succeeding in a dynamic world: supply management in the decade ahead

TRANSCRIPT

Succeeding in a Dynamic World: Supply Management

in the Decade Ahead

Authors> Phillip L. Carter, DBA

Executive Director for CAPS Research and

Professor of Supply Chain Management, Harold E.

Fearon Chair in Purchasing, W. P. Carey School of

Business at Arizona State University

> Joseph R. Carter, DBA, C.P.M. Avnet Professor, Department of Supply Chain

Management for W. P. Carey School of Business

at Arizona State University

> Robert M. Monczka, Ph.D., C.P.M. Director, Strategic Sourcing and Supply Chain

Strategy Research for CAPS Research, and

Distinguished Research and ISM Professor of

Supply Chain Management for the W. P. Carey

School of Business at Arizona State University

> John D. Blascovich Partner

A.T. Kearney, Inc.

> Thomas H. Slaight Partner

A.T. Kearney, Inc.

> William J. Markham Fellow Emeritus

A.T. Kearney, Inc.

2007A Joint Research Initiative of

CAPS Research

Institute for Supply Management™

A.T. Kearney, Inc.

CAPSFutureStudyCover07.indd 1 9/27/07 8:09:38 AM

Succeeding in a Dynamic World: Supply Management in the Decade Ahead

A Joint Research Initiative of:CAPS Research

Institute for Supply ManagementA.T. Kearney, Inc.

Phillip L. Carter, DBA, Executive Director for CAPS Research and Professor of Supply Chain Management, Harold E. Fearon Chair in Purchasing,

W. P. Carey School of Business at Arizona State University

Joseph R. Carter, DBA, C.P.M., Avnet Professor, Department of Supply Chain Management for W. P. Carey School of Business at Arizona State University

Robert M. Monczka, Ph.D., C.P.M., Director, Strategic Sourcing and Supply Chain StrategyResearch for CAPS Research, and Distinguished Research and ISM Professor of Supply Chain

Management for the W. P. Carey School of Business at Arizona State University

John D. BlascovichPartner

A.T. Kearney, Inc.

Thomas H. SlaightPartner

A.T. Kearney, Inc.

William J. MarkhamFellow Emeritus

A.T. Kearney, Inc.

Copyright © 2007 Institute for Supply Management™ and W. P. Carey School of Business at Arizona State University.

All rights reserved. Contents may not be reproduced in whole or in part without the express permission of CAPS Research.

The lead researchers for this study would like to thank the supply executives of the more than 260 companies thatparticipated in this study for their time and contributions. The research was greatly enriched by their insights andviewpoints on the challenges and opportunities that lie ahead.

The lead researchers would also like to publicly acknowledge and thank the following members of the extendedresearch team for their contributions to this effort.

• Nadine Schnell, Mary Alice McHale, Julie Couch, Stephanie Tsai, Jitender Uppal and Roshni Puri of A.T.Kearney, Inc. developed the web-based version of the survey questionnaire, managed the technical aspects ofits use and developed many of the data extract and analysis tools used by the team.

• Debbie Maciejewski of CAPS Research managed the solicitation process for the CPO focus groups, conferencecalls and interviews for the web survey, and administered the ongoing communications with surveyrespondents.

• Rebecca Sweda, Tuvan Sencalis, Matt Skindzier, Michael Phillips, Arthurine Barned and Deepa Bangaru ofA.T. Kearney, Inc. provided significant analytical and document preparation support throughout the research.

• Inigo Aranzabal, Stephen Easton, Jules Goffre, Mui-Fong Goh, Federico Mariscotti, Jesper Schade, HasanShafi, Per Thompsen, Alfredo Tsutumi, Jan Fokke van den Bosch and Danny Wyatt of A.T. Kearney, Inc.organized and led CPO focus groups and coordinated web survey participation by supply executives in theEuropean, Latin American and Asia/Pacific regions.

• Paul Laudicina, managing officer and Chairman of the Board of A.T. Kearney, Inc., provided valuableguidance and support throughout this effort.

• Jim Brown of A.T. Kearney, Inc., Steve Wade of CAPS Research and Steve Gozdecki, an independent writer,provided ongoing editorial guidance and communications support for the study.

• Sung Kang, Ph.D. candidate in the Department of Supply Chain Management in the W. P. Carey School ofBusiness at Arizona State University, conducted sophistical statistical analysis of the survey results, often withvery short lead times.

• Yusoon Kim, Ph.D. candidate in the Department of Supply Chain Management in the W. P. Carey School ofBusiness at Arizona State University, conducted literature reviews and investigated the feasibility of using awiki as a data collection tool.

• Steve Koch, IS/applications analyst at CAPS Research, provided IS support for the project and pioneered thedevelopment of a wiki for use with the project.

The principal researchers would also like to thank the Institute for Supply Management, and in particular its CEOPaul Novak, for ISM’s significant funding of the research project and for providing access to its membership toreport on the research results at the 2007 Annual International Supply Management Conference and in InsideSupply Management magazine.

ISBN 0-945968-70-1

2 Succeeding in a Dynamic World: Supply Management in the Decade Ahead

Acknowledgements

Acknowledgements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2Contents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3Index of Figures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

External Forces Will Affect All Businesses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8Tomorrow’s Business Models and Strategies Will Raise the Bar for Supply . . . . . 9Supply Must Pursue Seven Key Strategies in the Coming Decade. . . . . . . . . . . . 9

Section I — About the Research. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12Chapter 1 — Background and Previous Research Findings . . . . . . . . . . . . . . . . . . 13

A Look Back . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13The Need for New Research . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Chapter 2 — Research Design and Approach. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16Research Participant Demographics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16Research Methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16Report Structure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Section II — How the Environment for Supply Management Will Change . . . . . . 19Chapter 3 — Forces Driving Change . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Survey Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20Complex Interactions Between Forces . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20What Supply Managers Foresee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

Chapter 4 — Impacts on Business Models and Strategies . . . . . . . . . . . . . . . . . . . 28Keys to Future Success . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28Complex Business Models . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30Other Strategies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

Chapter 5 — New and Expanded Missions, Goals and Performance Expectations for Supply Management. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32Survey Findings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32Delivering More Innovation From Suppliers. . . . . . . . . . . . . . . . . . . . . . . . . . . 32Contributing More Broadly to Revenue Generation . . . . . . . . . . . . . . . . . . . . . 34Anticipating and Managing Supply Risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34Expanding Cost Management Efforts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35Even Broader Missions? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

Section III — How Supply Management Strategies Will Change . . . . . . . . . . . . . . 37Chapter 6 — Overview: Seven Key Strategies for the Coming Decade . . . . . . . . . . 38

E-Survey Findings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38Key Strategies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

Table of Contents

3CAPS Research

Chapter 7 — Developing Category Strategies. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43Achieving Leading-Edge Category Strategy Development and

Implementation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45Strategy Development. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45Strategy Enablers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

Chapter 8 — Developing and Managing Suppliers. . . . . . . . . . . . . . . . . . . . . . . . . 54Structuring the Supply Base . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55Supplier Relationship Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58Developing Supplier Capabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

Chapter 9 — Designing and Operating Multiple Supply Networks . . . . . . . . . . . . 62Modular Versus Integral Supply Chains . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62Managing Multiple Supply Chains . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63Assuring Supply Chain Agility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

Chapter 10 — Leveraging Technology Enablers . . . . . . . . . . . . . . . . . . . . . . . . . . . 70A Decade of Technology Change . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70Supply Executive Goals for Technology Over the Next Decade . . . . . . . . . . . . 72Technology over the Next Decade . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73Future Benefits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74Future Challenges. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

Chapter 11 — Collaborating Internally and Externally . . . . . . . . . . . . . . . . . . . . . 76Key Success Strategies for Collaboration. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77Keys to External Collaboration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77Keys to Internal Collaboration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78Technology Support . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79Protecting Intellectual Capital. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80

Chapter 12 — Attracting and Retaining Supply Management Talent . . . . . . . . . . . 81Identifying Needed Skills and Capabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81Acquiring, Developing and Retaining Talent. . . . . . . . . . . . . . . . . . . . . . . . . . . 84Managing a Diverse, Dispersed Global Workforce . . . . . . . . . . . . . . . . . . . . . . 89Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 90

Chapter 13 — Managing and Enabling the Supply Management Organization . . . 91Moving Away from the Center-Led Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91Integrating Supply with Other Functions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93Cross-Functional Teams . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94Outsourcing Supply Management. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95Measuring Supply Management Performance . . . . . . . . . . . . . . . . . . . . . . . . . . 95Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98

Section IV — Conclusions and Recommendations . . . . . . . . . . . . . . . . . . . . . . . . 100Chapter 14 — Research Summary and Potential Supply Challenges

for the Decade Ahead . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101Forces of Change . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101Supply Mission — The Era of Great Expectations . . . . . . . . . . . . . . . . . . . . . 102Category Strategy — The Era of Dynamic Value Acquisition Strategies . . . . . 102Developing and Managing Suppliers — The Era of Customer-centric

Supply Base Strategies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102Developing and Operating Multiple Supply Networks — The Era of

Complex and Dynamic Supply Networks . . . . . . . . . . . . . . . . . . . . . . . . . 103Collaboration — The Era of Collaboration Without Boundaries. . . . . . . . . . . 103Technology — The Era of Networked Analytics . . . . . . . . . . . . . . . . . . . . . . . 103Talent Management — The Era of Killer Talent in Supply Management . . . . . 104Organizational Design — The Era of Empowerment and Adaptation . . . . . . . 104

4 Succeeding in a Dynamic World: Supply Management in the Decade Ahead

Chapter 15 — Recommendations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 105Key Takeaways . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 105Recommendations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 108

Appendix A — CEO Survey Results. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 109Appendix B — Study Participant Demographic Profiles . . . . . . . . . . . . . . . . . . . . 112Appendix C — E-Survey Questionnaire. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 115Appendix D — Analysis Strategy and Results of Detailed Analyses . . . . . . . . . . . 131

5CAPS Research

Figure 2.1: Research Framework . . . . . . . . . . . 18

Figure 3.1: Average Ratings of External Forces’ Impact on Business. . . . . . . . . . . . . 21

Figure 3.2: Linear Versus Exponential Growth Rates. . . . . . . . . . . . . . . . . . . . . . . . 26

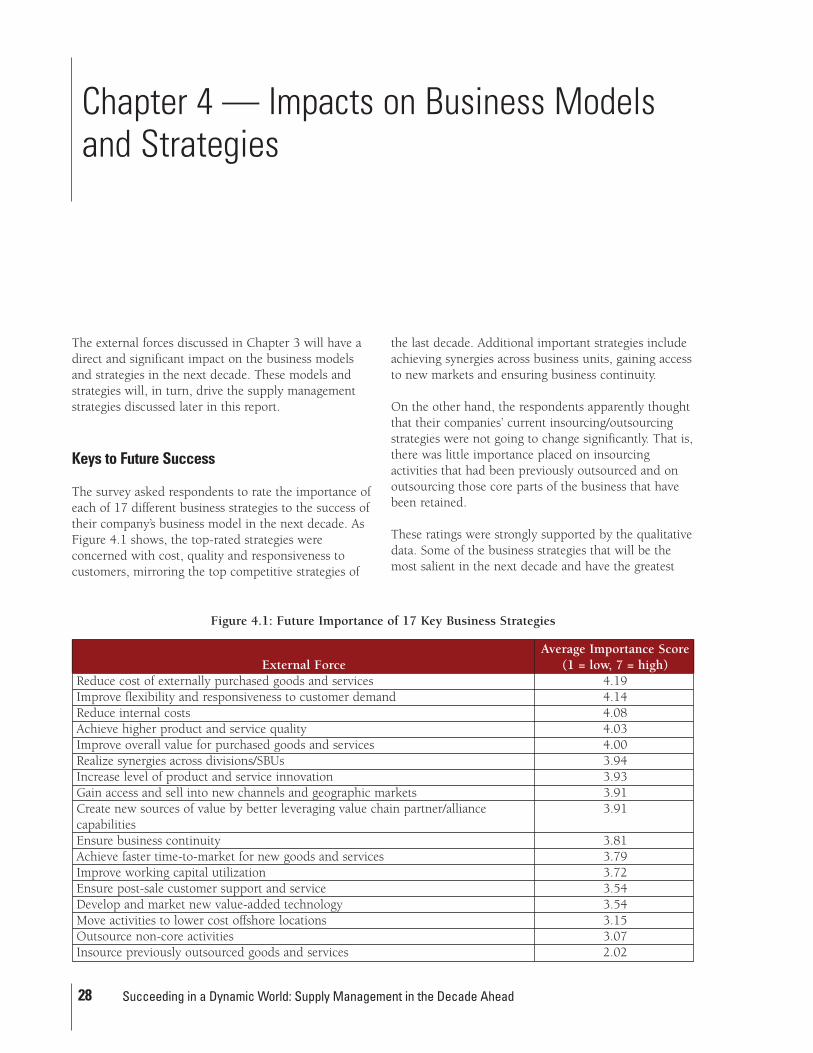

Figure 4.1: Future Importance of 17 Key Business Strategies . . . . . . . . . . . . . 28

