sunny days ahead

TRANSCRIPT

Sunny Days Ahead

1

Preface

For entrepreneurs and businesses exploring opportunities in the solar PV domain, power

production opportunities are the most apparent. Opportunities available along the other

parts of the solar PV value chain, especially in the manufacturing sector are much less in the

limelight.

While power production as a business opportunity has its attractions, especially taking into

account the National Solar Mission (NSM) incentives, this is essentially a PPA-based

business model, with little upside potential. On the other hand, in order for India to

become a leader in solar power sector, it is imperative that India is able to develop a strong

supporting eco-system to support the growth in solar PV power production. Of prime

importance to this support eco-system is the role of manufacturing activities within the solar

PV value chain.Unlike the power production opportunities, manufacturing opportunities

bring with them the possibility of higher innovation and significantly higher upsides.

In order to participate in these opportunities, and to take critical investment decisions, a

better understanding of these is essential for Indian businesses.The objective of this white

paper is to provide inputs and intelligence for the manufacturing activities in India for the

solar PV ecosystem – for both crystalline and thin film technologies.

EAI is India’s leading research and consulting group with a dedicated focus on the Indian

renewable energy sector. The white paper has been developed by EAI as a part of the

Solarcon India 2011 by SEMI, held at Hyderabad in November2011.

Narasimhan Santhanam

Director

Energy Alternatives India

Sunny Days Ahead

2

Sunny Days Ahead

3

Contents

INTRODUCTION .......................................................................................................................................... 5

POTENTIAL IN INDIA ..................................................................................................................................................................... 6

RESOURCE ASSESSMENT .............................................................................................................................................................. 6

REGIONAL POTENTIAL .................................................................................................................................................................. 7

PV TECHNOLOGIES ..................................................................................................................................... 8

CRYSTALLINE SILICON (C-SI) ....................................................................................................................................................... 8

THIN FILM (TF) ............................................................................................................................................................................. 8

COMPARISON BETWEEN CRYSTALLINE AND THIN FILM PANELS ............................................................................................. 9

SOLAR PV MANUFACTURING SCENARIO ............................................................................................. 16

CRYSTALLINE SILICON ................................................................................................................................................................ 16

Polysilicon ............................................................................................................................................................................ 17

Wafer ..................................................................................................................................................................................... 19

Cells........................................................................................................................................................................................ 20

Modules ............................................................................................................................................................................... 21

THIN FILMS .................................................................................................................................................................................. 22

Amorphous Silicon (a-Si) ............................................................................................................................................... 22

Cadmium Telluride (CdTe) ............................................................................................................................................ 23

Copper Indium Gallium (di)Selinide (CIGS) ............................................................................................................ 23

OTHER MANUFACTURING OPTIONS......................................................................................................................................... 24

Raw Material, Machineries and Equipment for Core Products ...................................................................... 24

Non-core Solar Products ............................................................................................................................................... 29

CENTRAL AND STATE POLICY ANALYSIS................................................................................................................................... 30

Central .................................................................................................................................................................................. 30

State Policy ......................................................................................................................................................................... 32

CONCLUSION ............................................................................................................................................. 33

ANNEXURE I ............................................................................................................................................... 34

ANNEXURE II ............................................................................................................................................. 37

ANNEXURE III ............................................................................................................................................ 38

EAI - ASSISTING YOUR COMPANY FOR ATTRACTIVE MANUFACTURING OPPORTUNITIES IN

SOLAR PV ................................................................................................................................................... 43

ABOUT SEMI AND PV GROUP ................................................................................................................. 47

Sunny Days Ahead

4

Highlights

Polysilicon

Currently, there is no polysilicon manufacturing capacity in India

To sustain 20 GW worth of installations, over 14,000 MT per year of polysilicon

manufacturing capacity would be required

Wafer

There is currently no wafer manufacturing company in India with significant

production capacity

To sustain 20 GW worth of targeted installations, over 2000 MW per year of

wafer manufacture would be required

Cells

Local content requirements will ensure robust demand for local cell

manufacturing

Stimulus for domestic cell manufacturing will not only be from the Central

policy, but also from some state policies promoting domestic manufacture

and vertical integration

Modules

Significant growth in domestic module uptake is expected in India; however,

this is not being exploited by Indian module makers owing to uncompetitive

prices

Vertical integration is the key factor that determines the cost-competitiveness

of solar modules

While thin films have as high an acceptance level in India as crystalline silicon

module, thin films do not have as much competition

Production Equipment

77% of the Indian manufacturing capacity is expected to be powered by turn-

key lines, indicating significant promise for this sector in terms of

manufacturing and system integration

Sunny Days Ahead

5

Introduction

Located close to the equator, India has a tropical climate and is endowed with abundant

sunshine. This, along with the fact both the country’s economic growth and energy demand

are burgeoning, makes solar a prime player in the renewable energy industry in India.

Solar Radiation Map (Energy Density) of the World (Source: AltE)

As can be seen from the above image, India is a prime location for the installation of solar

based energy systems as opposed to regions in, say, Europe. This is due to the higher

amount of solar radiation received, which is about 2-4 kwh/m2 higher than most regions in

Europe.

Despite this, the growth of solar in India (over the past few years) has not been as high as

regions in Europe. This may be attributed to investors being wary of a nascent technology

(within India) and the lack of a strong, structured and stable solar policy.

The National Solar Mission aims to address the issue of the lack of a stable policy. The results

of this mission are already evident – with the introduction of this policy, grid connected

installed capacity of solar grew from negligible levels to about 45 MW (As of July 2011) over

the span of only 2 years. The policy has provided the necessary impetus for the explosive

growth of solar in India. The mission aims to not only increase the installed solar power

production capacity (to 20 GW) but also envisages the development of a full-fledged

domestic solar equipment manufacturing ecosystem. The ambitious production targets

include

2 GW of Polysilicon capacity by 2022

4-5 GW of production capacity across the value chain by 2022

Sunny Days Ahead

6

Potential in India

Theoretically, about 5000 trillion kWh/m2 of solar energy is incident across the entire area of

the country, with daily averages of incident radiation falling between 4 and 7 kWh/m2/day.

While the theoretical potential stated seems like a large number, the actual potential is

significantly lower due to various constraints such as:

Available area for plant development

Useful solar energy capture area within the power plant

Theoretical conversion efficiency limits for solar PV based systems

Resource Assessment

The solar resource map of India has been developed using data extrapolated from satellite

imagery.The areas with the highest potential for solar based power generation are

concentrated in the peninsular region of the country – with Rajasthan being the only

noteworthy exception.About 1.75 million sq. km of land receives an annual irradiation of

about 5.5 to 6 kWh/m2/day. In addition to this, about 1.1 million sq. km of land receives

irradiation between 5 and 5.5 kWh/m2/day putting the total available (optimal) area for

setting up solar power plants at about 1.85 million square km.

Why resource assessment matters

Accurate site comparison and selection

Energy estimates can be made with greater confidence

Predicting financial viability (a function of revenue and hence electricity generated)

Increasing the bankability of the project

Performance validation

Utility forecasting and grid interfacing

Relative uncertainties for resource assessments1 (Source: AWSTruepower)

1 Satellite Modelled Data is what is commonlyused. GHI – Global Horizontal Irradiance data is what is

applicable to solar PV power plants and is measured on the ground (at the site) using a pyranometer

Sunny Days Ahead

7

As such, the accuracy of this information is not very high. Furthermore, data in some regions

with high suitability for solar power plants are available only at very low spatial resolutions

undermining the accuracy of it even more.

A key hindrance to the growth of solar power in India is the lack of availability of accurate

irradiation data. The lack of this information severely limits a developer’s capability to

accurately predict the amount of electricity which a plant is expected to generate and hence

the revenues he is expected to accrue. This is one of the major factors that has stunted new

investment in the solar energy sector.

Regional Potential

Regional potential of each state in India can be viewed from two angles – actual insolation

incident on the state and the state specific policy adopted. Ideally, the state with the highest

potential would have an intersection of the two.

