subscribed 2015: the new revenue standard: how saas are approaching the new revenue standard

TRANSCRIPT

New Revenue Standard:How SaaS companies are approaching the new revenue standard

May 2015

Agenda

Overview of the Standard

Changes and Transition

What’s Happening Today

Case Studies

Planning for Adoption

Wrap Up

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ('KPMG International'), a Swiss entity. All rights reserved.

Executive Overview of the Standard

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ('KPMG International'), a Swiss entity. All rights reserved.

■ Industry-specific software guidance is eliminated and replaced with a single accounting model for revenue recognition.

■ Significant judgments and estimates are required in many circumstances, especially around determining the transaction price and accounting for software licenses.

■ New business requirements to comply with the accounting policies will require changes to our accounting systems and expand our capture to include new source information.

■ The FASB and IASB has proposed delaying the effective date by 1 year and therefore we expect the new standard will become effective in calendar 2018.

■ There is a cumulative effect or retrospective transition method for adopting the standard which will require parallel processing of revenue for a period of time.

201820162013 2014 20172015

January 1st

Retrospective transition application date

January 1st

Effective date

May 28, 2014

Final standard

January 1st

Proposed Effective date

Timeline effective dates shown are for public entities with December 31 year ends. Nonpublic entities have a one year deferral in effective date.

Remove inconsistencies and weaknesses in existing requirements to improve comparability

Provide a more robust framework for addressing revenue issues

Provide more useful information through improved disclosure requirements

Simplify the preparation of financial statements by having one revenue framework

IASB/FASB Converged Standard

Objectives of the New Revenue Standard

… Broadly Impacting the Organization

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ('KPMG International'), a Swiss entity. All rights reserved.

New Revenue Recognition Standards & Corresponding Accounting Changes

■ Impact of new revenue recognition standard and mapping to new accounting rules

■ New accounting policies – historical results and transition

■ Reporting differences and disclosures

■ Tax reporting/planning

Revenue Recognition Automation and ERP Upgrades

■ Automation and customization of ERP environment

■ Impact on ERP systems

■ General ledger, sub-ledgers and reporting packages

■ Peripheral revenue systems and interfaces

Financial and Operational Process Changes

■ Revenue process allocation and management

■ Budget and management reporting

■ Communication with financial markets

■ Covenant compliance

■ Opportunity to rethink business practices

■ Coordination with other strategic initiatives

Governance and Change

■ Governance organization and changes

■ Impact on internal resources

■ Project management

■ Training (accounting, sales, etc.)

■ Revenue change management team

■ Multi-national locations

Revenue Recognition

Five Steps of the Model

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ('KPMG International'), a Swiss entity. All rights reserved.

Identify the contract(s) with

a customer

1

Identify the separate

performance obligations in the contract

2

Determinethe transaction

price

3

Allocate the transaction price to the

separate performance obligations

4

Recognize revenue

when (or as)the entity satisfies a

performance obligation

5

Agenda

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ('KPMG International'), a Swiss entity. All rights reserved.

Overview of the Standard

Changes and Transition

What’s Happening Today

Case Studies

Planning for Adoption

Wrap Up

Agenda

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ('KPMG International'), a Swiss entity. All rights reserved.

100+ sources for revenue guidance

Fees must be fixed or determinable

Must have “persuasive evidence” of arrangement

No recognition of contingent revenue

Unit of account based on “standalone value”

No rules on accounting for modifications

Capitalizing contract acquisition costs optional

Software industry held to higher standard (“VSOE”)

IP license recognized upfront or ratable based on practice

Revenue disclosures limited to policy discussion

Existing Standards New Standards

1 standard for all arrangements, all industries

Must have “legally binding” arrangement

Fees are estimated if sufficient history exists

No similar prohibition; subject to estimation

Unit of account based on “distinct”

Modification rules can result in complicated accounting

Software guidance eliminated

IP license subject to specific rules on how to recognize

Capitalizing contract acquisition costs required

Extensive disclosures required

Expected pervasive impact to Cloud Service Providers companies

Big 4 Guidance and Vendor Input

Is Revenue Automation right for you?

© 2015 Leeyo Software, Inc. CONFIDENTIAL AND PROPRIETARY - FOR INTERNAL USE ONLY - ALL RIGHTS RESERVED

Assessment Use Cases Address Data Gaps

Identify Process Changes

Evaluate Vendors Selection

What are the most important items to consider in a solution?Ability to handle both current and new revenue recognition guidanceRobust reporting capabilitiesAbility to grow and scale with your companyAbility to accept data from any sourceERP agnosticAbility to be a seamless add-on to existing system

The new revenue recognition guidance has every corporation examining their revenue processing.

