sub : loan policy 2014-15 - aiiboaaiiboa.in/circular/cir-13-14/adv_136.pdf · sub : loan policy...

TRANSCRIPT

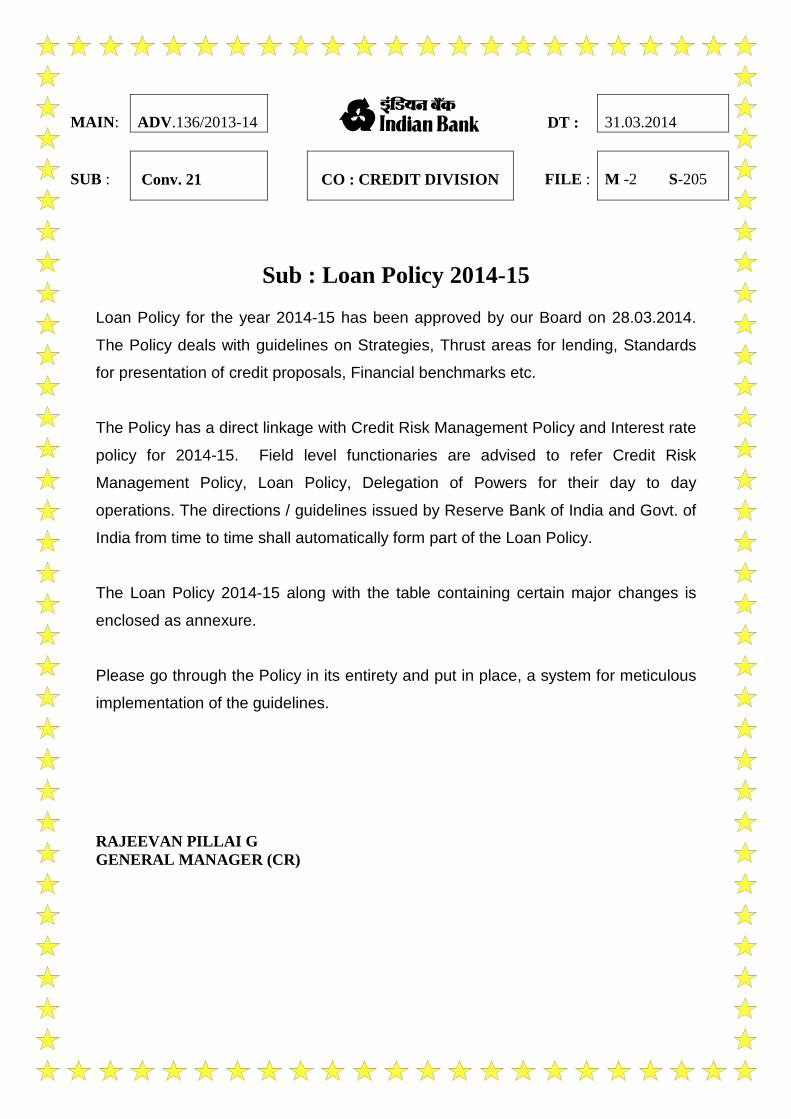

MAIN:

ADV.136/2013-14

a DT :

31.03.2014

SUB :

Conv. 21

CO : CREDIT DIVISION

FILE :

M -2 S-205

Sub : Loan Policy 2014-15

Loan Policy for the year 2014-15 has been approved by our Board on 28.03.2014.

The Policy deals with guidelines on Strategies, Thrust areas for lending, Standards

for presentation of credit proposals, Financial benchmarks etc.

The Policy has a direct linkage with Credit Risk Management Policy and Interest rate

policy for 2014-15. Field level functionaries are advised to refer Credit Risk

Management Policy, Loan Policy, Delegation of Powers for their day to day

operations. The directions / guidelines issued by Reserve Bank of India and Govt. of

India from time to time shall automatically form part of the Loan Policy.

The Loan Policy 2014-15 along with the table containing certain major changes is

enclosed as annexure.

Please go through the Policy in its entirety and put in place, a system for meticulous

implementation of the guidelines.

RAJEEVAN PILLAI G GENERAL MANAGER (CR)

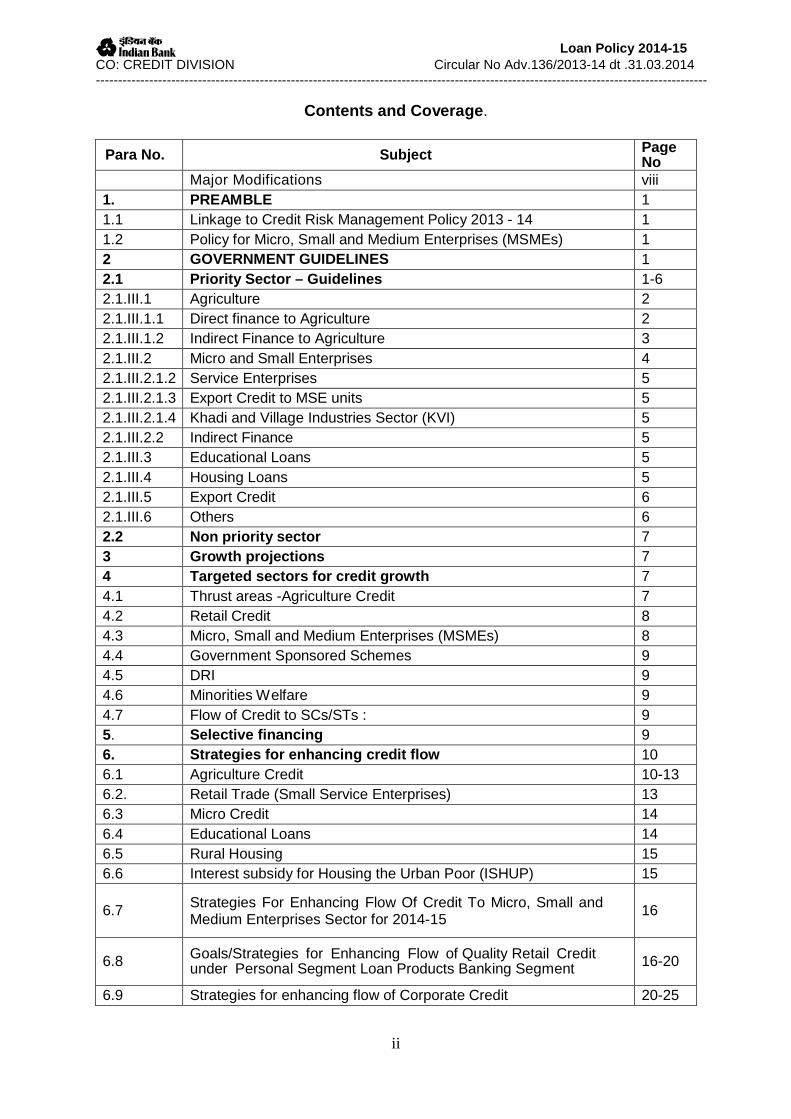

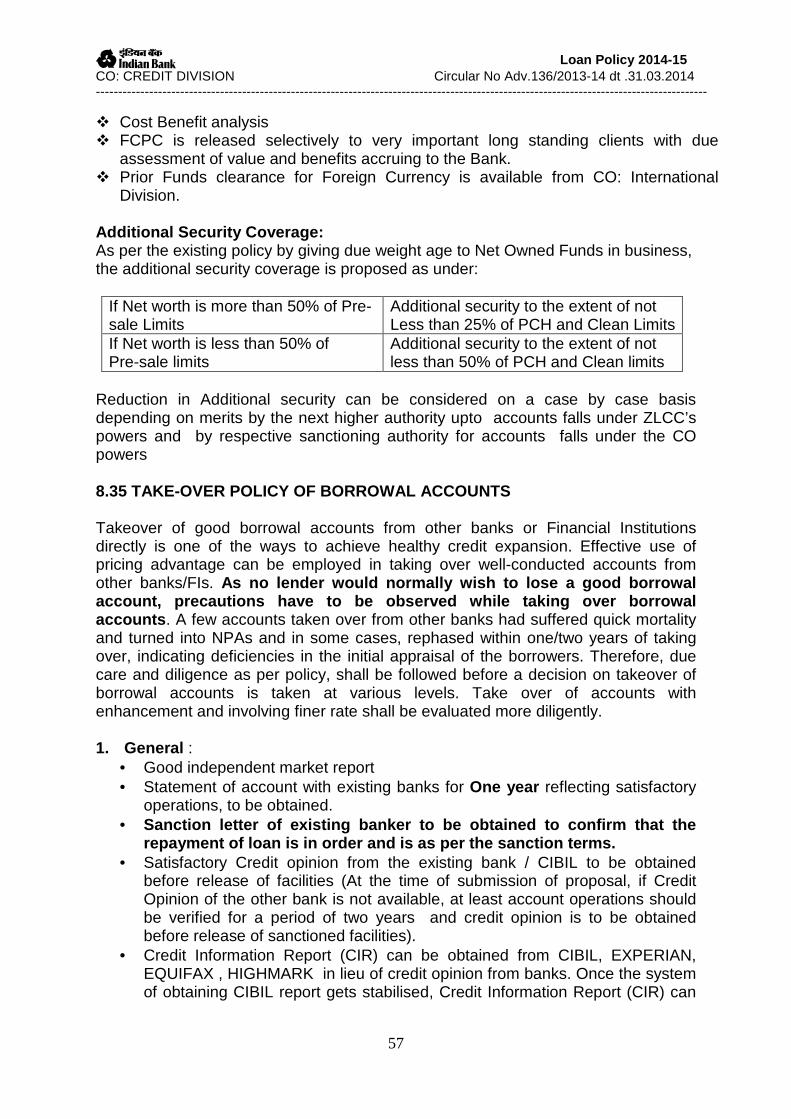

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

ii

Contents and Coverage .

Para No. Subject Page No

Major Modifications viii 1. PREAMBLE 1 1.1 Linkage to Credit Risk Management Policy 2013 - 14 1 1.2 Policy for Micro, Small and Medium Enterprises (MSMEs) 1 2 GOVERNMENT GUIDELINES 1 2.1 Priority Sector – Guidelines 1-6 2.1.III.1 Agriculture 2 2.1.III.1.1 Direct finance to Agriculture 2 2.1.III.1.2 Indirect Finance to Agriculture 3 2.1.III.2 Micro and Small Enterprises 4 2.1.III.2.1.2 Service Enterprises 5 2.1.III.2.1.3 Export Credit to MSE units 5 2.1.III.2.1.4 Khadi and Village Industries Sector (KVI) 5 2.1.III.2.2 Indirect Finance 5 2.1.III.3 Educational Loans 5 2.1.III.4 Housing Loans 5 2.1.III.5 Export Credit 6 2.1.III.6 Others 6 2.2 Non priority sector 7 3 Growth projections 7 4 Targeted sectors for credit growth 7 4.1 Thrust areas -Agriculture Credit 7 4.2 Retail Credit 8 4.3 Micro, Small and Medium Enterprises (MSMEs) 8 4.4 Government Sponsored Schemes 9 4.5 DRI 9 4.6 Minorities Welfare 9 4.7 Flow of Credit to SCs/STs : 9 5. Selective financing 9 6. Strategies for enhancing credit flow 10 6.1 Agriculture Credit 10-13 6.2. Retail Trade (Small Service Enterprises) 13 6.3 Micro Credit 14 6.4 Educational Loans 14 6.5 Rural Housing 15 6.6 Interest subsidy for Housing the Urban Poor (ISHUP) 15

6.7 Strategies For Enhancing Flow Of Credit To Micro, Small and Medium Enterprises Sector for 2014-15

16

6.8 Goals/Strategies for Enhancing Flow of Quality Retail Credit under Personal Segment Loan Products Banking Segment 16-20

6.9 Strategies for enhancing flow of Corporate Credit 20-25

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

iii

Para No. Subject Page No

7 Mandatory guidelines of RBI 25 7.1 Know Your Customer (KYC)/Anti Money Laundering Norms (AML) 136 7.2 Loans to NRI 136

7.3 Restrictions on Advances against Non-Resident (External) Rupee Account and FCNR (B) deposits

136

7.4 Commercial Real Estate Sector – Definition 136

7.5 Adherence of National Building Code specifications for safety of buildings 137

7.5.a National Disaster Management Guidelines on Ensuring Disaster Resilient construction of Buildings and Infrastructure 138

7.6 RBI directions on Unauthorised Construction, Misuse of properties and encroachement on Public Land 138

7.7 Advance against Bullion and Primary Gold 139 7.8 Collateral free loans to Micro and Small Enterprises (MSEs) 140 7.9 Advance against banned article 140 7.10 Advances against Sensitive Commodities 140 7.11 Valuation of Sugar Stocks 141

7.12 Advances against Fixed Deposit Receipts (FDRs) issued by other Banks 141

7.13 Advances to Agents/Intermediaries based on Consideration of Deposit Mobilization

141

7.14 Acceptance of 7% Savings Bonds 2002, 6.5% Savings Bonds 2003 (Non –taxable) & 8% Savings (taxable) Bonds 2003 as collateral security.

141

7.15 Advances against Certificate of Deposits (CDs) 141 7.16 RBI Guidelines on Discounting/Rediscounting of Bills by Banks 141 7.16.1 Co-acceptance of Bills 142 7.16.2 Discounting of Bills co-accepted by other Banks 143 7.17 Financing to Factoring Companies. 143 7.18 Advances against bank's own shares 143 7.19 Advances against shares 143 7.20 Exposure to Capital Market 143

7.21 Guidelines in respect of issue of guarantees to stock exchanges on behalf of stock brokers 144

7.21.1 Advances to Share and Stock Brokers / Commodity Brokers 144 7.22 Restrictions on Holding Shares in Companies 146 7.23 Guarantees for Export Advance 146 7.24 External Commercial Borrowings (ECB) 147 7.25 Forward Contracts 148 7.26 Restriction on Units consuming ozone depleting substances 149

7.27 Restriction on granting advances to Government / Semi-Government 149

7.28 Restriction on granting advances to Public Sector entities which are not corporate

149

7.29 Restrictions on Advances to Directors/Senior Officers of our Bank / to their Relatives / Directors of other banks and their relatives 149

7.30 Legal Compliance Certificate – Dr Mitra Committee Recommendations on Legal Aspects of Bank Frauds

150

7.31 Acknowledgement to all loan applicants 150

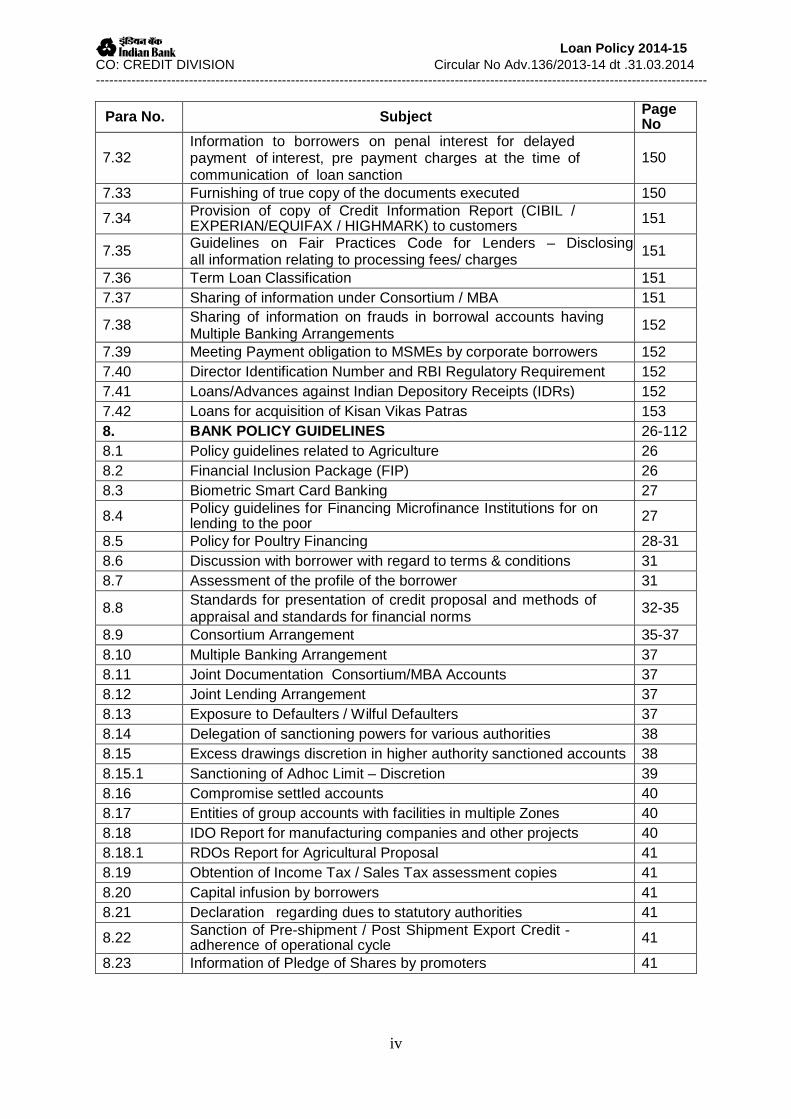

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

iv

Para No. Subject Page No

7.32 Information to borrowers on penal interest for delayed payment of interest, pre payment charges at the time of communication of loan sanction

150

7.33 Furnishing of true copy of the documents executed 150

7.34 Provision of copy of Credit Information Report (CIBIL / EXPERIAN/EQUIFAX / HIGHMARK) to customers 151

7.35 Guidelines on Fair Practices Code for Lenders – Disclosing all information relating to processing fees/ charges

151

7.36 Term Loan Classification 151 7.37 Sharing of information under Consortium / MBA 151

7.38 Sharing of information on frauds in borrowal accounts having Multiple Banking Arrangements

152

7.39 Meeting Payment obligation to MSMEs by corporate borrowers 152 7.40 Director Identification Number and RBI Regulatory Requirement 152 7.41 Loans/Advances against Indian Depository Receipts (IDRs) 152 7.42 Loans for acquisition of Kisan Vikas Patras 153 8. BANK POLICY GUIDELINES 26-112 8.1 Policy guidelines related to Agriculture 26 8.2 Financial Inclusion Package (FIP) 26 8.3 Biometric Smart Card Banking 27

8.4 Policy guidelines for Financing Microfinance Institutions for on lending to the poor 27

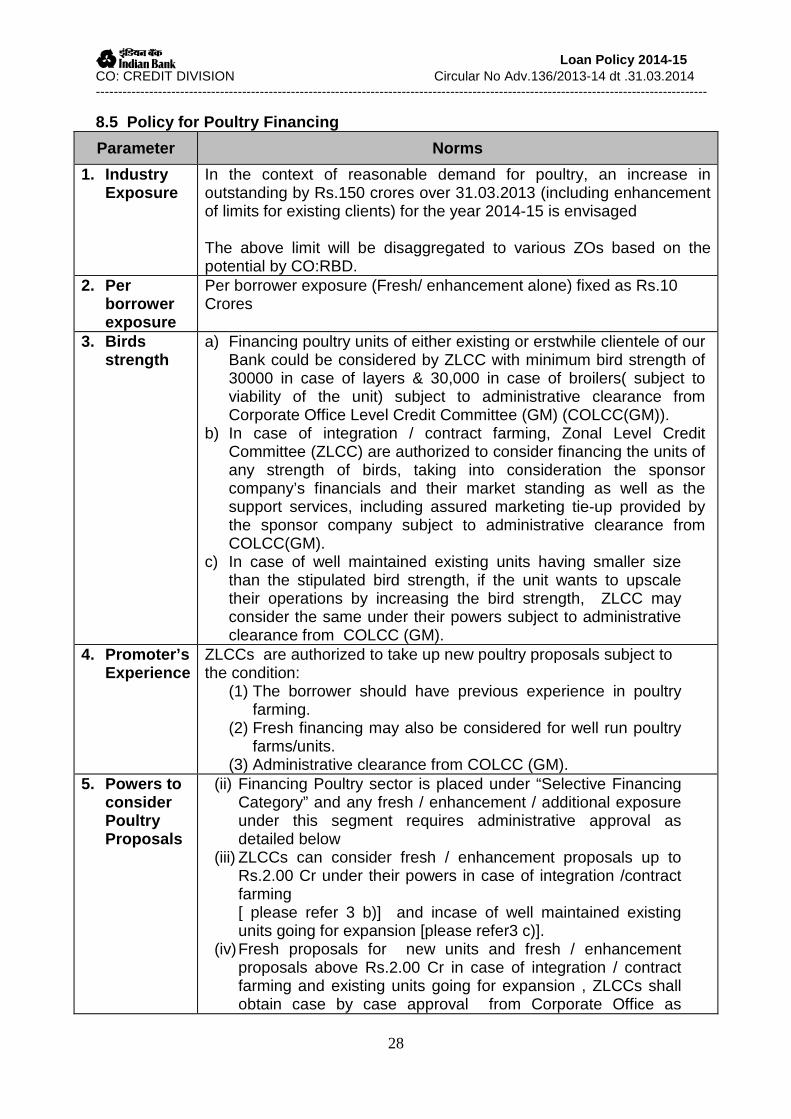

8.5 Policy for Poultry Financing 28-31 8.6 Discussion with borrower with regard to terms & conditions 31 8.7 Assessment of the profile of the borrower 31

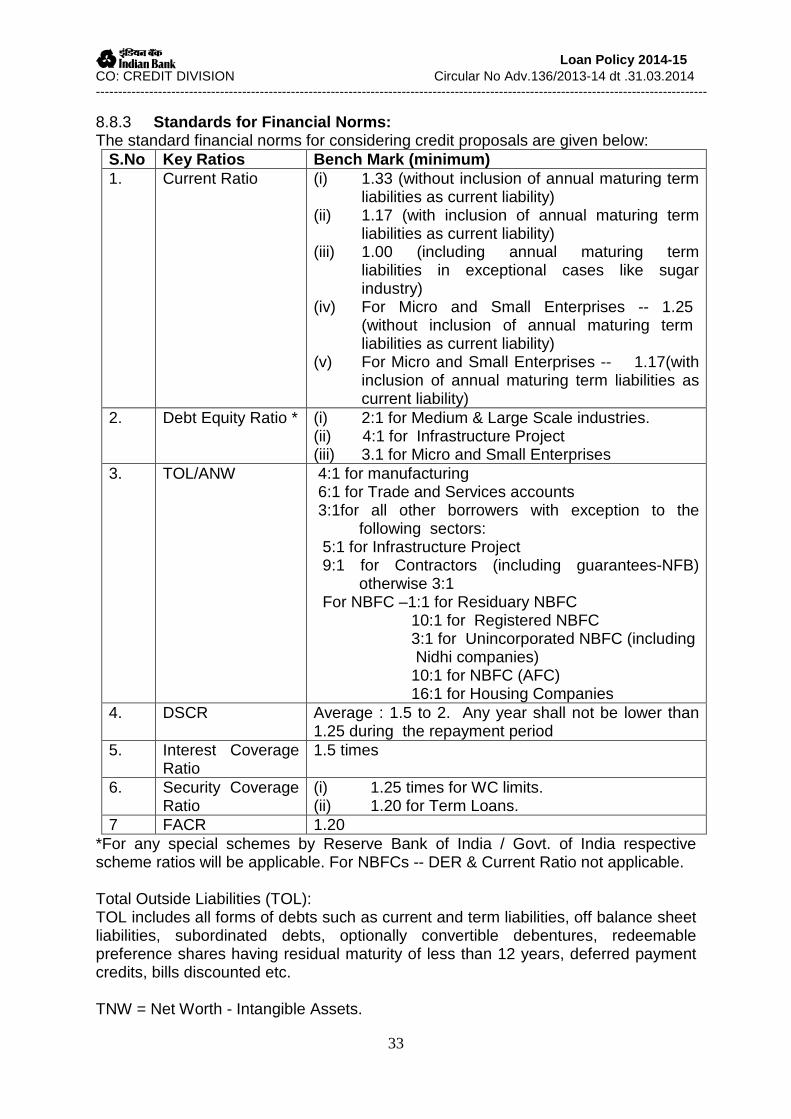

8.8 Standards for presentation of credit proposal and methods of appraisal and standards for financial norms

32-35

8.9 Consortium Arrangement 35-37 8.10 Multiple Banking Arrangement 37 8.11 Joint Documentation Consortium/MBA Accounts 37 8.12 Joint Lending Arrangement 37 8.13 Exposure to Defaulters / Wilful Defaulters 37 8.14 Delegation of sanctioning powers for various authorities 38 8.15 Excess drawings discretion in higher authority sanctioned accounts 38 8.15.1 Sanctioning of Adhoc Limit – Discretion 39 8.16 Compromise settled accounts 40 8.17 Entities of group accounts with facilities in multiple Zones 40 8.18 IDO Report for manufacturing companies and other projects 40 8.18.1 RDOs Report for Agricultural Proposal 41 8.19 Obtention of Income Tax / Sales Tax assessment copies 41 8.20 Capital infusion by borrowers 41 8.21 Declaration regarding dues to statutory authorities 41

