sumit k singhsumitsingh.yolasite.com/resources/indian automotive industry...maruti 18.26 25.58 22.93...

TRANSCRIPT

Sumit K Singh

IntroductionWhy automotive industry?

The industry has seen tremendous growth over last 5 years

Highly sensitive to demand and can be affected by external factors

Capital intensive industry

What are we doing?

Analyzing the financial ratios, financial statements to gauge the

health of three different companies

Sumit K Singh

Sumit K Singh

Liquidity Measurement Ratio

Ind. Ave. FY2009 FY2008 FY2007 FY2006 FY2005

Maruti 0.87 1.14 0.91 1.40 1.77 1.67

Tata 0.56 0.65 0.86 1.07 0.98

M&M 0.90 0.86 1.31 1.21 1.10

Current Ratio

Ind. Ave. FY2009 FY2008 FY2007 FY2006 Fy2005

Maruti 0.77 0.98 0.66 1.13 1.31 1.25

Tata 0.49 0.66 0.92 0.97 0.76

M&M 0.83 0.74 1.01 0.84 0.79

Quick Ratio

Sumit K Singh

Profitability Indicator Ratio

Ind. Ave. Fy2009 FY2008 FY2007 FY2006 FY2005

Maruti 5.20% 5.68% 9.34% 10.29% 9.53% 7.57%

Tata 3.90% 6.96% 6.94% 7.35% 7.02%

M&M 6.22% 9.45% 10.34% 10.28% 7.565

Net Profit Margin

Ind. Ave. FY2009 FY2008 FY2007 FY2006 Fy2005

Maruti 8.67% 11.95% 18.58% 20.87% 21.52% 18.21%

Tata 4.79% 14.37% 17.59% 18.04% 18.72%

M&M 9.00% 15.91% 20.59% 22.60% 16.73%

Return on Assets

Ind. Ave. FY2009 FY2008 Fy2007 Fy2006 Fy2005

Maruti 13.78% 17.31% 20.56% 22.79% 21.81% 19.49%

Tata 8.19% 25.98% 27.96% 27.74% 30.09%

M&M 16.03% 25.51% 30.18% 29.60% 25.66%

Return of Equity

Sumit K Singh

Debt Ratio

Ind. Ave. FY2009 Fy2008 Fy2007 Fy2006 Fy2005

Maruti 31.55% 6.85% 10.00% 8.00% 1.29% 6.56%

Tata 49.82% 44.00% 36.00% 34.66% 37.77%

M&M 44.00% 37.00% 32.00% 23.20% 34.30%

Debt Ratio

Ind. Ave. Fy2009 Fy2008 Fy2007 FY2006 Fy2005

Maruti 16.26 33.86 40.93 60.01 90.62 36.56

Tata 2.60 6.28 7.19 7.62 8.64

M&M 8.25 14.64 67.24 32.17 23.85

Interest Coverage Ratio

Sumit K Singh

Operating Performance Ratio

Ind. Ave. FY2009 Fy2008 Fy2007 FY2006 FY2005

Maruti 1.51 1.99 1.94 1.98 2.21 2.36

Tata 1.01 2.06 2.49 2.40 2.63

M&M 1.46 1.64 1.92 2.16 2.17

Total Assets Turnover

Ind. Ave. FY2009 FY2008 FY2007 FY2006 FY2005

Maruti 18.26 25.58 22.93 21.27 14.15 16.90

Tata 12.82 14.43 11.02 10.32 10.99