Figure 5.1: Supply Missions and Goals. . . . . . . 33

Figure 6.1: Future Importance Versus Current Level of Implementation. . . . . . . . . 39

Figure 6.2: Quadrant 1 Biggest Gap — Collaboration Remains a Challange . . . . . . . . . . . . . . . . . . . . 39

Figure 6.3: Quadrant 2 Biggest Gap — Information Sharing Across the Extended Supply Chain . . . . . . . . . 40

Figure 6.4: Many Supply Strategies Are Universally Seen as Very Important . . . . . . . . . . . . . . . . . . . . 40

Figure 6.5: North America — Emphasis on Internal Strategic Alignment . . . . . . 41

Figure 6.6: Europe — Emphasis on Global Strategies, External Integration andOrganization. . . . . . . . . . . . . . . . . . 41

Figure 6.7: Supply Chain Focus in Manufacturing Sector,Administration and Control Focus in Services Sector . . . . . . . . . . . . . . 41

Figure 7.1: Creating Additional Value by Thinking Differently about Categories. . . . . . . . . . . . . . . . . . . . 44

Figure 7.2: Category Strategy Framework. . . . . 45

Figure 7.3: Category Strategy Critical Element Change . . . . . . . . . . . . . . . . . . . . . . 46

Figure 7.4: Rapid Growth Seen for China, India and Eastern Europe as SourceMarkets . . . . . . . . . . . . . . . . . . . . . 48

Figure 7.5: Most Companies Expect a Net Decrease in Number of Suppliers by 2012 . . . . . . . . . . . . . . . . . . . . . 48

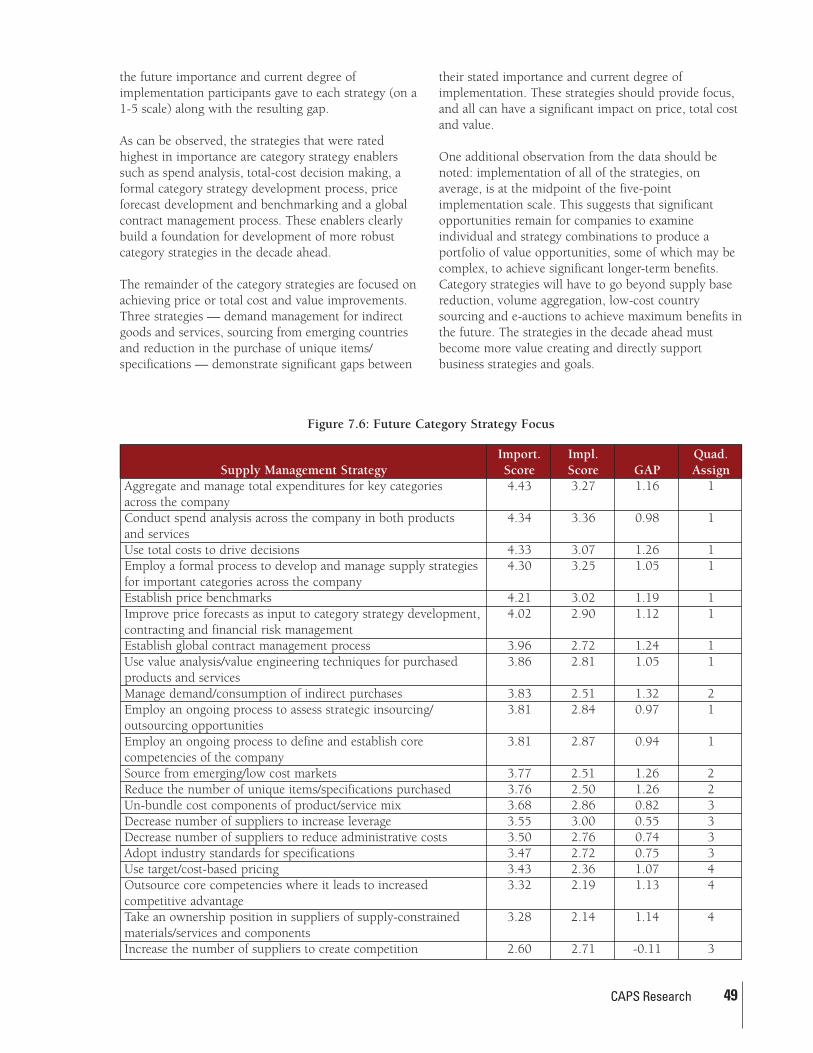

Figure 7.6: Future Category Strategy Focus . . . 49

Figure 8.1: Developing and Managing Suppliers . . . . . . . . . . . . . . . . . . . . 55

Figure 8.2: Developing and Managing Suppliers — Maturity Stages . . . . . 57

Figure 8.3: Typical Supplier Segmentation . . . . 59

Figure 8.4: Driving Toward Institutionalized Supplier Relationships . . . . . . . . . . 59

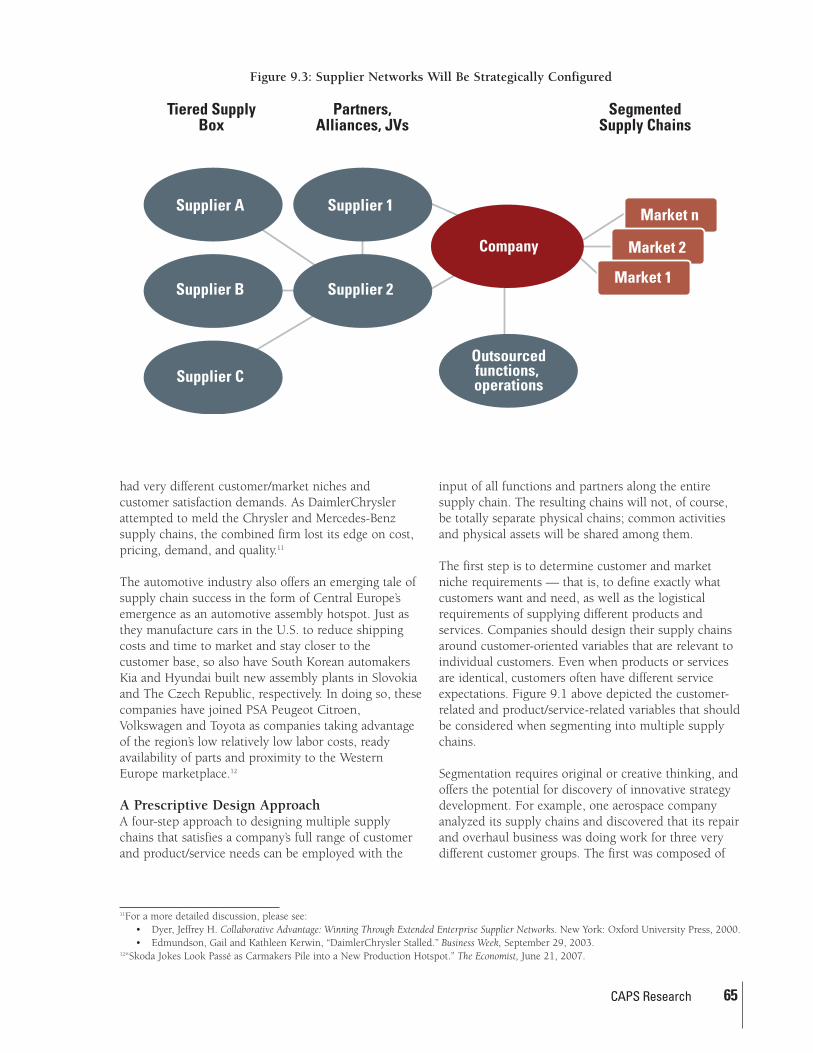

Figure 9.1: Supply Chains Will Be Segmented by Product/Customer . . . . . . . . . . . 63

Figure 9.2: Designing and Operating Multiple Supply Networks — Supply Management Strategy Gaps. . . . . . . 64

Figure 9.3: Supplier Networks Will Be Strategically Configured . . . . . . . . . 65

Index of Figures

6 Succeeding in a Dynamic World: Supply Management in the Decade Ahead

Figure 9.4: Complex Models Will Be Used To Evaluate Supply Chain Risk, Costs, Performance and Design. . . . . . . . . 67

Figure 9.5: Supply Network Flows . . . . . . . . . . 69

Figure 10.1: Technology Tool Evolution . . . . . . . 71

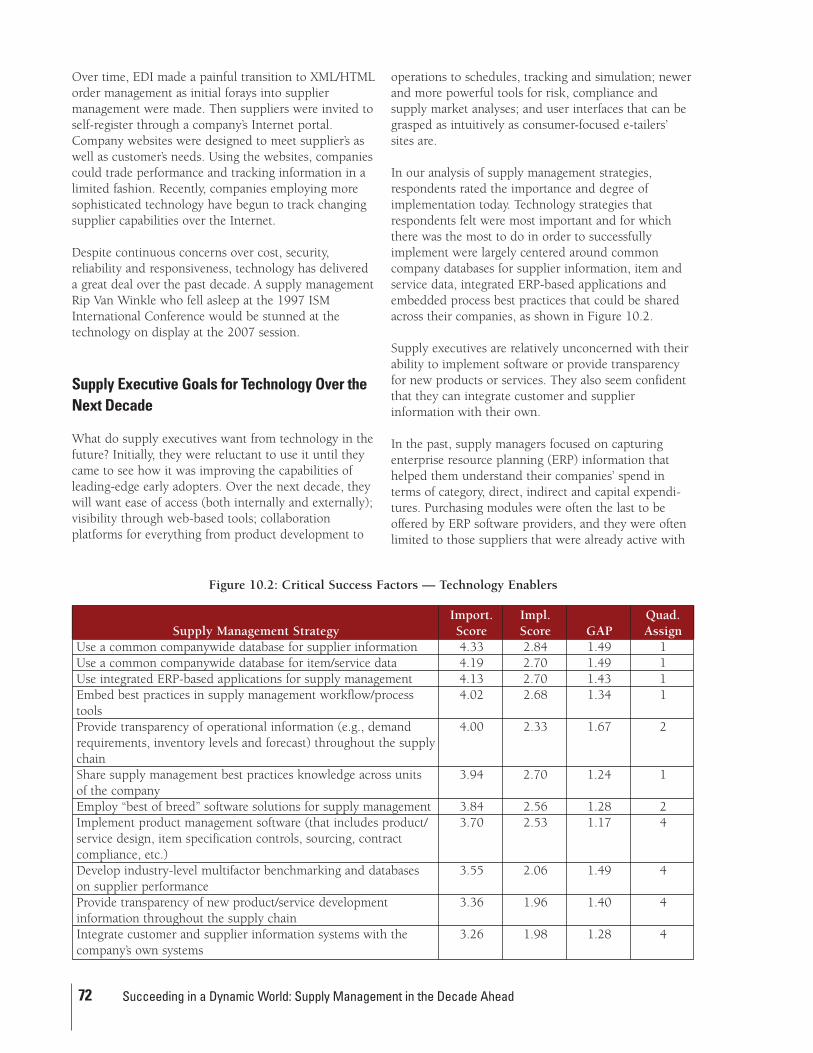

Figure 10.2: Critical Success Factors — Technology Enablers. . . . . . . . . . . . 72

Figure 10.3: Technology Tools Will Evolve Even Further . . . . . . . . . . . . . . . . . 73