8.22 Sanction of Pre-shipment / Post Shipment Export Credit - adherence of operational cycle 41

8.23 Information of Pledge of Shares by promoters 41

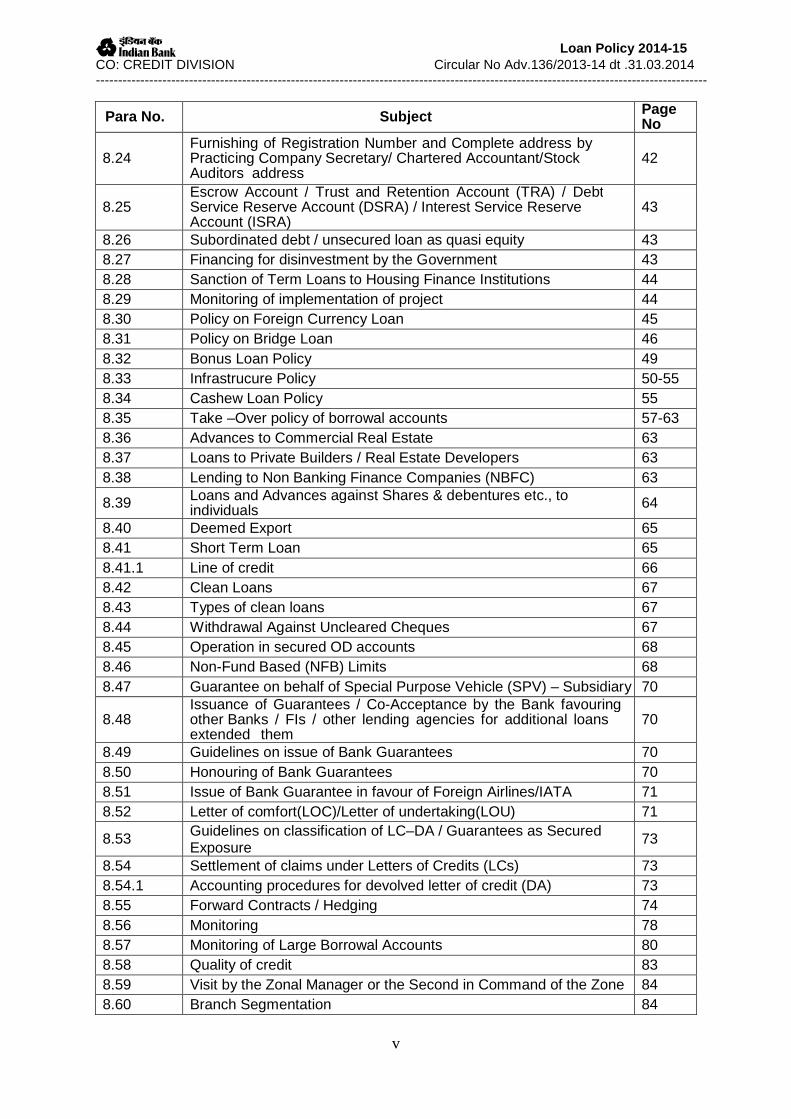

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

v

Para No. Subject Page No

8.24 Furnishing of Registration Number and Complete address by Practicing Company Secretary/ Chartered Accountant/Stock Auditors address

42

8.25 Escrow Account / Trust and Retention Account (TRA) / Debt Service Reserve Account (DSRA) / Interest Service Reserve Account (ISRA)

43

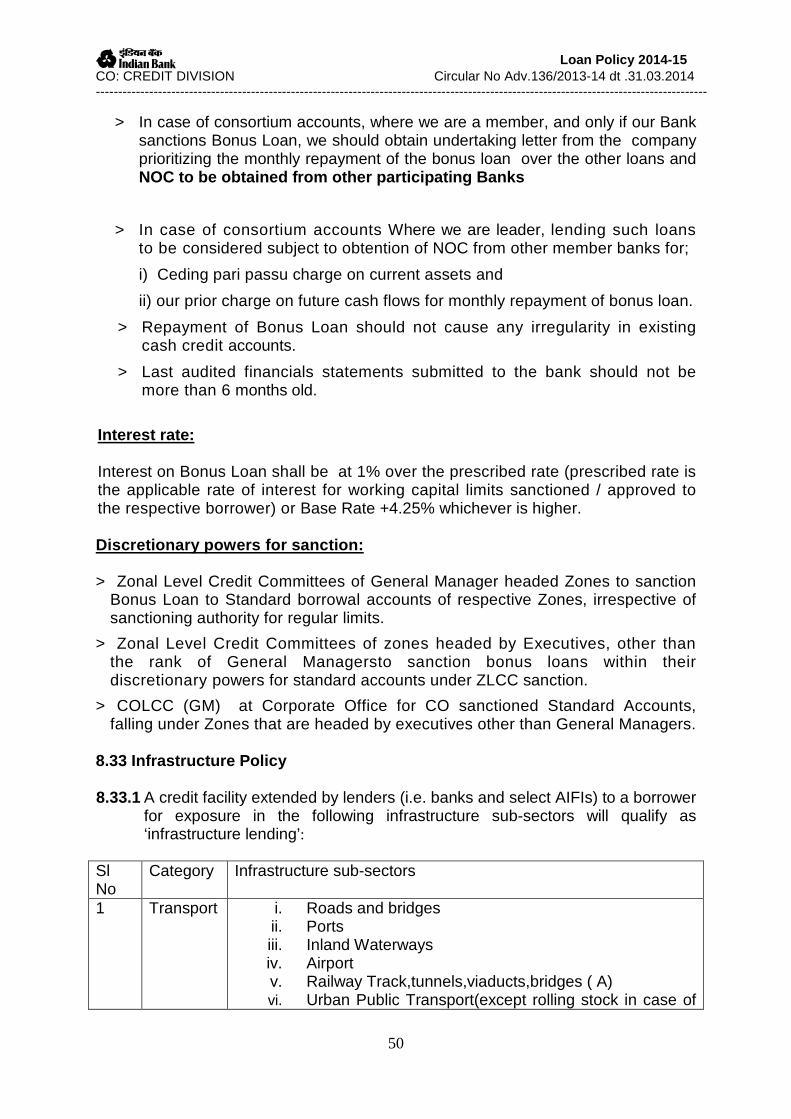

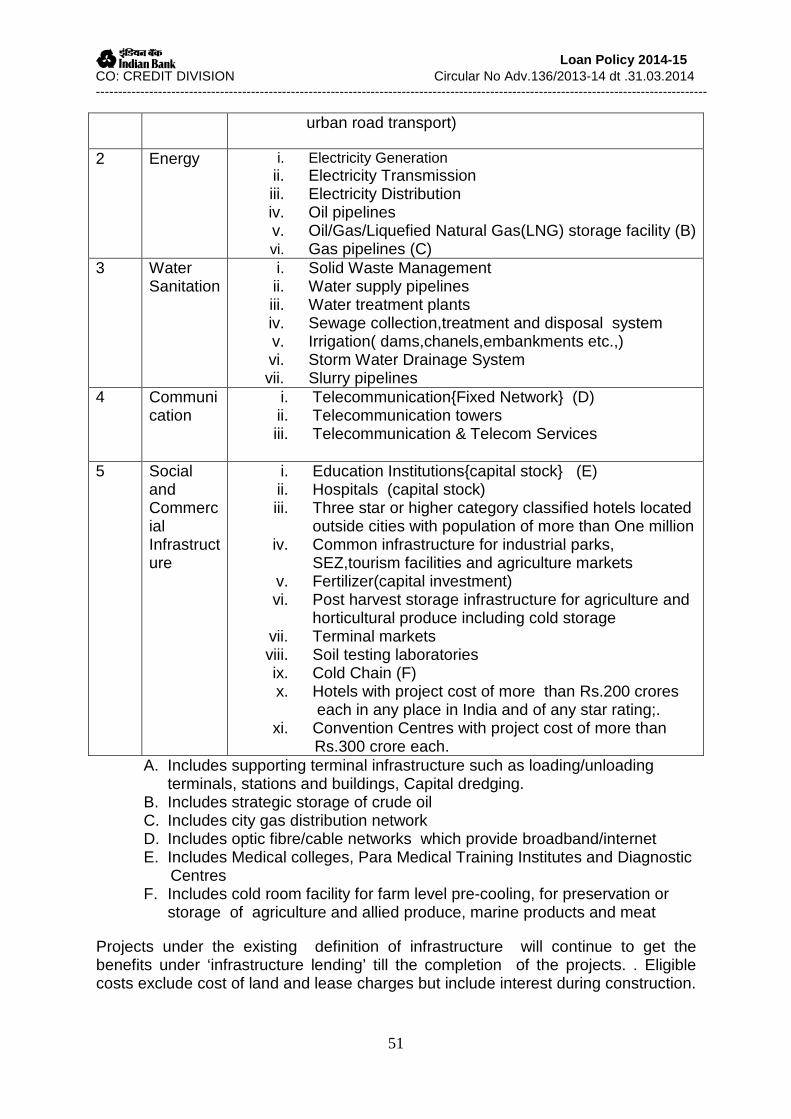

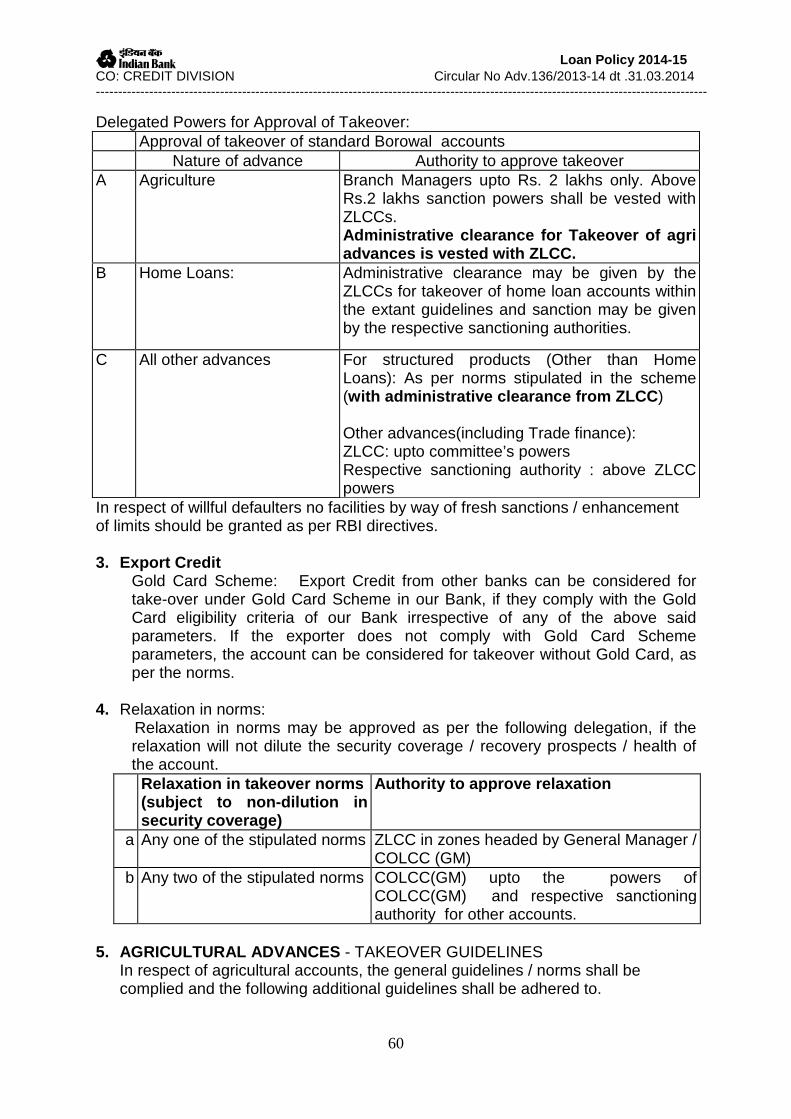

8.26 Subordinated debt / unsecured loan as quasi equity 43 8.27 Financing for disinvestment by the Government 43 8.28 Sanction of Term Loans to Housing Finance Institutions 44 8.29 Monitoring of implementation of project 44 8.30 Policy on Foreign Currency Loan 45 8.31 Policy on Bridge Loan 46 8.32 Bonus Loan Policy 49 8.33 Infrastrucure Policy 50-55 8.34 Cashew Loan Policy 55 8.35 Take –Over policy of borrowal accounts 57-63 8.36 Advances to Commercial Real Estate 63 8.37 Loans to Private Builders / Real Estate Developers 63 8.38 Lending to Non Banking Finance Companies (NBFC) 63

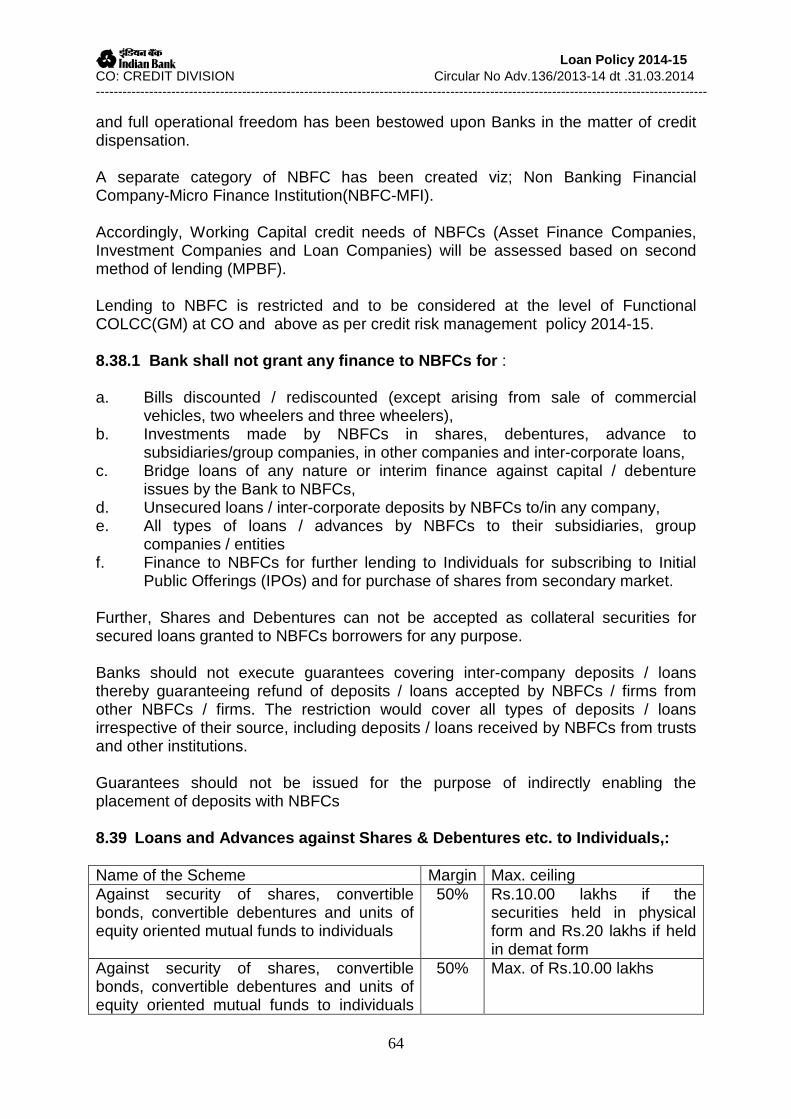

8.39 Loans and Advances against Shares & debentures etc., to individuals 64

8.40 Deemed Export 65 8.41 Short Term Loan 65 8.41.1 Line of credit 66 8.42 Clean Loans 67 8.43 Types of clean loans 67 8.44 Withdrawal Against Uncleared Cheques 67 8.45 Operation in secured OD accounts 68 8.46 Non-Fund Based (NFB) Limits 68 8.47 Guarantee on behalf of Special Purpose Vehicle (SPV) – Subsidiary 70

8.48 Issuance of Guarantees / Co-Acceptance by the Bank favouring other Banks / FIs / other lending agencies for additional loans extended them

70

8.49 Guidelines on issue of Bank Guarantees 70 8.50 Honouring of Bank Guarantees 70 8.51 Issue of Bank Guarantee in favour of Foreign Airlines/IATA 71 8.52 Letter of comfort(LOC)/Letter of undertaking(LOU) 71

8.53 Guidelines on classification of LC–DA / Guarantees as Secured Exposure

73

8.54 Settlement of claims under Letters of Credits (LCs) 73 8.54.1 Accounting procedures for devolved letter of credit (DA) 73 8.55 Forward Contracts / Hedging 74 8.56 Monitoring 78 8.57 Monitoring of Large Borrowal Accounts 80 8.58 Quality of credit 83 8.59 Visit by the Zonal Manager or the Second in Command of the Zone 84 8.60 Branch Segmentation 84

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

vi

Para No. Subject Page No

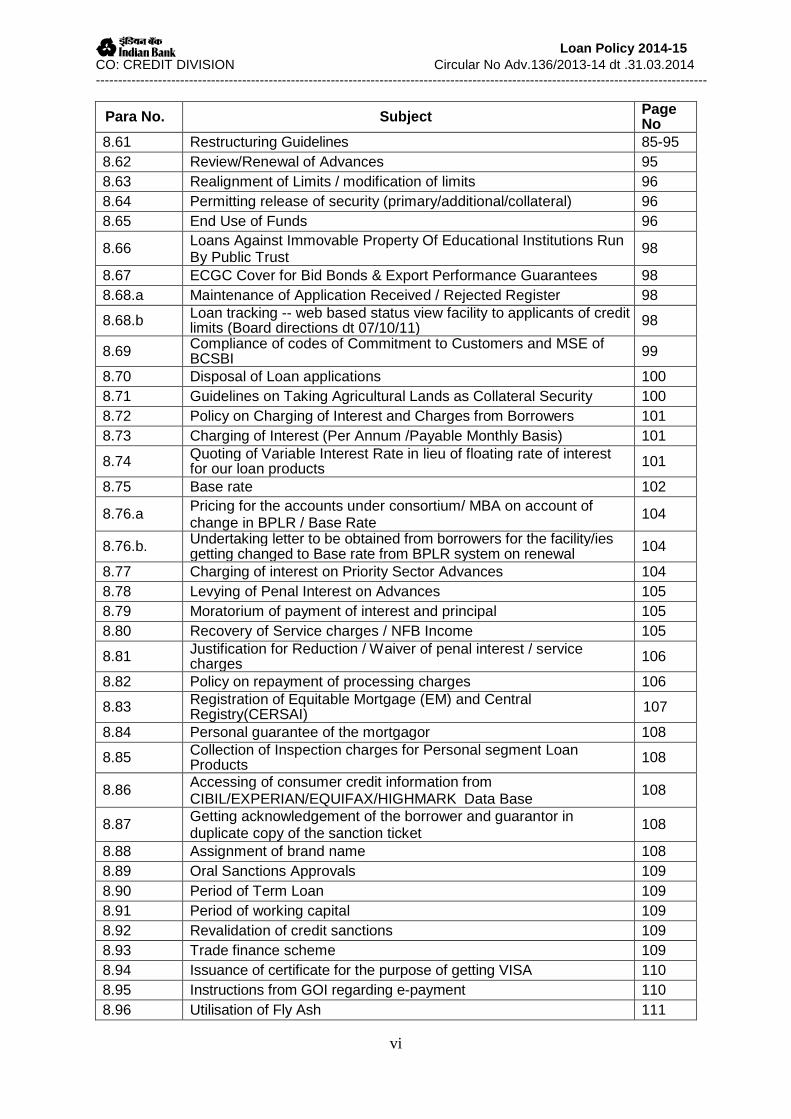

8.61 Restructuring Guidelines 85-95 8.62 Review/Renewal of Advances 95 8.63 Realignment of Limits / modification of limits 96 8.64 Permitting release of security (primary/additional/collateral) 96 8.65 End Use of Funds 96

8.66 Loans Against Immovable Property Of Educational Institutions Run By Public Trust

98

8.67 ECGC Cover for Bid Bonds & Export Performance Guarantees 98 8.68.a Maintenance of Application Received / Rejected Register 98

8.68.b Loan tracking -- web based status view facility to applicants of credit limits (Board directions dt 07/10/11) 98