M&M 14.60 12.49 11.75 9.48 8.92

Inventory Turnover

Sumit K Singh

Cash Flow Indicator Ratios

Ind. Ave. FY2009 Fy2008 Fy2007 Fy2006 Fy2005

Maruti 8.06% 7.87% 10.13% 13.69% 10.00% 9.70%

Tata 5.04% 21.40% 8.29% -1.10% 7.27%

M&M 12.42% 7.30% 11.70% 8.00% 5.75%

Operating Cash Flow-to-Sales Ratio

Ind. Ave Fy2009 Fy2008 FY2007 Fy2006 Fy2005

Maruti 23.00% 8.29% 9.78% 9.72% 9.69% 7.73%

Tata 28.80% 32.51% 35.34% 37.13% 41.68%

M&M 37.29% 29.10% 30.39% 32.45% 33.54%

Dividend Payout Ratio

Sumit K Singh

Investment Valuation Ratio

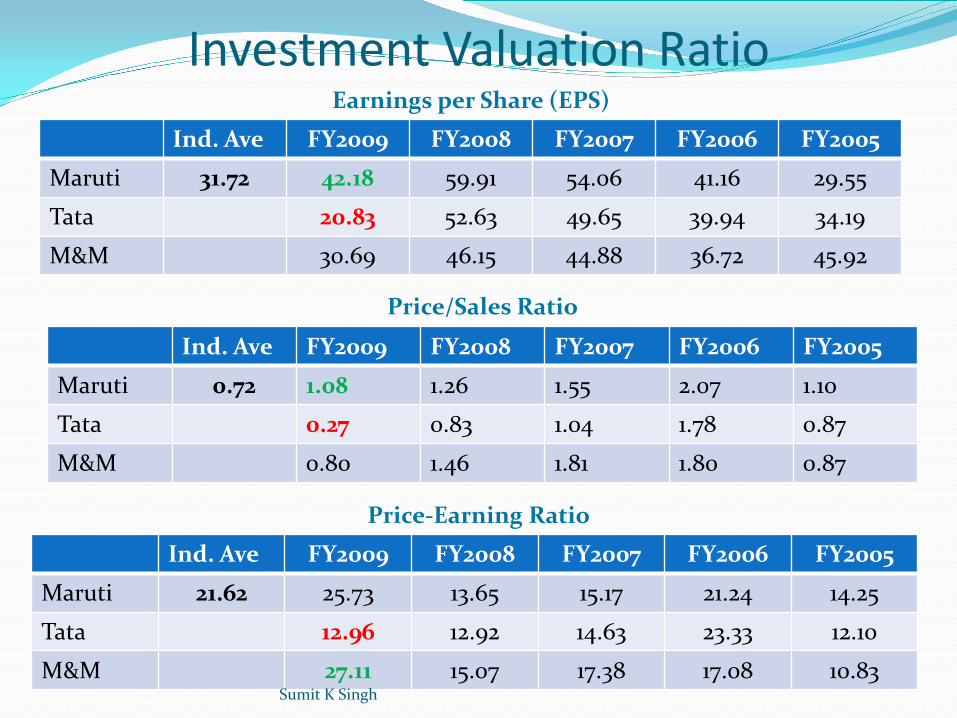

Ind. Ave FY2009 FY2008 FY2007 FY2006 FY2005

Maruti 31.72 42.18 59.91 54.06 41.16 29.55

Tata 20.83 52.63 49.65 39.94 34.19

M&M 30.69 46.15 44.88 36.72 45.92

Earnings per Share (EPS)

Ind. Ave FY2009 FY2008 FY2007 FY2006 FY2005

Maruti 0.72 1.08 1.26 1.55 2.07 1.10

Tata 0.27 0.83 1.04 1.78 0.87

M&M 0.80 1.46 1.81 1.80 0.87

Price/Sales Ratio

Ind. Ave FY2009 FY2008 FY2007 FY2006 FY2005

Maruti 21.62 25.73 13.65 15.17 21.24 14.25

Tata 12.96 12.92 14.63 23.33 12.10

M&M 27.11 15.07 17.38 17.08 10.83

Price-Earning Ratio

Sumit K Singh

Sumit K Singh

Trend Analysis

0.00

0.50

1.00

1.50

2.00

FY2005 FY2006 FY2007 FY2008

Liquidity ratios

CR

QR

0.00

5.00

10.00

15.00

20.00

25.00

FY2005 FY2006 FY2007 FY2008

Asset turnover

FA Turnover

TA Turnover

Inv Turnover

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

FY2005 FY2006 FY2007 FY2008

Leverage ratio

Debt Ratio

D/E Ratio

TIE

0.00%

10.00%

20.00%

30.00%

40.00%

FY05 FY06 FY07 FY08 FY09

Profitability ratios

Op Profit Margin

Net Profit Margin

ROA

ROE

BEP

Sumit K Singh

Trend Analysis

0

1

2

3

4

5

6

7

FY05 FY06 FY07 FY08 FY09

Investment valuation

EPS/10

Price/Book Value/10

PE Ratio/10

Price/Sales

Dividend Yield

Sumit K Singh

Sumit K Singh

Analysis –FY’04 to FY’08 Gradual increase in operating income over the years FY’08 operating income was 120% of that of FY’04

For FY’08 In FY ’08 Fixed asset turnover is 2.68( In FY’07---5.01) , Total asset turnover is 2.06 (relatively constant over 5 years) Current ratio has fallen to 0.65 from 0.86.

