student report notebook kit (cover, binder spine, divider...

TRANSCRIPT

C OV E N A N T U N I V E R S I T Y

T U T O R I A L K I T

P R O G R A M M E : A C C O U N T I N G

O M E G A S E M E S T E R

3 0 0 L E V E L

LIST OF CONTENTS

ACC 321: : FINANCIAL ACCOUNTING IV

ACC323: AUDITING PRINCIPLE AND PRACTICE

ACC325: : NIGERIAN TAXATION 1

ACC329: ACCOUNTING LABORATORY III

COVENANTUNIVERSITY CANAANLAND, KM 10, IDIROKO ROAD

P.M.B 1023, OTA, OGUN STATE, NIGERIA.

TITLE OF EXAMINATION: OMEGA SEMESTER EXAMINATION

COLLEGE: BUSINESS AND SOCIAL SCIENCES

DEPARTMENT: ACCOUNTING

SESSION: 2015/2016 SEMESTER: OMEGA

COURSE CODE: ACC 321 CREDIT UNIT: 3

COURSE TITLE: FINANCIAL ACCOUNTING IV

INSTRUCTION: ANSWER ALL QUESTIONS IN SECTION A AND B TIME: 3 HOURS

SECTION A - MULTIPLE CHOICE QUESTIONS (Total=20 marks)

Which of the following ledgers is opened in the books of the Head Office when branch sells goods on credit to the Head office?

Branch debtors b. Branch stock c. Branch cash and bank d. Branch expense account

The total long term debt of a business is N37,650. The Shareholders’ funds is N120,000. Which of the following options correctly

shows the long-term debt to shareholders’ fund ratio?

1:0.31 b. 1.31:1 c. 31.37 percent d. 131 percent

Which of the following options best describes current ratio?

Current Assets Less Current Liabilities

Current Assets plus Current Liabilities

Current Assets divided by Current Liabilities

Current Assets multiplied by Current Liabilities

Use the information below to answer question 4.

The following information has been extracted from the books of Fabulous Construction Ltd. For the year ended 31st

December

2010 in respect of an office block commissioned by the Imagine Development Corporation.

The following expenses were incurred during the year 2010: Plant N150; Wages N260; Materials N330; Subcontract work N200;

Sundries N30; Contract overheads 240

Balances at 31st

December 2010 were: Plant N100; Materials N50.

Work awaiting certification at 31st

December 2010 is N20.

The amount of work certified is ………………..

N1,210 b. N1,040 c. N1,060 d. N1,100

Use the following information to answer questions 5 and 6.

Lacruise commenced a voyage on 1st

May 2009 from Lagos to Nairobi and back. The voyage was completed on 30th

June 2009.

Lacruise carried 200 persons to Nairobi and 180 persons from Nairobi to Lagos. The ship was yet to be insured. Other information

are:

Salaries and wages of two (2) ship maintenance officers and five (5) ship cleaners amount to N800,000.

Port dues amounts to N400,000.

The passage money amounted to N20,000 each.

Depreciation amounts to N450,000.

Consumables utilized for the purpose of the voyage amounted to N300,000.

The total passage money for the voyage is……………………..

N4 million b. N3.2 million c. N3.6 million d. N7.6 million

The profit on the voyage is ………………………..

N3.35 million b. N7.6 million c. N5.65 million d. N5.75 million

Which one of the following options is not an agricultural activity?

Raising livestock b. Stud farms c. Forestry d. Managing game parks

According to IAS 41 there are two instances where the standard permits departure from current fair value. What are these two

instances?

When the asset is still in use beyond the fifth year of its estimated useful life and fair value cannot be measured reliably

When the asset’s estimated useful life cannot be ascertained correctly and fair value cannot be measured reliably

When the asset’s life is at the early stage and fair value cannot be measured reliably

When the asset is at an early stage, the asset falls under the category of endangered species and fair value cannot be measured

reliably

According to IAS 41, which of the following options best describes fair value?

Price for the asset in an active market

Recent transaction price for the asset if there is an active market

Market prices for similar assets

Present value of the future cash flows expected to be generated from the asset

i, ii and iv b. i, iii and iv c. ii, iii and iv d. All of the above

Use the information below to answer questions 10 and 11.

As at 31st

December, 2014 the following information was extracted from the books of Banana Gardens Nigeria Plc:

N’000

Authorized share capital 50,000

Issued and fully paid:

Ordinary shares @ N1 per share 54,000

Creditors 3,000

Investment (market value) 6,900

Freehold land for sale (at cost) 9,600

The opening bank balance as at 1st

January, 2014 was N4,520,000.

Additional information:

Proceeds from the sale of Arena amounted to N3 million.

Proceeds from the sale of Land amounted to N6million.

Investment income N300,000.

Dividend paid to shareholders amounted to N2.7 million.

Payments to trade creditors amounted to N250,000.

Profit for the year stands at N10.37million

Property, plant and equipment of the business is valued at N40 million.

What is the amount of balance carried down on the bank account of Banana Gardens Plc as at 31st

December 2014?

N10.87 million b. N13.57 million c. N13.82 million d. N 10.57 million

The total non-current assets of Banana Gardens Plc as at 31st

December 2014 are …….

N67.37 million b. N46.9 million c. N56.5 million d. N65.9 million

Which one of the following is a proprietary ratio?

Shareholders fund divided by Total Tangible Assets

Shareholders fund divided by Total Long-Term Liabilities

Shareholders fund divided by Profit for the Year

Shareholders fund divided by Retained Earnings

Which of the following options is the advance payment by an employer to the contractor to enable the commencement of the

contract work?

Starting Fee

Initial Fee

Mobilization Fee

Prepaid Fee

Which of the following options shows the correct accounting treatment of the advance payment by an employer to the contractor

to enable the commencement of the contract work in the books of the contractor?

The advance payment is treated as an asset and when the contract is fully executed, the payment is treated as revenue.

The advance payment is treated as a liability until the money is fully recovered.

The advance payment is treated as a liability and when the contract is fully executed, the payment is treated as profit.

The advance payment is treated as an asset until the money is fully recovered.

Pacific Ltd undertook a contract for building a factory for N150million. The contract cost of N30million was incurred up to 31

December 2009 and expects that further cost to completed the construction will be N150million. How much should be recognized

in the profit or loss account in 2009?

N30 million should be recognized as expense at the end of year 2009.

N180 million should be recognized as an expense at the end of year 2009.

N150 million should be recognized as an expense at the end of year 2009.

N120 million should be recognized as an expense at the end of year 2009.

