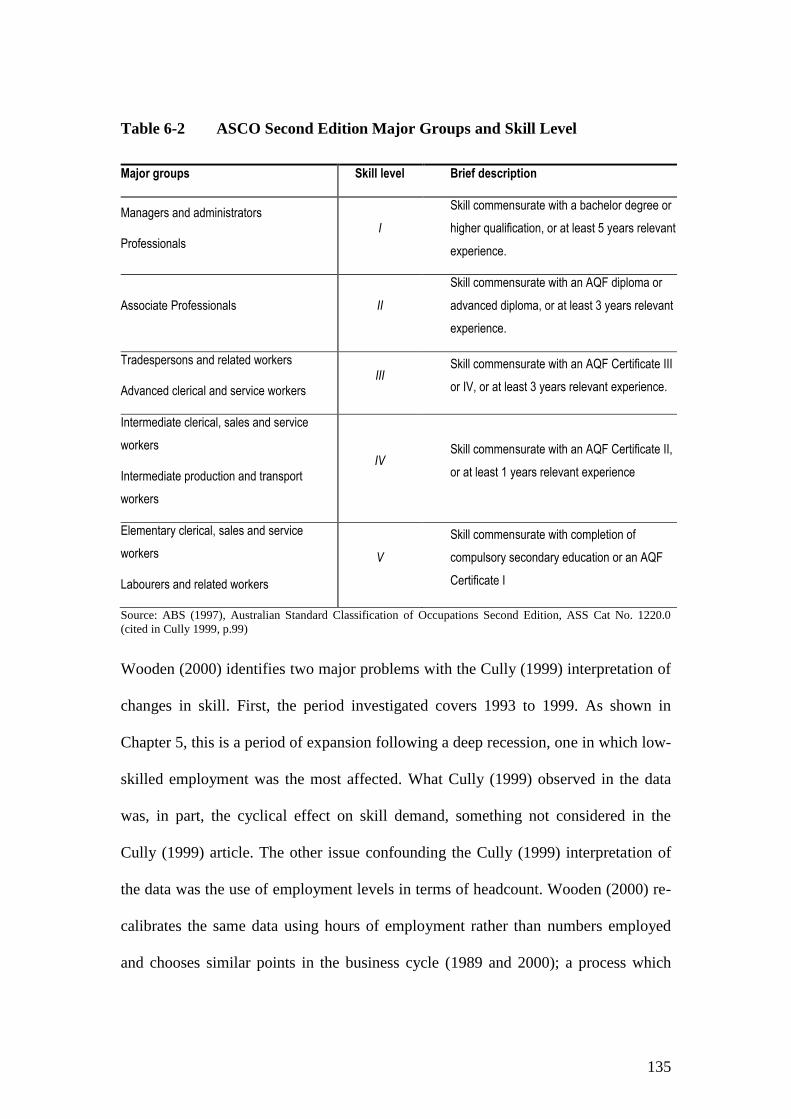

Table 6-2 ASCO Second Edition Major Groups and Skill Level ................................................................................... 135

Table 7-1 Four-Way Skill Grouping by Occupation ...................................................................................................... 159

Table 7-2 Scale of Complexity for Skill Categories ....................................................................................................... 164

Table 7-3 ASCO 2nd Edition Structure ........................................................................................................................... 165

Table 7-4 ASCO Task Descriptor - Medical Laboratory Technician ............................................................................. 169

Table 8-1 Average Skill Rating by Skill Dimension and Occupation, 2006 ................................................................... 176

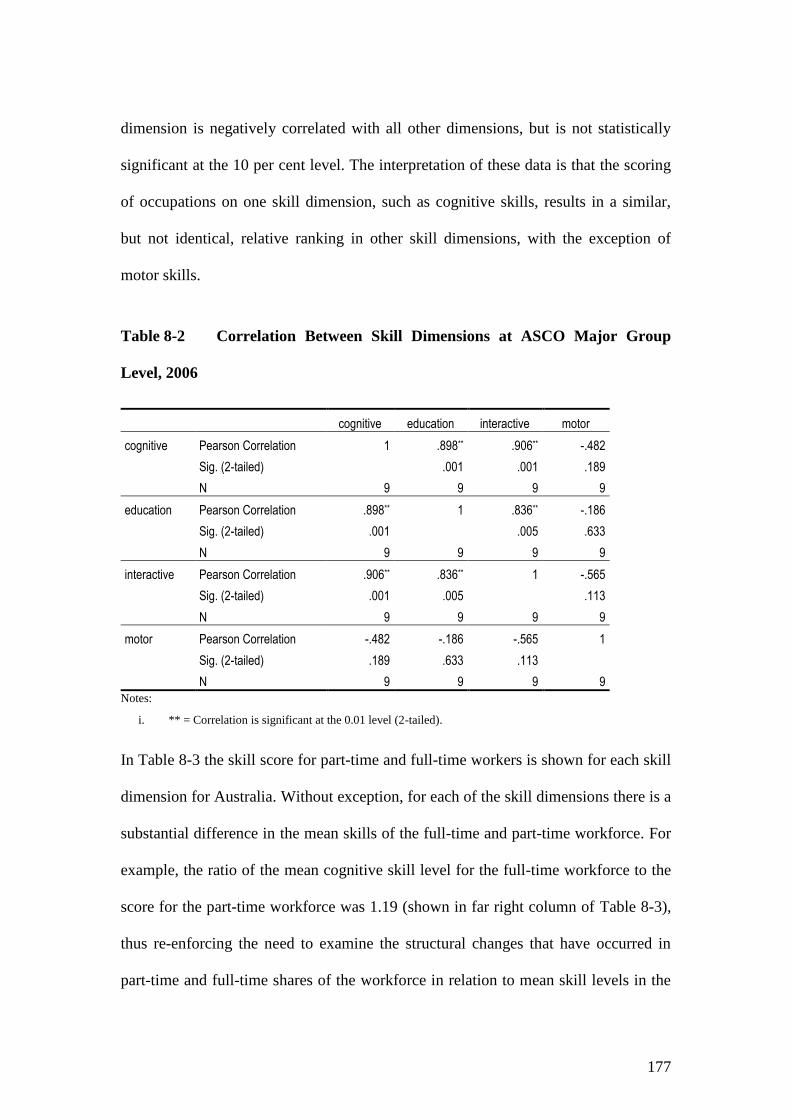

Table 8-2 Correlation Between Skill Dimensions at ASCO Major Group Level, 2006 ................................................. 177

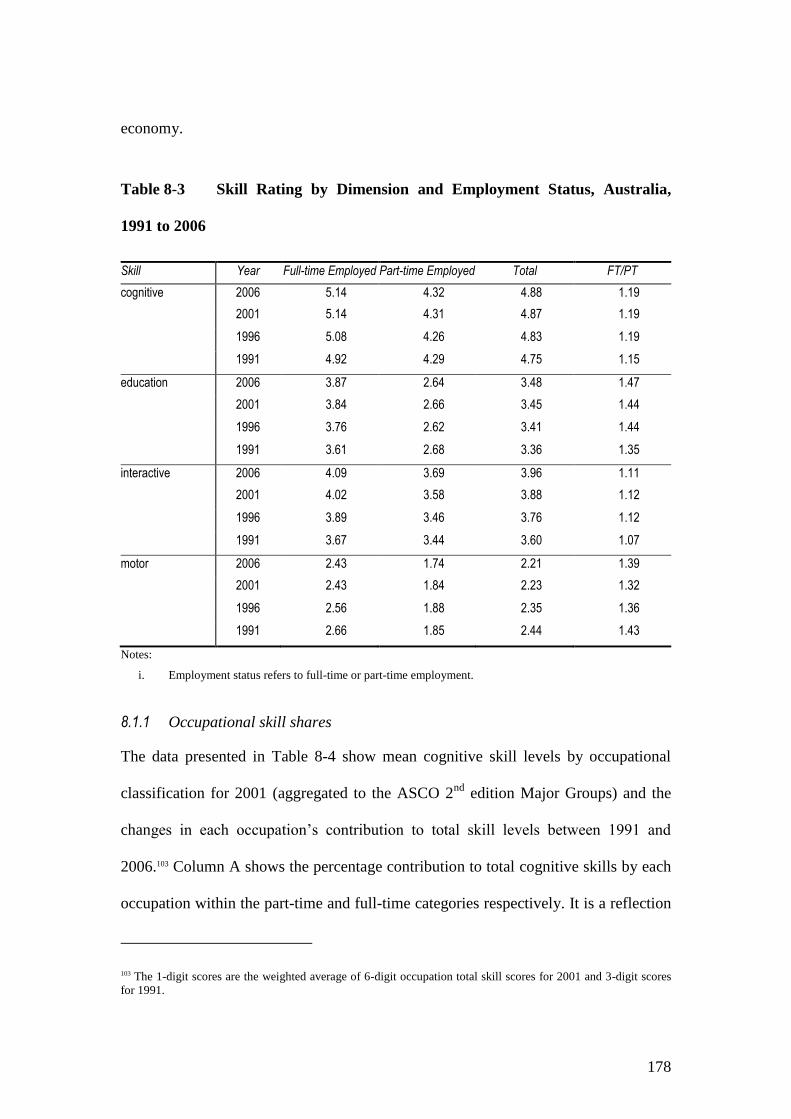

Table 8-3 Skill Rating by Dimension and Employment Status, Australia, 1991 to 2006 ............................................... 178

Table 8-4 Change in Occupation Cognitive Skill Shares, 1991-2006, Australia, Per Cent ............................................ 180

Table 8-5 Mean Skill Levels by ANZSIC Industry Division (1 Digit level), 2006 ........................................................ 183

Table 8-6 Change in Mean Skill Levels, 1991 to 2006, Per Cent ................................................................................... 185

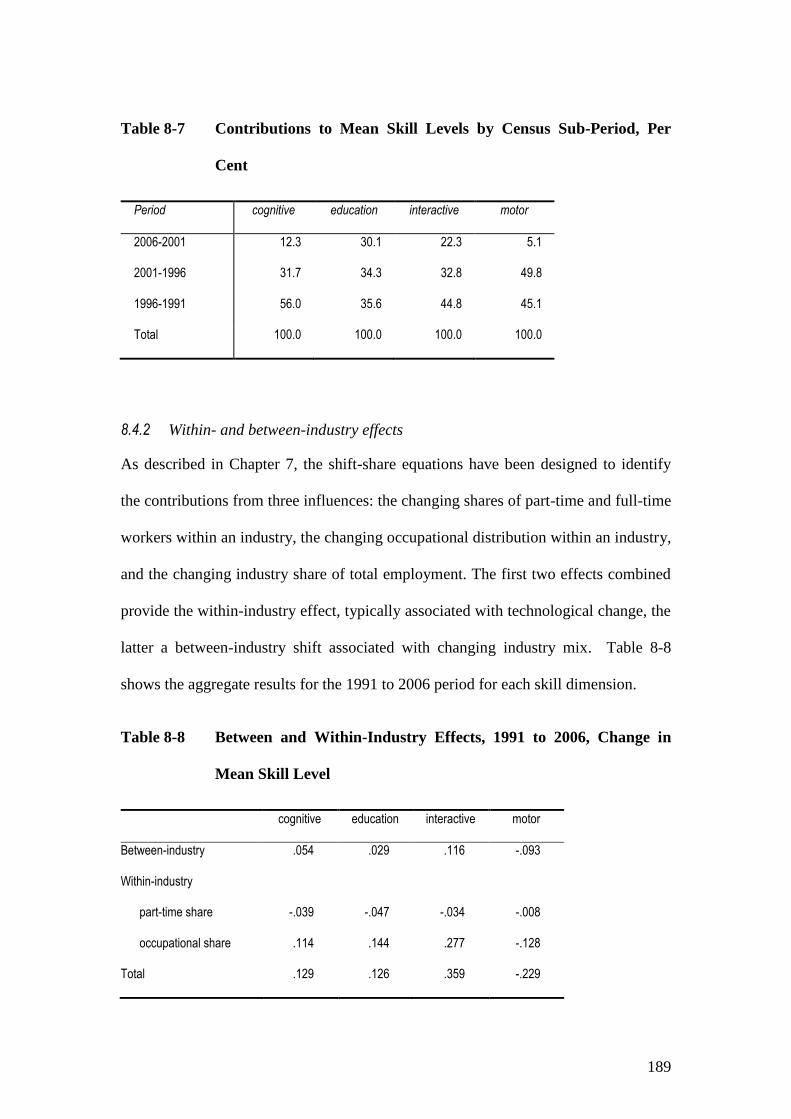

Table 8-7 Contributions to Mean Skill Levels by Census Sub-Period, Per Cent ............................................................ 189

Table 8-8 Between and Within-Industry Effects, 1991 to 2006, Change in Mean Skill Level ....................................... 189

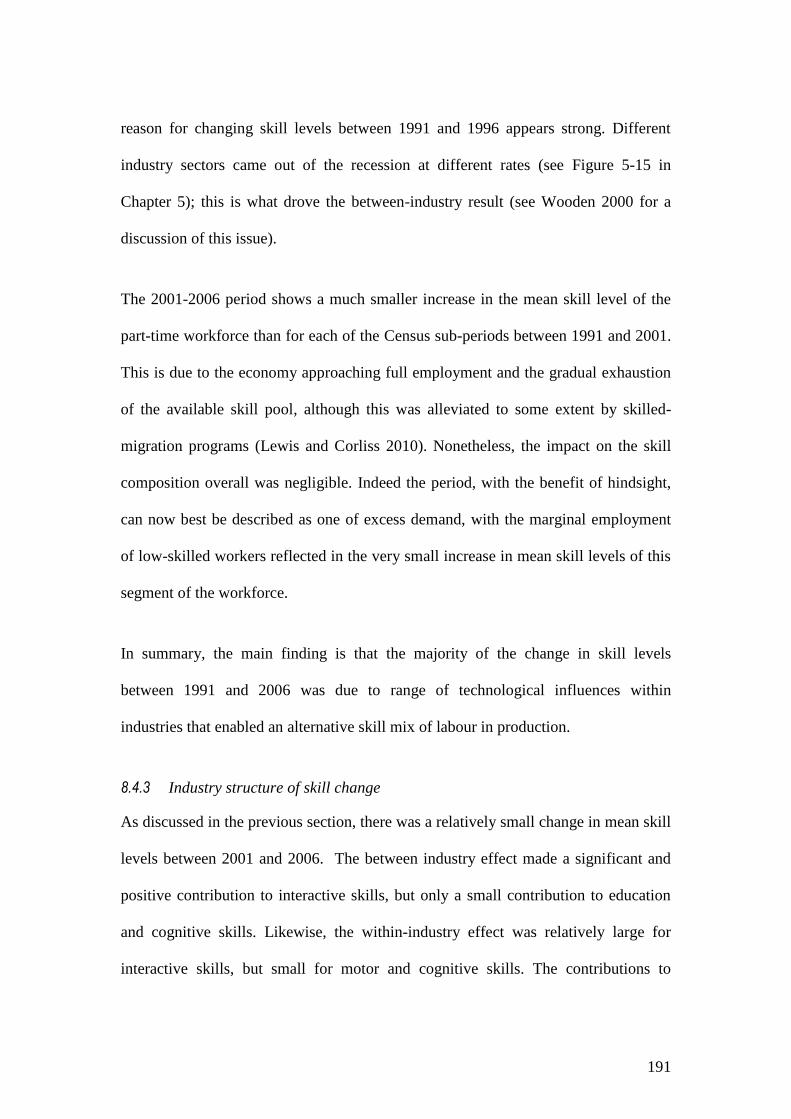

Table 8-9 Between and Within-Industry Effects, 1991 to 2006, Percentage Change in Mean Skill Level ..................... 190

Table 8-10 Mean Skill Level by Region and Skill Dimension, 2006 ............................................................................... 196

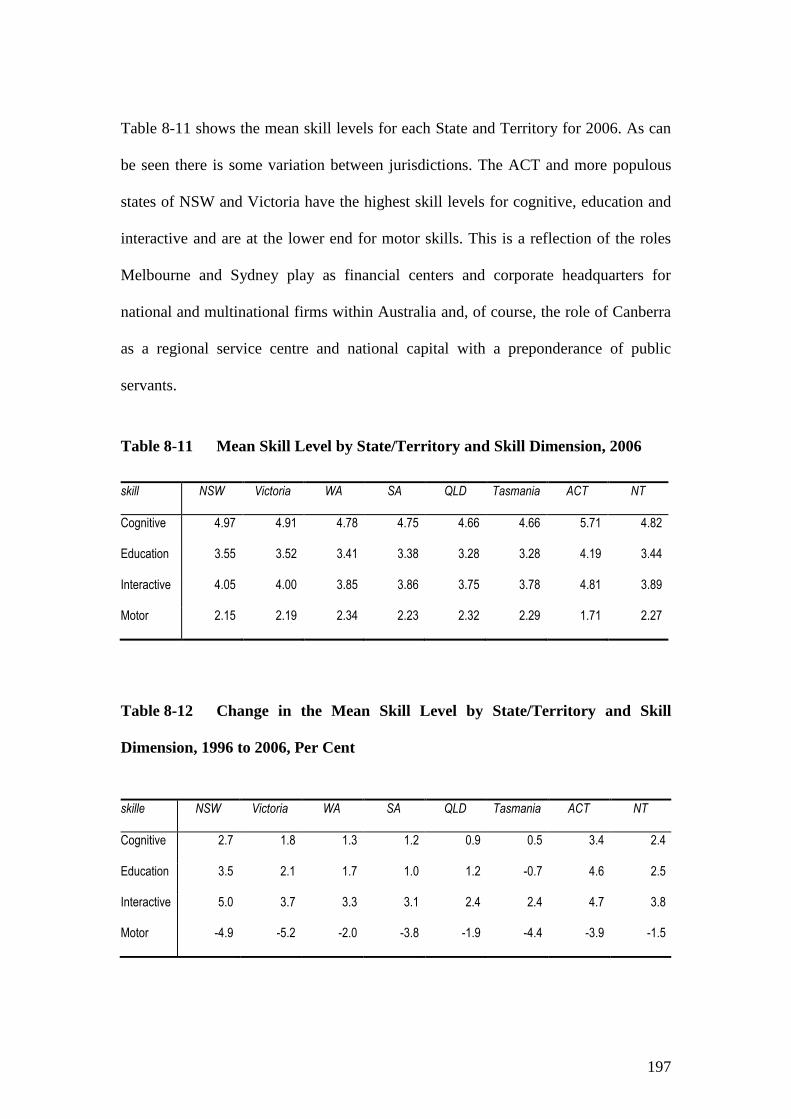

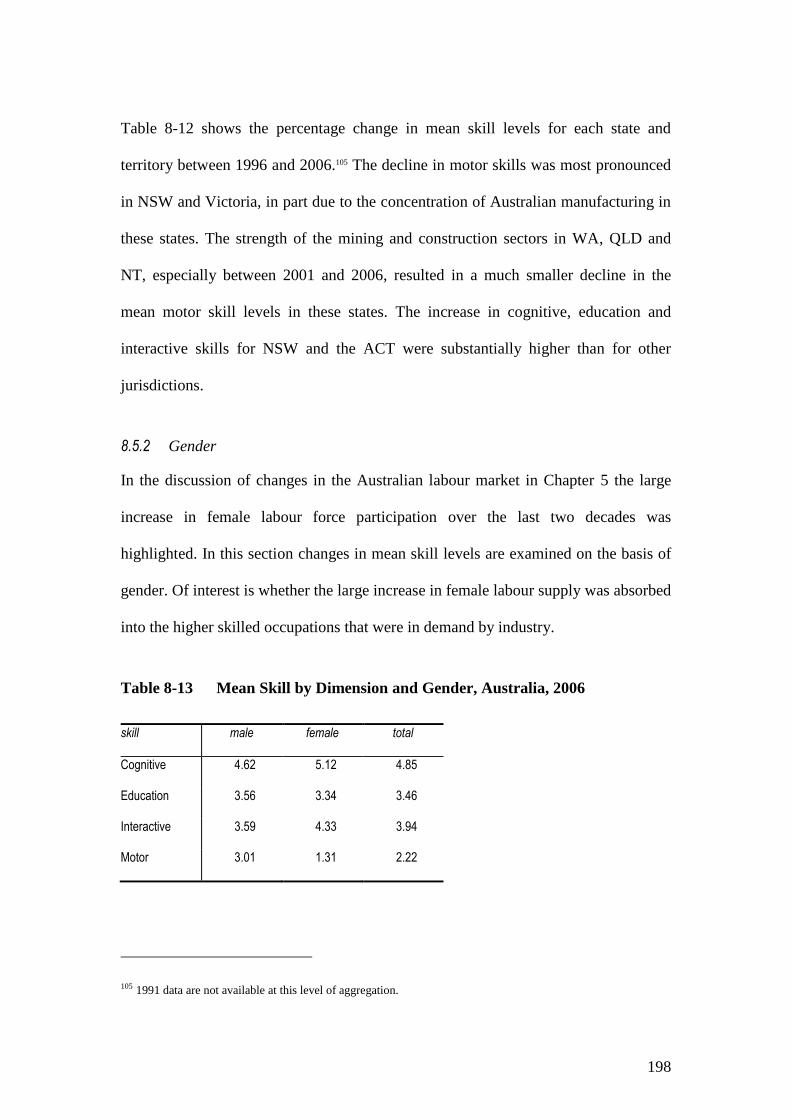

Table 8-11 Mean Skill Level by State/Territory and Skill Dimension, 2006 ................................................................... 197

Table 8-12 Change in the Mean Skill Level by State/Territory and Skill Dimension, 1996 to 2006, Per Cent ................ 197

xiv

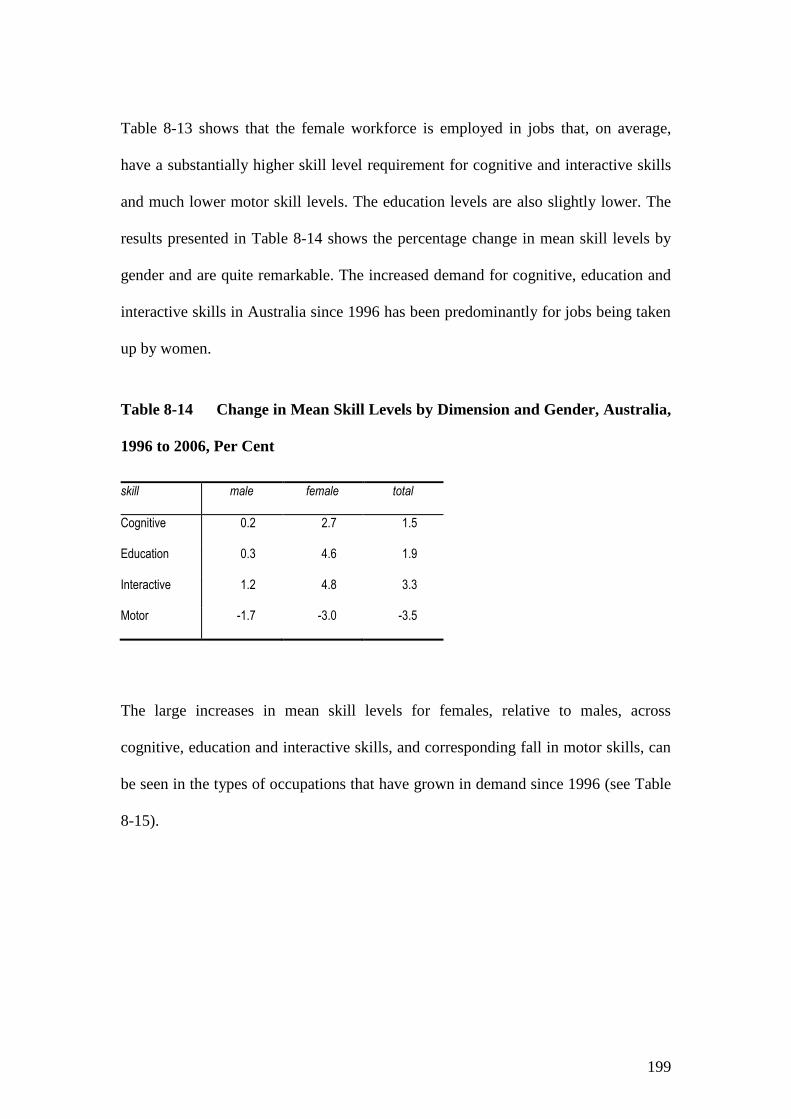

Table 8-13 Mean Skill by Dimension and Gender, Australia, 2006 ................................................................................. 198