Figure 11.1: Collaboration Strategies . . . . . . . . . 76

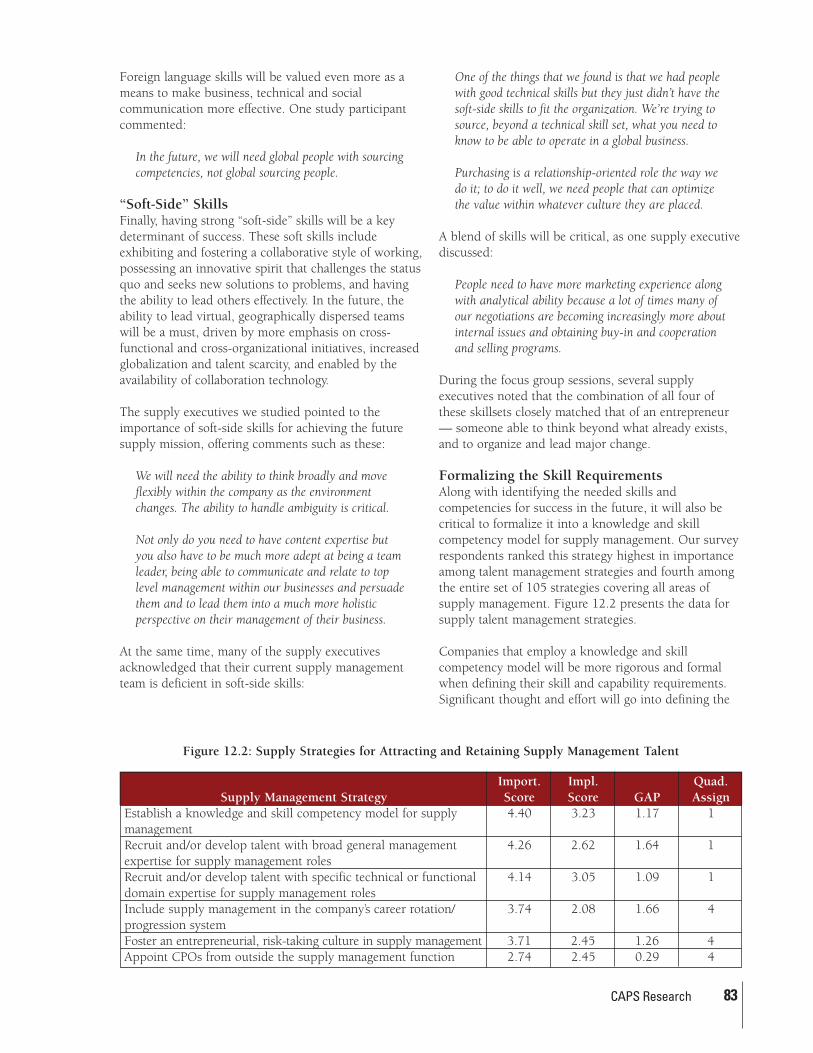

Figure 12.1: Future Skills and Capabilities for Supply Management Professionals . . . . . . . . . . . . . . . . . . 82

Figure 12.2: Supply Strategies for Attracting and Retaining Supply Management Talent . . . . . . . . . . . . . . . . . . . . . . . 83

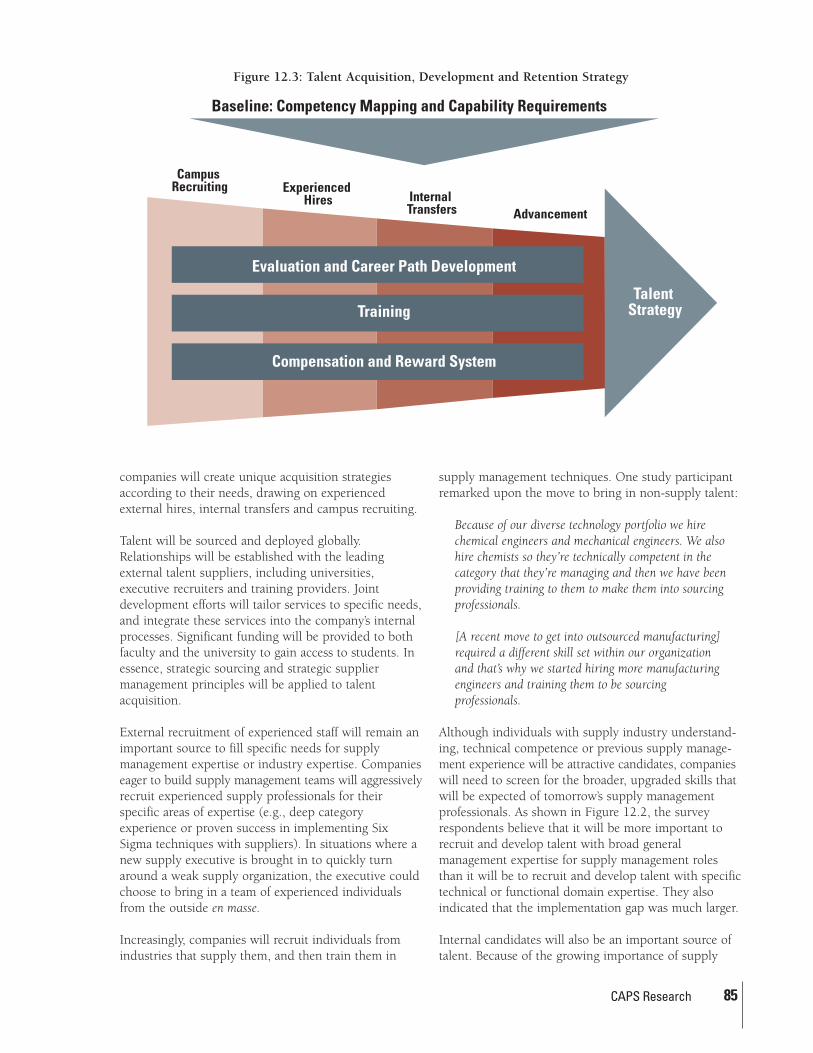

Figure 12.3: Talent Acquisition, Development and Retention Strategy . . . . . . . . . . 85

Figure 12.4: Supply Management Career Paths . . . . . . . . . . . . . . . . . . . . . . . 87

Figure 12.5: Managing the Workforce of Tomorrow. . . . . . . . . . . . . . . . . . . . 89

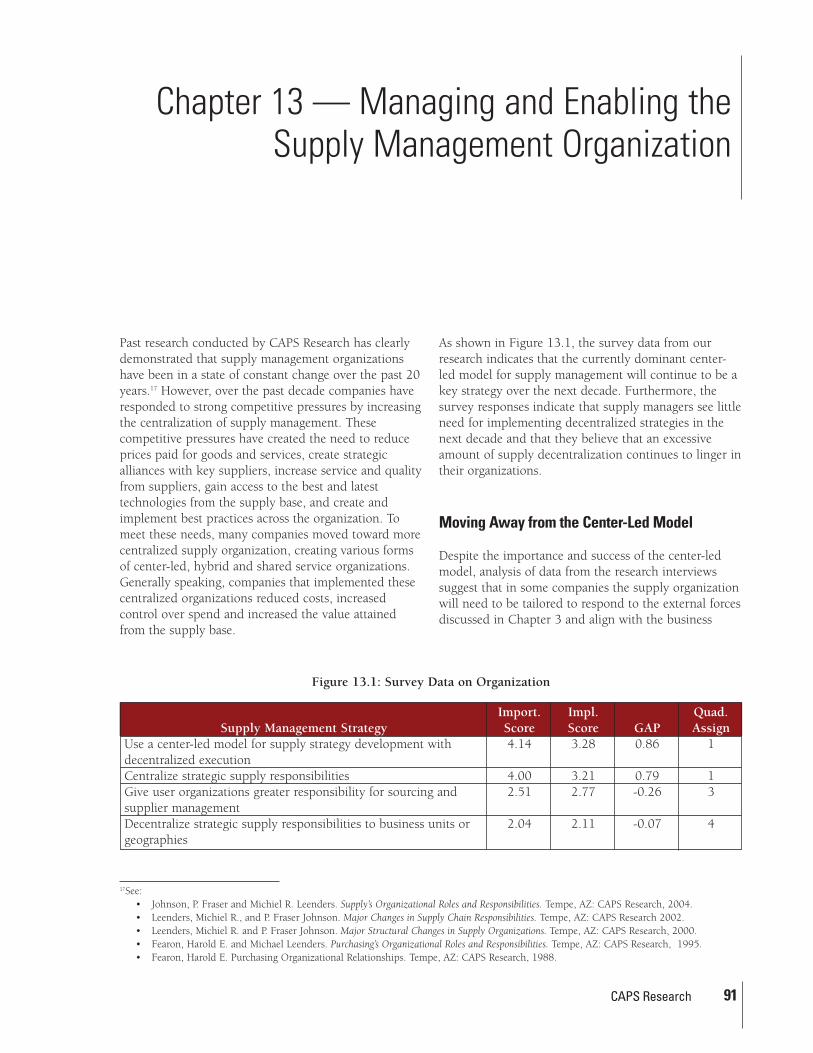

Figure 13.1: Survey Data on Organization . . . . . 91

Figure 13.2: Survey Data on Integration of Supply Management . . . . . . . . . . . . 93