As Total asset turnover is constant, Current assets in terms of short term investments have fallen, investments in long terms assets have increased causing increase in total assets thereby causing decrease in ROA and Fixed asset turnover as assets have increased at higher rate than sales and net income

Factors causing negative impact Factors causing positive impactOther recurring income fell drastically to 389 crore against 887 crore in FY’07

Expenses capitalized was highest at -1,131 crore (reducing total expense)

Debt to equity ratio increased to 0.8 thus interest expense rose from 1.75% to 2%

Depreciation was lowest

Thus, due to higher interest and tax expense PAT was only 6.78% despite highest PBDIT

Quick ratio almost equal to current ratio at 0.66 and inventory turnover was highest at 14.63%

Sumit K Singh

For FY’07

Operating income was highest and had record growth of 32% YOY with operating income in FY’07 at 26,664 crore against 20,088 crore in FY’06

Factors causing negative impact Factors causing positive impactCost for material consumed was highest at 73.24% of operating income, more than in FY’08 which had comparative higher sales

Depreciating expenses was lowest

Declining other sources of income Improved recovery as write offs were 0.32% of operating income was better than that of previous years

Despite record YOY growth due to factors mentioned above, duel to factors mentioned above PAT was at 6.32% as compared to 6.78% in FY’06

Sumit K Singh

For FY’06

Adjusted PBDIT was 14.10% was highest

Factors causing negative impact Factors causing positive impactIncrease in dept financing caused interest expense to rise 1.74% of operating income highest over the years

Availability of cheap raw material-71.56% of operating

Higher Tax expense as compared to FY’05 and FY’07

Efficient operationsAdministrative expense lowest

Thus due to higher interest and tax expense PAT was only 6.78% despite highest PBDIT

Other recurring income was highest at 3.41% of operating income

Sumit K Singh

-1500

-1000

-500

0

500

1000

1500

2000

FY-04 FY-05 FY-06 FY-07 FY-08

PAT

Other source of income

Expense capitalization

0

0.2

0.4

0.6

0.8

1

1.2

1.4

FY-04 FY-05 FY-06 FY-07 FY-08

Debt to Equity

EPS normalised

Relation between PAT-Other source of income and expense capitalization

Relation between EPS and Debt to equity ratio

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

FY-04 FY-05 FY-06 FY-07 FY-08

SSGR

YOY growth

SSGR vs Growth rate

Sumit K Singh

Sumit K Singh

ROE and its decline: An analysis

2004 2005 2006 2007 2008

Sales/TA 1.31 1.35 1.24 1.09 0.93

NPM (%) 7.56 10.28 10.34 9.45 6.22

TA/CE 2.52 2.08 2.27 2.39 2.69

Sumit K Singh

DuPont Analysis

As observed, Net profit margin is reduced by a bigger margin

It can be concluded based on DuPont analysis that the decline in net profit margin (i.e. – operational efficiency) is a major contributor to the decline in ROE.

Sumit K Singh

Trend Analysis

86.50%87.00%87.50%88.00%88.50%89.00%89.50%90.00%90.50%91.00%91.50%92.00%

Mar ' 04 Mar ' 05 Mar ' 06 Mar ' 07 Mar ' 08

0%1%2%3%4%5%6%7%8%

Mar ' 04 Mar ' 05 Mar ' 06 Mar ' 07 Mar ' 08

0%

1%

2%

3%

4%

5%

6%

7%

8%

Mar ' 04 Mar ' 05 Mar ' 06 Mar ' 07 Mar ' 08

Expenses Financial Expenses

Administrative Expenses

Sumit K Singh

Altman Bankruptcy Prediction Model

Z 2004 2005 2006 2007 2008

Tata Motors 4.28 4.27 4.02 4.05 3.15

Maruti 3.39 3.68 4.10 4.01 3.68

M&M 3.32 3.35 3.13 2.56 2.13

Sumit K Singh

Conclusion

As per the analysis, Maruti Suzuki looks to be the best among the three in terms of financial risk

As per the FY2008 data and the annual report loss of 25 billion rupees, Tata motors shows signs of decline

M & M's operational inefficiencies are prime cause of concern for the company and a key driver for it to land into distress zone in Altman's prediction model

Sumit K Singh

Sumit K Singh