8.69 Compliance of codes of Commitment to Customers and MSE of BCSBI 99

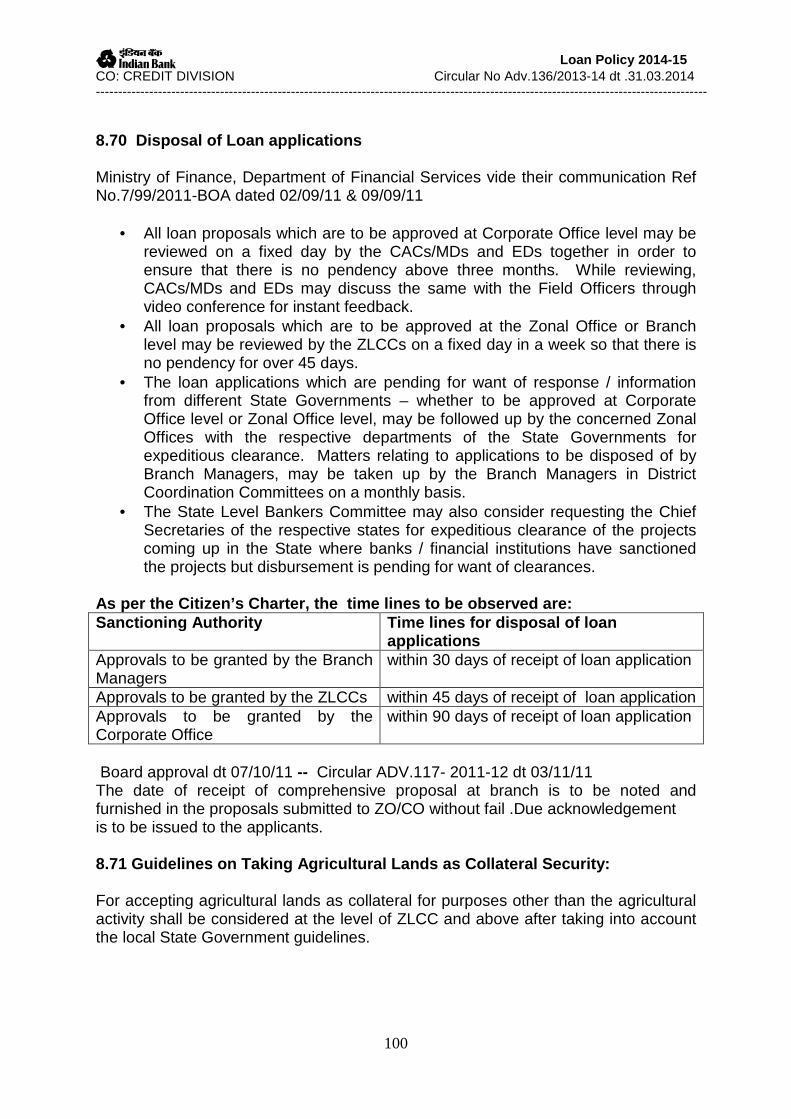

8.70 Disposal of Loan applications 100 8.71 Guidelines on Taking Agricultural Lands as Collateral Security 100 8.72 Policy on Charging of Interest and Charges from Borrowers 101 8.73 Charging of Interest (Per Annum /Payable Monthly Basis) 101

8.74 Quoting of Variable Interest Rate in lieu of floating rate of interest for our loan products 101

8.75 Base rate 102

8.76.a Pricing for the accounts under consortium/ MBA on account of change in BPLR / Base Rate

104

8.76.b. Undertaking letter to be obtained from borrowers for the facility/ies getting changed to Base rate from BPLR system on renewal 104

8.77 Charging of interest on Priority Sector Advances 104 8.78 Levying of Penal Interest on Advances 105 8.79 Moratorium of payment of interest and principal 105 8.80 Recovery of Service charges / NFB Income 105

8.81 Justification for Reduction / Waiver of penal interest / service charges 106

8.82 Policy on repayment of processing charges 106

8.83 Registration of Equitable Mortgage (EM) and Central Registry(CERSAI) 107

8.84 Personal guarantee of the mortgagor 108

8.85 Collection of Inspection charges for Personal segment Loan Products 108

8.86 Accessing of consumer credit information from CIBIL/EXPERIAN/EQUIFAX/HIGHMARK Data Base

108

8.87 Getting acknowledgement of the borrower and guarantor in duplicate copy of the sanction ticket

108

8.88 Assignment of brand name 108 8.89 Oral Sanctions Approvals 109 8.90 Period of Term Loan 109 8.91 Period of working capital 109 8.92 Revalidation of credit sanctions 109 8.93 Trade finance scheme 109 8.94 Issuance of certificate for the purpose of getting VISA 110 8.95 Instructions from GOI regarding e-payment 110 8.96 Utilisation of Fly Ash 111

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

vii

Para No. Subject Page No

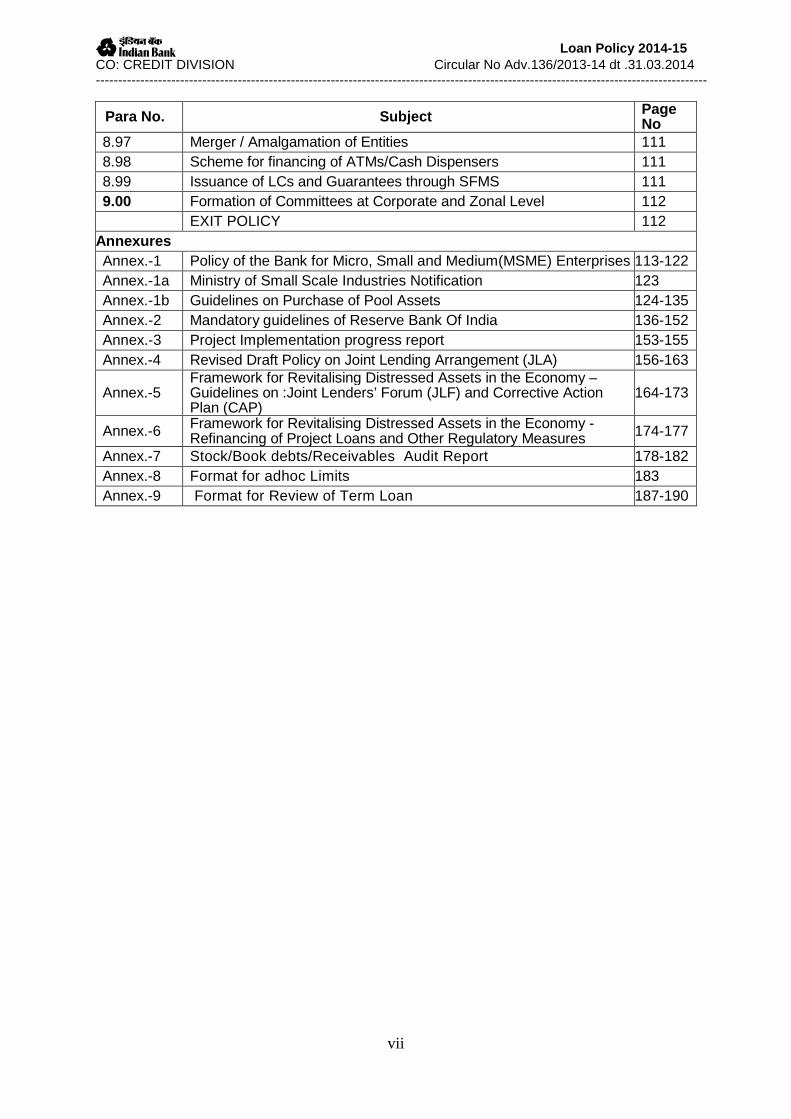

8.97 Merger / Amalgamation of Entities 111 8.98 Scheme for financing of ATMs/Cash Dispensers 111 8.99 Issuance of LCs and Guarantees through SFMS 111 9.00 Formation of Committees at Corporate and Zonal Level 112

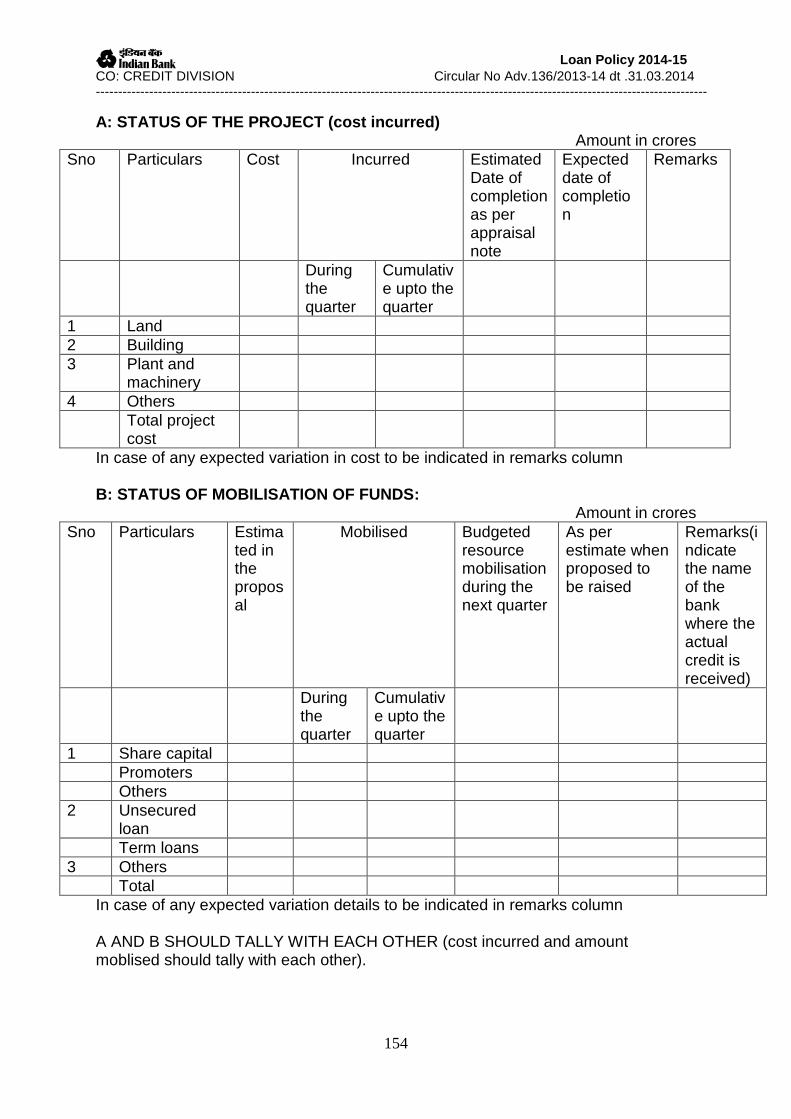

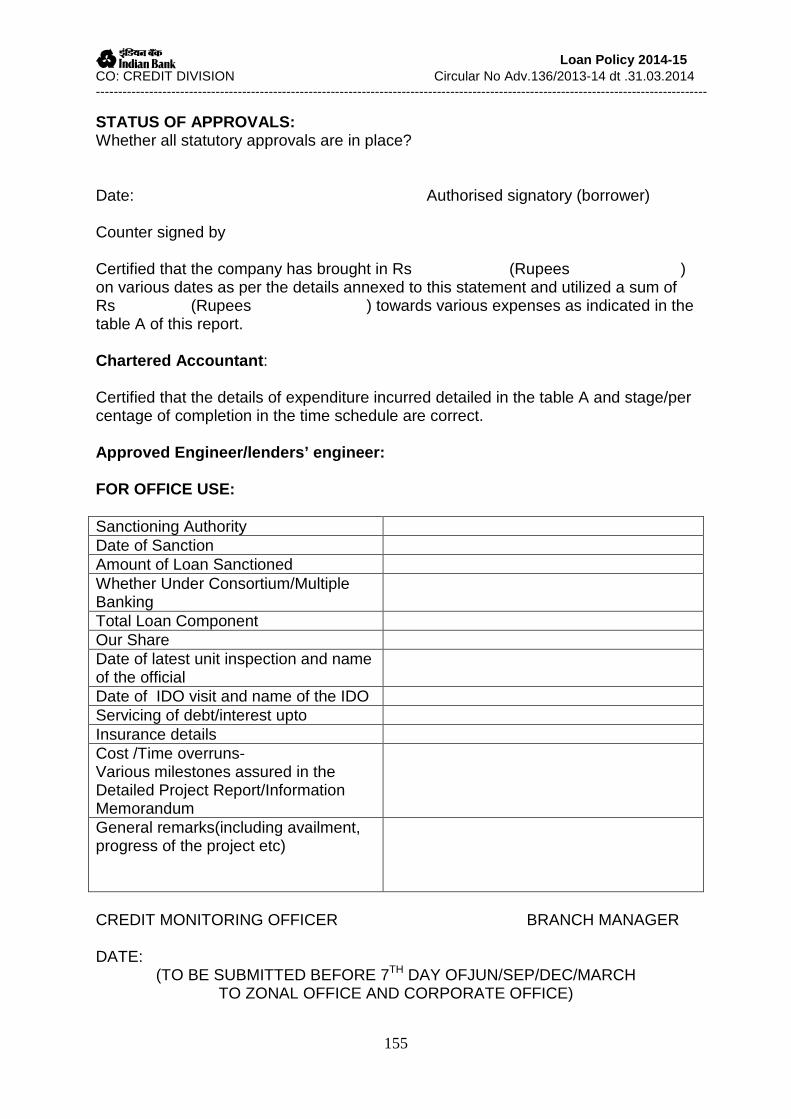

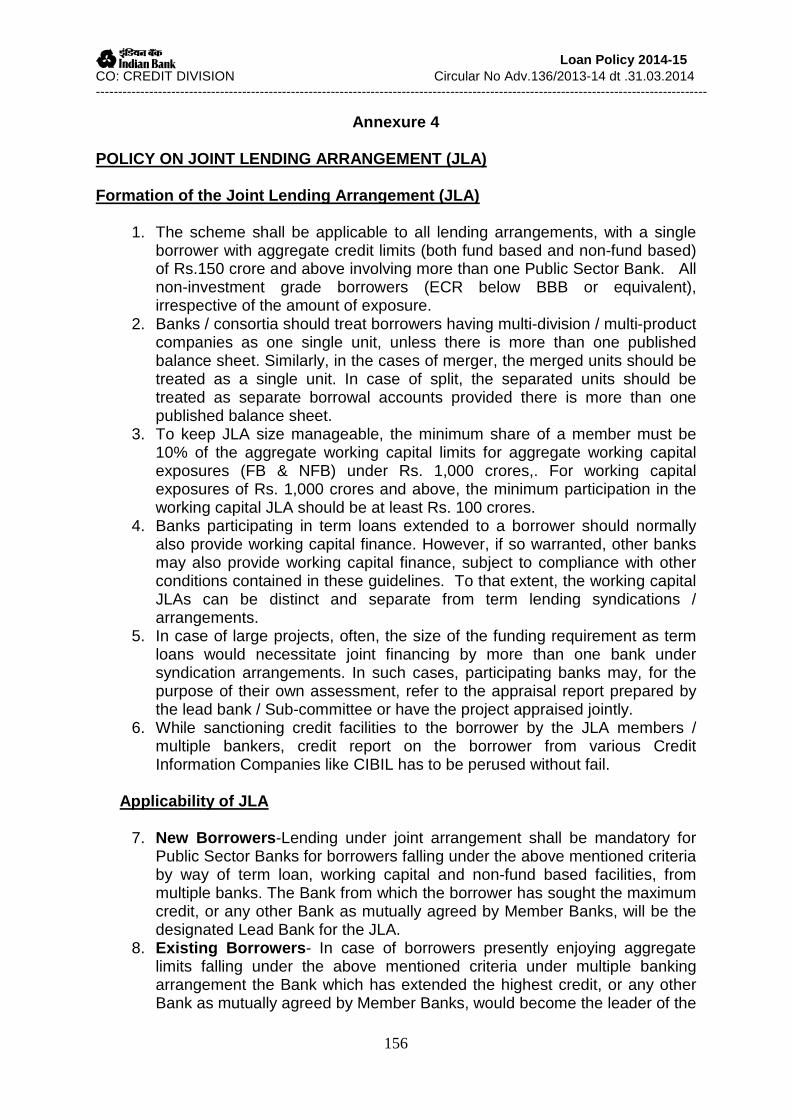

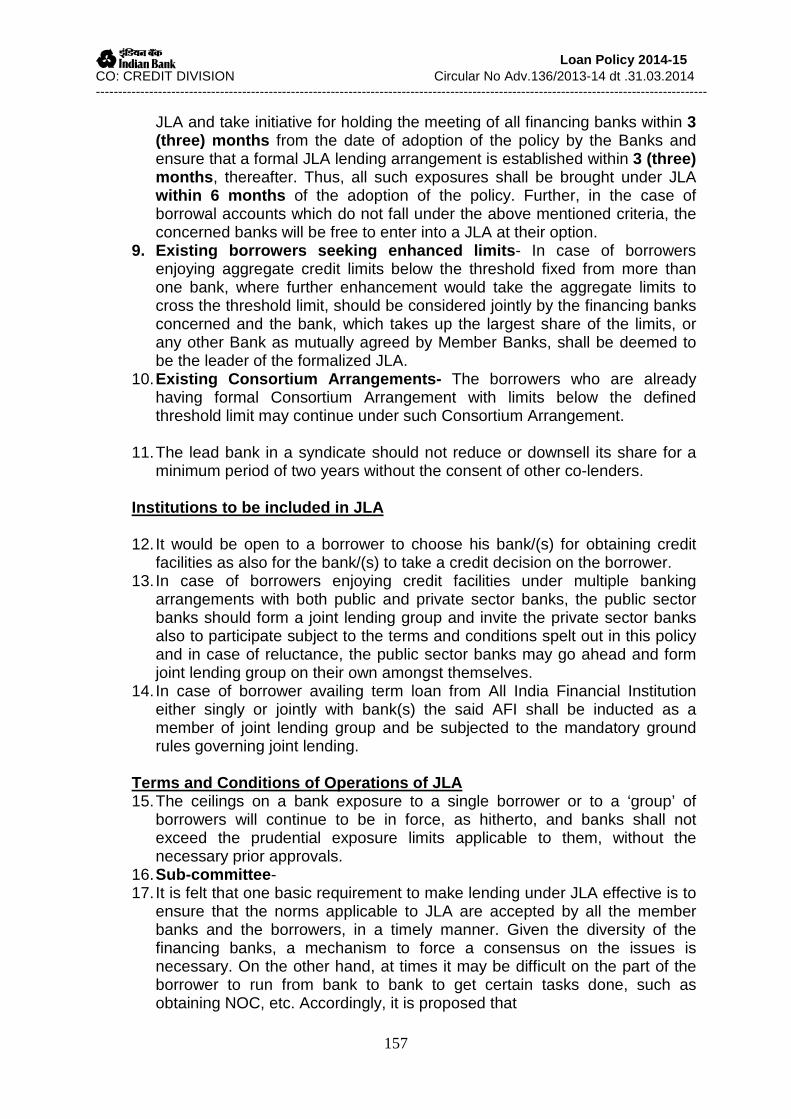

EXIT POLICY 112 Annexures Annex.-1 Policy of the Bank for Micro, Small and Medium(MSME) Enterprises 113-122 Annex.-1a Ministry of Small Scale Industries Notification 123 Annex.-1b Guidelines on Purchase of Pool Assets 124-135 Annex.-2 Mandatory guidelines of Reserve Bank Of India 136-152 Annex.-3 Project Implementation progress report 153-155 Annex.-4 Revised Draft Policy on Joint Lending Arrangement (JLA) 156-163

Annex.-5 Framework for Revitalising Distressed Assets in the Economy – Guidelines on :Joint Lenders’ Forum (JLF) and Corrective Action Plan (CAP)

164-173

Annex.-6 Framework for Revitalising Distressed Assets in the Economy - Refinancing of Project Loans and Other Regulatory Measures 174-177