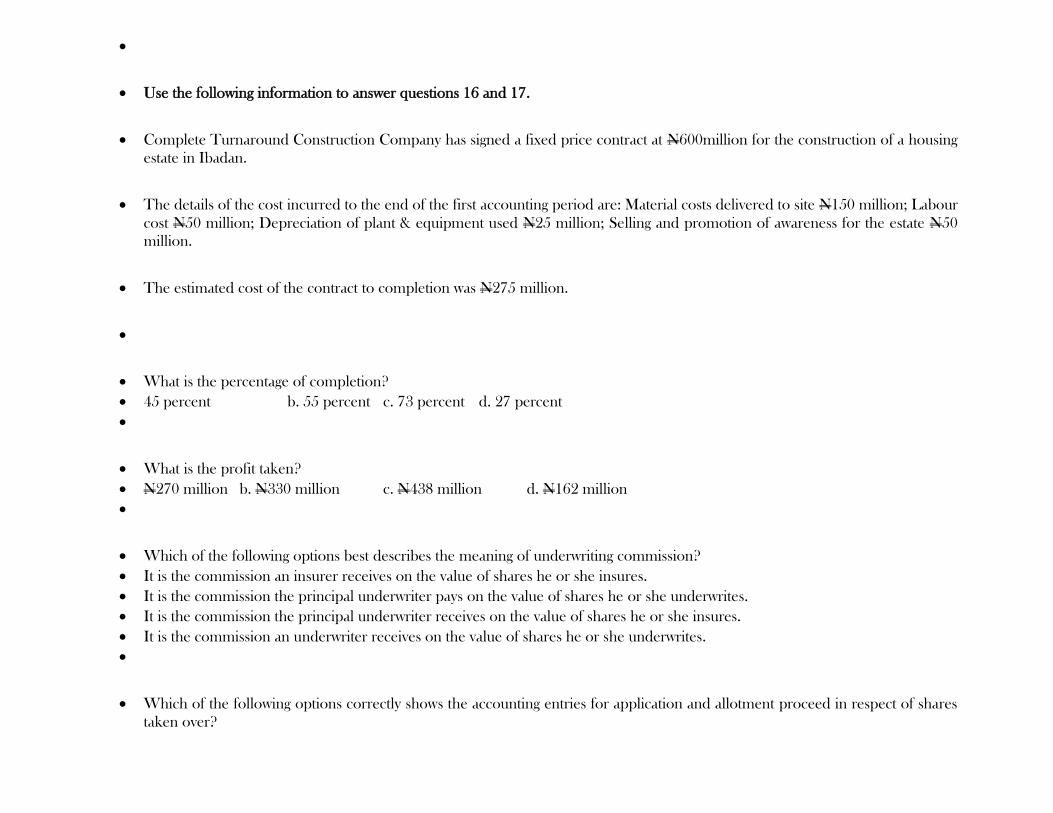

Use the following information to answer questions 16 and 17.

Complete Turnaround Construction Company has signed a fixed price contract at N600million for the construction of a housing

estate in Ibadan.

The details of the cost incurred to the end of the first accounting period are: Material costs delivered to site N150 million; Labour

cost N50 million; Depreciation of plant & equipment used N25 million; Selling and promotion of awareness for the estate N50

million.

The estimated cost of the contract to completion was N275 million.

What is the percentage of completion?

45 percent b. 55 percent c. 73 percent d. 27 percent

What is the profit taken?

N270 million b. N330 million c. N438 million d. N162 million

Which of the following options best describes the meaning of underwriting commission?

It is the commission an insurer receives on the value of shares he or she insures.

It is the commission the principal underwriter pays on the value of shares he or she underwrites.

It is the commission the principal underwriter receives on the value of shares he or she insures.

It is the commission an underwriter receives on the value of shares he or she underwrites.

Which of the following options correctly shows the accounting entries for application and allotment proceed in respect of shares

taken over?

Debit Cash/Bank account, Credit Underwriting account

Debit Underwriting account, Credit Profit and Loss account

Debit Profit and Loss account, Credit Underwriting account

Debit Underwriting account, Credit Cash/Bank account

Which of the following options correctly shows the accounting entries for loss on underwriting contract?

Debit Profit and Loss account, Credit Underwriting account

Debit Underwriting account, Credit Cash/Bank account

Debit Cash/Bank account, Credit Underwriting account

Debit Underwriting account, Credit Profit and Loss account

SECTION B – THEORY (TOTAL=50 marks)

1). a. International Traders Ltd, an English trading company, have a head office in London and a branch in Lille, France, which

submitted the following list of final balances to the head office in London on the 31st of December 2015. These balances are to

be converted at the fixed rate of 13. 72 French francs to the Pound. During the year the Lille remitted to Head office a sum of

money which was recorded in the head office books on 12 Pounds.

REQUIRED:

Show the Branch Account in the London Books after the necessary adjustments have been made.

The Head office current account in the books of the Lille branch.

(10 marks)

LILLE BRANCH- 31st DECEMBER

DR CR

Land and premises 30,744.00

Office Equipment 634.04

Stock, 31 December 1,250.75

Debtors 889.49

Creditors 952.45

Cash at Bank 112.59

Cash in hand 14.54

Remittance to head office 160.82

Head office account, 1st January 32,523.41

Profit and Loss Account

Profit for the year 330.37

33,806.23 3,806.23

b). The trial balance of a foreign branch is drawn up in local currency

Explain fully what rates of exchange are adopted for converting the various items into sterling to enable them to be combined with

the head office trial balance.

(3.5 marks)

If after conversion into sterling, the foreign branch trial balance fails to agree, explain how the differences are dealt with. (4

marks)

(Total = 17.5 marks)

2. Kunle and Kamoru are partners in an engineering company and on 1st

January 2002, they both agreed to purchase an established

mechanical business that belongs to Mr. Lawal who has decided to sell his business due to financial crises. The Statement of

Financial Position of Mr. Lawal is shown below:

LAWAL AND SONS (NIG.) ENTERPRISES

STATEMENT OF FINANCIAL POSITION AS AT 31-12-2002

Non-Current Assets N N

Land and Building 60,000

Plant and Machinery 40,000

Furniture and Fittings 20,000 120,000

Current Assets

Stock 20,000

Debtors 10,000

Cash in Bank 8,000 38,000

158,000

Equity Account 120,000

Add Net Profit 20,000 140,000

Loan- Ola 10,000

Current Liabilities

Creditor 5,000

Accruals 3,000 8,000

158,000

During the negotiation, the purchase price was agreed to be N180,000. For the payment of the money, Kunle and Kamoru agreed

to contribute the money equally through bank account which they opened with N5,000 each. It was also agreed that goodwill

account will be created in the company’s account. For the conclusion of this transaction, all the assets and liabilities of the business

were taken over, with the exception of the business cash account.

Required: Open up the necessary books of accounts to enter the above business transactions. (Total = 12.5 marks)

3). a. The following information was extracted from Pasture Farms for the months of January to February 2015.

N’000

January 3rd

Cash in hand 4,000

“ 10th

Cattle minerals purchased from ATK Ltd. by cash 32

“ 14th

Cheque received for milk sold 148

“ 25th

Heifer sold for cash 1,500

“ 26th

Payment for veterinary services by cash 120

“ 30th

Paid employee wages 1,500

“ 31st

Payment for fencing posts 260

“ 31st

Purchase of disinfectant 300

N’000

February 2nd

Bought maize seed 40

“ 2nd

Purchased Fencing wire with cash 175

“ 4th

Sold cow for cash 200

“ 15th

Cheque received for milk sold 150

“ 16th

Beans sold 1,250

“ 17th

Tractor repairs 475

“ 18th

Fuel 168

“ 19th

Bought Cattle feed and minerals 110

“ 21st

Bought Fertilizer for crops 65

“ 24th

Sold maize for cash 1,200

“ 28th

Wages 800

“ 28th

Cash received for milk sold 1,000

Required:

Prepare the Cash Book for Pasture Farms for the months of January and February, 2015. (4 marks)

Comment on the state of liquidity of Pasture Farms, with recommendations to the owners of the farm based on the farm’s state of

liquidity. (2 marks)

b. Mr. Success is a solicitor. The following transactions took place during the month of March

2011.