Table 8-14 Change in Mean Skill Levels by Dimension and Gender, Australia, 1996 to 2006, Per Cent ........................ 199

Table 8-15 Occupational Growth by Gender, Australia, 1996 to 2006, Per Cent ............................................................. 200

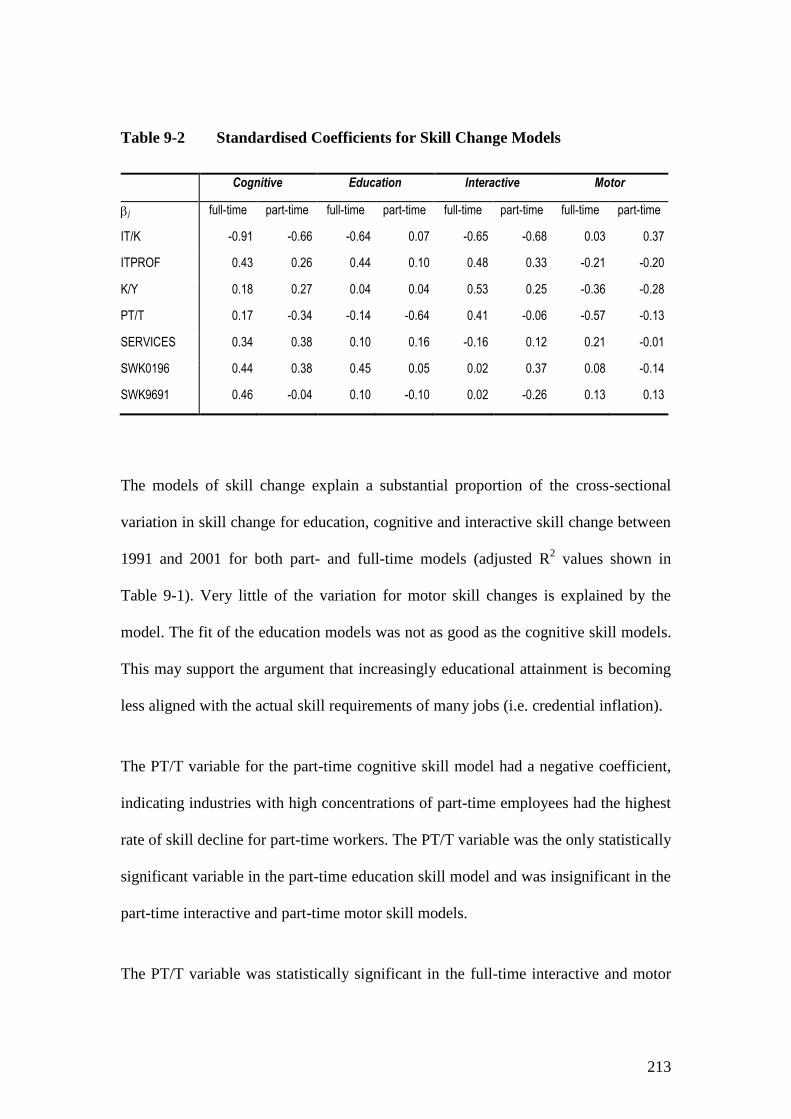

Table 9-1 Determinants of Skill Change, Australia, 1991 – 2001 .................................................................................. 212

Table 9-2 Standardised Coefficients for Skill Change Models ....................................................................................... 213

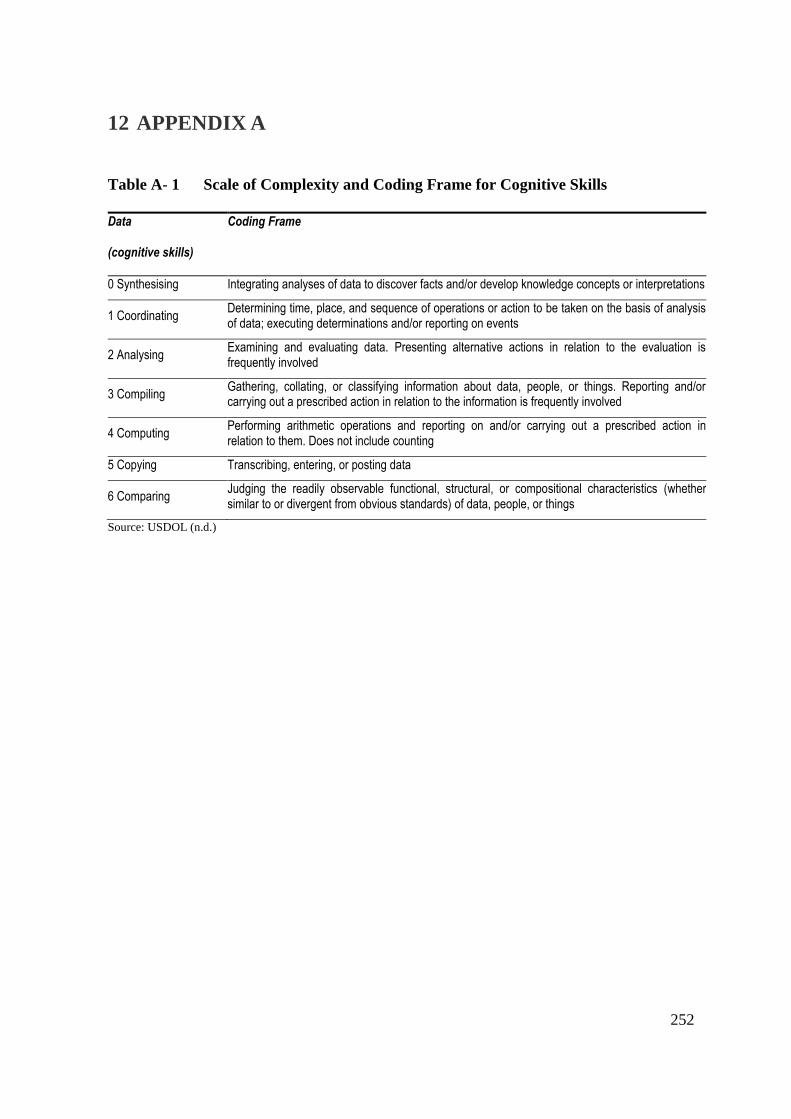

Table A- 1 Scale of Complexity and Coding Frame for Cognitive Skills ........................................................................ 252

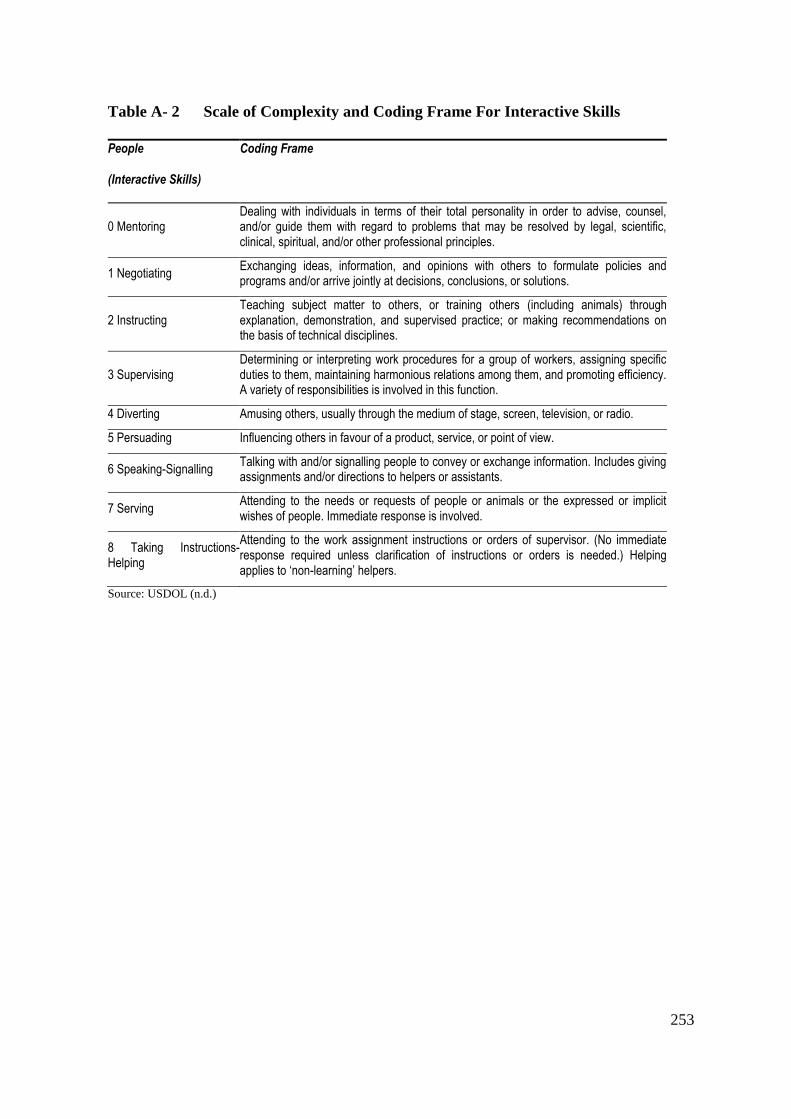

Table A- 2 Scale of Complexity and Coding Frame For Interactive Skills ...................................................................... 253

Table A- 3 Scale of Complexity and Coding Frame For Motor Skills ............................................................................. 254

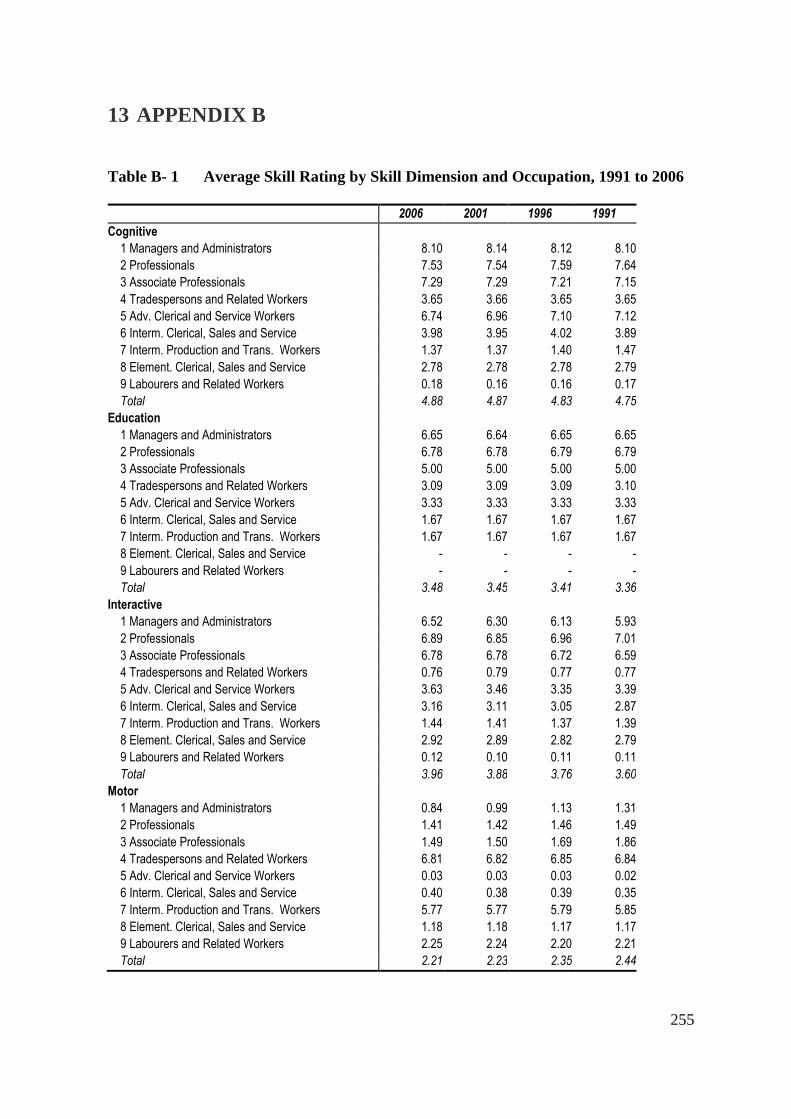

Table B- 1 Average Skill Rating by Skill Dimension and Occupation, 1991 to 2006 ...................................................... 255

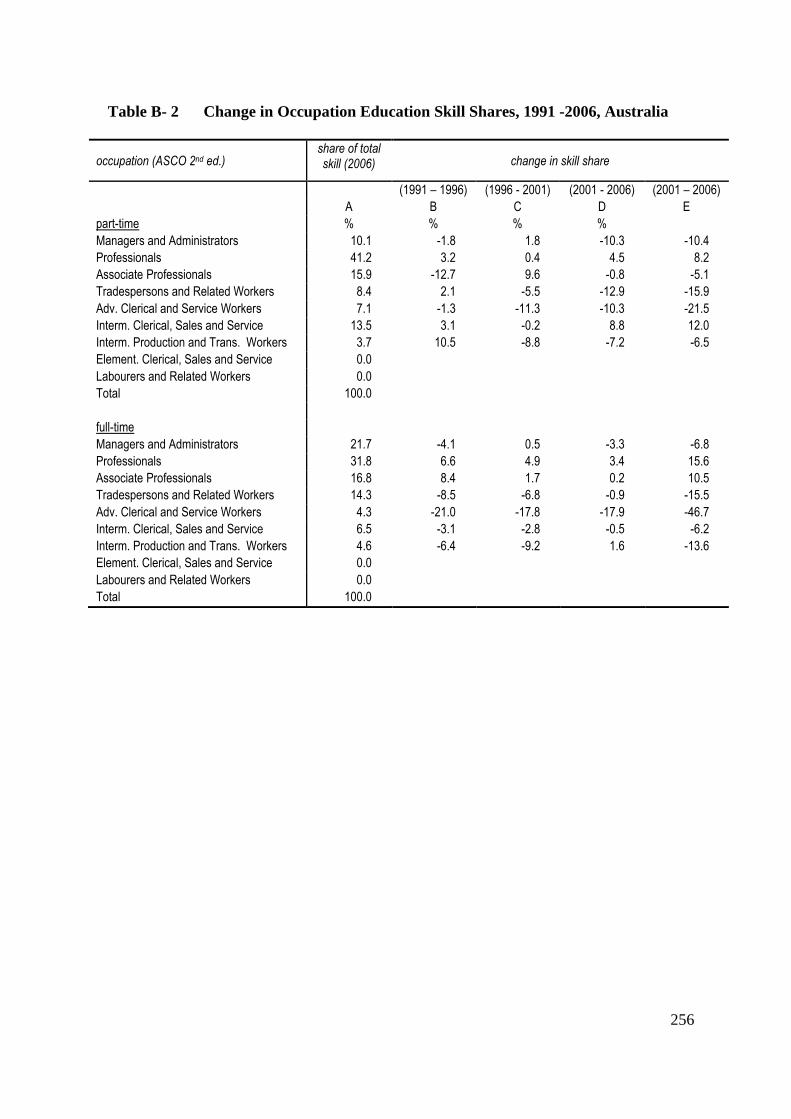

Table B- 2 Change in Occupation Education Skill Shares, 1991 -2006, Australia ........................................................... 256

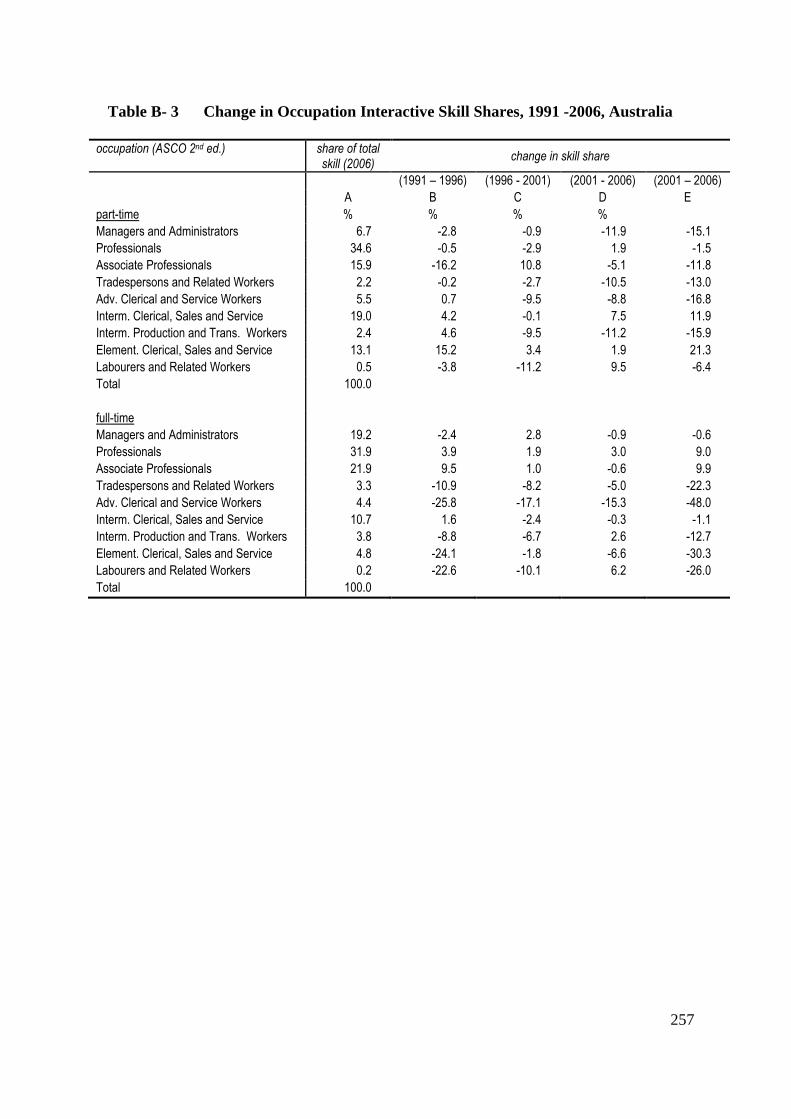

Table B- 3 Change in Occupation Interactive Skill Shares, 1991 -2006, Australia .......................................................... 257

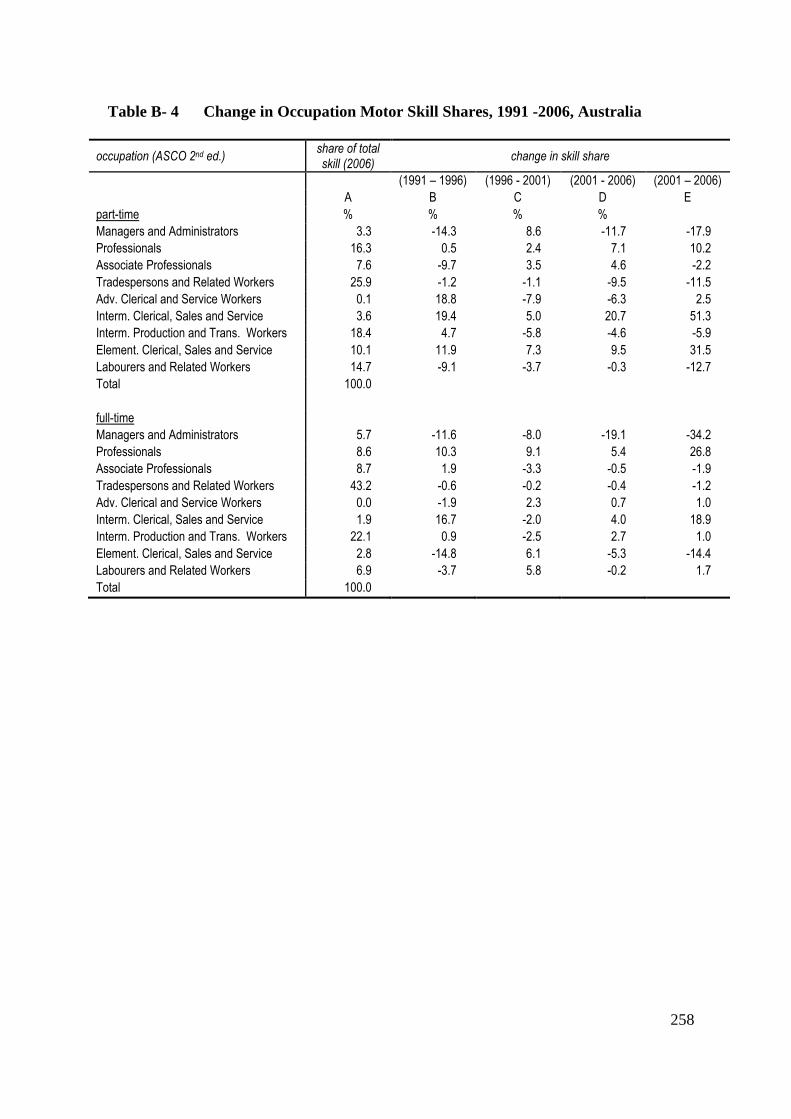

Table B- 4 Change in Occupation Motor Skill Shares, 1991 -2006, Australia ................................................................. 258

Table C- 1 Descriptive Statistics for Regression Variables .............................................................................................. 259

Table C- 2 Ramsey RESET Test ...................................................................................................................................... 260

Table C- 3 Breusch-Pagan / Cook-Weisberg Test ............................................................................................................ 261

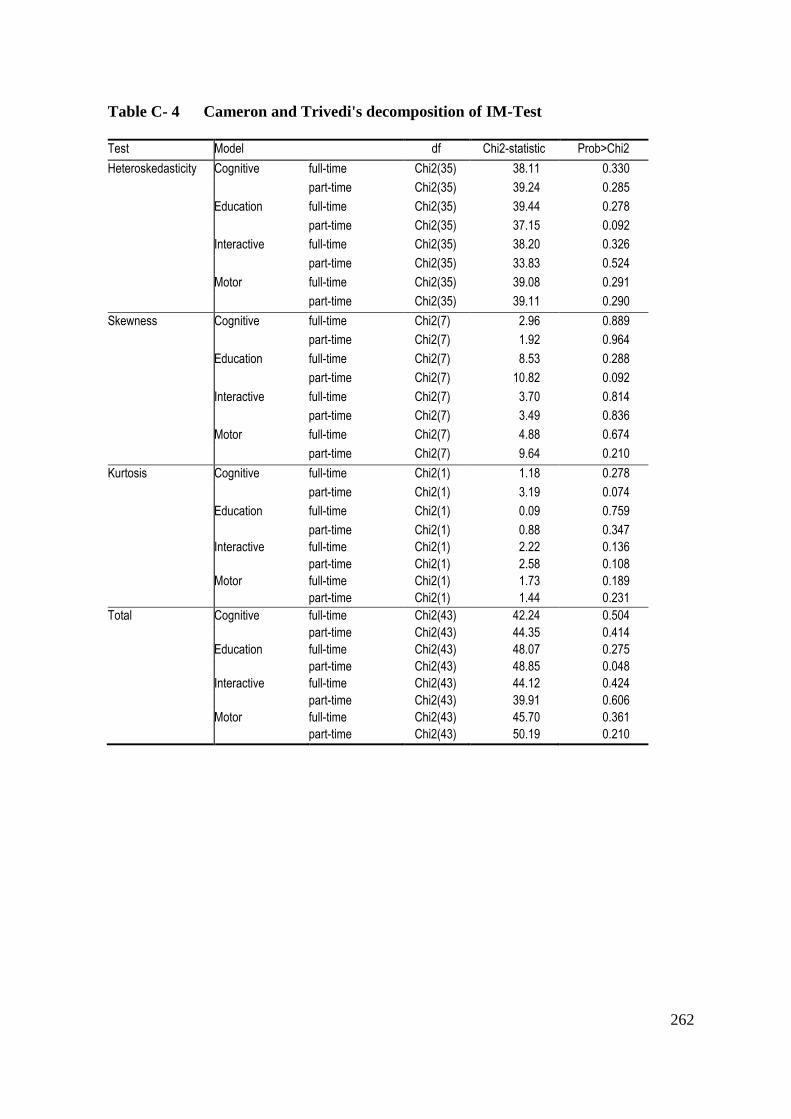

Table C- 4 Cameron and Trivedi's decomposition of IM-Test ......................................................................................... 262