What makes a good candidate for revenue automation?

• Multiple revenue streams• Multiple transaction sources• Complex revenue recognition policies• A high volume of transactions• Products representing a bundle of goods & services• Contract modifications

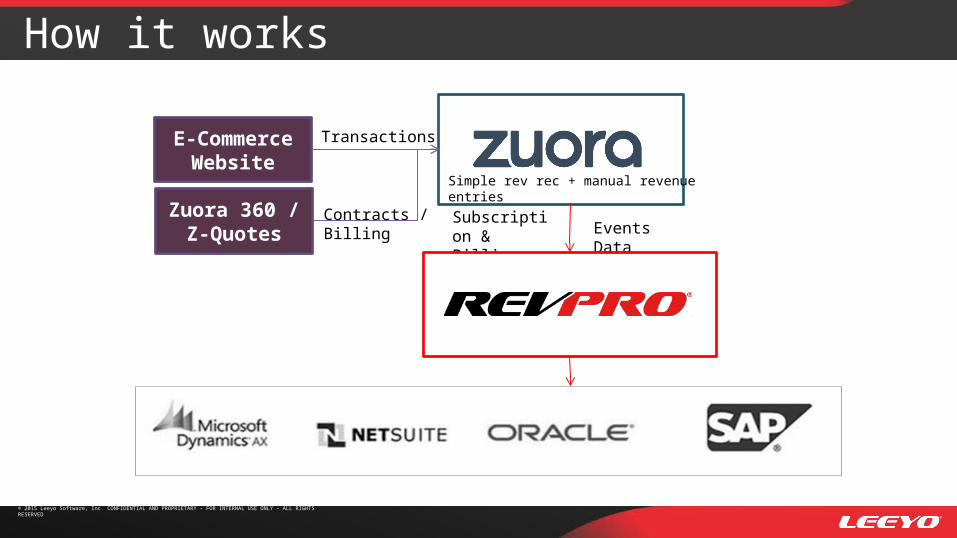

How it works

© 2015 Leeyo Software, Inc. CONFIDENTIAL AND PROPRIETARY - FOR INTERNAL USE ONLY - ALL RIGHTS RESERVED

E-Commerce Website

Zuora 360 / Z-Quotes

Transactions

Contracts / Billing

Manual Journal Entry

Simple rev rec + manual revenue entries

How it works

© 2015 Leeyo Software, Inc. CONFIDENTIAL AND PROPRIETARY - FOR INTERNAL USE ONLY - ALL RIGHTS RESERVED

E-Commerce Website

Zuora 360 / Z-Quotes

Transactions

Contracts / Billing

Simple rev rec + manual revenue entries

Subscription & Billing Data Events Data

How it works

To General Ledger

Revenue Policies / Setup

Revenue Contract Grouping

POB AssignmentTransaction Price Adjustments

Variable Consideration

SSP Assignment

Allocation

Subscription & Billing Data

Events Data

Accounting Entries Created

Revenue Recognition

SSP Calculation

Cost Applied Cost Estimates/Actuals

Reve

nue

Cont

ract

W

orkb

ench

Reporting & Forecasting© 2015 Leeyo Software, Inc. CONFIDENTIAL AND PROPRIETARY - FOR INTERNAL USE ONLY - ALL RIGHTS RESERVED

Agenda

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ('KPMG International'), a Swiss entity. All rights reserved.