Insolation Driver

A look at the solar insolation map of India shows that the southern states of Andhra Pradesh,

Karnataka, Tamil Nadu and states in north western India such as Gujarat, MP and Rajasthan

have the best solar radiation in the country. States such as Arunachal Pradesh, Haryana,

Jharkhand, Kerala, Orissa, Punjab, Uttar Pradesh and West Bengal also have reasonable

potential, but there is very little installed capacity in these regions.

Policy Driver

The key driver for region specific growth is not just the amount of solar insolation the

state receives, but the presence of a strong state solar policy.As of August 2011, only

three states have come up with concrete solar specific polices. These include – Gujarat,

Rajasthan and Karnataka.The Tamil Nadu and Maharashtra governments are expected to

come up with their state solar policy soon.

Of these, the Gujarat and Rajasthan state policies are the ones that are both aggressive and

ambitious, with Gujarat looking to add close to 1 GW of solar PV in the coming years.Due to

the policy, regulatory support and higher solar insolation, Gujarat and Rajasthan are likely to

be the hotbeds for solar PV development in India in the short term.

Sunny Days Ahead

8

PV Technologies

Solar PV systems can be broadly classified into two types based on the type of technology

employed

Crystalline Silicon (c-Si)

Thin Film (TF)

Crystalline Silicon (c-Si)

These solar cells are manufactured from bulk crystalline silicon material known as MGSi. This

raw material, through various processes is converted to semiconducting wafers which

generate electricity when exposed to solar radiation through a process known as the

photovoltaic effect.

Among the various technologies available, c-Si based generation is the oldest and most

mature electricity generation system. Based on the crystalline structure of the ingot/wafer

used, c-Si based modules are further divided into the following categories

Monocrystalline

Polycrystalline or Multicrystalline

Monocrystalline modules are more expensive than multicrystalline modules but at the same

time they are more efficient i.e. they produce more electricity per watt of installed capacity.

Thin Film (TF)

Thin film technologies evolved as a result of low polysilicon availability for the manufacture

of c-Si based modules. Thin film modules are typically characterised by their lower material

requirement for the manufacture of a photoactive layer. Due to the lower grade and quantity

of raw materials used, these modules are usually less efficient when compared to c-Si based

modules. These modules are significantly cheaper due to the lower material cost coupled

with the fact that there are fewer steps involved in the manufacturing process.

The lower efficiencies as well as other drawbacks are being overcome using more exotic

materials and diverse manufacturing processes. Based on the type of material used for cell

manufacture, TFPV can be further classified as

Amorphous Silicon (a-Si)

Cadmium Telluride (CdTe)

Copper Indium Gallium (di)Selinide (CIGS)

Sunny Days Ahead

9

The figure below illustrates some of the key differences between the various thin film based

solar cells. The difference lies mainly in the process employed to put the various layers of the

cell together as well as how the layers are laid out.

Overview of Thin Film Technologies

Comparison between Crystalline and Thin Film Panels

Thin film solar cells Monocrystalline solar

cells

Polycrystalline/

Multi crystalline

solar cells

Construction

Thin film made by

depositing one or more

thin layers (thin film)

of photovoltaic material

on a substrate.

Monocrystalline cells are

cut from a chunk of

silicon that has been

grown from a single

crystal.

A polycrystalline cell

is cut from

multifaceted silicon

crystal.

Sunny Days Ahead

10

Efficiency

Less efficient than

polycrystalline and

monocrystalline panels.

Efficiency range – 10%

to 12%

Efficient compared to

both polycrystalline and

thin film.

Efficiency range – 15% to

19%

More efficient than

thin film solar cell but

less efficient than

Monocrystalline solar

cell

Efficiency range –

11% to 15%

Flexibility Yes (using plastic

glazing)

No No

Weight Light weight compared

to monocrystalline cells

and polycrystalline

cells.

Heavier compared to

thin film but less in

weight compared to

polycrystalline cells.

Heavier than

monocrystalline

modules.

Price $0.93 per watt (€0.69

per watt)

$1.12 per watt(€0.83 per

watt)

$1.02 per watt

(€0.75 per watt)

Area

(Avg. capacity

per 1000 sq.

m)

0.623 MW

0.98 to 1MW

0.91MW

Stability Less stable Very good stability Good stability and

better than thin film

solar.

Performance Performance is less

compared to

monocrystalline solar

cells.

Better than

polycrystalline cells and

thin film solar cells.

Performance is less

compared to

monocrystalline cells

Temperature Thin film solar cells are

largely unaffected while

operating under higher

temperatures

Monocrystalline panels

operate at decreased

efficiencies in higher

temperatures

Multi crystalline

panels operate at

wide range of

temperatures.

Sunny Days Ahead

11

Market Share

Currently, c-Si dominates the global PV cell manufacturing segment with a share of about

83% of the total cell production. It is expected that the market share for thin film

technologies is expected to increase significantly with estimates pegging the number

between 21% and 29% by 20122.

With falling c-Si prices (estimates suggest that the price could drop below $1 per Wp by

20143), thin film’s market share would depend on

Maintaining the cost savings advantage offered by thin films (i.e. the absolute price

difference between thin films and c-Si modules has to be maintained. Thus thin film

module prices have to drop to match the crashing c-Si prices). This is the primary

factor that makes thin film technologies bankable as opposed to c-Si due to the lack

of availability of reliable information over the project life.

Improving efficiency of thin film cells

Reduction in balance of system costs associated with thin film based power plants

Higher rates of adoption in developing countries – mainly in Asia, Africaand South

America(owing to better suitability to higher temperature conditions in addition to

lower capital requirements)

Market share of various technologies (Source: GTM Research)

The Indian Context

It is interesting to note that this global trend does not necessarily apply to India. For

instance, of the 30 winners (28 of whom achieved financial closure) under Phase 1

Batch 1 of the National Solar Mission, 50% of the winners went with c-Si and the other

50% went with thin film.

2 Source: GTM Research

3 Source: iSuppli

Sunny Days Ahead

12

The primary factors driving this trend could be attributed to

Lower capital costs associated with thin film based power plants

Ease of availability and lower cost of landand lower labour BoS cost (lower labour,

project management, civil and construction costs) for setting up power plants

Availability of better financing options from foreign banks (E.g. Ex-Im bank offers

cheap loans at lower interest rate when procuring modules from US manufacturers).

Technology Suitability for India

Bankability

Banks tend to prefer well established technologies, with a proven track record for financing

projects. In view of this and the fact that the solar energy sector in itself is in a nascent stage

in India, c-Si has the upper hand considering the technology has been around for around 30

years meaning it is has proven credentials for a time period equal to the entire operational

life of a power plant.

However, in case of thin film, as the technology is new it does not have a proven track

record. Thus the performance of the system cannot be guaranteed over the lifetime of

operation of the power plant. This makes the system prone to heavier scrutiny frombanks.

Land Requirement

One of the prime criteria for selection of technology for a power plant is the availability of

suitable land (both in the qualitative and quantitative sense) to setup the power plant. Thin

film technologies typically require more land than c-Si based systems due to their lower

power density. However, in India, large tracts of land are readily available (at cheap rates

when compared with project costs), nullifying the advantage offered by c-Si in this regard. In

this scenario, the project cost becomes the limiting factor tipping the scales in favour of thin

films.

Project Cost

The overall project cost plays a major role in the final decision to go ahead with investment

as it lays the foundation for determining the profitability of the project. The project cost can

be considered to be the sum of two components – the modules and the balance of systems

cost.

Module Cost – this attributes to about 60% of the project cost. In this respect, thin

films hold the advantage.c-Si modules are about 25% to 40% more expensive per Wp

when compared with thin film4.

4 Source: EnergyTrend

Sunny Days Ahead

13

Capital Cost Breakup for Solar PV

BoS Cost – this component, in most cases forms the rest of the project cost of any

power plant. In this respect, c-Si holds the advantage. In general, BoS costs are about

9% higher for thin film technologies when compared to c-Si technologies5. However

in the Indian context, the BoS costs play a subdued role in choice of technology due

to lower labour, project management, civil and construction costs.

Comparison of BoS Costs Between c-Si and Thin Film Based Systems (Source: GTM Research)

The cost savings from module offsets the additional BoS cost requirement for thin film,

thus making the overall project cost of thin film based systems lower than that of c-Si

systems or in the worst case, comparable.