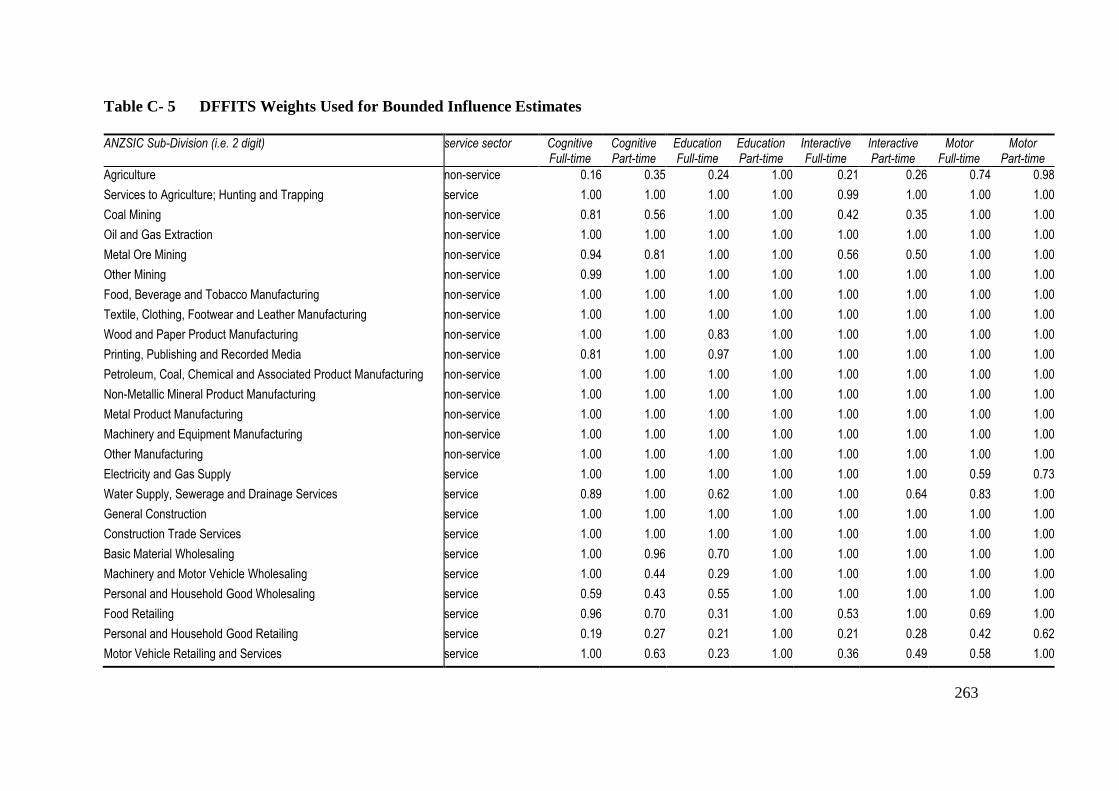

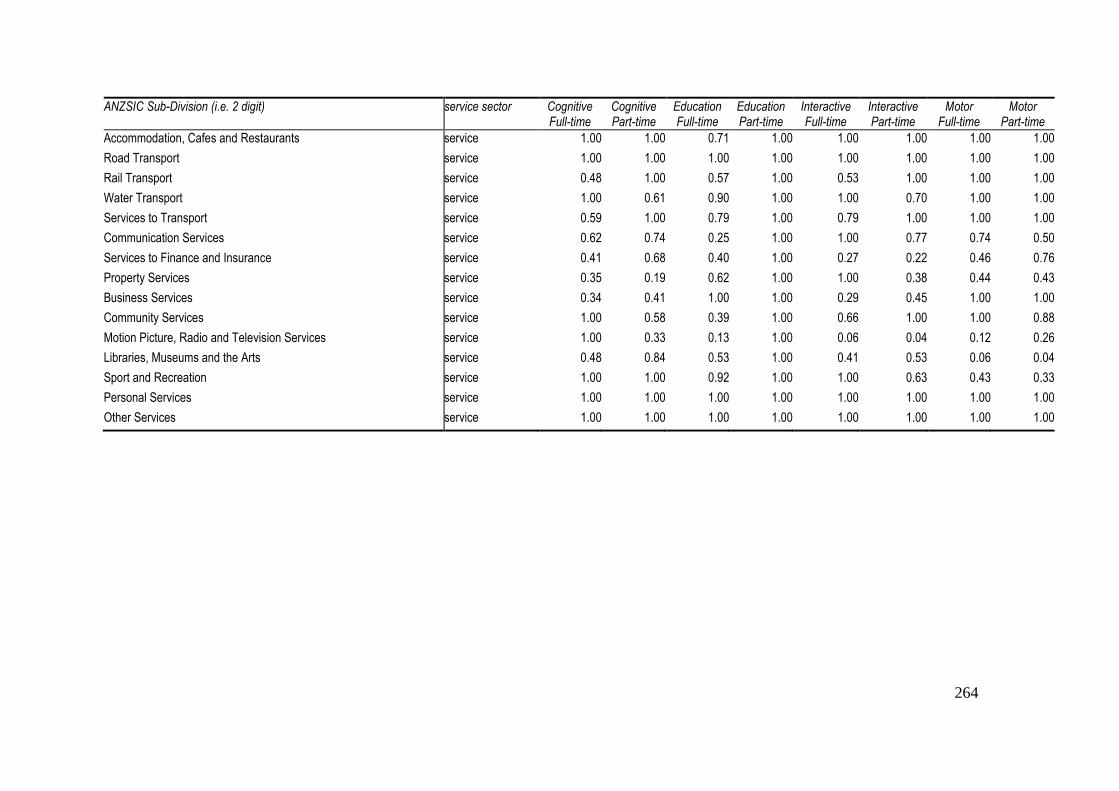

Table C- 5 DFFITS Weights Used for Bounded Influence Estimates .............................................................................. 263

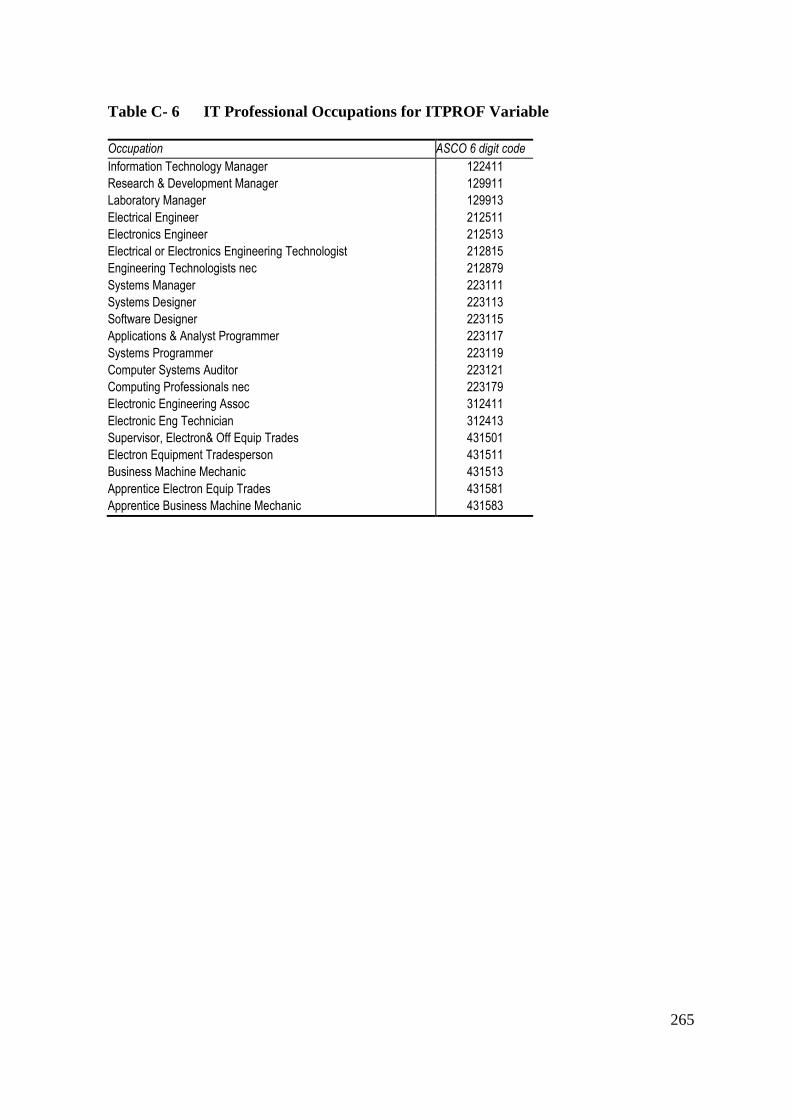

Table C- 6 IT Professional Occupations for ITPROF Variable ........................................................................................ 265

xv

LIST OF FIGURES

Figure 2-1 Distribution of Equivalised Disposable Household Income, 2007-08 .............................................................. 18

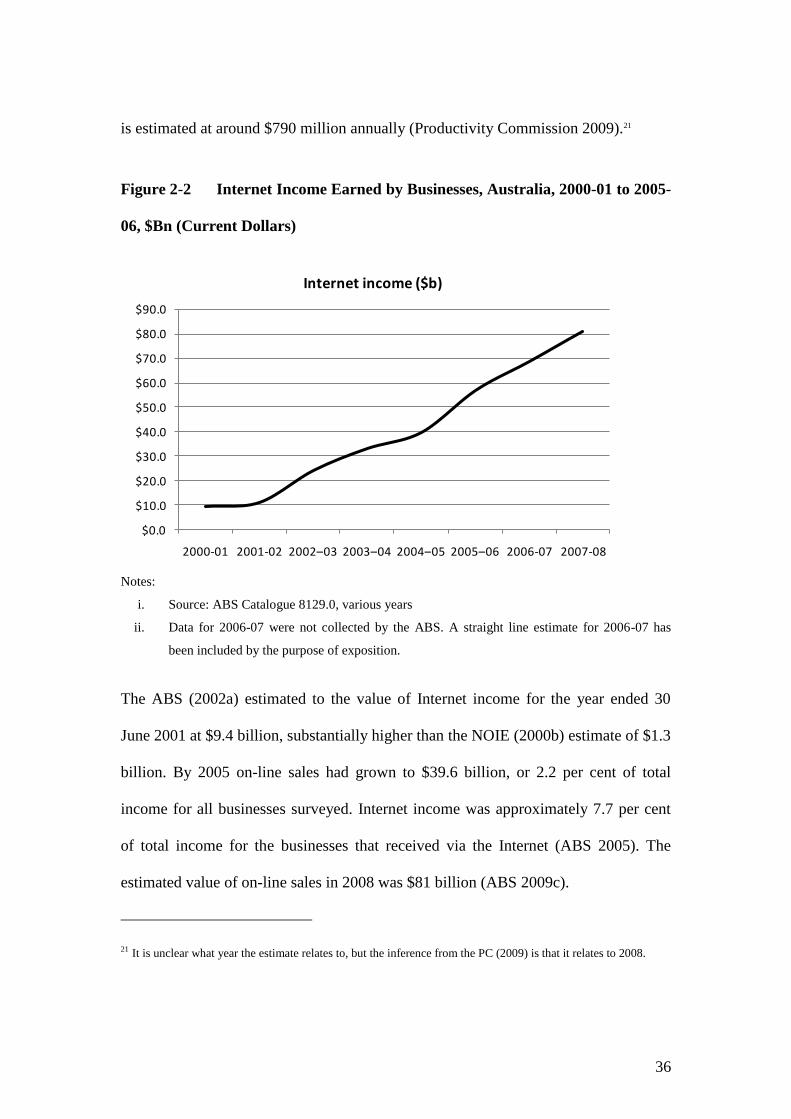

Figure 2-2 Internet Income Earned by Businesses, Australia, 2000-01 to 2005-06, $Bn (Current Dollars) ..................... 36

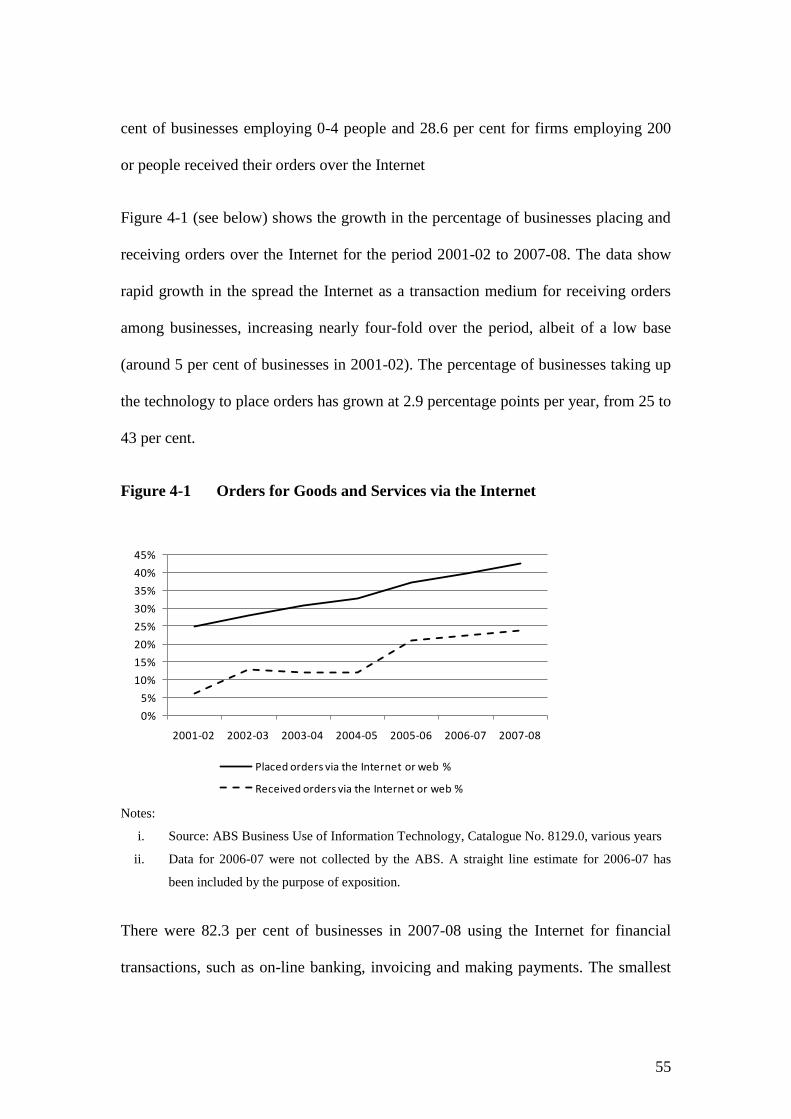

Figure 4-1 Orders for Goods and Services via the Internet ............................................................................................... 55

Figure 4-2 Change in Net Information Technology Capital Stock, Australia, 1990 to 2008 ($m) .................................... 58

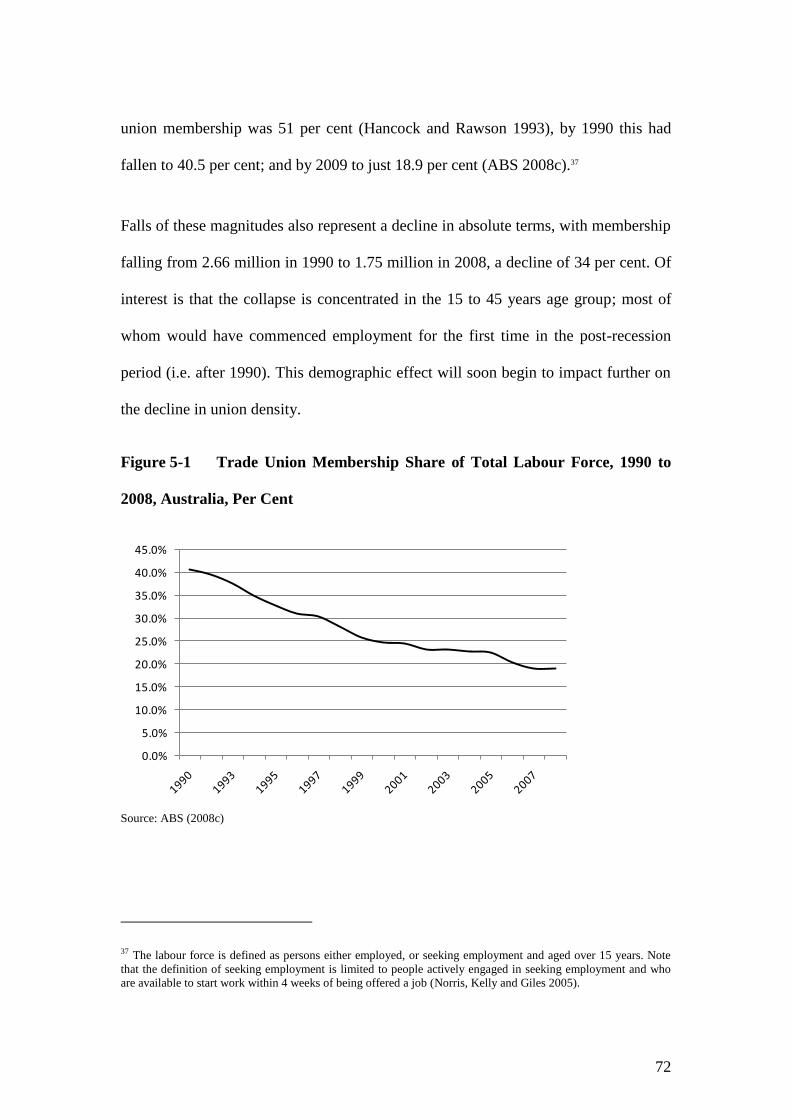

Figure 5-1 Trade Union Membership Share of Total Labour Force, 1990 to 2008, Australia, Per Cent ........................... 72

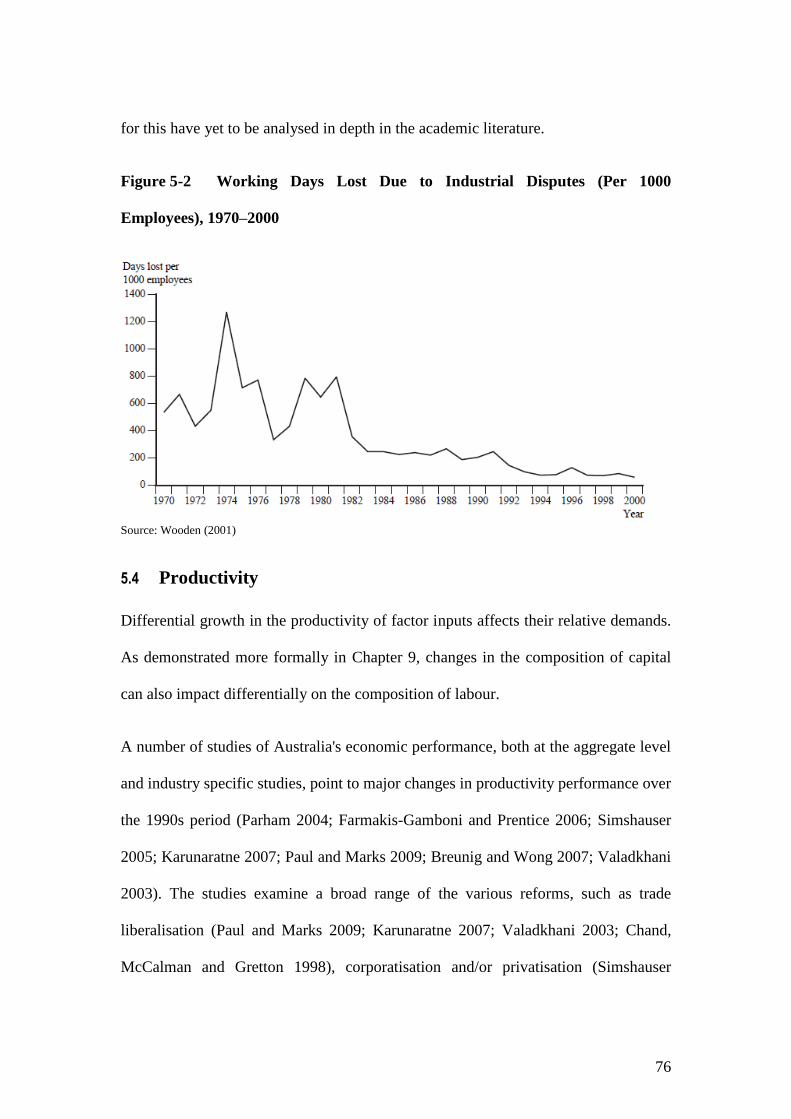

Figure 5-2 Working Days Lost Due to Industrial Disputes (Per 1000 Employees), 1970–2000 ........................................ 76

Figure 5-3 Multi-Factor Productivity Index, Australia, 1985-2009, (Jun-08=100) ............................................................ 77

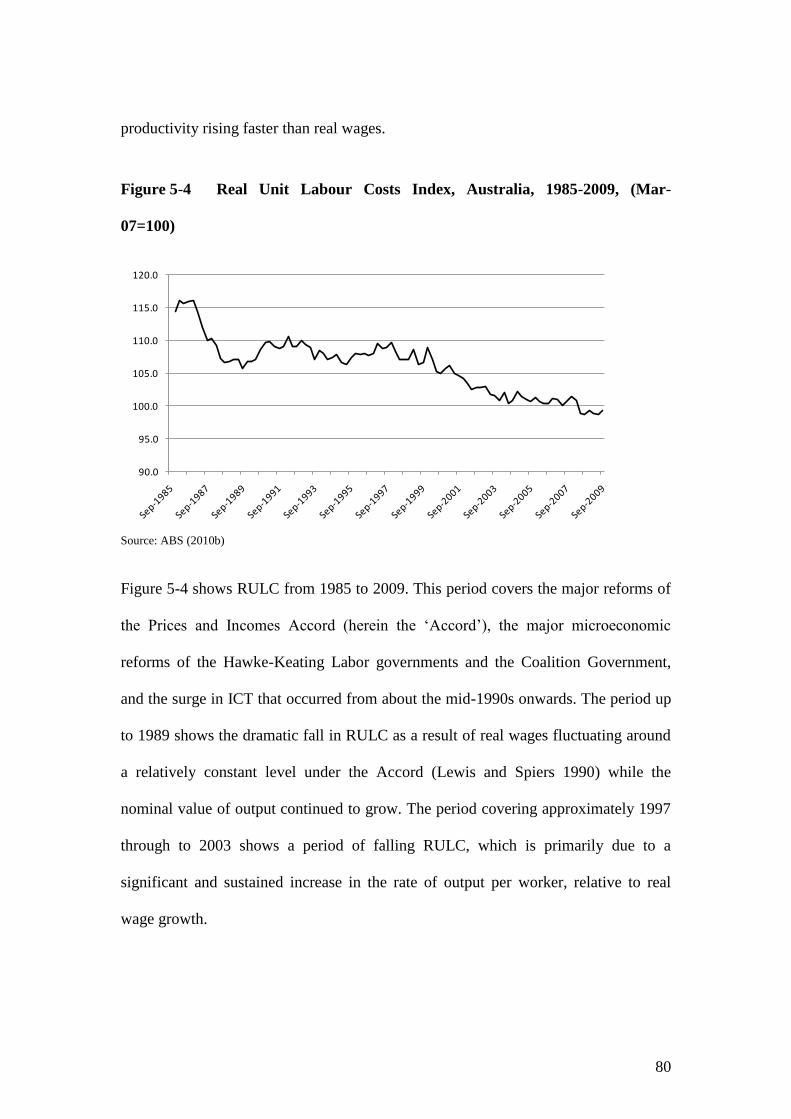

Figure 5-4 Real Unit Labour Costs Index, Australia, 1985-2009, (Mar-07=100) ............................................................. 80