March 17: Payment (by cheque) of N10,000 to Tripple Ltd, at the request of a client Wilsons, on account of a debt due by Wilsons

to Tripple Ltd, the client having no money in the hand of the solicitor.

March 19: Wilsons pays N40,000 by cheque to the solicitor to meet the N10,000 and discharge the balance of the debt due to

Tripple Ltd.

March 20: The solicitor gave a cheque of N25,000 to Tripple Ltd, the balance of the debt due, charges Wilsons with N1,000 for

costs which are agreed by the client and remits the balance to Wilsons by cheque.

Required: Show the clients’ ledger as they will appear in the books of Mr. Success. (4 marks)

(Total =10 marks)

4). The following information was extracted from the books of Adebisi Enterprises.

Statement of Financial Position as at 31st

December, 2015

N N N

Non-current Asset Cost Dep NBV

Property, plant and equipment 2600 (1600) 1000

Current Asset

Inventory 700

Accounts receivable 100

Cash 700

1500

Current Liability

Notes payable 200

Accounts payable 200

(400)

Working capital 1100

Net Asset 2100

Financed By:

Long-term debt 1200

Equity:

Common Stock 600

Capital surplus 200

Retained earnings 100

2100

Adebisi

Income Statement for the year ended 31st

December, 2015

N N

Sales 5100

Cost of goods sold 2800

Gross Profit 2300

Administrative

expenses 500

Depreciation 522 1022

Earnings before

interest

1278

Interest expenses 40

Taxable income 1238

Taxes 470

Net Income 768

Dividends 364

Addition to retained

earnings

404

Additional Information

Number of shares outstanding 600

Price per share 1.4

The industry average for the following ratios are:

Current ratio 3.10 Net Profit Margin 15%

Quick ratio 2.0 Return on Assets (ROA) 7%

Receivables Turnover and

Days’ Receivables

30

days Return on Equity (ROE) 19%

Inventory Turnover and

Days’ Inventory

28

days

Dividend per share

14

Debt Ratio

45

% Dividend pay-out ratio 28%

Debt to Equity Ratio 82% Dividend yield 10%

Required: Compute the relative ratios of Adebisi enterprise and compare it with the industry averages. For each comparison, pass

a comment as to the way Adebisi enterprise is faring. (8 marks)

Adebola and Co. ltd is an architectural venture that is also involved in real estate development. They undertook a project for Lagos

state government and after completing it, an external architect assesses the value of work done to be N805, 000.The Lagos state

government has already paid N200, 000. The agreed retention percentage is 30%.

Required: Compute the amount of the current progress payment (2 marks)

(Total =10 marks)

COVENANTUNIVERSITY CANAANLAND, KM 10, IDIROKO ROAD

P.M.B 1023, OTA, OGUN STATE, NIGERIA.

TITLE OF EXAMINATION: OMEGA SEMESTER EXAMINATION

COLLEGE: BUSINESS AND SOCIAL SCIENCES

DEPARTMENT: ACCOUNTING

SESSION: 2015/2016 SEMESTER: OMEGA

COURSE CODE: ACC 321 CREDIT UNIT: 3

COURSE TITLE: FINANCIAL ACCOUNTING IV

INSTRUCTION: ANSWER ALL QUESTIONS IN SECTION A AND B TIME: 3 HOURS

MARKING GUIDE

SECTION A - MULTIPLE CHOICE QUESTIONS (1 mark each = 20 marks)

A

A

C

B

D

C

D

C

B

A

B

A

C

B

A

A

A

D

D

A

SECTION B – THEORY (TOTAL=50 marks)

2. BOOKS OF KUNLE AND KAMORU

Purchase of Business

Vendor 180000 Land and Building 60000

Loan 10000 Plant and machinery 40000

Creditors 5000 Furniture 20000

Accrual 3000 Stock 20000

Debtor 10000

Goodwill 48000

198000 198000

Vendor Account

Kunle’s Capital 90000 Purchase of Business 180000

Kamoru’s Capital 90000

180000 180000

Kunle and Kamoru

Statement of Financial Position as at 31st Dec 2002

N N N

Non Current Assets

Goodwill 48000

Land and Building 60000

Plant and Machinery 40000

Furniture and Fittings 20000 120000

Current Assets

Stock 20000

Debtors 10000

Bank 10000 40000 160000

208000

Equity Account

Kunle 95000

Kamoru 95000 190000

Liabilities

Loan 10000

Creditor 5000

Accruals 3000 18000 208000

208000

3). a. i. Pasture Farms

Cash book for January 2015

N'000 N'000

3rd Jan Bal b/d 4,000

10th Jan Cattle minerals 32

14th Jan milk sold 148

26th Jan Veterinary services 120

25th Jan Heifer 1,500

30th Jan Wages 1,500

31st

Jan Fencing Post 260

31st

Jan Disinfectant 300

31st

Jan bal c/d 3,436

5,648 5,648

Cash book for February 2015

N'000 N'000

1st Feb Bal b/d 3,436

2nd Feb Maize seed 40

4th Feb Cow 200

2nd Feb Fencing wire 175

15th Feb Milk 150

17th Feb Tractor 475

16th Feb Beans 1,250

18th Feb Fuel 168

24th Feb Maize 1,200

19th Feb Cattle Feed and Min. 110

28th Feb Milk 1,000

21st Feb Fertilizer 65

28th

Feb Wages 800

28th

Feb Bal c/d 5,403

7,236 7,236 24 ticks * 0.17 = 4 marks

ii.

b.

Clients' Ledger (Wilson)

Da

te

Particul

ars

Offi

ce

(N)

Clie

nt

(N)

Da

te

Particul

ars

Offi

ce

(N)

Clie

nt

(N)

17t

h

M

ar Cash

advance

10,0

00

19t

h

M

ar Cash

40,0

00

19t

h Cash

transfer

10,0

00

19t

h Cash-

transfer

10,0

00

M

ar

M

ar

20t

h

M

ar Cash-

transfer

25,0

00

20t

h

M

ar Cash-Cost

1,00

0

20t

h

M

ar Cash-cost

1,00

0

20t

h

M

ar

Cash

balance

repaid

4,00

0

Bal c/d

1,00

0

11,0

00

40,0

00

11,0

00

40,0

00 10 ticks * 0.4 = 4 marks

4.

Current ratio: Total current asset/current liabilities = 1500/400= 3.75:1

Quick ratio = current asset – inventories/current liabilities = 2:1

Total Current Assets = 1500, Inventory = 700 and Total Current Liabilities = 400

Debtors turnover = Acct receivable/(sales on credit/365) = 100/(5100/365) = 7.16 days or 365/7.16 = 51 times

Stock turnover = inventory/ (cost of good sold)/365 = 700/ (2800/365) = 91.25 days of 365/91.25 = 4 times.

Debt ratio = total debt/ total asset = 1600/2500 * 100 = 64%

Debt to equity ratio = total debt / total owners equity = 1600/ 900 *100 = 177.8%

Net profit margin = net income / sales * 100 = 768/5100*100 = 15.06%

Return on assets = net income / total asset * 100 = 768 / 2500 = 30.72%

Return on equity = net income / total equity * 100 = 768/900 * 100 = 85.33%

Dividend per share = total dividend paid/ number of ord shares = 364/600 = N0.61

Dividend pay-out ratio = dividend/net income * 100 = 364/768 * 100 = 47.40

Dividend yield = dividend per share/share price * 100 = 0.61/1.4 = 0.44

(8 marks)

Current payment = –retention-payments already made.