5 Source: GTM Research

1%

52%

22%

9%

7%

2%

7%

Capital Cost Breakup for Solar PV

Land

PV Modules

PCU

Civil & General Works

Mounting Structures

Evacuation Cost

Preliminary & PreoperativeExpenses

Sunny Days Ahead

14

Alternative Financing

Alternate financing mechanisms are available for projects which import modules from

foreign countries. For instance Ex-Im, OPIC, EDC etc. offer attractive financing options at

lower interest rates for import of modules from USA and Canada respectively. In view of this,

more project developers are looking to import modules from abroad.

However, with JNNSM acting as the most popular (preferred) framework for solar

development in India, this route may be taken by thin film technologies alone. This is a direct

result of the local content requirement enforced by the policy which (as of Phase I, Batch II) is

applicable only to c-Si based power generation.

High temperature applications

The close proximity of India to the equator results in the country not only receiving abundant

solar irradiation but also being exposed to harsh temperatures. The average temperatures

for most locations suitable for putting up solar farms are in excess of 30 degree centigrade

(while guaranteed performance of modules is rated at 25 degrees under standard test

conditions).

Module performance degrades with increase in temperature (above standard conditions).

The degree to which the performance drops is measured through a factor known as

temperature coefficient. Thin film modules are inherently less prone to severe increases in

temperatures while c-Si modules show considerable performance losses at higher

temperatures. Owing to this, thin film might be more suitable to Indian climatic conditions.

Technology Performance at Different Locations & Under Different Climatic Conditions (Source: NREL,

GTM Research)

Sunny Days Ahead

15

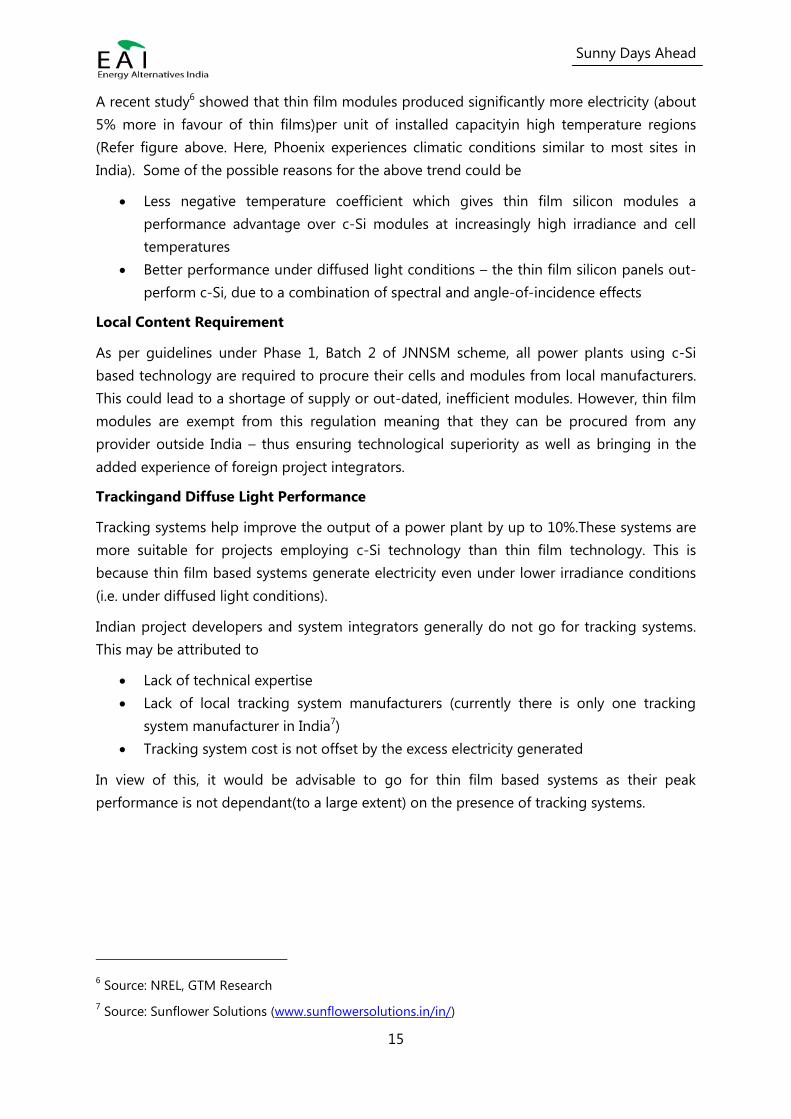

A recent study6 showed that thin film modules produced significantly more electricity (about

5% more in favour of thin films)per unit of installed capacityin high temperature regions

(Refer figure above. Here, Phoenix experiences climatic conditions similar to most sites in

India). Some of the possible reasons for the above trend could be

Less negative temperature coefficient which gives thin film silicon modules a

performance advantage over c-Si modules at increasingly high irradiance and cell

temperatures

Better performance under diffused light conditions – the thin film silicon panels out-

perform c-Si, due to a combination of spectral and angle-of-incidence effects

Local Content Requirement

As per guidelines under Phase 1, Batch 2 of JNNSM scheme, all power plants using c-Si

based technology are required to procure their cells and modules from local manufacturers.

This could lead to a shortage of supply or out-dated, inefficient modules. However, thin film

modules are exempt from this regulation meaning that they can be procured from any

provider outside India – thus ensuring technological superiority as well as bringing in the

added experience of foreign project integrators.

Trackingand Diffuse Light Performance

Tracking systems help improve the output of a power plant by up to 10%.These systems are

more suitable for projects employing c-Si technology than thin film technology. This is

because thin film based systems generate electricity even under lower irradiance conditions

(i.e. under diffused light conditions).

Indian project developers and system integrators generally do not go for tracking systems.

This may be attributed to

Lack of technical expertise

Lack of local tracking system manufacturers (currently there is only one tracking

system manufacturer in India7)

Tracking system cost is not offset by the excess electricity generated

In view of this, it would be advisable to go for thin film based systems as their peak

performance is not dependant(to a large extent) on the presence of tracking systems.

6 Source: NREL, GTM Research

7 Source: Sunflower Solutions (www.sunflowersolutions.in/in/)

Sunny Days Ahead

16

Solar PV Manufacturing Scenario

Solar PV manufacturing, being a technology intensive sector has for a considerable amount

of time been dominated by companies in Europe and USA. However, since 2005 the

manufacturing base has slowly shifted towards the East, primarily to China. With close to

60% of the global PV manufacturing base now in China it is safe to say that the country is the

undisputed global leader in the Solar PV manufacturing segment.

Global Solar PV Manufacturing Scenario (Source: EPIA)

Vertical integration is one of the key factors that help a company remain cost

competitive in this sector. In addition to this, the scale of manufacturing also plays a very

key role in determining the final cost of the module.

In India, there are very few companies in the upstream segment of the solar PV

manufacturing value chain viz., in the manufacturing of polysilicon and ingots/wafers.The

highest concentration of companies is limited to the manufacture of modules with

considerably fewer players (about ten) in the cell manufacturing segment. The cell and

module lines are expected to grow over the next few years with the National Solar Mission

stipulating strict domestic content requirements. These production lines are expected to be

powered by turn-key solutions from foreign companies, as opposed to home-built solutions.

Crystalline Silicon

The c-Si module manufacturing process begins with the manufacture of pure polycrystalline

silicon followed by their conversion into ingots/wafers through a method known as the

Sunny Days Ahead

17

Czochralski process. Following this, the ingots/wafers are converted into cells and finally

assembled into modules.

Solar PV Value Chain

Polysilicon

Polysilicon production is the first step in the c-Si solar PV value chain. The demand for

polysilicon for use in the solar energy industry has been growing at the rate of 30% annually.

Of the total global production of polysilicon, about 75% is used in the solar PV

manufacturing sector with the semiconductor industry coming in at a distant second8. The

primary difference in the polysilicon used in the solar PV sector and the electronics industry

is its purity. The former uses 6N grade polysilicon while the latter uses 9N grade (higher

purity).

The global production of polysilicon was about 350,000 MT in 2010. This figure is expected

to rise to about 370,000 MT in 2011, with the top 5 companies expected to ramp up

production to meet the increase in demand from the solar PV industry as well as remain cost

competitive.