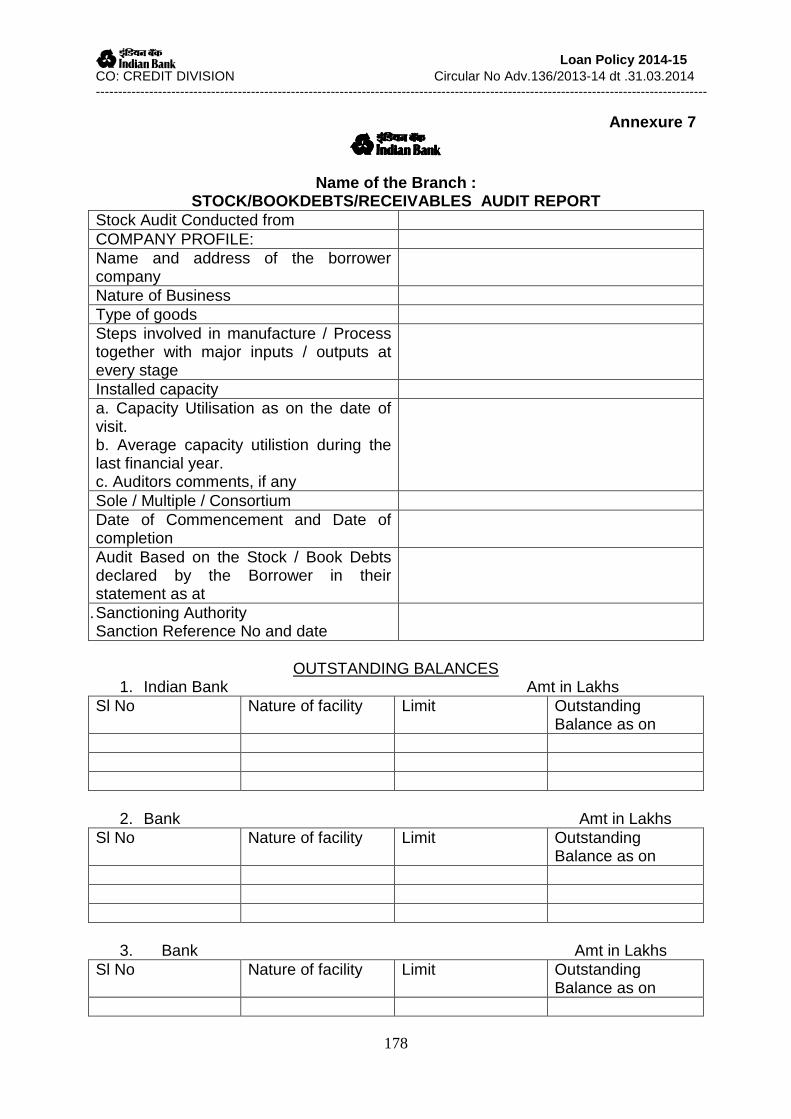

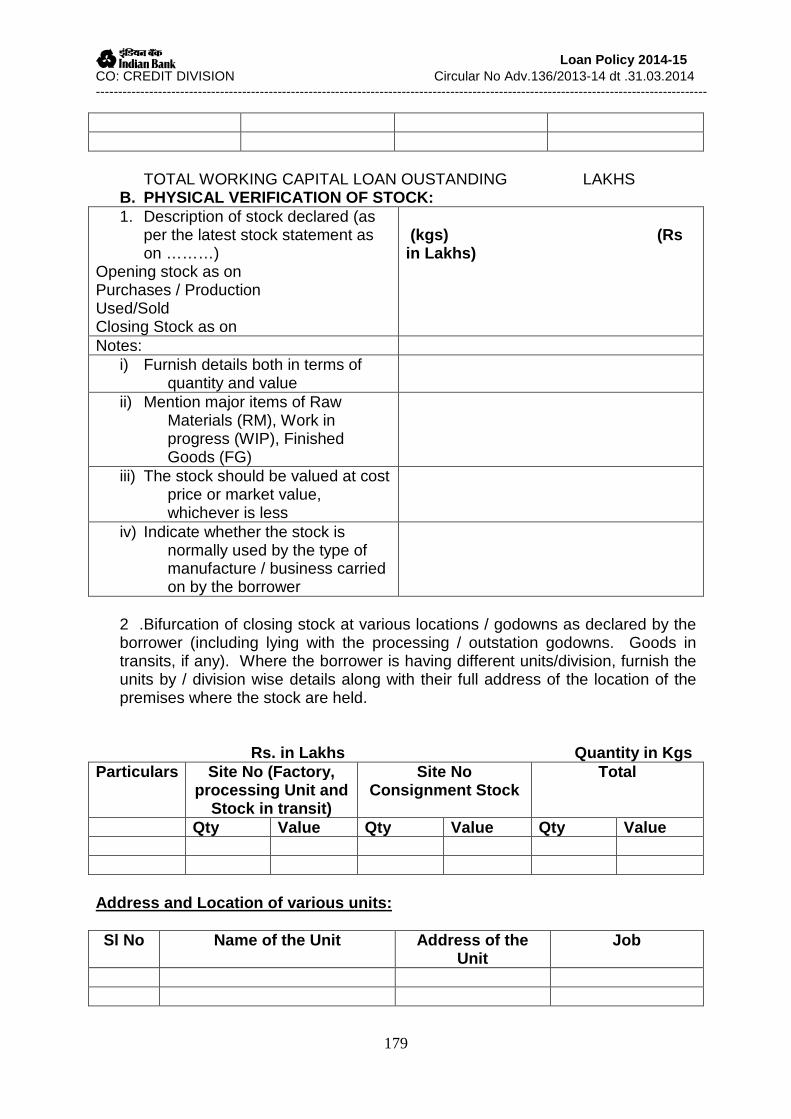

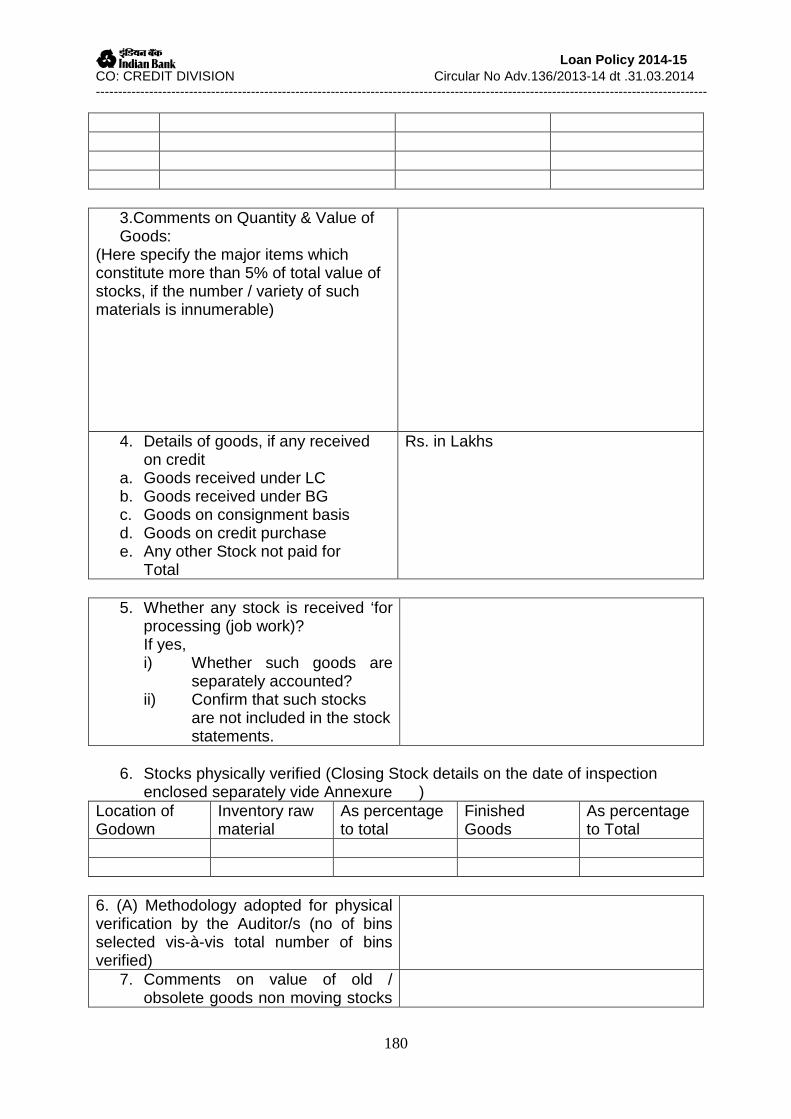

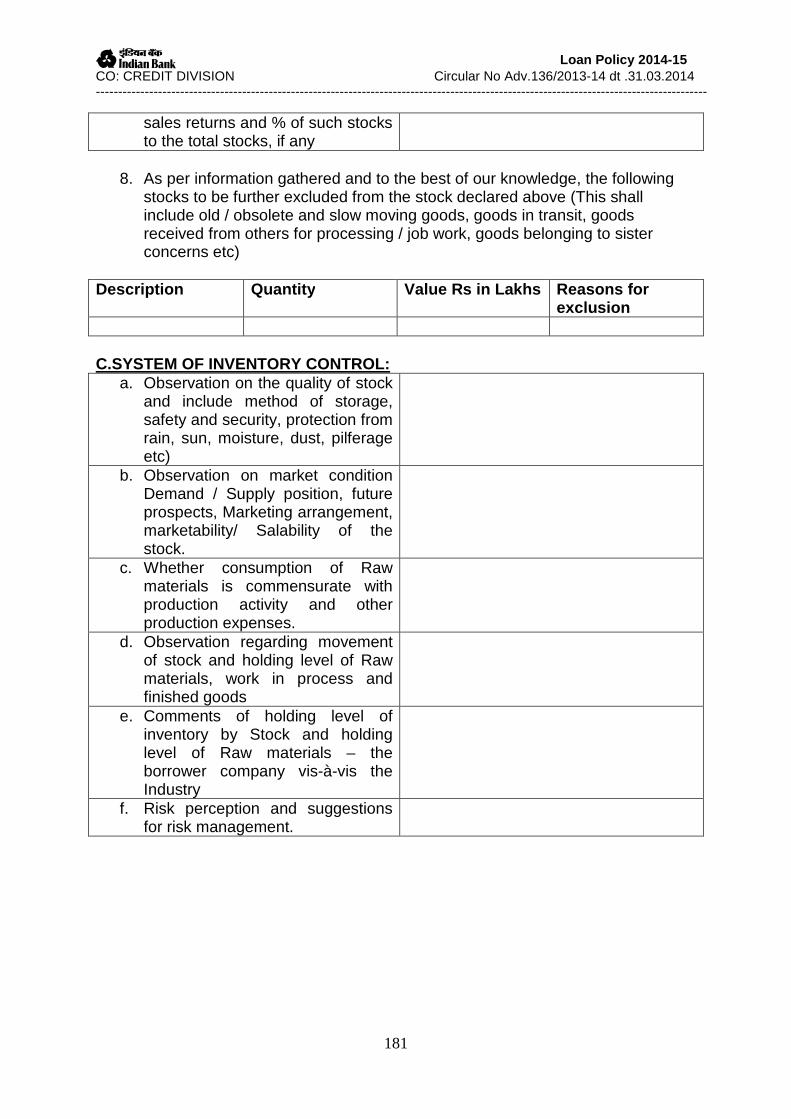

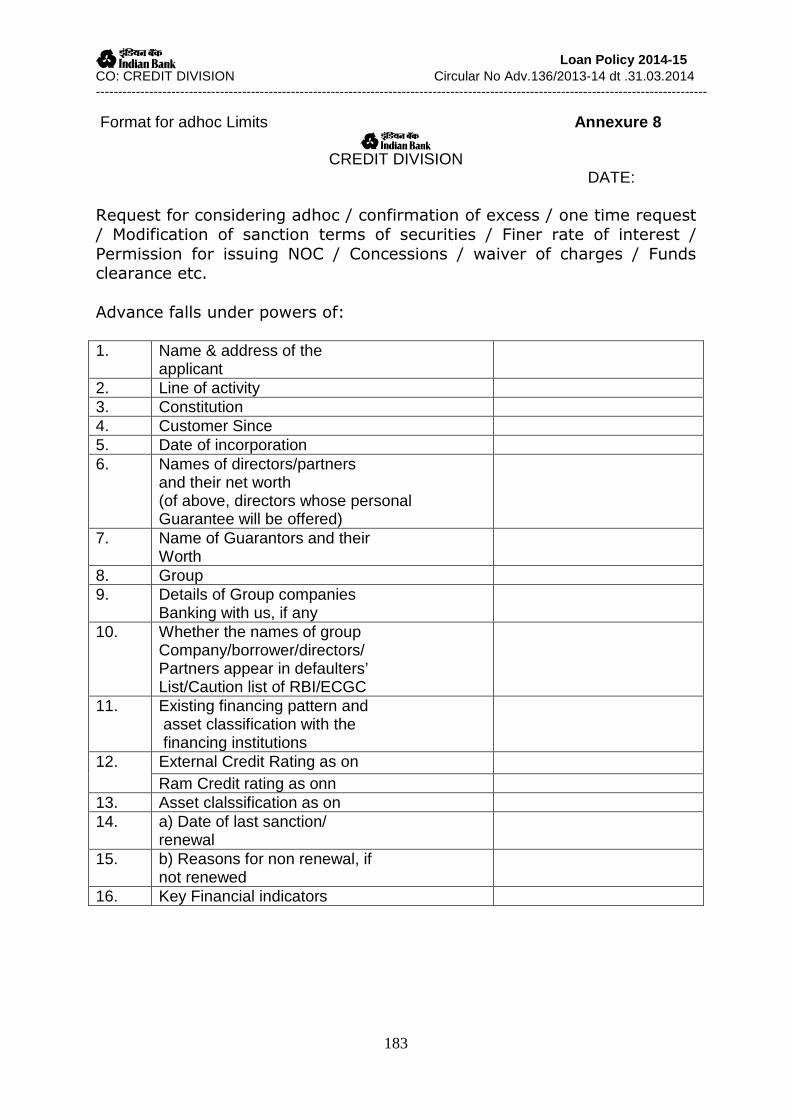

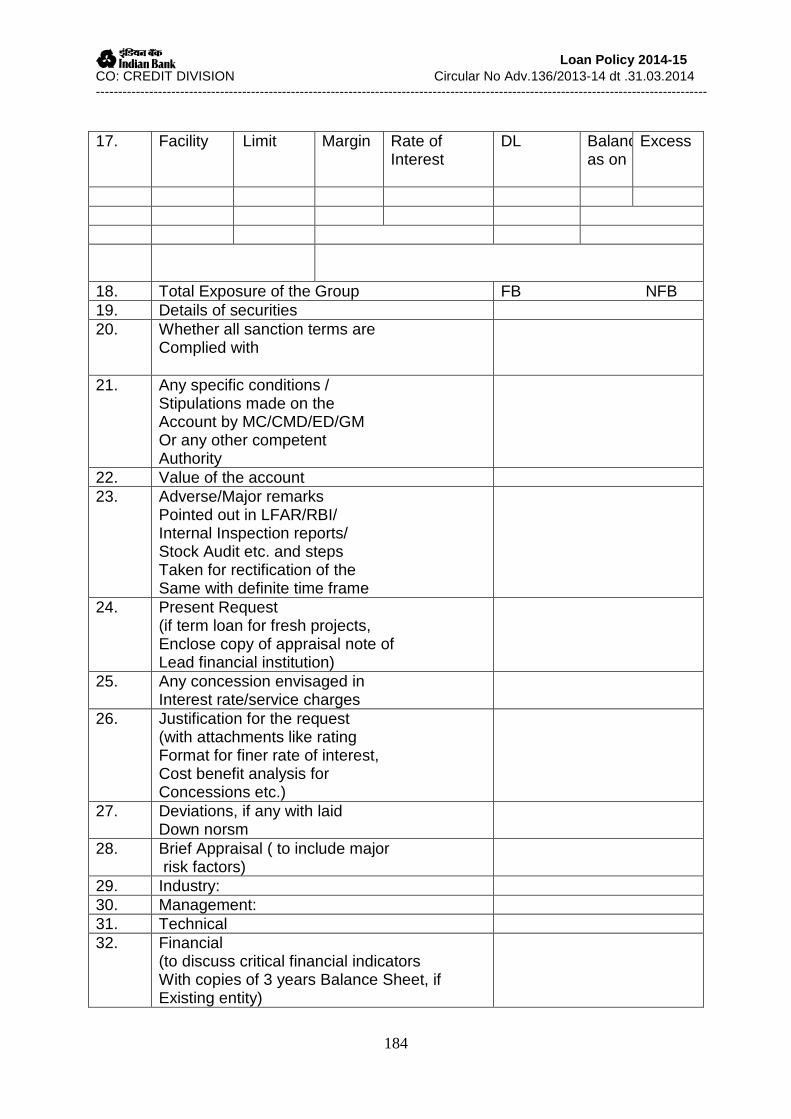

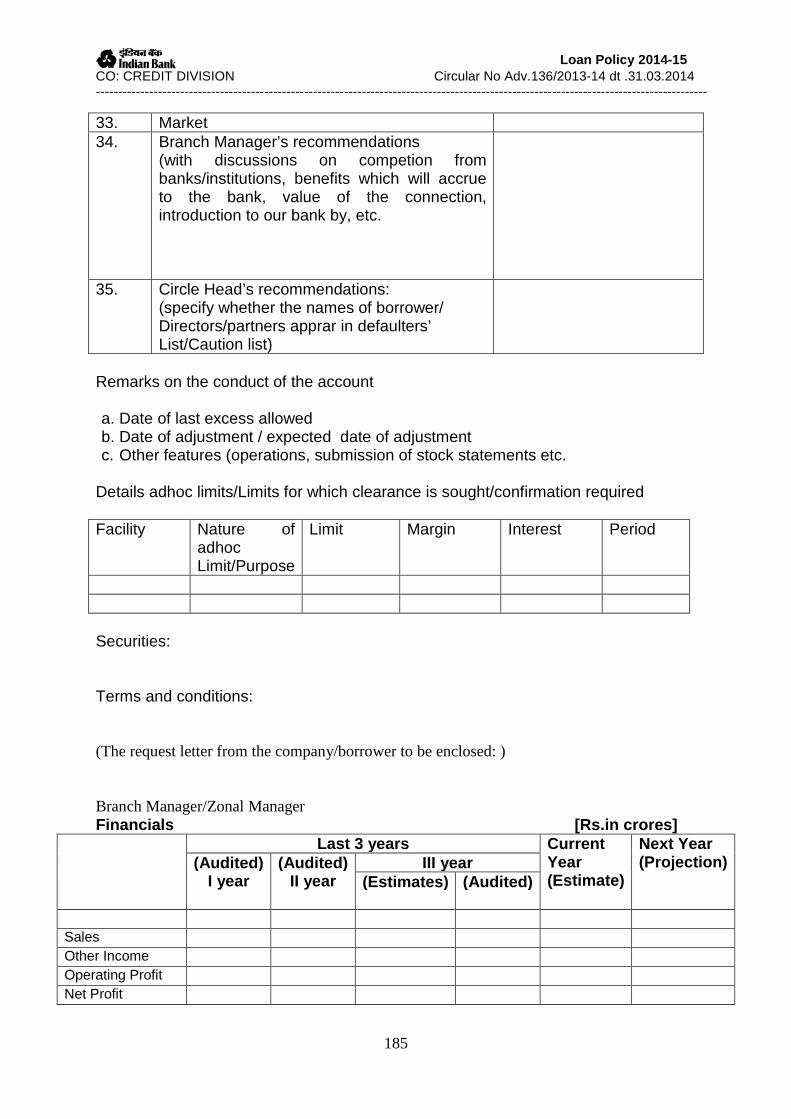

Annex.-7 Stock/Book debts/Receivables Audit Report 178-182 Annex.-8 Format for adhoc Limits 183 Annex.-9 Format for Review of Term Loan 187-190

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

viii

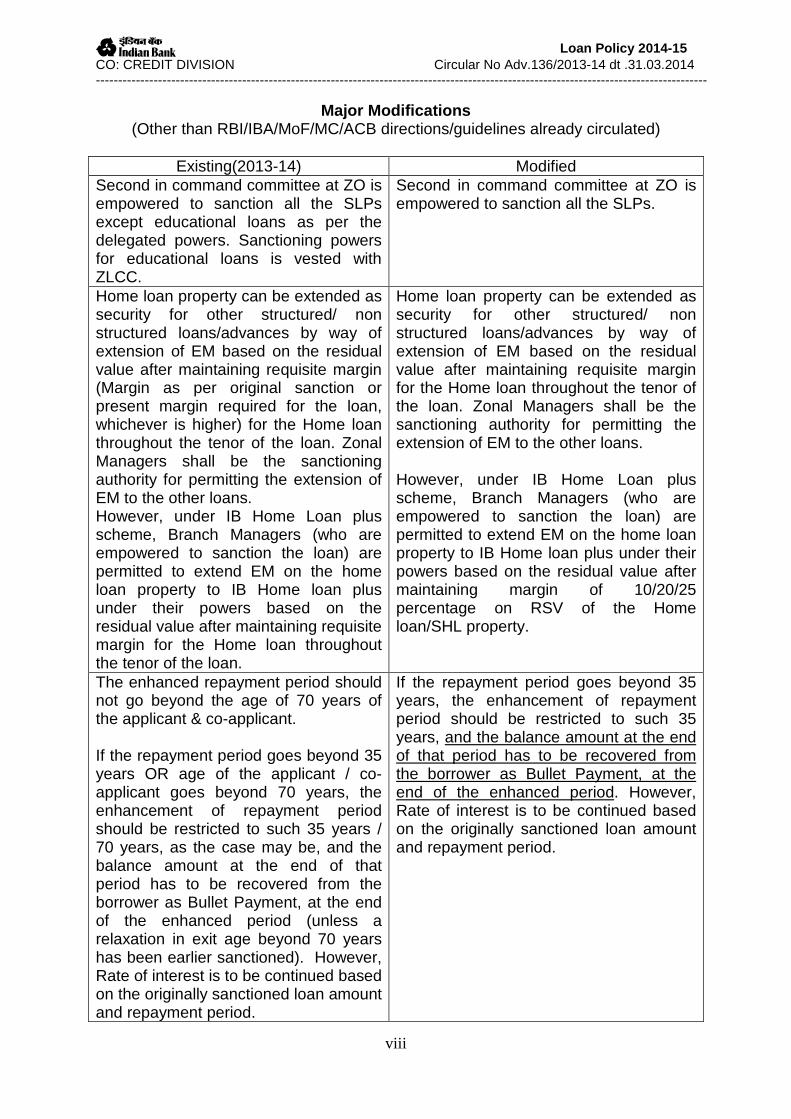

Major Modifications (Other than RBI/IBA/MoF/MC/ACB directions/guidelines already circulated)

Existing(2013-14) Modified

Second in command committee at ZO is empowered to sanction all the SLPs except educational loans as per the delegated powers. Sanctioning powers for educational loans is vested with ZLCC.

Second in command committee at ZO is empowered to sanction all the SLPs.

Home loan property can be extended as security for other structured/ non structured loans/advances by way of extension of EM based on the residual value after maintaining requisite margin (Margin as per original sanction or present margin required for the loan, whichever is higher) for the Home loan throughout the tenor of the loan. Zonal Managers shall be the sanctioning authority for permitting the extension of EM to the other loans. However, under IB Home Loan plus scheme, Branch Managers (who are empowered to sanction the loan) are permitted to extend EM on the home loan property to IB Home loan plus under their powers based on the residual value after maintaining requisite margin for the Home loan throughout the tenor of the loan.

Home loan property can be extended as security for other structured/ non structured loans/advances by way of extension of EM based on the residual value after maintaining requisite margin for the Home loan throughout the tenor of the loan. Zonal Managers shall be the sanctioning authority for permitting the extension of EM to the other loans. However, under IB Home Loan plus scheme, Branch Managers (who are empowered to sanction the loan) are permitted to extend EM on the home loan property to IB Home loan plus under their powers based on the residual value after maintaining margin of 10/20/25 percentage on RSV of the Home loan/SHL property.

The enhanced repayment period should not go beyond the age of 70 years of the applicant & co-applicant. If the repayment period goes beyond 35 years OR age of the applicant / co-applicant goes beyond 70 years, the enhancement of repayment period should be restricted to such 35 years / 70 years, as the case may be, and the balance amount at the end of that period has to be recovered from the borrower as Bullet Payment, at the end of the enhanced period (unless a relaxation in exit age beyond 70 years has been earlier sanctioned). However, Rate of interest is to be continued based on the originally sanctioned loan amount and repayment period.

If the repayment period goes beyond 35 years, the enhancement of repayment period should be restricted to such 35 years, and the balance amount at the end of that period has to be recovered from the borrower as Bullet Payment, at the end of the enhanced period. However, Rate of interest is to be continued based on the originally sanctioned loan amount and repayment period.

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

ix

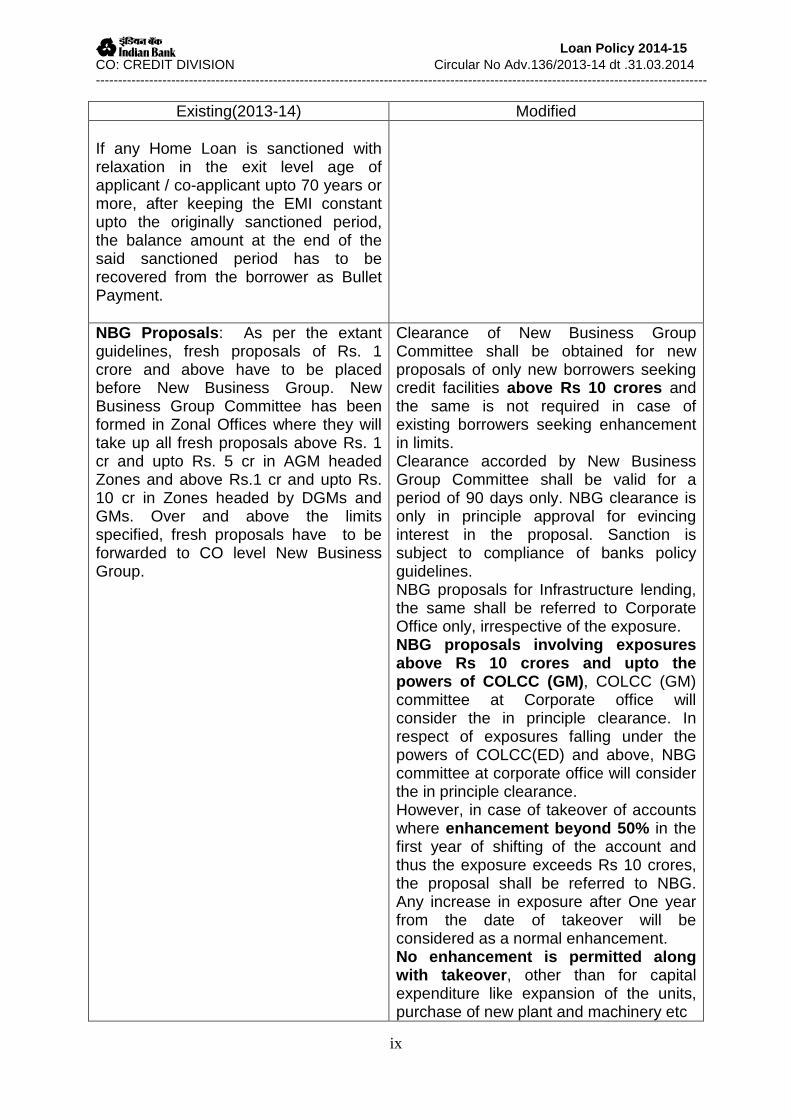

Existing(2013-14) Modified If any Home Loan is sanctioned with relaxation in the exit level age of applicant / co-applicant upto 70 years or more, after keeping the EMI constant upto the originally sanctioned period, the balance amount at the end of the said sanctioned period has to be recovered from the borrower as Bullet Payment. NBG Proposals : As per the extant guidelines, fresh proposals of Rs. 1 crore and above have to be placed before New Business Group. New Business Group Committee has been formed in Zonal Offices where they will take up all fresh proposals above Rs. 1 cr and upto Rs. 5 cr in AGM headed Zones and above Rs.1 cr and upto Rs. 10 cr in Zones headed by DGMs and GMs. Over and above the limits specified, fresh proposals have to be forwarded to CO level New Business Group.