= N805, 000 -15% (805,000) -200,000

=N484, 000

(2 marks)

(Total =10 marks)

COVENANTUNIVERSITY CANAANLAND, KM 10, IDIROKO ROAD

P.M.B 1023, OTA, OGUN STATE, NIGERIA. TITLE OF EXAMINATION: Omega Semester Examination

COLLEGE: Business and Social Science

SCHOOL: Business Studies

DEPARTMENT: Accounting

SESSION: 2013/2014 SEMESTER: Omega

COURSE CODE: ACC 322 CREDIT UNIT: 3 Units

COURSE TITLE: Advanced Cost Accounting

MARKING

GUIDE

SECTION A

C 16. OPPORTUNITY COST

E 17. A RELEVANT COST

D 18. OUT-OF-POCKET COST

C 19. TRUE

C 20. FALSE

C

C

C

A

B

B

B

C

C

C

SECTION B

1A). Cost accounting is concerned with recording, classifying and summarizing costs for determination of costs of products

or services, planning, controlling and reducing such costs and furnishing of information to management for decision making.

1B)

S/N Management

Accounting

Cost Accounting

1. Objective To provide information

for planning and

To ascertain and

control cost

decision making by the

management

2. Basic of recording Concerned with

transactions related to

the future

Based on both

present and future

transactions for

cost ascertainment

3. Coverage Covers a wider area:

financial accounts, cost

accounts, taxation, etc.

Covers matters

relating to

ascertainment and

control of cost of

product or service

4. Utility Only the needs of

internal management

The needs of both

internal and

external interested

groups

5. Types of

transactions

Deals with both

monetary any non-

monetary transactions,

covering both

quantitative and

qualitative aspects

Deals only with

monetary

transactions,

covering only

quantitative

aspect

C) Vc (b) = (Hc – Lc)/ (Ha –La)

b = (700,000 – 250,000) / (450 -150)

b = N 1,500

FC (a) = Y- bX

a = 700,000 – 1500 (450)

a = N25,000

D)

Calculate the contribution margin per unit.

N20 - N4 - N1.60 - N0.40 - N2 = $12

Calculate the number of units must sell each year to break even.

20X - 8X - 96,000 = 0; X = 8,000 units

Calculate the number of units ISM’s must sell to yield a profit of N144,000.

20X – 8X – 96,000 = N144,000; X = 20,000 units

2 a. Marginal costing is a costing technique that considers contribution in its decision making process. In marginal costing,

only variable costs are charged as a cost of sales and a contribution is calculated. Closing stocks of work in progress or

finished goods are valued at marginal (variable) cost of production.

Absorption costing is that costing method which charges a share of all overheads (variable and fixed) to products.

CIMA terminology defines it as ‘a principle whereby fixed as well as variable costs are alloted to cost units and total

overheads are absorbed according to activity level.

Under this method, total cost of production (fixed and variable) is used in calculating the unit cost of production.

The following are the differences between marginal and absorption costing techniques:

In absorption costing, items of stock are costed to include a ‘fair share’ of fixed production overhead, whereas in marginal

costing, stocks are valued at variable production cost only. The value of closing stock will be higher in absorption costing than

in marginal costing.

As a consequence of carrying forward an element of fixed production overheads in closing stock values, the cost of sales used

to determine profit in absorption costing will:

include some fixed production overhead costs incurred in a previous period but carried forward into opening stock values of

the current period;

exclude some fixed production overhead costs incurred in the current period by including them in closing stock values.

In contrast marginal costing charges the actual fixed costs of a period in full into the profit and loss account of the period.

(Marginal costing is therefore sometimes known as period costing.)

In absorption costing, ‘actual’ fully absorbed unit costs are reduced by producing in greater quantities, whereas in marginal

costing, unit variable costs are unaffected by the volume of production (that is, provided that variable costs per unit remain

unaltered at the changed level of production activity). Profit per unit in any period can be affected by the actual volume of

production in absorption costing; this is not the case in marginal costing.

In marginal costing, the identification of variable costs and of contribution enables management to use cost information more

easily for decision-making purposes (such as in budget decision making). It is easy to decide by how much contribution (and

therefore profit) will be affected by changes in sales volume. (Profit would be unaffected by changes in production volume).

In absorption costing, however, the effect on profit in a period of changes in both:

production volume; and

sales volume; is not easily seen, because behaviour is not analysed and incremental costs are not used in the calculation of

actual profit.

(Award 1 mark each for correct definition of the two concepts and award ½ mark each for every 4 correct diference identified).

2b.

Glory to Glory Ltd

Absorption Method

N N

Sales (45,000 x N20) 900,000

Less Cost of Production:

Opening stock ---

Variable costs (N12 x 50,000) 600,000

Fixed cost of production (N2 x 50,000) 100,000

700,000

Closing stock (N14 x 5,000) (70,000) Cost of Goods Sold

630,000 Gross Profit

270,000

Less Non-production expenses

Variable selling & Admin (N3 x 45,000) (135,000)

Fixed selling & Admin (15,000)

NET INCOME 120,000

Glory to glory Ltd

Marginal Method

N N

Sales (45,000 x N20) 900,000

Variable cost of goods sold:

Opening stock ----

Variable manufacturing costs (50,000xN12) 600,000

Closing stock (5,000 x N12) (60,000) (540,000)

Variable selling costs (45,000 x N3) (135,000)

Contribution 225,000

Fixed expenses:

Manufacturing (100,000)

Administrative (15,000)

Net income 110,000 .

3. Pricing Decision under Marginal Costing Techniques

Costs that need to be taken into account in any particular decision making process under marginal costing technique are the

relevant costs.

Replacement price: this represents the current market price of an item of raw material in the stock. In decision making,

replacement price will be used in valuing raw material, if it can be established that the raw material is frequently used in the

company or that the raw material is in continuous demand.

Net Realizable value: this is the current disposable value of an item of raw material held in stock. In decision making, net

realizable value will be used in valuing stock, if it can be established that certain materials purchased sometimes ago can no longer

be utilized for the initial objective.

Historical Value: In decision making, historical value represents irrelevant cost.

d) Full –time worker: this represents a fixed cost to the organization; it is therefore irrelevant in decision making. However, where

a full-time worker engages in over- time for the purpose of decision, the over-time cost will be considered, not the entire labour

cost.

New employees and casual workers for the project. Their costs are relevant under marginal costing technique.

f) Incremental Fixed Cost: If fixed cost will increase as a result of a decision it will be considered as relevant.

g) Common Cost: Common costs to alternative decisions may be ignored, because they will not affect the financial result in any

way.

