summer committee meetings. yoram bauman sightline institute

TRANSCRIPT

Summer Committee Meetings

Yoram BaumanSightline Institute

Carbon tax revenues Tax cuts0

1000

2000

3000

4000

5000

6000

Cumulative BC Carbon Tax Revenues and Tax Cuts 2008 – 2014

$5.0 Bn

$5.7 Bn

$ 3112 M Business Tax Cuts

$ 1221 M Personal Income Tax Cuts

$ 997 M Low Income Tax Credit

$ 108 M Other Personal Tax Cuts$ 221 M Rural/Northern Benefit

Source: BC Budgets 2008-2013

2007 2008 2009 2010 201194

96

98

100

102

104

106

Real GDP Growth Relative to 2007 (2007=100)

BC

Canada

Source: CANSIM 379-0025

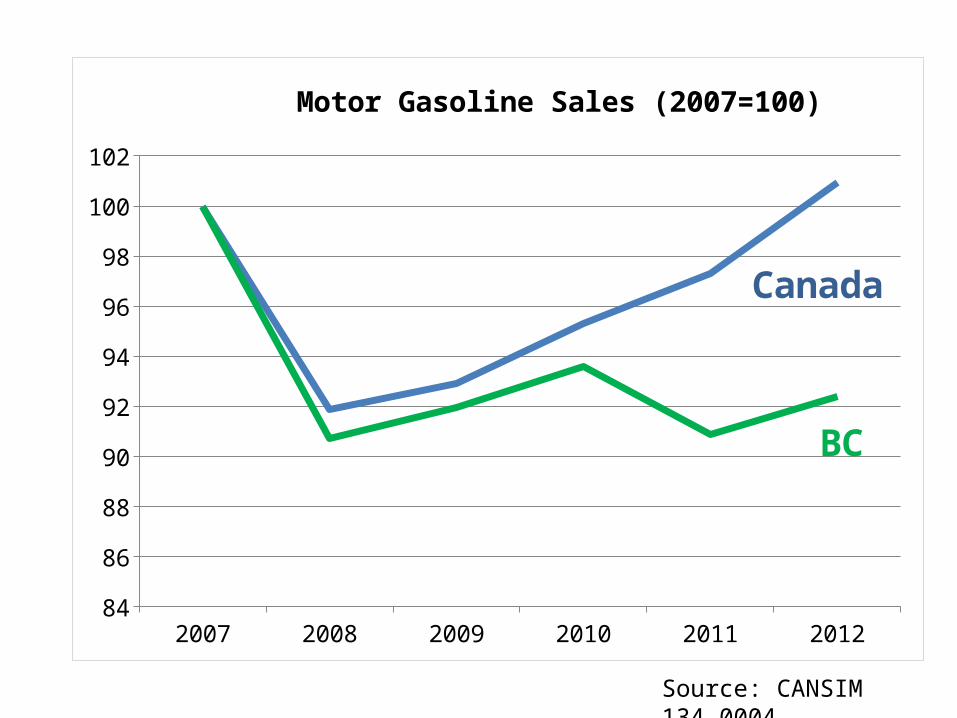

2007 2008 2009 2010 2011 201284

86

88

90

92

94

96

98

100

102

Motor Gasoline Sales (2007=100)

BC

Canada

Source: CANSIM 134-0004

Learning from the Regions

Learning from the Regions

Bruce BraineAmerican Electric Power

Comparison of Hypothetical U.S. CO2Cap and Trade vs. Tax

Bruce H. Braine

VP – Strategic Policy Analysis

NARUC Summer Committee Meetings

July 23, 2013

Background

Federal CO2 legislation very unlikely in next 3-5 years.

Obama Administration moving forward on CO2 regulations (e.g. utility NSPS on new and existing sources) BUT likely insufficient to meet long-term (post-2020) CO2 goals and NOT cost-effective.

If policymakers determine more long term CO2 reductions needed, federal legislation (either carbon tax or “cap and trade”) would be required.

How do these two approaches compare?