Clearance of New Business Group Committee shall be obtained for new proposals of only new borrowers seeking credit facilities above Rs 10 crores and the same is not required in case of existing borrowers seeking enhancement in limits. Clearance accorded by New Business Group Committee shall be valid for a period of 90 days only. NBG clearance is only in principle approval for evincing interest in the proposal. Sanction is subject to compliance of banks policy guidelines. NBG proposals for Infrastructure lending, the same shall be referred to Corporate Office only, irrespective of the exposure. NBG proposals involving exposures above Rs 10 crores and upto the powers of COLCC (GM) , COLCC (GM) committee at Corporate office will consider the in principle clearance. In respect of exposures falling under the powers of COLCC(ED) and above, NBG committee at corporate office will consider the in principle clearance. However, in case of takeover of accounts where enhancement beyond 50% in the first year of shifting of the account and thus the exposure exceeds Rs 10 crores, the proposal shall be referred to NBG. Any increase in exposure after One year from the date of takeover will be considered as a normal enhancement. No enhancement is permitted along with takeover , other than for capital expenditure like expansion of the units, purchase of new plant and machinery etc

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

x

Existing(2013-14) Modified For the group accounts of existing satisfactorily conducted accounts, NBG clearance is not needed. In other cases i.e., fresh exposures to Companies / Firms / Groups with External Rating (Bank loan rating) of “AA” and above, no NBG approval is necessary.

Poultry Proposals: (iii) Fresh proposals for new units and fresh / enhancement proposals above Rs.2.00 Cr in case of integration / contract farming and existing units going for expansion , Zonal Managers shall obtain case by case approval from Corporate Office as follows:

a. Administrative clearance for each proposal (Fresh/ enhancement alone) up to Rs.2 Cr shall be accorded by COLCC (GM)

b. Administrative clearance for each proposal (Fresh/ enhancement alone) between Rs.2 Cr up to Rs.10 Cr will require clearance from CO :Credit Steering Committee through CO:RBD. On recommendation by CO: CSC the proposals are to be sanctioned by appropriate sanctioning authority at CO/ZO.

(iii) Fresh proposals for new units and fresh / enhancement proposals above Rs.2.00 Cr in case of integration / contract farming and existing units going for expansion , Zonal Managers shall obtain case by case approval from Corporate Office as follows:

a. Administrative clearance for each proposal (Fresh/ enhancement alone) above Rs. 2 cr and up to Rs.10 Cr shall be accorded by COLCC (GM)

Discussion with borrowers: It is reiterated that the proposed ROI / Margin / Securities / Specific or general terms and conditions must be discussed with the applicant and a specific confirmation from ZM in the covering letter of the proposal, that the proposed terms have the consent of the applicant, must be submitted

It is reiterated that the proposed ROI / Margin / Securities / Specific or general terms and conditions including Pre-disbursement and Post-disbursement conditions must be discussed with the applicant and a specific confirmation from ZLCC in the covering letter of the proposal, that the proposed terms have the consent of the applicant, must be submitted

c. Integrity and r eputation of the borrower

c. Due diligence on the borrower/guarantor/group. Addition: k.Pancard details l. Din/Father’s name. m. Verification of CIBIL Detect n. Market information on Promoter(s)

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

xi

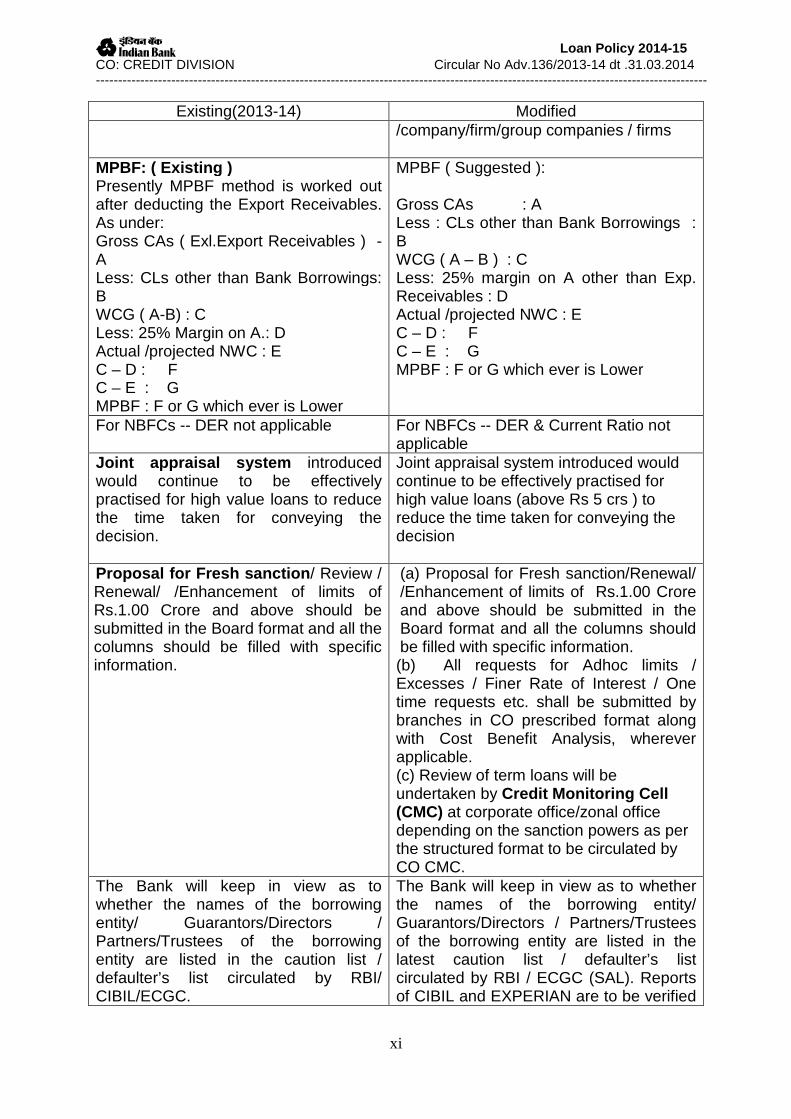

Existing(2013-14) Modified /company/firm/group companies / firms

MPBF: ( Existing ) Presently MPBF method is worked out after deducting the Export Receivables. As under: Gross CAs ( Exl.Export Receivables ) - A Less: CLs other than Bank Borrowings: B WCG ( A-B) : C Less: 25% Margin on A.: D Actual /projected NWC : E C – D : F C – E : G MPBF : F or G which ever is Lower

MPBF ( Suggested ): Gross CAs : A Less : CLs other than Bank Borrowings : B WCG ( A – B ) : C Less: 25% margin on A other than Exp. Receivables : D Actual /projected NWC : E C – D : F C – E : G MPBF : F or G which ever is Lower

For NBFCs -- DER not applicable For NBFCs -- DER & Current Ratio not applicable

Joint appraisal system introduced would continue to be effectively practised for high value loans to reduce the time taken for conveying the decision.

Joint appraisal system introduced would continue to be effectively practised for high value loans (above Rs 5 crs ) to reduce the time taken for conveying the decision

Proposal for Fresh sanction / Review / Renewal/ /Enhancement of limits of Rs.1.00 Crore and above should be submitted in the Board format and all the columns should be filled with specific information.

(a) Proposal for Fresh sanction/Renewal/ /Enhancement of limits of Rs.1.00 Crore and above should be submitted in the Board format and all the columns should be filled with specific information. (b) All requests for Adhoc limits / Excesses / Finer Rate of Interest / One time requests etc. shall be submitted by branches in CO prescribed format along with Cost Benefit Analysis, wherever applicable. (c) Review of term loans will be undertaken by Credit Monitoring Cell (CMC) at corporate office/zonal office depending on the sanction powers as per the structured format to be circulated by CO CMC.

The Bank will keep in view as to whether the names of the borrowing entity/ Guarantors/Directors / Partners/Trustees of the borrowing entity are listed in the caution list / defaulter’s list circulated by RBI/ CIBIL/ECGC.

The Bank will keep in view as to whether the names of the borrowing entity/ Guarantors/Directors / Partners/Trustees of the borrowing entity are listed in the latest caution list / defaulter’s list circulated by RBI / ECGC (SAL). Reports of CIBIL and EXPERIAN are to be verified

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

xii

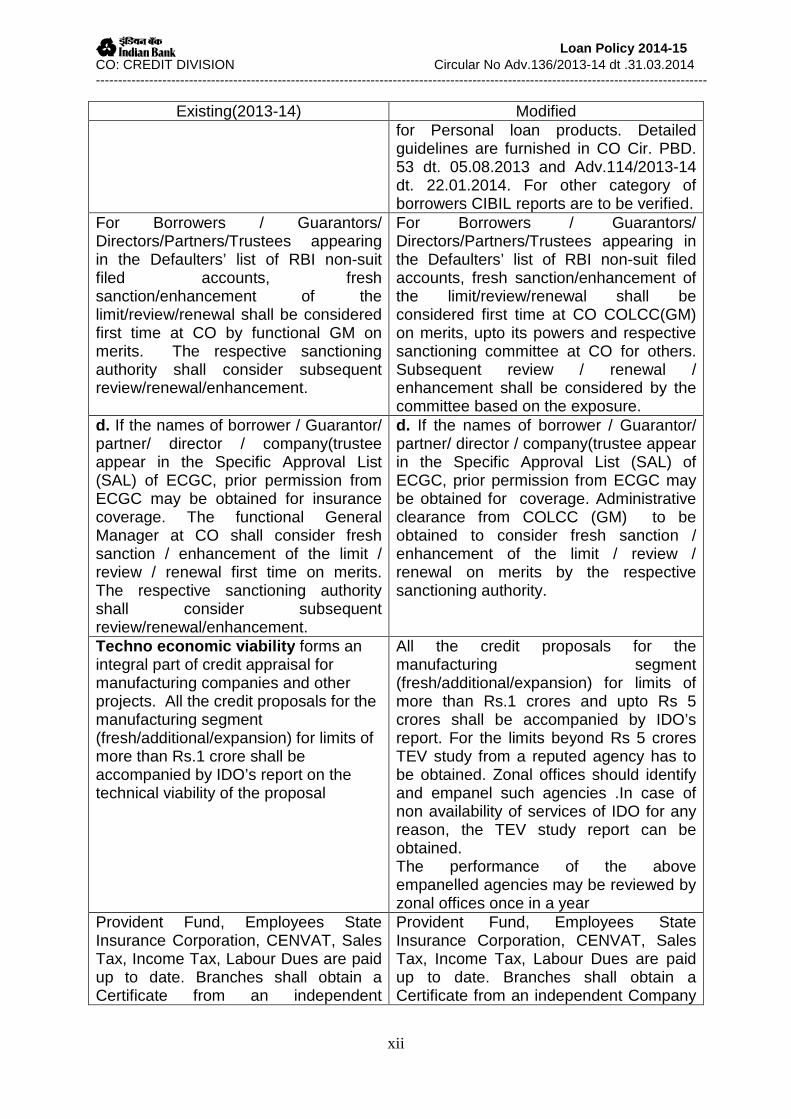

Existing(2013-14) Modified for Personal loan products. Detailed guidelines are furnished in CO Cir. PBD. 53 dt. 05.08.2013 and Adv.114/2013-14 dt. 22.01.2014. For other category of borrowers CIBIL reports are to be verified.

For Borrowers / Guarantors/ Directors/Partners/Trustees appearing in the Defaulters’ list of RBI non-suit filed accounts, fresh sanction/enhancement of the limit/review/renewal shall be considered first time at CO by functional GM on merits. The respective sanctioning authority shall consider subsequent review/renewal/enhancement.

For Borrowers / Guarantors/ Directors/Partners/Trustees appearing in the Defaulters’ list of RBI non-suit filed accounts, fresh sanction/enhancement of the limit/review/renewal shall be considered first time at CO COLCC(GM) on merits, upto its powers and respective sanctioning committee at CO for others. Subsequent review / renewal / enhancement shall be considered by the committee based on the exposure.

d. If the names of borrower / Guarantor/ partner/ director / company(trustee appear in the Specific Approval List (SAL) of ECGC, prior permission from ECGC may be obtained for insurance coverage. The functional General Manager at CO shall consider fresh sanction / enhancement of the limit / review / renewal first time on merits. The respective sanctioning authority shall consider subsequent review/renewal/enhancement.

d. If the names of borrower / Guarantor/ partner/ director / company(trustee appear in the Specific Approval List (SAL) of ECGC, prior permission from ECGC may be obtained for coverage. Administrative clearance from COLCC (GM) to be obtained to consider fresh sanction / enhancement of the limit / review / renewal on merits by the respective sanctioning authority.

Techno economic viability forms an integral part of credit appraisal for manufacturing companies and other projects. All the credit proposals for the manufacturing segment (fresh/additional/expansion) for limits of more than Rs.1 crore shall be accompanied by IDO’s report on the technical viability of the proposal

All the credit proposals for the manufacturing segment (fresh/additional/expansion) for limits of more than Rs.1 crores and upto Rs 5 crores shall be accompanied by IDO’s report. For the limits beyond Rs 5 crores TEV study from a reputed agency has to be obtained. Zonal offices should identify and empanel such agencies .In case of non availability of services of IDO for any reason, the TEV study report can be obtained. The performance of the above empanelled agencies may be reviewed by zonal offices once in a year

Provident Fund, Employees State Insurance Corporation, CENVAT, Sales Tax, Income Tax, Labour Dues are paid up to date. Branches shall obtain a Certificate from an independent

Provident Fund, Employees State Insurance Corporation, CENVAT, Sales Tax, Income Tax, Labour Dues are paid up to date. Branches shall obtain a Certificate from an independent Company

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

xiii

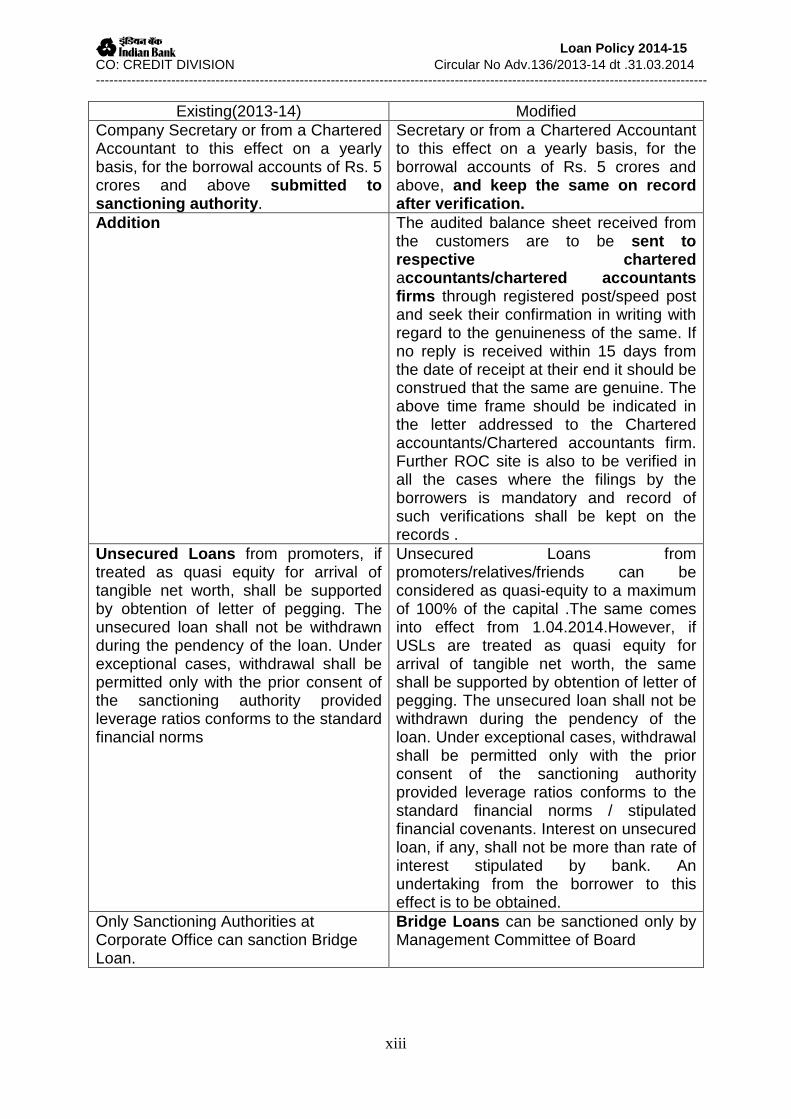

Existing(2013-14) Modified Company Secretary or from a Chartered Accountant to this effect on a yearly basis, for the borrowal accounts of Rs. 5 crores and above submitted to sanctioning authority .

Secretary or from a Chartered Accountant to this effect on a yearly basis, for the borrowal accounts of Rs. 5 crores and above, and keep the same on record after verification.

Addition The audited balance sheet received from the customers are to be sent to respective chartered accountants/chartered accountants firms through registered post/speed post and seek their confirmation in writing with regard to the genuineness of the same. If no reply is received within 15 days from the date of receipt at their end it should be construed that the same are genuine. The above time frame should be indicated in the letter addressed to the Chartered accountants/Chartered accountants firm. Further ROC site is also to be verified in all the cases where the filings by the borrowers is mandatory and record of such verifications shall be kept on the records .

Unsecured Loans from promoters, if treated as quasi equity for arrival of tangible net worth, shall be supported by obtention of letter of pegging. The unsecured loan shall not be withdrawn during the pendency of the loan. Under exceptional cases, withdrawal shall be permitted only with the prior consent of the sanctioning authority provided leverage ratios conforms to the standard financial norms

Unsecured Loans from promoters/relatives/friends can be considered as quasi-equity to a maximum of 100% of the capital .The same comes into effect from 1.04.2014.However, if USLs are treated as quasi equity for arrival of tangible net worth, the same shall be supported by obtention of letter of pegging. The unsecured loan shall not be withdrawn during the pendency of the loan. Under exceptional cases, withdrawal shall be permitted only with the prior consent of the sanctioning authority provided leverage ratios conforms to the standard financial norms / stipulated financial covenants. Interest on unsecured loan, if any, shall not be more than rate of interest stipulated by bank. An undertaking from the borrower to this effect is to be obtained.

Only Sanctioning Authorities at Corporate Office can sanction Bridge Loan.

Bridge Loans can be sanctioned only by Management Committee of Board

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

xiv

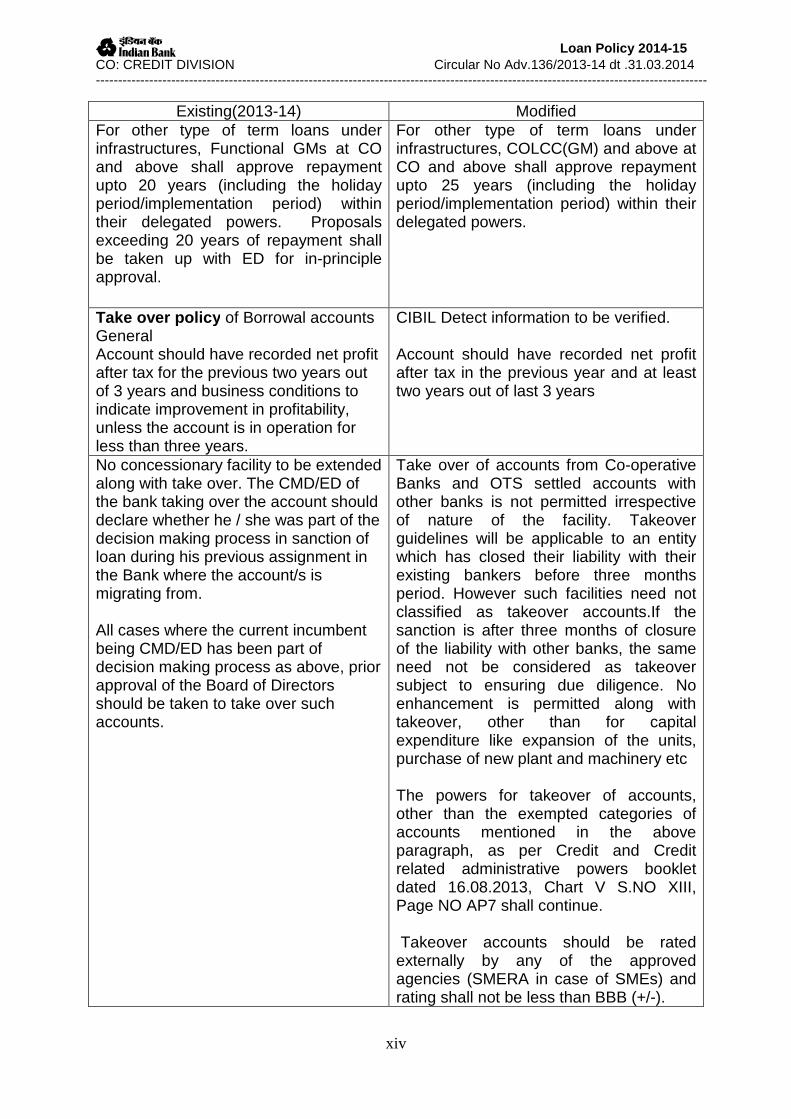

Existing(2013-14) Modified For other type of term loans under infrastructures, Functional GMs at CO and above shall approve repayment upto 20 years (including the holiday period/implementation period) within their delegated powers. Proposals exceeding 20 years of repayment shall be taken up with ED for in-principle approval.

For other type of term loans under infrastructures, COLCC(GM) and above at CO and above shall approve repayment upto 25 years (including the holiday period/implementation period) within their delegated powers.