4)

SOLUTION TO QUESTION 3

WONDERS DOUBLE LIMITED

CASH BUDGET FOR 2ND QUOTA OF 2016

Note April May June

N N N

Opening Cash Balance 14000 60400 32400

RECEIPTS:

Cash Sales (i) 42000 51,000 57,000

Collection from debtors (ii) 107800 100,800 110,600

TOTAL RECEIPTS 163,800 212,200 200,000

PAYMENTS:

Cos of goods sold (iii) 67200 98400 111600

Operating Expenses (iv) 11200 16400 18600

Tax - 40,000 -

Dividend - - 16000

Capital Expenditure 25000 25000 -

TOTAL EXPENDITURE 103400 179,800 146200

Closing Cash Balance: 60400 32,400 53800

WORKINGS

COLLECTION SCHEDULE

Feb March April May June

Cash sales: (30%) of sales 42000 51000 57000

Collection for debtors:

Credit sales: 112,000 105,000 98,000 119,000 133,000

One month after sales (60%) - 67200 63000 58800 71400

Two months after sale (40%) - - 44800 42000 39200

107800 100800 110,600

PAYMENT SCHEDULE

Cost of goods sold 96000 114000 126000

Less Fixed COS 12000 12000 12000

Variable COGS 84000 102000 114000

Actual Disbursements of VCOS: Month incurred 67200 81600 91200

One month after - 16800 20400

Total 67200 98400 111600

Operating Exp 22000 25000 27000

Less Fixed Operating Expenses 8000 8000 8000

Variable Operating Expenses 14000 17000 19000

Actual Disbursements of VOE: Month incurred 11200 13600 15200

One month after - 2800 3400

Total 11200 16400 18600

COVENANT UNIVERSITY

CANAANLAND, KM 10, IDIROKO ROAD

P.M.B 1023, OTA, OGUN STATE, NIGERIA

TITLE OF EXAMINATION: B.Sc. Degree

COLLEGE: BUSINESS AND SOCIAL SCIENCE

SCHOOL: BUSINESS

DEPARTMENT: ACCOUNTING

SESSION: 2015/2016 SEMESTER: OMEGA

COURSE CODE: ACC 323 CREDIT UNIT: 2

COURSE TITLE: AUDITING PRINCIPLE AND PRACTICE

INSTRUCTIONS: ANSWER ALL QUESTIONS TIME ALLOWED: 2HRS

Part A

Short answer and Objective questions

A modern internal audit staff should preferably include individuals:

a. with an earned degree in accounting

b. who have had previous experience with the organization

c. with a business administration degree and an understanding of the tool of mordern

management

d. with a spend background, such as system personnel

e. who collectively provide a reasonable balance of all the above background

Orientation for a staff auditor includes:

a. explaining the work paper for audit established by the auditor's organization

b. providing the auditor with an overview of the company organization

c. assigning the auditor to complete a research project

d. both a and b

e. none of the above

Which of the following items would be the best criterion for evaluating a staff auditors work performance?

a. number of definer by findings reported

b. ability to get along with auditees

c. neatness of work paper

d. fulfillment of requirements set forth in the approved audit programmes

e. completion of audit assignment on schedule

Practical training for internal auditing in computer system environment should include instruction in:

a. fortran programming

b. computer system, security standards

c. reading object code

d. computer logic

e. all of the above.

Which of the following would be included in establishing and maintaining a quality assurance programme for the internal audit

department?

establishing a programme for developing the personnel resources of internal audit department

supervision of internal audit work

review of internal audit work by a quality control group with the internal department

external reviews of internal audit department

all of the above

For Profit Corporation, the board is responsible to the -------------------------

In a Corporation, the duties of the Board of Directors are ------------------and --------------

In Not for Profit organisations, the board is particularly responsible to ---------------------

The guide line for drafting a report when drafting a report as a result of professional investigation is referred to as -------------------------

---------

--------------------- and ----------------- are the reasons for investigating fraud.

…………….. is the risk that an auditor expresses an inappropriate opinion on the financial statements.

The audit risk formula: Audit Risk = Inherent Risk x ………………….x Detection Risk.

The possibility of a material misstatement ignoring the client’s internal control is referred to as …………………………..

……………..is an integrated process of checks and balances established by management to provide reasonable assurance that

organization resources are protected, to prevent and detect intentional and unintentional errors, and to reduce risk.

Circumventing controls through collusion by individuals who oversee each other's work is one of the benefits in internal control.

True or False

At any ………….. a retiring auditor, however appointed, shall be re-appointed without any resolution being passed at the AGM unless

he is not qualified for re-appointment.

Auditors may be appointed by the directors of a company to fill a casual vacancy arising from the death, incapacity or sudden

resignation of an auditor.

A ………………….. may exist in the post of auditor, if the auditor dies before the expiration of his tenure of office.

Where a resolution removing an auditor is passed at a general meeting of a company, the company shall within………..give notice

of that fact in the prescribed form to the Commission.

A ……………………is an examination and review of internal procedures and records of an organization, in order to ascertain their

reliability as a basis for the compilation of the final accounts and balance sheet.

(20 Marks)

Part B

1a) Godfirst is a manufacturing company which has good structures, processes, cultures and systems that engender the

successful operation of the organization. Discuss the advantages of this practice to the company and its shareholders.

(8 marks)

b) In maximizing the profit of Godfirst, the management has agreed to partner with “In God we trust”. Identify the issues

which need to be considered on the proposed partnership by the investigator hired by Godfirst.

(4.5 marks)

(Total 12.5marks)

2a) Investigation is the act of detailed examination of activities of organization so as to achieve certain objectives. What are the

differences between investigation and auditing? (6marks)

b) Enumerate at least six areas where investigation can be conducted. (6marks)

c) Give another definition of investigation. (½ mark)

(Total 12.5marks)

3a) According to Idowu Freeron 2005, there are certain conditions that are favourable to corrupt practices in Nigeria.

Mention them and write full notes on each of them.

(4.5 marks)

b) What are the causes of corruption in Nigeria? Mention them and write full notes on them. (4 marks)

c) There are four requirements for fraud. Mention the four, with full notes on each. No diagram required. (4 marks)

(Total 12.5marks)

4a) Briefly describe your understanding of the following terms.

Statutory Audit

Interim audit

Private audit

Internal audit (8 marks)

b) Enumerate briefly, four (4) secondary objectives of an audit. (4 .5 marks)

(Total 12.5marks)

Total=70 marks

COVENANT UNIVERSITY

CANAANLAND, KM 10, IDIROKO ROAD

P.M.B 1023, OTA, OGUN STATE, NIGERIA

TITLE OF EXAMINATION: B.Sc. Degree

COLLEGE: BUSINESS AND SOCIAL SCIENCES

SCHOOL: BUSINESS

DEPARTMENT: ACCOUNTING

SESSION: 2015/2016 SEMESTER: OMEGA

COURSE CODE: ACC 323 CREDIT UNIT: 2

COURSE TITLE: AUDITING PRINCIPLE AND PRACTICE

INSTRUCTIONS: ANSWER ALL QUESTIONS TIME ALLOWED: 2HRS

MARKING GUIDE

Part A

SOLUTION TO OBJECTIVE QUESTIONS

E

D

D

B

E

Stockholders

Provides continuity for the organization and Represents the organization’s point of

view through its products and services and advocacy for them

The community of operation

Golden rule

To determine the extent of fraud committed and to establish the parties involved

Audit Risk

Control Risk

Inherent risk

Internal control

False

AGM

Directors

Casual Vacancy

14 Days

Procedural Audit

(20 Marks)

Part B

1a) Benefits of Good Corporate Governance:

To Companies

Improving access to capital and financial markets;

Helps to survive in an increasingly competitive environment through mergers, acquisitions, partnerships.

better system of internal control, thus leading to greater accountability and better profit margins

Good corporate governance practices can pave the way for possible future growth, diversification, or a sale, including the ability to

attract equity investors – nationally and from abroad

Benefits of Good Corporate Governance:

To Shareholders

Better corporate governance can also provide Shareholders with greater security on their investment.