8 Source: WackerChemie AG

Polysilicon

Ingots & Wafers

Cells

Modules

Rooftop/ Off grid Grid Power Plant Solar Products

Micro Mini Lanterns

and lights

Solar water

pumps

Other Solar

Products

a-Si, CdTe, CIGS

(Thin Film)

Sunny Days Ahead

18

Capacity Global – 350,000 MT (2010). Expected to grow to 370,000 MT (2011)

Local – none

Cost of Production Current – $30 to $35 per Kg

Expected – About $25 per Kg by 2011

Production Yield 1 tonne of pure polysilicon can be obtained from 1.2 to 1.6 tonnes of MGSi

Electricity Requirement About 100 to 200 kWh per Kg

Price Current – Between $42 and $51 per Kg

Global production is dominated by the top 5 companies in the industry. Together, these

companies account for close to 75% of the total global production (refer table below).

Currently, there is no significant production of polysilicon in India. Lanco Solar, Bhaskar

Silicon and Yash Birla Group have announced plans to set up polysilicon manufacturing

plants in India.

Rank Company Country Annual Production

2010 (MT)

Expected Production

2011 (MT)

1 Hemlock

Semiconductor

USA 36,000 36,000

2 WackerChemie Germany 30,500 33,000

3 OCI Company South Korea 27,000 42,000

4 GCL-Poly China 21,000 21,000

5 REC Silicon Norway 16,000 17,500

6 MEMC USA 12,500 15,000

7 LDK China 11,000 18,000

8 Tokuyama Japan 8,200 8,200

9 M.Seteck Japan 6,000 7,000

10 Daqo New

Energy

China 3,300 4,300

List of Top Global Manufacturers of Polysilicon (Source: PV Magazine)

Sunny Days Ahead

19

Wafer

A silicon wafer is a thin slice of crystal semiconductor, such as a material made up from

silicon crystal, which is circular in shape. They are used in the manufacturing of

semiconductor devices, integrated circuits and other small devices. There are multiple

processes through which silicon wafers are manufactured. These include

Czochralski Process – for manufacture of monocrystalline ingots

Bricking/Solidification – for manufacture of multicrystalline ingots

Capacity Global – About 29 GW (2010). Expected to grow to about 42 GW (2011)

Local – none

Cost of Production Current – 25 to 50 cents per Wp

Production Yield 1 Wp equivalent of wafer requires about 6 to 7 grams of pure polysilicon

Price Multi-Si Wafer (156mm x 156mm) - $1.87 to $2.10

Mono-Si Wafer (156mm x 156mm) - $2.43 to $2.85

As is the case with polysilicon, wafer production too is dominated by global players, with

little to no competition from Indian players. In fact,there is no significant production of

wafers in India. However, Lanco Solar, Yash Birla Group, Carborundum Universal, Bhaskar

Silicon and Reliance Solar are expected to setup their wafer manufacturing units in the

coming years.

Rank Company Country Production

Capacity 2010(MW)

Expected capacity

2011 (MW)

1 LDK Solar China 3,000 4,000

2 REC Wafer Norway 1,740 2,300

3 GCL Poly China 3,500 3,500

4 Solarworld Germany 1,250 1,260

5 Renesola China 1,210 1,800

6 Yingli China 1,000 1,700

7 Trina Solar China 750 1,200

8 MEMC USA 650 1,200

Sunny Days Ahead

20

9 Pillar Spain 700 720

10 Green Energy tech Taiwan 800 1,500

List of Top Global Wafer Manufacturers (Source: PV Magazine)

Cells

The third step in the solar PV value chain is the manufacture of cells from the wafers. This

step involves the conversion of the wafer to a photoactive diode i.e. a piece of

semiconductor that is able to generate free electrons when exposed to sunlight.

Capacity Global – About 33 GW (2010). Expected to grow to about 48 GW (2011)

Local – About 600 MW (2010)

Cost of Production Current – 25 to 40 cents per Wp (excluding feedstock)

Price Between 70 cents and 85 cents per Wp

The total global cell manufacturing capacity is about 30 GW. As with wafers, China dominates

this segment too, with about 50% of the total global manufacturing capacity. It is interesting

to note that of the top 10 companies globally, one is a thin film cell manufacturer (FirstSolar).

Furthermore, 50% of the companies in the list manufacture both cells and modules – a move

towards vertical integration and cost cutting.

Rank Company Country Annual Production

Capacity in

2010(MW)

Actual

Production in

2010(MW)

1 Suntech China 1800 1585

2 JA Solar China 2100 1463

3 First Solar(Thin film) USA 1502 1411

4 Trina China 1200 1050

5 Q-cells(includes Thin film) Germany 1265 1014

6 Yingli China 1000 980

7 Motech Taiwan 1200 945

8 Sharp(includes Thin Film) Japan 1000 910

9 Gintech Taiwan 930 827

Sunny Days Ahead

21

10 Kyocera Japan 650

List of Top Global Cell Manufacturers (Source: Photon)

The Indian scenario for cell manufacture is not as barren as is the case for polysilicon and

wafer production. There are about 10 companies involved in cell manufacture in India (refer

Annexure I for a detailed list). The total cell manufacturing capacity of these companies

amounts to about 600 MW which is still a far cry from the available capacities the world over.

The leading companies in terms of available capacity include Indosolar, Moser Baer (thin

film), TATA BP solar and Websol.

The key thing to note with the Indian companies is that they are strictly into cell and

module manufacturing with no vertical integration. This leads to their cells and modules

not being cost competitive with the cells/modules from world leaders such as the Chinese

manufacturers.

Modules

The final step in the value chain is the assembly of the various solar cells into modules. The

process in this stage involves the interconnection and packaging of multiple cells into a

single unit. The price of a PV module is mainly influenced by the price of the cells it

incorporates.

Capacity Global – About 37 GW (2010)

Local – About 1200 MW (2010)

Production Yield Dependent on module rating. Each cell has a rating of about 4 Watts.

Price About $1.2 per Wp

The solar module manufacturing segment is highly fragmented due to the ease of

manufacturing of the module – which in essence is just an assembly process and the low

capital cost involved in setting up of the assembly line. The top global manufacturers of

modules include Suntech Power, FirstSolar, Yingli Green Energy, Trina Solar and Sharp.

Sunny Days Ahead

22

Actual Production of Top Global Module Manufacturers (Source: GTM Research)

In India, there are about 40 module manufacturers with cumulative installed capacities of

about 1200 MW. A detailed list of the Indian module manufacturers can be found in

Annexure I.

Thin Films

Amorphous Silicon (a-Si)

a-Si is the oldest of the three thin film technologies. As such, it commands the largest market

share among the three available thin film technologies. a-Si modules have double the market

share of the nearest rival i.e. CdTe. The top global a-Si based module manufacturers include

Suntech, Sharp Thin Film and Trony Solar.

Rank Company Country Actual Production in 2010(MW)

1 Sharp Solar Japan 195

2 Trony Solar China 138

3 Uni-Solar USA 120

4 NexPower China 85

5 Kaneka Solartech Co. Ltd Japan 58

List of top Global a-Si Manufacturers (Source: GTM Research)

Sunny Days Ahead

23

In India, Moser Baer is the only company with a-Si based module manufacturing

facilities, with a production capacity of about 50 MW, making it one of the leading global

players too.

The costs associated with the manufacture of a-Si module is about $1.1 per Wp. Current

market price for a-Si modules is about $1.2 per Wp making the profit margin pretty low.

Since a-Si based solar modules have some of the lowest efficiencies compared to other solar

PV modules, in the future it is expected that pure a-Si would have very low demand. They are

scheduled to be replaced by some of the more advanced technologies such as tandem

junction cells, which employ a combination of both a-Si and c-Si technologies.

Cadmium Telluride (CdTe)

CdTe has the second highest market share of the three thin film technologies. CdTe has seen

significant growth mainly due to the aggressive push by US based FirstSolar who have a

virtual stranglehold on the CdTe (as well as the thin film) market. Their module production

capacity was about 1400 MW in 2010. To put their dominance in perspective, the next closest

company, Sharp (which manufactures a-Si based thin film modules) has a capacity of about

195 MW.

Rank Company Country Annual Production Capacity in 2010 (MW)

1 First Solar USA 1400

2 Abound Solar USA 65

3 PrimeStar Solar USA 30

4 Calyxo GmbH Germany 25

List of Top Global CdTe Manufacturers

Some of the other players in the CdTe segment are Abound Solar, Primestar Solar and Calyxo

GmbH. Currently, there are no manufacturing units producing CdTe based modules in India.