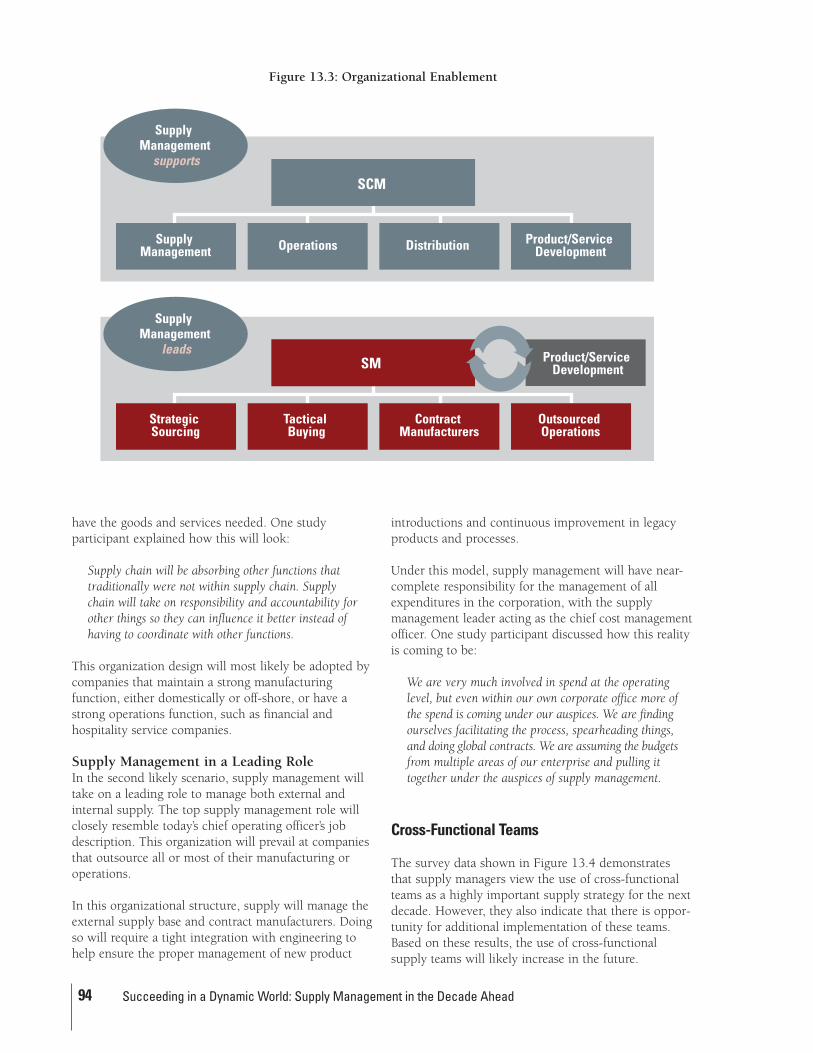

Figure 13.3: Organizational Enablement . . . . . . 94

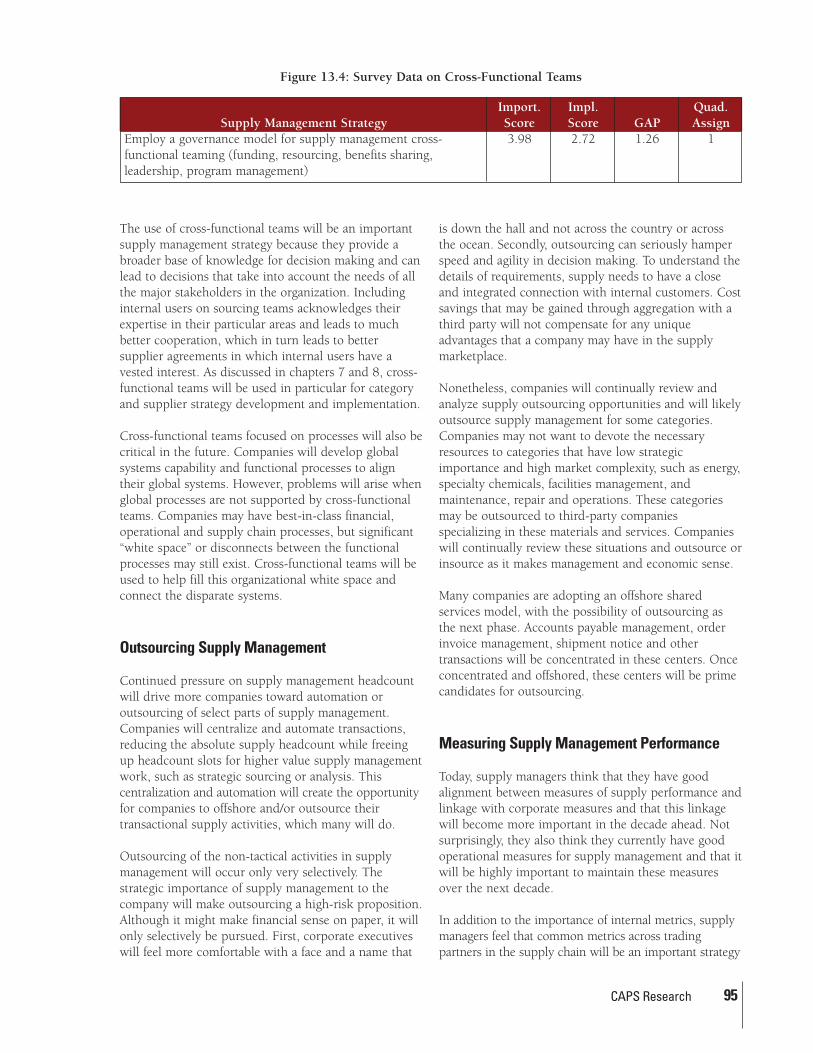

Figure 13.4: Survey Data on Cross-Functional Teams . . . . . . . . . . . . . . . . . . . . . . . 95

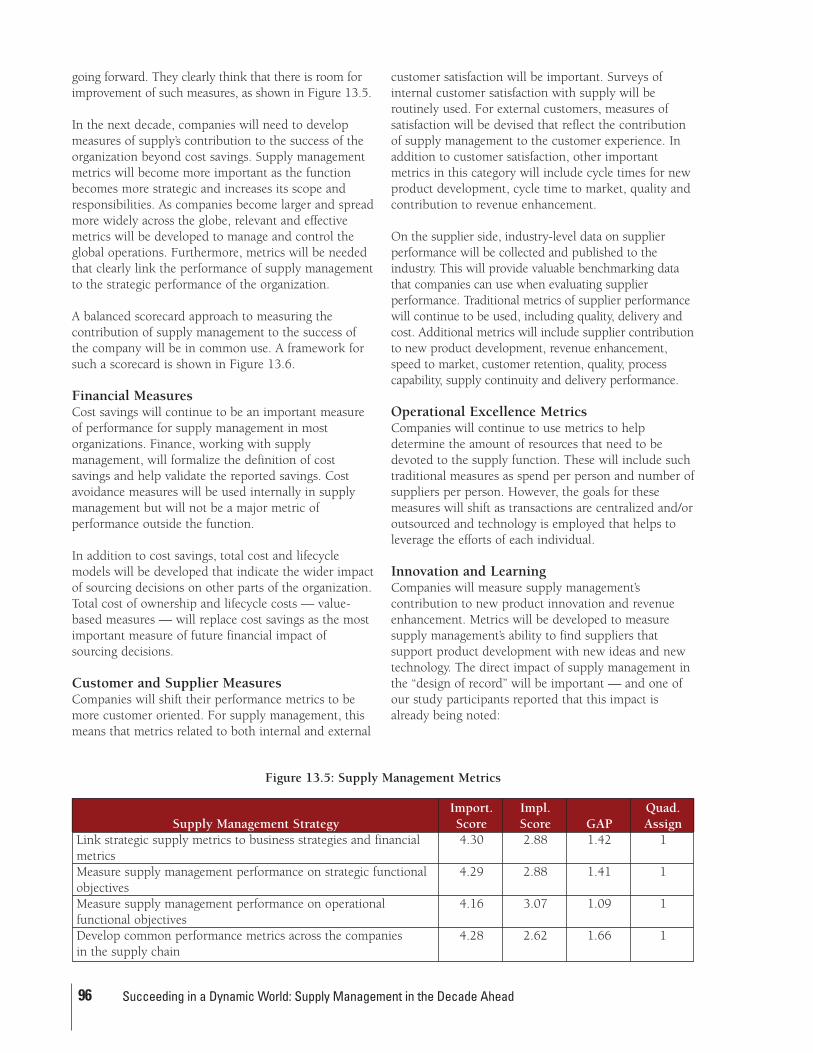

Figure 13.5: Supply Management Metrics . . . . . 96

Figure 13.6: Balanced Scorecard for SupplyManagement. . . . . . . . . . . . . . . . . . 97

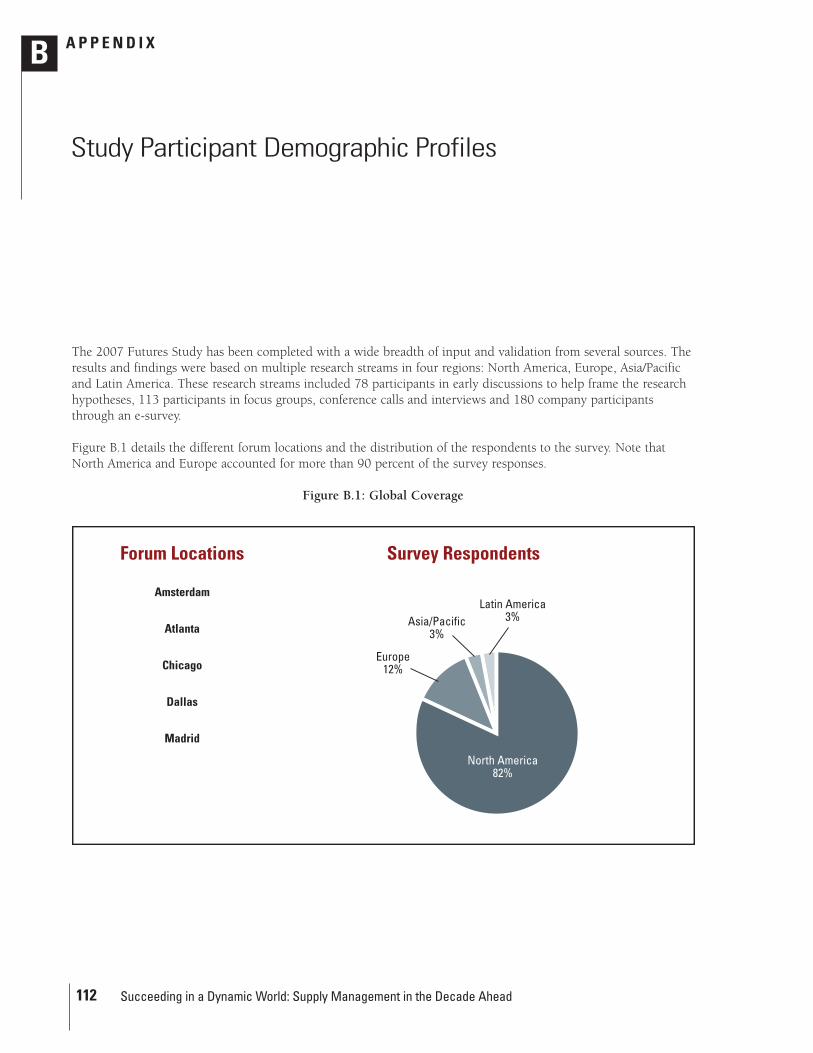

Figure B.1: Global Coverage . . . . . . . . . . . . . . 112

Figure B.2: E-Survey — Revenue Size . . . . . . 113

Figure B.3: E-Survey — Respondents’ Global Presence . . . . . . . . . . . . . . . . . . . . 113

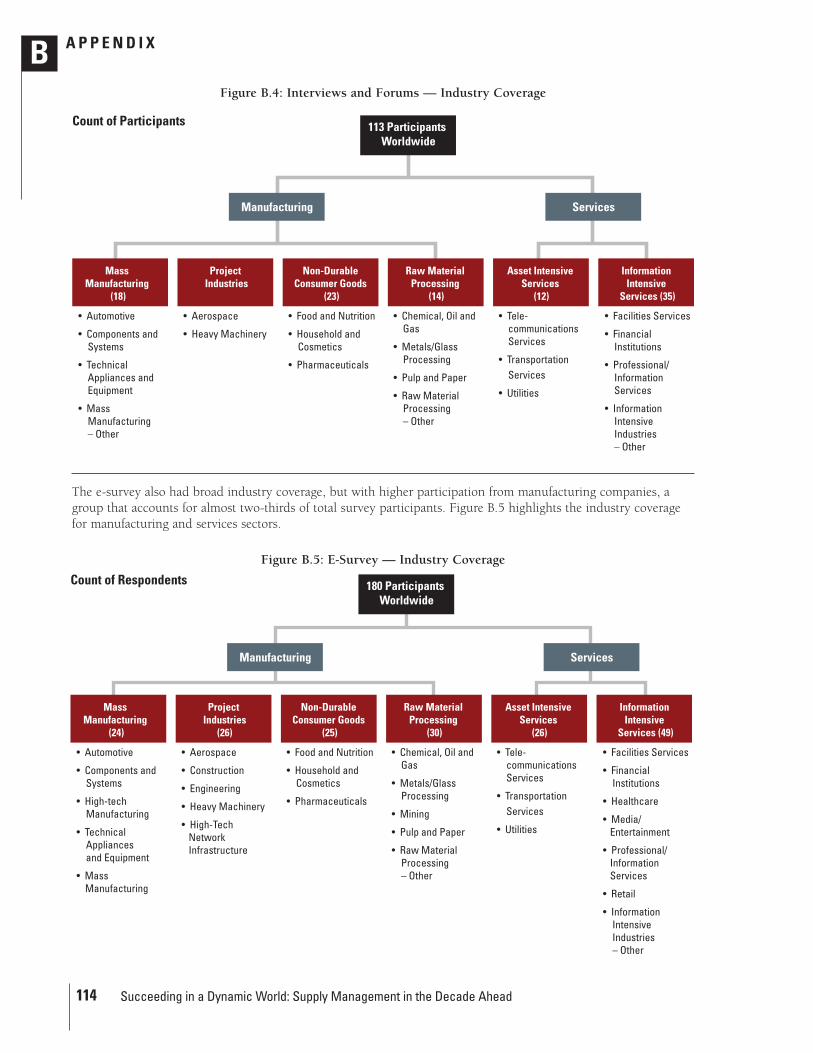

Figure B.4: Interviews and Forums — IndustryCoverage . . . . . . . . . . . . . . . . . . . 114

Figure B.5: E-Survey — Industry Coverage . . 114

Figure D.1: Forces of Changes — Sorted by Mean Response. . . . . . . . . . . . . . . 133