Better corporate governance also ensures that shareholders are sufficiently informed on decisions concerning fundamental issues

like amendments of statutes or articles of incorporation, sale of assets, etc.

Improvement in wealth maximization

Gives shareholders the right to appoint auditors

(8 marks)

1b)

Collect and verify information obtained from the owners of the firm

Analyse the data into performance, position and prospects of the partnership business

Nature and background of the partnership business

Demand for the reason for admitting new partner(s)

Obtain the partnership deed to establish the rules and regulations guiding the business

Obtain information relating to profit sharing arrangement

Obtain audited account of the partnership business

Obtain information relating to the liability of the incoming partner(s) for existing debt of the partnership

(4.5 marks)

(Total 12.5)

2a) Following differences can be seen between auditing and investigation:

The approach to investigation is different from the approach to a normal audit. Unlike conventional audit investigation is not in

accordance with generally accepted auditing standards. On the one hand it is more comprehensive than an audit and it may exclude

many steps which would be considered necessary as part of an audit.

Unlike an audit , the scope of work involved in an investigation depends entirely on the client’s requirements, consequently avoid

any subsequent misunderstanding, it is prudent to obtain the clients instructions in writing in a letter of engagement.

The statutory audit however cannot be constrained by the letter of engagement in terms of focus.

The responsibility of the accountant in an investigation is to the management who has appointed him to carry out the

investigation but in a statutory audit, the auditor is responsible to the shareholders.

The investigating accountant will have a responsibility to obtain all information necessary for the report he has agreed to prepare.

He will not have the right to all information and explanation that he considers necessary as provided by the CAMA1990 in a

statutory audit situation.

Period: An audit is related to only a year or six months while investigation may cover several years.

7. Statutory Obligation: In the case of listed companies, audit is compulsory under law while there is no such statutory obligation

with regard to investigation.

Investigation is made in suspected places or to obtain/corroborate facts.

Auditing is the act of examining books of accounts so as to prove true and fairness of operating results and financial position of a

business.

(any 6 points=6marks)

2b) Areas where Investigation can be Conducted include the following:

Investment Decisions

Purchase of a business

Purchase of shares in a company (by way of mergers, acquisition)

Participation in a partnership

Loan decision.

2. Investigation of special issues such as:

Loss of profit, costing and financial investigation, e.g. the profitability of a special factory, product or shop

Investigations where fraud is known or suspected to have taken place

Investigations on behalf of a client for credit purposes

Investigations under CAMA ‘90

Investigation for taxation purposes

3. Prospectus Reports

Accountants report for prospectus purposes

Report on the profit forecast included in a prospectus

(any 6 points=6marks)

2c) Investigation is the act of detailed examination of activities of organization so as to

achieve certain objectives. (1/2 mark)

(Total 12.5)

SOLUTION QUESTION 3

SOLUTION TO QUESTION 3a

Conditions favourable to corrupt practices. Idowu-fearon (2005), identifies the following as conditions that make the

perpetration of corrupt practices easy:

Concentration of power in decision makers who are not directly accountable

Lack of government transparency in decision making

Costly political campaign

Large amount of public capital project

Self interest close cliques

Weak legal profession

Weak accounting profession

Poorly paid government officials

Apathetic, uninterested or gullible populace that fail to give adequate attention to political process.

Absence of adequate control to prevent bribery

SOLUTION TO QUESTION 3b

Causes of corruption in Nigeria:

Obsession with Materialism

The causes of corruption in Nigeria are mostly as a result of obsession with materialism, compulsion for a short cut to

affluence, glorification and approbation of ill gotten wealth by the general public, are among reasons for the persistence of

corruption in Nigeria, Ndiulor (1999). It has been noted that one of the popular, but unfortunate indices of good life in Nigeria

is flamboyant affluence and conspicuous consumption. Because of this, some people get into dubious activities, including

committing ritual murder for money making. Lack of ethical standards

The lack of ethical standards throughout the agencies of government and business organizations in Nigeria is a serious

drawback. According to Bowman (1991), Ethics is action, the way we practise our value, it is a guidance system to be used in

making decisions. The issue of ethics in public sector (and in private life) encompasses a broad range including a stress on

obedience to authority, on the necessity of logic in moral reasoning and on the necessity of putting moral judgement into

practice, Bowman (1991). Unfortunately, many office holders in Nigeria appointed or elected do not have clear conceptions of

the ethical demands of their position. Even as corrupt practices going off the roof, little attention, if any is given to this ideal. Greed

Other factors are poor reward system and greed. Nigeria's reward is perhaps, the poorest in the world. Nigeria is a society

where national priorities are turned upside down, hard work is not rewarded, but rogues are often glorified in Nigeria. As

author, Schlesinger said of America in the 60s, the trouble with Nigeria is not that on capabilities are inadequate. It is that our

priorities, which is our values, are wrong by Howard (1982). And peer community and extended family pressures and

polygamous households are other reasons. The influence of extended family system pressure to meet family obligations are

more in less developed societies. The extended family system is an effective institution for survival, but note that it poses a big

obstacle for development. According to Letterman (2002) bad rules and ineffective taxing system, which makes it difficult to

track down people's financial activities. Inneffective taxing system is a serious problem for Nigeria. The society should

institute appropriate and effective taxing system where everyone is made to explain his or her sources of income, through end

of the year income tax filing. The brazen display of wealth by public officials, which they are unable to explain the source,

points to how bad corruption has reached in the socieety. Many of these officials before being elected or appointed into offices,

had little or modest official income, but now, they are now for many properties around the world (this day, 2002).

QUESTION 3c

Necessary requirements for fraud

All these four must be present, they are in alternatives:

Opportunity: to carry out that particular fraud

Advantage: to be gained from it

Motivation: need, greed or grudge

Moral weakness: without which fraud would not be attempted.

NOTE:

Students are expected to write short notes on the above four alternatives.

Question 4(a) Solution

Statutory Audit; this is the most popular audit. It is prescribed by the law for the limited liability companies. The objectives &

mode of carrying out the audit is spelt out by the statute. In Nigeria, situation, the statutory audit is being regulated by CAMA 1990

as amended.

Interim Audit; This is an audit is conducted to a particular date within the accounting period. The auditor may attend to audit

the figures for a month or for a quarter, as the work may require. It would defer distinctly from the final audit in the extent of the

work carried out; certain aspects of final audit such as verification of assets may be left out until the final audit.

Private audit; this is an audit carried out at the instance of the owner of the biz. It is not required by law but they are carried out

for the personal benefit of the individual owner of the business.

Internal audit; an internal audit is an independent appraisal activity within an organization set for the review of operations & as a

service to management. It is a form of management control which functions by measuring & evaluating the effectiveness of other

controls.

(Two (2) marks per tick for any correct answer) total marks (2*4 = 8 marks)

Question 4(b) Solution

Secondary objectives of auditing:

To detect any form of irregularity.

To evaluate the effectiveness or otherwise, of the internal control system within the enterprise.

To assist the management in the establishment of effective auditing system.

To advise on financial matters for efficient decision making by the management.

To ascertain and ensure that an enterprise conforms to statutory and professional requirement.

To prevent fraud and errors.