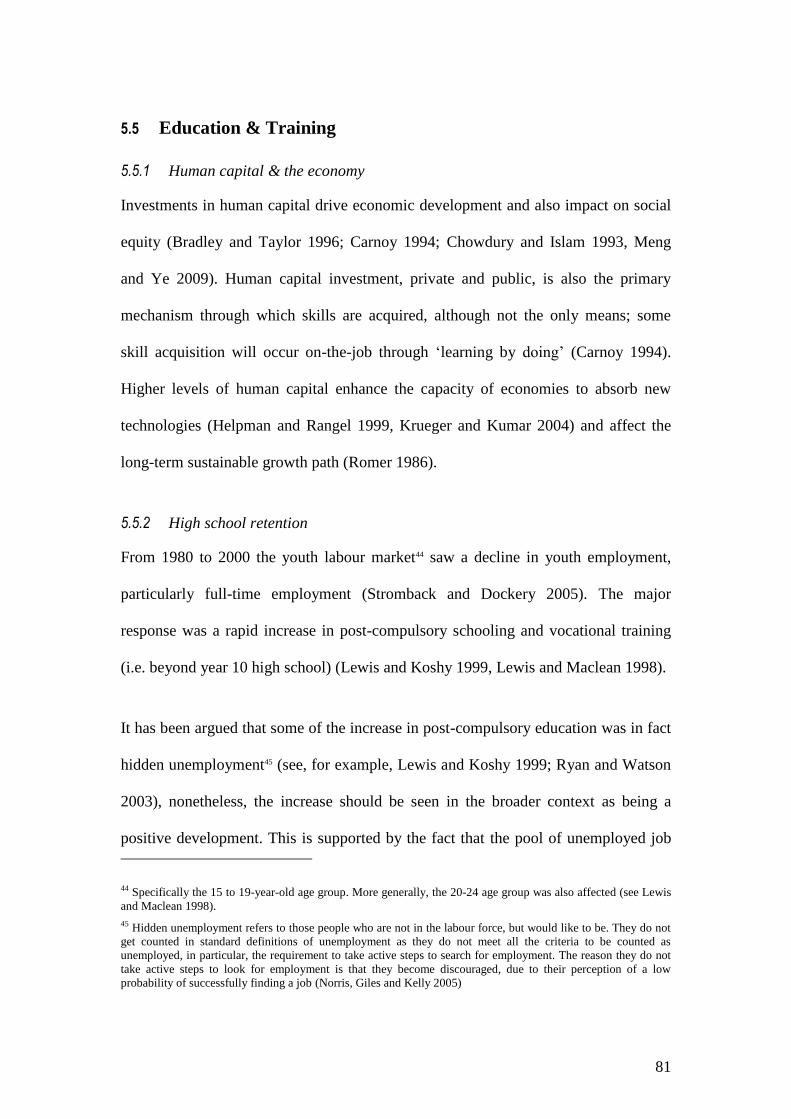

Figure 5-5 Apparent Retention Rates, 1990 to 1997, Australia, Per Cent .......................................................................... 82

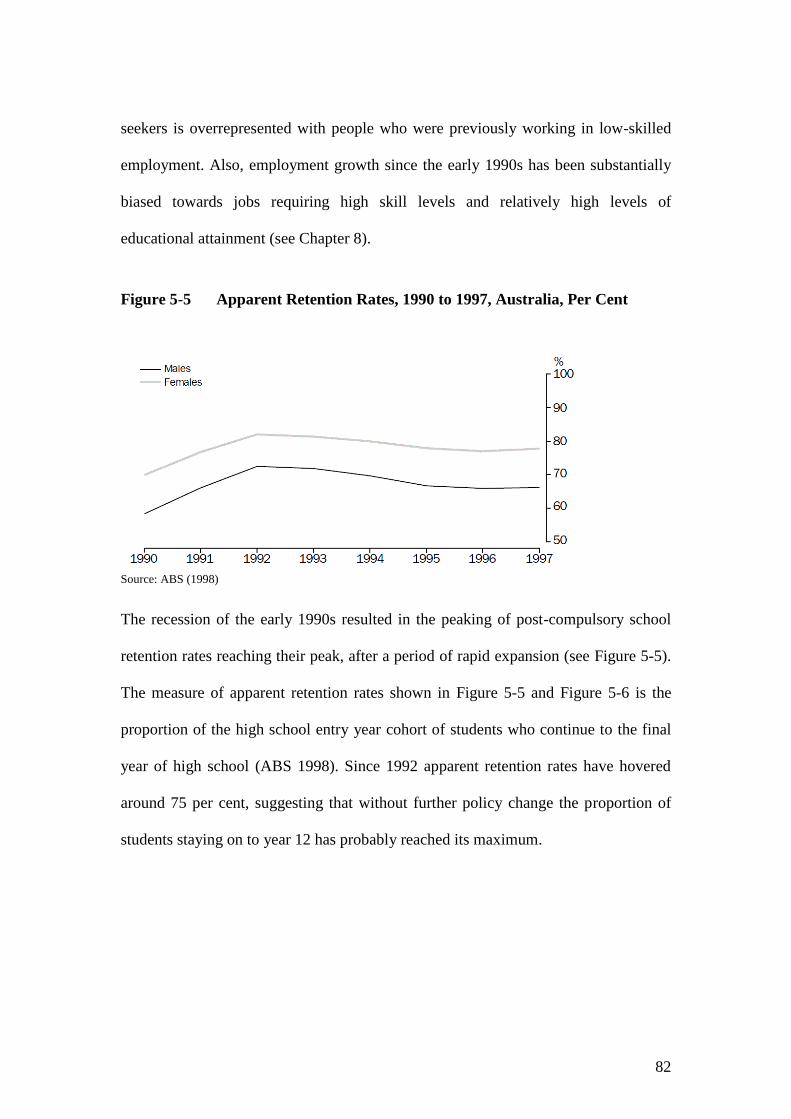

Figure 5-6 Apparent Retention Rates, 1993 to 2008, Australia, Per Cent .......................................................................... 83

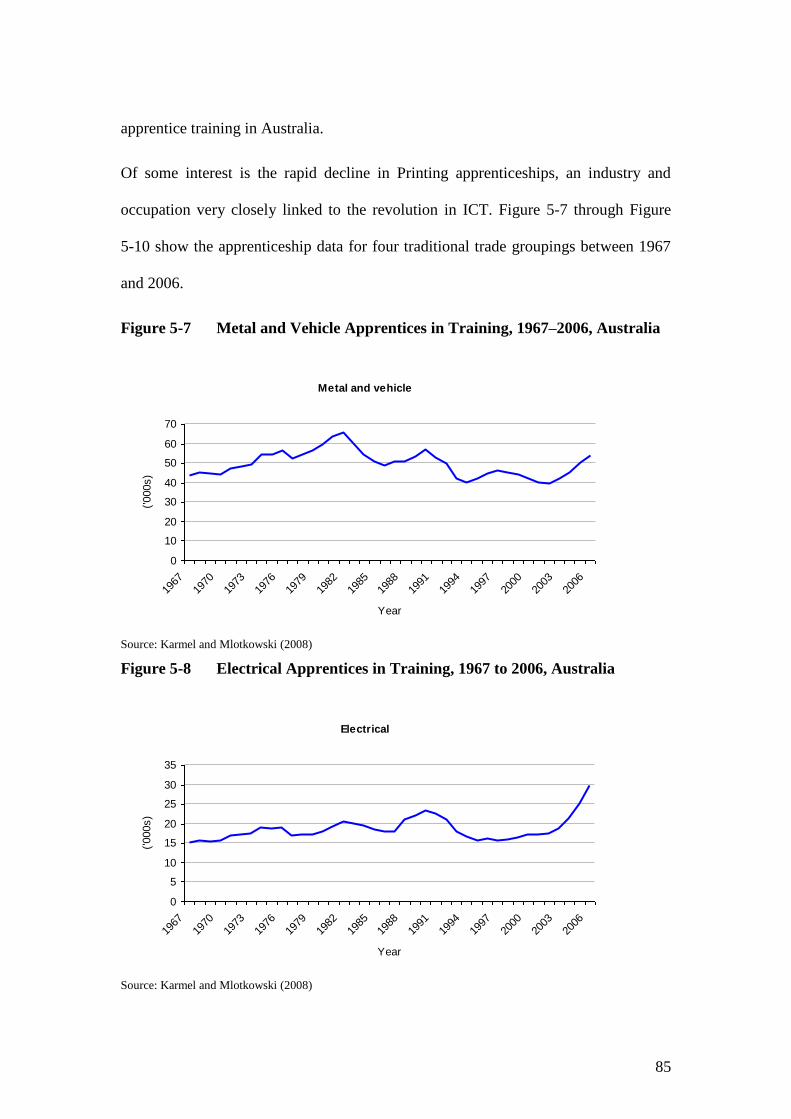

Figure 5-7 Metal and Vehicle Apprentices in Training, 1967–2006, Australia ................................................................. 85

Figure 5-8 Electrical Apprentices in Training, 1967 to 2006, Australia ............................................................................ 85

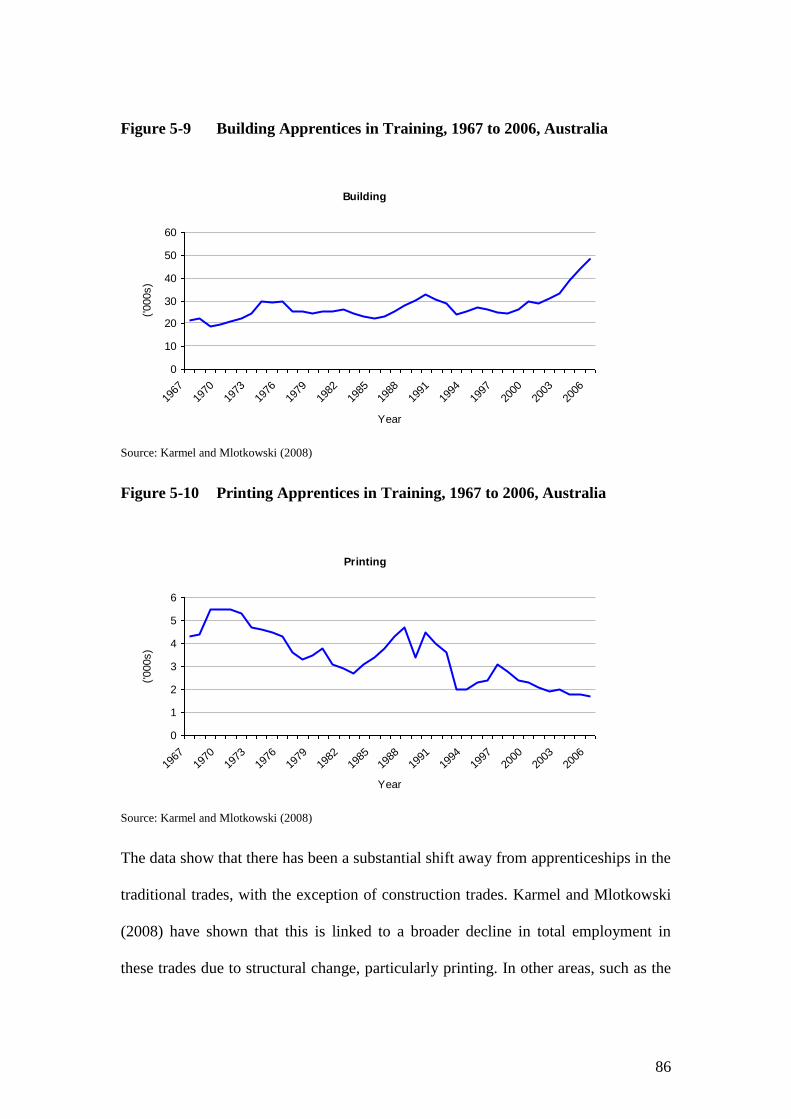

Figure 5-9 Building Apprentices in Training, 1967 to 2006, Australia.............................................................................. 86

Figure 5-10 Printing Apprentices in Training, 1967 to 2006, Australia ............................................................................... 86

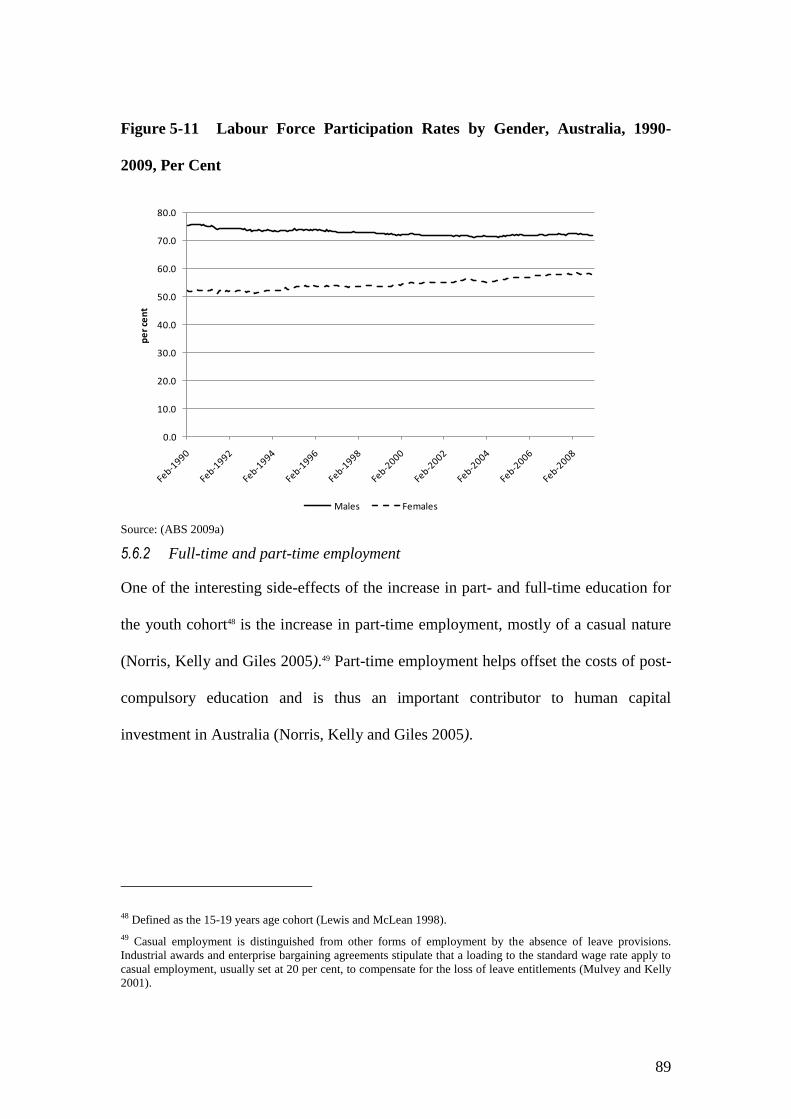

Figure 5-11 Labour Force Participation Rates by Gender, Australia, 1990-2009, Per Cent ............................................... 89

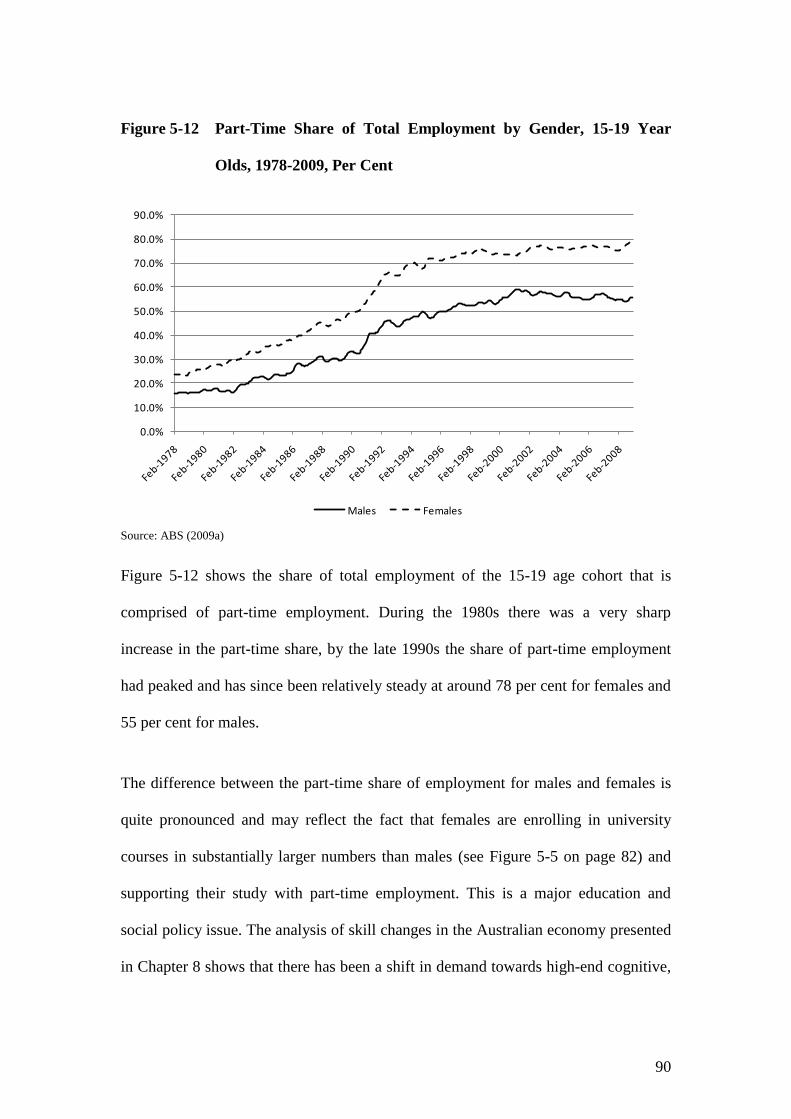

Figure 5-12 Part-Time Share of Total Employment by Gender, 15-19 Year Olds, 1978-2009, Per Cent ........................... 90

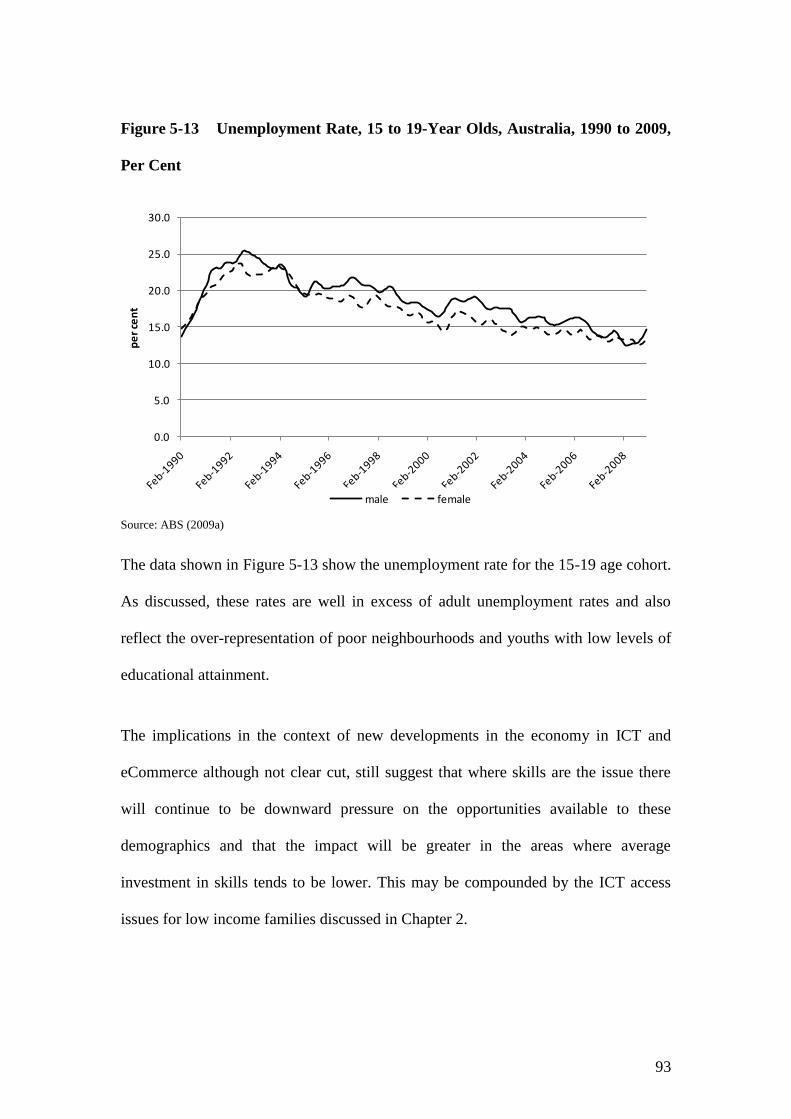

Figure 5-13 Unemployment Rate, 15 to 19-Year Olds, Australia, 1990 to 2009, Per Cent ................................................ 93

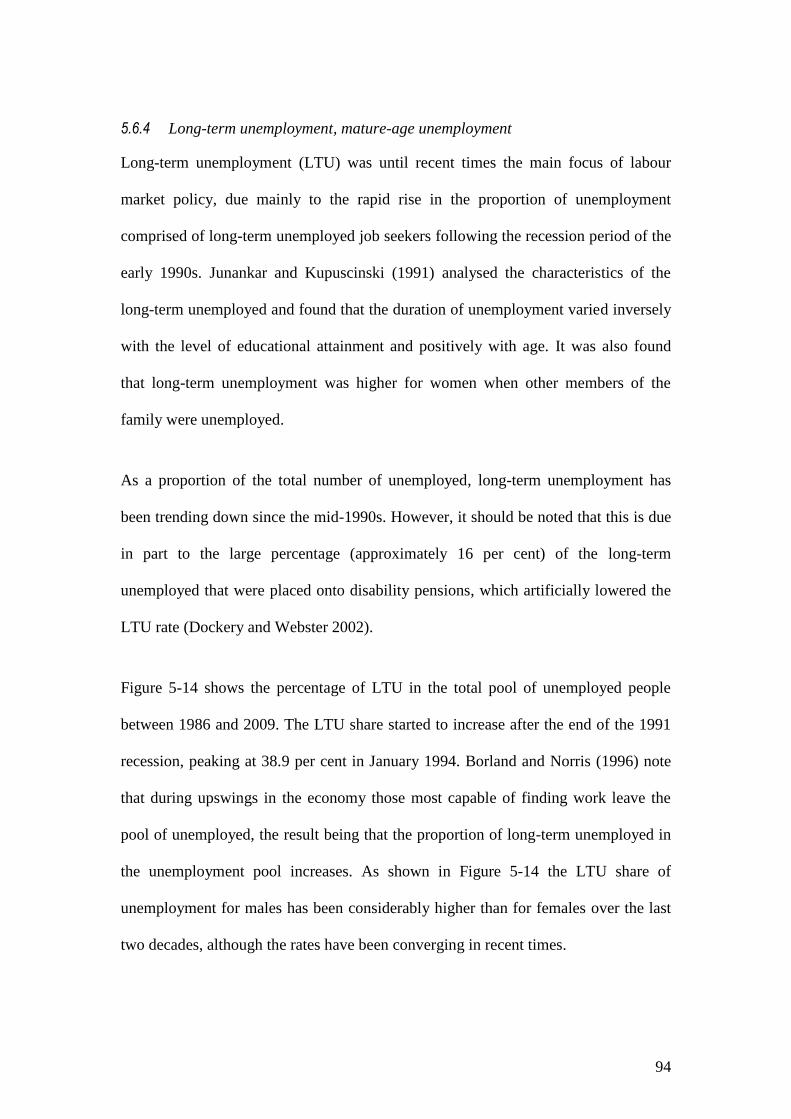

Figure 5-14 LTU to Total Unemployment Ratio, Australia, 1986-2009, Per Cent ............................................................. 95