Figure D.2: Forces of Change — Factors. . . . . 134

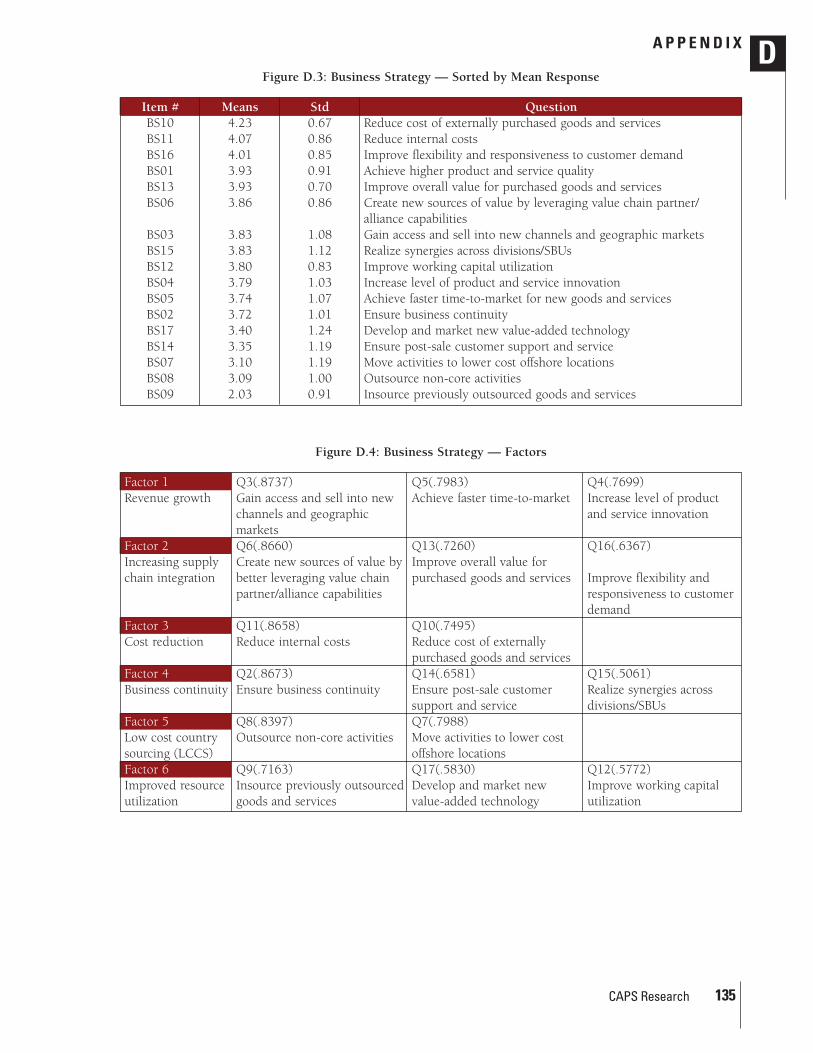

Figure D.3: Business Strategy — Sorted by Mean Response. . . . . . . . . . . . . . . 135

Figure D.4: Business Strategy — Factors. . . . . 135

Figure D.5: Supply Mission, Goals and Performance Expectations — Sorted by Mean Response. . . . . . . 136

Figure D.6: Supply Mission, Goals and Performance Expectations — Factors . . . . . . . . . . . . . . . . . . . . . 137

7CAPS Research

In 1998, CAPS Research, A.T. Kearney and the Instituteof Supply Management published “The Future ofPurchasing and Supply: A Five- and Ten-Year Forecast,”a research study that helped the procurement professionunderstand and prepare for the future. Although manyof the predictions from that report proved to be true,there has been significant change in the world since1998 — and each of these changes has consequencesfor how businesses and industries operate, and in turnhow companies manage supply.

As a result, CAPS Research, A.T. Kearney and theInstitute of Supply Management have once againexplored the future direction of supply management.The objective of the research was to find answers tothese questions:

• What external forces will have the greatest effecton business over the next ten years?

• How will business models change as a result ofthese forces?

• How will the mission, goals, performanceexpectations and strategies for supplymanagement change to support these newbusiness models?

More than 260 companies from North America, Europe,Latin America and Asia/Pacific participated in the 2007research. About two-thirds of the participatingcompanies came from manufacturing industries, whilethe rest were from service industries.

This executive summary distills the main findings andrecommendations of the research, while the completereport that follows presents the detailed results of thestudy.

External Forces Will Affect All Businesses

A multitude of external forces will reshape markets,products and industries over the course of the nextdecade. To survive, companies will have to rethink andrevamp their business strategies in order to anticipate,react to and even take advantage of these forces.

The research indicates that supply managers areconcerned about a variety of forces that will impactcompany and supply management strategies. Foremostamong these is the impact of China, India and otherlarge, developing countries on the competitivelandscape. The impact is expected to be felt on both thedemand and supply side, and will create opportunitiesas well as challenges.

To meet this onslaught of new competition, companiesheadquartered in developed economies will need toincrease in size, with improved economies of scale andmarket power on both the supply and sell sides, tosurvive. Thus, in order to successfully compete, manycompanies will be forced to merge and consolidate.

Government legislation and regulation of business willincrease, requiring companies to dedicate significantresources to ensure compliance. Government actions tosupport economic development, such as tax incentivesand trade restrictions, will have a large impact onsupply strategies. Political instability could require arapid change in supply strategies.

Technology breakthroughs will cause major changes tohow products and services are provided. These changesmay require capital investment, but will lower thecustomer’s total cost of ownership. In many industries,core technologies will eventually be commoditized,forcing geographic consolidation and concentration of

Executive Summary

8 Succeeding in a Dynamic World: Supply Management in the Decade Ahead

the supply base and fundamentally affecting supplychain structure and relationships.

In some industries, the downstream supply chain willchange rapidly due to economics and governmentpolicies. Within other industries, supply chaindynamics will be influenced by the poor financialcondition of major trading partners in the chain. Thisperformance will reverberate up and down the chain,altering relationships and causing suppliers to seekother customers and/or sources of revenue.

The impact of private equity firms will also besignificant. Many companies and suppliers have alreadybeen bought and taken private by these companies. Inlooking to recoup their investments, the private equityfirms tend to slash costs, raise prices and changebusiness relationships with their trading partners,affecting supply and supply chain strategies.

Companies in developed economies will be held to highstandards wherever they do business in the world.Supply management will be tasked with working withthe supply base to ensure that it meets environmentalstandards. Customers, consumers, shareholders, non-government organizations and government will allincrease their scrutiny of corporate environmentalpractices in all regions of the world. They will demandthat companies take environmentally friendly actions bydoing things like using less packaging material,reducing carbon emissions and making products thatcan be readily recycled.

Tomorrow’s Business Models and StrategiesWill Raise the Bar for Supply

In response to these forces, companies will shift theirbusiness models, adopt different strategies, pursue newrevenue streams, further squeeze costs, make their assetbase as lean as possible and reshape their capitalstructures. The mission and role of supply managementwill be changed in a variety of ways.

The need for innovation will accelerate as companiescontinue to aggressively pursue new geographic anddemographic markets. With the demand and supply forinnovation in a state of flux over the coming decade,and limited resources within any one firm, companiesmust overcome the usual “not invented here” barriersand tap into all available sources globally.

Relationships between companies and their externalinnovation sources may need to be structureddifferently in the future. This will be especially truewhere past adversarial approaches have deterred

suppliers from sharing their best and brightest ideas.Financial support, equitable sharing of risks andbenefits and two-way protection of intellectual propertyrights will need to be a part of the mix.

Supply management has always helped contribute torevenue generation. Close attention to costs for goodsand services leads to more competitively priced endproducts. A focus on quality and service reduces failurerates, improves availability and leads to higher customersatisfaction and loyalty. Innovations from the supplymarket lead to revenue increases from new productsand services.

Already, there is widespread acknowledgement amongsupply executives of heightened top-down attention tosupply risk management. Extended global supply chainsthat include geographically distant, unproven (or evenunknown) suppliers pose supply continuity, liability,reputational and intellectual property risks.

Supply management must more aggressively manageliability and safety risks as well. To ensure compliancewith Sarbanes-Oxley legislation, supply must addressinternal controls as well as a range of possible risk-exposure areas that includes supply chain disruption,outsourcing, long-term contracting, leasing and vendor-managed inventories.

Performance expectations will be raised considerably asglobal competition forces companies to squeezeunnecessary cost out of every part of their business. Forsupply management, this means widening the breadthof spend areas covered, managing costs more holisticallyand delivering cost savings faster.

Supply Must Pursue Seven Key Strategies in theComing Decade

Based on an analysis of the survey data and focussession and interview learnings, the research teamconcluded that seven main families of strategies willhave the greatest impact on supply management successin the future.

Developing Category Strategies that are Robustand Forward LookingCategory strategies will become more robust and requireengagement not only from multiple functions but alsoacross enterprises. They will become more agile due tothe fact that they will have to be quickly reconfigured asconditions change. Strategy development opportunitieswill be examined across categories where synergies arepossible; e.g., packing and specific product designs.

9CAPS Research

Strategy development will include approaches toinfluence supply markets. Category strategies willincreasingly aim to block competition, and early-warning or predictive approaches will be used as part ofan improved approach to risk.

Developing and Managing Value-AddingRelationships with SuppliersThree dominant themes will emerge around developingand managing suppliers. First, the supply managementfunction will have to clearly understand company needsand align with suppliers that have the capabilities toprovide innovation and help create value in support ofachieving competitiveness.

Second, working relationships between buying andselling companies that are strategically important toeach other will improve in order to unlock value-creating potential. The supply base will include supplynetworks, many of which will be in competition witheach other. This new reality will require leadingcompanies to provide leadership and manage entiresupply networks, not just individual suppliers, to gainpreferential treatment and competitive advantage.

Finally, companies will invest in reactive and proactivesupplier development efforts to maximize the valueachieved by the supply base. As strategic suppliersdevelop, they in turn will be afforded opportunities tohelp improve the buying company through continuoustwo-way communications and feedback.

Designing and Operating Multiple SupplyNetworks to Meet the Needs of Specific MarketSegmentsSupply chains that are seamless and driven by end useror customer needs will become the norm. Revenues willflow to companies that can get the correct product orservice bundles to customers at the lowest landed andtotal costs. Supply chain innovation and the use ofmultiple supply chains will be key to future revenueand market share growth.

Leading companies will pioneer tomorrow’s supplychains by combining multi-company capabilities in newways. They will create total service offerings that extenddeep into the customer’s value chain. They willanticipate changes, adapt their supply chains by using ablend of insight, strategy, creativity and technology, andaccelerate the achievement of results.

Leveraging Technology for Internal Productivityand External EffectivenessTechnology developers are positioned to provide aricher set of offerings for supply management. But there

will be many challenges moving forward. Managementwill pose one such challenge, as new technology willbring up concerns about inter-functional collaborationand potential loss of intellectual capital. Each of thesenew technologies also requires practitioners who havethe capabilities — the knowledge, insight and interests— to get the most out of them. In part due to theadoption of technology, the headcount of supplymanagement resources has been pared down over thepast decade, which may make obtaining additionalresources to learn and implement new technologies achallenge.

Collaborating Internally Across Functions andExternally with Suppliers and CustomersWhile collaboration was cited as an important successfactor for the future, it was also noted that it does noteasily fit in with the traditional view of supplymanagement’s role in the organization. Four mainthemes around collaboration emerged:

• Internal collaboration and integration mustadvance further if companies are to capitalize ontheir future needs.

• External collaboration will signal a shift from purecompetition to partnership for some segments of acompany’s supply base.

• Technology will be necessary to enable thisincrease in collaboration — internal systems willhave to provide more visibility to multiple dataviews, while external systems will have to shareinformation safely and effectively.

• The tension between the potential for strategicadvantage through supplier collaboration and theconcerns about managing risk and protectingintellectual property will not be easily resolved.

Attracting and Retaining Supply ManagementTalentSupply management organizations will take onincreased responsibility and a higher value role.Tomorrow’s supply management professionals will becharged with developing and executing valueacquisition strategies that find new value in the supplybase, deliver value as quickly as possible within the costparameters defined by the demand market andmaximize the return to the company. To do so, they willneed to find and leverage external sources ofinnovation, contribute to revenue generation, expandefforts to manage costs, and ensure business continuityand sustainability.

In many ways, talent management could be thedeciding factor between success and failure fortomorrow’s supply management organizations. Ingeneral, companies will have access to the same supply

10 Succeeding in a Dynamic World: Supply Management in the Decade Ahead

market information, the same suppliers and the samesupply management best practices and tools. What willbe different is how each company uses that information,works with those suppliers, and applies those practicesand tools, which will come down to the skills andcreativity of its people and the relationships thosepeople build with others.