The cost of production of a CdTe module is about $0.8 per Wp while the market sale price is

close to $1 per Wp. This makes CdTe based modules one of the cheapest modules available

in the market. Further, FirstSolar has stated that the price of the modules could fall to about

$0.75 per Wp by 2012.

Copper Indium Gallium (di)Selinide (CIGS)

Of the three thin film technologies, CIGS is the newest. The advantage of CIGS is that it does

not use any toxic or rare earth materials during the manufacturing process. Thus CIGS is

Sunny Days Ahead

24

expected to be the future of Thin Film based solar power generation systems if it can remain

cost competitive.

The cost of production of a CIGS module varies between $1.2 and $1.3 per Wp while the

selling price is about $1.4 per Wp making it the most expensive thin film based generation

system. However, there is significant potential for cost reduction considering the nascent

nature of the technology.

A significant portion of the total installed production capacity (about 800 MW) is attributed

to Solar Frontier. Other global production companies include Nanosolar, Avancis and Solibro

Solar (a subsidiary of Q-Cells).

In India, Shurjo Energy has a production capacity of about 7 MW9. No other company

manufactures CIGS based modules in India, as of September 2011.

Other Manufacturing Options

Raw Material, Machineries and Equipment for Core Products

Opportunities exist in manufacturing raw material and equipment for the following:

Ingots

Wafers

Cell

Modules

Raw Materials

A wide variety of raw materials and starting products are required for the entire solar PV

value chain. This section provides inputs on the key raw materials and starting products

required at each stage of the value chain. These inputs will provide the entrepreneurs

excellent insights into the types of opportunities that could be most suitable for them,

depending on their current line of business and their competencies.

In the tables below:

1) The LEFT HAND SIDE column indicates the MAIN MATERIALS required for

Manufacturing

2) The RIGHT HAND SIDE column indicates the sub components required for each

material

9 Source: Shurjo Energy (Company Website)

Sunny Days Ahead

25

Ingot

Main Materials Sub components to make the materials

Polysilicon

Modified Siemens CVD reactor, Vapor-to-Liquid deposition

reactor, Fluidized bed reactor

Recycled Materials Broken Wafer, Top/Tail of Ingot

Crucible Quartz crucible, Graphite Crucible, Ceramic Crucible

Carbon Felt Carbon Felt

Other Seed Crystal

Wafer

Main Materials Sub components to make the materials

Ingot Moncrystalline or Polycrystalline ingot

Saw Band Saw band

Slurry

Black Silicon Carbide, Green Silicon Carbide, Recycled cutting liquid

Recycled Silicon Carbide

Saw Wire Saw Wire

Ingot Mounting

Adhesives Adhesives

Acids Sulfuric Acid, Hydrochloric acid

Cell

Main Materials Sub components to make the materials

Wafers Moncrystalline and Polycrystalline wafers

Metallization Paste Silver Paste, Aluminum Paste

Screen Screen

Chemicals

Isopropyl Alcohol, Ammonia, Phosphorus oxychloride, Sulfuric acid,

hydrochloric acid, Potassium hydroxide, sodium hydroxide

Silane Silane

Crystalline Modules

Main Materials Sub components to make the materials

Ribbon Lead ribbon, Copper Ribbon. Lead free ribbon, tin coated copper ribbon,

Glass

Film

Ultra clear patterned glass, AR coated glass, TCO coated glass, BIPV glass

Back sheet, EVA

Cable Copper wires

Other Junction Box, Connector, Frame, Sealant and tapes

Thin Film Module

Main Materials Sub components to make the materials

Glass

Ultra clear patterned glass, TCO coated glass

AR coated glass

Chemicals

Boron, Cadmium Sulphide, Copper, Alumina, Gallium, Germanium,

Indium, Molybdenum, Phosphorus oxychloride, Tellurium, Tin

Sunny Days Ahead

26

TCO Material Diethyl Zinc

Oxides Zinc Oxide, Tin oxide

Acids Hydrochloric acid, Sulphuric acid

Other Junction Box, Connector, Cables, Frame, Sputtering Target

Machinery and Equipment

This segment covers the manufacturing of turnkey production line solutions for the thin-film

and silicon module production as well as other manufacturing components such as wafers

saws or analysis tools.

Turn-key lines dominate most of midstream PV manufacturing capacity locally. It is expected

that about 77% of manufacturing capacity would be powered by turn-key manufacturing

lines which when compared to global figures (about 15%) is significantly high10.Solarbuzz

analysis reveals that across all midstream PV manufacturing, c-Si cell lines account for over

90% of manufacturing capacity. Analysis reveals that the manufacturing capacity is expected

to cross 1 GW by the end of 2011. In order to keep up with this, it is expected that there

would be significant purchase of turn-key manufacturing units in the short term which

produce high efficiency c-Si based solar cells with higher yields.

Manufacturing capacities by Type (Source: Solarbuzz)

The top global machinery and turnkey solution providers for the various stages are Oerlikon

Solar, Applied Materials and Ulvac Solar. There are also other players in the market, including

Roth & Rau, Centrotherm, Spire Solar, Anwell Technologies and Leybold Optics.

10 Source: Solarbuzz

Sunny Days Ahead

27

Indian companies are yet to make serious forays into machinery and equipment

manufacturing for the solar PV industry. A detailed list of machineries and equipment

required for the various processes all along the solar PV value chain is provided below.

In the tables below:

1) The LEFT HAND SIDE indicates the process involved

2) The RIGHT HAND SIDE indicates the equipment involved in each process

Ingots

Process involved Equipment involved in each process

Inspecting/Testing

Life time Analyser, Ingot vision inspector, Resistivity Inspector, Material

Property Analyser, Polysilicon Tester

Cutting &

grinding Ingot Cutting Machine, Ingot Grinding Machine

Crystalline ingot

growing

MCZ process equipment, DSS process equipment, CZ process

equipment

Others Ingot Transportation and Storage Cart, Granular Feeder

Wafers

Process involved Equipment involved in each process

Cutting

Cutting Equipment, Wire Saws, Band Saws, Silicon Recovery System

Slurry Recovery System

Cleaning Ultrasonic Wafer Cleaner

Inspecting/Testing

Life time Analyser, Wafer vision inspector, Resistivity Inspector,

Material Property Analyser, Wafer Sorter, Wafer Counter, Wafer Tester

Polishing and

grinding Wafer Grinding equipment, Wafer Polishing Machine

Others

Wafer Handling System, Conveyor, Automatic Water Loading Machine

Cassette, Water Separation Equipment

Cell

Process

involved

Equipment involved in each process

Etching Laser Etching Equipment, Plasma Etching Equipment, Wet etching

equipment, Texturing Equipment, Power system and gas/Liquid

Flow Management System

Diffusion Diffusion Furnace, Waste gas Abatement system, Doping

Equipment

Sunny Days Ahead

28

Vaccum Pump for Diffusion, PreDiffusion Sprayer

Coating/Deposition Cell Coating Equipment, Cell Sputtering, Coating Control System

Cell PECVD system, Cell MOCVD, Cell CVD, Cell PVD, Cell AR

coating system.

Screen Printing Screen Printer

Furnaces Drying Furnace, Firing Furnace

Inspecting/Testing Cell sorter, Cell Tester, Cell vision inspector, Cell coating inspector

Others Cell Plating system, Cell handling system, conveyor cassette

Crystalline Silicon Modules

Process involved Equipment involved in each process

Inspecting/Testing Panel Solar Simulator, Environment Simulating Tester, Panel Cell

Position, String Measurement Equipment

Cleaning Glass Cleaner

Tabbing/Stringing Stringer, Tabber, Soldering Equipment

Laminating Laminator, Curing Furnace

Cutting/Scribbing Cell Laser Scribber, Cell Laser Cutter

Framing Framing Machine

Others Ribbon Cutter, Lay up station, Film Cutter, Silicone Dispenser,

Ribbon Flux Furnace, Panel Handling System.