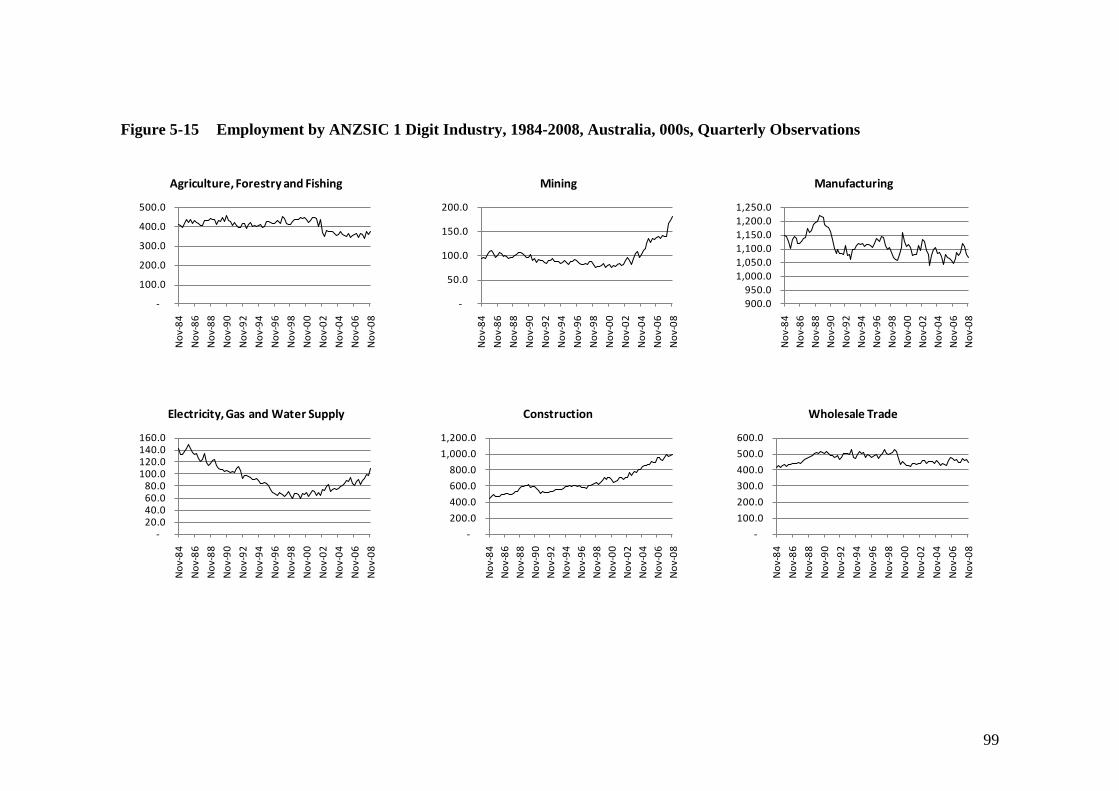

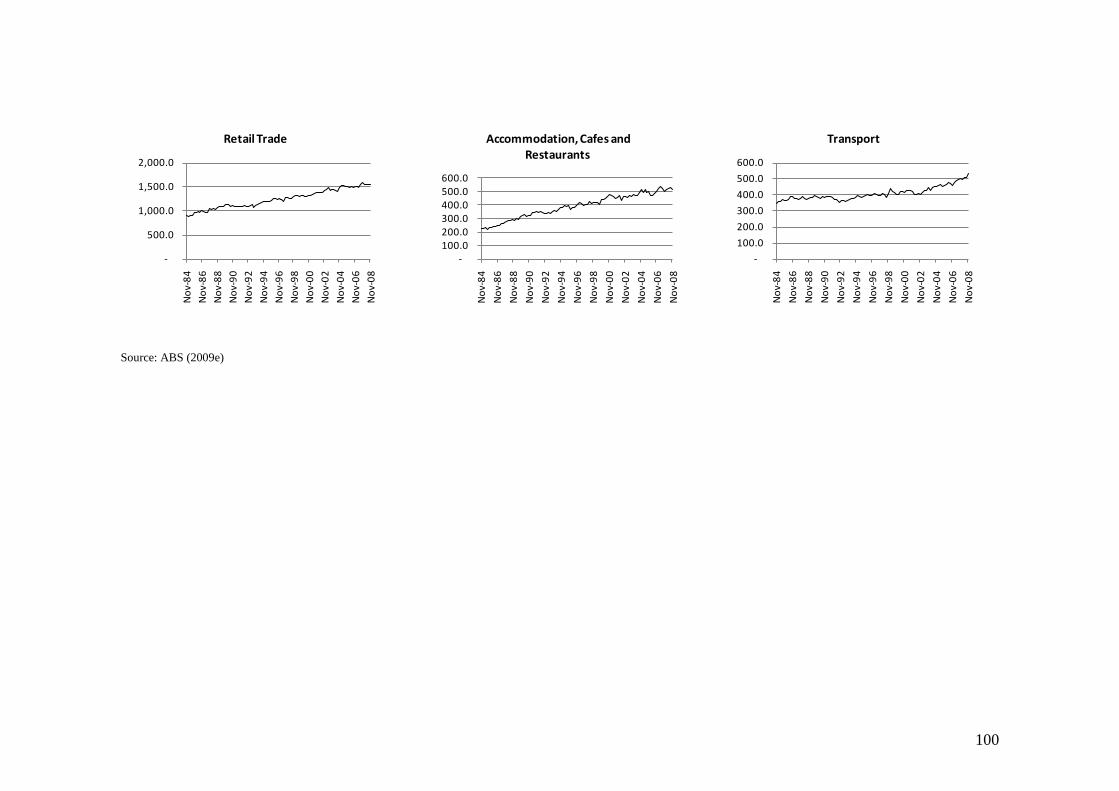

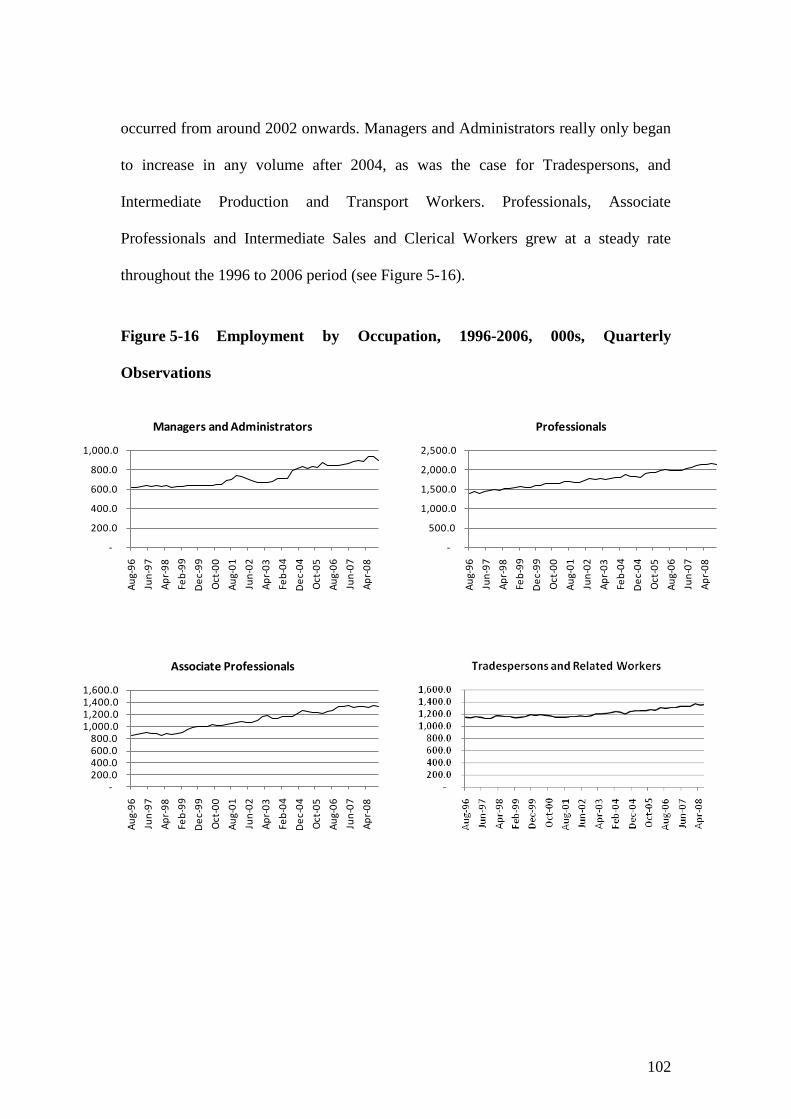

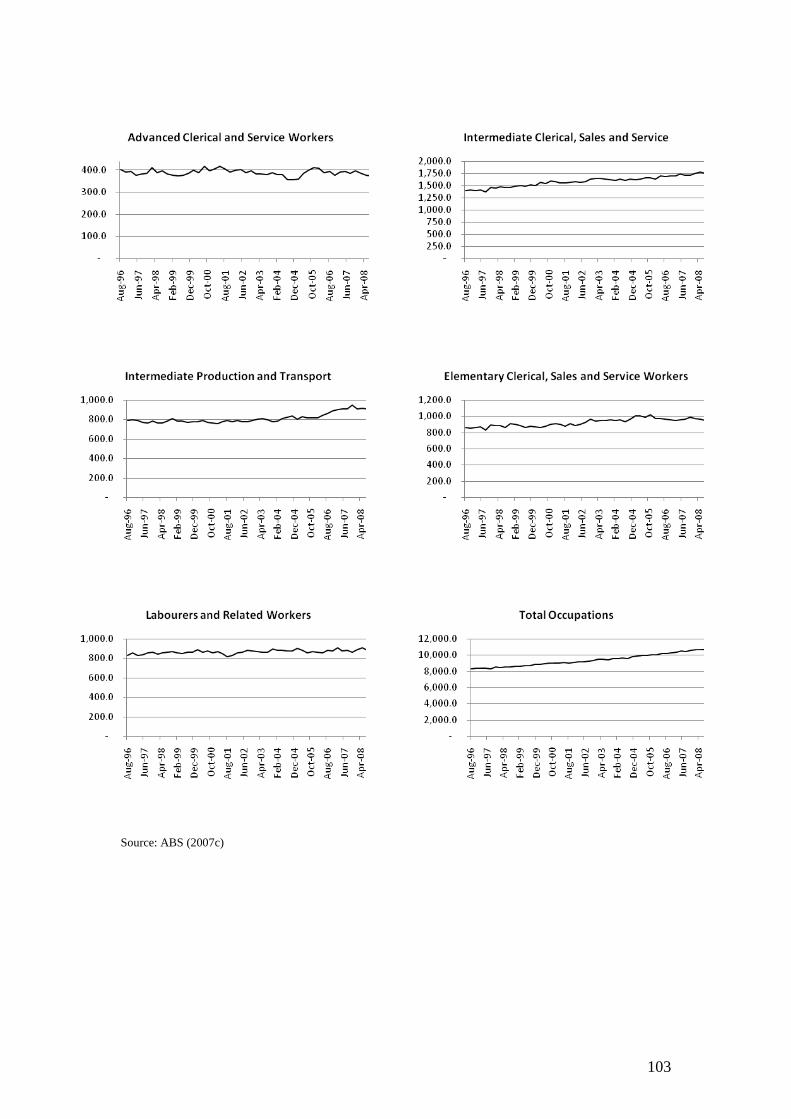

Figure 5-15 Employment by ANZSIC 1 Digit Industry, 1984-2008, Australia, 000s, Quarterly Observations ................... 99

Figure 5-16 Employment by Occupation, 1996-2006, 000s, Quarterly Observations ....................................................... 102

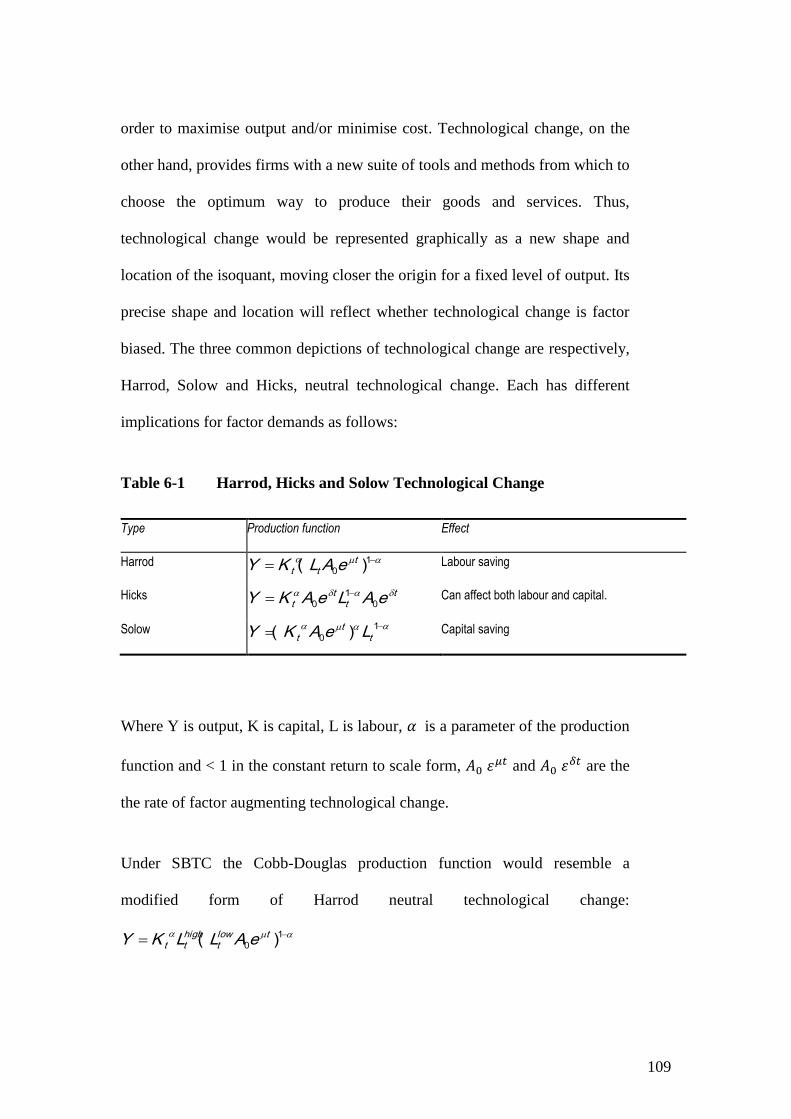

Figure 6-1 Technical Change in Response to Changes in Factor Prices .......................................................................... 111

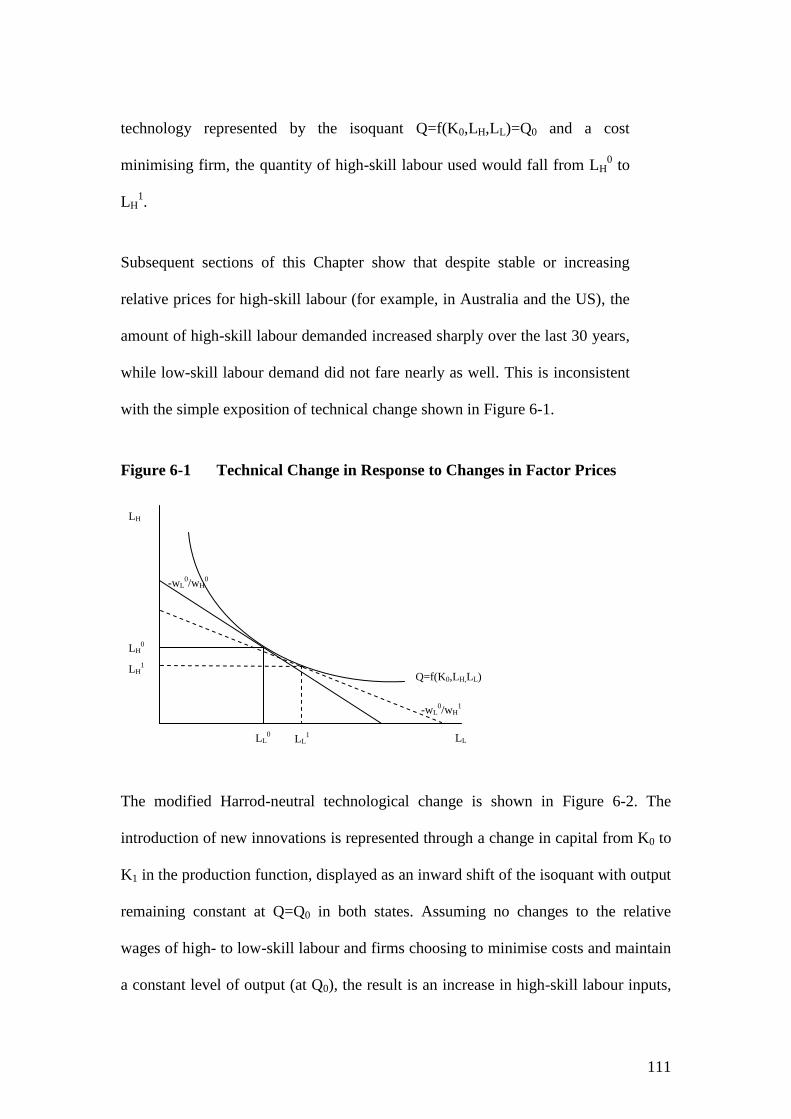

Figure 6-2 Harrod Neutral Technological Change and SBTC ......................................................................................... 112

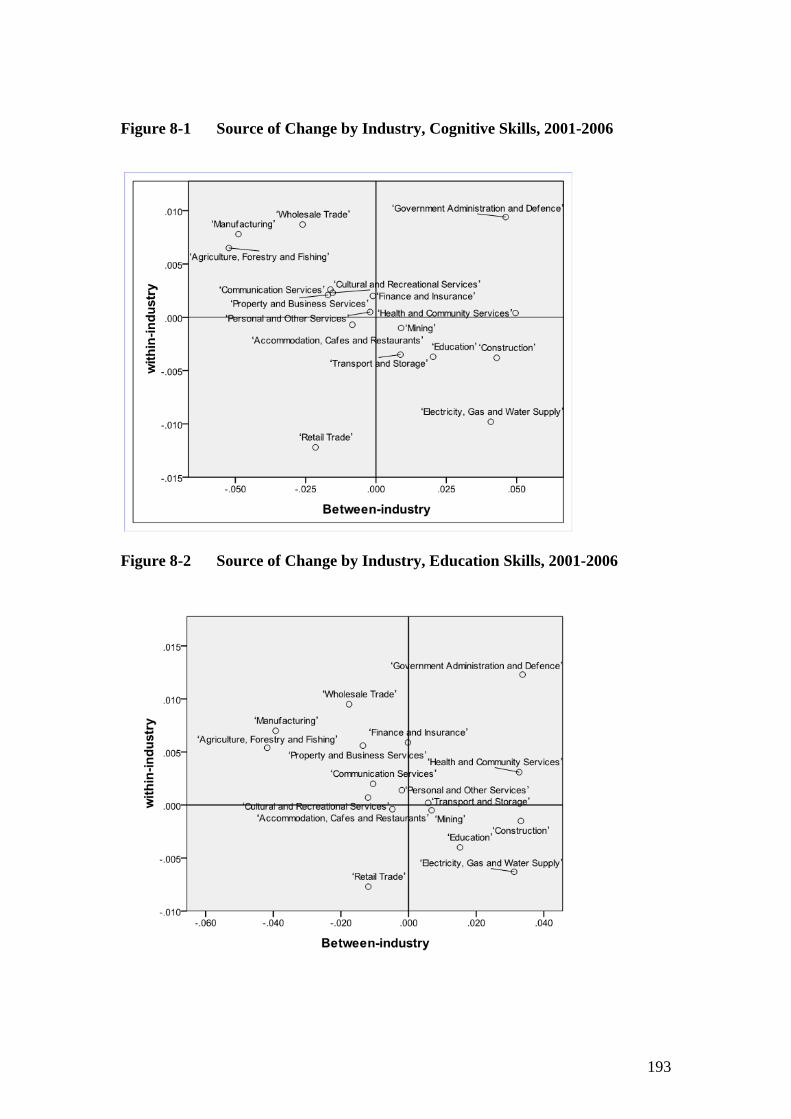

Figure 8-1 Source of Change by Industry, Cognitive Skills, 2001-2006 ......................................................................... 193

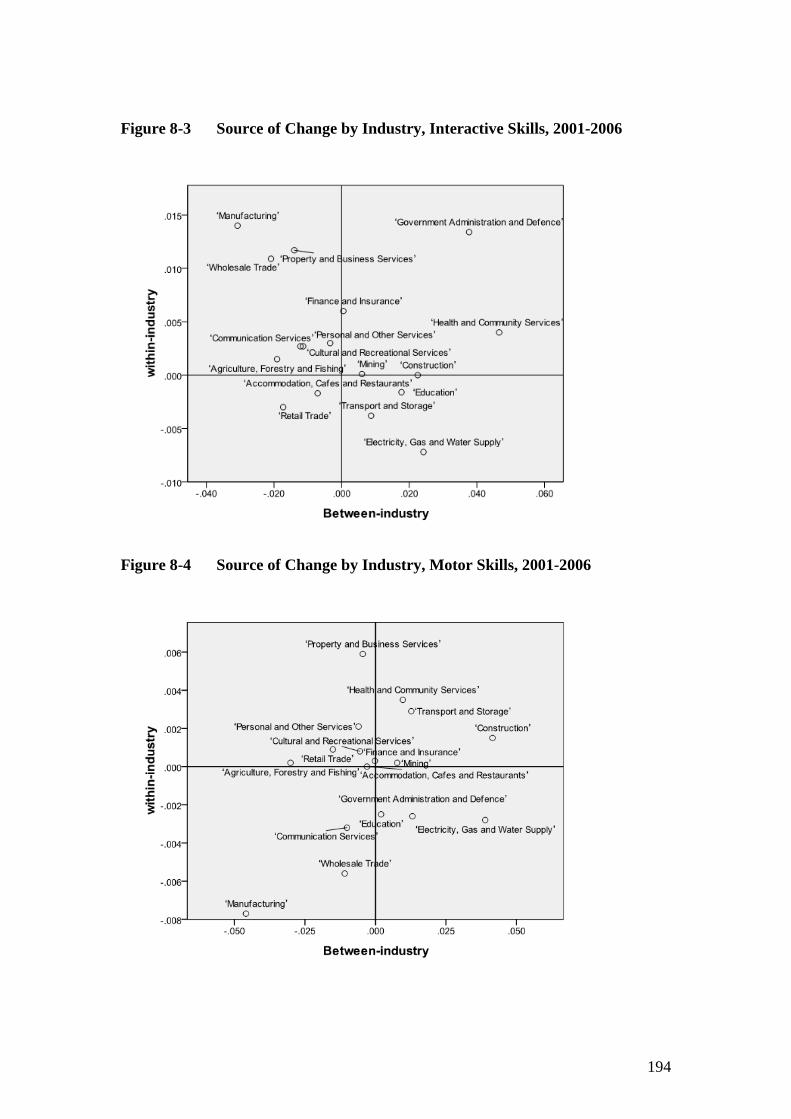

Figure 8-2 Source of Change by Industry, Education Skills, 2001-2006 ......................................................................... 193