Managing the Future Supply ManagementOrganizationDespite the importance and success of the center-ledmodel, some companies may benefit from tailoring thesupply organization for future needs.

Specifically, some of the factors that will drive thispotential adjustment are the need for local leadershipwithin a globally managed workforce, the relaxation oftight supply markets that allows category leadershipwithin business units and the maturation of technologyto support common practices across organizationalboundaries. This last point could mean that technologywill allow virtual collaboration among category teamsand free them from the necessity to be co-located at orconstantly traveling to a central location. Knowledgemanagement systems will give personnel access to thesame information regardless of their locations.

Aggregation of demand may benefit the corporation as awhole, but it can still be detrimental to the performanceof a specific unit. While centralized-versus-decentralizedcontrol is an old argument, large business units mayhave the superior argument in the future, to thedetriment of strong centralized supply organizations.Best practices created by center-led organizations canstill be implemented by business units at companiesthat no longer see the need for centralized control.

Continued pressure on supply management headcountwill drive more companies toward automation oroutsourcing of select parts of supply management,continuing a trend to allocate scarce resources to themost strategic activities.

Outsourcing of the non-tactical activities in supplymanagement will occur only very selectively. Thestrategic importance of supply management to thecompany will make outsourcing a higher-riskproposition.

11CAPS Research

Section I — About the Research

12 Succeeding in a Dynamic World: Supply Management in the Decade Ahead

In the early 1990s, purchasing began a long journey oftransformation from a tactical activity to a strategiclever. By 1998, new approaches were taking hold, suchas strategic sourcing and strategic cost management,and leading companies were using these to demonstratethat purchasing could contribute more to the businessthan low prices for purchased goods and services. E-procurement offered the promise of additional benefits,both to extend the reach of the purchasing organizationinto supply markets and to boost internal efficiencies.

In 1998, CAPS Research, A.T. Kearney and the Instituteof Supply Management undertook a study to help theprocurement profession understand what might comenext. The results of that research were released in areport entitled “The Future of Purchasing and Supply: A Five- and Ten-Year Forecast.”

A Look Back

As Danish physicist Niels Bohr once said, “Prediction isvery difficult, especially about the future.” Yet, lookingback on that 1998 study, many predictions about thefuture of supply management proved quite accurate.The 1998 study predicted that:

• Electronic commerce and supply e-systems wouldbe widely implemented and the internet wouldbecome the backbone of e-supply. This hasoccurred and growth continues.

• Strategic cost management, with a focus on costreduction, would continue to be the primarysupply focus. This has clearly proven to be the case,with outsourcing, volume aggregation, e-auctions, low-cost country sourcing and price give-backs being theprimary supply strategies at many companies.

• Strategic sourcing would be applied acrossorganizations worldwide; supplier evaluation and

selection criteria would become more extensive;and category strategies would become more fullydeveloped and somewhat more linked tocompanywide strategies. All of the above haveoccurred at numerous companies worldwide.

• Global sourcing would increase. This has clearlybeen the case.

• Performance measurement would continue to befocused on cost reduction, with companiesadopting total-cost-related measures of performanceand increased linkages with strategic businessmeasures. Numerous companies have implementedthese approaches, including engagement with finance.

• Tactical purchasing would increasingly beautomated and outsourced. Headcounts would bereduced through digitization. Both have occurred atorganizations worldwide, and there are now a numberof third-party providers of e-supply software.

• Process uncoupling would occur. This uncouplingis evidenced by the growth of outsourcing, theutilization of contract and original designmanufacturers and various supply chain models beingused to meet customer requirements; e.g., a thirdparty producing and shipping direct to the endcustomer.

Predictions in some other areas were directionallycorrect but did not achieve as extensive and broad-based implementation. These included:

• Competitive bidding, negotiation and negotiationstrategy would continue to be important butchange in nature, becoming more data driven andtotal-cost focused. However, possibly driven by abuyers’ market, e-reverse auctions and low-costcountry sourcing, this has not occurred to the degreeanticipated.

• Third-party purchasing, especially for non-criticalitems, would increase, although not across all

Chapter 1 — Background and Previous Research Findings

13CAPS Research

industries and for all categories of purchases. Thisstrategy still appears to be emerging.

• Supplier development would possibly become animportant supply initiative. This has been the casein some industries, especially automotive. However,there is no across-the-board drive to invest heavily inproactive supplier development.

• Strategic supplier alliances would become a focusacross numerous industries. This has only been thecase at a limited number of companies that havecarefully segmented suppliers into “eliminate,”“continue,” “preferred” and/or “strategic” categoriesand where supplier relationship management has beenestablished as a key strategy. Much still needs to bedone to modify behaviors and processes to fullycapitalize on the value-unlocking potential of strategicsupplier alliances.

Four areas where the 1998 predictions fell far shortwere:

• Demand-pull purchasing with full transparency ofsupply-and-demand requirements would bevisible across companies in the supply chain, alloperating in a synchronized manner andminimizing costs and waste. Implementation hasbeen severely limited by a lingering inability tointegrate data across disparate systems andunwillingness by some companies to share data acrossorganizations.

• Virtual supply chains would be created to meetshort-term needs. These virtual supply chainswould be characterized by risk/reward sharing,transparent resource commitments, operatingguidelines and means to end the relationship. Thishas not occurred, with traditional organizationsprevailing.

• Relationship management of a cross-organizational focus would be implemented.Again, given the relatively long-lived buyers’ marketduring the dot.com build-up, e-sourcing and reverseauctions may have contributed to delaying thedevelopment of inter-organizational relationships.

• Complexity management resolution would beachieved from both an inter-organizational andproduct/service design perspective. Organizationshave still not solved the complexities of how to conductbusiness between organizations to maximize valuecreation. Nor have companies been able to fullyminimize product/service specifications enablinggreater degrees of standardization and flexibility inoperations and design.

Overall, the 1998 study provided significant insight intothe decade that lay ahead. Supply leaders were able to

use these predictions to prepare their company’stransformation strategies and focus attention.

The Need for New Research

Much can change in a decade’s time. When the previousstudy was released, there were no iPods. The Euro hadnot been introduced. Business process outsourcing toIndia was still in its infancy. The dot.com boom andbust had not yet occurred. Terrorism was but a remotepossibility in most of the developed world.

Yet in ten short years, each of these changes has cometo deeply affect how businesses and industries operate.In turn they affected how companies manage supply —what they buy, where they source from, how they workwith suppliers, and which tools and organizationalmodels they use.

Changes have already included extensive e-systemimplementation, outsourcing, globalization and low-costcountry sourcing, movement to center-led supplyorganizations and cross-functional teaming, formalcategory strategies, enhanced understanding of supplierand supply chain costs, and efforts to better integratesupply chains applying lean principles and Six Sigma.

Will the future just be an extension of these changes, orwill radical new approaches emerge? What will be themost effective supply models in the decade ahead? Inwhat direction will organization strategies be driven? Towhat extent will supplier working relationships driveperformance? How will technology be applied? Whatextensions of category strategies are required, and howwill these strategies be linked to companywidestrategies? What performance metrics will drive supplybehavior? What should the human resources strategybe?

These questions are of critical importance to companyand supply leaders. One supply executive summed it upthis way:

What comes next after implementing many changes insupply strategy, structure, processes and people overthe prior decade?

To answer these and other questions, CAPS Research,A.T. Kearney and the Institute of Supply Managementundertook this second broad-based study to determinethe forces of change that would impact a company’sbusiness models, how these would affect executiveexpectations of supply, and what the future might holdfor supply strategies, processes and enablers.

14 Succeeding in a Dynamic World: Supply Management in the Decade Ahead

The current look forward into the next decade shouldprovide valuable insights, as the predecessor researchdid. This study, extending and further globalizing the1998 research, may be even more important because ofthe dramatic and fast-changing macro trends and eventsoccurring worldwide. The growth of China and India askey markets and suppliers, population growth trends,terrorism, political uncertainties, the financial distressbeing felt in a number of industries, and mergers andacquisitions are but a few. These, combined withincreasing customer and competitive pressures andtechnology capabilities, provide an environment inwhich business and supply models must be agile inanticipating and reacting to competitive shifts.

This report discusses how we conducted the study,identifies forces of change and resulting businessmodels, and the key supply strategies, processes andenablers unfolding in the decade ahead. While some ofthe concepts under discussion will extend currentstrategies, others will denote some bold changes.

In addition, these results should stimulate considerablediscussion among a company’s supply leadership andother executives about supply strategy choices andwhere best to invest in supply and across the company.The findings should also help supply executives decidewhere to make their next “bold moves” to improve theglobal competitiveness of the firm. We anticipate theresults of this study will provide supply leadership witha better understanding of the likely paths forward.

15CAPS Research

The overall purpose of this research initiative was todevelop an updated forecast for supply management inthe decade ahead. The goal was to build on the workdone in our 1998 study, updating it to reflect currentconditions and expected changes while expanding andextending participation to include greater globalcoverage.

The objective of the research was to find answers tothese questions:

• What external forces will have the greatest effecton business over the next ten years?

• How will business models change as a result ofthese forces?

• How will the mission, goals, performanceexpectations and strategies for supplymanagement change to support these newbusiness models?

Although the horizon for our projections and forecastsof the future is the next decade (2007-2017), theforecast is likely to be most accurate over the next fiveyears.

Research Participant Demographics

More than 260 companies representing North America,Europe, Latin America and Asia/Pacific participated inthe research. This included involvement by 113 supplymanagement executives who participated in meetingsand teleconferences with the research team, and 180company responses to the e-survey. (Many companiesparticipated in both.) About two-thirds of theparticipating companies came from manufacturingindustries, while the rest were from service industries.More detail on study participant demographics isavailable in Appendix B.

Research Methodology

The research team began by defining specific areas to beinvestigated. This resulted in an initial researchframework covering these topics:

• Forces of change — The marketplace andcompetitive forces most likely to impact acompany’s business model in the future

• Business models and strategies — The ways inwhich an organization’s overall business modeland various elements of business strategy couldchange in response to the forces of change

• Supply mission, goals and performanceexpectations — The roles and objectives thatsenior executives could assign to the supplyorganization in support of the future businessmodel and strategies

• Supply strategies, processes and enablers — Theapproaches that companies could use to achievethe future supply mission, goals and performanceexpectations

As a starting point for hypothesis development, theresearch team used this framework to create an initialset of predictions about the future of supply manage-ment. More than 50 supply executives participated insmall group breakout sessions at the CAPS ExecutiveRoundtable in March 2006, where they rated, discussedand debated the likelihood of the predictions and addedtheir own. Another 28 supply executives (primarilyfrom Western companies operating in China)contributed their ideas in a CAPS Executive Roundtablesession held in Shanghai in June 2006.

Based on the success of these sessions, the researchteam expanded its efforts to engage supply executives indirect dialog about the future. Throughout the springand summer of 2006, the research team conducted

Chapter 2 — Research Design andApproach

16 Succeeding in a Dynamic World: Supply Management in the Decade Ahead

several half-day in-person sessions with senior supplyexecutives in Atlanta, Chicago, Dallas, New York, Milan,Madrid, Amsterdam, São Paulo and Mexico City. Inadvance of these sessions, participants completed a briefsurvey that probed the importance of selected supplystrategies, and the degree of implementation currentlyand in five years. The survey also asked about the degreeof impact expected in the next three to five years due toselect forces of change. During the sessions, the researchteam presented the survey results and led discussionson those areas with the highest scores as well as thosewhere scoring showed the greatest dispersion.

These in-person sessions were supplemented by a seriesof additional focus group sessions that the researchteam conducted via conference call and several one-on-one interviews with supply executives. All of thesediscussions provided further insight into their visions ofand concerns for the future.

In addition, several chief purchasing officers used theopportunity presented by the study to conduct separateinterviews with their companies’ chief executive officers.CEO findings were grouped into five major areas:

• Globalization and strategic importance• Risk management and supply continuity• Supply management strategies beyond price• Senior supply relationships• Capabilities and organization

While the CEO areas of concern matched up with thegeneral survey population and are discussed throughoutthe body of this report, their input is also elaboratedupon in Appendix A.

In parallel with these discussions, the research teamdeveloped and deployed a comprehensive e-survey (seeAppendix C) that provided a statistical base of dataabout the following:

• To what degree will a range of marketplace andcompetitive forces impact the company’s businessmodel?

• How important will various business strategies beto the future success of the company’s businessmodel?

• How important will various elements of supplymission, goals and performance expectations betoward supporting the company’s future businessmodel?

• How important will each of more than 100 supplystrategies, processes and enablers be for achievingthe future supply mission, goals and performanceexpectations? To what degree are these alreadyimplemented?

• What is the expected magnitude/direction ofchange in key indicators of supply strategy, suchas the use of particular geographic supply marketsand size of the supply base?

The research team carefully analyzed focus grouptranscripts and interview notes, both via manual reviewand text-mining software, to uncover themes andconnections. In parallel, the team explored the surveydatabase for supporting information and new themes.From these analyses, the research team identified thekey drivers of change — major external forces,changing business models and new expectations forsupply management — that lie ahead. Further, the teamidentified seven critical success factors for future successin supply management. Figure 2.1 illustrates therelationship between these drivers and the successfactors.

As a final part of the research, the research teampresented preliminary study results at the March 2007CAPS Executive Roundtable, conductedreview/feedback sessions in April 2007 with seniorsupply executives in Atlanta, Dallas, Chicago andNewark, and previewed the final report executivesummary at the 2007 Institute for Supply ManagementInternational Conference in May 2007. These stepsenabled the team to test its findings and conclusionsabout the drivers and success factors, to verify theirrelevance to supply executives and to sharpen themessages contained in this report.

Report Structure

The remainder of this report presents the results of theresearch study. Sections II and III parallel theframework depicted in Figure 2.1, while Section IVpresents overall conclusions and recommendations.

• Section II — How the Environment for SupplyManagement Will Change

•• Chapter 3 — Forces Driving Change•• Chapter 4 — Impacts on Business Models

and Strategies•• Chapter 5 — New and Expanded Missions,

Goals and Performance Expectations forSupply Management

• Section III — How Supply Management StrategiesWill Change

•• Chapter 6 — Overview: Seven KeyStrategies for the Coming Decade

•• Chapter 7 — Developing CategoryStrategies

•• Chapter 8 — Developing and ManagingSuppliers

17CAPS Research

•• Chapter 9 — Designing and OperatingMultiple Supply Networks

o Chapter 10 — Leveraging TechnologyEnablers

o Chapter 11 — Collaborating Internally andExternally

o Chapter 12 — Attracting and RetainingSupply Management Talent

o Chapter 13 — Managing and Enabling theSupply Management Organization

• Section IV — Conclusions and Recommendationso Chapter 14 — Research Summary and

Potential Supply Challenges for the DecadeAhead

o Chapter 15 — Recommendations• Appendixes

o A — CEO Survey Resultso B — Study Participant Demographic Profileso C — E-Survey Questionnaireo D — Analysis Strategy and Results of

Detailed Analyses

18 Succeeding in a Dynamic World: Supply Management in the Decade Ahead

Figure 2.1: Research Framework

Critical Success Factors

Addressing the forces of change

Managing and enabling the future

SM organization

Developing category strategies

Developing and managing

suppliers

Designing and operating multiple

supply networksLeveraging technology

enablers

Collaborating internally and

externally

Attracting and retaining supply

management talent

Adapting business models

and strategies

External and organizational drivers

Expanding the mission, goals and

performance expectations

Section II — How the Environment forSupply Management Will Change

19CAPS Research

A multitude of external forces will reshape markets,products, industries and competition over the course ofthe next decade. To survive, companies will have torethink and revamp their business strategies in order toanticipate, react to and even take advantage of theseforces.

The research team relied on previous work done by A.T.Kearney, as reported in the book World Out of Balance,1

to identify the important external forces at a macrolevel. This work identified six external forces that will,without question, impact companies and their strategiesin the coming decade. These external forces are:

• Globalization of the world economy• Demographics• Changing consumer demand• Natural resources and environmental pressures• Regulation and activism• Technology

In addition, seven “wildcard” forces were identified that,while not certain to occur, may well require companiesto adjust their strategies. These wildcard forces are:

• Global epidemic• Military conflict• Country disintegration• New protectionism• Terrorist resurgence• Hacker Hell• Quantum leap

This report will focus on a subset of these forces thatwere identified by the supply managers whoparticipated in our research, either through discussions

or the e-survey, as particularly important to them. Thereader is invited to refer to World Out of Balance formore discussion and detail of the other external forces.

Survey Results

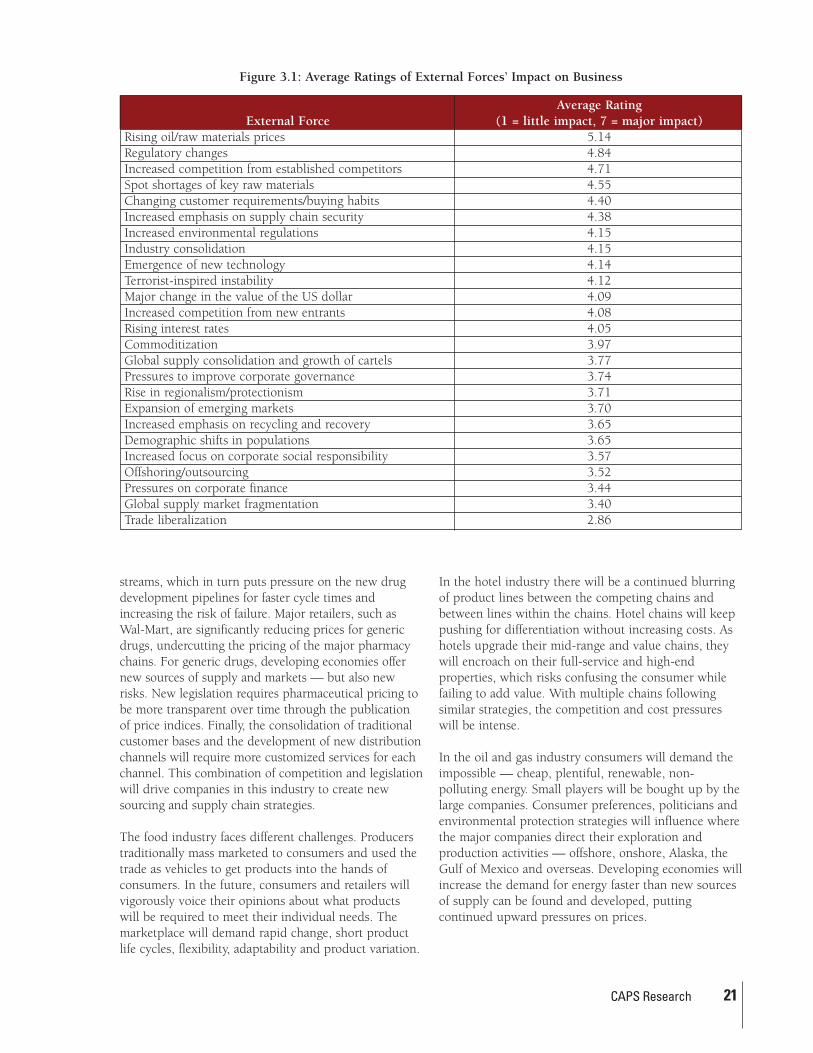

The survey asked the respondents to rate the impact of20 specific external forces on their businesses, as shownin Figure 3.1. The qualitative data generally supportedthe importance of these forces. Specific forces arediscussed below.

Complex Interactions Between Forces

Uncertainty, instability, and material shortages createmultiple axes of change. Forces that may appearinnocuous when looked at individually have a muchmore dramatic and hard-to-predict effect whencombined. Time to market, proliferation of newproducts, shorter life cycles, supply base consolidation,new competitors, pressure to reduce costs and increasequality, and environmental and socially responsibilityforces create a complex and competitive businessenvironment. This can lead to a condition in whichbusinesses are optimized for the past but do notunderstand enough about the future. At a high level,these forces and complex interactions are ubiquitous inthe business community. At the industry level, they takeon more specific forms and directions.

For example, in the health care sector the pharmaceuticalsupply chain is fundamentally changing. Several large-scale branded drugs are moving to generic formulations,cutting into their originating companies’ revenue

Chapter 3 — Forces Driving Change

20 Succeeding in a Dynamic World: Supply Management in the Decade Ahead

1Laudicina, Paul. World Out of Balance. New York: McGraw-Hill, 2005.

streams, which in turn puts pressure on the new drugdevelopment pipelines for faster cycle times andincreasing the risk of failure. Major retailers, such asWal-Mart, are significantly reducing prices for genericdrugs, undercutting the pricing of the major pharmacychains. For generic drugs, developing economies offernew sources of supply and markets — but also newrisks. New legislation requires pharmaceutical pricing tobe more transparent over time through the publicationof price indices. Finally, the consolidation of traditionalcustomer bases and the development of new distributionchannels will require more customized services for eachchannel. This combination of competition and legislationwill drive companies in this industry to create newsourcing and supply chain strategies.

The food industry faces different challenges. Producerstraditionally mass marketed to consumers and used thetrade as vehicles to get products into the hands ofconsumers. In the future, consumers and retailers willvigorously voice their opinions about what productswill be required to meet their individual needs. Themarketplace will demand rapid change, short productlife cycles, flexibility, adaptability and product variation.

In the hotel industry there will be a continued blurringof product lines between the competing chains andbetween lines within the chains. Hotel chains will keeppushing for differentiation without increasing costs. Ashotels upgrade their mid-range and value chains, theywill encroach on their full-service and high-endproperties, which risks confusing the consumer whilefailing to add value. With multiple chains followingsimilar strategies, the competition and cost pressureswill be intense.

In the oil and gas industry consumers will demand theimpossible — cheap, plentiful, renewable, non-polluting energy. Small players will be bought up by thelarge companies. Consumer preferences, politicians andenvironmental protection strategies will influence wherethe major companies direct their exploration andproduction activities — offshore, onshore, Alaska, theGulf of Mexico and overseas. Developing economies willincrease the demand for energy faster than new sourcesof supply can be found and developed, puttingcontinued upward pressures on prices.

21CAPS Research

Figure 3.1: Average Ratings of External Forces’ Impact on Business

Average RatingExternal Force (1 = little impact, 7 = major impact)

Rising oil/raw materials prices 5.14Regulatory changes 4.84Increased competition from established competitors 4.71Spot shortages of key raw materials 4.55Changing customer requirements/buying habits 4.40Increased emphasis on supply chain security 4.38Increased environmental regulations 4.15Industry consolidation 4.15Emergence of new technology 4.14Terrorist-inspired instability 4.12Major change in the value of the US dollar 4.09Increased competition from new entrants 4.08Rising interest rates 4.05Commoditization 3.97Global supply consolidation and growth of cartels 3.77Pressures to improve corporate governance 3.74Rise in regionalism/protectionism 3.71Expansion of emerging markets 3.70Increased emphasis on recycling and recovery 3.65Demographic shifts in populations 3.65Increased focus on corporate social responsibility 3.57Offshoring/outsourcing 3.52Pressures on corporate finance 3.44Global supply market fragmentation 3.40Trade liberalization 2.86

As the above examples illustrate, supply managers willneed to examine the specific forces at work in their ownindustry sectors before formulating strategies.

What Supply Managers Foresee

Analysis of the responses from supply managersindicates that several forces will have a major impact oncompany and supply management strategies across allindustry sectors in the next decade, including:

• Global competition• Mergers, acquisitions and supply market

consolidation• Increased governmental regulation• Technology advances• Customer and channel dynamics• Increased product variety and shorter life cycles• Social responsibilities• Environmental responsibilities

The following discussion examines these forces andtheir ramifications for supply in greater detail.

Global CompetitionThe impact of China on the world economy willcontinue to be enormous over the next ten years. Toprosper, and perhaps even simply to survive, companiesmust embrace China both as a market and a source ofsupply for their goods and services. And while China isexpected to have the largest impact, other developingeconomies — including India, Brazil, Eastern Europeand Russia — will also make their mark in the globalmarketplace.

The “gravitational pull” of China will impact mostcompanies and markets. As it continues to modernizeand urbanize, China will consume an increasing shareof the world’s raw materials, driving up prices and/orcreating shortages. Steel, specialty metals and energywill be particularly impacted by demand from Chinaand other emerging markets.