10

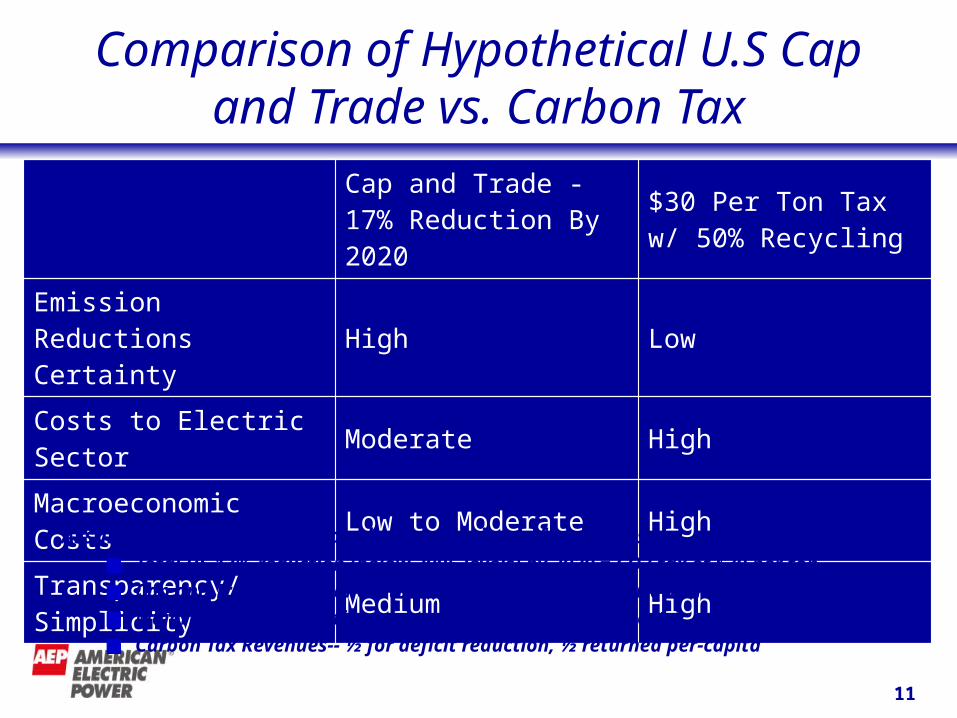

Comparison of Hypothetical U.S Cap and Trade vs. Carbon Tax

Cap and Trade - 17% Reduction By 2020

$30 Per Ton Tax w/ 50% Recycling

Emission Reductions Certainty High Low

Costs to Electric Sector Moderate High

Macroeconomic Costs Low to Moderate High

Transparency/Simplicity Medium High

11 11

Assumptions for ‘apples to apples’ comparison of programs:Total US 17% reduction (below 2005 levels) by 2020 = CO2 tax of $30 per ton