(0.9 marks per tick for any five correct answer mentioned) total marks (0.9*5 = 4.5 marks)

(Total 12.5marks)

Total 70 Marks

COVENANTUNIVERSITY CANAANLAND, KM 10, IDIROKO ROAD

P.M.B 1023, OTA, OGUN STATE, NIGERIA. TITLE OF EXAMINATION: B.SC EXAMINATION

COLLEGE: COLLEGE OF DEVELOPMENT STUDIES

SCHOOL: SCHOOL OF BUSINESS

DEPARTMENT: ACCOUNTING

SESSION: 2015/2016 SEMESTER: OMEGA

COURSE CODE: ACC325 CREDIT UNIT: 3

COURSE TITLE: NIGERIAN TAXATION 1

INSTRUCTION: Answer All TIME: 3.00 HOURS

MULTIPLE-CHOICE QUESTIONS [20Marks]

The objectives of taxation are as follows EXCEPT

a]. To provide fiscal tool for stimulating economic growth and development

b]. To promote healthy competition among different tiers of government

c]. For revenue generation to meet the needs of the government

d]. To redistribute income wealth in order to reduce inequality

Listed below are the examples of indirect taxes EXCEPT

a]. Import duties b]. Value added tax c]. Excise duties d]. Withholding tax

The following are the cannons of taxation EXCEPT

a]. Accountability b]. Equity c]. Economy d]. Ability to pay

,

The following are the sources of tax EXCEPT

a]. Opinion of income tax experts b]. Court judgment until overruled

c]. Opinion of a member of House of Assembly of any State

d]. Constitution

Tax system includes the following:

a]. Tax law only b]. Tax administration only c]. Tax policy only

d]. Tax law, tax policy and tax administration

The following are the duties of the Joint Tax Board in Nigeria EXCEPT

a]. To enlighten members of the public generally on Federal and State government

revenue matters.

b] To settle disputes between the states as regards tax matters.

c]. To promote uniformity both in the application and incidence of the provision of

tax laws on individuals throughout the country.

d]. To advise the government on request in respect of double taxation arrangements,

rates of capital allowances and other tax matters.

A forum is formed at any meeting of the State Internal Revenue Board where there is in attendance.

a. The chairman and three other members b. The chairman or a Director and two other members. c. The chairman or a

Director and four other members

The chairman and seven other members

Appeals can only be lodged later than 30 days if the delay in lodging the notice of appeal is

due to the following EXCEPT

a. The objector’s absence from the country b Sickness of objector c. Other reasonable clause

d. Wedding of objector

The Tax Clearance Certificate discloses in respect of the last three years of assessment of

the following EXCEPT

a Chargeable income b. Tax payable c. Tax paid d. Projected income

Tax is evaded through the following ways EXCEPT

a. Refusing to register with the relevant tax authority b. Failure to furnish returns

c. Incorporating tax payers sole proprietor into Limited Liability Company

d. Entering into artificial transactions

The person making a will is a/an …………………………………

Executor (b) Administrator (c) Trustee (d) Testator

12. An individual in receipt of an annuity or fixed annual amount paid out of the income of a settlement, trust, or estate

shall be assessable to tax on ………… of the annuity.

half (b) 200% (c) the full amount (d) 20%

Basis of assessment for an old established company is …………….

actual basis (b) preceding year basis (c) continuity basis (d) succeeding year basis

……… basis period occurs when a basis period is common to more than one year of assessment.

In a situation where there is a change of accounting date or cessation of business, there is always a ……… between the basis

periods of two assessment years.

Capital allowances unrelieved in the year of cessation can be carried backward and set-off against remainder of profits for:

2 years of assessment preceding year of cessation

5 years of assessment preceding year of cessation

3 years of assessment preceding year of cessation

4 years of assessment preceding year of cessation

Current year loss relief is only applicable to ………….

individuals (b) petroleum companies (c) limited liability companies (d) unincorporated companies

Unrelieved loss which can no longer be carried forward upon the cessation of a business is known as …………….

A company’s trading loss from one source can be relieved against assessable profits from other sources within the same year.

True or False?

Other than on commencement or cessation of a business or change of accounting date, adjusted profits is the same as

………… (a) Net profits (b) Total profits (c) Assessable profits (d) Accounting profits.

SECTION B

1a] Mr. Adewale, A chief Executive Officer in BAC Shipping Plc provided the Tax Authorities with the following information

which represented his income as agreed from all sources for 2014 Assessment Year.

Salary from employment #1,720,000

Commission on sale 350,000

Income from part-time business 1,120,000

Dividend (net) for 2013 100,000

Pension from previous employment 310,000

Rent received from property 2013 350,000

Annual Bonus 210,000

Interest on bank deposit 2013 70,000

Required:

Compute Mr. Adewale’s statutory total income and his personal allowance for 2014. (10Mks)

b] Nigerian tax law is purely statutory. The tax system thus features a wide and mixed range of statutes by which the various

governments in the country seek to charge and collect revenue for public expenditure. Discuss briefly five major sources of tax

revenue open to Federal Government of Nigeria (5Mks)

2] Write short notes on the following:

Itinerant worker

Earned and Unearned Income

Taxable Persons

Back Duty Audit

e) Principal Place of Residence (10Mks)

3] (a) Covenant White Limited is a company engaged in the entertainment business. It commenced business on 1st September

2001 and made up accounts as follows:

-9 months ended 30/06/02

-Year ended 30/06/03

Determine the basis period for assessment and for capital allowances for the first four years of assessment.

(10 Mks)

(b)A company sold a machine forming part of its fixed assets at N1.8million. The machinery which costs N1.5million on

acquisition had tax written down value of N880,000 on disposal. Compute the balancing adjustment on disposal.

(5 Mks)

4] Dr Glory to Glory runs a clinic and makes up accounts to 31st December each year. The results from the clinic for tax

purpose were: N

Year ended 31-12-03 18,000 Profits

Year ended 31-12-04 42,000 Loss

Year ended 31-12-05 12,000 Profits

He receives gross rental income of N21,600 per annum from his Ota house.

Required: Show his total income for 2004 and 2005 years of assessment, assuming all reliefs were claimed as soon as

possible. (10 Mks)

COVENANTUNIVERSITY CANAANLAND, KM 10, IDIROKO ROAD

P.M.B 1023, OTA, OGUN STATE, NIGERIA. TITLE OF EXAMINATION: B.SC EXAMINATION

COLLEGE: COLLEGE OF DEVELOPMENT STUDIES

SCHOOL: SCHOOL OF BUSINESS

DEPARTMENT: ACCOUNTING

SESSION: 2015/2016 SEMESTER: OMEGA

COURSE CODE: ACC325 CREDIT UNIT: 3

COURSE TITLE: NIGERIAN TAXATION 1

INSTRUCTION: Answer All TIME: 3.00 HOURS

MARKING

GUIDE

MULTIPLE-CHOICE SOLUTION [20Marks]

1] B

2] D

3] A

4] C

5] D

6] A

7] C

8] D

9] D

10] C

11]. D

12]. C

13]. B

14]. OVERLAPPING

15]. GAP

16]. B

17]. A

18]. TERMINAL LOSS

19]. FALSE

20]. C

SOLUTION: Q1

Mr. James

Computation of Total Income for 2012 Assessment Year.