Overview of the Standard

Changes and Transitions

Case Studies

Planning for Adoption

Wrap Up

What’s Happening Today

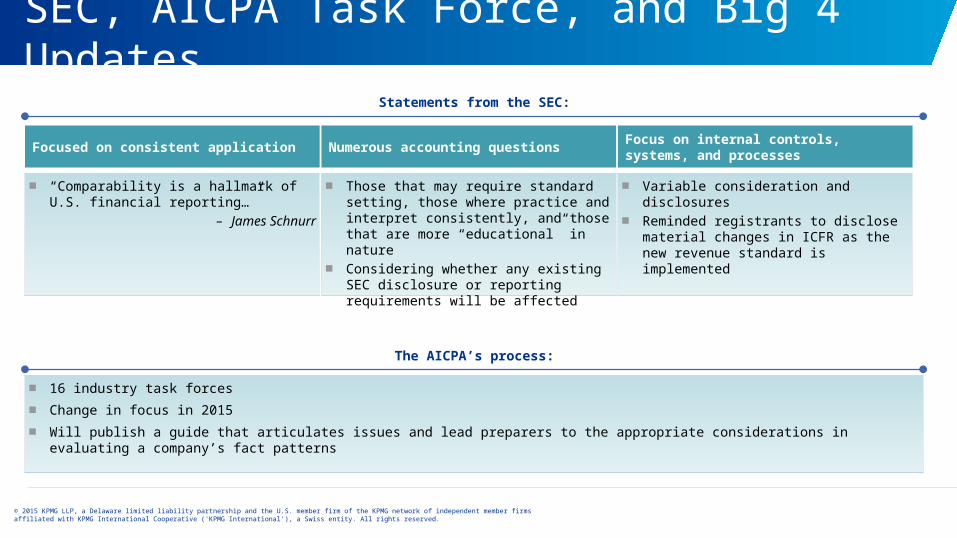

SEC, AICPA Task Force, and Big 4 Updates

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ('KPMG International'), a Swiss entity. All rights reserved.

Statements from the SEC:

■ “Comparability is a hallmark of U.S. financial reporting…”

– James Schnurr

Focused on consistent application

■ Those that may require standard setting, those where practice and interpret consistently, and those that are more “educational” in nature

■ Considering whether any existing SEC disclosure or reporting requirements will be affected

Numerous accounting questions

■ Variable consideration and disclosures■ Reminded registrants to disclose material

changes in ICFR as the new revenue standard is implemented

Focus on internal controls, systems, and processes

The AICPA’s process:

■ 16 industry task forces

■ Change in focus in 2015

■ Will publish a guide that articulates issues and lead preparers to the appropriate considerations in evaluating a company’s fact patterns

Deferral of effective date and transition considerations

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ('KPMG International'), a Swiss entity. All rights reserved.

■ FASB proposed a deferral of Effective Date (comment letter period end May 29, 2015)

■ Proposed Effective Date would be January 1, 2018

■ In addition to 1-year deferral FASB requested comments on whether 2-year deferral would be appropriate

■ Early application permitted (but not before original effective date e.g., January 1, 2017)

■ Both Cumulative Effect and Retrospective transition methods are available. Practical expedients for the Retrospective transition method still allowed

■ IASB has voted to propose a one-year deferral of the Effective Date of IFRS 15

CUMULATIVE EFFECT METHOD

2014 2015 2016 2017 20182013 and prior 2019 and beyond

Evaluate Existing Contracts for Cumulative Effect Adjustment

Maintain Existing Systems and Processes for Legacy GAAP Reporting

RETROSPECTIVE METHOD

Interim Solution / Maintain New Systems & Processes

Dual reporting

2014 2015 2016 2017 20182013 and prior 2019 and beyond

Evaluate Existing Contracts for Cumulative Effect Adjustment

Maintain Existing Systems and Processes for Legacy GAAP Reporting

Maintain New Systems & Processes

Effective Date?

May 6, 2015

Effective Date

Interpretation Considerations

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ('KPMG International'), a Swiss entity. All rights reserved.

FASB expects to issue several exposure drafts to clarify the application of the Standard. Interpretation of an accounting standard during adoption period is normal and requires close monitoring for impacts to ADSK.

Expected Exposure DraftsIssuance Date / Expected

Date of Issuance Description

Exposure Draft 1 –Deferral of Effective Date

April 28, 2015 ■ FASB proposed a deferral of Effective Date (comment letter period end May 29, 2015)

Exposure Draft 2 – Licenses and Performance Obligations

May 12, 2015 ■ Application of the “distinct in the context of the contract” criterion (Step 2) ■ License of intellectual property and the scope and application of the sales- and

usage-based royalties exception (comment letter period end June 30, 2015)

Exposure Draft 3 –Collectibility and other clarification issues

Expected in Q3 2015

■ Collectibility (Accounting for Partial Receipt)■ Additional Issues to be included (comment letter period 30-45 days after Issuance of

the ED)

Exposure Draft 4 – Gross vs. Net presentation

Expected in Q3 2015

■ Comprehensive review of application guidance on gross vs net presentation (comment letter period 30-45 days after Issuance of the ED)

Agenda

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ('KPMG International'), a Swiss entity. All rights reserved.

Overview of the Standard

Changes and Transitions

What’s Happening Today

Planning for Adoption

Wrap Up

Case Studies

Case Study 1: Variable ConsiderationContingent Revenue

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ('KPMG International'), a Swiss entity. All rights reserved.