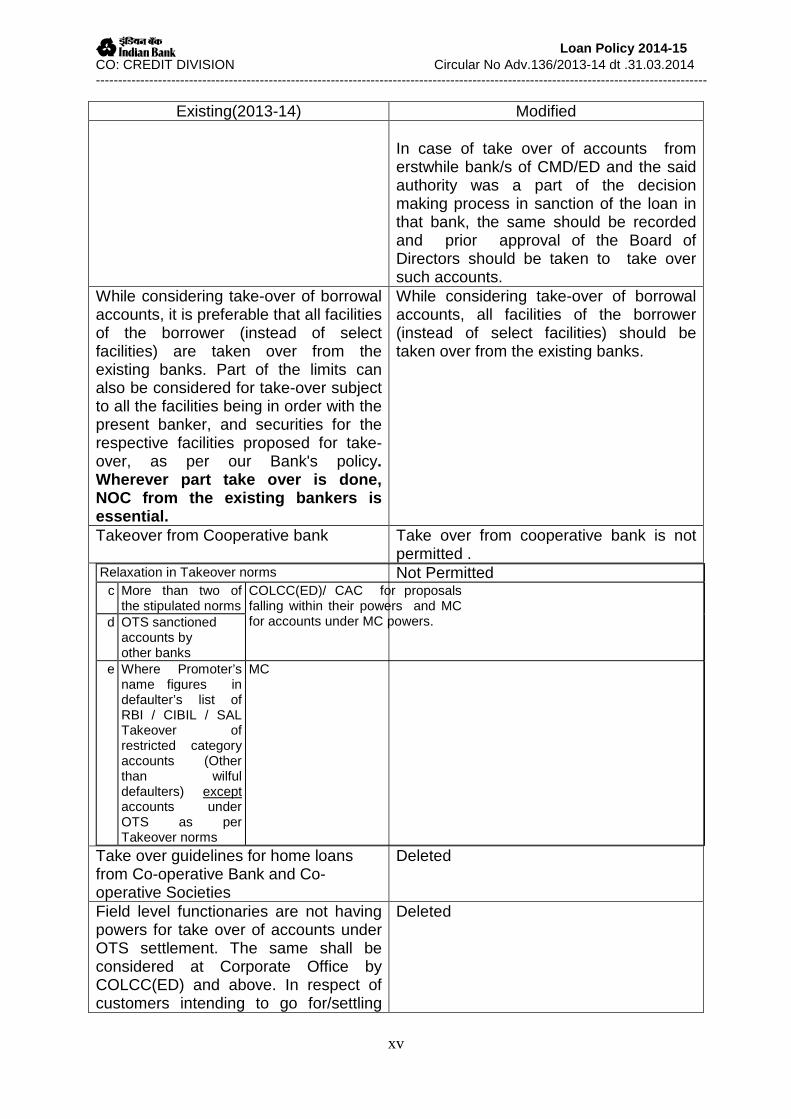

Take over policy of Borrowal accounts General Account should have recorded net profit after tax for the previous two years out of 3 years and business conditions to indicate improvement in profitability, unless the account is in operation for less than three years.

CIBIL Detect information to be verified. Account should have recorded net profit after tax in the previous year and at least two years out of last 3 years

No concessionary facility to be extended along with take over. The CMD/ED of the bank taking over the account should declare whether he / she was part of the decision making process in sanction of loan during his previous assignment in the Bank where the account/s is migrating from. All cases where the current incumbent being CMD/ED has been part of decision making process as above, prior approval of the Board of Directors should be taken to take over such accounts.

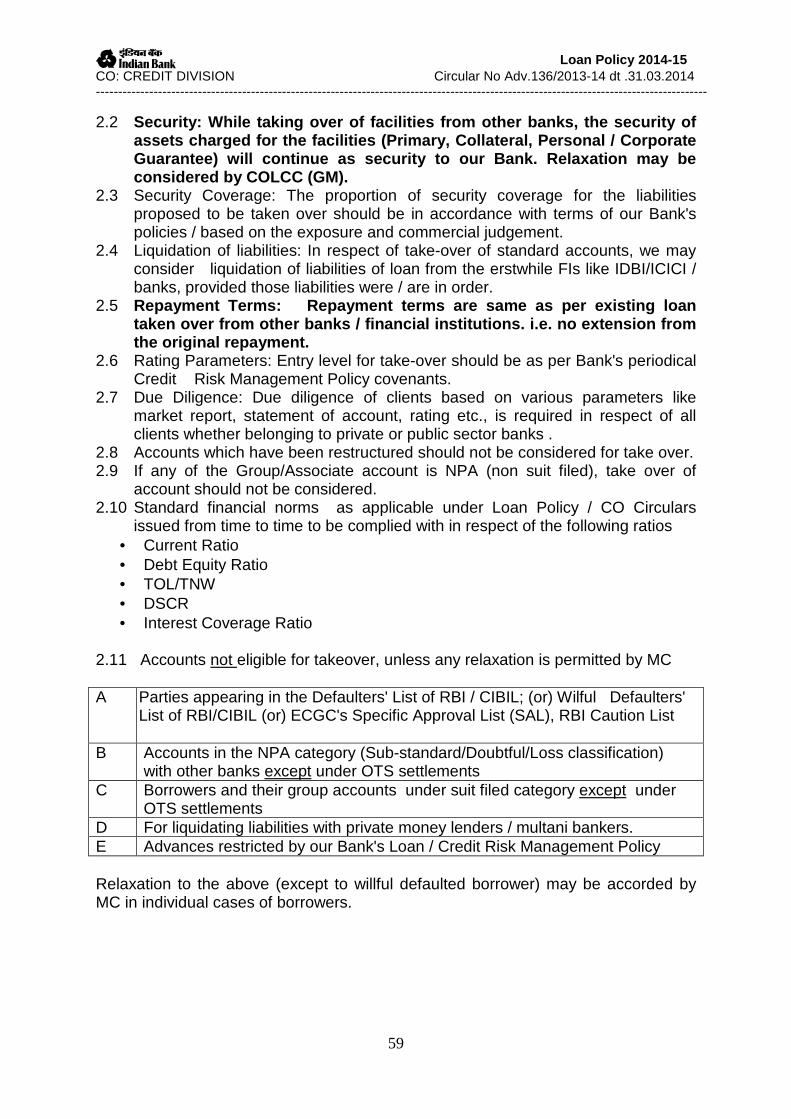

Take over of accounts from Co-operative Banks and OTS settled accounts with other banks is not permitted irrespective of nature of the facility. Takeover guidelines will be applicable to an entity which has closed their liability with their existing bankers before three months period. However such facilities need not classified as takeover accounts.If the sanction is after three months of closure of the liability with other banks, the same need not be considered as takeover subject to ensuring due diligence. No enhancement is permitted along with takeover, other than for capital expenditure like expansion of the units, purchase of new plant and machinery etc The powers for takeover of accounts, other than the exempted categories of accounts mentioned in the above paragraph, as per Credit and Credit related administrative powers booklet dated 16.08.2013, Chart V S.NO XIII, Page NO AP7 shall continue. Takeover accounts should be rated externally by any of the approved agencies (SMERA in case of SMEs) and rating shall not be less than BBB (+/-).

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

xv

Existing(2013-14) Modified In case of take over of accounts from erstwhile bank/s of CMD/ED and the said authority was a part of the decision making process in sanction of the loan in that bank, the same should be recorded and prior approval of the Board of Directors should be taken to take over such accounts.

While considering take-over of borrowal accounts, it is preferable that all facilities of the borrower (instead of select facilities) are taken over from the existing banks. Part of the limits can also be considered for take-over subject to all the facilities being in order with the present banker, and securities for the respective facilities proposed for take-over, as per our Bank's policy. Wherever part take over is done, NOC from the existing bankers is essential.

While considering take-over of borrowal accounts, all facilities of the borrower (instead of select facilities) should be taken over from the existing banks.

Takeover from Cooperative bank Take over from cooperative bank is not permitted .

Relaxation in Takeover norms c More than two of

the stipulated norms COLCC(ED)/ CAC for proposals falling within their powers and MC for accounts under MC powers. d OTS sanctioned

accounts by other banks

e Where Promoter’s name figures in defaulter’s list of RBI / CIBIL / SAL Takeover of restricted category accounts (Other than wilful defaulters) except accounts under OTS as per Takeover norms

MC

Not Permitted

Take over guidelines for home loans from Co-operative Bank and Co-operative Societies

Deleted

Field level functionaries are not having powers for take over of accounts under OTS settlement. The same shall be considered at Corporate Office by COLCC(ED) and above. In respect of customers intending to go for/settling

Deleted

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

xvi

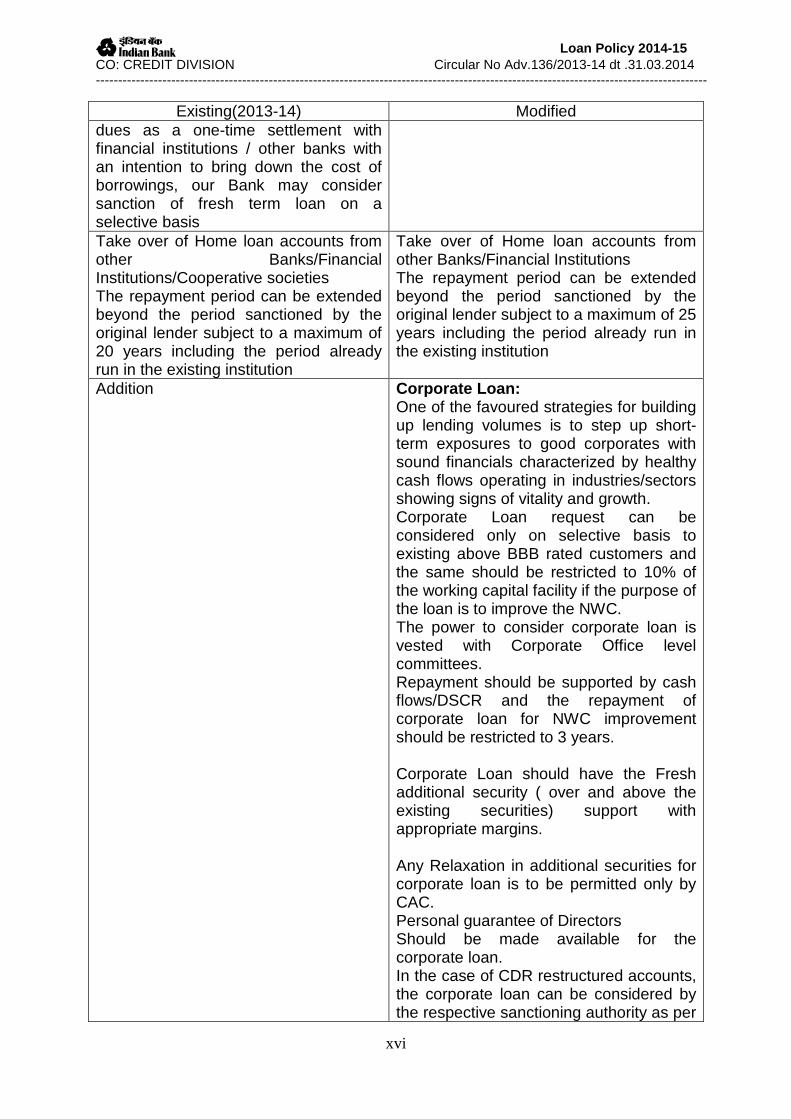

Existing(2013-14) Modified dues as a one-time settlement with financial institutions / other banks with an intention to bring down the cost of borrowings, our Bank may consider sanction of fresh term loan on a selective basis Take over of Home loan accounts from other Banks/Financial Institutions/Cooperative societies The repayment period can be extended beyond the period sanctioned by the original lender subject to a maximum of 20 years including the period already run in the existing institution

Take over of Home loan accounts from other Banks/Financial Institutions The repayment period can be extended beyond the period sanctioned by the original lender subject to a maximum of 25 years including the period already run in the existing institution

Addition Corporate Loan: One of the favoured strategies for building up lending volumes is to step up short-term exposures to good corporates with sound financials characterized by healthy cash flows operating in industries/sectors showing signs of vitality and growth. Corporate Loan request can be considered only on selective basis to existing above BBB rated customers and the same should be restricted to 10% of the working capital facility if the purpose of the loan is to improve the NWC. The power to consider corporate loan is vested with Corporate Office level committees. Repayment should be supported by cash flows/DSCR and the repayment of corporate loan for NWC improvement should be restricted to 3 years. Corporate Loan should have the Fresh additional security ( over and above the existing securities) support with appropriate margins. Any Relaxation in additional securities for corporate loan is to be permitted only by CAC. Personal guarantee of Directors Should be made available for the corporate loan. In the case of CDR restructured accounts, the corporate loan can be considered by the respective sanctioning authority as per

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

xvii

Existing(2013-14) Modified the terms of the Final Package of the Monitoring Institution subject to approval of CDR.

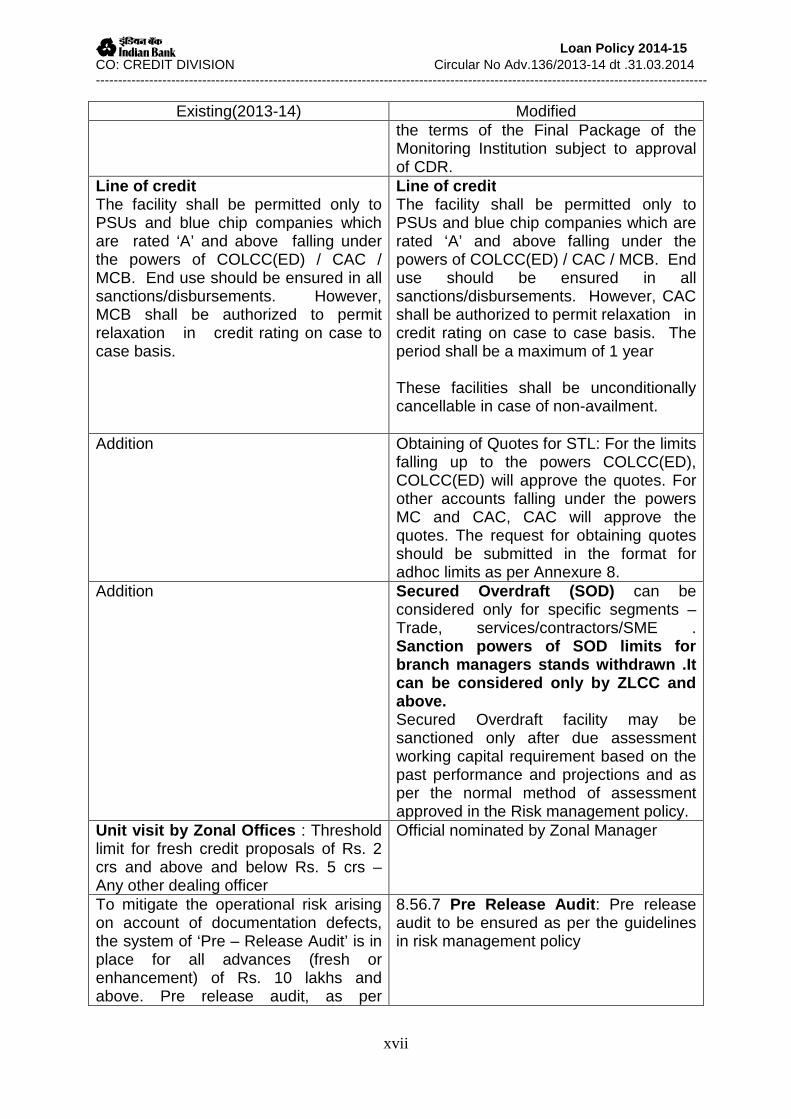

Line of credit The facility shall be permitted only to PSUs and blue chip companies which are rated ‘A’ and above falling under the powers of COLCC(ED) / CAC / MCB. End use should be ensured in all sanctions/disbursements. However, MCB shall be authorized to permit relaxation in credit rating on case to case basis.

Line of credit The facility shall be permitted only to PSUs and blue chip companies which are rated ‘A’ and above falling under the powers of COLCC(ED) / CAC / MCB. End use should be ensured in all sanctions/disbursements. However, CAC shall be authorized to permit relaxation in credit rating on case to case basis. The period shall be a maximum of 1 year These facilities shall be unconditionally cancellable in case of non-availment.

Addition Obtaining of Quotes for STL: For the limits falling up to the powers COLCC(ED), COLCC(ED) will approve the quotes. For other accounts falling under the powers MC and CAC, CAC will approve the quotes. The request for obtaining quotes should be submitted in the format for adhoc limits as per Annexure 8.

Addition Secured Overdraft (SOD) can be considered only for specific segments – Trade, services/contractors/SME . Sanction powers of SOD limits for branch managers stands withdrawn .It can be considered only by ZLCC and above. Secured Overdraft facility may be sanctioned only after due assessment working capital requirement based on the past performance and projections and as per the normal method of assessment approved in the Risk management policy.

Unit visit by Zonal Offices : Threshold limit for fresh credit proposals of Rs. 2 crs and above and below Rs. 5 crs – Any other dealing officer

Official nominated by Zonal Manager

To mitigate the operational risk arising on account of documentation defects, the system of ‘Pre – Release Audit’ is in place for all advances (fresh or enhancement) of Rs. 10 lakhs and above. Pre release audit, as per

8.56.7 Pre Release Audit : Pre release audit to be ensured as per the guidelines in risk management policy

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

xviii

Existing(2013-14) Modified guidelines in force shall be completed before disbursal of the advances. In Corporate Branches/Credit Intensive Branches where the service of a Concurrent Auditor is available, the pre-release audit shall be carried out by the respective Concurrent Auditor. For other Branches, the services of the inspection centre officials/ officer of the same branch conversant with credit portfolio but not working in the credit department /nearby branch loan’s officer/Zonal Office loan’s officer shall be utilized. To improve the credit disbursals by the Branches, the following guidelines are issued. Immediately on receipt of sanction letters and completion of documentation, Zonal Office/Branch has to arrange for pre-release audit on the same day. Pre-release audit exercise should be completed within 24 hours. For PSLP advances of Rs 10 lakhs &above and less than Rs 50 lakhs,the pre release audit may be carried out by officers other than processing officer/s & Sanctioning authority. If the pre-release audit report is an unqualified one, Corporate / Credit Intensive Branch Managers are empowered to release the limits strictly as per the sanction terms and draw down schedule without waiting for permission from the respective Zonal Manager and report it to Zonal Manager. b. Monthly meeting of all CMO’s at the respective Zonal Offices for review of accounts of Rs. 1 crores and above.

- deleted e. All SMA category accounts are to be monitored through Special Mention Account (SMA) system for recovery of overdues. f. Framework for Revitalising Distressed Assets in the Economy – Guidelines on Joint Lenders’ Forum (JLF) and Corrective Action Plan (CAP); Framework for Revitalising Distressed Assets in the Economy - Refinancing of Project Loans and Other Regulatory Measures as per annexure 5 and 6 (RBI circular 97 & 98 dated 26.02.2014 ) are to be followed .Detailed guidelines will be issued CO

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

xix

Existing(2013-14) Modified Credit Monitoring Cell .

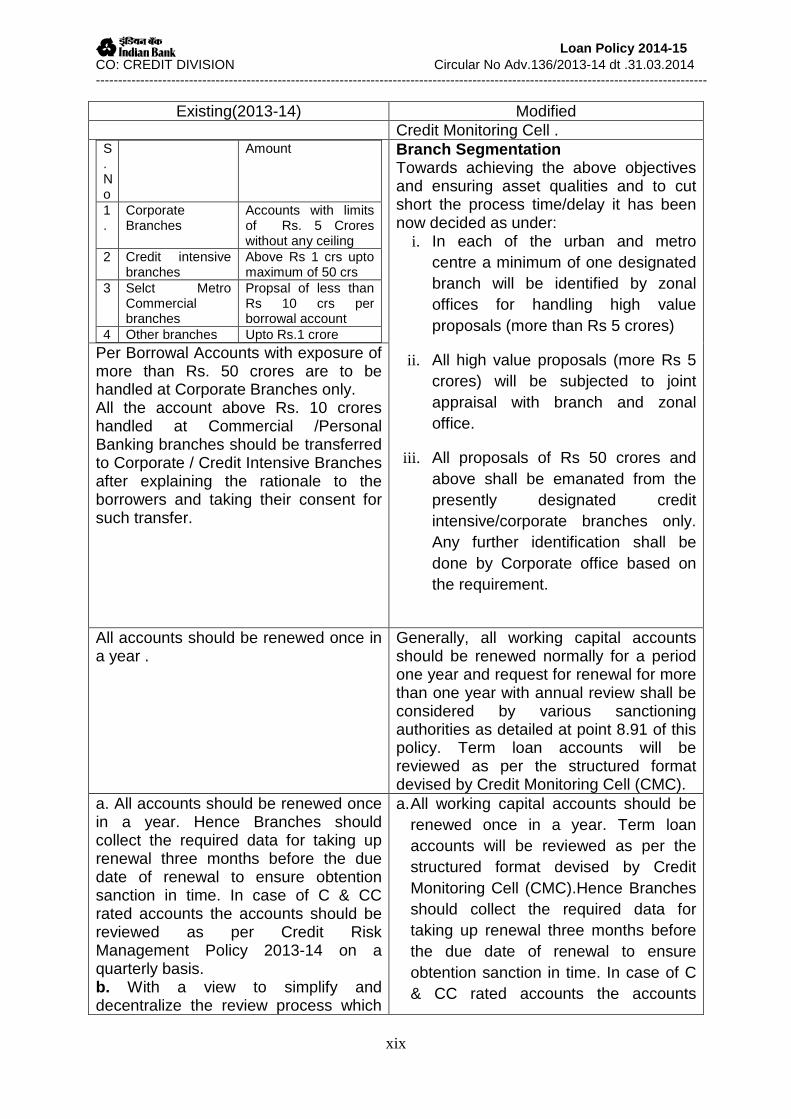

S. No

Amount

1.

Corporate Branches

Accounts with limits of Rs. 5 Crores without any ceiling

2 Credit intensive branches

Above Rs 1 crs upto maximum of 50 crs

3 Selct Metro Commercial branches

Propsal of less than Rs 10 crs per borrowal account

4 Other branches Upto Rs.1 crore

Branch Segmentation Towards achieving the above objectives and ensuring asset qualities and to cut short the process time/delay it has been now decided as under:

i. In each of the urban and metro centre a minimum of one designated branch will be identified by zonal offices for handling high value proposals (more than Rs 5 crores)

ii. All high value proposals (more Rs 5 crores) will be subjected to joint appraisal with branch and zonal office.

iii. All proposals of Rs 50 crores and above shall be emanated from the presently designated credit intensive/corporate branches only. Any further identification shall be done by Corporate office based on the requirement.

Per Borrowal Accounts with exposure of more than Rs. 50 crores are to be handled at Corporate Branches only. All the account above Rs. 10 crores handled at Commercial /Personal Banking branches should be transferred to Corporate / Credit Intensive Branches after explaining the rationale to the borrowers and taking their consent for such transfer.

All accounts should be renewed once in a year .