Earned Income # #

Salary 1,720,000

Commission 350,000

Income from Part-time Business 1,120,000

Pension 310,000

Annual Bonus 210,000

Total Earned/Employment Income 3,710,000

Unearned Income

Dividend (Gross) 111,111

Rent 350,000

Interest on bank deposit 70,000

Statutory Total Income 4,241,111

Less: Consolidated Allowance (200,000)

Less Personal Allowance (848,222) 1,048,222

Taxable Income 3,192,889

1st #300,000 at 7% 21,000

Next #300,000 at 11% 33,000

Next #500,000 at 15% 75,000

Next #500,000 at 19% 95,000

Next #1,592,889 at 21% 334,507

Tax Due 558,507

Workings: Dividend Personal Allowance

Net Amount = #100,000 20% of Gross Income

Withholding Tax 10% #848,222

= Gross Amount 100/90 x 100,000

= 111,111

SOLUTION Q2

ITINERANT WORKER

This is an individual who carries out his working activities in more than one place in Nigeria, or who earns daily wages other

than members of the armed forces. Where an itinerant worker is treated as a question business entity, then the application of both

the commencement and cessation rules may be relevant for tax purpose. A tax authority may in fact assess him depending on his

place of work at the point when tax is being computed. In the course of doing this his gross income to date, the tax paid to date

and the fine pay to date in existence from any other tax authority shall be recognized and utilized. In addition unpaid tax before

leaving a tax jurisdiction shall be kept in abeyance until his return but he will be given credit for payments made in other tax

jurisdiction

Principal Place of Residence

Where an individual has more one place of residence on the relevant day, the principal place of residence for tax purpose shall

be:

Individual Holding Foreign employment: The territory in which the principal of the employer is resident

Individual Holding a Nigerian Employment:- The place where he normally resides

Where only source of income in Nigerian is Pension:- The place where he usually resides. Where he has no place of residence

i.e. he is not resident in Nigeria, the territory where the pension is wholly payable. In a similar manner, where the pension is

payable by more than one state government, then he is deemed to be resident in the federal capital territory.

Where pension is not a Nigerian Pensioner, The territory of the principal office of the pension fund.

Where there is unearned income:- The place where he usually reside or the place where the income is derived from. Where the

income is from more than one source, the federal capital territory.

Corporate sole or body of individuals, other than itinerant worker:- The territory where the principal office is situated or the

territory in which any part or whole of the income liable to tax arise from in a year of assessment.

Earned Income

Earned income in relation to an individual, means income derived by him from a trade, business, profession, vocation or

employment carried on or exercised by him and the pension derived by him in respect of a previous employment.

Unearned Income

Unearned income under the pension income tax decree 1993, is mostly limited to investment income such as dividends, rents,

and interest. they are received net of withholding tax. Unearned income are subject to tax on the preceding year basis.

[1ai] BACK DUTY AUDIT. The relevant tax authority may carry out a back duty audit on a taxpayer under

the provisions of companies’ income Tax Act 1990 or personal income tax decree of 1993. The law allows

the relevant tax authority to audit up to 6 years backward. The records of the taxpayer are audited to examine

the truth in the information that was earlier provided in the annual returns or tax computations. To confirm

that income has not been materially understated, and that expenses have not been overstated.

SOLUTION Q3

DETERMINATION OF BASIS PERIOD FOR ASSESSMENT YEARS AND CAPITAL ALLOWANCES

Assessment Year Basis Period for Ass. Basis Period for Capital Allowance

2001 1/9/01-31/12/01 1/9/01-31/12/01

2002 1/9/01-31/8/02 1/1/02-31/8/02

2003 1/9/01-31/8/02 -

2004 1/7/03-30/6/03 1/9/02-30/6/03

Computation of Balancing Adjustment N

Tax Written Down Value on Disposal 880,000

Less: Sales Proceeds (1,800,000)

Balancing charge 920,000

However, the balancing charge that can be clawed-back is restricted to capital allowances previously granted and it is

calculated as follows: N

Tax Written Down Value 880,000

Less: Cost of Acquisition (1,500,000)

Actual balancing charge 620,000

SOLUTION Q4

DR GLORY TO GLORY

STATEMENT OF TOTAL INCOME FOR 2004 AND 2005

2004 Year of Assessment

Earned Income N N

lncome from Clinic

Year ended 31-12-03 18,000

Unearn ed Income

Gross Rental Income 21,600

39,600

2004 loss from business 42,000

Relieved (39,600) (39,600)

Total Income Nil

2005 Year of Assessment

Earned Income

Income from clinic

Year ended 31-12-2004 (42,000)

Previously relieved 39,600

Loss c/f 2,400

Unearned Income

Gross rental income 21,600

Total Income 21,600

NOTES

The loss from the business has been relieved in 2004 applying the current year loss relief.

In 2005, the loss of N2,400 cannot be set-off against income from rent; hence, it is carried forward to 2006.

COVENANT UNIVERSITY

CANAANLAND, KM 10, IDIROKO ROAD

P.M.B 1023, OTA, OGUN STATE, NIGERIA.

TITLE OF EXAMINATION: B.Sc DEGREE EXAMINATION

COLLEGE: COLLEGE OF BUSINESS AND SOCIAL SCIENCES

SCHOOL: SCHOOL OF BUSINESS

DEPARTMENT: ACCOUNTING

SESSION: 2015/2016 SEMESTER: OMEGA

COURSE CODE: ACC 329 CREDIT UNIT: 1

COURSE TITLE: ACCOUNTING LABORATORY III

INSTRUCTION: WORK TO BE DONE IN SAGE ACCOUNT TIME: 1 HOUR

A Soft Drink dealer REWARD ENTERPRISES (Your Matric No) whose fiscal year runs from

January to December started operations on January, 2016 with a Capital of 8,000,000 which was

deposited into the following banks:

GT Bank Account - 4,500,000.00

ECO Bank Account - 3,000,000.00

Cash on Hand - 500,000.00

The Customers and Suppliers list are shown below:

Customers Suppliers

CUST (1) Dayo

Ent.

SUPP (1) Coca-

Cola

Company

CUST (2) Greg Nig.

Ltd.

SUPP (2) 7 up

Company

CUST (3) Brown

Nig. Ltd.

The Product List is shown below:

ID Description Cost Price Selling

Price

Unit

of

Sale

CK001 Coke N3,000.00 N4,500.00 Crate

FT001 Fanta N3,300.00 N4,200.00 Crate

MR001 Mirinda N3,200.00 N4,000.00 Crate

The following transactions took place during the month:

22/04/16: Purchased 200 crates of CK001 and 250 crates of FT001 from SUPP (1) and paid 80%

using GT Bank. In addition, 300 crates of MR 001 was also purchased from SUPP (2) and paid

60% of the amount using ECO Bank Cheque.

23/04/16: Sold 150 crates of FT001 and 100 crates of CK001 to CUST (2) and received 70%

into GT Bank. Also sold 100 crates of MR 001 to CUST (1) and received 80% of the cost which

was deposited into the ECO Bank account.

24/04/16: Sold 30 crates of MR001 and 50 crates of FT001 to CUST (3) and received 90% of

the cost which was deposited into the GT Bank Account.

25/04/16: Bought a Motor Vehicle at the Cost of N600, 000, 00 using a GT Bank Cheque with

a depreciation of 15% on cost. In addition, a Landed Property worth N700, 000.00 was bought

using ECO Bank Cheque with 5% depreciation on cost.

26/04/16: Paid the following overhead expenses from Cash in Hand: N

Salaries and Wages 350,000

Transportation 50,000

Electricity 50,000

Required:

Create a new company using the company name and your Matric no. Enter the transactions

above

Run your month end wizard

Print the Trial balance as at 30th April 2016

Print the Profit and Loss for the month of April 2016