Cap and Trade w/ full allocation of allowances for electric utilities/customers

Majority of CO2 reductions come from/required from electric sector

Carbon Tax Revenues-- ½ for deficit reduction, ½ returned per-capita

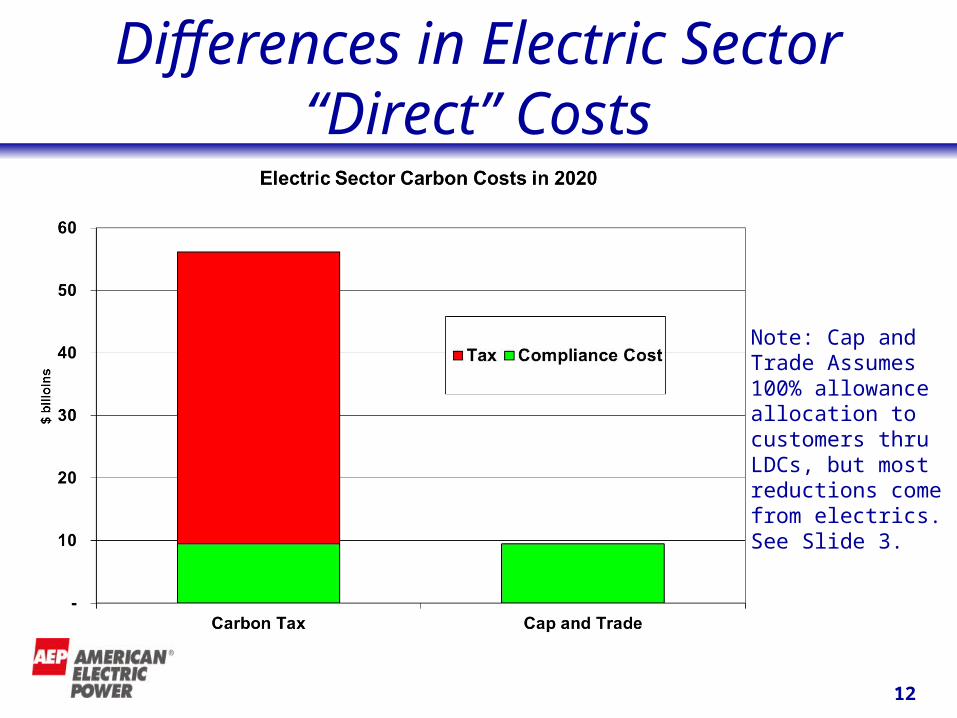

Differences in Electric Sector “Direct” Costs

12 12

Note: Cap and Trade Assumes 100% allowance allocation to customers thru LDCs, but most reductions come from electrics. See Slide 3.

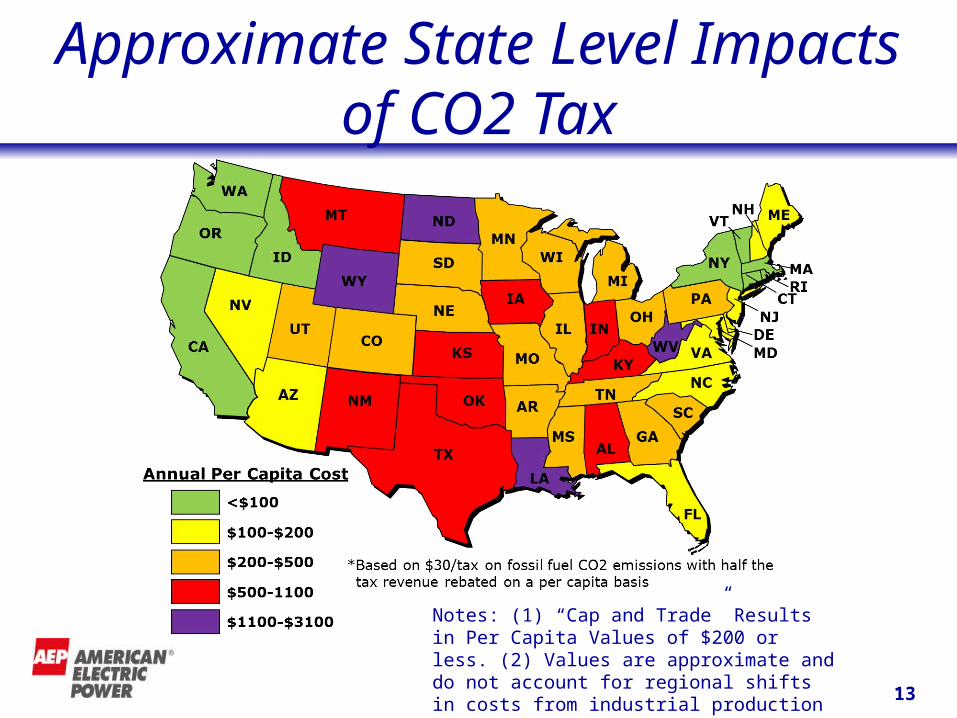

Approximate State Level Impacts of CO2 Tax

13 13

Notes: (1) “Cap and Trade” Results in Per Capita Values of $200 or less. (2) Values are approximate and do not account for regional shifts in costs from industrial production and/or exports.

Positive Track Record for Cap and Trade

U.S. Acid Rain Program European Union GHG ETS

14 14

Source: European Environmental Agency

Comparison of Other Forms of Cap and Trade and Taxes

Cap and Trade with Full Allocation results in a much smaller “negative” impact than Tax with 50% recycling on electricity consumers and overall US GDP and jobs.

However, Cap and Trade with 100% Auction and 50% recycling would have similarly large negative impacts as a Carbon Tax.

Carbon tax “could” be a net positive for the economy if MOST ALL of proceeds are used to reduce less efficient taxes (e.g. marginal income tax rates). BUT

High regional costs and negative distributional impacts on lower/middle income consumers.

15 15

Learning from the Regions