Generally, all working capital accounts should be renewed normally for a period one year and request for renewal for more than one year with annual review shall be considered by various sanctioning authorities as detailed at point 8.91 of this policy. Term loan accounts will be reviewed as per the structured format devised by Credit Monitoring Cell (CMC).

a. All accounts should be renewed once in a year. Hence Branches should collect the required data for taking up renewal three months before the due date of renewal to ensure obtention sanction in time. In case of C & CC rated accounts the accounts should be reviewed as per Credit Risk Management Policy 2013-14 on a quarterly basis. b. With a view to simplify and decentralize the review process which

a. All working capital accounts should be renewed once in a year. Term loan accounts will be reviewed as per the structured format devised by Credit Monitoring Cell (CMC).Hence Branches should collect the required data for taking up renewal three months before the due date of renewal to ensure obtention sanction in time. In case of C & CC rated accounts the accounts

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

xx

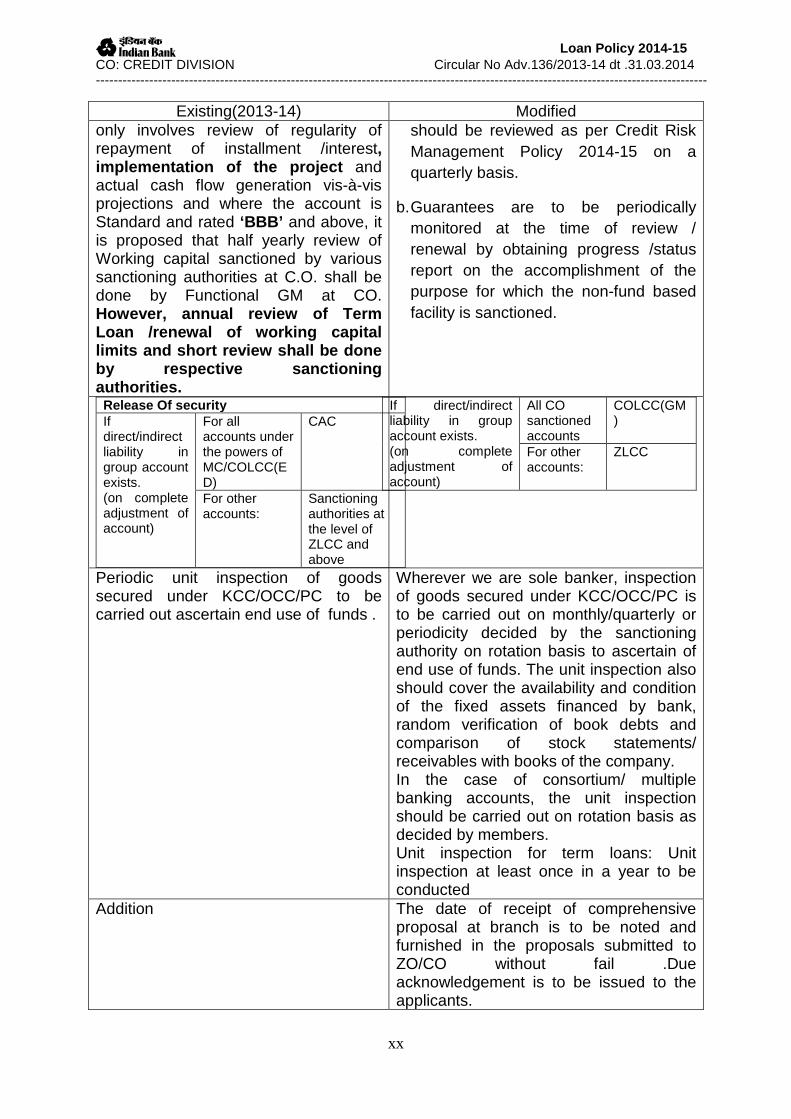

Existing(2013-14) Modified only involves review of regularity of repayment of installment /interest, implementation of the project and actual cash flow generation vis-à-vis projections and where the account is Standard and rated ‘BBB’ and above, it is proposed that half yearly review of Working capital sanctioned by various sanctioning authorities at C.O. shall be done by Functional GM at CO. However, annual review of Term Loan /renewal of working capital limits and short review shall be done by respective sanctioning authorities.

should be reviewed as per Credit Risk Management Policy 2014-15 on a quarterly basis.

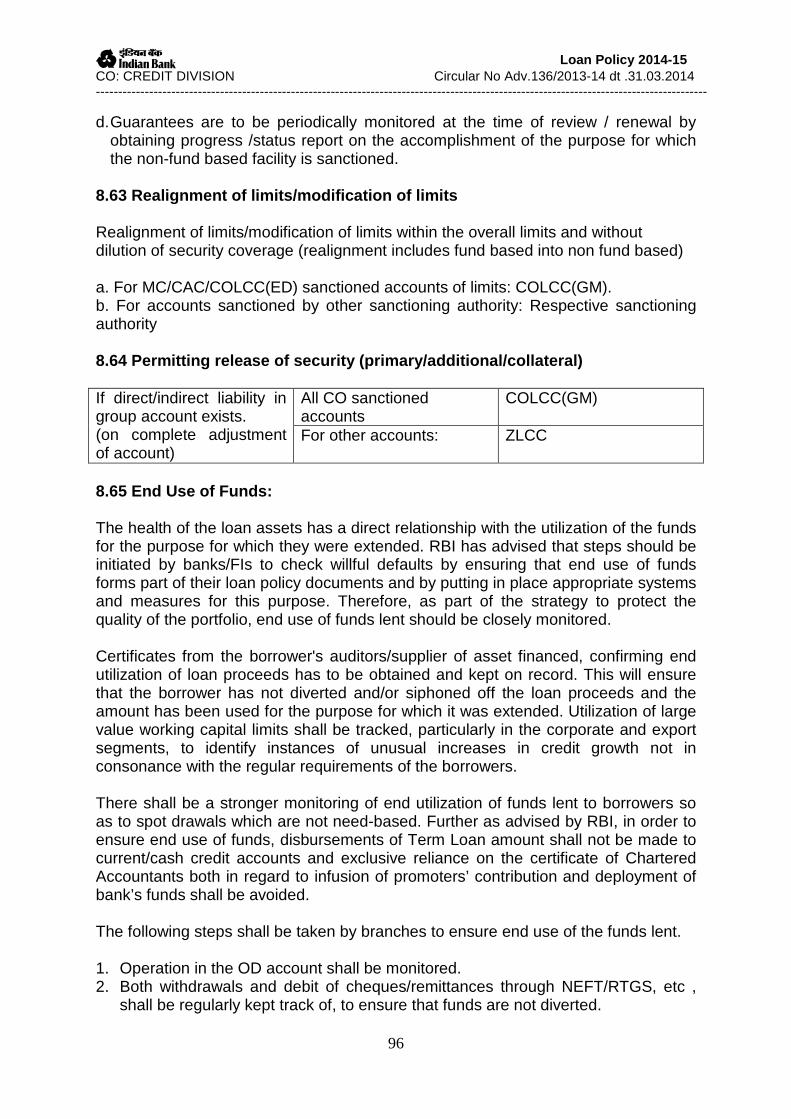

b. Guarantees are to be periodically monitored at the time of review / renewal by obtaining progress /status report on the accomplishment of the purpose for which the non-fund based facility is sanctioned.

Release Of security If direct/indirect liability in group account exists. (on complete adjustment of account)

For all accounts under the powers of MC/COLCC(ED)

CAC

For other accounts:

Sanctioning authorities at the level of ZLCC and above

If direct/indirect liability in group account exists. (on complete adjustment of account)

All CO sanctioned accounts

COLCC(GM)

For other accounts:

ZLCC

Periodic unit inspection of goods secured under KCC/OCC/PC to be carried out ascertain end use of funds .

Wherever we are sole banker, inspection of goods secured under KCC/OCC/PC is to be carried out on monthly/quarterly or periodicity decided by the sanctioning authority on rotation basis to ascertain of end use of funds. The unit inspection also should cover the availability and condition of the fixed assets financed by bank, random verification of book debts and comparison of stock statements/ receivables with books of the company. In the case of consortium/ multiple banking accounts, the unit inspection should be carried out on rotation basis as decided by members. Unit inspection for term loans: Unit inspection at least once in a year to be conducted

Addition The date of receipt of comprehensive proposal at branch is to be noted and furnished in the proposals submitted to ZO/CO without fail .Due acknowledgement is to be issued to the applicants.

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

xxi

Existing(2013-14) Modified

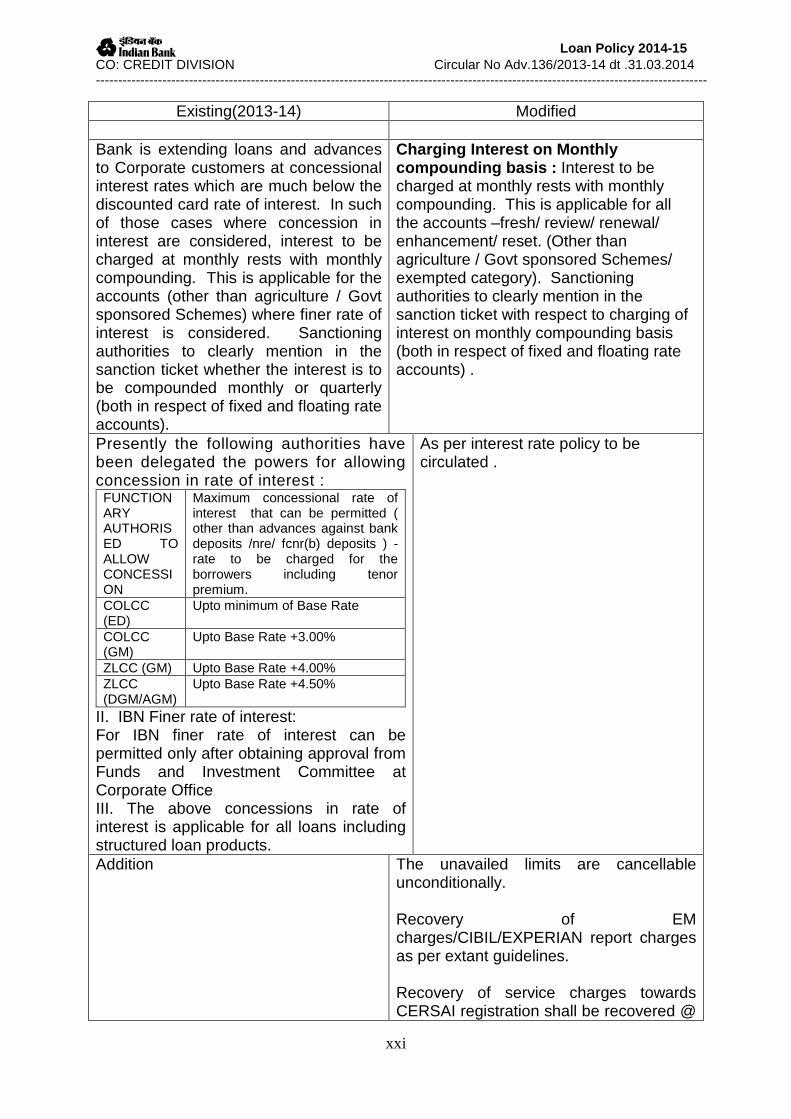

Bank is extending loans and advances to Corporate customers at concessional interest rates which are much below the discounted card rate of interest. In such of those cases where concession in interest are considered, interest to be charged at monthly rests with monthly compounding. This is applicable for the accounts (other than agriculture / Govt sponsored Schemes) where finer rate of interest is considered. Sanctioning authorities to clearly mention in the sanction ticket whether the interest is to be compounded monthly or quarterly (both in respect of fixed and floating rate accounts).

Charging Interest on Monthly compounding basis : Interest to be charged at monthly rests with monthly compounding. This is applicable for all the accounts –fresh/ review/ renewal/ enhancement/ reset. (Other than agriculture / Govt sponsored Schemes/ exempted category). Sanctioning authorities to clearly mention in the sanction ticket with respect to charging of interest on monthly compounding basis (both in respect of fixed and floating rate accounts) .

Presently the following authorities have been delegated the powers for allowing concession in rate of interest :

FUNCTIONARY AUTHORISED TO ALLOW CONCESSION

Maximum concessional rate of interest that can be permitted ( other than advances against bank deposits /nre/ fcnr(b) deposits ) - rate to be charged for the borrowers including tenor premium.

COLCC (ED)

Upto minimum of Base Rate

COLCC (GM)

Upto Base Rate +3.00%

ZLCC (GM) Upto Base Rate +4.00% ZLCC (DGM/AGM)

Upto Base Rate +4.50%

II. IBN Finer rate of interest: For IBN finer rate of interest can be permitted only after obtaining approval from Funds and Investment Committee at Corporate Office III. The above concessions in rate of interest is applicable for all loans including structured loan products.

As per interest rate policy to be circulated .

Addition The unavailed limits are cancellable unconditionally. Recovery of EM charges/CIBIL/EXPERIAN report charges as per extant guidelines. Recovery of service charges towards CERSAI registration shall be recovered @

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

xxii

Existing(2013-14) Modified Rs. 500/-+ applicable Service Tax, shall be recovered per each document / property registered.

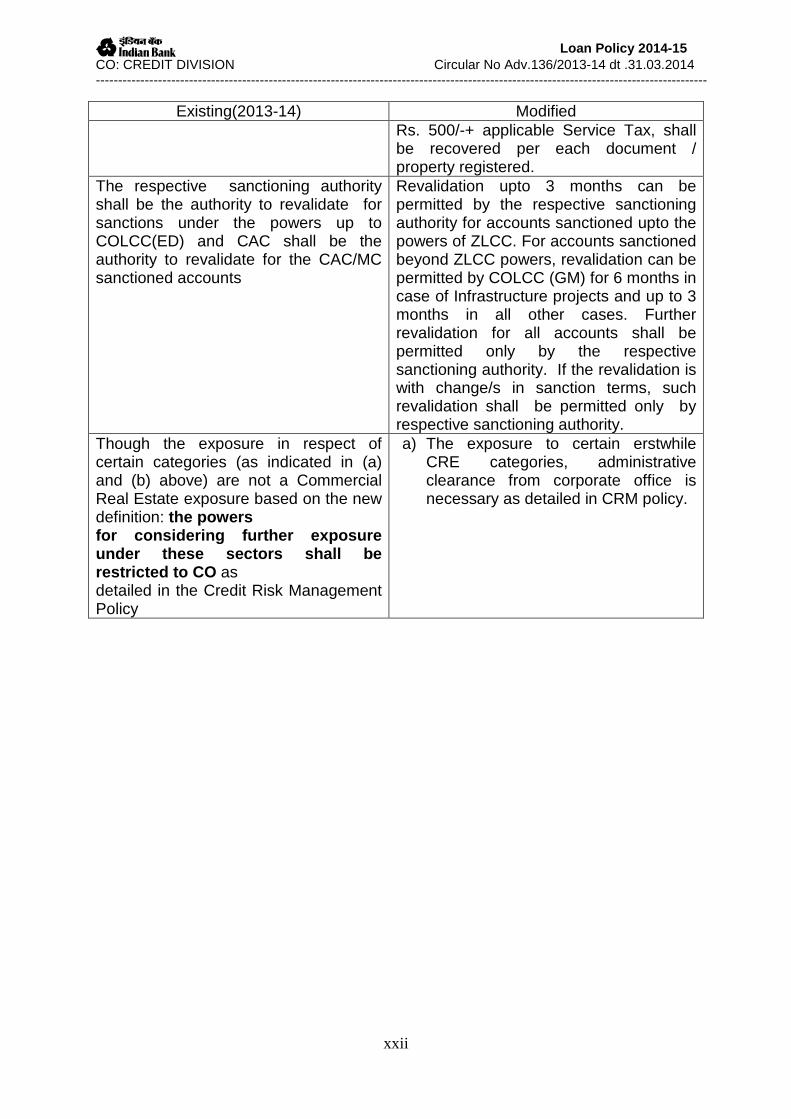

The respective sanctioning authority shall be the authority to revalidate for sanctions under the powers up to COLCC(ED) and CAC shall be the authority to revalidate for the CAC/MC sanctioned accounts

Revalidation upto 3 months can be permitted by the respective sanctioning authority for accounts sanctioned upto the powers of ZLCC. For accounts sanctioned beyond ZLCC powers, revalidation can be permitted by COLCC (GM) for 6 months in case of Infrastructure projects and up to 3 months in all other cases. Further revalidation for all accounts shall be permitted only by the respective sanctioning authority. If the revalidation is with change/s in sanction terms, such revalidation shall be permitted only by respective sanctioning authority.

Though the exposure in respect of certain categories (as indicated in (a) and (b) above) are not a Commercial Real Estate exposure based on the new definition: the powers for considering further exposure under these sectors shall be restricted to CO as detailed in the Credit Risk Management Policy

a) The exposure to certain erstwhile CRE categories, administrative clearance from corporate office is necessary as detailed in CRM policy.

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

1

1. PREAMBLE 1.1 Linkage to Credit Risk Management Policy 2014-15 The Policy document prepared during the current year has linkage with Credit Risk Management Policy 2014-15 in respect of the various standards such as, Standards for collaterals, Exposure limits fixed to various sectors / industries, Rating-wise exposures, Single Borrower and Group Borrower exposures, Substantial exposures. The field level functionaries should use both the Credit Risk Management Policy 2014-15 and Loan Policy document 2014-15 for their day-to-day operations. 1.2 Policy for Micro, Small and Medium Enterprises (MSMEs) As per requirements under Code of Bank’s commitment, Policy for Micro, Small and Medium Enterprises, is separately given as Annexure 1, page No. 113 and the same shall form part of the Bank’s Loan Policy for the year 2014-15. 2. GOVERNMENT GUIDELINES: 2.1 Revised Priority Sector Lending-Targets and Cla ssification-Guidelines RBI vide their circular RBI/2013-14/107.RPCD.CO.plan.BC 9/04.09.01/2013-14 dated July 01, 2013 has communicated the revised guidelines and the same have been given immediate effect. I. Categories under revised priority sector guideli nes are:

I. Agriculture II. Micro and Small Enterprises

III. Education IV. Housing V. Export Credit

VI. Others II. Targets /Sub-targets for Priority sector In terms of RBI guidelines, the targets and sub-targets under priority sector lending would be linked to Adjusted Net Bank Credit (Net Bank Credit plus investments made by banks in non-SLR bonds held in HTM category) or Credit Equivalent amount of Off Balance Sheet Exposures whichever is higher, as on March 31st of the previous year. The targets and sub-targets set under priority sector lending for domestic and foreign banks operating in India are:

Categories Targets /Sub -targets

Total Priority Sector 40 percent of Adjusted Net Bank Credit [ANBC defined in sub paragraph (iii) below] or credit equivalent amount of Off-Balance Sheet Exposure, whichever is higher.

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

2

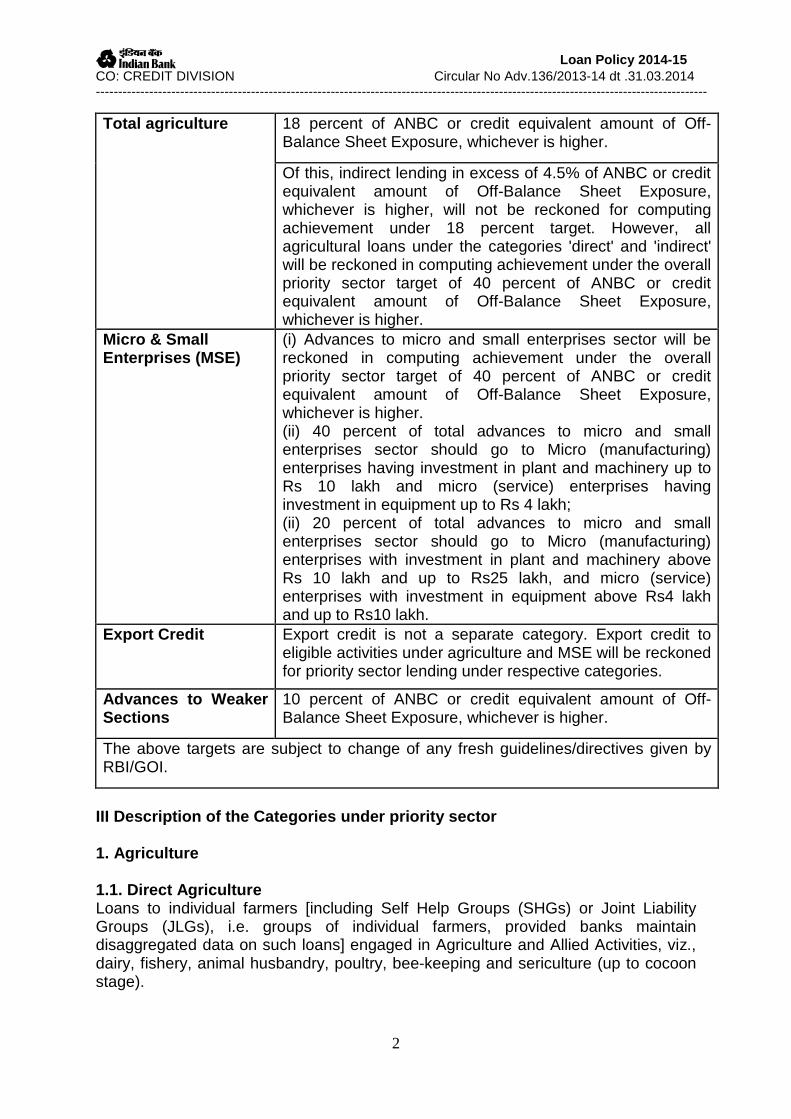

Total agriculture 18 percent of ANBC or credit equivalent amount of Off-Balance Sheet Exposure, whichever is higher.

Of this, indirect lending in excess of 4.5% of ANBC or credit equivalent amount of Off-Balance Sheet Exposure, whichever is higher, will not be reckoned for computing achievement under 18 percent target. However, all agricultural loans under the categories 'direct' and 'indirect' will be reckoned in computing achievement under the overall priority sector target of 40 percent of ANBC or credit equivalent amount of Off-Balance Sheet Exposure, whichever is higher.

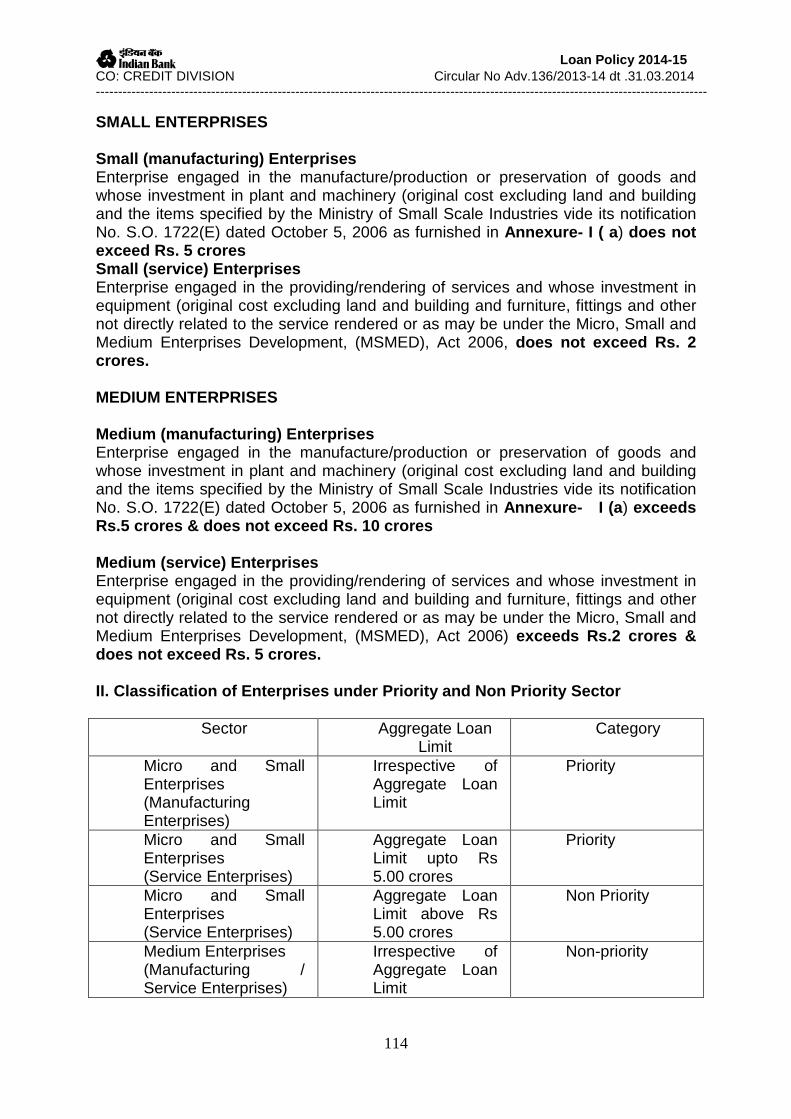

Micro & Small Enterprises (MSE)

(i) Advances to micro and small enterprises sector will be reckoned in computing achievement under the overall priority sector target of 40 percent of ANBC or credit equivalent amount of Off-Balance Sheet Exposure, whichever is higher. (ii) 40 percent of total advances to micro and small enterprises sector should go to Micro (manufacturing) enterprises having investment in plant and machinery up to Rs 10 lakh and micro (service) enterprises having investment in equipment up to Rs 4 lakh; (ii) 20 percent of total advances to micro and small enterprises sector should go to Micro (manufacturing) enterprises with investment in plant and machinery above Rs 10 lakh and up to Rs25 lakh, and micro (service) enterprises with investment in equipment above Rs4 lakh and up to Rs10 lakh.