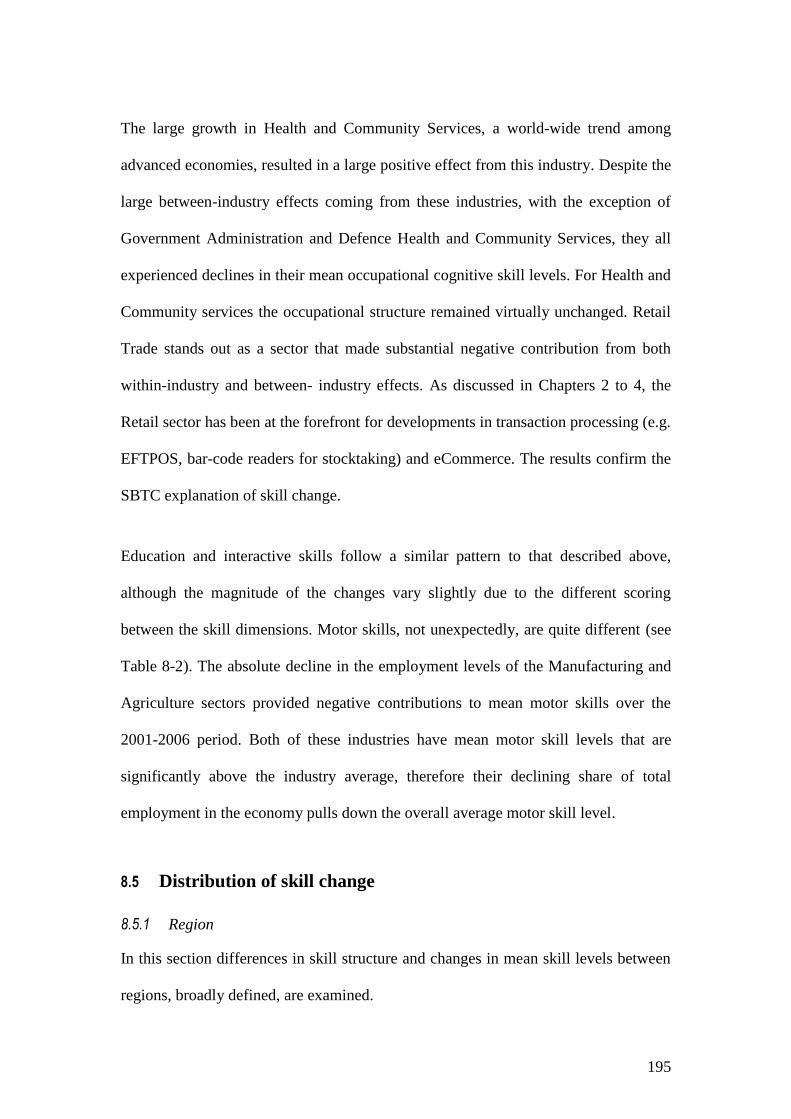

Figure 8-3 Source of Change by Industry, Interactive Skills, 2001-2006 ........................................................................ 194

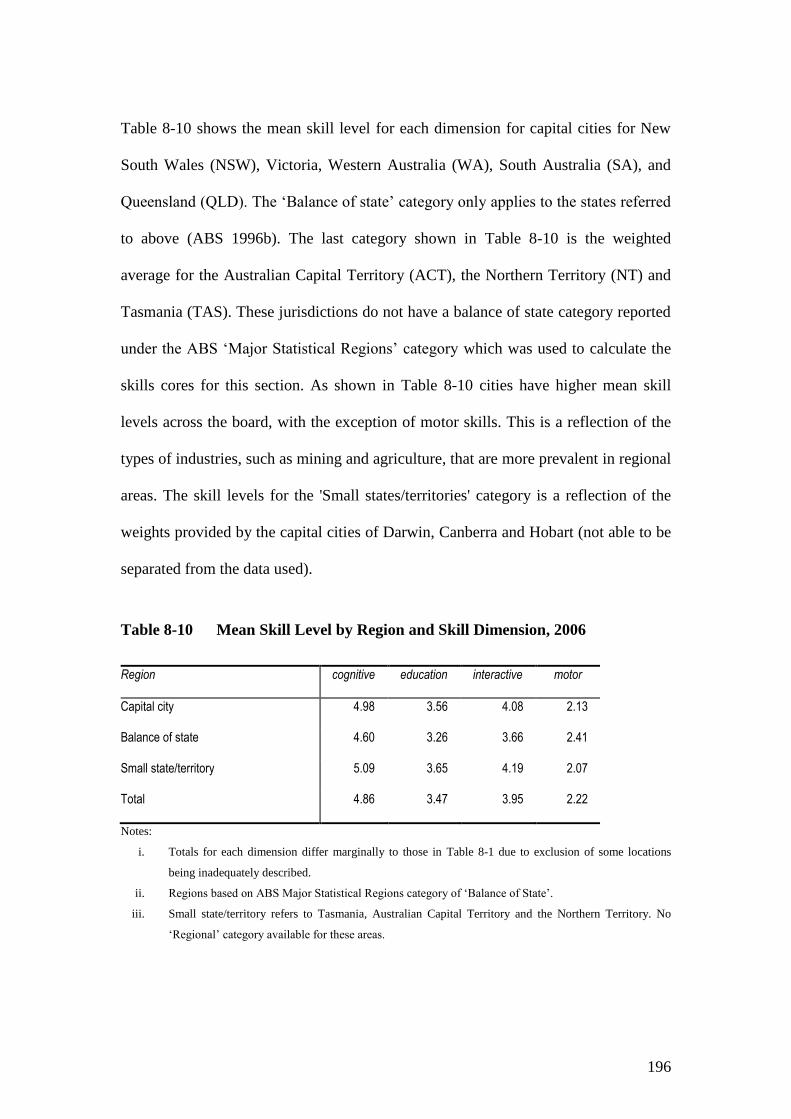

Figure 8-4 Source of Change by Industry, Motor Skills, 2001-2006 ............................................................................... 194

1

1 INTRODUCTION

The primary objective of this thesis is to gauge the extent to which the structural and

technological change that has occurred in Australia since 1991, in particular, the widespread

integration of information and communication technologies (ICT), has influenced the demand

for skills.

Structural adjustment, particularly when brought about by changes in technology, will affect

people differently, depending on the market sector they are in, their location, skills and age.

Indeed, all sections of society are affected in some way by innovation and, in the vast

majority of cases, it is for the better. In some instances, though, people will be not be able to

access the benefits brought about by new innovations, or they will be disadvantaged in some

way by new developments and economic reforms. People displaced by economic change

draw cold comfort from the fact that productivity improvements are good for the economy.

In Australia there are institutional constraints and other features, such as minimum wages or

geographic isolation, that prevent labour markets from clearing rapidly and smoothly in the

face of structural adjustments. This brings into question whether there is a role for labour

market policies and, if so, what form these should take.

One of the most notable technological developments over the last three decades has been the

rapid advancement in computerisation and its role in production. In the last two decades it has

also become highly visible in the workplace and the home as the price of personal computers

has fallen dramatically (in terms of computing power) and the sophistication and usability of

computers has improved. The spread and improvement of computers has facilitated (and in

large part been motivated by) rapid developments in information, graphical and statistical

2

applications. This has profoundly altered the social and workplace environment. It is difficult

to imagine how people could successfully integrate into the labour market without some

exposure to the tools of the information age – computers and the Internet – other than for low-

skill, manual entry-level jobs.

In the workplace the computer has extended its reach to the point where it would be unusual

to enter any workplace where the computer was not a vital part of the production process and

some, or even most, of the workforce would be using one. This is particularly the case for the

service sector of the economy, which has also grown to become the dominant sector of the

economy, accounting for around 70 per cent of gross domestic product (GDP) in 2010.

1.1 Change in the Australian Labour Market

The Australian labour market has experienced dramatic changes since the early 1980s. Some

of the changes have been institutional, or systemic, in nature, such as the Prices and Incomes

Accord between the union movement and the Labor Government of the Hawke-Keating era

spanning 1983 to 1992 (Norris, Kelly and Giles 2005; Lewis and Spiers 1990). During this

time an accord between the union movement and the government resulted in an extended

period of wage restraint that resulted in a large decrease in the real wages received by workers

across Australia (Lewis and Spiers 1990). The impact on employment, not surprisingly, was

large, with unemployment falling from a recessionary high of 10.3 per cent to 5.7 per cent

between 1983 and 1989 (ABS 2009a).

Other major changes to impact on the labour market include the continued push to liberalise

the Australian economy. Examples include tariff reductions in the manufacturing sector,

privatisation of the Commonwealth Bank and Commonwealth Serum Laboratories, foreign

banks being issued licences to operate in Australia and the floating of the Australian currency.

3

Other major reforms include the privatisation of utilities owned and run by State and Territory

governments, incentivised through Commonwealth Grant payments to the States for meeting

agreed milestones (Borland 2001). The Industrial Relations Commission (IRC) in 1991 also

promoted employers and unions to bargain over pay and conditions at the enterprise level and

this was later reinforced under the Industrial Relations Reform Act 1993 (Lansbury, Wailes

and Yazbeck 2007).

As Australia changed governments, from Labor to the Liberal-National Party Coalition in

1996, there was a continuation of the reform agenda, with the national telecommunications

carrier, Telstra, being gradually privatised. The Reserve Bank of Australia (RBA) was also

formally given independence, enabling it to set interest rates without direct interference from

the government (Lewis et al. 2006). The Coalition Government also introduced a new labour

relations framework that reduced the power of centralised wage fixing (Lansbury, Wailes and

Yazbeck 2007).

Taken together, these changes have contributed to dramatic improvements in total factor

productivity for the economy (Productivity Commission 2006). While this has, in large part,

been facilitated through increased labour market flexibility, the broader microeconomic

reforms have also imposed the need for greater flexibility in the labour market.

1.2 Skills in the Australian Economy

The typical notion of skills is embedded in occupational composition and qualification levels.

One of the more dramatic changes for the Australian labour market has been the massive

increase in the number of students completing secondary schooling and progressing to

university. This was another plank of the Hawke-Keating Labor Government and numbers

peaked with the recession in 1990-1992. As Lewis and Koshy (1999) point out, some of the

4

increase was actually due to hidden unemployment among youths.

The continued decline of manufacturing has brought with it a decline in the various blue-

collar trades that have traditionally been the mainstay of the industry. The substantial rise in

the financial and business services sector, likewise, has seen the number of business

professionals increase dramatically.

1.3 Influence of ICT on Skill Change in Australia

A feature of advanced economies around the world, including Australia, has been the

dramatic rise in the use of ICT. Studies for Germany, the United States (US), United

Kingdom (UK), the European Union (EU) and Australia have shown some connection

between skill demand and ICT (see Autor, Levy and Murnane 2003; Berman, Bound and

Machin 1998; Bresnahan, Brynjolfsson and Hitt 2002; Corvers and Marikull 2007; Pappas

1998; Spitz 2003; Howell and Wolff 1990; Wolff 1995). The timing of the studies for

Australia and the skill measurement methods have precluded much of the development and

change that has occurred since the development of the Internet and have spanned periods that

are heavily nuanced by the deep recession of the 1990s.

1.4 Overview of Thesis

In this thesis the effect that information and communication technologies have had on skill

demand are examined, with the focus being on the structure of skills in the economy and the

way skills are defined and measured. The analysis draws on changes observed in the

occupational and industry structure since 1991. Although the focus of the thesis is on the

scope and nature of changes that have taken place and their likely causes, it is also concerned

with the burden of change; that is, in broad terms, the distribution across various dimensions

of society and the economy, such as location, occupation, income, gender and industry is

5

examined.

The remainder of the thesis is set out as follows. Chapter 2 examines the growth of

information and communication technologies in the economy. In particular it explores the

expectations of researchers in the field in the 1990s as the Internet started to emerge as a

significant commercial development with the potential to reshape transactions between agents

and the organisation of firms.

The results of a survey of firms undertaken in 2001 are presented in Chapter 3. The survey

focused on changes to business and customer interaction, and expected impacts on skills and

training. Chapter 4 provides an examination of the latest trends in business use of, and

investment in, ICT.

Chapter 5 examines the features of the Australian labour market and observed changes in key

aggregates, institutional features, and changes to occupational and industry structure. A

discussion of the drivers of change over the last 25 years is provided. In particular,

microeconomic reforms, the overhaul of industrial relations and the literature examining the

impact on labour productivity are examined.

Chapter 6 presents the literature on skill-biased technological change (SBTC) in the broader

context of structural change. The chapter concludes with a critique of the SBTC hypothesis,

including alternative explanations for the observed changes in the skill structure of advanced

economies, such as trade and organisational change.

Issues of skill measurement are examined in Chapter 7 and a shift-share model for measuring

skill change in the Australian economy is outlined.

6

The results of the shift-share analysis are presented and discussed in Chapter 8. Chapter 9

presents the estimation of a model showing the determinants of intra-industry skill change.

Chapter 10 presents the conclusions, major findings and policy implications of the thesis. The

chapter concludes with an overview of avenues for further research.

This thesis embodies all of the previously published work by the author and expands on this

through more thorough and extensive exploration of the subject matter. It builds on previously

published material by the author by estimating the determinants of skill change for motor,

interactive and education skills, whereas previous work was limited to the measurement of

cognitive skills. The thesis also provides an expanded discussion of policy implications and

future research directions.

7

2 INFORMATION AND COMMUNICATION

TECHNOLOGIES (ICT) AND THE ECONOMY

2.1 Introduction

The Australian economy, like most advanced and developing economies around the

world, has witnessed a massive growth in ICT since the early 1990s in many forms.

Examples include interfaces for electronic data interchange devices (EDI), such as

Electronic Funds Transfer Point of Sale (EFTPOS), Automatic Teller Machines

(ATM), microelectronic scanning devices and global positioning systems (GPS). The

scanning of products being in supermarkets rather than manually keying the prices

has increased the speed of processing customers at checkout counters. ATMs have

substantially reduced the number of face-to-face transactions in banks and GPS has

revolutionised the fishing and agriculture industries as well as transport and logistics.

The latter improves ‘just-in-time’ manufacturing, driving down inventory levels,

reducing costs and improving efficiency. In addition, the spread of computers has

increased to a point where they could now be considered to be pervasive technology.

Moreover, the introduction of the Internet and its increasing speed, quality and the

applications it now supports, is having a radical effect on the economy and ultimately

the skill structure.

In this chapter the main focus is on outlining some of the key developments and

supporting evidence of their diffusion in the economy.

8

2.2 Growth of the Internet

Perhaps the most telling indication of the rapid rise of the Internet is the relatively

short period of time it took to reach 50 million people in the United States (US).

Radio took 38 years, television 13 years and cable television 10 years; the Internet

only took 5 years (Rayport and Jaworski 2001). In 1997 only 32 per cent of the

largest 500 companies in the US1 had any kind of Internet presence. In 1998 that

figure had grown to 82 per cent (Chief Executive 1999, p.8).

Table 2-1 World Internet Usage and Population by Region, June 2009

World Regions Population

( 2009 Est.)

millions

Internet Users

Dec. 31, 2000

millions

Internet Users

2009

Penetration

(% Population)

Users

Growth

2000-2009

Users

% of

Table

Africa 991 4.5 65.9 6.7 % 1,359.9 % 3.9 %

Asia 3,808 114.3 704.2 18.5 % 516.1 % 42.2 %

Europe 804 105.1 402.4 50.1 % 282.9 % 24.2 %

Middle East 203 3.3 48.0 23.7 % 1,360.2 % 2.9 %

North America 341 108.1 251.7 73.9 % 132.9 % 15.1 %

Latin America/Caribbean 587 18.1 175.8 30.0 % 873.1 % 10.5 %

Oceania / Australia 35 7.6 20.8 60.1 % 173.4 % 1.2 %

WORLD TOTAL 6,769 360.0 1,668.8 24.7 % 362.3 % 100.0 %

Notes:

i. Internet Usage and World Population Statistics are estimates for June 30, 2009.

ii. Demographic (Population) numbers are based on data from the US Census Bureau .

iii. Internet usage information comes from data published by Nielsen On-line, by the

International Telecommunications Union, by GfK, local Regulators and other reliable

sources.

iv. This information has been reproduced from www.internetworldstats.com.

1 Ranked by gross revenue adjusted for excise taxes collected (i.e. these are the ‘US Fortune 500’ companies).

9

By June 2009 the estimated number of people connected to the Internet was 1.7

billion, or 24.7 per cent of the world’s population. In the United States the percentage

of the population with connection to the Internet was 74 per cent, for Australia 60 per

cent and Europe 50 per cent (Internet World Stats n.d.).2

2.2.1 Increase in Internet speeds

The growth of the Internet has been accompanied by increases in download speeds

for Internet traffic as consumers switch from dial-up Internet connections to

broadband Internet connections. A commonly used definition of broadband is a

download speed for data of 144 kilobits per second (Kbs) or greater (Stordahl and

Elnegaard 2007). This represents around a 15 fold or greater increase in data

transmission speeds compared to the superseded dial-up speeds and obviously

increases the appeal and usefulness of the Internet as it expands the number of

applications that it can be used for. In 2007 there were around 43 per cent of Western

European households with a broadband connection to the Internet, this was forecast to

grow to 60 per cent by 2010 (Stordahl and Elnegaard, 2007).

In September 2009 the Australian Government announced a commitment to spend up

to $43bn over an eight-year period to roll out an Australia-wide broadband network,

predominantly fibre-optic cable to individual premises, but with wireless broadband

to cover approximately 10 per cent of households and locations where a fibre-optic

roll-out is not feasible, thus giving effective 100 per cent coverage for Australia and

removing any remaining technical barriers for businesses and consumers to connect

2 Internet World Stats have sourced the information from AC Nielsen.

10

to broadband Internet (Department of Broadband, Communications and the Digital

Economy (DBCDE), 2009).

The introduction of fibre-optic will allow for speeds up to 100 megabits per second

(Mbs), far in excess of the 144 Kbs currently used to define broadband transmission

speeds. Even in areas where wireless will be used the expected speeds are 12 Mbs.

This will in most cases provide substantial increases in data transmission speeds,

enabling real-time carrier grade video, data and voice to be delivered on-line (and

television transmission and movies to be screened) (DBCDE 2009).

2.3 Household Access to the Internet

Early studies of the Internet focused on the issue of who had access, which in turn

defined who could benefit from the expanding array of goods and services available

on-line.

Madden and Savage (2000) using data from a web based survey of Australian Internet

users found a positive relationship between income and Internet usage and that the

probability of greater usage is inversely related to age (see also Soete and Weel

1998). Other studies pointed to education and using a computer at work as being

important indicators of the likelihood of Internet adoption (see, for example,

Goolsbee and Klenow 1999; Greenstein 1998).

A study using 2002-03 European Social Survey data by Demoussis and

11

Giannakopoulos (2006) examines the ‘digital-divide’ for EU countries.3 The main

findings are that income is positively related to Internet usage for people with access

to the Internet. The cost of access and level of education are also positively related.

Importantly, there appears to be structural differences between northern and southern

EU countries. That is, for the same values of the determinants of usage, the rate of

usage was lower in southern Europe4 (Demoussis and Giannakopoulos 2006).

More recent studies (Devins, Darlow and Webber 2008) undertook a study of

households in the UK and their access in terms of participation in eCommerce, such

as on-line banking and shopping and find that women, ethnic minorities, and people

living in less affluent areas utilise these services to a much lower extent, even when

income is controlled for. Women were also considerably less likely to access

information that would enhance or support their social and economic inclusion.

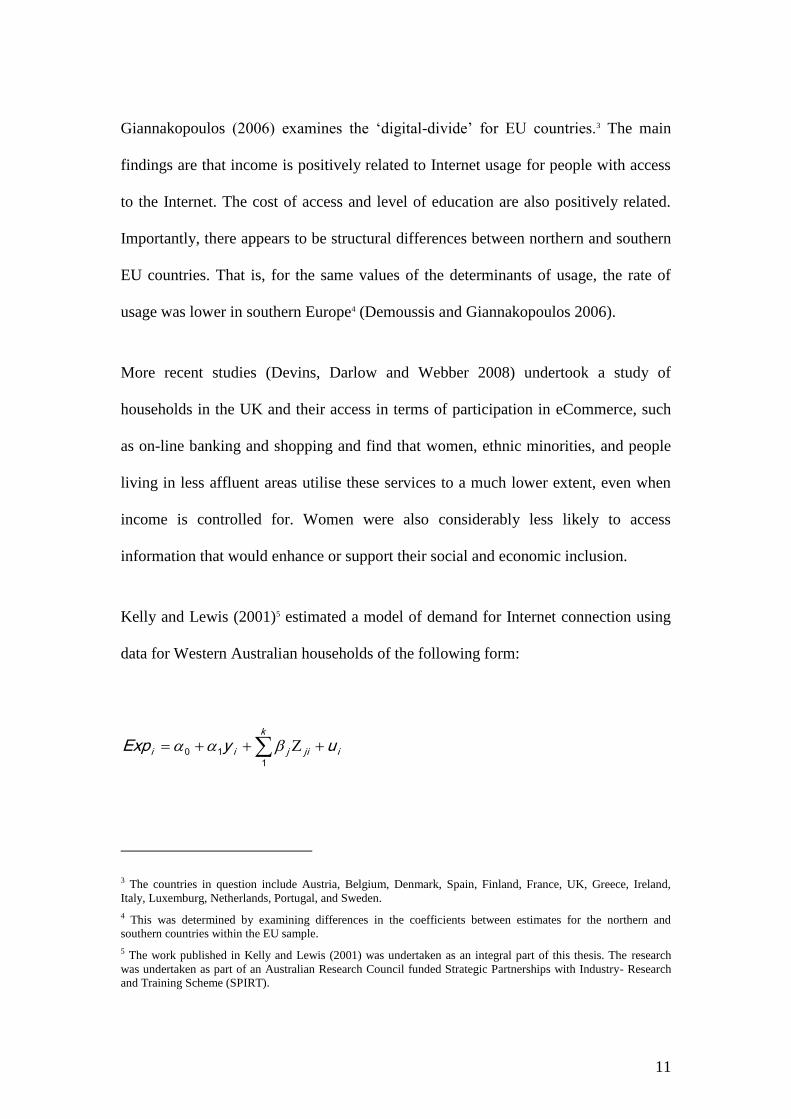

Kelly and Lewis (2001)5 estimated a model of demand for Internet connection using

data for Western Australian households of the following form:

3 The countries in question include Austria, Belgium, Denmark, Spain, Finland, France, UK, Greece, Ireland,

Italy, Luxemburg, Netherlands, Portugal, and Sweden.

4 This was determined by examining differences in the coefficients between estimates for the northern and

southern countries within the EU sample.

5 The work published in Kelly and Lewis (2001) was undertaken as an integral part of this thesis. The research

was undertaken as part of an Australian Research Council funded Strategic Partnerships with Industry- Research

and Training Scheme (SPIRT).

i

k

jijii uyExp 1

10

12

where:

Expi is the percentage of households with an Internet connection;

yi is the average household income;

Zji are a set of variables measuring characteristic j in area i;

0, 1, and j are parameters;

ui is an error term, assumed to be independently identically normally distributed with

constant variance.

The dependent variable was Percentage of Households in a Census collection district6

connected to the Internet, while the Z vector included age, non-English speaking

background, percentage of people in a collection district attending university,

percentage attending a technical and further education college (TAFE) and a dummy

denoting region of state.

The key finding of the Kelly Lewis (2001) study was that income, location, age and

education all significantly affected Internet adoption. Poorer neighbourhoods and

certain regions had significantly lower connection rates.

Universal service is an important theme in US government communications policy

and in the past was reflected in telephone networks being extended into rural and low

6 A collection district until 2006 was the base or smallest unit for capturing household information, equating to

approximately 250 households. Note in the 2006 Census that the ABS moved to a different methodology that now

allows for much finer detail for spatial units (ABS 2006a).