Thin Film Modules

Process involved Equipment involved in each process

Inspecting/Testing Thin Film Solar Simulator, Thin Film Optical Inspection System,

Thin Film Thickness Measurer, Thin Film Time Analyser

Coating/Deposition Thin Film PECVD system, Thin Film Sputtering, Thin Film CVD, Thin

Film PVD, Thin Film AR coating system

Cutting/Scribbing Thin Film Laser Scribber, Thin Film Mechanical Scribber

Cleaning Ultrasonic Thin Film Cleaner

Etching Thin Film Laser Etching Equipment, Thin Film Plasma Etching

Equipment, Thin Film Wet etching equipment, Thin Film Texturing

Equipment

Source: ENF.cn, http://www.enf.cn/database/equipment.html

The above tables provide a glimpse of the range of components, subcomponents and

equipment required to make the key products along the solar PV value chain. The list

Sunny Days Ahead

29

provided is by no means exhaustive but is intended to make entrepreneurs acquainted with

the diverse opportunities.

Non-core Solar Products

In addition to the core business opportunities in manufacturing available along the solar PV

value chain, there are non-core opportunities for entrepreneurs and investors in this industry.

Some of the prominent non-core manufacturing opportunities are given below.

Solar Glasses

For crystalline cells, solar glass is used for protection and performance enhancement. In the

case of thin films, glass is used as a substrate.

Worldwide, in 2007, 138 million tons of glass was produced. Of this, 50 million tons were flat

glass, which is used in solar modules and reflectors. The flat glass market is worth €21 billion

annually but, only four companies namely NSG Group, AGC, Saint-Gobain and Guardian

Industries produce around 60% of the world's high quality float glass.

Few companies in India currently make glasses for solar cells, and Saint Gobain is one of

them; the Indian arm of the French glass giant is making serious efforts at extending its glass

products to cater to the demand of solar panels sector. Recently, Gujarat Borosil launched

solar grade glasses in Dec 2010.

Electrical Components: Inverters, Wires and Transformers

The manufacturing of inverters, charge controllers, wires and transformers is largely a

commodities business.

In the case of inverters, efficiencies of these devices are already relatively high, offering only

limited room for technical differentiation. There are exceptions - for instance, Steca Solar of

Germany provides a solution to the problem of partial shading when solar modules become

as inefficient as under full shading. The global leaders in inverters are SMA Solar

Technologies, Kaco and Fronius.

In India, the transformer and wires are sourced locally. Inverter manufacturers like Su-kam,

Luminous and Numeric are yet to fully start producing inverters for grid connected power

plants; hence, the inverters for MW scale solar PV power plants are mostly being imported.

Manufacturing Chemicals for Solar Industry

The manufacturing of photovoltaic modules, thermal receivers and reflectors requires a

number of chemicals and materials such as coatings, laminates, photovoltaic materials and

solar glass. Some of these chemicals have been listed above under Cells.

Sunny Days Ahead

30

Production of many of these chemicals also offers opportunities to Indian companies already

in the chemicals industry.

Central and State Policy Analysis

Central

The JNNSM has set an ambitious target of 20 GW of installed solar PV capacity in India by

2022. The policy aims to support this large scale of installation by fostering the growth of a

purpose built ecosystem which caters to every stage of the solar PV value chain. The

following sections discuss the implication of targets on the value chain.

Polysilicon

To sustain 20 GW worth of installations, India would require between 14,000 and

15,000 MT per year of polysilicon manufacturing capacity from the current non-

existent levels. As mentioned earlier, the main factor that determines the production output

of a polysilicon plant is the availability of uninterrupted power supply which poses a huge

challenge to the weak national grid with its heavy voltage fluctuations and generally poor

reliability (not to mention the high percentages of peak deficit in electricity supply that the

country is currently facing). The JNNSM document does not detail how this is to going to be

ensured.

Manufacturing plants need to be setup to produce polysilicon at large scales to remain cost

competitive (as cost of each stage in the value chain is propagated downstream and reflects

in the final module price). This translates to a high capital associated with the setting up of

manufacturing plants. Although the JNNSM document recommends low interest rate loans

and priority sector lending for manufacturing to achieve the installed capacity targets, they

would still be a far cry from what the global leaders (China) offer to their manufacturing

bases. The scale of investment required is unprecedented and the JNNSM scheme must

ensure that this is met.

Ingot/Wafer

It is estimated that by the end of the decade, the requirement for ingots/wafers would be

about 2000 MW. Production has to be scaled about 20 fold (from planned levels) to meet

this requirement.

As with polysilicon, ingots/wafers also require very large capital investment. Polysilicon cost

attributes to about 50% of the production cost. The lack of local supply means that this

cost of production becomes too large to sustain a profitable business. Thus incentives would

Sunny Days Ahead

31

have to be provided upstream to ensure growth. The incentives offered for ingot/wafer thus

is a function of the incentives offered for polysilicon, which has been discussed above.

Cells

Currently, a lack of a local ecosystem for the subcomponents required for solar cell

manufacture has stunted the growth of the sector in the country. Majority of the

components such as

Gases and chemicals used during the manufacturing process

Primary manufacturing equipment etc.

Have to be imported which results in a sharp increase in production costs. As with

polysilicon, the lack of uninterrupted power is also a source of major concern as the

manufacturing plants then would have to operate using backup power which further

increases the running cost of the plant.

Phase 1, Batch 2 of JNNSM stipulates that, for power plants using c-Si based modules, the

cells used would have to be locally manufactured. Although this is a positive step, it is

unsustainable as upstream components for cell manufacture would still have to be imported

which leads to a situation where locally manufactured cells/modules would not be cost

competitive with those available in the international market. With thin film modules not

having any domestic content requirement, the project developers would then prefer to go

for import of thin film modules thereby putting a dent on the local manufacturing

aspirations.

Modules

About 3000 MW per year module manufacturing capacity would be required by 2012 to

sustain the growth projected under JNNSM. With a current installed base of about 600 MW,

this target seems to be the one that is most achievable. Also, module manufacturing is

technically not a manufacturing process as such, but more of an assembly process which

adds to the ease of production.

As with cells, a stricter implementation of domestic content is required under JNNSM to

promote the local manufacture of modules.

Vertical Integration

The only way a local manufacturing system would be cost competitive is to ensure that all

manufacturing facilities are vertically integrated. JNNSM does not specifically promote

vertical integration of companies which, under current conditions is the most critical

Sunny Days Ahead

32

requirement. Thus the policy would have to promote vertical integration with specific

incentives for the same.

State Policy

As of September 2011, only 3 states have come up with a solar specific state policy – Gujarat,

Karnataka and Rajasthan. Of these only the Rajasthan state policy has clauses specifically

ensured to promote local manufacturing.

Under the Rajasthan policy, domestic manufacture is being promoted not by mandating

domestic content requirements, but by providing incentives for setting up of manufacturing

plants. The incentive provided is in the form of additional capacity allocation (of 200 MW) for

module manufacturers for setting up solar power plants.

The key point to be noted under the Rajasthan state policy is that it aims to promote

vertical integration. Incentives are provided only to those manufacturers who produce

modules, cells and wafers.Although this is a step in the right direction, the time frame

stipulated under the state scheme is far too short for proper implementation of a vertically

integrated line.

Sunny Days Ahead

33

Conclusion

In order for the costs of solar PV power to come down (so that it no longer remains a

policy driven industry), it is critical to build a complete ecosystem for solar PV rather than

just show significant growth at the tail end of the value chain (i.e. power production). This

implies that there is a genuine need for the creation of hundreds of companies along the

entire value chain - from polysilicon production to wafer to cell and module manufacturing,

as well as production of the supporting components. However, except for cells and

modules, there is hardly any manufacturing in India for the rest of the solar PV value

chain. There is thus a significant gap between what is needed and what is available.

The above facts have not been lost on the Indian government, which is coming up

with plans and incentives to facilitate the entry of many more Indian companies into the

manufacturing segment of the solar PV value chain. These efforts by the government to

build a complete solar PV ecosystem in India open up attractive opportunities for investors.