Export Credit Export credit is not a separate category. Export credit to eligible activities under agriculture and MSE will be reckoned for priority sector lending under respective categories.

Advances to Weaker Sections

10 percent of ANBC or credit equivalent amount of Off-Balance Sheet Exposure, whichever is higher.

The above targets are subject to change of any fresh guidelines/directives given by RBI/GOI.

III Description of the Categories under priority se ctor 1. Agriculture 1.1. Direct Agriculture Loans to individual farmers [including Self Help Groups (SHGs) or Joint Liability Groups (JLGs), i.e. groups of individual farmers, provided banks maintain disaggregated data on such loans] engaged in Agriculture and Allied Activities, viz., dairy, fishery, animal husbandry, poultry, bee-keeping and sericulture (up to cocoon stage).

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

3

I. Short-term loans to farmers for raising crops, i.e. for crop loans. (This will include traditional/non-traditional plantations, horticulture and allied activities)

II. Medium & long-term loans to farmers for agriculture and allied activities (e.g. purchase of agricultural implements and machinery, loans for irrigation and other developmental activities undertaken in the farm, and development loans for allied activities).

III. Loans to farmers for pre-harvest and post-harvest activities, viz., spraying, weeding, harvesting, sorting, grading and transporting of their own farm produce.

IV. Loans to farmers up to Rs.50 lakh against pledge/hypothecation of agricultural produce (including warehouse receipts) for a period not exceeding 12 months, irrespective of whether the farmers were given crop loans for raising the produce or not.

V. Loans to small and marginal farmers for purchase of land for agricultural purposes.

VI. Loans to distressed farmers indebted to non-institutional lenders. VII. Bank loans to Primary Agricultural Credit Societies (PACS), Farmers’ Service

Societies (FSS) and Large-sized Adivasi Multi Purpose Societies (LAMPS) ceded to or managed/ controlled by such banks for on lending to farmers for agricultural and allied activities.

VIII. Loans to farmers under Kisan Credit Card Scheme. IX. Export credit to farmers for exporting their own farm produce.

Bank loans to following entities would also qualify for lending to Direct agriculture:- Loans to corporate, including farmers, producer companies of individual farmers, partnership firms and co-operatives of farmers directly engaged in Agriculture and Allied Activities, viz., dairy, fishery, animal husbandry, poultry, bee-keeping and sericulture (up to cocoon stage) up to an aggregate limit of Rs.2 crore per borrower for the following purposes. (i) Short-term loans for raising crops, i.e. for crop loans.

(This will include traditional/non-traditional plantations, horticulture and allied activities)

(ii) Medium & long-term loans for agriculture and allied activities (e.g. purchase of agricultural implements and machinery, loans for irrigation and other developmental activities undertaken in the farm, and development loans for allied activities).

(iii) Loans for pre-harvest and post-harvest activities, viz., spraying, weeding, harvesting, grading and sorting.

(iv) Export credit for exporting their own farm produce. 1.2. Indirect agriculture 1.2.1. Loans to corporate, partnership firms and in stitutions engaged in Agriculture and Allied Activities [dairy, fishery, animal husbandry, poultry, bee-keeping and sericulture (up to cocoon stage)]

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

4

(i) Short-term loans for raising crops, i.e. for crop loans (more than Rs 2 crores).This will include traditional/non-traditional plantations, horticulture and allied activities.

(ii) Medium & long-term loans for agriculture and allied activities (e.g. purchase of agricultural implements and machinery, loans for irrigation and other developmental activities undertaken in the farm, and development loans for allied activities) [ more than Rs 2 crores].

(iii) Loans for pre –harvest and post-harvest activities such as spraying , weeding, harvesting, grading and sorting (more than Rs.2.crs)

(iv) Loans up to Rs 50 lakh against pledge / hypothecation of agricultural produce (including warehouse receipts) for a period not exceeding 12 months, irrespective of whether the farmers were given crop loans for raising the produce or not.

(v) Export credit to corporate, partnership firms and institutions for exporting their own farm produce ( more than Rs 2 crores)

(vi) Loans upto Rs 5 crore to Producer Companies set up exclusively by only small and marginal farmers under Part IXA of Companies Act, 1956 for agricultural and allied activities.

(vii)Bank loans to Primary Agricultural Credit Societies (PACS), Farmers’ Service Societies (FSS) and Large-sized Adivasi Multi Purpose Societies (LAMPS) other than those covered under paragraph III (1.1) (vii) of this circular.

1.2.2. Other indirect agriculture loans

i. Loans up to 5 crore per borrower to dealers /sellers of fertilizers, pesticides, seeds, cattle feed, poultry feed, agricultural implements and other inputs.

ii. Loans for setting up of Agriclinics and Agribusiness Centres iii. Loans up to 5 crore to cooperative societies of farmers for disposing of the

produce of members. iv. Loans to Custom Service Units managed by individuals, institutions or

organizations who maintain a fleet of tractors, bulldozers, well-boring equipment, threshers, combines, etc., and undertake farm work for farmers on contract basis.

v. Loans for construction and running of storage facilities (warehouse, market yards, godowns and silos), including cold storage units designed to store agriculture produce/products, irrespective of their location. If the storage unit is a micro or small enterprise, such loans will be classified under loans to Micro and Small Enterprises sector

vi. Loans to MFIs for on-lending to farmers for agricultural and allied activities as per the conditions specified in the RBI Master Circular.

vii. Loans sanctioned to NGOs, which are SHG Promoting Institutions, for on-lending to members of SHGs under SHG-Bank Linkage Programme for agricultural and allied activities. The all inclusive interest charged by the NGO/SHG promoting entity should not exceed the Base Rate of the lending bank plus eight percent per annum

viii. Loans sanctioned to RRBs for on-lending to agriculture and allied activities

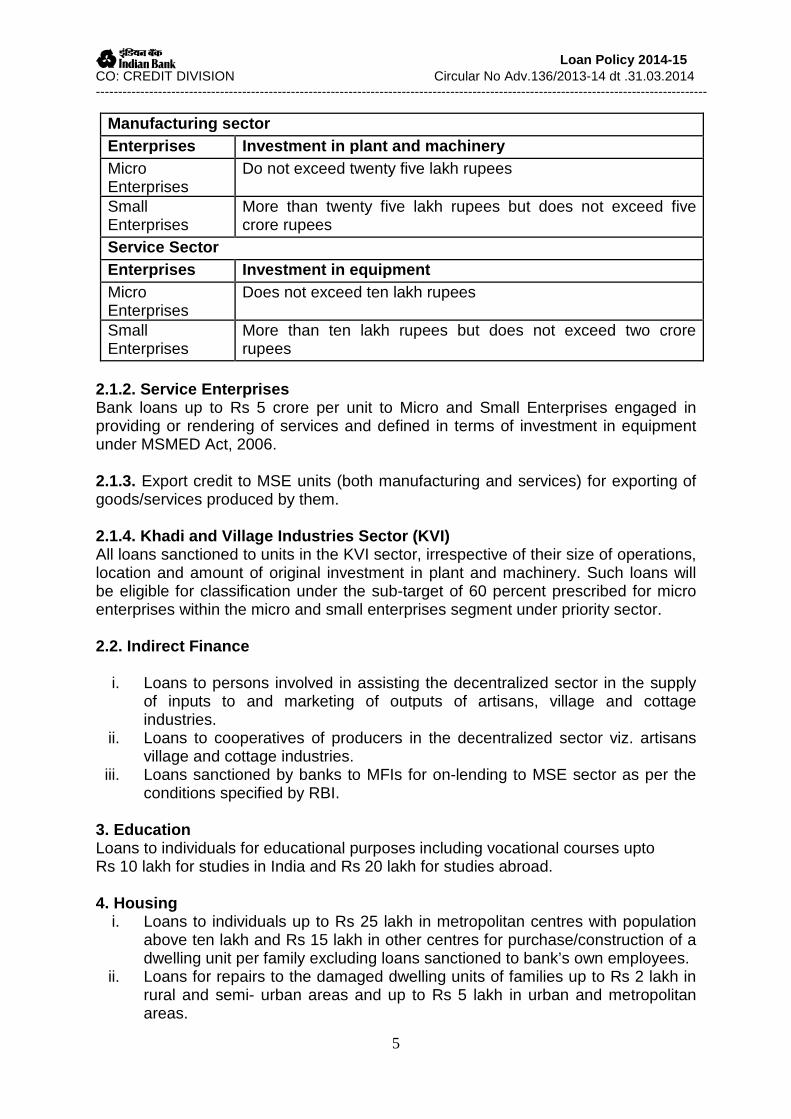

2. Micro and small enterprises 2.1.1 The limits for investment in plant and machinery/equipment for manufacturing / service enterprise, as notified by Ministry of Micro Small and Medium Enterprises, vide, S.O.1642(E) dated September 29, 2006 are as follows:-

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

5

Manufacturing sector Enterprises Investment in plant and machinery Micro Enterprises

Do not exceed twenty five lakh rupees

Small Enterprises

More than twenty five lakh rupees but does not exceed five crore rupees

Service Sector Enterprises Investment in equipment Micro Enterprises

Does not exceed ten lakh rupees

Small Enterprises

More than ten lakh rupees but does not exceed two crore rupees

2.1.2. Service Enterprises Bank loans up to Rs 5 crore per unit to Micro and Small Enterprises engaged in providing or rendering of services and defined in terms of investment in equipment under MSMED Act, 2006. 2.1.3. Export credit to MSE units (both manufacturing and services) for exporting of goods/services produced by them. 2.1.4. Khadi and Village Industries Sector (KVI) All loans sanctioned to units in the KVI sector, irrespective of their size of operations, location and amount of original investment in plant and machinery. Such loans will be eligible for classification under the sub-target of 60 percent prescribed for micro enterprises within the micro and small enterprises segment under priority sector. 2.2. Indirect Finance

i. Loans to persons involved in assisting the decentralized sector in the supply of inputs to and marketing of outputs of artisans, village and cottage industries.

ii. Loans to cooperatives of producers in the decentralized sector viz. artisans village and cottage industries.

iii. Loans sanctioned by banks to MFIs for on-lending to MSE sector as per the conditions specified by RBI.

3. Education Loans to individuals for educational purposes including vocational courses upto Rs 10 lakh for studies in India and Rs 20 lakh for studies abroad. 4. Housing

i. Loans to individuals up to Rs 25 lakh in metropolitan centres with population above ten lakh and Rs 15 lakh in other centres for purchase/construction of a dwelling unit per family excluding loans sanctioned to bank’s own employees.

ii. Loans for repairs to the damaged dwelling units of families up to Rs 2 lakh in rural and semi- urban areas and up to Rs 5 lakh in urban and metropolitan areas.

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

6

iii. Bank loans to any governmental agency for construction of dwelling units or for slum clearance and rehabilitation of slum dwellers subject to a ceiling of Rs 10 lakh per dwelling unit. The loans sanctioned by banks for housing projects exclusively for the purpose of construction of houses only to economically weaker sections and low income groups, the total cost of which do not exceed Rs 10 lakh per dwelling unit. For the purpose of identifying the economically weaker sections and low income groups, the family income limit of Rs 1, 20,000 per annum, irrespective of the location, is prescribed.

iv. Bank loans to Housing Finance Companies (HFCs), approved by NHB for their refinance, for on-lending for the purpose of purchase/construction/reconstruction of individual dwelling units or for slum clearance and rehabilitation of slum dwellers, subject to an aggregate loan limit of Rs.10 lakh per borrower, provided the all inclusive interest rate charged to the ultimate borrower is not exceeding lowest lending rate of the lending bank for housing loans plus two percent per annum.

5. Export Credit Export Credit extended by foreign banks with less than 20 branches will be reckoned for priority sector target achievement. As regards the domestic banks and foreign banks with 20 and above branches, export credit is not a separate category under priority sector. Export credit mentioned under paragraphs (III) (1.1) (ix), (III) (1.2.1) (v) and (III) (2.1.3) of this circular will count towards the respective categories of priority sector, i.e. Agriculture and MSE sector. 6. Others a. Loans, not exceeding Rs 50,000/- per borrower provided directly by banks to individuals and their SHG/JLG, provided the borrower’s household annual income in rural areas does not exceed Rs 60,000/- and for non-rural areas it should not exceed Rs 1,20,000/-. b. Loans to distressed persons [other than farmers-already included under III (1.1) (vi)] not exceeding Rs 50,000/- per borrower to prepay their debt to non-institutional lenders. c. Loans outstanding under loans for general purposes under General Credit Cards (GCC). If the loans under GCC are sanctioned to Micro and Small Enterprises, such loans should be classified under respective categories of Micro and Small Enterprises. d. Overdrafts, up to Rs 50,000/- (per account), granted against 'no-frills' / basic banking / savings accounts provided the borrowers household annual income in rural areas does not exceed Rs 60,000/- and for non-rural areas it should not exceed Rs 1,20,000/-. e. Loans sanctioned to State Sponsored Organisations for Scheduled Castes/ Scheduled Tribes for the specific purpose of purchase and supply of inputs to and/or the marketing of the outputs of the beneficiaries of these organisations. f. Loans sanctioned by banks directly to individuals for setting up off-grid solar and other off-grid renewable energy solutions for households.

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

7

IV Weaker Sections Priority sector loans to the following borrowers will be considered under Weaker Sections category:- (a) Small and marginal farmers; (b) Artisans, village and cottage industries where individual credit limits do not exceed Rs 50,000/-; (c) Beneficiaries of Swarnjayanti Gram Swarozgar Yojana (SGSY), now National Rural Livelihood Mission (NRLM); (d) Scheduled Castes and Scheduled Tribes; (e) Beneficiaries of Differential Rate of Interest (DRI) scheme; (f) Beneficiaries under Swarna Jayanti Shahari Rozgar Yojana (SJSRY); (g) Beneficiaries under the Scheme for Rehabilitation of Manual Scavengers (SRMS); (h) Loans to Self Help Groups; (i) Loans to distressed farmers indebted to non-institutional lenders; (j) Loans to distressed persons other than farmers not exceeding Rs 50,000 per borrower to prepay their debt to non-institutional lenders; (k) Loans to individual women beneficiaries upto Rs 50,000 per borrower; (l) Loans sanctioned under (a) to (k) above to persons from minority communities as may be notified by Government of India from time to time.

2.2 NON PRIORITY SECTOR: All other credit not covered under priority Sector including Medium Enterprises are considered as Non Priority Sector. 3 GROWTH PROJECTIONS: Credit Growth budget for 2014-15

Sector-wise credit targets are being finalised by Corporate Office (CO)/Department of Planning and Economic Research and will be placed to the Board for approval. On approval, the detailed segment-wise credit targets will become part of this Loan Policy for implementation during 2014-15. 4 TARGETED SECTORS FOR CREDIT GROWTH: 4.1 Thrust areas - Agriculture Credit:

a. Bank shall continue to provide thrust to improve lending to Revised KCC and Term loans for various agricultural and allied agricultural activities to increase clientele and volume of business.

b. Thrust shall be given for financing vulnerable farmers viz. Small and Marginal Farmers, Tenant Farmers, Share Croppers, Oral Lessees either directly or through Joint Liability Groups.

c. 2.5% of loan amount disbursed to new farmers shall be directed towards tenant farmers/share croppers/oral lessees.

d. Fresh/new farmers numbering at least 250 on an average per rural/semi urban Branch on incremental basis (excluding jewel loan) shall be covered.

e. Agricultural jewel loans for other than crop production purposes may also be encouraged.

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

8

f. Intensive financing shall be taken up for crop cultivation and investment purposes in areas where watershed development work is taken up by the State Governments concerned.

g. Thrust shall be given by the branches for Investment Credit ( Term Loans) under agriculture

h. Financing Agricultural export zones, food / Agricultural Park, units for export of dehydrated vegetables, organically grown food shall be given thrust.

i. Financing for setting up of water saving devices like DRIP, Sprinkler etc and Precision farming shall be encouraged and

j. Contract farming: Financial intermediation shall be encouraged in the field of contract farming for up scaling the outreach.

k. Intermediation by reputed Corporate Service providers of agriculture inputs/ technology shall be encouraged for enhancing volume. Loans under tie up arrangement (contract farming) with companies for cultivation of Bio-fuel plants, cultivation of medicinal plants, gherkins, oilseeds, horticultural crops etc., shall be given continued thrust.

l. Farm mechanization credit including credit for second hand tractors to be given for certified tractors which comply with Minimum Performance Standard norms shall be a thrust area. (certified by Central Farm Machinery Training and Testing Institute).

m. Financing Rural Godown /Cold Storages/Warehouses involving construction, expansion, modification or modernization or rehabilitation shall be encouraged.

n. Advances to input dealers in fertilizer, seed, farm machinery etc., shall be encouraged.

o. As per revised Priority Sector guidelines, advances to Food & Agro Based Processing Units comes under MSE sector

p. Agri. Clinics /Agri. Business centre scheme shall be marketed aggressively. q. Area Specific Potentials under agricultural sector shall be identified by the

Zones and special products shall be developed to garner the maximum potential. Focus branches for such special products shall be identified and necessary support including training shall be provided.

4.2 Retail Credit: As economy is getting stabilized globally and more particularly in our country, there is good scope for growth in retail credit. Our interest rates are competitive in the industry. There is good scope for increasing the credit under this sector despite market competition, customers’ preference and competitive pricing offered by the other bankers. For credit limit upto Rs 200 Lakhs (Priority sector), we have realigned interest rate, on competitive terms 4.3 Micro, Small and Medium Enterprises (MSMEs):

MSMEs are the most important economic proposition as it promotes growth with

equity and has potential for growth.As per the policy package pronounced by the Government of India for stepping up credit to MSME sector, a minimum of 20% year-

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

9

on-year growth is envisaged in credit to MSEs. Our Bank will continue to focus advancing to MSMEs. Within the MSME growth, the thrust area would be lending to viable units to Micro Enterprises to achieve 60% target prescribed by RBI. 4.4. Government Sponsored Schemes: Physical & financial targets allocated under various Government Sponsored Schemes like Swarna Jayanthi Gram Swarojgar Yojana (SGSY) now restructured as National Rural Livelihoods Mission (NRLM), Swarna Jayanthi Sahari Rojgar Yojana (SJSRY), Prime Minister’s Employment Generation Programme (PMEGP) should be achieved within stipulated time frame. While implementing, commitments under various sub targets (SC/ST, Women, minorities, physically handicapped) should also be accomplished All eligible accounts should be linked to subsidy processing in order to ensure that interest is not charged for the subsidy component. 4.5 DRI: Branches shall take advantage of increased quantum of loan amount (Rs.20,000/- for housing and Rs.15000/- for others), increased income ceiling for eligibility (Rs 18000/- p.a. for rural areas and Rs.24000/-p.a for urban areas) and eligibility under Indira Awaas Yojana (IAY) Housing Loan Scheme(beneficiaries are eligible for top up loan of up to Rs.20000/- which can be considered under DRI scheme subject to the borrower fulfilling DRI norms) 4.6 Minorities welfare : The Prime Minister’s new-15 Point program for the “Welfare of Minorities” envisages inter-alia encouraging credit flow to the minority communities. The GOI has decided to step up the lending to minorities to 15% of total priority sector advances by 2010-11 and the same should be continued subject to continuation of the scheme. Branches should sensitize minority communities on credit facilities available from our bank through appropriate media and ensure increased flow of credit to Minority communities. 4.7 Flow of Credit to SCs/STs : Special emphasis has to be given by the Branches to ensure adequate credit flow to SC/STs in all bankable schemes. If any application in respect of SCs/STs are to be rejected, it should be done by the controlling authority. 5. SELECTIVE FINANCING For Selective Financing please refer to Credit Risk Management Policy 2014-15

A Loan Policy 2014-15 CO: CREDIT DIVISION Circular No Adv.136/2013-14 dt .31.03.2014 ------------------------------------------------------------------------------------------------------------------------------------------

10

6. STRATEGIES FOR ENHANCING CREDIT FLOW 6.1 Agriculture Credit Priority Sector Lending: RBI has stipulated that advances to Priority Sector should form 40% of Adjusted Net Bank Credit of previous year. Accordingly, Priority Sector lending will be one of the focus areas for credit expansion. All branches located in rural/ semi-urban areas shall make all-out efforts to increase Priority Sector lending and achieve the stipulated level. Similarly, branches should focus attention on financing Self Help Groups, directly or by taking the assistance of NGOs, Block Development Offices, Municipalities and Corporations. 6.1.1 Zones shall conduct series of campaigns in cluster of Branches in such a way that a rural/semi - urban/urban branch conducts campaign based on seasonality/ local conditions/ festivals, to step up agriculture credit. 6.1.2. Branches not extending jewel loan shall introduce jewel loan facility immediately. Jewel loan is a preferred form of credit by the farming community and shall continue to be marketed aggressively. All Jewel Loan products like Agri Jewel loan, Agri Term Loan against Gold Ornaments, Jewel Loan (Non Agri), Jewel loan for Traders scheme, Jewel loan (Non Priority) and Jewel loan to Senior Citizens shall be aggressively marketed by the branches. 6.1.3: Interest subvention for crop loans at the applicable rate shall be implemented as per periodic guidelines of GOI/RBI in this regard. (Present rates are 2% interest subvention + 3% ince ntive subvention for prompt repayment). Benefits of interest subvention will be available to small and marginal farmers having Kisan Credit Card (KCC) for a further period of upto six months post harvest on the same rate as available to crop loan against negotiable warehouse receipt for keeping their produce in warehouses. Branches are, therefore, advised to ensure that all crop loans against which they are claiming interest subvention should satisfy, inter alia, the following criteria: