sudarshan kr viva

TRANSCRIPT

8/6/2019 Sudarshan Kr Viva

http://slidepdf.com/reader/full/sudarshan-kr-viva 1/17

µA STUDY ON CREDIT

RISK MANGEMENT¶

SUDARSHAN K R1PT09MBA09

KARNATAKA STATE

FINANCIAL CORPORATION

INTERNAL GUIDE

Prof. NAGARAJ

SENOY

EXTERNAL GUIDE

Mr. M.A. MURTHY

(AGM dept of BD &CR)

8/6/2019 Sudarshan Kr Viva

http://slidepdf.com/reader/full/sudarshan-kr-viva 2/17

COMPANY PROFILE

Background and Inception of the Company

� Established by the state government in theyear of 1959 under the SFC Act 1951 withauthorized capital of Rs. 2 crores

� prior to November 1st

1973 were known asMYSORE STATE FINANCIALCORPORATION

� Since inception KSFC has assisted more than1.60 lakh units with cumulative sanction of more than Rs.9102 crore out of which about

than 50% towards SMEs� start up assistance to industries such asInfosys, Biocon & MTR, which are today Indiabrand ambassadors

8/6/2019 Sudarshan Kr Viva

http://slidepdf.com/reader/full/sudarshan-kr-viva 3/17

PRODUCT PROFILE

� CORPORATE LOAN SCHEME

� NATIONAL EQUITY FUND SCHEME

� HIRE PURCHASE

� NON-CONVERTIBLE DEBENTURE

� FOREIGN LETTER OF CREDIT (FLC)

� CREDIT LINKED CAPITAL SUBSIDY

SCHEME (CLCSS)

8/6/2019 Sudarshan Kr Viva

http://slidepdf.com/reader/full/sudarshan-kr-viva 4/17

MCKINSEY¶S 7S MODEL

STRATEGY:

� KSFC believes its employees are greatest

assets to the corporation so retaining the

talent heads to avoid competition fromprivate institutions is their main strategy

STRUCTURE: Hierarchical structure

SYSTEM: integrated system by MIS

SKILLS� Highly qualified professionals in the

company have major skills like technical,

finance, economical, marketing, and public

skill.

8/6/2019 Sudarshan Kr Viva

http://slidepdf.com/reader/full/sudarshan-kr-viva 5/17

MCKINSEY¶S 7S MODEL

STAFF

� There are about 38 branches in whichaltogether there are 1281 employees in thecorporation, out of them 408 are class A-

Officers, 703 Class B- Assistance and clericalstaff and 170 are Class C-other subordinatestaff.

STYLE

� Top down and bottom up

� Participative styleSHARED VALUES

� The value that the company upholds most is³Customer¶s Satisfaction´

8/6/2019 Sudarshan Kr Viva

http://slidepdf.com/reader/full/sudarshan-kr-viva 6/17

SWOT ANALYSIS

STRENGTHS:

� presence of highly expertise people

� Public sector

� Network: KSFC has its branch in alldistricts of Karnataka gives it strength to

access to reach every nook and corner

WEAKNESSES

� Comparatively higher interest rates.� long procedure in case of certain

schemes.

� system followed in KSFC is out dated.

8/6/2019 Sudarshan Kr Viva

http://slidepdf.com/reader/full/sudarshan-kr-viva 7/17

SWOT ANALYSIS

OPPORTUNITIES

� Development of infrastructure

� Department of credit research

� Websites« online Advertisements

THREATS

� Commercial banks

� IDBI, SIDBI, co-operative banks are

gearing up for term loan financing toSME¶s

8/6/2019 Sudarshan Kr Viva

http://slidepdf.com/reader/full/sudarshan-kr-viva 8/17

OBJECTIVES OF PROJECT

� To study the various credit risk parameters

used at KSFC.

� To analyze the scoring given to the various

parameters.� To assess the effectiveness of these risk

management activities and suggest

improvements for the same.

8/6/2019 Sudarshan Kr Viva

http://slidepdf.com/reader/full/sudarshan-kr-viva 9/17

Reseach methodology

� STATEMENT OF PROBLEM: The lending

parameters used by SFC¶s are traditional

and they are need to be revised to

formulate new techniques

� Type of data: secondary historical data

collected from annual reports and journals

released by the corporation

� Scope of study: restricted only to head

office

8/6/2019 Sudarshan Kr Viva

http://slidepdf.com/reader/full/sudarshan-kr-viva 10/17

Limitations

� The collection of data for analysis is

restricted to KSFC Head Office only.

� The study is limited to a single

organization and there is no competitionwith another company.

� The results of the study are based on the

assumption that all the information

provided is correct.

� In depth analysis could not be done due to

time constraint

8/6/2019 Sudarshan Kr Viva

http://slidepdf.com/reader/full/sudarshan-kr-viva 11/17

Credit rating models

Model-A Applicable for units with loans below Rs.25.00 lakhs

(both new and existing units)

Model-B Applicable for existing units with loans aggregatingmore than Rs.25.00 lakhs and Rs.75.00 lakhs (existing

units)

Model-C Applicable to new units with loans aggregating more

than Rs.25.00 lakhs (new units)

Model-D Applicable for existing units with loans aggregating to

Rs.75.00 lakhs and above (existing units)

8/6/2019 Sudarshan Kr Viva

http://slidepdf.com/reader/full/sudarshan-kr-viva 12/17

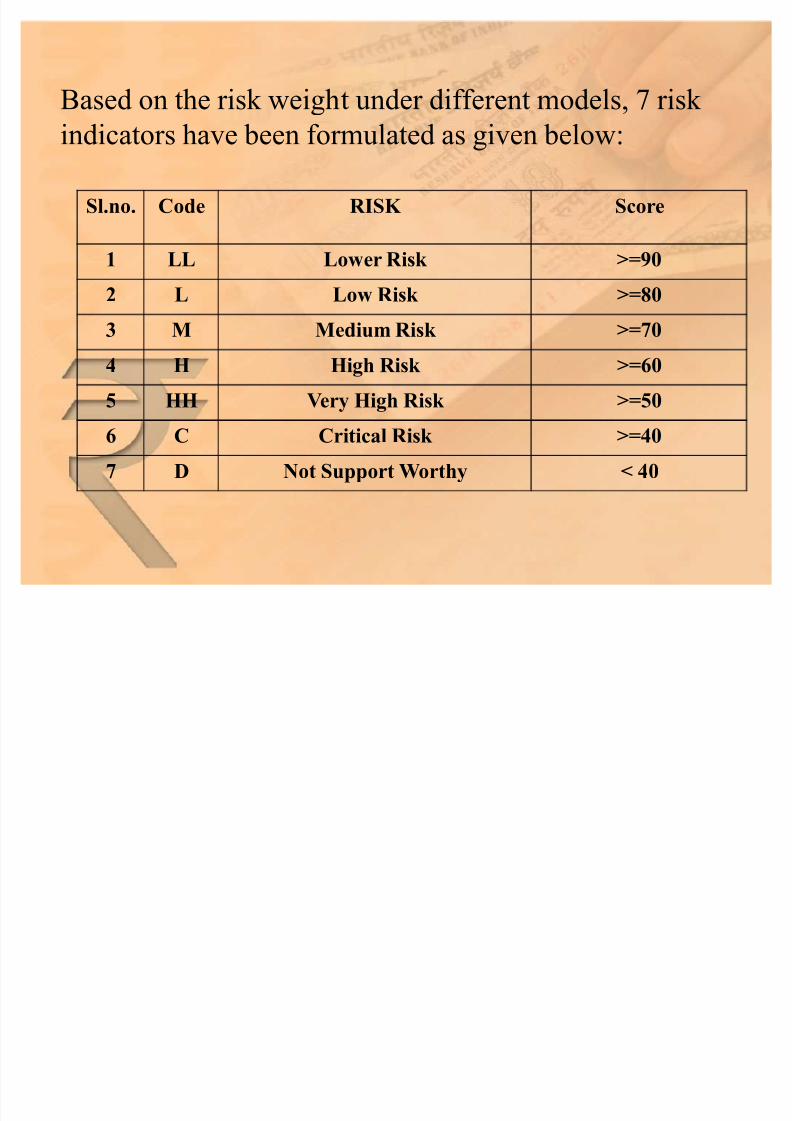

Based on the risk weight under different models, 7 risk

indicators have been formulated as given below:

Sl.no. Code RISK Score

1 LL Lower Risk >=90

2 L Low Risk >=80

3 M Medium Risk >=70

4 H High Risk >=60

5 HH Very High Risk >=50

6 C Critical Risk >=40

7 D Not Support Worthy < 40

8/6/2019 Sudarshan Kr Viva

http://slidepdf.com/reader/full/sudarshan-kr-viva 13/17

CREDIT RISK PARAMETERS

� Current ratio

� PAT/net sales ratio

� Interest coverage ratio

� Return on capital employed� Networth

� Debt equity ratio

� Repayment period

� Average debt service coverage ratio

� Security Margin on Primary Security

� Ratio of Overall Security to OverallOutstandings

8/6/2019 Sudarshan Kr Viva

http://slidepdf.com/reader/full/sudarshan-kr-viva 14/17

FINDINGS

� Firms are awarded higher scores if their

financial ratios found to be higher and its

vice versa

� According to KSFC the collateral securityshould be high compared to the loan

outstanding to get the maximum mark.

� Larger the guarantee higher the marks it

may be personal or corporate

� Entrepreneurs experienced in the same

field for a long time to get the maximum

mark

8/6/2019 Sudarshan Kr Viva

http://slidepdf.com/reader/full/sudarshan-kr-viva 15/17

� the firm will get the maximum marks if it is

going for diversification or modernization

� Finally a firm is to score minimum of 70 to

be eligible for the loan. If it is less then 70it is very difficult to get the loan

sanctioned.

8/6/2019 Sudarshan Kr Viva

http://slidepdf.com/reader/full/sudarshan-kr-viva 16/17

SUGGESTIONS

� KSFC should consider net cash accrual to totaldebt as a parameter

� Consider moving average

- in current ratio

- debt equity ratio

- return on capital employed� Consider vulnerability to macro-economic

environment as a parameter.

� Consider distribution network as a parameter

� Consider ability to manage change

� Consider integrity of the parameter � Consider past success in introducing new projects

� Consider CRISIL, ICRA and SMERA ratings

8/6/2019 Sudarshan Kr Viva

http://slidepdf.com/reader/full/sudarshan-kr-viva 17/17

CONCLUSION

Risk cannot be avoided always but as far

as possible measures should be taken to

reduce the risk. The Credit Risk

Department at KSFC does a good job in

managing the risk of the organization. But

there is always scope for improvement and

several suggestions have been made so

that the organization can do what it seems

best for it.