Compared to the PPA-bound power generation sector primarily driven by operational

efficiencies, the significantly higher potential for innovation in the manufacturing

sector also implies that companies could invest in building innovative and

differentiated businesses with significant upsides in future.

We foresee a future in which many Indian companies use their experience in the

manufacturing sector to participate in the manufacturing opportunities in the exciting solar

PV industry.

Sunny Days Ahead

34

Annexure I - List of Indian Companies in the Solar PV

Module Value Chain

Company Status Capacity

Crystalline Silicon

Polysilicon

Maharishi Solar Commissioned 10 T per Year

Lanco Solar Planned

N/A

Bhaskar Solar Planned

N/A

Yash Birla Group Planned

N/A

Wafer

Maharishi Solar Commissioned 3 MW

Lanco Solar Planned

N/A

Yash Birla Group Planned

N/A

Carborundum Universal Planned

N/A

Bhaskar Solar Planned

N/A

Reliance Solar Planned

N/A

c-Si Cells

IndoSolar Commissioned 160 MW

Moser Baer Commissioned 150 MW

Tata BP Solar Commissioned 84 MW

Websol Commissioned 60 MW

Jupiter Solar Commissioned 45 MW

Euro Multivision Commissioned 40 MW

USL Photovoltaics Commissioned 35 MW

KL Solar Commissioned 30 MW

Central Electronics Commissioned 15 MW

Sunny Days Ahead

35

Shurjo Energy Commissioned 6 MW

Bharat Electronics Commissioned 5 MW

Modules

Solar Semiconductor Commissioned 195 MW

TATA BP Solar Commissioned 125 MW

EMMVEE Solar Systems Pvt.

Ltd

Commissioned 114 MW

Synergy Renewable Commissioned 110 MW

Moser Baer Photovoltaic Ltd. Commissioned 100 MW

PLG Power Commissioned 100 MW

Titan Energy Systems Ltd. Commissioned 100 MW

Photon Energy Systems Commissioned 50 MW

HHV Commissioned 45 MW

Websol Commissioned 42 MW

Surana Commissioned 40 MW

Andromeda Commissioned 30 MW

Premier Solar Systems Pvt.

Ltd.

Commissioned 30 MW

Reliance Industries Commissioned 30 MW

Waaree Commissioned 30 MW

Ajit Solar Commissioned 25 MW

KotakUrjaPvt. Ltd. Commissioned 25 MW

Vikram Solar Commissioned 25 MW

Icomm Commissioned 20 MW

Modern Solar Commissioned 18 MW

Alpex Exports Commissioned 15 MW

Maharishi Solar Commissioned 15 MW

Microsol Power Pvt. Ltd. Commissioned 14 MW

Sunny Days Ahead

36

PV Power Tech Commissioned 14 MW

Green Brilliance Commissioned 12 MW

Shurjo Energy Commissioned 12 MW

Sova Commissioned 12 MW

Access Solar Commissioned 10 MW

Central Electronics Ltd. Commissioned 10 MW

Photonix Solar Commissioned 10 MW

Sungrace Commissioned 10 MW

Rajasthan Electronics and

Instruments Ltd.

Commissioned N/A

Udaya SL Photovoltaics Pvt.

Ltd.

Commissioned N/A

Ammini Solar Pvt. Ltd. Commissioned

N/A

Thin Film

a-Si Thin Film

Moser Baer Commissioned 30 MW

HHV Solar Commissioned

N/A

Novergy Energy Commissioned

N/A

CIGS Thin Film

Shurjo Energy Commissioned 6 MW

Sunny Days Ahead

37

Annexure II

Summary of Central/State Solar Policies

JNNSM Gujarat Rajasthan Karnataka

Targets 20 GW by 2022 1 GW by 2012

& 3 GW (in next

5 years)

10 GW – 12 GW (in

12 years)

350 MW by 2015

-2016

Timelines Phase 1(2012-13)

Phase 2(2013 -17)

Phase 3(2017 -22)

300 MW (Grid

Connected) by

DEC 2011

Phase 1: 200 MW

(PV) up to 2013

Phase 2: 400 MW

(2013-2017)

126 MW by 2013

- 2014

40 MW per year

till 2016

Local

Content Applicable for c-Si

Modules and Cells;

Not applicable for

TF

None None; But

incentives for local

manufacturing

None

Feed-in-

Tariff Reverse Bidding :

Round 1 -Solar PV

Rs. 10.9 -

12.75/kWh

Rs. 15/kW (1st

12 years)

Rs. 5/kWh (13th

to 25th year)

Decided through

Reverse Bidding

Up to 200 MW.

Reverse Bidding

with base price

@

Rs. 14.50 /kWh

(max)

Current

Status Phase 1 : 150 MW

PV allotted; 300

MW by end of

2011

PPAs signed for

about 1200 MW

Allotment in

progress

Allotment in

progress

Sunny Days Ahead

38

Annexure III

SEMI Standards

The SEMI International Standards Program brings together industry experts to exchange

ideas and develop globally accepted technical standards for manufacturing. SEMI provides a

forum for the collaboration essential to move new and existing markets forward efficiently

and profitably.

The Economic Benefits of Standardization

• US National Institute of Standards and Technology (NIST) Study:

– Calibration, Standard Test Methods, and Software Standards resulted in

• $9.6 billion in benefits between 1996 and 2011

• Association Française de Normalisation (AFNOR) Study:

– Over 70% of companies participating in standardization reported that it

enabled them to anticipate future market requirements

• German Industry Study (DIN):

– Standards contribute more to economic growth than patents and licenses

• UK Department of Trade and Industry:

– Standards contribute £2.5 billion annually to economic growth in the UK

The Need for PV Standards

The solar PV industry needs to look at meaningful cost reduction through a global, robust

and well-organized supply chain. The current learning curve for the industry is not as steep

as other electronic industries, especially semiconductors which use many of the same

processes, materials, and suppliers as PV. A faster learning curve for the solar PV industry

could be accomplished through better industry collaboration, including industry standards

and technology roadmaps.

The progress made by semiconductors in cost reduction is one of the technological marvels

of our time. Since 1975, the cost of one transistor has been reduced by a factor of about

4,000,000. This achievement has often been ascribed to Moore’s Law, the prediction that

the number of transistors that can be placed inexpensively on an integrated circuit would

double approximately every two years. Many observers see Moore’s Law as a useful guide

to cost reduction in the PV industry. While thin film and c-Si cells do not benefit from

lithography-enabled feature-size reductions that comprise much of cost reductions in

semiconductors, much of Moore’s Law is directly related to productivity, yield, and other cost

Sunny Days Ahead

39

reductions not related to feature-size reductions. Since PV manufacturing is based upon

many of the same processes and materials as IC and display manufacturing, there remain

important learnings from these industries that can be applied to solar cells and modules.

• The PV industry currently has few standards to support the manufacturing process

and help achieve cost reduction and process efficiency goals

• The PV market, already large, is growing rapidly, with many new companies entering

the manufacturing supply chain

• Different applications and processes lead to diverse manufacturing challenges – this

is where industry standards can play a critical role by:

– Bringing the global supplier and customer communities together

– Collectively reducing the number of options in a given process

– Agreeing on common parameters and terminology

Why SEMI?

• Similarity between semiconductor, FPD and PV manufacturing – many SEMI

Standards are immediately applicable

• Well-established (35+years), transparent process for developing international

consensus manufacturing Standards

• Global infrastructure serving major PV manufacturing regions & over 500 volunteer

experts working in SEMI PV Standards Activities, led by PV industry veterans

Photovoltaic Standards at SEMI

Overview

For over 35 years, the SEMI International Standards Program has been well known for

developing global consensus standards for the semiconductor industry. Less well-known,

but now increasing in visibility, is the long SEMI history of developing PV Standards,

leveraging the many similarities that photovoltaic (PV) manufacturing has to that of the

semiconductor and FPD industries. The first SEMI Photovoltaic Standard, M6, Specification

for Silicon Wafers for Use as Photovoltaic Solar Cells, was published in 1981, now replaced

by SEMI PV22. With a global infrastructure serving major PV manufacturing regions, PV

Standardization activity at SEMI is now taking center stage.