This pull may have a particularly large impact on Africa,where China and other nations are actively seeking newsources of raw materials. Additionally, companies mayfinally start considering Africa as a source of low-costlabor for manufacturing operations. This latterdevelopment will largely depend on whether Africannations can reach a reasonable level of political stability.

The growth of China as a supply and demand marketwill create opportunities for all competitors. Those thatembrace the China opportunities will create profoundadvantages over those that do not. And it is not just the

low labor costs that will be important. Enormousintellectual capital exists in China that can be tapped forinvention, innovation and new technology. China willalso come to be a significant source of managementtalent in the next decade.

Emerging players are clearly weighing heavily onpurchasing executives’ minds, as our study participantsmade clear:

China makes everything else dwarf into insignificancein relationship to the impact that it is going to haveover the next ten years. Just when I start to think Iunderstand the cost structure of Chinese companies, Ilearn more that tells me I really don’t understand it.

We’re dealing with the whole new set of competitors inour particular business. The Asians, and the Koreansin particular, have competitors today that five yearsago weren’t on the radar screen.

China will also be a target for much capital investmentand will capture the attention of suppliers from aroundthe world. Companies in developed economies may findit increasingly difficult to get the attention of traditionalsuppliers that see China as a more lucrative market, asone study participant noted:

It’s increasingly difficult to keep suppliers’ attention. Inthe utilities’ transmission and distribution sector, Italywill invest € 8 billion in the next 10 years; China willinvest € 115 billion

Looking beyond China, other developing countries willcontinue to emerge as attractive supply sources andgrow as bases for new companies that will be significantplayers in the world economy. Already, Gazprom fromRussia, Cemex from Mexico, Tata Motors from Indiaand Koc Holdings from Turkey are major globalcompanies. Additionally, suppliers in these economiesthat currently sell through established distributionchannels to reach the markets of developed economieswill learn how to distribute, market, finance and createtheir own distribution channels to these markets. Thiswill result in significant distermediation of existingsupply chains throughout the next decade.

Mergers, Acquisitions and Supply MarketConsolidationsTo meet this onslaught of new competition, companiesheadquartered in developed economies will need toincrease in size, with improved economies of scale andmarket power on both the supply and sell sides, tosurvive. Thus, in order to successfully compete, manycompanies will be forced to merge and consolidate.

22 Succeeding in a Dynamic World: Supply Management in the Decade Ahead

Mergers, acquisitions and consolidation amongcompetitors, suppliers and customers will requireboards of directors and top executives to carefullyconsider the potential impact on supply chains andrelated risks. An untimely merger could put a strategicsupplier in the hands of a fierce competitor, leavingonly less desirable suppliers available as tradingpartners. Of course, all concerned can play this game,and a company could opt to acquire a competitor’s keysupplier in order to gain competitive advantage.Consolidation is clearly on the mind of purchasingexecutives:

Some of our domestic competitors are waving thewhite flag and going away, and so we are entering intoa second wave of consolidation in our overall industry.

As the merger-and-acquisition game plays out, supplymanagement will be tasked with assessing the impacton the supply chain, including costs, risks andopportunities. As companies merge or are acquired, theacquisition price is often driven by forecasted synergieson the supply side. Thus, supply management will needto understand the new supply base, how it can be usedto gain advantage and how to find the forecasted costsavings. At the same time, supply management will beasked to produce many of the cost savings to supportthe mergers and acquisitions. The promised economiesof scale will have to be delivered, along with creativeways of taking out costs from the supply chain.

As the supply base consolidates, the balance of powerbetween buyers and sellers will shift, at leasttemporarily, in favor of the supplier. Buyers will have tofind creative ways to avoid the price increases thatnewly empowered suppliers may try to implement.

Consolidation of prime contractors and a major supplybase consolidation will occur in many industries,including aerospace, automotive and financial services.In a consolidating industry, the role of supply manage-ment changes. For example, a company can be sourcingand building a strategic relationship with a supplier thatis unexpectedly acquired by a company with which thebuying company has traditionally had a poor relation-ship. The buying company must then change suppliersor try to improve the relationship with the newlyconsolidated entity.

Other consolidation plays may include gaining access tothe potential acquiree’s supply base. These types ofboard-level decisions will require input from supplymanagement. Supply management must know whichsupplier will be in the best position to provideparticular technologies. Paying a premium for anacquisition can better position the company with

respect to a technology and at the same time block ordelay a competitive company from gaining access to thenew technology.

Oligopolies created by supplier consolidation shiftpower in the marketplace, diminishing customerbargaining power and creating a major threat for buyingcompanies. This power shift has already happened inthe steel and chemical industries in Brazil and otherLatin American countries.

Some companies pursuing a growth strategy focusstrongly on mergers and acquisitions. These companiesmust ensure that they have the right processes in placeto evaluate the potential partners and the synergiesachievable in the new supply chains, including costsavings, risks and liabilities. As one study participantcommented:

We look to the supply chain to be able to help usunderstand the companies that are potentialacquisition targets for us, what is their supply chain.When we acquire somebody, if we know that we canleverage the volumes that they already have or withpeople who we already have great contracts with orgreat deals with, then those instantly flow through thefinancial synergies and the acquisition becomes moreattractive. At that point, we are generally willing topay perhaps a little bit more to make sure that we canget that acquisition or at least we go into it with eyeswide open, knowing what we think the completeintegrated and acquired value would be for us.

Increased Governmental RegulationIn the coming decade government legislation andregulation of business will increase, requiringcompanies to dedicate significant resources to ensurecompliance. This will be especially true in the U.S. andthe European Union. Homeland Security rules will forcecloser scrutiny of suppliers, and privacy rules willrequire closer monitoring of contract discussions. In theU.S., the Sarbanes-Oxley Act will create the incentivefor companies to give supply management the authorityto work closely with finance in order to manage allcorporate spending.

Privacy legislation and regulations will mean thatsignificant time will be dedicated to discussing theseissues when constructing contracts. Any time thatcustomer information is sent outside the company,legislation regulates what has to be done to protect theprivacy of the customers. Government regulationsrequire that new suppliers be subject to backgroundchecks for terrorist activities. If a company is usingmany new suppliers or doing new business with asignificant number of different suppliers, it will need

23CAPS Research

processes and procedures to handle the backgroundchecks.

Governmental activity is weighing heavily on supply, asone study respondent indicated:

We have an enormous number of regulatory issuesthat are creating a nightmare in terms of how weoperate and fly in the face of what seemingly would begood business practices (e.g., whether it’s how wehedge materials or how we account for things or howwe deal with the government around importing, howwe deal with safety and security issues). Thegovernment clearly does not understand theramifications of what they’re declaring and it’s just anabsolute nightmare.

In addition to regulation, government actions tosupport economic development, such as tax incentivesand trade restrictions, will have a large impact onsupply strategies. Political instability could changesituations overnight and require a rapid change insupply strategies.

Technology AdvancesIn many industries, technology breakthroughs willcause major changes to how products and services areprovided. These changes may require capitalinvestment, but will lower the customer’s total cost ofownership. In many industries, core technologies willeventually be commoditized, forcing geographicconsolidation and concentration of the supply base andfundamentally affecting supply chain structure andrelationships. Increased competition for, and someshortages of, key raw materials will lead to technologychanges and the use of other materials. For example,plastic bottles may not be cost effective when oil reaches$100 a barrel, which will bring about the need for newpackaging technology. This type of change is alreadycoming to light, according to one study participant:

Supply chain disintegration will be a major change.For example, in the television business 20-30 yearsago you had huge glass factories, made tubes andassembled everything in-house. Now, for flat panelsthe supply base is in Korea, Japan and Taiwan, whichmakes all the panels for all places in the world and allsuppliers in the world. Consumer product companiesdon’t differentiate on any kind of industrial technologyanymore but compete only on the features, thesoftware and some additions to the core of the product.

Customer and Channel DynamicsIn some industries, the downstream supply chain willchange rapidly due to economics and governmentpolicies. Consider pharmaceuticals, where there is a

significant amount of volume shifting away fromindependent pharmacies and moving toward the largerchains of drug and general merchandise stores includingCVS, Walgreen’s and Wal-Mart. At the same time, thewhole healthcare experience in the United States ischanging as the government comes to pick up more andmore of the bill. The government will force more valueand integration in the supply chain, specifically aroundelectronic health records, data sharing and security ofpatient records. The supply chain will need tocustomize services and value to the various channels,including hospitals, traditional clinics and theincreasing number of retail clinics. The flow of dollarsand information will become much more valuable inchannel management than the flow of products.

Within other industries (e.g., airlines and aircraftmanufacturers), supply chain dynamics will beinfluenced by the poor financial condition of majortrading partners in the chain. This performance willreverberate up and down the chain, alteringrelationships and causing suppliers to seek othercustomers and/or sources of revenue.

The impact of private equity firms will also besignificant. Many companies and suppliers have alreadybeen bought and taken private by these companies. Inlooking to recoup their investments, the private equityfirms will generally slash costs, raise prices and changebusiness relationships with their trading partners,affecting supply and supply chain strategies.

Increased Product Variety and Shorter ProductLifecyclesVariety will take several forms, including more models,brands, and products tailored to different geographiesand price points. For example, the market size for anyparticular consumer food product will continue toshrink as more and more varieties are made available,forcing more emphasis on quickly getting in and outof new and unique flavors. Consumer tastes inemerging economies will be new and different fromtraditional markets, necessitating new products andnew distribution channels. Traditional lines ofcompetition will blur as companies try new productsand markets and engage new suppliers from newindustries.

Social ResponsibilitiesCompanies in developed economies will be held to highstandards wherever they do business in the world.Shareholder proposals related to social concerns willcontinue to be brought forth, requiring companies tomonitor working conditions in their supply chains allthe way back to basic extractive and farming practices.Supply management will be tasked with working with

24 Succeeding in a Dynamic World: Supply Management in the Decade Ahead

the supply base to ensure that it meets environmentalstandards.

As companies consolidate their supply bases to becomemore competitive, their commitments to a diversified(i.e., women- and minority-owned businesses) supplybase will come under pressure. Many diversifiedsuppliers are positioned in the long tail of those small-sized suppliers that will be cut from the supply base.Furthermore, it will be difficult to grow expenditureswith those that survive the supply base rationalization.To maintain their commitments, companies will rethinktheir strategies in this area. New approaches will includeinvestment in the companies, either directly or byhelping to secure outside financing, allowing thediversified suppliers to grow and better compete in theglobal marketplace. Other strategies will be to sharegood practices with them to strengthen their businessand to help them find new customers. Ultimately,companies will find ways to keep their commitments todisadvantaged suppliers, as one study participant noted:

A couple of things we’ve tried to do in the supplierdiversity space is really try to put a little less emphasison the dollars we spend and a little more emphasis onhow we can help minority businesses to grow theirbusiness.

Environmental ResponsibilitiesEnvironmental concerns will continue to increase on aworldwide basis as the interrelationships amongindustrial activity in various regions of the world cometo be better recognized and understood. Customers,consumers, shareholders, non-government organizationsand governmental bodies will all increase their scrutinyof corporate environmental practices in all regions ofthe world and demand that companies take environ-mentally friendly actions by doing things like using lesspackaging material, reducing carbon emissions andmaking products that can be readily recycled.Companies will be forced to meet the environmentalexpectations of the general populace.

Environmental issues will ultimately become brand-related issues and influence how companies are viewedin the marketplace. Information on the environmentalimpact of both purchased and sold products will bereadily available to consumers and impact their buyingdecisions. Retailers will be increasingly conscious ofenvironmental-sustainability issues and will give veryspecific goals to their suppliers, such as taking out somespecific amount of packaging over a defined timeframe.They will not put products on the shelf if the productsare not in compliance with their customers’environmental expectations, as several of our studyparticipants commented:

We are starting to get a lot more scrutiny aroundenvironmental concerns, particularly being a retailerwith catalogs. The interest is on the type of forests weuse for the paper products we use for catalogs,recycled content, and all those kinds of things.

The government, as a customer, is involved in greenprocurement. We had to drive green down all the wayto our office supply buying.

Companies will develop and publish “green statements”that declare their intentions to be environmentallyresponsible. Legislation and regulation will drive someof this behavior, but other action will be influenced bythe costs and benefits. Some of the benefits come frompositive public perception or the avoidance of negativepublicity. To meet these commitments, companies willput together cross-functional teams with executiveleadership to monitor environmental concerns in theextended supply base.