13

income areas (Greenstein, 1998). This has also heavily influenced Australian decision

making and was a major issue in the privatisation debate on the national carrier,

Telstra, in the 1990s (see, for example, Doherty and Gratten 2000, Gratten 2000,

Lewis 2000).

Telstra, as the National Universal Service Provider, is responsible for meeting

Universal Service Obligations (USO) under the Telecommunications Act 1997. They

are required to ensure that standard telephone services are reasonably accessible to all

people in Australia on an equitable basis, regardless of where they reside. Their

obligations are to provide voice grade standard telephone services throughout

Australia. Their charter also includes the pursuit of international best practice in the

telecommunications industry, including compliance with relevant industry

performance standards (DCITA 2000).

Recent developments in the national broadband arena (see DCBDE, 2009) will

completely change the USO landscape, as ‘voice over Internet’ (VoIP)7 technologies

will enable cheap and accessible telephone services everywhere.

In the early phases of Internet uptake, issues of access were critical; from both a

social equity perspective and the economics of market penetration facing firms. The

principle factors limiting the use of eCommerce markets in the early phase of

diffusion were physical roll out of the Internet, the question of a means of secure

payment, trust, consumer protection, and the ability of consumers to access the

7 VoIP is a general term for delivery of voice communications over Internet Protocol (IP) networks such as the

Internet.

14

Internet (OECD 1998a; Kelly and Lewis 2001).

Since 2000 however, computer prices, network coverage, download speeds have all

improved dramatically, public access is widely available at very low cost through

Internet cafes and booths within shopping malls. It would now be the exception,

rather than the norm, for households not to have acceptable levels of access. The final

roll out of the fibre optic broadband network in Australia over the next decade will

confine access largely to an issue of choice.

2.3.1 Current access levels in Australia

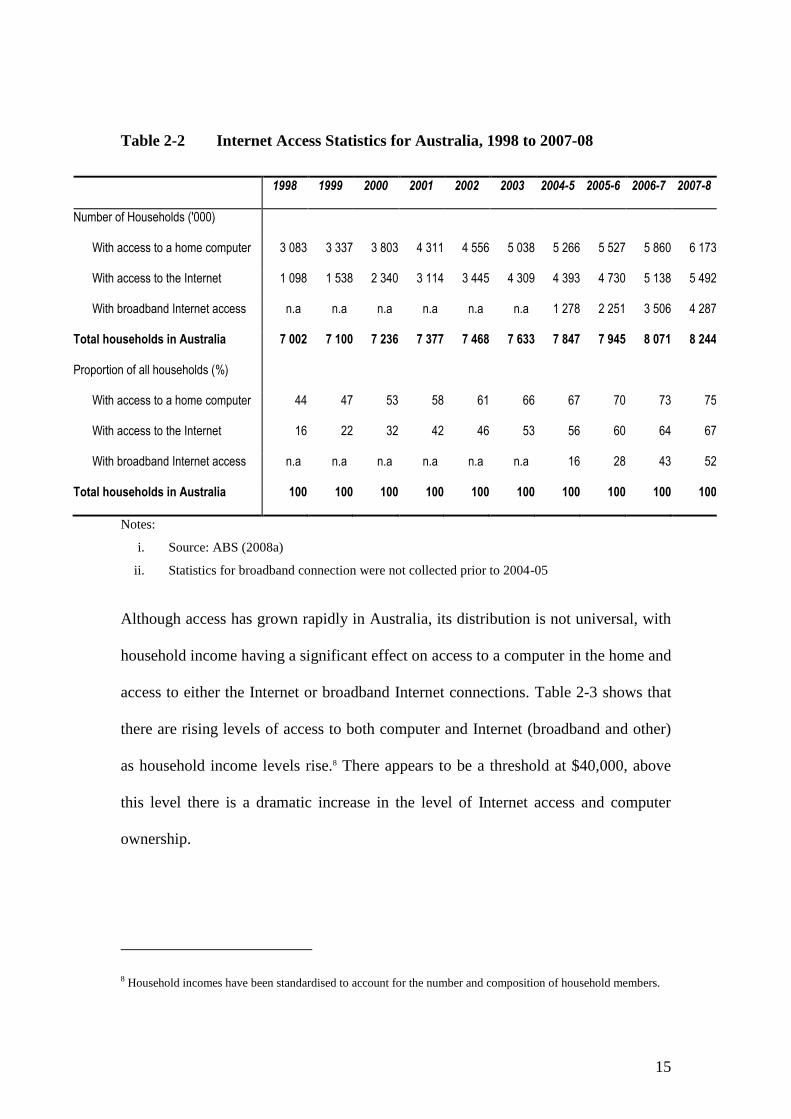

As shown in Table 2-2 there has been a substantial increase between 1998 and 2007-

08 in the number of households with access to a computer, more than doubling over

that period with around 75 per cent of all households in 2007-08 having access to a

computer. Over the same period the number of households with a computer grew by

100 per cent, or 8 per cent per year. Internet access grew by 19.6 per cent per year,

while for the three years that broadband access statistics are available the growth rate

was 49.7 per cent per year. The number of households has been growing at 1.8 per

cent per year. The growth rates for households’ Internet access, in Australia and

especially broadband access, are very large and demonstrate how pervasive it has

become.

15

Table 2-2 Internet Access Statistics for Australia, 1998 to 2007-08

1998 1999 2000 2001 2002 2003 2004-5 2005-6 2006-7 2007-8

Number of Households ('000)

With access to a home computer 3 083 3 337 3 803 4 311 4 556 5 038 5 266 5 527 5 860 6 173

With access to the Internet 1 098 1 538 2 340 3 114 3 445 4 309 4 393 4 730 5 138 5 492

With broadband Internet access n.a n.a n.a n.a n.a n.a 1 278 2 251 3 506 4 287

Total households in Australia 7 002 7 100 7 236 7 377 7 468 7 633 7 847 7 945 8 071 8 244

Proportion of all households (%)

With access to a home computer 44 47 53 58 61 66 67 70 73 75

With access to the Internet 16 22 32 42 46 53 56 60 64 67

With broadband Internet access n.a n.a n.a n.a n.a n.a 16 28 43 52

Total households in Australia 100 100 100 100 100 100 100 100 100 100

Notes:

i. Source: ABS (2008a)

ii. Statistics for broadband connection were not collected prior to 2004-05

Although access has grown rapidly in Australia, its distribution is not universal, with

household income having a significant effect on access to a computer in the home and

access to either the Internet or broadband Internet connections. Table 2-3 shows that

there are rising levels of access to both computer and Internet (broadband and other)

as household income levels rise.8 There appears to be a threshold at $40,000, above

this level there is a dramatic increase in the level of Internet access and computer

ownership.

8 Household incomes have been standardised to account for the number and composition of household members.

16

Table 2-3 Computer and Internet Access by Household Equivalised Income,

Australia, 2007-08

Total number of all

households

Households with

access to a home

computer

Households with

access to the

Internet at home

Households with

access to

broadband at

home

Equivalised household income '000 % % %

$0 - $39,999 3 689 63 53 38

$40,000 - $79,999 2 141 86 79 65

$80,000 - $119,999 513 93 89 76

$120,000 or over 203 94 91 81

Notes

i. Source: ABS (2008a)

ii. Table shows data for the 79.4 per cent of households where an equivalised income could be

determined.

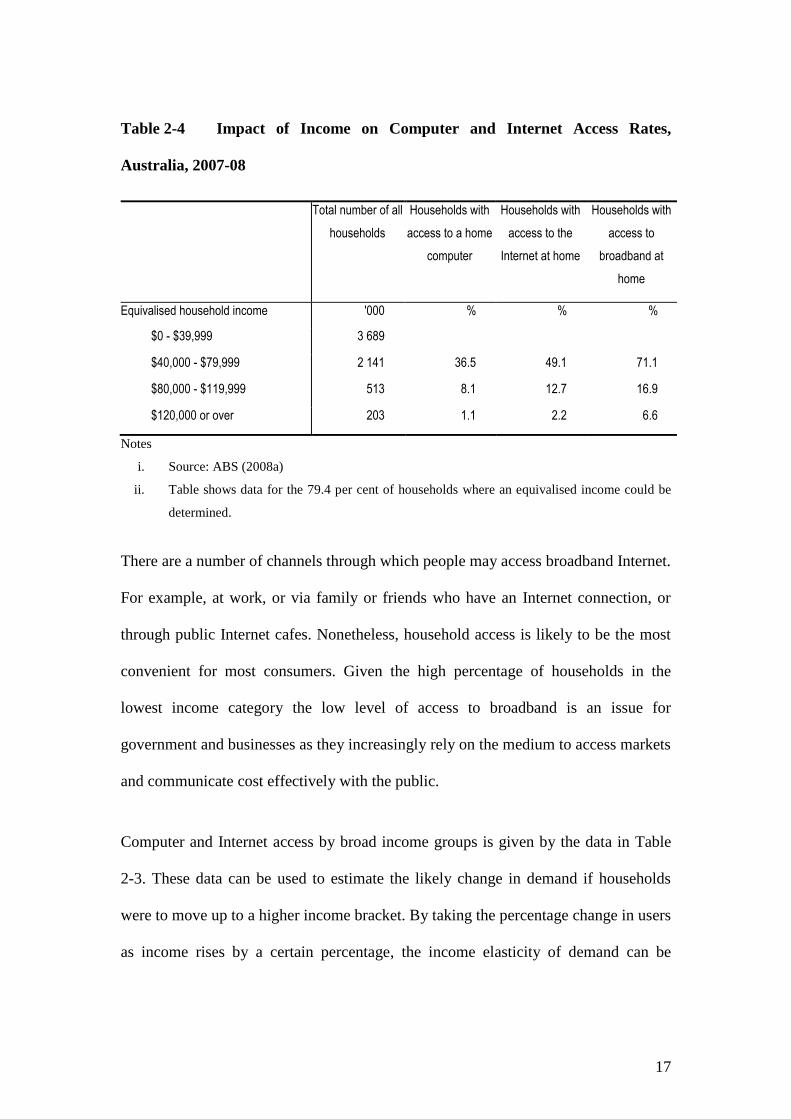

The data shown in Table 2-4 show the increase in access and ownership rates for

Internet and computers, respectively, as the level of household income increases.9 As

income increases from 0–$39,999 to $40,000–$79,999 the computer ownership rate

increases by 36.5 per cent, while the increase to the next income increment shown in

Table 2-4 results in a 8.1 per cent increase in computer ownership. The increase to the

next level of $120,000 and over makes very little difference to household ownership

rates for computers. The impact on access rates for the Internet are more pronounced,

suggesting that Internet access is perhaps considered more of a luxury item by

households than is the case for computer ownership. For broadband connections the

impact is even more dramatic.

9 Measured in Australian Dollars, current prices (as at time of survey in 2007).

17

Table 2-4 Impact of Income on Computer and Internet Access Rates,

Australia, 2007-08

Total number of all

households

Households with

access to a home

computer

Households with

access to the

Internet at home

Households with

access to

broadband at

home

Equivalised household income '000 % % %

$0 - $39,999 3 689

$40,000 - $79,999 2 141 36.5 49.1

71.1

$80,000 - $119,999 513 8.1 12.7

16.9

$120,000 or over 203 1.1 2.2 6.6

Notes

i. Source: ABS (2008a)

ii. Table shows data for the 79.4 per cent of households where an equivalised income could be

determined.

There are a number of channels through which people may access broadband Internet.

For example, at work, or via family or friends who have an Internet connection, or

through public Internet cafes. Nonetheless, household access is likely to be the most

convenient for most consumers. Given the high percentage of households in the

lowest income category the low level of access to broadband is an issue for

government and businesses as they increasingly rely on the medium to access markets

and communicate cost effectively with the public.

Computer and Internet access by broad income groups is given by the data in Table

2-3. These data can be used to estimate the likely change in demand if households

were to move up to a higher income bracket. By taking the percentage change in users

as income rises by a certain percentage, the income elasticity of demand can be

18

estimated.

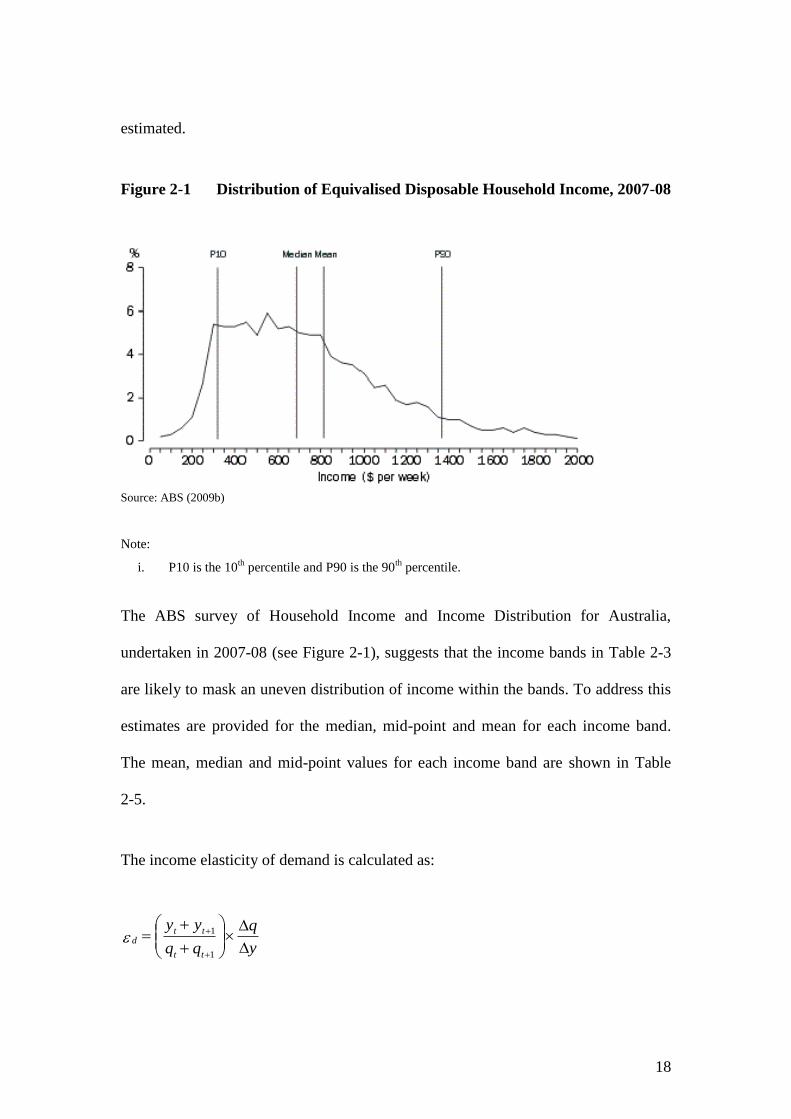

Figure 2-1 Distribution of Equivalised Disposable Household Income, 2007-08

Source: ABS (2009b)

Note:

i. P10 is the 10th

percentile and P90 is the 90th

percentile.

The ABS survey of Household Income and Income Distribution for Australia,

undertaken in 2007-08 (see Figure 2-1), suggests that the income bands in Table 2-3

are likely to mask an uneven distribution of income within the bands. To address this

estimates are provided for the median, mid-point and mean for each income band.

The mean, median and mid-point values for each income band are shown in Table

2-5.

The income elasticity of demand is calculated as:

y

q

yy

tt

ttd

1

1

19

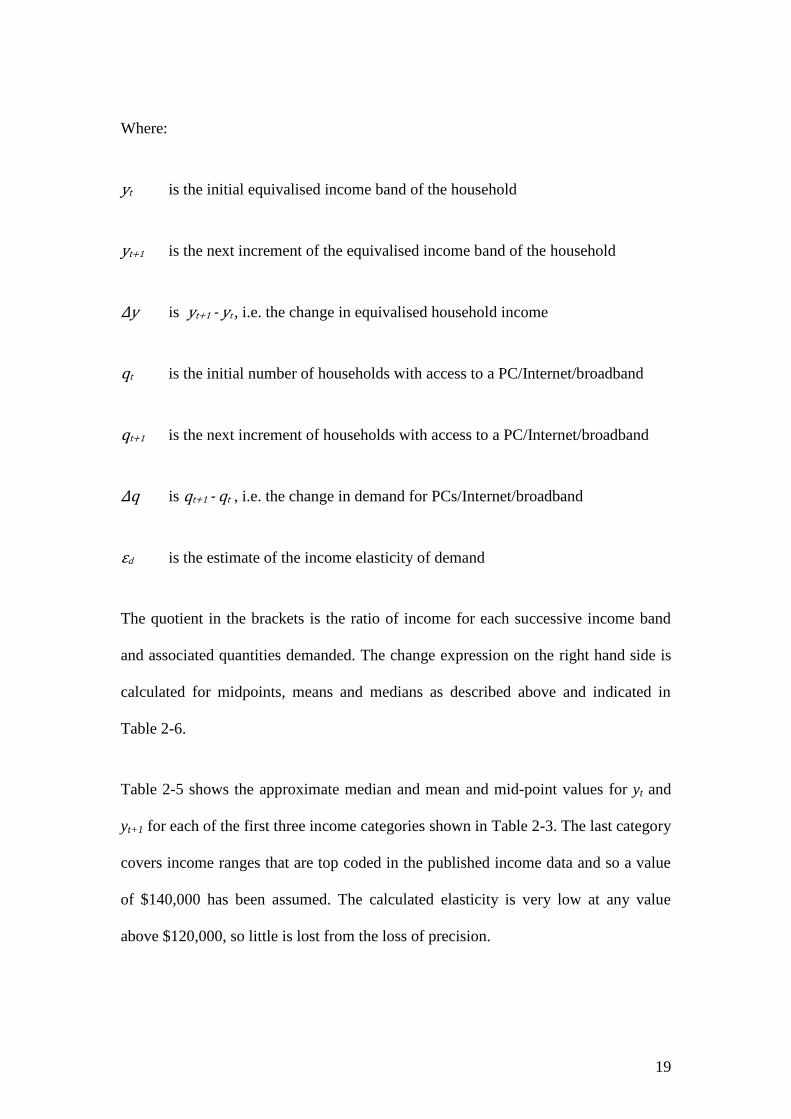

Where:

yt is the initial equivalised income band of the household

yt+1 is the next increment of the equivalised income band of the household

Δy is yt+1 - yt , i.e. the change in equivalised household income

qt is the initial number of households with access to a PC/Internet/broadband

qt+1 is the next increment of households with access to a PC/Internet/broadband

Δq is qt+1 - qt , i.e. the change in demand for PCs/Internet/broadband

εd is the estimate of the income elasticity of demand

The quotient in the brackets is the ratio of income for each successive income band

and associated quantities demanded. The change expression on the right hand side is

calculated for midpoints, means and medians as described above and indicated in

Table 2-6.

Table 2-5 shows the approximate median and mean and mid-point values for yt and

yt+1 for each of the first three income categories shown in Table 2-3. The last category

covers income ranges that are top coded in the published income data and so a value

of $140,000 has been assumed. The calculated elasticity is very low at any value

above $120,000, so little is lost from the loss of precision.

20

Table 2-5 Annual Equivalised Income, Australia, 2007-08, ($A, current

prices)

Income band method yt yt+1

low median 27,600 57,800

mean 26,200 57,400

mid point 20,000 60,000

medium median 57,800 100,000

mean 57,400 100,000

mid point 60,000 100,000

high median 100,000 140,000

mean 100,000 140,000

mid point 100,000 140,000

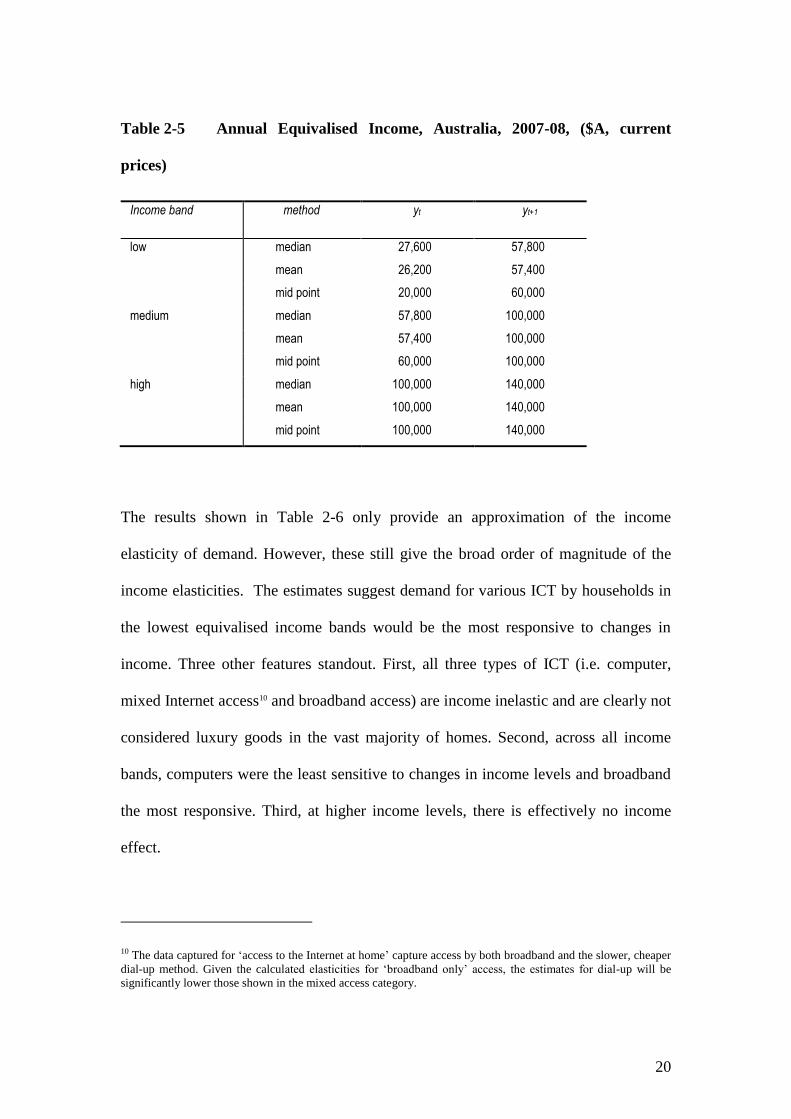

The results shown in Table 2-6 only provide an approximation of the income

elasticity of demand. However, these still give the broad order of magnitude of the

income elasticities. The estimates suggest demand for various ICT by households in

the lowest equivalised income bands would be the most responsive to changes in

income. Three other features standout. First, all three types of ICT (i.e. computer,

mixed Internet access10 and broadband access) are income inelastic and are clearly not

considered luxury goods in the vast majority of homes. Second, across all income

bands, computers were the least sensitive to changes in income levels and broadband

the most responsive. Third, at higher income levels, there is effectively no income

effect.

10 The data captured for ‘access to the Internet at home’ capture access by both broadband and the slower, cheaper

dial-up method. Given the calculated elasticities for ‘broadband only’ access, the estimates for dial-up will be

significantly lower those shown in the mixed access category.

21

Table 2-6 Income Elasticity of Demand for Selected Household ICT,

Australia, 2007-08

Income band method Households with

access to a home

computer

Households with

access to the Internet

at home

Households with

access to broadband

at home

low median 0.47 0.60 0.79

mean 0.41 0.53 0.70

mid point 0.31 0.39 0.52

medium median 0.13 0.20 0.27

mean 0.14 0.22 0.29

mid point 0.16 0.24 0.31

high median 0.03 0.07 0.19

mean 0.03 0.07 0.19

mid point 0.03 0.07 0.19

Notes:

i. Based on household equivalised income.

ii. Insufficient information was available to modify the top coded income band. This also applies

to the $80,000 to $119,999 category, although what information was available suggests the

mean exceeds $100,000.

iii. Note that the survey timing implies that households are faced with the same vector of prices

for the ICT items shown.

iv. The calculated elasticities are an approximation of aggregate behaviour and relate to whether

there is access in the household or not. The calculated elasticities do not take into account the

volumes and quality that households might consume. For example, some households may

have large download quotas on their broadband accounts, or have access to faster speeds.