Sunny Days Ahead

40

Photovoltaic Standards Committee

The first SEMI Standards Committee specifically dedicated to photovoltaics was formed in

2007, and rapidly developed SEMI PV1, a test method for solar-grade silicon feedstock, and

SEMI PV2, guide for PV equipment communication interfaces. There are now over 30 PV

Standardization activities underway at SEMI, both in crystalline silicon and thin film cell

technologies, and new PV Automation and PV Materials Committees have recently been

formed to specifically address standardization topics related to hardware and software

automation, materials and test methods.

Committees are now active in Europe, Japan, North America, and Taiwan, and a Working

Group is forming in China. Over 500 technical experts from leading companies in all

segments of the photovoltaic supply chain are currently involved in PV Standards efforts at

SEMI. Join them in this important effort.

Registration is free. Visit www.semi.org/standardsmembership.

Industry Participation is Critical

Momentum is building for the development and widespread adoption of standards in the

solar photovoltaic manufacturing industry. The SEMI Standards Program allows companies

to collaborate in a pre-competitive environment to define the best path to encourage

technical innovation and market growth. Companies that actively participate in the

development process stay current with industry technology trends, and more importantly,

these companies shape the development of the industry.

Published SEMI PV Standards

SEMI PV1 - Test Method for

MeasuringTrace Elements in Silicon

Feedstock for Silicon Solar Cells by High-

Mass Resolution Glow Discharge Mass

Spectrometry

• SEMI PV2 - Guide for PV Equipment

Communication Interfaces (PVECI)

• SEMI PV3 - Guide for High Purity Water

Used in Photovoltaic Cell Processing

• SEMI PV4 - Specification for Range of

5th Generation Substrate Sizes for Thin

Film Photovoltaic Applications

• SEMI PV5 - Guide for Oxygen (O2), Bulk,

Used In Photovoltaic Applications

• SEMI PV6 - Guide for Argon (Ar), Bulk,

Used In Photovoltaic Applications

• SEMI PV7 - Guide for Hydrogen (H2),

Bulk, Used In Photovoltaic Applications

• SEMI PV8 - Guide for Nitrogen (N2),

Bulk, Used In Photovoltaic Applications

• SEMI PV9 -Test Method For Excess

Charge Carrier Decay In PV Silicon

Materials By Non-Contact Measurements

Of Microwave Reflectance After A Short

Illumination Pulse

Sunny Days Ahead

41

• SEMI PV10 - Test Method For

Instrumental Neutron Activation Analysis

(INAA) Of Silicon

• SEMI PV11- Specifications for

Hydrofluoric Acid, Used In Photovoltaic

Applications

• SEMI PV12 - Specifications for

Phosphoric Acid, Used In Photovoltaic

Applications

• SEMI PV13 - Test Method for

Contactless Excess-Charge-Carrier

Recombination Lifetime Measurement in

Silicon Wafers, Ingots, and Bricks Using an

Eddy-Current Sensor

• SEMI PV14 - Guide For Phosphorus

Oxychloride, Used In Photovoltaic

Applications

• SEMI PV15 - Test Method for Measuring

BRDF Metrics to Monitor the Surface

Roughness and Texture of PV Materials

• SEMI PV16 - Specifications for Nitric

Acid, Used In Photovoltaic Applications

• SEMI PV17 - Specification for Virgin

Silicon Feedstock Materials for

Photovoltaic Applications

• SEMI PV18 - Guide for Specifying a

Photovoltaic Connector Ribbon

• SEMI PV19 - Guide for Testing

Photovoltaic Connector Ribbon

Characteristics

• SEMI PV20 - Specifications for

Hydrochloric Acid Used In Photovoltaic

Applications

• SEMI PV21 - Guide for Silane (SiH4),

Used In Photovoltaic Applications

• SEMI PV22 - Specification for Silicon

Wafers for Used in Photovoltaic Solar Cells

• SEMI PV23 - Test Method for

Mechanical Vibration of Crystalline Silicon

Photovoltaic (PV) Modules in Shipping

Environment

• SEMI PV24 - Guide for Ammonia (NH3)

In Cylinders, Used In Photovoltaic

Applications

• SEMI PV25 - Test Method for

Simultaneously Measuring Oxygen,

Carbon, Boron and Phosphorus in Solar

Silicon Wafers and Feedstock by

Secondary Ion Mass Spectrometry

• SEMI PV26 - Specifications for Hydrogen

Selenide (H2Se), Used In Photovoltaic

Applications

• SEMI PV27 - Specifications for

Ammonium Hydroxide (NH4OH), Used In

Photovoltaic Applications

Other SEMI Standards Applicable for PV Manufacturing

SEMI E10 - Specification for Definition and

Measurement of Equipment Reliability,

Availability, and Maintainability (RAM)

• SEMI F47 - Specification for

Semiconductor Processing Equipment

Voltage Sag Immunity

• SEMI M44 - Guide to Conversion Factors

for Interstitial Oxygen in Silicon

• SEMI MF1727 - Practice for Detection of

Oxidation Induced Defects in Polished

Silicon Wafer

Sunny Days Ahead

42

Current PV Standards Activities

• Analytical test methods

• Cell and module vibration test method

• Cell appearance and defect detection

• Cell specification template

•Equipment to equipment communication

• Minority carrier lifetime

• Process chemicals and gases

PV Standards Developing Organizations

Application of Standards in the PV Industry

To learn more, please visit www.pvgroup.org/standards or www.semi.org/standards

• PV wafer defect metrology

• PV wafer and cell transport carriers

• PV wafer mark and ID

• Single substrate tracking

• Solar grade silicon feedstock

• Thin film substrate dimensions

• Transparent conductive oxide

Sunny Days Ahead

43

EAI - Assisting Your Company for Attractive

Manufacturing Opportunities in Solar PV

EAI offers intelligence on the overall manufacturing opportunities in

Solar PV upstream – Polysilicon, Ingots and Wafers

Solar PV downstream – Cells and Modules

Thin Film manufacturing

Components – sub-components for cells and modules, chemicals and other

consumables

Balance of systems – inverters, monitoring systems

Equipment and machineries – Furnaces, wafer cutting tools, cell production line,

module production line

Identifying the most attractive opportunities for your company

Understanding your company’s aspirations in the context of solar energy sector

Understanding your company’s manufacturing competencies

Evaluating the fit between your aspirations + competencies and the available

opportunities

Clearly identifying the attractive opportunities appropriate for your company

Feasibility study for shortlisted opportunities

Demand and supply analysis

Costs and returns estimates

Strategic dimensions – extent of competition, buyer and supplier power, dominant

designs and industry concentration, degree of innovation, barriers to entry

Possibilities of JVs and technology partnerships

Identification of key success factors

Key characteristics of each opportunity

Sunny Days Ahead

44

Strengths

Dedicated Focus on Renewables - We work only in renewable energy and nothing

else.

Wide Expert Network - We work with over 100 technical and business experts across

all primary renewable energy sources.

Financial Assistance - We work with over 25 different PE, VC firms and banks

providing our client easy access to finance.

Clients

EAI's consulting team has been assisting several organizations in diverse renewable energy

domains. Some of our esteemed clients include:

PepsiCo

Reliance Industries

World Bank

Sterlite Technologies

Bill & Melinda Gates Foundation

iPLON GmbH

Minda Group

GE

Bhavik Energy

Agarwal Group

Prominent companies that have benefitted from our research and reports:

Accenture

AT Kearney

Shell

Lafarge

Exxon Mobil

Boston Consulting Group

Schneider Electric

Bosch

GE

Danfoss Solar

IFC

Siemens

Sharp

Gehrlicher Solar AG

Reliance Solar

Emergent Ventures

Videocon

Q Cells

Emerson Network Power

Indian Railways

Sunny Days Ahead

45

EAI’s Replacing Diesel with Solar

Looking to save on diesel by moving to captive solar power? EAI’s Replacing Diesel with

Solar report is a one-stop resource for all the information you will need to assess, implement,

and profit from substituting diesel with solar. Within this report you will find

• Captive solar PV technology and components

• Constraints in replacing diesel with solar

• Government incentives and regulations

• Inputs on capital and operational costs and financial scenario analysis

• Case studies for those businesses that already use solar for captive power

• Financing options

• Vendors, component suppliers, and system integrators

• List of solar PV captive power plant systems all over India