Step 3

The amount allocable to the delivered unit or units of accounting is NO LONGER limited to the amount that is not contingent upon the delivery of additional items or meeting other specified performance conditions (the non-contingent amount)

A Cloud Service Provider (CSP) enters into a contract with a customer to provide hosting services for three years for a total consideration of $3,000. The customer is required to pay the vendor $100 per month starting in month seven of the contract. ( 6 months of “free service”)

The agreement has a contractual provision entitles the customer to a refund equal to the pro-rata amount of the undelivered services if it is not provided (i.e., if the customer cancels the contract by end of month six no consideration is due from the customer).

A contractual provision that entitles the customer to a refund equal to the prorata amount of the undelivered services if it is not provided would no longer result in an automatic full revenue deferral.

Under the new guidance and assuming there is no significant risk of revenue reversal $3,000 in total consideration would be recognized over a three year period (i.e., $83.33 per month); as compared to current guidance which would result in no revenue for the first 6 months.

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ('KPMG International'), a Swiss entity. All rights reserved.

Step 3

Example – SaaS contract with usage-based fees

A CSP has contracted with a Customer to provide hosted-only access to its software application for two years for a fixed access fee of $200,000 (billed quarterly in advance) plus variable fees of $1 per transaction processed using the hosted software over 1,000 transactions.

CSP, in pricing this contract, has estimated (using a probability-weighted approach) that it would earn $20,000 in transaction-based fees. CSP vendor has entered into similar contracts with other customers; however, none of those customers are in the same business as Customer, so that experience is only partially relevant. Given the lack of relevant experience with similar customers, CSP vendor determines that only $10,000 of variable fees do not carry a risk of resulting in a subsequent revenue reversal.

The Company has a business practice of alerting the customer if the limit of 1,000 transactions is about to be met, or is consistently surpassed so that the customer can consider modifying their current contract.

Considerations when evaluating under the New Standard:

■ In determining the Transaction Price, the Vendor would apply the guidance Variable Consideration (and Constraint).

■ The usage based component does not qualify for the exception because it is not a royalty promised in exchange for a license of IP

■ The SAAS obligation is satisfied overtime (rather than point in time)

■ Modification guidance would need to be applied. Consideration of the frequency of modifications and it’s impact on estimating variable consideration might impact the Vendor’s determination of constraint.

Various approaches available: Currently being discussed at the Transition Committee

Case Study 2: Example SaaS contract with usage-based fees

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ('KPMG International'), a Swiss entity. All rights reserved.

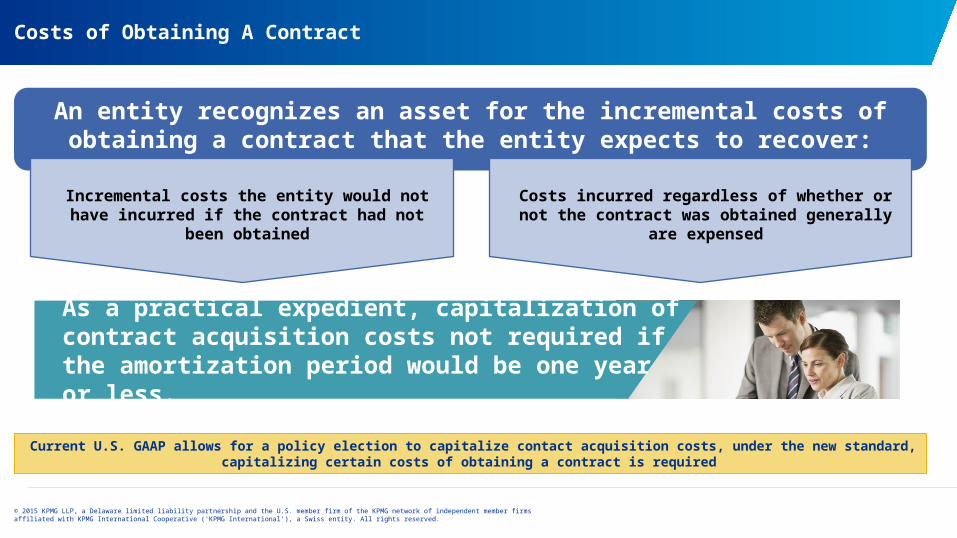

Costs of Obtaining A Contract

As a practical expedient, capitalization of contract acquisition costs not required if the amortization period would be one year or less.