Similarly, computers come in many different specifications affecting the speed, computing

power, storage and facilities (e.g. DVD players, extra installed software etc.)

2.3.2 International comparison of broadband access

Compared to other countries Australia is towards the upper end of Internet and

broadband access. The ABS (2007a) shows the broadband access data available in

2007 for selected countries made up of Organisation for Economic Co-operation and

Development (OECD) and European Union (EU) members. The uptake of broadband

22

Internet connections varies widely, ranging from Korea with 94 per cent to under 2

per cent for Turkey. The number of Australian households with broadband access at

home was around 52 per cent, compared to the EU average of just over 43 per cent.

Australian access levels were very similar in 2007 to Switzerland, the US and

Germany. The northern European economies, such as Denmark, the Netherlands,

Sweden and Belgium tended to be much higher. Eastern and Southern EU economies,

such as the Czech and Slovak Republics, Greece, Italy and Turkey tended to be at the

lower end of access rates.

2.4 The Economics of eCommerce

The Internet and eCommerce has been widely lauded as a medium that has changed

and will continue to change the face of the economy. It has provided a new medium

through which businesses, consumers and government interact with each other. It has

also provided new ways to organise, to produce and to sell. However, for this to have

happened there must have been a compelling economic reason. As Shapiro and

Varian (1999) point out, the technologies may have changed, but the economics has

not.

2.4.1 eCommerce defined

The term eCommerce essentially means using ICT to support business activities.

Currently, there are a number of descriptions of eCommerce. Some examples are

transactions conducted over the telephone and fax machine, electronic payment and

money transfer systems, electronic data interchange and the Internet (DIST 1998).

The OECD (1998a) defined eCommerce as:

23

business occurring over networks which use non-proprietary protocols that are

established by an open standard setting process such as the Internet. (p.1)

A contemporary textbook definition describes it as follows:

Technology-mediated exchanges between parties (individuals, organisations, or

both) as well as the electronically based intra- or inter-organisational activities that

facilitate such exchanges. (Rayport and Jaworski, 2001, p.3)

There are also alternative terms like ‘eBusiness’, ‘Internet business’ and ‘Internet

commerce’. The term ‘business’ can also be extended broadly to include both

networked activity between, and within, economic units like firms, households and

government agencies (Shapiro and Varian 1999).

In the Australia’s Digital Economy: Future Directions Final Report a slightly broader

definition encompasses the eCommerce definitions provided above within the rubric

of the ‘digital economy’ (Department of Broadband, Communications and the Digital

Economy (DBCDE) 2009, p.2):

The Australian Government defines the digital economy to be:

‘The global network of economic and social activities that are enabled by information

and communications technologies, such as the Internet, mobile and sensor networks.’

The latest definition of eCommerce provided by the OECD (2006) is as follows:

An Internet transaction is the sale or purchase of goods or services, whether between

businesses, households, individuals, governments, and other public or private

organisations, conducted over the Internet. The goods and services are ordered over

the Internet, but the payment and the ultimate delivery of the good or service may be

conducted on or off-line. (p. 14)11

11 Note that this definition includes orders received or placed on any Internet application used in automated

transactions such as Web pages, Extranets and other applications that run over the Internet, such as EDI over the

Internet, Minitel over the Internet, or over any other Web enabled application regardless of how the Web is

accessed (e.g. through a mobile or a TV set etc.). The definition excludes orders received or placed by telephone,

facsimile, or conventional e-mail. This is the ‘narrow’ definition of eCommerce used by the ABS for its surveys

on business use of ICT (see ABS 2009c).

24

All of the definitions outlined above encompass the types of developments that

appear to be driving substantial changes in the structure of the economy in terms of

outputs, consumption patterns, production technology and skills over the last two

decades, and especially over the last five to ten years.

2.4.2 Consumer behaviour

Koivumäki et al. (2002) use theoretical consumer behaviour models to demonstrate

the conditions under which Internet based purchasing and consumption will prevail

over traditional forms. They break down the process of purchasing into time spent on

shopping and the emotional experience related to shopping.

Koivumäki et al. (2002) argue that the Internet is primarily an information and

communication tool, regardless of the goods being traded. Therefore, an information

intensive approach will perform best. On-line sites must provide both a wide variety

of information and the means to interact with it.

The potential changes in consumer behaviour in response to on-line shopping

outlined by Koivumäki et al. (2002) are:

part of the consumer basket is bought on-line, but underlying preferences do

not change (i.e. the shape of the consumer’s indifference curve is unaffected).

These items typically will be highly homogenous between the shopping

mediums, such as music downloads or groceries;

The consumption bundle changes due to a change in a constraint, such as time

or money. This could be due to the prices of on-line goods becoming cheaper,

25

or because on-line shopping may provide more time for leisure related

commodities.

Finally, the switch to on-line goods may change both the effective constraints

on consumption as well as the underlying preference structure in response to a

wider array of consumption possibilities opened up by the Internet.

In summary, it is the ‘full cost of goods’ that takes into account the consumer’s time

allocation, prices, attributes and money income as well as tastes and preferences, that

determines the decision between purchasing goods on-line or in physical stores. The

Internet and complementary technologies including search engines like Google™

lends itself to minimising the time cost of consumption by streamlining search costs.

Given that the purchases can take place in the comfort of the home or at work, the

experiential nature of purchasing may also be altered. Finally, if the economics is

compelling, and the goods and services are available, then the expectation is that

there will be a rise in on-line sales. As shown in subsequent sections, this is borne out

by the evidence.

2.4.3 Contestability of markets

One mechanism that has enabled the growth of Internet based business and

businesses12 is that it promotes competition through low sunk costs. Low sunk costs

reduce the consequences of failure and therefore barriers to entry are also lowered. It

12 Some firms utilise the Internet to conduct business for some or all of its products and services. This may be just

one of the many channels through which they make sales; banks and newspapers fall into this category. However,

there will also be businesses that only operate within an on-line environment. Examples include on-line auction

sites such as ‘eBay’, or Amazon books.

26

potentially reduces the cost of exit and the ‘break even’ constraint as well (see

Schwartz 1986), giving rise to so-called ‘hit and run’ entry into markets. This has also

been assisted by the reduction in scale required to compete with existing firms (Goel

and Hseih 2002).

2.4.4 Market segmentation and consumer surplus

Shapiro and Varian (1999) describe the concept of ‘versioning’ to explain how the

consumer surplus can be captured for different market segments for various

information goods – goods that can be turned into a digital or electronic form, such as

text, music, and software. One of the characteristics of these goods is that they have

high fixed costs, or, to put it another way, the cost of the first copy produced is very

high. The marginal cost of such goods is very low. Versioning provides the means by

which variants of the underlying product can be sold to a wider audience to help

cover the initial copy or fixed costs. It allows different pricing to each segment of the

market depending on whether they have a high or low value for the product, and

everything in between.

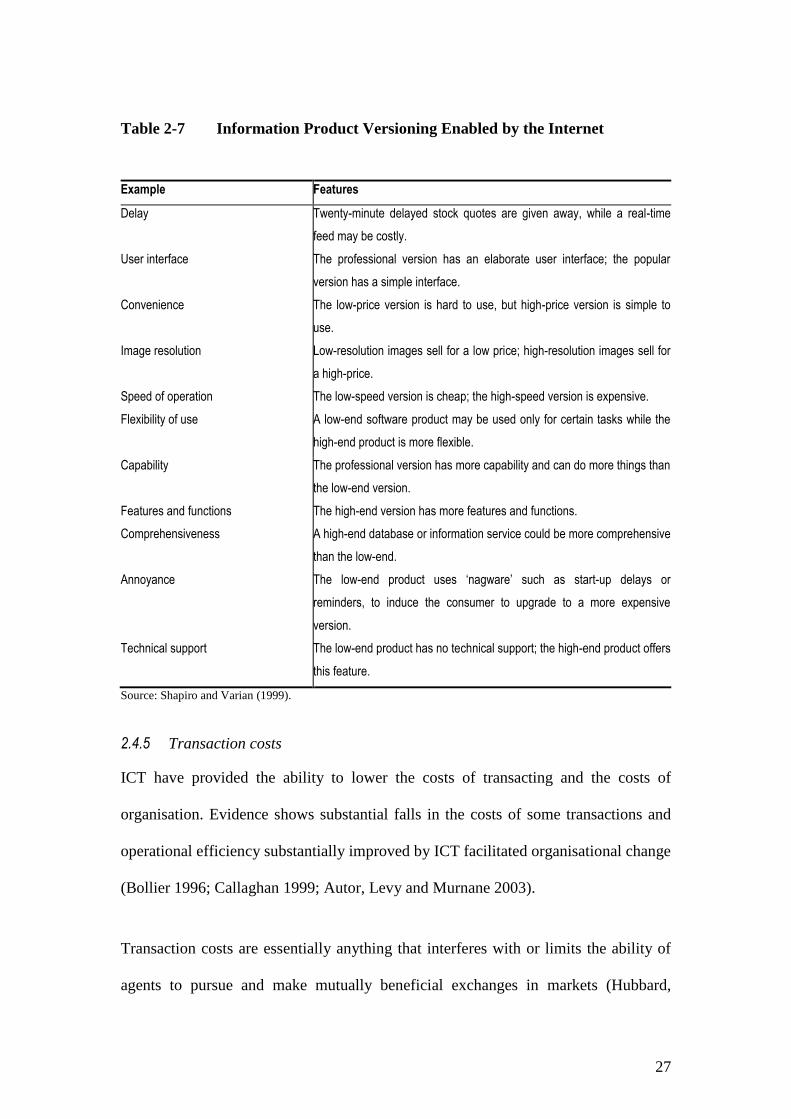

Shapiro and Varian (1999) argue that although versioning is a common strategy for

conventional information goods, such as when movies come out in theatres at a high

price per view and are then released six months later in home video, the flexibility of

digital media has enabled new forms of versioning. Examples of versioning are

shown in Table 2-7.

27

Table 2-7 Information Product Versioning Enabled by the Internet

Example Features

Delay Twenty-minute delayed stock quotes are given away, while a real-time

feed may be costly.

User interface The professional version has an elaborate user interface; the popular

version has a simple interface.

Convenience The low-price version is hard to use, but high-price version is simple to

use.

Image resolution Low-resolution images sell for a low price; high-resolution images sell for

a high-price.

Speed of operation The low-speed version is cheap; the high-speed version is expensive.

Flexibility of use A low-end software product may be used only for certain tasks while the

high-end product is more flexible.

Capability The professional version has more capability and can do more things than

the low-end version.

Features and functions The high-end version has more features and functions.

Comprehensiveness A high-end database or information service could be more comprehensive

than the low-end.

Annoyance The low-end product uses ‘nagware’ such as start-up delays or

reminders, to induce the consumer to upgrade to a more expensive

version.

Technical support The low-end product has no technical support; the high-end product offers

this feature.

Source: Shapiro and Varian (1999).

2.4.5 Transaction costs

ICT have provided the ability to lower the costs of transacting and the costs of

organisation. Evidence shows substantial falls in the costs of some transactions and

operational efficiency substantially improved by ICT facilitated organisational change

(Bollier 1996; Callaghan 1999; Autor, Levy and Murnane 2003).

Transaction costs are essentially anything that interferes with or limits the ability of

agents to pursue and make mutually beneficial exchanges in markets (Hubbard,

28

Garnett, Lewis and O’Brien 2009). Organisational costs are anything that inhibits the

ability of agents to consciously coordinate their activity to achieve some understood

object within a single economic entity, that is, a particular firm, household or

government agency.

Bollier (1996) provides some of the earliest estimates of the cost of a transaction

undertaken through different mediums. For example, it has been estimated for the US

computer software industry that seller transaction costs were $US15 for face-to-face

transactions, $US5 for telephone transactions, and between $US0.20 and 0.50 cents

for Internet transactions. A set of Australian estimates for 1998 puts the transaction

costs for a sales representative visit at $A300, a customer initiated face-to-face

transaction at $A25 to $A30, a telephone transaction at $A4 to $A8, and an Internet

transaction at less than 25 cents (Callaghan 1999, p30). These estimates put the cost

of eCommerce transactions for sellers at something in the order of 3 to 6 per cent of

the cost of telephone transactions and 1 per cent or less for face-to-face transactions.

One transaction cost related hypothesis refers to the reduction of the cost of economic

activities in remote areas using information technologies, thereby reducing the need

for urban agglomeration.13 A study by de Blasio (2008) examined data on Italian

households' usage of the Internet, eCommerce, and e-banking to test this theory and

concluded that the Internet did not reduce the role of distance. The main findings

were that geographically remote consumers were discouraged from purchasing goods

on-line because they could not look at goods before they purchased them. Where the

13 Also known as the ‘global–village hypothesis’, ‘Internet/cities’ and ‘death of distance’ (de Blasio, 2008, p.341).

29

goods were amenable to download, such as music, books, and tickets to events, use of

the on-line purchasing was higher than for metropolitan users. Surprisingly, electronic

banking was not related to geographic factors, the reason being that non-urban

customers gave more importance to personal interaction than urban clients, in part

because they were more likely to have taken out a loan.14

Only 15 per cent of the households in the sample used by de Blasio (2008) indicated

they bought goods and services over the Internet in the year of the survey. Moreover,

only 5 per cent of the households surveyed had used Internet banking. One reason for

the low usage of Internet banking might be due to the full suite of financial services

not being available on the Web. With the only means of accessing a comprehensive

range of services through direct access to a physical bank branch, consumers will be

less inclined to use Internet banking services.

It should be noted that the de Blasio (2008) study was based on 2002 survey data for

Italy. The relative maturity and sophistication of the products, services and

information on-line, ease of making an on-line transaction, data download speeds and

security for on-line transactions have all advanced significantly since 2002. The same

study undertaken in 2009 may yield different results. For example, developments in

Australia have demonstrated a significant expansion of the capability of Internet

banking. In February 2009 the Commonwealth Bank of Australia (CBA) introduced

their ‘First On-line’ service. They claim to have made transactions effectively ‘real-

time’, with full approval of home loan ‘top-ups’ reducing from 14-22 days to 15

14 The inference is that they have ‘preference’ for personal interaction because of previous complex transactions

(i.e. taking out a loan) requiring face-to-face interaction (see de Blasio 2008).

30

minutes (DBCDE, 2009).

There has been a switch in emphasis by CBA in the purpose of the Internet banking

service they provide. When first established in the late 1990s it was intended to

provide a third node of access, a complement to telephone banking and ATMs for the

more routine transactions. The latest transformation is intended to provide fully

linked access across all consumer accounts with one point of access ‘full self-

service’, thus avoiding the need to go into a branch or contact a call centre (DBCDE,

2009).

Another area that has seen substantial falls in transaction costs is stock market

transactions, especially for individual trading. A cross-sectional study of US

households by Bogan (2008) found a 7 per cent increase in the probability of owning

stock in retirement-age households. Between 1992 and 2004 the participation rate in

stock ownership increased from 31.2 per cent among US households to 34.7 per cent,

due mostly to the advent of on-line trading. Bogan (2008) reports data for a large US

stock market broker with 8 million actively trading clients in 2002. Prior to 1992

none of the trades made by clients were made on-line, by 2002 80 per cent of their

clients’ trades were made on-line. The cost of on-line trades was up to 79 per cent

lower than broker-assisted trades, the differentials being much higher for low volume

trading.15 A Swedish study of on-line trading through an Internet discount brokerage

firm showed that small investors tended to perform much worse than the overall

market, by around 8.5 per cent per year, half of which was due to trading costs. The

15 Data cited in Bogan (2008) are for October 2000 and include E*Trade, Ameritrade, Schwab, Datek and CSFB

Direct.

31

inference is that this is due to excessive trading among small stockholders (Anderson

2007). Despite low transaction fees, the increased volume of trades relative to gains

and losses per trade has had an adverse impact on returns.

In 2002 National Office of the Information Economy (NOIE) undertook a review of

the Commonwealth Government’s ‘e-government’ programs delivering on-line

services (NOIE 2003). The study considered the economic, financial and social

benefit/cost ratio for 38 e-government programs. The study found that of the 24

programs where a net financial benefit was expected the observed aggregate

benefit/cost ratio was 92.5 per cent. For the remaining programs the ratio was 61 per

cent. It was estimated that the benefits to the users of these services was $1.1 billion

dollars in 2002 (NOIE 2003)16.

2.4.6 Business-to-business (B2B) transactions

Productivity gains from B2B electronic commerce may be realised through cost

efficiencies from automation of transactions; competition provided by new market

intermediaries, consolidation of demand and supply through organised exchanges,

and improved vertical integration within firms (Lucking-Reiley and Spulber 2001).

The core innovation provided by the Internet is its role as an information and

communication tool, regardless of the goods being traded (Koivumäki et al. 2002). It

is through the separation of physical and information flows connected with each

transaction that the Internet provides an alternative way to trade goods and services,

16 Current dollar estimates.

32

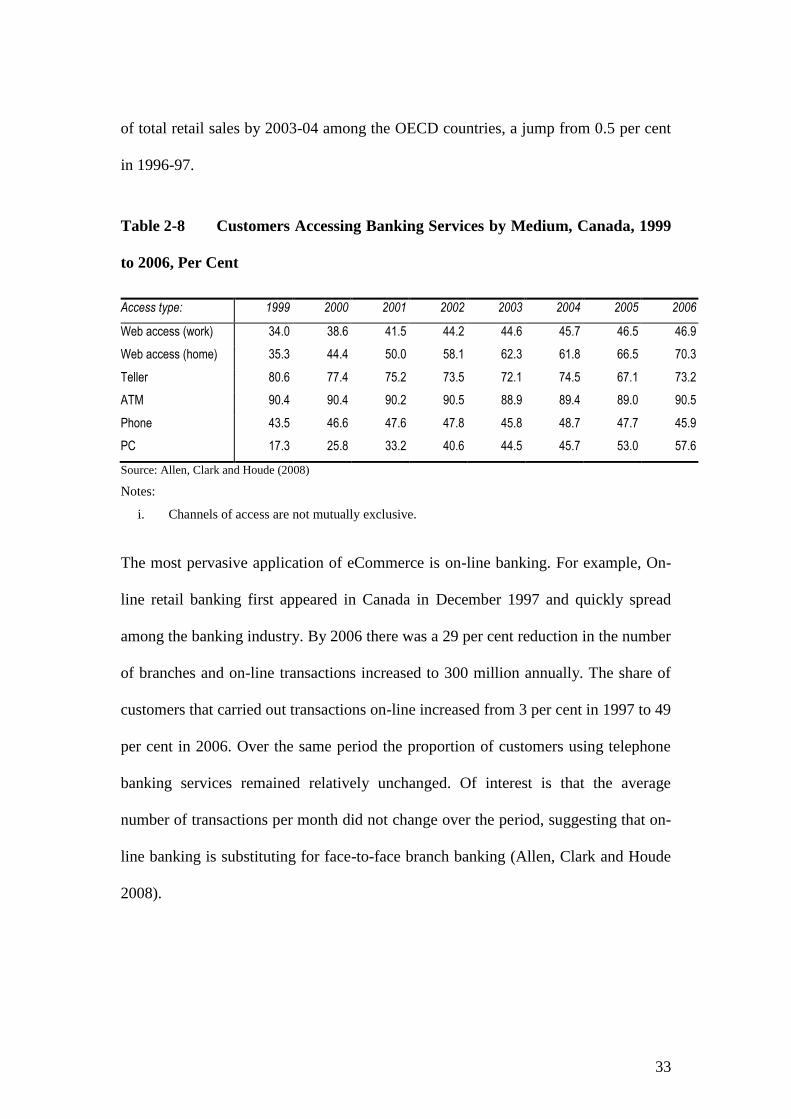

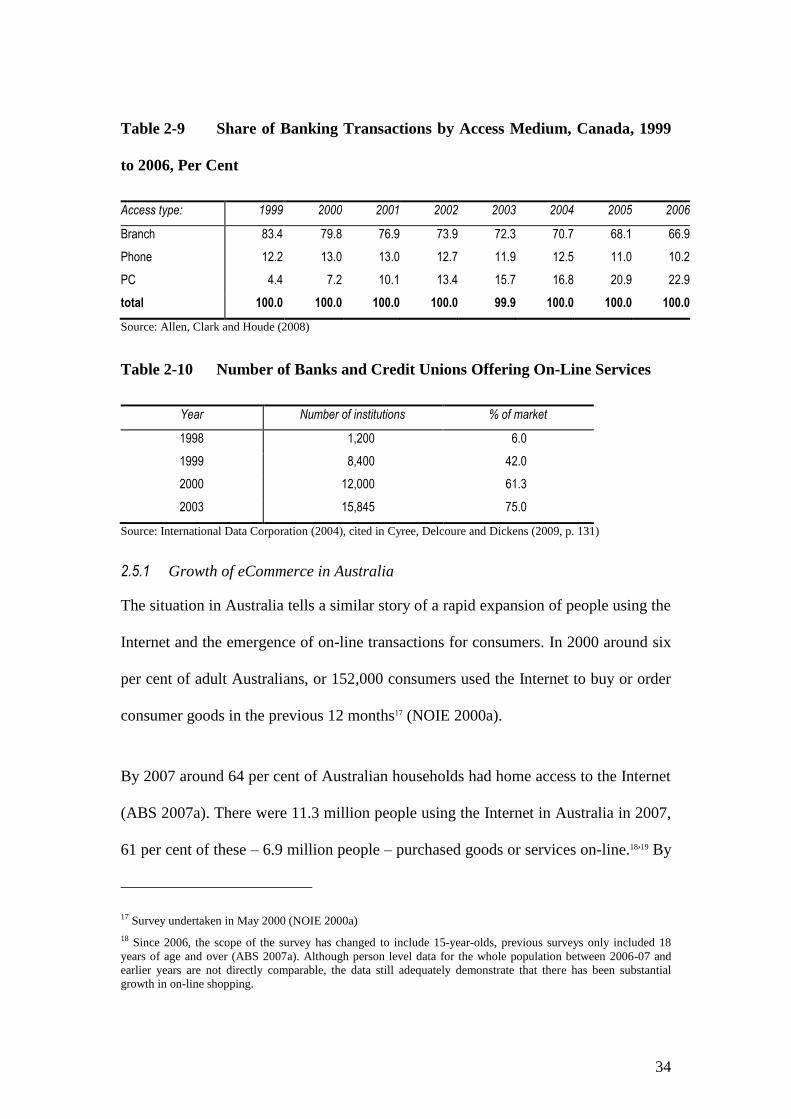

with the transaction cost ultimately determining the choice of selling medium

(Garicano and Kaplan 2001).

Coordination costs are ‘...those `related to the need to determine prices and other

details of the transaction, to make the existence and location of potential buyers and

sellers known to one another, and to bring the buyers and sellers together to transact’

(Garicano and Kaplan 2001, p.463). Improved coordination costs can lower

transaction costs.

Garicano and Kaplan (2001) analysed the transaction costs of the wholesale used car

market in the US, which records around 9 million vehicle sales per year (as of 1999)

at an average value of just under $US14,000. They found that the costs of

coordinating sales and processing the final transactions were reduced by 80 per cent,

or the equivalent of 5 per cent of the car value.

Given price advantages of these magnitudes at the onset of the ‘on-line revolution’,

the massive growth in uptake that has been observed for business and consumers is

uncontroversial and predictable.

2.5 Growth of eCommerce

In 1991 there were fewer than 3 million Internet users worldwide. By 1999 this had

swelled to 250 million, with around a quarter making on-line purchases valued at

around $US110 billion (Coppel 2000). The OECD (1998a) forecast eCommerce sales

among OECD countries would jump from $US26 billion in 1996-97 to $US1,000