An entity recognizes an asset for the incremental costs of obtaining a contract that the entity expects to recover:

Incremental costs the entity would not have incurred if the contract had not been obtained

Costs incurred regardless of whether or not the contract was obtained generally are expensed

Current U.S. GAAP allows for a policy election to capitalize contact acquisition costs, under the new standard, capitalizing certain costs of obtaining a contract is required

© 2015 Leeyo Software, Inc. CONFIDENTIAL AND PROPRIETARY - FOR INTERNAL USE ONLY - ALL RIGHTS RESERVED

© 2015 Leeyo Software, Inc. CONFIDENTIAL AND PROPRIETARY - FOR INTERNAL USE ONLY - ALL RIGHTS RESERVED

RevPro Reporting

Revenue Waterfall (Actuals and Forecast) Deferred Revenue/Contract Liability Roll-forward Unreleased Performance Obligations Contract Asset Roll-forward Unbilled Roll-forward Arrangement Move Adjusted Allocation Accounting Detail Revenue Disclosure Billing and booking reports User-configurable Reporting Interface

Agenda

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ('KPMG International'), a Swiss entity. All rights reserved.

Overview of the Standard

Changes and Transitions

What’s Happening Today

Case Studies

Wrap Up

Planning for Adoption

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ('KPMG International'), a Swiss entity. All rights reserved.

Where are companies today?

2015 2018

Assess Tax and Broader Business Impact

Determine Budget Required for Implementation

Design Processes and Additional Internal Controls

Implement & Test Controls

2017

Evaluate Assessment Alternatives and Prioritize

Impacts

Design System and Process Functionalities

Evaluate Information and Data & Define Data Requirements

Create Catalog for Changes in Performance Obligations

Automate and Streamline Monthly Close Procedures

Enact Policies and Perform Dual Close Procedures

2016

Build and Test IT SolutionPrepare Adoption Period Financial Statements with

Disclosures

Prepare a Long-Term Communication & Education

Plan

Determine Preliminary Transition Method Decision

Research and Draft Initial Accounting Policies (high

impact)

Revise Accounting Policies & Model Pro Forma Results

Refine Systems and Data Requirements

Sustain New Standard IT Solution

Deploy IT Solution (which includes dual reporting)

Perform Accounting DiagnosticFormalize Steering Committee &

Communication Plan

Evaluate Potential for “Lost Revenue” & “Recycled Cost”

Review Representative Contracts to Confirm Relevant

Differences

Evaluate Interim Transition Solution(s) for Systems

Develop Standalone Selling Prices for new Performance

Obligations

Calculate Transition Adjustments

Monitor Industry & Regulatory Guidance

Note: this timeline is generic in nature and for example purposes only

Initial Assessment

Impact Assessment

Design Processes, Systems, Policy and Controls

SustainGo LiveImplement Processes,

Systems Policy & Controls

© 2015 Leeyo Software, Inc. CONFIDENTIAL AND PROPRIETARY - FOR INTERNAL USE ONLY - ALL RIGHTS RESERVED

Companies Should Already be Working

2015 2016 2017 2018

Awesome if you started already Most companies are here You don’t want to be here

• Plan, review and document policies• Educate cross-functional teams• Make process and system changes• Systematically capture required

information upstream• Implement new or upgrade existing

systems for rev rec automation• Process and analyze data in

multiple ways to see how the new rules impact your revenue

Ample Time To:• Quickly plan, review and decide

policies• Identify methods to capture

required data points for new and existing transactions (systematic or manual upload)

• May not have enough time to implement upstream system process changes

• May have to start processing new transactions under new guidance and catch-up on old transactions over time

Still Time Left To:• Internal and external resource

constraints• Disconnected automation or

manual processing will be the only option

• Risk of delayed Q1 close• Risk of mis-stating revenue

Better to avoid this situation

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ('KPMG International'), a Swiss entity. All rights reserved.

Standard Implementation – Early Lessons Learned

■ High-impact areas may not necessary coincide with the most material financial statement captions. Focus on high impact revenue recognition areas – deprioritize less significant areas

■ Use contract reviews to validate business understanding

■ Involve internal and external auditors early in the process to avoid surprises at end of assess phase

Risk-based approach

■ Better engage management, stakeholders and other business functions to process

■ Educate key employees

■ Assist with more accurately scoping remainder of assess phase

■ Develop a more accurate timeline

Leverage “accounting diagnostic”

■ Help ensure consistent process throughout business units

■ Strengthen controls and documentation around accounting change process

■ Enable consolidated status reporting to management and stakeholders

■ Involve end users at an early stage

■ Maintain dedicated technology resources from KPMG and your team

Leverage technology

Agenda

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ('KPMG International'), a Swiss entity. All rights reserved.

Overview of the Standard

Changes and Transitions

What’s Happening Today

Case Studies

Planning for Adoption

Wrap Up

What Questions do You Have?

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ('KPMG International'), a Swiss entity. All rights reserved.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ('KPMG International'), a Swiss entity. All rights reserved.

The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.